INDUSTRIAL AND COMMERCIAL BANK OF CHINA LIMITED

656

IMPORTANT: If you are in any doubt about any of the contents of this prospectus, you should obtain independent professional advice. INDUSTRIAL AND COMMERCIAL BANK OF CHINA LIMITED (a joint stock limited company incorporated in the People’s Republic of China with limited liability) GLOBAL OFFERING Number of Offer Shares under the Global Offering: 35,391,000,000 H shares (subject to adjustment and over- allotment option) Number of Hong Kong Offer Shares: 1,769,550,000 H shares (subject to adjustment) Number of International Offer Shares: 33,621,450,000 H shares (subject to adjustment and over- allotment option) Maximum offer price: HK$3.07 per H share (payable in full on application, plus brokerage of 1%, SFC transaction levy of 0.005% and Hong Kong Stock Exchange trading fee of 0.005% and subject to refund) Nominal value: RMB1.00 each Stock code: 1398 Joint Global Coordinators China International Capital Corporation Limited ICEA Capital Limited Merrill Lynch & Co. Joint Bookrunners Merrill Lynch & Co. China International Capital Corporation Limited Credit Suisse (Hong Kong) Limited Deutsche Bank AG, Hong Kong Branch ICEA Capital Limited Joint Sponsors China International Capital Corporation (Hong Kong) Limited ICEA Capital Limited Merrill Lynch Far East Limited The Stock Exchange of Hong Kong Limited and Hong Kong Securities Clearing Company Limited (“HKSCC”) take no responsibility for the contents of this prospectus, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this prospectus. A copy of this prospectus, having attached thereto the documents specified in “Appendix X—Documents Delivered to the Registrar of Companies and Available for Inspection,” has been registered by the Registrar of Companies in Hong Kong as required by Section 342C of the Hong Kong Companies Ordinance (Chapter 32 of the Laws of Hong Kong). The Securities and Futures Commission and the Registrar of Companies in Hong Kong take no responsibility for the contents of this prospectus or any other document referred to above. The offer price is expected to be fixed by agreement between the Joint Bookrunners (on behalf of the underwriters) and us (for ourselves and on behalf of the Selling Shareholders) on the price determination date which is expected to be on or before October 20, 2006 and, in any event, not later than October 25, 2006. The offer price will be not more than HK$3.07 and is currently expected to be not less than HK$2.56. The underwriters may, with our consent, reduce the number of Hong Kong Offer Shares and/or the indicative offer price range below that stated in this prospectus at any time prior to the morning of the last day for lodging applications under the Hong Kong Public Offering. Further details are set forth in the sections headed “Structure of the Global Offering” and “How to Apply for Hong Kong Offer Shares.” We are incorporated, and substantially all of our businesses are located, in China. Potential investors should be aware of the differences in the legal, economic, and financial systems between China and Hong Kong, and that there are different risk factors relating to investment in companies incorporated in China. Potential investors should also be aware that the regulatory framework in China is different from the regulatory framework in Hong Kong, and should take into consideration the different market nature of our H shares. Such differences and risk factors are set forth in the sections headed “Risk Factors” and “Appendix VII—Summary of Principal Legal and Regulatory Provisions” and “Appendix VIII—Summary of Articles of Association.” October 16, 2006 Global Reports LLC

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of INDUSTRIAL AND COMMERCIAL BANK OF CHINA LIMITED

IMPORTANT: If you are in any doubt about any of the contents of this prospectus, you should obtainindependent professional advice.

INDUSTRIAL AND COMMERCIAL BANK OF CHINA LIMITED(a joint stock limited company incorporated in the People’s Republic of China with limited liability)

GLOBAL OFFERING

Number of Offer Shares under the Global Offering: 35,391,000,000 H shares (subject to adjustment and over-allotment option)

Number of Hong Kong Offer Shares: 1,769,550,000 H shares (subject to adjustment)Number of International Offer Shares: 33,621,450,000 H shares (subject to adjustment and over-

allotment option)Maximum offer price: HK$3.07 per H share (payable in full on application, plus

brokerage of 1%, SFC transaction levy of 0.005% andHong Kong Stock Exchange trading fee of 0.005% andsubject to refund)

Nominal value: RMB1.00 eachStock code: 1398

Joint Global Coordinators

China International CapitalCorporation Limited

ICEA Capital Limited Merrill Lynch & Co.

