Industrial Location Policy - World Bank Documents

149

SWP620 Industrial Location Policy The Indian Experience A. Uday Sekhar WORLD BANK STAFF WORKING PAPERS Number 620 Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Industrial Location Policy - World Bank Documents

SWP620

Industrial Location PolicyThe Indian Experience

A. Uday Sekhar

WORLD BANK STAFF WORKING PAPERSNumber 620

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

WORLD BANK STAFF WORKING PAPERSNumber 620

Industrial Location PolicyThe Indian Experience

A. Uday Sekhar

INTERNATIO??EL MO'?-EARY FuNDJOINT MEH99Y

[A/AR 2'. 1984

INTEIRNATIONAL D:piiK FORrL'.E:O5i'JTrCTION i!JD DIVELCPIENT

WARlSl2NOTCN,'L .C. 2Ve91

The World BankWashington, D.C., U.S.A.

Copyright 0 1983The International Bank for Reconstructionand Development / THE WORLD BANK1818 H Street, N.W.Washington, D.C. 20433, U.S.A.

First printing October 1983All rights reservedManufactured in the United States of America

This is a working document published informally by the World Bank. Topresent the results of research with the least possible delay, the typescript hasnot been prepared in accordance with the procedures appropriate to formalprinted texts, and the World Bank accepts no responsibility for errors. Thepublication is supplied at a token charge to defray part of the cost ofmanufacture and distribution.

The views and interpretations in this document are those of the author(s) andshould not be attributed to the World Bank, to its affiliated organizations, or toany individual acting on their behalf. Any maps used have been preparedsolely for the convenience of the readers; the denominations used and theboundaries shown do not imply, on the part of the World Bank and its affiliates,any judgment on the legal status of any territory or any endorsement oracceptance of such boundaries.

The full range of World Bank publications is described in the Catalog of WorldBank Publications; the continuing research program of the Bank is outlined inWorld Bank Research Program: Abstracts of Current Studies. Both booklets areupdated annually; the most recent edition of each is available without chargefrom the Publications Sales Unit of the Bank in Washington or from theEuropean Office of the Bank, 66, avenue d'Iena, 75116 Paris, France.

A. Uday Sekhar is deputy manager of the Industrial Development Bank ofIndia and a consultant to the World Bank.

Library of Congress Cataloging in Publication Data

Sekhar, Uday.Industrial location policy.

(World Bank staff working papers ; no. 620)Bibliography: p.1. India--Industries--Location. I. Title. II. Series.

HC44o.D5S44 1983 338.6'042'0954 83-21774ISBN 0-8213-0273-6

ABSTRACT

The Government of India has been utilizing a wide-ranging setof measures to influence the location of industry. They are generallyintended to disperse industries from large metropolitan areasand to promote the development of less developed regions. Thispaper probes into the working and impact of individual location policies,and demonstrates certain serious deficiencies and lacunae in thejustification, design and implementation of many of them. These short-comings call for a thorough overhauling in the approach of the Governmenttowards industrial location policy. In particular, this paper recommendsthat whenever there is evidence that the existing concentration isinoptimal or inequitable, policy makers should operate with incentivesrather than controls, as this form of industrial location policyinstrument appears to provide the least damage to the economy whileachieving the locational objectives.

ACKNOWLEDGMENTS

The views expressed in this paper are personal and do not reflectthose of the institution in which I am employed. I wish to record mydeep indebtedness tco Rakesh Mohan, Professor Edwin Mills, Douglas Keare,Peter Townroe, Koichi Mera and other members of the former Urban andRegional Economics Division of the World Bank for their invaluableassistance in the preparation of this paper.

TABLE OF CONTENTS

SUMMARY ................................................................... viii

Chapter I -- INTRODUCTION ................................................ 1

Chapter II -- INDUSTRIAL LOCATION POLICIES IN INDIA .......................1. Policies Influencing Inter-State Distribution of Industry .. 15

i. IndustriaL Licensing ........................ 15ii. Location of Public Sector Plants ............................ 22iii. Distribution and Pricing Policies for Basic

Industrial Inputs ...................................... 31iv. State Government Incentives ................................. 35

2. Policies Influencing the Intra-Regional Distributionof Industry ............................................ 36

i. Policies to Encourage the Small Scale Sector ................ 37ii. IndustriaL Estate Program ................................... 43iii. Rural Industries Projects ................................... 49iv. Metropolitan Planning ....................................... 56v. Incentives to Develop Backward Districts .................... 59

Chapter III -- TRENDS 'IN INDIAN INDUSTRIAL LOCATION ...................... 691. Trends in the Inter-State Distribution of Industry ............... 692. Trends in the :Intra-Regional Distribution of Industry ............ 77

Chapter IV -- AN OVERALL ASSESSMENT OF INDUSTRIAL LOCATION POLICY ......... 911. Rationale of Industrial Location Policy . . 91

i. Resource ALlocation and Growth ............................... 92ii. Equity .................... ..... ...... ............... 96

2. Limitations of Industrial Location Policy . . 97

POSTCRIPT..102POSCRPT.................................................................101. National Committee on the Development of Backward Areas .......... 102

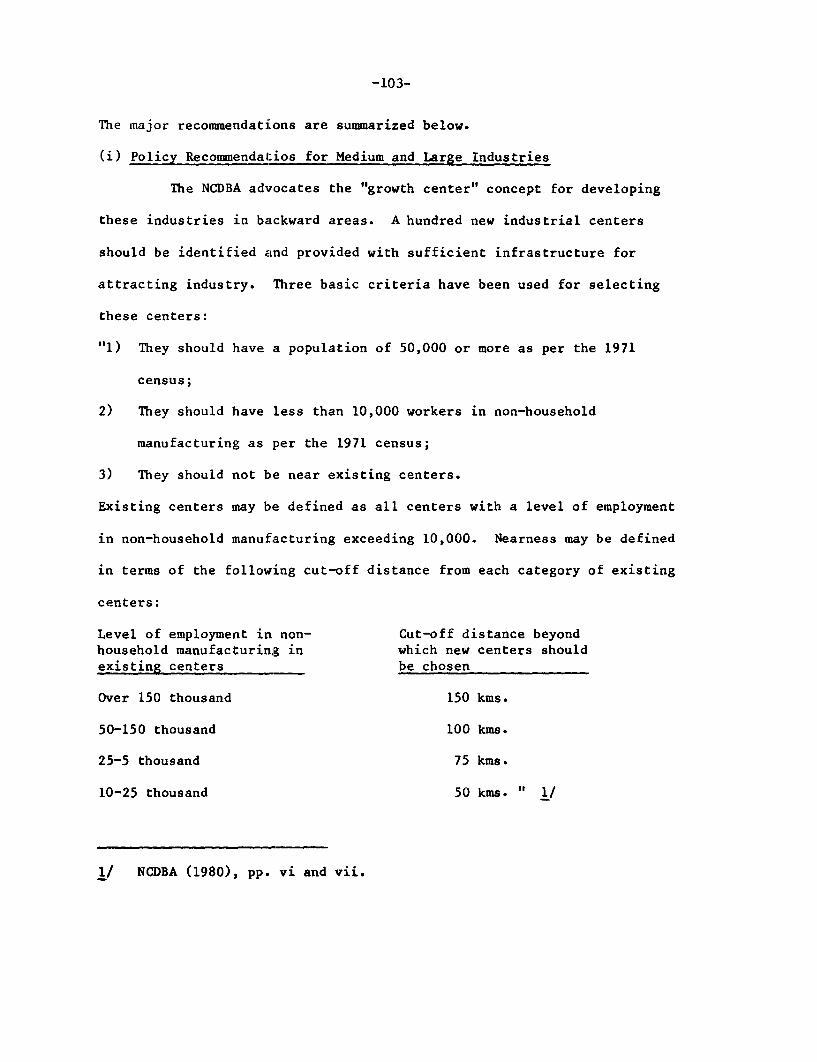

i. Policy Recommendations for Medium and LargeIndustries ............................................. 103

ii. Policy Recommendations for Small Industries,Anci:Llary Industries and Agro-Industries ............... 104

iii. Recommendations for Maximizing the Local Impact ofIndustrial Development ................................. 105

2. A Critique of lthe NCDBA Report ................................... 106

BIBLIOGRAPHY .............................................................. 109

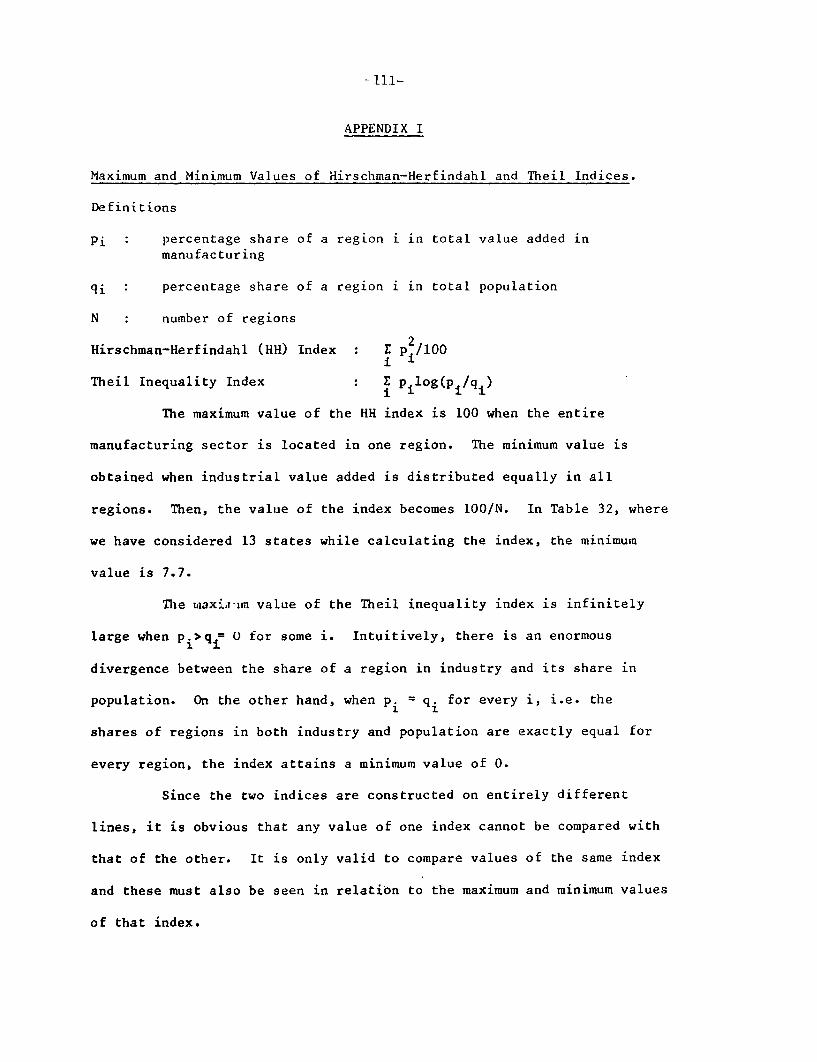

APPENDIX I: Maximum and Minimum Values of Hirschman-Herfindahl andThei:L Indices .......................................... ll

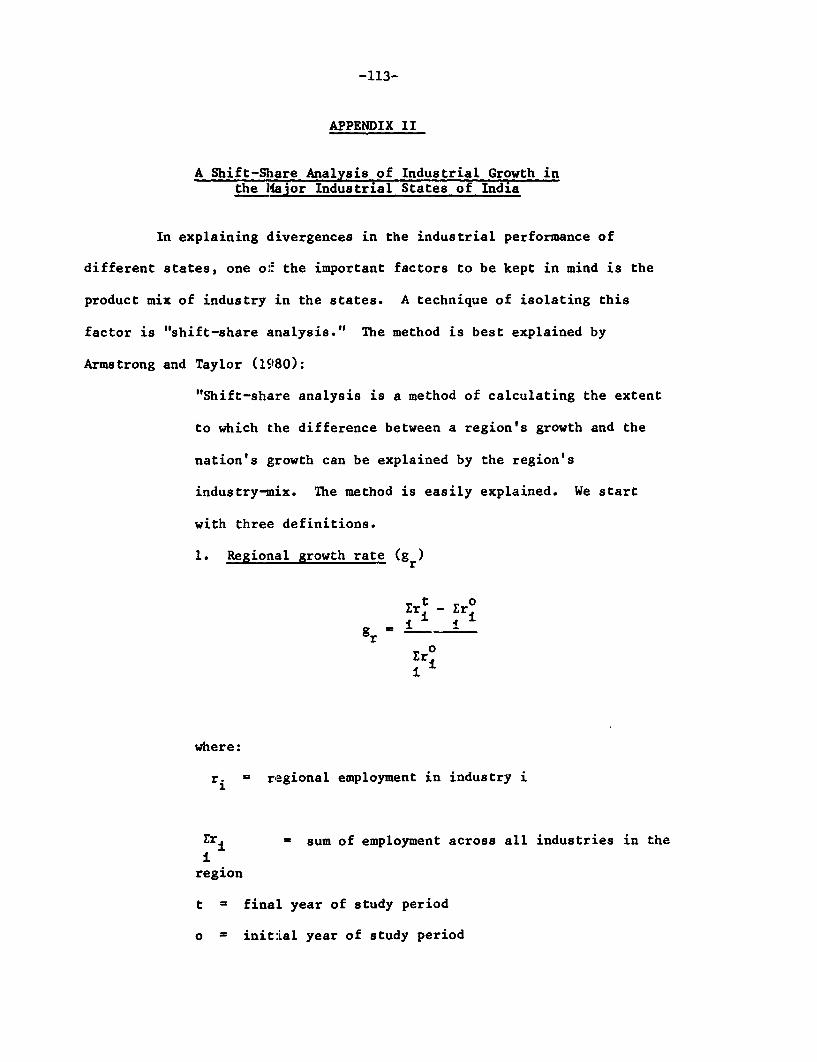

APPENDIX II: A Shift-Shasre Analysis of Industrial Growth inthe lMajor Industrial States of India ................... 113

LIST OF TABLES

Table Page

1. Share of Manufacturing in GDP (7) in some DevelopingEconomies, 1977 2

2. Structure of the Indian Manufacturing Sector, 1974 4

3. Trend Growth Rates (7 per annum) in the Manufacturing 6Sector

4. Value Added in Factory Manufacturing Sectoras a Proportion of State NDP (7) 7

5. VAM/NDP For Each State Divided by VAM/NDP for All-India 8

6. Share of States in Total Value Added in FactoryManufacturing Sector (7) 10

7. Share of States in Total Factory Employment inManufacturing (7) 11

8. Distribution of Urban Employment and Population inNon-Household Industry by the Size of Cities,Towns, and Town Groups (TG)/Urban Agglomerations (UA) 12India, 1961 & 1971

9. Approved Licenses as a Percentage of LicenseApplications, 1959-66 18

10. Correlation Coefficients between State-WiseProportions of Licenses Approved and Indices ofState Development 20

11. Share of States in Cumulative Investment(Gross Block) in Central Public Undertakings (7) 24

12. Share of States in Annual Investment In CentralPublic Undertakings (7) 25

13. Correlation Coefficients Between State-Wise PerCapita Investment in Central Public Undertakings andIndicators of State Development 26

14. Distribution of Cumulative Public SectorInvestment (7) 28

15. Share of Employment in Central Public Undertakingsin Total Employment in Manufacturing and Mining (7) 29

16. Orders placed by Public Sector Undertakings to SmallScale Units as a Percentage of Output of Modern SmallScale Sector 30

