Market Development for Genetically Modified Foods

313

Market Development for Genetically Modified Foods

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Market Development for Genetically Modified Foods

Market Development for Genetically Modified Foods

Market Development for GeneticallyModified Foods

Edited by

Vittorio Santaniello

Dipartimento di Economia e IstituzioniUniversita degli Studi Roma ‘Tor Vergata’

Rome, Italy

Robert E. Evenson

Economic Growth CenterDepartment of Economics

Yale UniversityConnecticut, USA

and

David Zilberman

Department of Agricultural and Resource EconomicsUniversity of California

Berkeley, USA

CABI Publishing

CABI Publishing is a division of CAB International

CABI Publishing CABI PublishingCAB International 10 E 40th StreetWallingford Suite 3203Oxon OX10 8DE New York, NY 10016UK USA

Tel: +44 (0)1491 832111 Tel: +1 212 481 7018Fax: +44 (0)1491 833508 Fax: +1 212 686 7993Email: [email protected] Email: [email protected] site: www.cabi-publishing.org

© CAB International 2002. All rights reserved. No part of this publication may bereproduced in any form or by any means, electronically, mechanically, by photocopy-ing, recording or otherwise, without the prior permission of the copyright owners.

A catalogue record for this book is available from the British Library, London, UK

Library of Congress Cataloguing-in-Publication DataMarket development for genetically modified foods / edited by Vittorio Santaniello,Robert E. Evenson, and David Zilberman.

p. cm.Includes bibliographical references and index.Papers presented at a conference.ISBN 0–85199–573-X (alk. paper)

1. Genetic engineering industry--Europe--Congresses. 2. Genetically modified foods--Europe--Congresses. 3. Food industry and trade--Europe--Congresses. 4. Genetic engineering industry--North America--Congresses.5. Genetically modified foods--North America--Congresses. 6. Food industry andtrade--North America--Congresses. 7. Market surveys--Europe--Congresses. 8. Market surveys--North America--Congresses. I. Santaniello, V. II. Evenson,Robert E. (Robert Eugene), 1934-III. Zilberman, David.

HD9999.G453 E8516 2001381’.45664--dc21 2001043187

ISBN 0 85199 573 X

Typeset in Adobe Garamond by Wyvern 21 Ltd, Bristol.Printed and bound in the UK by Cromwell Press, Trowbridge.

Contents

Contributors viiAcknowledgements xIntroduction 1

1. A Way Forward for Frankenstein Foods 7M. Burton, S. James, B. Lindner and J. Pluske

PART I EVALUATING CONSUMER ATTITUDES TO GM FOODS

2. A Comparison of Consumer Attitudes towards GM Food in Ireland and the United States:a Case Study Over Time 25M. McGarry Wolf and C. Domegan

3. Differences in Public Acceptance between Generic and Premium Branded GM Food Products: an Analytical Model 39A. Verdurme, X. Gellynck, J. Viaene and W. Verbeke

4. Is European Consumers’ Refusal of GM Food a Serious Obstacle or a Transient Fashion? 49C.-H. Hanf and A. Böcker

5. Estimates of Willingness to Pay a Premium for Non-GM Foods: a Survey 55C.A. Mendenhall and R.E. Evenson

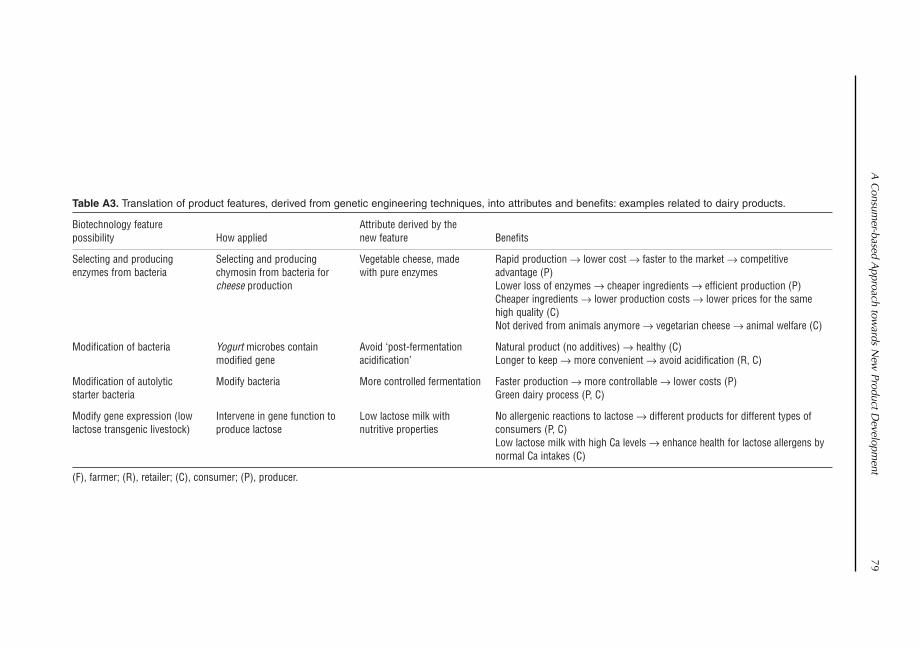

6. A Consumer-based Approach towards New Product Development throughBiotechnology in the Agro-food Sector 63N.M. Spetsidis and G. Schamel

PART II ACCEPTANCE BY FARMERS OF BIOTECH PRODUCTS

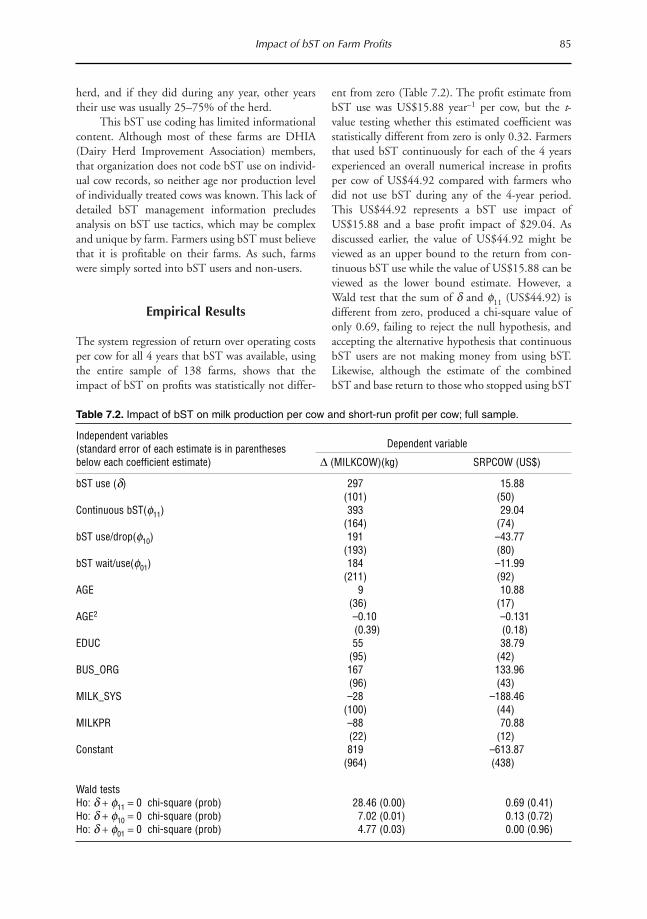

7. The Impact of Bovine Somatotropin on Farm Profits 81L.W. Tauer

8. The Importance of Feed Management Technologies in the Decision to Adopt BovineSomatotropin: an Application to California Dairy Producers 91I. Henriques and L.J. Butler

9. The Potential Effect of Recombinant Bovine Somatotropin on World Dairying 101L.S. Jarvis

10. Gains to Yield-increasing Research in the Evolving Canadian Canola Research Industry 113R.S. Gray, S. Malla and P.W.B. Phillips

v

11. Determinants of GMO Use: a Survey of Iowa Maize–Soybean Farmers’ Acreage Allocation 127C. Alexander, J. Fernandez-Cornejo and R.E. Goodhue

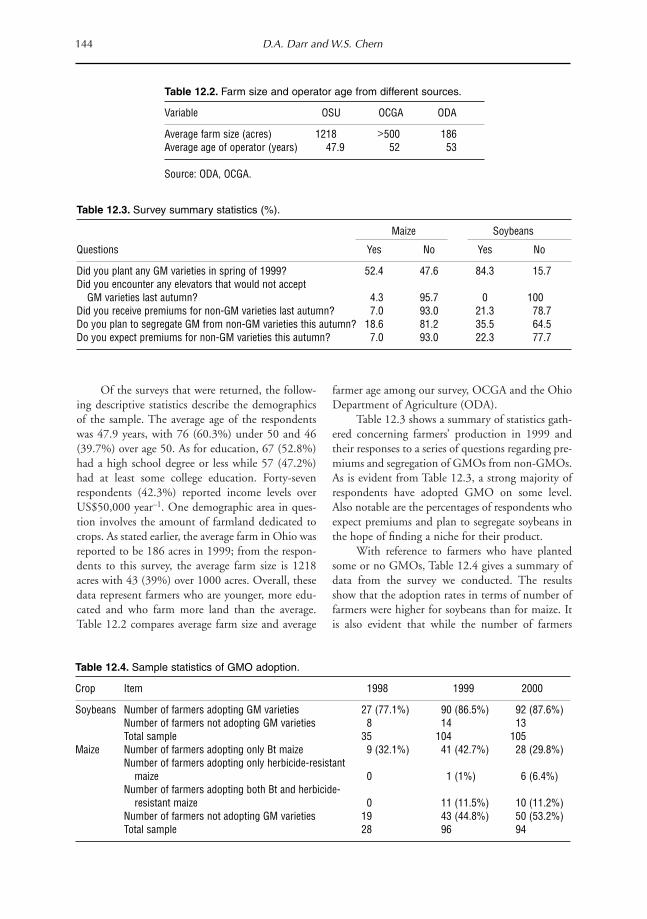

12. Estimating Adoption of GMO Soybeans and Maize: a Case Study of Ohio, USA 141D.A. Darr and W.S. Chern

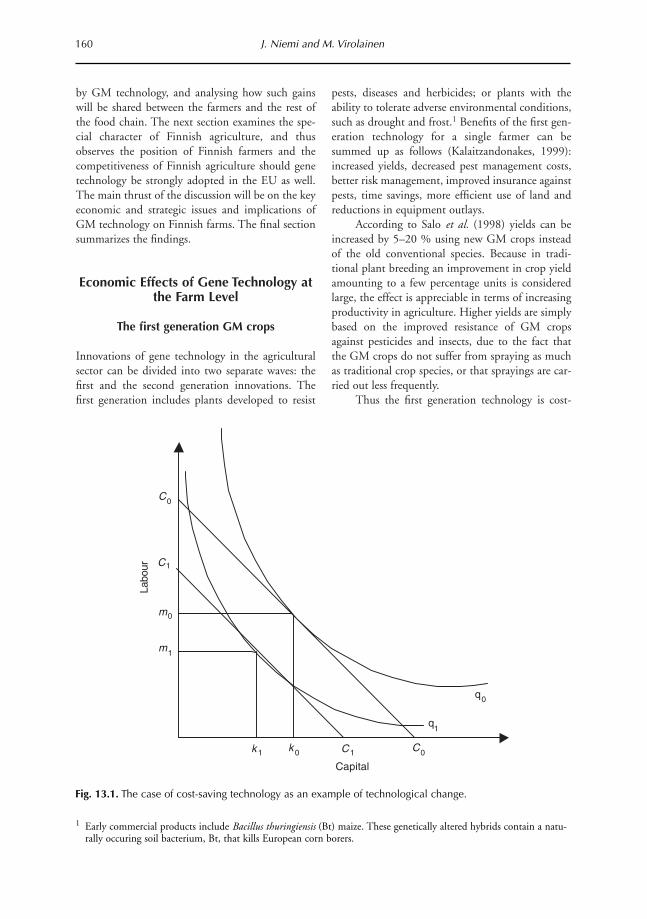

13. Ex ante Economic Assessment of Adopting Genetically Engineered Crops in Finland 159J. Niemi and M. Virolainen

14. Biotechnology, Farm Management and Local Agricultural Development 167M.T. Gorgitano and V. Sodano

PART III THE ROLE OF INFORMATION SYSTEMS AND OF ASSOCIATED REGULATORY DEVELOPMENTS

15. Public Acceptance of and Benefits from Agricultural Biotechnology: a Key Role for VerifiableInformation 179W.E. Huffman and A. Tegene

16. Science and Regulation: Assessing the Impacts of Incomplete Institutions and Information in the Global Agricultural Biotechnology Industry 191S. Smyth and P.W.B. Phillips

17. Quantifying Scientific Risk Communications of Agrobiotechnology 205L.A. Marks, S. Mooney and N. Kalaitzandonakes

18. Time Series Analysis of Risk Frames in Media Communication of Agrobiotechnology 217L.A. Marks, N. Kalaitzandonakes, K. Allison and L. Zakharova

19. Case Study in Benefits and Risks of Agricultural Biotechnology: Roundup Ready Soybeans 227J.E. Carpenter and L.P. Gianessi

20. Labelling for GM Foods: Theory and Practice 245P.W.B. Phillips and H. McNeill

21. Estimating the Costs of Segregation for Non-biotech Maize and Soybeans 261W.W. Lin

22. Endogenous Demand and Optimal Product Regulation: the Case of Agricultural Biotechnology 271A. Artuso

PART IV INDUSTRY STRUCTURE ISSUES

23. Tobin’s q and the Value of Agriceutical Firms 279M. Boland

24. The Structure of the European Agro-food Biotechnology Industry: Are Strategic AlliancesHere to Stay? 283W.B. Traill and C.E. Duffield

25. Market Structure in Biotechnology: Implications for Long-run Comparative Advantage 291B.F. Lavoie and I.M. Sheldon

26. Biotechnology in the Supply Chain: Managing a Product Differentiating Technology 301R.D. Weaver and T. Kim

Index 313

vi Contents

Corinne Alexander, Department of Agricultural and Resource Economics, University of California, OneShields Avenue, Davis, CA 95616, USA

Kevin Allison, Economics and Management of Agrobiotechnology Center, Department of AgriculturalEconomics, University of Missouri-Columbia, 125D Mumford Hall, Columbia, MO 65211, USA. Presentaddress: Harvard University, John F. Kennedy School of Government, USA

Anthony Artuso, Department of Agricultural Food and Resource Economics, 55 Dudley Road, Cook College,Rutgers University, New Brunswick, NJ 08901, USA

Andreas Böcker, Department of Agricultural Economics and Market Research, Justus-Liebig-University,Senckenbergstrasse 3, 35390 Giessen, Germany

Michael Boland, Department of Agricultural Economics, 342 Waters Hall, Kansas State University,Manhattan, KS 66506, USA

Michael Burton, Department of Agricultural and Resource Economics, Faculty of Agriculture, University ofWestern Australia, 35 Stirling Highway, Crawley (Perth), WA 6009, Australia

Leslie J. Butler, Department of Agricultural and Resource Economics, Room 2111, Social Science andHumanities, University of California, One Shields Avenue, Davis, CA 95616, USA