Joint Bookrunners

Merrill Lynch & Co. China InternationalCapital Corporation

Limited

Credit Suisse(Hong Kong) Limited

Deutsche Bank AG,Hong Kong Branch

ICEA CapitalLimited

Joint Sponsors

China International CapitalCorporation (Hong Kong) Limited

ICEA Capital Limited Merrill Lynch Far East Limited

The Stock Exchange of Hong Kong Limited and Hong Kong Securities Clearing Company Limited (“HKSCC”) take no responsibility for thecontents of this prospectus, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any losshowsoever arising from or in reliance upon the whole or any part of the contents of this prospectus.

A copy of this prospectus, having attached thereto the documents specified in “Appendix X—Documents Delivered to the Registrar of Companiesand Available for Inspection,” has been registered by the Registrar of Companies in Hong Kong as required by Section 342C of the Hong KongCompanies Ordinance (Chapter 32 of the Laws of Hong Kong). The Securities and Futures Commission and the Registrar of Companies in HongKong take no responsibility for the contents of this prospectus or any other document referred to above.

The offer price is expected to be fixed by agreement between the Joint Bookrunners (on behalf of the underwriters) and us (for ourselves and onbehalf of the Selling Shareholders) on the price determination date which is expected to be on or before October 20, 2006 and, in any event, not laterthan October 25, 2006. The offer price will be not more than HK$3.07 and is currently expected to be not less than HK$2.56.

The underwriters may, with our consent, reduce the number of Hong Kong Offer Shares and/or the indicative offer price range below that stated inthis prospectus at any time prior to the morning of the last day for lodging applications under the Hong Kong Public Offering. Further details are setforth in the sections headed “Structure of the Global Offering” and “How to Apply for Hong Kong Offer Shares.”

We are incorporated, and substantially all of our businesses are located, in China. Potential investors should be aware of the differences in the legal,economic, and financial systems between China and Hong Kong, and that there are different risk factors relating to investment in companiesincorporated in China. Potential investors should also be aware that the regulatory framework in China is different from the regulatory framework inHong Kong, and should take into consideration the different market nature of our H shares. Such differences and risk factors are set forth in thesections headed “Risk Factors” and “Appendix VII—Summary of Principal Legal and Regulatory Provisions” and “Appendix VIII—Summary ofArticles of Association.”

October 16, 2006

Global Reports LLC

EXPECTED TIMETABLE(1)

Latest time to lodge white and yellow application forms . . . . . . . . . 12:00 noon on Thursday, October 19, 2006

Latest time to complete electronic applications under the WhiteForm eIPO service through the designated websitewww.eipo.com.hk(2) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12:00 noon on Thursday, October 19, 2006

Latest time to give electronic application instructions toHKSCC(3) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12:00 noon on Thursday, October 19, 2006

Application lists open(4) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11:45 a.m. on Thursday, October 19, 2006

Application lists close . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12:00 noon on Thursday, October 19, 2006

Expected price determination date . . . . . . . . . . . . . . . . . . . . . . . . . . . Friday, October 20, 2006

Announcement of the offer price for H shares under the GlobalOffering and the offer price for A shares under the A ShareOffering expected to be published in South China Morning Post(in English) and Hong Kong Economic Times (in Chinese) . . . . . Monday, October 23, 2006

Announcement of

Š the level of applications in the Hong Kong PublicOffering;

Š the level of indications of interest in the InternationalOffering; and

Š the basis of allotment of the Hong Kong Offer Shares

to be published in South China Morning Post (in English) andHong Kong Economic Times (in Chinese) . . . . . . . . . . . . . . . . . . Thursday, October 26, 2006

Results of allocations in the Hong Kong Public Offering (withsuccessful applicants’ identification document numbers, whereappropriate) to be available through a variety of channels (see“How To Apply For Hong Kong Offer Shares—10. Results ofAllocations”) from . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Thursday, October 26, 2006

Despatch of H share certificates(5) on or before . . . . . . . . . . . . . . . . . Thursday, October 26, 2006

Despatch of refund cheques on or before . . . . . . . . . . . . . . . . . . . . . . Friday, October 27, 2006

Dealings in H shares on the Hong Kong Stock Exchange expectedto commence on . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Friday, October 27, 2006

(1) All times refer to Hong Kong local time.(2) You will not be permitted to submit your application to the eIPO Service Provider through the designated website www.eipo.com.hk

after 11:30 a.m. on the last day for submitting applications. If you have already submitted your application and obtained a paymentreference number from the designated website prior to 11:30 a.m., you will be permitted to continue the application process (bycompleting payment of application monies) until 12:00 noon on the last day for submitting applications, when the application lists close.

