technical specification for sub-station automation for sixteen

Upload

khangminh22Category

view

0download

0

Financial Statements of

KJH SWEET SIXTEEN FUND

Year Ended December 31, 2020

KJH SWEET SIXTEEN FUND

Page 1

ANNUAL AUDITED FINANCIAL STATEMENTS

December 31, 2020

MANAGER’S LETTER

The accompanying financial statements have been prepared by K.J. Harrison & Partners Inc., in its capacity as

Manager of the Fund and approved by the Board of Directors of the Manager. The Fund Manager is responsible for

the information and representations contained in these financial statements.

The Manager maintains appropriate processes to ensure that relevant and reliable financial information is produced.

The financial statements have been prepared in accordance with International Financial Reporting Standards and

include certain amounts that are based on estimates and judgments made by the Manager. The significant

accounting policies which the Manager believes are appropriate for the Fund are described in Note 2 to the financial

statements.

Grant Thornton LLP are the external auditors of the Fund, appointed by the Manager. They have audited the financial

statements in accordance with Canadian generally accepted auditing standards to enable them to express to the

unitholders their opinion on the financial statements. Their report is set out below.

“Joel A.B. Clark” “Christine Fulsang”

Joel A.B. Clark Christine Fulsang

Chief Executive Officer Chief Financial Officer

March 31, 2021

KJH SWEET SIXTEEN FUND

Page 2

ANNUAL AUDITED FINANCIAL STATEMENTS

December 31, 2020

INDEPENDENT AUDITOR’S REPORT

To the Unitholders of KJH Sweet Sixteen Fund

Opinion

We have audited the financial statements of the KJH Sweet Sixteen Fund (the “Fund”), which comprise the statement

of financial position as at December 31, 2020, and the statement of comprehensive income, statement of changes

in net assets attributable to unitholders of redeemable units and statement of cash flows for the year then ended,

and notes to the financial statements, including a summary of significant accounting policies and other explanatory

information.

In our opinion, the accompanying financial statements present fairly, in all material respects, the financial position

of the Fund as at December 31, 2020, and its operations and its cash flows for the year then ended in accordance

with International Financial Reporting Standards.

Basis of Opinion

We conducted our audit in accordance with Canadian generally accepted auditing standards. Our responsibilities

under those standards are further described in the Auditor's Responsibilities for the Audit of the Financial

Statements section of our report. We are independent of the Fund in accordance with the ethical requirements that

are relevant to our audit of the financial statements in Canada, and we have fulfilled our other ethical responsibilities

in accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and

appropriate to provide a basis for our opinion.

Responsibilities of Management and Those Charged with Governance for the Financial Statements

Management is responsible for the preparation and fair presentation of the financial statements in accordance with

International Financial Reporting Standards, and for such internal control as management determines is necessary

to enable the preparation of financial statements that are free from material misstatement, whether due to fraud

or error.

In preparing the financial statements, management is responsible for assessing the Fund’s ability to continue as a

going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of

accounting unless management either intends to liquidate the Fund or to cease operations, or has no realistic

alternative but to do so.

Those charged with governance are responsible for overseeing the Fund’s financial reporting process.

KJH SWEET SIXTEEN FUND

Page 3

Auditor’s Responsibilities for the Audit of the Financial Statements

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from

material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion.

Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with

Canadian generally accepted auditing standards will always detect a material misstatement when it exists.

Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they

could reasonably be expected to influence the economic decisions of users taken on the basis of these financial

statements.

As part of an audit in accordance with Canadian generally accepted auditing standards, we exercise professional

judgment and maintain professional skepticism throughout the audit. We also:

• Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error,

design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and

appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from

fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions,

misrepresentations, or the override of internal control.

• Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are

appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the

Fund’s internal control.

• Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and

related disclosures made by management.

• Conclude on the appropriateness of management's use of the going concern basis of accounting and, based on

the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast

significant doubt on the Fund’s ability to continue as a going concern. If we conclude that a material uncertainty

exists, we are required to draw attention in our auditor's report to the related disclosures in the financial

statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit

evidence obtained up to the date of our auditor's report. However, future events or conditions may cause the

Fund to cease to continue as a going concern.

• Evaluate the overall presentation, structure and content of the financial statements, including the disclosures,

and whether the financial statements represent the underlying transactions and events in a manner that

achieves fair presentation.

We communicate with those charged with governance regarding, among other matters, the planned scope and

timing of the audit and significant audit findings, including any significant deficiencies in internal control that we

identify during our audit.

“Grant Thornton LLP”

Markham, Canada Chartered Professional Accountants March 31, 2021 Licensed Public Accountant

KJH SWEET SIXTEEN FUND

The accompanying notes are an integral part of these financial statements. Page 4

STATEMENT OF FINANCIAL POSITION

As at December 31st

(‘000s, except units outstanding and per unit information)

Note 2020 2019

Cash 7 3,711$ 2,399$

Due from broker 78 2,290

Interest for distribution purposes receivable 4 4

Dividends receivable 47 39

Financial assets at fair value through profit or loss 5 45,028 35,526

Total Assets 48,868$ 40,258$

Liabilities

Due to broker 214$ 636$

Accrued liabilities 9.2 151 51

Financial liabilities at fair value through profit or loss 5 - 440

365$ 1,127$

Net Assets Attributable to Holders of Redeemable Units 48,503$ 39,131$

* Financial assets at fair value through profit or loss, at cost 43,276$ 36,203$

Financial liabilities at fair value through profit or loss, at cost - 407

2017-Q1 Series 36,588$ 35,257$

2018-Q1 Series 2,307 2,186

2018-Q2 Series - 8

2018-Q3 Series - 456

2018-Q4 Series - 526

2019-Q1 Series - 104

2019-Q2 Series - 154

2020-Q1 Series 5,453 -

2020-Q2 Series 558 -

2020-Q3 Series 1,971 -

2020-Q4 Series 1,626 -

USD Series - 440

48,503$ 39,131$

Total Liabilities (excluding net assets attributable to holders of

redeemable units)

Net Assets Attributable to Holders of Redeemable Units per Series

KJH SWEET SIXTEEN FUND

The accompanying notes are an integral part of these financial statements. Page 5

STATEMENT OF FINANCIAL POSITION (CONTINUED)

As at December 31st

(‘000s, except units outstanding and per unit information)

Note 2020 2019

8

2017-Q1 Series 274,057 286,194

2018-Q1 Series 21,563 22,068

- 83

2018-Q3 Series - 4,632

- 5,099

- 997

- 1,488

50,916 -

5,000 -

17,798 -

15,745 -

- 3,146

133.51$ 123.19$

2018-Q1 Series 107.01 99.04

- 99.69

2018-Q3 Series - 98.40

- 103.20

- 104.60

- 103.67

107.09 -

111.54 -

110.76 -

103.27 -

- 139.93

2019-Q2 Series

2020-Q4 Series

2020-Q1 Series

2020-Q2 Series

2020-Q1 Series

2020-Q3 Series

2019-Q2 Series

2020-Q3 Series

2020-Q4 Series

2018-Q4 Series

USD Series

2020-Q2 Series

2018-Q4 Series

2018-Q2 Series

2019-Q1 Series

2019-Q1 Series

Redeemable Units Outstanding

Net Assets Attributable to Holders of Redeemable Units per Unit

2017-Q1 Series

USD Series

2018-Q2 Series

Approved on behalf of KJH Sweet Sixteen Fund by K.J. Harrison & Partners Inc., the Manager

“Joel A.B. Clark” “Christine Fulsang”

Joel A.B. Clark Christine Fulsang

Director, President & Chief Executive Officer Director, Chief Financial Officer &

Chief Operating Officer

KJH SWEET SIXTEEN FUND

The accompanying notes are an integral part of these financial statements. Page 6

STATEMENT OF COMPREHENSIVE INCOME

Year Ended December 31st

(‘000s)

Note 2020 2019

Operating Income

Interest for distribution purposes 146$ 444$

Dividends 465 446

1,288 (143)

2,462 3,012

Net foreign currency gains (losses) 149 (90)

