Field Verification of GP's for Nirmal Gram Puraskar in Satara ...

Upload

khangminh22Category

view

0download

0

HOPETURNEDSOUR

HOPETURNEDSOUR

HOPETURNEDSOUR

HOPETURNEDSOUR

The second wave of the coronavirus pandemic poses a grave threat to

economic recoveryin India

RNI No. MAHENG/2009/28962 | Volume 13 Issue 04 | 16th - 30th Apr ’21Mumbai | Pages 50 | For Pr ivate Circulat ion

SIPs – ForInvestors With

Di�erent Pocket Sizes

SIPs – ForInvestors With

Di�erent Pocket Sizes

SIPs – ForInvestors With

Di�erent Pocket Sizes

Disclaimer: "Mutual Fund Investments are subject to market risks. Please read the offer documents carefully before Investing.” Nirmal Bang Niveshalaya Pvt Ltd | ARN - 111233 | Mutual Fund Distributor Regd. Office: Nirmal Bang Niveshalaya Pvt Ltd. B - 201,

Khandelwal House, Poddar Road, Near Poddar Park, Malad (East). Mumbai - 400097 | *conditions apply

Start investing in mutual funds through Systematic Investment Plans (SIPs) with as little as `1,000/month or as much as you want

Contact : 09026922443 | [email protected]

Beyond Market 16th - 30th Apr ’21 It’s simpli�ed...3

DB Corner – Page 5

A Di�cult ChapterThe RBI, which has to raise `12 lakh crore for the government, faces a daunting task amidst rising in�ation, capital out�ows and Covid-19 resurgence, which may lead to a rise in rates – Page 6Hope Turned SourThe second wave of the coronavirus pandemic poses a grave threat to economic recovery in India – Page 10The BeelinersThe IPO pipeline this year looks strong with as many as 28 companies looking to list on the bourses to raise funds – Page 13Same But Di�erentWhile key rates have been left unchanged, the RBI has experimented with a few innovative tools to manage liquidity in the system – Page 16Sore No More The coronavirus pandemic is showing no signs of slowing down, aiding the growth of stocks in the health care space, which till some time back were performing badly – Page 19Trolls On A RollMinor slights are enough for trolls to unleash their wrath on brands, and companies as well as advertisers are growing wary of cyber bullies – Page 22Shaping The Future Of Entertainment New mediums are overtaking the old in unimaginable ways in the media and entertainment industry in a bid to survive the impact of Covid-19 – Page 26Staving O� DebtAvoid allowing debt to get the better of you by following a few crucial steps – Page 29

A Dollop Of PositivityMarch ’21 saw positive �ows into equity mutual funds after 8 months of out�ows – Page 32Farsighted SecurityIndividuals should buy term insurance plans despite the likely rise in premiums to secure the future of their dependents – Page 34

MF Blackboard – Page 36Technical Outlook – Page 41

A Journey Of Self-discoveryValue investor Guy Spier shares lessons and real-life skills in his best-selling book ‘The Education of a Value Investor’ – Page 42

Important Jargon – Page 47

Editor-in-Chief & Publisher: Rakesh BhandariEditor: Tushita NigamSenior Sub-Editor: Kiran V Uchil

Art Director: Sachin KambleJunior Designer: Orianne Fernandes

Operations: Namrata Sabbani

Printed and published by Mr Rakesh Bhandari on behalf of Nirmal Bang Financial Services Pvt Ltd, printed at Uchitha Graphic Printers Pvt Ltd65, Ideal Ind. Estate, Senapati Bapat Marg, Lower Parel, Mumbai – 400013 and published at Nirmal Bang Financial Services Pvt Ltd, 601/6th Floor, Khandelwal House, Poddar Road, Malad (E) Mumbai - 400097. Editor: Tushita Nigam

REGISTERED OFFICE Nirmal Bang Financial Services Pvt Ltd601/6th Floor, Khandelwal House, Poddar Road, Malad (East) Mumbai - 400097Tel: 022 - 6273 9600

Web: www.nirmalbang.com [email protected] No: 022 - 6273 8047

Research Team: Sunil Jain, Vikas Salunkhe, Swati Hotkar Shewale, Nirav Chheda, Amit Bhuptani, Ritu Poddar, Aniket Jadhav, Swapnil Ufale

Volume 13 Issue: 04, 16th - 30th Apr ’21

Beyond Thinking

Beyond Basics

Beyond Learning

Beyond Numbers

Beyond Buzz

CONTENTS

India is currently battling the harsh repercussions of the second wave of the deadly coronavirus pandemic. About a month back, the first wave of the virus was calming down. In fact, the country was witnessing green shoots of revival across sectors and the economy on the whole. However, we are now being pushed back and all the gains are being lost to the second wave of the pandemic.

The cover story dwells on revised forecasts by industry experts and other economic parameters that continue to be a cause of concern.

Also, in this issue we have elaborated on how the Reserve Bank of India (RBI) plans to manage the massive borrowing programme of `12 lakh crore, announced by the Indian government, without causing risk to the debt markets as well as the recently announced Monetary Policy Review where the RBI has experimented with new tools to manage liquidity in the system.

You will also find other interesting reads on the resurgence of Initial Public Offerings (IPOs) in the Indian markets, the impetus the current pandemic has given to health care companies, false claims by consumer brands and the backlash they face through digital vigilantism and trolling, the introduction of newer avenues and concepts in the media and entertainment space to keep up with the slump in this segment due to the pandemic and finally simple but concrete ways for an individual to remain debt-free.

In the Beyond Basics section, we have spoken about heavy inflows in the equity mutual fund space last month and the importance of having a term insurance plan in spite of rising premiums being charged by insurance companies.

Do read the article in the Beyond Learning section as it offers interesting takeaways from famed value investor Guy Spier’s book ‘The Education Of A Value Investor: My Transformative Quest For Wealth, Wisdom And EnlightenmenT.’

Beyond Market 16th - 30th Apr ’21 It’s simpli�ed...

DRAB AND DREARYDRAB AND DREARY

Disclaimer It is safe to assume that my clients and I may have an investment interest in the stocks/sectors discussed. Investors are required to take an independent decision before investing. Investment in equity is subject to market risk. Our research should not be considered as an advertisement or advice, professional or otherwise. The investor is requested to take into consideration all the risk factors including their financial condition, suitability to risk return profile and the like and take professional advice before investing.

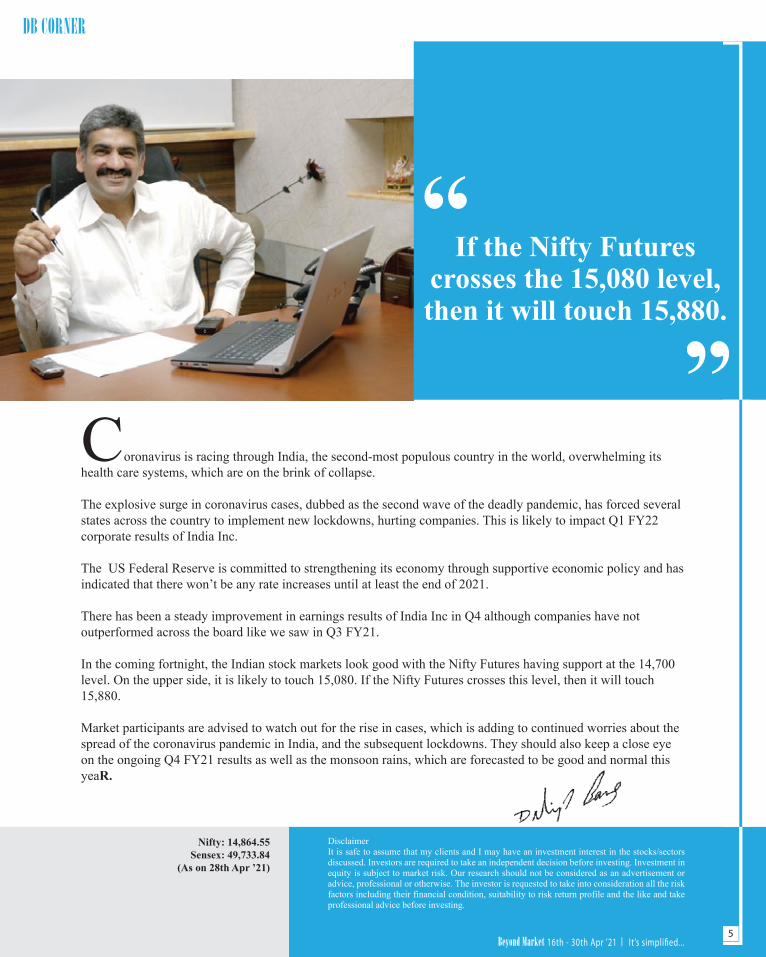

Coronavirus is racing through India, the second-most populous country in the world, overwhelming its health care systems, which are on the brink of collapse.