Janet E. Carpenter, National Center for Food and Agricultural Policy, 1616 P Street NW, First Floor,Washington, DC 20036, USA

Wen S. Chern, Department of Agricultural, Environmental and Development Economics, The Ohio StateUniversity, 2120 Fyffe Road, Columbus, OH 43210, USA

David A. Darr, Department of Agricultural, Environmental and Development Economics, The Ohio StateUniversity, 2120 Fyffe Road, Columbus, OH 43201, USA

Christine Domegan, Department of Marketing, National University of Ireland, Newcastle Road, Galway,Ireland

Christopher E. Duffield, Department of Agricultural and Food Economics, PO Box 237, The University ofReading, Reading, RG6 6AR, UK

Robert E. Evenson, Economic Growth Center, Department of Economics, Yale University, New Haven, CT06520, USA

Jorge Fernandez-Cornejo, Economic Research Service, USDA, 1800 M. Street, NW Room 4052, Washington,DC 20036-5831, USA

Xavier Gellynck, Faculty of Agriculture and Applied Biological Sciences, Department of AgriculturalEconomics, Division of Agro-Marketing, Ghent University, Coupure Links 653-9000, Ghent, Belgium

Contributors

vii

viii Contributors

Leonard P. Gianessi, National Center for Food and Agricultural Policy, 1616 P Street NW, First Floor,Washington, DC 20036, USA

Rachael E. Goodhue, Department of Agricultural and Resource Economics, University of California, OneShields Avenue, Davis, CA 95616, USA

Maria Teresa Gorgitano, Department of Agricultural Economics, University of Naples – Federico II, ViaUniversita 96, 80055 Portici, Italy

Richard S. Gray, Department of Agricultural Economics, 3D34 Agriculture Building, University ofSaskatchewan, 51 Campus Drive, Saskatoon, Saskatchewan, S7N 5A8, Canada

Claus-Hennig Hanf, Department of Agricultural Economics, Chair of Agribusiness Management, Christian-Albrechts-University, Olshausenstrasse 40, 24118 Kiel, Germany

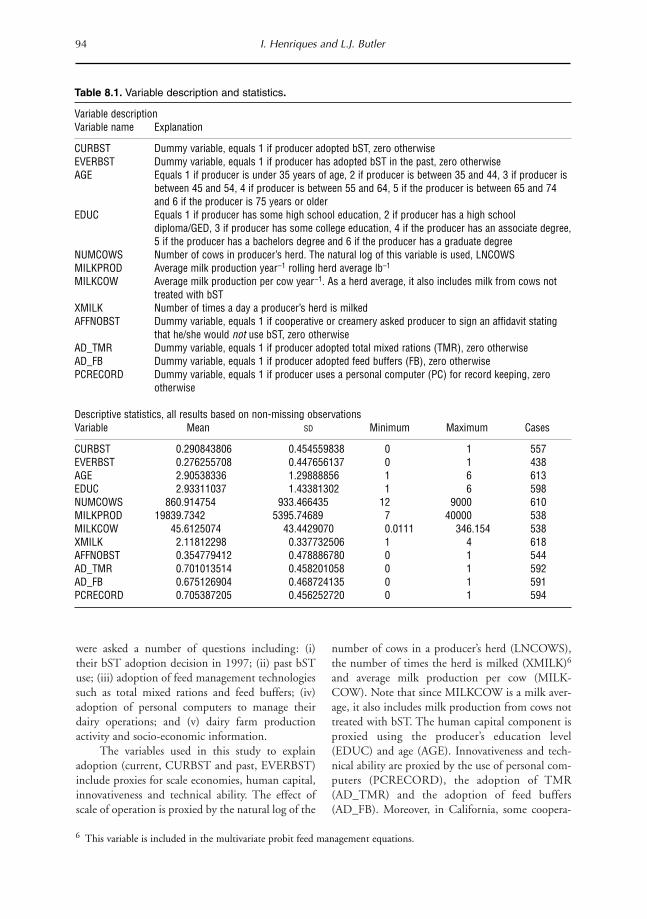

Irene Henriques, Schulich School of Business, York University, 4700 Keele Street, Toronto, Ontario, M3J 1P3,Canada

Wallace E. Huffman, Department of Economics, 260 Heady Hall, Iowa State University, Ames, IA 50011,USA

Sallie James, Department of Agricultural and Resource Economics, Faculty of Agriculture, University of WesternAustralia, 35 Stirling Highway, Crawley (Perth), WA 6009, Australia

Lovell S. Jarvis, College of Agricultural and Environmental Sciences, University of California, 150 Mrak Hall,Davis, CA 95616, USA

Nicholas Kalaitzandonakes, Economics and Management of Agrobiotechnology Center, Department ofAgricultural Economics, University of Missouri-Columbia, 125D Mumford Hall, Columbia, MO 65211,USA

Taeho Kim, 207D Armsby Building, Pennsylvania State University, University Park, PA 16802, USABrian F. Lavoie, Department of Agricultural, Environmental and Development Economics, The Ohio State

University, 2120 Fyffe Road, Columbus, OH 43210, USAWilliam W. Lin, ERS, USDA, 1800 M Street NW, Suite S5206, Washington, DC 20036-5831, USABob Linder, Faculty of Agriculture, University of Western Australia, 35 Stirling Highway, Crawley (Perth), WA

6009, AustraliaMarianne McGarry Wolf, Agribusiness Department, California Polytechnic State University, San Luis Obispo,

CA 93407, USA Heather McNeill, Department of Agricultural Economics, 3D34 Agriculture Building, University of

Saskatchewan, 51 Campus Drive, Saskatoon, Saskatchewan, S7N 5A8, Canada. Present address: 903-101Cumberland Avenue, Saskatoon, Saskatchewan, S7N 1L5, Canada

Stavroula Malla, Department of Agricultural Economics, 3D34 Agriculture Building, University ofSaskatchewan, 51 Campus Drive, Saskatoon, Saskatchewan, S7N 5A8, Canada

Leonie A. Marks, Economics and Management of Agrobiotechnology Center, Department of AgriculturalEconomics, University of Missouri-Columbia, 125D Mumford Hall, Columbia, MO 65211, USA

Catherine A. Mendenhall, Environmental Health Sciences, Department of Epidemiology and Public Health,Yale University, 60 College Street, PO Box 208034, New Haven, CT 06520, USA

Siân Mooney, Department of Agricultural Economics, Montana State University, Bozeman, MT 59717, USAJyrki Niemi, MTT Agrifood Research Finland, Economic Research (MTTL), PO Box 3 (Luutnantinnie 13),

FIN-00411, Helsinki, Finland Peter W.B. Phillips, Department of Agricultural Economics, 3D34 Agriculture Building, University of

Saskatchewan, 51 Campus Drive, Saskatoon, Saskatchewan, S7N 5A8, CanadaJo Pluske, Department of Agricultural and Resource Economics, Faculty of Agriculture, University of Western

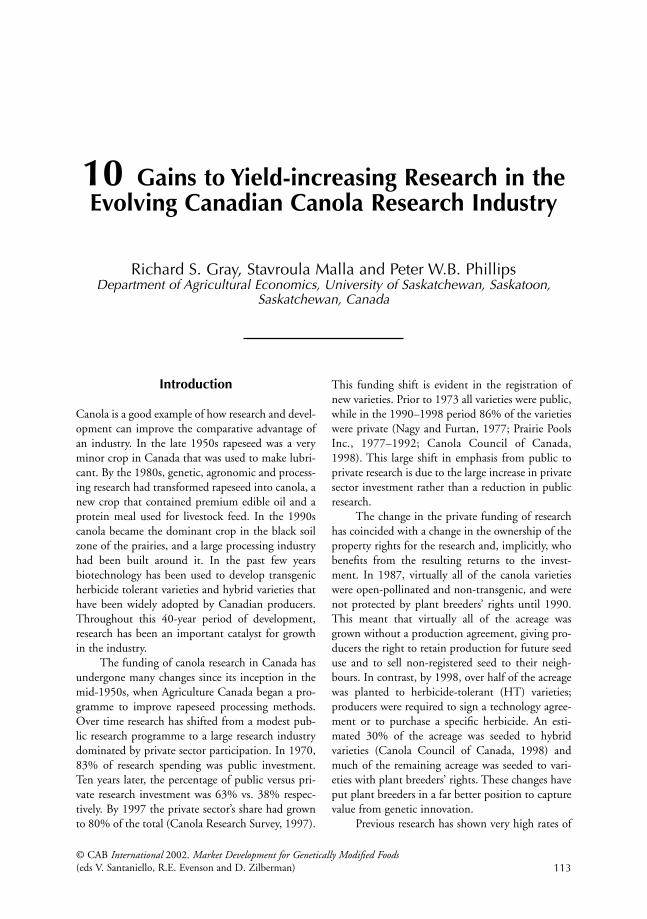

Australia, 35 Stirling Highway, Crawley (Perth), WA 6009, Australia Vittorio Santaniello, Dipartimento di Economia e Istituzioni, Universita degli Studi Roma ‘Tor Vergata’,

Rome, ItalyGünter Schamel, Faculty of Agriculture and Horticulture, Institute of Economic and Social Sciences,

Humboldt University at Berlin, Luisenstrasse 56, 10099, Berlin, GermanyIan M. Sheldon, Department of Agricultural, Environmental and Development Economics, The Ohio State

University, 2120 Fyffe Road, Columbus, OH 43210, USA

Contributors ix

Stuart Smyth, Department of Agricultural Economics, 3D34 Agriculture Building, University ofSaskatchewan, 51 Campus Drive, Saskatoon, Saskatchewan, S7N 5A8, Canada

Valeria Sodano, Department of Agricultural Economics, University of Naples – Federico II, Via Universita 96,80055 Portici, Italy

Nickolas M. Spetsidis, Faculty of Agriculture and Horticulture, Institute of Economic and Social Sciences,Humboldt University of Berlin, Luisenstrasse 56, 10099 Berlin, Germany. Present address:55 A. Papandreou Avenue, GR-71305, Iraklion – Crete, Greece

Loren W. Tauer, Cornell University, 451 Warren Hall, Ithaca, NY, 148503, USAAbebayehu Tegene, Resource Economic Division, ERS, USDA, 1800 M Street NW, Room 54194,

Washington DC, 20036-5837, USAW. Bruce Traill, Department of Agricultural and Food Economics, PO Box 237, The University of Reading,

Reading, RG6 6AR, UKWim Verbeke, Faculty of Agriculture and Applied Biological Sciences, Department of Agricultural Economics,

Division of Agro-Marketing, Ghent University, Coupure Links 653-9000, Ghent, Belgium Annelies Verdurme, Faculty of Agriculture and Applied Biological Sciences, Department of Agricultural

Economics, Division of Agro-Marketing, Ghent University, Coupure Links 653-9000, Ghent, BelgiumJacques Viaene, Faculty of Agriculture and Applied Biological Sciences, Department of Agricultural Economics,

Division of Agro-Marketing, Ghent University, Coupure Links 653-9000, Ghent, BelgiumMeri Virolainen, MTT Agrifood Research Finland, Economic Research (MTTL), PO Box 3 (Luutnantinnie

13), FIN-00411, Helsinki, FinlandRobert D. Weaver, 207D Armsby Building, Pennsylvania State University, University Park, PA 16802, USALudmila Zakharova, Economics and Management of Agrobiotechnology Center, Department of Agricultural

Economics, University of Missouri-Columbia, 129D Mumford Hall, Columbia, MO 65211, USADavid Zilberman, Department of Agricultural and Resource Economics, University of California, Berkeley, CA

94720, USA

Acknowledgements

This book has arisen from the conference entitled Biotechnology, Science and Modern Agriculture: a NewIndustry at the Dawn of the Century, convened by the International Consortium on AgriculturalBiotechnology Research (ICABR), held in Ravello, Italy on 15–18 June 2001.

The editors would like to acknowledge the sponsorship provided by the following institutions:CEIS–University of Rome ‘Tor Vergata’; Center for Sustainable Resource Development, University ofCalifornia at Berkeley; and Economic Growth Center, Yale University. The editors would also like to thankthe Italian National Research Council (CNR) for its financial support of the conference.

x

The investment climate for firms producing geneti-cally modified (GM) agricultural products haschanged considerably in recent months. In the US,transgenic crop production has reached very highlevels. The global area planted to transgenic cropsreached approximately 40 Mha in 1999 (12 coun-tries planted transgenic crops and 84% of transgenicarea was in industrialized countries). This was a verypromising beginning for GM products.

However, consumer resistance has turned outto be much stronger than anticipated. Consumerattitudes regarding GM foods are being expressed ina setting where premiums and discounts for GMfood products and GM-free food products havegenerally not yet emerged. At least part of the prob-lem can be seen as a coordination problem. Thesuppliers of ag-biotech products sell to farmers whoproduce GM foods. These foods in turn must beprocessed and marketed by the food industry.Consumer attitudes (after all, ‘the customer isalways right’) must be reflected in farm productmarkets and in farm input (ag biotech) markets.

Consumer movements have already promotedgovernment actions in the form of import restric-tions and prohibitions of the sale of GM products.These actions have the support of groups with alliedinterests. Farm producer groups in importing coun-tries and in the European Union generally have aninterest in maintaining both tariff and non-tariffbarriers to trade. They thus have common interestswith consumer groups opposing GM food sales,even though they may not share consumer attitudes.

The opposition to GM foods has also beenincorporated into broader political movementsopposing ‘globalization’ and related issues. Thegrowth in the political opposition to the expansionin world trade and to the international organizationssupporting this expansion, notably the World TradeOrganization (WTO), but including the WorldBank and the International Monetary Fund, has alsobeen surprising. This movement has many conflict-ing cross currents and reflects a number of interests.Because biotechnology interests and particularlyGM concerns have been incorporated into thisbroader movement, policy issues associated withGM and GM-free food markets are more urgent.

This urgency is further heightened by the cur-rent (early 2001) rise in concern over a related foodissue, the ‘Mad Cow’ disease issue, in a number ofEuropean countries. As there are more reports of theincidence of this disease and of related incidence ofCreutzfeldt-Jakob disease in human populations,confidence in governments’ capacity to monitor andprevent food-related illnesses has fallen. This loss ofconfidence in food safety and regulatory agenciesspills over to biotechnology issues associated withthe environment. It is perhaps not an exaggerationto suggest that public confidence in food safety andregulatory agencies was, particularly in Europe,lower at the end of the 20th century than at almostany other time during the century.

All parties engaged in agricultural biotech-nology activities – the firms developing biotechproducts, the farmers producing food and other

1

Introduction

Robert E. Evenson, Vittorio Santaniello and David Zilberman

© CAB International 2002. Market Development for Genetically Modified Foods(eds V. Santaniello, R.E. Evenson and D. Zilberman)

products, the food and related agribusiness industri-al firms and the consumers of food – will be affectedby changes in regulatory, trade and food safetyregimes. The present system is in disequilibrium.Changes are rapidly being made. Economists have anopportunity and a responsibility to inform and influ-ence these changes to produce a new equilibriumthat is in the public interest in all countries. This newequilibrium may well take different forms in differ-ent countries, but international issues are involved.

