Industry Internship and Report on

98

Industry Internship and Report on A STUDY ON WORKING CAPITAL MANAGEMENT AT ANUGRAHA TOURS AND TRAVELS BY NISHMITHA N M 1NZ16MBA42 Submitted to DEPARTMENT OF MANAGEMENT STUDIES NEW HORIZON COLLEGE OF ENGINEERING, OUTER RING ROAD, MARATHALLI, BANGALORE In partial fulfillment of the requirements for the award of the degree of MASTER OF BUSINESS ADMINISTRATION Under the guidance of INTERNAL GUIDE EXTERNAL GUIDE Ms. KERENA ANAND M. DEVA RAO Senior Assistant Professor Anugraha Tours and Travels 2016-2018

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of Industry Internship and Report on

Industry Internship and Report on

A STUDY ON WORKING CAPITAL MANAGEMENT AT ANUGRAHA

TOURS AND TRAVELS

BY

NISHMITHA N M

1NZ16MBA42

Submitted to

DEPARTMENT OF MANAGEMENT STUDIES

NEW HORIZON COLLEGE OF ENGINEERING,

OUTER RING ROAD, MARATHALLI,

BANGALORE

In partial fulfillment of the requirements for the award of the degree of

MASTER OF BUSINESS ADMINISTRATION

Under the guidance of

INTERNAL GUIDE EXTERNAL GUIDE

Ms. KERENA ANAND M. DEVA RAO Senior Assistant Professor Anugraha Tours and Travels

2016-2018

CERTIFICATE

This is to certify that NISHMITHA N M bearing USN 1NZ16MBA42, is a bonafide student of

Master of Business Administration course of the Institute 2016-2018, autonomous program,

affiliated to Visvesvaraya Technological University, Belgaum. Internship report on “A STUDY

ON WORKING CAPITAL MANAGEMENT AT ANUGRAHA TOURS AND TRAVELS”

is prepared by her under the guidance of Ms. KERENA ANAND, in partial fulfillment of

requirements for the award of the degree of Master of Business Administration of Visvesvaraya

Technological University, Belgaum Karnataka.

Signature of Internal Guide Signature of HOD Signature of Principal

DECLARATION

I, NISHMITHA N M , hereby declare that the Internship report entitled “A STUDY ON

WORKING CAPITAL MANAGEMENT AT ANUGRAHA TOURS AND TRAVELS”

prepared by me under the guidance of Ms. KERENA ANAND , faculty of M.B.A Department,

New Horizon College of Engineering and external assistance by M. DEVA RAO, Proprietor

,ANUGRAHA TOURS AND TRAVELS.

I also declare that this Internship work is towards the partial fulfillment of the university

regulations for the award of the degree of Master of Business Administration by Visvesvaraya

Technological University, Belgaum.

I have undergone an industry internship for a period of Twelve weeks. I further declare that this

report is based on the original study undertaken by me and has not been submitted for the award

of a degree/diploma from any other University / Institution.

Signature of Student

Place: Bangalore

Date

ACKNOWLEDGEMENT

I take this opportunity to express my gratitude and profound thanks to our chairman DR.

MOHAN MANGHNANI and our respected Principal DR. MANJUNATHA.

I express my sincere thanks and deep sense of gratitude to our Head of Department DR.

SHEELAN MISRA and my Internal Guide Ms. KERENA ANAND, Department of

Management Studies for providing me with an opportunity to study and for her encouragement,

support and guidance to complete this project work successfully.

The internship opportunity I had with ANUGRAHA TOURS AND TRAVELS was a great

chance for learning and professional development. Therefore, I consider myself as a very lucky

individual as I was provided with an opportunity to be a part of it. I am also grateful for having a

chance to meet so many wonderful people and professionals who led me though this internship

period.

I express a deep sense of gratitude to my External Guide M. DEVA RAO, Proprietor, Augraha

Tours and Travels for taking part in useful decision and giving necessary advices and guidance

and arranged all facilities to make life easier. I choose this moment to acknowledge his

contribution gratefully.

Finally, I express my sincere thanks and deep sense of gratitude to my parents and friends for

giving timely advice in all the ways and in all aspects for doing the project

Name of the Student with USN

NISHMITHA N M

1NZ16MBA42

TABLE OF CONTENTS

Chapter

No.

Title

Page No.

Executive Summary

1

Theoretical background of the study

1-33

2

Industry and Company profile

34-56

3

Research Methodology

57-62

4

Data Analysis and Interpretation

63-78

5

Finding, Suggestions and Conclusion

79-81

6

Learning Experience

82

Bibliography

Annexure(s)

LIST OF TABLES

Table No.

Particulars

Page No.

Table - 4.1

Table showing working capital ratio of Anugraha Tours

and Travels

63

Table - 4.2

Table Showing Current ratio of Anugraha Tours and

Travels

65

Table - 4.3

Table showing Cash ratio of Anugraha Tours and

Travels

67

Table - 4.4

Table showing Fixed asset turnover ratio of Anugraha

Tours and Travels

69

Table - 4.5

Table showing Debtors turnover ratio of Anugraha

Tours and Travels

71

Table - 4.6

Table showing Asset turnover ratio of Anugraha Tours

and Travels

73

Table - 4.7

Table Showing Current asset to Total asset ratio of

Anugraha Tours and Travels

75

Table - 4.8

Table Showing Working Capital Turnover ratio of

Anugraha Tours and Travels

77

LIST OF CHARTS

Chart No.

Particulars

Page No.

Chart - 4.1

Chart showing working capital ratio of Anugraha Tours

and Travels

64

Chart - 4.2

Chart Showing Current ratio of Anugraha Tours and

Travels

66

Chart - 4.3

Chart showing Cash ratio of Anugraha Tours and

Travels

68

Chart - 4.4

Chart showing Fixed asset turnover ratio of Anugraha

Tours and Travels

70

Chart - 4.5

Chart showing Debtors turnover ratio of Anugraha

Tours and Travels

72

Chart - 4.6

Chart showing Asset turnover ratio of Anugraha Tours

and Travels

74

Chart - 4.7

Chart Showing Current asset to Total asset ratio of

Anugraha Tours and Travels

76

Chart - 4.8

Chart Showing Working Capital Turnover ratio of

Anugraha Tours and Travels

78

EXECUTIVE SUMMARY

It is compulsory for every student to take up a project work in an industry, besides it gives an

exposure of working atmosphere of the office, it also gives an experience, to apply the

theoretical knowledge that we have learnt, to the practical problems of the Industrial project that

they undertake.

Therefore, I have taken up the project at Anugraha Tours and Travels, and have undertaken the

study in Working Capital Management. This study will help the company in the better

management of its working capital and thus improve the performance of company.

The goal of working capital management is to ensure that a firm is able to continue its operations

and that it has sufficient ability to satisfy both maturing short-term debt and upcoming

operational expenses. The management of working capital involves managing inventories,

accounts receivable and payable, and cash. The objective of the study is to study the concept and

importance of working capital management, to study and analysis the working capital trend

through ratio analysis, to study the Liquidity position of Anugraha Tours and Travels, to suggest

measures for effective management of working capital,this study will help us to know the

financial position of the company and this study is to carry out a critical analysis of Anugraha

Tours and Travels working capital.The study of working capital is based on tools like ratio

analysis, statement of changes in working capital.

The financial statements (mainly balance sheet along with profit & loss accounts) are used to

work out various ratios which help us in better understanding the organization’s working capital

management. Ratio analysis is been done by studying the past performance of the organization

and by doing so other relevant details are also studiedThe analysis and interpretation has been

carried out by preparing tables and by using the graphs which is shown in pictorial

representation.

Scanned with CamScanner

Scanned with CamScanner

1

CHAPTER -1

THEORETICAL BACKGROUND OF THE STUDY

INTRODUCTION

Business concern needs finance to meet their requirement in the economic world. Any kind of

business activity depends on the finance. Hence, it is called as lifeblood of business organization.