The explosive surge in coronavirus cases, dubbed as the second wave of the deadly pandemic, has forced several states across the country to implement new lockdowns, hurting companies. This is likely to impact Q1 FY22 corporate results of India Inc.

The US Federal Reserve is committed to strengthening its economy through supportive economic policy and has indicated that there won’t be any rate increases until at least the end of 2021.

There has been a steady improvement in earnings results of India Inc in Q4 although companies have not outperformed across the board like we saw in Q3 FY21.

In the coming fortnight, the Indian stock markets look good with the Nifty Futures having support at the 14,700 level. On the upper side, it is likely to touch 15,080. If the Nifty Futures crosses this level, then it will touch 15,880.

Market participants are advised to watch out for the rise in cases, which is adding to continued worries about the spread of the coronavirus pandemic in India, and the subsequent lockdowns. They should also keep a close eye on the ongoing Q4 FY21 results as well as the monsoon rains, which are forecasted to be good and normal this yeaR.

If the Nifty Futurescrosses the 15,080 level,then it will touch 15,880.

Nifty: 14,864.55Sensex: 49,733.84

(As on 28th Apr ’21)

5

DB CORNER

Beyond Market 16th - 30th Apr ’21 It’s simpli�ed...

BEYOND THINKING

ADIFFICULTCHAPTER

The RBI, which has to raise `12 lakh crore for the government, faces a daunting task

and Covid-19 resurgence, which may lead to a rise in rates

BEYOND THINKING

Beyond Market 16th - 30th Apr ’21 It’s simpli�ed...6

Beyond Market 16th - 30th Apr ’21 It’s simpli�ed...7

basis from the market.

INTEREST COST CHALLENGE

A large increase in the government’s borrowing costs limits its ability to spend elsewhere. But more impor-tantly, it raises the cost of borrowing for private firms and others, hamper-ing economic growth. The rise in government borrowing costs is also due to a jump in the term premium and credit spread in recent years.

Term premium, which is the difference between the repo rate and the government’s borrowing cost, poses a bigger challenge. The repo rate, or the overnight lending rate that the RBI charges banks, is the short-term risk-free rate.

From an average rate of 73 basis points since 2011, and 120 basis points in 2018 and 2019, the 10-year term premium is currently 215 basis points, having risen 35 basis points since the Union Budget presentation, and among the highest in the world.

A credit spread is a difference in yield between a government bond and another debt security of the same maturity but different credit quality. LIQUIDITY MEASURES

The central bank is resorting to measures such as Operation Twist, or simultaneous buying and selling of bonds via Open Market Operations (OMOs) to keep rates down. It conducted `3 lakh crore of bond purchases under OMOs in the last fiscal.

In Operation Twist, the central bank buys longer maturity papers and sells shorter maturity papers to keep liquidity neutral.

However, as corporates raise money at a shorter yield, Operation Twist is

would raise the borrowing costs of the government.

A 1% increase in the borrowing cost could lead to an extra interest burden of more than `1 lakh crore. Hence, as the debt manager of the government, the RBI has to keep the borrowing costs low.

However, the RBI’s main mandate is to keep inflation low. If it spirals, the central bank has to raise interest rates, which conflicts with its mandate of keeping the government’s borrowing costs under a lid.

So how will the RBI Governor Shantikanta Das do the balancing act?

THE BORROWING PLAN

The government plans to borrow `7.24 lakh crore by September, or 60% of the full-year gross borrowing target of `12.05 lakh crore, keeping with its practice of front-loading market borrowing.

The borrowing will be done across the yield curve ranging from two-year bonds to 40 years, includ-ing using Floating Rate Bonds (FRBs).

The borrowing calendar released on the RBI website showed there would be `48,000 crore of such FRBs. The 25 weekly borrowings will be in sizes of `26,000 crore to `32,000 crore ending by September ’24. The frequency of 5, 10, 14, and 20 years would be relatively higher. This segment has a relatively higher demand in the market than that of the ultra-long maturity profile.

In the current quarter ending June, the government is scheduled to borrow `3.48 lakh crore on a gross basis, and `2.43 lakh crore on a net

As Economic Affairs Secretary, Shaktikanta Das oversaw the biggest economic disruption in India. The man behind the plethora of rules and regulations that guided the ban of high-value notes in 2016 has been praised for steering the RBI during the pandemic by going out of the traditional modes of central banking to provide support to the flailing economy while keeping inflation at bay. He faces a bigger challenge now. Das has to steer the economy as the second wave of Covid-19 rages.

Along with the rescue operations, the RBI has to manage huge government borrowings at lower costs this fiscal without letting inflation out of sight. And a fierce Covid-19 resurgence has made the task more difficult. THE CHALLENGE

The government of India plans to borrow a huge sum of `12 lakh crore this fiscal, which will be managed by the RBI. In addition to this, the state governments could borrow another `10 lakh crore. While the borrowing requirement from the private sector is down, but if that picks up it will add to the demand pressure. On the other hand, the deposit growth, or loanable funds, this year is unlikely to be more than `15 lakh crore.

With the shortage of deposits, the interest rates will go up, which

Beyond Market 16th - 30th Apr ’21 It’s simpli�ed...8

crowding them out of the market. The central bank has also undertaken long-term repo operations and targeted long-term repo operations to infuse liquidity into the system.

THE G-SAP PROGRAMME

Along with the OMOs and direct intervention in the secondary market, the government recently announced Government Securities Acquisition Programme (G-SAP), a definite calendar for open market purchases of bonds. Under G-SAP, the RBI has committed to `1 lakh crore bond buys this quarter and said it will buy more. The RBI programme is a variant of the Quantitative Easing (QE) policy followed by central banks in advanced economies to tide over the global financial crisis of 2008.

Under QE, central banks conduct large-scale purchases of assets, including treasury bills and private sector bonds, to directly influence rates and risk premiums on private debt.

However, the RBI is committing to buying only government securities. G-SAP provides certainty to bond investors that the RBI will step in to buy bonds, infuse liquidity and bring down yields.

SCEPTICAL MARKETS

However, the bond market has given a tepid response to G-SAP. While the G-Sec yields fell after the announce-ment of G-SAP, they are on an upswing following rising inflation and capital outflows from India after the second surge of Covid-19.

The benchmark 10-year yield keeps breaching 6%, a level that’s seen as a line in the sand for the RBI. The central bank has refused to sell bonds

at the yield demanded by bond investors and is forcing underwriters to buy the bonds.

WHY ARE THE BOND MARKETS WARY?

While the central bank has assured that it will do whatever it takes to ensure that the borrowing programme goes through smoothly, the market doesn’t seem to be convinced.

The yardstick for a monetary bazooka is Mario Draghi’s “whatever it takes” moment at the European Central Bank in the summer of 2012, or Haruhiko Kuroda’s bold 2013 campaign at the Bank of Japan to end 15 years of deflation. The RBI’s manoeuvre isn’t in the same league. It’s just a formal announcement of bond buys the authority does on an ad hoc basis anyway. So instead of a QE, the traders see G-SAP as a yield-curve flattener, which should help the central bank manage a bloated government borrowing programme.

Bond markets see the government borrowings staying high for the next few years as the latter has announced it will target a fiscal deficit of 4.5% over the next five years. Even state government borrowings will also rise.

The RBI’s strategy of pursuing multiple objectives such as exchange rate management, inflation control and liquidity management is also leading to distortions and has confused the market.

Also, following huge stimulus unleashed by the western countries, including the US, yields are attrac-tive there, which may lead to capital outflows and slowing down of bond investments in India.

Additionally, bond investors estimate that the RBI is likely to buy securi-ties worth up to `4 lakh crore in the current year, which falls well short of the `6 lakh crore gap between demand and supply of bonds estimated by traders. Consequently, a rise in bond yields is seen as being inevitable.

To assuage the bond market, the RBI has promised to cut the net supply of central government bonds hitting the market in the current quarter by at least 41%.

‘THE YIELD TANDAV’

The RBI said while there is a “restless urgency in the air” in India to return to high growth, the bond market has remained unyielding, despite its efforts.

According to a paper by RBI’s staff, the central bank wants to maintain order in the yield curve and avoid a “tandav.” “As countries rush to inoculate their populations, the global economy should regain lost momentum in July-September. Bond vigilantes could, however, undermine the recovery, unsettle financial markets and trigger capital outflows from emerging markets,” the RBI’s paper noted.

“The Reserve Bank is striving to ensure an orderly evolution of the yield curve, but it takes two to tango and forestall a tandav,” it said.