Total Income (Loss) 4,510 3,669

Operating Expenses

Management fees 9.2 476 456

Performance fees 9.2 92 -

Transaction costs 9.3 59 28

Operating and unitholder reporting costs 33 28

Custodian fees 32 32

Trustee fees 10 3

Audit fees 9 9

Dividends paid on investments sold short 8 20

Interest - 3

719 579

Profit before Taxes 3,791 3,090

Withholding taxes 33 31

3,758$ 3,059$

Net realized gains (losses) on financial assets and liabilities at fair value

through profit or loss

Net change in unrealized appreciation on financial assets and liabilities at

fair value through profit or loss

Total Operating Expenses

Increase in Net Assets Attributable to Holders of Redeemable Units

KJH SWEET SIXTEEN FUND

The accompanying notes are an integral part of these financial statements. Page 7

STATEMENT OF COMPREHENSIVE INCOME (CONTINUED)

Year Ended December 31st

(‘000s)

Note 2020 2019

2017-Q1 Series 2,834$ 2,767$

2018-Q1 Series 171 166

2018-Q2 Series - 1

2018-Q3 Series - 34

2018-Q4 Series - 50

2019-Q1 Series - 4

2019-Q2 Series - 5

2020-Q1 Series 525 -

2020-Q2 Series 58 -

2020-Q3 Series 148 -

2020-Q4 Series 34 -

USD Series (12) 32

3,758$ 3,059$

8

2017-Q1 Series 10.12$ 9.10$

2018-Q1 Series 7.83 7.34

2018-Q2 Series - 7.29

2018-Q3 Series - 7.22

2018-Q4 Series - 8.47

2019-Q1 Series - 2.99

2019-Q2 Series - 3.47

2020-Q1 Series 11.09 -

2020-Q2 Series 11.54 -

2020-Q3 Series 11.16 -

2020-Q4 Series 2.62 -

(3.73) 4.21

Increase (Decrease) in Net Assets Attributable to Holders of Redeemable

Units per Series

Increase (Decrease) in Net Assets Attributable to Holders of Redeemable

Units per Unit

USD Series

KJH SWEET SIXTEEN FUND

The accompanying notes are an integral part of these financial statements. Page 8

STATEMENT OF CHANGES IN NET ASSETS ATTRIBUTABLE TO HOLDERS OF REDEEMABLE UNITS

Year Ended December 31st

(‘000s)

Increase

Net Assets (Decrease) in Net Assets

Attributable Net Assets Attributable

to Holders of Attributable to Holders of

Redeemable to Holders of Reinvestment Net Redeemable

Units, Beginning Redeemable Series Issue Redemption of Investment Capital Units, End

of Year Units Consolidation of Units of Units Distributions Income Gains of Year

2017-Q1 Series 35,257$ 2,834$ -$ -$ (1,503)$ 92$ -$ (92)$ 36,588$

2018-Q1 Series 2,186 171 - - (50) 5 - (5) 2,307

2018-Q2 Series 8 - - - (8) - - - -

2018-Q3 Series 456 - (456) - - - - - -

2018-Q4 Series 526 - (526) - - - - - -

2019-Q1 Series 104 - (104) - - - - - -

2019-Q2 Series 154 - (154) - - - - - -

2020-Q1 Series - 525 1,240 4,030 (342) 17 - (17) 5,453

2020-Q2 Series - 58 - 500 - 2 - (2) 558

2020-Q3 Series - 148 - 1,823 - 4 - (4) 1,971

2020-Q4 Series - 34 - 1,592 - 1 - (1) 1,626

USD Series 440 (12) - - (428) - - - -

39,131$ 3,758$ -$ 7,945$ (2,331)$ 121$ -$ (121)$ 48,503$

Redeemable Unit Transactions Distributions

2020

KJH SWEET SIXTEEN FUND

The accompanying notes are an integral part of these financial statements. Page 9

STATEMENT OF CHANGES IN NET ASSETS ATTRIBUTABLE TO HOLDERS OF REDEEMABLE UNITS (CONTINUED)

Year Ended December 31st

(‘000s)

Net Assets Increase in Net Assets

Attributable Net Assets Attributable

to Holders of Attributable to Holders of

Redeemable to Holders of Reinvestment Net Redeemable

Units, Beginning Redeemable Series Issue Redemption of Investment Capital Units, End

of Year Units Consolidation of Units of Units Distributions Income Gains of Year

2017-Q1 Series 38,477$ 2,767$ -$ -$ (5,987)$ -$ -$ -$ 35,257$

2018-Q1 Series 2,183 166 - - (163) - - - 2,186

2018-Q2 Series 9 1 - - (2) - - - 8

2018-Q3 Series 424 34 - - (2) - - - 456

2018-Q4 Series 863 50 - - (387) - - - 526

2019-Q1 Series - 4 - 492 (392) - - - 104

2019-Q2 Series - 5 - 161 (12) - - - 154

USD Series 1,232 32 - - (824) - - - 440

43,188$ 3,059$ -$ 653$ (7,769)$ -$ -$ -$ 39,131$

Redeemable Unit Transactions Distributions

2019

KJH SWEET SIXTEEN FUND

The accompanying notes are an integral part of these financial statements. Page 10

STATEMENT OF CASH FLOWS

Year Ended December 31st

(‘000s)

Note 2020 2019

Cash Flows from Operating Activities

3,758$ 3,059$

Adjustments for:

Interest for distribution purposes income (146) (444)

Dividend income (465) (446)

Interest expense - 3

Dividends paid on investements sold short 8 20

Withholding taxes 33 31

Net realized (gains) losses on financial assets and liabilities at fair value

through profit or loss (1,288) 143

Net change in unrealized appreciation on financial assets and liabilities

at fair value through profit or loss (2,462) (3,012)

(562) (646)

Purchase of investments (258,108) (125,562)

Proceeds from the sale of investments 253,067 135,620

Purchase of investments to cover investments sold short (14,337) (6,882)

Proceeds from investments sold short 13,162 6,153

Cash settlement of derivative contracts 24 (31)

Change in non-cash working capital items:

Net decrease (increase) in due from broker 2,212 (2,290)

Net increase (decrease) in due to broker (422) (586)

Net increase (decrease) in accrued liabilities 100 (7)

Net Cash Provided by (Used in) Operations (4,864) 5,769

Interest for distribution purposes received 146 440

Dividends received 457 425

Interest paid - (3)

Dividends paid (8) (22)

Withholding taxes paid (33) (31)

Net Cash Provided by (Used in) Operating Activities (4,302) 6,578

Cash Flows from Financing Activities

Proceeds from issuance of redeemable units 7,945 653

Payment on redemption of redeemable units (2,331) (7,769)

5,614 (7,116)

1,312 (538)