17. Region-Wise Installed Capacity of Cement (%) 31

18. Share of Unregistered Sector in Value Added inManufacturing (%) 38

19. Employment and Output in Modern Small Scale Sector,1972 39

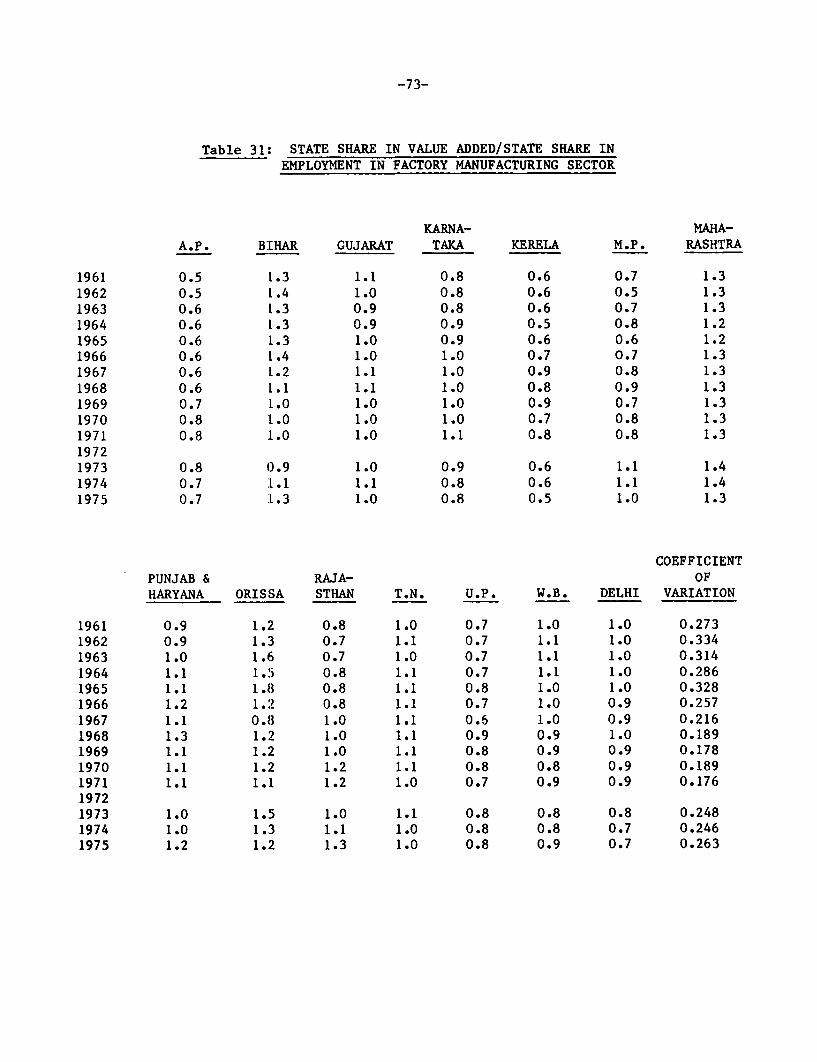

20. Percentage of Sheds Completed but not Functioning 46

21. Share of Industrial Estates in Industrial Employmentand Output (%) 50

22. Public Expenditure on Rural Industries Projects 53

23. Proportion of Saimple Units Availing of R.I.P.Assistance (%) 54

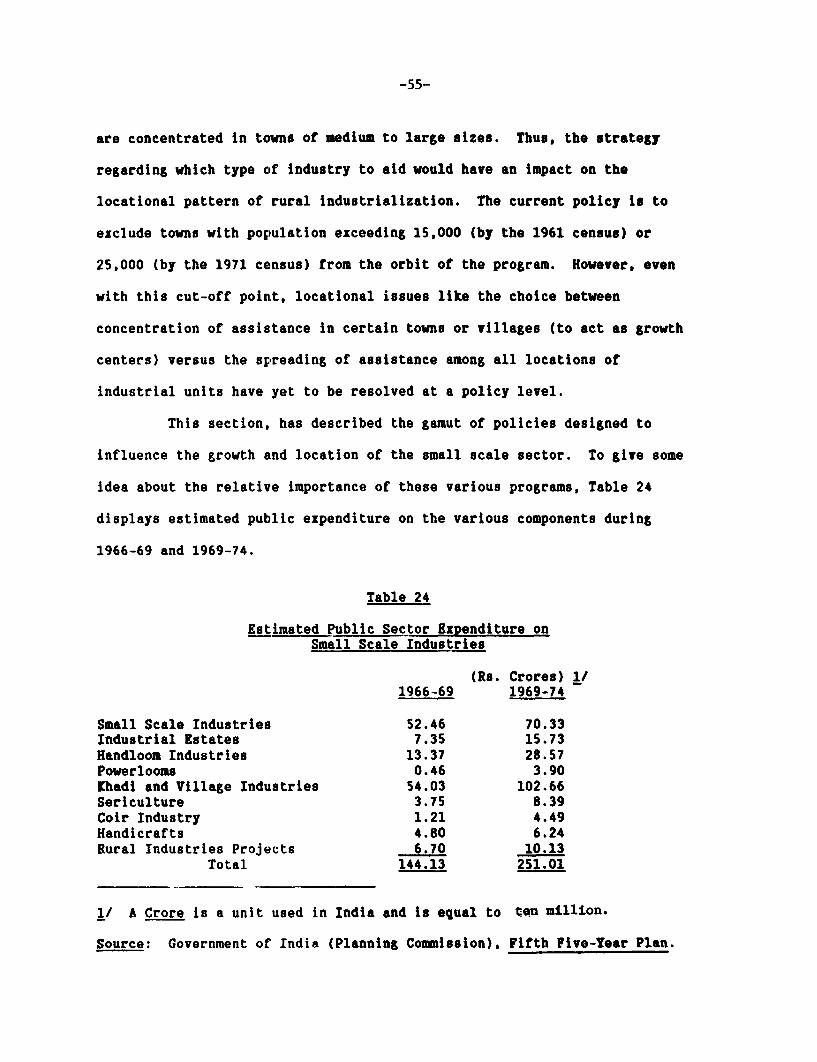

24. Estimated Public Sector Expenditure on Small ScaleIndustries 55

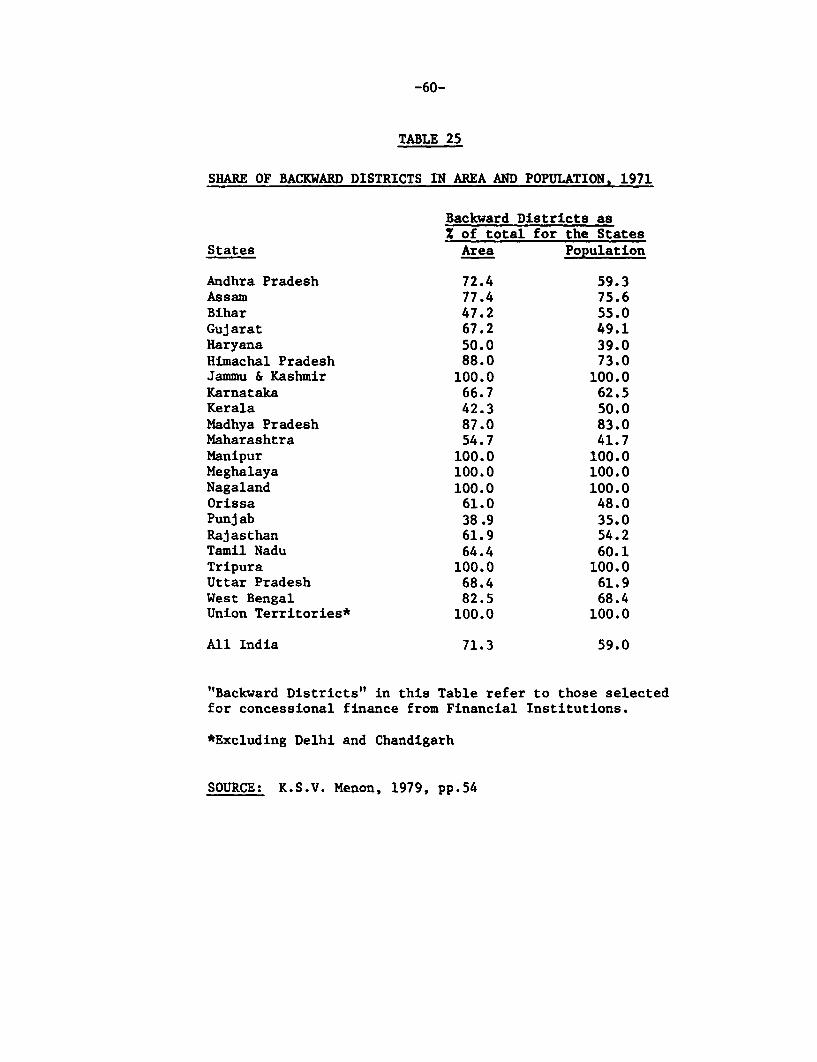

25. Share of Backward Districts in Area and Population,1971 60

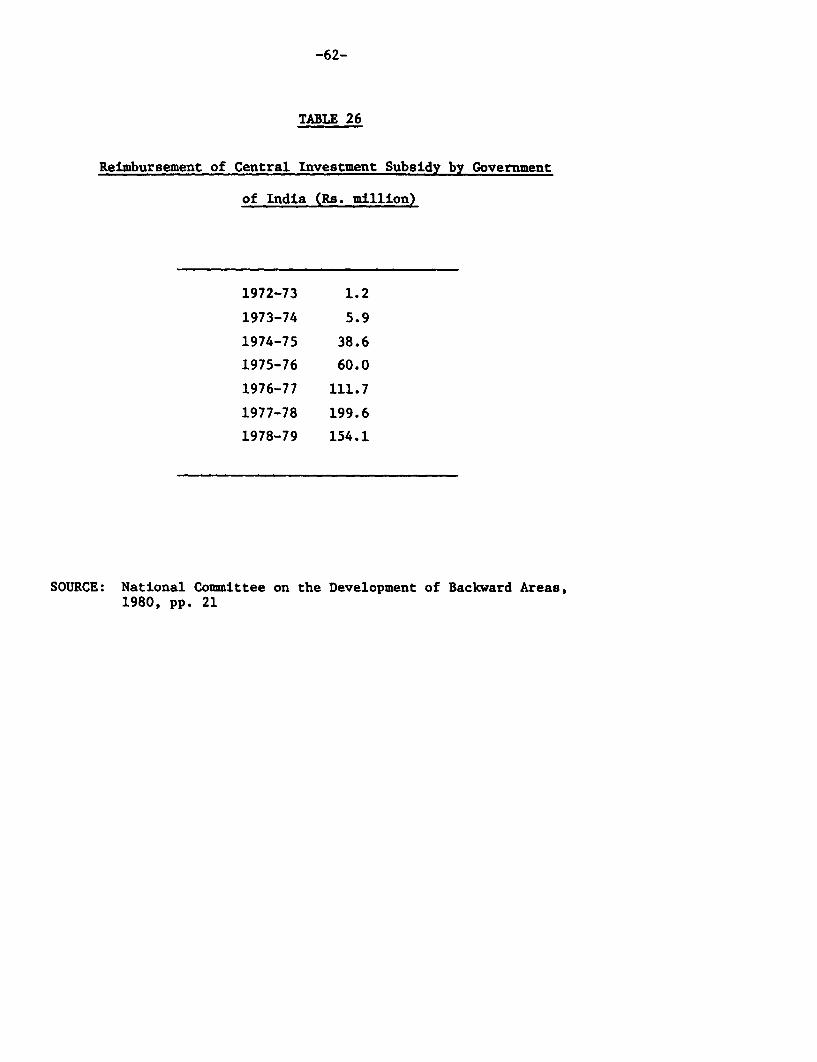

26. Reimbursement of Central Investment Subsidy byGovernment of India (Rs.m) 62

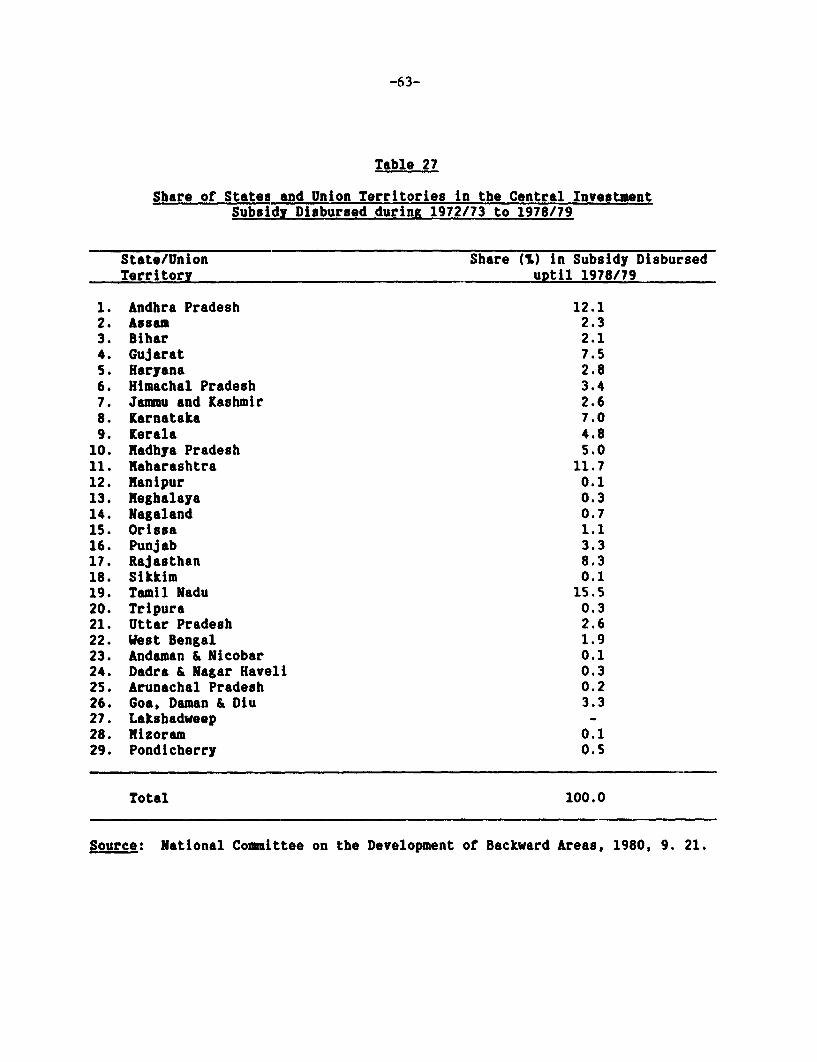

27. Share of States and Union Territories in the CentralInvestment Subsidly Disbursed during 1972/73 to1978/79 63

28. Terms of Concess ional Finance for Units in BackwardDistrict/Areas, 1975 66

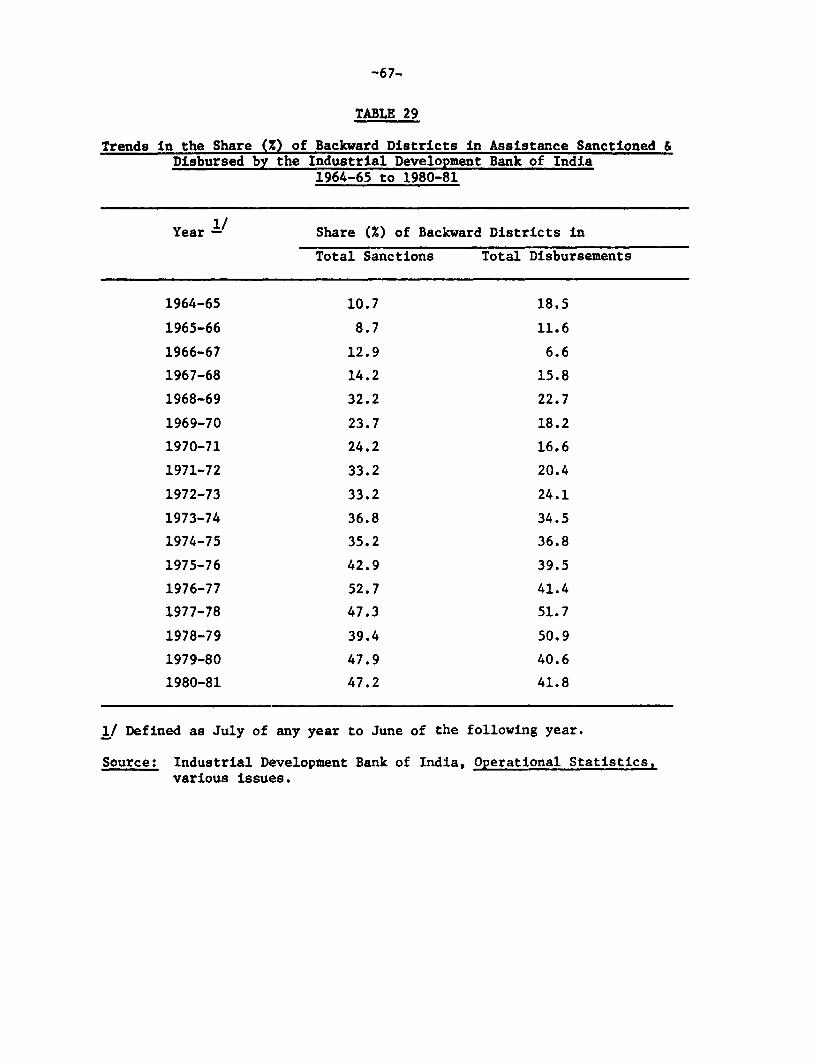

29. Trends in the Share (%) of Backward Districts inAssistance Sanctioned and Disbursed by the IndustrialDevelopment Bank of India, 1964/65 to 1980/81 67

