INVESTOR PRESENTATION - First Abu Dhabi Bank

55

INVESTOR PRESENTATION May 2021

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of INVESTOR PRESENTATION - First Abu Dhabi Bank

INVESTOR PRESENTATION

May 2021

FAB in brief

2

FAB in brief 3

The UAE’s leading bank, and one of the world’s largest and safest financial

institutions

Investor Presentation May 2021

ESG Leader

All figures as on 31 Mar 2021

256USD Bn

Total Assets

941AED Bn

Largest UAE Bank

2nd Largest in the MENA

43USD Bn

Market Cap

159AED Bn

Dominant and Diversified banking franchise

Strategic international presence

> 30% Market Share(by assets)

141%LCR

13.7%CET1

Robust Foundation 29.6%CI ratio

(ex-integration

costs)

12.8%RoTE

Superior Returns AA MSCI

ESG

Strongest Combined

Credit Rating in MENA

AA- Credit

Rating

Moody’s / S&P / Fitch

Market Heavyweight

Among top #50 largest banks

in the world

Largest UAE constituent in

global EM & ESG equity indices

FAB in brief 4

The safest and strongest bank in the Middle East

Investor Presentation May 2021

1 Global Finance Magazine safest bank rankings, October 2020

2 The Banker’s 2020 Top 1000 World Banks Rankings, July 2020

MOODY’S S&P Fitch

LT Aa3 AA- AA-

ST P-1 A-1+ F1+

Outlook Stable Stable Stable

Strongest combined credit ratings

amongst any other bank in MENA

Recognised as one of the safest and strongest banks worldwide

in UAE & Middle East

in Emerging Markets

Safest Commercial Bank Worldwide

#1

#4

#16

#1in UAE

by Tier 1 capital strength

#85Worldwide

by Tier 1 capital strength

Safest banks’ rankings by Global Finance1 Top 1000 banks’ rankings by The Banker2

#2in Middle East

by Tier 1 capital strength

#109Worldwideby Total Assets

MSCI ESG

AAHighest ESG-

rated bank in

UAE & MENA

FAB in brief 5

Leading UAE and regional bank

Investor Presentation May 2021

1 Central Bank information as of the latest available data; Assets are gross including provisions

2 Company information as of 31 Mar 2021, unless specified otherwise

3 Defined as the largest bank in the country by total assets

4 Based on 31 Mar 2021; Source Bloomberg

868

794

456

240

206

94

UAE

Qatar

KSA

Kuwait

Oman

Bahrain

Banking sector assets1

(USD Bn)

National

champion2,3

0.7

0.9

0.9

0.3

0.5

Q1’21

Net Profit2

(USD Bn)

256

159

284

99

28.0

22.2

25.5

13.6

Total Assets2

(USD Bn)

Equity2

(USD Bn)

Market Cap4

(USD Bn)

43.4

42.5

45.0

19.0

6.9

3.6

Credit Ratings4

(Moody’s/S&P/Fitch)

Aa3 / AA- / AA-

A1 / BBB+ / A-

Aa3 / A / A+

A1 / A / AA-

NA / BBB / BB+

Ba3 / B+ / BB-

40 5.0

SNB

QNB

NBK

AUB

Bank Muscat

FAB

0.1 33 5.2

(FY20)

FAB in brief 6

Globally outstanding rating and returns

Investor Presentation May 2021

Notes: Based on the available financials on Bloomberg, RoTE for peer banks are estimated as: {net attributable profit less Tier-1 interest or Coupon payable on capital securities} / [average tangible equity]; ^Banks in the above peer group have

different financial year endings; FY ending other than 31-Dec are highlighted with special characters: * for 31-Mar; ** for 30-Jun; *** for 30-Sep & **** for 31-Oct; Source: Bloomberg

FAB is amongst the most profitable AA- rated banks globally

BB+ BB

Composite Rating

Re

turn

on

Ta

ng

ible

Eq

uit

y (

%)

Western banks

GCC banks

APAC banks

StanChart

Lloyds

Barclays

HSBC

UBS

Credit Suisse

Deutsche Bank

ING

BNP

Credit Agri

GS

Morgan Stanley

Citigroup

BofA

JP Morgan

RBC****

Scotia****

BMO****

TDBank****

Nordea

Swedbank

Handelsbanken

Nomura*

Sumitomo*

Mizuho*

MUFG*

ANZ***

CBA**

NAB***

Macquarie*

Westpac***

OCBC

UOB

DBS

ICBC

Bank of China

Agri Bank China

Ind. Bank of Korea

Woori Bank

ICICI* State Bank of India*

HDFC Bank*

ENBD

ADCB

QNB

Doha Bank

CBQ

Al Rajhi

NCB

Saudi Fransi

KFHNBK

0%

5%

10%

15%

20%

25%

A+AA-AAAA+ A A- BBB+ BBB BBB-

FAB in brief

86% 14%

7

Diversified franchise with strategic international presence

Investor Presentation May 2021

76% 24%

Revenue Profit after taxes

Loans Deposits

72% 28%74% 26%

Revenue Profit after taxes

Q1’21 Q1’21

Loans Deposits

81%

19%

UAE International

83%

17%

1 All figures as of 31 Mar 2021 / Q1’21 financials

Breakdown by Business Breakdown by Geography

69% 33%

-2%

Corporate & Investment Banking Personal Banking Group HO & Subsidiaries

Q1’2183%

22%

-6%

Q1’21

FAB in brief 8

Strategic international network to facilitate inward/outward liquidity, trade

and investment flows

Investor Presentation May 2021

All figures as on 31 Mar 2021

1 Full Time Employees, excludes outsourced staff

2 includes Ratibi (Wages Protection System) and E-dirham customers

France

UK

Switzerland

USA

Brazil

UAE

Bahrain

Egypt

Kuwait

Libya

Oman

Saudi Arabia

Europe, Americas, Middle East & Africa (EAMEA) Asia Pacific (APAC)

China/Hong Kong

India

Indonesia

Labuan (Malaysia)

Singapore

South Korea

5Continents

Global presence

72Branches/ Cash

offices in UAE

406ATMs/CDMs in UAE

5,032Employees

globally (FTEs1)

>3 MillionUAE Customers2

The above map summarises market presence for FAB and its subsidiaries, where the Group currently has active operations; For information about legal presence please refer to Notes #1 and #23 of Mar-end 2021 financial statements

FAB in brief 9

A market heavyweight

Investor Presentation May 2021

1. Based on closing prices as of 31 Mar 2021 and Q1’21 financials, where applicable

2. Free float designates FAB shares available for purchase in public equity markets which are not strategic in nature

Strong shareholding3

• Listed on Abu Dhabi Securities Exchange (ADX)

• Symbol: FAB, ISIN: AEN000101016

• Market capitalisation: AED 159Bn (USD 43Bn)

(Amongst the top 50 banks globally)

• No. of shares issued: 10,920Mn

• Foreign Ownership Limit (FOL): 40%

• Free Float2: 44%

• Valuation multiples (based on Q1’21 financials)

Overview1

P/TE – 16.7x I P/TB – 2.2x I D/Y – 5.1%(2020 dividend)

ADIC PJSC, 33.3%

Mamoura Diversified Global Holding PJSC, 3.7%

Abu Dhabi Ruling Family, 15.4%

Other UAE Entities/Individuals 31.5%

GCC (ex-UAE) 1.5%

Foreigners (ex-GCC), 14.7%

MIC,

37.0%4

5

Index1 Ticker Weight%

Abu Dhabi Securities Market ADSMI 37.66%

MSCI Emerging Markets(Pro forma weight post MSCI semi-annual review effective 27 May 2021)

MXEF 0.21%

FTSE Emerging Markets FTAG01 0.22%

MSCI EM ESG Leaders M1EFES 0.25%

FTSE 4 Good Emerging Markets (ESG) F4GEM 0.51%

2017 2018 2019 2020

Cash Dividend6(AED Mn) 7,628 8,064 8,081 8,081

Cash Dividend (fils per share) 70 fils 74 fils 74 fils 74 fils

Payout ratio7 73% 70% 68% 80%3. Shareholding percentage based on outstanding shares (net of 8.4Mn treasury shares) as of Mar-end 2021

4. Through its 100% owned subsidiaries ADIC PJSC and Mamoura Diversified Global Holding PJSC (formerly known as Mubadala Development

Company PJSC); MIC (Mubadala Investment Company) is 100% owned by the Emirate of Abu Dhabi

5. Members of/companies owned by the Abu Dhabi ruling family: Each investor (natural of legal person) within this group, owns less than 5% of

the company’s shares, and is free to buy or sell FAB shares

6 Total Dividends = Dividends per share x Number of shares issued

7 Payout ratio: Cash dividends as a percentage of net attributable profits (Net profit after minority interest less coupon on Tier-1 capital notes)

The largest constituent on ADX, UAE’s largest and one of the largest MENA

constituents on Emerging Markets and ESG indices

Delivering superior and sustainable shareholder returns

60

80

100

120

140

160

Apr-17 Oct-17 Apr-18 Oct-18 Apr-19 Oct-19 Apr-20 Oct-20 Apr-21

FAB ADX MSCI EM Banks Rebased to 100

FAB in brief 10

FAB took decisive actions in response to COVID-19Prioritising the welfare of our employees, customers and the community at large

Investor Presentation May 2021

Business Continuity

• Activation of Work From Home (WFH) for 90%

employees1 and Return to Work (RTW) plan

for 30% employees

• Retail branches 100% operational since 2nd

Jan 2021

• IT infrastructure scaled up to accommodate

WFH

• Use of cloud-based virtual desktop capabilities

• Enhanced cybersecurity, fraud prevention and

monitoring

We continued to operate with a robust

Business Continuity & Crisis Management

Plan enabling the bank’s functions to operate

with speed and efficiency

Employees

• Flexible working policies implemented

• Weekly PCR testing organised for staff

• Tie up with health authorities to provide

COVID-19 vaccines to employees

• Self declaration portal for vaccinated staff

• Tele/Video doctor consultations

• Employee wellbeing programmes

• Extensive sanitisation measures across our

facilities

We took care of our employees, to safeguard

their health and safety

As the leading UAE bank, it is our duty to

support our customers and communities through

these challenging times

Customer and Community

• Over AED 11Bn payment deferrals provided

to customers under TESS and the bank’s own

programmes (more details on slide #40)

• Reduction of charges & fee waivers

• Leveraged digital platform to provide

uninterrupted banking services, and innovative

products and solutions

• Facilitated UAE’s first ever virtual GAMs

• Donated AED 1Mn to the Emirates

Foundation, AED 2Mn to the Emirates Red

Crescent (ERC) & AED 5Mn to provide laptops

to students

• Donated 133 PCs to Emirates Foundation to

support students in their virtual home learning.

