KIVOV CONSULTING - EMMA.MSRB.org.

93

_________________________________________________________________________ 475 K Street NW, Suite 1005Washington, DC 20001202-321-4780202-540-9882(f)[email protected] KIVOV CONSULTING Retirement Housing & Long-Term Care Affiliated with Joseph Howell Consulting, LLC STRATEGIC POSITIONING ANALYSIS For THE GROVES IN LINCOLN LINCOLN, MA APRIL 2012 Prepared for MASONIC HEALTH SYSTEM OF MASSACHUSETTS

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of KIVOV CONSULTING - EMMA.MSRB.org.

_________________________________________________________________________ 475 K Street NW, Suite 1005Washington, DC 20001202-321-4780202-540-9882(f)[email protected]

KIVOV CONSULTING Retirement Housing & Long-Term Care Affiliated with Joseph Howell Consulting, LLC

STRATEGIC POSITIONING ANALYSIS For

THE GROVES IN LINCOLN

LINCOLN, MA

APRIL 2012

Prepared for

MASONIC HEALTH SYSTEM OF MASSACHUSETTS

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 1

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

TABLE OF CONTENTS

I. Introduction and Project Background……………………………………… 2

II. Site and Neighborhood Analysis………………………………………………. 8

III. Market Area………………………………………………………………………………. 16

IV. Demographic Analysis……………………………………………………………….. 20

V. Competitive Analysis…………………………………………………………………. 34

VI. Pricing and Positioning Analysis………………………………………………… 47

VII. Demand Analysis……………………………………………………………………….. 61

VIII. Retirement Housing and Long-Term Care Industry Overview…. 67

IX. Conclusions & Strategic Recommendations…………………………….. 73

Appendix……………………………………………………………………………………. 86

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 2

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

I. INTRODUCTION & PROJECT BACKGROUND A. Understanding of Engagement Masonic Health System of Massachusetts (MHS) has engaged Kivov Consulting to conduct a thorough strategic positioning analysis of The Groves in Lincoln, a luxury continuing care retirement community located in Lincoln, Massachusetts. The property consists of 168 independent living units with a mix of apartments in two distinct buildings and cottages, and a main community center with common areas and amenities. It is a full-service CCRC with long-term care services available. The health care services are provided through a Visiting Nurse Association (VNA) owned and operated by MHS; there are no long-term facilities on The Groves campus. The property has struggled to fill units since its official opening in July 2010 and in particular in the past year. As of the end of March 2012 it has just 77 occupied independent living units (out of a total of 168), an occupancy rate of 46%, and occupancy has yet at any time to reach 50%. There are a total of 98 reservation deposits, but the likelihood of converting the additional 21 deposits into actual sales and move-ins is uncertain. Sales have been particularly slow in the past year, and in the six full months since September 2011 there have been just 7 new net reservations (an average of just over 1 per month) and 10 move-ins. Exacerbating the slow sales pace has been an inordinate number of cancellations of reservations. In the past six months The Groves actually has secured 13 new deposits, but also has suffered 7 withdrawals of existing reservations. Additionally, some brief momentum that appeared to have been built at the end of 2011 appears to have been lost: there were 8 new reservation deposits in the fourth quarter of 2011 and a net of 5 new reservations after 3 cancellations, but the first quarter of 2012 has yielded just 5 new reservations and 4 cancellations. Given the situation, MHS is fully examining the property and the situation in an attempt to get things turned around as rapidly as possible. Management believes it has identified some issues that have contributed to the underperformance of the property. Specifically, there are questions as to whether the property is appropriately priced for what it provides. Other issues, however, may exist. Management is looking to build consensus internally and with stakeholders in identifying the primary issues that are leading to the underperformance, the depth and gravity of these challenges, and the steps that will need to be taken in order to address and hopefully resolve these issues. Before a comprehensive repositioning plan can take shape and in order for strategic initiatives to address the challenges to be developed, the challenges need to be more clearly and thoroughly identified and assessed.

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 3

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

MHS is looking for this strategic positioning analysis to lay the foundation for and begin the process of developing a strategic approach to addressing the main challenges and turning around the performance of the property. Therefore, the primary purpose of this analysis is to thoroughly examine and analyze the pricing and positioning of The Groves in the market and relative to its competition, as well as the fundamental dynamics of the market, in order to identify both internal and external factors that are adversely impacting the subject. Beyond this, the analysis is to then present conclusions on the impact and ramifications of these challenges and deficiencies, and where possible provide strategic recommendations for addressing and hopefully overcoming or at least mitigating these challenges, with the overall objective of improving the performance of the property. The strategic positioning analysis then could be utilized as the basis from which to formulate a more detailed repositioning plan. The strategic positioning analysis is intended for use by executive management and ownership of MHS in its deliberations about how to proceed at The Groves and next steps that should be undertaken. We understand it also will be shared with bond holders, investors, and other key stakeholders in the project. The report therefore is being developed as a full narrative document that is appropriate for distribution to these third parties. B. Subject Property History and Background The Groves in Lincoln originally was envisioned and conceived by Deaconess Abundant Life Communities, a Massachusetts based non-profit health care and long-term care/continuing care provider. Deaconess and its partners created the concept for the property, developed and began the construction of the property, and began the pre-sales effort for the property, before eventually partnering with MHS. Reportedly, Deaconess ran into significant financial difficulties during construction. The organization reached out to MHS, and a partnership ensued. MHS in November 2009 took ownership of 80% of the project – which it still current holds – and completed the construction and opened the property. Deaconess remains a 20% owner and partner in the project, despite the location of Newbury Court a competitive (but also technically a “sister”) property just a few miles away in Concord. By all accounts, MHS owns and operates The Groves and Deaconess is much more of a silent partner. Pre-sales efforts by Deaconess began back in 2006-2007 and reportedly went very well. When it became a partner, MHS reportedly was told by Deaconess that the property was 82% sold. Data provided by MHS shows 100 net sales on record as of the end of January 2010. Unfortunately, it turns out that many of these “sales” were not solid. MHS management estimates that as much as 60% of the presales commitments became cancellations. As a result, at opening in July 2010 there were far fewer move-ins than originally anticipated. In the first month of occupancy there were 15 move-ins; August saw 10 more move-ins, followed by 5

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 4

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

each in September and October. The data shows there actually were more cancellations than sales throughout 2010, by a margin of 40 to 31. By then end of 2010 approximately 28% of the community (47 units) was occupied and there were 92 net sales on record; there were 6 more move-ins in January 2011, but then sales and move-in activity hit a wall, and there has been only limited progress since the beginning of 2011. Over 2011 the community netted 27 new move-ins to bring occupancy to 44% by the end of the year. Even more alarming was that cancellations effectively were cancelling out new sales. It should be noted that in only one month since January of 2010 were more than 4 sales recorded and the average number of sales per month since January 2010 is 2.1. Over this same period, the average number of cancellations per month has been 2.3. Thus, on net, the community has lost 0.2 sales per month since the beginning of 2010. Table 1 displays the historic occupancy data and Table 2 the sales velocity data provided by MHS.

Table 1

Month Move-Ins Occ. Units Occ. %

July-10 15 15 8.9%

August-10 10 25 14.9%

September-10 5 30 17.9%

October-10 5 35 20.8%

November-10 8 43 25.6%

December-10 4 47 28.0%

December-11 4 74 44.0%

March-12 2 76 45.2%

Historic Occupancy Data

The Groves

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 5

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

Table 2

Month New Sales Cancellations Net Sales

January-10 0 2 100

February-10 1 2 99

March-10 1 3 97

April-10 1 0 98

May-10 2 2 98

June-10 9 3 104

July-10 4 12 96

August-10 2 4 94

September-10 2 6 90

October-10 2 2 90

November-10 3 3 90

December-10 3 1 92

January-11 1 0 93

February-11 2 1 94

March-11 3 5 92

April-11 4 1 95

May-11 1 1 95

June-11 0 2 93

July-11 0 2 91

August-11 3 1 93

September-11 0 1 92

October-11 1 2 91

November-11 4 0 95

December-11 3 1 97

January-12 2 1 98

February-12 1 3 96

March-12 2 0 98

MONTHLY AVG. 2.1 2.3 94.9

Historic Sales Velocity

The Groves

From the start The Groves was somewhat of a unique property and lacking in continuity. It had three distinct product lines: traditional entrance fee CCRC apartment units (Russell Building); entrance fee cottages; and a mid-market/moderate income targeted rental units (Flint Building). Additionally, from the start the property was utilizing a virtual or in-home continuing/long-term care concept. There was no assisted living or nursing care facilities on