It is difficult to predict, at this point, how themove towards a new equilibrium will unveil itself.We almost certainly will see strong labelling require-ments and segregated markets. The current GMproducts are being sold as ‘cost-saving’ products tofarmers. Future products will very likely have foodquality elements for consumers. As price differen-tials and quality differentials become available toconsumers, new equilibria will emerge. The foodindustry has a record of success in introducing manynew products into food markets each year.

The acceptance of biotech products in thehealth field suggests that consumers are likely toaccept GM products that they believe contribute totheir welfare. As new GM foods incorporate desir-able health-related features, it is quite likely thatthey will gain consumer acceptance. Recent devel-opments in Europe indicate that the scientific estab-lishment is attempting to develop better informa-tion for the public regarding safety issues. With therecent publication in Science and Nature of theHuman Genome, a landmark in biological sciencehas been achieved. There is little doubt that a scien-tific revolution is underway and that it will affect theway we do science and the way we produce technol-ogy in the future.

The International Consortium on AgriculturalBiotechnology Research (ICABR) hosted the fourthin a series of conferences on Economics ofAgricultural Biotechnology at Ravello, Italy, on24–28 August 2000. Papers presented at that con-ference (and at the preceding conferences as well)addressed many of the relevant economic policyissues inherent in the move to a new market equi-librium. A subset of those papers is included in thisvolume, which addresses market development issuesin developed countries, primarily in Europe andNorth America. This volume focuses on consumerreactions to GM food information and regulatoryissues, farmer acceptance of biotech products, andchanges in industrial organization in the life scienceand food sector.

The volume is organized in four parts. Part Iincludes chapters evaluating consumer attitudes toGM foods. Part II addresses the acceptance by farm-ers of biotech products. Part III addresses the role ofinformation systems and of associated regulatorydevelopments. Part IV addresses industry structureissues.

The studies reported in this volume do notconstitute a comprehensive treatment of all policyissues associated with GM product market develop-ment. The industries and economic entities are deal-ing with changing conditions and problems contin-uously. In this context, these studies should informand improve this complex process.

The initial chapter by Burton et al. provides ageneral framework for assessing the nature of thenew equilibrium under conditions of market devel-opment as opposed to an equilibrium produced bya high degree of regulation and prohibition of pro-duction and sale of GM food products. The alterna-tives of a partially regulated market outcome withlabelling, segregation and certification and a highlyregulated market outcome with trade prohibitionsand selective food prohibitions are real. The failureto move towards a partially regulated market out-come will lead to the alternative highly regulatedoutcome.

Chapter 1 sets forth the fundamentals for mar-ket development, with labelling and segregation. Amodel is developed and applied to a GM crop(canola). While the model itself is technical, it isinstructive in that it illustrates the types of premi-ums and discounts in the food markets that emergefrom consumer preferences, which are then reflectedin farm price premiums and discounts for canolawith and without GM content. The model incorpo-rates costs of identity preservation. Alternative sim-ulations of the model illustrate the complexities ofmoving to a new market equilibrium. The simula-tions show the importance of identity preservationcosts and of the incorporation of a technology fee bythe suppliers of the biotech seeds. Net welfare meas-ures are also calculated.

Part I of this volume includes five chapters address-ing consumer attitudes and preferences. As the firstchapter demonstrates, if sufficient consumer prefer-ence exists, premiums for non-GM goods willemerge (alternatively, discounts for GM foods willemerge). The magnitude of these premiums (dis-counts) will ultimately depend not just on the cur-rent attitudes of consumers, but on attitudes and on

2 R.E. Evenson et al.

a ‘willingness to pay’ non-GM premiums over a longperiod of time. One of the difficulties of assessingconsumer attitudes under conditions where the pre-miums are not actually paid is that there is uncer-tainty about how consumers will actually behavewhen faced with premiums.

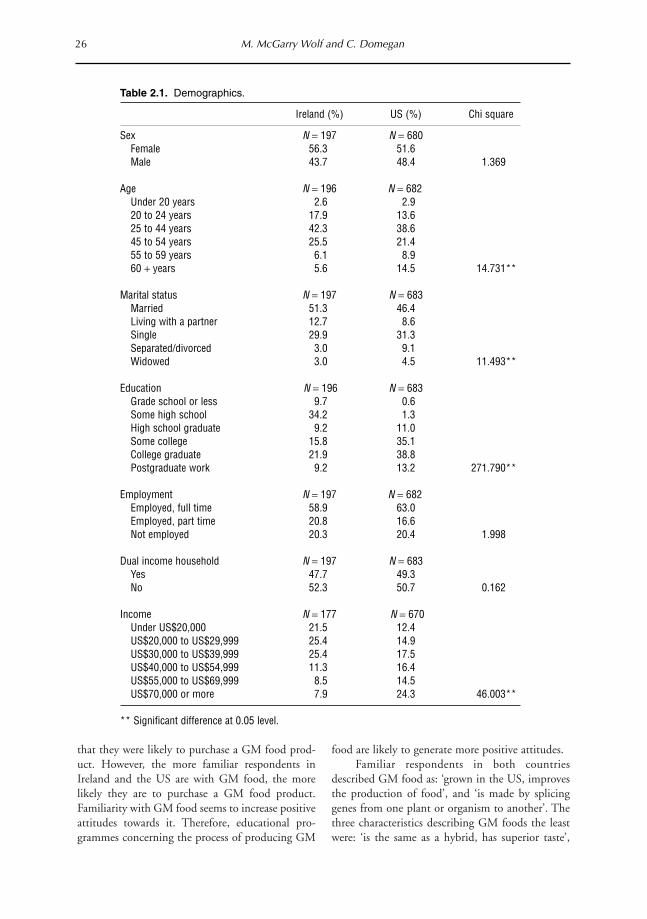

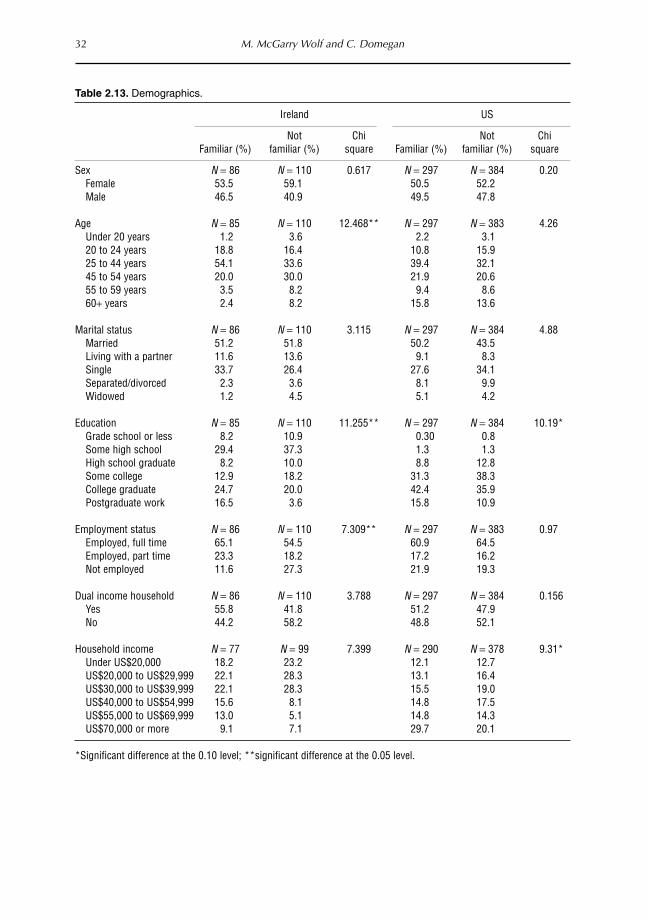

Chapter 2 (Wolf and Domegan) reports a com-parison of consumer attitudes in the USA andIreland. The authors use market survey researchtechniques to develop this comparison. Their sur-veys sought to determine differences in Europeanand US attitudes. Interestingly, the chapter reports asimilar level of familiarity with GM goods betweenconsumers in the USA and Ireland. A minority ofconsumers in both countries indicated a willingnessto pay a non-GM food premium. Consumers inIreland also attributed more negative attributes toGM foods.

Chapter 3 (Verdurme et al.) reports findingsfrom a literature survey, group discussions and in-depth interviews of European consumers where adistinction is made between premium branded andnon-branded food products. This study finds thatconsumer attitudes towards GM technology weremore negative than attitudes towards specific GMfood products. The chapter also reports that, amongGM products, premium branded products are bet-ter accepted than generic products.

Chapter 4 (Hanf and Böcker) focuses on thenon-GM premium and the perception of health andother dangers associated with GM foods. Theauthors conclude that consumers are likely to con-tinue to hold attitudes regarding dangers that aredifficult to overcome with cost reductions. They alsoconclude that high quality GM foods are unlikely toovercome consumer hesitation regarding GMfoods.

Chapter 5 (Mendenhall and Evenson) reports asmall survey of consumers’ ‘willingness to pay’ a pre-mium for non-GM foods. This survey illustrates animportant dimension of market development.Consumers will ultimately have to pay a premiumsufficient to cover the identity preservation (segrega-tion and certification) costs associated with non-GM foods if these markets are to develop. Theauthors find that consumers want labelling but thatnot all are willing to pay a premium for non-GMfoods. The chapter concludes, however, that forfood products where the ratio of consumer value tofarm value is high, even small non-GM premiumscan support non-GM markets.

Chapter 6 (Spetsidis and Schamel) provides a

review of studies of new product development anddiscusses consumer acceptance of GM food prod-ucts in the context of this literature. The chapterprovides a useful European perspective to GM foodissues.

The studies in Part I of this volume are gener-ally based on attitude surveys and related market sur-vey techniques. To date, few true market experimentswhere non-GM foods are actually priced at a premi-um have been conducted. As non-GM premiums(GM discounts) emerge, more studies of consumerattitudes, and especially of ‘willingness to pay’, willbe required to establish guidelines for non-GMproduct market developments. These new studieswill be informed by the studies reported here.

Part II of the volume includes eight chaptersaddressing farmer acceptance and farm profitabilityof ag biotech products. Three chapters (7, 8 and 9)deal with farmer acceptance of bovine somatotropin(bST), one of the earliest biotech products intro-duced to farmers. Other chapters deal with cropbiotech products. These chapters find that farmershave adopted several biotech products rapidly. In thecase of some crop products, diffusion rates havebeen comparable to hybrid maize diffusion rates inthe 1930s and green-revolution wheat and rice dif-fusion rates in the 1960s.

Farmer acceptance of biotech products hasbeen driven by profitability. However, acceptance ofthese products to date has been under conditionswhere few GM discounts have been in place. Thechapters are important in indicating the extent ofprofitability and hence of the possible effects of GMdiscounts on this market.

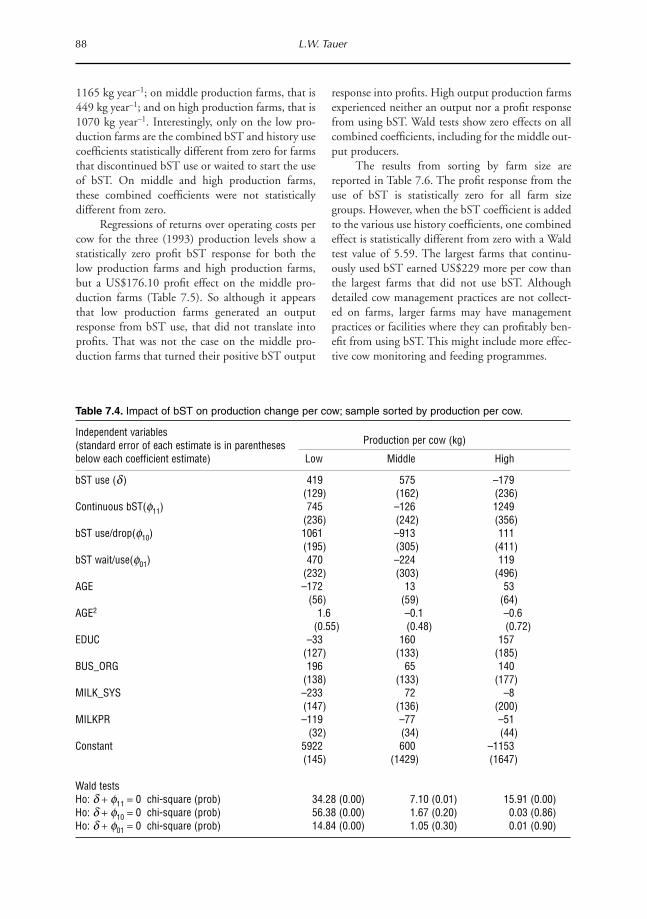

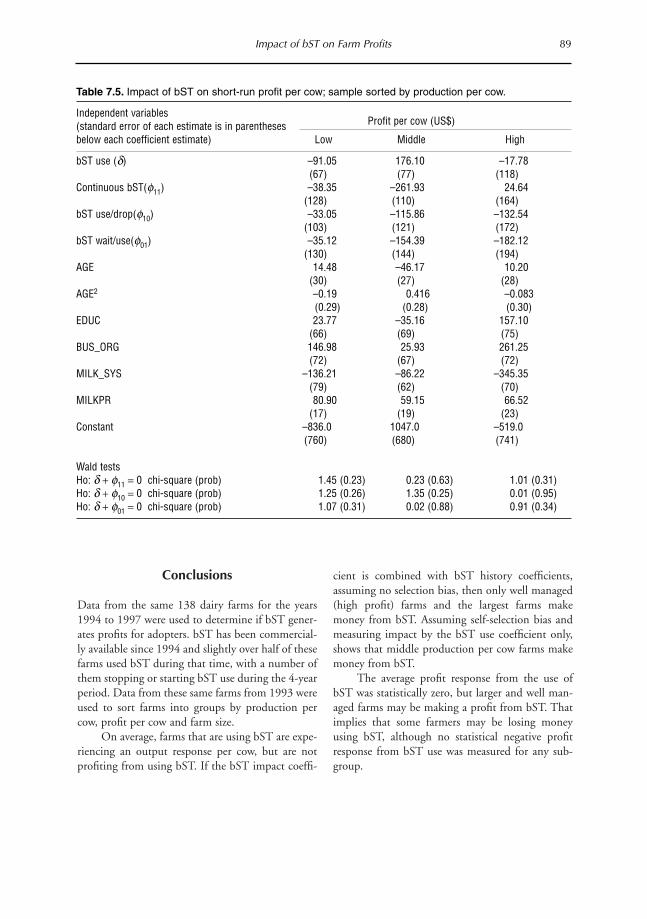

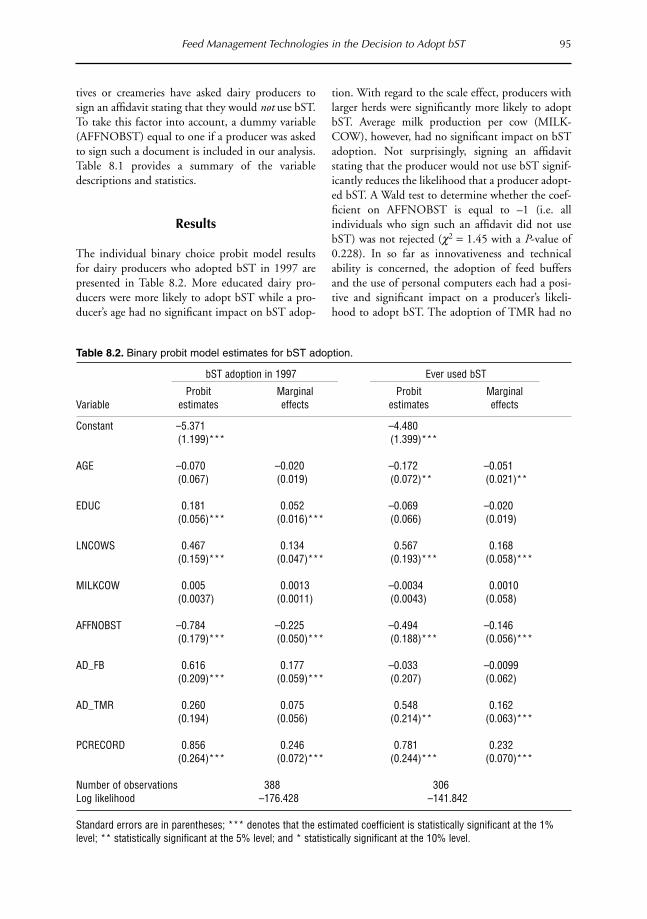

Chapters 7 and 8 report bST adoption in NewYork (Chapter 7, Tauer) and California (Chapter 8,Henriques and Butler). The New York study reportsrepeated surveys of 138 dairy farms for the years1994 through 1997. Statistical procedures for selec-tivity bias are utilized in the study. This study findsthat bST use results in increased milk productionper cow, but that higher than average profits forbST are generally not being realized. The studyfinds, under one statistical procedure, that only thewell-managed, high-profit farms make profits frombST. The California study of bST adoption consid-ered the complementary use of feed managementpractices. This study concluded that feed manage-ment techniques are important to bST adoption and use. The study has implications for extensionservices.