1 WFH is activated for 90% employees, excluding those in branches

Economic and banking

sector review

11Investor Presentation May 2021

Economic & Banking sector review 12

Economy poised to rebound in 2021Growth prospects improving, but remain tied to evolving dynamics of the pandemic

Investor Presentation May 2021

UAE PMI has recovered from lockdown lows3UAE economy poised to rebound

after contracting in 2020

52.7

40

45

50

55

60

Dec-1

8

Ma

r-1

9

Jun

-19

Se

p-1

9

Dec-1

9

Ma

r-2

0

Jun

-20

Se

p-2

0

Dec-2

0

Ma

r-2

1

1 In-house GDP forecast for FY’21 and FY’22; IMF forecasts for prior years;

FY’21 GDP growth has been revised from 2.9% communicated in Q1’21 earnings presentation

2 Bloomberg OPCRUAE Index, Mar 2021

3 Markit Economics-PMI (Purchasing Manager Index) (Apr 2021)

4 The Conference Board® Global Consumer Confidence Index, Q1’21

2.6

66

- 10 20 30 40 50 60 70 80 90

Dec-1

8

Ma

r-1

9

Jun

-19

Se

p-1

9

Dec-1

9

Ma

r-2

0

Jun

-20

Se

p-2

0

Dec-2

0

Ma

r-2

1

- 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0

Oil Production (Mn bl/day) (LHS)

Brent Monthly Average (USD/bl) (RHS)

Stablising oil prices supported by OPEC production cuts 2

UAE consumer confidence4 also increased from 105 in Q4’20 to 121 in Q1’21,

ranking second in the region after Saudi Arabia (125)

13.8

4.6

3.1

0.9

0.1

(2.8)

UAE

Saudi Arabia

Oman

Bahrain

Kuwait

Qatar

2021e Nominal GDP(USD Bn)

2021e Fiscal Balance(% GDP)

2021e Gross Debt(% GDP)

A robust and diversified economy5 UAE remains top FDI destination in GCC (USD Bn)6

805

402

166

127

74

38

KSA

UAE

Qatar

Kuwait

Oman

Bahrain

(3.8)

(1.3)

1.4

(6.8)

(4.4)

(9.1)

31.0

37.1

59.8

13.7

71.3

129.4

2020e

(11.1)

(7.4)

1.3

(9.4)

(17.3)

(18.3)

Avg breakeven oil price(2021-22) USD/bbl

69

48

55

72

75

85

YoY%

14.7

13.3

13.6

17.6

17.3

10.6

0.5% 1.2%1.7%

-6.6%

2.4% 3.0%

-8%

-4%

0%

4%

8%

2017 2018 2019 2020e 2021f 2022f

UAE Real GDP growth (%)

5 IMF World Economic Outlook, April 2021; Fitch

6 World Investment Report 2020 - UNCTAD Federal Competitiveness and

Statistics Authority

Economic & Banking sector reviewInvestor Presentation May 2021 13

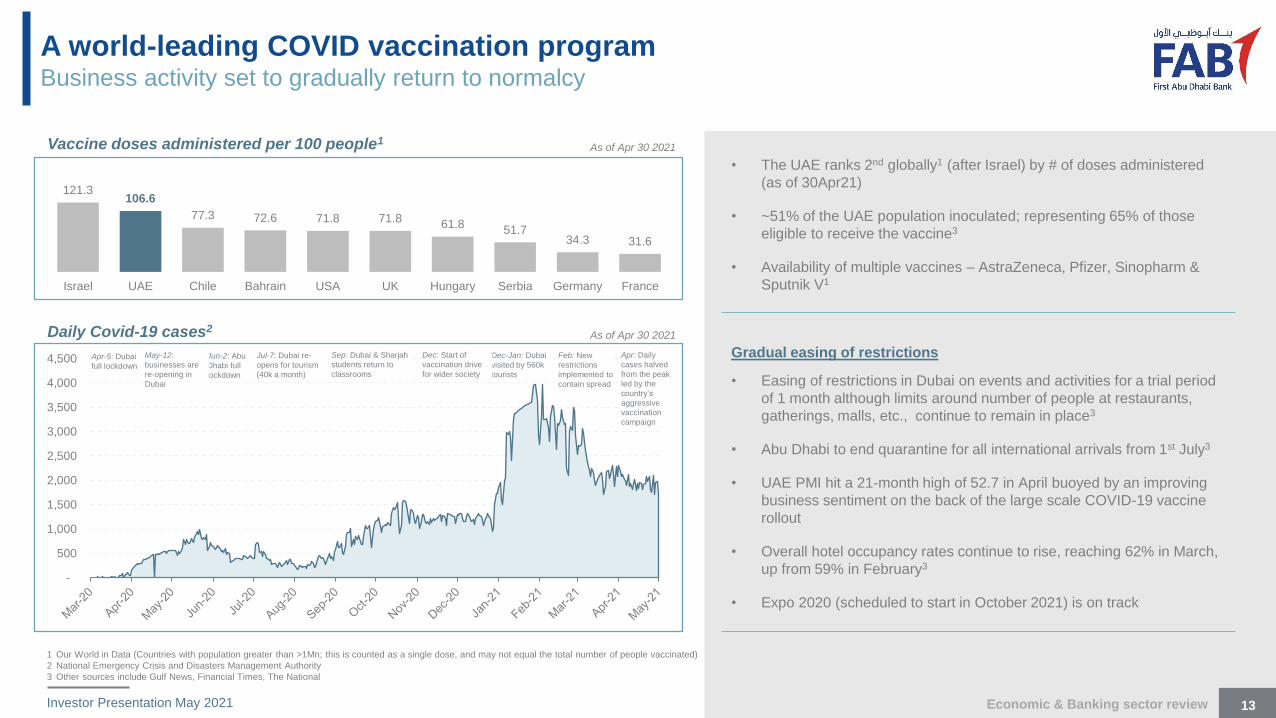

Vaccine doses administered per 100 people1

1 Our World in Data (Countries with population greater than >1Mn; this is counted as a single dose, and may not equal the total number of people vaccinated)

2 National Emergency Crisis and Disasters Management Authority

3 Other sources include Gulf News, Financial Times, The National

As of Apr 30 2021

121.3106.6

77.3 72.6 71.8 71.861.8

51.734.3 31.6

Israel UAE Chile Bahrain USA UK Hungary Serbia Germany France

• The UAE ranks 2nd globally1 (after Israel) by # of doses administered

(as of 30Apr21)

• ~51% of the UAE population inoculated; representing 65% of those

eligible to receive the vaccine3

• Availability of multiple vaccines – AstraZeneca, Pfizer, Sinopharm &

Sputnik V1

Gradual easing of restrictions

• Easing of restrictions in Dubai on events and activities for a trial period

of 1 month although limits around number of people at restaurants,

gatherings, malls, etc., continue to remain in place3

• Abu Dhabi to end quarantine for all international arrivals from 1st July3

• UAE PMI hit a 21-month high of 52.7 in April buoyed by an improving

business sentiment on the back of the large scale COVID-19 vaccine

rollout

• Overall hotel occupancy rates continue to rise, reaching 62% in March,

up from 59% in February3

• Expo 2020 (scheduled to start in October 2021) is on track

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500 Jun-2: Abu

Dhabi full

lockdown

Apr-5: Dubai

full lockdown

May-12:

businesses are

re-opening in

Dubai

Jul-7: Dubai re-

opens for tourism

(40k a month)

Dec-Jan: Dubai

visited by 560k

tourists

Sep: Dubai & Sharjah

students return to

classrooms

Dec: Start of

vaccination drive

for wider society

Daily Covid-19 cases2As of Apr 30 2021

Feb: New

restrictions

implemented to

contain spread

A world-leading COVID vaccination programBusiness activity set to gradually return to normalcy

Apr: Daily

cases halved

from the peak

led by the

country’s

aggressive

vaccination

campaign

Economic & Banking sector reviewInvestor Presentation May 2021 14

0.9%

-4.3%

-10%

-8%

-6%

-4%

-2%

0%

2%

Dec'19 Mar'20 Jun'20 Sep'20 Dec'20 Mar'21

Abu Dhabi - All Properties (YoY Change)

Dubai - All Properties (YoY Change)

-5.4%

-8.7%

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

Dec'19 Mar'20 Jun'20 Sep'20 Dec'20 Mar'21

Abu Dhabi - All Properties (YoY Change)