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 6

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

campus, just the independent living units. All care was to be provided by the VNA that was owned and operated by MHS, and within residents’ homes in their independent living units. Collectively, the property was being positioned and marketed as a luxury, upscale CCRC. Choice and flexibility – hallmarks of the evolving concept of continuing care and retirement housing for today’s consumer – were considered the cornerstone of the concept. Beyond the distinct product options and the in-home care delivery, MHS even offered a number of different independent living service packages in which the key supportive services (meals and housekeeping) varied. MHS’ management found, however, that while choice was indeed a concept that was resonating with consumers, too much choice at the property was in fact confusing some consumers and that much more education was needed. Prospects were pricing the Flint Building units against market rate rental apartments in the market. As a result, management added an entrance fee option for these units, with entrance fees set at prices well below market and those of the Russell Building units. Additionally, while the virtual/in-home care concept was cutting edge, it was possibly ahead of its time, and somewhat beyond many consumers in the market that wanted – or believed they needed – to see “bricks and mortar” long-term care facilities on campus, as is the case at The Grove’s competitors. Clearly, much more education, and a different approach, was needed to sell this concept. During 2011, management at MHS and The Groves began selling the concept of the VNA and the homecare services as a model with superior care delivery and better economics for residents. This appeared to develop some traction in the market. The Groves also offers for a transfer arrangement to the Alzheimer’s care and nursing facilities at Newbury Court to meet the demands of prospects that prefer actual long-term care facilities to which to transfer. Today (as of the end of March 2012) 77 of the 168 independent living units at The Groves are occupied, an occupancy rate of 46%. Beyond this there are 21 depositors on record that have yet to move in. A number of these, however, date back to 2007 and 2008 and seem highly unlikely to be converted to move-ins. Eight of the deposits have been placed since mid 2010 when MHS was the primary owner and operating entity. These seem to provide a better opportunity for conversion to occupancy, although only one at this time has a set move-in date. For the remaining depositors, the likelihood of move-in and potential timing of move-in is uncertain. Entrance fee price points for the cottages and Russell apartment units have been set high to reflect the premier location within Lincoln, a highly affluent town in which home values are extremely strong. The community offers all units through three different entrance fee refund plans, with 90% refund, 50% refund, or 0% refund options. The Groves is considered a Type B – or modified contract – community, as all continuing care contracts utilize a fee-for-service base, but allow for some health care benefit. Specifically, residents that transfer to the Alzheimer’s

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 7

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

care and/or nursing components of Newbury Court are entitled to care in these facilities at discounted prices of 80% of the prevailing market rate per diems. Additionally, residents utilizing MHS’s VNA in-home care receive a discount off of market rates. Identifying that one particular challenge for the property appears to be well above market pricing of its cottage units, management moved aggressively to address this by offering a $100,000 price reduction and $50,000 incentive (to be used towards in-unit upgrades). Results reportedly have been inconclusive. While the price reductions did seem to generate more lead activity, sales did not experience a measurable positive impact. Admittedly, this initiative was instituted only recently, and there has not been a concerted and ongoing program promoting these incentives. Management at this time is uncertain whether such a program provided over an extended timeframe would yield positive results. Another looming challenge of which management is aware is a planned construction project that will build an overpass from Route 2 along The Groves campus. As a result, part of the campus – and a number of units in Flint Building – will be adjacent to a massive construction site for several years. The impact on the marketability of these units is uncertain, but it seems likely to be dramatic. How and what can be done to mitigate the impact of the construction project, and to find a way to make these units viable during this project, are strategies that will need to be developed going forward.

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 8

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

II. SITE & NEIGHBORHOOD ANALYSIS A. Site & Location The Groves in Lincoln is located along Route 2 (Cambridge Turnpike) in Lincoln, Massachusetts. The property is located on the south side of Route 2 just before it forks with the Cambridge Turnpike leading into downtown Concord, and the Concord Turnpike, which bypasses the town center. The property site is approximately three miles west of the Route 2 exchange with I-95 and less than two miles from downtown Concord. Map 1 provides a broader depiction of the site location relative to its surroundings. Lincoln is a small, but highly affluent bedroom community of Boston. Its picturesque setting, classic and attractive New England style homes, accessibility to Boston, and high incomes make it a very desirable location. The town is just over a 20-mile drive (and depending on traffic a 30-plus minute drive) from downtown Boston. Its convenience to I-95 and location along Route 2 also is a major benefit as this facilitates commuting patterns and access to and from Lincoln and surrounding greater Boston areas. The property is situated along a primary artery that is at points largely undeveloped. Most developed uses that exist in the more immediate vicinity of the subject are residential. As a result, surrounding land uses on the whole are compatible with the subject. We do note that immediately adjacent to the subject property are several tiny, worn, single family detached homes, including one across the street that appears semi-dilapidated. This is in stark contrast to the rest of the residential development in the immediate area, which is predominately attractive. The project enjoys strong drive-by exposure due to its location along Route 2, which is a primary east-west artery serving the region. Visibility along the road is fine, as there is ground level signage at the entrance to the community. Ingress and egress, however, are awkward. While a right turn into the property traveling east on Route 2 is simple and direct, the left turn into the property traveling west on Route 2 is not direct. More significantly, exiting the property a left turn is not permitted, forcing all traffic to travel east on Route 2. Due to a lack of turns off of Route 2, it can easily take nearly two miles traveling east on Route 2 before traffic is able to turn around and head back to the west on Route 2.

_________________________________________________________________________ 475 K Street NW, Suite 1005Washington, DC 20001202-321-4780202-540-9882(f)[email protected]

Map 1

The Groves Site Location

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 10

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

Accessibility of the property, however, is a strength due to the location along Route 2 and proximity to I-95. As noted, Route 2 is a primary east-west artery in the area. It interchanges with I-95 approximately three miles to the east, before continuing into and its apex around Somerville. To the west Route 2 leads to an exchange with I-495, approximately 12 miles driving distance from the subject. Past I-495, Route 2 continues west through Leominster, and beyond to I-91 and northwestern Massachusetts. Aside from Route 2, east-west travel in the vicinity of the subject property is less direct and quick. Consequently, the proximity to I-95 is a key to the accessibility of the subject. Interstate 95 provides for relatively direct (although not always quick, depending on the time of day and traffic) access to Route 3 and I-93 to the northeast, and past this continues into the North Shore communities, a popular day trip and vacation destination. To the south I-95 provides a connection to the Massachusetts Turnpike and then provides access to the affluent and desirable Route 9 corridor communities (including Natick, Wellesley, Newtown, and Brookline) before heading towards the South Shore communities of the Boston area. In summary, I-95 is the key artery connecting much of the suburbs of the Boston area. B. Subject Property The Groves is a full service CCRC with 168 independent living units including apartments and cottages, as well as a main community center with amenities and common areas. An even 100 of the units are within Russell Building, the main multi-story structure of the campus and within which the community center is situated (technically the residential areas are connected by the main community center). Thirty units are located within a distinct structure, the Flint Building. There are also 38 cottage units situated around the campus. There are no physical long-term care facilities on the campus; rather, all health and long-term care is provided within residents’ independent living units, through the VNA owned and operated by MHS. The Groves also has a transfer arrangement with the assisted living and nursing care centers on the Newbury Court campus, a sister community (but also a competitor) owned by Deaconess a few miles away in Concord. The Groves provides a modified, Type B entrance fee contract which is based on a fee-for-service concept, but allows for a health care benefit of discounted VNA home care rates or a discount at the long-term care components at Newbury Court. Entrance fee contracts come with three different refund options: 90% refund, 50% refund, and 0% refund plans. The ingress into the community off of Route 2 (which as noted is not ideal) leads to a short access road that winds its way slightly uphill to the community. An attractive stone barrier lines the access road. The access road runs to the middle of the campus, and delivers traffic to the front of the main building with the community center and Russell House apartments. This is a relatively attractive multi-story structure of three and four stories, with yellowish vinyl siding, white trim, and a gray tile slanted roof. Single-story cottages of a similar architectural design