THE INFLATION FACTOR

The rising global crude and commodity prices are already translating into higher input costs and thus higher broad-based inflation.

The WPI-based inflation has hit an eight-year high. If inflation maintains its upward trajectory and the bond

12:40 AM 100%

12:40Sunday, 12 November

> slide to unlock

XYZ Stock

11:15

XYZ

XYZ

XYZ

XYZ

UNRAVEL THEUNKNOWN

The BEYOND App untangles complex market movements, offering you in-depth research calls and investment strategies

that help meet your requirements.Explore the unknown absolutely free.

eyond P o w e r e d b y

Download BEYOND App on

For free account opening, call on +91 022 62738000 | www.nirmalbang.com

Disclaimer: Insurance is a subject matter of solicitation. Mutual Fund investments are subject to market risks. Investment in Securities/Commodities market are subject to market risks. Read all the related documents carefully before investing. Please read the Do’s and Don’ts prescribed by the Commodity Exchange before trading. We do not offer PMS Service for the Commodity segment .The securities quoted are exemplary and are not recommendatory. NIRMAL BANG SECURITIES PVT LTD – BSE (Member ID- 498): INB011072759, INF011072759, Exchange Registered Member in CDS; NSE MEMEBR ID- 09391): INB230939139, INF230939139, INE230939139; MSEI Member ID-1067) : INB260939138, INF260939138, INE260939139: Single Registration No.INZ000202536,PMS Registration No: INP000002981; Research Analyst Registration No: INH000001766; NSDL/ CDSL: IN-DP-CDSL 37-99. NIRMAL BANG COMMODITIES PVT LTD – MCX (Member ID -16590 /NCDEX Member ID -0362 /ICEX Member ID -1165) : Single Registration No. INZ000043630; NCDEX Spot: 10084; Comtrack Participants: CPID -5040; CDSL Commodity Repository Ltd: 12013300 Nirmal Bang Securities Private

Limited CIN: U99999MH1997PTC110659; Nirmal Bang Commodities Private Limited CIN: U67120MH1995PTC093213

Regd. O�ce: B-2, 301/302, 3rd Floor, Marathon Innova, O� Ganpatrao Kadam Marg, Lower Parel (W), Mumbai - 400013. Tel: 62738000/01; Fax: 62738010

Beyond Market 16th - 30th Apr ’21 It’s simpli�ed...9

street doesn’t relent, the RBI, which has placed bigger priority on reviving growth, would have to change its accommodative stance and consider rate hikes, which could complicate the debt management function of the RBI. As inflation rises, the trade-off between inflation management and debt management could become sharper.

NEW BORROWERS

In the last 15 years, the share of banks in the ownership of outstand-

ing central government bonds has fallen from 53% to 40% now. However, no alternative buyer of the equal size has emerged to fill the space.

Despite improving penetration, the share of pension and insurance inflows in bonds has shrunk over the last 15 years.

The RBI at times buys bonds to inject money into the economy, but it is now using the funds to buy dollars to stop the rupee from appreciating.

It is now looking to tap retail investors for direct bond invest-ments. But that avenue won’t be sizeable for many years. The limit for foreign portfolio holders in bonds has been raised over the years.

However, without Indian bonds being included in the global bond indices, those flows won’t be substantial. The FTSE putting India on a watch-list for “potential future inclusion” in the Emerging Markets Government Bonds Index, has raised hopes of increased FPI flowS.

BEYOND THINKING

HOPETURNED SOUR

HOPETURNED SOUR

HOPETURNED SOUR

The second wave of the coronavirus pandemic poses a

grave threat to economic recovery in India

Beyond Market 16th - 30th Apr ’21 It’s simpli�ed...10

Beyond Market 16th - 30th Apr ’21 It’s simpli�ed...11

But as the virus’ second wave lashed the country ferociously, many organizations have reduced their growth projections for this fiscal, though it is still expected in the double-digits, which is the only saving grace. Lockdowns, though partial, have come into effect in many places including in the economically-critical states of Delhi, Maharashtra (which includes Mumbai) and Gujarat. The situation in Delhi and Mumbai, in particular, are reported to be serious. Leading companies from the financial sector have lowered their growth projection for FY22 from their earlier projections.

India’s Reserve Bank of India (RBI), has pegged the country’s growth at 10.5%, while the International Monetary Fund (IMF) at 12.5% and the World Bank (WB) at 10.1%.

Many brokerages are in agreement that India had succeeded in bringing the pandemic under control by end- 2020 and that the country’s economy was rapidly returning to normalcy.

However, the second wave and its virulence and rapid spread seem to have caught the government unawares and the economy has once again been affected. All the good work done in the past to control the pandemic seems to have been undone by the second wave.

Financial services major UBS said that if the government’s efforts to conquer the virus are successful soon, then recovery should gather steam from Q2 FY22. It expects the current mobility restrictions to remain in force till end-May and then be lifted with economic activity largely returning to normalcy by end-June.

If the economic disruptions last

since early-to-mid-April and the virulence with which it has struck the country in what is being called the second wave of attack of the virus. It has the potential to undo all the good that has accrued to the Indian economy in the last three months following the start of the recovery process post the total lockdown imposed in end-March last year, which heavily damaged the economy.

Since mid-April, the second wave has increased in virulence, compel-ling the central government to impose partial lockdowns - these have increased in severity in some places though the government has stopped short of a total lockdown, which, however, could be imposed if the spread of the virus cannot be countered effectively with the present steps.

In FY21 (last fiscal or the 1st Apr ’20 to 31st Mar ’21 period), the country’s economy is expected to contract around 8%. The severity of the economic damage in the last fiscal can be gauged from the fact that in Q1 FY21, the economy contracted by a huge 24.4% while in Q2 the contraction was 7.3%.

After these two consecutive months of contraction, there was a small improvement, signalling that perhaps the worst was behind us. In Q3 (the October to December period), India’s GDP grew by a miniscule 0.4%. Growth projections for FY22 were optimistic given the apparent recovery visible in the economy till early April. The low base was also taken as a factor, which would aid growth in the current fiscal.

Many economists and organizations had projected a double-digit growth this fiscal. For the next fiscal (FY23), however, they had moderated it to around the 6.8% to 7%-mark.

Coronavirus has returned to plague India once again. Just when it appeared that the massive economic turbulence of last year (2020) was behind us forever and the economy was getting back on rails, the virus has struck again, leading to distur-bances, which could derail our economy for some more time.

Economists were beginning to talk about the bright spots in India’s economy till about a month-and-a-half ago such as the falling number of coronavirus-affect-ed patients and the increasing number of vaccinations taking place pan-India.

While the pace of vaccinations was expected to increase in the coming weeks, it was felt that at least about 40% to 45% of India’s population would be vaccinated against the virus by the end of this year (2021).

As a large part of the population got vaccinated, it was felt that the threat presented by the virus would correspondingly dissipate. This, in turn, would lead to the total ‘unlock-ing’ of the economy, which would give a big boost to the country’s economic growth.

The services sector, which has emerged as a successful sector in India in recent years would have got a big boost from the total ‘unlocking’ of the economy.

This, however, is not to be because of the resurgence of the coronavirus

Beyond Market 16th - 30th Apr ’21 It’s simpli�ed...12

longer, then India’s real GDP growth could slow down by a larger magnitude to 3.5% to 5% in FY22.

The restrictions this time are less severe than last year, but as the pandemic spreads, the severity of the restrictions also increases.

A point that needs highlighting here is that this time the virus’ virulence is centred to a large extent in Delhi, Maharashtra and Gujarat; all three are financially and industrially critical for India’s economy.

The rapid spike and spread of the virus are causing panic and shortages but it also meant that it would be less protracted.

Growth was still weak and this was amplified by the steep slide in key economic activity indicators and anaemic loan growth. It described the surging pandemic cases as worri-some for economic growth.

An important point was made by Fitch Solutions, which called for increased investments in the health care sector in the country. It said that the economy had managed to get over the pandemic by the end of last year but in recent weeks the pandem-ic spread rapidly “partly due to complacency on the social distancing measures and mask-wearing policies.”

Pointing out that India lagged behind in immunisation per capita, it said that the “unprecedented crisis has highlighted the need to increase investment in the health care sector in the country.”

Another challenge not only to India but globally relates to divergences in the speed of recovery, both across and within countries. This is coupled with the potential for persistent economic damage from the crisis.

Gita Gopinath, the Chief Economist at the International Monetary Fund (IMF) said that recoveries are diverging dangerously across and within countries as economies with slower vaccine roll out, more limited policy support and more reliant on tourism do less well.