30. Value Added per Employee (Rs. '000) in Industry 72

31. State Share in Value Added/State Share in Employmentin Factory Manufacturing Sector 73

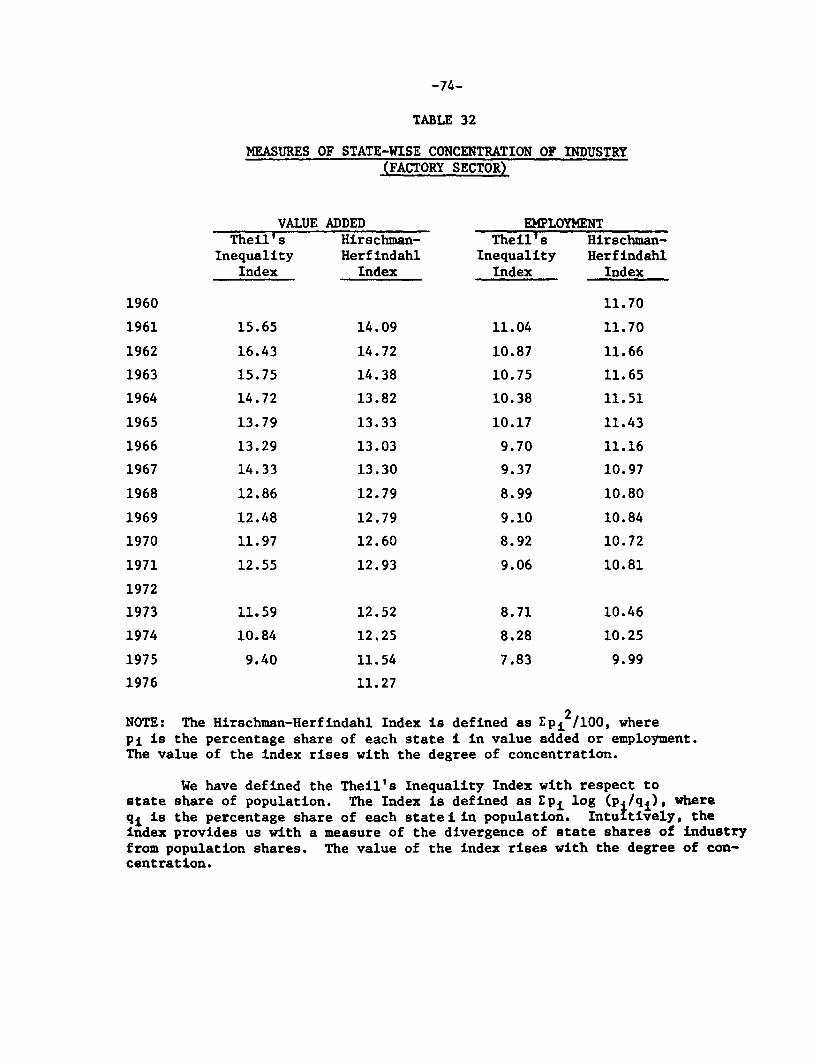

32. Measures of State-Wise Concentration of Industry(Factory Sector) 74

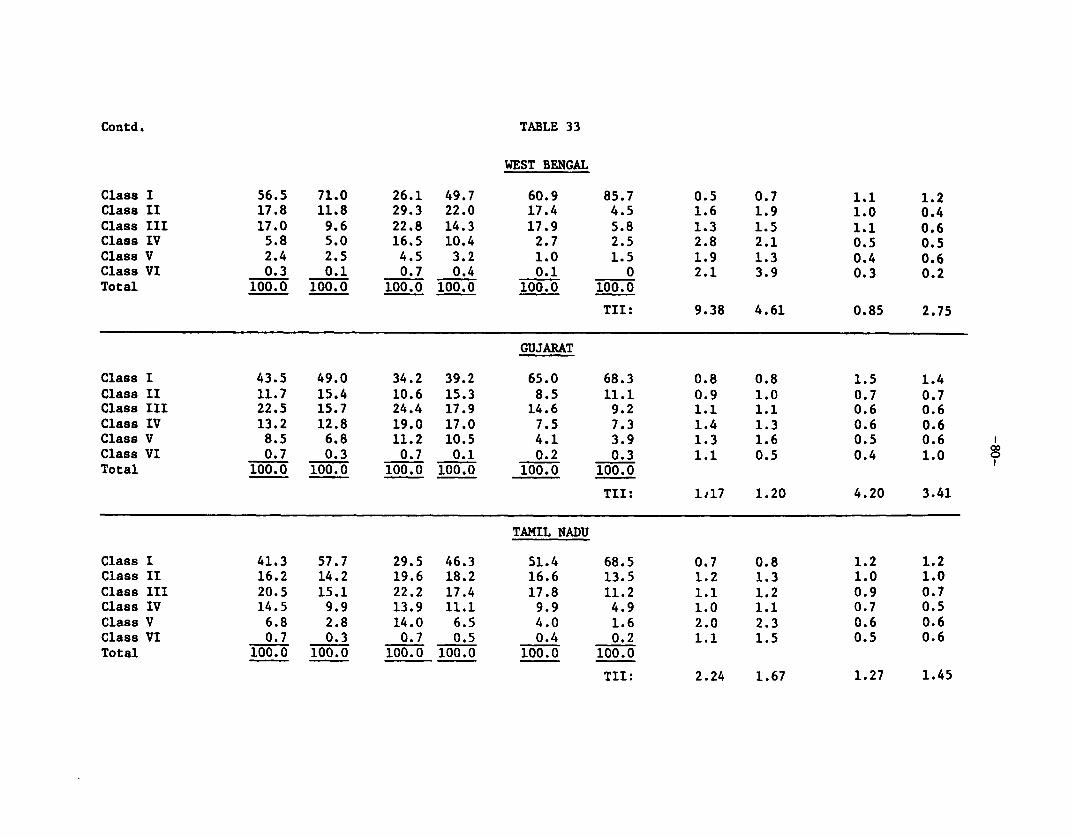

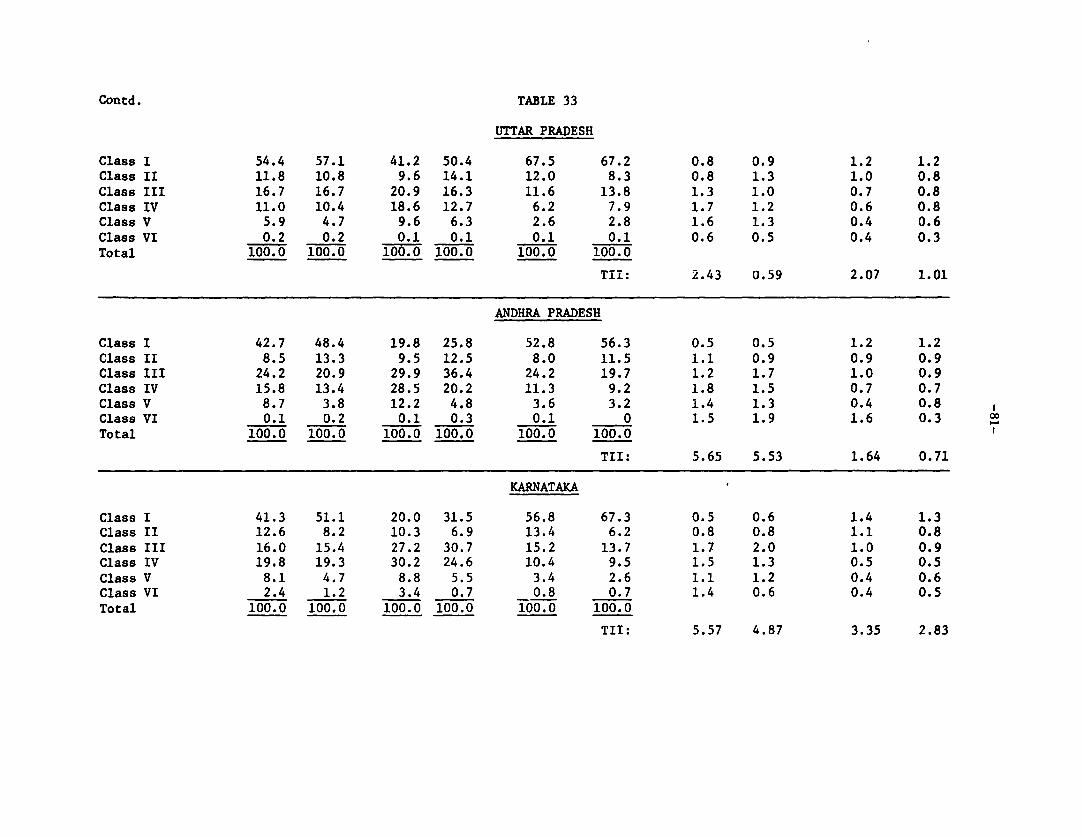

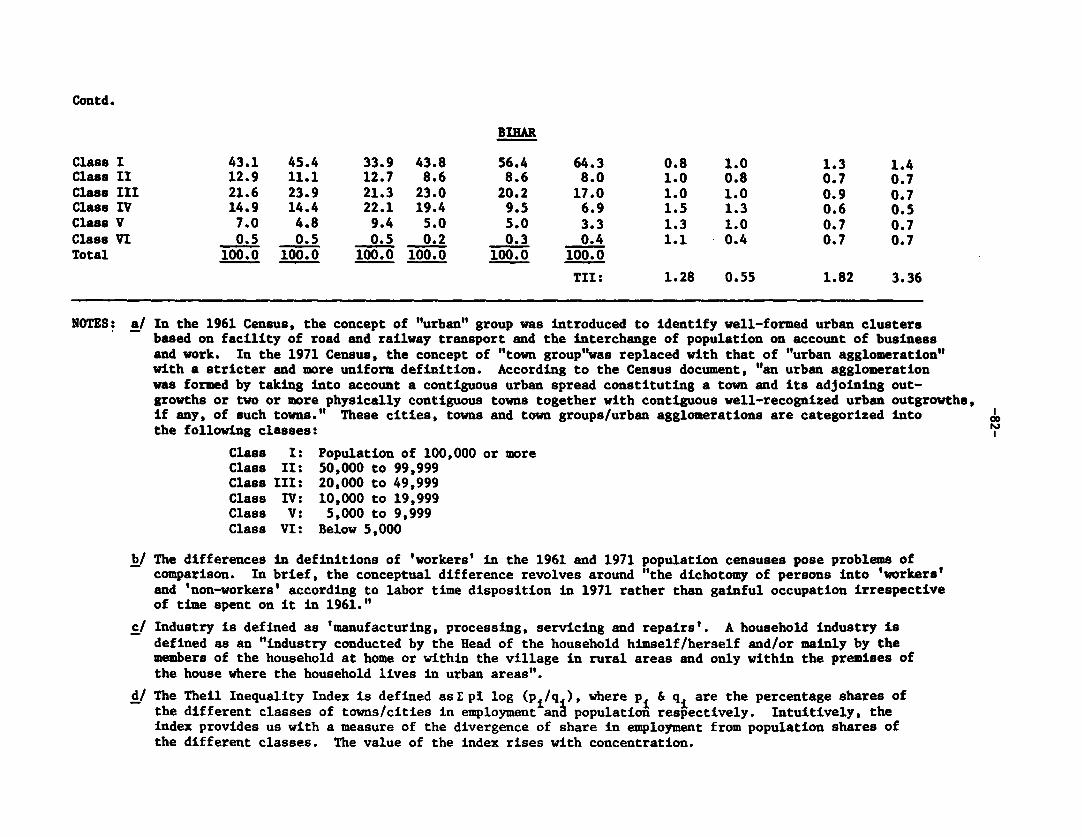

33. Distribution of Industrial Employment in Cities,Towns, and Town Groups (TG)/Urban Agglomerations (UA),1961 & 1971 79

LIST OF FIGURES

Figure Page

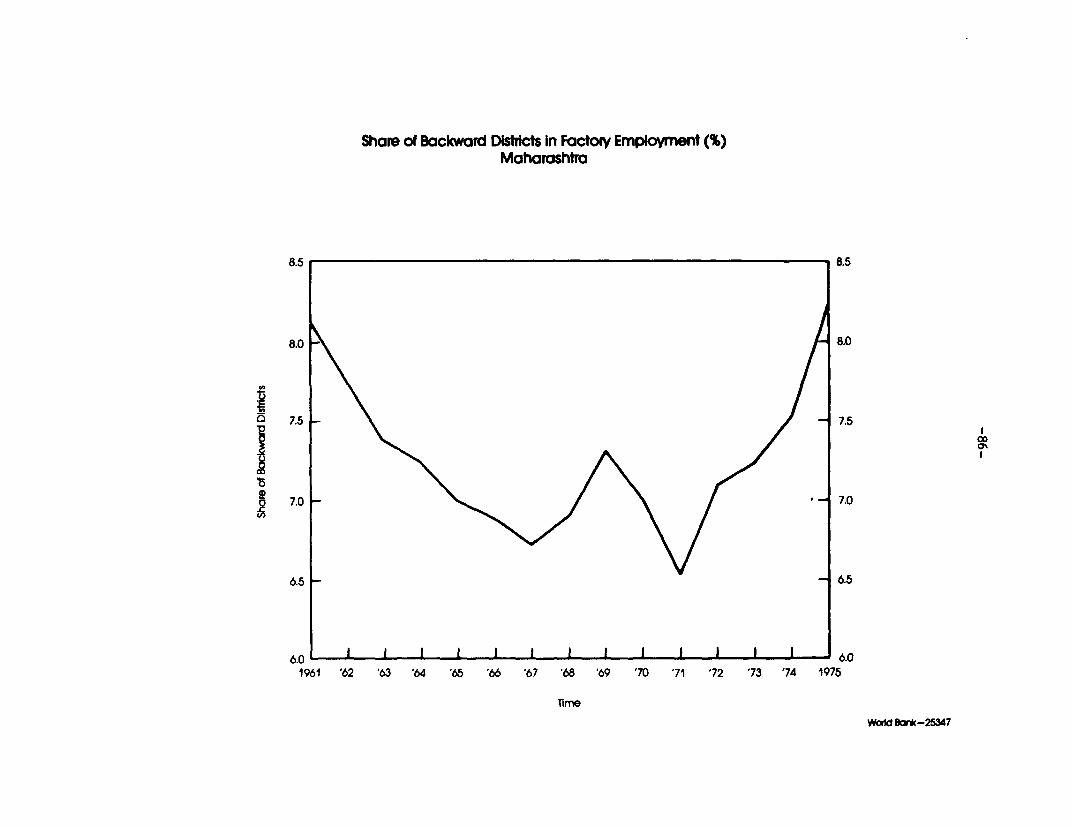

1. Share of Backward Districts in Factory Employment(7), Maharashtra 86

2. Share of Backward Districts in Factory Employment(7), Haryana 87

3. Share of Backward Districts in Factory Employment(7), Punjab 88

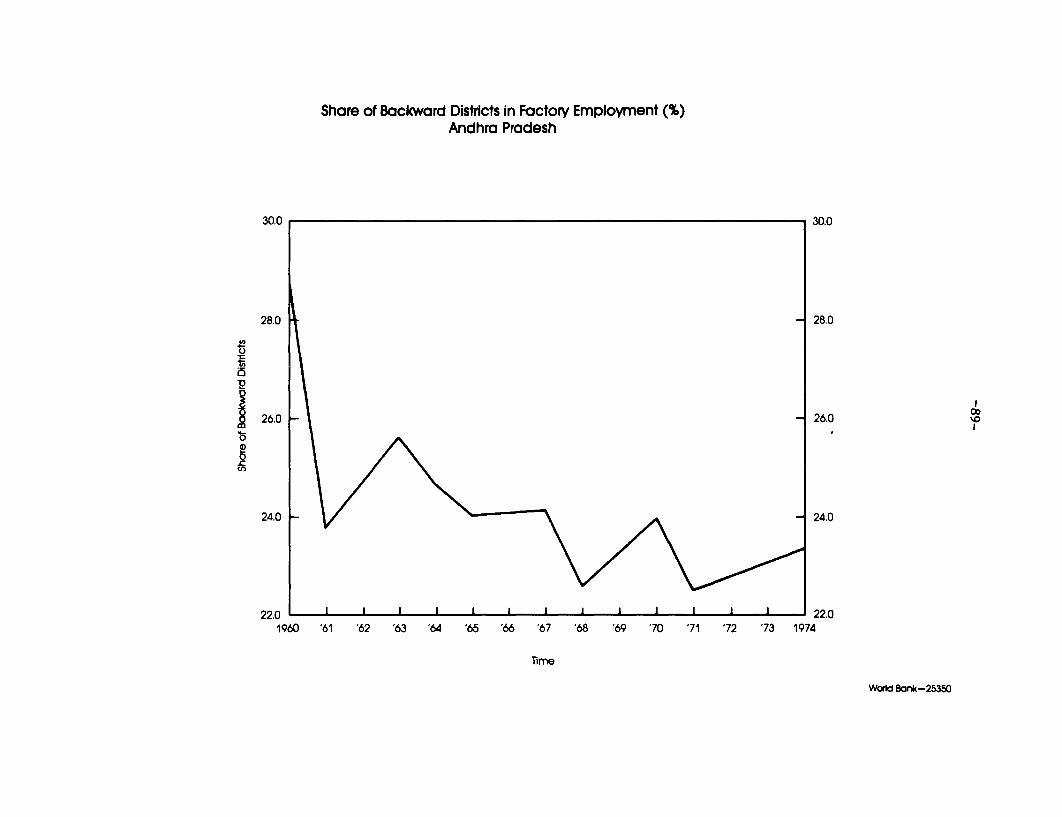

4. Share of Backward Districts in Factory Employment(7), Andhra Pradesh 89

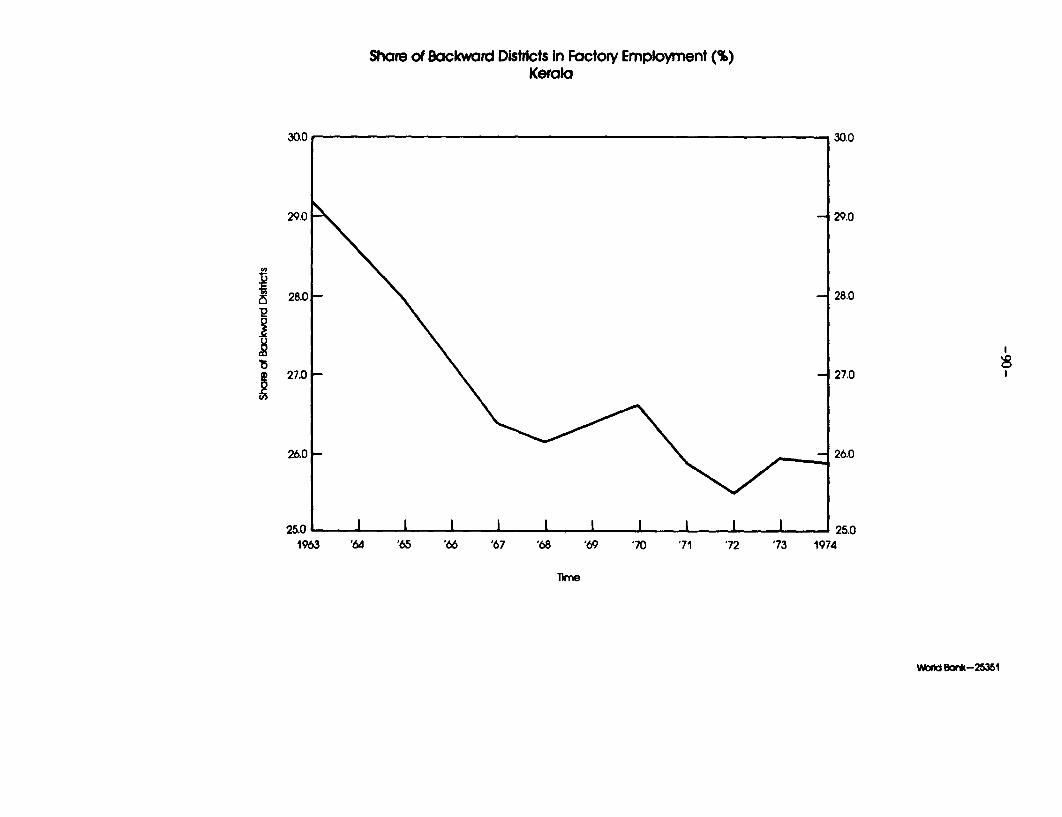

5. Share of Backward Districts in Factory Employment(.), Kerala 90

Map

1. Map of India 118

SUMMARY

As in most other developing countries, India had been experiencing

since her independence a high and perhaps increasing concentration of

population and economic activities at selected locations such as Bombay and

Calcutta and severe disparity in welfare among different regions within the

country. In response, the Government of India adopted a series of measures to

promote a more decentralized and spatially "balanced" development. Most of

the measures are directed at influencing the location of manufacturing

establishments as they are viewed as the prime determinant of spatial

development. This policy has been followed by state and local governments as

well. However, these measures cannot be without unintended side effects.

The purposes of this paper are first to identify the intended

objectives of industrial location policies which have been instituted in India

in order to assess to the extent possible their effectiveness in achieving the

objectives, and then to evaluate their possible unintended as well as intended

effects in order to arrive at a more balanced view on this subject.

In the first chapter, the manufacturing sector of India is reviewed

with emphasis on identifying its spatial pattern of distribution. On the

state basis, Maharashtra, West Bengal, Gujarat and Tamil Nadu are most

industrialized, although the share of West Bengal has been eroding

consistently since the early 1960's.

Chapter 2 presents a review of industrial location policies

currently in effect. Those influencing interstate distribution of industry

comprise (1) industrial licensing, (2) location of public sector plants, (3)

distribution and pricing policies for intermediate industrial inputs and (4)

state government incentives. Since 1951, the Central Government has been

authorized to license a new industrial establishment or a substantial

expansion. This instrument has been used to achieve a "balanced" regional

development. This policy orientation has been strengthened since 1965, and

since 1977 an explicit decision has been made to prohibit the setting up of

licensable industries within certain geographical limits of large metropolitan

cities with a population exceeding one million and urban agglomerations with a

population greater than half a million.

Location decisions of public sector plants are also an important

policy instrument, because many basic and capital goods are produced by the

public sector in India. The less developed states of Madhya Pradesh and Bihar

received large shares of investment, followed by Orissa and West Bengal.

Since location decisions were made on the basis of technical and economic

considerations as well as regional balance, it is impossible to isolate the

degree of regional consideration which went into location decisions, but an

analysis shows that the per capita cumulative investment in this sector has

been consistently negatively related to state per capita income and

undoubtedly it contributed to balancing the distribution of industry among

states.

With regard to the distribution of such basic commodities as cement,

steel and coal, "freight-pooling" is exercised by the Central Government so

that firms in every location may equally benefit from the provision of these

goods. This policy, as well as the preceding ones, disturts firms' locations

from the economically rational locations.

State governments provide a host of incentives aimed at attracting

industries to their own states. They include financial assistance for

investment, the provisioin of infrastructure and industrial estates,

concessions in power and water tariffs and concessions in taxes.

The policies Lnfluencing intra-regional distribution of industries

include (1) those for encouraging village and cottage industries as well as

modern small-scale enterprises, (2) industrial estate programs, (3) the Rural

Industries Project Program, (4) metropolitan planning and (5) incentives to

promote industrial development in backward districts. Generally they are

designed to promote the development of rural and backward areas by encouraging

industries in those areas or by encouraging traditional or small enterprises

which are more equally distributed over space. One exception is metropolitan

planning which is frequently oriented to zoning out industries to peripheral

areas. One example is the Bombay Metropolitan Regional Plan of 1973 which

attempted to divert most industries to the "counter magnet" across the bay.

Then, Chapter 3 analyzes changes in the spatial pattern of

industrial location during recent decades. As far as interstate distribution

of industry is concerned, various indices indicate that the concentration of

industry subsided from the 1960's to the 1970's. For example, converging

trends among states were observable from 1961 to 1975 in the share of the

manufacturing sector in the state product and in the value added per employee

in the manufacturing sector. Also, the industrial value added and employment

became more equally distributed among states from 1960 to 1975 as measured by

the Theil's Inequality and the Hirschman-Herfindhal Indices. Since the trends

in industrial location are results of both market forces and government

policy, it is not possible to conclude that the industrial location policies

have successfully narrowed disparities among states. However, there are good

reasons for speculating that some of the policies were instrumental in

narrowing the disparities.

The intra-regional distribution of industry was examined next. By

comparing the degree of concentration of industrial employment in 1961 and

1971 by grouping cities by size, the following conclusions were obtained: for

India as a whole, the employment in the household industry lost the degree of

concentration substantially from 1961 to 1971, due to a reduction of

concentration (relative to population) in the smaller classes of towns.

However, the non-household industry maintained its level of concentration

during the period. This means that the industrial policy apparently had not

resulted in any substantial shift of industry away from large cities to

smaller towns.

Chapter 4 presents an overall assessment of industrial location

policy. From the viewpoint of efficiency in resource allocation, one should

not expect a regionally balanced industrial development because natural

resources are not evenly distributed and there are economies of scale and

agglomeration in production processes. Industrial policies by the public

sector are needed for the provision of infrastructure because in principle

they cannot be provided adequately by the private sector and for correcting

externalities which arise in the form of congestion and pollution. However,

the former can best be provided by identifying gaps in infrastructure based on

the demand for infrastructure and the costs of providing it. Externalities

can best be dealt with by adjusting prices to reflect externalities.

Therefore, from the viewpoint of efficiency, the best set of measures to

correct inefficient locational distribution of industries operates via

readjustments in infrastructural investment and the prices charged for their

utilization. Direct industrial location policies such as licensing and input

rationing are poor substitutes. Even if the best solutions are not workable,

it would be advisable to operate through incentives and disincentives rather

than through controls, because the latter were crude devices and may lead to

extremely large efficiency loss in the national economy without being detected

by any observer.

A stronger argument may be made for industrial location policy for

the sake of spatial equity. However, as population and labor are mobile

within a country and particularly within a state, the need of achieving

spatial equity itself can be questioned.

In addition, there is serious doubt about the effectiveness of

industrial location policy in achieving spatial equity. One serious

limitation of locational control is that, contrary to expectations, controls

cannot induce industrialists to invest in non-viable areas. Therefore, if

licensing is utilized actively for locational purposes, the result will be a

decrease in investment in the restricted areas without a compensating increase

in the other areas. This involves not only a loss in efficiency, but also a

defeat of the objective of industrializing non-restricted areas.

This and other examples of serious inefficiencies generated by

industrial location policies imply that not enough thought has been given to

the rationale of these policies. Our exploration of their ramifications

reveals that a thorough overhauling is required in the approach toward

locational concentration of industry.

-1-

Chapter I

INTRODUCTION

Economic development, by its very nature, is a dynamic process

characterized by various types of "imbalances." Nowhere is this more striking

than in the spatial dimensions of growth, growth which tends to get

concentrated in certain regions within the economy and, in the case of

non-agricultural activities, at a few nodal metropolitan centers. Whether

this spatial "imbalance" is a "natural" and dynamically efficient (in the

Pareto sense) concomitant of the growth process or whether it is partly a

result of imperfectly functioning markets and externalities is a debatable

issue. The answer varies, of course, from country to country and must be

settled by empirical evidence. Even if spatial concentration is efficient,

one is still faced with the equity issue, which is extremely important in a

geographically large federal polity such as India. Motivated by these welfare

and efficiency considerations, the Indian government has been adopting a

series of measures to promote a more decentralized and "balanced" form of

development. In this study, we are only concerned with those measures

affecting the manufacturing sector. Our objective is to examine the various

explicit policies that have been used by the state to influence industrial

location and to assess their effects. But before embarking on a study of

these policies, it would be useful to set the stage by briefly surveying the

pattern of industrial growth in India.

The origins of modern industry in India can be traced as far back as

the nineteenth century. Even the diversification of the manufacturing sector

from its predominant emphasis on consumer goods started early in the twentieth

-2-

century when Jamshedji Tata succeeded in setting up a steel plant in 1911

against tremendous odds. Because of these early origins, the Indian

manufacturing sector at the time of independence in 1947 was already quite

large in comparison with other developing countries. After 1947, the era

of planned development began, and this gave further impetus to

industrialization. The State also took an active role in setting up

industries producing basic and capital goods, especially during the Second

Five-year Plan (1956-61).

However, despite these early traditions of entrepreneurship,

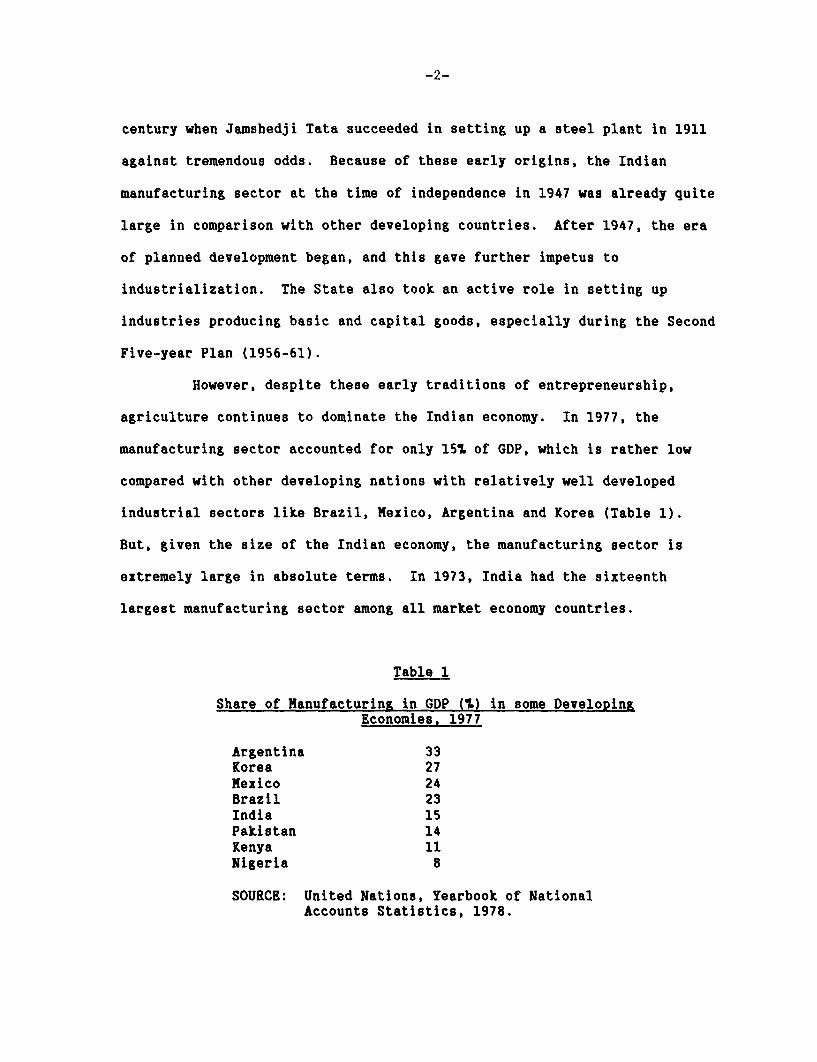

agriculture continues to dominate the Indian economy. In 1977, the

manufacturing sector accounted for only 157. of GDP, which is rather low

compared with other developing nations with relatively well developed

industrial sectors like Brazil, Mexico, Argentina and Korea (Table 1).

