Market & Fund update - Meetings, agendas, and minutes

21

Prepared by Aon Presentation to London Borough of Enfield Market & Fund update Royal Borough of Kingston upon Thames Pension Fund May 2020

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Market & Fund update - Meetings, agendas, and minutes

Prepared by AonPresentation to London Borough of Enfield

Market & Fund updateRoyal Borough of Kingston upon Thames Pension Fund

May 2020

2

May 2020

Aon Hewitt Limited is authorised and regulated by the Financial Conduct Authority.

Agenda

Market update

Asset class and manager update

Strategic considerations

Market update

4

May 2020

Aon Hewitt Limited is authorised and regulated by the Financial Conduct Authority.

Market impact

Government responseGovernments globally introduced lockdowns in a bid to halt the Covid-19 spread which hampered economic activity.

Central bank responseCentral banks simultaneously introduced support packages to dampen the economic fall-out which caused equities to rebound considerably.

Equity marketsWhen equity markets initially viewed Covid-19 as an emerging market problem, developed market equities were little changed.

When it became clear that the virus would be widespread, global equity markets fell dramatically.

Investor sentimentWe saw increased volatility across asset classes as investors shied away from riskier assets in favour of safer havens, triggering liquidity challenges in certain credit sectors.

PricingUncertainty remains on the horizon as the full impact on economic and earnings data feeds through.

5

May 2020

Aon Hewitt Limited is authorised and regulated by the Financial Conduct Authority.

0

250

500

750

1,000

US UK Japan Eurozone

US$b

n

New Quantitative Easing MeasuresGovernment Bonds MBS Flexible

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

US UK Japan Eurozone

Central Bank Policy Rates (%)Start of 2020 Today

Central Bank Actions

Past performance is no guarantee of future results.Source: Aon, Bloomberg OIS Pricing

• Where possible central banks around the world have eased policy, but with rates being low there is a limit. • Unprecedented new quantitative easing measures have been announced to provide further monetary stimulus.

BoE emergency rate cut takes the base rate to an all-time low of 0.1%

“QE Infinity”: purchases of unlimited amount of treasuries, MBS, corporate bonds. Plans to buy high yield bonds ETFs announced.

QE endpoint? The BoJ is extending purchases of everything from government and corporate bonds to equities ETFs

Asset class and manager update

7

May 2020

Aon Hewitt Limited is authorised and regulated by the Financial Conduct Authority.

Equities: Asset class update

0 50 100 150 200 250 300 350

Nov 28, 1980Aug 2, 1956

Nov 29, 1968Mar 24, 2000Jan 11, 1973

Oct 9, 2007Feb 9, 1966

Mar 10, 1937Dec 12, 1961May 29, 1946

Jul 16, 1990Aug 25, 1987Sep 16, 1929Feb 19, 2020

Source: Aon Calculations, S&P, FactSet

Date of Market Peak Between 21st of February and 23rd March, US equities fell by

about a third from their highs and the S&P moved into bear market territory quicker than ever before (see chart to the right).

Looser monetary policy from Central Banks has led to the equity market retracing some of their losses.

Our view is that this upwards move has now captured the ‘goods news’ adequately.

Equities still look expensive relative to the average previous bear markets, indicating that earnings expectations are yet to be fully priced in.

With no easy exit strategy from these lockdowns, the drawdown effects of Coronavirus on economic activity and corporate cash flows could still be large even after recent normalisation.Dec-19 Jan-20 Feb-20 Mar-20 Apr-20 May-20

6065707580859095

100105110

-8%

-21%

Source: FactSet

Equity Market YTD (GBP terms)Price (Indexed to 100)

MSCI AC World FTSE 100

8

May 2020

Aon Hewitt Limited is authorised and regulated by the Financial Conduct Authority.

Equities: manager update

The strategy is active and seeks to outperform the MSCI All World Index by 1.5% to 2.0% p.a. Fidelity build a portfolio of stocks using bottom-up stock selection based on fundamental research and quantitative risk control. Although active, Fidelity tend to make allocations very close to benchmark. The fund outperformed its benchmark in Q1 2020 and for the year ending 31 March 2020. Over the quarter, stock selection was beneficial, driven by holdings in popular heavyweights such as Microsoft. Furtheractive positions in communication and pharmaceutical sectors contributed positively.

