F ICT F ICT F 1 ( 2552 ) F F F 80 5 2550 F ( 6) F F F 10210 F(02 ...

Naomi-‐Jane Scroggins

Page 1 of 30

International Market Opportunity Proposal Of Brazil and Chile

For

Fisher & Paykel Appliances Limited

Student: Naomi-Jane Scroggins

Naomi-‐Jane Scroggins

Page 2 of 30

Executive Summary

Fisher and Paykel are Australasia’s leading manufacturer of innovative major

appliance products. The company has global manufacturing facilities located in

Mexico, Italy, the US and Thailand.

International growth objectives for the company are directly focused towards

continued growth and protection of Australasian markets whilst also seeking

profitable growth within niche market segments across other countries. Their market

entry strategies include a low-cost entry approach to build niche positions through the

commercial segment in selected cities.

The global economic downturn left Fisher & Paykel seriously exposed with

significant debt after implementing a global manufacturing strategy. Financial goals

were not met for the year ending 2011 with total revenue for the company down by

$83 million.

Brazil and Chile have been identified as candidates for international market expansion

of the Fisher and Paykel Brand. GDP and population differences between both

countries indicate that Brazil has a stronger and larger economy that is 12 times larger

than that of Chile. Brazil and Chile are both politically stable however corruption

appears to be a problem within the existing Brazilian government.

The refrigeration market in Brazil far outweighs that of Chile with Brazil selling

US$6.4 billion worth of refrigeration products in 2011 compared to Chile’s US$255

million. Investment in premium products is expected to grow within Brazil’s

refrigeration sector as middle-class consumers and those in high-income segments

choose to replace their refrigeration appliances with more technologically advanced

products.

Competitive intensity within the Brazilian sector was high with appliance giants

Whirlpool, Brastemp and Consul brands holding 45%, 25% and 20% market share

respectively. Competitive intensity is again high within Chile with CTI, Fensa and

Naomi-‐Jane Scroggins

Page 3 of 30

Mademsa holding 36%, 19% and 17% market share respectively. Refrigeration

products are mainly sold in Brazil through durable goods retailers, hypermarkets and

department stores. In comparison most consumers within Chile purchase refrigeration

goods through department stores only. Both markets have seen an increase in Internet

trading for the purchase of white ware goods.

Imports to Brazil are subject to a number of heavily structured taxes and tariffs when

bringing goods in from overseas. Chile has a free trade agreement with New Zealand

with a flat tariff rate of only 1.9%. In addition, it is cheaper to ship goods to Chile

than to Brazil.

Cultural differences are apparent between New Zealand, Brazil and Chile.

Fisher and Paykel should investigate the possibility of licensing agreements with

Brazilian refrigerator manufacturers to avoid Brazil’s high export/trade barriers. In

order to maximise the highest growth market within Brazil it is suggested that Fisher

and Paykel target the growing middle-class segment. It is also suggested that in

order to penetrate the market effectively, Fisher and Paykel target the middle-class

segment with an affordable alternative such as the Haier brand, to establish a foothold

and grow market share. Customisation of products to adapt to the Brazilian market is

suggested and cultural differences should be considered when tailoring promotional

strategies. Distribution networks should include durable goods retailers,

hypermarkets, and department stores. Pricing strategies should be focused towards

2011’s market average of US$885 per unit.

Naomi-‐Jane Scroggins

Page 4 of 30

Table of Contents

1 Table of Contents 2 Introduction .................................................................................................................... 5 3 Country Analysis ........................................................................................................... 7 4 Macroeconomic Indicators .......................................................................................... 7

4.1 Population, GDP & Economic Landscape .................................................................... 7 4.2 Political Landscape ............................................................................................................ 9 4.3 Culture ............................................................................................................................... 10

5 Microeconomic Indicators ........................................................................................ 12 5.1 Market Sizes ..................................................................................................................... 12 5.2 Growth Potential .............................................................................................................. 14

5.2.1 Brazilian Market Growth Potential .................................................................................... 14 5.2.2 Chilean Market Growth Potential ....................................................................................... 14

5.3 Competitive Intensity ...................................................................................................... 15 5.3.1 Brazilian Competitive Intensity .......................................................................................... 15 5.3.2 Chilean Competitive Intensity ............................................................................................. 17

5.4 Marketing Infrastructure .............................................................................................. 18 5.4.1 Refrigerator Products & Pricing ......................................................................................... 18 5.4.2 Distribution ................................................................................................................................ 19 5.4.3 Buyer Behaviour ...................................................................................................................... 19

5.5 Trade Barriers .................................................................................................................. 20 5.5.1 Brazilian Trade Barriers ........................................................................................................ 20 5.5.2 Chilean Trade Barriers ........................................................................................................... 21

5.6 Transportation ................................................................................................................. 21 5.6.1 Exporting From Thailand ...................................................................................................... 22 5.6.2 Exporting From Mexico ........................................................................................................ 22 5.6.3 Exporting From USA .............................................................................................................. 23 5.6.4 Exporting From Italy .............................................................................................................. 23 5.6.5 Importing To Brazil ................................................................................................................. 24 5.6.6 Importing To Chile .................................................................................................................. 24

5.7 Premium Market Potential ............................................................................................ 25 5.7.1 Brazil Premium Potential ...................................................................................................... 25 5.7.2 Chile Premium Potential ........................................................................................................ 25

6 Brazil & Chile - Country Criteria and Score ....................................................... 26 7 Recommendations ...................................................................................................... 27

7.1 Market Entry Mode ........................................................................................................ 27 7.2 Target Market .................................................................................................................. 27 7.3 Positioning ......................................................................................................................... 28 7.4 Standardisation vs Customisation ............................................................................... 28

References ........................................................................................................................... 29

Naomi-‐Jane Scroggins

Page 5 of 30

2 Introduction

Established in 1934, Fisher and Paykel Appliances Holdings Limited (FPAH) are

New Zealand’s leading brand of major household appliances. The company is the

foremost manufacturer of state-of-the-art innovative household appliances within

Australasia’s refrigerator and cookware categories. The company employs 3,500 staff

worldwide and currently operates in 50 countries including New Zealand, Australia,

Thailand, Singapore, USA, Canada and the UK. Fisher & Paykel’s product lines

include major kitchen appliances such as dishwashers, refrigerators, freezers, ovens,

cooktops and range hoods; the company also specialises in laundry appliances such as

washing machines and clothes dryers (Fisher & Paykel New Zealand Limited, 2012).