Whether the business concerns are big or small, they need finance to fulfil their business

activities.

In the modern world, all the activities are concerned with the economic activities and very

particular to earning profit through any venture or activities. The entire business activities are

directly related with making profit. (according to the economic concept of factors of production,

rent given to landlord, wage given to labour interest given to capital and profit given to

shareholders or profiteers), a business concern needs finance to meet all the requirements. Hence

finance may be called as capital, investment, fund etc. but each term is having different meanings

and unique characters. Increasing the profit is the main aim of any kind of economic activity.

Finance is the lifeblood of every business activity without which the wheels of modern business

organization system cannot be greased.

MEANING OF FINANCE

Finance may be defined as the art and science of managing money. It includes financial service

and financial instruments. Finance also is referred as the provision of money at the time when it

is needed. Finance function is the procurement of funds and their effective utilization in business

concerns.

The concept of finance includes capital, funds, money, and amount. But each word is having

unique meaning. Studying and understanding the concept of finance become an important part of

the business concern.

2

DEFINITION OF FINANCE

According to khan and Jain, ―finance is the art and science of managing money‖.

According to Simon Andrade Finance is "Area of economic activity in which money is the basis

of the various embodiments, whether stock market investments, real estate, industrial,

construction, agricultural development, so on. ", and "Area of the economy in which we study

the performance of capital markets and supply and price of financial assets‖

According to Howard and Upton, ―finance may be defined as that administrative area or set of

administrative functions in an organization which relates with the arrangement of each and credit

so that the organization may have the means to carry out the objectives as satisfactorily as

possible.

TYPES OF FINANCE

Finance is one of the important and integral part of business concerns, hence, it plays a major

role in every part of the business activities. It is used in all the area of the activities under the

different names.

Finance can be classified into two major parts:

3

FINANCIAL MANAGEMENT

Finance management is managerial activity, which is concerned with planning and controlling

of the firm‘s financial Resources. It was a branch of economics till 1890, and as a separate

discipline, it is of recent origin. Still, it has no unique body of knowledge of its own, and draws

heavily on economics for its theoretical concepts even today. Finance is a scarce resource and it

has to be managed efficiency for the successful functioning of any company. Several companies

have come to grief mainly because of inefficient management of finance in spite of other

favourable conditions.

DEFINITION OF FINANCIAL MANAGEMENT

According to Solomon and Pringle Financial Managment, "is concerned with the efficient use of

an important economic resource, namely, capital funds."

AccordingTo Walker, "Financial Management is the application of planning and control

function to the finance functions."

SCOPE OF FINANCIAL MANAGEMENT

Financial management is one of the important part of overall management, which is directly

related with various functional departments like personnel, marketing and production. Financial

management covers wide area with multidimensional approaches. The following are the

important scope of financial management.

Financial management and economics

Economic concepts like micro and macroeconomics are directly applied with the financial

management approaches. Investment decisions, micro and macro environmental factors are

closely associated with the functions of financial manager. Financial management also uses the

economic equations like money value discount factor, economic order quantity etc. financial

economics is one of the emerging area, which provides immense opportunities to finance, and

economical areas.

4

Financial management and accounting

Accounting records includes the financial information of the business concern. hence, we can

easily understand the relationship between the financial management and accounting. In the

olden periods, both financial management and accounting are treated as a same decision. But

nowadays financial management and accounting discipline are separate and interrelated.

Financial management or mathematics

Modern approaches of the financial management applied large number of mathematical and

statistical tools and techniques. They are also called as econometrics. Economic order quantity,

discount factor, time value of money, present value of money, cost of capital structure theories,

dividend theories, ratio analysis and working capital analysis are used as mathematical and

statistical tools and techniques in the field of financial management.

Financial management and production management

Production management is the operational part of the business concern, with helps to multiple

the money into profit. Profit of the concern depends upon the production performance.

Production performance needs finance, because production department requires raw material,

machinery, wages, operating expenses etc. these expenditures are decided and estimated by the

financial department and the financial manager allocates the appropriate finance to production

department. The financial manager must be aware of the operational process and finance

required for each process of production activities.

Financial management and marketing

Produced goods are sold in the market with innovative and modern approaches. For this the

marketing department needs finance to meet their requirements. The financial management is

responsible to allocate the adequate finance to the marketing department. Hence, marketing and

financial management are interrelated and depends on each other‘s.

Financial management and human resource

Financial management is also related with human resource department, which provides

manpower to all the functional areas of the management. Financial manager should carefully

evaluate the requirement of manpower to each department and allocate the finance to the human

resource department as wages, salary, remuneration, commission, bonus, pension and other

5

monetary benefits to the human resource department. Hence, financial management is directly

related with human resource management.

WORKING CAPITAL MANAGEMENT

Working capital management Is a relationship between a firm's short-term assets and its

short-term liabilities. The working capital management is used to ensure that a firm is able to

continue its operations and it has sufficient ability to satisfy both short-term debt and upcoming

operational expenses. The management of working capital involves managing inventories,

accounts receivable and payable, and cash.

DEFINITION

According to Hoagland, ―Working capital is descriptive of that capital which is not fixed. But the

more common use of the working capital is to consider it as the difference between the book

value of the current assets and the current liabilities‖.

According to Field, Backer and Maillot, ―Working capital means a sum of current assets only‖.

According to Lincoln, Saliers, Stevens, ―Working capital means current assets less current

liabilities‖.

NATURE OF WORKING CAPITAL

Working capital management is concerned with the problems that arise in attempting to manage

the current assets, the current liabilities and the interrelationship that exists between them. The

term current assets refer to those assets, which in the ordinary course of business can be, or will

be, converted into cash within one year without undergoing a diminution in value and without

disrupting the operations of the firm. Current liabilities are those liabilities, which are intended,

at their inception, to be paid in the ordinary course of business, within a year, out of the current

assets or earnings of the concern. The goal of working capital management is to manage the

firm‘s current assets and liability in such a way that satisfactory level of working capital is

6

maintained. The interaction between current assets and current liabilities is, therefore, the main

theme of the theory of working management.

The working capital management may be defined as the management of firm‘s source and uses

of working capital in order to maximize the wealth of shareholders. The proper working capital

management requires both medium term planning (up to 3 years) and also the immediate

adoption to change arising due to fluctuations in operating levels of firm.

CLASSIFICATION OF WORKING CAPITAL

WORKING CAPITAL IS CLASSIFIED AS

1. ON THE BASIS OF CONCEPT

Gross Working Capital

Refers to the firm‘s investment in current assets. Current assets are the assets which can be

converted into cash within an accounting year and include cash, short-term securities, debtors,

bills receivable and stock.

Networking Capital

Refers to the difference between the current assets and current liabilities. Current liabilities are

those claims of outsiders, which are expected to mature for payment within an accounting year

On the basis of concept On the basis of time

Gross Working

Capital

Net Working

Capital Permanent or

Fixed Working

Capital

Temporary or

variable Working

Capital

Regular Working

Capital

Reserve Working

Capital Seasonal Working

Capital

Special Working

Capital

7

and include creditors, bills payable, and out-standing expenses. Net working capital can be

positive or negative. A positive net working Capital will arise when current assets exceed

current liabilities. A negative networking capital occurs when current liabilities are in excess of

current assets.