Fidelity

Select Global Plus Fund

The strategy is active and seeks to outperform MSCI All Country World Index by 2.5% to 3.0% p.a. Similar to Fidelity in fundamental approach however this portfolio tends to focus on growth stocks and takes a more high conviction approach. The fund significantly outperformed its benchmark over Q1 2020. Stock selection was beneficial, driven by the funds holdings in consumer discretionary and communication services. Positive relative performance was also aided by an underweight to financials and energy.

Columbia Threadneedle

TPEN Global Equity Fund

The strategy is active and seeks to outperform MSCI All Country World Index by 3.0% p.a. The fund can be classified as unconstrained and follows a quantitative approach. Schroders follow a value approach and look to invest in stocks where they believe the current market price is less than the intrinsic value. The fund lagged its benchmark in Q1 2020 due to its overweight in more cyclically exposed areas such as resources and energy. Not owning popular heavyweights (e.g. Microsoft, Amazon and Apple) was also detrimental. The ‘value’ style in general has struggled in recent years, and managers with ‘value’ styles have underperformed wider equity peers.

Schroders

Global Value Fund

9

May 2020

Aon Hewitt Limited is authorised and regulated by the Financial Conduct Authority.

Bonds: asset class update

Both fixed and real gilt yields trended lower since the start of the year, driven by large central bank rate cuts and investor demand for safe haven assets.

Investors seeking to turn government bonds into cash in illiquid trading conditions and concerns about increased borrowing levels from fiscal stimulus measures drove a sharp rise in yields mid-March.

Lower inflation expectations due to a collapse in oil price and weaker economic outlook meant that index-linked gilts underperformed fixed gilts over the quarter.

Credit matched equities last month, as US investment grade spreads went to levels not seen outside the financial crisis.

Surging downgrades, the BBB overhang risk of falling angels and illiquidity drove spreads higher. The pandemic policy responses and Fed buying has calmed things recently.

An elusive post-pandemic recovery, and its impact on credit risk premiums is likely to keep volatility high and spreads under pressure for longer. Against this, central bank buying and the continued global search for yield does cushion credit to a degree.

Real Yields (%)

-2.66-2.31-2.13

-3.5

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

May-18 Aug-18 Nov-18 Feb-19 May-19 Aug-19 Nov-19 Feb-20 May-2010-year 20-year 30-year

Source: Bloomberg

May-18 Aug-18 Nov-18 Feb-19 May-19 Aug-19 Nov-19 Feb-20 May-200

50100150200250300350400450

189209222

Source: Factset

Investment Grade Credit Spreads (bps)

ICE BofA US Corporate ICE BofA Sterling CorporateICE BofA Euro Corporate

10

May 2020

Aon Hewitt Limited is authorised and regulated by the Financial Conduct Authority.

Bonds: manager update

The fund is active and aims to provide a return, from a combination of income and capital growth over the long-term, and invests at least 80% of the assets in sterling denominated investment grade corporate bonds. The performance target of the fund is to outperform the Market iBoxx GBP Non-Gilts All Maturities Index by 1% p.a. The fund delivered a negative absolute return over Q1 2020 but outperformed its benchmark. An underweight in credit risk relative to the benchmark and an underweight in cyclicals contributed to relative performance during the recent sell-off. Furthermore, an underweight to senior Banks and Insurance bonds and Housing Association contributed to relative outperformance.

Janus Henderson

All Stocks Credit Fund

The fund seeks to generate returns from rotating between fixed income asset classes and invests in bonds of any quality including governments, companies or any other type of issuer in any country. The fund is actively managed and targets outperformance of the Euro base rate by at least 2% p.a. over any 5 year period. The fund delivered a modest negative return over Q1 2020. Positions in government bonds in the US, Canada and Europe performed well. The fund was able to avoid the worst of the market falls in March due to limited exposure to high-yield corporates and through credit hedges.

Janus Henderson

Total Return Bond Fund

Multi asset credit strategies focus solely on deriving value from either sector rotation or bottom up credit ideas or a combination of both in credit markets. The fund invests in bonds across any quality and from any issuer. The strategy is active and seeks to achieve a return of 4-5% p.a. in excess of LIBOR. Over 50% of the allocation as at 31 March 2020 was in the US and UK. Quarterly performance was disappointing and in the double digit negative range. The poor performance was a function of various types of credit held. All asset classes held by the fund performed poorly and the negative performance was exacerbated by the need for the fund to raise cash for margin calls related to the sell-off in sterling.