She, however, said that the IMF was now projecting a stronger recovery for the global economy both this year and the next as compared to its earlier forecast with growth at 6% in 2021 and 4.4% next year. Emphasis should be laid on conquering the pandemic by prioritizing health care spending on vaccinations, treatments and health care infrastructure.

On monetary policy, Gopinath said that it should remain accommodative wherever inflation was well-balanced while financial stability risks should be tackled using macro-prudential tools.

The resilience and the much talked-about strong fundamentals of India’s economy will be tested rigorously over the next two to three-months.

However, one need not be too pessimistic as there are factors that could help India recover more rapidly than other economies globally.

For example, there are some economists who argue that the lockdowns presently are lighter than those imposed last year. According to them and this is very important as both businesses and consumers have by now managed to adjust to the new environment.

India has begun its vaccination programme and it was proceeding smoothly till very recently before news reports of vaccine as well as oxygen shortages started trickling in.

To successfully overcome the pandemic and perk up its economy, India needs to run its vaccination programme, amongst the biggest in the world, successfully. Thankfully, the government is taking several steps to tackle the emerging problems and resolve them promptly so as to keep the vaccination drive running smoothly.

With the vaccination now opened up to all above 18 years of age, it is expected that close to half the country’s population would be vaccinated by the end of this year. An eye needs to be kept on retail inflation, also known as Consumer Price Index (CPI)-based inflation, which has risen to 5.52% in March. This is the fourth consecutive month that retail inflation has come within the RBI’s upper margin of 6%.

The upward movement was influenced primarily by inflation in the food basket. While vegetable prices dipped (minus) 4.83% year-on-year (y-o-y) in March, prices of other items such as oils and fats, meat and fish, eggs, pulses and products and non-alcoholic beverag-es all moved northward.

Economically, India is presently poised on the edge - things can move either way - up or down, improve or deteriorate. After being in a very good position till end-March, things have slid southward precariously in the last one month.

India’s economic progress now hinges upon conquering the pandem-ic as swiftly and effectively as possible. Fortunately, India’s economic fundamentals are still robust. What is needed is for the government is to get its act together and for all citizens to co-operate with the government in suppressing the pandemiC.

BEYOND THINKING

India’s IPO market, which has been weak for the past few years, has seen a sudden resurgence with as many as six IPOs hitting the market in April of 2021 alone. This includes big names such as Macrotech Developers (formerly known as Lodha Develop-ers), Aadhar Housing Finance Ltd and KIMS Hospitals.

The IPO pipeline this year looks strong with 28 companies holding market regulator Securities and Exchange Board of India’s (SEBI's) approval for raising almost `30,000

than the `20,352 crore raised in 2019-20. In 2018-19, companies raised `14,719 crore through IPOs. And in 2017-18, companies mopped up `82,109 crore from initial share sale.

Last year was particularly good for the IPO market. Since July ’20, 13 big companies launched IPOs to raise funds. Three of these were subscribed more than 150 times. The biggest IPOs were Gland Pharma (about `6,480 crore), Indian Railway Finance Corporation (`4,633 crore), CAMS (`2,240 crore) and UTI Asset Management Company (`2,160 crore).

The issue of MTAR Technologies received the best response with a subscription of over 200 times. It was followed by Mrs Bectors Food Specialties at 198 times. Investors showed an appetite for stocks of

crore through the IPO route.

Fundraising through IPOs is at a 13-year high. There is a lot of interest from foreign and retail investors, which has made India one of the hottest IPO markets in the world today.

According to data from Refinitiv, a global provider of financial market data and infrastructure, Indian companies have raised $2.2 billion through IPOs this year. This is the highest amount since the blockbuster IPO year of 2008. And the year has only just begun.

The IPO resurgence started in 2020, with Indian companies raising $9.2 billion through share sale - the third biggest after the United States and China. In fiscal year 2020-21, 30 companies raised `31,277 crore through IPOs, significantly higher

THEBEELINERS

The IPO pipeline this year looks strong with as many as 28 companies looking to list on the bourses to raise funds

Beyond Market 16th - 30th Apr ’21 It’s simpli�ed...13

Beyond Market 16th - 30th Apr ’21 It’s simpli�ed...14

might be forced to list in the US because of the strict listing rules in India.

Media reports hint at Flipkart listing in the US in the fourth quarter of this year. Its listing in the US could value the company at more than $35 billion. Flipkart has not yet confirmed this and the company can list in another country as well.

In an attempt to encourage e-com-merce companies to list in India, SEBI has made changes to its Innovators Growth Platform (IGP). In 2019, SEBI created an alternative listing platform called IGP to enable start-ups to list their shares on stock exchanges. But the platform didn’t see any traction, prompting SEBI to make changes to its regulations.

SEBI has reduced the requirement for issuers to have 25% of pre-issue capital held by eligible investors to one year from two years. It has allowed start-ups to allocate up to 60% of the shares to be sold in the IPO to select investors on a discre-tionary basis before the issue opens to all investors. This provision is akin to the anchor allotment rule for companies floating IPOs on the main board of stock exchanges.

Companies looking at listing on IGP can issue shares with differential voting rights (DVRs) to promoters. SEBI has also proposed to increase the open offer trigger to 49% from 25%, giving more flexibility to start-ups.

Also, for loss-making companies, SEBI has reduced the requirement for migration from IGP to the main board from 75% of capital held by Qualified Institutional Buyers (QIBs) on the date of application to 50%.

Analysts say SEBI is trying to replicate the success of the American

The companies that have listed so far this year have done exceptionally well. According to data from Prime Database, 18 of the 23 IPOs this year saw first-day gains – 78% of stock listing in FY21. The number of stocks with first-day gains on debut has been the highest in three years.

Things are about to get even better. There is news of e-commerce giants launching IPOs. Flipkart, PolicyBa-zaar, Zomato, Ola, Freshworks, PepperFry, Nykaa and Delhivery have all declared their intention to go public.

But this may not be possible in India. SEBI has rules that make it difficult for loss-making companies to list on the Indian stock exchanges. The other problem is some of these start-ups are registered in Singapore, which makes it impossible for them to list in India.

India has 34 unicorns (valuation of $1 billion or more) as of February ’21. An HSBC Global Research report estimates that over $60 billion was invested in India’s internet sector in the last five years. Around $12 billion of this was invested in 2020 alone.

Start-ups have been booming in India thanks to the Covid-19 pandemic, which has increased the number of online buyers. In 2020, over 1,600 start-ups were founded, taking the total number of start-ups to over 12,500, according to a report by Nasscom. The trade body estimates that almost 55 of these start-ups are potential unicorns.

While many of these tech start-ups have reached over $1 billion in valuation, almost all of them are loss-making. This includes Walmart Inc-owned online retailer Flipkart Online Services Pvt and food-deliv-ery start-up Zomato Pvt Ltd, which

companies from diverse sectors from ready-to-eat food makers, broking firms to even biotechnology compa-nies.

The stock market’s bull run has improved sentiments among investors, leading to successful IPOs. Excess liquidity among global investors and optimism about the Indian growth story has also helped the IPO market.

Foreign investors have been pumping in huge amounts of money into India. As a response to the economic destruction that followed the Covid-19 outbreak, central banks all over the world released stimulus packages. And some of that money has come into the emerging markets, especially India. In January and February of this year, foreign investors invested $6.1 billion in India, the highest among all countries in Asia.

The IPO market has also received record levels of participation from individual investors. In January, new investors reached 51.5 million, showing an increase of 1 million every month from 39.5 million investors in January ’20. Indian investors have reposed faith in Indian companies, which is a big motivating factor for companies to go public.

This year, the big IPOs to watch out for are LIC, HDB Financial Services, NCDEX and ESAF Small Finance Bank. LIC is expected to raise around `70,000 crore to `1 lakh crore from the markets in October this year.

The other IPOs of interest are that of Nykaa and Bajaj Energy. Nykaa is looking at a stock exchange listing by the end of 2021 or early 2022 at a valuation of $3 billion. Bajaj Energy is expected to raise around `5,450 crore.