But, given the size of the Indian economy, the manufacturing sector is

extremely large in absolute terms. In 1973, India had the sixteenth

largest manufacturing sector among all market economy countries.

Table 1

Share of Manufacturing in GDP (C) in some DevelopingEconomies, 1977

Argentina 33Korea 27Mexico 24Brazil 23India 15Pakistan 14Kenya 11Nigeria 8

SOURCE: United Nations, Yearbook of NationalAccounts Statistics, 1978.

-3-

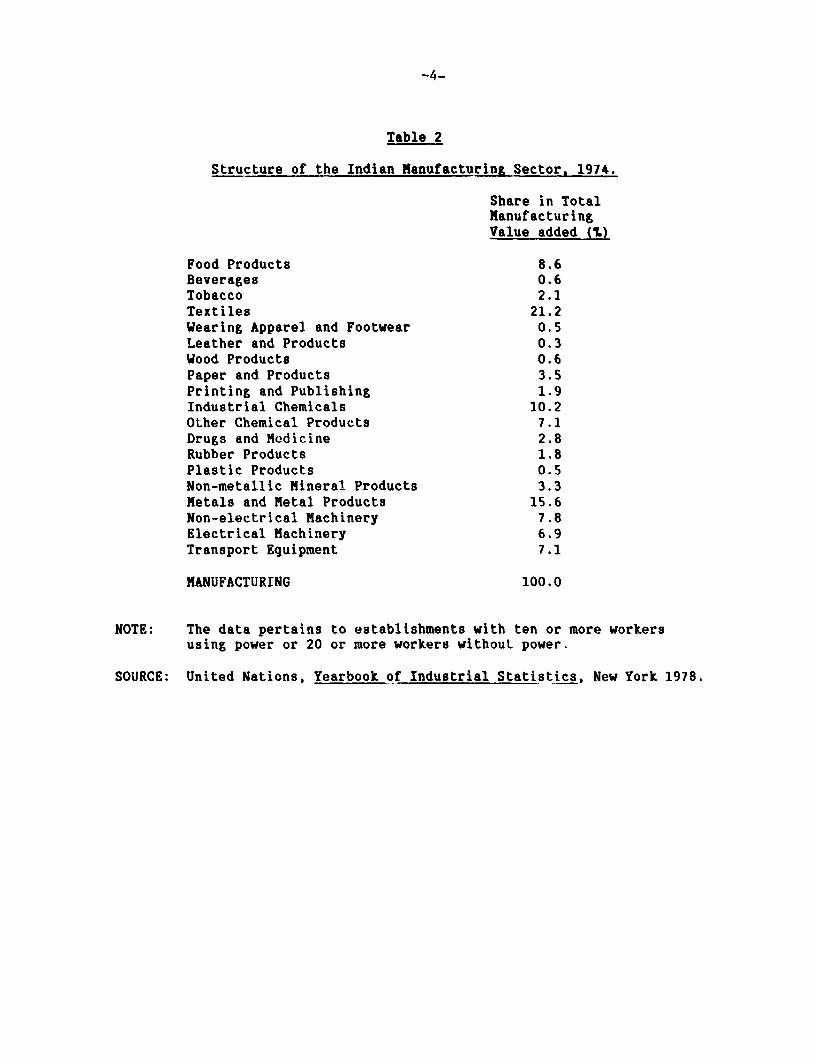

As Table 2 shows, the Indian manufacturing sector is quite

diversified, with capital goods constituting as much as 22% of value added

in manufacturing in 1974. The corresponding shares for consumer and

intermediate goods were 32% and 46% respectively. The institutional

milieu of Indian manufacturing displays an interesting diversity. The

most remarkable aspect is the importance of production by traditional and

small scale enterprise. The so-called "unregistered sector," consisting

predominantly of cottage and village industries utilizing traditional

techniques and employing household labor to a significant extent,

contributed more than a third of total value added in manufacturing in

1975. Small modern enterprises (which, in 1980, were defined as factories

with fixed capital value of less than Rs. two million) accounted for 16%.

In addition, there are imanufacturing units operated by the State, whose

output constituted only 12% of total manufacturing output in 1973.

However, this understates their real importance, since public sector units

are mainly engaged in tlhe production of certain critical items like steel

and various types of machinery and transport equipment. In comparison

with certain other deveLoping countries, foreign capital plays a

relatively minor role in the Indian industrial sector. Only 8.5% of total

paid-up capital in Indimn joint stock companies in 1969-70 originated from

foreign sources. Value added in foreign subsidiaries constituted only

about one tenth of total value added in manufacturing in the same year.

The remaining part of the manufacturing sector is, of course, the private

sector steered by domestic entrepreneurship.

-4-

Table 2

Structure of the Indian Manufacturing Sector, 1974.

Share in TotalManufacturingValue added (IL)

Food Products 8.6Beverages 0.6Tobacco 2.1Textiles 21.2Wearing Apparel and Footwear 0.5Leather and Products 0.3Wood Products 0.6Paper and Products 3.5Printing and Publishing 1.9Industrial Chemicals 10.2Other Chemical Products 7.1Drugs and Modicine 2.8Rubber Products 1.8Plastic Products 0.5Non-metallic Mineral Products 3.3Metals and Metal Products 15.6Non-electrical Machinery 7.8Electrical Machinery 6.9Transport Equipment 7.1

MANUFACTURING 100.0

NOTE: The data pertains to establishments with ten or more workersusing power or 20 or more workers without power.

SOURCE: United Nations, Yearbook of Industrial Statistics, New York 1978.

-5-

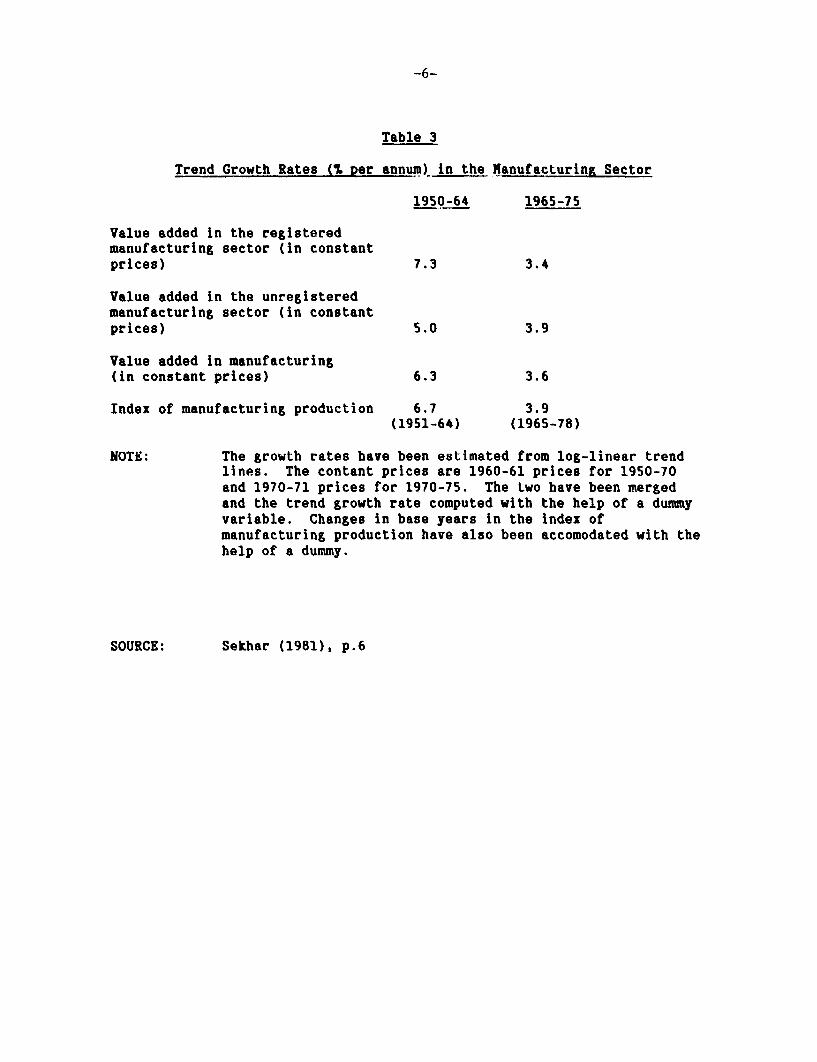

Table 3 shows the growth rates of value added in the registered

and unregistered manufaLcturing sectors and in the index of manufacturing

production during the periods 1951-64 and 1965-78. The major feature of

industrial development during Lhe post 1965 period that has attracted

attention is the slowdown in growth of the organized sector, which

declined sharply from 7.37 per annum to about 3.47 per annum in the two

periods. The deceleration of the unregistered manufacturing sector has

been more moderate, though significant. The net result has been that the

growth rate of real value added in the manufacturing sector as a whole

fell from 6.37 per annum in 1950-64 to 3.67 per annum during 1965-75.

One of the striking characteristics of Indian industrial

development is its uneven geographical spread. In order to identify the

relative degree of industrialization of different states, we computed the

share of value added in the factory manufacturing sector in NDP for each

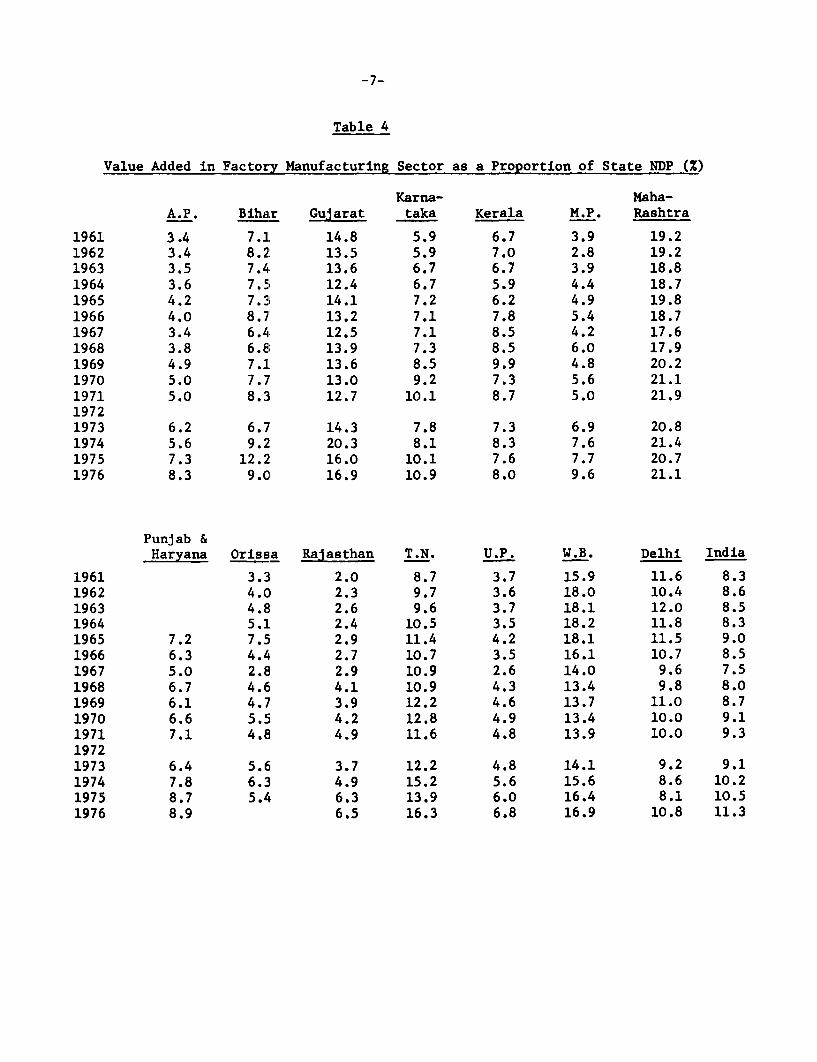

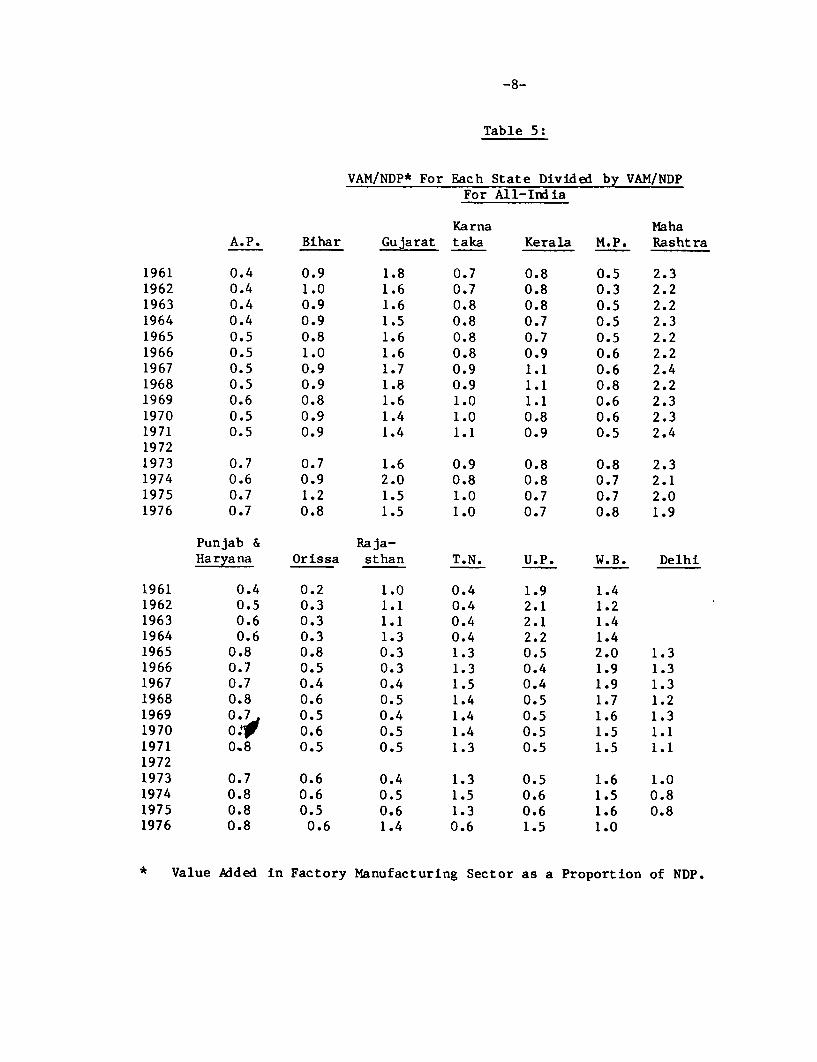

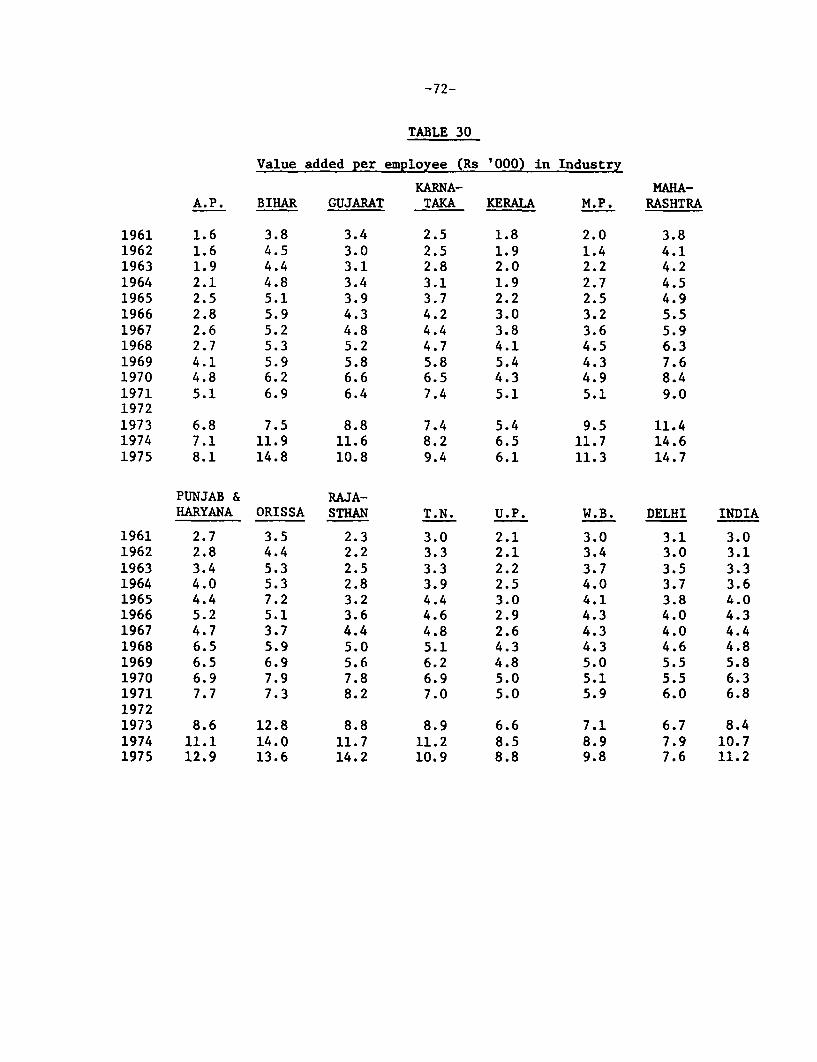

state (Tables 4 & 5). Comparing the ratios for 1976, one finds that

Maharashtra, West Bengal, Gujarat and Tamil Nadu were the industrial

leaders, in the sense that they had an above average manufacturing value

added/NDP (VAM/NDP) ratio. In 1961, also, these states (along with Delhi)

were relatively more industrialized (with the exception of Tamil Nadu).

However, during 1961-76, the manufacturing sectors of the other states

have been growing at a faster pace relative to NDP. As a result, a trend

towards equalization of state VAMP/NDP ratios is apparent.

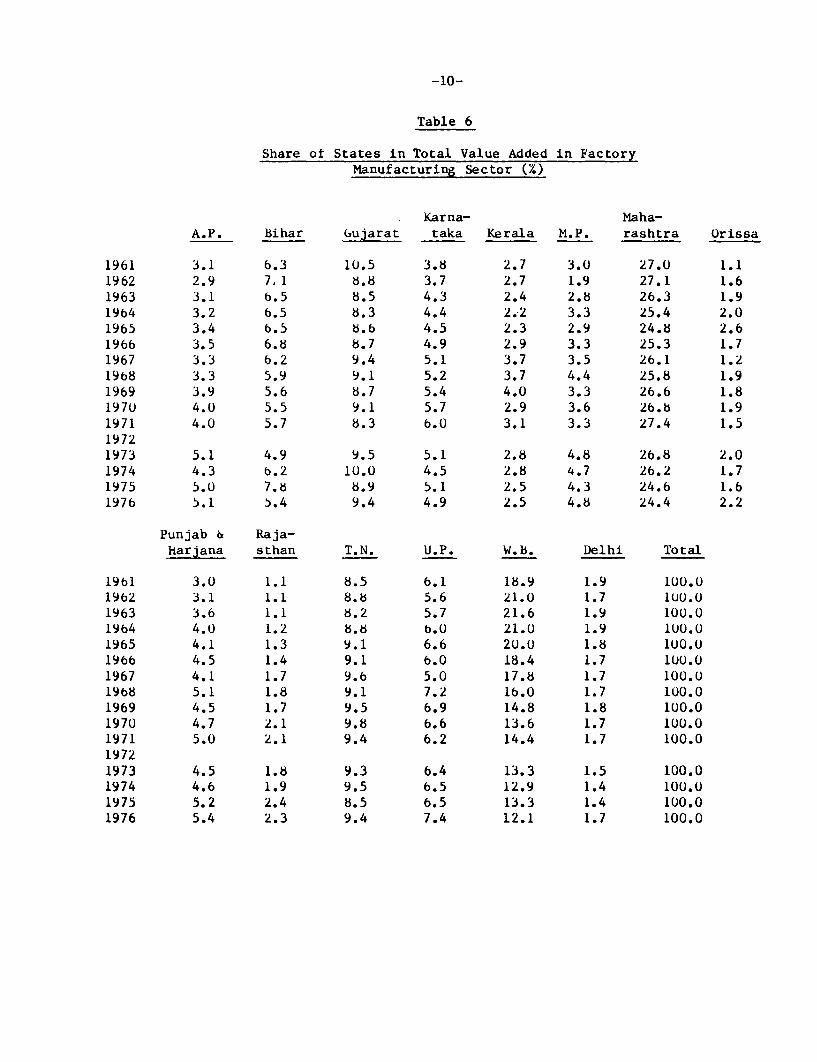

In 1976, Maharashtra, West Bengal, Gujarat, and Tamil Nadu

together accounted for about 557 of value added and 527 of employment in

the manufacturing sector (Tables 6 & 7). The contribution of Maharashtra

alone was about 257 of value added and 197 of employment. However, the

shares of these states hiave been falling since 1961, when they

contributed as much as two-thirds of value added and 587 of employment.