CQS (LCIV)

Multi-Asset Credit

11

May 2020

Aon Hewitt Limited is authorised and regulated by the Financial Conduct Authority.

Property: asset class update

Property Currently uncertainty within real estate markets and valuation impacts expected to lag liquid markets.

We are seeing high volatility in REIT markets. Many REITS trading at steep discount to NAVS, especially those sectors most impacted by Covid-19 (e.g. retail, office).

Property Fund SuspensionsMany valuers have placed material

uncertainty clauses on valuations. In response to this we are seeing a spate of

property funds suspend trading.

These measures reflect the inability to value assets with any degree of confidence and are

being put in place to protect investors.

12

May 2020

Aon Hewitt Limited is authorised and regulated by the Financial Conduct Authority.

Property: manager update

The fund is a core, actively managed balanced UK focused fund investing in strategic growth locations with sustainable income streams. Due to the material uncertainty clauses, the fund has deferred redemption requests payable after 31 March 2020. The length of the deferral will be reviewed quarterly. The fund delivered a small negative return, outperforming its benchmark over Q1 2020. The relative performance was assisted by significant rental uplift achieved on a business park holding. In addition, a recently acquired property experienced a marginal capital uplift.

UBS

Triton Property Fund

The Fund has made a commitment of £25m (c. 3% of total assets), to the M&G Residential Property Fund. Capital drawdowns are yet to be made. M&G’s valuers added a material uncertainty clause to the 31 March 2020 valuation. M&G state that the UK housing market had been transacting normally for most of the quarter and lettings were only nominally affected. Therefore 31 March reporting sawminimal impact. M&G are cognisant that 31 March was close to the start of the COVID-19 pandemic and have communicated that the fund is meeting its funding obligations and continues to receive developer coupon payments. Q1 distributions were paid in full and M&G will continue to assess the appropriateness of distributions and will communicate any further developments. In light of the current situation, M&G have advised that capital calls for the Pension Fund are likely to be completed by end of the Q3 2020.

M&G

Residential Property Fund

13

May 2020

Aon Hewitt Limited is authorised and regulated by the Financial Conduct Authority.

Diversified Growth Funds: asset class update

Diversified Growth Funds (“DGFs”) seek to deliver returns from multiple different sources, diversifying risk and reducing volatility. As such the DGF funds will hold multiple different asset classes and will differ significantly with each fund.

The impact of the recent market movements will differ on each DGF, depending on the underlying asset allocation. Aon analysis shows that the majority of DGFs delivered negative absolute returns while outperforming equities in Q1 with the bulk delivering returns between -6% and -12%.

The graphic below shows the categories Aon typically assigns to DGF funds:

In general, DGFs within the ‘Growth’ category typically have higher equity allocations and the performance is more correlated to equity market performance.

Absolute Return strategies typically have the lowest correlation to equity markets, thus should perform better in environments with higher market volatility.

Capital preservation strategies typically aim to provide greater downside protection than equities whilst still participating in growth markets.

14

May 2020

Aon Hewitt Limited is authorised and regulated by the Financial Conduct Authority.