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 11

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

and look (but with a mix of exterior colored vinyl siding including yellow, tan, and blue) are situated around the campus. A large portico extends out from the main entrance and provides for a covered drop-off. There is some landscaping, but not much grounds. All told, the property sits on approximately 30 acres, and there is a relatively attractive, densely wooded area to the back of the site plan. On the whole, however, the campus and setting are not particularly striking. Overall the exterior appearance and “curb appeal” of the subject is good; it is attractive, but not striking, and a little lacking in some of the upscale exterior design elements that might be expected from a top of the market luxury community. The main entrance opens into a grand lobby area with high ceilings, tabled ceiling design features, recessed lighting, and nice décor. This is a strength of the community. Reception is to the right from the entrance and common areas are situated all around the lobby, which forms the hub of the community. Resident halls extend out in either direction from the main hub of common areas. Straight back from the entrance across the lobby is the main dining/restaurant. This is attractive, and does capture the look of a restaurant rather than a dining facility, with very high vaulted ceilings, and separate rooms to break up the space. This too is a strength of the property. Other common areas and amenities of note on the main floor include a casual dining café, a poker room (that was converted from a Wi-Fi café that received only limited use), an arts and crafts room, a library. These areas are decent spaces, but not to the level of the restaurant or lobby. A unique design feature is an elevated second story walkway that cuts through the main lobby, overlooking the entrance and lobby on one side and the main dining room on the other. A story below entrance on the lower level there are additional commons areas. This includes an auditorium/great room below the dining room. This space is attractive, but a little small for the community (it reportedly holds 100 people). There is also an indoor pool, and a somewhat small fitness room with a separate studio room. There are outdoor walking areas that connect to the trail system in Lincoln. Another significant amenity at the subject is an underground parking garage. The apartment units within Russell Building are solid but not spectacular. The offerings range in size from a one bedroom floor plan of 770 square feet to a two bedroom with den floor plan of 1,440 square feet. Units feature 10’ ceilings, recessed lighting, and crown molding. A number of the kitchens, however, are somewhat closed off making the layout and plan seem less modern. Finishes are relatively basic consisting of laminate type counters, white appliances, Pergo-wood flooring in the kitchen in some units, and vinyl floors in baths. All units do contain a stacked washer and dryer. The cottages are attached structures that are situated around the campus. Most are attached in quads, with some duplexes. Cottage units are spacious, with attractive, modern layouts and

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 12

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

floor plans featuring large, open entertaining kitchens and vaulted ceilings in some units. Many feature a loft design with a second level that has a loft landing and can be used as a guest room (although there is no enclosed, private room). Some units have an attic rather than the loft. All units feature ground floor master bedroom and bathroom and living area. The main floor living areas range from approximately 1,400 to 2,400 square feet; the largest unit also has a 1,000 square foot basement with option to finish. According to floor plans and information provided by management, the cottage units come in four advertised floor plans ranging in size from 1,800 to 3,400 square feet. Finishes in the cottages – aside from vaulted ceilings, recessed lighting, and crown molding – are somewhat lacking for luxury priced and positioned product: standard carpeting, Pergo-wood floor in some kitchens, laminate counters, and white appliances. All cottages come with an integral garage; depending on location throughout the campus, some of the garages are side loading rather than front loading. The Flint Building does not fit with the rest of the campus and product. It reportedly was a result of the zoning and land use process that required an allocation of affordable units at the property. Reportedly 12 of the 30 units in Flint are set aside for low income use, although the parameters and guidelines for this are not clear. What is clear is that the Flint Building is a second rate product compared to the rest of The Groves. The building and its units are built to a moderate income apartment standard. Units with the original finishes still in place have plastic borders on the bottom of walls and no crown molding or any other upscale features or fixtures of note; MHS has upgraded some units to remove the plastic strip and add crown molding. Also as noted, there is a pending construction project (the Route 2 overpass) that will alter the landscape of the campus and specifically will directly impact a handful of units in Flint Building. Over the course of the overpass construction project – which by all estimates could be a three to as many as five year timeframe – this handful of units in Flint Building will effectively be adjacent to a massive construction site. Whether the impacts of this project can be mitigated and these units will have any marketability – and/or if there is a way to temporarily reposition or convert these units to another beneficial use – during this period is an issue that will need to be addressed moving forward. Entrance fees under the 90% refund plan at The Groves range from approximately $463,000 to $775,000 for Russell apartment units and are in the $900,000s for the cottage units. This translates to the high $500s per square foot for the Russell apartments and mid $400s to low $500s per square foot for all but the largest cottage unit. The weighted average Russell apartment unit entrance fee is nearly $669,000 and the weighted average cottage is just under $947,000. The weighted average unit across all of these market rate units has a 90% refundable entrance fee of over $745,000. The 30 units in Flint Building range in size from 732 to 1,127 square feet. The well below market entrance fees under the 90% refund plan range

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 13

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

from $195,000 to $375,000, and average approximately $265,000, or $285 per square foot. The per square foot price on average is less than half that of the Russell apartments. As noted, there is flexibility at the subject with regard to monthly service packages. Residents may choose an “all inclusive” package that provides for regular weekly housekeeping and a full meal plan with a debit system that allows for $480 per month in dining debit. The $480 can be used in either the main restaurant or café, at the resident’s desire, with items offered on the menus on an a la carte basis. The monthly service fee for the “all inclusive” package ranges from $2,780 to $5,050 for Russell apartments, from $5,180 to $6,260 for the cottages, and from $2,420 to $3,740 for the Flint apartments. Residents have the choice to opt out of housekeeping services and to opt for a half meal plan or opt out completely, with the monthly service fees adjusted downward accordingly. There also is an option to opt out of a wellness package ($160 per month) that is part of the “all inclusive” package. C. Surrounding Neighborhood & Amenities The surrounding neighborhood around the subject is an attractive, affluent, residential suburban area, comprised predominately of low density residential development. There are lots of small, tertiary roads that are densely wooded at frontage, with homes set back. There are many large home sites and properties and nice (although general not spectacular estate) homes are the norm. In some areas there are larger, estate-like properties. Much of the area to the west of the subject is only moderated developed and low density. Even along Route 2 heading east from Lincoln/Concord towards Boston there is limited development, and the major thoroughfare appears mostly densely wooded and exurban until reaching I-95. To the west of the subject there is little development of note. Tracy’s (a gas station/convenience store) on Route 2 just after the fork with Route 2A, is approximately one mile from the subject. After this, Route 2 is primarily a parkway cutting through large swaths of undeveloped land. Along Route 2A to the northwest lies Concord Center, with downtown Concord just under two miles from subject. Downtown Concord is a classic, historic town center, surrounded by attractive single family homes. The quaint historic town center goes on for a few blocks with a steady procession of galleries, stores/shops, and a few restaurants. A Rite Aid pharmacy is past the town center. Further past this nearly 2.5 miles from subject at Sudbury Road and Thoreau Street is a retail/commercial concentration including Concord Shopping Center, which is anchored by a local supermarket, an Ace Hardware, and a CVS pharmacy. Around this is a Starbuck’s, several convenience stores and gas stations, and Concord Depot, which contains a series of stores.