NET WORKING CAPITAL = CURRENT ASSETS – CURRENT LIABILITIES

Current assets Current liabilities

Cash Accounts Payable

Accounts Receivable Notes payable

Notes Receivable Accrued expenses

Marketable securities Taxes payable

Inventory short term loans

Prepaid expenses Bank overdraft

Total current assets Total current liabilities

2. ON THE BASIS OF TIME

Permanent or Fixed Working Capital:

Permanent or Fixed working capital is the minimum amount which is required to ensure effective

utilization of fixed facilities and for maintaining the circulation of current assets. It also refers to

the Hard core working capital. There is always a minimum level of current assets which is

continuously required by the enterprise to carry out its normal business operations. For example,

every firm has to maintain a minimum level or raw material, work-in-process, finished goods,

and cash balance. This minimum level of current assets is called permanent or fixed working

capital as this part of capital is permanently blocked in current assets.

The permanent working capital can be further be classified as:

(a) Regular Working Capital

(b) Reserve Working Capital

8

Regular working capital required to ensure circulation of current assets from cash to inventories,

from inventories to receivables and from receivables to cash and so on.

Reserve working capital is the excess amount over the requirement for regular working capital,

which may be provided for contingencies that may arise at unstated periods such as strikes, rise

in prices, depression, etc.

Temporary or Variable Working Capital

Temporary or variable working capital is the amount of working capital, which is required to

meet the seasonal demands and some special exigencies. Variable working capital can be further

classified as seasonal working capital and special needs. The capital required to meet the

seasonal needs of the enterprise is called seasonal working capital.

Special working capital is that part of working capital which is required to meet special

exigencies such as launching of extensive marketing campaigns for conducting research, etc.

FACTORS DETERMINING WORKING CAPITAL

The actual amount of working capital requirements differs from industry to industry and from

business unit to unit.

Nature of Industry

While determining the amount of working capital requirements, the financial executive has to

consider the nature of industry in which his company is operating. The business may be

manufacturing, trading or rendering a service. A trading unit dealing in the sale and purchase of

goods would require more of working capital.

Size of the business unit

Size of a business unit means its scale of operations. If a company is operating its business in

national and international markets, its working capital requirements would be regular than a

company operating in a local or state-level market.

9

Terms of purchase and sale

If an entrepreneur is buying its requirements such as raw materials, inventories etc. Strictly on a

cash basis, then his working capital requirements would be fairly large. On the other hand, if he

avails of credit facilities, his working capital requirements would be relatively lower. Similarly,

credit sales will require larger working capital while cash sales will require lower working

capital.

Inventory Turnover

If the inventory turnover is high, the working capital requirements will below. But if

inventories large and their turnover is slow, a company would require large working capital.

Importance of Labour

Industries which are capital-intensive will require lower working capital, while labour-intensive

industries will need a larger working capital.

Length of Processing Period

The longer the period of manufacturing the finished products, the greater would be the

requirements of working capital. On the other hand, a simple and short period process of

production will be required lower working capital.

Proportion of raw material to total costs

If a company is using costly raw materials, it will require a larger working capital. If raw

materials are cheap, then it would require a lower working capital.

Seasonal Variations

During the busy season, a business enterprise needs a larger, working capital while during the

slack season, it requires a lower working capital.

Changes in technology

Technological changes related to the manufacturing process have a sharp impact on the need for

large working capital.

10

Inflation

As a result of inflation in the economy, working capital requirements increase, whereas during

the time of a recession, it decreases.

Growth and Expansion

With the normal rate of expansion in the volume of business, the economy would require a larger

amount of working capital.

Profit Planning and control

The amount of working capital needed is decided by the management in accordance with its

policy profit planning and control.

INTERPRETATIONS OF WORKING CAPITAL CONCEPTS

There are two possible interpretations of the working capital concepts.

1. Balance sheet concept

There are two interpretations of working capital under the balance sheet concept working capital

is represented by the excess of current assets over current liabilities and is the amount normally

available to finance current operations. But, sometimes working capital is also used as a

synonym for gross or total current assets. In that case, the excess of current assets over current

liabilities is called the Net Working Capital.

However, there are certain arguments when it comes to supporting the above mentioned views of

working capital. Few economists‘ support that current assets should be considered as working

capital as the whole of it helps to earn profits and the management is more concerned with the

total current assets as they constitute the total funds available for operational purposes. On the

contrary, other economists argue that –

a. In the long run what matters is the surplus of current assets over current liabilities.

b. It is this concept, which helps creditors and investors to judge the financial soundness of

the enterprise.

11

c. What can always be relied upon to meet the contingencies, is the excess of current assets

over current liabilities since this amount is not to be returned and

d. This definition helps to find out the correct financial position of companies having the

same amount of current assets.

2. Operating Cycle Concept

Investment in working capital is influenced by four key events in the production and sales cycle

of the firm.

Purchase of the raw materials.

Payment of raw materials.

Sale of finished goods

Collection of cash for sales.

The cycle begins with the purchase of raw materials, which are paid for after a delay, which

represents the accounts payable period. The firm coverts the raw materials into finished goods

and then sells the same. The time lag between the purchase of raw materials and the sale of

finished goods is the inventory period. Customers pay their bills sometime after the sales. The

period that elapses between the date of sales and the date of collection of receivables in the

accounts receivable period.

Cash

Purchase

s Collections

Materials

Inventory

Accounts

Receivable

Sales

Finished

Inventory

Accounts

Payable

Production

12

The time that elapses between the purchase of raw material and the collection of cash for sales is

referred to as the operating cycle, whereas the time length between the payment of raw material

purchases and the collection of cash for sales is referred to as the accounts receivable period,

whereas the cash cycle is equal to the operating cycle less the accounts payable period.

CASH MANAGEMENT

Cash, the most liquid asset, is of vital importance to the daily operations like acquiring supplies,

resources, equipments etc., used in generating the products and services provided by the firm and

making payments like wages and salaries to the workers and managers, taxes to the government,

etc., of business firms. More fundamentally, cash is the medium of exchange, which allows

management to carry on the various activities of this business firms from day to day. While the

proportion of corporate assets held in the form of cash is very small its efficient management is

crucial to the solvency of the business because in a very important sense cash is the focal point of

funds flows in a business.

MOTIVES FOR HOLDING CASH

There are three possible motives of holding of cash

Transaction motive

Firms need cash to meet their transaction need. The collection of cash from sale of goods and

services, sale of assets and additional financing is not perfectly synchronized with the

disbursement of cash for purchase of goods and services, acquisition of capital assets and

meeting other obligations. Hence, some cash balance is required as a buffer.

Precautionary motive

There may be some uncertainty about the magnitude and timing of cash inflows from the sales to

goods and services, sale of assets and issuance of securities. Likewise, there may be uncertainty

about cash outflows on account of purchases and other obligations. To protect itself against such

uncertainties, a firm may required some cash balance.

13

Speculative motive

Firms would like to tap profit – making opportunities arising from fluctuations in commodity

prices, security prices, interest rates and foreign exchange rates. A cash – rich firm is better

prepared to exploit such bargains. Hence, firms which have such speculative leanings, may carry

additional liquidity. However, for most firms there reserve, borrowing capacity and marketable

securities would suffice to meet their speculative needs.

CASH BUDGETING

Cash budgeting or short term cash forecasting is the principle tool of cash management cash

budget, routinely prepared by business firms are helpful in

Estimating Cash requirements

Planning short term financing.

Schedule payments in connection with capital expenditure projects.

Planning purchases of materials,

Developing credit policies.

Checking the accuracy of long term forecasts.

Short term cast forecasting

Firms use multiple short term forecasts for varying lengths and detail, suited to meet different

needs. The point to be emphasized here is that the multiple formats used by the firms for cash

forecasting serves different purposes and should not be regarded as mutually exclusive. The

principle method of short term forecasting is the receipts and payments method.

Receipts and payment method.

The cash budget prepared under this method shows the timing and the magnitude of expected

cash receipts and cash payments over the forecast period. It includes all expected cash receipts

and cash payments irrespective of how they are classified in accounting.