Cash, Beginning of Year 7 2,399 2,937

7 3,711$ 2,399$

Net Cash Provided by (Used in) Financing Activities

Net Increase (Decrease) in Cash

Cash, End of Year

Increase in Net Assets Attributable to Holders of Redeemable Units

KJH SWEET SIXTEEN FUND

Page 11

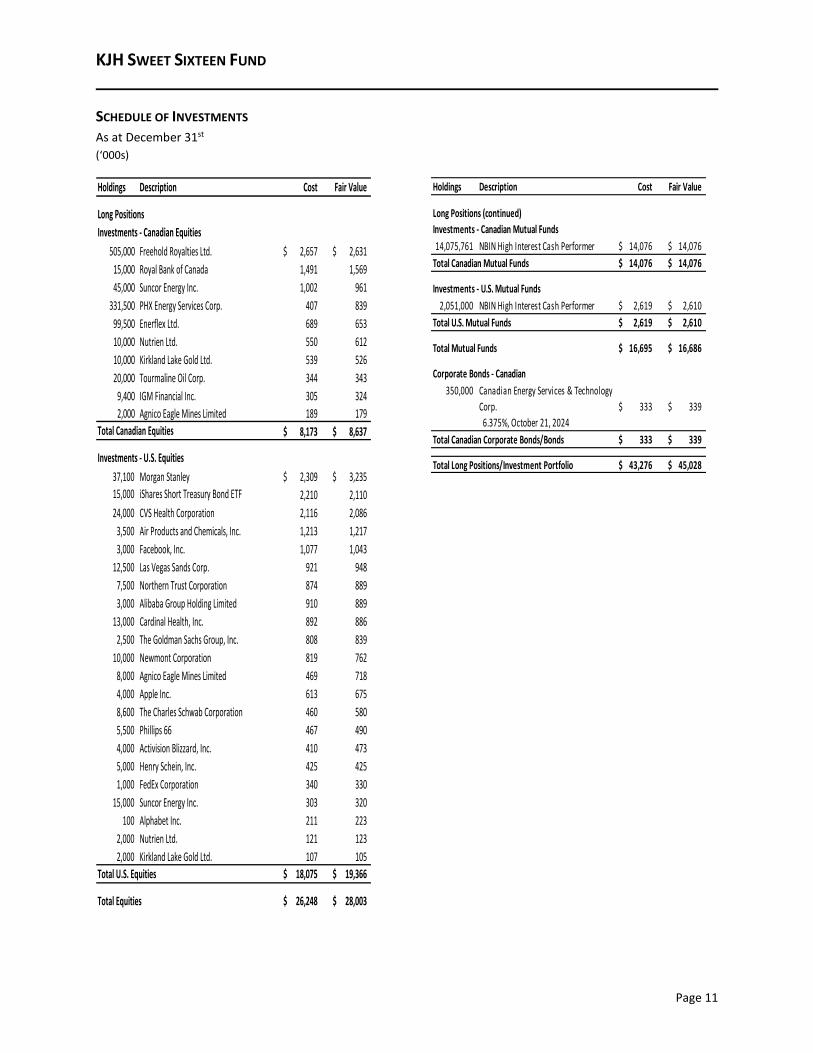

SCHEDULE OF INVESTMENTS

As at December 31st

(‘000s)

Holdings Description Cost Fair Value

Long Positions

Investments - Canadian Equities

505,000 Freehold Royalties Ltd. 2,657$ 2,631$

15,000 Royal Bank of Canada 1,491 1,569

45,000 Suncor Energy Inc. 1,002 961

331,500 PHX Energy Services Corp. 407 839

99,500 Enerflex Ltd. 689 653

10,000 Nutrien Ltd. 550 612

10,000 Kirkland Lake Gold Ltd. 539 526

20,000 Tourmaline Oil Corp. 344 343

9,400 IGM Financial Inc. 305 324

2,000 Agnico Eagle Mines Limited 189 179

Total Canadian Equities 8,173$ 8,637$

Investments - U.S. Equities

37,100 Morgan Stanley 2,309$ 3,235$

15,000 iShares Short Treasury Bond ETF 2,210 2,110

24,000 CVS Health Corporation 2,116 2,086

3,500 Air Products and Chemicals, Inc. 1,213 1,217

3,000 Facebook, Inc. 1,077 1,043

12,500 Las Vegas Sands Corp. 921 948

7,500 Northern Trust Corporation 874 889

3,000 Alibaba Group Holding Limited 910 889

13,000 Cardinal Health, Inc. 892 886

2,500 The Goldman Sachs Group, Inc. 808 839

10,000 Newmont Corporation 819 762

8,000 Agnico Eagle Mines Limited 469 718

4,000 Apple Inc. 613 675

8,600 The Charles Schwab Corporation 460 580

5,500 Phillips 66 467 490

4,000 Activision Blizzard, Inc. 410 473

5,000 Henry Schein, Inc. 425 425

1,000 FedEx Corporation 340 330

15,000 Suncor Energy Inc. 303 320

100 Alphabet Inc. 211 223

2,000 Nutrien Ltd. 121 123

2,000 Kirkland Lake Gold Ltd. 107 105

Total U.S. Equities 18,075$ 19,366$

Total Equities 26,248$ 28,003$

Holdings Description Cost Fair Value

Long Positions (continued)

Investments - Canadian Mutual Funds

14,075,761 NBIN High Interest Cash Performer 14,076$ 14,076$

Total Canadian Mutual Funds 14,076$ 14,076$

Investments - U.S. Mutual Funds

2,051,000 NBIN High Interest Cash Performer 2,619$ 2,610$

Total U.S. Mutual Funds 2,619$ 2,610$

Total Mutual Funds 16,695$ 16,686$

Corporate Bonds - Canadian

350,000 Canadian Energy Services & Technology

Corp. 333$ 339$

6.375%, October 21, 2024

Total Canadian Corporate Bonds/Bonds 333$ 339$

Total Long Positions/Investment Portfolio 43,276$ 45,028$

KJH SWEET SIXTEEN FUND

NOTES TO THE FINANCIAL STATEMENTS Year Ended December 31, 2020

Page 12

1. THE FUND

The KJH Sweet Sixteen Fund (the “Fund”) is an open-ended pooled fund trust established under the laws of

the province of Ontario and governed by a Third Amended and Restated Trust Indenture dated January 1,

2019.

K.J. Harrison & Partners Inc. (the “Manager”), with its registered office at 60 Bedford Road, Toronto, Ontario,

is the principal distributor and manager of the Fund. The Fund pays fees in accordance with the fee schedule

contained in the Manager’s Relationship Disclosure and Supplementary Information document. NBIN Inc. is

the custodian, SS&C Fund Administration Company provides fund accounting and unitholder recordkeeping

services, and Computershare Trust Company of Canada provides trustee services.

The investment objective of the Fund is to generate long-term capital growth, predominantly through the

ownership of a concentrated portfolio of North American equity securities. The goal of the Fund is to

outperform the equity benchmark over a full market cycle. The Fund is highly concentrated and will typically

hold no more than 16 positions. Volatility is expected to be commensurate with an undiversified equity

portfolio.

The Fund is responsible for the expenses relating to its operations, including, but not limited to, trustee and

registration fees, custodian fees and other services to unitholders, legal and audit fees, costs related to the

preparation of financial statements and other reports, taxes, brokerage fees and interest.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The principal accounting policies applied in the preparation of these financial statements are set out below.

2.1 Statement of Compliance

These financial statements have been prepared in accordance with International Financial Reporting

Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”).

The financial statements were approved by the Manager and authorized for issue on March 31, 2021.

2.2 Basis of Preparation

These financial statements have been prepared on the historical cost basis, except for the revaluation

of certain financial instruments. Historical cost is generally based on the fair value of the consideration

given in exchange for assets.

Judgments made by the Manager in the application of IFRS that have significant effects on the financial

statements are disclosed, where applicable, in the relevant notes to the financial statements.

KJH SWEET SIXTEEN FUND

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED) Year Ended December 31, 2020

Page 13

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

2.3 Foreign Currency

(a) Functional and Presentation Currency

The functional and measurement currency of the Fund is the Canadian dollar (“CAD”). The

financial statements are presented in CAD.

(b) Foreign Currency Translation

Monetary financial assets and financial liabilities denominated in a foreign currency are

translated into CAD at the rates of exchange in effect at the period end date.

Transactions denominated in a foreign currency are translated into CAD at the rates of exchange

prevailing at the dates of the transactions. Foreign exchange gains and losses resulting from the

settlement of such transactions and from the remeasurement of monetary items at period end

exchange rates are recognized in profit or loss.

2.4 Revenue Recognition

Dividend income is recognized when the Fund’s right to receive the payment has been established,

normally being the ex-dividend date. Dividend income is recognized gross of withholding tax, if any.

Interest income for distribution purposes (interest expense for investments sold short) is recorded on

the accrual basis.

2.5 Financial Assets and Financial Liabilities at Fair Value Through Profit or Loss

Financial instruments include financial assets and liabilities such as debt and equity securities, open-

ended investment funds and derivatives. The Fund classifies and measures financial instruments in

accordance with IFRS 9.

(a) Classification

Assets

The Fund classifies investments based on both the Fund’s business model for managing those

financial assets and the contractual cash flow characteristics of the financial assets. The portfolio

of financial assets is managed and performance is evaluated on a fair value basis. The Fund is

primarily focused on fair value information and uses that information to assess the assets’

performance and to make decisions. The Fund has not taken the option to irrevocably designate

any equity securities as fair value through other comprehensive income (“FVOCI”). The

contractual cash flows of the Fund’s debt securities are solely principal and interest; however,

these securities are neither held for the purposes of collecting contractual cash flows nor held

both for collecting contractual cash flows and sale. The collection of contractual cash flows is

only incidental to achieving the Fund’s business models.

KJH SWEET SIXTEEN FUND

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED) Year Ended December 31, 2020

Page 14

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

Liabilities

The Fund may make short sales in which a borrowed security is sold in anticipation of a decline

in the market value of that security or it may use short sales for various arbitrage transactions.