-6-

Table 3

Trend Growth Rates (. Rer annum) in the Manufacturinz Sector

1950-64 1965-75

Value added in the registeredmanufacturing sector (in constantprices) 7.3 3.4

Value added in the unregisteredmanufacturing sector (in constantprices) 5.0 3.9

Value added in manufacturing(in constant prices) 6.3 3.6

Index of manufacturing production 6.7 3.9(1951-64) (1965-78)

NOTE: The growth rates have been estimated from log-linear trendlines. The contant prices are 1960-61 prices for 1950-70and 1970-71 prices for 1970-75. The two have been mergedand the trend growth rate computed with the help of a dummyvariable. Changes in base years in the index ofmanufacturing production have also been accomodated with thehelp of a dummy.

SOURCE: Sekhar (1981), p.6

-7-

Table 4

Value Added in Factory Manufacturing Sector as a Proportion of State NDP (%)

Karna- Maha-A.P. BihaLr Gujarat taka Kerala M.P. Rashtra

1961 3.4 7.1 14.8 5.9 6.7 3.9 19.21962 3.4 8.2 13.5 5.9 7.0 2.8 19.21963 3.5 7.4 13.6 6.7 6.7 3.9 18.81964 3.6 7.5 12.4 6.7 5.9 4.4 18.71965 4.2 7.31 14.1 7.2 6.2 4.9 19.81966 4.0 8.7 13.2 7.1 7.8 5.4 18.71967 3.4 6.4 12.5 7.1 8.5 4.2 17.61968 3.8 6.8 13.9 7.3 8.5 6.0 17.91969 4.9 7.1 13.6 8.5 9.9 4.8 20.21970 5.0 7.7 13.0 9.2 7.3 5.6 21.11971 5.0 8.3 12.7 10.1 8.7 5.0 21.919721973 6.2 6.7 14.3 7.8 7.3 6.9 20.81974 5.6 9.2 20.3 8.1 8.3 7.6 21.41975 7.3 12.2 16.0 10.1 7.6 7.7 20.71976 8.3 9.C0 16.9 10.9 8.0 9.6 21.1

Punjab &Haryana Orissa Rajasthan T.N. U.P. W.B. Delhi India

1961 3.3 2.0 8.7 3.7 15.9 11.6 8.31962 4.0 2.3 9.7 3.6 18.0 10.4 8.61963 4.8 2.6 9.6 3.7 18.1 12.0 8.51964 5.1 2.4 10.5 3.5 18.2 11.8 8.31965 7.2 7.5 2.9 11.4 4.2 18.1 11.5 9.01966 6.3 4.4 2.7 10.7 3.5 16.1 10.7 8.51967 5.0 2.8 2.9 10.9 2.6 14.0 9.6 7.51968 6.7 4.6 4.1 10.9 4.3 13.4 9.8 8.01969 6.1 4.7 3.9 12.2 4.6 13.7 11.0 8.71970 6.6 5.5 4.2 12.8 4.9 13.4 10.0 9.11971 7.1 4.8 4.9 11.6 4.8 13.9 10.0 9.319721973 6.4 5.6 3.7 12.2 4.8 14.1 9.2 9.11974 7.8 6.3 4.9 15.2 5.6 15.6 8.6 10.21975 8.7 5.4 6.3 13.9 6.0 16.4 8.1 10.51976 8.9 6.5 16.3 6.8 16.9 10.8 11.3

-8-

Table 5:

VAM/NDP* For Each State Divided by VAM/NDPFor All-India

Karna MIahaA.P. Bihar Gujarat taka Kerala M.P. Rashtra

1961 0.4 0.9 1.8 0.7 0.8 0.5 2.31962 0.4 1.0 1.6 0.7 0.8 0.3 2.21963 0.4 0.9 1.6 0.8 0.8 0.5 2.21964 0.4 0.9 1.5 0.8 0.7 0.5 2.31965 0.5 0.8 1.6 0.8 0.7 0.5 2.21966 0.5 1.0 1.6 0.8 0.9 0.6 2.21967 0.5 0.9 1.7 0.9 1.1 0.6 2.41968 0.5 0.9 1.8 0.9 1.1 0.8 2.21969 0.6 0.8 1.6 1.0 1.1 0.6 2.31970 0.5 0.9 1.4 1.0 0.8 0.6 2.31971 0.5 0.9 1.4 1.1 0.9 0.5 2.419721973 0.7 0.7 1.6 0.9 0.8 0.8 2.31974 0.6 0.9 2.0 0.8 0.8 0.7 2.11975 0.7 1.2 1.5 1.0 0.7 0.7 2.01976 0.7 0.8 1.5 1.0 0.7 0.8 1.9

Punjab & Raja-Haryana Orissa sthan T.N. U.P. W.B. Delhi

1961 0.4 0.2 1.0 0.4 1.9 1.41962 0.5 0.3 1.1 0.4 2.1 1.21963 0.6 0.3 1.1 0.4 2.1 1.41964 0.6 0.3 1.3 0.4 2.2 1.41965 0.8 0.8 0.3 1.3 0.5 2.0 1.31966 0.7 0.5 0.3 1.3 0.4 1.9 1.31967 0.7 0.4 0.4 1.5 0.4 1.9 1.31968 0.8 0.6 0.5 1.4 0.5 1.7 1.21969 0.7 0.5 0.4 1.4 0.5 1.6 1.31970 0.1 0.6 0.5 1.4 0.5 1.5 1.11971 0.8 0.5 0.5 1.3 0.5 1.5 1.119721973 0.7 0.6 0.4 1.3 0.5 1.6 1.01974 0.8 0.6 0.5 1.5 0.6 1.5 0.81975 0.8 0.5 0.6 1.3 0.6 1.6 0.81976 0.8 0.6 1.4 0.6 1.5 1.0

* Value Added in Factory Manufacturing Sector as a Proportion of NDP.

-9-

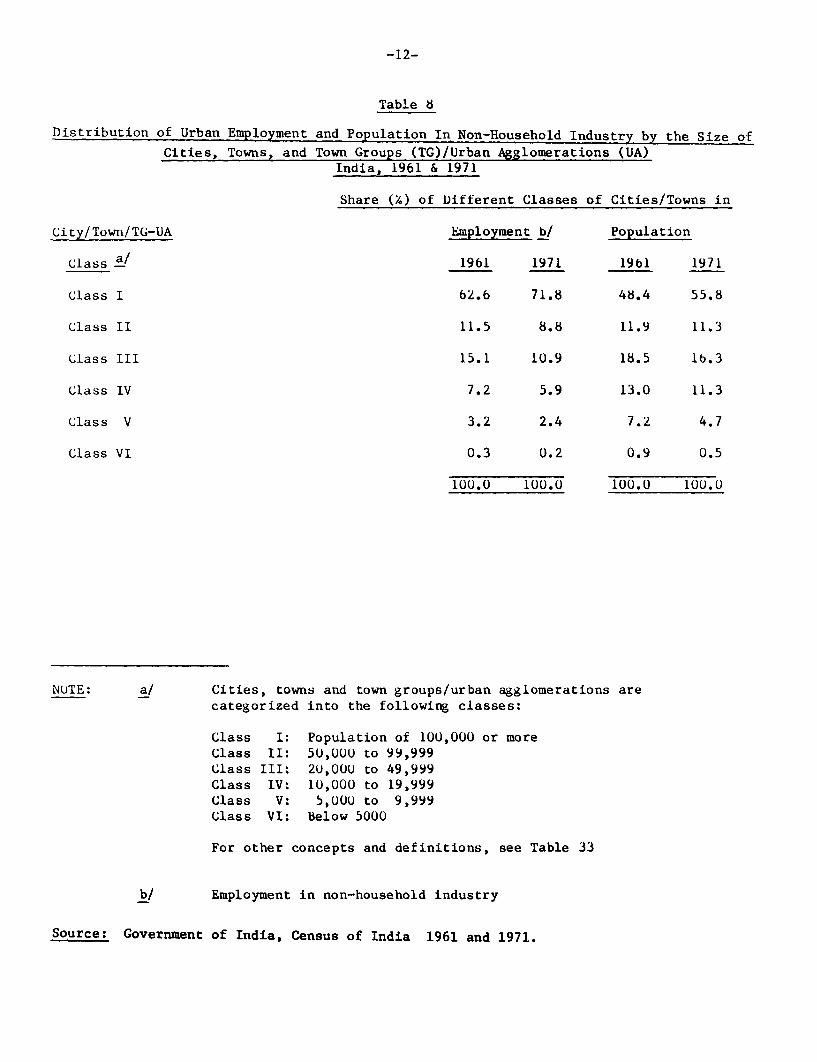

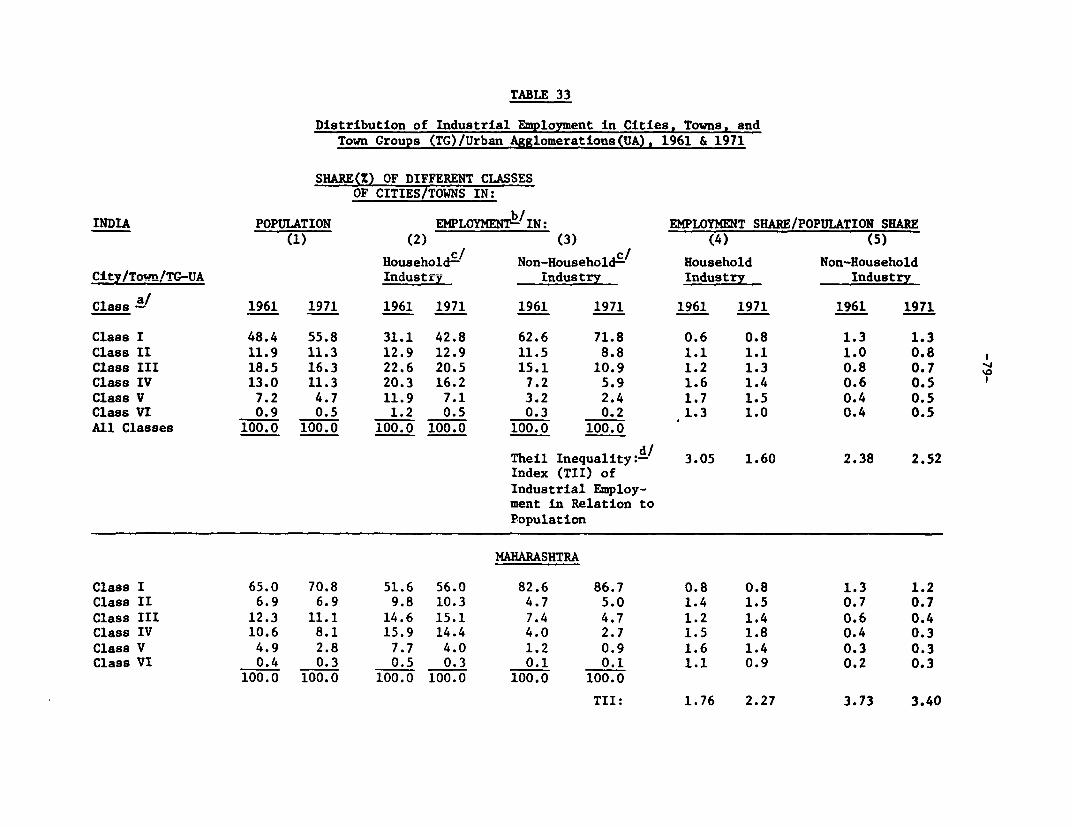

The distribution of industrial employment (in household and

non-household industry) among different classes of cities and towns in

1961 and 1971 is presented in Table 8. Factory industry is heavily

concentrated in cities with population exceeding 100,000 - cities which in

1971 employed over 70'S of factory workers.

We shall ana:lyze trends in industrial location in greater depth

later in this paper. Here, we have merely tried to present the marked

inter- and intrastate differences in industrialization which are the

motivating forces behind the design and implementation of locational

policies, to which we now turn our attention.

-10-

Table 6

Share of States in Total Value Added in FactoryManufacturing Sector (7.)

Karna- Maha-A.P. Bihar Gujarat taka Kerala M.P. rashtra Orissa

1961 3.1 6.3 10.5 3.8 2.7 3.0 27.0 1.11962 2.9 7, 8.8 3.7 2.7 1.9 27.1 1.61963 3.1 6.5 8.5 4.3 2.4 2.8 26.3 1.91964 3.2 6.5 8.3 4.4 2.2 3.3 25.4 2.01965 3.4 6.5 8.6 4.5 2.3 2.9 24.8 2.61966 3.5 6.8 8.7 4.9 2.9 3.3 25.3 1.71967 3.3 6.2 9.4 5.1 3.7 3.5 26.1 1.21968 3.3 5.9 9.1 5.2 3.7 4.4 25.8 1.91969 3.9 5.6 8.7 5.4 4.0 3.3 26.6 1.81970 4.0 5.5 9.1 5.7 2.9 3.6 26.b 1.91971 4.0 5.7 8.3 6.0 3.1 3.3 27.4 1.519721973 5.1 4.9 9.5 5.1 2.8 4.8 26.8 2.01974 4.3 b.2 10.0 4.5 2.8 4.7 26.2 1.71975 5.0 7.8 8.9 5.1 2.5 4.3 24.6 1.61976 5.1 5.4 9.4 4.9 2.5 4.8 24.4 2.2

Punjab & Raja-harjana sthan T.N. U.P. W.B. Delhi Total

1961 3.0 1.1 8.5 6.1 18.9 1.9 100.01962 3.1 1.1 8.8 5.6 21.0 1.7 100.01963 3.6 1.1 8.2 5.7 21.6 1.9 100.01964 4.0 1.2 8.8 b.0 21.0 1.9 100.01965 4.1 1.3 9.1 6.6 20.0 1.8 100.01966 4.5 1.4 9.1 6.0 18.4 1.7 100.01967 4.1 1.7 9.6 5.0 17.8 1.7 100.01968 5.1 1.8 9.1 7.2 16.0 1.7 100.01969 4.5 1.7 9.5 6.9 14.8 1.8 100.01970 4.7 2.1 9.8 6.6 13.6 1.7 100.01971 5.0 2.1 9.4 6.2 14.4 1.7 100.019721973 4.5 1.8 9.3 6.4 13.3 1.5 100.01974 4.6 1.9 9.5 6.5 12.9 1.4 100.01975 5.2 2.4 8.5 6.5 13.3 1.4 100.01976 5.4 2.3 9.4 7.4 12.1 1.7 100.0

-11-

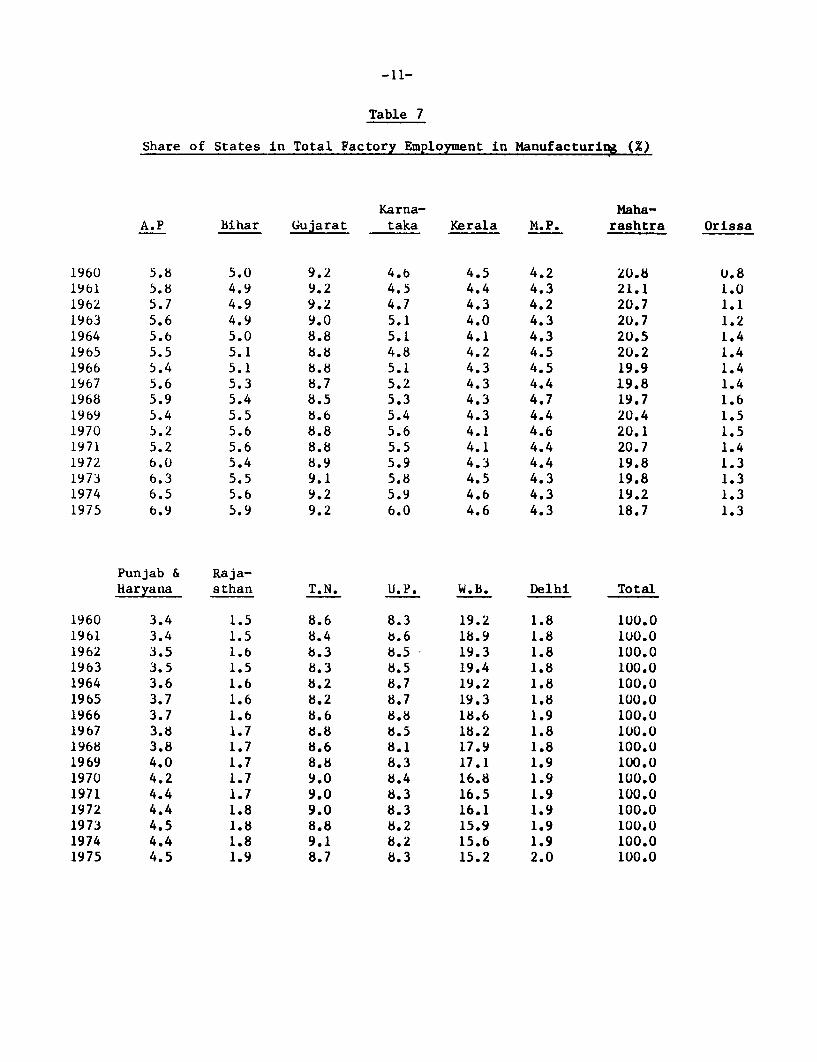

Table 7

Share of States in Total Factory Employment in Manufacturing (X)

Karna- Maha-A.P Bihar Gujarat taka Kerala M.P. rashtra Orissa

1960 5.8 5.0 9.2 4.6 4.5 4.2 20.8 0.81961 5.8 4.9 9.2 4.5 4.4 4.3 21.1 1.01962 5.7 4.9 9.2 4.7 4.3 4.2 20.7 1.11963 5.6 4.9 9.0 5.1 4.0 4.3 20.7 1.21964 5.6 5.0 8.8 5.1 4.1 4.3 20.5 1.41965 5.5 5.1 8.8 4.8 4.2 4.5 20.2 1.41966 5.4 5.1 8.8 5.1 4.3 4.5 19.9 1.41967 5.6 5.3 8.7 5.2 4.3 4.4 19.8 1.41968 5.9 5.4 8.5 5.3 4.3 4.7 19.7 1.61969 5.4 5.5 8.6 5.4 4.3 4.4 20.4 1.51970 5.2 5.6 8.8 5.6 4.1 4.6 20.1 1.51971 5.2 5.6 8.8 5.5 4.1 4.4 20.7 1.41972 6.0 5.4 8.9 5.9 4.3 4.4 19.8 1.31973 6.3 5.5 9.1 5.8 4.5 4.3 19.8 1.31974 6.5 5.6 9.2 5.9 4.6 4.3 19.2 1.31975 6.9 5.9 9.2 6.0 4.6 4.3 18.7 1.3

Punjab & Raja-Haryana sthan T.N. U.P. W.B. Delhi Total

1960 3.4 1.5 8.6 8.3 19.2 1.8 100.01961 3.4 1.5 8.4 b.6 18.9 1.8 1U0.O1962 3.5 1.b 8.3 8.5 19.3 1.8 100.01963 3.5 1.5 8.3 8.5 19.4 1.8 100.01964 3.6 1.6 8.2 8.7 19.2 1.8 100.01965 3.7 1.6 8.2 8.7 19.3 1.8 100.01966 3.7 1.6 8.6 8.8 18.6 1.9 100.01967 3.8 1.7 8.8 8.5 18.2 1.8 100.01968 3.8 1.7 8.6 8.1 17.9 1.8 100.01969 4.0 1.7 8.8 8.3 17.1 1.9 100.01970 4.2 1.7 9.0 8.4 16.8 1.9 100.01971 4.4 1.7 9.0 8.3 16.5 1.9 100.01972 4.4 1.8 9.0 8.3 16.1 1.9 100.01973 4.5 1.8 8.8 8.2 15.9 1.9 100.01974 4.4 1.8 9.1 8.2 15.6 1.9 100.01975 4.5 1.9 8.7 8.3 15.2 2.0 100.0

-12-

Table 8

Distribution of Urban Employment and Population In Non-Household Industry by the Size of

Cities, Towns, and Town Groups (TG)/Urban Agglomerations (UA)India, 1961 & 1971

Share (.) of Different Classes of Cities/Towns in

City/Town/TG-UA Employment b/ Population

Class a/ 1961 1971 1961 1971

Class I 62.6 71.8 48.4 55.8

Class II 11.5 8.8 11.9 11.3

Class III 15.1 10.9 18.5 16.3

Class IV 7.2 5.9 13.0 11.3

Class V 3.2 2.4 7.2 4.7

Class VI 0.3 0.2 0.9 0.5

100.0 100.0 100.0 100.0

NuTE: a/ Cities, towns and town groups/urban agglomerations arecategorized into the following classes:

Class I: Population of 100,000 or moreClass II: 50,0UU to 99,999Class III: 2U,000 to 49,999Class IV: 10,000 to 19,999Class V: 5,000 to 9,999Class VI: Below 5000

For other concepts and definitions, see Table 33

b/ Employment in non-household industry

Source: Government of India, Census of India 1961 and 1971.