The company has widespread global production capacity with manufacturing facilities

located in Mexico, Italy, the US and Thailand (Euromonitor International, 2010).

Current revenues for the year ended 31 March 2012 was $891 million, down 7.6%

compared to the previous year. Current Export earnings for the year ended 31 March

2012 were $715M including Australian, North American, European and other global

markets (Fisher & Paykel, 2012).

The acquision of US manufacturer Dynamic Cooking Systems in 2004 provided F&P

an entry point into the US market, where it has positioned itself as a premium major

appliances brand. In December 2009, the company also successfully launched its

products within Sears, a major US department store chain (Euromonitor International,

2010). F&P’s sale of a 20% stake to Haier effectively provided the company with a

zero-cost entry approach to the Chinese market (Euromonitor International, 2010).

The company has also commenced sales within the Indian sector. The market entry

strategy is to target the specifier, designer and architect community, starting with one

distributor in the Delhi region (Fisher & Paykel, 2012).

As outlined in their 2012 Annual Report (Fisher & Paykel, 2012) the company’s

international growth objectives are directly focused towards continued growth and

protection of their existing home markets in New Zealand and Australia whilst also

Naomi-‐Jane Scroggins

Page 6 of 30

seeking profitable growth within niche market segments across North America and

other countries. The company has identified Chinese and Indian markets as a long-

term growth strategy – with both countries expecting double-digit growth in

appliances sales over the next five years. Their market entry strategies include a low

cost entry approach to build niche positions throughout the commercial segment in

selected cities.

The global economic downturn left Fisher & Paykel seriously exposed with

significant debt after implementing a global manufacturing strategy to support their

international growth objectives. The rising cost of production, a weak NZ dollar and

a slump in demand for Major Appliances as disposable incomes fell, all hit sales.

Following these losses the company has committed to re-aligning it’s manufacturing

strategy firstly to locate production as close as possible to new markets it is seeking to

develop and secondly to relocate manufacturing plants in less expensive labour

markets (Euromonitor International, 2010).

In addition, figures obtained from the F&P Annual Report indicate financial goals

were not met for the year ended 2011, with total revenue for the company down by

$83 million to $1,038 million. More specifically Appliances’ revenue was down

7.6% from $965 million to $891 million (Fisher & Paykel, 2012).

The existing Fisher and Paykel product range is currently targeted towards the

premium niche market segments. In targeting these small high-end market segments

the company is severely limited to maximising growth in the larger “affordable”

appliances market.

In order to meet the company’s international growth objectives Fisher and Paykel has

requested this report to investigate possible growth opportunities within Latin

America, specifically Brazil and Chile. Both countries have been researched based on

their suitability to meet Fisher and Paykel’s international growth objectives whilst

taking into account the company’s constraints in expanding to either of these markets.

In depth analysis and comparison of each market is provided (including macro and

micro level indicators) with final recommendations given on what market is more

attractive and what marketing approach should be undertaken.

Naomi-‐Jane Scroggins

Page 7 of 30

3 Country Analysis

Brazil and Chile have been identified as candidates for international market expansion

for the Fisher and Paykel brand. Both countries are located in Latin America and

have been assessed comparatively based on Fisher and Paykel’s international

marketing objectives and existing operating constraints.

Table 1 Comparative Macro Environment Indicators

Indicators Brazil Chile Population 205.7 million 1 16.8 million 3 GDP (US$) $2.4 billion 2 $248 million 2 GDP (PPP$) $2.2 billion 2 $299 million 2 Inflation % 6.6 1 3.1 3 Unemployment rate % 6.2 1 7.2 3 Per capita annual disposable income $US

$6,789 4 $7,184 5

Political stability Stable 1 Stable 3 Source: 1. (Marketline International, 2012) 2. (Euromonitor International, 2012) 3. (Marketline International, 2012) 4. (Euromonitor International, 2011) 5. (Euromonitor International, 2011)

4 Macroeconomic Indicators

4.1 Population, GDP & Economic Landscape

As shown in Table 1, the GDP and population differences between both countries

indicate that Brazil has a stronger and larger economy. With a population of 205.7

million, Brazil’s economy is 12 times larger than that of Chile and GDP of $2.4

billion far exceeds Chiles $248 million. However, Brazil’s inflation rate of 6.6% is

double that of Chile’s rate at 3.1%.

Due to a tightly regulated economy, Brazil has not been as badly affected as other

countries following the global economic downturn. As shown in Figure 1 Brazil’s

growth rate declined in 2008 reaching 5.8% due to tighter credit conditions and a slow

down in demand for Brazilian exports. GDP contracted by 0.6% in 2009 as a result of

the global economic crisis, however the Brazilian economy recovered strongly and

Naomi-‐Jane Scroggins

Page 8 of 30

grew by 7.5% in 2010. Monetary policy tightening by the Brazilian Central Bank

(BCB) to prevent the economy overheating resulted in a drop in growth of 3.25% in

2011. The government introduced an increase of 14.3% in minimum wages in early

2012 to help boost consumption and stimulate the economy. The Brazilian

government is expected to focus on an expansionary fiscal policy in 2012, supported

by an easing monetary policy and increased lending by the banking system.

According to Marketline forecasts, GDP is expected to grow at a rate of 3.2%

annually in 2012. Fiscal spending ahead of the 2014 presidential elections, the 2014

FIFA World Cup, and the 2016 Summer Olympics may see growth within the

Brazilian economy accelerate at a much faster rate (Marketline International, 2012).

Figure 1 Evolution of the Brazilian economy, 1991 - 2011

Source: (Marketline International, 2012)

Naomi-‐Jane Scroggins

Page 9 of 30

Figure 2 Chile – historical GDP growth, 1991 - 2010

Source: (Marketline International, 2012) As shown in Figure 2 Chile’s GDP grew at an annual rate of about 7% throughout the

1990’s, however this slowed towards the end of the decade as a result of the Asian

financial crisis. In recent years Chile has returned to the high growth rates it saw in

the 1990’s with 2004 and 2005 GDP growing by 6% and 5.6% respectively. Higher

energy prices and lagging consumer demand slowed the Chilean economy in 2006 to

4.3% and high copper prices had a positive effect increasing GDP to 5.1% in 2007.