Diversified Growth Fund: manager update

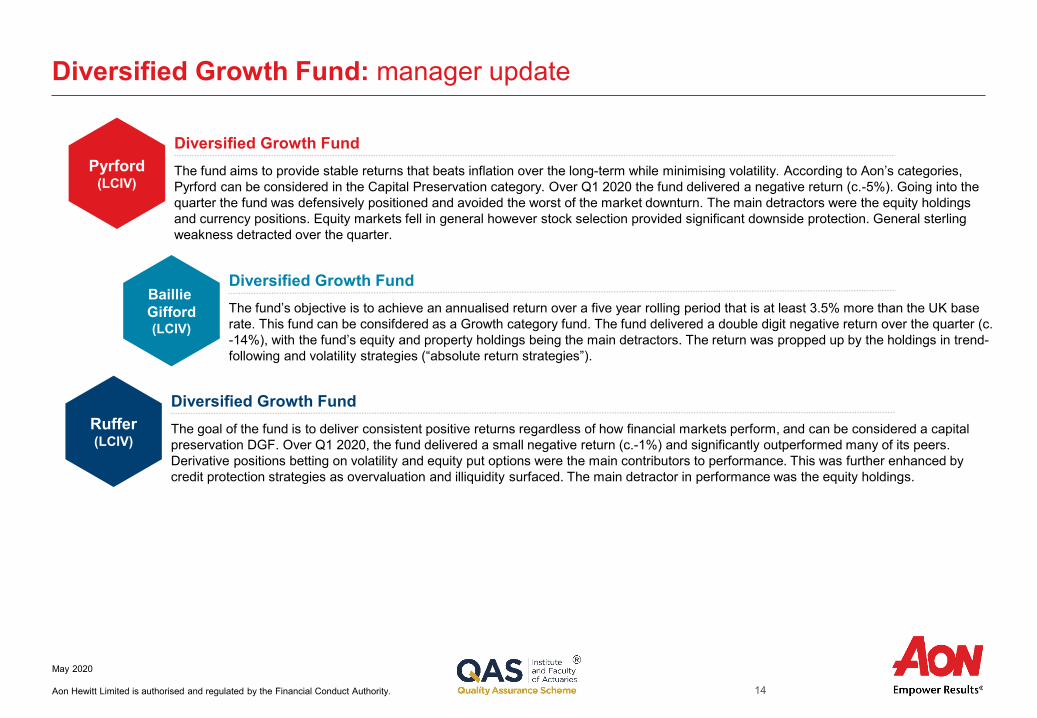

The fund aims to provide stable returns that beats inflation over the long-term while minimising volatility. According to Aon’s categories, Pyrford can be considered in the Capital Preservation category. Over Q1 2020 the fund delivered a negative return (c.-5%). Going into the quarter the fund was defensively positioned and avoided the worst of the market downturn. The main detractors were the equity holdings and currency positions. Equity markets fell in general however stock selection provided significant downside protection. General sterling weakness detracted over the quarter.

Pyrford(LCIV)

Diversified Growth Fund

The fund’s objective is to achieve an annualised return over a five year rolling period that is at least 3.5% more than the UK base rate. This fund can be consifdered as a Growth category fund. The fund delivered a double digit negative return over the quarter (c. -14%), with the fund’s equity and property holdings being the main detractors. The return was propped up by the holdings in trend-following and volatility strategies (“absolute return strategies”).

Baillie Gifford(LCIV)

Diversified Growth Fund

The goal of the fund is to deliver consistent positive returns regardless of how financial markets perform, and can be considered a capital preservation DGF. Over Q1 2020, the fund delivered a small negative return (c.-1%) and significantly outperformed many of its peers. Derivative positions betting on volatility and equity put options were the main contributors to performance. This was further enhanced by credit protection strategies as overvaluation and illiquidity surfaced. The main detractor in performance was the equity holdings.

Ruffer(LCIV)

Diversified Growth Fund

Strategic considerations

16

May 2020

Aon Hewitt Limited is authorised and regulated by the Financial Conduct Authority.

