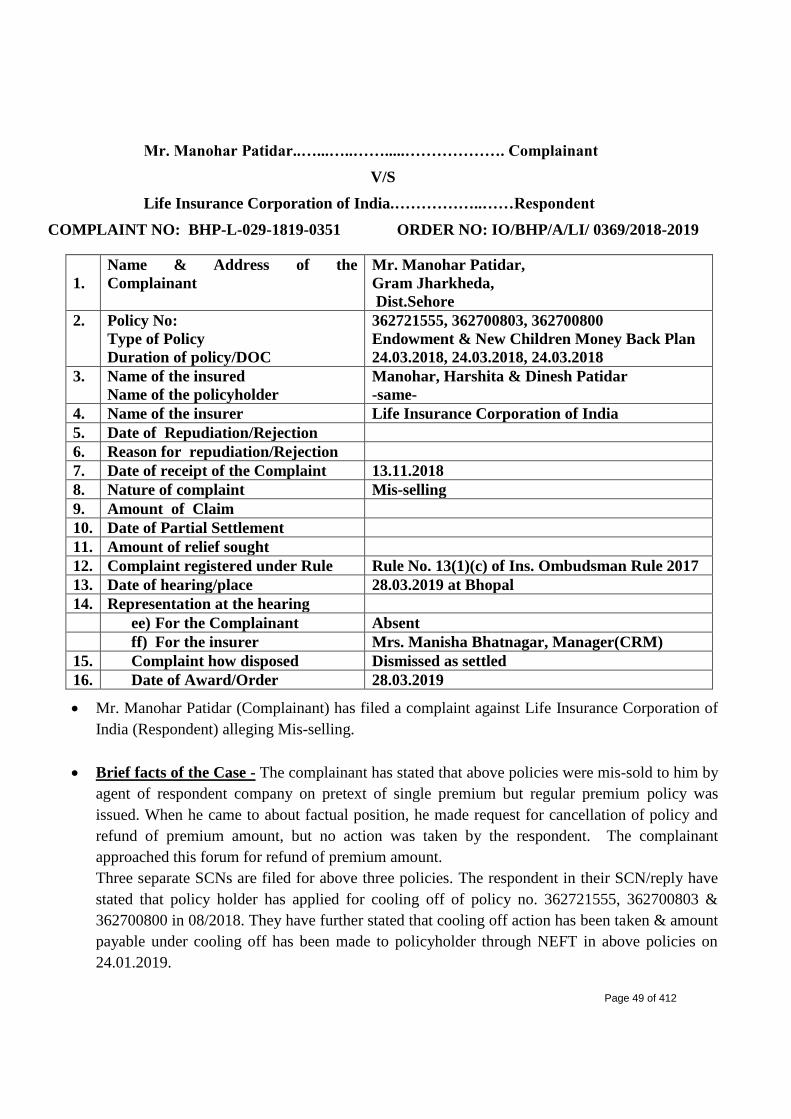

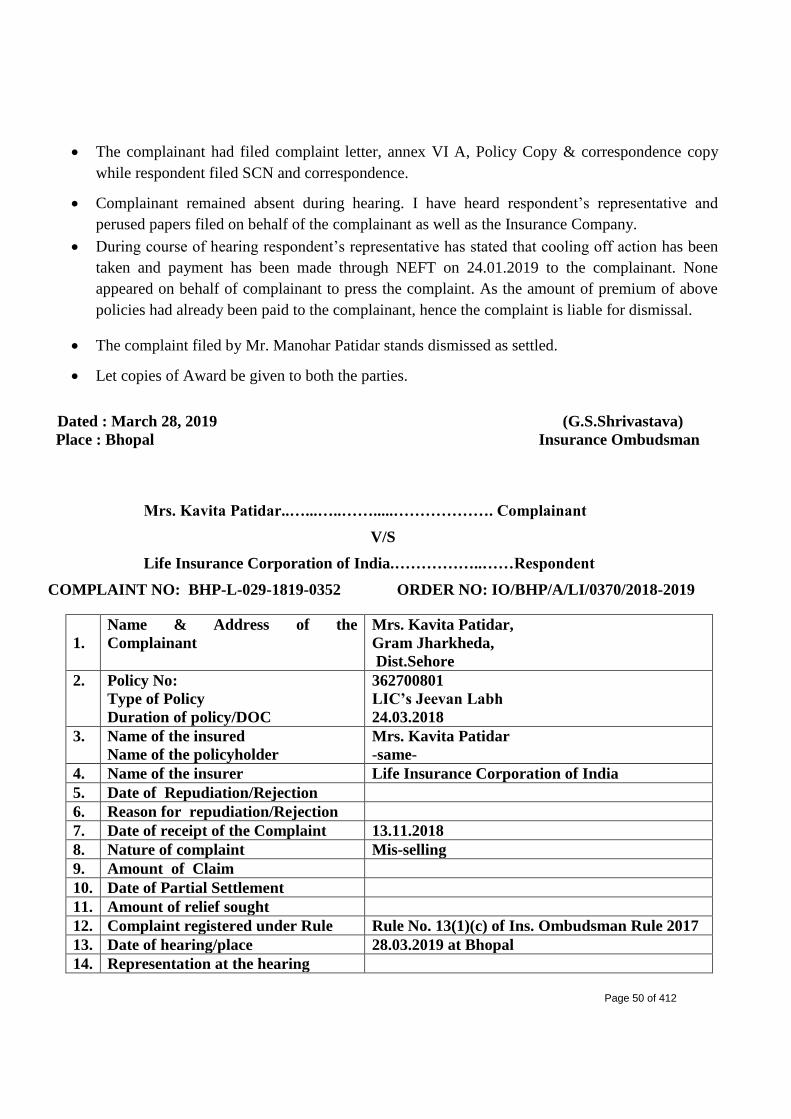

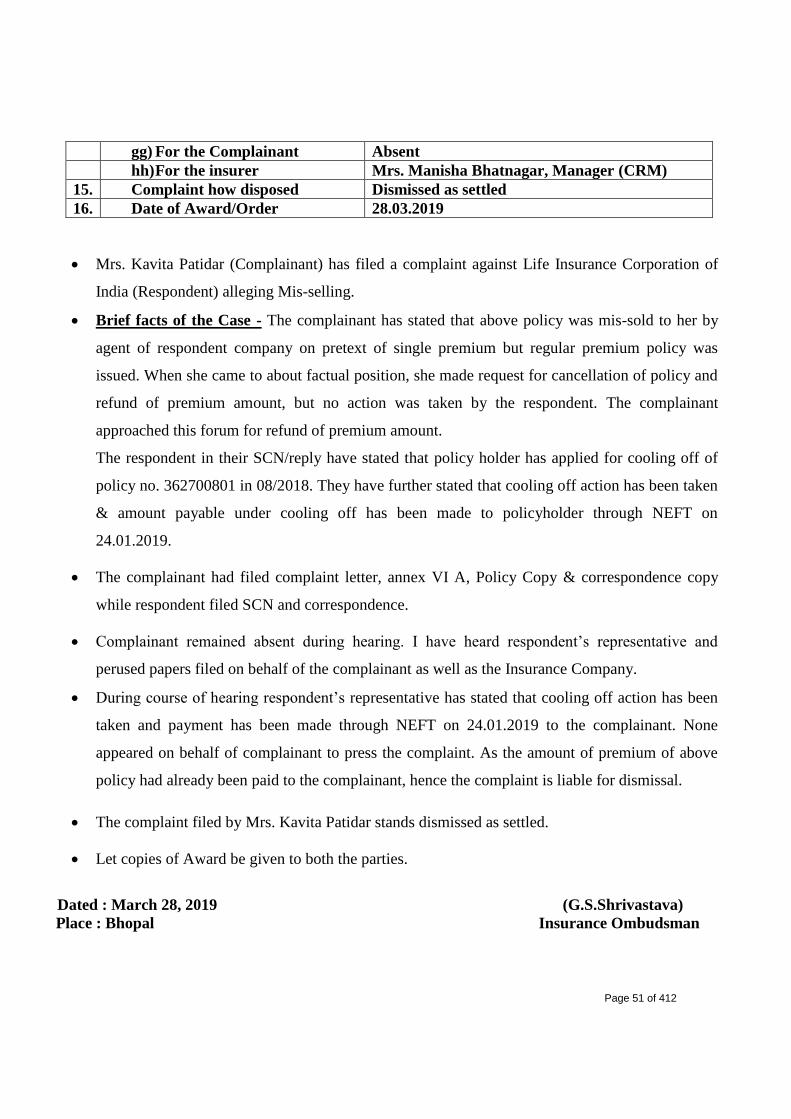

Hague v. CIO: Mr. Justice Stone's Test of Federal Jurisdiction—A

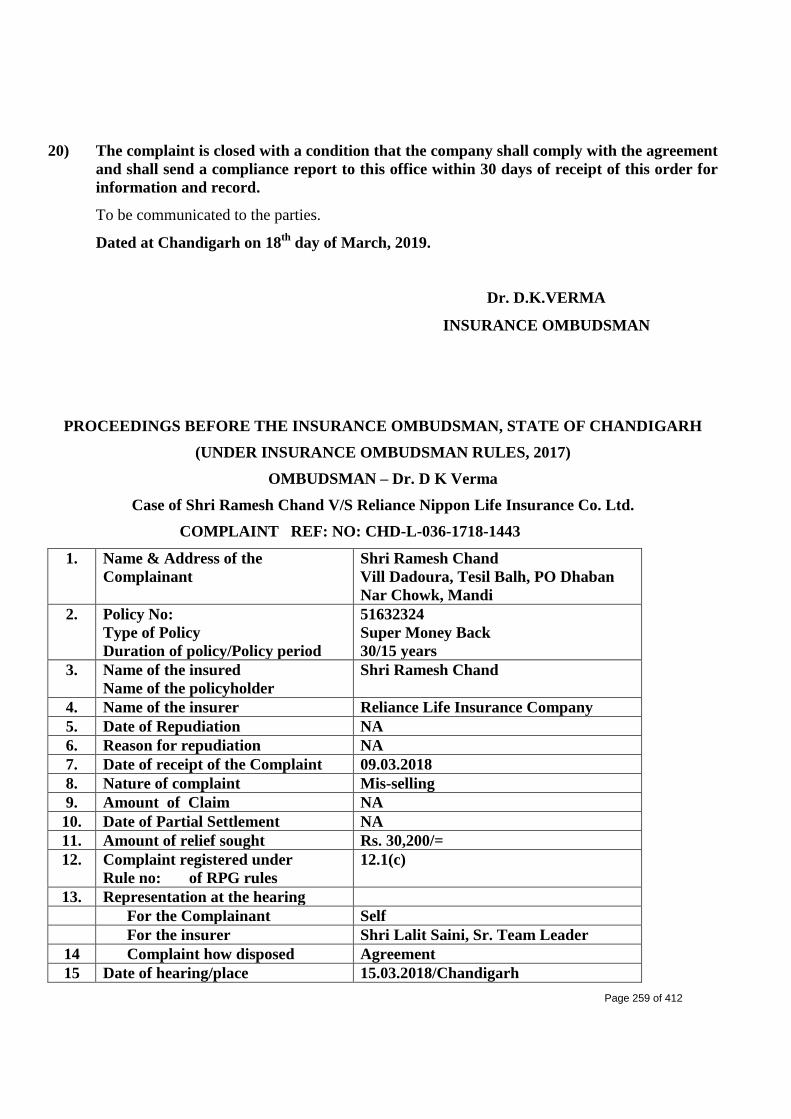

Upload

khangminh22Category

view

0download

0

Page 1 of 412

PROCEEDINGS BEFORE THE INSURANCE OMBUDSMAN, AHMEDABAD State of Gujarat and Union Territories of Dadra, Nagar Haveli and Daman & Diu

(Under Rule No: 16/17 of The Insurance Ombudsman Rules, 2017)

Ombudsman: M. Vasantha Krishna Case of:- Mr. Natarajan Sivasurya V/s HDFC Life Insu. Co. Ltd.