-13-

Chapter II

INDUSTRIAL LOCATION POLICIES IN INDIA

Before examining the content of the industrial location policies,

we shall aLtempt to throw some light on the factors that influenced the

policy-makers in adopting these measures. Unfortunately, these factors

are not clearly formulated in any of the policy documents, for example,

the five-year plans. The justifications for state intervention in

industrial location are couched in efficiency and equity terms, but there

is no precise idea about the trade-offs involved (wherever these exist).

This probably reflects, to a significant extent, a major weakness of the

theoretical development literature and its failure to develop an empirical

methodology to assess the most "desirable" spatial distribution of

industry.

However, a clear difference in motivation can be perceived

between policies influencing inter and intra regional distribution of

industry. In India, It is individual states that form the basis of

regionalization by the decision makers, though sometimes the

North-South-East-West divisions are also utilized. The original

demarcation of the states was on a linguistic basis, with a corresponding

cultural and ethnic homogeneity. Thus, strong sociological bonds tie the

inhabitants of each state together, and create effective demands for

receiving "just" shares of the national pie. The Indian Republic attained

independence only about three decades back, so that these demands can be

backed by arguments about unequal treatment during the colonial period.

The setting-up of infrastructure and transportation networks during

British rule was determined largely by political exigencies and the

colony-metropolis tracle relationship. This obviously meant that, at the

-14-

time of independence, the regions started with different infrastructural

endowments - a problem with which the new government had to come to

terms. Apart from these historical reasons, physical endowments and

various socio-economic factors are responsible for the diverging

performances of different regions. However, even in instances where these

factors dominate, it is politically infeasible to let these differences in

growth exceed certain limits in keeping with the character of the federal

polity. All these political and equity considerations have led the Indian

government to attempt to implement policies to promote a more balanced

inter-state distribution of industry.

Policies targeted at affecting intra-regional industrial location

have been motivated both by efficiency and welfare arguments. Efficiency

justifications have focused on the inoptimal distribution of

infrastructure and imperfectly functioning markets that have led to the

concentration of industry in certain metropolitan regions to the neglect

of smaller towns and backward areas. It is argued that the latter possess

industrial potential but have not developed because of insufficient

infrastructural investment, high risk aversion on the part of

entrepreneurs in the face of uncertainty, and imperfectly functioning

capital markets. Proponents of these policies also point out that

agglomeration economies and economies of scale have been exhausted in

certain cities, and their continued expansion implies inefficient resource

allocation. However, apart from these efficiency issues, equity factors

are also seen as extremely important justifications of policies such as

those encouraging the village and handicrafts industries that have

traditionally formed an important component of rural economic life. These

industries utilize highly labor-intensive techniques which may be able to

-15-

absorb some part of the under-employment that characterizes Indian

agriculture. It is felt that encouragement of modern small-scale

enterprises, which tencl to be concentrated in the metropolitan areas, will

promote a moro equitable distribution of income by increasing the returns

to small entrepreneurs.

All these efficiency and equity issues and their implications for

industrial location and policy will be explored at length in Chapter 4

where we draw lessons from the Indian experience with industrial location

policies. First, however, we look at those designed to promote a more

balanced inter-state distribution of industry.

1. Policies Influencing Inter-State Distribution of Industry

Chronologically arranged in order of their implementation, these

policies have been of the following kinds:

(i) Industrial licensing;

(ii) Location oDf Public Sector Plants;

(iii) Distribution and pricing policies for intermediate industrial

inputs; and

(iv) State Government incentives.

(i) Industrial Licensing

The basic attitude of the Government of India towards the

direction and character of industrial development is still epitomized by

the "Industrial Policy Rtesolution" (IPR) that was adopted in 1956. 1/ One

of the important objectives of industrial policy listed in the IPR is

1/ This replaced an earlier resolution formulated soon after independence.

-16-

balanced regional development.l/ The mechanism of implementing industrial

policy was the Industries (Development and Regulation) Act of 1951. This

Act provided the legislative framework for the licensing and regulation of

industrial investment. A licence from the Central Government was required

for the establishment of a 'new' industrial undertaking or for

'subsLantial expansion' of existing units. 2/

There is heuristic evidence that the state governments have tried

to influence the licensing authorities in order to attract industry. The

testimony of officials to the Estimates Committee (1967-68) illustrates

this:

"It has been sLated by the official representative of the

Ministry that 'Quite a number of states keep on representing that

their areas have not received adequate share of licenses' we have

no compulsive means of attracting people to particular areas. We

consider the applications as we receive them and provided the

location in a particular area is not too uneconomic, other things

being reasonably equal, we do give preference to the more

underdeveloped areas." 3/

1/ Other, perhaps more important, objectives are: rapid industrializationin conformity with plan priorities and targets, development of basicand capital goods industries, expansion of the public and co-operativesector, protection and encouragement of the small scale sector and thecurbing of monopoly in industry.

2/ The precise rules relating to the licensing system have varied overtime. It must also be noted that additional licenses were requiredfor imports of equipment. Furthermore, there are a number of otherGovernment controls, e.g. price and distribution controls. Freshinvestment involving the large business houses or foreigncollaboration were subjected to further scrutiny by special statutorycommittees.

3/ However, the correlation coefficient with per capita income is only0.07.

-17-

The Industrial Licensing Policy Inquiry Committee Report (1967)

also reported that "there have been cases where, because of persistent

pressure by the state authorities concerned, licenses have been granted

for location within those states. Our case studies show that there were

certain states which followed up applications for location in their

territories very systematically and persistently and these states were

often able to ensure that applicants for licenses within their territory

succeeded." (p. 113)

However, the actual weightage assigned to regional location by

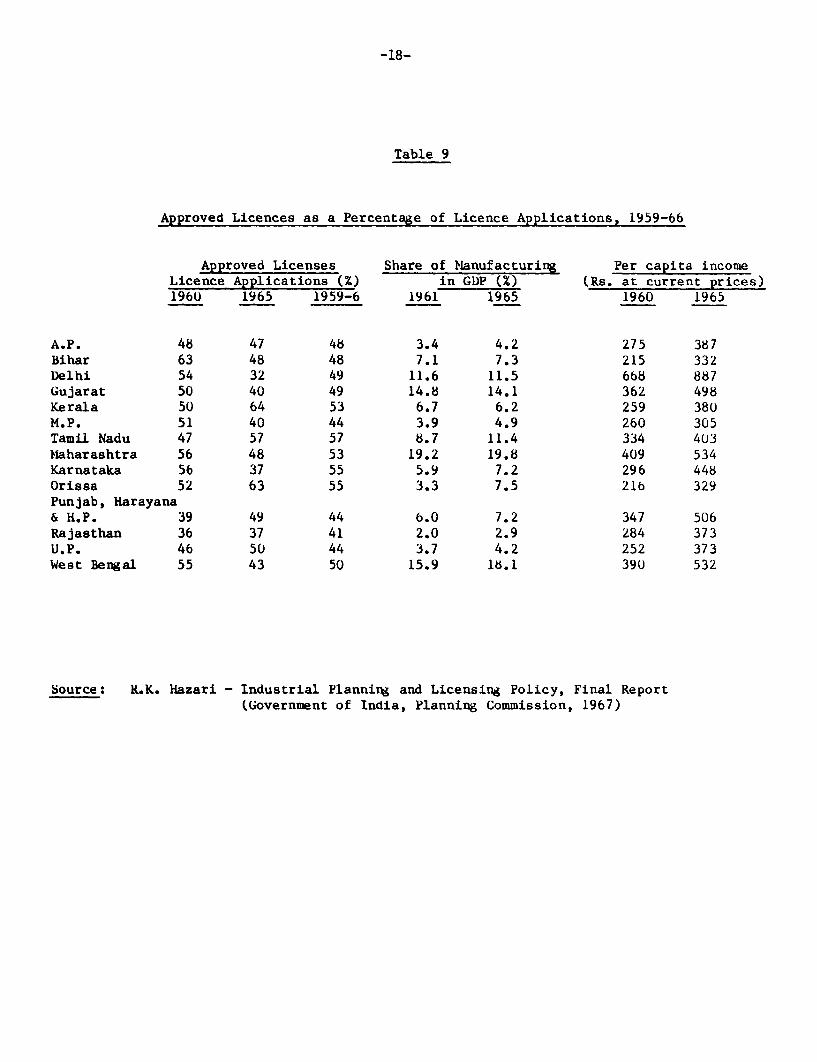

the licensing authorities is a moot point. The Hazari report, which

examined industrial planning and licensing policy, contains information

relating to state-wise licensing applications and approvals for the-period

1959-66. This is presented in Table 9. In order to assess the importance

of the "balanced regional development" objective, we correlated these

approval ratios with an index of state industrial development, i.e., the

share of industry in GDI?. The correlation coefficient turned out to be

0.40. 1/ Now, this result cannot be interpreted from a purely regional

perspective. This is because the approval ratio Is a function of many

other variables, like the techno-economic character of license

applications, and the other industrial policy objectives including the

relationship with plan piriorities, encouragement of the public and

small-scale sector, and the curbing of monopoly. Despite these

qualifications, the positive correlation does Indicate that the "balanced

regional development" objective has not prevented the more advanced

industrial states from faring better in the licensing decision process.

1/ However, the correlation coefficient with per capita Income is only0.07

-18-

Table 9

Approved Licences as a Percentage of Licence Applications, 1959-66

Approved Licenses Share of MIanufacturing Per capita incomeLicence Applications (X) in GDP (%) (Rs. at current prices)1960 1965 1959-6 1961 1965 1960 1965

A.P. 48 47 48 3.4 4.2 275 387Bihar 63 48 48 7.1 7.3 215 332Delhi 54 32 49 11.6 11.5 6W8 887Gujarat 50 40 49 14.8 14.1 362 498Kerala 50 64 53 6.7 6.2 259 380M.P. 51 40 44 3.9 4.9 260 305Tamil Nadu 47 57 57 8.7 11.4 334 403Miaharashtra 56 48 53 19.2 19.8 409 534Karnataka 56 37 55 5.9 7.2 296 448Orissa 52 63 55 3.3 7.5 21b 329Punjab, Harayana& H.P. 39 49 44 6.0 7.2 347 506Rajasthan 36 37 41 2.0 2.9 284 373U.P. 46 50 44 3.7 4.2 252 373West Bengal 55 43 50 15.9 1i.1 390 532

Source: L.K. liazari - Industrial Planning and Licensing Policy, Final Report(Government of India, Planning Commission, 1967)

-19-

An important contributory factor - apart from techno-economic superiority

of the applications from the advanced states - could be that the big and

more established producers in these states had the resources to

successfully lobby for allocation of licenses. For example, it was

financially less burdensome for them to maintain liaison offices at New

Delhi for this purpose.

This general conclusion pertains to the period 1959-66 as a

whole. The period is too small to permit trend analysis. Nevertheless,

it is interesting to compute the relationship between license approvals

and state development separately for 1960 and 1965 and compare the two

years. The results are presented in Table 10. The picture for 1960 is

essentially the same as that for the period 1959-66 as a whole, the

license approval ratio having a significant positive correlation with the

level of state industrial development while being almost unrelated to

state per capita incomes. However, for 1965, there is a dramatic switch -

the approval ratio displays a significant negative correlation with state

industrial development, while continuing to show little relationship with

per capita income. Thisi may be indicative of an increased importance

assigned to the objective of allocating licenses on an equitable basis to

the states.

-20-

Table 10

Correlation Coefficients between State-Wise Proportionsof Licenses Approved and Indices of State Development

Correlation of state-wise "approvedlicenses as a proportion of licenseapplications" with

1960 1965 1959-66 3/

Value added in manufacturingGDP for States 0.44 -0.09 0.40

State per capita income 2/ -0.10 -0.50 0.07

Notes

1/ Certain small states and union territories havebeen left out for lack of data.

2/ In current prices.

3/ The indices of state development used in computingthe coefficients are the averages of 1960 and 1965.

-21-

However, it would be premature to reach a definitive conclusion until it

is possible to extend our licensing data beyond 1966.

In our discusslon of industrial licensing, we have focused only

on inter-state allocation of licenses. In 1971, another regional

dimension was added to the licensing criteria by the decision to prohibit

the setting up of licensable industries within certain geographical limits

of large metropolitan cities with a population exceeding one million, and

urban agglomerations with a population greater than 0.5 million as per the

1971 census. 1/ In 1980, it was decided that undertakings in a large

number of industries could increase their capacity by 257 over a five year

period without having tco apply for a licence. Moreover, undertakings in

certain industries "of importance to the national economy" and "engaged in

the production of articles of mass consumption" which had installed

capacities in excess of licensed capacity were permitted to regularize

these. Both these types of liberalizations were available even to

undertakings located in the metropolitan areas mentioned earlier which had

been barred from expanding under the 1977 policy. Moreover, this

locational policy was also relaxed in certain other cases including those

units exporting 1007 of their output.

1/ Earlier, in 1973, it had been decided that units normally exempt fromthe licensing requir,ement (for example, the small scale sector) wouldhave to apply for a license if they were located in these areas.

-22-

(ii) Location of Public Sector Plants

Soon after independence, in 1954, the ruling Congress party

adopted the resolution of "constructing a socialistic pattern of society"

in India. Since then, the industrial policy statements of the Indian

government have given considerable priority to the development of the

public sector. In 1972, public sector units contributed to 127. of total

value added in the manufacturing sector. The Indian goverment has

explicitly sought to restrict the production of many types of basic and

capital goods to the public sector. Therefore, the public sector is the

major supplier of items like iron and steel, heavy electricals, petroleum

products, shipping and railway equipment. V/

Direct public investment in manufacturing commenced on a large

scale during the Second Fivo-year plan (1951-61). Regional considerations

have always been quite important in the location of these units. For

example, the Third Five-year plan (1961-66) stated that "in the location

of public sector projects, the claims of relatively backward areas have

been kept in view wherever this could be done without giving up essential

technical and economic criteria. The location of several important

projects like the steel plants have been determined on the basis of expert

study and on economic considerations. But as they are situated in areas

which were hitherto industrially backward, the latter will benefit." (3rd

Five-year plan, p. 145)

1/ For example, in the early '70s, the share of the public sector wasover 90% of output of saleable pig iron, heavy electrical equipmentlike synchronous condensers, steam and hydro turbines, generators andalternators, ships and locomotive boilers.