For free account opening, call on +91 022 62738000 | www.nirmalbang.com

Disclaimer: Insurance is a subject matter of solicitation. Mutual Fund investments are subject to market risks. Investment in Securities/Commodities market are subject to market risks. Read all the related documents carefully before investing. Please read the Do’s and Don’ts prescribed by the Commodity Exchange before trading. We do not offer PMS Service for the Commodity segment .The securities quoted are exemplary and are not recommendatory. NIRMAL BANG SECURITIES PVT LTD – BSE (Member ID- 498): INB011072759, INF011072759, Exchange Registered Member in CDS; NSE MEMEBR ID- 09391): INB230939139, INF230939139, INE230939139; MSEI Member ID-1067) : INB260939138, INF260939138, INE260939139: Single Registration No.INZ000202536,PMS Registration No: INP000002981; Research Analyst Registration No: INH000001766; NSDL/ CDSL: IN-DP-CDSL 37-99. NIRMAL BANG COMMODITIES PVT LTD – MCX (Member ID -16590 /NCDEX Member ID -0362 /ICEX Member ID -1165) : Single Registration No. INZ000043630; NCDEX Spot: 10084; Comtrack Participants: CPID -5040; CDSL Commodity Repository Ltd: 12013300 Nirmal Bang Securities Private Limited CIN:

U99999MH1997PTC110659; Nirmal Bang Commodities Private Limited CIN: U67120MH1995PTC093213Regd. Office: B-2, 301/302, 3rd Floor, Marathon Innova, Off Ganpatrao Kadam Marg,

Lower Parel (W), Mumbai - 400013. Tel: 62738000/01; Fax: 62738010

INFORMATIONTHAT

MATTERSThe BEYOND App provides stock-specific data like

Company Overview, Updated Financials, Key Ratios, Shareholding Patterns, Mutual Fund Holdings and

much more to help you take right investment decisions based on information that matters to you.

Download BEYOND App on

eyondP o w e r e d b y

Beyond Market 16th - 30th Apr ’21 It’s simpli�ed...15

Exchange - Nasdaq - through these changes. Nasdaq allowed US tech giants such as Google, Facebook, Apple, Amazon and Netflix to list as start-ups. These measures are intended to encourage start-ups to list in India.

It is anybody’s guess whether these measures will encourage start-ups to list in India. Indian start-ups might still prefer foreign markets, with a history of successful tech IPOs. Also, investors in India have a low

exposure to tech stocks. Many Indian companies are looking at listing in the US or Singapore because of their friendlier norms.

Compliance requirements are fewer in these markets, which makes it tempting for start-ups to list there. If the markets regulator SEBI can convince companies to list here, it would be a big win for them as well as the domestic investors.

Analysts expect the IPO market in

India to be strong for the next 2-3 years because of the domestic growth story. With the Sensex performing well, more and more companies are looking to raise money from the market.

Excess liquidity and better-than-ex-pected economic recovery have improved sentiments among foreign and retail investors. The current bullish IPO run might just continue to make money for companies and investors alikE.

BEYOND THINKING

SAME BUTDIFFERENT

While key rates have been left unchanged, the RBI has experimented with a few innovative tools to manage

liquidity in the system

Beyond Market 16th - 30th Apr ’21 It’s simpli�ed...16

Beyond Market 16th - 30th Apr ’21 It’s simpli�ed...17

Currently, CPI inflation stands at 5% for February rising from 4.1% in January ‘21.

Importantly, both upside as well as downside pressures on inflation prevail. Inflation may witness an upside pressure due to higher commodity prices and increase in logistics costs for goods and services.

On the other hand, inflation may see a downside due to lower global crude oil prices and normalization of global supply chains.

Better monsoons and higher food production will also limit the upside risks.

ECONOMIC GROWTHOUTLOOK

The RBI has projected India’s GDP growth for FY21-22 at 10.5%, reiterating its outlook from its February meet.

This has surprised many as India has been currently witnessing a surge in Covid-19 cases in recent weeks.

RBI’s outlook on the economy has factored in the impact of the pandemic. The second wave of the pandemic may not hurt economic growth much as the lockdowns are very selective.

Additionally, resilient rural demand and increase in vaccination will help economic growth.

Also, the RBI is optimistic that the

wording gives them more manoeuvrability in altering its stance in the future without any disruption to the markets, while still keeping an eye on inflation.

After all it is the mandate of the MPC to keep inflation measured by consumer price index (retail inflation) at 4% with a tolerance level of two percentage points on either side.

POLICY RATES

To achieve its inflation target of 4%, the MPC uses the repurchase rate (repo) as a tool and tweaks it when needed.

Repo rate is the rate at which banks borrow from the RBI during times of liquidity crunch.

This repo rate acts as a benchmark and influences other interest rates in the economy like banks’ lending and savings interest rates, corporate bonds, government bonds, etc.

Thus by tweaking the repo rate, the Reserve Bank ensures a stable interest rate environment in the financial system. Currently, the MPC has left the repo rate unchanged at 4%.

INFLATION OUTLOOK

The RBI expects CPI inflation to range between 4.1% and 5.2% in FY22. These projections are higher than what were estimated in earlier policy meets.

The Reserve Bank of India’s (RBI’s) six-member monetary policy committee left policy interest rates unchanged in its April meet. All members of the MPC decided unanimously on this. It was the first policy meet for the fiscal year 2021-22.

Importantly, the MPC has maintained its ‘accommodative’ stance. This implies that interest rates are not likely to rise in the near future.

However, the forward guidance on its accommodative stance has been worded differently this time.

Earlier, the MPC had guided to keep its accommodative stance well into fiscal year 2021-22.

Now, the forward guidance simply says that “the stance of monetary policy will remain accommodative till the prospects of sustained recovery are well secured while closely monitoring the evolving outlook for inflation.”

LESS DOVISH

Clearly, the RBI is not committing to any time frame now. The RBI will start increasing key rates once the economy shows signs of recovery. It need not wait for a stretch of period.

Market participants have taken the differently-worded forward guidance to be less dovish.

But from the MPC’s perspective, the

Repo RateReverse Repo RateMSFBank Rate

Key Policy Rates (%)

Feb '205.154.95.45.4

Mar '204.4

44.654.65

May '204

3.754.254.25

Feb '214

3.354.254.25

Apr '214

3.354.254.25

Source: RBI

Beyond Market 16th - 30th Apr ’21 It’s simpli�ed...18

government’s public capital expenditure programme, the production-linked incentive (PLI) scheme should support the Indian economy.

Having said thus, the Reserve Bank’s growth projections are more realistic than IMFs’, which has forecasted India’s FY22 economic growth at 12.5%.

REGULATORY MOVES

While policy rates remained unchanged, the RBI has announced a number of innovative measures to ensure that there is adequate liquidity in the system and availability of funds to critical sectors of the economy.

Secondary Market G-Sec Acquisition Programme Or G-SAP 1.0:

For the first time, the RBI has committed to purchasing a specific amount of government securities from the market through its open market operations.

Bonds worth `1 trillion are scheduled to be purchased in the April-June quarter of fiscal year 2022.

Earlier depending on the liquidity needs of the financial system, the RBI used to undertake open market operations.

Now, with G-SAP, the RBI will ensure lower volatility in the bond market, efficiently manage borrowing for the government and ensure stable interest rate scenario in the system.

The move has boosted sentiments in the bond market. G-SAP will complement other liquidity management tools.

VRRR (Variable Rate Reverse Repo) Auctions:

VRRR of longer maturity beyond the current 14 days will be conducted to manage liquidity.

This will help absorb surplus liquidity in the system and rein in volatility in the markets. The move kind of offsets G-SAP.

But here the RBI has made it clear that VRRR should not be seen as a liquidity-tightening measure. The amount and tenor of auctions under VRRR will be decided on evolving liquidity and financial conditions in the economy.

On-Tap LTRO Extended:

Given the impact of the Covid-19 pandemic, last year the RBI announced on-tap targeted long-term repo operations scheme as a tool to enhance liquidity and ensure credit availability to certain important sectors of the economy.

Under the scheme, banks and NBFCs can borrow one- to three-year funds from the RBI at the repo rate.

It is called targeted as the money so borrowed has to be mandatorily invested in corporate bonds, commercial papers, and non-convertible debentures or for direct loans to specific sectors. Now, the RBI has extended the scheme by six months till 30th September.

Ways And Means Advances Hiked:

Ways and means advances refers to

the short-term advances facility provided by the RBI to tide over temporary mismatches in the receipts and payments of the central and state governments.

Now, the RBI has increased the limit under WMA. Additionally, an interim limit of `51,560 crore set last year under WMA to help states and union territories in order to tide over the liquidity crunch due to the pandemic has been extended till 30th September.

IN A NUTSHELL

Clearly, the RBI is juggling with multiple objectives. On one side it has to ensure that inflation stays lower, on the other hand it has to support economic growth with ample liquidity.

It also has to manage the government’s borrowing programme without any disruption.

The RBI in its April policy has done well to change its time-based forward guidance to state-based. For now the state-based guidance provides some continuation, ensuring lower policy interest rates. But future course will be data-dependent.

Eventually, the RBI will have to start adjusting the reverse repo rate higher.

The timing will depend on impact of the second wave of the pandemic on the economy, international commodity prices, inflation numbers and global currency markets, among other things. The next meeting of the MPC is scheduled during June ’21.