Complaint Ref No. : AHD-L-019-1718-0246 Award No. IO/AHA/A/LI/0004/2018-2019

1 Name and address of

the Complainant

Mr. Natarajan S Sivasurya,

99/591, Vijaynagar

Opp: Verai Mata Mandir,

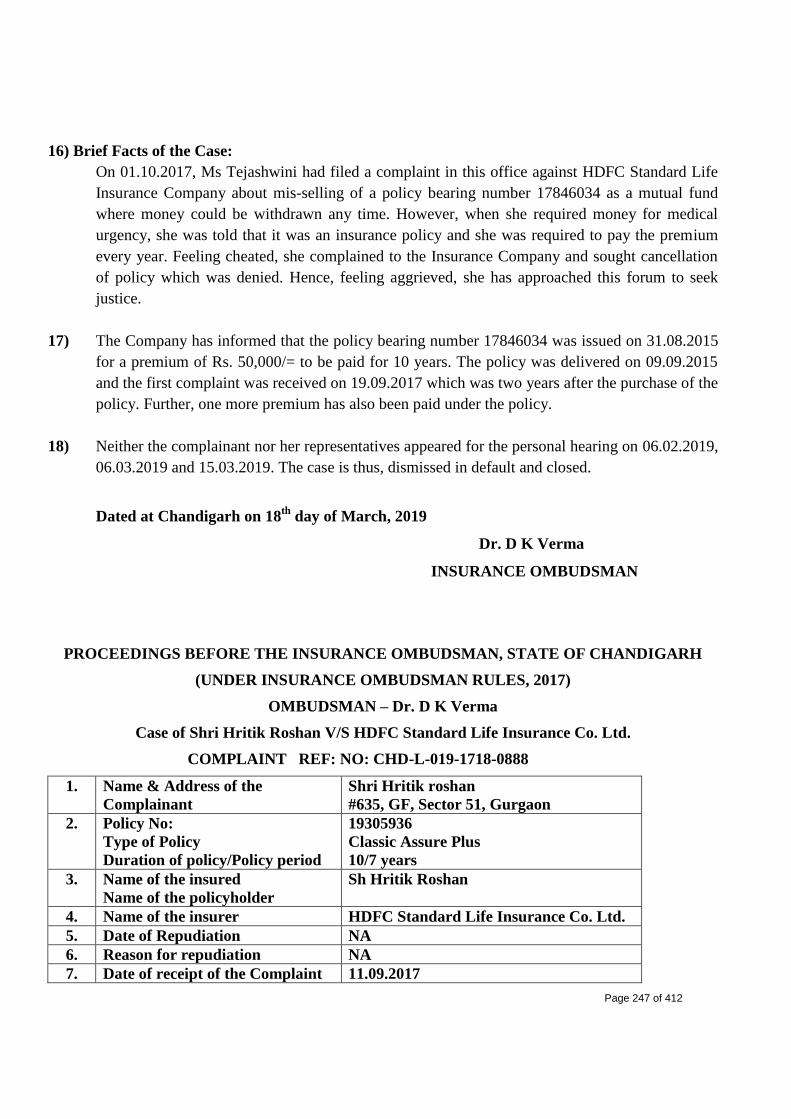

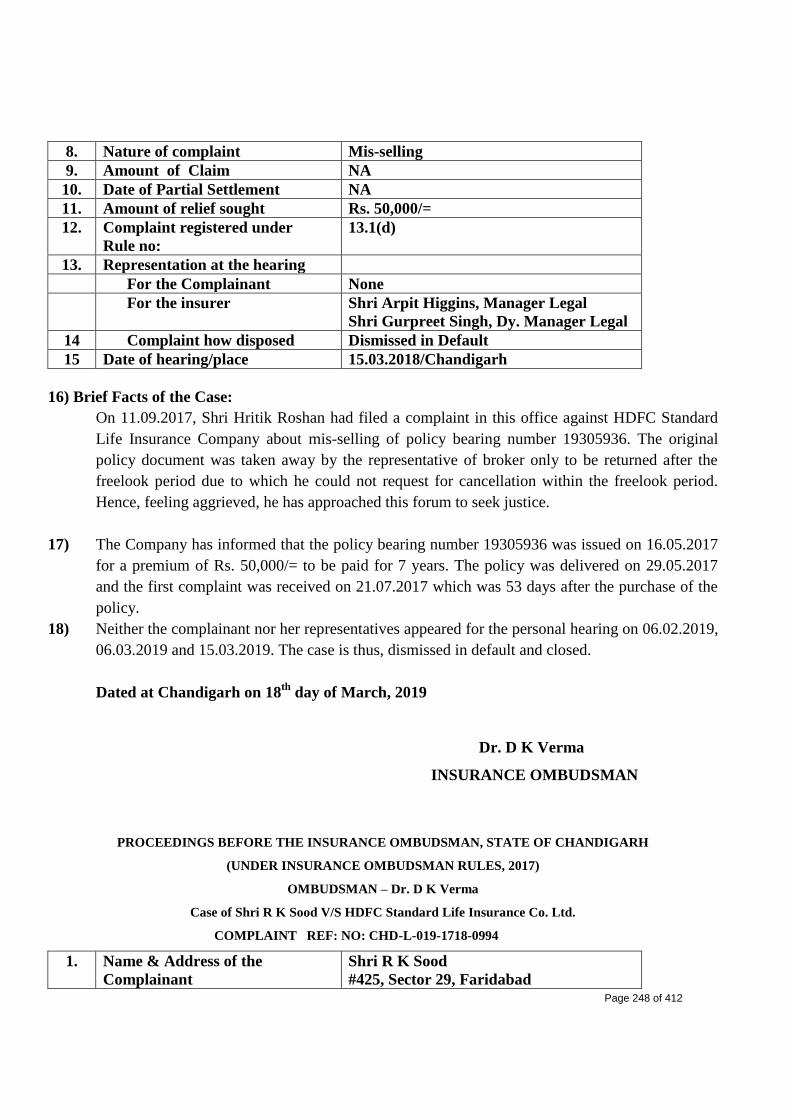

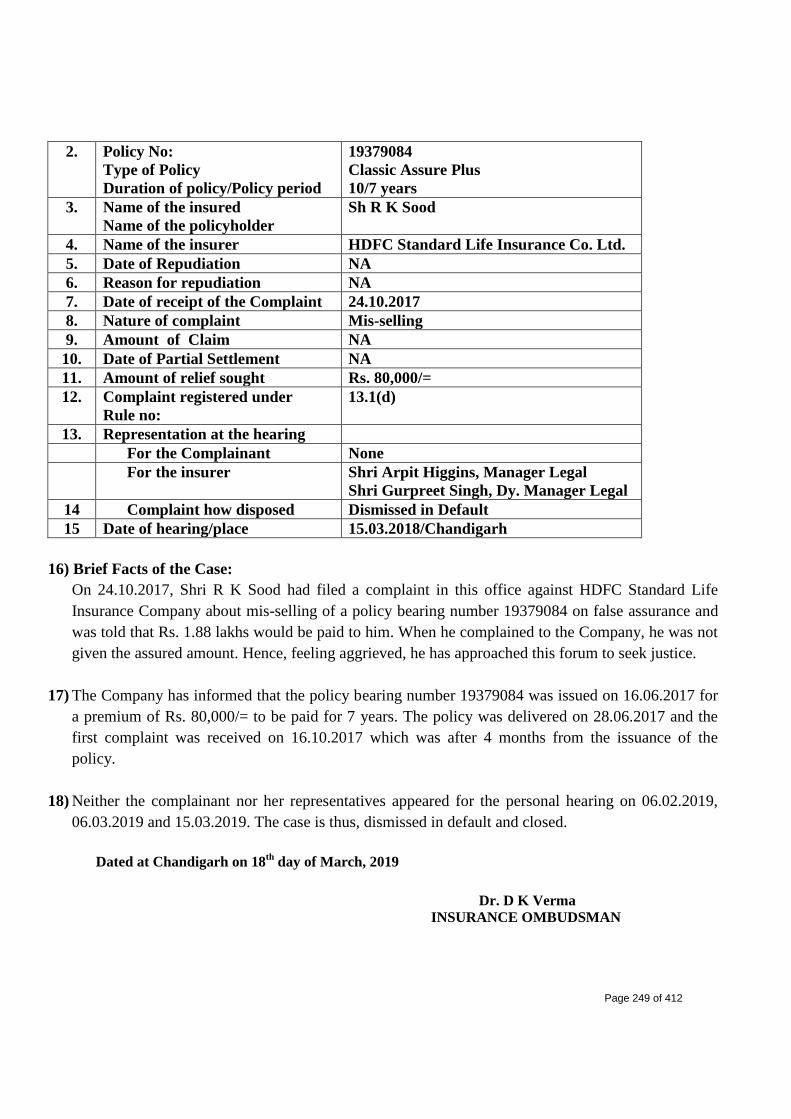

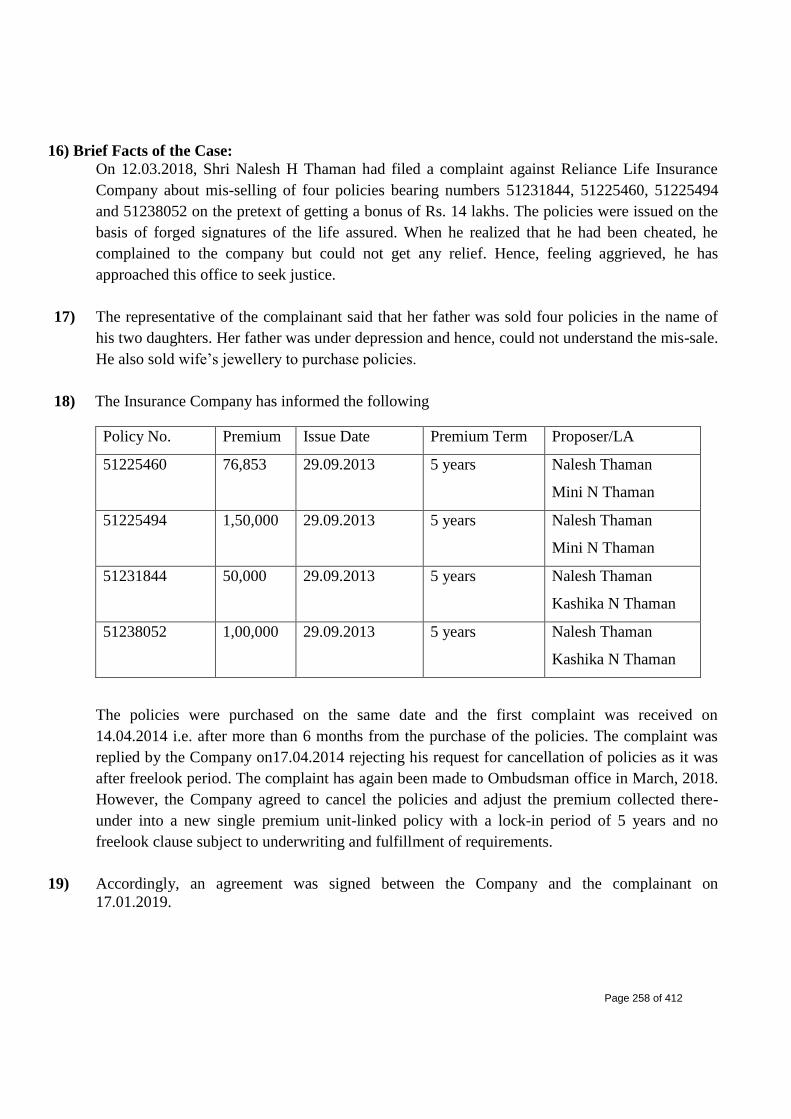

Naranpura, A’bad-380013

2

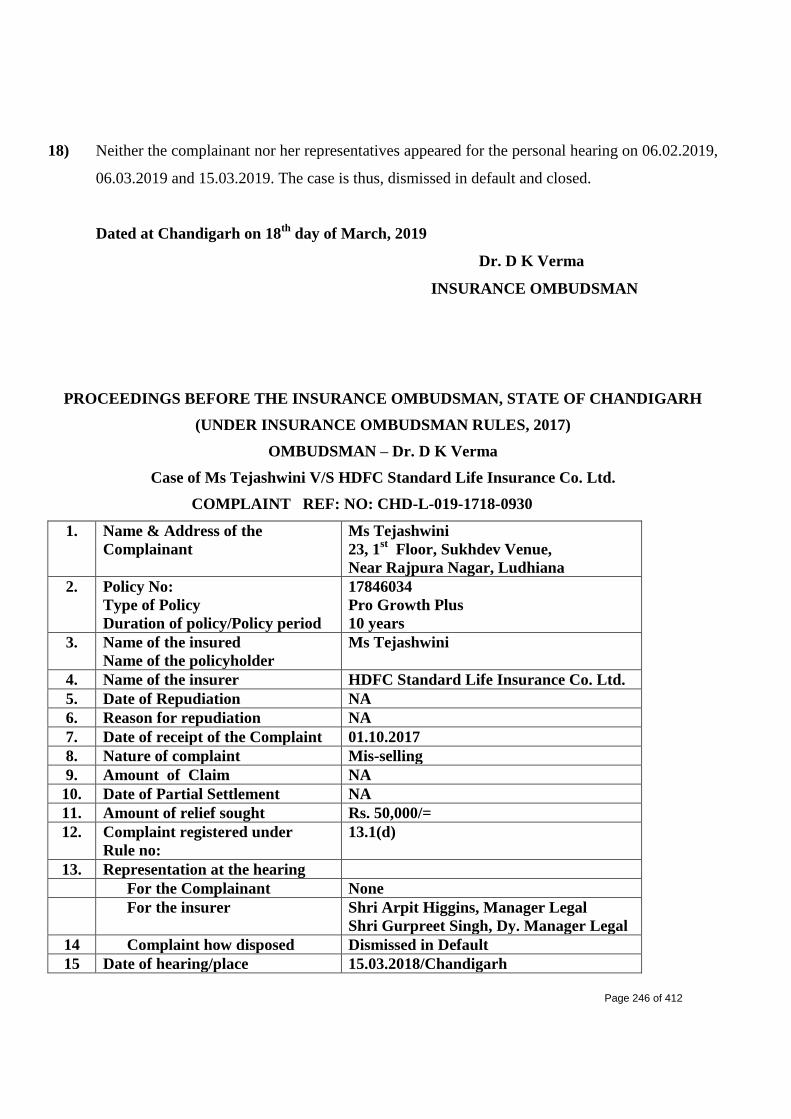

Policy No:

Type of Policy

D.O.C

18483145

HDFC Life Personal Pension Plus

30/05/2016

3 Name of the L.A

Name of the Proposer

Mr. Natarajan Sivasurya

Mr. Natarajan Sivasurya

4 Name of the insurer HDFC Life Insu. Co.Ltd.

5 Date of Repudiation Not applicable

6 Reason of repudiation Not applicable

7 Date of receipt of complaint 16/06/2017

8 Nature of complaint Mis-sale;

request for policy cancellation rejected

9 Amount of relief sought Rs.94,880/-

10 Date of receipt of VI-A / SCN 27/06/2017 / 14/06/2018

11 Complaint registered under Rule. Section 13 (1) (d) of the I.O. Rules, 2017

12 Date of hearing/place 30/11/2018 / Ahmedabad

13

Representation at the hearing:

For the Complainant

For the Insurer

Mr. Natarajan

Ms. Shikha Dedhia

14 Complaint how disposed Award

15 Date of Award / Order 29/03/2019

16. Brief facts of the case:

The Complainant claims that he received a call from New Delhi, promising pension from 6th year

on purchasing a life insurance policy and after paying premium for 5 years. Being convinced

with the proposition, he took the policy but received the policy with premium paying term of 10

years He then understood that he had been cheated. He had sent complaints to the Insurer

alleging malpractice and unfair business practices. He also requested the respondent insurer to

Page 2 of 412

convert the policy to one with 5 years premium paying term or cancel the policy and refund the

premium but the same was rejected. He has therefore requested this Forum to intervene and

get the premium refunded.

17. Arguments during the Hearing:-

A. Complainant’s contention:

The complainant submitted that the respondent insurance company canvassed with him for

the sale of a pension benefits policy through telephone calls from their Delhi Office with lot

of misrepresentation/suppression of material facts/fraudulent promises, while taking care to

ensure that no records were available with the customer to establish such

misrepresentations / suppression of material facts / fraudulent promises / assertions etc. He

was cunningly convinced to purchase the policy with the promise of pension from 6th year

after 5 years of premium payment. The caller managed to collect the cheque towards first

year premium and his signature in haste and did not allow him time to study the documents.

The insurance company had issued him a policy totally contrary to the discussions /

promises given. When the policy was posted to his address, he was out of station. Hence

he was not able to return the policy for cancellation within 15 days / one month, as he had

found that the premium paying term was 10 years instead of 5 years. He wrote to Grievance

Manager of the insurer on 03/01/2017 to get the policy converted in to one with 5 years

premium paying term or alternatively for cancellation of the policy and refund of premium.

But his efforts were deceptively and deviously evaded by the insurance company. He was

frustrated with the amount of lies and deception the insurance company was indulging in to

cheat the customers and deprive them of their hard earned money. His request was

declined by the insurance company through e-mail dated 21/05/2017 on the ground that

cancellation request was not received within free look period. He once again wrote to the

Grievance Manager of the insurer on 19/06/2017 for cancellation of the policy to which the

insurer was yet to respond. Since the sale was done through fraud & false promise, he

requested the Forum to direct the respondent insurer to refund the premium along with

interest and penalties.

B. Insurer’s contention:

The representative of insurance company submitted that after receipt of the duly filled and

signed proposal form along with the other relevant documents and the subscription premium

amount, the Company had issued the subject policy in favor of the complainant. The same

Page 3 of 412

was delivered to the complainant’s registered address through courier on 10/06/2016. She

confirmed that complaints were received by them from the complainant regarding

malpractices and unfair business practices and that the Insurance company had denied all

the allegations and averments made by the complainant. She added that the Insurance

Company was in receipt of a request for cancellation of policy from the complainant which

was refused on the ground that the said request was made after expiry of free look period of

15 days. Therefore, the Company could not find any ground to accede to the request for

cancellation of the policy & refund of premium. The complainant had approached

Ombudsman and had also raised his concerns vide letter dated 14/09/2017. The Insurance

Company as a matter of goodwill gesture had proposed for refund of premium vide letter

dated 15/09/2017 and the complainant had submitted the requisite documents on

18/09/2017. The Insurance Company had cancelled the policy and an amount of

Rs.95,000/- was refunded through NEFT on 22/09/2017. But now the complainant is

claiming interest which is an afterthought. It is pertinent to mention that the complainant is

not entitled to receive any such interest as the premium was refunded after his consent

which was received on 18/09/2017. She also added that the Pre- Issuance Verification Call

clearly mentions premium payment term as 10 years and not 5 years as alleged by the

complainant. It was also the contention of the insurer that the policy had been sourced by

an independent insurance broker, namely, S.B. Insurance Brokers and that the insurer

neither privy to nor bound by any communication/assurances/transactions made/taken or

given between the complainant and the broker. Under the circumstances, it is submitted that

the complaint is devoid of any substance and is without merit.

18. Result of hearing (Observation & Conclusion):

1. After the complainant approached this Forum, the respondent insurer had offered to refund

the premium to the complainant as a goodwill gesture which was accepted by the

complainant. He also signed a declaration accepting a refund only of the premiums paid by

him in full and final discharge of all liabilities by the insurer, based on which the policy was

cancelled and the premium amount of Rs. 95,000 was refunded by the insurer on

22/09/2017.

2. The Forum is of the view that having accepted the amount of Rs. 95,000 in full and final

settlement, discharging the insurer from any further liability, the complainant is not entitled

to any interest as claimed by him.

Page 4 of 412

AWARD

Taking into account the facts & circumstances of the case and the submissions

made by both the parties, The Forum finds no merit in the complainant’s claim for

interest.

Hence the complaint is not admitted.

19. In case the complainant is dissatisfied with the decision of the Forum, he may approach any

other forum or appropriate court of law, as thinks fit.

Dated at Ahmedabad on 29th March, 2019.

M. Vasantha Krishna

Insurance Ombudsman

PROCEEDINGS BEFORE THE INSURANCE OMBUDSMAN, AHMEDABAD State of Gujarat and Union Territories of Dadra, Nagar Haveli and Daman & Diu

(Under Rule No: 16/17 of The Insurance Ombudsman Rules, 2017) Ombudsman : M. Vasantha Krishna

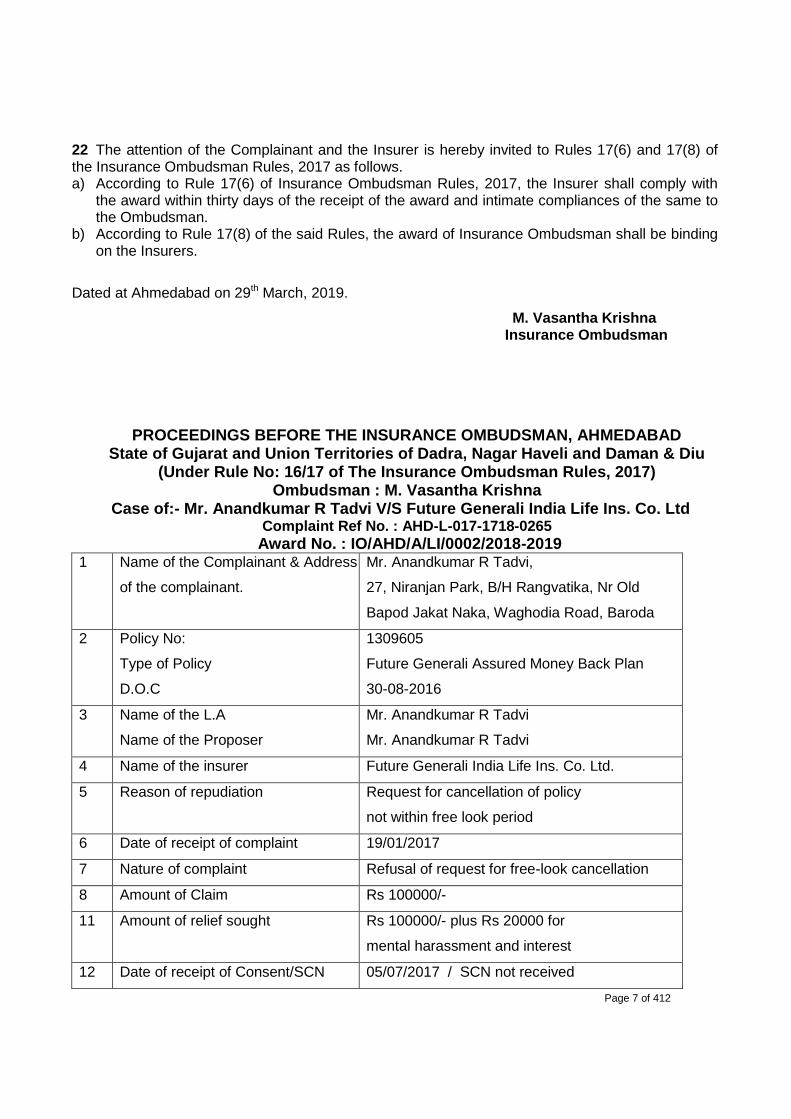

Case of:- Mr. Anandkumar R Tadvi V/S Future Generali India Life Ins. Co. Ltd Complaint Ref No. : AHD-L-017-1718-0265

Award No. : IO/AHD/A/LI/0002/2018-2019 1 Name of the Complainant & Address

of the complainant.

Mr. Anandkumar R Tadvi,

27, Niranjan Park, B/H Rangvatika, Nr Old

Bapod Jakat Naka, Waghodia Road, Baroda

2 Policy No:

Type of Policy

D.O.C

1309605

Future Generali Assured Money Back Plan

30-08-2016

3 Name of the L.A

Name of the Proposer

Mr. Anandkumar R Tadvi

Mr. Anandkumar R Tadvi

4 Name of the insurer Future Generali India Life Ins. Co. Ltd.

5 Reason of repudiation Request for cancellation of policy

Page 5 of 412

not within free look period

6 Date of receipt of complaint 19/01/2017

7 Nature of complaint Refusal of request for free-look cancellation

8 Amount of Claim Rs 100000/-

11 Amount of relief sought Rs 100000/- plus Rs 20000 for

mental harassment and interest

12 Date of receipt of Consent/SCN 05/07/2017 / SCN not received

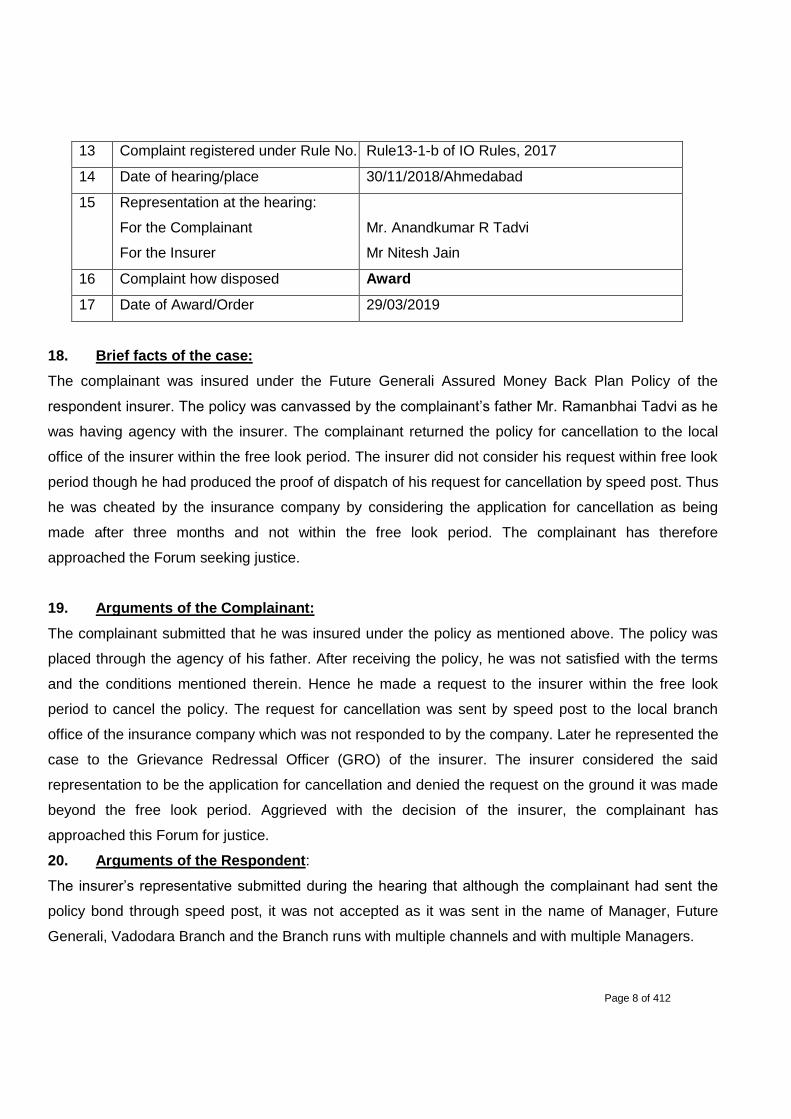

13 Complaint registered under Rule No. Rule13-1-b of IO Rules, 2017

14 Date of hearing/place 30/11/2018/Ahmedabad

15 Representation at the hearing:

For the Complainant

For the Insurer

Mr. Anandkumar R Tadvi

Mr Nitesh Jain

16 Complaint how disposed Award

17 Date of Award/Order 29/03/2019

18. Brief facts of the case:

The complainant was insured under the Future Generali Assured Money Back Plan Policy of the

respondent insurer. The policy was canvassed by the complainant’s father Mr. Ramanbhai Tadvi as

he was having agency with the insurer. The complainant returned the policy for cancellation to the

local office of the insurer within the free look period. The insurer did not consider his request within

free look period though he had produced the proof of dispatch of his request for cancellation by

speed post. Thus he was cheated by the insurance company by considering the application for

cancellation as being made after three months and not within the free look period. The complainant

has therefore approached the Forum seeking justice.

19. Arguments of the Complainant:

The complainant submitted that he was insured under the policy as mentioned above. The policy

was placed through the agency of his father. After receiving the policy, he was not satisfied with the

terms and the conditions mentioned therein. Hence he made a request to the insurer within the free

look period to cancel the policy. The request for cancellation was sent by speed post to the local

branch office of the insurance company which was not responded to by the company. Later he

represented the case to the Grievance Redressal Officer (GRO) of the insurer. The insurer

considered the said representation to be the application for cancellation and denied the request on

Page 6 of 412

the ground it was made beyond the free look period. Aggrieved with the decision of the insurer, the

complainant has approached this Forum for justice.

20. Arguments of the Respondent:

The insurer’s representative submitted during the hearing that although the complainant had sent

the policy bond through speed post, it was not accepted as it was sent in the name of Manager,

Future Generali, Vadodara Branch and the Branch runs with multiple channels and with multiple

Managers.

21. Result of hearing (Observations & Conclusion):

1. The request for the cancellation was made within free look period. The complainant has

produced the evidence thereof by way of speed post receipt which shows that request for

cancellation along with policy bond was sent on 10.9.2016, within 15 days from date of coverage of

30.08.2016.

2. The respondent insurer admitted to the fact that the complainant sent the policy bond for

cancellation by speed post. However he argued that it was not properly addressed and since the

local branch of the insurer runs with multiple channels with multiple managers, the request of the

complainant was not acted upon. This argument of the insurer is unconvincing and untenable. The

speed post receipt submitted by the complainant reveals that his communication was properly

addressed to the insurer’s Vadodara office and it was up to the insurer to ensure that the

communication was forwarded to the right channel/manager for necessary action. They utterly

failed to do so.