The impact of the global economic crisis greatly affected Chile with GDP growth

declining to 3.1% in 2008 and the county contracting by 1.7% in 2009. Thorough

economic policies by the Chilean government in 2010 saw the economy bounce back

and grow by over 5.2% (Marketline International, 2012).

4.2 Political Landscape

Brazil is a stable democracy with changeovers between elected governments

predominantly smooth since the end of military rule in 1985. Various corruption

scandals however, have damaged the reputation of some politicians though regulatory

Naomi-‐Jane Scroggins

Page 10 of 30

institutions still remain solid. Despite the number of parliamentary commissions that

have been undertaken to investigate these scandals, those involved have been rarely

punished for their offences. The existing government headed by President Dilma

Roussef has adopted a more pro-Western policy in trade relations, and thus bilateral

ties with the US have significantly improved. Potential instability is a concern within

the Roussef administration due to disagreements with awkward coalition partners,

hindering legislative reforms. The government’s reform agenda for the near future is

not overly ambitious and is predominantly focused towards socioeconomic and

infrastructure improvements (Marketline International, 2012).

Following the end of General Augusto Pinochet’s dictatorship in 1973, Chile is still

recovering politically from the economic and political aftermaths of Pinochet’s rule,

which still continue to haunt the country. In terms of the World Bank’s Worldwide

Governance Indicators, which include voice, accountability and political stability

parameters, Chile far outperforms that of Brazil (Marketline International, 2012).

4.3 Culture

Cultural comparisons between New Zealand, Brazil and Chile have been researched

using Geert Hofstede’s classification scheme to understand the similarities and

differences between these societies.

As discussed by Hofstede, power distance is used to determine the attitude of a

specific culture towards the inequalities amongst society (Hofstede, 2012). New

Zealand scores low on this dimension (22) compared with those of Brazil and Chile

indicating a low hierarchical structure. At 69, Brazil reflects a society that believes

hierarchies should be respected and inequalities amongst people are acceptable, thus

power holders have more benefits than the less powerful in society. Status symbols of

power are crucial in indicating social positions and “communicate” the respect that

should be shown. Chile however, shows a lower score at 63 indicating an

intermediate to high position on this dimension. A hierarchical social structure is

present with status symbols used to emphasise power differences within Chilean

society. Privileges for power holders are common (Hofstede, 2012).

Naomi-‐Jane Scroggins

Page 11 of 30

Figure 3 Hofstede’s Cultural Comparison: New Zealand, Brazil & Chile

Source: (Hofstede, 2012) Individualism is used to determine the degree of interdependence a society maintains

amongst its members (Hofstede, 2012). Individualist societies are focused towards

taking care of themselves or direct family only. Within collectivist societies people

belong to ‘in groups’ that take care each other in exchange for loyalty. New Zealand

with a score of 79 is an individualist culture. Comparatively Brazil and Chile are

collectivist societies with lower scores of 38 and 23 respectively. These scores

indicate that in these countries people from birth onwards are integrated into strong

interconnected groups (especially represented by extended family), which continues

protecting its members in exchange for loyalty (Hofstede, 2012).

Masculinity/Femininity is used to indicate what motivates people. A high score

(masculine) indicates that society is driven by competition, achievement and success.

A low score (feminine) indicates that central values within society are caring for

others and quality of life (Hofstede, 2012). New Zealand scores high on this

dimension at 58 indicating that as a masculine society behaviour in school, work and

play are based on the shared values that people should “strive to be the best they can

be” and that success is important. Brazil has an equidistant score of 49 indicating that

the softer aspects of culture such as levelling with others, consensus, and sympathy

22

79 58

49 69

38 49

76 63

23 23

86

0 10 20 30 40 50 60 70 80 90 100

Dimension Rating

Cultural Dimension

Hofstede's Cultural Comparison: New Zealand, Brazil & Chile

New Zealand

Brazil

Chile

Naomi-‐Jane Scroggins

Page 12 of 30

for the underdog are valued and encouraged. Chilean society scores 23 on MAS

revealing that Chilean men and women are of a feminine character showing a modest

behaviour or attitude to one another. Chileans feel a sense of belonging within their

social groups and place value on approval and warm interpersonal links amongst their

groups. Thus they are more supportive of each other within social networks

(Hofstede, 2012).

Uncertainty avoidance (UAI) is used to measure the extent to which members of a

culture feel threatened by unknown situations and thus have created attitudes and

customs that try to avoid these insecurities (Hofstede, 2012). New Zealand scores 49

on this dimension and is a fairly laid back culture in terms of uncertainty avoidance.

New Zealander’s do not show much emotion, are fairly relaxed and not averse to

taking risks. Subsequently, there is a larger degree of acceptance for new ideas,

innovative products and a willingness to try something new or different. Brazil scores

76 on UAI showing a strong need for rules and legal systems in order to structure

society. Brazilians strive for happy relaxing moments throughout life, especially

spending time with family and friends. Due to this high score Brazilians are very

passionate and emotions are easily shown throughout their body language. Chile

scores very high on UAI and again show a strong need for rules and legal systems in

order to structure society (Hofstede, 2012).

Whilst long-term orientation is the fifth dimension in Hofstede’s cultural analysis, no

comparative data is available for Chile so this has not been given.

5 Microeconomic Indicators

5.1 Market Sizes

As shown in Figure 4, the refrigeration market size in value for Brazil far outweighs

that of Chile with Brazil selling $6.4 billion worth of refrigeration products in 2011

compared to Chile’s $255 million. Refrigeration appliances for Brazil increased by

17% in current value terms and 7% in volume terms for 2011, reaching 7.2 million

units (Figure 5). Comparatively refrigeration appliances for Chile increased by 13%

in current value terms and 10% in volume terms for 2011 reaching 492 thousand units

(Figure 5) (Euromonitor International, 2012).