GDP GrowthCPI Inflation

RBI's Outlook

Q1 FY2226.21

5.2

Q2 FY228.35.2

Q3 FY225.44.4

Q4 FY226.25.1

FY2210.5

Source: RBI

BEYOND THINKING

Covid-19 has changed individual preferences like never before. People

CY18. But in CY19 savvy investors began looking at pharmaceutical and health care companies as value picks. In the time after Covid-19 pandemic, these companies became the top favourite of many investors and the stocks zoomed. From the bottom of 4,597 recorded on 23rd Mar ’20, the Nifty Healthcare TRI zoomed 93.21% till 13th Apr ’21.

Though the returns appear impres

have begun valuing their health over other areas of their lives even since the coronavirus pandemic struck nations around the world and brought economies to their knees, subse-quently benefitting health care and pharmaceuticals companies, which are poised for growth from a long-term perspective.

Not long ago, the valuations of many pharma companies were down in

SORENO

MORE

The coronavirus pandemic is showing no signs of slowing down, aiding the growth of stocks in the health care space, which till some time back were performing badly

Beyond Market 16th - 30th Apr ’21 It’s simpli�ed...19

Beyond Market 16th - 30th Apr ’21 It’s simpli�ed...20

There will be large investments in this sector – both public and private. These investments will throw open many opportunities for investors.

The Covid-19 pandemic also underlined the role co-morbidities play in our health and treatment protocols to be followed. Ignorance or the inability to manage health conditions has been an expensive proposition for many.

Going forward, there will be more awareness and many individuals will demand better diagnostic services as ‘prevention’ takes greater importance in the ambit of overall health care services. Hospitals and drug makers will also benefit in the process.

One big beneficiary of the Covid-19 shock has been health insurance companies. Individuals began realizing the need for health insurance. Though there are no standalone health insurers available for investing in, the stocks of non-life insurers would nevertheless benefit from increased demand.

Many pharmaceutical companies have of late invested a lot in the wellness vertical. This is an upcom-ing business. As lifestyle diseases catch up, there will be a huge section of the population that would look forward to wellness products and services.

While offering these products, wellness companies would be able to enjoy better pricing power given the brand premium. Health supplements and similar such products may help these companies enjoy the predicta-bility of demand, and thereby earnings too. Hence, such companies should also benefit from better valuations.

Going forward, expect some initial public offerings (IPOs) from the

caution to the wind. The government and regulatory bodies are monitoring the situation actively. Signs of super-normal profits will attract restrictions and price control at various levels.

For example, the government of Maharashtra has advised measured usage of Remdesivir only when required. The Central government has also banned the exports of the drug after its shortages were reported in the country.

The government had already defined the cost of Covid-19 treatment packages in various parts of the country. This approach should ensure that the companies are not allowed to make outsized profits.

In the medium- to long-term, the Indian pharmaceutical business will be driven by domestic and export demand. Covid-19 pandemic has disturbed many supply chains across the world.

Though multinational companies looked at China as the preferred destination for manufacturing, the search for another country to build manufacturing facilities has begun. India is expected to benefit from this search.

Some of the pharma manufacturing is expected to come to India. And Indian companies may get some opportunities in the ‘contract manufacturing’ space. Exports of ‘Made in India’ drugs can be a growth driver to the sector.

As far as domestic growth is considered, the demand for health care is expected to be strong. The Covid-19 situation has exposed our vulnerabilities. Although India is the world’s second-fastest growing economy in the world, it scores poorly in health infrastructure.

sive, they are not linear, especially if one looks at the recent past. After the economy started to open up, the investors shifted from defensive stocks (such as pharmaceuticals) to cyclical stocks (such as banking) after September ’20.

Nifty Healthcare TRI lost 3.87% and 6.07% in the month of October ’20 and January ’21, respectively. Though the index sprung up and regained lost ground, investors need to take a serious relook at the sector before committing fresh money to it.

In the short term, it is investors’ sentiments that matter. If we are staring at a second wave of Covid-19 infections and further restrictions or lockdown in Maharashtra and various parts of the country, there may be a change in investor prefer-ence.

Some investors may want to cut their exposure to cyclical stocks like banking and capital goods, and shift to defensive stocks such as pharma-ceuticals and information technology (IT) sectors.

When money flows from one sector to another, it supports stock prices. But the earnings of the companies are more reliable factors while making investment decisions.

In the short term, there will be increased demand for diagnostics services, drugs and other health care services. Though there is not much of a vaccine play here in India, barring Dr Reddy’s Laboratories, investors can still expect increased demand for health care services – including health insurance, among other things. Indian pharmaceuticals and health care companies should see some increase in earnings in the second wave of Covid-19.

However, investors should not throw

It’s Simplified

For free account opening, call on +91 022 62738000www.nirmalbang.com

powered by

Disclaimer: Insurance is a subject matter of solicitation. Mutual Fund investments are subject to market risks. Investment in Securities/Commodities market are subject to market risks. Read all the related documents carefully before investing. Please read the Do’s and Don’ts prescribed by the Commodity Exchange before trading. We do not offer PMS Service for the Commodity segment .The securities quoted are exemplary and are not recommendatory. NIRMAL BANG SECURITIES PVT LTD – BSE (Member ID- 498): INB011072759, INF011072759, Exchange Registered Member in CDS; NSE MEMEBR ID- 09391): INB230939139, INF230939139, INE230939139; MSEI Member ID-1067) : INB260939138, INF260939138, INE260939139: Single Registration No.INZ000202536,PMS Registration No: INP000002981; Research Analyst Registration No: INH000001766; NSDL/ CDSL: IN-DP-CD-SL 37-99. NIRMAL BANG COMMODITIES PVT LTD – MCX (Member ID -16590 /NCDEX Member ID -0362 /ICEX Member ID -1165) : Single Registration No. INZ000043630; NCDEX Spot: 10084; Comtrack Participants: CPID -5040; CDSL Commodity Repository Ltd: 12013300 Nirmal Bang Securities Private Limited CIN: U99999MH1997PTC110659; Nirmal

Bang Commodities Private Limited CIN: U67120MH1995PTC093213Regd. O�ce: B-2, 301/302, 3rd Floor, Marathon Innova, O� Ganpatrao Kadam Marg,

Lower Parel (W), Mumbai - 400013. Tel: 62738000/01; Fax: 62738010

Beyond Market 16th - 30th Apr ’21 It’s simpli�ed...21

health care sector to help investors further diversify their investments. For example, over the last few years, we have seen notable listings of stocks of companies that are operating in the field of diagnostics.

However, investors are still waiting for listed investment options such as stocks of companies in health care technology, medicine distribution, and health insurance.

Investors will be better off investing in the health care sector after

studying global trends. The global health care system is driven more by technology. There are substantial investments in health care technolo-gy, which has led to economies of scale and better margins at various levels of health care delivery.

Indian investors can take advantage of these by investing in a few of the global names by routing some of their money through dedicated health care mutual fund schemes that are investing overseas or on their own.Though stock-specific investment

opportunities always exist, investors need to understand that valuations are stretched for the health care sector. Investors cannot simply rely on past performance of stocks to commit their money towards such investments.

Typically, sectors take some time to consolidate before making further upmove. Therefore, investors have to look at the health care sector with moderate expectations of returns in the future and with a relatively long-term vieW.

BEYOND THINKING

TROLLS ONA ROLL

Minor slights are enough for trolls to unleash their wrath

on brands, and companies as well as advertisers are

growing wary of cyber bullies

Beyond Market 16th - 30th Apr ’21 It’s simpli�ed...22

Beyond Market 16th - 30th Apr ’21 It’s simpli�ed...23

prash, with the power of more than 40 herbs like Ashwagandha, Giloy and Amla has always stood for boosting immunity to fight illnesses. Akshay Kumar is emblematic of health, fitness, and inner strength, the properties of Dabur Chyawanprash.”

In December ’20, Dabur India announced Akshay Kumar as the new face of its flagship health supplements brand Dabur Chyawan-prash.

The irony of the situation was not lost on netizens who trolled the brand and the actor for its Covid-protection claims.

NETIZEN TWEETS

A user said on Twitter ‘#Akshay Kumar tests positive, unfortunately, the #Dabur #Chyawanaprash didn’t help’

Another user tweeted “Don’t fall for #Covid19 immunity ads, masks, and social distancing would keep you safe. #Dabur”

A section of netizens also slammed the actor and the company for being reckless while promoting products with Covid-protection claims.

REPERCUSSIONS

Netizens didn’t spare ad regulator the Advertising Standards Council of India (ASCI) either and dragged it into a controversy and asked whether action will be taken against the company and the actor for making such claims.