Short sales are classified as financial liabilities at fair value through profit or loss (“FVTPL”).

Derivative contracts that have a negative fair value are presented as liabilities at FVTPL.

As such, the Fund classifies all of its investment portfolio as financial assets or liabilities at FVTPL.

Financial assets or financial liabilities designated at fair value through profit or loss at inception

are those that are managed and their performance evaluated on a fair value basis in accordance

with the Fund’s investment strategy and information about these financial assets and financial

liabilities are evaluated by the Manager on a fair value basis together with other relevant

financial information. The Fund classifies its investments in equity and debt securities as

designated at fair value through profit or loss.

(b) Recognition

Financial assets and financial liabilities at fair value through profit or loss are recognized when

the Fund becomes party to the contractual provisions of the instrument. Recognition takes place

on the trade date where the purchase or sale of an investment is under a contract whose terms

require delivery of the investment within the timeframe established by the market concerned.

Dividend and interest for distribution purposes revenue relating to the Fund’s investments in

debt and equity securities is recognized according to Note 2.4 – Revenue Recognition. Dividend

expense relating to equity securities sold short is recognized when the shareholders’ right to

receive the payment has been established.

(c) Measurement

Financial assets and financial liabilities at fair value through profit or loss are recognized and

subsequently measured at fair value. Transaction costs are expensed as incurred in the

statement of comprehensive income.

Gains and losses arising from changes in their fair value are included in the statement of

comprehensive income for the period in which they arise. Dividends earned on financial assets

at fair value through profit or loss and dividends expense on financial liabilities at fair value

through profit or loss are disclosed in a separate line item in the statement of comprehensive

income. Fair value is determined in the manner described in Note 5.

KJH SWEET SIXTEEN FUND

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED) Year Ended December 31, 2020

Page 15

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

The fair value of financial assets and financial liabilities traded in active markets (such as publicly

traded derivatives and securities) are based on the last traded market price where the last

traded price falls within that day’s bid-ask spread. In circumstances where the last traded price

is not within the bid-ask spread, the Manager determines the point within the bid-ask spread

that is most representative of fair value based on the specific facts and circumstances.

The financial instrument is regarded as quoted in an active market if quoted market prices are

readily and regularly available from an exchange, dealer, broker, industry group, pricing service

or regulatory agency, and those prices represent actual and regularly occurring market

transactions on an arm’s length basis.

The fair value of financial assets and financial liabilities that are not traded in an active market

is determined using valuation techniques. The Fund uses a variety of methods and makes

assumptions that are based on market conditions existing at each period end date. Valuation

techniques used for non-standardized financial instruments such as options and warrants,

include the use of comparable recent arm’s length transactions, option pricing models and other

valuation techniques commonly used by market participants making the maximum use of

market inputs and relying as little as possible on entity-specific inputs.

The following table provides an analysis of financial instruments that are measured subsequent

to initial recognition at fair value, grouped into Levels 1 to 3 based on the degree to which the

inputs to estimate the fair value are observable.

• Level 1: Quoted prices (unadjusted) in active markets for identical assets or liabilities;

• Level 2: Inputs other than quoted prices included in Level 1 that are observable for the asset

or liability, either directly (i.e. as prices) or indirectly (i.e. derived from prices); and

• Level 3: Valuation techniques that include inputs for the asset or liability that are not based

on observable market data (unobservable inputs).

The inputs are considered observable if they are developed using market data, such as publicly

available information about actual events or transactions, and that reflect the assumption that

market participants would use when pricing the assets or liability.

If an asset or liability classified as Level 1 subsequently ceases to be actively traded, it is

transferred into Level 2, unless the measurement of its fair value requires the use of significant

unobservable inputs, in which case it is reclassified to Level 3. All transfers are recorded at fair

value at the beginning of the period of the transfer.

KJH SWEET SIXTEEN FUND

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED) Year Ended December 31, 2020

Page 16

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

(d) Derecognition

Financial assets at fair value through profit or loss are derecognized when the contractual rights

to the cash flows from the investments have expired or the Fund has transferred substantially

all risks and rewards of ownership.

Financial liabilities at fair value through profit or loss are derecognized when the obligation

specified in the contract is discharged, cancelled or expired.

Realized gains and losses on derecognition are determined using the average cost method and

are included in profit or loss for the period in which they arise.

(e) Offsetting

The Fund only offsets financial assets and financial liabilities at fair value through profit or loss if

the Fund has a legally enforceable right to offset recognized amounts and either intends to settle

on a net basis or to realize the asset and settle the liability simultaneously.

2.6 Due From and Due To Broker

Amounts due from brokers are receivables for securities sold (in a regular way transaction) that have

been contracted for but not yet delivered on the reporting date.

Amounts due to brokers are payables for securities purchased (in a regular way transaction) that have

been contracted for but not yet delivered on the reporting date.

2.7 Cash

Cash is comprised of deposits with financial institutions.

2.8 Other Financial Assets and Financial Liabilities

In accordance with IFRS 9 Financial Instruments all other financial assets are classified and measured

at amortized cost. Other financial liabilities are measured at amortized cost.

The carrying value of current assets and liabilities approximates fair value due to their short-term

nature.

2.9 Expenses

All expenses are recognized in the statement of comprehensive income on an accrual basis.

KJH SWEET SIXTEEN FUND

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED) Year Ended December 31, 2020

Page 17

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

2.10 Redeemable Units and Net Assets Attributable to Holders of Redeemable Units

Redeemable units are classified as financial liabilities and are measured at the redemption amounts.

Redeemable units can be put back to the Fund at any time for cash equal to a proportionate share of

the Fund’s net asset value (“NAV”) attributable to the unit class.

Redeemable units are issued and redeemed based on the Fund’s NAV per unit, calculated by dividing

the net assets of the Fund, calculated in accordance with the Fund’s Trust Indenture and Fund

Regulation, by the number of redeemable units in issue. The Fund’s Trust Indenture and Fund

Regulation require that investment positions are valued on the basis of the last traded market price for

the purpose of determining the trading net asset value per unit for subscriptions and redemptions.

The increase (decrease) in net assets attributable to holders of redeemable units per unit is calculated

by dividing the increase (decrease) in net assets attributable to holders of redeemable units by the

weighted average number of units outstanding during the period.

3. FUTURE ACCOUNTING STANDARDS

The International Accounting Standards Board (“IASB”) has issued or revised a number of standards as of

December 31, 2020 that are not yet effective and have not been early-adopted in preparing the Fund Financial

Statements. The Manager is in the process of assessing the impact of these standards on financial reporting

and disclosure.

4. CRITICAL ACCOUNTING JUDGMENTS AND KEY SOURCES OF ESTIMATION UNCERTAINTY

In the application of the Fund’s accounting policies, which are described in Note 2, the Manager is required

to make judgments, estimates and assumptions about the carrying amounts of assets and liabilities that are

not readily available from other sources. The estimates and associated assumptions are based on historical

experience and other factors that are considered to be relevant. Actual results may differ from these

estimates.

The estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting

estimates are recognized in the period in which the estimate is revised, if the revision affects only that period,

or in the period of the revision and future periods, if the revision affects both current and future periods.

KJH SWEET SIXTEEN FUND

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED) Year Ended December 31, 2020

Page 18

4. CRITICAL ACCOUNTING JUDGMENTS AND KEY SOURCES OF ESTIMATION UNCERTAINTY (CONTINUED)

4.1 Critical Judgments in Applying Accounting Policies

The following are the critical judgments, apart from those involving estimates (see below), that the

Manager has made in the process of applying the Fund’s accounting policies.

Functional Currency

The Manager considers the currency of the primary economic environment in which the Fund operates

to be the CAD as this is the currency which, in its opinion, most faithfully represents the economic

effects of underlying transactions, events and conditions. Furthermore, the CAD is the currency in

which the Fund measures its performance and also issues and redeems its redeemable units.

4.2 Key Sources of Estimation Uncertainty

The following are the key assumptions concerning the future and other key sources of estimation

uncertainty at the statement of financial position date that have a significant risk of causing a material

adjustment to the carrying amounts of assets and liabilities within the next financial year.