Introduction 3

Chapter 9 (Jarvis) provides a comprehensivereview of bST adoption in the USA and in 16 othercountries where the technology has been adopted.This study also concludes that bST rewards man-agement skills and higher quality feed. Attitudinal aswell as economic factors are considered in the study.

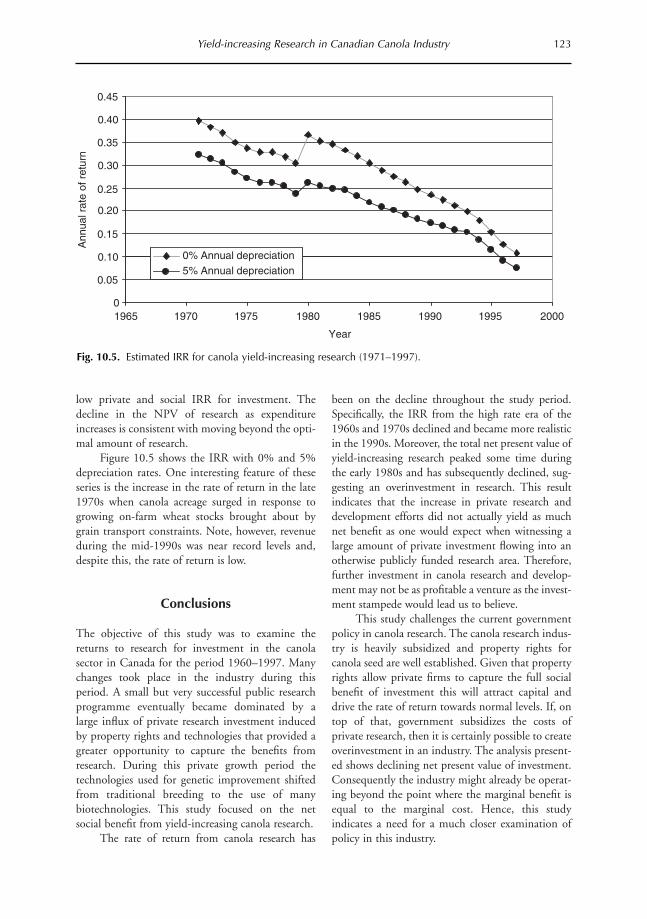

Chapters 10–13 report evaluations of cropbiotech adoption. Canola is the subject of Chapter10 (Gray et al.). Canola is exceptional in that itemerged from minor crop status in the 1950s to thatof a major crop in Canada today. Plant breeders’rights were important in encouraging private sectorinvestment in canola research. Chapter 10 reportsestimates of rates of return to canola research. Itconcludes that biotechnology has yet to producemeasurable high social rates of return in the canolasector.

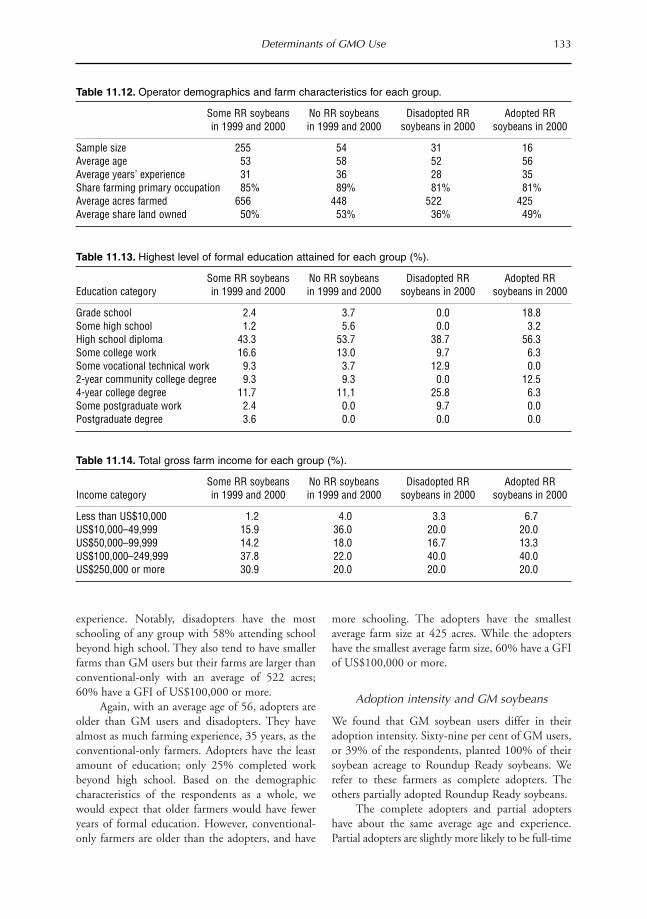

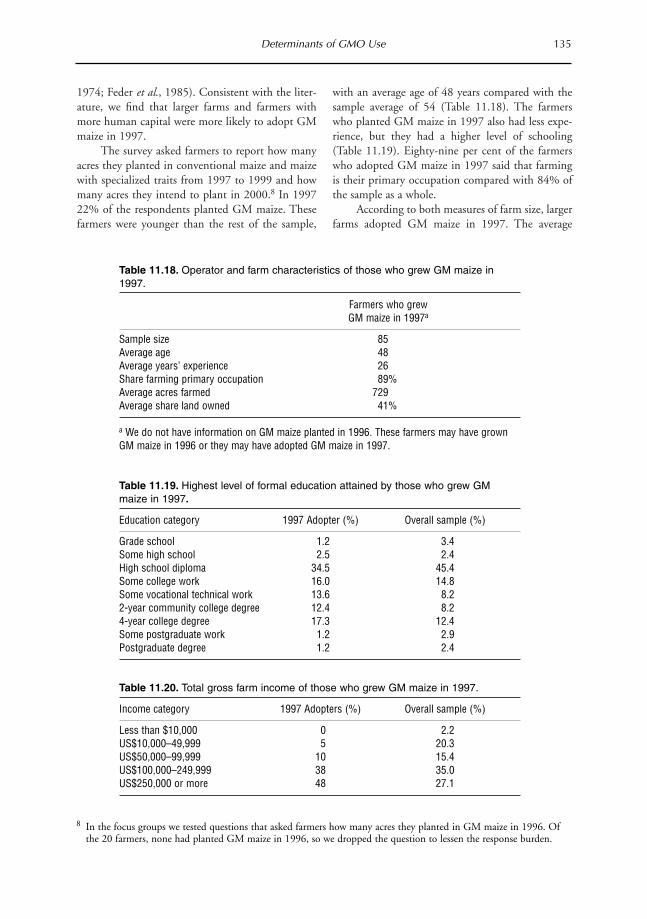

Chapter 11 (Alexander et al.) reports a study of adoption of GM maize and soybeans by Iowamaize–soybean farmers. The study concludes thatearly adopters of GM maize and soybean fit the styl-ized facts of early adopters for other agriculturalinnovation.

Chapter 12 (Darr and Chern) reports a surveyof Ohio farmers designed to measure attitudes,beliefs and behaviours. Adoption rates are estimatedfor GMO maize and soybeans.

Chapters 13 and 14 report assessments ofadoption of GM crops in Europe. Chapter 13(Niemi and Virolainen) reports adoption rates ofGM crops in Finland and concludes that GM tech-nology will lower farm costs, increase yields andprovide improved insurance against pests. The chap-ter also considers the implications for consumersand for farm income.

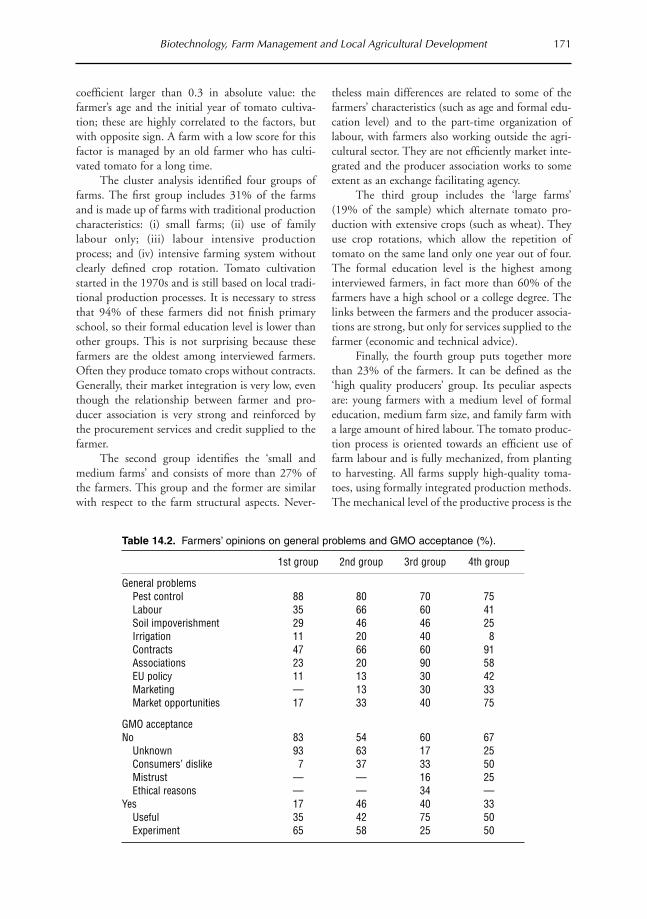

Chapter 14 (Gorgitano and Sodano) evaluatesthe potential effects of biotechnology on theprocessed tomato sector in southern Italy. This studyconsiders local agricultural development issues.

Part III of the volume includes eight chaptersaddressing the information, regulatory and institu-tional issues associated with market development.

Chapter 15 (Huffman and Tegene) provides ananalytical review of models of information and com-munication of information. Verifiable informationis critical to efficient market development. It canreduce the scope for disputes and uncertainty. Oneof the responsibilities of social scientists is to objec-tively evaluate data and provide policy makers withanalytical insight. The development of more verifi-able information will have considerable social value.

Chapter 16 (Smyth and Phillips) also address-es the role of information in shaping the regulatoryenvironment for biotech products. A contrastbetween responses to controversial scientific studiesin the USA (where regulatory agencies have highcredibility) and the UK (where they do not) isdrawn. The chapter concludes that the UK regula-tory responses to consumer concerns were likely tobe more costly and less efficient than the US regula-tory response to similar concerns.

Chapter 17 (Marks et al.) focuses on how therisks of ag biotech have been communicated via themedia in the USA and UK. The media can be seenas one of many influences in the overall acceptanceof ag biotech by consumers. Acceptance has differedbetween the two countries and media reporting haslikewise differed significantly.

Chapter 18 (Marks et al.) documents a poten-tial gap in perceived food safety risks and benefitsbetween food scientists and reporters. The authorsfind, from the journals investigated, that no safetytests of GM foods have been published in them and,hence, are not in the public domain. A tentativeconclusion is that the media (and the public) do nothave easy access to studies of the safety (or lackthereof ) of GM foods from peer-reviewed sources,although this conclusion cannot be generalized to alljournals.