-23-

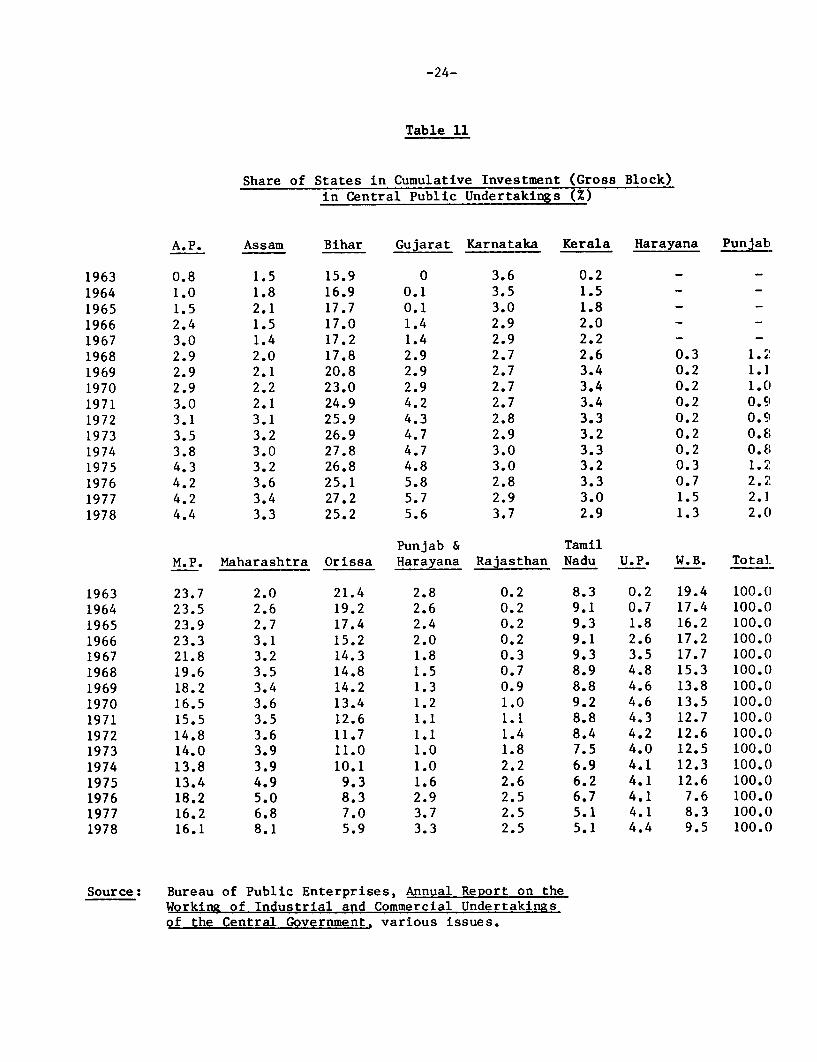

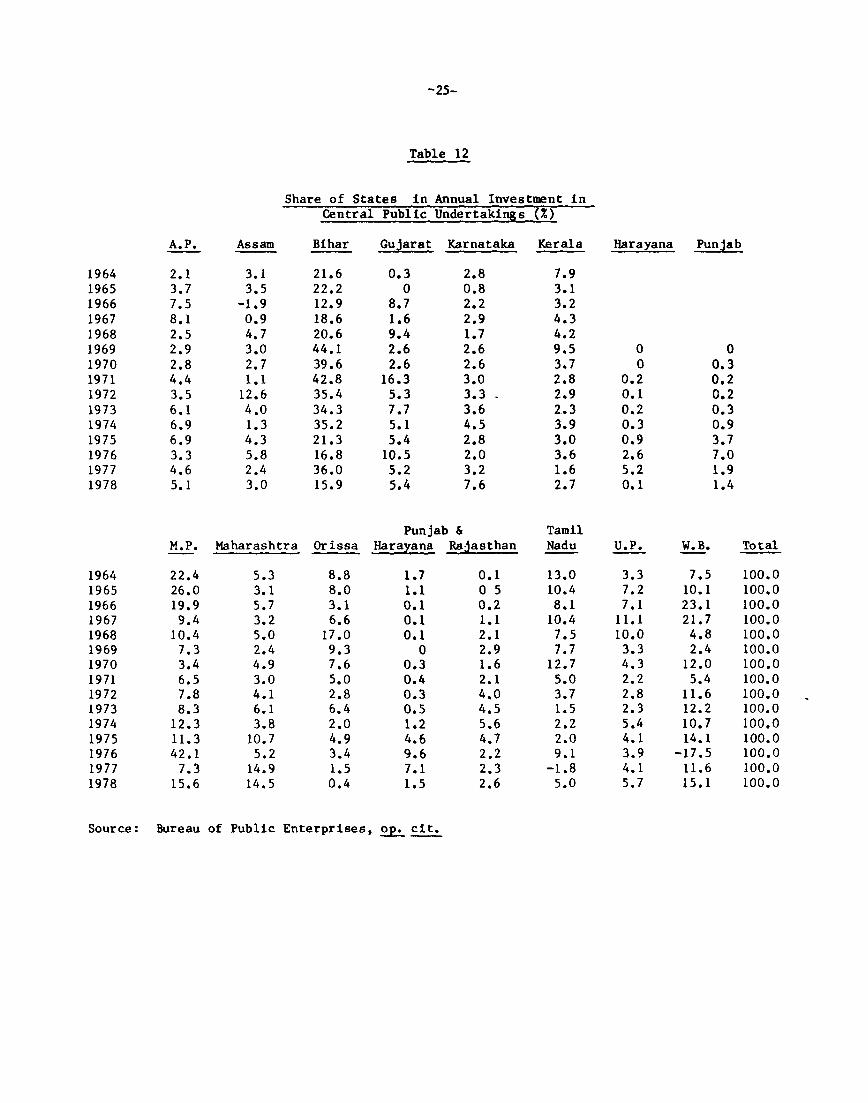

The shares of the states in cumulative and annual investment in

central public undertakings during 1963-78 are exhibited in Tables 11 and

12. In 1963, about 80* of this investment was concentrated in the four

states of Bihar, Nadhya Pradesh, Orissa and West Bengal. Since 1963, many

important public undertakings have come up in the other states, so that

the distribution across states has become somewhat more balanced. By

1978, the share of thet four states (just mentioned) in cumulative

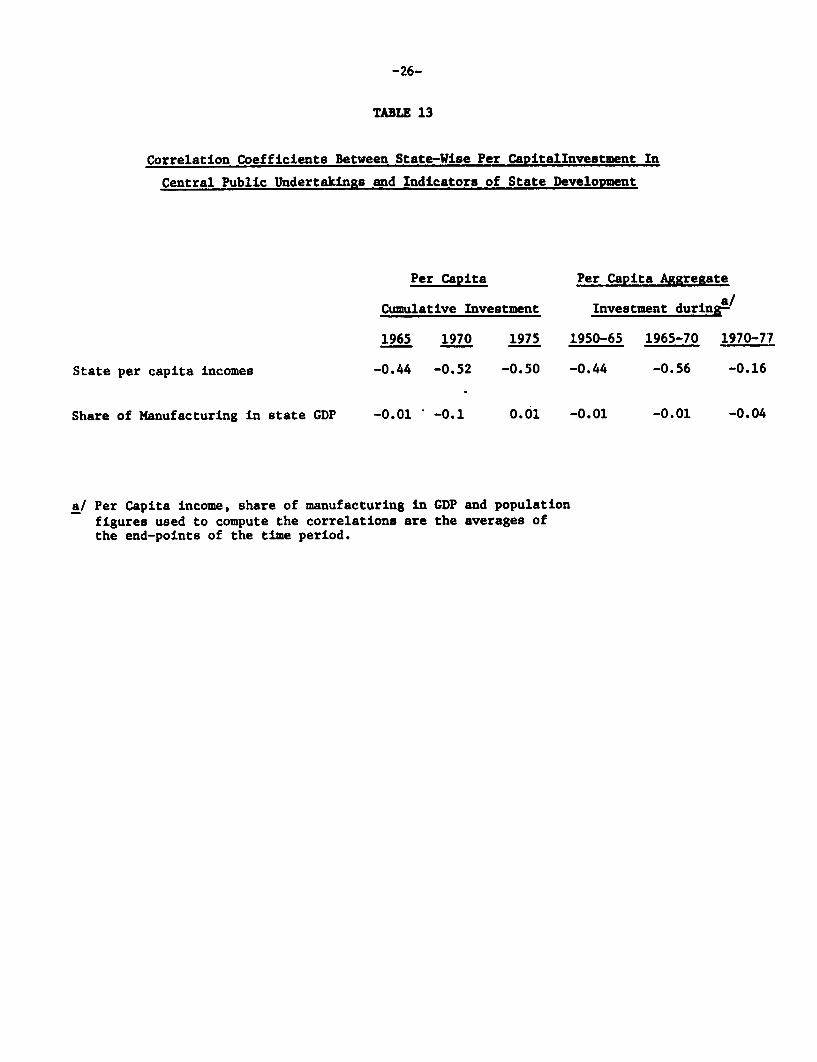

investment had come down to 57*. We attempted an empirical test of the

importance of regional considerations in the location of public sector

units. Just as in evaluating industrial licensing, this was done by

correlating Investment in Central Government public sector undertakings

per capita for each state with indices of state backwardness like per

capita income and the share of manufacturing in state income. The results

are presented in Table 13.

It appears that before 1970, states with low per capita incomes

have been favored in their share of public sector projects. However, as

the just-cited quote from the Third Plan suggests, this result may be

explained by the plentiful supply of appropriate raw materials in the

backward states rather than explicit locational considerations. To

illustrate this, consider the composition of the public sector in the

major low-income states favored before 1970 - Bihar, Madhya Pradesh and

Orissa. One finds that in 1969, steel plants accounted for one-third of

cumulative investment in Bihar, two-thirds in Madhya Pradesh and 90% in

Orissa.

-24-

Table 11

Share of States in Cumulative Investment (Gross Block)in Central Public Undertakings (%)

A.P. Assam Bihar Gujarat Karnataka Kerala Harayana Punjab

1963 0.8 1.5 15.9 0 3.6 0.2 - -

1964 1.0 1.8 16.9 0.1 3.5 1.5 - -

1965 1.5 2.1 17.7 0.1 3.0 1.8 - -1966 2.4 1.5 17.0 1.4 2.9 2.0 - -1967 3.0 1.4 17.2 1.4 2.9 2.2 - -1968 2.9 2.0 17.8 2.9 2.7 2.6 0.3 1.21969 2.9 2.1 20.8 2.9 2.7 3.4 0.2 1.1

1970 2.9 2.2 23.0 2.9 2.7 3.4 0.2 1.0

1971 3.0 2.1 24.9 4.2 2.7 3.4 0.2 0.9

1972 3.1 3.1 25.9 4.3 2.8 3.3 0.2 0.9

1973 3.5 3.2 26.9 4.7 2.9 3.2 0.2 0.8

1974 3.8 3.0 27.8 4.7 3.0 3.3 0.2 0.81975 4.3 3.2 26.8 4.8 3.0 3.2 0.3 1.2

1976 4.2 3.6 25.1 5.8 2.8 3.3 0.7 2.2

1977 4.2 3.4 27.2 5.7 2.9 3.0 1.5 2.1

1978 4.4 3.3 25.2 5.6 3.7 2.9 1.3 2.0

Punjab & TamilM.P. Maharashtra Orissa Harayana Rajasthan Nadu U.P. W.B. Total

1963 23.7 2.0 21.4 2.8 0.2 8.3 0.2 19.4 100.0

1964 23.5 2.6 19.2 2.6 0.2 9.1 0.7 17.4 100.0

1965 23.9 2.7 17.4 2.4 0.2 9.3 1.8 16.2 100.0

1966 23.3 3.1 15.2 2.0 0.2 9.1 2.6 17.2 100.01967 21.8 3.2 14.3 1.8 0.3 9.3 3.5 17.7 100.0

1968 19.6 3.5 14.8 1.5 0.7 8.9 4.8 15.3 100.0

1969 18.2 3.4 14.2 1.3 0.9 8.8 4.6 13.8 100.0

1970 16.5 3.6 13.4 1.2 1.0 9.2 4.6 13.5 100.0

1971 15.5 3.5 12.6 1.1 1.1 8.8 4.3 12.7 100.0

1972 14.8 3.6 11.7 1.1 1.4 8.4 4.2 12.6 100.()1973 14.0 3.9 11.0 1.0 1.8 7.5 4.0 12.5 100.0

1974 13.8 3.9 10.1 1.0 2.2 6.9 4.1 12.3 100.0

1975 13.4 4.9 9.3 1.6 2.6 6.2 4.1 12.6 100.01976 18.2 5.0 8.3 2.9 2.5 6.7 4.1 7.6 100.01977 16.2 6.8 7.0 3.7 2.5 5.1 4.1 8.3 100.01978 16.1 8.1 5.9 3.3 2.5 5.1 4.4 9.5 100.0

Source: Bureau of Public Enterprises, Annual Report on theWorkinz of Industrial and Commercial Undertakingsof the Central Government- various issues.

-25-

Table 12

Share of States in Annual Investment inCentral Public Undertakings (%)

A.P. Assam Bihar Gujarat Karnataka Kerala Harayana Punjab

1964 2.1 3.1 21.6 0.3 2.8 7.91965 3.7 3.5 22.2 0 0.8 3.11966 7.5 -1.9 12.9 8.7 2.2 3.21967 8.1 0.9 18.6 1.6 2.9 4.31968 2.5 4.7 20.6 9.4 1.7 4.21969 2.9 3.0 44.1 2.6 2.6 9.5 0 01970 2.8 2.7 39.6 2.6 2.6 3.7 0 0.31971 4.4 1.1 42.8 16.3 3.0 2.8 0.2 0.21972 3.5 12.6 35.4 5.3 3.3 2.9 0.1 0.21973 6.1 4.0 34.3 7.7 3.6 2.3 0.2 0.31974 6.9 1.3 35.2 5.1 4.5 3.9 0.3 0.91975 6.9 4.3 21.3 5.4 2.8 3.0 0.9 3.71976 3.3 5.8 16.8 10.5 2.0 3.6 2.6 7.01977 4.6 2.4 36.0 5.2 3.2 1.6 5.2 1.91978 5.1 3.0 15.9 5.4 7.6 2.7 0.1 1.4

Punjab & TamilM.P. Maharashtra Orissa Harayana Rajasthan Nadu U.P. W.B. Total

1964 22.4 5.3 8.8 1.7 0.1 13.0 3.3 7.5 100.01965 26.0 3.1 8.0 1.1 0 5 10.4 7.2 10.1 100.01966 19.9 5.7 3.1 0.1 0.2 8.1 7.1 23.1 100.01967 9.4 3.2 6.6 0.1 1.1 10.4 11.1 21.7 100.01968 10.4 5.0 17.0 0.1 2.1 7.5 10.0 4.8 100.01969 7.3 2.4 9.3 0 2.9 7.7 3.3 2.4 100.01970 3.4 4.9 7.6 0.3 1.6 12.7 4.3 12.0 100.01971 6.5 3.0 5.0 0.4 2.1 5.0 2.2 5.4 100.01972 7.8 4.1 2.8 0.3 4.0 3.7 2.8 11.6 100.01973 8.3 6.1 6.4 0.5 4.5 1.5 2.3 12.2 100.01974 12.3 3.8 2.0 1.2 5.6 2.2 5.4 10.7 100.01975 11.3 10.7 4.9 4.6 4.7 2.0 4.1 14.1 100.01976 42.1 5.2 3.4 9.6 2.2 9.1 3.9 -17.5 100.01977 7.3 14.9 1.5 7.1 2.3 -1.8 4.1 11.6 100.01978 15.6 14.5 0.4 1.5 2.6 5.0 5.7 15.1 100.0

Source: Bureau of Public Enterprises, op. cit.

-26-

TABLE 13

Correlation Coefficients Between State-Wise Per CapitalInvestment In

Central Public Undertakinms and Indicators of State Development

Per Capita Per Capita Aggregate

Cumulative Investment Investment durinR

1965 1970 1975 1950-65 1965-70 1970-77

State per capita incomes -0.44 -0.52 -0.50 -0.44 -0.56 -0.16

Share of Manufacturing in state GDP -0.01 * -0.1 0.01 -0.01 -0.01 -0.04

a/ Per Capita income, share of manufacturing in GDP and populationfigures used to compute the correlations are the averages ofthe end-points of the time period.

-27-

Clearly the availability of iron ore and coal was the major

reason for the location of the steel plants in these states. In this

context, it is interesting to find that during 1970-77, the correlation of

per capita investment in public undertakings with state per capita income

turns out to be extremely weak (though negative). Thus, it could be

hypothesized that once the steel plants had been constructed and the

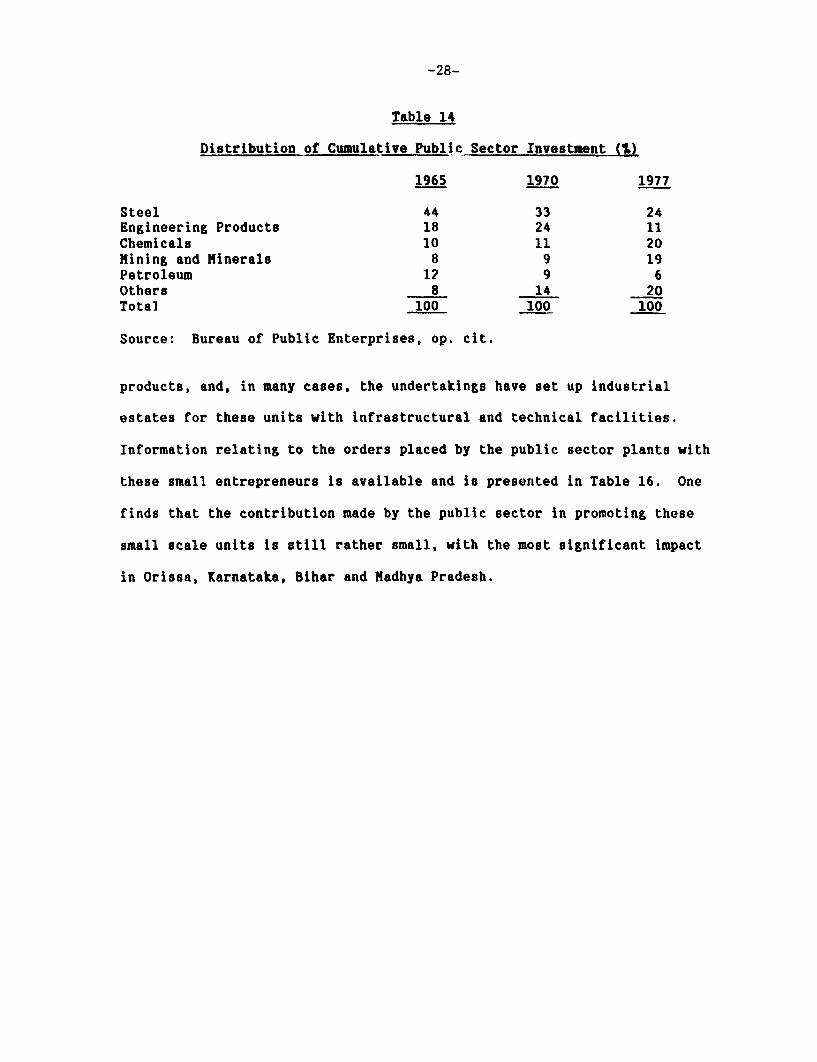

public sector started diversifying into other types of products (Table 14)

where the techno-economic advantages of different states were more

balanced, the link between investment and regional backwardness becomes

tenuous. This argument seems to be further buttressed by the low

correlations of public investment with the share of manufacturing in state

GDP. However, a more important explanation for this result is that the

operation of the public sector plants in the backward states has directly

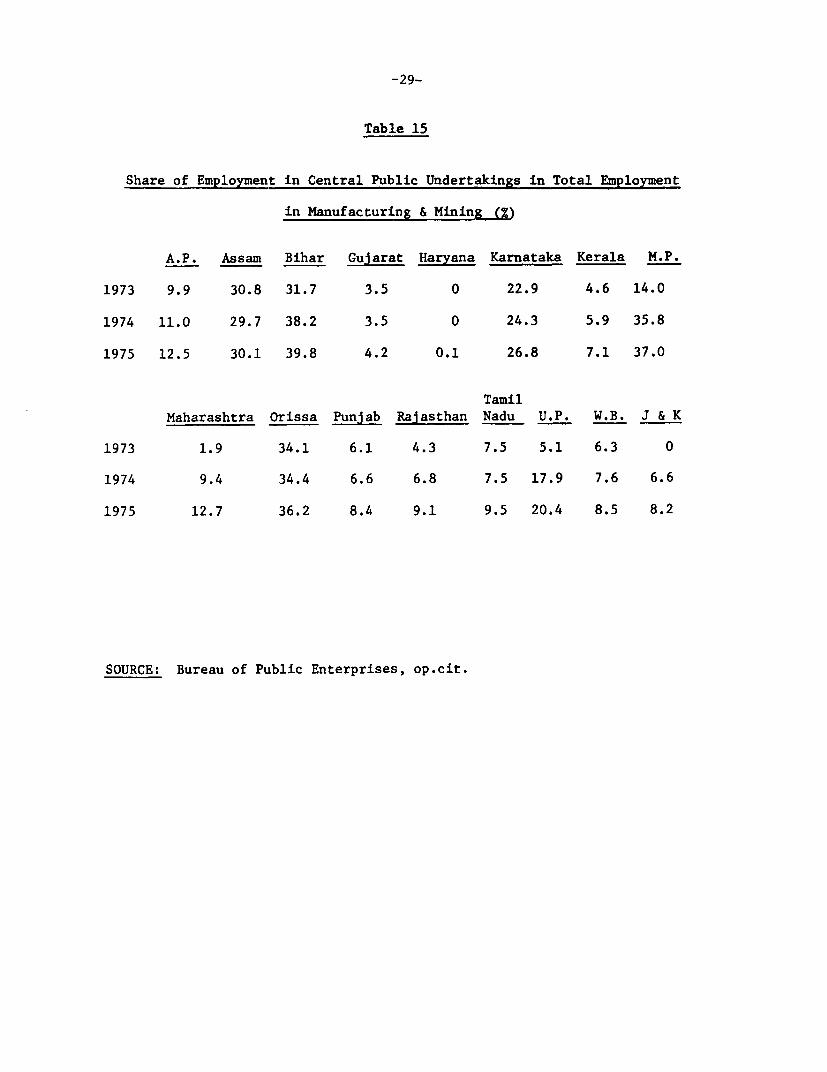

contributed to their industrial development. This is quite clear from

Table 15. One finds that in states like Assam, Bihar, Madhya Pradesh and

Orissa, employment in Central Public Undertakings constitutes more than

307 of total employment in the factory sectors.

Apart from the direct contribution of public enterprises to the

state economy through their production and employment, they also promote

industrial development through their backward (input demand) and forward

(supply of output) linkages with the other sectors. 1/ These are

difficult to measure with the exception of one type of linkage. Public

sector undertakings have made special attempts to develop small-scale

ancillary units to suplply various kind of components and sub-assembled

1/ Moreover, public sector units have invested significantly in townshipsfor their employeeis as a means of fulfilling broader social goals.The spatial implications of these townships have not been analyzedsince they fall somewhat outside the scope of our paper.

-28-

Table 14

Distribution of Cumulative Public Sector Investment (7)

1965 1970 1977

Steel 44 33 24Engineering Products 18 24 11Chemicals 10 11 20Mining and Minerals 8 9 19Petroleum 12 9 6Others 8 14 20Total 100 100 100

Source: Bureau of Public Enterprises, op. cit.

products, and, in many cases, the undertakings have set up industrial

estates for these units with infrastructural and technical facilities.

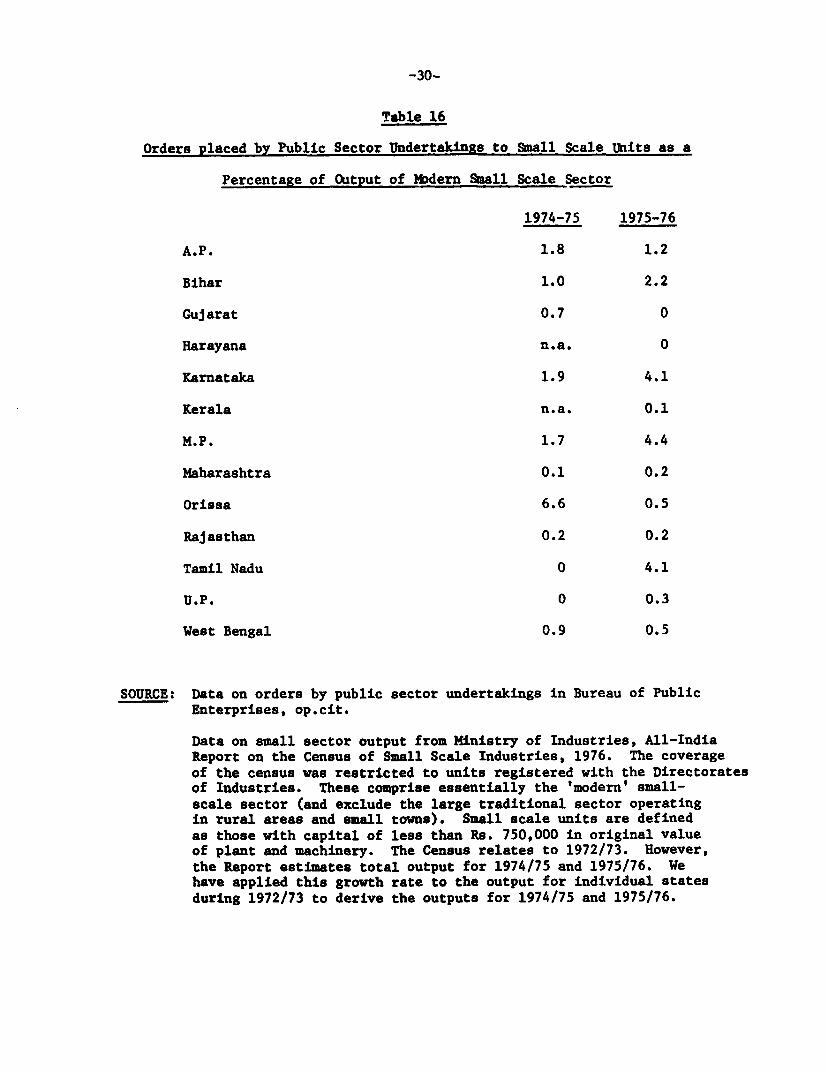

Information relating to the orders placed by the public sector plants with

these small entrepreneurs is available and is presented in Table 16. One

finds that the contribution made by the public sector in promoting these

small scale units is still rather small, with the most significant impact

in Orissa, Karnataka, Bihar and Madhya Pradesh.