Naomi-‐Jane Scroggins

Page 13 of 30

Figure 4 Value sales of refrigeration appliances in Brazil & Chile

Source: (Euromonitor International, 2012) Figure 5 Volume sales of refrigeration appliances in Brazil & Chile

Source: Euromonitor International

$2,960 $3,607

$4,581 $4,588

$5,478

$6,418

$164 $171 $178 $170 $226 $255

$-‐

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

2006 2007 2008 2009 2010 2011

Market Sizes Value US$ mn

Year

Sales of Refrigeration Appliances Value US$ mn -‐ 2006 -‐ 2011

Brazil

Chile

4,053 4,597

5,477 6,183

6,765 7,249

358 363 369 400 449 492

-‐

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2006 2007 2008 2009 2010 2011

Market Sizes Volum

e '000 Units

Year

Sales of Refrigeration Appliances Volume 2006 -‐ 2007

Brazil

Chile

Naomi-‐Jane Scroggins

Page 14 of 30

5.2 Growth Potential

5.2.1 Brazilian Market Growth Potential

The Brazilian government announced a reduction in Industrialised Product Tax (IPI)

beginning December 2011 for some categories within the major appliances sector.

Refrigeration appliances fell into this category, which will benefit from the tax

reduction. Fridges, fridge-freezers and freezers had their IPI reduced from 15% to 5%

until March 2012. It is unknown whether this reduction will be extended into the

foreseeable future (Euromonitor International, 2012).

Investment in premium products is expected to grow in the near future as middle-class

consumers and those in high-income segments choose to replace their existing

refrigeration appliances with more technologically advanced products. This is

predominantly driven by purchasing power and the improvement in payment facilities

at durable goods retailers (Euromonitor International, 2012).

Refrigeration appliances are expected to increase by 41% in constant value terms

from 2011 to 2016. More specifically fridge-freezers are expected to show the

strongest increase, with a CAGR of 9% in constant value terms. This growth in the

purchase of fridge-freezers is expected to increase due to low-income consumers

replacing their old fridges with fridge-freezers (Euromonitor International, 2012).

The Brazilian government is investing in new housing programs such as Minha Casa,

Minha Vida (My House, My Life), which is estimated to build two million homes for

the population. These strategies are expected to have a large impact on the sales of

major appliances, in particular refrigeration appliances, as these are considered

essential for Brazilians when purchasing a new home (Euromonitor International,

2012).

5.2.2 Chilean Market Growth Potential

Refrigeration appliances within the Chilean sector showed a positive volume trend

over the last decade and is expected to see interesting growth over the next five years

Naomi-‐Jane Scroggins

Page 15 of 30

of 5% CAGR in volume terms and 7% CAGR in current value terms, due to price

increases and the sale of higher-priced products (Euromonitor International, 2012).

Chile’s economy is strengthening due to the fact that consumers now have higher

disposable incomes. Unit sales of frost-free and bottom fridge-freezers are expected

to increase due to the better functionalities they offer to the average Chilean consumer

(Euromonitor International, 2012).

Government initiatives to reduce energy consumption are expected to result in a rise

in energy-efficient refrigeration products. This is due to the energy crisis, which has

affected Chile, and consumers are now more responsive towards the positive impact

of investing in energy-efficient appliances. This is expected to be a permanent trend,

as energy shortages are a growing problem for Chile (Euromonitor International,

2012).

Sales of fridge-freezers and electric wine coolers/chillers are expected to show the

highest growth over the next year with volume CAGRs of 5% and 7% respectively.

This is due in part to Chilean consumers choosing to purchase products with higher

quality, profiles and functionality (Euromonitor International, 2012).

5.3 Competitive Intensity

5.3.1 Brazilian Competitive Intensity

According to the latest data from Euromonitor International (Table 1), competitive

intensity amongst the Brazilian refrigeration sector in 2011 was high amongst

appliance giants with Whirlpool holding the largest volume share of 45%. This is due

in part to the company successfully targeting separate segments of the market with its

Brastemp brand aimed at higher-income consumers (25% share) and the Consul brand

targeting the lower-income segment (20% share). Electrolux do Brasil and Mabe

Eletrodomésticos ranked second and third behind Whirlpool with 34% and 17%

volume share respectively (Euromonitor International, 2012).

Mabe Eletrodomésticos has adopted a similar penetration strategy to Whirlpool, by

Naomi-‐Jane Scroggins

Page 16 of 30

discontinuing its Mabe brand in 2011, and concentrating its efforts towards targeting

separate segments with its Dako, Contintental and GE brands. GE is positioned

towards high-income consumers, Continental targets mainly the middle-classes and

Dako is positioned to cater for low-income consumers (Euromonitor International,

2012).

Korean appliance giants LG & Samsung are expected to threaten the market

dominance of both Whirlpool and Electrolux in the near future with both companies

investing in US$115 million (LG) and US$300 million (Samsung) to open new

manufacturing facilities located in the city of Sao Paolo (Euromonitor International,

2012).

In order to differentiate from other competitors within the sector, manufacturers

appear to be investing in technological innovations such as energy-efficiency,

functionality and design (Euromonitor International, 2012).

Table 1 Brand Shares of Refrigeration Appliances 2008-2011 (Brazil) % retail volume Brand Company 2008 2009 2010 2011 Electrolux Electrolux do Brasil SA 30.5 32.4 33.2 33.6 Brastemp Whirlpool S/A 26.2 25.5 24.9 24.5 Consul Whirlpool S/A 20.6 19.8 19.9 20.1 Dako Mabe Eletrodomésticos SA 6.1 6.2 6.4 6.7 Continental Mabe Eletrodomésticos SA - 3.9 3.1 4.0 GE Mabe Eletrodomésticos SA 3.5 3.8 3.6 3.8 Mabe Mabe Eletrodomésticos SA 1.2 2.3 3.0 1.7 Dynasty Full-Fit Indústria Importação e Comércio Ltda 0.3 0.4 0.5 0.6 Tocave Klar Indústria e Comércio de Eletro