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 14

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

Also a relatively short distance from the subject (approximately four miles and seven to eight minutes driving time) to the south is Lincoln Station, the small town center of South Lincoln. This small town center has a supermarket, bistro, and post office, and is along railroad tracks and true to its name is a functioning train station. Surrounding the town center are attractive homes, horse farms, and large pieces of land. Much of the area to the south of the subject is comprised of winding roads through rolling hills, and is quite picturesque. To the east of the subject on Route 2A (which runs roughly parallel to Route 2) it is densely wooded along the road frontage and very low density residential. Route 2A passes Hanscom Field and Air Force Base, and historic sites such as the Paul Revere Capture site and Minute Man National Historic Park and visitor center. Inside of I-95 along both Route 2A and in particulate Route 2 the area becomes a little more modest, and more densely developed with moderate size, mature homes, on typical one-quarter to one-third acre lots. Parts of Lexington have a more modest, working class residential look. There also is a greater concentration of commercial/retail development in this area, including a Shaw’s supermarket, several retail plazas, in-line retailers, and the like. Big box retail and a concentration of comparison shopping retail options requires a somewhat more lengthy drive from the site. The Burlington Mall, at I-95 and US Highway 3, is the nearest full service mall, nearly a nine mile drive from the subject. A Simon Mall, Burlington Mall features more than 185 retailers, a recently renovated food court, and is anchored by mid-market to more upscale department stores Nordstrom, Lord & Taylor, Macy’s, and Sears. Health care is much more accessible, as Emerson Hospital is just three miles straight line drive from the subject along Route 2 in Concord. The aging looking hospital is surrounded by professional offices including some medical office uses with various physicians and practices. The non-profit run acute care center has 168 staffed beds. Based on data from the American Hospital Directory online (www.ahd.com), in the cost reporting year ending September 2010, the hospital reported over 6,400 discharges and nearly $500 million in patient revenue. Clinical and specialty services at Emerson Hospital include cardiovascular, emergency, neurosciences, oncology, orthopedic, radiology/imaging, rehabilitation, intensive care, and wound care, as well as psychiatric and skilled nursing units. While not part of a larger healthcare network, Emerson Hospital has clinical collaborations with several leading Boston area medical institutions including Brigham and Women’s Hospital, Childrens Hospital Boston, Hospice of the North Shore and Greater Boston, Lahey Clinic (specializing in pain management, neurosurgery, spine surgery, and urology), Mass General Hospital, and Tufts Medical Center (specializing in nephrology). The greater Boston area is known as a bastion of some of the world’s most advanced and high quality health care research and services, including some of the

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 15

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

aforementioned facilities/networks and others. Much of this is within a reasonable distance (although not the immediate market area) of the subject.

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 16

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

III. MARKET AREA The primary market area represents the geographic area surrounding the subject site from which we anticipate that the majority of prospects and move-ins would originate and within which the direct competition for the subject is located. Primary market areas vary in size depending on:

The product type and services and care being offered (the more specialized a product or service, the larger the area from which it attracts prospects);

The size of the subject property (larger properties have greater critical mass and typically larger marketing budgets allowing them to reach more prospects and attract them from a larger area; Erickson Living communities are a good example of this dynamic).

The amount of competition or alternative housing and care options in the area (the fewer alternatives, generally the larger the area from which a community will attract residents); and

The density of the area (urban markets are smaller in size and rural markets are larger) Market areas are typically defined by physical barriers (such as bodies of water or other major topographical features and primary arteries) and psychosocial barriers/boundaries, such as changing neighborhoods, socioeconomic make-up of areas, and the like. Rings or radii often are utilized as primary market areas for retirement housing and long-term care communities; while such a market area is not necessarily invalid, it is generally an oversimplification. The best indicator of a market area for an existing community is the geographic origin of its current residents or recent admissions. While trends can change and certainly a shift in the marketing philosophy or approach can impact from where future move-ins originate, this data at least provides an actual, historical accounting. Thus, our determination of the market area focuses on this actual geographic origin data. For the purposes of this analysis, we determined the market area for the subject to be a polygon surrounding the subject and demarcated by major roadways and intersections. Based on the polygon virtually the entire market area is contained within a 10-mile radius of the subject, and much of it within eight miles or less of the subject. The primary market area polygon has seven points. It extends further to the southeast and northwest, running along the Route 2 corridor:

To the east it extends into Arlington, to the intersection of Massachusetts Avenue and US Highway 3, approximately 8.5 miles from the subject.

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 17

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

To the east/northeast it extends to the intersection of I-95 and US Highway 3, approximately 5.5 miles from the subject.

To the north it extends to US Highway 3 and Treble Cove Road, short of Billerica, approximately 7.5 miles from the subject.

To the northwest the market area boundary is I-495 and State Road 119, just over 10 miles from the subject. This is furthest point from the subject.

To the west the boundary is State Road 117 and Gleasondale Road, in the town of Stow, approximately 9.5 miles from the subject.

To the south it extends to the intersection of State Road 30 (Commonwealth Road) and Rice Road, just north of the Massachusetts Turnpike and outside of Cochituate, approximately 8.5 miles from the subject site.

To the southeast the market area boundary is along US Highway 20 (Main Street) at Waverley Avenue in Watertown, approximately 8.5 miles from the subject.

Map 2 depicts the primary market area (within the blue polygon) for The Groves, with the site location marked by the highlighted icon near the center. As noted, the depiction of the market area is based in large part upon actual geographic origin of existing residents at the subject. According to this data (which exhibits the ZIP code of origin for 73 resident households at the property), 43 of these households, or 59%, originated from municipalities located within the boundaries of our defined market area. The largest portion of these resident households came from the more immediate backyard: 18% from Lincoln and another 16% from Lexington. Beyond this, all other municipalities in the primary market area accounted for no less than 1.4% (1 household) and no more than 5.5% (4 households) of resident households. Table 3 displays the geographic origin data of current resident households of the subject. Beyond the resident origin data, the market area as defined takes into account highly relevant physical features of the area. It extends further from the subject to the southeast and northwest, running along the Route 2 corridor. This reflects that access to the subject is quickest and most direct along this route and in these directions. Access is much less direct to the north and south, and not surprisingly resident origin patterns were not as strong in these directions. Thus the market area does not extend as far in these directions. Additionally, the market area is drawn so that it remains north of The Massachusetts Turnpike and west of US Highway 3. We believe that both of these primary arteries create a real physical barrier in the area and appropriately serve as demarcations for the market.

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 18

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

Table 3

Municipality Households % of HHs Municipality Households % of HHs

Lincoln 13 17.8% Centerville 1 1.4%

Lexington 12 16.4% Franklin 1 1.4%

Concord 4 5.5% Maynard 1 1.4%

Winchester 4 5.5% Natick 1 1.4%

Acton 2 2.7% Needham 1 1.4%

Bedford 2 2.7% Newton 1 1.4%

Brookline 2 2.7% Randolph 1 1.4%

Cambridge 2 2.7% Reading 1 1.4%

Wayland 2 2.7% Sherborn 1 1.4%

Wellesley 2 2.7% Somerville 1 1.4%

Weston 2 2.7% Stoneham 1 1.4%

Arlington 2 2.7% Watertown 1 1.4%

Belmont 1 1.4% Waltham 1 1.4%

Carlisle 1 1.4% Out of State 9 12.3%

Total 73 100.0%

Within PMA 43 58.9%

Origin by Municipality of Resident Households

The Groves

We note that the nearly 60% of move-ins that have originated from within the primary market area is somewhat low but not completely out of line by industry standards. In our experience, often approximately 65% to 75% of move-ins to the subject originate from within the defined primary market area. What is of even more note with the subject’s resident origin patterns – due to the irregularity of the finding – is the low number of move-ins from out of state. Many CCRCs attract as many as 20% to 25% or more of move-ins from out of state, due primarily to the presence in the market of adult children or other family members that are influential in their parents decision to relocate into community that is proximate to family. The Groves has to date has attracted only 12% of its move-ins from out of state. Reasons for this are not readily apparent. Given the small sample size, it is possible that this is just an anomaly and would increase over time.

_________________________________________________________________________ 475 K Street NW, Suite 1005Washington, DC 20001202-321-4780202-540-9882(f)[email protected]

Map 2

The Groves Primary Market Area

_________________________________________________________________________ 475 K Street NW, Suite 1005Washington, DC 20001202-321-4780202-540-9882(f)[email protected]

IV. DEMOGRAPHIC ANALYSIS This section examines the demographics of the defined primary market area. Demographic data features current year (2011) estimates and five-year future projections (2016). The estimates and projections are developed by Nielsen Claritas, one of the country’s largest demographers. Nielsen Claritas demographic data utilizes the US Census 2000 as its base and then applies proprietary interpolations and adjustments. It is our understanding that all of the data from the 2010 Census has not yet been completely integrated into the modeling. Due to a lack of certain detail in the data in its 2011/2016 estimates and projections, we utilize both the 2009/2014 data (which has greater detail and specificity by age and income cohorts) and the 2011/2016 data sets. We perform some interpolations as necessary to extend the level of detail and precision provided in the 2009/2014 data to the 2011/2016 data, building the new data for 2011/2016 on top of the data foundation, and to develop certain data points as necessary for our analysis. A. Population and Household Trends Population and Household data and trends show that the market area is relatively mature and has a strong concentration of older adults. It also is experiencing little growth, which is typical of older towns in Massachusetts, in which there is little land available for new residential development and often zoning, land use, or other ordinances designed specifically to limit growth in many townships. Table 4 shows population trends and Table 5 displays household trends in the market area; key data and findings are summarized below.