Investment Outlook

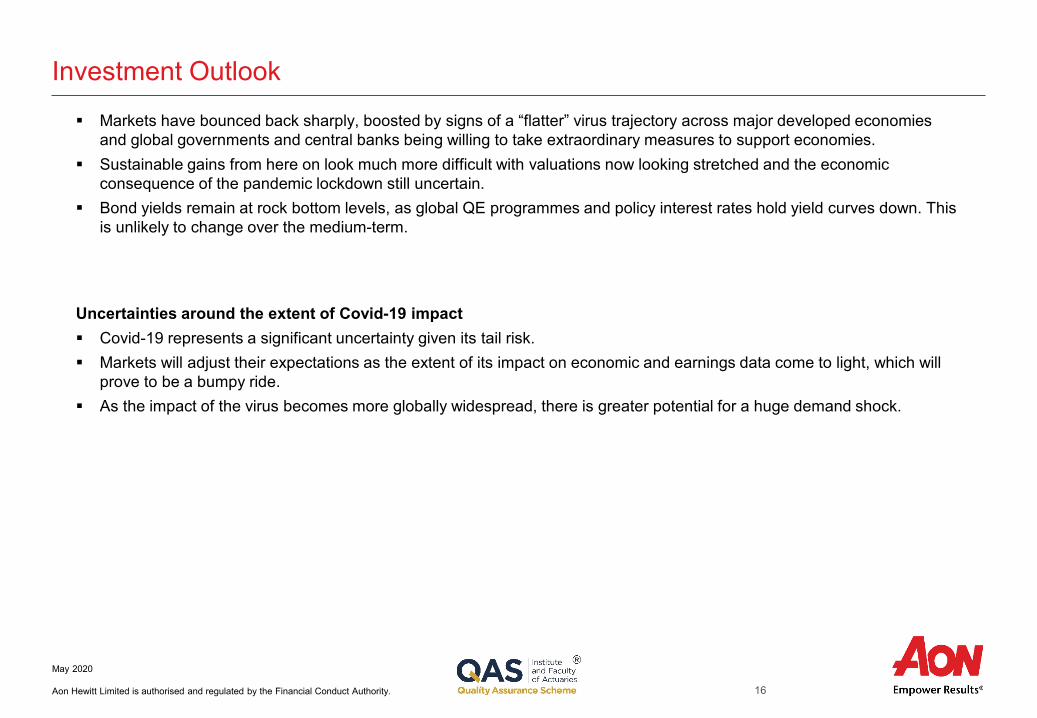

Markets have bounced back sharply, boosted by signs of a “flatter” virus trajectory across major developed economies and global governments and central banks being willing to take extraordinary measures to support economies.

Sustainable gains from here on look much more difficult with valuations now looking stretched and the economic consequence of the pandemic lockdown still uncertain.

Bond yields remain at rock bottom levels, as global QE programmes and policy interest rates hold yield curves down. This is unlikely to change over the medium-term.

Uncertainties around the extent of Covid-19 impact Covid-19 represents a significant uncertainty given its tail risk. Markets will adjust their expectations as the extent of its impact on economic and earnings data come to light, which will

prove to be a bumpy ride. As the impact of the virus becomes more globally widespread, there is greater potential for a huge demand shock.

17

May 2020

Aon Hewitt Limited is authorised and regulated by the Financial Conduct Authority.

Portfolio valuation as at 31 March 2020

Source: JP Morgan

*£25m was committed to M&G Residential Property. At 31 March 2020 no capital calls had been made. .

31 March 2020 Strategic

Mar

ket

Valu

e(£

m)

Wei

ght (

%)

Targ

et (%

)

Rel

ativ

e (%

)

Low

er

Ran

ge (%

)

Upp

er

Ran

ge (%

)

Equities 510.58 63.2 57.0 6.2 55.0 65.0Fidelity 203.78 25.2 - - - -Col. Threadneedle 200.99 24.9 - - - -Schroders 105.81 13.1 - - - -Bonds 100.89 12.5 15.0 -2.5 10.0 20.0Janus Henderson ASC 34.66 4.3 - - - -Janus Henderson TRB 38.55 4.8 - - - -LCIV - CQS 27.68 3.4 - - - -Diversified Growth Funds 146.83 18.2 20.0 -1.8 15.0 25.0LCIV - Pyford 78.53 9.7 - -LCIV – Baillie Gifford 32.59 4.0 - -LCIV - Ruffer 35.71 4.4 - -Property* 41.37 5.1 8.0 -2.9 n/a n/aUBS 41.37 5.1 - - - -Cash 7.64 0.9 0.0 0.9 n/a n/aCash 7.64 0.9 - - - -Total 807.31 100.0 100.0 0.0 n/a n/a

18

May 2020

Aon Hewitt Limited is authorised and regulated by the Financial Conduct Authority.