3. The Forum therefore concludes that the request for cancellation of policy was made by the

complainant well within the free look period. The insurer should therefore honour the request,

cancel the policy and refund the premium to the complainant. The Forum has no jurisdiction to

award compensation for mental harassment as claimed by the complainant.

4. The Forum regrets to note non-submission of SCN by the insurer and records its strong

disapproval over the same.

AWARD

Taking into account the documents submitted to the Forum and the submissions

made during the hearing the Forum, hereby, directs the Respondent Insurer to cancel

the policy and refund the premium Rs 100000/- to the Complainant along with interest

as provided under Rule 17(7) of the Insurance Ombudsman Rules, 2017.

Page 7 of 412

22 The attention of the Complainant and the Insurer is hereby invited to Rules 17(6) and 17(8) of the Insurance Ombudsman Rules, 2017 as follows. a) According to Rule 17(6) of Insurance Ombudsman Rules, 2017, the Insurer shall comply with

the award within thirty days of the receipt of the award and intimate compliances of the same to the Ombudsman.

b) According to Rule 17(8) of the said Rules, the award of Insurance Ombudsman shall be binding on the Insurers.

Dated at Ahmedabad on 29th March, 2019.

M. Vasantha Krishna Insurance Ombudsman

PROCEEDINGS BEFORE THE INSURANCE OMBUDSMAN, AHMEDABAD State of Gujarat and Union Territories of Dadra, Nagar Haveli and Daman & Diu

(Under Rule No: 16/17 of The Insurance Ombudsman Rules, 2017) Ombudsman : M. Vasantha Krishna

Case of:- Mr. Anandkumar R Tadvi V/S Future Generali India Life Ins. Co. Ltd Complaint Ref No. : AHD-L-017-1718-0265

Award No. : IO/AHD/A/LI/0002/2018-2019 1 Name of the Complainant & Address

of the complainant.

Mr. Anandkumar R Tadvi,

27, Niranjan Park, B/H Rangvatika, Nr Old

Bapod Jakat Naka, Waghodia Road, Baroda

2 Policy No:

Type of Policy

D.O.C

1309605

Future Generali Assured Money Back Plan

30-08-2016

3 Name of the L.A

Name of the Proposer

Mr. Anandkumar R Tadvi

Mr. Anandkumar R Tadvi

4 Name of the insurer Future Generali India Life Ins. Co. Ltd.

5 Reason of repudiation Request for cancellation of policy

not within free look period

6 Date of receipt of complaint 19/01/2017

7 Nature of complaint Refusal of request for free-look cancellation

8 Amount of Claim Rs 100000/-

11 Amount of relief sought Rs 100000/- plus Rs 20000 for

mental harassment and interest

12 Date of receipt of Consent/SCN 05/07/2017 / SCN not received

Page 8 of 412

13 Complaint registered under Rule No. Rule13-1-b of IO Rules, 2017

14 Date of hearing/place 30/11/2018/Ahmedabad

15 Representation at the hearing:

For the Complainant

For the Insurer

Mr. Anandkumar R Tadvi

Mr Nitesh Jain

16 Complaint how disposed Award

17 Date of Award/Order 29/03/2019

18. Brief facts of the case:

The complainant was insured under the Future Generali Assured Money Back Plan Policy of the

respondent insurer. The policy was canvassed by the complainant’s father Mr. Ramanbhai Tadvi as he

was having agency with the insurer. The complainant returned the policy for cancellation to the local

office of the insurer within the free look period. The insurer did not consider his request within free look

period though he had produced the proof of dispatch of his request for cancellation by speed post. Thus

he was cheated by the insurance company by considering the application for cancellation as being

made after three months and not within the free look period. The complainant has therefore

approached the Forum seeking justice.

19. Arguments of the Complainant:

The complainant submitted that he was insured under the policy as mentioned above. The policy was

placed through the agency of his father. After receiving the policy, he was not satisfied with the terms

and the conditions mentioned therein. Hence he made a request to the insurer within the free look

period to cancel the policy. The request for cancellation was sent by speed post to the local branch

office of the insurance company which was not responded to by the company. Later he represented the

case to the Grievance Redressal Officer (GRO) of the insurer. The insurer considered the said

representation to be the application for cancellation and denied the request on the ground it was made

beyond the free look period. Aggrieved with the decision of the insurer, the complainant has

approached this Forum for justice.

20. Arguments of the Respondent:

The insurer’s representative submitted during the hearing that although the complainant had sent the

policy bond through speed post, it was not accepted as it was sent in the name of Manager, Future

Generali, Vadodara Branch and the Branch runs with multiple channels and with multiple Managers.

Page 9 of 412

21. Result of hearing (Observations & Conclusion):

5. The request for the cancellation was made within free look period. The complainant has produced the

evidence thereof by way of speed post receipt which shows that request for cancellation along with policy bond

was sent on 10.9.2016, within 15 days from date of coverage of 30.08.2016.

6. The respondent insurer admitted to the fact that the complainant sent the policy bond for cancellation by

speed post. However he argued that it was not properly addressed and since the local branch of the insurer

runs with multiple channels with multiple managers, the request of the complainant was not acted upon. This

argument of the insurer is unconvincing and untenable. The speed post receipt submitted by the complainant

reveals that his communication was properly addressed to the insurer’s Vadodara office and it was up to the

insurer to ensure that the communication was forwarded to the right channel/manager for necessary action.

They utterly failed to do so.

7. The Forum therefore concludes that the request for cancellation of policy was made by the complainant well

within the free look period. The insurer should therefore honour the request, cancel the policy and refund the

premium to the complainant. The Forum has no jurisdiction to award compensation for mental harassment as

claimed by the complainant.

8. The Forum regrets to note non-submission of SCN by the insurer and records its strong disapproval over the

same.

AWARD

Taking into account the documents submitted to the Forum and the submissions made

during the hearing the Forum, hereby, directs the Respondent Insurer to cancel the

policy and refund the premium Rs 100000/- to the Complainant along with interest as

provided under Rule 17(7) of the Insurance Ombudsman Rules, 2017.

23 The attention of the Complainant and the Insurer is hereby invited to Rules 17(6) and 17(8) of the Insurance Ombudsman Rules, 2017 as follows.

A) According to Rule 17(6) of Insurance Ombudsman Rules, 2017, the Insurer shall comply with the award within thirty days of the receipt of the award and intimate compliances of the same to the Ombudsman.

B) According to Rule 17(8) of the said Rules, the award of Insurance Ombudsman shall be binding on the Insurers.

Dated at Ahmedabad on 29th March, 2019.

M. Vasantha Krishna Insurance Ombudsman

Page 10 of 412

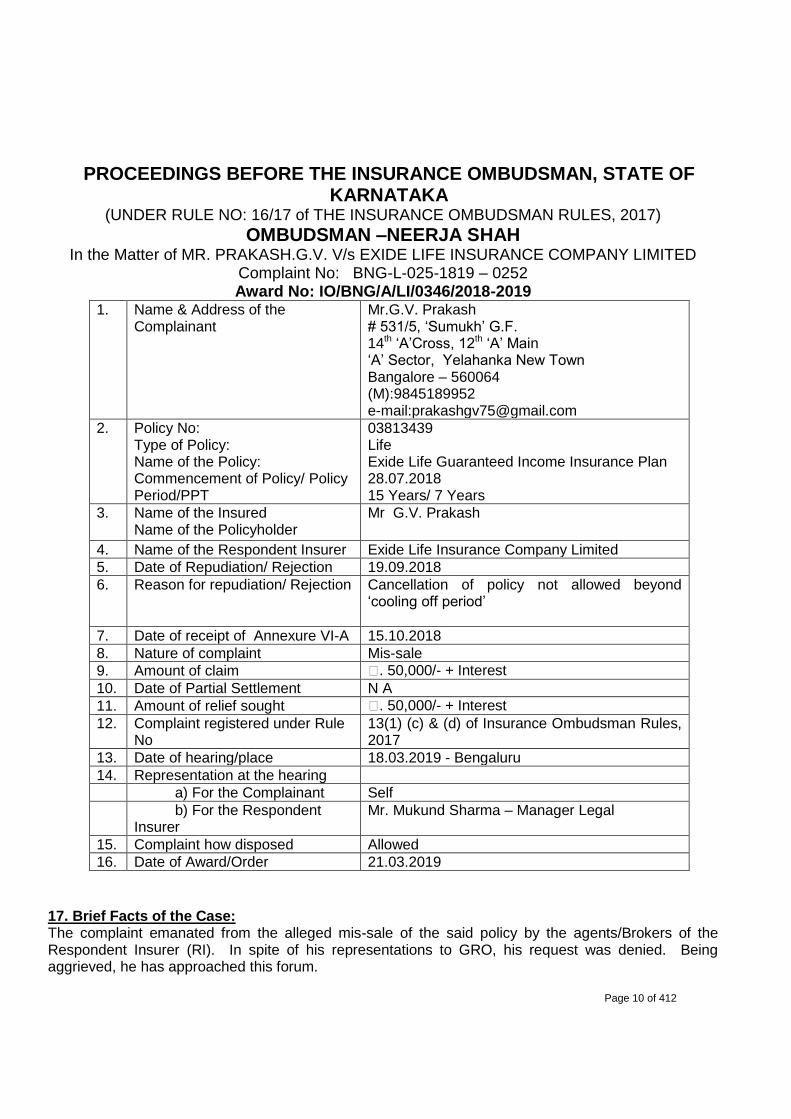

PROCEEDINGS BEFORE THE INSURANCE OMBUDSMAN, STATE OF KARNATAKA

(UNDER RULE NO: 16/17 of THE INSURANCE OMBUDSMAN RULES, 2017)

OMBUDSMAN –NEERJA SHAH In the Matter of MR. PRAKASH.G.V. V/s EXIDE LIFE INSURANCE COMPANY LIMITED

Complaint No: BNG-L-025-1819 – 0252 Award No: IO/BNG/A/LI/0346/2018-2019

1. Name & Address of the Complainant

Mr.G.V. Prakash # 531/5, ‘Sumukh’ G.F. 14th ‘A’Cross, 12th ‘A’ Main ‘A’ Sector, Yelahanka New Town Bangalore – 560064 (M):9845189952 e-mail:[email protected]

2. Policy No: Type of Policy: Name of the Policy: Commencement of Policy/ Policy Period/PPT

03813439 Life Exide Life Guaranteed Income Insurance Plan 28.07.2018 15 Years/ 7 Years

3. Name of the Insured Name of the Policyholder

Mr G.V. Prakash

4. Name of the Respondent Insurer Exide Life Insurance Company Limited

5. Date of Repudiation/ Rejection 19.09.2018

6. Reason for repudiation/ Rejection Cancellation of policy not allowed beyond ‘cooling off period’

7. Date of receipt of Annexure VI-A 15.10.2018

8. Nature of complaint Mis-sale

9. Amount of claim ₹. 50,000/- + Interest

10. Date of Partial Settlement N A

11. Amount of relief sought ₹. 50,000/- + Interest

12. Complaint registered under Rule No

13(1) (c) & (d) of Insurance Ombudsman Rules, 2017

13. Date of hearing/place 18.03.2019 - Bengaluru

14. Representation at the hearing

a) For the Complainant Self

b) For the Respondent Insurer

Mr. Mukund Sharma – Manager Legal

15. Complaint how disposed Allowed

16. Date of Award/Order 21.03.2019

17. Brief Facts of the Case: The complaint emanated from the alleged mis-sale of the said policy by the agents/Brokers of the Respondent Insurer (RI). In spite of his representations to GRO, his request was denied. Being aggrieved, he has approached this forum.

Page 11 of 412

18. Cause of Complaint: - a. Complainant’s argument: The Complainant vide his letter dated 28.09.2018 that he was cheated by the representatives of the RI by promising health insurance package, for the entire family for the next 15 years and ₹. 8 lakhs on surrender after 15 years. When he represented the issue to the officials of the RI, they informed the complainant that he would be receiving the medical health insurance policy in the next 45 days. But even after the long wait nothing has happened and these agents/brokers/officials remained incommunicado. Realising fraud, he has approached this Forum for cancellation of the said policy and refund of premium paid. b. Respondent Insurer’s argument: The RI vide their SCN dated 17.12.2018 has admitted to the issuance of the said policy after receipt of all requirements from the Complainant in order. The said policy was issued and sent to the Complainant along with ‘Cooling Off Cancellation’ clause which stipulates that in the event of the Complainant not being satisfied with the terms and conditions of the policy, he could cancel the same within 15 days from the date of receipt of the policy bond. The features, benefits, terms and conditions of the policy were explained in detail to the Complainant and Complainant availed the said policy only after understanding the policy conditions, benefits, and its features of the policy. The Complainant has not alleged forgery and hence he is estopped from denying the contents of the proposal forms signed by him at the proposal stage. The Complainant has not reverted back to the Company during the cooling off period and lately has brought vague, ambiguous, and evasive plea that the said policy was mis-sold to him on the assurance of medical assurance and incorrect policy benefits. The RI denies such allegation as vague baseless and devoid of any merits. Further the Complainant has adequate financial capacity to pay the premium. As the Complainant has not submitted any proof of mis-selling, and he did not avail the opportunity of ‘Cooling Off Cancellation’ the Company rejected his request of delayed ’cooling off cancellation’. The RI has prayed the Forum that condonation of delay in approaching the RI would lead to mis-carriage of justice and has prayed the Forum to dismiss the said complaint. 19. Reason for Registration of complaint: - The complaint falls within the scope of Insurance Ombudsman Rules, 2017 under Sec 13(1)(d) and hence, it was registered. 20. The following documents were placed for perusal: -

a. Complaint along with enclosures,

b. Respondent Insurer’s SCN along with enclosures and

c. Consent of the Complainant in Annexure VIA &and Respondent Insurer in VII A.

21. Result of personal hearing with both the parties (Observations & Conclusions): The issue to be decided by the Forum is whether this is a case of mis-sale? During the personal hearing on 18.03.2019 the Complainant reiterated his earlier stand. From the records placed before the Forum it is observed that the Complainant wanted a medical health insurance package along with the above policy. But he was sold a traditional life insurance policy only which was totally at variance with the requirements. During the hearing the Complainant informed the Forum that he would like to continue this policy only if it included medical health policy to which the RI informed that they do not have mediclaim policy to offer. Hence, the Forum concludes that the medical

Page 12 of 412

health insurance package sought by the Complainant along with life insurance was not sold to him. Therefore the ‘Mis-Sale’ is established. The representatives of the RI strongly defended the case and informed the Forum that they had taken a decision to cancel the said policy under ‘cooling off cancellation’ by waiving the delay. Since the issue is of ‘Mis-Sale’ the RI should have cancelled the policy on the date of receipt of complaint i.e. 11.09.2018. Instead they have now come forward to return the premium amount after 6 months under ’Cooling Off Cancellation’. In view of Mis-Sale the RI is liable to refund the full premium amount with interest.

AWARD Taking into account, the facts & circumstances of the case, and the submissions made by both the parties during the course of Personal hearing, the RI is directed to refund total premiums received together with interest at 8.25%(6.25% bank rate +2% as per Regulation 14(2)(ii) of Policy Holders Protections Rules 2017) from the date of filing the complaint i.e. 11.09.2018 till the date of payment. Hence, the complaint is ‘Allowed’.

22) Compliance of Award:

The attention of the Complainant and the Respondent Insurer is hereby invited to the provisions of the Insurance Ombudsman Rules, 2017, whereby, the Complainant is directed to submit all the requirements/documents required for settlement of award within 15 days of receipt of the award to the Respondent Insurer. According to Rule 17 (6) of the said Rules, the Respondent Insurer shall comply with the Award within 30 days of the receipt of the Award and shall intimate compliance of the same to the Ombudsman. Dated at Bengaluru on 21th day of March 2019

(NEERJA SHAH) INSURANCE OMBUDSMAN

FOR THE STATE OF KARNATAKA

Page 13 of 412

PROCEEDINGS BEFORE THE INSURANCE OMBUDSMAN, STATE OF

KARNATAKA (UNDER RULE NO: 16/17 of THE INSURANCE OMBUDSMAN RULES, 2017)

OMBUDSMAN – NEERJA SHAH

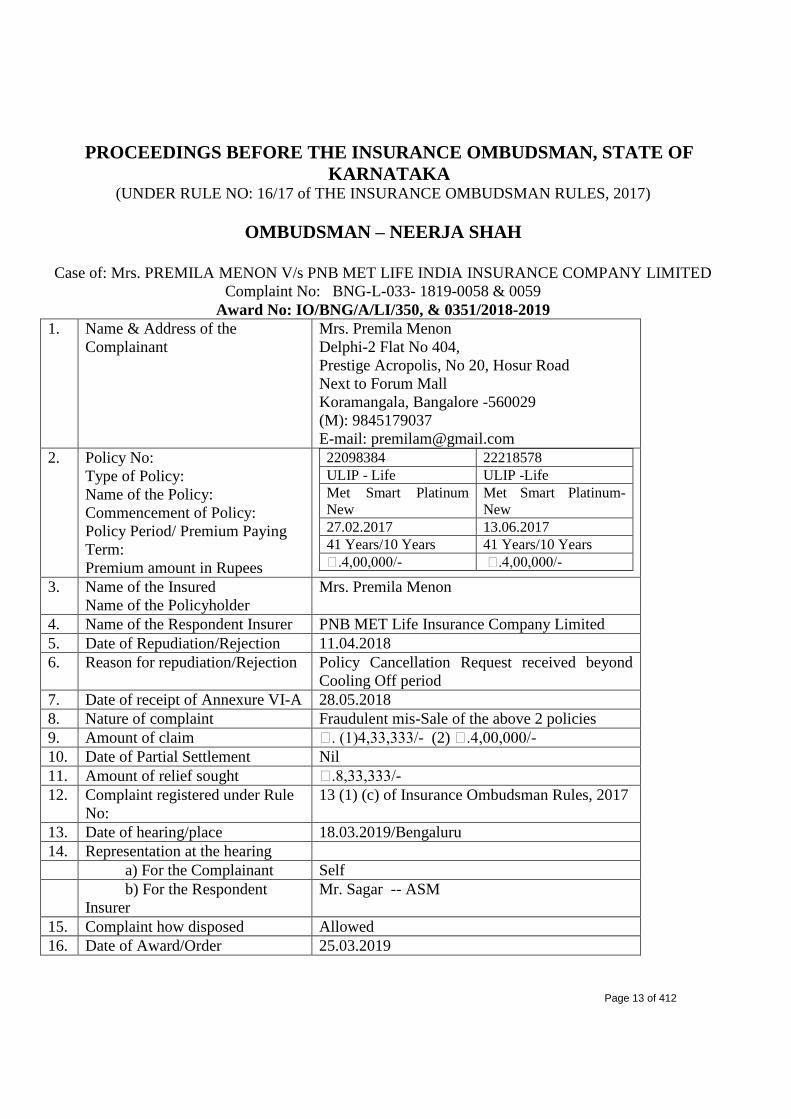

Case of: Mrs. PREMILA MENON V/s PNB MET LIFE INDIA INSURANCE COMPANY LIMITED

Complaint No: BNG-L-033- 1819-0058 & 0059

Award No: IO/BNG/A/LI/350, & 0351/2018-2019

1. Name & Address of the

Complainant

Mrs. Premila Menon

Delphi-2 Flat No 404,

Prestige Acropolis, No 20, Hosur Road

Next to Forum Mall

Koramangala, Bangalore -560029

(M): 9845179037

E-mail: [email protected]

2. Policy No:

Type of Policy:

Name of the Policy:

Commencement of Policy:

Policy Period/ Premium Paying

Term:

Premium amount in Rupees

22098384 22218578

ULIP - Life ULIP -Life

Met Smart Platinum

New

Met Smart Platinum-

New

27.02.2017 13.06.2017

41 Years/10 Years 41 Years/10 Years

₹.4,00,000/- ₹.4,00,000/-

3. Name of the Insured

Name of the Policyholder

Mrs. Premila Menon

4. Name of the Respondent Insurer PNB MET Life Insurance Company Limited

5. Date of Repudiation/Rejection 11.04.2018

6. Reason for repudiation/Rejection Policy Cancellation Request received beyond

Cooling Off period

7. Date of receipt of Annexure VI-A 28.05.2018

8. Nature of complaint Fraudulent mis-Sale of the above 2 policies

9. Amount of claim ₹. (1)4,33,333/- (2) ₹.4,00,000/-

10. Date of Partial Settlement Nil

11. Amount of relief sought ₹.8,33,333/-

12. Complaint registered under Rule

No:

13 (1) (c) of Insurance Ombudsman Rules, 2017

13. Date of hearing/place 18.03.2019/Bengaluru

14. Representation at the hearing

a) For the Complainant Self

b) For the Respondent

Insurer

Mr. Sagar -- ASM

15. Complaint how disposed Allowed

16. Date of Award/Order 25.03.2019

Page 14 of 412

17. Brief Facts of the Case:

The complaint emanated from the alleged fraudulent mis-sale of the said 2 policies by the associates of

Respondent Insurer (RI). In spite of her representation to G.R.O. of the RI, seeking cancellation of the

policies, the G.R.O. declined her request as the same was received by them beyond the ‘Cooling Off

Period’. Hence the Complainant approached this Forum for cancellation of hers policies and refund the

premium thereon.