Will the advertising council now make the actor announce that he doesn’t consume the product is what needs to be seen.

As soon as the news of Kumar’s Covid positive status and his

Not only companies and brands, even celebrity brand ambassadors have to face criticism from tech-savvy consumers. Dabur India’s advertising campaign promoting its immuni-ty-boosting product Chyawanprash was trolled on social media after its brand ambassador Akshay Kumar announced that he had tested positive for Covid-19.

While other actors and celebrities mostly get sympathy on social media after announcing that they have tested Covid positive, Kumar on the contrary, was trolled heavily.

The advertisement of Chyawanprash had claimed that it offered protection against coronavirus by boosting immunity. In the advertisement, Akshay Kumar is seen holding a bottle of Chyawanprash while claiming that just two teaspoons of chayawanprash daily was enough to ward off the virus as it boosted immunity to fight against the virus. The copy of the ad read: “According to a clinical study conducted across five centres, Dabur Chyawanprash helps in protection against Covid-19.”

After Kumar announced that he had tested positive for coronavirus, netizens asked whether Kumar himself was consuming Dabur Chyawanprash at all or if the product’s efficacy tests were fabricated. Netizens questioned the authenticity of the claims made in Kumar’s advertisement for Dabur Chyawanprash.

Mohit Malhotra, Chief Executive Officer, Dabur India during the launch of the ad had said, “The times we are living in today have under-lined the need for and importance of immunity more than ever before. Strong immunity is the need of the hour with the threat of illnesses looming around us. Dabur Chyawan-

As the reach of the internet has deepened, brands have been struggling to cope with trolling by new-age tech-savvy consumers over the last two years.

Gone are the days when companies could happily get away with tall claims they made while advertising their products through certain punch lines or by highlighting a few benefits that may or may not be true.

With the arrival of social media and alert consumers, things have become difficult for companies. And making tall claims is just not enough to gain customer loyalty.

According to experts, companies are walking on eggshells while deciding their advertising and branding strategies as any slight dissatisfaction will result in trolling by 100s and 1,000s of disgruntled consumers, severely impacting a brand’s reputation.

Even a renowned and an old brand may have to face the wrath of its consumers for misleading them or creating controversial ads.

ADS TROLLED

Tata-owned Tanishq had to endure a backlash in 2020 on social media for its advertisement featuring an interfaith couple. The brand had to face the wrath of netizens who trolled it massively on social media, and the company was forced to finally pull off the ad.

Beyond Market 16th - 30th Apr ’21 It’s simpli�ed...24

subsequent hospitalization came out, Dabur had to pull off its ad from TV because the advertisement and its product Chyawanprash were both being heavily trolled on social media.

After Kumar’s Covid-19 positive reports, the Advertising Standards Council of India took cognisance of the matter and has asked Dabur to reply to the claim made in its advertisement.

This is not the first time when a celebrity or a brand has been trolled on social media for a similar blunder. A few months ago, Sourav Ganguly suffered a heart attack when his fans started massively trolling Ganguly the Brand Ambassador of Fortune Rice Bran Oil, which later had to be removed from TV commercials.

In the second ad, Ganguly was seen saying that he may have suffered a heart attack due to family history and he used the oil to adopt a healthy lifestyle.

As mentioned earlier, Tata-owned Tanishq had to pull off its ad last year for its advertisement featuring an interfaith couple.

COPING WITH TROLLS

Social media trolling is common and is no longer a marketing depart-ment’s problem alone. With heavy trolling by netizens for misleading ads or claims, companies have had to rethink ways to manage such situations as it can heavily damage brands, impacting sales.

During a crisis, brands have had to lay out a prioritization roadmap for responses from various executive levels going up to the Chief Execu-tive Officer, according to brand guru Harish Bijoor.

As per industry experts, even after

vaccinations people are getting infected with Covid. Hence, tall claims of brands about offering protection or immunity against coronavirus honestly do not stand a chance.

However, legal action is not possible against these brands or companies as these ads are mere claims and are not a guarantee offered by the brands. Legal action is only possible on brands when they offer some kind of guarantee on the product.

When companies say that their ad is 99.99% correct, such percentage also amounts to claims. However, if the research behind the claim is false, a case can be made in the consumer court. The Central Consumer Protection Authority can impose a fine of `10 lakh and jail for two years against advertisers who make false claims, cautioned experts.

The ASCI recently said that lately there has been a surge in misleading ads during the Covid-19 pandemic. Several products have had to change their packaging and labeling after complaints were filed against them.

COUNTERING NEGATIVE PUBLICITY

After Ganguly suffered a heart attack that resulted in an angioplasty, the internet was filled with memes mocking Ganguly’s association with Adani Wilmar’s Fortune Rice Bran Oil, which claimed to strengthen heart health.

Soon after Sourav Ganguly was discharged from hospital following his second angioplasty, Fortune Rice Bran Health Oil was back with a new ad featuring Ganguly.

In the print ad, released on Valentine’s Day, Ganguly assured his fans that his “heart is just fine,” and

urged people to take good care of their heart health.

The ambassador of a brand that positions itself as ‘heart-healthy oil’ suffering a heart attack is nothing short of a nightmare. Will the new ad help control the damage done to the brand’s reputation or could the brand manager have handled the situation any differently?

Ganguly was named as the brand ambassador of Adani Wilmar Ltd’s (AWL) Fortune Rice Bran Health Oil in January 2020. Since 23rd Oct ’19, he has been President of the Board of Control for Cricket in India (BCCI).

Fortune oil positions itself as the healthy oil for the 40-plus age group. This was a keenly contested segment with many competitors including Saffola Oil, a Marico Ltd brand. Fortune came out with an advertise-ment with the tagline “Dada bole (says) welcome to the 40s.”

The company also used the hashtag #WelcomeToThe40s. In the televi-sion commercial, it clearly states that the Fortune Rice Bran Health cooking oil has Gamma Oryzanol, which increases good cholesterol and reduces bad cholesterol, and as a result, keeps the heart healthy. Towards the end, Ganguly says, “Fortune Rice Bran Health is healthier than healthy oils.”

On 7th Apr ’20, Ganguly shared the ad on Twitter: “Yes, you can live your life to the fullest even in your 40s. Just have to play it smart. Make sure you’re taking care of your heart and immunity. It starts with your oil. Switch to an oil that cuts bad cholesterol and increases good cholesterol. An oil that boosts your immunity.”

But as luck would have it, on 2nd Jan ’21, Ganguly complained of chest

Beyond Market 16th - 30th Apr ’21 It’s simpli�ed...25

pain during his regular workout and doctors said he had suffered a mild heart attack and had to undergo angioplasty. The news came as a shock to cricket fans as he is just 48 years old, and known to maintain a healthy lifestyle.

Following this health scare, the Fortune brand faced a backlash across all social media platforms. Netizens questioned brand endorse-ments and if celebrities even used the products they endorsed. To add the

its woes, soon news surfaced that another angioplasty was performed on 28th Jan ’21, after Ganguly complained of chest pain on 27th January, leading to a crisis for AWL.

Industry observers pointed out that far too many brands have found themselves in similarly sticky situations, and, in most cases, the brand ambassadors were just dropped.

Indian cricketer Yuvraj Singh was the

first brand ambassador for Revital H Capsule but the company replaced him with actor Salman Khan after the cricketer was diagnosed with lung cancer.

In the year 2020, Dabur Chyawan-prash replaced actor Amitabh Bachchan with another actor Akshay Kumar after Bachchan contracted coronavirus. Ironically, Akshay Kumar himself tweeted that he tested positive for Covid after a few monthS.

We help you get your money’s worth without letting volatility

in the markets reduce its value.