Summary

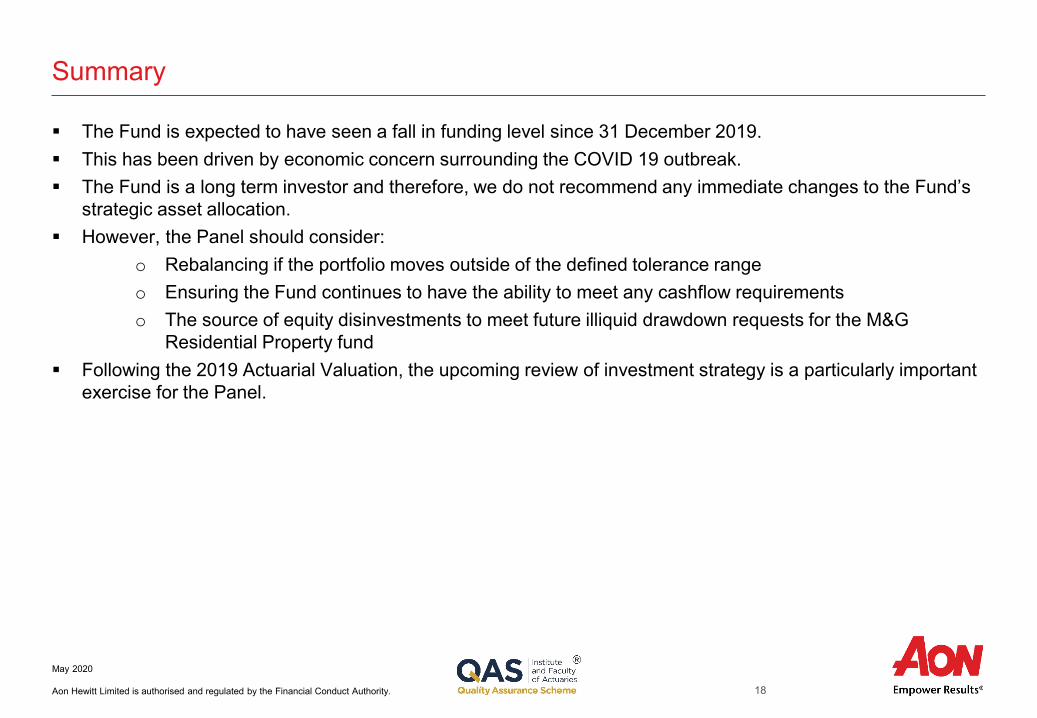

The Fund is expected to have seen a fall in funding level since 31 December 2019. This has been driven by economic concern surrounding the COVID 19 outbreak. The Fund is a long term investor and therefore, we do not recommend any immediate changes to the Fund’s

strategic asset allocation. However, the Panel should consider:

o Rebalancing if the portfolio moves outside of the defined tolerance rangeo Ensuring the Fund continues to have the ability to meet any cashflow requirementso The source of equity disinvestments to meet future illiquid drawdown requests for the M&G

Residential Property fund Following the 2019 Actuarial Valuation, the upcoming review of investment strategy is a particularly important

exercise for the Panel.

19

May 2020

Aon Hewitt Limited is authorised and regulated by the Financial Conduct Authority.