18. Cause of Complaint: -

a. Complainant’s argument: The Complainant had an old policy with RI wherein she had been paying the premium regularly for the

past 10 years. During the year January 2017, she went to the office of RI to close the old policy as she

had some urgent financial commitment. The sales representatives of the RI convinced the Complainant

that she could avail an insurance cover of over 10 times the single premium i.e. for ₹. 40,00,000/- by

paying a single premium of ₹. 4,00,000/-. The sales representatives also advised the Complainant to

redeem the old policy and in 2 instalments so that the Complainant could avoid some penalty. The first

policy was made in January 2017 and the second policy was made in June 2017. The premium for both

the policies were paid from the proceeds of the old policy. When she received the policy documents,

she was shocked to know that the both the policies were issued for an annual premium of ₹. 4,00,000/-

for a period of 10 years. Though the Complainant informed the sales representatives that she was a

senior citizen without any pensionary benefits, the Sales representatives insisted that she need not worry

and that they would look after the issue. Subsequently the Complainant started getting reminders and

calls from the office of RI to pay renewal premiums. When the Complainant confronted the associates of

the RI, they asked the Complainant to ignore the tele calls. In the month of March 2018, the associates

of the RI came to Complainants house and asked the Complainant to pay an additional amount of ₹.

35,000/- as the market had crashed and the value of the said policy was less than 1 annual premium. To

make good the deficit, the Complainant paid the said amount of ₹.35,000/-. Later on the Complainant

realized that the said amount of ₹.35,000/- was utilized to pay renewal premium on the 1st policy under

monthly mode. The RI sent reminders after reminders saying that the policy premiums had become

overdue and the risk cover had been suspended. Sensing trouble the Complainant went to office of RI

seeking cancellation of the said policy as she had lost confidence with the RI. But the RI declined her

request saying that the Complainant had approached the RI beyond ’Cooling-Off Period’. Being a

senior citizen, she could not sustain the magnitude of fraud being played on her. Hence, the

Complainant approached this Forum seeking cancellation of the said policies and refund of premiums

paid.

b. Respondent Insurer’s argument:

The RI vide their SCN dated 10.09.2018 has admitted to the issuance of said policies. The Complainant

applied for the said 2 policies by submitting all the necessary documents including benefit illustration

and the same being in order. The policy features were explained to the Complainant and she has

understood the same and only after she signed and submitted the same to the RI, the RI issued the said

policies and despatched the same to the Complainant on 03.03.2017 & 26.06.2017 respectively along

with necessary ‘Cooling Off cancellation’ and the Complainant has received the same.

It is implied that the Complainant being highly educated person, duly signed the proposal and

voluntarily applied for the said policies after understanding the product features. The Complainant

Page 15 of 412

submitted a request for changing his address and mode of payment of the premium on 08.02.2018 which

means the Complainant was satisfied with the terms and conditions of the policy. The Complainant

alleged the mis-sale for the first time on 28.03.2018 and as a customer centric organisation the RI sent

a regret letter on 11.04.2018 since the Complainant failed to approach the RI within ‘cooling off period’.

Also the RI mentioned that since the Complainant failed to pay further premiums, the policy is in lapsed

conditions with status ‘discontinued fund’.

Since the RI is not liable to entertain cancellation request which is beyond ‘Cooling Off Period’ as per

IRDA Regulations, the RI rejected the cancellation request of the Complainant. As the Complainant

failed to demonstrate any genuine grievance which is amenable, the present complaint is filed with mala

fide intentions by the Complainant to gain undue advantage of cancellation beyond ‘Cooling Off

Period’, the RI has prayed for dismissal of the same.

19. Reason for Registration of complaint: -

The complaint fell within the scope of the Insurance Ombudsman Rules, 2017 under Sec 13(1)(c) and

so, it was registered.

20. The following documents were placed for perusal: - d. Complaint along with enclosures,

e. Respondent Insurer’s SCN along with enclosures and

f. Consent of the Complainant in Annexure VIA &and Respondent Insurer in VII A

21. Result of personal hearing with both the parties (Observations & Conclusions):

The issue to be decided by the Forum is whether this is a case of fraudulent mis-sale and whether the

Complainant is eligible for refund of premium on such cancellation.

During the personal hearing on 18.03.2019 both the parties reiterated their respective stand.

The Forum after careful deliberations and examination of records notes that the Complainant went to RI

office to redeem their old policy. Instead of redeeming her old policy, the sales representatives of the RI

sold the said insurance policies on the assurance that they were ‘Single Premium Policies’, wherein the

premium is to be paid only once. But when she received the policy documents, she was shocked to note

that they were annual premium policies where an amount of ₹.4,00,000/- is to be paid every year.

The Forum further observes that RI erred in selling the said policies to the Complainants. Being senior

citizens, and of advanced age, instead of redeeming the old policy, they were sold ULIP policies. Further

the Complainants informed the Forum that they did not fill up the proposal forms. They only signed the

proposal in the last page of the proposal form. The RI informed the Forum that they changed the mode

of premium in the 1st policy to monthly mode, in order to enable the Complainants to pay further

premium

instead of single premium. In the process the RI collected ₹.4,00,000/ -+ ₹.4,00,000/- and thereafter

₹.33,333/- as renewal premium payable monthly. The Forum notes that the RI should not have

changed the mode without the consent of the Complainant. The Complainants informed the forum that

Page 16 of 412

the auto debit for the premiums on the said policies were effected by these sales representatives without

their consent.

Hence, considering the facts and circumstances of the case the Forum notes that this is a case of ‘Mis-

Sale’ as non-single premium policy were sold instead of single premium policy.

AWARD

Taking into account the facts & circumstances of the case and the submissions made by both

the parties during the course of the Personal Hearing, the RI is directed to refund the total

premiums received without any deduction and with interest at the rate of 8.25% (6.25%

bank rate +2% as per Policy Holders Protection Rules 2017) from the date of complaint with

the RI i.e. 28.03.2018 to till the date of payment.

Hence the complaint is ‘Allowed’.

23) Compliance of Award:

The attention of the Complainant and the Respondent Insurer is hereby invited to the provisions of the

Insurance Ombudsman Rules, 2017, whereby, the Complainant is directed to submit all the

requirements/documents required for settlement of award within 15 days of receipt of the award.

According to Rule 17 (6) of the said Rules, the Respondent Insurer shall comply with the Award within

30 days of the receipt of the Award and shall intimate compliance of the same to the Ombudsman.

Dated at Bengaluru this 25th

Day of March 2019.

(NEERJA SHAH)

INSURANCE OMBUDSMAN

FOR THE STATE OF KARNATAKA

PROCEEDINGS BEFORE THE INSURANCE OMBUDSMAN, STATE OF

KARNATAKA (UNDER RULE NO: 16/17 of THE INSURANCE OMBUDSMAN RULES, 2017)

OMBUDSMAN – NEERJA SHAH

Case of: MR. MOHAN MENON V/s PNB MET LIFE INDIA INSURANCE COMPANY LIMITED

Complaint No: BNG-L-033- 1819-0037 & 0038

Award No: IO/BNG/A/LI/0352, & 0353/2018-2019

1. Name & Address of the

Complainant

Mr. Mohan Menon

Delphi-2 Flat No 404,

Prestige Acropolis, No 20, Hosur Road

Next to Forum Mall

Page 17 of 412

Koramangala, Bangalore -560029

(M): 9972872327

E-mail: [email protected]

2. Policy No:

Type of Policy:

Name of the Policy:

Commencement of Policy:

Policy Period/ Premium Paying

Term:

22098439 22218732

ULIP - Life ULIP -Life

Met Smart Platinum Met Smart Platinum

31.01.2017 24.05.2017

33 Years/10 Years 33 Years/10 Years

3. Name of the Insured

Name of the Policyholder

Mr. Mohan Menon

4. Name of the Respondent Insurer PNB MET Life Insurance Company Limited

5. Date of Repudiation/Rejection 06.04.2018

6. Reason for repudiation/Rejection Policy Cancellation Request received beyond

Cooling Off period

7. Date of receipt of Annexure VI-A 09.05.2018

8. Nature of complaint Fraudulent mis-Sale of the above 2 policies

9. Amount of claim (1) ₹.3,00,000/- (2) ₹.3,00,000/-

10. Date of Partial Settlement Nil

11. Amount of relief sought ₹.6,25,000/-

12. Complaint registered under Rule

No:

13 (1) (c) of Insurance Ombudsman Rules, 2017

13. Date of hearing/place 18.03.2019 /Bengaluru

14. Representation at the hearing

a) For the Complainant Self

b) For the Respondent

Insurer

Mr. Sagar -- ASM

15. Complaint how disposed Allowed

16. Date of Award/Order 25.03.2019

17. Brief Facts of the Case:

The complaint emanated from the alleged fraudulent mis-sale of the said 2 policies by the associates of

Respondent Insurer (RI). In spite of his representation to G.R.O. of the RI, seeking cancellation of the

policies, the G.R.O. declined his request as the same was received by them beyond the ‘Cooling Off

Period’. Hence the Complainant approached this Forum for cancellation of his policies and refund the

premium thereon.

18. Cause of Complaint: -

a. Complainant’s argument: The Complainant had an old policy with RI wherein he had been paying the premium regularly for the

past 10 years. During the year January 2017, he went to the office of RI to close the old policy as he had

some urgent financial commitment. The sales representatives of the RI convinced the Complainant that

he could avail an insurance cover of ₹. 21,00,000/- by paying a single premium of ₹. 3,00,000/- i.e. he

could enjoy the risk cover 7 times the single premium. The sales representatives also advised the

Page 18 of 412

Complainant to redeem the said policy in 2 instalments (one in January & another in April) so that the

Complainant could avoid some penalty. The first policy was made in Jan 2017 and the 2nd

policy was

made in April 2017. The premium for both the policies were adjusted from the maturity sale proceeds

of the old policy. When he received the policy documents, he was shocked to know that the policy was

issued for an annual premium of ₹. 3,00,000/-for a period of 10 years. Though the Complainant

informed the sales representatives that he was a senior citizen without any pensionary benefits, the Sales

representatives insisted that he need not worry and that they would take care of Complainants policies.

Subsequently the Complainant started getting reminders and calls from the office of RI. When the

Complainant confronted the associates of the RI, they asked the Complainant to ignore the tele calls. In

the month of March 2018, the associates of the RI came to Complainants house and asked the

Complainant to pay an additional amount of₹. 25,000/- as the market had crashed and the value of the

said policy was less than 1 annual premium. To make good the deficit, the Complainant paid the said

amount of ₹.25,000/-. Later on the Complainant realized that the said amount of ₹.25,000/- was

utilized to pay renewal premium on the first policy. The RI sent reminders after reminders saying that

the policy premiums had become overdue and the risk cover had been suspended. Sensing trouble the

Complainant went to office of RI seeking cancellation of the said policy as he had lost confidence with

the RI. But the RI declined his request saying that the Complainant had approached the RI beyond

’Cooling-Off Period’. Being a senior citizen, he could not sustain the magnitude of fraud being played

on him. Hence, the Complainant approached this Forum seeking cancellation of the said policies and

refund of premiums paid.

b. Respondent Insurer’s argument:

The RI vide their SCN dated 27.08.2018 has admitted to the issuance of said policies. The Complainant

applied for the said 2 policies by submitting all the necessary documents including benefit illustration

and the same were in order. The policy features were explained to the Complainant and he has

understood the same and only after he signed and submitted the same to the RI, the RI issued the said

policies and despatched the same to the Complainant on 18.02.2017 & 12.06.2017 along with necessary

‘Cooling Off cancellation’ and the Complainant has received the same.

It is implied that the Complainant being highly educated person, duly signed the proposal and

voluntarily applied for the said policies after understanding the product features. The Complainant

submitted a request for changing his address and mode of payment of the premium on 08.02.2018 which

means the Complainant was satisfied with the terms and conditions of the policy. The Complainant

alleged the mis-sale for the first time on 28.03.2018 and as a customer centric organisation the RI sent

a regret letter on 11.04.2018 since the Complainant failed to approach the RI within ‘cooling off period’.

Also the RI mentioned that since the Complainant failed to pay further premiums, the policy is in lapsed

condition with status ‘discontinued fund’.

Since the RI is not liable to entertain cancellation request which is beyond ‘Cooling Off Period’ as per

IRDA Regulations, the RI rejected the cancellation request of the Complainant. As the Complainant

failed to demonstrate any genuine grievance which is amenable, the present complaint is filed with mala

fide intentions by the Complainant to gain undue advantage of cancellation beyond ‘Cooling Off

Period’, the RI has prayed for dismissal of the same.

Page 19 of 412

19. Reason for Registration of complaint: -

The complaint fell within the scope of the Insurance Ombudsman Rules, 2017 under Sec 13(1)(c) and

so, it was registered.

20. The following documents were placed for perusal: - g. Complaint along with enclosures,

h. Respondent Insurer’s SCN along with enclosures and

i. Consent of the Complainant in Annexure VIA &and Respondent Insurer in VII A

21. Result of personal hearing with both the parties (Observations & Conclusions):

The issue to be decided by the Forum is whether this is a case of fraudulent mis-sale and whether the

Complainant is eligible for refund of premium on such cancellation.

During the personal hearing on 18.03.2019 both the parties reiterated their respective stand.

The Forum after careful deliberations and examination of records, notes that the Complainant went to RI

office to redeem their old policy. Instead of redeeming his old policy, the sales representatives of the RI

sold the said insurance policies on the assurance that they were ‘Single Premium Policies’, wherein the

premium is to be paid only once. But when he received the policy documents, he was shocked to note

that they were annual premium policies where an amount of ₹.3,00,000/- is to be paid every year.

The Forum further observes that RI erred in selling the said policies to the Complainants. Being senior

citizens, and of advanced age, instead of redeeming the old policy they have sold ULIP policies. Further

the Complainants informed the Forum that they did not fill the proposal forms. They only signed the

proposal in the last page. The RI informed the Forum that they changed the mode of premium in the

policy to monthly mode in order to enable the Complainants to pay further premium instead of single

premium. In the process the RI collected ₹.3,00,000/ -+ ₹.3,00,000/- and thereafter ₹.25,000/- as

renewal premium payable monthly. The Forum notes that the RI should not have changed the mode

without the consent of the Complainant. The Complainants informed the forum that the auto debit for

the premiums on the said policies were effected by these sales representatives without the Complaint’s

consent.

Hence, considering the facts and circumstances of the case the Forum that this is a case of ‘Mis-Sale’ as

Non Single premium policies were sold instead of single premium policy.

AWARD

Taking into account the facts & circumstances of the case and the submissions made by both

the parties during the course of the Personal Hearing, the RI is directed to refund the total

premiums paid without any deduction with interest at the rate of 8.25%(6.25% bank rate +

2% extra as per Policy Holders Protection Rules 2017) from the date of filing the complaint

i.e. 28.03.2018 to till date of making the payment.

Hence the complaint is ‘Allowed’.

Page 20 of 412

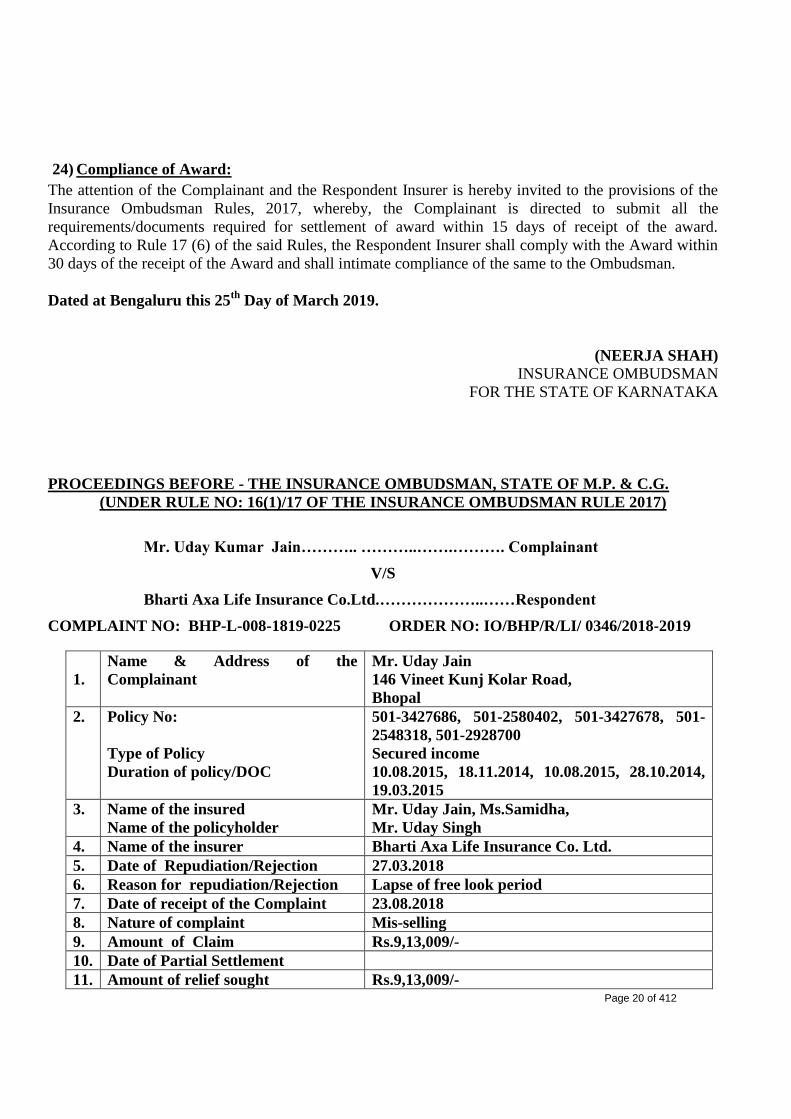

24) Compliance of Award:

The attention of the Complainant and the Respondent Insurer is hereby invited to the provisions of the

Insurance Ombudsman Rules, 2017, whereby, the Complainant is directed to submit all the

requirements/documents required for settlement of award within 15 days of receipt of the award.

According to Rule 17 (6) of the said Rules, the Respondent Insurer shall comply with the Award within

30 days of the receipt of the Award and shall intimate compliance of the same to the Ombudsman.

Dated at Bengaluru this 25th

Day of March 2019.

(NEERJA SHAH)

INSURANCE OMBUDSMAN

FOR THE STATE OF KARNATAKA

PROCEEDINGS BEFORE - THE INSURANCE OMBUDSMAN, STATE OF M.P. & C.G.

(UNDER RULE NO: 16(1)/17 OF THE INSURANCE OMBUDSMAN RULE 2017)

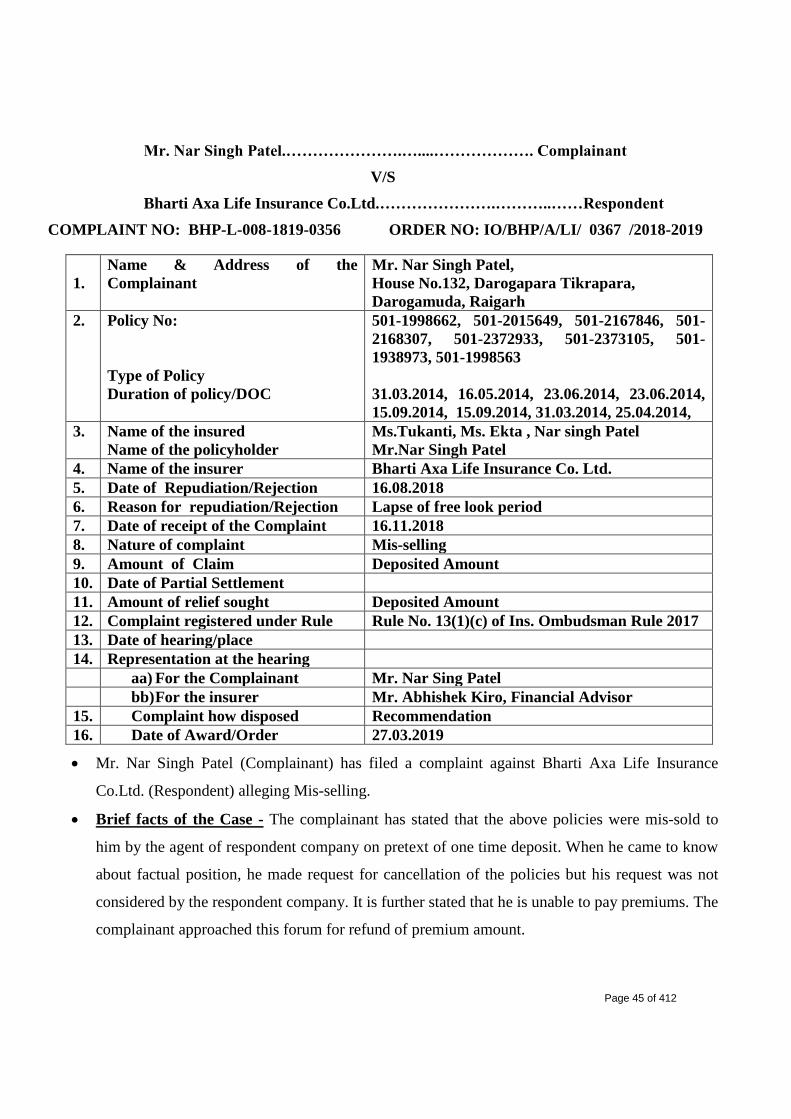

Mr. Uday Kumar Jain……….. ………..…….………. Complainant

V/S

Bharti Axa Life Insurance Co.Ltd.………………..……Respondent

COMPLAINT NO: BHP-L-008-1819-0225 ORDER NO: IO/BHP/R/LI/ 0346/2018-2019

1.