14

RECEIVABLES MANAGEMENT

Receivable management refers to the decisions a business makes regarding its overall credit and

collection policies and the evaluation of individual credit applicants. Receivable management

proves for a firm both an asset and a problem of an asset because of the promise of a future cash

flow and a problem because of the need to obtain financing while waiting for the future cash

flow.

Trade credit is considered as an essential marketing tool, acting as a bridge for the movement of

goods through production and distribution stages to customers. A firm grants trade credit to

protect it sales from the competitors and to attract potential customers to buy its products on

favorable terms. This creation of credit and creating debtors result in creation of receivables.

Thus granting credit and creating debtors amounts to the blocking of the firms funds. The

interval between the date of sales and the date of payment that is the operating cycle has to be

financed out of working capital. This necessitates the firms to get funds from banks or other

sources. Thus, trade debtors or receivables represent investment. As substantial amounts are tied

up in trade debtors, it needs careful analysis and proper management.

Receivables

Receivables are defined as an asset account representing the claims of a firm against its

customers, which is the result of credit sales of goods / services in the ordinary course of

business. So receivables are the result of extension of credit facilities to the customers.

Purposes of receivables.

The purpose of receivables is directly related with the objectives of credit sales. The objectives

of credit sales are

Achieving growth in sales

By selling goods on credit, a firm will generally be in a position to sell more goods that if it

insisted on immediate cash payment.

15

Increase in profits

Increase in profits result in higher profits for the firm not only because of increase in volume of

sales but also because of the firm charging a higher margin of profit on credit sales as compared

to cash sales.

Meeting competition

A firm may have to resort to granting of credit to its customers because of similar facilities being

granted by the competing firms to avoid the loss of sales from customers who would buy

elsewhere if they did not receive the expected credit.

The overall objective of committing funds to accounts receivable is to generate a large flow of

operating revenue and hence profit than what would be achieved in the absence of no such

commitment.

Cost of maintaining receivable

The cost with respect to maintenance of receivables can be identified as follows.

1. Capital costs

Maintenance of accounts receivable results in blocking of the firms financial resources with

them. Thus is because there is a time lag between the sales of goods to customers and the

payment by them. The firm has therefore to arrange for additional funds to meet its own

obligations such as payment to employees, suppliers of raw materials, etc., while waiting for

payments for its customers, so to raise the additional funds so as to meet its requirements the

firm incurs a cost called capital cost.

2. Administration cost

The firm has to incur additional administrative costs for maintaining account receivable in the

form of salaries to the staff kept for maintaining accounting record related to customer and to

determine their credit worthiness.

16

3. Collection costs

This refers to the costs incurred by a firm for collection of payments from its credit customers.

4. Defaulting costs

Sometimes after making all the serious efforts to collect money from the defaulting customers,

the firm may not be able to recover the over dues because of the inability of the customers. Such

debts are treated as bad debts and have to be written off since they cannot be realized.

So creation of receivables is a double edged weapon. If it is created and administered well it may

result in increase in sales and hence profits, but if there is any complacence on the part of the

management in the administration of receivables, it will increase the chances of bad debts and

may cause overall decline in profits of the firm. Hence the management should formulate on

optimum credit policy for the efficient management and administration of receivables.

CREDIT POLICY

The term Credit policy refers to those decision variables that influence the amount of trade credit

that is, the investment in receivables.

Credit policy Variables

Credit Standards

Credit Period

Cash Discount

Collection Efforts.

A firm‘s credit policy as a matter of fact, determines the amount of risk a firm is willing to

undertake in its sales activities. The extent of risk and return involved in receivables is largely

based on the credit policy adopted by a firm. Broadly speaking credit policy of a firm can be of

the following two types.

17

a) Lenient (liberal) Credit Policy

b) Stringent Credit Policy

EFFECTS OF LENIENT (LIBERAL) CREDIT POLICY

INCREASE IN SALES

Liberal credit policy will result in increase in the sales of goods and services, due to the

availability of easy terms and standards of credit provided by a firm due to the customers.

INCREASE IN PROFIT

Increase in sales will ultimately result in the increase in profits of the organization.

Increase in cost of maintenance of receivables

Liberal credit policy demands more investment in receivables and bad debts. The various costs,

which may increase due to increase in the amount of receivable, are – capital costs

administration costs, collection costs and defaulting costs.

EFFECTS OF STRINGENT CREDIT POLICY

LESS SALES

As a stringent credit policy restricts the level of extension of credit to its customers it may result

in less sales because of the movement of the customers towards other competent firm in the

industry granting credit facilities on easy terms and standards.

LESS PROFIT

Decrease in the level of sales will ultimately result in the decrease in the level of profit also.

Decrease in cost of maintenance of receivables.

18

As in the case of stringent credit policy, the scope of credit creation is reduced, so there is an

overall reduction in the cost of their maintenance and the risk of bad debts are also reduced.

Thus a lenient credit policy and stringent credit policy approaches are both on two extremes.

Neither of them can therefore help in efficient receivables management. The trade off between

these two that is the optimum credit policy can give satisfactory results.

OPTIMUM CREDIT POLICY.

Having established the optimum credit policy and the terms of sales to be offered the firm must

evaluate the credit worthiness of individual credit applicants and consider the possibilities of bad

debts or scope of payments. In judging the credit worthiness of an applicant the three basic

factors – the three C‘s are character, capacity and collateral.

Character

It refers to the willingness of the customer to honour his obligations.

Capacity

Capacity refers to the customer to pay in time. It depends on the financial situation particularly

the working capital position and profitability of the debtor.

Collateral

Represents security offered by the firm in the form of mortgages.

The credit evaluation procedure involves three steps – obtaining information on the applicants,

analyzing this information to determine the applicants credit worthiness and making credit –

granting decision.

19

NEED FOR WORKING CAPITAL

Working capital gives an idea of the solvency of a concern. Its proper calculations provide to

the business, the right amount of cash to maintain regular outflow of in operation.

If proper cash balance is maintained the business can avail of the cash discount facilities

offered to it by suppliers. Besides, it enhances the image reputation of the concern.

The concern by maintaining an adequate amount of working capital is able to maintain a

sound bank credit, trade credit, and can escape insolvency, take advantage of cash discount

facility offered by suppliers by making prompt payment and bargain profitability in any

business transaction.

Besides, the basic objectives of financial management‘s object of maximizing shareholder‘s

wealth can be realized only when the concern continues to earn profits year after year.

Moreover, fixed assets cannot work without working capital.

ADEQUACY OF WORKING CAPITAL

Working capital should be adequate for the following reasons:

1. It protects a business from the adverse effects of shrinkage in the values of current assets.

2. It is possible to pay all the current obligation promptly and to take advantage of cash

discounts.

3. It ensures to greater extent the maintenance of a company‘s credit standing and provides for

such emergencies as strikes, floods, fire etc.

4. It permits the carrying of investments at a level that would enable a business to serve

satisfactorily the needs of its customers.

5. It enables a company to operate its business more efficiency because there is no delay in

obtaining materials etc., because of credit difficulties.

INADEQUACY OF WORKING CAPITAL

1. When working capital is adequate, a company faces following problems:

2. It stagnates growth becomes difficult for the firm to undertake profitable projects for no

availability of working capital funds.

20

3. Difficulty in implementing operation plan and achieving the firm‘s profit target.

4. Operating inefficiencies creep in which it becomes difficult even to meet day- to- day

commitments.

5. Fixed assets are not utilized efficiently thus the firm‘s profitability would deteriorate.

6. Paucity of working capital funds renders the firm unable to avail attractive credit

opportunities.

7. The firm loses its reputation when it is not in a portion to honor it short- term obligation

thereby lending to tight credit items.

DANGERS OF WORKING CAPITAL

Too much working capital is as dangerous as too little of it. Excessive working capital raises the

following problems:

1. Result in unnecessary accumulations of inventories. Thus, chance of inventories means

handling, waste, theft and losses increased.