Dubai - All Properties (YoY Change)

• Real estate sale prices in Abu Dhabi witnessed their

first increase yoy in over 6 years

• Property market expected to benefit from a pick-up

in demand, and the launch of new programs and

initiatives, including long-term residency reforms

Real estate market sees signs of revivalAbu Dhabi witnesses its first residential property sales price increase yoy in over 6 years

1 REIDIN, UAE Monthly Report Mar 2021

2 JLL Real Estate Market Overview – Q1’21

69 120

12 46 55

584

1.4 16

AbuDhabi

Dubai AbuDhabi

Dubai AbuDhabi

Dubai AbuDhabi

Dubai

Office Residential Retail Hospitality

FY’21e deliveries Total existing stock

3,800

8,900

264585

2,8004,100

30 131

UAE real estate market total existing stock vs FY’21e supply2

Gross lettable area

(‘000 sqm)

Gross lettable area

(‘000 sqm)

Units (‘000) Hotel keys (‘000)

• Project deliveries for FY’21, in both Abu Dhabi and

Dubai, are lower vs the beginning of 2021; which

should help partly alleviate the market’s oversupply

Sale prices - mainstream residential market property1 Rental prices - mainstream residential market property1

Economic & Banking sector review 15

Sound and highly capitalised banking sectorTESS extension to further support the financial system and economic recovery

Investor Presentation May 2021

1 Source: UAE Central Bank, FAB Data as of 28 Feb 2021

2 Net of Provisions

3 Source: Bloomberg, based on the latest available financials reported by 14 listed UAE banks as of 2 May 2021

4 Total advances (net lending + net financial guarantees & stand-by LC+ Interbank placements more than 3 months)/

sum of (net free capital funds + total other stable resources)

UAE Banking Sector Key Indicators1

Figures in USD Bn Feb’21 YTD YoY

Total Assets, net2 823 -0.3% 2.1%

Loans and Advances, net2 441 -0.2% 0.6%

Customer Deposits 511 -0.3% 2.7%

LDR2 86% +11bps -184bps

Lending to Stable Resources Ratio4 78% +80bps -260bps

CAR (Basel III) (Dec’20) 18.2% - +50bps

CET1 (Basel III) (Dec’20) 14.9% - +20bps

FAB has a dominant position in UAE 3

LDR (%) 93 90 87 87 86 86

Liquidity remains ample while credit growth reflects subdued demand1

5.8%

1.7%4.3%

5.7%

0.1% 0.6%

6.2%4.1%

7.9% 6.5%

0.8% 2.7%

2016 2017 2018 2019 2020 Feb'21

Credit growth, net (YoY) Deposits growth (YoY)UAE CB’s AED 50Bn TESS programme was further extended:

• TESS deferrals programme under zero cost facility (ZCF) extended until

the end of 2021, with a gradual phase out, i.e. not to exceed 50% of the

allocated limit for each financial institution by 30 Sep’21, with full phase out

by 31 Dec’21

• TESS recovery program collateralized, extended until 30 June 2022

UAE CB further extends TESS program

• UAE banking sector : 21 Local and 38 Foreign banks (Incl. 11 wholesale banks)

• FAB is one of the 4 Domestic Systematically Important Banks (DSIBs) in UAE

Assets

USD 812Bn

Gross Loans

USD 468BnDeposits

USD 524Bn

78% 77% 77%

32% 23% 30%

Top 4 (incl FAB)

FAB

Total

(UAE listed banks3)

(FY’20: 31%) (FY’20: 23%) (FY’20: 29%)

Strategic overview

16Investor Presentation May 2021

Strategic overview 17

Our strategy is clear Positioning FAB for long-term success

Investor Presentation May 2021

Group MissionWhat we aspire to

become

To be the region's strongest and the most profitable bank, building deep and trusted relationships with

customers through simplified banking

Group PurposeWhy we exist

To create sustainable value for our stakeholders by powering the UAE's growth

MARKET LEADERSHIP

• Customer obsessed

• Market leading product offerings

• Smart expansion, leveraging Digital and Partnerships

• Unwavering focus on sustainable returns

AFFIRM POSITION OF STRENGTH

• Superior credit ratings

• Regional sustainability leader

• Abu Dhabi House Bank status

• Comprehensive banking offerings covering all segments

Key enablersDigital-first mindset/

Technology and data-drivenScale Talent and culture

Strategic overview 18

Accelerating our digital transformationTo enhance efficiency and stakeholder value

Investor Presentation May 2021

Establish World Class Technology Foundations

Build Strong Digital Capabilities

Enabling New Ways of Working (“WoW”)

• Migrate to Cloud and modernise on-premise infrastructure

• Build fully automated & reusable templates that enable Group Tech to stand

immutable components in minutes not months

• Embed advanced analytics, ML, and AI into all business services

• Roll out fit-for-purpose real-time architecture governance

• Improving efficiency and customer friendliness amongst channels

• Ensuring instant and seamless customer experiences via channels

• Partnering with Fintechs to launch leaner & faster innovative services

• Leveraging analytics and AI to improve customer experience and implement

data-driven decision making

• Ensuring the highest security standards by investing in technologies, capabilities,

and partners

• Target balance of inhouse talent vis-à-vis outsourced staff, thereby improving

retention of intellectual property and quicker decision making while maintaining

low-cost profile

• Adopt service delivery model powered by business product, tech, & delivery trinity

• Implement bank-wide customer centred agile WoW

• Build digital, cloud, & data-ready workforce

• Digital FLEX - a training program to build digital and technical capabilities that best

support our transformation goals

In line with our ongoing digital transformation strategy,

FAB continues to build on its strong momentum to

accelerate its digital transformation to enhance

efficiency and stakeholder value

OUR DIGITAL AMBITIONS

Strategic overview 19

Our digital transformation journey

Investor Presentation May 2021

1 As of 31 March 2021

2 Defined as total digital (mobile + internet banking) transactions as a percentage of all transactions performed digitally or at the branch and call centers

• Established our Analytics & AI unit

• Launched unified FAB Online Banking and

Mobile channels (following merger and

systems integration)

• Instant money transfers to India

• Instant opening of savings account, gold

accounts & terms deposits

• Launched FABRIC (FAB Research &

Innovation Centre) – platform to develop

new products, services & solutions with

partners, startups, accelerators & tech

• 20 automations delivered

2018

• Instant joining FAB through Mobile Banking

• Manage credit cards digitally

• Freeze or unfreeze credit cards instantly

• Control supplementary cards instantly

2019

2020

• Launched (teller-less) digital branches

• COVID-19 relief to qualifying customers through requests via

digital channels

• Launched FAB corporate mobile app, FAB ePay, FAB eSign and

SME Digital Account (Basher)

• FAB rewards to instantly view & redeem rewards on mobile

• Instant money transfers to accounts/wallets across multiple

countries

• Personalised spend driven offers through mobile banking

• Increase in digital transactions by 39%

• Digitisation of over 20 service requests

• Rolled out of new payit features

• 76 automations delivered

• 22 automations delivered

• 30 initiatives completed

• Instant virtual cards

• Instant personal loan top ups

• Launched UTC (the region’s largest

blockchain based trade network), after

soft launch in 2020

Q1’21

Bank

transactions2

performed

digitally

>85%

>90%GTB clients

migrated to digital

channels

Increase in

registered

users to over

300,000+100%

yoy

PIONEERING SOLUTIONS IN CIB

IMPROVED SELF-SERVICE CAPABILITIES

NEW FUNCTIONALITIES

INNOVATION IN PAYMENTS

+20% yoy

Mobile registrations

and engagement

INCREASED DIGITAL ADOPTION1

Strategic overview 20

Our commitment to sustainabilityIntegration of ESG into risk management framework is a key focus for 2021

Investor Presentation May 2021

1 Euromoney Awards for Excellence 2020

2 Constituent for 2 years in a row

3 The report can be downloaded at http://www.forcegood.org

Our ESG Ratings

Voluntary initiatives

and public commitments in

alignment with national and

global frameworks

FAB’s robust framework is

anchored on 4 strategic

pillars Governance,

Integrity and Risk

Management

Sustainable

BankingResponsible

Employer

Positive Societal

Impact

AA MSCI ESG

‘Leader’

CDP Score(formerly the Carbon Disclosure Project)A-

ESG scope of

implementation and

estimated timeline of

implementation

Note: Please refer to the Sustainability section of our corporate website to learn more about FAB’s

sustainability practices and disclosures (including FAB’s Corporate ESG, Green Bond and Equator

Principles Reports)

2021

• Operationalisation of ESG

through roll out of ESG tools

• Group sustainability strategy and

roadmap

• ESG risk framework

• UAE Vision 2021

• The Abu Dhabi Economic Vision 2030

• Equator Principles

• The Green Bond Principles

• UN Sustainable Development Goals

• UN Global Impact

• TCFD (Task Force on Climate-Related

Financial Disclosures)

• CDP (Carbon Disclosure Project)

• MSCI ESG

• FTSE4Good

• SASB (Sustainability Accounting Standards

Board) & GRI (Global Reporting Initiative)

• MSCI ESG ratings recently upgraded from A to AA

• FAB named Middle East’s Best Bank for Corporate

Responsibility1

• Amongst the largest MENA constituents on the

FTSE4Good2 and MSCI ESG Index

• Annual CDP score upgraded from B to A-

• FAB Green Bonds outstanding exceed USD 1 Billion

(equivalent), across 5 issuances and 3 different currencies.