Strategic considerations

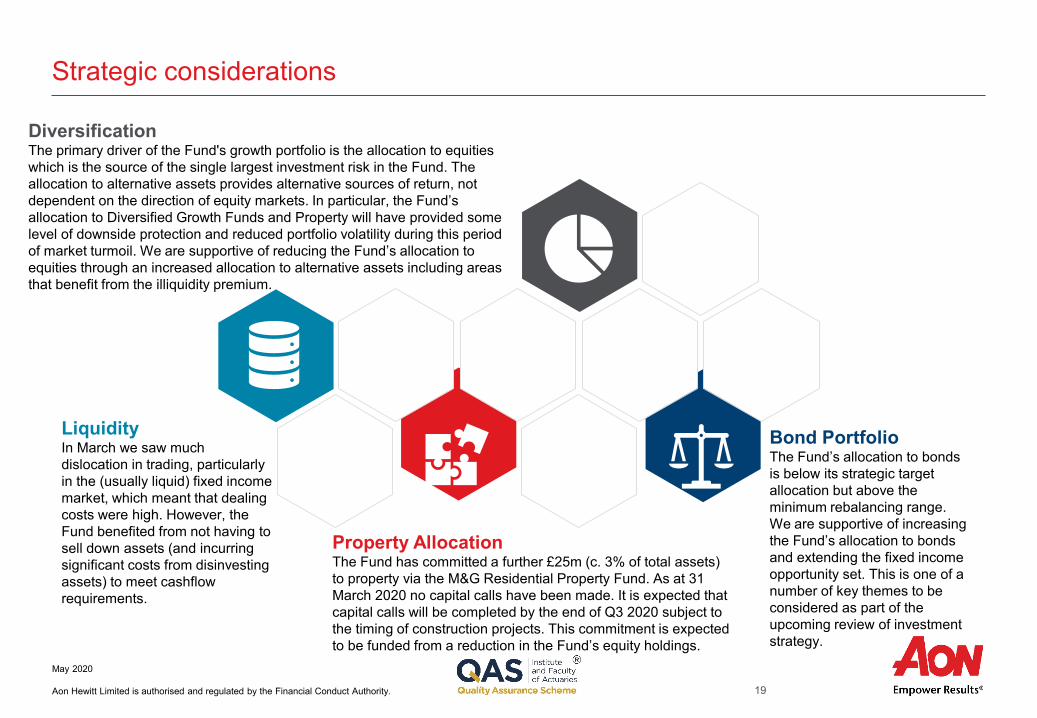

LiquidityIn March we saw much dislocation in trading, particularly in the (usually liquid) fixed income market, which meant that dealing costs were high. However, the Fund benefited from not having to sell down assets (and incurring significant costs from disinvesting assets) to meet cashflow requirements.

Property AllocationThe Fund has committed a further £25m (c. 3% of total assets) to property via the M&G Residential Property Fund. As at 31 March 2020 no capital calls have been made. It is expected that capital calls will be completed by the end of Q3 2020 subject to the timing of construction projects. This commitment is expected to be funded from a reduction in the Fund’s equity holdings.

Bond PortfolioThe Fund’s allocation to bonds is below its strategic target allocation but above the minimum rebalancing range. We are supportive of increasing the Fund’s allocation to bonds and extending the fixed income opportunity set. This is one of a number of key themes to be considered as part of the upcoming review of investment strategy.

DiversificationThe primary driver of the Fund's growth portfolio is the allocation to equities which is the source of the single largest investment risk in the Fund. The allocation to alternative assets provides alternative sources of return, not dependent on the direction of equity markets. In particular, the Fund’s allocation to Diversified Growth Funds and Property will have provided some level of downside protection and reduced portfolio volatility during this period of market turmoil. We are supportive of reducing the Fund’s allocation to equities through an increased allocation to alternative assets including areas that benefit from the illiquidity premium.

20

May 2020

Aon Hewitt Limited is authorised and regulated by the Financial Conduct Authority.

Disclaimer

This document and any enclosures or attachments are prepared on the understanding that it is solely for the benefit of the addressee(s). Unless we provide express prior written consent, no part of this document should be reproduced, distributed or communicated to anyone else and, in providing this document, we do not accept or assume any responsibility for any other purpose or to anyone other than the addressee(s) of this document. Notwithstanding the level of skill and care used in conducting due diligence into any organisation that is the subject of a rating in this document, it is not always possible to detect the negligence, fraud, or other misconduct of the organisation being assessed or any weaknesses in that organisation's systems and controls or operations. This document and any due diligence conducted is based upon information available to us at the date of this document and takes no account of subsequent developments. In preparing this document we may have relied upon data supplied to us by third parties (including those that are the subject of due diligence) and therefore no warranty or guarantee of accuracy or completeness is provided. We cannot be held accountable for any error, omission or misrepresentation of any data provided to us by third parties (including those that are the subject of due diligence). This document is not intended by us to form a basis of any decision by any third party to do or omit to do anything.Any opinions or assumptions in this document have been derived by us through a blend of economic theory, historical analysis and/or other sources. Any opinion or assumption may contain elements of subjective judgement and are not intended to imply, nor should be interpreted as conveying, any form of guarantee or assurance by us of any future performance. Views are derived from our research process and it should be noted in particular that we cannot research legal, regulatory, administrative or accounting procedures and accordingly make no warranty and accept no responsibility for consequences arising from relying on this document in this regard. Calculations may be derived from our proprietary models in use at that time. Models may be based on historical analysis of data and other methodologies and we may have incorporated their subjective judgement to complement such data as is available. It should be noted that models may change over time and they should not be relied upon to capture future uncertainty or events.

21

May 2020

Aon Hewitt Limited is authorised and regulated by the Financial Conduct Authority.

Aon Hewitt LimitedAon Hewitt Limited is authorised and regulated by the Financial Conduct Authority.Registered in England & Wales No. 4396810Registered office:The Aon Centre | The Leadenhall Building | 122 Leadenhall Street | London | EC3V 4AN

To protect the confidential and proprietary information included in this material, it may not be disclosed or provided to any third parties without the prior written consent of Aon Hewitt Limited.

Aon Hewitt Limited does not accept or assume any responsibility for any consequences arising from any person, other than the intended recipient, using or relying on this material.

Copyright © 2020 Aon Hewitt Limited. All rights reserved.