Eletrônicos Ltda 0.3 0.4 0.4 0.4

Bosch Mabe Eletrodomésticos SA - 0.8 0.6 0.3 LG LG Electronics de São Paulo Ltda - 0.1 0.1 0.1 Suggar Suggar Electrodomésticos SA - 0.1 0.1 0.1 Continental BSH Continental Eletrodomésticos Ltda 3.4 - - - Bosch BSH Continental Eletrodomésticos Ltda 0.9 - - - Springer Springer Carrier Ltda 0.4 0.3 0.1 - Metalfrio Metalfrio Solutions Ltda 0.2 0.1 - - Brastemp Multibrás SA Eletrodomésticos - - - - Consul Multibrás SA Eletrodomésticos - - - - GE GE Dako SA - - - - Others 6.4 4.0 4.0 4.1 Total 100.0 100.0 100.0 100.0 Source: (Euromonitor International, 2012)

Naomi-‐Jane Scroggins

Page 17 of 30

5.3.2 Chilean Competitive Intensity

As illustrated in Table 2 competitive intensity in 2011 was high amongst the Chilean

refrigeration sector with CTI Cía Tecno Industrial (CTI) holding the largest volume

share at 36% with its Fensa (19%) and Mademsa (17%) brands. This leadership was

followed closely by LG Electronics Chile and Daewoo Electronics Corp holding 17%

and 11% volume share respectively (Euromonitor International, 2012).

CTI’s market dominance was due in part to CTI’s positioning towards high quality at

affordable prices, and its strong presence in static fridge-freezers. In contrast Korean

brands such as LG and Daewoo have positioned themselves as innovative, energy-

efficient and reasonably priced alternatives within the market (Euromonitor

International, 2012).

Samsung showed the fastest growth in 2011 with an increase of 4% market share

following the opening of its own office located in Santiago. CIT, LG and Daewoo

also showed an increase in their shares due to concentrated marketing efforts within

the industry (Euromonitor International, 2012).

Haier entered the market in the second half of 2011 with its wide portfolio of products

offering affordable and innovative alternatives to standard products within the sector.

These interesting alternatives show promise for Haier to be able to compete and

position themselves against leading brands Samsung, Daewoo and LG (Euromonitor

International, 2012).

Although price is still a leading factor within the Chilean refrigerator market, other

aspects such as quality, energy-efficiency, functionality and design are all influencing

consumers’ decision-making. Brands are now observing this trend and are acting

accordingly within certain segments (Euromonitor International, 2012).

Naomi-‐Jane Scroggins

Page 18 of 30

Table 2 Brand Shares of Refrigeration Appliances 2008-2011 (Chile) % retail volume Brand Company 2008 2009 2010 2011 Fensa CTI Cía Tecno Industrial SA 21.7 21.8 19.1 19.4 LG LG Electronics Chile 11.4 16.0 16.5 16.8 Mademsa CTI Cía Tecno Industrial SA 20.7 18.8 16.9 16.5 Daewoo Daewoo Electronics Corp Chile SA 6.6 5.7 10.7 10.9 Samsung Samsung Electronics Chile Ltda - - 9.0 9.4 Mabe Comercial Mabe Chile Ltda 1.7 3.6 6.7 6.4 Whirlpool Whirlpool Chile Ltda 8.7 10.8 5.3 5.4 Frigidaire Electrolux Chile SA 5.4 1.8 5.1 5.2 GE General Electric de Chile SA 4.8 2.9 3.4 2.4 Electrolux Electrolux Chile SA 1.1 2.6 2.4 2.0 Haier Climo Chile SA - - - 1.1 Sindelen Sindelen SA 1.9 2.6 0.2 0.2 Consul Whirlpool Chile Ltda 5.9 8.4 1.2 0.2 Bosch Emasa SA 1.5 0.5 0.2 0.2 Samsung RCL Distribución Ltda 7.0 2.5 - - Albin Trotter Albin Trotter SA 0.1 - - - LG Coelsa SA - - - - Private Label Private Label 0.2 0.2 0.2 0.3 Others 1.2 1.9 2.9 3.7 Total 100.0 100.0 100.0 100.0 Source: (Euromonitor International, 2012)

5.4 Marketing Infrastructure

5.4.1 Refrigerator Products & Pricing Table 3 Market Sizes Retail Selling Price (Brazil & Chile US$)

Refrigeration Appliances 2006 2007 2008 2009 2010 2011 Brazil $730.2 $784.6 $836.3 $742.1 $809.8 $885.4 Chile $459.3 $471.8 $482.3 $426.4 $503.1 $517.0

Source: (Euromonitor International, 2012) Refrigeration products within the Brazilian market include built in refrigeration

appliances, freestanding refrigeration appliances, electric wine coolers/chillers,

freezers, fridge freezers and fridges. The average retail selling price of refrigeration

appliances within the Brazilian sector are provided in the table above. Prices are

given in $US for comparison (Euromonitor International, 2012).

Refrigeration products within the Chilean market include freestanding refrigeration

appliances, electric wine coolers/chillers, freezers, fridge freezers and fridges. The

average retail selling price of refrigeration appliances within the Chilean sector are

Naomi-‐Jane Scroggins

Page 19 of 30

provided in the table above. Prices are given in $US for comparison (Euromonitor

International, 2012).

5.4.2 Distribution

According to research obtained from Euromonitor International (2012), Refrigeration

products throughout Brazil are mainly sold through durable goods retailers, which

accounted for 37% volume share of sales in 2011, this was closely followed by

hypermarkets with 29% volume share and finally department stores with 23% share.

Consumers are also turning to Internet retailing due to the convenience of consumers

comparing prices and payment facilities (Euromonitor International, 2012).

Research obtained from Euromonitor International (2012), indicates that for the year

2011, the main distribution channel for refrigeration appliances throughout Chile was

department stores with almost three out of four purchases made through this channel.

This prevalence to purchase through department stores is due to increased access to

credit, allowing Chilean consumers to buy major appliances. In addition, DIY and

hardware stores are gaining traction within the market due to better pricing and

promotions. Internet trading has also seen major growth due to an increase in trust

and online trade (Euromonitor International, 2012).