• Green bond framework expanded to a Sustainable

Finance framework

• Became a corporate partner with Aurora50, a UAE-

based social enterprise that aims to increase board-level

gender diversity while also creating and bolstering a female

talent pipeline for future independent director appointments

Recent Highlights

Integration of ESG into FAB’s risk

management framework is a key focus for

2021, which will be supported by the new

dedicated ESG Risk function

Strategic overview

Completed carve-out of our payments business, and launched

Acquisition of Bank Audi Egypt finalised; integration to be completed by 2022

21Investor Presentation May 2021

Optimisation of property portfolio, and rundown of non-strategic assets to enhance risk-adjusted returns

Ongoing digital transformation, to enhance productivity and efficiencies

Ongoing commitment to sustainability, planning to finalise ESG roadmap in 2021

Delivering on our strategic priorities

Strategic overview 22

Magnati at a glanceA story of market leadership, continued growth in scale and profitability

Investor Presentation May 2021

Direct Acquiring

Market Share

Issuing Market

Share (WPS Segment)

Government

Solutions

Merchants

Served

Total Processed

Value

Terminals

Prepaid cards

Issued

Leadership Scale Performance

Top 2

#1

>30,000

~US$18 Bn

>40,000

~2 Mn

Double digit CAGR of

processed value

High EBITDA

Margin

Diversified Across

Business Lines

Issuer Processing

Market Share (Captive FAB )

~20%

*Based on 2020 figures

#1

For further details on Magnati, please refer to the Magnati presentation uploaded on the FAB IR website

Strategic overview 23

Firmly laying the foundations for long term success

Investor Presentation May 2021

Driving specialisation and competitive advantage to build a future-

proof FAB around our customers’ evolving needs:

• Business structure realigned to strengthen capabilities, and

enhance future income generation; 4 distinct business lines including

Investment Banking and Private Banking

• Streamlined Technology, Data Analytics & AI, operations and

administrative functions, in order to create a robust service delivery

model, enhance organisational agility, and offer a distinct customer

experience

• Evolving Group strategy: 3-year plan to be presented at FAB’s

Analyst & Investor Day in the second half of the year

Committed to unlocking

new opportunities for

growth, and delivering

superior and sustainable

shareholder returns

Q1’21

Financial Performance

24

Q1’21 Financial PerformanceInvestor Presentation May 2021

Key Messages

▪ Continued resilient performance

amid slow recovery: Q1’21 NPAT at

AED 2.5 Bn, up 3% yoy

▪ Balance sheet strength across

liquidity, funding, and capital ratios;

while asset quality remains resilient

▪ Delivering on our strategic agenda,

while firmly laying the foundations

for long term success

0.7USD Bn

Net profit+3% year-on-year

2.5AED Bn

Revenue-4% year-on-year

1.2USD Bn

4.4AED Bn

12.8Return on

Tangible Equity(Q1’20: 13.0%)

Common Equity Tier 1 Ratio

(Q1’20: 12.2%)

13.7

2525

Q1’21 Financial Performance

2,408 2,476

+35

+268

(184)

(51)

Q1'20NPAT

OperatingIncome

OperatingCosts

Impairmentcharges,net

Taxes &MinorityInterest

Q1'21NPAT

Q1 2021 results reflect gradual economic recovery

Net profit bridge

- Adverse impact from rate cuts and

COVID-19 disruption

+ partially offset by continued

momentum in the CIB business led

by Global Markets

+ Higher other income from property-

related gains (+294Mn)

Net profit (AED Bn)

QoQ ↓23%, YoY ↑3%

Lower impairment charges

reflect improvement in

projected macro-economic

indicators, and adequate

provision levels

+3% yoy

2.4 2.4 2.53.2

2.5

Q1'20 Q2'20 Q3'20 Q4'20 Q1'21

Revenue (AED Bn)

4.6 4.8 4.3 4.9 4.4

Q1'20 Q2'20 Q3'20 Q4'20 Q1'21

QoQ ↓11%, YoY ↓4%

Disciplined cost

management amidst

ongoing investments

in strategic and digital

initiatives

Operating Profit (AED Bn)

3.2 3.6 3.1 3.6 3.1

Q1'20 Q2'20 Q3'20 Q4'20 Q1'21

QoQ ↓16%, YoY ↓5%

(AED Mn)

Investor Presentation May 2021 26

Q1’21 Financial Performance

CIB performanceHeadwinds from rate cuts and subdued demand, largely offset by GM momentum, property portfolio optimisation

Note: Real estate businesses (previously structured under Subsidiaries) and SME business (previously structured under PBG) were re-organised under CIB effective 1 April 2020; prior

period numbers have been restated where applicable

293 296 299 296 288

Mar'20 Jun'20 Sep'20 Dec'20 Mar'21

119 134 152 153 182

421 442525

457 487

Mar'20 Jun'20 Sep'20 Dec'20 Mar'21

CASA Notice, Time & Others

Loans (AED Bn) Deposits (AED Bn)

QoQ ↓3%, YoY ↓2% QoQ ↑7%, YoY ↑16%

2,020

2,401 +23 +294

+319 +4

(259)

Q1'20Operating profit

GCF revenue GTB revenue GM revenue Other revenue Operating costs Q1'21Operating profit

58% 60% 61% 60% 51%

42%40% 39%

40%49%

2.63.2

2.83.4

3.0

Q1'20 Q2'20 Q3'20 Q4'20 Q1'21

NII Non-int inc

QoQ ↓12%, YoY ↑14%

Operating Profit

Quarterly Revenue trend (AED Bn)

+19% yoy(+4% ex-property-related gains)

Q1’21 YoY%

Revenue 3,016 +14

Costs (615) -1

Operating

Profit2,401 +19

Impairment

charges, net(238) -10

Taxes (99) +114

Profit after taxes 2,064 +21

CI Ratio 20.4% -307bps

RoRWA 2.0% +26bps

Contribution to

Group revenue69% +11.4%

Q1’21 summary P&L (AED Mn)(AED Mn)

• +3% despite subdued

loan markets

• Strong fee generation

across several

transactions, helped

offset lower NII

-28% due to

margin

compression from

rate cuts despite

CASA ↑53% yoy

+32% driven by

strong trading

performance and

benefit from

market volatility

Primarily driven

by property-

related gains

Investor Presentation May 2021 27

Q1’21 Financial Performance

PBG performanceReflects impact from rate cuts, lower business volumes

Note: Real estate businesses (previously structured under Subsidiaries) and SME business (previously structured under PBG) were reorganised under CIB effective 1 April 2020; prior

period numbers have been restated where applicable

88 87 88 90 89

Mar'20 Jun'20 Sep'20 Dec'20 Mar'21

Loans (AED Bn) Deposits (AED Bn)

QoQ ↓1%, YoY ↑1% QoQ ↓1%, YoY ↑9%

966 807

+44

(58)(145)

Q1'20Operating profits

Net interest income Non-interest income Operating costs Q1'21Operating profits

76% 82% 77% 80% 82%

24%18% 23% 20% 18%

1.61.4

1.6 1.5 1.4

Q1'20 Q2'20 Q3'20 Q4'20 Q1'21

NII Non-int inc

QoQ ↓6%, YoY ↓12%

Primarily reflecting rate cuts and lower

volumes, with solid sales momentum in

credit cards, personal loans and mortgages

being offset by run-offs

Operating Profit

Quarterly Revenue trend (AED Bn)

-16% yoy

+ Reflects shift towards digital

channels and cost save initiatives

taken to counter impact of slowdown

- Continued Investments in digital

infrastructure and international

network (KSA, Egypt)

Q1’21 YoY%

Revenue 1,440 -12

Costs (633) -7

Operating

Profit807 -16

Impairment

charges, net(238) -47

Taxes (13) -44

Profit after taxes 556 +13

CI Ratio 44.0% +275bps

RoRWA 2.9% +28bps

Revenue

Contribution33% -313bps

Q1’21 summary P&L (AED Mn)

(AED Mn)

Investor Presentation May 2021 28

60 60 6268 68

73 74 7481 79

Mar'20 Jun'20 Sep'20 Dec'20 Mar'21

CASA Notice, Time & Others

Q1’21 Financial Performance

+22

+6

+7

(9)

(2)

+27

+8

(6)

QoQ change (AED Bn)

Cash & balances with CB's

DFB & Reverse repos

Investments

Loans & advances

DTB, Repos & CPs

Customer deposits

Term borrowings(incl Sub-debt)

Shareholders’ equity

• Excess liquidity prudently and tactically

deployed into highly liquid assets

• LCR remains solid at 141%; HQLAs1

amounted to AED 345Bn

• Loans down ytd on muted demand,

repayments in our GRE loan book and tactical

run-down of our FI trade loans (↓11Bn yoy)

• Healthy Govt/GRE lending pipeline, with

demand expected to gradually pick-up on

rebound in economic activity in H2’21

(Undrawn commitments AED 74Bn ↑17% yoy)

• TESS2 allocation utilised at end-Mar 2021

was AED 4.4Bn, +1Bn from Dec’20 (FAB’s

allocation - AED 8Bn)

• Strong deposit growth (+AED 27Bn qoq)

underlines FAB’s role as an aggregator of

regional and global liquidity

• CASA at record high levels of AED 250Bn,

up 38% yoy, represent 44% of total deposits

Sustained balance sheet strengthStrong liquidity position as deposits growth remains robust