2. Indication of defective credit policy and slack collection period. Consequently, it results in

higher incidents of bad debts, adversely affecting profits.

3. Makes the management complacent which degenerates in to managerial inefficiency.

4. The tendencies of accumulation inventories to make speculative profits, which tend to

liberalize the divided policy, make it difficult for the concern to cope in the future when it is

not able to make speculative profits.

5. A company may enjoy high liquidity and, at the same time, suffer from low profitability.

6. There may be an imbalance between liquidity and profitability.

7. A company may invest heavily in its fixed assets equipment‘s, which may not be justified by

actual sales and production.

EFFECTS OF INADEQUATE WORKING CAPITAL

1. A company cannot utilize its production capacity for the want of working capital.

2. The credit worthiness of the company is likely to be jeopardized because of lack of

liquidity.

21

3. Modernization of equipment and even routine and maintenance facilities may be difficult

to administer.

4. A company will not be able to pay dividend because of non-availability of funds.

5. A company may have to borrow funds at exorbitant rates of interest.

6. Its low liquidity may lead to low profitability in the same way as low profitability results

in low liquidity.

SOURCES OF WORKING CAPITAL FINANCE

The major sources, financing the working capital are:

1. Trade credit

2. Bank credit

3. Factoring of receivables

4. Commercial paper

SOME OF THE OTHER SOURCES OF THE WORKING CAPITAL

FINANCIAL ARE:

Long term financing:

Loans from financial institutions

Floating debentures

Accepting public deposits

Issue of shares

Raising funds by internal financing

Short – term financing

Short term bank loans

Commercial paper

Factoring of receivables

Spontaneous financing

Trade credit

Outstanding expenses

22

SCIENTIFIC APPROACH TO WORKING CAPITAL

In a simple study undertaken by A.K. Mukherjee of 20 central government undertakings

production non- homogenous products during the period 1947-1979, the following observation

were made.

Their overall investments represented 60% to 70% to the total current assets.

Considering the government policies regarding the size of inventory which was prescribed as

more that 6 months operational requirement the size of inventories was found to be much

more than the norms prescribed by the government.

Receivable represented 12% to 16% of the total current assets of the units. As a whole,

receivable position was not satisfactory.

Investments in cash and near- cash items represent 8% to 13% of the total current assets.

Overall investments in cash were found to be equal to one to 1 to 4 months operational which

showed poor liquidity.

WORKING CAPITAL CYCLE:

Cash flows in a cycle into, around and out of business. It is the business‘s life blood and every

manager‘s primary task is to help keep it flowing and to use the cash flow to generate profits. If a

business is operating profitability, then it should, in theory, generate cash surpluses.

If it doesn‘t generate surpluses, the business will eventually run out of cash and expire. Click

here for more information about the vital distinction between profit and cash flow.

There are two elements in the business cycle that absorb cash – inventory (stocks and work –in-

progress) and receivables (debtors owing you money). The main sources of cash are payables

your creditors) and equity and loans.

23

Each component of working capital (namely inventory, receivables and payables) has two

dimensions TIME and MONEY. When it comes to managing working capital – TIME IS

MONEY. If you can get money to move faster around the cycle (e.g. reduce inventory levels

relative to sales), the business will generate more cash or it will need to borrow less money to

fund working capital. As a consequence, you could reduce the cost of bank interest or you‘ll

have additional free money available to support additional sales growth or investment.

RATIOS

Ratio analysis is the process of determining and interpreting numerical relationships based on

financial statements. A ratio is a statistical yardstick that provides a measure of the relationship

between two variables or figures.

Ratio analysis is the process of examining and comparing financial information by calculating

meaningful financial statement figure percentages instead of comparing line items from each financial

statement.

24

RATIO ANALYSIS:

Ratio analysis is a widely used tool of financial analysis. It is defined as the systematic use of

ratios to interpret the financial statements so that the strengths and weaknesses of a firm as well

as its historical performance and current financial condition can be determined. The term ratio refers to

the numerical or quantitative relationship between two items/ variables.

This relationship can be expressed as:

1. Percentages, say, net profits are 25% of sales (assuming net profits of 25000 and sales of rest.

100000)

2. Fraction (net profit is one fourth of sales), and

3. Proportion of numbers (the relationship between net profits and sales is 1:4)

These alternative methods of expressing items which are related to each other are, for purpose of

financial analysis, referred to as ratio analysis. Ratios are relative figures reflecting the relationship

between variables. It concentrates on the inter-relationship among the figures appearing in the financial

statements. They enable analysis to draw conclusion regarding financial operations. Ratio analysis helps

us to analyze the past performance of the company and to make future projections.

MEANING OF RATIO ANALYSIS

This analysis is the most widely used tool of analysis. ―A ratio is a quotient of two numbers and is an

expression of relationship of two numbers and is an expression of relationship between figures or two

amounts.‖ It indicates a quantitative relationship which is used for a quantified judgment and decision

making or it can be defined as a ―the indicated quotient of two mathematical expressions‖ and as ―the

relationship between two or more things or figures, expressed mathematically, is known as financial

ratios.

25

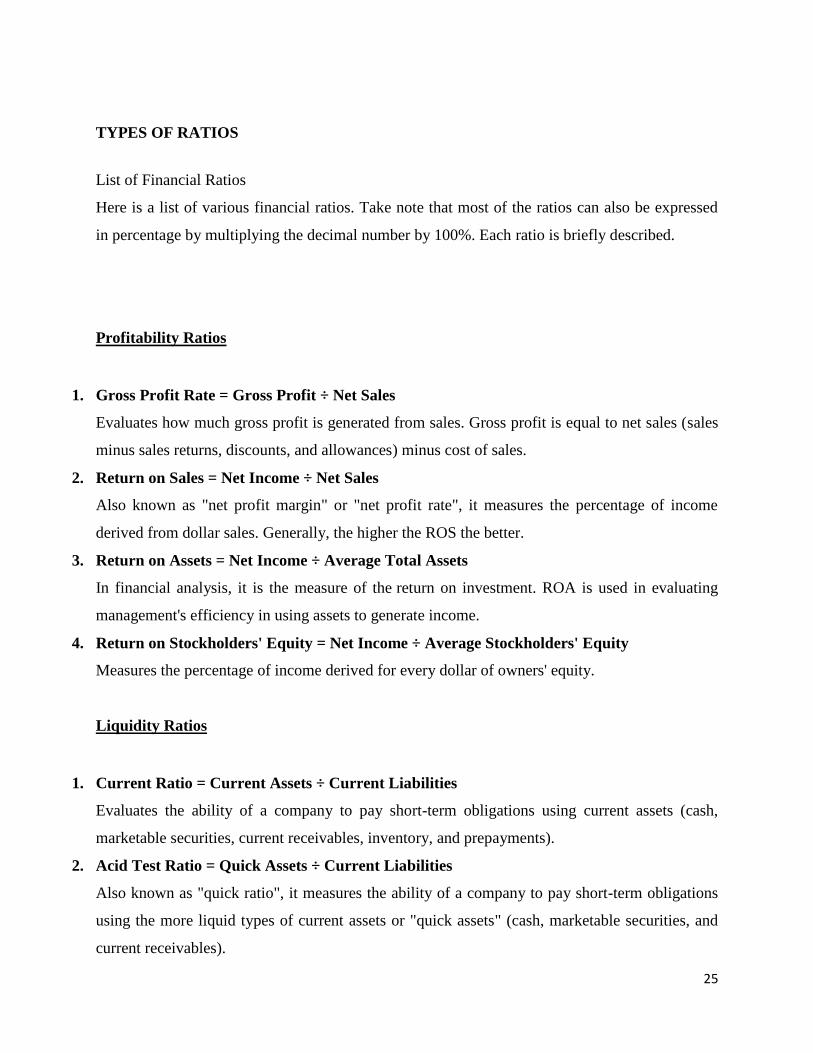

TYPES OF RATIOS

List of Financial Ratios

Here is a list of various financial ratios. Take note that most of the ratios can also be expressed

in percentage by multiplying the decimal number by 100%. Each ratio is briefly described.