Fair Value of Securities Not Quoted in an Active Market and Over-the-Counter Derivative Instruments

As described in Note 5.3, the Manager uses its judgment in selecting an appropriate valuation

technique for financial instruments that are not quoted in an active market. Valuation techniques

commonly used by market practitioners are applied. For derivative financial instruments, assumptions

are made based on quoted market rates adjusted for specific features of the instrument. Other

financial instruments using a discounted cash flow analysis based on assumptions supported, where

possible, by observable market prices or rates. The estimation of fair value of unlisted shares includes

some assumptions not supported by observable market prices or rates.

The carrying amount of these instruments at December 31, 2020 is Nil (2019 – Nil).

5. FINANCIAL ASSETS AND FINANCIAL LIABILITIES AT FAIR VALUE THROUGH PROFIT OR LOSS

5.1 Significant Accounting Policies

Details of the significant accounting policies and methods adopted, including the criteria for

recognition, the basis of measurement and the basis on which income and expenses are recognized, in

respect of its financial assets and financial liabilities are disclosed in Note 2.5.

5.2 Derivative Financial Instruments

The Fund holds forward foreign exchange contracts. In accordance with the Fund’s investment

objectives and policies, the Fund may enter into forward foreign exchange contracts traded over-the-

counter to hedge specific foreign currency payments.

KJH SWEET SIXTEEN FUND

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED) Year Ended December 31, 2020

Page 19

5. FINANCIAL ASSETS AND FINANCIAL LIABILITIES AT FAIR VALUE THROUGH PROFIT OR LOSS (CONTINUED)

The Fund holds investments denominated in the currency of the United States (USD) at the reporting

date and has entered into forward foreign exchange contracts for terms not exceeding three months

to hedge the exchange rate risk arising from future cash flows on these investments. The fair value of

the forward foreign exchange contracts are included in derivatives held for trading classified as financial

assets or financial liabilities at fair value through profit or loss.

The following table summarizes the Fund’s holdings in outstanding forward foreign exchange contracts

as at December 31, 2019.

Fair Value

Contract Contract in CAD

Value Value Financial Assets

Year End Settlement in CAD in USD (Liabilities)

Counterparty / Rating Date ('000s) ('000s) ('000s)

National Bank / A1 January 31, 2020 307$ 237$ 1$

Notes:

Forward Rate = 1.2960 Current Rate = 1.2988

December 31, 2019

5.3 Fair Value of Financial Instruments

The following tables summarize the fair value hierarchy of the Fund’s assets and liabilities measured at

fair value as at December 31, 2020 and 2019.

Level 1 Level 2 Level 3 Total

('000s) ('000s) ('000s) ('000s)

Equity securities 28,003$ -$ -$ 28,003$

Open-ended investment funds - 16,686 - 16,686

Debt securities - 339 - 339

28,003$ 17,025$ -$ 45,028$

Financial Assets

Total

December 31, 2020

KJH SWEET SIXTEEN FUND

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED) Year Ended December 31, 2020

Page 20

5. FINANCIAL ASSETS AND FINANCIAL LIABILITIES AT FAIR VALUE THROUGH PROFIT OR LOSS (CONTINUED)

Level 1 Level 2 Level 3 Total

('000s) ('000s) ('000s) ('000s)

Equity securities 19,314$ -$ -$ 19,314$

Open-ended investment funds - 15,762 - 15,762

Debt securities - 333 - 333

Options & warrants - 116 - 116

Derivatives - 1 - 1

19,314$ 16,212$ -$ 35,526$

Equity securities sold short 440$ -$ -$ 440$

440$ -$ -$ 440$ Total

Financial Assets

Total

Financial Liabilities

December 31, 2019

All fair value measurements above are recurring. The carrying value of cash, other receivables, other

payables and the Fund’s obligation for net assets attributable to holders of redeemable units are

assumed to approximate their fair values due to their short-term nature.

During the years ended December 31, 2020 and 2019, there were no transfers between Level 1 and

Level 2. In addition, there were no transfers into and/or out of Level 3 during these periods.

6. FINANCIAL RISK MANAGEMENT

The Fund is exposed to a number of risks due to the nature of its activities. These risks include market risk

(including currency risk, interest rate risk and price risk), credit risk and liquidity risk. The value of investments

within the Fund’s portfolio can fluctuate on a daily basis as a result of changes in interest rates, economic

conditions, the market and company news related to specific securities within the Fund. The level of risk

depends on the Fund’s investment objectives and the type of securities it invests in.

The Fund is also exposed to operational risks such as custody risk. Custody risk is the risk of a loss being

incurred on securities in custody as a result of a custodian’s insolvency, negligence, misuse of assets, fraud,

poor administration or inadequate recordkeeping. Although an appropriate legal framework is in place that

reduces the risk of loss of value of the securities held by the custodian, in the event of its failure, the ability

of the Fund to transfer the securities might be temporarily impaired.

The Fund’s objective in managing these risks is the protection and enhancement of unitholder value. The

Fund’s overall risk management approach seeks to maximize the returns derived for the level of risk to which

the Fund is exposed and seeks to minimize potential adverse effects on the Fund’s financial performance. The

risk management system is an ongoing process of identification, measurement, monitoring and controlling

risk.

KJH SWEET SIXTEEN FUND

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED) Year Ended December 31, 2020

Page 21

6. FINANCIAL RISK MANAGEMENT (CONTINUED)

The Manager uses a focused and disciplined approach in its investment selection and oversight

responsibilities. The Manager determines the timing of buying or selling security holdings to enhance the

Fund’s portfolio performance and/or limit risk. Investments of the Fund are managed in accordance with the

investment objectives and strategies of the Fund. The Manager has developed policies and procedures to

manage the Fund’s specific risks.

On March 11, 2020, the World Health Organization declared the global outbreak of COVID-19 a pandemic.

Market disruptions associated with the COVID-19 pandemic have had a global impact and uncertainty exists

as to the long-term implications. Such disruptions can adversely impact the financial instrument risks and the

fair values of each of the Funds’ portfolios.

Risk Management Structure

The Manager is ultimately responsible for the overall risk management within the Fund, including identifying

and controlling risk.

Risk Measurement and Reporting System

The Fund uses different methods to measure and manage the various types of risk to which it is exposed;

these methods are explained below.

Risk Mitigation

The Fund’s Trust Indenture and Fund Regulation detail its investment policy and guidelines that encompass

its overall investment strategy, its tolerance for risk and its general risk management philosophy.

The Fund uses derivatives and other instruments for trading purposes and for risk management.

Excessive Risk Concentration

A concentration of risk exists where: (i) positions in financial instruments are affected by changes in the same

risk factor or group of correlated factors; and (ii) the exposure could, in the event of large but plausible

adverse developments, result in significant losses.

Concentrations of liquidity risk may arise from the repayment terms of financial liabilities, sources of

borrowing facilities or reliance on a particular market in which to realize liquid assets. Concentrations of

foreign exchange risk may arise if the Fund has a significant net open position in a single foreign currency or

aggregate net open positions in several currencies that tend to move together. Concentrations of

counterparty risk may arise when a number of financial instruments or contracts are contracted with the same

counterparty, or where a number of counterparties are engaged in similar business activities or activities in

the same geographic region or have similar economic features that would cause their ability to meet

contractual obligations to be similarly affected by changes in economic, political or other conditions.

KJH SWEET SIXTEEN FUND

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED) Year Ended December 31, 2020

Page 22

6. FINANCIAL RISK MANAGEMENT (CONTINUED)

6.1 Credit Risk

Credit risk is the risk that a counterparty to a financial instrument will default on its contractual

obligations resulting in a financial loss to the Fund.

At the reporting date, financial assets exposed to credit risk include debt instruments and derivatives

disclosed in Note 5.2. It is the opinion of the Manager that the carrying amounts of these financial

assets represent the maximum credit risk exposure at the reporting date.

The following table summarizes the quality of the Fund’s investments in debt securities as at December

31, 2020 and 2019.

Credit Rating * 2020 2019

100.0% 100.0%

100.0% 100.0%

Percent of Total Debt Securities

B

Total

* Credit ratings are obtained from Standards & Poor’s and/or Dominion Bond Rating Services. Where one or

more rating is obtained for a security, the lowest rating has been used.

All transactions executed by the Fund in listed securities are settled/paid for upon delivery using

approved brokers. The risk of default is considered minimal as delivery of securities sold is only made

once the broker has received payment. Payment is made on a purchase once the securities have been

received by the custodian. The trade will fail if either party fails to meet its obligation.