Mar’21QoQ%

change

YoY%

change

250 +10% +42%

78 +9% +31%

160 +4% +20%

378 -2% -1%

142 -2% +14%

568 +5% +14%

71 +13% +23%

103 -5% +10%

1 HQLA including cash and central bank placements

2 For more details, please see slide #41 in Appendix

Investor Presentation May 2021 29

Q1’21 Financial Performance

70

108

44 37 51

122

67

CoR (L&A) (bps) CoR - gross (L&A) (bps)

738

1,060

504

318 470

1,097

771

Q1'20 Q2'20 Q3'20 Q4'20 Q1'21

Net impairment charges Gross impairment charges

Resilient asset quality and adequate provision levelsLower impairment charges reflect improvement in projected macro-economic indicators

Impairment charges, net (AED Mn) & CoR1 (%)

13.915.6 15.7 15.8 15.7

13.214.2

15.1 15.0 15.1

Mar'20 Jun'20 Sep'20 Dec'20 Mar'21

NPLs (AED Bn) Provisions (AED Bn)

95 91 96 95 96

3.5 3.9 3.9 4.04.0

Provision Coverage (%) NPL Ratio (%)

1 Annualised

2 Gross impairment charges and gross CoR on loans and advances: excludes provision reversals as a result of partial resolution of a few large corporate accounts

3 NPLs = Stage 3 exposure + adjusted POCI (Purchase or originally impaired credit) of AED 4,929Mn as of Mar’21 considered as par to NPLs, net of IIS

4 ECL = ECL on loans & advances + ECL on unfunded exposures + IFRS9 impairment reserves

Note: Gross loans and advances and NPLs are net of interest in suspense; see Note #29 ‘Credit quality analysis’ in Q1’21 financials for more details on IFRS9 exposures and ECL

NPLs3 and ECLs4 (%)

2

2

Investor Presentation May 2021 30

Q1’21 Financial Performance

13.3% 13.7%

1.60%

+4bps

+49bps

-14bps

CET1 Dec'20 Change in RWA Q1'21 profits Other movements CET1 Mar'21

14.9%

Strong capital position comfortably above regulatory requirementsCET1 strengthened year-to-date, to 13.7%

1 UAE CB has reduced the minimum CET1, Tier 1 and CAR requirement to 8%, 9.5% and 11.5% respectively until 31 Dec 2021 under TESS (previous minima of

11%, 12.5% & 14.5%, respectively)

2 ECL add-back to CET1 under IFRS9 prudential filter – AED 995Mn (20bps of CET1)

CET11 ratio progression Q1’21

DPS: 74 fils

AED 8.08Bn

+ 39bps

• March-end 21 CET1 at 13.7%, up from 13.3% as of

December-end 2020

• Risk discipline maintained despite balance sheet

growth

• Capital ratios remain well above minimum

regulatory requirements; Tier 1 and CAR ratios at

15.8% and 16.9%, respectively

• Capital ratios in upcoming quarters to reflect the

impact of Bank-Audi Egypt acquisition and the

implementation of specific Basel III capital

requirementsBasel III

regulatory

minimum: 11%

Regulatory

minimum

under TESS: 8% 1.97 1.97 1.97 2.13 1.99

RoRWA (%ytd) and RWAs (AED Bn)

497.4 498.6 509.7 505.3 504.1

Q1'20 H1'20 9M'20 FY'20 Q1'21

Investor Presentation May 2021 31

Q1’21 Financial Performance

• NII was 13% lower yoy, reflecting the

adverse impact of rate cuts, partly offset

by the placement of short-term liquidity with

Central Banks earning positive yields; QoQ

decline primarily due to lower IIS reversals

• P&L impact from a +/-25bps parallel

movement in interest rates is estimated at

approximately +/- AED 260Mn1, if no

offsetting action is taken by management

• Continued focus on tactical deployment

of excess liquidity

• NIM expected to stabilise broadly around

current levels

Net interest income and marginsPrimarily reflect impact from rate cuts

3,080 3,244 2,854

3,079 2,679

Q1'20 Q2'20 Q3'20 Q4'20 Q1'21

Net interest income

1 For further details, please refer to Market Risk note #43.3 of FY’20 financial statements

Note: All percentage figures are annualised

Net interest margin (%)

QoQ ↓13%, YoY ↓13%

1.90 1.90 1.62 1.62

1.47

1.80 1.75

Q1'20 Q2'20 Q3'20 Q4'20 Q1'21

Quarterly YTD

4.14 3.71

3.05 3.33

2.80

3.91 3.62 3.55

Q1'20 Q2'20 Q3'20 Q4'20 Q1'21

Quarterly YTD

1.12

0.60 0.42 0.34 0.30

0.85 0.69 0.60

Q1'20 Q2'20 Q3'20 Q4'20 Q1'21

Quarterly YTD

Performing loan yields (%) Cost of customer deposits (%)

0

100

200

300

Q1'20 Q2'20 Q3'20 Q4'20 Q1'21

Negative yielding Positive yielding

Central bank placements2

2 Daily average balances of placements on a quarterly basis with

overseas central banks; Data rebased to 100 as of Jan 2020

(AED Mn)

Investor Presentation May 2021 32

Q1’21 Financial Performance

Non-interest income trendsSupported by FX & investment income, property-related gains

Non-interest income(In AED Mn)

Q1’21 Q4’20 QoQ% Q1’20 YoY%

Fees & Commissions, net 663 653 +1 841 -21

FX & Investment income 677 590 +15 603 +12

Other income 363 586 -38 43 +752

Non-interest income 1,703 1,829 -7 1,487 +15

% of Group total income 39% 37% 33%

Fees & commissions, net

603

371

627 590 677

Q1'20 Q2'20 Q3'20 Q4'20 Q1'21

QoQ ↑15%, YoY ↑12%

FX & investment income • Fees and commissions in Q1’21 vs. Q1’20

- lower PBG fees reflecting lower business volumes

due to COVID-19 induced economic slowdown

+ partly offset by continued strength in capital markets

and corporate finance/ advisory fees

• FX & investment income in Q1’21 vs. Q1’20

+ higher income from trading and liquidations, and

continued strength in strategic client flow products

- lower income from our liquidity arbitrage activity

1,096 1,287

1,110 1,380 1,475

400 256 362 302 255

Q1'20 Q2'20 Q3'20 Q4'20 Q1'21

CIB PB

Non-interest income trends in CIB & PB

• Other income in Q1’21 vs. Q1’20

+ Property-related gains (net) - AED 294Mn

(AED Mn)

Investor Presentation May 2021 33

452 309

441 395 320

220

217

220 214

204

168

111

120

44 138

841

637

781

653 663

Q1'20 Q2'20 Q3'20 Q4'20 Q1'21

Loan-related Trade-related Other

QoQ ↑1%, YoY ↓21%

Q1’21 Financial Performance

Strong cost discipline maintainedAmidst continued investments in our digital capabilities and efficiency enhancing initiatives

FY’21 C/I ratio guidance: <30%

Cost savings to be deployed to support further digital and technology

investments; cost discipline to be maintained through the cycle, with

several initiatives underway to create future efficiencies

1,352 1,318

+49

(64) (20)

Q1'20 Staff Costs Depreciation &Amortisation

Other G&A Q1'21

Proactively managing variable costs and

headcount adapting to the prevailing

business conditions

Cost savings continue to be

invested in digital and

technology infrastructure to

further enhance productivity,

create future efficiencies and

an agile operating model

755 671 624 734 692

427 368 386 327 407

171 197 197 204 219

1,352 1,236 1,207 1,264 1,318

Q1'20 Q2'20 Q3'20 Q4'20 Q1'21

Staff costs Other G&A costs Depreciation & Amortisation

Operating expenses trend (AED Mn) and C/I ratio (%)

29.1 25.5

28.0 25.7

29.6

C/I ratio (ex-integration)

QoQ↑4%, YoY↓3%

Opex drivers YoY

Operating expenses improve 3% year-on-year

(AED Mn)

Investor Presentation May 2021 34

Reiterating FY’21 financial guidance

FY’21 financial guidance

Loan growth Mid-single digit

C/I Ratio (ex-integration costs)

<30%

Cost of Risk <100bps

Provision

coverage ~ 90%

CET1 (pre-dividend)

> 13.5%

• We expect underlying operating performance to

improve in H2’21, driven by a healthy Government/

GRE pipeline, continued focus on cross-sell, and

M&A (Egypt)

• We will continue to invest in our digital

transformation to enhance productivity and

efficiency, while ensuring cost discipline

• Prudent provisioning to continue

• Capital position to remain comfortable, and well

above Basel III minimum requirement

Investor Presentation May 2021 35

Q1’21 Financial Performance

Wrapping up

▪ Continued resilient performance in the first quarter of 2021, in an improving yet

challenging backdrop

Vaccine roll-out and improving macro outlook to underpin a gradual return to economic normalcy

and a pick-up in business activity in the second half

▪ Our foundation continues to be robust

Strong liquidity and funding profile

Solid capital position with CET1 at 13.7%

Resilient asset quality with NPL ratio at 4.0%, and adequate provision coverage

▪ We are firmly laying the foundations for long term success, confident in our

capacity to deliver superior and sustainable shareholder returns

Strengthening business capabilities to drive specialisation and competitive advantage

Core businesses realigned, with enhanced focus on Investment Banking and Private Banking

Evolving our strategy: 3-year plan to be presented at FAB’s Analyst & Investor Day in H2’21