-29-

Table 15

Share of Employment in Central Public Undertakings in Total Employment

in Manufacturing & Mining (%)

A.P. Assam Bihar Gujarat Haryana Karnataka Kerala M.P.

1973 9.9 30.8 31.7 3.5 0 22.9 4.6 14.0

1974 11.0 29.7 38.2 3.5 0 24.3 5.9 35.8

1975 12.5 30.1 39.8 4.2 0.1 26.8 7.1 37.0

TamilMaharashtra Orissa Punjab Rajasthan Nadu U.P. W.B. J & K

1973 1.9 34.1 6.1 4.3 7.5 5.1 6.3 0

1974 9.4 34.4 6.6 6.8 7.5 17.9 7.6 6.6

1975 12.7 36.2 8.4 9.1 9.5 20.4 8.5 8.2

SOURCE: Bureau of Public Enterprises, op.cit.

-30-

Table 16

Orders placed by Public Sector Undertakings to Small Scale Units as a

Percentage of Output of Mbdern Small Scale Sector

1974-75 1975-76

A.P. 1.8 1.2

Bihar 1.0 2.2

Gujarat 0.7 0

Harayana n.a. 0

Karnataka 1.9 4.1

Kerala n.a. 0.1

M.P. 1.7 4.4

Maharashtra 0.1 0.2

Orissa 6.6 0.5

Rajasthan 0.2 0.2

Tamil Nadu 0 4.1

U.P. 0 0.3

West Bengal 0.9 0.5

SOURCE: Data on orders by public sector undertakings in Bureau of PublicEnterprises, op.cit.

Data on small sector output from Ministry of Industries, All-IndiaReport on the Census of Small Scale Industries, 1976. The coverageof the census was restricted to units registered with the Directoratesof Industries. These comprise essentially the 'modern' small-scale sector (and exclude the large traditional sector operatingin rural areas and small towns). Small scale units are definedas those with capital of less than Rs. 750,000 in original valueof plant and machinery. The Census relates to 1972/73. However,the Report estimates total output for 1974/75 and 1975/76. Wehave applied this growth rate to the output for individual statesduring 1972/73 to derive the outputs for 1974/75 and 1975/76.

-31-

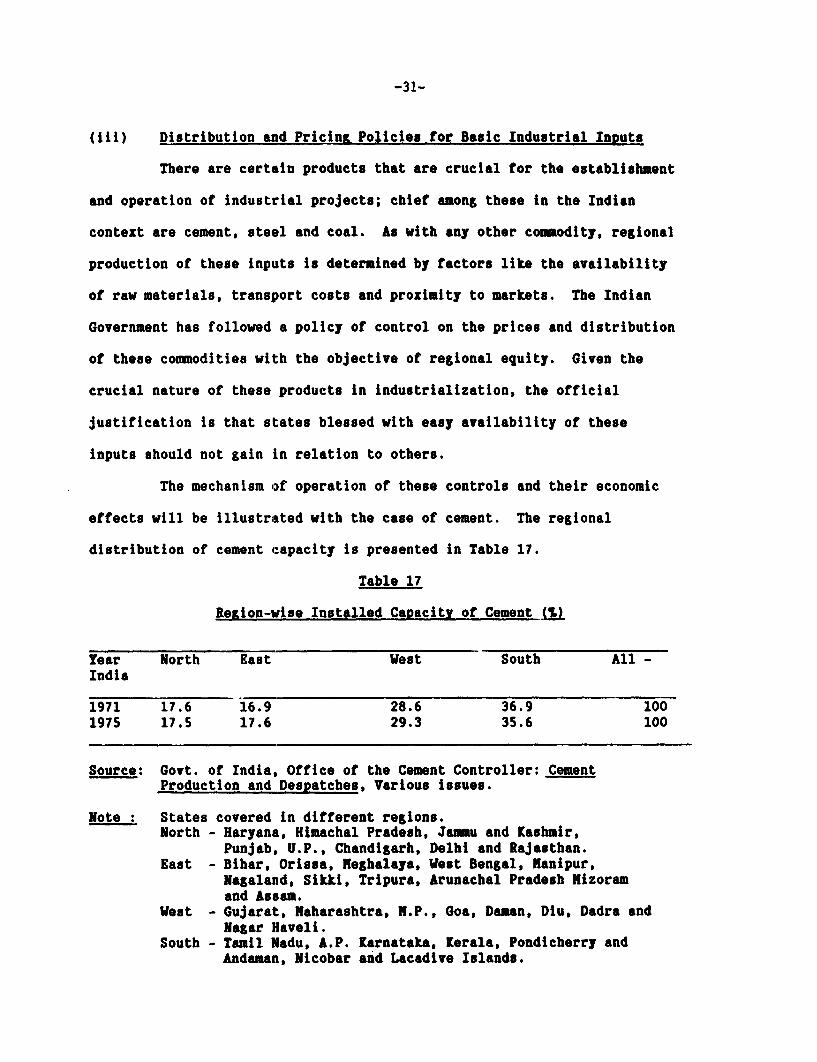

(iii) Distribution and Pricinz Policies for Basic Industrial Inouts

There are certain products that are crucial for the establishment

and operation of industrial projects; chief among these in the Indian

context are cement, steel and coal. As with any other comodity, regional

production of these inputs is determined by factors like the availability

of raw materials, transport costs and proximity to markets. The Indian

Government has followed a policy of control on the prices and distribution

of these cozmodities with the objective of regional equity. Given the

crucial nature of these products in industrialization, the official

justification is that states blessed with easy availability of these

inputs should not gain in relation to others.

The mechanism Of operation of these controls and their economic

effects will be illustrated with the case of cement. The regional

distribution of cement capacity is presented in Table 17.

Table 17

Region-wise Installed Capacity of Cement jfl

Year North East West South All -India

1971 17.6 16.9 28.6 36.9 1001975 17.5 17.6 29.3 35.6 100

Source: Govt. of India, Office of the Cement Controller: CementProduction and Despatches, Various issues.

Note : States covered in different regions.North - Haryana, Himachal Pradesh, Jaiu and Kashmir,

Punjab, U.P., Chandigarh, Delhi and Rajasthan.East - Bihar, Orissa, Meghalaya, West Bengal, Manipur,

Nagaland, Sikki, Tripura, Arunachal Pradesh Mizoramand Assam.

West - Gujarat, Kaharashtra, M.P., Goa, Daman, Diu, Dadra andNagar Haveli.

South - Tamil Nadu, A.P. Karnataka, Kerala, Pondicherry andAndaman, Nicobar and Lacadive Islands.

-32-

Production of cement is concentrated in the Western and Southern

regions which accounted for almost two-thirds of cement capacity in 1971

and 1976. Furthermore, within these regions, there is considerable

variation in production by individual states. The price control exercised

by the Government to balance these regional variations takes the following

shape. In the first instance, the Government fixes the 'retention price'

- the price payable to the manufacturer. Second, through suitable

subsidies, railway freight charges for the transportation of cement to all

destinations are kept the same. Thus, the F.O.R. (free on rail) price of

cement is uniform in all parts of the country. However, the actual retail

prices vary according to the incidence of state taxes.

These prices and distribution controls have resulted in various

kinds of distortions of the market mechanism and led to certain

irrationalities in the industrial location process. The most important

effects are explored below. .

First, the "freight-pooling" arrangement has obvious implications

for the location of cement plants. Since transportation charges to

markets are the same irrespective of distance, entrepreneurs will locate

their plants in accordance with raw material availability - the major ones

being limestone, gypsum and coal. As a corollary, these controls lead to

the disappearance of natural protection in the form of transportation

charges that would have led to some development of cement capacity in

states less well-endowed with these raw materials.

Second, freight-pooling was introduced in 1966. Thus, cement

units set up earlier in proximity to markets have found themselves at a

disadvantage vis-a-vis new units.

-33-

Third, there is less of an incentive for the utilization of

substitutes for cement in "deficit" states. For instance, in the North

Eastern Region, states like Kashmir and other areas with plentiful timber

resources, the utilization of these is sub-optimal because of the

artificial lowering of cement prices.

Fourth, there is8 an excessive use of railway transport especially

to distant consuming areas. This is particularly important in the context

of frequent bottlonecks in transport that have affected Indian industrial

growth.

Fifth, a fiscal burden is imposed on the Government to the extent

that a subsidy has to be provided to support this freight equalization

mechanism.

Finally, the transportation subsidy reduces the scope for "split

location" of clinker and grinding plants, i.e. setting up of clinker

plants near raw materials and grinding plants at consuming centers. A

major advantage of this division is saving in transportation costs

(because of reductions in tonnage that needs to be transported) and

convenience in transportstion (clinker can be dispatched in bulk in open

wagons). Because of the subsidy on transport, these advantages are not

enough to outweigh the additional expenses involved in setting up grinding

facilities in consuming areas.

There has been it persistent shortage of cement in India despite

the ready availability of' essential raw materials. There is little doubt

that price and distribution controls are important reasons for this

phenomenon. Cement produc:ers have resented the "unremunerative" prices

-34-

fixed by the Government. 1/ Besides this, irrationalities in the location

of production and utilization of cement resulting from these controls have

also played their part.

It is not easy to assess the precise locational impact of the

freight equalization schemes without a detailed study of the regional

distribution of raw materials, markets and other factors influencing the

industrial location process and the policy changes and their linkage in

a general equilibrium context. It is obvious that, in the case of

cement, the concentration of capacity in the Southern and Western Regions

implies that freight equalization has benefited the Northern and Eastern

Regions. 2/ On the other hand, for steel and coal, the Eastern Region

which dominates in production has lost vis-a-vis the rest of India. A

careful analysis of these policies is urgently called for to eliminate

some of the resulting irrationalities and to gauge the extent of

efficiency loss in relation to the gains in regional equity.

1/ Recently, in February 1982, the Government introduced a policy ofpartial decontrol of the cement industry whereby units could sellcement output in excess of two-thirds of their capacity at free marketprices. In the short while that this policy has been in force,available information indicates that there has been a dramaticimprovement in the supply situation of cement. Moreover, a number ofcompanies have started diversifying into the production of cement inresponse to the increased profitability of this industry.

2/ For a detailed analysis, see National Council of Applied EconomicResearch. Cement Industry in India, 1979, New Delhi.

-35-

(iv) State Government Incentives

A variety of ilncentives are offered by individual states to

attract entrepreneurs to establish industries within their borders. There

are also state-level financial institutions and industrial development

agencies whose major taisk is the provision of industrial finance and

promotion of industry. The major incentives fall into three broad

categories: 1/

a. Reduction in capital cost and infrastructural expenditure

Provision of financial assistance (both in the form of loans and

equity); infrastructural facilities and availability of plots and sheds in

industrial estates; assistance in acquisition of land; and assistance in

the preparation of feasibility reports.

b. Incentives related to the prices and availability of inputs

Reductions in power tariffs and electricity duties; financial

assistance to units for setting up power generating sets; reduced water

rates; and assistance in the procurement of controlled raw materials.

c. Tax incentives

Concessions (on loans) for payment of sales taxes, octroi stamp

duties and property taxes.

These three types of incentives exist in almost every state.

However, the precise content of each incentive varies from state to

state. It would be interesting to determine the extent to which these

differences have influenced the decisions of entrepreneurs In plant

location. Unfortunately, there has been no research study of this nature

essentially because of the paucity of detailed information required for a

rigorous analysis. For example, one needs state-level data relating to

1/ The magnitude of the incentives are often increased further for smallscale units or units set up in "backward" districts.

-36-

land rents, location of estates, power tariffs, water rates, tax levels etc.

The task is also complicated by the fact that these incentives keep changing

over time for every state. A priori, it can be argued that if the Governments

of individual states were serious enough about industrialization within their

boundaries, they would not allow the overall attractiveness of their

incentives to fall much below those offered by other states. However,

"rationality" cannot always be taken for granted in Governmental decision

making. Moreover, there are other objective factors which influence the

offering of incentives - the budgetary position, for instance. Finally, it is

not merely the announcement of incentives but the actual effectiveness with

which they are implemented that will influence industrial location. Here

again, there is little doubt that the efficiency of the implementing agences

varies across states.

Finally, there is the similarity between state incentives and the

phenomenon of different developing countries competing with each other to

attract foreign investment. The advantages that are derived from

inter-country co-operation in this analogy may be of some relevance.

Otherwise, there is the danger that unhealthy competition between the state

Governments will unnecessarily drain state budgetary resources (in the form of

transfers to the private sector) with no net gain from a national viewpoint.

2. Policies Influencing the Intra-Regional Distribution of Industry

Having looked at the locational policies aimed at a more equitable

inter-state distribution of industry, we now turn our attention to those

affecting intra-regional industrial growth. Chronologically arranged in the

order of their implementation, these consist of:

(i) policies for encouraging (a) village and cottage industries and

(b) modern small scale enterprises;

-37-

(ii) the indusltrial estates program;

(iii) The Rural Industries Project Program;

(iv) metropolitan planning in the major cities;

(v) incentives to promote industrial development in backward

districts: (a) Central Government incentives, (b) Concessional

finance from all-India financial institutions and (c) State

Government incentives. 1/

(i) Policies to Encourage the Small Scale Sector

A major aspect of Indian industrial policy has been its emphasis on

encouraging the small scale sector. The reasons for this are summed up in the

following quote from the Industrial Policy Resolution of 1956:

'They (village and small scale enterprises) provide immediate large

scale employment, they offer a method of ensuring a more equitable

distribution of national income and they facilitate an effective mobilization

of resources of capital and skill which might otherwise remain unutilized.

Some of the problems that unplanned urbanization tends to create will be

avoided by the establishmaent of small centers of industrial production all

over the country.'

Thus, the desire to promote a decentralized form of development is

quite central in the rationale for supporting the small scale sector.

The small scale sector can conceptually be broken up into two

categories - the traditional village and cottage industries operating in the

rural and semi-urban areas and modern small scale enterprises. It is

extremely difficult to draw a precise dividing line between the small scale

sector and the rest of the manufacturing sector. The Government uses capital

investment as the criterion for defining the modern small sector. The precise

1/ We have described State Government incentives in an earlier section

-38-

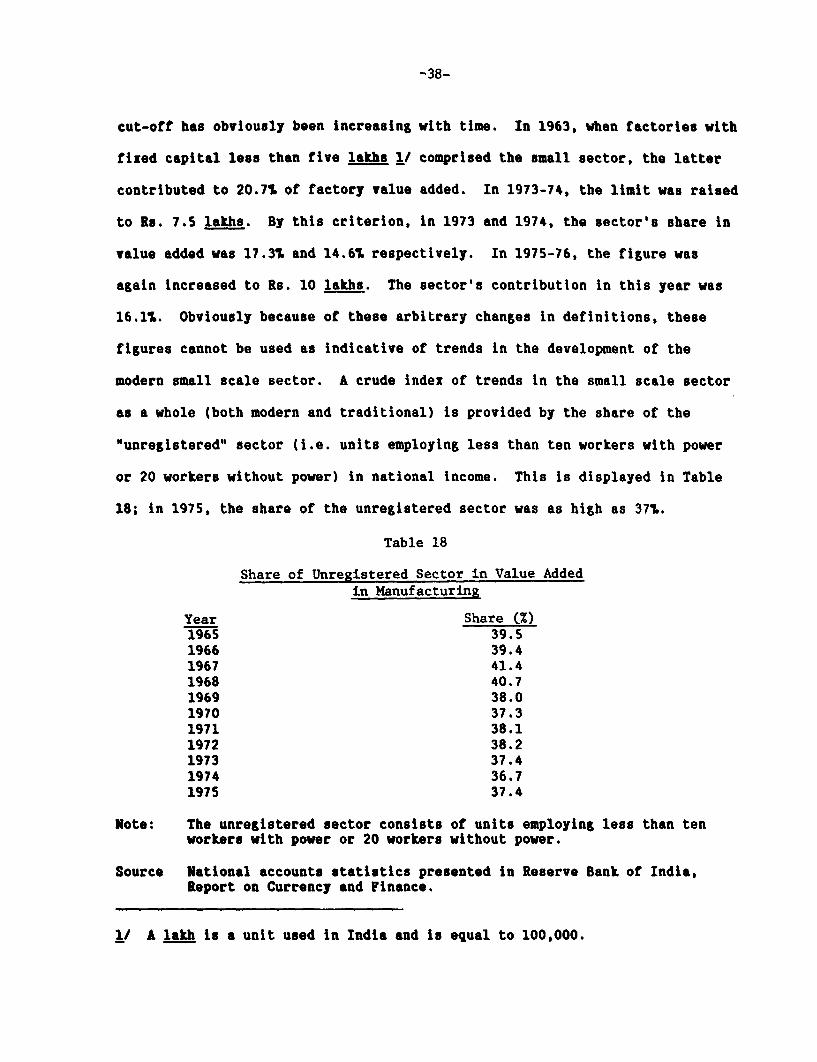

cut-ott has obviously been increasing with time. In 1963, when factories with

fixed capital less than five lakhs V/ comprised the small sector, the latter

contributed to 20.77 of factory value added. In 1973-74, the limit was raised

to Re. 7.5 lakhs. By this criterion, in 1973 and 1974, the sector's share in

value added was 17.37 and 14.67 respectively. In 1975-76, the figure was

again increased to Rs. 10 lakhs. The sector's contribution in this year was

16.17. Obviously because of these arbitrary changes in definitions, these

figures cannot be used as indicative of trends in the development of the

modern small scale sector. A crude index of trends in the small scale sector

as a whole (both modern and traditional) is provided by the share of the

"unregistered" sector (i.e. units employing less than ten workers with power

or 20 workers without power) in national income. This is displayed in Table

18; in 1975, the share of the unregistered sector was as high as 37t.

Table 18

Share of Unregistered Sector in Value Addedin Manufacturing

Year Share (%)1965 39.51966 39.41967 41.41968 40.71969 38.01970 37.31971 38.11972 38.21973 37.41974 36.71975 37.4

Note: The unregistered sector consists of units employing less than tenworkers with power or 20 workers without power.

Source National accounts statistics presented in Reserve Bank of India,Report on Currency and Finance.

I/ A lakh is a unit used in India and is equal to 100,000.

TABLE 19

Employment and Output in Modern Small Scale Sector, 1972

EMPLOYMENT GROSS OUTPUTRatio of Ratio of

Number Percentage small scale sector Value Percentage small scale sector to(000s) distribution to factory sector(%) (Rs.crs)-/distribution factory sector(%)

Food Products 131.2 7.9 1.9 152.3 5.9 4.5Beverages 4.6 0.3 2.3 7.4 0.3 1.4Hosiery & Readymade

garments 75.3 4.6 393.8 155.4 6.0 322.0Wood Products 94.7 5.7 125.5 102.6 3.9 81.9Paper Products,Printing, etc. 89.1 5.4 35.5 126.4 4.9 20.9

Leather Products 31.8 1.9 71.3 88.6 3.4 49.2Rubber & Plastic

Prods. 81.7 4.9 87.7 151.2 5.8 62.5Chemicals 159.0 9.6 49.5 346.7 13.3 15.1Glass & Ceramics 202.3 12.2 250.4 125.5 4.8 106.6Basic Metal Indus. 109.6 6.6 24.0 294.1 11.3 14.4Metal Products 300.1 18.2 170.8 469.1 18.0 87.9Machinery & parts 145.3 8.8 44.8 211.0 8.1 20.3Electrical &

Electronic Prods. 65.9 4.0 26.1 151.7 5.8 13.6Transport equip. 83.5 5.1 21.3 134.8 5.2 12.0Miscellaneous 40.0 2.4 - 62.7 2.4 -Repairing, servicing& job work 39.0 2.4 26.3 23.3 0.9 9.8

TOTAL 1653.2 100.0 31.3 2602.7 100.0 14.1

2/ Crore is a unit used in India and is equal to ten million.

SOURCE: Computed from Development Commissioner, Small Scale Industries (Ministry of Industry & Civil Supplies),All-India Report on the Census of Small Scale Industries (1976).

-40-

In sharp contrast to the concentration of traditional enterprises in

simple consumer goods production, modern small scale units are engaged in

manufacturing a wide variety of commodities (Table 19). In fact, basic

metals, metal products, machinery and transport equipment are the most

important activities, together accounting for 437 of employment and 487 of

gross output in this sector.

Despite the problems of definition, there is no doubt about the

critical importance of trends in the small sector in an analysis of Indian

industrial development. Within the small scale sector, it is the traditional

industries that dominate. Because of the labor-intensive character of

production in traditional enterprises, their share in employment is striking.

The 1971 census estimated that as much as 77.4* of the labor force in the

manufacturing sector was employed in household units. The most important

activities in traditional enterprises are textiles and textile products; in

1971, almost one-third of household workers were engaged in this activity.

Another indication of the significance of these industries is the estimate

that, in 1976, about 50* of total cloth output in the country was produced by

the decentralized sector, i.e., the non-mill sector where the utilization of

handlooms is quite common. Apart from textiles, other major household

industries are agro-processing (like the processing of cereals and pulses,

&ur 1/ and khandsari 1/), carpentry and blacksmiths, coir and coir products,

sericulture and handicrafts.

The Indian Constitution assigns major responsibility for development

of small scale industries to the State Governments. However, the Government