The total population in the primary market area in the current year is estimated to be approximately 262,000 persons.

The total population will increase by just approximately 4,000 over the next five years, realizing an average annual increase of just 0.3%.

The total population age 65 and older in the market area is approximately 39,600 in the current year, comprising 15.1 percent of the total population. This is significantly higher than the corresponding national concentration of the 65+ population of 12.6% (per the 2005-2009 American Community Survey).

The 75+ population in the market area is estimated at nearly 19,600 in the current year, comprising 7.5% of the total population. Again, this is well above the corresponding national concentration of the 75+ population of 6.1% (per the 2009 ACS).

The 65+ population is projected to grow by 2.7% per annum over the next five years to a projected total of over 44,800 by 2016.

The 75+ population is projected to increase by 0.8% per annum through 2016 to a projected total of just under 20,400.

The strongest projected growth by percentage is in the 65 to 69 age cohort (5.3% per annum), followed by the 60 to 64 age cohort (3.7% per annum) and the 70 to 74 age cohort (3.4% annually). The 75 to 79 age cohort shows some modest projected growth, but the 80 to 84 age cohort is projected to experience a contraction over the next five years. This is in line with national trends as across the country the 75 to 84 age segment

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 21

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

is decreasing or showing no growth in most markets; this is due to the birth dearth that occurred nationally coming out of the Great Depression.

Table 4

Population

# % of Total # % of Total # % of Total (2000-2011) (2011-2016)

Total 255,524 100.0% 262,089 100.0% 266,103 100.0% 0.2% 0.3%

55 to 59 13,541 5.3% 18,969 7.2% 20,807 7.8% 3.6% 1.9%

60 to 64 10,419 4.1% 15,450 5.9% 18,301 6.9% 4.4% 3.7%

65 to 69 9,414 3.7% 11,351 4.3% 14,352 5.4% 1.9% 5.3%

70 to 74 9,112 3.6% 8,635 3.3% 10,108 3.8% -0.5% 3.4%

75 to 79 7,741 3.0% 7,413 2.8% 7,625 2.9% -0.4% 0.6%

80 to 84 5,334 2.1% 5,789 2.2% 5,752 2.2% 0.8% -0.1%

85+ 5,163 2.0% 6,397 2.4% 7,004 2.6% 2.2% 1.9%

55+ 60,724 23.8% 74,004 28.2% 83,949 31.5% 2.0% 2.7%

65+ 36,764 14.4% 39,585 15.1% 44,841 16.9% 0.7% 2.7%

70+ 27,350 10.7% 28,234 10.8% 30,489 11.5% 0.3% 1.6%

75+ 18,238 7.1% 19,599 7.5% 20,381 7.7% 0.7% 0.8%

% Annual Change

Older Adult Population by Age and Year

The Groves Primary Market Area2000 2011 2016

There are approximately 100,600 households in the market area in the current year.

As with population, there will be relatively nominal growth in the number of households in the market over the next five years, with total households increasing by just 0.2% per annum.

There are approximately 24,200 households age 65 and older in the market area, comprising 24.1% of all households. The number of 65+ households is projected to increase by 0.8% per annum over the next five years, adding approximately 600 such households each year.

There are just over 11,900 households age 75 and older in the market area, comprising 11.8% of all households. The number of 75+ households is projected to increase by 0.6% per annum through 2016, adding approximately 70 such households annually.

As with the population data, the strongest growth amongst older adults is projected in the 65 to 69 age cohorts. Also as with population, the 75 to 79 age cohort is projected to experience relatively nominal growth and 80 to 84 age cohort is projected to contract, reflecting national trends.

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 22

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

Table 5

Households

# % of Total # % of Total # % of Total (2000-2011) (2010-2016)

Total 97,261 100.0% 100,627 100.0% 101,758 100.0% 0.3% 0.2%

55 to 59 8,211 8.4% 11,044 11.0% 11,995 11.8% 3.1% 1.7%

60 to 64 5,764 5.9% 9,152 9.1% 10,751 10.6% 5.3% 3.5%

65 to 69 6,074 6.2% 6,925 6.9% 8,681 8.5% 1.3% 5.1%

70 to 74 5,247 5.4% 5,382 5.3% 6,249 6.1% 0.2% 3.2%

75 to 79 5,435 5.6% 4,729 4.7% 4,823 4.7% -1.2% 0.4%

80 to 84 3,487 3.6% 3,866 3.8% 3,801 3.7% 1.0% -0.3%

85+ 2,329 2.4% 3,324 3.3% 3,655 3.6% 3.9% 2.0%

55+ 36,547 37.6% 44,422 44.1% 49,955 49.1% 2.0% 0.8%

65+ 22,572 23.2% 24,226 24.1% 27,209 26.7% 0.7% 0.8%

70+ 16,498 17.0% 17,301 17.2% 18,528 18.2% 0.4% 0.4%

75+ 11,251 11.6% 11,919 11.8% 12,279 12.1% 0.5% 0.6%

Older Adult Households by Age and Year

The Groves Primary Market Area2000 2011 2016 % Annual Change

B. Household Composition The following displays the relationship between households and population in the market area by age group. As shown in Table 6, the headship ratio in the market is 0.38, meaning that there are 0.39 households per person. This is equivalent to an average household size of 2.60 persons per household. In most markets, as households age, household size typically becomes smaller (and thus the headship ratio increases); we note that this pattern essentially holds true in the market area with the exception of an increase in household size from the 80 to 84 to 85+ age cohorts.

Table 6

Age HHs Pop. HH Size Ratio

Total 100,627 262,089 2.60 0.38

65 to 69 6,925 11,351 1.64 0.61

70 to 74 5,382 8,635 1.60 0.62

75 to 79 4,729 7,413 1.57 0.64

80 to 84 3,866 5,789 1.50 0.67

85+ 3,324 6,397 1.92 0.52

2011 Headship Ratios

The Groves Primary Market Area

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 23

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

Household tenure in the market area is weighted towards homeownership and reflects national trends. According to the data, a little over two-thirds of all households are homeowners while approximately 33% are renters. (Nationally homeownership is approximately 67%.) As is typical in most markets, and as shown in Table 7, homeownership is higher amongst older adult households than it is amongst the overall population. Amongst households age 75 and older, a slightly higher 69% are owner occupied. This data is impacted by the high ratio of renters (44%) amongst the 85 and older population; homeownership is in the 70% to 80% range for households aged in their 60s and 70s. This is based on year 2000 Census data.

Table 7

Age

# % # % # %

All Households 66,202 67.5% 31,852 32.5% 98,054 100.0%

55-64 12,038 82.6% 2,529 17.4% 14,567 100.0%

65-74 9,366 80.8% 2,228 19.2% 11,594 100.0%

75-84 6,411 72.6% 2,425 27.4% 8,836 100.0%

85+ 1,499 56.1% 1,175 43.9% 2,674 100.0%

75+ 7,910 68.7% 3,600 31.3% 11,510 100.0%

Household Tenure (2000 Census)

TotalOwner Renter

The Groves Primary Market Area

An examination of households by household type (again as of the year 2000 Census data) displays that amongst households at or above poverty level, nearly three in four are married couples while just 16% are unrelated individuals (Table 8). As households age, this relationship shifts. Approximately half of households age 75+ are married couples and 37% are unrelated individuals.

Table 8

Household Type

Pop % Pop % Pop %

Total At/Above Poverty 236,265 100.0% 17,480 100.0% 14,958 100.0%

Married Couple 174,145 73.7% 12,228 70.0% 7,422 49.6%

Male Householder 7,096 3.0% 522 3.0% 511 3.4%

Female Householder 17,979 7.6% 1,028 5.9% 1,494 10.0%

Unrelated Individuals 37,045 15.7% 3,702 21.2% 5,530 37.0%

Population by Household Type (2000 Census)

75+All Households 65-74

The Groves Primary Market Area

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 24

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

Table 9 shows the breakdown of households by living arrangement and households living alone for the 65 and older population in the market area as of the year 2000. (Data is not available for the 75+ cohort specifically or for the current year.) The bottom panels summarize the population living alone and show that 26% of persons age 65+ in the market area live alone. Additionally, approximately 43% of all 65+ households are single persons living alone.