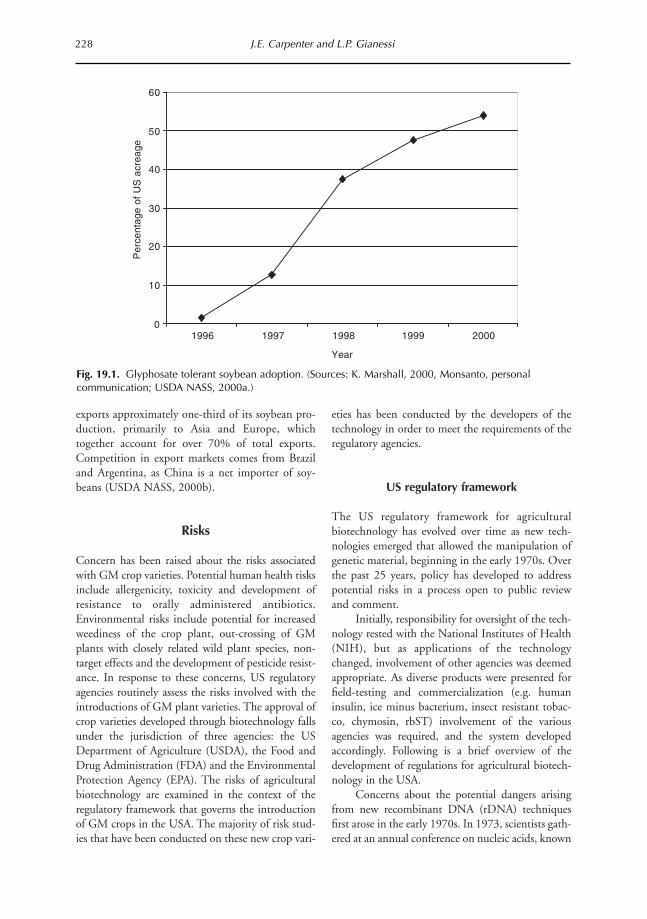

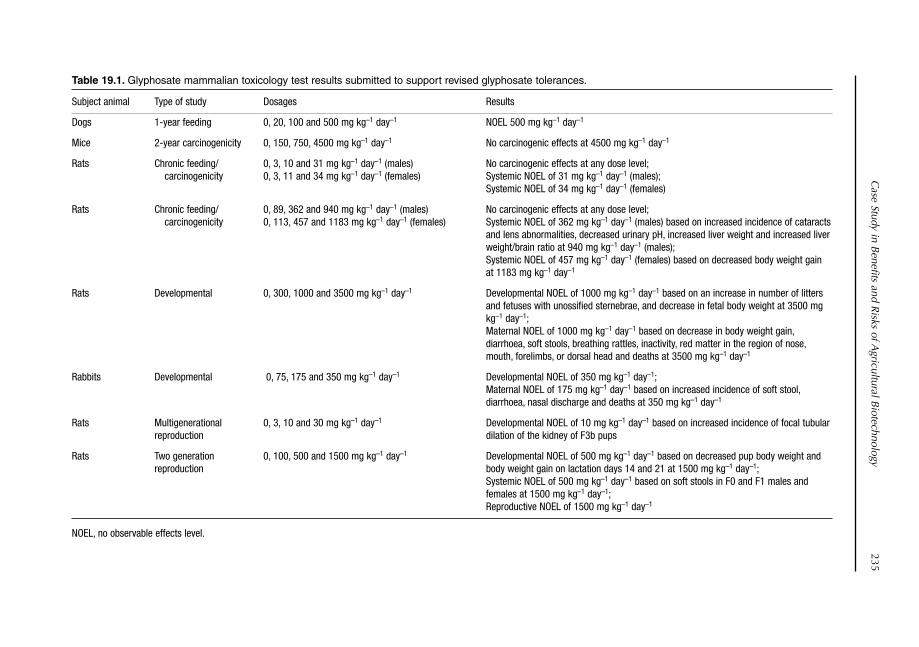

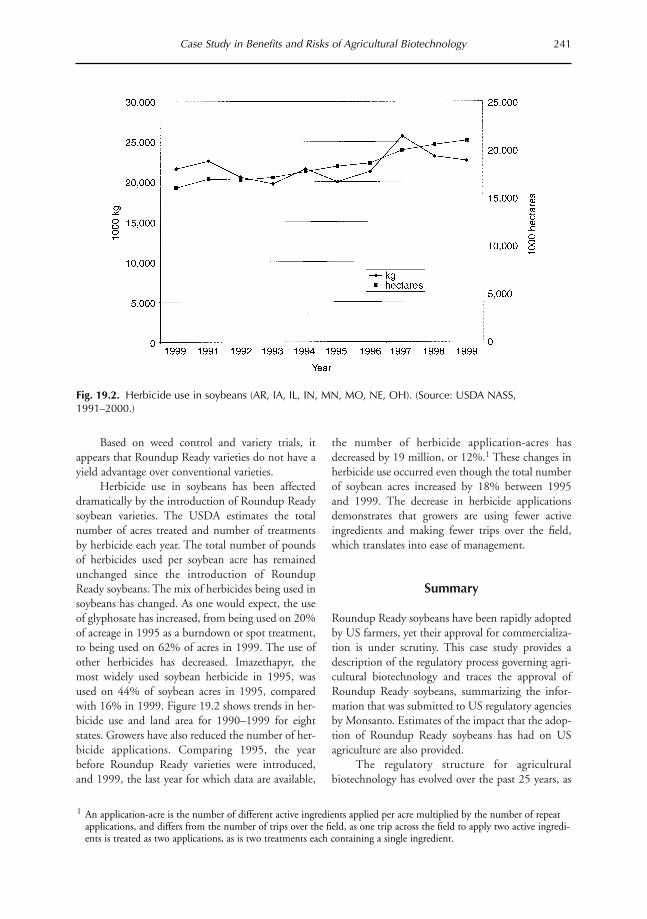

Chapter 19 (Carpenter and Gianessi) reports acase study of risk assessment practice in the case of amajor agricultural biotech product, Roundup Readysoybeans. The study concludes that ‘no indication ofgreater health or environmental risks were foundcompared to those associated with conventionalvarieties’. The study also reports estimates of eco-nomic benefits from reduction in weed controlcosts.

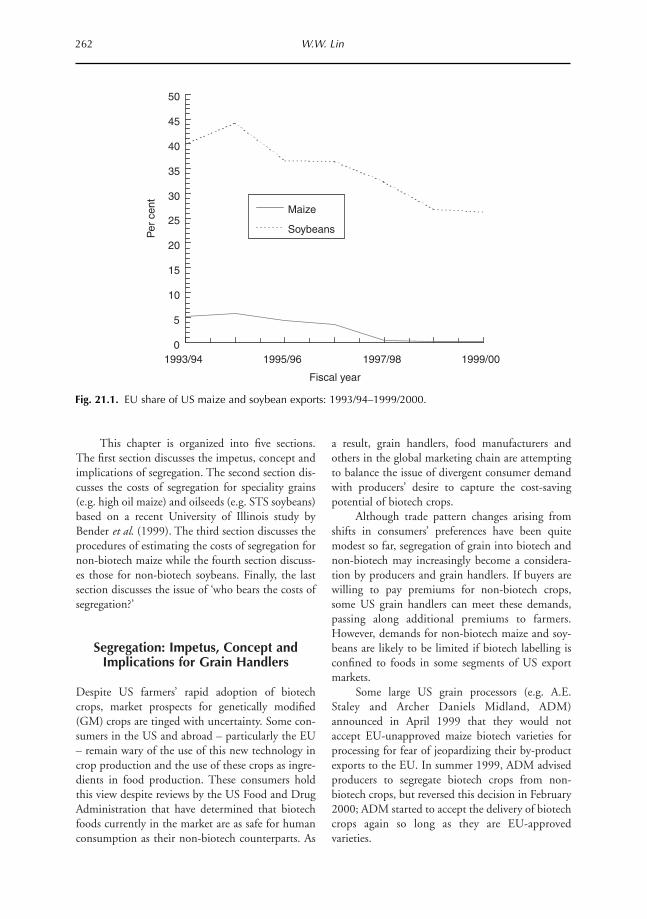

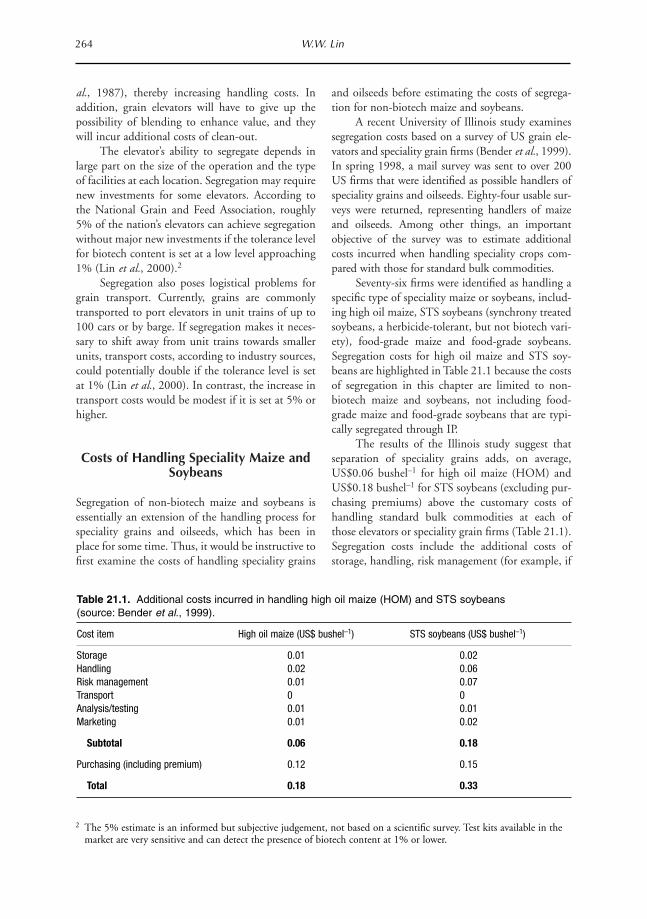

Chapters 20 and 21 report studies addressingtwo important components of identity preservation:labelling, and segregation and certification costs.

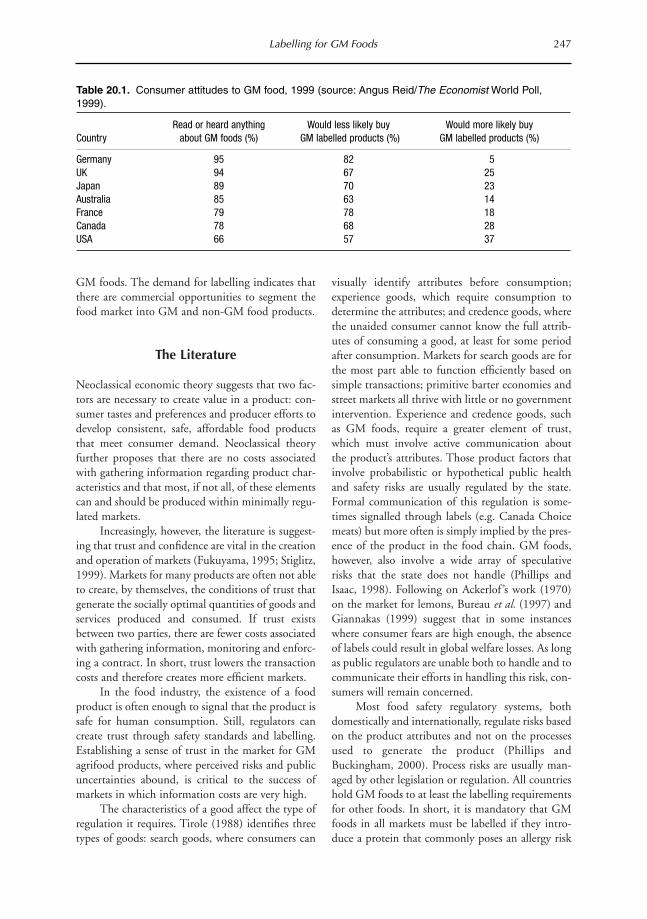

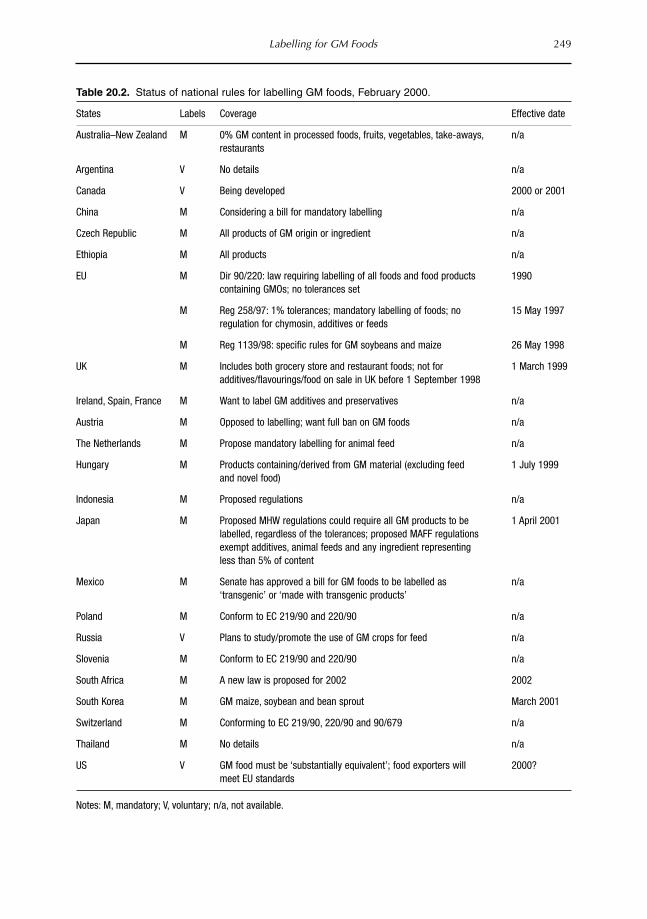

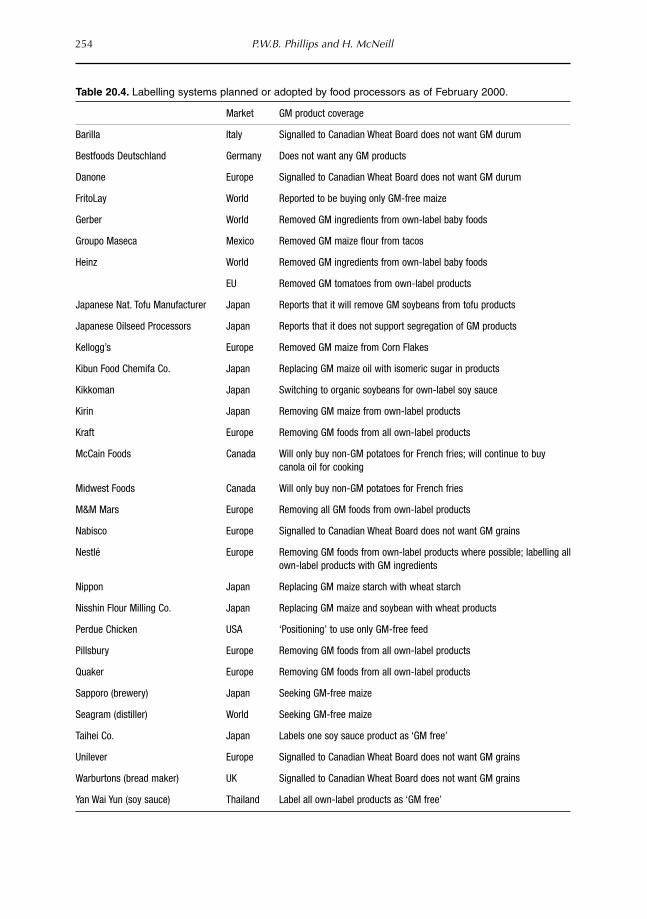

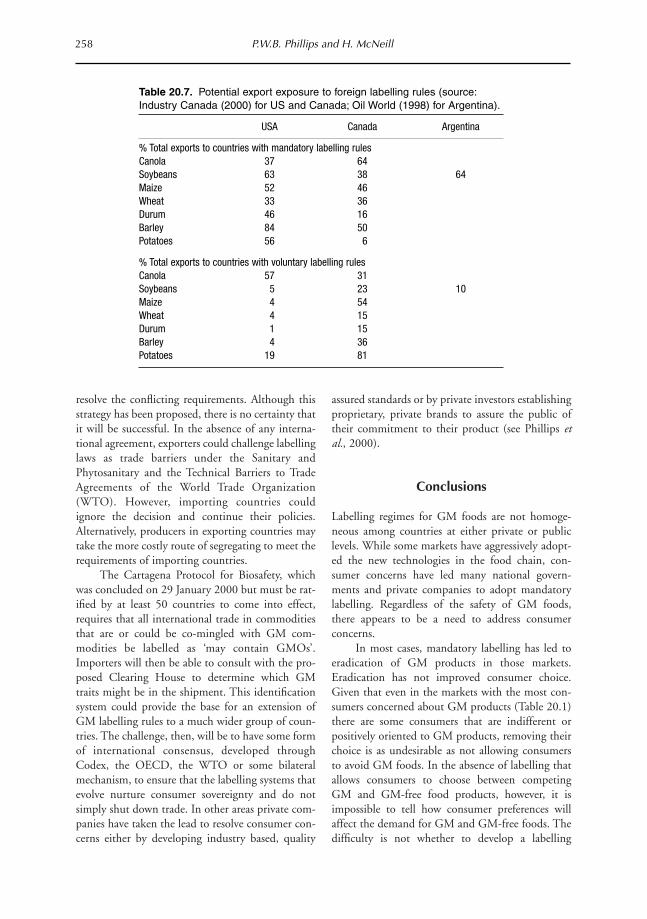

Chapter 20 (Phillips and McNeill) reviews thecurrent state of labelling requirements in a numberof countries. The study reports that 18 countriesplus the EU, 29 manufacturers, 21 retailers and sixrestaurant chains have signalled intentions to adoptvoluntary or mandatory labels for GM foods. Thestudy found little convergence in labelling standards.