Name & Address of the

Complainant

Mr. Uday Jain

146 Vineet Kunj Kolar Road,

Bhopal

2. Policy No:

Type of Policy

Duration of policy/DOC

501-3427686, 501-2580402, 501-3427678, 501-

2548318, 501-2928700

Secured income

10.08.2015, 18.11.2014, 10.08.2015, 28.10.2014,

19.03.2015

3. Name of the insured

Name of the policyholder

Mr. Uday Jain, Ms.Samidha,

Mr. Uday Singh

4. Name of the insurer Bharti Axa Life Insurance Co. Ltd.

5. Date of Repudiation/Rejection 27.03.2018

6. Reason for repudiation/Rejection Lapse of free look period

7. Date of receipt of the Complaint 23.08.2018

8. Nature of complaint Mis-selling

9. Amount of Claim Rs.9,13,009/-

10. Date of Partial Settlement

11. Amount of relief sought Rs.9,13,009/-

Page 21 of 412

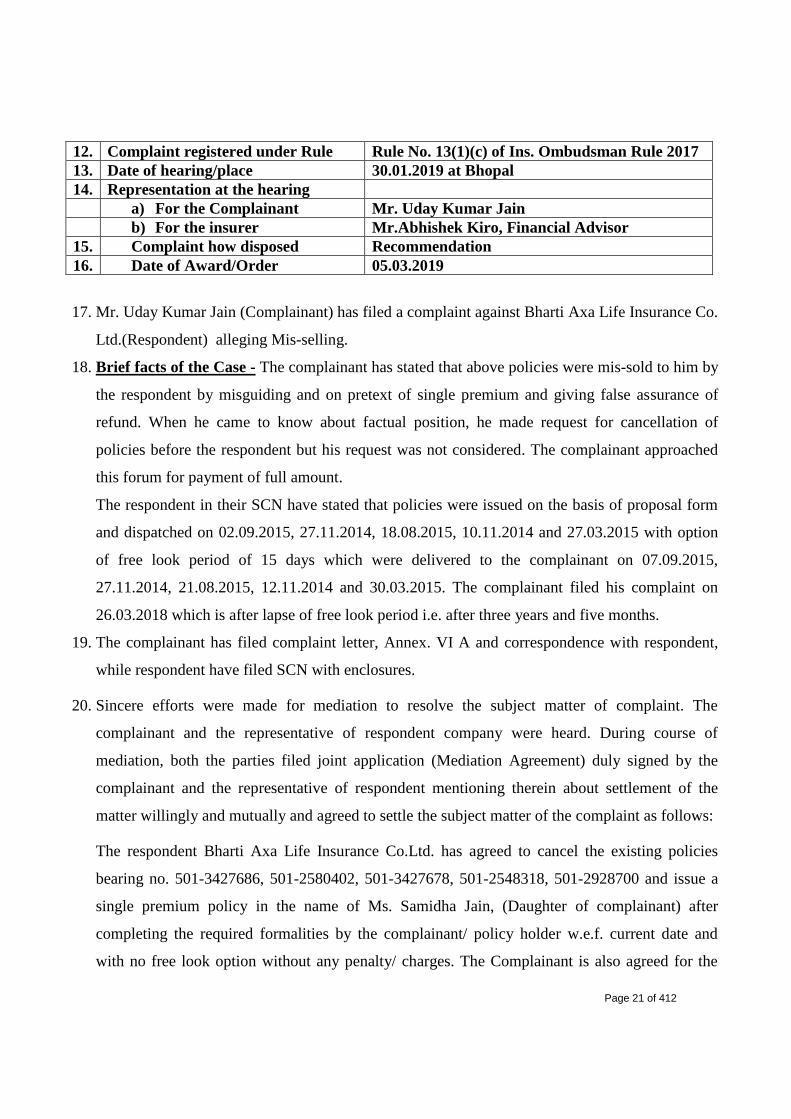

12. Complaint registered under Rule Rule No. 13(1)(c) of Ins. Ombudsman Rule 2017

13. Date of hearing/place 30.01.2019 at Bhopal

14. Representation at the hearing

a) For the Complainant Mr. Uday Kumar Jain

b) For the insurer Mr.Abhishek Kiro, Financial Advisor

15. Complaint how disposed Recommendation

16. Date of Award/Order 05.03.2019

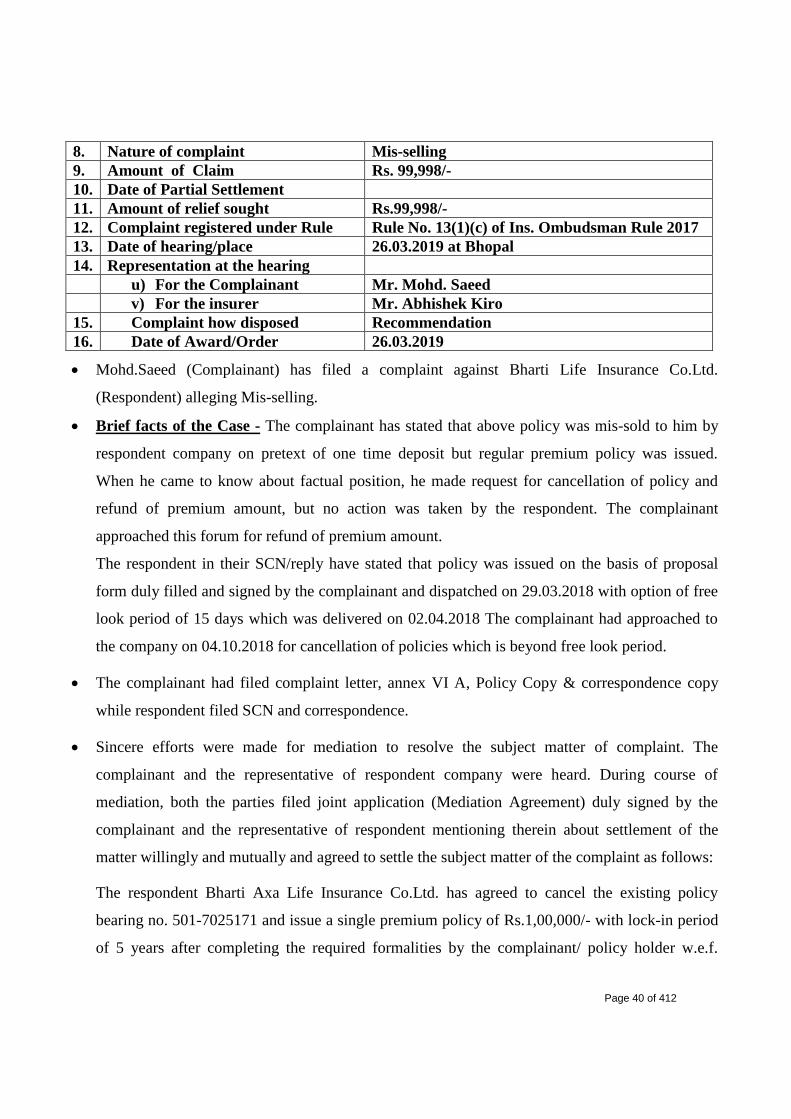

17. Mr. Uday Kumar Jain (Complainant) has filed a complaint against Bharti Axa Life Insurance Co.

Ltd.(Respondent) alleging Mis-selling.

18. Brief facts of the Case - The complainant has stated that above policies were mis-sold to him by

the respondent by misguiding and on pretext of single premium and giving false assurance of

refund. When he came to know about factual position, he made request for cancellation of

policies before the respondent but his request was not considered. The complainant approached

this forum for payment of full amount.

The respondent in their SCN have stated that policies were issued on the basis of proposal form

and dispatched on 02.09.2015, 27.11.2014, 18.08.2015, 10.11.2014 and 27.03.2015 with option

of free look period of 15 days which were delivered to the complainant on 07.09.2015,

27.11.2014, 21.08.2015, 12.11.2014 and 30.03.2015. The complainant filed his complaint on

26.03.2018 which is after lapse of free look period i.e. after three years and five months.

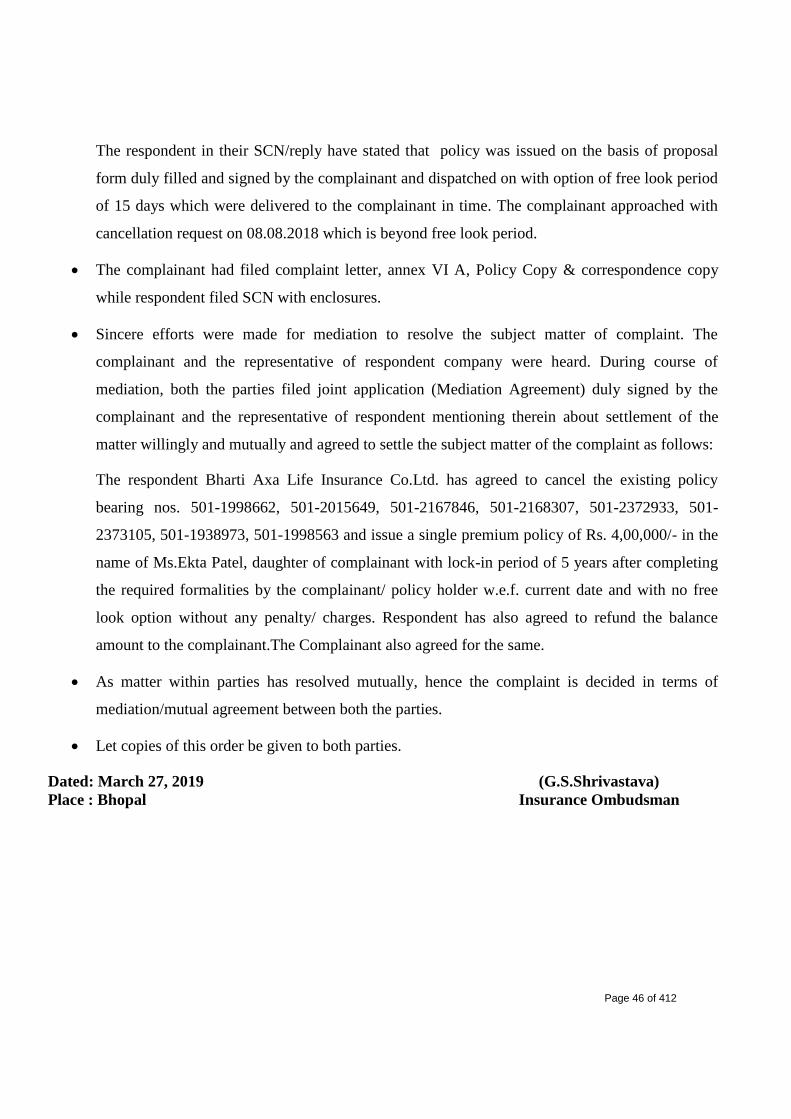

19. The complainant has filed complaint letter, Annex. VI A and correspondence with respondent,

while respondent have filed SCN with enclosures.

20. Sincere efforts were made for mediation to resolve the subject matter of complaint. The

complainant and the representative of respondent company were heard. During course of

mediation, both the parties filed joint application (Mediation Agreement) duly signed by the

complainant and the representative of respondent mentioning therein about settlement of the

matter willingly and mutually and agreed to settle the subject matter of the complaint as follows:

The respondent Bharti Axa Life Insurance Co.Ltd. has agreed to cancel the existing policies

bearing no. 501-3427686, 501-2580402, 501-3427678, 501-2548318, 501-2928700 and issue a

single premium policy in the name of Ms. Samidha Jain, (Daughter of complainant) after

completing the required formalities by the complainant/ policy holder w.e.f. current date and

with no free look option without any penalty/ charges. The Complainant is also agreed for the

Page 22 of 412

same. Respondent is also agreed to make an enquiry with respect to amount of two DD as

mentioned in complaint and inform complainant accordingly.

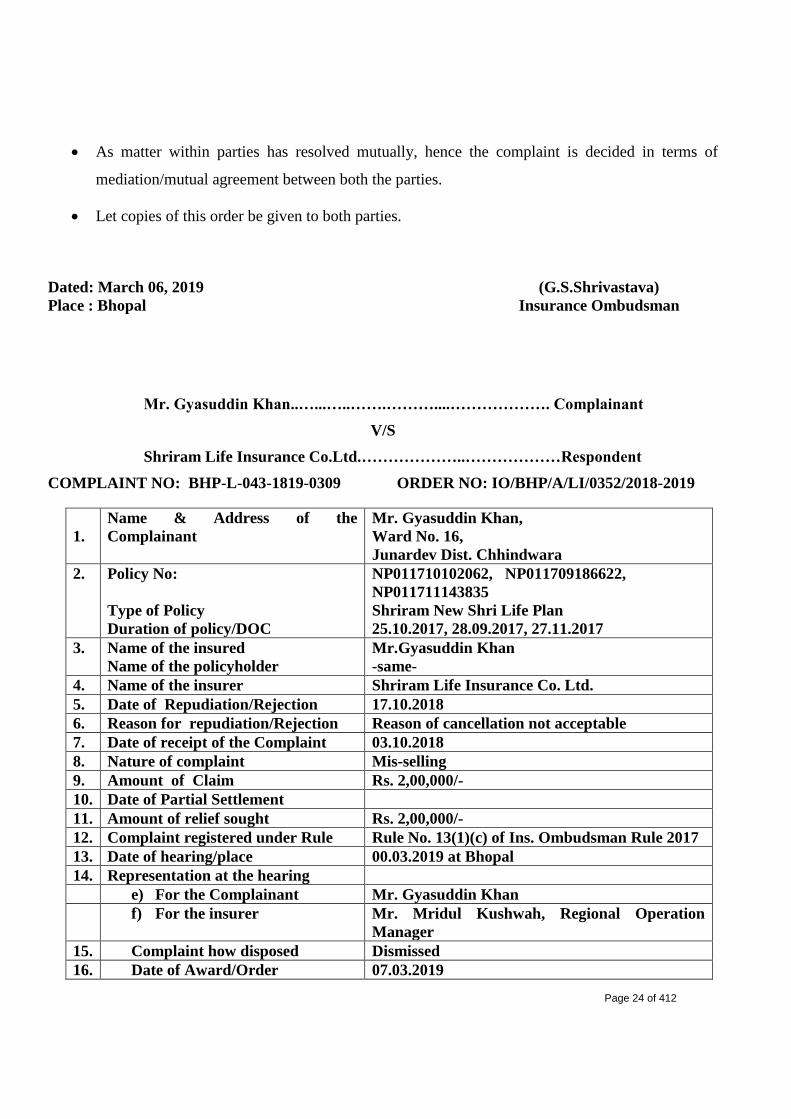

21. As matter within parties has resolved mutually, hence the complaint is decided in terms of

mediation/mutual agreement between both the parties.

22. Let copies of this order be given to both parties.

Dated: March 05, 2019 (G.S.Shrivastava)

Place : Bhopal Insurance Ombudsman

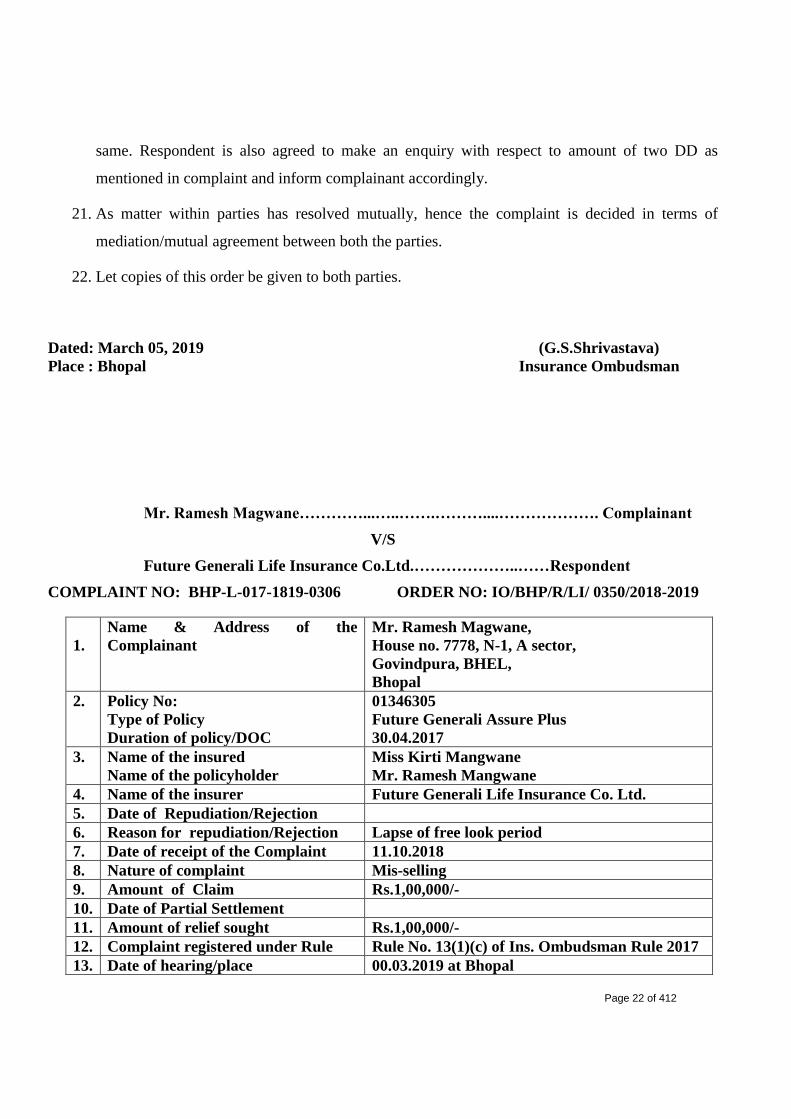

Mr. Ramesh Magwane…………...…..…….………....………………. Complainant

V/S

Future Generali Life Insurance Co.Ltd.………………..……Respondent

COMPLAINT NO: BHP-L-017-1819-0306 ORDER NO: IO/BHP/R/LI/ 0350/2018-2019

1.