Profitability Ratios

1. Gross Profit Rate = Gross Profit ÷ Net Sales

Evaluates how much gross profit is generated from sales. Gross profit is equal to net sales (sales

minus sales returns, discounts, and allowances) minus cost of sales.

2. Return on Sales = Net Income ÷ Net Sales

Also known as "net profit margin" or "net profit rate", it measures the percentage of income

derived from dollar sales. Generally, the higher the ROS the better.

3. Return on Assets = Net Income ÷ Average Total Assets

In financial analysis, it is the measure of the return on investment. ROA is used in evaluating

management's efficiency in using assets to generate income.

4. Return on Stockholders' Equity = Net Income ÷ Average Stockholders' Equity

Measures the percentage of income derived for every dollar of owners' equity.

Liquidity Ratios

1. Current Ratio = Current Assets ÷ Current Liabilities

Evaluates the ability of a company to pay short-term obligations using current assets (cash,

marketable securities, current receivables, inventory, and prepayments).

2. Acid Test Ratio = Quick Assets ÷ Current Liabilities

Also known as "quick ratio", it measures the ability of a company to pay short-term obligations

using the more liquid types of current assets or "quick assets" (cash, marketable securities, and

current receivables).

26

3. Cash Ratio = ( Cash + Marketable Securities ) ÷ Current Liabilities

Measures the ability of a company to pay its current liabilities using cash and marketable

securities. Marketable securities are short-term debt instruments that are as good as cash.

4. Net Working Capital = Current Assets - Current Liabilities

Determines if a company can meet its current obligations with its current assets; and how much

excess or deficiency there is.

Management Efficiency Ratios

1. Receivable Turnover = Net Credit Sales ÷ Average Accounts Receivable

Measures the efficiency of extending credit and collecting the same. It indicates the average

number of times in a year a company collects its open accounts. A high ratio implies efficient

credit and collection process.

2. Days Sales Outstanding = 360 Days ÷ Receivable Turnover

Also known as "receivable turnover in days", "collection period". It measures the average

number of days it takes a company to collect a receivable. The shorter the DSO, the better. Take

note that some use 365 days instead of 360.

3. Inventory Turnover = Cost of Sales ÷ Average Inventory

Represents the number of times inventory is sold and replaced. Take note that some authors use

Sales in lieu of Cost of Sales in the above formula. A high ratio indicates that the company is

efficient in managing its inventories.

4. Days Inventory Outstanding = 360 Days ÷ Inventory Turnover

Also known as "inventory turnover in days". It represents the number of days inventory sits in

the warehouse. In other words, it measures the number of days from purchase of inventory to the

sale of the same. Like DSO, the shorter the DIO the better.

5. Accounts Payable Turnover = Net Credit Purchases ÷ Ave. Accounts Payable

Represents the number of times a company pays its accounts payable during a period. A low

ratio is favored because it is better to delay payments as much as possible so that the money can

be used for more productive purposes.

6. Days Payable Outstanding = 360 Days ÷ Accounts Payable Turnover

27

Also known as "accounts payable turnover in days", "payment period". It measures the average

number of days spent before paying obligations to suppliers. Unlike DSO and DIO, the longer

the DPO the better (as explained above).

7. Operating Cycle = Days Inventory Outstanding + Days Sales Outstanding

Measures the number of days a company makes 1 complete operating cycle, i.e. purchase

merchandise, sell them, and collect the amount due. A shorter operating cycle means that the

company generates sales and collects cash faster.

8. Cash Conversion Cycle = Operating Cycle - Days Payable Outstanding

CCC measures how fast a company converts cash into more cash. It represents the number of

days a company pays for purchases, sells them, and collects the amount due. Generally, like

operating cycle, the shorter the CCC the better.

9. Total Asset Turnover = Net Sales ÷ Average Total Assets

Measures overall efficiency of a company in generating sales using its assets. The formula is

similar to ROA, except that net sales is used instead of net income.

Leverage Ratios

1. Debt Ratio = Total Liabilities ÷ Total Assets

Measures the portion of company assets that is financed by debt (obligations to third parties).

Debt ratio can also be computed using the formula: 1 minus Equity Ratio.

2. Equity Ratio = Total Equity ÷ Total Assets

Determines the portion of total assets provided by equity (i.e. owners' contributions and the

company's accumulated profits). Equity ratio can also be computed using the formula: 1

minus Debt Ratio.

The reciprocal of equity ratio is known as equity multiplier, which is equal to total assets divided

by total equity.

3. Debt-Equity Ratio = Total Liabilities ÷ Total Equity

Evaluates the capital structure of a company. A D/E ratio of more than 1 implies that the

company is a leveraged firm; less than 1 implies that it is a conservative one.

4. Times Interest Earned = EBIT ÷ Interest Expense

28

Measures the number of times interest expense is converted to income, and if the company can

pay its interest expense using the profits generated. EBIT is earnings before interest and taxes.

Valuation and Growth Ratios

1. Earnings per Share = ( Net Income - Preferred Dividends ) ÷ Average Common Shares

Outstanding

EPS shows the rate of earnings per share of common stock. Preferred dividends is deducted from

net income to get the earnings available to common stockholders.

2. Price-Earnings Ratio = Market Price per Share ÷ Earnings per Share

Used to evaluate if a stock is over- or under-priced. A relatively low P/E ratio could indicate that

the company is under-priced. Conversely, investors expect high growth rate from companies

with high P/E ratio.

3. Dividend Pay-out Ratio = Dividend per Share ÷ Earnings per Share

Determines the portion of net income that is distributed to owners. Not all income is distributed

since a significant portion is retained for the next year's operations.

4. Dividend Yield Ratio = Dividend per Share ÷ Market Price per Share

Measures the percentage of return through dividends when compared to the price paid for the

stock. A high yield is attractive to investors who are after dividends rather than long-term capital

appreciation.

5. Book Value per Share = Common SHE ÷ Average Common Shares

Indicates the value of stock based on historical cost. The value of common shareholders' equity

in the books of the company is divided by the average common shares outstanding.

USES OF RATIO ANALYSIS:

The ratio analysis is one of the most powerful tools of financial analysis. It is used as a device to

analyze and interpret the financial health of enterprise. Thus, ratios have wide applications and

are of immense use today:

29

(a) Managerial Uses of Ratio Analysis:

1. Helps in decision-making:

Financial statements are prepared primarily for decision-making. But the information provided in

financial statements is not an end in itself and no meaningful conclusion can be drawn from these

statements alone. Ratio analysis helps in making decisions from the information provided in

these financial statements.

2. Helps in financial forecasting and planning:

Ratio Analysis is of much help in financial forecasting and planning. Planning is looking ahead

and the ratios calculated for a number of years work as a guide for the future. Meaningful

conclusions can be drawn for future from these ratios. Thus, ratio analysis helps in forecasting

and planning.

3. Helps in communicating:

The financial strength and weakness of a firm are communicated in a more easy and

understandable manner by the use of ratios. The information contained in the financial

statements is conveyed in a meaningful manner to the one for whom it is meant. Thus, ratios help

in communication and enhance the value of the financial statements.

4. Helps in co-ordination:

Ratios even help in co-ordination which is of utmost importance in effective business

management. Better communication of efficiency and weakness of an enterprise results in better

coordination in the enterprise.

5. Helps in Control:

Ratio analysis even helps in making effective control of the business. Standard ratios can be

based upon proforma financial statements and variances or deviations, if any, can be found by

comparing the actual with the standards so as to take a corrective action at the right time. The

weaknesses or otherwise, if any, come to the knowledge of the management which helps in

effective control of the business.