Worth It!

eyond P o w e r e d b y

11:15

12:40PM 80%

eyond

Download BEYOND App on

For free account opening, call on +91 022 62738000 | www.nirmalbang.com

Disclaimer: Insurance is a subject matter of solicitation. Mutual Fund investments are subject to market risks. Investment in Securities/Commodities market are subject to market risks. Read all the related

documents carefully before investing. Please read the Do’s and Don’ts prescribed by the Commodity Exchange before trading. We do not offer PMS Service for the Commodity segment .The securities

quoted are exemplary and are not recommendatory. NIRMAL BANG SECURITIES PVT LTD – BSE (Member ID- 498): INB011072759, INF011072759, Exchange Registered Member in CDS; NSE MEMEBR

ID- 09391): INB230939139, INF230939139, INE230939139; MSEI Member ID-1067) : INB260939138, INF260939138, INE260939139: Single Registration No.INZ000202536,PMS Registration No:

INP000002981; Research Analyst Registration No: INH000001766; NSDL/ CDSL: IN-DP-CDSL 37-99. NIRMAL BANG COMMODITIES PVT LTD – MCX (Member ID -16590 /NCDEX Member ID -0362

/ICEX Member ID -1165) : Single Registration No. INZ000043630; NCDEX Spot: 10084; Comtrack Participants: CPID -5040; CDSL Commodity Repository Ltd: 12013300 Nirmal Bang Securities Private

Limited CIN: U99999MH1997PTC110659; Nirmal Bang Commodities Private Limited CIN: U67120MH1995PTC093213

Regd. O�ce: B-2, 301/302, 3rd Floor, Marathon Innova, O� Ganpatrao Kadam Marg, Lower Parel (W), Mumbai - 400013. Tel: 62738000/01; Fax: 62738010

BEYOND THINKING

SHAPING THE FUTUREOF ENTERTAINMENT

New mediums are overtaking the old in unimaginable ways in the media and

entertainment industry in a bid to survive the impact of Covid-19

Beyond Market 16th - 30th Apr ’21 It’s simpli�ed...26

Beyond Market 16th - 30th Apr ’21 It’s simpli�ed...27

Another key factor that will have a severe impact on the industry’s revenues is big film stars contracting coronavirus. This means that the industry will not only suffer on the production side but also on the distribution side. TELEVISION India’s television industry was relatively less impacted in 2020 as the coronavirus-induced lockdown resulted in increased viewership for television.

As per the FICCI-EY report, television advertising in 2021 is expected to be close to 2019 levels. It is likely to grow over 20% to reach `30,400 crore on the back of a line up of fresh sports content, regional channel rate increases and continued growth of free television.

The report observes that subscription income would grow 5% to reach `45,600 crore owing to fresh content, several marquee sports events and pending movie releases.

The television segment’s revenues are expected to grow at a compound annual growth rate (CAGR) of 7% to reach `84,700 crore by 2023 driven by increased base of subscribers as households continue to get televised and TV’s price competitiveness as against [OTT + data] alternatives, notes the FICCI-EY report. One of the key changes expected from television in 2021 is that the segment will focus more on mass content, and, hence, mass audience. The report observes that television content - especially paid television content - will continue to grow marginally as states like UP, Bihar, Rajasthan and West Bengal get electrified.

It is estimated that easily available

producers. The FICCI-EY report states that the value of broadcast rights fell 68% due to fewer complet-ed new films and business caution by broadcasters.

Digital rights consequently grew 86% to reach `3,540 crore as films were released directly on to the streaming platforms at rates, which compensated producers (wholly or in part) for lost theatrical revenues. At least 15 Hindi films were released on streaming platforms. It started with the direct release of Gulabo Sitabo on Amazon Prime Video. Besides, films such as Dil Bechara, Sadak 2, Laxmii and Coolie No.1 were also released there.

Netflix, Disney+Hotstar and Amazon Prime Video had the biggest market share in India for the direct release of such movies.

The report notes that industry and internet search data indicate that direct-to-digital releases did result in a spike in viewership on streaming platforms, especially in smaller towns and cities. But this impact was not uniform across platforms.

According to industry experts and analysts, producers will continue to prefer a theatrical release window to optimize the revenue-generating potential of marquee film products. But in 2021 these trends may not transpire. A large number of films released on streaming platforms failed to attract new eyeballs and subscriptions. This is one of the reasons why streaming platforms are cautious about buying new films. Also, prolonged lockdown will make it difficult for producers to release films in theatres in 2021 also.

This means that producers will have to postpone the release of films.

India’s entertainment industry is going through a delicate phase. The long-stretched pandemic has thwarted almost every hope for the industry to return to normalcy.

Year 2021 started on a promising note with many expecting people to throng crowded places like movie theatres following the discovery of the vaccine to treat coronavirus,

But the second wave of the coronavi-rus pandemic seems to have squashed all such hopes. So, how different is 2021 from 2020? The recently released annual report on the media and entertainment industry by FICCI-EY reveals more about the status of the sector.

Let us understand the implication of the coronavirus pandemic on three key segments, namely, films, television and digital media. FILMS Prolonged lockdown has dashed hopes of recovery in business for the film industry. In 2020, around 441 films were released in comparison with 1,833 in 2019. This was due to lockdown and social distancing.

According to the FICCI-EY report, “Filmed entertainment segment saw an 80% decline across domestic and international theatrical revenues.”

In this situation, streaming platforms emerged as the last resort for

Beyond Market 16th - 30th Apr ’21 It’s simpli�ed...28

broadband services provided either through telecommunications firms or private internet service providers will boost the growth of television sets in areas beyond tier-II cities.

Overall TV connections will keep growing at a healthy pace of over 5% per year to cross 71% of Indian households by 2025.

There is another fundamental factor, which will make content on TV massy and escapist. The report notes that most top-end subscribers opt for smart and connected television sets. This will change the demographics of the universe of TV audience. The socio-economic status of the audience available to watch televi-sion will lower.

It is believed that audiences, which opt for free television bouquet channels, will cross 150 million by 2025. Hence, the report states, “We expect content on television will adapt to become more escapist and mass in nature. This fact can help control the increase in average content costs for television program-ming, though marquee/ tent-pole programmes and reality shows will always have their place.”

Low-budget direct-to-television films as well as low-cost content created by news channels are expected to distinguish one channel from another.

In the coming months, regional television will drive advertising rate growth. It is observed that companies like Zee have already started producing defined offerings for its regional audiences.

This will be driven by the increase in regional content consumption on TV to 60% of total TV consumption improved quality and higher quantity of content on regional channels.

The report notes that for television subscriptions to grow it would need to remain cost-efficient as compared to the price of the streaming platforms. It notes, “The impact of data prices and bundling of popular streaming platform packages will be the benchmark against which television subscription will need to be maintained.” A key segment in which competition is expected to be stiff is sports events. The report highlights that the move of sports events to prime time - through day-night matches and evening scheduling - can impact general entertainment viewership. It emphasizes on the fact that having a sports product in the bouquet will become increasingly important for broadcasters. The report foresees the emergence of an era of “connected consumption.” Connected televisions will change the way people consume content. It will help people interact with each other from their homes while viewing content.

The report states, “We expect to see several innovations around connect-ed TV content: live chats between viewers, live polls and contests, play-along games (specially around sports) with real-time leader boards and challenge-a-friend formats to enable community interactivity, TV content with live interactive elements (singing/ dancing/ quizzing).” Lastly, the report foresees newer ways of monetization of already existing content libraries in the coming months. Television channels are likely to collaborate and produce content not only to appear on channels but also on their own streaming platforms. These channels will also sell content to other streaming platforms and make money.

DIGITAL MEDIA The digital media is expected to record high growth in 2021. It must be noted that the segment became the second largest in 2020, overtaking print. The report expects the segment to grow to `42,450 crore by 2023, growing at a CAGR of 22%.

The report says, “We expect digital media to continue to reduce the gap with television as digital infrastruc-ture (screens, broadband connections, e-commerce, digital payments, etc.) continues to grow. The demand for original content will double by 2023 from 2019 levels to over 3,000 hours per year. Curated short video platforms will garner 25% of the total time spent on online video viewing by 2023.” Besides, the report says the share of regional language consumption on streaming platforms will cross 50% of the total time spent by 2025, easily surpassing Hindi at 45%. Sports will play a key role in growing subscrip-tion revenues, leading to a growth in valuation of digital media rights. Given these facts, it is clear that not all segments of India’s media and entertainment industry will be impacted in 2021. This is not the situation in other industries, which offer non-essential services.

In the coming months, it is quite clear that value growth in subscrip-tions will be more in digital media than in print and television. A key reason for this is: tastes of audiences are changing.

Today, audiences have clear and specific expectations. For content producers to succeed in the coming months, how well they score on meeting audiences’ specific expecta-tions will determine their sustenance and growtH.

BEYOND THINKING

‘Don’t live beyond your means’ is an old adage, which is highly relevant in financial management. This simple statement highlights an important facet of achieving financial freedom, that is, having control over one’s finances to be able to lead a financially responsible life. This in no way deters individuals from

inflows, the total debt should be within acceptable limits.

Furthermore, one should have the repayment discipline, which means that a person should adhere to the payment schedule so that it doesn’t tarnish his/her credit history.

Despite knowing the evils of living beyond one’s means, individuals do often fall into the debt trap at times owing to lack of discipline and indulgences. And in some cases due to an emergency that may have wiped off their savings.

resorting to borrowings or taking on debt.

In fact, in many ways, debt or borrowings if accessed in the right proportion can help individuals achieve their lifetime goals such as buying a house or upgrading their skills by enrolling in an educational programme.