Chapter 21 (Lin) provides information on thecosts of segregation and certification that are essen-tial to the development of non-GM food markets.There are very few data on segregation costs, andthis study provides badly needed data. It concludes

4 R.E. Evenson et al.

that costs depend on tolerance levels for biotechcontent. The chapter also discusses implications forthe grain handling industry.

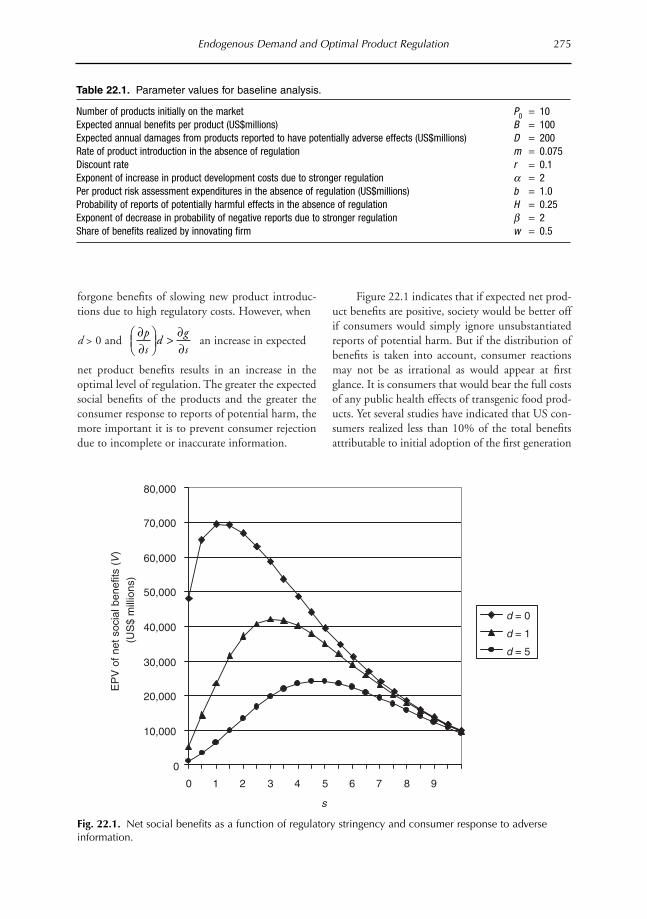

In Chapter 22 (Artuso), a formal model ofoptimal product regulation is presented. The linkbetween consumer risk perceptions and regulatorypolicy is emphasized. Under certain conditions it is shown that regulatory requirements may be called for other than those based on scientific riskassessment.

Part IV of the volume includes four chaptersaddressing industrial development to date. It shouldbe noted that the ag-biotech industry is in a state ofdisequilibrium at present.

Chapter 23 (Boland) examines agricultural or‘Life Science’ firm performance. The techniqueapplied is to determine value of Tobin’s q (the ratioof a firm’s market role to its asset value) for firms inthe ag-biotech industries. All firms studied had qvalues greater than one with pharmaceutical firmshaving the highest values.

Chapter 24 (Traill and Duffield) examines theEuropean agro-food biotechnology industry. Theauthors note that the industry has developed‘alliances’ with universities and specialized or dedi-

cated biotech firms. The chapter relies on the‘dynamic capabilities’ business strategy model tosuggest that these alliances are likely to be main-tained over long periods.

Chapter 25 (Lavoie and Sheldon) also exam-ines the dynamics of the biotechnology industry.The role of foreign-based multinational firms in theUSA is considered. The US comparative advantagein these industries is analysed in a real optionsframework. This framework explains the earlieradvantage of US firms. It is also used to explain whyforeign multinationals find it attractive to be in thenew consolidating industrial structure in the USA.

The final chapter in the volume, Chapter 26(Weaver and Kim), addresses industry structure inan integrative supply chain assessment. As noted inthe early part of this review, ag-biotechnology deci-sions made in one part of the supply chain (thebiotech-supplying firms) have implications for otherparts of the supply chain (farmers and the foodindustry). At present, important tensions andincompatibilities must be resolved between differentparts of the supply chain. Chapter 26 offers insightsfor managing technologies for different parts of thesupply chain.

Introduction 5

1 As reported by Thomas Walkom, The Toronto Star, Editorial, ‘GMO folks have a little surprise from Alberta’, 2 May 2000 (www.plant.uoguelph.ca/safefood).

Introduction

Up until the end of the 1990s the future for geneti-cally modified organisms (GMOs) looked bright.Plantings of transgenic soybean, maize, cotton andcanola by American, Argentine and Canadian farm-ers set new benchmarks for the rate of adoption of anew agricultural technology. Virtually the onlycloud on the horizon was widespread consumerresistance to GMOs in Europe. Industry assumedthat this was a temporary problem that could beovercome by an ‘educational programme’ that pro-vided more information about the benefits ofGMOs (Marshall, 1998).

Now, though, the outlook has changed.Consumer resistance to GMOs has intensifiedrather than waned in Europe. Furthermore, it hasnow spread to many other countries as well. Even inCanada and the USA, there are press reports ofsupermarket chains stocking items labelled as genet-ically-modified (GM)-free.1 Moreover, the effect ofeducation programmes may be questionable givenfindings by Zechendorf (1998) that suggest con-sumer acceptance depends on people’s socio-cultur-al attitudes as well as their knowledge about thebenefits of biotechnology.

Despite the uncertainty surrounding consumeracceptance of GMOs, there are lessons to be learntfrom studies of innovation adoption. First and fore-

most, for an innovation to be adopted enduringly, itmust not only create value but also must delivermeaningful net benefits to all potential adopters.That is, the benefits of adoption must be distributedall along the supply chain, including to consumers.

Genetically engineered crops that are alreadybeing grown commercially include tobacco, cotton,soybean, corn/maize, canola/rapeseed, tomato andpotato. In a review, James (1999) noted that seventransgenic crops were grown commercially by 1996on approximately 2.8 Mha, mostly in the US andCanada. Between 1996 and 1998, there was a fur-ther increase in the global area of transgenic crops to27.8 Mha (James, 1999). As James (1999) pointsout adoption rates have been some of the highestever for new agricultural technologies, and reflectgrower satisfaction with significant benefits rangingfrom more flexible crop management, higher pro-ductivity and a safer environment through decreaseduse of conventional pesticides and herbicides.

To date, the overwhelming majority of GMfoods are the products of first generation GM crops.The principal transgenic traits in 1999 were herbi-cide tolerance, insect and viral resistance, and hybridtechnology (James, 1999). As explained by Fultonand Keyowski (1999a), these ‘input traits’ loweraverage costs of production through some combina-tion of reduced costs of control of, and/or smallerlosses from weed, pest and disease infestation, and

7

1 A Way Forward forFrankenstein Foods

Michael Burton, Sallie James, Bob Lindner and Jo PluskeFaculty of Agriculture, University of Western Australia, Perth, Australia

© CAB International 2002. Market Development for Genetically Modified Foods(eds V. Santaniello, R.E. Evenson and D. Zilberman)

through increased yields. Because these beneficialtraits can be introduced into a plant without dis-turbing the rest of the plant’s genetic code, theresulting varieties are potentially much more prof-itable for growers. Realized profitability will fallshort of potential profitability to the extent that aproduct price discount applies to the GM crop,and/or to the extent that growers have to pay a pre-mium to grow the GM crop relative to comparable‘conventional’ crop varieties. Even though thesecrops may deliver lower costs of production to farm-ers, they typically deliver no or least negligible ben-efits to consumers2 unless some of the lower pro-duction costs are passed on as lower retail prices forGM food relative to non-GM food. This has nothappened to date, and will not happen until thenecessary preconditions of retail labelling under-pinned by a credible and verifiable system of identi-ty preserved production and marketing are imple-mented.

Second generation or quality enhanced GMcrops, most of which are still under development,incorporate crop attributes that provide direct bene-fits to the consumer, or in some cases to intermedi-ate producers. Delayed ripening tomatoes, oilseedrape with modified fatty acid, high oleic acid soy-bean, and carnations with extended shelf-life andmodified colour, are examples of second generationcrops that are already in commercial production.Some companies are predicting that the third gener-ation of GM crops will be nutraceuticals.Nutraceuticals are foods that prevent or treat dis-eases or otherwise provide medical or health bene-fits. GMOs that include genes coding for pharma-ceutical drugs are touted as GM crops of the future.In contrast to first generation crops, qualityenhanced crops have not been widely adopted so far(James, 1999).

Alerted by activists, consumers are increasinglyaware of public health concerns about GMOs andthis appears to be the most important considerationregarding their development and use. Within thescientific community, there also are worries aboutthe long-term effects on human health (for example,through the use of antibiotic resistant marker genesand the risk of allergen transfer) and the environ-ment from widespread use of genetically engineeredcrops. Other concerns about GM crops include theinfluence of multinational seed companies on coun-

tries’ economies; and the possible demise of thesmall-scale farmer. While various special interestgroups share these concerns, it is a growing reluc-tance to eat GM food by the general public that islimiting the size of the market for GMOs, threaten-ing the realization of substantial value creation fromgenetic manipulation technologies and perhaps eventhreatening the financial viability of some life sci-ence companies.

Some advocates of GM foods point out thatconsumer reactions to real price differentiatedchoices (as opposed to hypothetical choices)between conventional (i.e. non-GM) and GM foodshave yet to be observed (see, e.g. Caulder, 1998) fora significant number of foodstuffs. They anticipatethat when consumers are more regularly exposed toGM foods, and compare them favourably (or at leastneutrally) with conventional foods, the anticipatedprice differential between GM and non-GM foodswill create a viable market for GM foods (Caulder,1998). If correct, such a response will belie the sur-vey results that suggest such a market is likely to besmall at best.

Work completed by Gamble et al. (2000) indi-cates that when second generation foods becomeavailable, the market for these foods may be largerthan for first generation foods as consumers appre-ciate the extra direct benefits they offer (such aslonger shelf-life, or enhanced nutritional value). It ispossible, depending on the extent of extra benefitsand the willingness of consumers to accept any per-ceived risk associated with the technology, that theseproducts might command a price premium overconventional foods.

That is, for now, a hypothetical scenario. Theimmediate challenge facing producers and advocatesof GM foods is to convince consumer and environ-mental groups that regardless of its generation, anyfood produced using recombinant gene technologyis safe to consume and to produce. General accept-ance of second and third generation crops will notbe realized if the market potential of first generationcrops is thwarted by health and environmental fears,regardless of their legitimacy.

For the biotechnology industry, there is a clearlesson about how to solve the consumer ‘problem’and current lack of demand for GMOs. Trying toallay consumer concerns about the health risk fromeating GMOs by relying on scientific argument has

8 M. Burton et al.

2 There may be indirect benefits to consumers by knowing farmers benefit from lower on-farm costs or by valuingreduced environmental costs.

not, and will not succeed. Consumers want to beassured about the origins of their food, and waysmust be found to allow them to knowingly choosebetween GM and non-GM foods. Moreover, prod-ucts from first generation GM crops will have to sellat a discount (relative to the GM-free equivalents) toinduce significant numbers of consumers to buythem.

The technology component of GM foods is,for our purposes here, a credence attribute. Thismeans that the technology used to produce a (firstgeneration) food is indistinguishable to the con-sumer both before and after purchase (Caswell andMojduszka, 1996; Caswell, 2000). Thus the onlyway a non-GM food producer is able to elicit a pricepremium for his or her product is by indicating thestatus of the product by the use of a label supportedby a credible testing and assurance programme.

So long as identity preservation remains hap-hazard and labelling regulations ambiguous, pricepremiums for any type of good – GM or non-GM,first, second or third generation – are likely to besmall.3 That is, so long as there is no way of differ-entiating between types of good, consumers have nocertain or reliable way of knowing whether the foodthey eat is GM-free. Producers of GM-free productsare unable to advertise (with any integrity) the sta-tus of their product and, as such, rational consumerswill be unwilling to pay more than the ‘non-seg-mented’ market price. This is especially true for firstgeneration GM foods since there are no enhancedattributes from which consumers could derive extra(direct) benefit. Consumer rejection of GM foods isrational if they are not offered it at a lower price.After all, what rational consumer would accept a‘bad’ characteristic in the absence of no offsettingbenefits such as a lower price?4

To deliver a price premium for non-transgenicfood, industry must provide verifiable labelling andmaintain credible identity preserved production andmarketing (IPPM) systems, thus facilitating choiceby consumers of food products that align with theirpreferences. However, work completed by KPMG(1999) indicated that the introduction of an IPPMsystem could prove to be prohibitively expensive.This conclusion, however, is difficult to sustain

given the current widespread practice of segregatingdifferent grades of non-GM crops to separate high-er added value products from other commodities inorder to exploit niche markets. In the case of GMcrops, it is the absence of genetic engineering infood that is the key ‘attribute’ being demanded, soonly non-transgenic food would need to be segre-gated in the marketing chain, labelled and subject tosome form of verification. A particularly appositecase is marketing systems for organic food.

Buckwell et al. (1999) estimated that theincreased cost of segregating GM products couldrange between 5 and 15% of the usual farm gateprice. Despite this cost, the same authors explainthat there could be benefits both to consumers andto farmers as long as consumers are willing to paythe added cost of separating GM from non-GMcrops. Labelling is likely to be the most efficientalternative because market forces would determinethe acceptance of the new technology. So long asmost people demand food that is GM-free, theadvantage of labelling may be minimal, andarguably even unnecessarily expensive if IPPM costsexceed cost savings from growing first generationGM crops. If and when demand for non-transgenicfood declines in the longer run to the point where itbecomes a speciality product, then requiring com-pulsory labelling of GMOs is likely to prove undulycostly. Ultimately, the magnitude and cost structureof an IPPM system will determine, inter alia, themarket determined equilibrium level of the pricedifferential between GM and non-GM foods atfarm gate, and at retail level.

The rest of this chapter reports the findingsfrom some preliminary analyses of the impact onprices at farm gate and at retail of introducing a sys-tem of retail labelling of non-GM food. Estimatedprice differentials obviously depend on the likelycosts of introducing and maintaining a credibleIPPM system. Of interest here is the nature of mar-ket segmentation and price differentiation after afirst generation GM crop (canola, in this example) isproduced and marketed. The simple model that fol-lows explores some possible scenarios for futureprices for GM and non-GM canola under a few keyassumptions. Firstly, the GM crop is of the first

A Way Forward for Frankenstein Foods 9

3 Price premiums for non-GM food will, of course, be market determined, and depend on the proportion of supplythat is non-GM. Recent market reports for maize and soybean have, however, reported premiums of 10–15% and5–35%, respectively (Miranowski et al., 1999).