Table 9

Household Arrangement Pop %

Total Population 36,929 100.0%

In Households 34,082 92.3%

In Family Households

Male Householder 9,881 26.8%

Female Householder 2,807 7.6%

Spouse 8,712 23.6%

Parent 1,105 3.0%

Other Relatives 1,124 3.0%

Non-Relatives 114 0.3%

Total In Family HHs 23,743 64.3%

In Non-Family Households

Male HHer Living Alone 2,150 5.8%

Male Hher Not Living Alone 162 0.4%

Female Hher Living Alone 7,461 20.2%

Female Hher Not Living Alone 260 0.7%

Non-Relatives 307 0.8%

Total In Family HHs 10,340 28.0%

In Group Quarters 2,847 7.7%

Household Arrangement # %

Total Population 36,929 100.0%

Population Living Alone 9,611 26.0%

Total Households 22,572 100.0%

Population Living Alone 9,611 42.6%

65+ Population by Household Arrangement and

Living Alone (2000 Census)

65+ Living Alone Summary

The Groves Primary Market Area

The Groves Primary Market Area

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 25

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

C. Household Income The following examines older adult households by income within the market area. The data shows that on the whole older adult households in the market are relatively affluent and have strong income. We note that the very high reported incomes of Lincoln are somewhat tempered on aggregate by the inclusion of somewhat less affluent municipalities within the defined market area. Table 10 and Table 11 display 65+ and 75+ households in the market by income, respectively; Table 12 displays the median income by age cohort. Some of the key findings are summarized below:

Of the 24,226 households age 65 and older in the market in the current year, approximately 53% (12,800 households) are estimated to have incomes in excess of $50,000 and 8,963 households (or 37%) are estimated to have an annual income in excess of $75,000.

The number of age 65+ households with incomes in excess of $50,000 will increase by over 2,800 over the next five years to over 15,600 by 2016, representing 58% of all 65+ households. This represents an increase of 4.4% per annum.

The number of age 65+ households with incomes in excess of $75,000 will increase by over 2,400 over the next five years to nearly 11,400 by 2016, representing over 42% of all 65+ households. This represents an increase of 5.4% per annum.

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 26

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

Table 10

Income

# % # % # % (2000-2011) (2011-2016)

<$10,000 2,091 9.3% 1,735 7.2% 1,717 6.3% -1.5% -0.2%

$10,000 - $14,999 1,831 8.1% 1,154 4.8% 1,073 3.9% -3.4% -1.4%

$15,000 - $19,999 1,742 7.7% 1,444 6.0% 1,371 5.0% -1.6% -1.0%

$20,000 - $24,999 1,515 6.7% 1,415 5.8% 1,404 5.2% -0.6% -0.2%

$25,000 - $29,999 1,459 6.5% 1,255 5.2% 1,363 5.0% -1.3% 1.7%

$30,000 - $34,999 1,258 5.6% 1,210 5.0% 1,209 4.4% -0.3% 0.0%

$35,000 - $39,999 1,198 5.3% 1,175 4.8% 1,164 4.3% -0.2% -0.2%

$40,000 - $49,999 2,123 9.4% 2,039 8.4% 2,274 8.4% -0.4% 2.3%

$50,000 - $59,999 1,612 7.1% 1,719 7.1% 1,852 6.8% 0.6% 1.6%

$60,000 - $74,999 1,780 7.9% 2,118 8.7% 2,398 8.8% 1.7% 2.6%

$75,000 - $99,999 2,122 9.4% 2,432 10.0% 2,890 10.6% 1.3% 3.8%

$100,000 - $149,999 1,977 8.8% 3,046 12.6% 3,781 13.9% 4.9% 4.8%

$150,000+ 1,864 8.3% 3,484 14.4% 4,714 17.3% 7.9% 7.1%

Total 22,572 100.0% 24,226 100.0% 27,209 100.0% 0.7% 2.5%

$35,000+ 12,676 56.2% 16,014 66.1% 19,073 70.1% 2.4% 3.8%

$50,000+ 9,355 41.4% 12,800 52.8% 15,635 57.5% 3.3% 4.4%

$75,000+ 5,963 26.4% 8,963 37.0% 11,385 41.8% 4.6% 5.4%

$100,000+ 3,841 17.0% 6,530 27.0% 8,495 31.2% 6.4% 6.0%

Households 65+ by Income

% Annual Change2000 2011 2016

The Groves Primary Market Area

Of the approximately 11,900 households age 75 and older in the market in the current year, approximately 43% (5,134 households) are estimated to have incomes in excess of $50,000 and approximately 3,430 households (or 29%) are estimated to have incomes in excess of $75,000.

The number of age 75+ households with incomes in excess of $50,000 will increase by approximately 630 over the next five years to 5,767 by 2016, representing 47% of all 75+ households. This represents an increase of 2.5% per annum.

The number of age 75+ households with incomes in excess of $75,000 will increase by over 500 over the next five years to approximately 3,960 by 2016, representing 32% of all 75+ households. This represents an increase of 3.1% per annum.

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 27

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

Table 11

Income

# % # % # % (2000-2011) (2011-2016)

<$10,000 1,307 11.6% 1,057 8.9% 990 8.1% -1.7% -1.3%

$10,000 - $14,999 1,191 10.6% 745 6.2% 647 5.3% -3.4% -2.6%

$15,000 - $19,999 1,081 9.6% 946 7.9% 858 7.0% -1.1% -1.9%

$20,000 - $24,999 953 8.5% 884 7.4% 854 7.0% -0.7% -0.7%

$25,000 - $29,999 832 7.4% 789 6.6% 785 6.4% -0.5% -0.1%

$30,000 - $34,999 676 6.0% 722 6.1% 728 5.9% 0.6% 0.2%

$35,000 - $39,999 625 5.6% 649 5.4% 647 5.3% 0.3% -0.1%

$40,000 - $49,999 1,013 9.0% 994 8.3% 1,003 8.2% -0.2% 0.2%

$50,000 - $59,999 629 5.6% 826 6.9% 858 7.0% 2.9% 0.8%

$60,000 - $74,999 678 6.0% 873 7.3% 947 7.7% 2.6% 1.7%

$75,000 - $99,999 878 7.8% 978 8.2% 1,047 8.5% 1.0% 1.4%

$100,000 - $149,999 679 6.0% 1,154 9.7% 1,312 10.7% 6.4% 2.7%

$150,000+ 707 6.3% 1,301 10.9% 1,603 13.1% 7.6% 4.6%

Total 11,249 100.0% 11,919 100.0% 12,279 100.0% 0.5% 0.6%

$35,000+ 5,209 46.3% 6,776 56.8% 7,417 60.4% 2.7% 1.9%

$50,000+ 3,571 31.7% 5,134 43.1% 5,767 47.0% 4.0% 2.5%

$75,000+ 2,264 20.1% 3,434 28.8% 3,962 32.3% 4.7% 3.1%

$100,000+ 1,386 12.3% 2,456 20.6% 2,915 23.7% 7.0% 3.7%

Households 75+ by Income

% Annual Change2000 2011 2016

The Groves Primary Market Area

Median household income is much stronger for “younger old” households than for “older old” households. Specifically, the median household income by five-year age cohort ranges from a high of nearly $113,000 for households age 55 to 59 to approximately $32,700 for households age 85 and older.

The median household income declines with age, with the most significant drop from the 60 to 64 age cohort (approximately $106,300) to the 65 to 69 age cohort (approximately $68,300).

All age cohorts show a projected increase in median income of between 2% to 3% – or 0.6% to 1.0% per annum – over the next five years.