Investor Presentation May 2021 36

Supplementary

financial slides

37Investor Presentation May 2021

Supplementary financial slides

25%

8%

16%9%

42%27%

8%

17%8%

40%Cash & CB Balances

DFB and Reverse Repos

Investments

Others

Loans and Advances

Overdrafts7%

Term Loans78% Trade related

loans,6%

Personal Loans8%

Credit Cards1%

Vehicle financing

loans, 0.3%

Agriculture0.2%

Energy10%

Manufacturing5%

Construction3%

Real Estate23%

Trading6%

Transport and communication 9%

Banks1%

Other financial institutions 9%Services 5%

Government 10%

Personal - Loans & Credit Cards

13%

Personal - Retail Mortgage

6%

10% 10%

23% 23%

43% 48%

18% 19%2% 2%

Dec'20 Mar'21

Banks

Personal/ Retail

Corporate/ Private

Public Sector

Government

403.3 394.9

38

Asset & loan mixConservative asset mix with a well diversified, high-quality loan book

Investor Presentation May 2021

AED 394.9Bn

Mar’21

AED 378.0Bn

Mar’21

AED 394.9Bn

Mar’21

Gross loans by counterparty

Gross loans by economic sector Net loans by geography2 Gross loans by product

1

1 Real Estate by geography: Abu Dhabi 45%, Dubai 25%, Other UAE 3%, UK 18%, Other Intl 9% 2 Based on loan origination / coverage

Mar’21

AED 940.7Bn

Dec’20

AED 919.1Bn

UAE74%

GCC7%

Asia6%

Europe8%

MENA2%

America3%

Asset mix

AED Bn

Supplementary financial slides

181.0 196.2 215.9 223.2 250.1

316.1 322.5 385.9 317.7 318.3

497.1 518.7 601.8

540.9 568.3

Mar'20 Jun'20 Sep'20 Dec'20 Mar'21

Notice,Time &Others

CASA

292.7 295.8 299.4 295.9 287.6

88.1 87.2 88.5 89.7 89.1 1.0 1.6 1.0 1.1 1.3

381.8 384.6 388.8 386.6 378.0

Mar'20 Jun'20 Sep'20 Dec'20 Mar'21

Others

PB

CIB

39

Strong liquidity position LCR at 141% and LDR at 67%

Investor Presentation May 2021

Loans and advances, net

QoQ ↓2%, YoY↓1%

1 Minimum regulatory LCR requirement is 100% effective Jan’19; relaxed to 70% until 31

Dec 2020 under TESS by UAE CB

• Loans declined in Q1’21 on muted

demand, repayments in our GRE loan book

and tactical run-down of our FI trade loans

(↓11Bn yoy)

Customer Deposits

QoQ ↑5%, YoY ↑14%

LCR(%)1 110 129 155 143 141

LDR (%) 77 74 65 72 67

• Strong inflows in Q1’21 driven by

corporates, slightly offset by outflows in

GREs

• FAB’s international network continues to be

a key differentiator to source liquidity and

funding; international deposits were up

28% (+34Bn) yoy driven by our UK and US

offices attracting SWFs and asset

managers looking for high-rated

counterparties like FAB

• CASA +38% yoy to AED 250Bn, represents

44% of customer deposits, highlights strong

momentum in cash management

403 395

(1) (4) (3) (1) -

Q4'20 Govt GREs Banks Corp/PvtSector

Personal/Retail

Q1'21

Gross loans & advances

541 568

+2 +27 +2 +1 (5)

Q4'20 Govt GREs Corp/PvtSector

Personal/Retail

CDs Q1'21

(AED Bn)

(AED Bn)

Supplementary financial slides

1 For more information, refer to note 29 of FAB’s Q1’21 financial statements

40

Supporting our customers through payment deferralsUAECB TESS facility further extended to end-June 2022

Investor Presentation May 2021

Trading, 28%

Real Estate (incl hospitality), 21%

Construction, 35%

Services, 7%Loans to Individuals, 3%

Others, 6%

From April 1st 2020, relief measures were extended to

our retail, SME and corporate customers in the form of

payment deferrals on interest and principal between 3-6

months, under the UAE Central Bank’s Targeted

Economic Support Scheme (TESS), as well as FAB’s

own initiatives. TESS deferral programme has now

been further extended to end-Dec 2021, while TESS

recovery programme has been extended to

end-June 2022.Segment(figures in AED Mn)

Payment

deferrals under

TESS

Total Loans &

Advances

% of Gross

Loans (Mar’21)

CIB

Group 1 2,801 24,281 6.1%

Group 2 1,584 3,792 1.0%

PB

Group 1 27 312 0.1%

Group 2 2 14 0.0%

Total 4,414 28,399 7.2%

TESS utilisation

AED 4.4Bn

• FAB’s TESS allocation is AED 8Bn

• As of March-end 2021, our customers benefitted from

deferrals under the TESS programme as well as from

Bank’s own initiatives:

• Majority of clients benefitting from relief measures are

corporates, mainly from trading, real estate (incl.

hospitality), construction and services sectors

The Group undertook a comprehensive portfolio review in Q2’20 in line with the UAE CB

guidance

• Preemptive action taken to identify clients benefitting under TESS under two main categories:

⏵Group 1: Borrowers temporarily and mildly impacted by COVID-19

⏵Group 2: Borrowers expected to be significantly impacted by COVID -19 in the long term

AED Bn TESS Non-TESS Total

as of Mar’21 4.4 0.4 4.8

as of Dec’20 3.5 0.7 4.2

Cumulative

since Apr’2010.4 1.1 11.5

Supplementary financial slides

2.7

4.2

8.2

Stage 1

Stage 2

Stage 3 +Adj POCI

41

NPLs and Loans/ECL by stage

Investor Presentation May 2021

NPLs1 by segment

66% 64% 67% 70% 69%

34% 36% 33% 30% 31%13.9 15.6 15.7 15.8 15.7

Mar'20 Jun'20 Sep'20 Dec'20 Mar'21

PB CIB (incl Subsidiaries)

3.0%3.3% 3.4% 3.6% 3.7%

5.2% 6.2% 5.6% 5.1% 5.2%

NPL

ratio

Loans by stage

354.5

20.0

15.7

Stage 1

Stage 2

Stage 3 +Adj POCI

AED 390.2Bn(Gross loans net of IIS)

Ratio% of gross loans

90.8%

5.1%

4.0%1

as of Mar’21

NPLs1 by sector (%)

ECL2 by stage

as of Mar’21

AED 15.1Bn

Energy, 1%

Manufacturing, 6%

Real Estate & Construction, 40%

Trading, 15%

Transport & Communication, 1%

Services, 3%Loan to Individuals, 32%

Others, 2%

1 NPLs = Stage 3 exposure + adjusted POCI (Purchase or originally impaired credit) of AED 4,929Mn as of Mar’21 considered as par to NPLs, net of IIS; Stage 3 + POCI, net of IIS as per Note #29 in Q1’21 financials is AED 15.8Bn

2 ECL = ECL on loans & advances (12.4bn) + ECL on unfunded exposures (0.9Bn) + IFRS9 impairment reserve (1.9Bn), IFRS9 specific reserve incl in Stage3 (1.2Bn), IFRS9 collective reserve incl in Stage2 (0.7Bn)

Note: Gross loans & advances and NPLs are net of interest in suspense; see Note #29 Credit Risk in Q1’21 financials for more details on IFRS9 exposures and ECL

(AED Bn)

(AED Bn) (AED Bn)

AED 15.7Bn

Mar’21

Supplementary financial slides 42

High-quality investment book

Investor Presentation May 2021

Investments by type

Investments by geography

Investment by ratings

Investments by counterparty

FVTPL - Debt, 13%

FVTPL - Equity & Funds, 1%

Amortised Cost (Debt Inv), 2%

FVOCI - Equity, 0.5%

FVOCI - Debt, 83%

AED 159.6Bn

Mar’21

AAA13%

AA32%

A27%

BBB9%

BB & below14%

Unrated -Debt 3%

Equity & Funds

2%

AED 159.6Bn

Mar’21

Europe17%

GCC16%

MENA (ex-GCC&UAE)6%

USA10%

Others incl A&NZ2%

Asia16%

UAE33%

AED 159.6Bn

Mar’21Sovereign

58%

GREs14%

Covered Bonds(Banks & FIs)

3%

Banks, 18%

Corporate/ Pvt Sector6%Supranatl, 1%

AED 159.6Bn

Mar’21

FVTPL – Fair value through profit or loss (previously HFT), Amortised cost – previously HTM, FVOCI – Fair value through other comprehensive income (previously AFS)

Sovereign bonds include sovereign guaranteed bonds issued by GREs, banks & FIs

Note: All totals are Gross investments before ECL

Supplementary financial slides

UAE72%

GCC 2%

Asia 2%

Europe12%

MENA2%

America9%

AED 568.3Bn

Mar’21

43

Customer deposits

Investor Presentation May 2021

Customer deposits by account type

Customer deposits by geography1

Customer Deposits

Customer deposits by counterparty

36% 38% 36% 41% 44%

497.1 518.7 601.8

540.9 568.3

Mar'20 Jun'20 Sep'20 Dec'20 Mar'21

Total Customer Deposits CASA

25% 24%

21% 19%

30% 33%

16% 15%

9% 9%

Dec'20 Mar'21

Certificates of deposits

Personal/retail sector

Corporate / private sector

Public Sector

Government sector

540.9568.3

59% 47%

39% 42%

2% 2%9% 9%1% 1%

Dec'20 Mar'21

Margin Accounts

Certificates of deposits

Saving Accounts

Current Accounts

Notice and time deposits

540.9 568.3

1 Based on deposit origination / coverage

2 Current, savings and call accounts; prior periods reclassified to include call accounts earlier grouped with notice and time deposits