The credit risk on cash transactions and transactions involving derivative financial instruments is

mitigated by transacting with counterparties that are regulated entities subject to prudential

supervision, or with high credit-ratings assigned by international credit-rating agencies. The Fund

reduces the settlement risk on gross settled foreign exchange derivatives by using a foreign exchange

clearing house which allows transactions to be settled on a delivery versus payment basis.

The Fund is exposed to credit risk with the custodian. Should the custodian become insolvent, it could

cause a delay for the Fund in obtaining access to its assets.

At December 31, 2020 and 2019, none of these financial assets were either impaired or past due but

not impaired. The Fund does not hold any collateral as security.

KJH SWEET SIXTEEN FUND

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED) Year Ended December 31, 2020

Page 23

6. FINANCIAL RISK MANAGEMENT (CONTINUED)

6.2 Liquidity Risk

Liquidity risk is the risk that the Fund may not be able to generate sufficient cash resources to settle its

obligations in full as they come due or can only do so on terms that are materially disadvantageous.

As described in Note 2.10, the Fund’s redeemable units are redeemable at the unitholders’ option at

any time for cash equal to a proportionate share of the Fund’s net asset value. The Fund is therefore

potentially exposed to weekly redemptions by its unitholders.

The Fund invests primarily in marketable securities and other financial instruments which, under

normal market conditions, are readily convertible to cash.

The Fund’s financial assets may however include investments listed below which may limit the ability

of the Fund to liquidate some of its investments at an amount close to its fair value to meet its liquidity

requirements:

• Investments in open-ended investment funds which may not be readily realizable due to lock-up

periods; extended withdrawal, notice or settlement periods; or in extraordinary cases periods in

which redemptions are suspended due to adverse market conditions.

• Investments in debt securities that are traded over-the-counter and unlisted equities that are not

traded in an active market.

• Investments in derivative contracts traded over-the-counter, which are not quoted in an active

market and which generally may be illiquid.

At December 31, 2020 and 2019, the Fund’s remaining contractual maturity for its non-derivative

financial liabilities with agreed repayment periods is less than one month.

Redeemable units are redeemable on demand at the holder’s option. However, the Manager does not

foresee that the contractual maturity will be representative of the actual cash outflows, as holders of

these instruments typically retain them for the medium to long-term.

6.3 Market Risk

Market risk is the risk that the fair value of future cash flows of financial instruments will fluctuate due

to changes in market variables such as interest rates, foreign exchange rates and market prices. The

maximum risk resulting from financial instruments, except for written options and securities sold short,

equals their fair value.

KJH SWEET SIXTEEN FUND

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED) Year Ended December 31, 2020

Page 24

6. FINANCIAL RISK MANAGEMENT (CONTINUED)

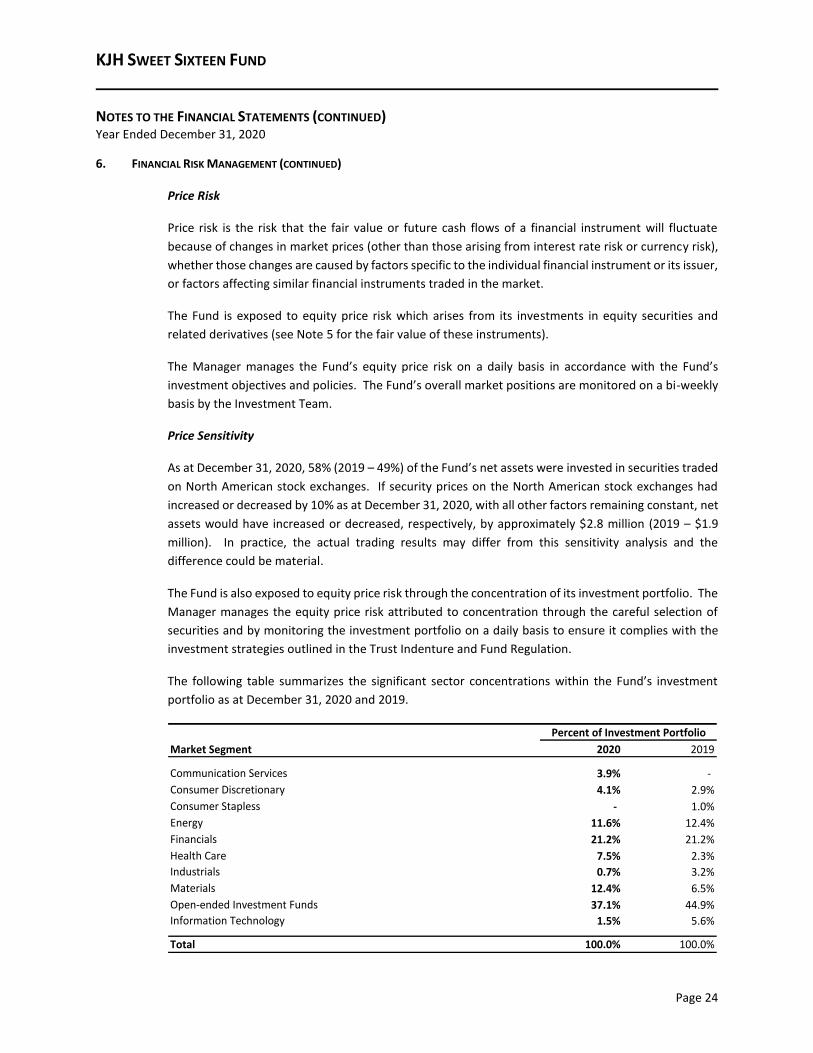

Price Risk

Price risk is the risk that the fair value or future cash flows of a financial instrument will fluctuate

because of changes in market prices (other than those arising from interest rate risk or currency risk),

whether those changes are caused by factors specific to the individual financial instrument or its issuer,

or factors affecting similar financial instruments traded in the market.

The Fund is exposed to equity price risk which arises from its investments in equity securities and

related derivatives (see Note 5 for the fair value of these instruments).

The Manager manages the Fund’s equity price risk on a daily basis in accordance with the Fund’s

investment objectives and policies. The Fund’s overall market positions are monitored on a bi-weekly

basis by the Investment Team.

Price Sensitivity

As at December 31, 2020, 58% (2019 – 49%) of the Fund’s net assets were invested in securities traded

on North American stock exchanges. If security prices on the North American stock exchanges had

increased or decreased by 10% as at December 31, 2020, with all other factors remaining constant, net

assets would have increased or decreased, respectively, by approximately $2.8 million (2019 – $1.9

million). In practice, the actual trading results may differ from this sensitivity analysis and the

difference could be material.

The Fund is also exposed to equity price risk through the concentration of its investment portfolio. The

Manager manages the equity price risk attributed to concentration through the careful selection of

securities and by monitoring the investment portfolio on a daily basis to ensure it complies with the

investment strategies outlined in the Trust Indenture and Fund Regulation.

The following table summarizes the significant sector concentrations within the Fund’s investment

portfolio as at December 31, 2020 and 2019.

Market Segment 2020 2019

3.9% -

4.1% 2.9%

- 1.0%

11.6% 12.4%

21.2% 21.2%

7.5% 2.3%

0.7% 3.2%

12.4% 6.5%

37.1% 44.9%

1.5% 5.6%

100.0% 100.0%Total

Materials

Consumer Discretionary

Consumer Stapless

Open-ended Investment Funds

Percent of Investment Portfolio

Health Care

Information Technology

Energy

Industrials

Financials

Communication Services

KJH SWEET SIXTEEN FUND

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED) Year Ended December 31, 2020

Page 25

6. FINANCIAL RISK MANAGEMENT (CONTINUED)

Interest Rate Risk

Interest rate risk is the risk that the fair value of future cash flows of a financial instrument will fluctuate

because of changes in market interest rates.

The Fund is exposed to interest rate risk as it invests in listed debt securities bearing interest at fixed

interest rates and related derivative instruments. The Fund is also exposed to cash flow interest rate

risk as it holds a limited amount of cash subject to variable interest rates.

The Manager manages the Fund’s exposure to interest rate risk on a daily basis in accordance with the

Fund’s investment objectives and policies. The Fund’s overall exposure to interest rate risk is

monitored on a bi-weekly basis by the Investment Team.