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 28

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

Table 12

Age 2000 2011 2016

# # # (2000-2011) (2011-2016)

55 to 59 $92,239 $112,914 $118,109 2.0% 0.9%

60 to 64 $87,114 $106,306 $109,663 2.0% 0.6%

65 to 69 $54,235 $68,336 $71,785 2.4% 1.0%

70 to 74 $47,963 $60,658 $63,539 2.4% 0.9%

75 to 79 $35,201 $45,353 $47,659 2.6% 1.0%

80 to 84 $31,287 $39,195 $40,339 2.3% 0.6%

85+ $26,016 $32,725 $34,217 2.3% 0.9%

Median Household Income of Older Adult Households by Age

% Annual Change

The Groves Primary Market Area

D. Home Value Nielsen Claritas provides current year estimates and future year projections of home value. This data is based on US Census data and interpolated and adjusted by Nielsen Claritas. It is not considered as reliable or valid of an indicator of home values/prices in a market as is actual sales data. We note, however, that it can be a good indicator of relative value or affluence of one area as compared to another. The Nielsen Claritas home value data displayed in Table 13 shows that the estimated median home value across the market in the current year is approximately $496,000. This is an increase of approximately 52% since the year 2000, which takes into account the significant gains in the residential real estate values experienced in the early to mid 2000s then tempered for the pullback in values and struggles of the home market in the past few years. The median value in the market is projected to increase to over $558,000 by 2016. This is an increase of approximately 13%, or 2.5% per annum, over the next five years. It is estimated that nearly half of all homes in the market area have a value of $500,000 or greater. This is a meaningful benchmark in that entrance fees for the Russell apartment units at the subject start in the $460,000s and suggest that prospects would need to have home values in excess of $500,000 to afford the entrance fee at the subject. (While many prospects have total assets well in excess of entrance fees, it is our experience that the majority of prospects would prefer to utilize the proceeds generated from the sale of the primary home to fund the entrance fee payment rather than liquidate and utilize assets for this purpose. Thus, the home value often is critical in determining a prospect’s capacity to “afford” the entrance fee.) We note that this data was not available by age cohort or for older adults. In our experience, however, home values for the older adult population tend to be higher than those for the

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 29

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

overall population as many homeowners in these age cohorts have bought up over the years. Older adults also as a rule will have significantly more equity in their homes than younger homeowners.

Table 13

Home Values # % # % # % Period Per Annum

<$60,000 495 0.7% 338 0.5% 302 0.4% -10.7% -2.1%

$60,000 - $99,999 641 1.0% 243 0.3% 218 0.3% -10.3% -2.1%

$100,000 - $149,999 2,414 3.6% 618 0.9% 472 0.7% -23.6% -4.7%

$150,000 - $199,999 6,362 9.6% 1,470 2.1% 1,111 1.6% -24.4% -4.9%

$200,000 - $299,999 19,044 28.8% 7,628 10.8% 5,749 8.1% -24.6% -4.9%

$300,000 - $399,999 15,242 23.0% 12,778 18.2% 10,864 15.3% -15.0% -3.0%

$400,000 - $499,999 8,881 13.4% 12,594 17.9% 11,662 16.4% -7.4% -1.5%

$500,000 - $749,999 8,112 12.3% 21,149 30.1% 22,388 31.4% 5.9% 1.2%

$750,000 - $999,999 2,822 4.3% 7,350 10.4% 10,754 15.1% 46.3% 9.3%

$1,000,000+ 2,189 3.3% 6,200 8.8% 7,677 10.8% 23.8% 4.8%

Total 66,202 100.0% 70,368 100.0% 71,197 100.0% 1.2% 0.2%

Median Home Value $327,200 $496,154 $558,302 12.5% 2.5%

$150,000+ 62,652 94.6% 69,169 98.3% 70,205 98.6% 1.5% 0.3%

$250,000+ 46,768 70.6% 63,885 90.8% 66,220 93.0% 3.7% 0.7%

$300,000+ 37,246 56.3% 60,071 85.4% 63,345 89.0% 5.5% 1.1%

$400,000+ 22,004 33.2% 47,293 67.2% 52,481 73.7% 11.0% 2.2%

$500,000+ 13,123 19.8% 34,699 49.3% 40,819 57.3% 17.6% 3.5%

2011-2016 Growth

Home Value Distribution (Census Data)

201620112000

The Groves Primary Market Area

To lend further insight into this issue, and in an attempt to gather what may be more accurate home value data that what is provided by Nielsen Claritas, we also examined active listings and recent home sales in the market as compiled and provided online by Realtor.com. This listings clearinghouse is not necessarily all inclusive, but is supposed to provide a mirror of the generally comprehensive listings data available to realtors via multiple listings and MRIS data (at the very least it is a conglomeration of listings data provided by many of the larger realtors and brokerages in most areas). Listings can be searched for by defined geographies. Realtor.com also provides records of recent sales (the past six months) within a defined geography. For the purposes of this analysis we examined both listings and recent sales, and gathered data both for Lincoln specifically, and more importantly for the overall market area. To approximate the geography of the market area we included in our search process the following municipalities that are situated within the primary market: Lincoln, Lincoln Center, Concord, West Concord, Lexington, Stony Brook, Kendal Green, Weston, Hastings, Silver Hill, Waltham,

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 30

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

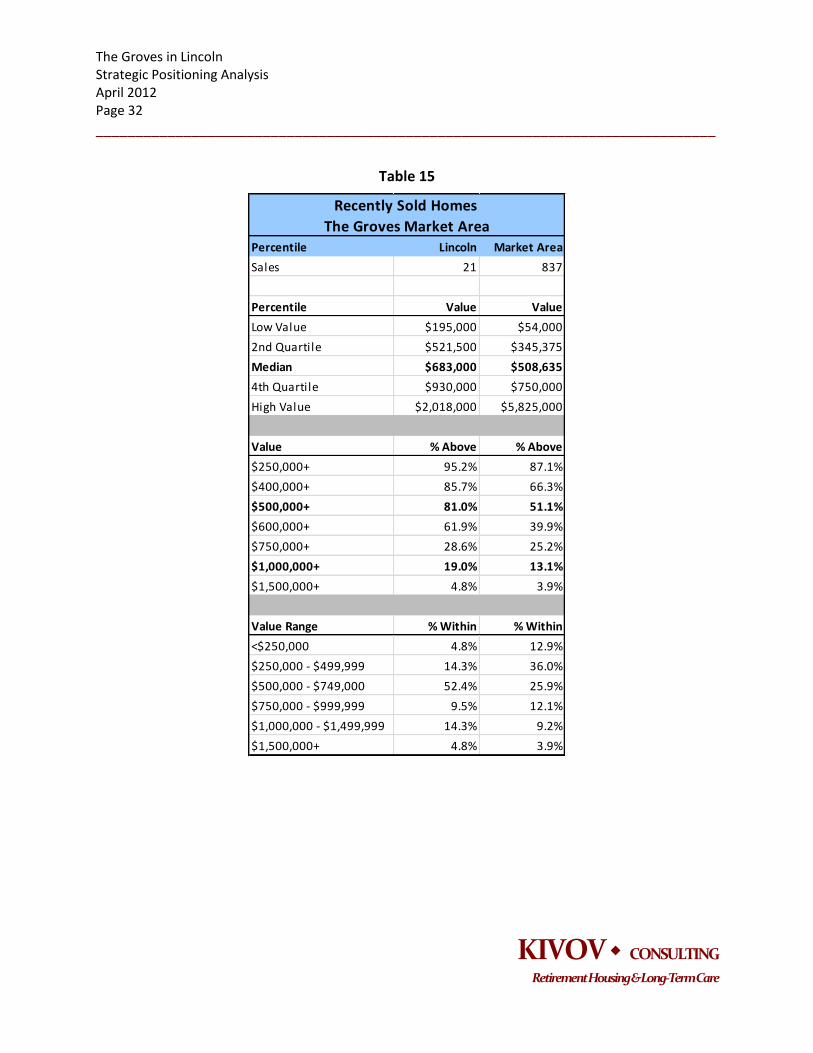

Cherry Brook, Bedford, Wayland, South Waltham, Waverley, Sudbury, North Sudbury, Belmont, Maynard, Carlisle, Acton, West Acton. Overall, the data shows that home values are extremely high in Lincoln, and much stronger than those of the market area overall (although across the market area home values are still strong on aggregate, and somewhat higher than the indicated in the Nielsen Claritas data). Table 14 shows that the median active list price in Lincoln was $1,100,000. This is based on a very small inventory of only 45 homes. Across the market area the median price of an actively listed unit was approximately $639,000. The compilation of recent sales, however, shows notably lower prices. In a small sample of 21 sales in Lincoln the median sale price from October 2011 through March 2012 was $683,000; across the market area the median sale price over the same six month period was approximately $509,000, much more in line with the Nielsen Claritas median home value. Additionally, only approximately 13% of homes sold were for in excess of $1 million; this is the core of the market for the subject’s cottage units with 90% refund entrance fees that begin in the $900,000s. This data is displayed in Table 15. The 837 sales recorded over the past six months is an average of nearly 140 sales per month. Assuming this sales pace moving forward, the 1,264 active listings in the market would equate to 9.1 months of inventory. Table 16 provides a comparison of listings to recorded sales throughout the primary market area. The data shows that on average, the sale price has been approximately 80% of the list price (comparing the two medians).