2 (AED Bn)

(AED Bn)

(AED Bn)

Supplementary financial slides 44

Liability mix and funding profileLeading issuer in the MENA region – conventional, Sukuks and Green bonds

Investor Presentation May 2021

Medium-term wholesale funding

Due to Banks & Repos, 14%

Commercial Paper, 3%

Customer Deposits,

68%Term Borrowings &

Sub Debt, 8%

Others, 7%AED 838.0Bn

Mar’21

Liability mix

250

72

114

78

322

192

Cash &AAA/AAbonds

ST WholesaleFunding

CDs & CPs

DTB & Repos

AAA & AAbonds

Cash & Bal withCBs

Cash & AAA/AA bonds vs. ST wholesale4

(AED Bn)

1 All figures based on historical FX with the maturity of callables bonds set at next call date

2 Year-to-date as of 21 April 2021

3 For the remainder period of 2021

4 FAB has access to place deposits with ECB & FED

• AED 12Bn equivalent (USD 3.3Bn) ytd of senior wholesale

funding across multiple formats and 8 different currencies

• Inaugural Euro public transaction (EUR 750Mn 5-year) marking

the first MENA FI in this format since 2015

• Return to the Sterling market (GBP 400Mn short 5-year) where

FAB is the only MENA FI with public bonds outstanding

• CHF 260Mn long 6-year Public Green Bond which was the

largest ever CHF denominated Green Bond issued by a foreign

FI

• Regional leader in Green Bond issuance with over US$1Bn of

Green Bond notional outstanding across 5 transactions and 3

currencies

8,513

21,358

16,154

12,047

5,143

13,271 11,484

12,870

17,801

8,852

2018 2019 2020 2021 2021 2022 2023 2024 2025 2026

USD

CNH

GBP

CHF

EUR

Other

Year-to-date highlights:

Maturities1Issuances1 (AED Mn)

2 3

Supplementary financial slides 45

Diversified Term Funding portfolioFrequent Issuer across multiple products, currencies and geographies

Investor Presentation May 2021

Term Funding Portfolio by Type1

• Diversified investor base spanning Asia, the Middle East and Europe

• Active issuer across currencies with US$1bn equivalent or greater outstanding across each of USD, CNH, GBP, CHF and EUR

• Source and maturity profile of US$ denominated debt spread across multiple products

Term Funding Portfolio by Currency1

1. All figures based on historical FX

Asian Currency ex-

Formosa9% US$ Bullet

Private Placement

8%

European Currency

19%

Callables incl-Formosa

28%

US$ Public18%

Formosa Bullet18% Callable

42%

Sukuk Public23%

Formosa FRN19%

Conventional Public

4%

Private Placement

12%

USD67%CNH

9%

GBP6%

CHF7%

EUR6%

Other5%

Supplementary financial slides 46

Q1’21 financial highlights – Group financials

Investor Presentation May 2021 Scan to download full financials

Income Statement - Summary (AED Mn) Q1'21 Q4'20 QoQ % Q1’20 YoY %

Net interest Income 2,679 3,079 (13) 3,080 (13)

Non- interest Income 1,703 1,829 (7) 1,487 15

Total Operating Income 4,382 4,908 (11) 4,566 (4)

Operating expenses (1,318) (1,264) 4 (1,352) (3)

Operating profit 3,064 3,643 (16) 3,214 (5)

Impairment charges, net (470) (318) 48 (738) (36)

Non Controlling Interests and Taxes (118) (96) 24 (67) 76

Net Profit 2,476 3,230 (23) 2,408 3

Basic Earning per Share (AED)1 0.88 1.18 (26) 0.82 7

Balance Sheet - Summary (AED Bn) Mar'21 Dec'20 QoQ % Mar'20 YoY %

Loans and advances, net 378 387 (2) 382 (1)

Customer deposits 568 541 5 497 14

CASA (deposits) 250 223 12 181 38

Total Assets 941 919 2 835 13

Equity (incl Tier 1 capital notes) 103 109 (5) 94 10

Tangible Equity 73 79 (7) 63 15

Key Ratios1 (%) Q1’21 Q4’20QoQ

(bps)Q1’20

YoY

(bps)

Net Interest Margin 1.47 1.62 (15) 1.90 (43)

Cost-Income ratio (ex-integration costs) 29.6 25.7 385 29.1 47

Cost of Risk (bps) (loans & advances) 51 37 14 70 (19)

Non-performing loans ratio 4.0 4.0 5 3.5 49

Provision coverage 96 95 164 95 158

Liquidity Coverage Ratio (LCR) 141 143 (175) 110 >999

Return on Tangible Equity (RoTE) 12.8 16.4 (360) 13.0 (24)

Return on Risk-weighted Assets (RoRWA) 1.99 2.53 (54) 1.97 2

CET1 ratio 13.7 13.3 39 12.2 148

Capital Adequacy ratio 16.9 16.5 38 15.5 143

1 All ratios are annualised, where applicable

Supplementary financial slides 47

Q1’21 financial highlights – Segmental

Investor Presentation May 2021 Scan to download full financials

AED Mn Q1'21 Q4’20 QoQ % Q1’20 YoY %

Revenues 4,382 4,908 (11) 4,566 (4)

CIB 3,016 3,423 (12) 2,639 14

PB 1,440 1,536 (6) 1,643 (12)

HO & Subsidiaries (74) (51) 46 284 Na

UAE 3,570 4,082 (13) 3,838 (7)

International 812 825 (2) 728 12

Profit after taxes 2,479 3,236 (23) 2,399 3

CIB 2,064 2,507 (18) 1,709 21

PB 556 813 (32) 494 13

HO & Subsidiaries (141) (84) 67 195 Na

UAE 2,050 2,937 (30) 2,125 (3)

International 429 298 44 274 56

AED Bn Mar'21 Dec'20 QoQ % Mar'20 YoY %

Loans & advances, net 378 387 (2) 382 (1)

CIB 288 296 (3) 293 (2)

PB 89 90 (1) 88 1

HO & Subsidiaries 1 1 22 1 27

UAE 279 284 (2) 279 -

International 99 103 (3) 103 (4)

Customer deposits 568 541 5 497 14

CIB 487 457 7 421 16

PB 79 81 (1) 73 9

HO & Subsidiaries 2 3 (44) 3 (47)

UAE 411 406 1 374 10

International 157 135 16 123 28

Supplementary financial slides 48

A strong financial track recordBalance Sheet & Income Statement

Investor Presentation May 2021

TOTAL ASSETS (AED Bn) LOANS & ADVANCES (AED Bn) CUSTOMER DEPOSITS (AED Bn)

TANGIBLE EQUITY1 (AED Bn) OPERATING INCOME (AED Bn) NET PROFIT (AED Bn)

669.0

743.9

822.0

919.1

940.7

Dec'17

Dec'18

Dec'19

Dec'20

Mar'21

CAGR 2017-Q1’21: 11%

330.5

353.0

407.9

386.6

378.0

Dec'17

Dec'18

Dec'19

Dec'20

Mar'21

CAGR 2017-Q1’21: 4%

395.8

465.2

519.2

540.9

568.3

Dec'17

Dec'18

Dec'19

Dec'20

Mar'21

CAGR 2017-Q1’21: 12%

71.1

71.2

77.4

78.6

72.7

Dec'17

Dec'18

Dec'19

Dec'20

Mar'21

CAGR 2017-Q1’21: 1%

14.5

14.6

15.2

13.7

4.4

FY'17

FY'18

FY'19

FY'20

Q1'21

10.9

12.0

12.5

10.6

2.5

FY'17

FY'18

FY'19

FY'20

Q1'21

1 Post-dividend; Tangible equity = Total equity less minority interest, Tier 1 capital notes and intangible assets

Supplementary financial slides 49

A strong financial track record (…contd)Key ratios

Investor Presentation May 2021

NIM - YTD (%) NPL RATIO1 (%) PROVISION COVERAGE1 (%)COST-TO-INCOME RATIO - YTD (%)

(EX-INTEGRATION COSTS)

ROTE3 - YTD (%) RORWA - YTD (%)NON-INT INC / REVENUES (%) CET1 & CAR2 (%)

2.5 2.42.1

1.81.5

FY'17 FY'18 FY'19 FY'20 Mar'21

12.8 12.4 13.5 13.3 13.7

16.2 15.7 16.9 16.5 16.9

Dec'17 Dec'18 Dec'19 Dec'20 Mar'21

CET1 CAR

3.01 3.15 3.233.97 4.02

Dec'17 Dec'18 Dec'19 Dec'20 Mar'21

109 11093 95 96

Dec'17 Dec'18 Dec'19 Dec'20 Mar'21

27.7 25.8 26.7 27.0 29.6

FY'17 FY'18 FY'19 FY'20 Mar'21

33 3337

3430

FY'17 FY'18 FY'19 FY'20 Mar'21

14.616.2 16.1

13.0 12.8

FY'17 FY'18 FY'19 FY'20 Mar'21

2.26 2.46 2.562.13 1.99

FY'17 FY'18 FY'19 FY'20 Mar'21

1 2017 figures are pre-IFRS9 implementation

2 Capital ratios are post dividend as per UAE CB’s Basel III framework

3 Return on Average Tangible Equity, annualised; based on attributable profit to equity shareholders' excl Tier 1 notes coupon

Ratios annualised, based on actual/365 day count, where relevant

Appendix

50Investor Presentation May 2021

Appendix 51

UAE economic overviewDiversified economy with a strong fiscal position

Investor Presentation May 2021

1 IMF World Economic Outlook - April 2021

2 Federal Competitiveness and Statistics Authority, 2019 Nominal GDP Preliminary Estimates

A cosmopolitan country~11.1Mn people (2020e)1

Expatriates ~85%

2nd largest economy in GCC(35th largest in the world)