5.4.3 Buyer Behaviour

Brazil is experiencing a period of prosperity, due to the decrease in the economic gap

between the rich and the poor. This expanding middle class is allowing more

Brazilians the opportunity to have a stable job and greater remuneration than in the

past. This new middle class is composed of about 94.9 million people and many are

choosing to invest in their homes, increasingly spending on more sophisticated

products including household appliances as many do not possess a microwave, a

decent refrigerator a functioning stove. This consumer has become and will continue

to be the main purchasing consumer in the near future (Euromonitor International,

2012).

Naomi-‐Jane Scroggins

Page 20 of 30

Chilean consumers are optimistic about their financial futures and the direction of

their economy, with consumer confidence at it’s highest in 2 years. Most Chileans

choose to shop in malls and 97% of big-ticket items are brought in retail stores. In

general, Chileans go to more than one store to compare prices and those consumers

who are computer savvy generally undertake Internet browsing. Online shopping has

seen a boom with per capita online spending increasing from CLP$7,400 to

CLP$23,000 in 2011. A study by the University of Chile undertaken in 2011 revealed

that 51% of Internet buyers choose to buy online because prices are more competitive

(Euromonitor International, 2012).

5.5 Trade Barriers

5.5.1 Brazilian Trade Barriers

Imports to Brazil are subject to a number of heavily structured taxes and tariffs when

bringing in goods from overseas. These fees, which are usually paid during customs

clearance and account for the bulk of import costs, include Import Duty (II),

Industrialised Product Tax (IPI) and Merchandise and Service Circulation Tax

(ICMS). There are also a number of smaller taxes and fees that should be accounted

for. The Import Duty (II) tax is required under government law and ranges from 10%

to 35%, levied on a CIF (Cost, Insurance and Freight) basis (New Zealand Trade &

Enterprise, 2011).

Brazil is included in the Mercosur partners trade agreement including Argentina,

Paraguay and Uruguay. The Mercosur Common External Tarrif (CET) maintains a

separate exemption list of items for tariffs, allowing free trade between member

countries (New Zealand Trade & Enterprise, 2011).

The Brazilian government however, announced a reduction in the Industrialised

Product Tax (IPI) following weak GDP in 2010. This reduction included specific

categories, including refrigeration products in the major appliances sector.

Refrigerators, fridge-freezers and freezers had their IPI reduced from 15% to 5% until

March 2012. It is unclear whether this initiative would be extended into the

foreseeable future (Euromonitor International, 2012).

Naomi-‐Jane Scroggins

Page 21 of 30

5.5.2 Chilean Trade Barriers

Exporting products to Chile are subject to relatively low import barriers and most

goods imported from New Zealand enter Chile duty free. The country utilises the

Harmonised System for tariffs and has a flat uniform rate of 6%, although New

Zealand has a free-trade agreement with Chile, lowering the effective rate to 1.9%

(New Zealand Trade & Enterprise, 2011).

In November, 2006 New Zealand, Singapore, Brunei and Chile signed the Trans-

Pacific Partnership Agreement (TPP). This multilateral free-trade agreement aims to

integrate the economies of the Asia-Pacific region. Five additional countries,

including Australia, Malaysia, Peru, United States and Vietnam, are currently

negotiating to join the group (New Zealand Trade & Enterprise, 2011).

The majority of imports can enter Chile free from controls, however there is a

document called the Informe de Importacion that is required for all goods entering the

country. An import registration tax of 3% applies based on the cost, insurance and

freight (CIF) value of imports and is paid at the issue of the Informe de Importacion.

The tax value is deducted from the import duty payment on the import of goods as

they enter the country (New Zealand Trade & Enterprise, 2011).

All imported goods are required to pay a Value Added Tax (VAT) rate of 19%

calculated on the CIF value of the good. It should be noted that importers can

generally recover taxes paid in imports and in some cases can defer payment of duties

and VAT for up to five years (New Zealand Trade & Enterprise, 2011).

5.6 Transportation

Fisher and Paykel Appliances Limited has numerous manufacturing facilities located

in Thailand, Mexico the US and Italy. The cost to export a standard container of

goods from these locations has been provided below in US$.

Naomi-‐Jane Scroggins

Page 22 of 30

5.6.1 Exporting From Thailand

Thailand ranks 17 in the ranking of 183 economies on the ease of trading across

borders globally. In order to export a standard 20-foot container of goods by ocean

from Thailand requires 5 documents including certificate of origin, customs export

declaration, commercial invoice, terminal handling receipts and bill of lading. Total

export clearance procedures takes 14 days and costs US$625 (The World Bank,

2012). These export procedure costs are broken down and provided in Table 4 below.

Table 4 Procedures & Costs – Exports from Thailand Procedures to Export Time (days) Cost (US$) Documents preparation 8 $290 Customs clearance and technical control 1 $50 Ports and terminal handling 3 $85 Inland transportation and handling 2 $200 Totals 14 $625 Source: (The World Bank, 2012)

5.6.2 Exporting From Mexico

Mexico ranks 59 in the ranking of 183 economies on the ease of trading across

borders globally. In order to export a standard 20-foot container of goods by ocean

from Mexico requires 5 documents including bill of lading, customs export

declaration, commercial invoice, certificate of origin and packing list. Total export

clearance procedures takes 12 days and costs $US1450 (The World Bank, 2012).

These export procedure costs are broken down and provided in Table 5 below.

Table 5 Procedures & Costs – Exports from Mexico Procedures to Export Time (days) Cost (US$) Documents preparation 6 $200 Customs clearance and technical control 2 $150 Ports and terminal handling 2 $200 Inland transportation and handling 2 $900 Totals 12 $1450 Source: (The World Bank, 2012)

Naomi-‐Jane Scroggins

Page 23 of 30

5.6.3 Exporting From USA

The United States ranks 20 in the ranking of 183 economies on the ease of trading

across borders globally. In order to export a standard 20-foot container of goods by

ocean from the United States requires 5 documents including bill of lading, certificate

of origin, commercial invoice and customs export declaration. Total export clearance

procedures takes 6 days and costs $US1050 (The World Bank, 2012). These export

procedure costs are broken down and provided in Table 6 below.