The following table summarizes the Fund’s exposure to interest rate risk as at December 31, 2020 and

2019 by remaining term to maturity.

2020 2019

Assets ('000s) ('000s)

Less 1 year -$ -$

1 to 3 years - -

3 to 5 years 339 333

Beyond 5 years - -

Total 339$ 333$

Interest Rate Sensitivity

As at December 31, 2020, the Fund’s sensitivity to interest rate fluctuations was approximately $12,000

(2019 – $14,000). The analysis is based on the assumption that the prevailing market interest rates

change by 100 basis points, with all other variables held constant, and that there is a parallel shift in

the Fund’s yield curve.

Currency Risk

Currency risk is the risk that the value of a financial instrument will fluctuate due to changes in foreign

exchange rates. The Fund invests in securities and other investments that are denominated in

currencies other than the CAD. As a result, the value of the Fund’s assets may be affected favourably

or unfavourably by fluctuations in currency rates and the Fund will be subject to foreign exchange risks.

The Fund undertakes certain transactions denominated in foreign currencies and hence is exposed to

the effects of exchange rate fluctuations. Exchange rate exposures are managed within approved

policy parameters utilizing forward foreign exchange contracts as detailed in Note 5.2.

KJH SWEET SIXTEEN FUND

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED) Year Ended December 31, 2020

Page 26

6. FINANCIAL RISK MANAGEMENT (CONTINUED)

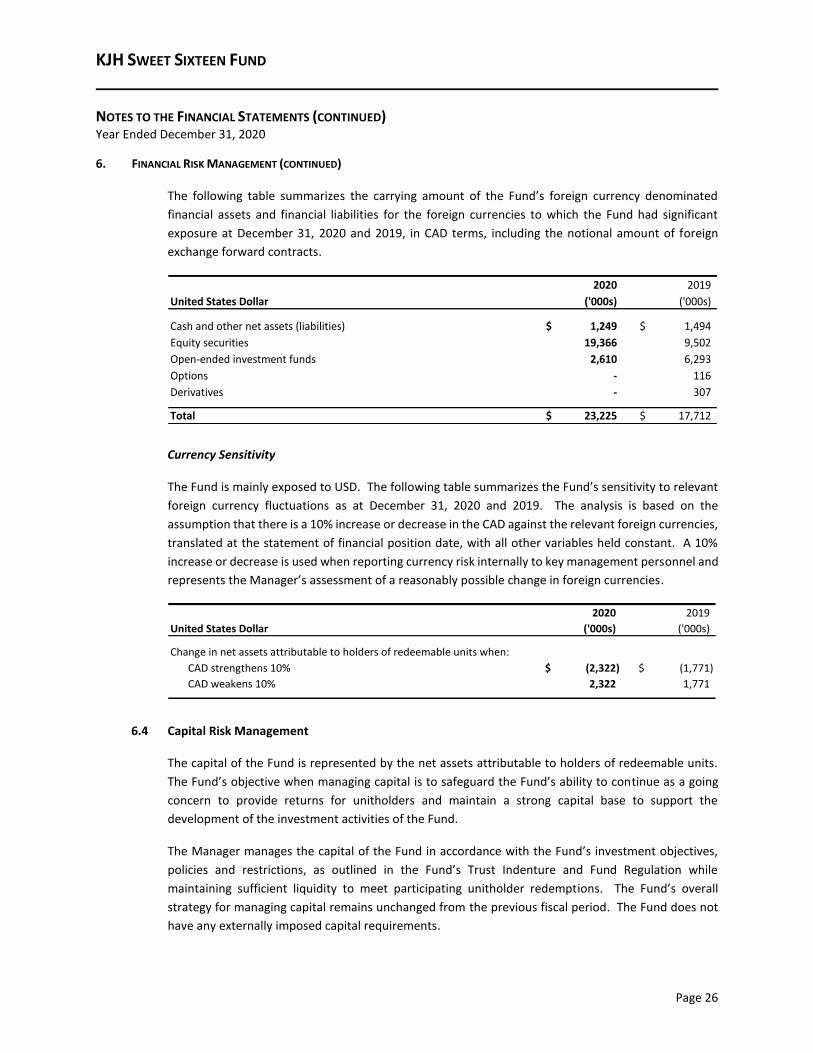

The following table summarizes the carrying amount of the Fund’s foreign currency denominated

financial assets and financial liabilities for the foreign currencies to which the Fund had significant

exposure at December 31, 2020 and 2019, in CAD terms, including the notional amount of foreign

exchange forward contracts.

2020 2019

United States Dollar ('000s) ('000s)

Cash and other net assets (liabilities) 1,249$ 1,494$

Equity securities 19,366 9,502

Open-ended investment funds 2,610 6,293

Options - 116

Derivatives - 307

Total 23,225$ 17,712$

Currency Sensitivity

The Fund is mainly exposed to USD. The following table summarizes the Fund’s sensitivity to relevant

foreign currency fluctuations as at December 31, 2020 and 2019. The analysis is based on the

assumption that there is a 10% increase or decrease in the CAD against the relevant foreign currencies,

translated at the statement of financial position date, with all other variables held constant. A 10%

increase or decrease is used when reporting currency risk internally to key management personnel and

represents the Manager’s assessment of a reasonably possible change in foreign currencies.

2020 2019

United States Dollar ('000s) ('000s)

CAD strengthens 10% (2,322)$ (1,771)$

CAD weakens 10% 2,322 1,771

Change in net assets attributable to holders of redeemable units when:

6.4 Capital Risk Management

The capital of the Fund is represented by the net assets attributable to holders of redeemable units.

The Fund’s objective when managing capital is to safeguard the Fund’s ability to continue as a going

concern to provide returns for unitholders and maintain a strong capital base to support the

development of the investment activities of the Fund.

The Manager manages the capital of the Fund in accordance with the Fund’s investment objectives,

policies and restrictions, as outlined in the Fund’s Trust Indenture and Fund Regulation while

maintaining sufficient liquidity to meet participating unitholder redemptions. The Fund’s overall

strategy for managing capital remains unchanged from the previous fiscal period. The Fund does not

have any externally imposed capital requirements.

KJH SWEET SIXTEEN FUND

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED) Year Ended December 31, 2020

Page 27

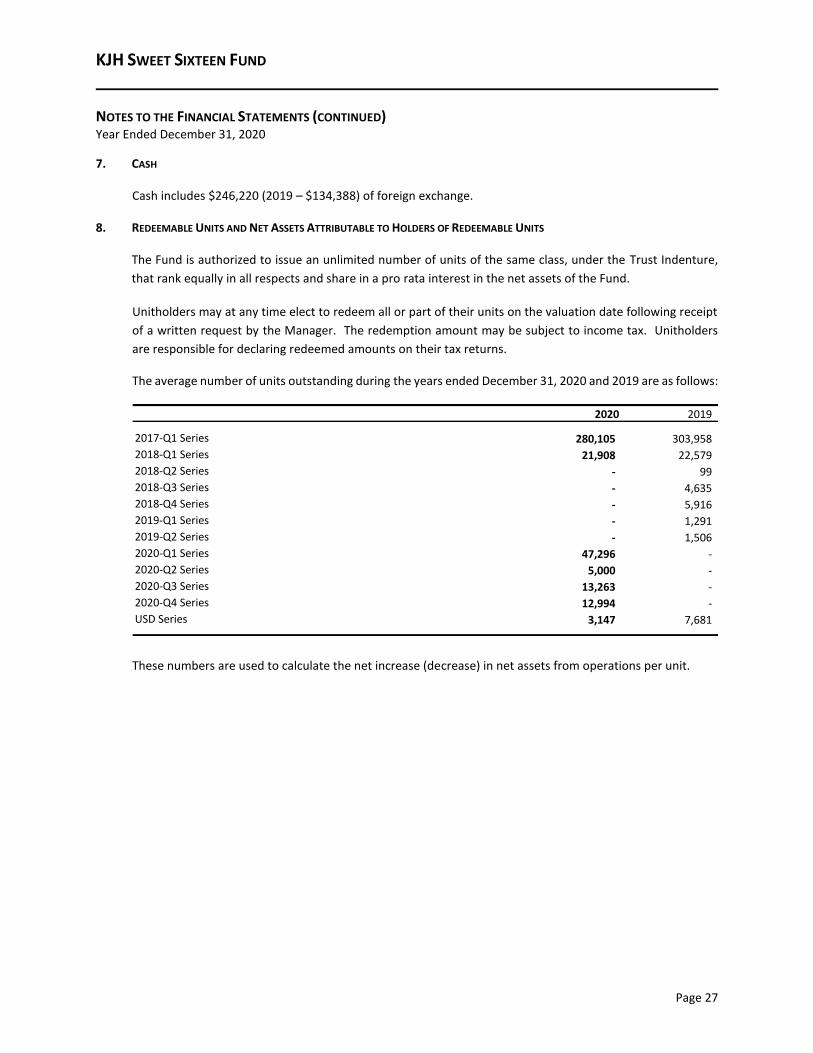

7. CASH

Cash includes $246,220 (2019 – $134,388) of foreign exchange.