USD 354Bn 2020e Nominal GDP1

USD 31,982 GDP per capita

6th largest proven oil reserves~98Bn boe (~8% of global oil reserves)3

Current capacity ~4.0Mn barrels/day

One of the highest rated

sovereignsAa2 / AA-

Moody’s/ Fitch

Economy poised for a strong

recovery in 2021

Diversified & competitive

economy

75%non-oil sector

contribution

to nominal

GDP2

16th

ease of doing

business

rankings4

-8%

-4%

0%

4%

8%

2017 2018 2019 2020e 2021f 2022f

Real GDP Growth5

3 OPEC Annual Statistical Bulletin 2020; boe (barrel of oil equivalent)

4 World Bank’s Ease of Doing Business Rankings 2020

5 In-house GDP forecast for FY21 and FY22; IMF forecasts for prior years; FY21 GDP

growth has been revised from 2.9% communicated in Q1’21 earnings presentation

• The UAE’s policy response to the COVID-19 pandemic was

proactive and decisive in the form of fiscal and monetary stimulus

packages, including an AED 256Bn (USD 69.7Bn) stimulus plan

launched by the UAE Central Bank (more details on slide #52)

• Despite ongoing uncertainties, the country’s best in class COVID-19

vaccination programme is expected to drive UAE’s economic outlook with

the real GDP5 expected to grow by 2.4% in 2021, further supported by

tailwinds including stabilised oil prices and government stimulus

measures

• “The UAE plans to double the size of its economy over the next 10

years, implying a nominal GDP growth rate of 7% per annum (Target of

AED 3Tn)” – Minister of Economy, The National (News)

Nominal GDP breakdown2

14%

25%

9%

14%9%

29%

Construction and Real Estate

Mining and quarrying

Manufacturing

Trade, Restaurants & Hotels

Finance

Others

UAE

USD 421Bn

(2019)

Others include Agriculture, Utilities, Transportation, Communication, Government and Other activities

Appendix

Highest sovereign rating in MENAAa2 / AA / AA

Moody’s / S&P / Fitch

Major contributor to UAE GDPUSD 249Bn 2019e Nominal GDP1

59% of UAE’s 2019e Nominal GDP

3rd highest GDP per capita

in the worldUSD 85,6952

Strong fiscal positionSovereign foreign assets – 218% of GDP3

Government debt – only 16% of GDP4

On clear path to economic

diversification59% non-oil sector contribution to nominal GDP1,

up from 45% in 2013

Long term vision

To transform Abu Dhabi into a knowledge-

based economy and reduce its dependence on

the hydrocarbon sector

(2030 Economic Vision, Ghadan 2021)

52

Abu Dhabi - the capitalHighest rated ‘sovereign’ across MENA reflecting strong fiscal and external metrics

Investor Presentation May 2021

(Estimated population4 : 2.9 Mn)

1 Statistical Yearbook of Abu Dhabi 2020 as of 13th May 2020, preliminary estimates; Federal Competitiveness and Statistics Authority

2 After Luxembourg & Switzerland - IMF World Economic Outlook, April 2021; GDP per capita based on 2019e Nominal GDP, 2016 Population (SCAD)

“The ‘AA’ rating reflects Abu Dhabi's strong fiscal and

external metrics and high GDP per capita…

“Long term growth outlook is supported by continued

structural reforms. The government is undertaking further

reforms (…) including opening some sectors to 100%

foreign ownership and a relaxation of visa rules.”

Extract from Fitch report published on 29 October 2020, reaffirming

Abu Dhabi’s AA credit rating, with a stable outlook

In the context of COVID-19, Abu Dhabi announced that previously budgeted capital

expenditure plans would be maintained, and that oil production would be proactively

managed to stabilise oil prices and revenues

3 Fitch Ratings (29 October 2020)

4 S&P Global Ratings (26 March 2020)

Nominal GDP breakdown1

14%

41%

6%6%

8%

25%

Construction and Real Estate

Mining and quarrying

Manufacturing

Trade, Restaurants & Hotels

Finance

Others

Abu Dhabi

USD 249Bn

(2019)

Others include Agriculture, Utilities, Transportation, Communication, Government and Other activities

Appendix 53

Policy response to COVID-19 has been swift and effective

Investor Presentation May 2021

Monetary stimulus launched by the UAE

Central Bank - AED 256Bn (USD 70Bn)

• AED 50Bn (USD 13.6Bn) TESS1 facility to provide zero

interest rate collateralised loans to banks – utilisation down to

44% as of mid-Mar’21 from a peak of 89% as of end-July’20;

facility maturity was extended to 30 June 2022, after initial

extension to 30 June 2021, from original expiry date of 31 Dec

2020

• AED 61Bn (USD 16.6Bn) from reduction in cash reserve

requirements ratio on demand deposits to 7% from 14%

• AED 95Bn (USD 25.9Bn) Liquidity Buffer - flexibility to

maintain a minimum LCR of 70% (reduced from 100%) and a

minimum ELAR of 7% (reduced from 10%); additional

measure effective 8 Aug 2020 - minimum NSFR to 90% (from

100%) and maximum ASRR to 110% (from 100%)

• AED 50Bn (USD 13.6Bn) Relaxation in capital buffers –

60% of CCB (capital conservation buffer) and 100% of D-SIB

buffer (until 31 Dec 2021)

• Application of prudential filter by banks to incremental IFRS9

expected loss provisions (5-year phasing period ending 31

Dec 2024)

Stimulus package under Abu Dhabi’s Ghadan 21 initiative

• AED 6bn (USD 1.6Bn) supply chain initiative to increase liquidity for SMEs in various sectors.

Phase 1 of the initiative focuses on the healthcare sector and is delivered in partnership with

FAB and Daman

• AED 5bn (USD 1.4Bn) to subsidise water and electricity for citizens and commercial and

industrial activities, as well as to subsidise electricity connection fees for startups until the end

of 2020

• AED 3bn (USD 817Mn) allocated to SME credit guarantee scheme, to provide funding support

to SMEs and stimulate financing by local banks

• AED 1Bn (USD 272Mn) to establish a market maker fund, to enhance liquidity and sustain

balance between supply and demand for stocks

• Performance guarantees for projects up to AED 50Mn waived for startups

• Exemptions provided from, i) individual or commercial real estate registration fees, ii) annual

registration fees for commercial vehicles and, iii) toll gate tariffs for all vehicles until the end of

2020

• Rebates on rentals of up to 20% for restaurants and businesses in the tourism and

entertainment sectors

• Suspension of tourism & municipality fees for the tourism and entertainment sectors,

initially until the end of 2020, extended to 30 June 2021

1 TESS – Targeted Economic Support Scheme by UAE CB, April 2020

Appendix 54

Prestigious awards highlight FAB’s strength and industry expertise

Investor Presentation May 2021

MEA Finance• Best Neo Bank

• Best User Experience

Euromoney

• Best Investment Bank in the United Arab Emirates

• Best Bank for Transformation in Middle East

• Middle East’s Best Bank for Financing

• Middle East’s Best Bank for Corporate Responsibility

The Banker• Most Innovative Investment Bank from the Middle East

• Ranked 1st in UAE in Top 1000 World Banks 2020

Global Capital• Best Fixed Income of the Year

• Most Impressive Middle East Bank Issuer

Global Trade Review • Best Trade Finance Bank in MENA

Global Custodian

Magazine • Best UAE Custodian

Bonds, Loans &

Sukuk

• Best FI Deal of the Year 2018

• Financial Institution Funding Team of the Year

International Finance

Magazine• Best Cash Management Bank in the UAE

Asia Money • Middle East’s Best Banks for Asia

FinX Awards • Digital Transformation Leader of the Year

Wealthbriefing GCC

AWARDS• Fund Manager (Regional Reach)

MENA Fund Manager• Best Fixed Income of the Year

• UAE Asset Manager of the Year

Gulf Business • Banking Company of the year 2020

Global Finance

• Best Bank in UAE

• Best Equity Bank in the Middle East 2018-2021

• Best Investment Bank in the UAE 2018-2021

• Best Bank for Cash Management in the Middle East

• Best Bank for Payments & Collections

• Best Bank for Liquidity Management in the Middle East

• Safest Bank in the UAE

• Safest Bank in the Middle East

• Top 50 Safest Bank in Emerging Markets

• Top 50 Safest Commercial Bank

• Top 50 Safest Bank in the World

• The Innovators 2019 for Cash Management

• Best Trade Finance Provider in UAE

• Best FX provider in UAE

• Best Debt Bank in the Middle East

• Best Bill Payment & Presentment

EMEA Finance• Best Equity House in the Middle East

• Best M&A House in the Middle East

Seamless • Best Seamless Government Experience

The M&A

Atlas Awards• Emerging Markets M&A Deal of the Year

The Asian Banker • Strongest bank in the UAE and Middle East

Asset Asian Awards

• Sukuk House of the Year - UAE

• Best Islamic Deal of the Year

• Best Islamic Structured Trade Finance Deal of the Year

CMD Portal • Best Sukuk Issuer Award

Forbes • Ranked 1st in UAE in Forbes Global 2000 list

Scan to

download

For more information, please visit

www.bankfab.com or contact FAB Investor Relations team at

You can also download FAB’s Investor Relations App from

App Store /Google Play to access latest corporate updates

THANK YOU!