6. Other Uses:

30

These are so many other uses of the ratio analysis. It is an essential part of the budgetary control

and standard costing. Ratios are of immense importance in the analysis and interpretation of

financial statements as they bring the strength or weakness of a firm.

(b) Utility to Shareholders/Investors:

An investor in the company will like to assess the financial position of the concern where he is

going to invest. His first interest will be the security of his investment and then a return in the

form of dividend or interest. For the first purpose he will try to asses the value of fixed assets and

the loans raised against them. The investor will feel satisfied only if the concern has sufficient

amount of assets.

Long-term solvency ratios will help him in assessing financial position of the concern.

Profitability ratios, on the other hand, will be useful to determine profitability position. Ratio

analysis will be useful to the investor in making up his mind whether present financial position

of the concern warrants further investment or not.

(c) Utility to Creditors:

The creditors or suppliers extend short-term credit to the concern. They are interested to know

whether financial position of the concern warrants their payments at a specified time or not. The

concern pays short- term creditor, out of its current assets. If the current assets are quite

sufficient to meet current liabilities then the creditor will not hesitate in extending credit

facilities. Current and acid-test ratios will give an idea about the current financial position of the

concern.

(d) Utility to Employees:

The employees are also interested in the financial position of the concern especially profitability.

Their wage increases and amount of fringe benefits are related to the volume of profits earned by

the concern. The employees make use of information available in financial statements. Various

profitability ratios relating to gross profit, operating profit, net profit, etc. enable employees to

put forward their viewpoint for the increase of wages and other benefits.

31

(e) Utility to Government:

Government is interested to know the overall strength of the industry. Various financial

statements published by industrial units are used to calculate ratios for determining short-term,

long-term and overall financial position of the concerns. Profitability indexes can also be

prepared with the help of ratios. Government may base its future policies on the basis of

industrial information available from various units. The ratios may be used as indicators of

overall financial strength of public as well as private sector, in the absence of the reliable

economic information, governmental plans and policies may not prove successful.

(f) Tax Audit Requirements:

Section 44 AB was inserted in the Income Tax Act by the Finance Act, 1984. Under this section

every assesse engaged in any business and having turnover or gross receipts exceeding Rs. 40

lakh is required to get the accounts audited by a chartered accountant and submit the tax audit

report before the due date for filing the return of income under Section 139 (1). In case of a

professional, a similar report is required if the gross receipts exceed Rs 10 lakh.

Clause 32 of the Income Tax Act requires that the following accounting ratios should be given:

(i) Gross Profit/Turnover

(ii) Net Profit/Turnover

(iii) Stock-in-trade/Turnover

(iv) Material Consumed/Finished Goods Produced.

Further, it is advisable to compare the accounting ratios for the year under consideration with the

accounting ratios for the earlier two years so that the auditor can make necessary enquiries, if

there is any major variation in the accounting ratios.

32

LIMITATIONS OF RATIO ANALYSIS:

The ratio analysis is one of the most powerful tools of financial management.Though ratios are

simple to calculate and easy to understand, they suffer from some serious limitations:

1. Limited Use of a Single Ratio:

A single ratio, usually, does not convey much of a sense. To make a better interpretation a

number of ratios have to be calculated which is likely to confuse the analyst than help him in

making any meaningful conclusion.

2. Lack of Adequate Standards:

There are no well accepted standards or rules of thumb for all ratios which can be accepted as

norms. It renders interpretation of the ratios difficult.

3. Inherent Limitations of Accounting:

Like financial statements, ratios also suffer from the inherent weakness of accounting records

such as their historical nature. Ratios of the past are not necessarily true indicators of the future.

4. Change of Accounting Procedure:

Change in accounting procedure by a firm often makes ratio analysis misleading, e.g., a change

in the valuation of methods of inventories, from FIFO to LIFO increases the cost of sales and

reduces considerably the value of closing stocks which makes stock turnover ratio to be lucrative

and an unfavorable gross profit ratio.

5. Window Dressing:

Financial statements can easily be window dressed to present a better picture of its financial and

profitability position to outsiders. Hence, one has to be very careful in making a decision from

ratios calculated from such financial statements. But it may be very difficult for an outsider to

know about the window dressing made by a firm.

6. Personal Bias:

Ratios are only means of financial analysis and not an end in itself. Ratios have to be interpreted

and different people may interpret the same ratio in different ways.

33

7. Un-comparable:

Not only industries differ in their nature but also the firms of the similar business widely differ in

their size and accounting procedures, etc. It makes comparison of ratios difficult and misleading.

Moreover, comparisons are made difficult due to differences in definitions of various financial

terms used in the ratio analysis.

8. Absolute Figures Distortive:

Ratios devoid of absolute figures may prove distortive as ratio analysis is primarily a quantitative

analysis and not a qualitative analysis.

9. Price Level Changes:

While making ratio analysis, no consideration is made to the changes in price levels and this

makes the interpretation of ratios invalid.

10. Ratios no Substitutes:

Ratio analysis is merely a tool of financial statements. Hence, ratios become useless if separated

from the statements from which they are computed.

11. Clues not Conclusions:

Ratios provide only clues to analysts and not final conclusions. These ratios have to be

interpreted by these experts and there are no standard rules for interpretation.

34

CHAPTER- 2

INDUSTRY PROFILE

TRAVEL AND TOURISM INDUSTRY

Travel and tourism is the largest service industry in India. It provides heritage, cultural, medical,

business and sports tourism. The main objective of this sector is to develop and promote tourism,

maintain competitiveness of India as tourist destination and improve and expand existing tourism

products to ensure employment generation and economic growth. In this section, we provide

information about various tourist destinations, modes of travel, accommodation and approved

travel agents.

The Indian tourism industry has emerged as one of the key driver of growth among the services

sector in India. Tourism in India has significant potential considering the rich cultural and

historical heritage, variety in ecology, terrains and places of natural beauty spread across the

country. Tourism is also a potentially large employment generator besides being a significant

source of foreign exchange for the country. India's Foreign Exchange Earnings (FEEs) increased

by 17.6 per cent year-on-year in January 2018 over January 2017.

Market Size

India is the most digitally-advanced traveller nation in terms of digital tools being used for

planning, booking and experiencing a journey@@, India‘s rising middle class and increasing

disposable incomes has continued to support the growth of domestic and outbound tourism.

Domestic Tourist Visits (DTVs) to the States/Union Territories (UTs) grew by 15.5 per cent y-o-

y to 1.65 billion (provisional) during 2016 with the top 10 States/UTs contributing about 84.2 per

cent to the total number of DTVs, as per Ministry of Tourism.

Foreign Tourist Arrivals (FTAs) in India increased 8.4 per cent year-on-year to 1.06 million and

the number of FTAs on e-tourist visa increased 58.5 per cent to 2.40 lakh foreign tourist as per

Ministry of Tourism, Government of India.

35

India is expected to move up five spots to be ranked among the top five business travel market

globally by 2030, as business travel spending in the country is expected to treble until 2030 from

US$ 30 billion in 2015.#

International hotel chains will likely increase their expansion and investment plans in India, and

are expected to account for 50 per cent share in the Indian hospitality industry by 2022, from the

current 44 per cent.

Investments

The tourism and hospitality sector is among the top 10 sectors in India to attract the highest

Foreign Direct Investment (FDI). During the period April 2000-December 2017, the hotel and

tourism sector attracted around US$ 10.90 billion of FDI, according to the data released by

Department of Industrial Policy and Promotion (DIPP).

Government Initiatives

The Indian government has realised the country‘s potential in the tourism industry and has taken

several steps to make India a global tourism hub.

Some of the major initiatives planned by the Government of India to give a boost to the tourism

and hospitality sector of India are as follows:

The Government of India signed a loan agreement for US$ 40 million with the World

Bank for the Uttar Pradesh Pro-Poor Tourism Development Project aimed at developing

tourism facilities in the state.