4 This clearly ignores the possibility of consumers buying GM food because they derive utility from knowing it hasbeen produced using techniques beneficial to the environment.

generation such that consumers will not purchasefood produced using GM canola unless it is sold ata lower price than conventional canola. Clearly themodel would need to be adjusted to allow for anypositive attributes associated with GM foods, suchas those in second or third generation GM foods.Secondly, the production function for both types offoods is assumed to be constant returns to scale witha constant elasticity of substitution. The market ischaracterized by perfect competition. Identitypreservation costs are presented as simple fixed costsin each market.5

Model Specification

Formal modelling of the market with segregatedproduction/consumption will be presented in twoparts. In the first, a simplified model is developedwhich allows for an analytical solution, but is restric-tive. In the second, a more general model is present-ed which can be solved numerically, but not analyt-ically. These models are similar in structure to thosedeveloped by Fulton and Keyowski (1999b) andFalck-Zepeda et al. (1999) but provide a number ofextensions. There is a more formal representation ofthe technology than used in either. Our models alsoremove the restriction of a fixed output level used byFulton and Keyowski, and do not assume that allconsumers accept the product, as assumed by Falck-Zepeda et al.

The simple model

Representative demand functions for the two typesof good, non-GM (subscript, n) and GM (subscript,g) are assumed to be simple linear functions of (nor-malized) own price. It is assumed that at the indi-vidual level, consumers make a decision to purchaseeither one or the other, but not both. Hence, theprice of the alternative form of the product is not anargument to the representative demand functions:

dn = a0 + a1Pn (1.1)

dg = a0 + a1Pg (1.2)

However, the relative price of the two goods doesdetermine which form of the product is selected. As

the good under consideration is a first generationGM crop, there are no intrinsic benefits in con-sumption. Hence we assume there will be nodemand for the GM version if the prices of the twoforms are equal. This is consistent with the argu-ment above that even the slightest residual percep-tion of risk from consuming the product, or concernabout potential non-consumptive issues (on farmecological effects for example) will lead consumersto reject GMOs unless there is price differential.

Assume that there is some latent index of con-cern, c, and some underlying discrete choice processwhich means consumer i will consume the GMproduct if:

f (Pg / Pn) < ci (1.3)

That is, if the price differential is large enough theywill be induced to change. Assuming the functionf (•) is linear in the price ratio, and that c is distrib-uted across the population as a uniform variablefrom 0 to 1, the share of the population that con-sumes non-GM is determined by:

Sn = Pg / Pn (1.4)

With no loss of generality, normalizing the con-sumer population size to unity gives aggregatedemands of:

Dn = (a0 + a1Pn) Pg / Pn (1.5)

Dg = (a0 + a1Pg) (1 – Pg / Pn) (1.6)

The supply side of the model is represented by themarginal cost of production:

MCn = b0 + b1(Qn + Qg) (1.7)

MCg = b0 – bt + b1(Qn + Qg) (1.8)

where bt is the cost advantage enjoyed by the GMcrop. Assuming b1 is positive implies a rising mar-ginal cost, determined by the aggregate productionof both crops. Given the similarity in the two goods,it would be expected that there will be interactionsbetween the two goods in production, leading eitherto joint decreasing marginal productivity ofresources, or common impacts on costs through theinput markets.

Assuming profit maximization and perfectcompetition allows one to equate the marginal cost

10 M. Burton et al.

5 Market forces (specifically the relative elasticities of supply and demand) will determine the incidence of IPPM costs.The likely scenario is that farmers will have to bear part of the cost of segregating, testing and marketing of non-GMcrops and consumers will bear the rest through higher prices.

with the product price, and the market clearing con-dition of Dj = Qj allows a solution to be identified.

Defining Q as aggregate quantity (i.e. Dn + Dg)of both crops leads to:

Q = (a0+ a1Pn)Pg / Pn + (a0 + a1Pg)(1 – Pg / Pn)

(1.9)

Pn = b0 + b1Q + IPn (1.10)

Pg = b0 – bt + b1Q + IPg (1.11)

where Pn and Pg are prices at retail, and IPj is themarginal cost of identity preservation of crop j whenthe GM crop is introduced.

Substituting Equations 1.10 and 1.11 intoEquation 1.9 leads to a single equation which can besolved for Q (see Appendix I), which can then beused to identify prices and quantities of the individ-ual commodities.

The model leads to a number of intuitive con-clusions. So long as there are no identity preserva-tion (IP) costs, the extent of market penetration ofthe GM crop will be directly related to the degree ofcost advantage it enjoys. Furthermore, there will bean increase in the aggregate market for the com-modity as the average cost of producing GMOs fallsbecause the increase in the GM segment of the mar-ket will be larger than the non-GM segment it dis-places. Since marginal cost is specified to rise withincreasing aggregate output, the marginal cost andhence price of the non-GM commodity must risefollowing the introduction of the GM crop. In turn,this will cause a movement along the representativenon-GM demand curve, which will compound thereduction in non-GM demand due to the segmen-tation of the market. The greater the cost advantageenjoyed by the GM crop, the greater the size of theseeffects. Introduction of an IP cost on the non-GMproduct widens the gap between GM and non-GMprices, although the rise in non-GM prices willdepend on the elasticities of non-GM demand andsupply curves: the standard incidence argument.However, that widening will cause further restruc-turing of the market between the two crops. Theintroduction of IP costs on the GM product alonecan simply be seen as an offset for the technologicalcost reduction. If the IP cost is sufficiently large, theGM product may not be able to penetrate themarket.

If the IP costs fall on both sectors, and they arelarge enough, it is possible for both consumer prices

to rise relative to the pre-GM situation, and foraggregate consumption/production to be less. Thiswould lead to the interesting situation that aggregatewelfare would be reduced, and yet all markets wouldbe in equilibrium, and there would be no competi-tive pressure for production of GM to cease.

The model structure used here is rather restric-tive. In particular, the segmentation of the market isa linear function of the ratio of prices, and onemight expect that the expansion of the GM sectorwould accelerate as the price differential expanded.Secondly, the production side of the market is verysimplified, with no differentiation of technicalchange and input market effects on the marginalcost of production.

The extended model

Attempts to derive analytical solutions from moreelaborate models were not successful. Consequently,it was decided to resort to numerical methods toobtain solutions from a somewhat more realisticmodel outlined below. Dropping the requirementfor the model to be solved analytically allowed anumber of changes to be made, including explicitintroduction of production functions utilizing twoinputs, characterized respectively as a seed and her-bicide complex on the one hand, and on the other acomposite factor for all other inputs, including land.Nevertheless, it should be noted that the model isstill very simplified. In particular, the model doesnot explicitly include trade; processing and market-ing activities are subsumed into supply/demandfunctions; and it is assumed that there is a singleconsumer good generated from the farm product(i.e. joint or by-products are not considered).

The representative demand functions areexpressed as a constant elasticity form:

dn = a0Pna1 (1.12)

dg = a0Pga1 (1.13)

The function determining the share of the marketallocated to non-GM is extended, as the proportionof the people consuming the GM product may risenon-linearly as the price differential increases:

Sn = (Pg / Pn)l l > 1 (1.14)

This gives aggregate demands of:

A Way Forward for Frankenstein Foods 11

Dn = a0Pna1(Pg / Pn)

l (1.15)

Dg = a0Pga1(1 – (Pg / Pn)

l) (1.16)

The production functions are given by a two-inputconstant returns to scale (CRTS), constant elasticityof substitution (CES) production function:

(1.17)

(1.18)

where k1n is the amount of input 1 used by the non-GM sector, k2n, the amount of input 2 and so on.

In the GM sector t1 and t2 are the input aug-menting technical change associated with the newinnovation. Setting t1 > 1 implies that k1g is becom-ing more effective. Hicks neutral technical changecan be represented by setting tg > 1.

The other parameters in the function can beinterpreted as follows: g is a general scaling factor; ddetermines (in part) the slope of the isoquant andmust lie between 0 and 1 for it to be downwardsloping; while q determines the elasticity of substi-tution (s) between the two inputs (s = 1/(1 + q)).

For this CRTS, CES the marginal costs of pro-duction are given by:

(1.19)

(1.20)

where P1 and P2 are the prices of k1 and k2 respec-tively, and tf is the technology fee charged by theprovider of the improved inputs. The form of thisfee will be described later, when the model is param-etrized.

Assuming profit maximizing, perfectly com-petitive behaviour, one can directly infer that atequilibrium the product price and marginal cost willbe equal, allowing for any identity preservation coststhat may arise:

Pn = MCn + IPn (1.21)

Pg = MCg + IPg (1.22)

With fixed input prices (P1, P2), marginal costs arenot dependent on the scale of production, andEquations 1.19 to 1.22 will define the product pricefor the two commodities, and hence the resultingdemands. However, things are more interesting ifone makes the input markets endogenous.

The optimal input demand, for a given level ofoutput, is given by:

(1.23)

(1.24)

(1.25)

(1.26)

The (inverse) supply curve associated with eachinput is assumed to be linear and a function ofaggregate input demand:

P1 = b0 + b1(K1n + K1g) (1.27)

P2 = b2 + b3(K2n + K2g) (1.28)

So, although there are no direct interactionsbetween the two types of goods on the cost of pro-duction as a result of changing output levels, thereare indirect effects through the input markets.

12 M. Burton et al.

Q k kn n n= + -( )[ ]- - -g d dq q q

1 2

11

/

Q t t k t kg g g= ( ) + -( )( )È

ÎÍ

˘

˚˙

- --

g d dgq q

q

1 1 2 2

1

1

/

MCP P

Pn = -ÊËÁ

ˆ¯

ÊËÁ

ˆ¯

+Ê

ËÁÁ

ˆ

¯˜1 1 2

1

1

11

gd d

dq

s qs q/

/

+ -( ) -ÊËÁ

ˆ¯

ÊËÁ

ˆ¯

+Ê

ËÁÁ

ˆ

¯˜

P PP

2 1 1

2

1

11

1g

d dd

qs qs q

/

/

MCPt t

PPg = -Ê

ËÁˆ¯

ÊËÁ

ˆ¯

+Ê

ËÁÁ

ˆ

¯˜1

1

1 2

1

1

11

gd d

dg

qs qs q

/

/

+ + -( ) -ÊËÁ

ˆ¯

ÊËÁ

ˆ¯

+Ê

ËÁÁ

ˆ

¯˜

P tft t

PP

2

2

1 1

2

1

11

1g

d ddg

qs qs q

/

/

KQ P

Pnn

1

12

1

1

11= -Ê

ËÁˆ¯

ÊËÁ

ˆ¯

+Ê

ËÁÁ

ˆ

¯˜

dg

dd

q s qs q/

/

KQ P

Pnn

2

1

1

2

11

11=

-( )-

ÊËÁ

ˆ¯

ÊËÁ

ˆ¯

+Ê

ËÁÁ

ˆ

¯˜

dg

dd

q s qs q/ /

KQ

t tPPg

g1

1

1

2

1

1

11= -Ê

ËÁˆ¯

ÊËÁ

ˆ¯

+Ê

ËÁÁ

ˆ

¯˜

dg

dd

q

g

s qs q/

/

KQ

t tPPg

g2

1

2

1

2

11

11=

-( )-

ÊËÁ

ˆ¯

ÊËÁ

ˆ¯

+Ê

ËÁÁ

ˆ

¯˜

dg

dd

q

g

s qs q/ /

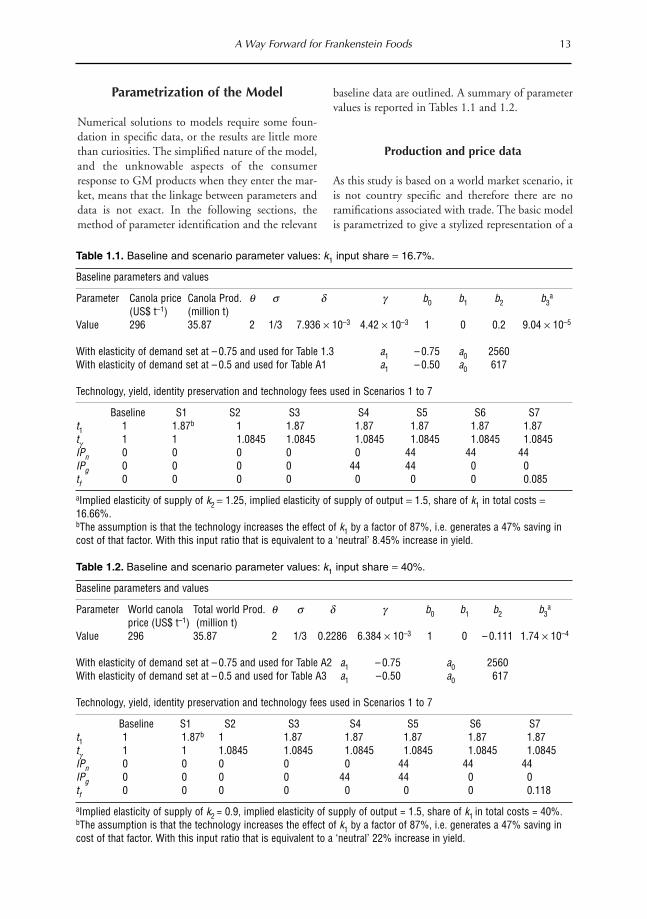

Parametrization of the Model

Numerical solutions to models require some foun-dation in specific data, or the results are little morethan curiosities. The simplified nature of the model,and the unknowable aspects of the consumerresponse to GM products when they enter the mar-ket, means that the linkage between parameters anddata is not exact. In the following sections, themethod of parameter identification and the relevant

baseline data are outlined. A summary of parametervalues is reported in Tables 1.1 and 1.2.

Production and price data

As this study is based on a world market scenario, itis not country specific and therefore there are noramifications associated with trade. The basic modelis parametrized to give a stylized representation of a

A Way Forward for Frankenstein Foods 13

Table 1.1. Baseline and scenario parameter values: k1 input share = 16.7%.

Baseline parameters and values

Parameter Canola price Canola Prod. q s d g b0 b1 b2 b3a

(US$ t–1) (million t)Value 296 35.87 2 1/3 7.936 ¥ 10–3 4.42 ¥ 10–3 1 0 0.2 9.04 ¥ 10–5

With elasticity of demand set at – 0.75 and used for Table 1.3 a1 – 0.75 a0 2560With elasticity of demand set at – 0.5 and used for Table A1 a1 – 0.50 a0 617

Technology, yield, identity preservation and technology fees used in Scenarios 1 to 7

Baseline S1 S2 S3 S4 S5 S6 S7t1 1 1.87b 1 1.87 1.87 1.87 1.87 1.87tg 1 1 1.0845 1.0845 1.0845 1.0845 1.0845 1.0845IPn 0 0 0 0 0 44 44 44IPg 0 0 0 0 44 44 0 0tf 0 0 0 0 0 0 0 0.085

aImplied elasticity of supply of k2 = 1.25, implied elasticity of supply of output = 1.5, share of k1 in total costs =16.66%.bThe assumption is that the technology increases the effect of k1 by a factor of 87%, i.e. generates a 47% saving incost of that factor. With this input ratio that is equivalent to a ‘neutral’ 8.45% increase in yield.