Name & Address of the

Complainant

Mr. Ramesh Magwane,

House no. 7778, N-1, A sector,

Govindpura, BHEL,

Bhopal

2. Policy No:

Type of Policy

Duration of policy/DOC

01346305

Future Generali Assure Plus

30.04.2017

3. Name of the insured

Name of the policyholder

Miss Kirti Mangwane

Mr. Ramesh Mangwane

4. Name of the insurer Future Generali Life Insurance Co. Ltd.

5. Date of Repudiation/Rejection

6. Reason for repudiation/Rejection Lapse of free look period

7. Date of receipt of the Complaint 11.10.2018

8. Nature of complaint Mis-selling

9. Amount of Claim Rs.1,00,000/-

10. Date of Partial Settlement

11. Amount of relief sought Rs.1,00,000/-

12. Complaint registered under Rule Rule No. 13(1)(c) of Ins. Ombudsman Rule 2017

13. Date of hearing/place 00.03.2019 at Bhopal

Page 23 of 412

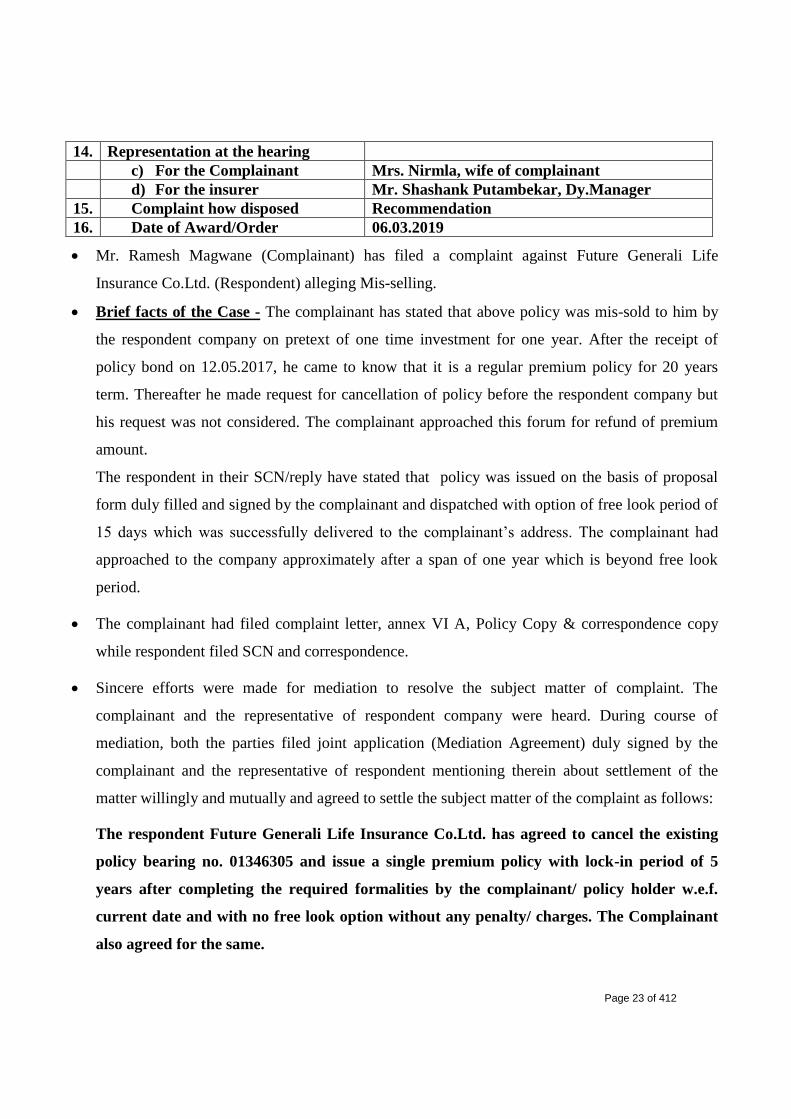

14. Representation at the hearing

c) For the Complainant Mrs. Nirmla, wife of complainant

d) For the insurer Mr. Shashank Putambekar, Dy.Manager

15. Complaint how disposed Recommendation

16. Date of Award/Order 06.03.2019

Mr. Ramesh Magwane (Complainant) has filed a complaint against Future Generali Life

Insurance Co.Ltd. (Respondent) alleging Mis-selling.

Brief facts of the Case - The complainant has stated that above policy was mis-sold to him by

the respondent company on pretext of one time investment for one year. After the receipt of

policy bond on 12.05.2017, he came to know that it is a regular premium policy for 20 years

term. Thereafter he made request for cancellation of policy before the respondent company but

his request was not considered. The complainant approached this forum for refund of premium

amount.

The respondent in their SCN/reply have stated that policy was issued on the basis of proposal

form duly filled and signed by the complainant and dispatched with option of free look period of

15 days which was successfully delivered to the complainant’s address. The complainant had

approached to the company approximately after a span of one year which is beyond free look

period.

The complainant had filed complaint letter, annex VI A, Policy Copy & correspondence copy

while respondent filed SCN and correspondence.

Sincere efforts were made for mediation to resolve the subject matter of complaint. The

complainant and the representative of respondent company were heard. During course of

mediation, both the parties filed joint application (Mediation Agreement) duly signed by the

complainant and the representative of respondent mentioning therein about settlement of the

matter willingly and mutually and agreed to settle the subject matter of the complaint as follows:

The respondent Future Generali Life Insurance Co.Ltd. has agreed to cancel the existing

policy bearing no. 01346305 and issue a single premium policy with lock-in period of 5

years after completing the required formalities by the complainant/ policy holder w.e.f.

current date and with no free look option without any penalty/ charges. The Complainant

also agreed for the same.

Page 24 of 412

As matter within parties has resolved mutually, hence the complaint is decided in terms of

mediation/mutual agreement between both the parties.

Let copies of this order be given to both parties.

Dated: March 06, 2019 (G.S.Shrivastava)

Place : Bhopal Insurance Ombudsman

Mr. Gyasuddin Khan..…...…..…….………....………………. Complainant

V/S

Shriram Life Insurance Co.Ltd.………………..………………Respondent

COMPLAINT NO: BHP-L-043-1819-0309 ORDER NO: IO/BHP/A/LI/0352/2018-2019

1.

Name & Address of the

Complainant

Mr. Gyasuddin Khan,

Ward No. 16,

Junardev Dist. Chhindwara

2. Policy No:

Type of Policy

Duration of policy/DOC

NP011710102062, NP011709186622,

NP011711143835

Shriram New Shri Life Plan

25.10.2017, 28.09.2017, 27.11.2017

3. Name of the insured

Name of the policyholder

Mr.Gyasuddin Khan

-same-

4. Name of the insurer Shriram Life Insurance Co. Ltd.

5. Date of Repudiation/Rejection 17.10.2018

6. Reason for repudiation/Rejection Reason of cancellation not acceptable

7. Date of receipt of the Complaint 03.10.2018

8. Nature of complaint Mis-selling

9. Amount of Claim Rs. 2,00,000/-

10. Date of Partial Settlement

11. Amount of relief sought Rs. 2,00,000/-

12. Complaint registered under Rule Rule No. 13(1)(c) of Ins. Ombudsman Rule 2017

13. Date of hearing/place 00.03.2019 at Bhopal

14. Representation at the hearing

e) For the Complainant Mr. Gyasuddin Khan

f) For the insurer Mr. Mridul Kushwah, Regional Operation

Manager

15. Complaint how disposed Dismissed

16. Date of Award/Order 07.03.2019

Page 25 of 412

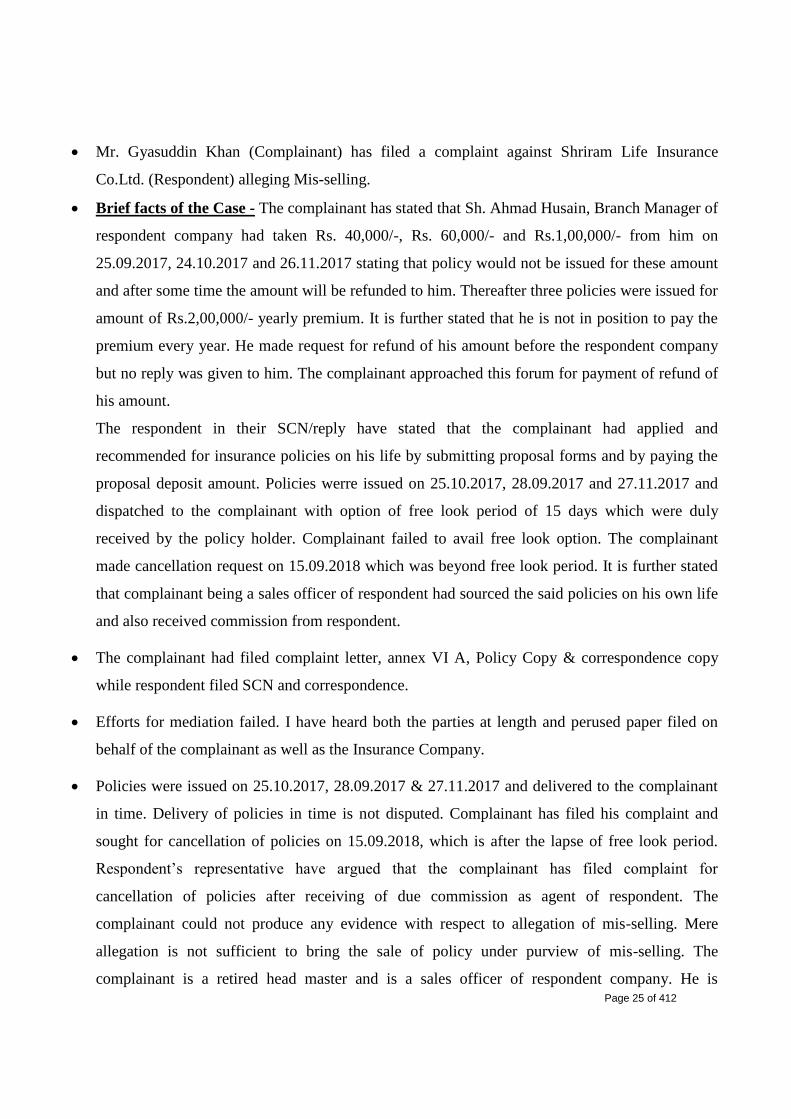

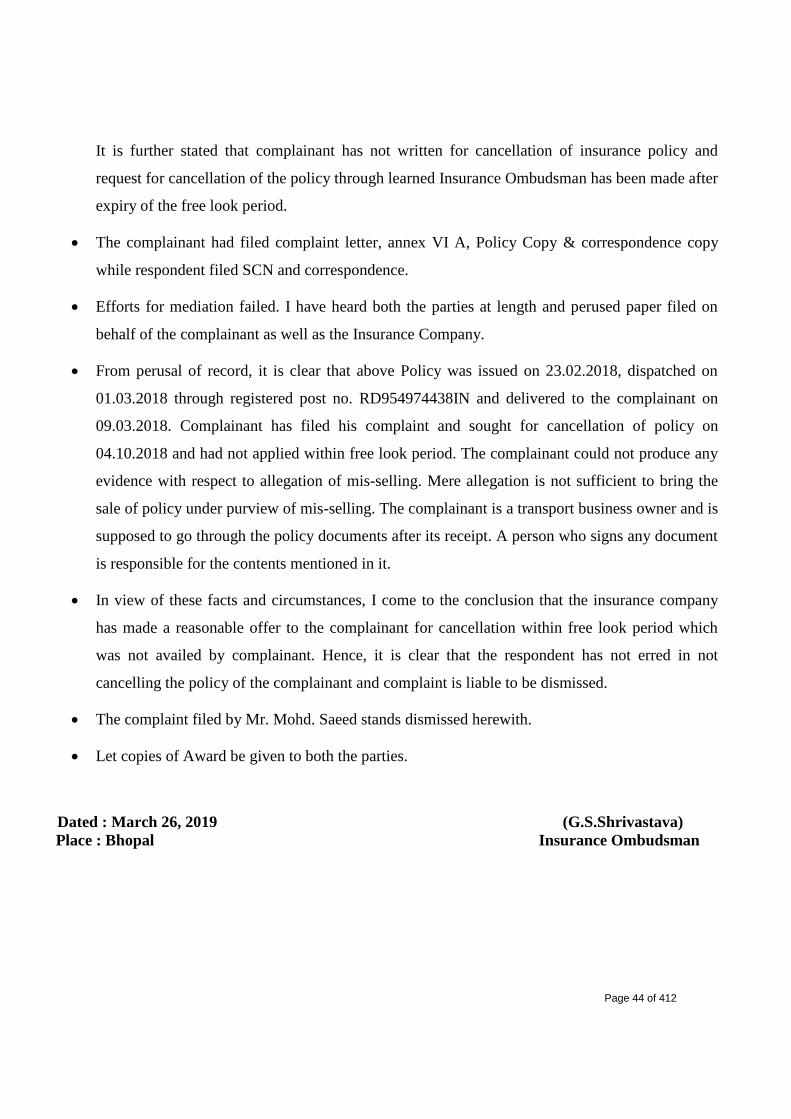

Mr. Gyasuddin Khan (Complainant) has filed a complaint against Shriram Life Insurance

Co.Ltd. (Respondent) alleging Mis-selling.

Brief facts of the Case - The complainant has stated that Sh. Ahmad Husain, Branch Manager of

respondent company had taken Rs. 40,000/-, Rs. 60,000/- and Rs.1,00,000/- from him on

25.09.2017, 24.10.2017 and 26.11.2017 stating that policy would not be issued for these amount

and after some time the amount will be refunded to him. Thereafter three policies were issued for

amount of Rs.2,00,000/- yearly premium. It is further stated that he is not in position to pay the

premium every year. He made request for refund of his amount before the respondent company

but no reply was given to him. The complainant approached this forum for payment of refund of

his amount.

The respondent in their SCN/reply have stated that the complainant had applied and

recommended for insurance policies on his life by submitting proposal forms and by paying the

proposal deposit amount. Policies werre issued on 25.10.2017, 28.09.2017 and 27.11.2017 and

dispatched to the complainant with option of free look period of 15 days which were duly

received by the policy holder. Complainant failed to avail free look option. The complainant

made cancellation request on 15.09.2018 which was beyond free look period. It is further stated

that complainant being a sales officer of respondent had sourced the said policies on his own life

and also received commission from respondent.

The complainant had filed complaint letter, annex VI A, Policy Copy & correspondence copy

while respondent filed SCN and correspondence.

Efforts for mediation failed. I have heard both the parties at length and perused paper filed on

behalf of the complainant as well as the Insurance Company.

Policies were issued on 25.10.2017, 28.09.2017 & 27.11.2017 and delivered to the complainant

in time. Delivery of policies in time is not disputed. Complainant has filed his complaint and

sought for cancellation of policies on 15.09.2018, which is after the lapse of free look period.

Respondent’s representative have argued that the complainant has filed complaint for

cancellation of policies after receiving of due commission as agent of respondent. The

complainant could not produce any evidence with respect to allegation of mis-selling. Mere

allegation is not sufficient to bring the sale of policy under purview of mis-selling. The

complainant is a retired head master and is a sales officer of respondent company. He is

Page 26 of 412

supposed to go through the policy documents after its receipt. A person who signs any document

is responsible for the contents mentioned in it.

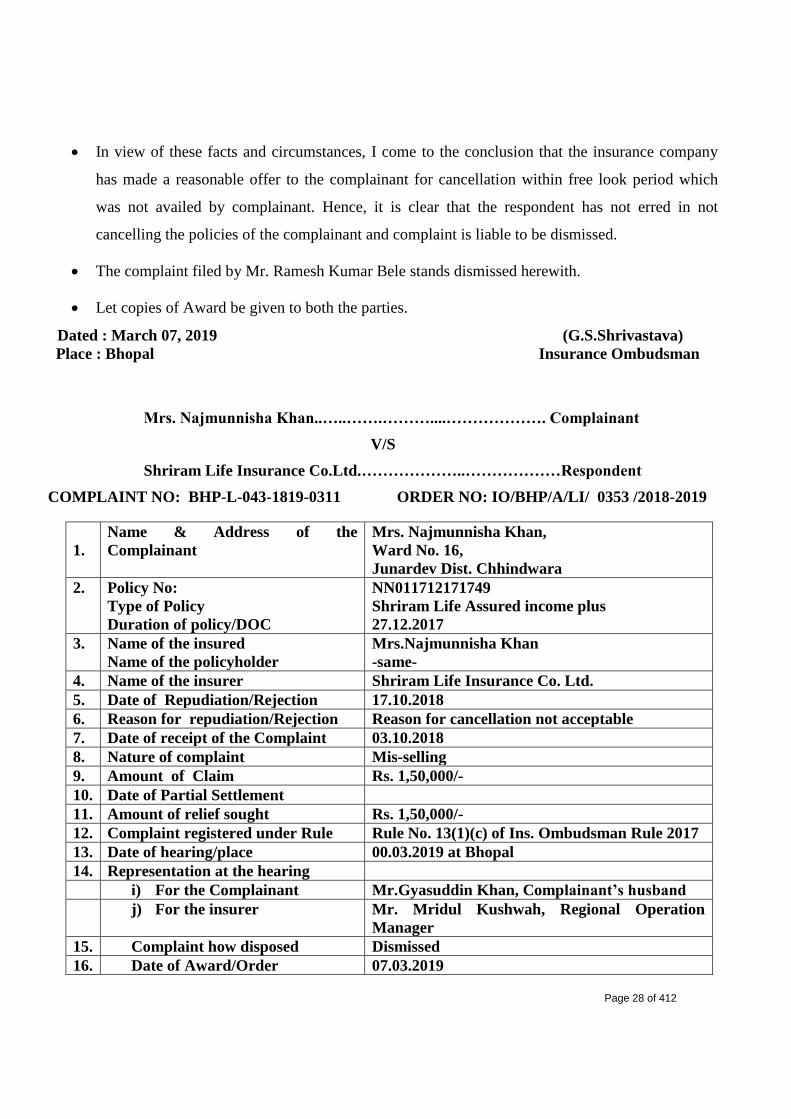

In view of these facts and circumstances, I come to the conclusion that the insurance company

has made a reasonable offer to the complainant for cancellation within free look period which

was not availed by complainant. Hence, it is clear that the respondent has not erred in not

cancelling the policies of the complainant and complaint is liable to be dismissed.

The complaint filed by Mr. Gyasuddin Khan stands dismissed herewith.

Let copies of Award be given to both the parties.

Dated : March 07, 2019 (G.S.Shrivastava)

Place : Bhopal Insurance Ombudsman

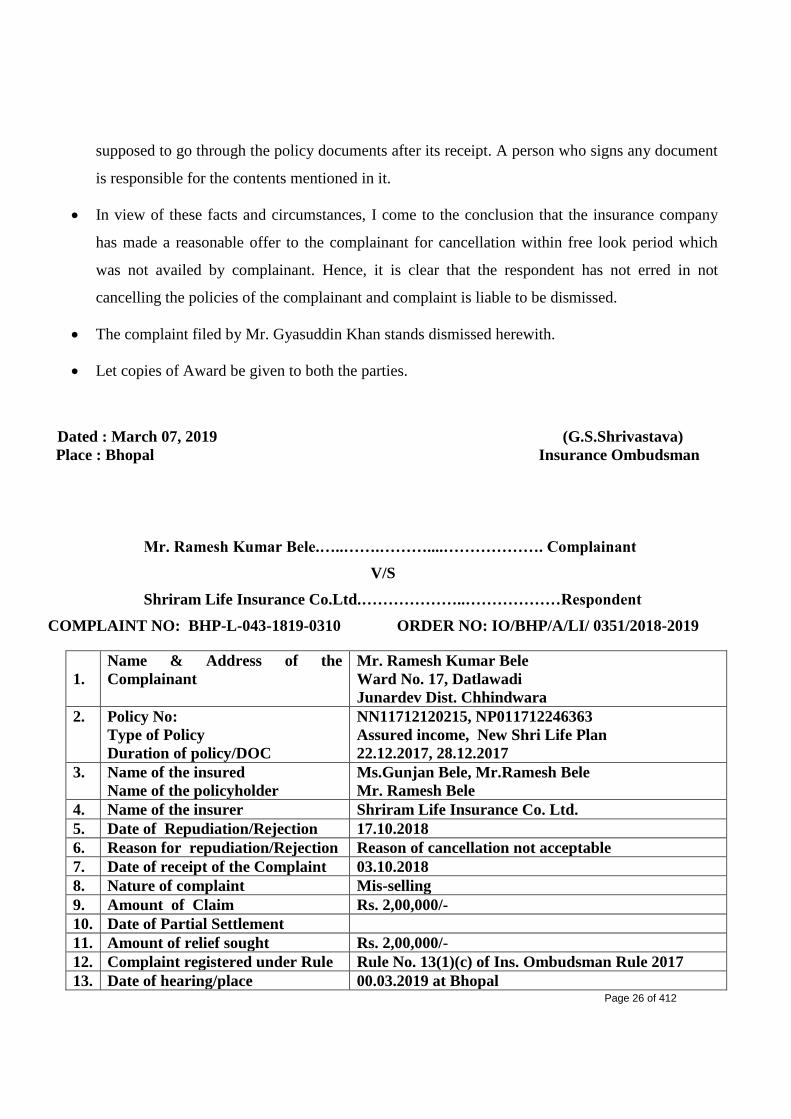

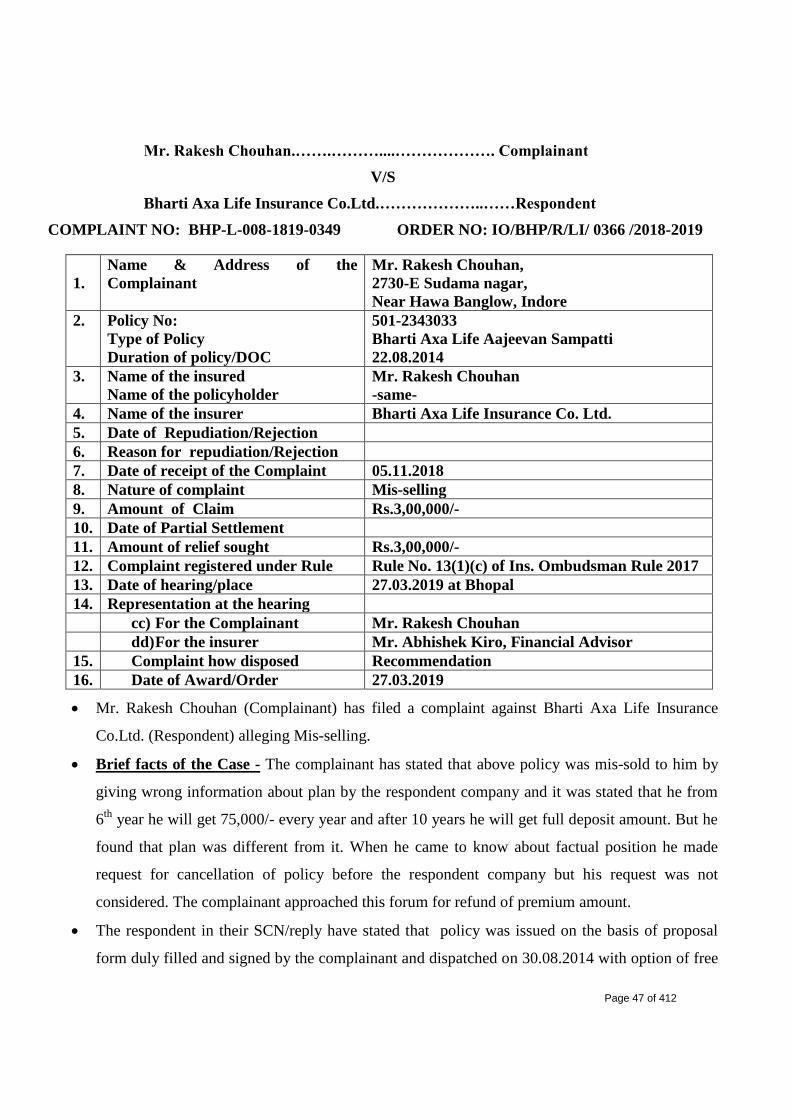

Mr. Ramesh Kumar Bele.…..…….………....………………. Complainant

V/S

Shriram Life Insurance Co.Ltd.………………..………………Respondent

COMPLAINT NO: BHP-L-043-1819-0310 ORDER NO: IO/BHP/A/LI/ 0351/2018-2019

1.