8. REDEEMABLE UNITS AND NET ASSETS ATTRIBUTABLE TO HOLDERS OF REDEEMABLE UNITS

The Fund is authorized to issue an unlimited number of units of the same class, under the Trust Indenture,

that rank equally in all respects and share in a pro rata interest in the net assets of the Fund.

Unitholders may at any time elect to redeem all or part of their units on the valuation date following receipt

of a written request by the Manager. The redemption amount may be subject to income tax. Unitholders

are responsible for declaring redeemed amounts on their tax returns.

The average number of units outstanding during the years ended December 31, 2020 and 2019 are as follows:

2020 2019

2017-Q1 Series 280,105 303,958

2018-Q1 Series 21,908 22,579

2018-Q2 Series - 99

2018-Q3 Series - 4,635

2018-Q4 Series - 5,916

2019-Q1 Series - 1,291

2019-Q2 Series - 1,506

2020-Q1 Series 47,296 -

2020-Q2 Series 5,000 -

2020-Q3 Series 13,263 -

2020-Q4 Series 12,994 -

USD Series 3,147 7,681

These numbers are used to calculate the net increase (decrease) in net assets from operations per unit.

KJH SWEET SIXTEEN FUND

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED) Year Ended December 31, 2020

Page 28

8. REDEEMABLE UNITS AND NET ASSETS ATTRIBUTABLE TO HOLDERS OF REDEEMABLE UNITS (CONTINUED)

The following tables summarize the changes in the number of issued redeemable units for the years ended

December 31, 2020 and 2019.

ReinvestedBeginning of Series from Consolidation End of

December 31, 2020 the Year Consolidation Issued Redeemed Distributions of Units the Year

2017-Q1 Series 286,194 - - (12,137) 686 (686) 274,057

2018-Q1 Series 22,068 - - (505) 51 (51) 21,563

2018-Q2 Series 83 - - (83) - - -

2018-Q3 Series 4,632 (4,632) - - - - -

2018-Q4 Series 5,099 (5,099) - - - - -

2019-Q1 Series 997 (997) - - - - -

2019-Q2 Series 1,488 (1,488) - - - - -

2020-Q1 Series - 12,403 41,995 (3,482) 157 (157) 50,916

2020-Q2 Series - - 5,000 - 17 (17) 5,000

2020-Q3 Series - - 17,798 - - - 17,798

2020-Q4 Series - - 15,745 - - - 15,745

USD Series 3,146 - - (3,146) - - -

Redeemable Units

ReinvestedBeginning of Series from Consolidation End of

December 31, 2019 the Year Consolidation Issued Redeemed Distributions of Units the Year

2017-Q1 Series 337,047 - - (50,853) - - 286,194

2018-Q1 Series 23,789 - - (1,721) - - 22,068

2018-Q2 Series 100 - - (17) - - 83

2018-Q3 Series 4,650 - - (18) - - 4,632

2018-Q4 Series 9,026 - - (3,927) - - 5,099

2019-Q1 Series - - 4,921 (3,924) - - 997

2019-Q2 Series - - 1,608 (120) - - 1,488

USD Series 9,218 - - (6,072) - - 3,146

Redeemable Units

KJH SWEET SIXTEEN FUND

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED) Year Ended December 31, 2020

Page 29

9. RELATED PARTY TRANSACTIONS

The Manager, the shareholders of the Manager, individuals directly related to the shareholders of the

Manager and other funds managed by the Manager are considered related parties of the Fund due to the

direct or indirect common control.

All transactions between the related parties are conducted at arm’s length and can be summarized as follows:

9.1 Units

As at December 31, 2020, related parties owned 64,346 units of the 2017-Q1 Series, 20,138 units of

the 2018-Q1 Series, 39,709 units of the 2020-Q1 Series, 4,760 units of the 2020-Q3 Series and 15,335

units of the 2020-Q4 Series (2019 – 64,490 units of the 2017-Q1 Series, 20,138 units of the 2018-Q1

Series, 3,999 units of the 2018-Q3 Series, 5,099 units of the 2018-Q4 Series, 1,488 units of the 2019-

Q2 Series and 153 units of the USD Series) of the Fund.

9.2 Management and Performance Fees

Management fees are calculated on each valuation date based on the net asset value of the Fund on

the previous valuation date at an annual rate of 1.0%. Management fees are paid to the Manager in

consideration of the provision of management, distribution and portfolio advisory services. For the

year ended December 31, 2020, management fees totaled $475,875 (2019 – $455,996).

The Manager is also entitled to receive an annual performance fee of 20% based on the difference

between the net asset value of the Fund on the last valuation day of the year and the highest net asset

value of the Fund on last valuation day of any preceding year, as adjusted and weighted for

contributions and redemptions, and that exceeds 6% of the Fund’s net asset value at the beginning of

the year. For series launched during the year, the performance fee is based on the difference between

the net asset value of the Fund on the last valuation day of the year and the launch price of the series.

For the years ended December 31, 2020 and 2019, performance fees are as follows:

Performance Fees 2020 2019

2017-Q1 Series -$ -$

2018-Q1 Series 7 -

2018-Q2 Series - -

2018-Q3 Series - -

2018-Q4 Series - -

2019-Q1 Series - -

2019-Q2 Series - -

2020-Q1 Series 66 -

2020-Q2 Series 8 -

2020-Q3 Series 11 -

2020-Q4 Series - -

USD Series - -

92$ -$ Total

KJH SWEET SIXTEEN FUND

NOTES TO THE FINANCIAL STATEMENTS (CONTINUED) Year Ended December 31, 2020

Page 30

9. RELATED PARTY TRANSACTIONS (CONTINUED)

Accrued liabilities includes $137,962 (2019 – $38,870) payable to the Manager for management and

performance fees.

9.3 Transaction Costs

For the year ended December 31, 2020, commissions paid to brokers on security transactions totaled

$59,192 (2019 – $27,585). Approximately 80% (2019 – 80%) of these commissions were paid to the

Manager for its role as primary investment dealer.

Brokerage commissions paid on the purchase and sale of securities are included in transaction costs in

the statement of comprehensive income. In allocating brokerage business, consideration may, from

time to time, be given by the Manager of the Fund to dealers that provide research services, in addition

to order execution services. These services assist the Manager with its investment decision making for

the Fund. Where client brokerage commissions are charged, the amount paid for services other than

order execution is not generally divisible.

10. INCOME TAXES AND DISTRIBUTIONS TO UNITHOLDERS

The Fund qualifies as a mutual fund trust under the provisions of the Income Tax Act (Canada) and,

accordingly, is not subject to tax on its income, including net realized capital gains, which is paid or payable

to unitholders at the end of the tax year.

The Trust Indenture provides that all net income and net capital gains realized during the tax year are payable

to unitholders. Net income and net realized capital gains are distributed annually, as of the end of the tax

year, less any applicable losses from current or prior years or distributions.

As at December 31, 2020, the Fund had no non-capital losses available for use against future net income. In

addition, the Fund had no capital losses available for use against future net realized capital gains.

11. FILING OF FINANCIAL STATEMENTS

Pursuant to the exemption under section 2.11 of NI 81-106, Investment Fund Continuous Disclosure, the

financial statements of the Fund have not been filed with the provincial regulators. This exemption is

available when the financial statements have been sent to the unitholders by the fund as required.

Copyright © 2022 FDOKUMEN