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 31

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

Table 14

Percentile Lincoln Market Area

Listings 45 1,264

Percentile Value Value

Low Value $228,000 $85,000

2nd Quartile $599,000 $410,000

Median $1,100,000 $638,750

4th Quartile $1,727,500 $1,148,000

High Value $8,590,000 $19,500,000

Value % Above % Above

$250,000+ 97.8% 93.4%

$400,000+ 86.7% 75.9%

$500,000+ 77.8% 65.1%

$600,000+ 71.1% 53.6%

$750,000+ 62.2% 41.5%

$1,000,000+ 51.1% 27.4%

$1,500,000+ 31.1% 13.9%

Value Range % Within % Within

<$250,000 2.2% 6.6%

$250,000 - $499,999 20.0% 28.2%

$500,000 - $749,000 15.6% 23.7%

$750,000 - $999,999 11.1% 14.1%

$1,000,000 - $1,499,999 20.0% 13.4%

$1,500,000+ 31.1% 13.9%

The Groves Market Area

Active Home Listings

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 32

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

Table 15

Percentile Lincoln Market Area

Sales 21 837

Percentile Value Value

Low Value $195,000 $54,000

2nd Quartile $521,500 $345,375

Median $683,000 $508,635

4th Quartile $930,000 $750,000

High Value $2,018,000 $5,825,000

Value % Above % Above

$250,000+ 95.2% 87.1%

$400,000+ 85.7% 66.3%

$500,000+ 81.0% 51.1%

$600,000+ 61.9% 39.9%

$750,000+ 28.6% 25.2%

$1,000,000+ 19.0% 13.1%

$1,500,000+ 4.8% 3.9%

Value Range % Within % Within

<$250,000 4.8% 12.9%

$250,000 - $499,999 14.3% 36.0%

$500,000 - $749,000 52.4% 25.9%

$750,000 - $999,999 9.5% 12.1%

$1,000,000 - $1,499,999 14.3% 9.2%

$1,500,000+ 4.8% 3.9%

Recently Sold Homes

The Groves Market Area

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 33

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

Table 16

Percentile Listings Sales

Number 1,264 837

Percentile Value Value

Low Value $85,000 $54,000

2nd Quartile $410,000 $345,375

Median $638,750 $508,635

4th Quartile $1,148,000 $750,000

High Value $19,500,000 $5,825,000

Value % Above % Above

$250,000+ 97.8% 87.1%

$400,000+ 86.7% 66.3%

$500,000+ 77.8% 51.1%

$600,000+ 71.1% 39.9%

$750,000+ 62.2% 25.2%

$1,000,000+ 51.1% 13.1%

$1,500,000+ 31.1% 3.9%

Value Range % Within % Within

<$250,000 2.2% 12.9%

$250,000 - $499,999 20.0% 36.0%

$500,000 - $749,000 15.6% 25.9%

$750,000 - $999,999 11.1% 12.1%

$1,000,000 - $1,499,999 20.0% 9.2%

$1,500,000+ 31.1% 3.9%

Home Listings Versus Recent Sales

The Groves Market Area

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 34

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

V. COMPETITIVE ANALYSIS This analysis focuses exclusively on service-enriched independent living, and will not address the competitive marketplace for long-term care. All residents at the subject are admitted as independent living; furthermore, whatever is done to address and provide for long-term care to residents of The Groves, the ongoing success and viability of the subject will be predominately dependent on independent living. A. Independent Living The independent living competitive analysis focuses specifically on service enriched or “congregate” style communities, in which a range of supportive services, typically to include meals, housekeeping services, transportation, and others, are provided to residents as part of the monthly fee. The analysis includes both rental arrangement communities and entrance fee communities as in our experience both models are part of the overall universe of options that would be considered by the target market and would represent competition for the subject. The competitive inventory also includes both freestanding service enriched independent-living communities as well as those that are part of a larger property and provide either a partial, pseudo, or full continuum of care, including lifecare and fee-for-service CCRCs. Not considered to be directly competitive – and thus not included in this analysis – are age-qualified properties without supportive services in which residents pay strictly for the real estate component, either with for-sale or rental structures. These properties target the active adult market. In our experience, while service enriched independent living is not nearly as need-driven as assisted living, there may be some element of need or frailty that is underlying prospective residents’ decision to move in beyond the lifestyle choices that are the primary motivation behind relocation into active adult housing. The retirement housing industry typically utilizes need for assistance with instrumental activities of daily living (IADLs) – which includes activities such as meal preparation, cleaning/housekeeping, driving/transportation, and the like – as a barometer for service enriched independent living. The active adult target market tends to be younger and healthier than prospects for service enriched independent living, and these two sub-markets of independent living are relatively discrete. Also not included in this analysis are low- and moderate-income housing options, including subsidized and tax credit communities; rather, this analysis focuses exclusively on a market rate product that serves the age- and income-qualified target market. On the whole the market area is relatively sophisticated, but not heavily developed with retirement communities and service enriched independent living product. We have identified four competitive service enriched independentliving providers within the market area. Three of

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 35

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

these are CCRCs and one is a rental provider. All four possess some partial continuum of care beyond just independent living as the rental community provides for both independent and assisted living and the CCRCs are all full service with a complete continuum of care. We also include in our analysis a fourth CCRC, North Hill, located a few miles outside of the market area in Needham. This community is in the midst of a massive repositioning and campus redevelopment effort. Despite its location outside of the market area, it was named by sales and marketing personnel at The Groves as a competitor, and we believe it does exert some competitive influence on The Groves and its market. All four of the competitive CCRCs are non-profit owned and three of the four are single-entity organizations. Deaconess Abundant Life – which is MHS’s partner in The Groves – is the other provider present in the competitive market, and the only one that is a multi-property organization. All four of the CCRCs are well established in the market, having opened between 1982 and 1994. All four also have undergone expansions and/or relatively extensive renovation efforts over time. One of the four – Brookhaven at Lexington – is a true lifecare community, and a second – North Hill – offers both a lifecare as well as a fee-for-service contract option. Carleton-Willard Village is a Type B community with a modified contract that allows for some health care benefit, while Newbury Court is strictly a Type C, fee-for-service community. The five service enriched independent living communities in the analysis provide a total of 1,001 units. Overall the market is performing extremely well and appears to be quite healthy; at the time of our analysis the aggregate occupancy rate across the inventory was 93.8%. This is well above the industry-wide average of 87.6% according to data from The State of Seniors Housing 2011 published by the National Investment Center for the Senior Housing and Care Industry (NIC) in collaboration with the American Seniors Housing Association (ASHA), American Association of Homes and Services for the Aging (AAHSA), and other industry partners. Beyond this, all of the communities individually are performing extremely well, with the exception of North Hill. We note that occupancy at this community may be artificially low due to ongoing redevelopment process. According to sales personnel, a number of units have been taken offline and the total operating inventory is now 290 units (reduced from 309). Beyond this, as a number of units recently turned over they have been held open to facilitate the redevelopment. Historically, occupancy at this property reportedly has been much stronger. The aggregate occupancy across the rest of the competitive inventory excluding North Hill was 96.5%. Table 17 inventories and displays the occupancy data for the competitive providers in this analysis.

The Groves in Lincoln

Strategic Positioning Analysis April 2012 Page 36

______________________________________________________________________________

KIVOV CONSULTING Retirement Housing & Long-Term Care

Table 17

Community City Distance Year Open Ownership

(In Miles) Units Occupied Occupancy

Brookhaven at Lexington Lexington 4.8 1989 Non-Profit Private 240 235 97.9%

Carleton-Willard Village Bedford 4.7 1982 Non-Profit Private 148 145 98.0%

Newbury Court Concord 3.1 1994 Non-Profit Private 230 216 93.9%

North Hill Needham 11.3 1984 Non-Profit Private 290 253 87.2%

Norumbega Point at Weston Weston 7.1 N/A Private 93 90 96.8%