Name & Address of the

Complainant

Mr. Ramesh Kumar Bele

Ward No. 17, Datlawadi

Junardev Dist. Chhindwara

2. Policy No:

Type of Policy

Duration of policy/DOC

NN11712120215, NP011712246363

Assured income, New Shri Life Plan

22.12.2017, 28.12.2017

3. Name of the insured

Name of the policyholder

Ms.Gunjan Bele, Mr.Ramesh Bele

Mr. Ramesh Bele

4. Name of the insurer Shriram Life Insurance Co. Ltd.

5. Date of Repudiation/Rejection 17.10.2018

6. Reason for repudiation/Rejection Reason of cancellation not acceptable

7. Date of receipt of the Complaint 03.10.2018

8. Nature of complaint Mis-selling

9. Amount of Claim Rs. 2,00,000/-

10. Date of Partial Settlement

11. Amount of relief sought Rs. 2,00,000/-

12. Complaint registered under Rule Rule No. 13(1)(c) of Ins. Ombudsman Rule 2017

13. Date of hearing/place 00.03.2019 at Bhopal

Page 27 of 412

14. Representation at the hearing

g) For the Complainant Mr. Gyasuddin Khan, representative of complainant

h) For the insurer Mr. Mridul Kushwah, Regional Operation Manager

15. Complaint how disposed Dismissed

16. Date of Award/Order 07.03.2019

Mr. Ramesh Kumar Bele (Complainant) has filed a complaint against Shriram Life Insurance

Co.Ltd. (Respondent) alleging Mis-selling.

Brief facts of the Case - The complainant has stated that he had given Rs.2,00,000/- to Sh.

Ahmad Husain, Branch Manager of respondent company for issuance of single premium policy

but he fraudulently issued a policy for premium paying term of 10 years. He is unable to pay

premium every year and made request for cancellation of policies and refund of amount before

the respondent company but no reply was given to him. The complainant approached this forum

for payment of refund of his amount.

The respondent in their SCN/reply have stated that the complainant had proposed for insurance

policy on his life by submitting proposal form and by paying the proposal deposit amount. Policy

was issued on 22.12.2017 & 28.12.2017 and dispatched to the complainant for option of free

look period of 15 days which were duly received by the policy holder. Complainant has failed to

avail free look option. The complainant made cancellation request on 15.09.2018 which was

beyond free look period.

The complainant had filed complaint letter, annex VI A, Policy Copy & correspondence copy

while respondent filed SCN and correspondence.

Efforts for mediation failed. I have heard both the parties at length and perused paper filed on

behalf of the complainant as well as the Insurance Company.

Policies were issued on 22.12.2017 & 28.12.2017 and delivered to the complainant in time.

Delivery of policies in time is not disputed. Complainant has filed his complaint and sought for

cancellation of policies on 15.09.2018, which is after the lapse of free look period. The

complainant could not produce any evidence with respect to allegation of mis-selling. Mere

allegation is not sufficient to bring the sale of policy under purview of mis-selling. The

complainant is a post graduate. He is supposed to go through the policy documents after its

receipt. A person who signs any document is responsible for the contents mentioned in it.

Page 28 of 412

In view of these facts and circumstances, I come to the conclusion that the insurance company

has made a reasonable offer to the complainant for cancellation within free look period which

was not availed by complainant. Hence, it is clear that the respondent has not erred in not

cancelling the policies of the complainant and complaint is liable to be dismissed.

The complaint filed by Mr. Ramesh Kumar Bele stands dismissed herewith.

Let copies of Award be given to both the parties.

Dated : March 07, 2019 (G.S.Shrivastava)

Place : Bhopal Insurance Ombudsman

Mrs. Najmunnisha Khan..…..…….………....………………. Complainant

V/S

Shriram Life Insurance Co.Ltd.………………..………………Respondent

COMPLAINT NO: BHP-L-043-1819-0311 ORDER NO: IO/BHP/A/LI/ 0353 /2018-2019

1.

Name & Address of the

Complainant

Mrs. Najmunnisha Khan,

Ward No. 16,

Junardev Dist. Chhindwara

2. Policy No:

Type of Policy

Duration of policy/DOC

NN011712171749

Shriram Life Assured income plus

27.12.2017

3. Name of the insured

Name of the policyholder

Mrs.Najmunnisha Khan

-same-

4. Name of the insurer Shriram Life Insurance Co. Ltd.

5. Date of Repudiation/Rejection 17.10.2018

6. Reason for repudiation/Rejection Reason for cancellation not acceptable

7. Date of receipt of the Complaint 03.10.2018

8. Nature of complaint Mis-selling

9. Amount of Claim Rs. 1,50,000/-

10. Date of Partial Settlement

11. Amount of relief sought Rs. 1,50,000/-

12. Complaint registered under Rule Rule No. 13(1)(c) of Ins. Ombudsman Rule 2017

13. Date of hearing/place 00.03.2019 at Bhopal

14. Representation at the hearing

i) For the Complainant Mr.Gyasuddin Khan, Complainant’s husband

j) For the insurer Mr. Mridul Kushwah, Regional Operation

Manager

15. Complaint how disposed Dismissed

16. Date of Award/Order 07.03.2019

Page 29 of 412

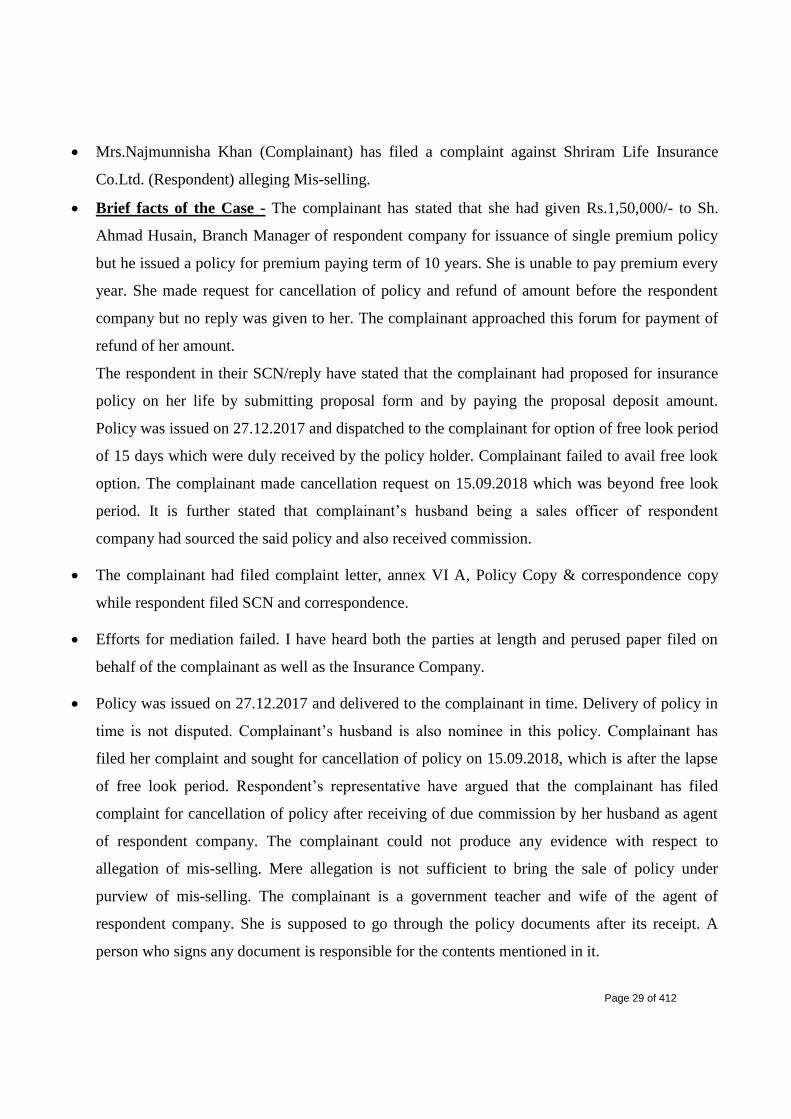

Mrs.Najmunnisha Khan (Complainant) has filed a complaint against Shriram Life Insurance

Co.Ltd. (Respondent) alleging Mis-selling.

Brief facts of the Case - The complainant has stated that she had given Rs.1,50,000/- to Sh.

Ahmad Husain, Branch Manager of respondent company for issuance of single premium policy

but he issued a policy for premium paying term of 10 years. She is unable to pay premium every

year. She made request for cancellation of policy and refund of amount before the respondent

company but no reply was given to her. The complainant approached this forum for payment of

refund of her amount.

The respondent in their SCN/reply have stated that the complainant had proposed for insurance

policy on her life by submitting proposal form and by paying the proposal deposit amount.

Policy was issued on 27.12.2017 and dispatched to the complainant for option of free look period

of 15 days which were duly received by the policy holder. Complainant failed to avail free look

option. The complainant made cancellation request on 15.09.2018 which was beyond free look

period. It is further stated that complainant’s husband being a sales officer of respondent

company had sourced the said policy and also received commission.

The complainant had filed complaint letter, annex VI A, Policy Copy & correspondence copy

while respondent filed SCN and correspondence.

Efforts for mediation failed. I have heard both the parties at length and perused paper filed on

behalf of the complainant as well as the Insurance Company.

Policy was issued on 27.12.2017 and delivered to the complainant in time. Delivery of policy in

time is not disputed. Complainant’s husband is also nominee in this policy. Complainant has

filed her complaint and sought for cancellation of policy on 15.09.2018, which is after the lapse

of free look period. Respondent’s representative have argued that the complainant has filed

complaint for cancellation of policy after receiving of due commission by her husband as agent

of respondent company. The complainant could not produce any evidence with respect to

allegation of mis-selling. Mere allegation is not sufficient to bring the sale of policy under

purview of mis-selling. The complainant is a government teacher and wife of the agent of

respondent company. She is supposed to go through the policy documents after its receipt. A

person who signs any document is responsible for the contents mentioned in it.

Page 30 of 412

In view of these facts and circumstances, I come to the conclusion that the insurance company

has made a reasonable offer to the complainant for cancellation within free look period which

was not availed by complainant. Hence, it is clear that the respondent has not erred in not

cancelling the policy of the complainant and complaint is liable to be dismissed.

The complaint filed by Mrs. Najmunnisha Khan stands dismissed herewith.

Let copies of Award be given to both the parties.

Dated : March 07, 2019 (G.S.Shrivastava)

Place : Bhopal Insurance Ombudsman

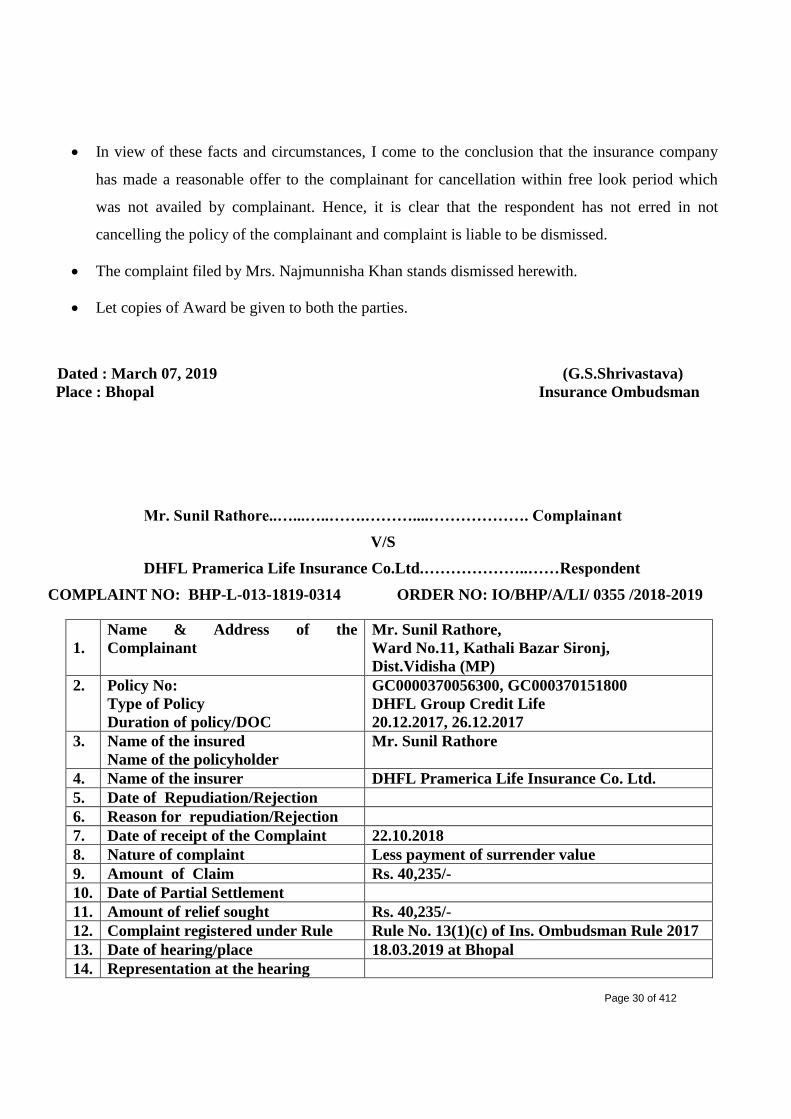

Mr. Sunil Rathore..…...…..…….………....………………. Complainant

V/S

DHFL Pramerica Life Insurance Co.Ltd.………………..……Respondent

COMPLAINT NO: BHP-L-013-1819-0314 ORDER NO: IO/BHP/A/LI/ 0355 /2018-2019

1.

Name & Address of the

Complainant

Mr. Sunil Rathore,

Ward No.11, Kathali Bazar Sironj,

Dist.Vidisha (MP)

2. Policy No:

Type of Policy

Duration of policy/DOC

GC0000370056300, GC000370151800

DHFL Group Credit Life

20.12.2017, 26.12.2017

3. Name of the insured

Name of the policyholder

Mr. Sunil Rathore

4. Name of the insurer DHFL Pramerica Life Insurance Co. Ltd.

5. Date of Repudiation/Rejection

6. Reason for repudiation/Rejection

7. Date of receipt of the Complaint 22.10.2018

8. Nature of complaint Less payment of surrender value

9. Amount of Claim Rs. 40,235/-

10. Date of Partial Settlement

11. Amount of relief sought Rs. 40,235/-

12. Complaint registered under Rule Rule No. 13(1)(c) of Ins. Ombudsman Rule 2017

13. Date of hearing/place 18.03.2019 at Bhopal

14. Representation at the hearing

Page 31 of 412

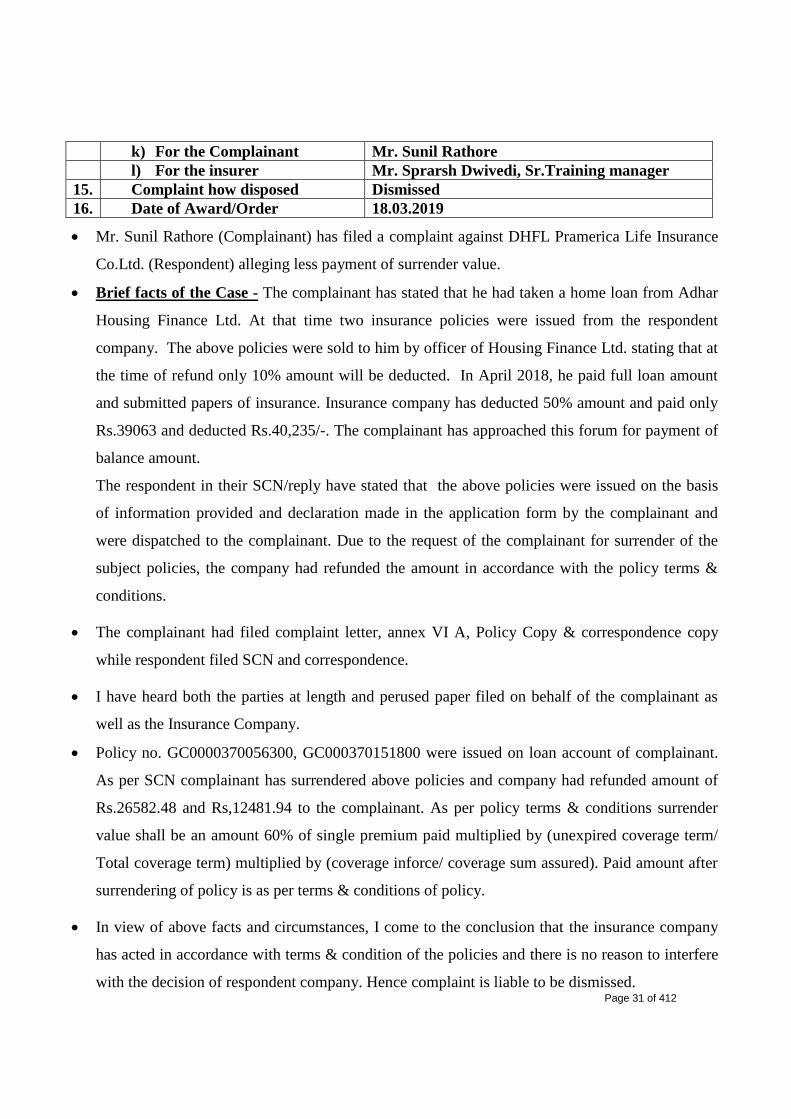

k) For the Complainant Mr. Sunil Rathore

l) For the insurer Mr. Sprarsh Dwivedi, Sr.Training manager

15. Complaint how disposed Dismissed

16. Date of Award/Order 18.03.2019

Mr. Sunil Rathore (Complainant) has filed a complaint against DHFL Pramerica Life Insurance

Co.Ltd. (Respondent) alleging less payment of surrender value.

Brief facts of the Case - The complainant has stated that he had taken a home loan from Adhar

Housing Finance Ltd. At that time two insurance policies were issued from the respondent

company. The above policies were sold to him by officer of Housing Finance Ltd. stating that at

the time of refund only 10% amount will be deducted. In April 2018, he paid full loan amount

and submitted papers of insurance. Insurance company has deducted 50% amount and paid only

Rs.39063 and deducted Rs.40,235/-. The complainant has approached this forum for payment of

balance amount.

The respondent in their SCN/reply have stated that the above policies were issued on the basis

of information provided and declaration made in the application form by the complainant and

were dispatched to the complainant. Due to the request of the complainant for surrender of the

subject policies, the company had refunded the amount in accordance with the policy terms &

conditions.

The complainant had filed complaint letter, annex VI A, Policy Copy & correspondence copy

while respondent filed SCN and correspondence.

I have heard both the parties at length and perused paper filed on behalf of the complainant as

well as the Insurance Company.

Policy no. GC0000370056300, GC000370151800 were issued on loan account of complainant.

As per SCN complainant has surrendered above policies and company had refunded amount of

Rs.26582.48 and Rs,12481.94 to the complainant. As per policy terms & conditions surrender

value shall be an amount 60% of single premium paid multiplied by (unexpired coverage term/

Total coverage term) multiplied by (coverage inforce/ coverage sum assured). Paid amount after

surrendering of policy is as per terms & conditions of policy.