Under Budget 2018-19, the government allotted Rs 1,250 crore (US$193.08 million) for

Integrated development of tourist circuits under Swadesh Darshan and Pilgrimage

Rejuvenation and Spiritual Augmentation Drive (PRASAD).

India is on a high growth path and with tourism-friendly policies initiated by the

government, we are optimistic that this will continue in the upcoming budget coupled

with sustained delivery on ground. The tourism industry is one of the largest and most

dynamic sectors globally, accounting for more than a third of the total service trade. The

UNWTO also expects the sector to provide 296 million jobs globally by 2019. Recent

tourism statistics reveal that both domestic and foreign tourism are on a robust growth

36

path. India's rising middle class and increasing disposable incomes have also contributed

to this continued growth in domestic and outbound tourism.

This is reiterated in the data shared by the Ministry of Tourism that from 2010 to 2015,

we saw an 8.7% increase in total outbound trips to 19.9 million in 2015. The inbound

tourist volume also grew at a Compound Annual Growth Rate (CAGR) of 6.8% during

2010-15.

The tourism industry of India is economically important and grows rapidly. The World

Travel & Tourism Council calculated that tourism generated INR6.4 trillion or 6.6% of

the nation‘s GDP in 2012. It supported 39.5 million jobs, 7.7% of its total employment.

The sector is predicted to grow at an average annual rate of 7.9% from 2013 to 2023.

This gives India the third rank among countries with the fastest growing tourism

industries over the next decade. India has a large medical tourism sector which is

expected to grow at an estimated rate of 30% annually to reach about 95 billion by 2015.

This paper discusses how India is emerging as a popular tourist destination in the world,

driven by the focus on innovation and creating value for tourists. It aimed change the

attitude and behavior toward foreign tourists by stressing on the aspect that a guest has

been held in high esteem in India since ancient times. It also examines the impact of

India‘s economic growth on tourism, Contributors to economic growth, Role of Tourism

industry in India‘s GDP, Foreign versus Domestic Tourists. The paper also explores that

there has been a tremendous growth in tourism in India because of the policies of the

government and support from all levels. Tourism is considered to be an economic

bonanza. It is a multi-segment industry. While gauging the positive economic effects of

tourism, we study its contribution to the generation of national income, expansion of

employment opportunities, rising of tax revenue, generation of foreign exchange .and

transformation of regional economy. Travel & Tourism is an important economic activity

in most countries around the world. As well as its direct economic impact, the industry

has significant indirect and induced impacts. Indian Tourism offers a potpourri of

different cultures, traditions, festivals, and places of interest. There are a lot of options for

the tourists. India is a country with rich cultural and traditional diversity. This aspect is

37

even reflected in its tourism. The different parts of the country offer wide variety of

interesting places to visit.

Keywords

Employment opportunities; Foreign versus domestic tourists; GDP; Tourism industry

Introduction

Throughout the world, tourism brings money to cities and countries. Tourism also

provides jobs for the local residents, further benefiting the destination. India has realized

the profits available from this sector. Thanks to its growing economy and promoting itself

as a culturally rich and diverse nation, India‘s tourism industry now brings billions of

dollars into the economy each year. The growth in the tourism industry is due to the rise

in the arrival of more and more foreign tourists and the increase in the number of

domestic tourists.

Words are few to explain the beauty of India. India is a country with diversified culture

and traditions. The natural beauty of India, festivals, dresses, heritage sites of India are

very popular among tourists. These things fascinate travelers to come here. India has so

many scenic blesses places like Kerala, Darjeeling, Goa, Kashmir, Shimla(I am just

having few names) and Manali. These places are very popular. These places are prime

attraction of travelers from across the world .There are also so many other places worth

visiting ., like Delhi Kutub Minar /Agra Tajmahal/Hyderabad Charminar and Salarjung

museum /Chennai a city of fine arts / Bangalore., Known as the Garden City for its lush

landscape, lakes and temperate climate, it aptly represents India‘s marriage of past and

present,/ kerala known as god‘s own country/ Kolkata was arguably second only to

London in administrative importance in the British Empire. Home of luminaries like

Rabindranath Tagore, Amartya Sen, Mother Teresa, and Satyajit Ray, the city is often

referred to as the ―cultural capital of India‖ etc. The Government of India has established

the Ministry of Tourism in order to boost Tourism in India. The Ministry of Tourism has

undertaken many projects to showcase India as a perfect Tourist destination and create a

visitor-friendly image of the country. The major steps taken by the Government were the

Atithi Devo Bhavah Campaign which gave a widespread message of ―honour your Guest

as he is always equivalent to God‖ and the Incredible India Campaign which was

incredibly successful in creating a colorful and a gorgeous image of our country as a

38

perfect holiday destination. Dr. K. Chiranjeevi, Hon‘ble Minister for State for Tourism

(IC) launched the Ministry of Tourism‘s Incredible India 2013 Calendar. The attractive

Calendar is based on the theme ―Find What You Seek‖ as part of Phase II of the

Incredible India campaign, which was launched during World [1].

Travel Mart (WTM), London 2012. This was mainly because of extensive Publicity

Campaigns in which the IT industry played a remarkable role.

Methodology

The present study is based on the secondary data published by various agencies and

organizations. The present study makes use of data and information provided by,

UNWTO, Ministry of Tourism, Ministry of Statistics and Programme Implementation,

Newspapers, Magazines, Books, Economic journals and Internet etc.

Initiatives by the government for tourism promotion

Hunar se rozgar’ programme: A special initiative was launched in 200910 for the

create ion of employable skills among youth belonging to economically weaker sections

of the society in the age group of 18- 25 years (upper age limit raised to 28 years in

November, 2010) with the basic objective to reduce the skill gap affecting the hospitality

and tourism sector and to ensure the spread of economic benefit of tourism to the poor.

The programme offers short duration courses of 6 to 8 weeks which are fully funded by

the Ministry of Tourism

Visa on arrival: Considering the importance of Visa facilities in enhancing tourist

inflow, the facility of „Long Term Tourist Visas‟ of five years duration with multiple

entries, carrying a stipulation of 90 days for each visit, has been introduced on a pilot

basis f or the nationals of the 18 selected countries. The findings of an evaluation study

conducted by this

Ministry has reinforced the belief that the presence of the facility of ―Visa on Arrival‖

(VoA) significantly influences the tourists'' travel plans to any country. During 2012, a

total number of 16,084 VoAs (Visa on Arrival) were issued as compared to 12,761 VoAs

during the corresponding period of 2011, thereby showing a growth of 26%. Efforts are

on to extend the VoA facility for the nationals of more countries

39

Types of tourism in india

India is a country which witnesses a lot of diversity pertaining to its ecology, mythology,

history, its geoCHARTical diversity in terms of mountains, planes and plateaus and also

the medicinal diversity teaching us the Science of Life (Ayurveda). India showcases a

variety of tourism options which includes Ecological Tourism, Pilgrimage Tourism,

Historical Tourism, Adventure Tourism, Medical Tourism and an upcoming Ayurveda

Tourism. So Tourism in India could be broadly classified on the basis of above

mentioned categories

Leisure tourism: Leisure time can be defined as ―free time‖, not doing any work. It is

that time to do things that you normally have no time for in your daily life. Leisure

tourism includes a holiday with the following:

Relaxation: Sleep, relax, reading, walk on the beach, taking a scenic drive o

Sport activities: hiking, swimming, surfing, running

Visit places of interest and local attractions Visiting friends and relatives

Shopping for goods that will be used by the tourist.

Business tourism: Business tourism can be defined as ―travel for the purpose of

business‖.

Business Tourism can be divided into three sections:-

(a) Trading for goods to be resold on a wholesale basis.