Table 1.2. Baseline and scenario parameter values: k1 input share = 40%.

Baseline parameters and values

Parameter World canola Total world Prod. q s d g b0 b1 b2 b3a

price (US$ t–1) (million t)Value 296 35.87 2 1/3 0.2286 6.384 ¥ 10–3 1 0 – 0.111 1.74 ¥ 10–4

With elasticity of demand set at – 0.75 and used for Table A2 a1 – 0.75 a0 2560With elasticity of demand set at – 0.5 and used for Table A3 a1 – 0.50 a0 617

Technology, yield, identity preservation and technology fees used in Scenarios 1 to 7

Baseline S1 S2 S3 S4 S5 S6 S7t1 1 1.87b 1 1.87 1.87 1.87 1.87 1.87tg 1 1 1.0845 1.0845 1.0845 1.0845 1.0845 1.0845IPn 0 0 0 0 0 44 44 44IPg 0 0 0 0 44 44 0 0tf 0 0 0 0 0 0 0 0.118

aImplied elasticity of supply of k2 = 0.9, implied elasticity of supply of output = 1.5, share of k1 in total costs = 40%.bThe assumption is that the technology increases the effect of k1 by a factor of 87%, i.e. generates a 47% saving incost of that factor. With this input ratio that is equivalent to a ‘neutral’ 22% increase in yield.

canola market. In the model the aggregate quantityof canola grain is set at 35.87 Mt and is based onFAO data for world production of canola grain in1998 (FAOSTAT, 2000). The price for canola grainis assumed to be US$296 t–1 which, according to theUSDA’s Foreign Agricultural Service, was the canolagrain price for 1998 (FAS Online, 2000).

Farm input costs and benefits

Without GM inputs

The two inputs in the production function are char-acterized as k1, the canola complex (seed and herbi-cide) and k2, all other inputs. Fulton and Keyowski(1999a) suggest that the share of the canola complexis some 16% in total cost, and the parameters of theproduction function are selected to generate thisresult at the pre-GM equilibrium. Given an elasticityof substitution (s) set exogenously at 1/3, and nor-malizing the input prices to unity allows the inputratio to be determined (the ratio of Equations 1.23and 1.24) as a function of a single parameter, d.

The scale parameter g is then identified byequating marginal cost (Equation 1.19) with canolaprice.

As an alternative, the original share of 16% isincreased to 40%, which may be closer to the valuefor Australia. This leads to alternative values for dand g (see Table 1.2).

Having identified all parameters of the produc-tion function, the equilibrium input quantities areidentified (Equations 1.23, 1.24). The units inwhich these are measured cannot be interpreted, asthe input prices have been normalized to unity, andthey will change with the differing assumptionabout the input share (or s, if it were altered).However, once the input quantities have been estab-lished at equilibrium, the parameters of their(inverse) supply functions can be obtained.

With GM inputs

Fulton and Keyowski (1999b) suggest that farmerswho have adopted some form of reduced tillage sys-tem are more likely to profit from using HR (herbi-cide resistant) seed. Production of GM canola

requires a one-pass chemical operation (as opposed totwo passes required by non-GM canola) so eliminatesthe cost of additional machine operations over thefield; enables control of the entire spectrum of weedsso giving farmers much more flexibility in terms ofthe timing and type of weed control; and has thepotential to improve the crop yield by removingcompetition for moisture and nutrients (Fulton andKeyowski, 1999a). Even so, the benefits of the newtechnology will only be recognized if returns increasethrough reduced weed control costs and/or increasedyields (CCGA, 2000). Therefore, where weed controlis not a major concern farmers are unlikely to benefitand may be better off using conventional varieties(CCGA, 2000). Ballenger et al. (2000) state that pro-ducers in different countries will consider the relativeprices for biotech and non-biotech crops in relationto their local farming conditions when deciding whatto plant. For the purpose of this study, this statementis extended further to assume that producers will useGMO technology only if it is beneficial to their pro-duction method thereby capturing benefits associat-ed with herbicide reduction and yield increase.Therefore, while acknowledging the argument byFulton and Keyowski (1999a) that total benefitsderived from GMO technology will depend on agro-nomic, management and technology factors facingindividual farmers, we assume here that farmersincluded in this study are alike.

The GM innovation is assumed to have twopotential modes of action in the production func-tion that may occur separately or together. The firstis a change in the effectiveness of the canola complexinputs. This is represented by assuming that theeffectiveness of this input rises by some 87% (t1 =1.87), a figure derived using results found by Fultonand Keyowski (1999a). The implied reduction inmarginal costs (before allowing for substitution andinput price effects) is approximately 8.5% if theinput share is 16%.

The second mode of action is a Hicks neutralshift in the production function. Fulton andKeyowski (1999a) found a yield decrease of around7%6 with the introduction of Roundup Ready™canola; James (1998) found that the average canolayield in Canada increased by 7.5% between 1996and 1997.7 Here we set this value at 8.5%, so that

14 M. Burton et al.

6 As Fulton and Keyowski (1999a) note, farmers were not differentiated in the study and those who have not adoptedconservation practices are unlikely to receive the same benefits as those who have.

7 From Fulton and Keyowski (1999a) almost 4% of canola grown in Canada was GM canola in 1996 compared to33% in 1997 and therefore it could be assumed that part of the overall yield increase could be contributed toproduction of GM canola.

the change in marginal cost due to this change isequivalent to that induced by the input-specificshift.

It should be noted that when the input shareof k1 is raised to 40%, the economic impact of theinnovation is significantly increased for the sameincrease in effectiveness: equivalent to a 22% reduc-tion in marginal cost. In the simulations with thishigher share the yield effect is retained at 8.5%.

Elasticities of supply and demand

The elasticity of supply of the canola complex (k1) isassumed to be infinite. Given constant returns toscale, imposing an elasticity of supply on the otherinputs effectively determines the long-run equilibri-um response of output to changes in the canolaprice. While Johnson et al. (1996) found elasticity ofsupply to be up to 0.85, for the purpose of this proj-ect it was deemed that the long-run supply elastici-ty would be set at 1.5. If the input share of k2 is setat 84% (because the share of k1 has been set at 16%as described above), this implies an elasticity of sup-ply of k2 of 1.25. If the input share is 60%, then theelasticity of supply of k2 is set at 0.9. In both casesthe parameters of the linear marginal supply func-tion for the input can subsequently be identified.

Johnson et al. (1996) indicate the elasticity ofdemand of canola oil to be –0.6 for Canada, –0.69for the USA and for the EU, –0.56. Goddard andGlance (1989) quote elasticity of demand for canolaoil ranging from –1.17 to –0.31 with a mean andmedian of –0.78. Here, we simply specify a singlederived demand for oilseed, with no differentiationby end-use, and an elasticity of demand of either–0.75 or –0.5. This, combined with the base quan-tity/price data allows the parameters of the represen-tative demand functions to be identified.

Market share

Phillips (1999) and Buckwell et al. (1999) argue thatfor non-GM products to enter the market, the mar-ket would have to segment and the cost that this seg-mentation could bear would depend on the willing-ness of consumers to pay extra for non-GMproducts. In the long run consumers around theworld will decide on the premiums they will pay fornon-biotech products (Ballenger et al., 2000).

Miranowski et al. (1999) add that the price pre-mium for a non-GM crop will depend on the sup-ply of that crop and costs of identity preservation.The size of these premiums is unknown and anymarket intelligence concerning GM food is scarce.Differences in regional attitudes towards GM food-stuffs complicate the picture, as does the fact thatcanola generates two products, oil and meal, withhuman and animal feed end-markets. If public con-cerns about GM products do not extend to productsfrom animals raised on GM feeds, then the deriveddemand for meal will not segment.

In the face of uncertainty about possibleresponses, l is set at an arbitrary value of 3, a valuewhich leads to significant segmentation at relativelylow price differentials (e.g. for a GM product pricedat 10% less than non-GM product, the market sharefor the GM product would be 27% of individuals).

Identity preservation costs

Smyth and Phillips (1999) found the cost of anidentity preservation and marketing system forcanola in Canada to be between 12 and 15% of thefarm gate price. This cost is assumed to impose awedge between farm and retail price by raising theeffective marginal cost of supply at retail level. In thesimulations that follow, the cost is set at US$44 t–1,or approximately 15% of the pre-GM farm gateprice.

Farmers must pay for GM canola seed as it isassumed that they are not able to retain any seed forplanting from the previous year. From Fulton andKeyowski (1999a) the increase in GM canola seedprice over non-GM was found to be 2% of the totalreturn. To acquire Roundup Ready™ canola seed,farmers must attend a sign-up meeting and agree toa Technology Use Agreement, pay US$37 ha–1 tech-nology fee and buy a package of seed andRoundup™ herbicide (Phillips, 1999). In thisstudy, these costs are referred to as ‘the technologyfee that is associated with the GM technology’ andis applied to the ‘other’ input (k2), leading to aneffective increase in its price. This is emerging as acommon practice in the industry, with the technol-ogy fee applied to land area planted, rather thanoutput levels or seed. In an initial simulation thetechnology fee is set at 7% of total revenue (at pre-GM equilibrium input quantities and output price).

A Way Forward for Frankenstein Foods 15

Summary of data

Tables 1.1 and 1.2 summarize the data used in themodel. Table 1.1 generates the production parame-ters on the assumption that the input share for k1 is16.7%, and reports alternative values for thedemand elasticity. The lower half reports the valuesfor the technological change parameters, identitypreservation costs and technology fee for seven sce-narios. Table 1.2 is generated on the basis of aninput share of 40%.

The scenarios explore the response of themodel to:

• different forms of technical change;• different incidence of identity preservation costs;• the impact of a technology fee.

Scenarios 1–3 introduce a factor saving innovation,a Hicks neutral innovation and a combination ofboth, but no identity preservation costs. The mostlikely outcome from adoption of herbicide resistantGM canola is assumed to be significant savings inthe cost of the canola complex input, as well as anadditional factor neutral yield increase.

Scenarios 4–6 build on Scenario 3 by intro-ducing identity preservation costs that respectively

affect the cost of retail supply of the GM commod-ity alone, on both commodities and finally on thenon-GM commodity alone. Again for reasons out-lined above, it is thought that the latter is the mostlikely outcome in the market. Finally, a technologyfee is added to the system and is fixed exogenouslyat the rate suggested by Phillips (1999) (Scenario 7).

Results

The full set of simulation results is reported inAppendix II. For simplicity, the discussion will focuson one set of results presented in Table 1.3 based onan input share for the canola complex of 16% andan elasticity of demand of –0.75 (i.e. based onparameter values drawn from Table 1.1).

The first column of Table 1.3 reports the base-line simulation, with the equilibrium price andquantity as initially set. In Scenario 1, the GM tech-nology is depicted as a factor saving technicalchange with an impact on k1 alone. The market seg-ments, with the GM crop taking some of the mar-ket, with non-GM price rising slightly and a sub-stantial fall in the GM price compared with theinitial equilibrium. The expansion in demand by

16 M. Burton et al.

Table 1.3. Simulated values for canola price and quantity, input quantities and welfare impacts.

Baseline S1 S2 S3 S4 S5 S6 S7

Pn 296 298 296 298 296 328 338 333Pg n/a 275 273 254 296 285 250 265Qn 35.8 28.0 28.1 22.0 35.8 21.8 13.1 16.5Qg n/a 8.1 8.2 15.5 0.1 12.7 24.2 19.4

Q 35.8 36.1 36.3 37.5 35.9 34.5 37.3 35.9P2 1 1.01 0.99 1.01 1 0.95 0.99 0.97k1n 1770 1388 1389 1087 1765 1061 647 809k1g 0 215 375 377 2.3 305 588 468

k1 1770 1603 1764 1464 1366 1366 1235 1277k2n 8850 6921 6949 5423 8828 5395 3244 4088k2g 0 2005 1876 3517 21 2900 5517 4423

k2 8850 8926 8825 8940 8849 8295 8761 8511Dcsn –48 16 –44 0 –715 –579 –629(share) (0.78) (0.78) (0.85) (1.0) (0.65) (0.40) (0.50)Dcsg 81 100 319 0 –94 253 62Dps1 0 0 0 0 0 0 376Dps2 61 –20 72 0 –430 –71 –266

∆W 94 96 347 0 –1239 –397 –457

Note: The bottom six rows of the table contain estimates of changes in consumer and producer welfare relative tothe baseline scenario representing no production of GM food. The estimate of share is the proportion of the con-sumers consuming the non-GM food.Dcsj is the change in consumer surplus for those consuming good j, Dpsl the change in producer surplus for suppli-er of input 1(k1), and DW the aggregate effect. See Appendix III for further details on the method of calculation.

those who switch to GM product leads to an expan-sion in aggregate output. While this increased out-put is produced using less of k1 (due to the techni-cal change), an expansion in k2 is necessary due tothe scale effect. The latter causes the price of k2 to bebid up, which is the cause of the increased cost (andhence price) of non-GM output. Note that thereduction in demand for k1 gives no compensatingrelief, as its price does not vary with output.

In the reported estimates of welfare effects, itshould be noted that the changes in consumer sur-plus are reported for the sub-populations of con-sumers. The proportion of the market that remainswith non-GM food is reported. Per capita estimatesof welfare changes could be obtained by multiplyingthe aggregate change in welfare by the share. Thosewho remain with non-GM product are worse offdue to the increased price, while those who switch tothe GM alternative are better off due to the lowerprice. Net, there is an increase in welfare, which isincreased when the increase in producer surplus ofthose supplying k2 is included.8 Parenthetically,comparison of changes in consumer welfare betweenscenarios should be conducted with care, becausethe size of the sub-populations involved varies.

Under Scenario 2, the input specific technicalchange is replaced with a Hicks neutral effect,which, at initial quantities and prices, leads to thesame reduction in marginal cost. However, the dis-tributional effects on the input side differ. Demandfor both inputs falls, despite a slight increase in out-put and hence input price P2 falls. This reduces themarginal cost of producing the non-GM product,leading to welfare gains for both sets of consumers(the price Pn declines by less than the rounding fac-tor used in Table 1.3).

Scenario 3 combines both forms of technicalchange. The increased cost advantage allows theGM market to expand significantly, leading to gainsin consumer surplus of that group. However, due tothe scale effect, adoption of the GM crop againresults in increased demand for k2 and consequentialincreased cost (and hence price) of non-GM food.Thus consumers who continue to purchase the non-GM product despite the price differential are worseoff than they were prior to the introduction of theGM crop, even though there are no identity preser-vation costs under this scenario.

Under Scenario 4, the incidence of the cost ofidentity preservation is assumed to fall exclusively

on the GM crop. In this case, these costs almost out-weigh the benefits of the technical change and,although GM enters the market, it does so onlymarginally.