Table 6 Procedures & Costs – Exports from USA Procedures to Export Time (days) Cost (US$) Documents preparation 2 $190 Customs clearance and technical control 1 $60 Ports and terminal handling 2 $400 Inland transportation and handling 1 $400 Totals 6 $1050 Source: (The World Bank, 2012)

5.6.4 Exporting From Italy

Italy ranks 63 in the ranking of 183 economies on the ease of trading across borders

globally. In order to export a standard 20-foot container of goods by ocean from Italy

requires 4 documents including bill of lading, customs export declaration, commercial

invoice and technical standard/health certificate. Total export clearance procedures

takes 20 days and costs $US1245 (The World Bank, 2012). These export procedure

costs are broken down and provided in Table 7 below.

Table 7 Procedures & Costs – Exports from Italy Procedures to Export Time (days) Cost (US$) Documents preparation 10 $220 Customs clearance and technical control 3 $155 Ports and terminal handling 3 $345 Inland transportation and handling 4 $525 Totals 6 $1245 Source: (The World Bank, 2012)

Naomi-‐Jane Scroggins

Page 24 of 30

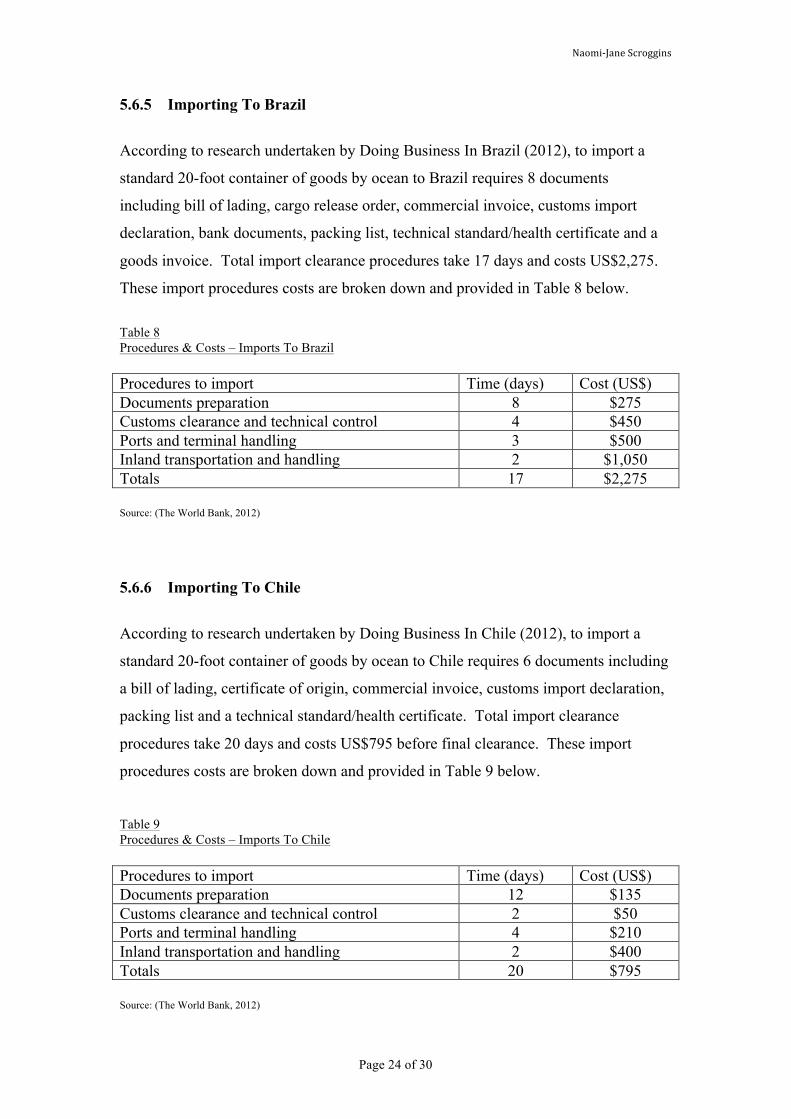

5.6.5 Importing To Brazil

According to research undertaken by Doing Business In Brazil (2012), to import a

standard 20-foot container of goods by ocean to Brazil requires 8 documents

including bill of lading, cargo release order, commercial invoice, customs import

declaration, bank documents, packing list, technical standard/health certificate and a

goods invoice. Total import clearance procedures take 17 days and costs US$2,275.

These import procedures costs are broken down and provided in Table 8 below.

Table 8 Procedures & Costs – Imports To Brazil Procedures to import Time (days) Cost (US$) Documents preparation 8 $275 Customs clearance and technical control 4 $450 Ports and terminal handling 3 $500 Inland transportation and handling 2 $1,050 Totals 17 $2,275 Source: (The World Bank, 2012)

5.6.6 Importing To Chile

According to research undertaken by Doing Business In Chile (2012), to import a

standard 20-foot container of goods by ocean to Chile requires 6 documents including

a bill of lading, certificate of origin, commercial invoice, customs import declaration,

packing list and a technical standard/health certificate. Total import clearance

procedures take 20 days and costs US$795 before final clearance. These import

procedures costs are broken down and provided in Table 9 below.

Table 9 Procedures & Costs – Imports To Chile Procedures to import Time (days) Cost (US$) Documents preparation 12 $135 Customs clearance and technical control 2 $50 Ports and terminal handling 4 $210 Inland transportation and handling 2 $400 Totals 20 $795 Source: (The World Bank, 2012)

Naomi-‐Jane Scroggins

Page 25 of 30

5.7 Premium Market Potential

5.7.1 Brazil Premium Potential

Due to increased purchasing power amongst Brazil’s middle-class, consumers are

now purchasing more value-added products within the refrigeration sector such as

stainless steel and personalised colours. The activities by Korean giants Samsung and

LG to open new manufacturing facilities in order to assemble more higher value

products, shows a significant growing trend towards this market. There is a growing

trend towards luxury products such as electric wine coolers/chillers fuelled by the

growing sales of wine in Brazil (Euromonitor International, 2012).

5.7.2 Chile Premium Potential

Data obtained from Euromonitor International suggests that more consumers are

beginning to demand premium products within the refrigeration sector. A study from

McCann Erickson shows that 54% of Chileans are wishing to choose energy-efficient

refrigeration products at a higher price than standard products within the market.

Although mid-priced double door fridge freezers currently hold 94% of the market,

they are slowly losing share to more expensive and innovative models. There is also a

growing trend towards the purchase of luxury refrigeration products such as electric

wine coolers/chillers (Euromonitor International, 2012).