In view of above facts and circumstances, I come to the conclusion that the insurance company

has acted in accordance with terms & condition of the policies and there is no reason to interfere

with the decision of respondent company. Hence complaint is liable to be dismissed.

Page 32 of 412

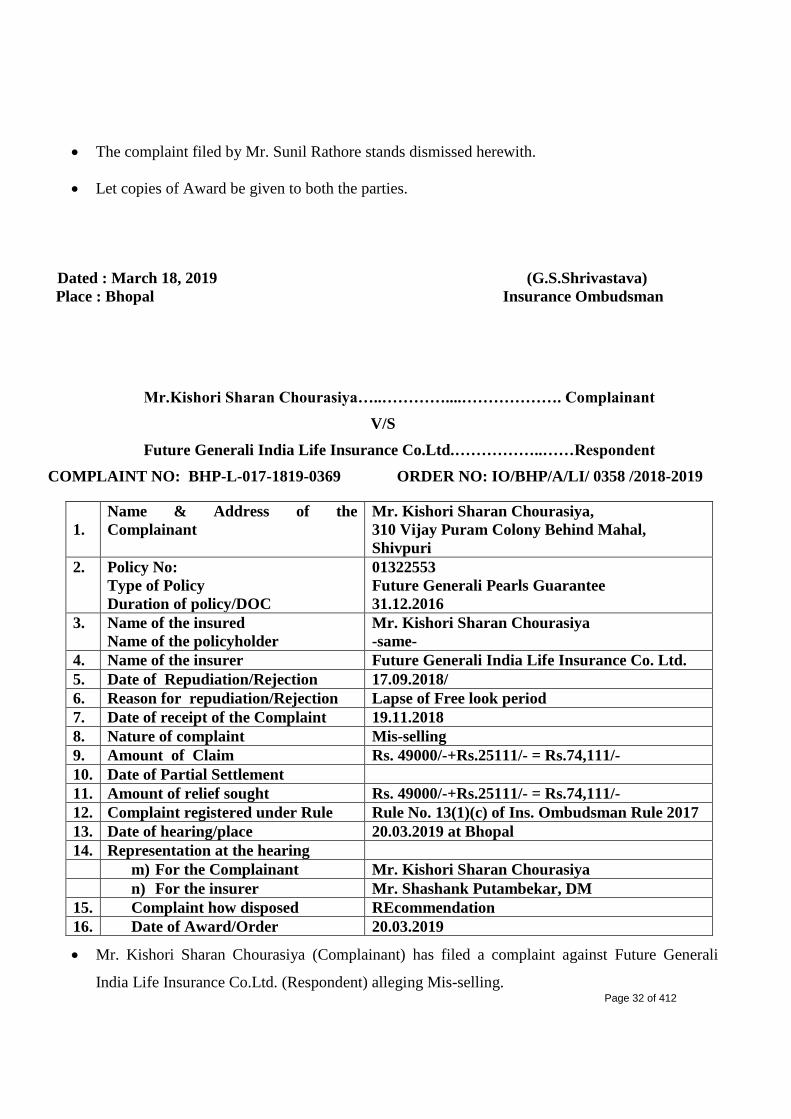

The complaint filed by Mr. Sunil Rathore stands dismissed herewith.

Let copies of Award be given to both the parties.

Dated : March 18, 2019 (G.S.Shrivastava)

Place : Bhopal Insurance Ombudsman

Mr.Kishori Sharan Chourasiya…..…………....………………. Complainant

V/S

Future Generali India Life Insurance Co.Ltd.……………..……Respondent

COMPLAINT NO: BHP-L-017-1819-0369 ORDER NO: IO/BHP/A/LI/ 0358 /2018-2019

1.

Name & Address of the

Complainant

Mr. Kishori Sharan Chourasiya,

310 Vijay Puram Colony Behind Mahal,

Shivpuri

2. Policy No:

Type of Policy

Duration of policy/DOC

01322553

Future Generali Pearls Guarantee

31.12.2016

3. Name of the insured

Name of the policyholder

Mr. Kishori Sharan Chourasiya

-same-

4. Name of the insurer Future Generali India Life Insurance Co. Ltd.

5. Date of Repudiation/Rejection 17.09.2018/

6. Reason for repudiation/Rejection Lapse of Free look period

7. Date of receipt of the Complaint 19.11.2018

8. Nature of complaint Mis-selling

9. Amount of Claim Rs. 49000/-+Rs.25111/- = Rs.74,111/-

10. Date of Partial Settlement

11. Amount of relief sought Rs. 49000/-+Rs.25111/- = Rs.74,111/-

12. Complaint registered under Rule Rule No. 13(1)(c) of Ins. Ombudsman Rule 2017

13. Date of hearing/place 20.03.2019 at Bhopal

14. Representation at the hearing

m) For the Complainant Mr. Kishori Sharan Chourasiya

n) For the insurer Mr. Shashank Putambekar, DM

15. Complaint how disposed REcommendation

16. Date of Award/Order 20.03.2019

Mr. Kishori Sharan Chourasiya (Complainant) has filed a complaint against Future Generali

India Life Insurance Co.Ltd. (Respondent) alleging Mis-selling.

Page 33 of 412

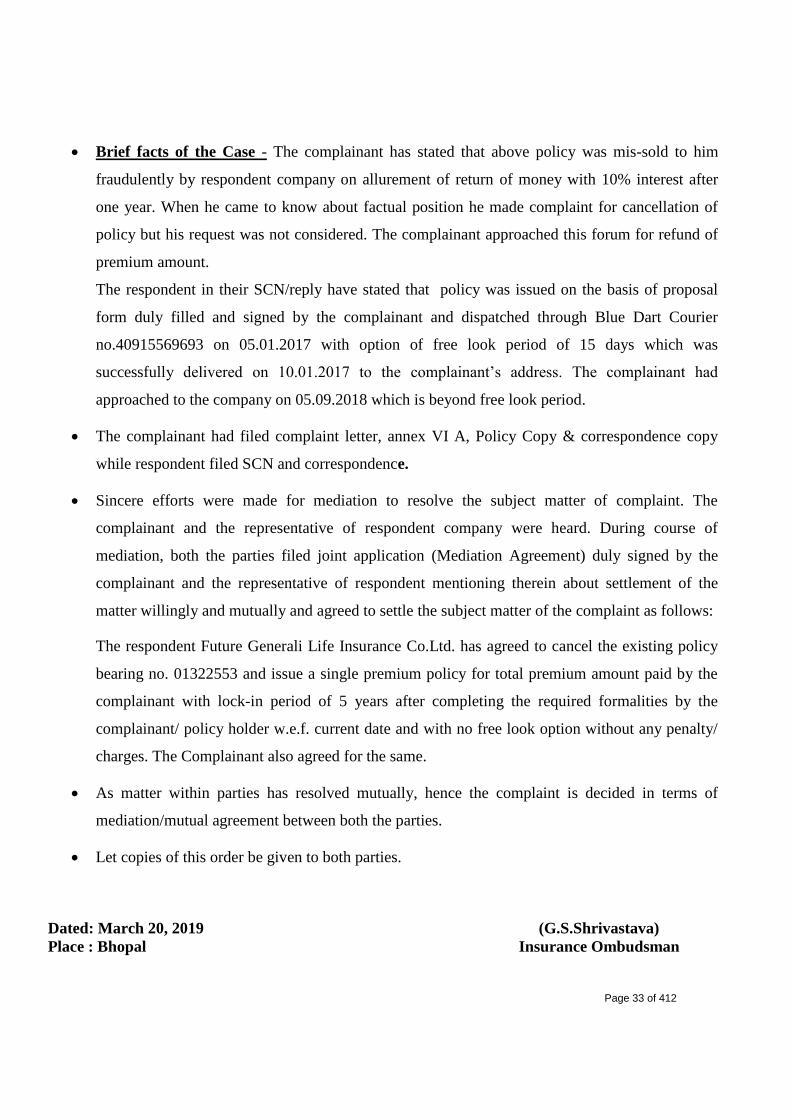

Brief facts of the Case - The complainant has stated that above policy was mis-sold to him

fraudulently by respondent company on allurement of return of money with 10% interest after

one year. When he came to know about factual position he made complaint for cancellation of

policy but his request was not considered. The complainant approached this forum for refund of

premium amount.

The respondent in their SCN/reply have stated that policy was issued on the basis of proposal

form duly filled and signed by the complainant and dispatched through Blue Dart Courier

no.40915569693 on 05.01.2017 with option of free look period of 15 days which was

successfully delivered on 10.01.2017 to the complainant’s address. The complainant had

approached to the company on 05.09.2018 which is beyond free look period.

The complainant had filed complaint letter, annex VI A, Policy Copy & correspondence copy

while respondent filed SCN and correspondence.

Sincere efforts were made for mediation to resolve the subject matter of complaint. The

complainant and the representative of respondent company were heard. During course of

mediation, both the parties filed joint application (Mediation Agreement) duly signed by the

complainant and the representative of respondent mentioning therein about settlement of the

matter willingly and mutually and agreed to settle the subject matter of the complaint as follows:

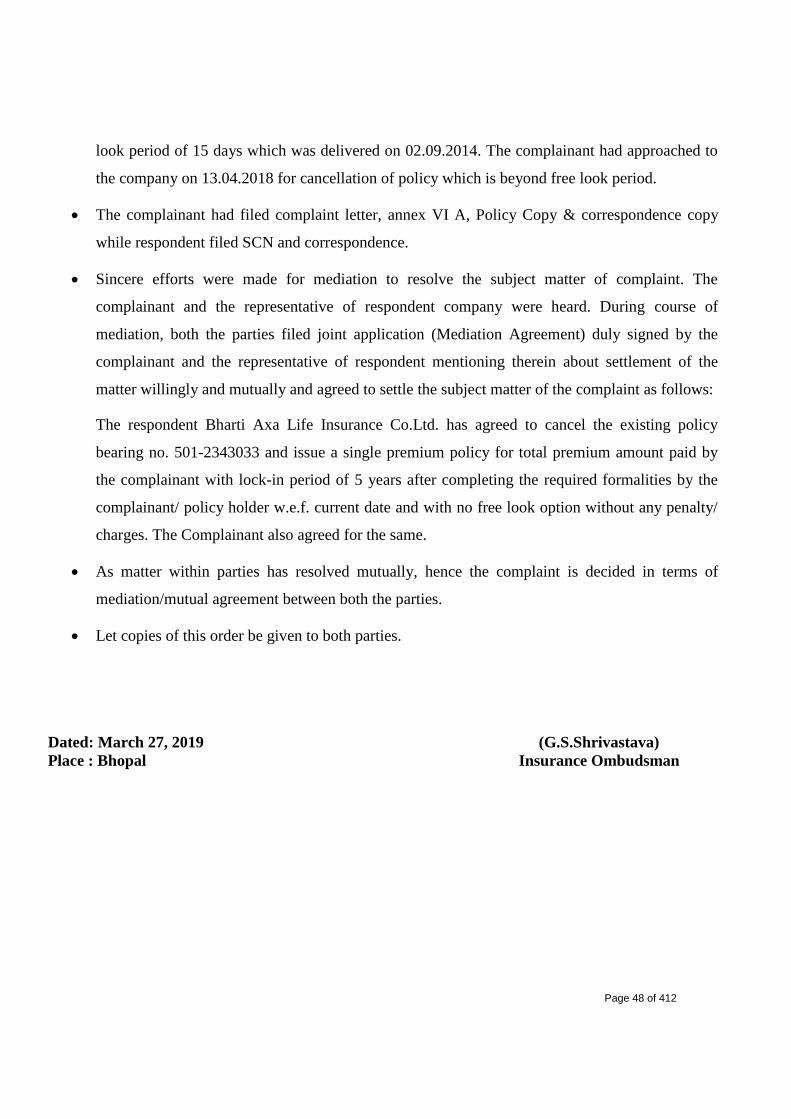

The respondent Future Generali Life Insurance Co.Ltd. has agreed to cancel the existing policy

bearing no. 01322553 and issue a single premium policy for total premium amount paid by the

complainant with lock-in period of 5 years after completing the required formalities by the

complainant/ policy holder w.e.f. current date and with no free look option without any penalty/

charges. The Complainant also agreed for the same.

As matter within parties has resolved mutually, hence the complaint is decided in terms of

mediation/mutual agreement between both the parties.

Let copies of this order be given to both parties.

Dated: March 20, 2019 (G.S.Shrivastava)

Place : Bhopal Insurance Ombudsman

Page 34 of 412

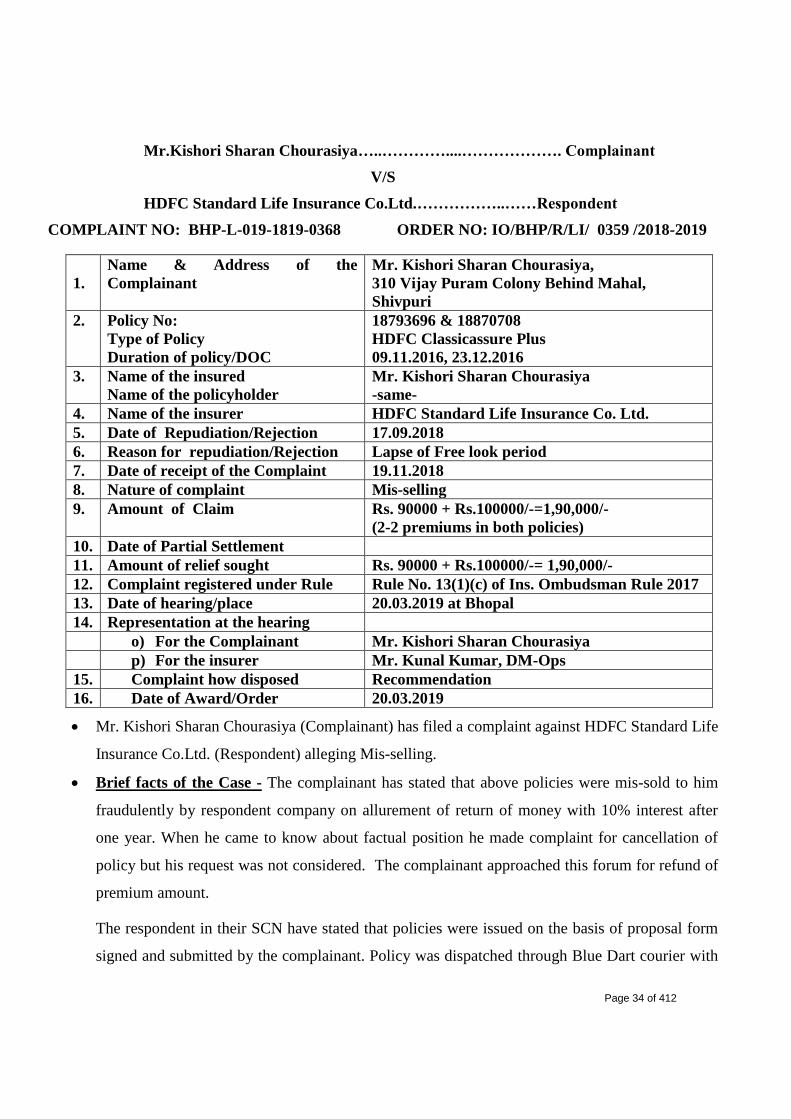

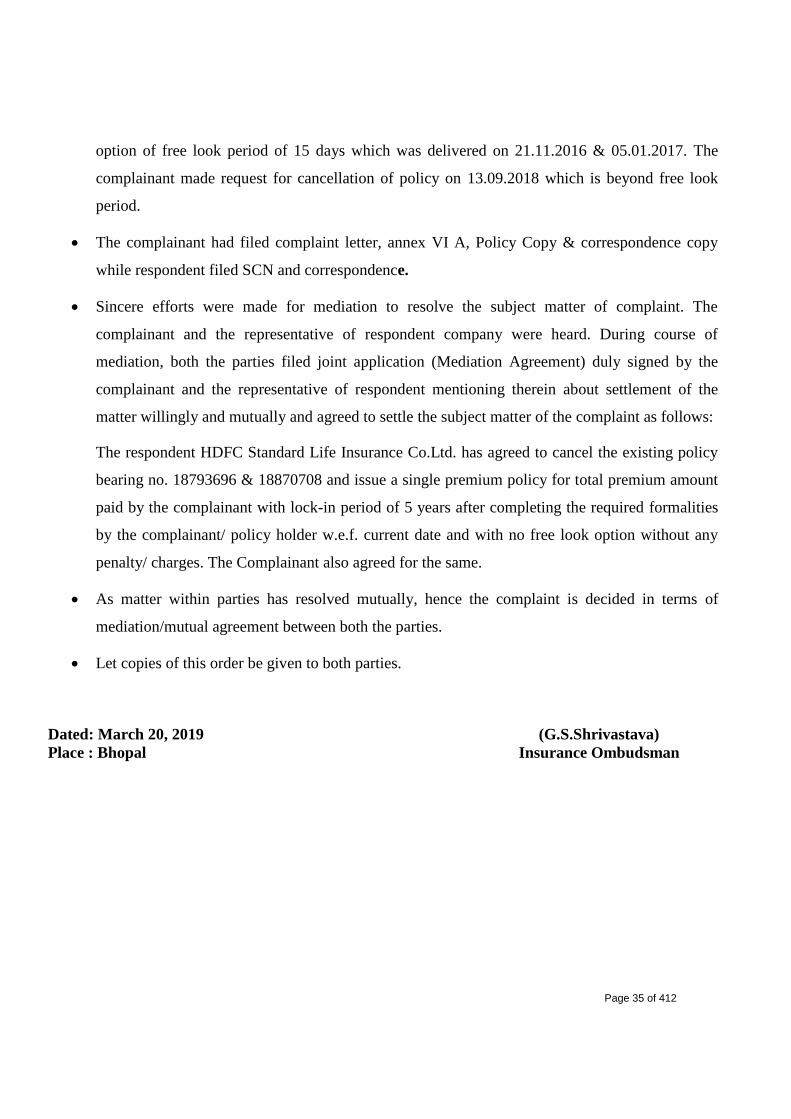

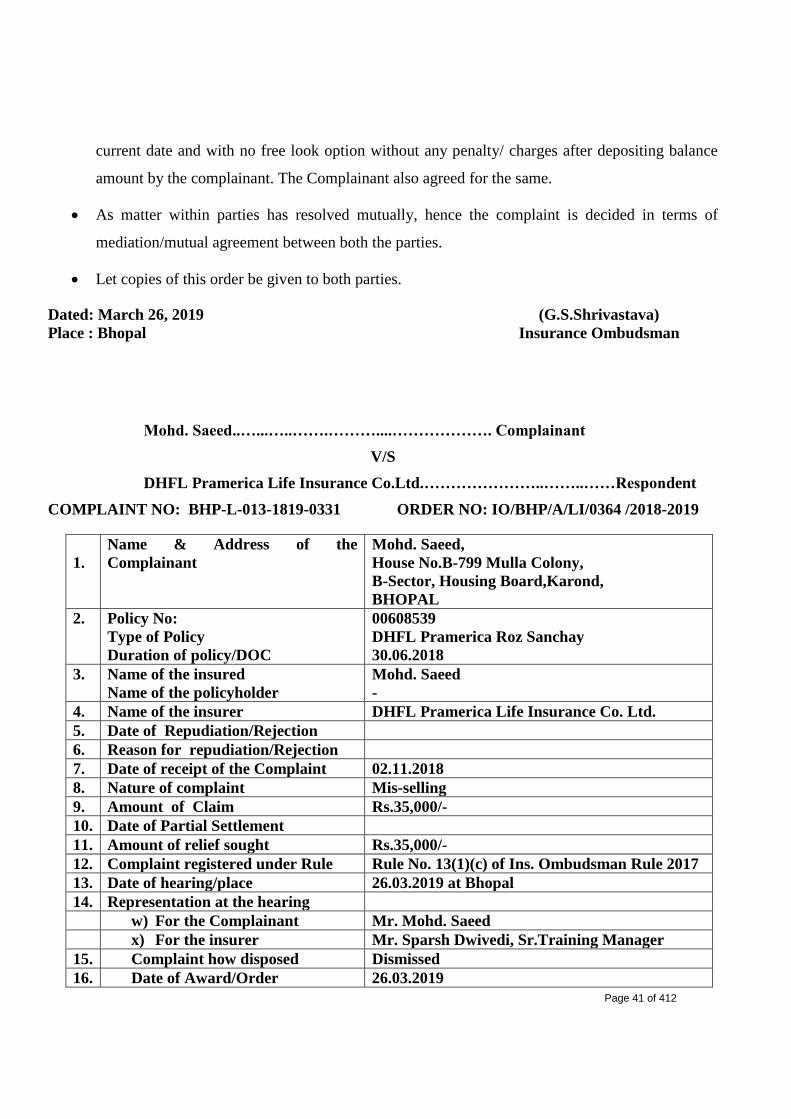

Mr.Kishori Sharan Chourasiya…..…………....………………. Complainant

V/S