Naomi-‐Jane Scroggins

Page 26 of 30

6 Brazil & Chile - Country Criteria and Score Table 10 Country Criteria and Score Analysis Brazil Chile Criteria Factor

Weight R A R A

Market Growth (10 = high growth potential)

20.00% 8.00 1.60 6.00 1.20

Hofstede’s Culture Score 5.00% 5.00 0.25 3.00 0.60 Distributors 10.00% 8.00 0.80 7.00 0.70 Market Size – GDP (1 = smallest)

20.00% 8.00 1.60 2.00 0.40

Competitive Intensity (1 = strong)

10.00% 1.00 0.10 4.00 0.40

Trade Barriers (1 = high)

20.00% 1.00 0.20 7.00 1.40

High-End Market Potential (10 = high niche potential)

15.00% 6.00 0.90 4.00 0.60

Total 100.00% 5.45 5.30

Naomi-‐Jane Scroggins

Page 27 of 30

7 Recommendations

Based on the research obtained and comparisons made against the export markets

discussed in this report; in order to meet Fisher & Paykel’s international growth

objectives it is suggested that the most appropriate country for market entry is Brazil.

Although weighted scores on the comparison table were relatively close, the Brazilian

market has been chosen due to its higher score, larger market, and its growth

opportunities.

7.1 Market Entry Mode

With Fisher and Paykel’s strategy towards a low cost entry approach it is suggested

that the company should investigate the possibility of licensing agreements with

Brazilian refrigerator manufacturers to avoid Brazil’s high trade barriers.

Alternatively, should Fisher and Paykel wish to import goods to Brazil from its

manufacturing facilities located overseas, it is suggested that these are shipped from

it’s Thai manufacturing facility due to the low export costs from this location.

However, there are limitations within this report, such as the ability to obtain full

shipping costs from each of these locations. It is advised that full costs are obtained

for comparison to confirm that shipping from Thailand is the most cost-effective

route. With the market growth potential available in Brazil, the costs to import are far

outweighed by this opportunity.

7.2 Target Market

In order to maximise the highest growth market within Brazil it is suggested that

Fisher and Paykel target the growing middle-class segment. This market has the

potential to demand more premium product availability as consumers within this

segment choose to invest in their homes.

Naomi-‐Jane Scroggins

Page 28 of 30

7.3 Positioning

Many consumers within the growing middle-class segment may still be demanding

premium products at an affordable price. It is suggested that in order to penetrate the

market, Fisher and Paykel target this segment with an affordable alternative such as

the Haier brand, to establish a foothold and grow market share. Future strategies

could involve the introduction of Fisher and Paykel branded products with value-

added innovative technology positioned towards the high-cost premium segment.

7.4 Standardisation vs Customisation

In order to penetrate the Brazilian market effectively it is suggested that further

research be undertaken to determine the exact requirements Brazilian consumers

demand, with regards to buying a refrigerator. Although there is a growing trend

towards premium products, value-added alternatives may differ in functionality and

design to those products that are already manufactured by the Fisher and Paykel

brand. Customisation of products to adapt to the Brazilian market is therefore

suggested.

Due to the cultural differences between New Zealand and Brazil it is suggested that

marketing programs are customised to suit the Brazilian market. Brazil is a

collectivist culture therefore products many not diffuse as quickly through the market

than programs adapted for New Zealand’s individualist society. To overcome

Brazil’s high uncertainty avoidance, Fisher and Paykel should offer tactics to

encourage Brazilians to try their products. This could include the use of opinion

leaders within Brazilian society and the use of extended warranty periods on the

purchase of Fisher and Paykel branded refrigerators.

It is advised that products are distributed through the use of durable goods retailers,

hypermarkets and department store channels. Internet retailing should also be

considered due to the growing trend towards this alternative. Pricing strategies should

be focused and targeted towards 2011’s average RSP of US$885.

Naomi-‐Jane Scroggins

Page 29 of 30

References Euromonitor International. (2010). Fisher & Paykel Industries Ltd in Consumer Appliances: World. London: Euromonitor International. Euromonitor International. (2011). Income & Expenditure: Brazil. London: Euromonitor International. Euromonitor International. (2011). Income & Expenditure: Chile. London: Euromonitor International. Euromonitor International. (2012). Market Sizes: Brazil & Chile. London: Euromonitor International. Euromonitor International. (2012). Refrigeration Appliances In Brazil. London: Euromonitor International. Euromonitor International. (2012). Refrigeration Appliances In Chile. London: Euromonitor 2012. Fisher & Paykel. (2012, March 31). Annual Reports. Retrieved August 6, 2012, from Fisher & Paykel: http://www.fisherpaykel.co.nz/global/investors/reports.cfm Fisher & Paykel New Zealand Limited. (2012, August 28). Who We Are. Retrieved August 28, 2012, from Fisher & Paykel: http://www.fisherpaykel.co.nz/global/company/who_we_are.cfm Hofstede, G. (2012, September 11). National Culture: Countries. Retrieved September 11, 2012, from Geert Hofstede: http://geert- hofstede.com/countries.html New Zealand Trade & Enterprise. (2011). Exporter Guide Brazil: Country Profile. New Zealand Trade & Enterprise. New Zealand Trade & Enterprise. (2011). Exporter Guide Chile: Country Brief. New Zealand Trade & Enterprise. Marketline International. (2012). Brazil In Depth Pestle Analysis. London: Marketline International. Marketline International. (2012). Chile In Depth Pestle Analysis. London: Marketline International. The World Bank. (2012). Doing Business In Brazil. Washington DC: The World Bank. The World Bank. (2012). Doing Business In Chile. Washington DC: The World Bank.

Naomi-‐Jane Scroggins

Page 30 of 30

The World Bank. (2012). Doing Business In Italy. Washington DC: The World Bank. The World Bank. (2012). Doing Business In Mexico. Washington, DC: The World Bank. The World Bank. (2012). Doing Business In Thailand. Washington DC: The World Bank. The World Bank. (2012). Doing Business in The USA. Washington DC: The World Bank.

Copyright © 2022 FDOKUMEN