(3) Applicants who apply for Hong Kong Offer Shares by giving electronic application instructions to HKSCC should refer to the sectionheaded “How to Apply for Hong Kong Offer Shares—6. Applying by giving electronic application instructions to HKSCC.”

(4) If there is a tropical cyclone warning signal number 8 or above, or a “black” rainstorm warning on Thursday, October 19, 2006, theapplication lists will not open on that day. See “How to Apply for Hong Kong Offer Shares—7. When may applications be made—(e) Effects of bad weather conditions on the opening of the application lists.”

(5) H share certificates will only become valid certificates of title if the Hong Kong Public Offering has become unconditional andneither of the underwriting agreements has been terminated in accordance with its terms, which will be at 8:00 a.m. on Friday,October 27, 2006. Investors who trade H shares on the basis of publicly available allocation details prior to the receipt of sharecertificates or prior to the share certificates becoming valid certificates of title do so entirely at their own risk.

For details of the structure of the Global Offering, including its conditions, see the sectionheaded “Structure of the Global Offering.”

i

Global Reports LLC

CONTENTS

IMPORTANT NOTICE TO INVESTORS

This prospectus is issued by Industrial and Commercial Bank of China Limited solely inconnection with the Hong Kong Public Offering and the Hong Kong Offer Shares and does notconstitute an offer to sell or a solicitation of an offer to buy any security other than the HongKong Offer Shares offered by this prospectus pursuant to the Hong Kong Public Offering. Thisprospectus may not be used for the purpose of, and does not constitute, an offer or invitation inany other jurisdiction or in any other circumstances. No action has been taken to permit apublic offering of the Offer Shares in any jurisdiction other than Hong Kong and Japan and noaction has been taken to permit the distribution of this prospectus in any jurisdiction other thanHong Kong. The distribution of this prospectus and the offering and sale of the Offer Shares inother jurisdictions are subject to restrictions and may not be made except as permitted underthe applicable securities laws of such jurisdictions pursuant to registration with orauthorization by the relevant securities regulatory authorities or an exemption therefrom.

You should rely only on the information contained in this prospectus and the applicationforms to make your investment decision. We have not authorized anyone to provide you withinformation that is different from what is contained in this prospectus. Any information orrepresentation not made in this prospectus must not be relied on by you as having beenauthorized by us, the Selling Shareholders, the Joint Global Coordinators, the Joint Bookrunners,the Joint Sponsors, the underwriters, the financial advisor, any of their respective directors orany other person or party involved in the Global Offering.

Page

Expected Timetable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . i

Contents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ii

Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Definitions and Conventions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Forward-looking Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Risk Factors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

Information about this Prospectus and the Global Offering . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

Parties Involved in the Global Offering . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41

Corporate Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

Banking Industry in China . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

Regulation and Supervision . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57

Our Restructuring and Operational Reform . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 82

Our Strategic Investors and Other Investors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 88

Business . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 102Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 102Our Competitive Strengths . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 103Our Strategy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 107Our Principal Business Activities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 111Product Pricing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 123Distribution Channels . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 124

ii

Global Reports LLC

CONTENTS

Page

Information Technology . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 126Competition . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 127Employees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 128Intellectual Property . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 130Properties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 130Legal and Regulatory . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 132

Risk Management . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 136

Relationship with Our Promoters and Connected Transactions . . . . . . . . . . . . . . . . . . . . . . . 156

Directors, Supervisors and Senior Management . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 168

Substantial Shareholders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 186

Share Capital . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 189

Assets and Liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 195Assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 195Liabilities and Sources of Funds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 235

Financial Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 239Financial Impact of Our Restructuring . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 239General Factors Affecting Our Results of Operations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 240Interim Results of Operations for the Six Months Ended June 30, 2006 and 2005 . . . . . . . . 241Results of Operations for the Years Ended December 31, 2005, 2004 and 2003 . . . . . . . . . . 260Summary Segment Operating Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 281Liquidity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 282Cash Flows . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 284Capital Resources . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 286Off-balance Sheet Commitments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 288Tabular Disclosure of Contractual Obligations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 288Quantitative and Qualitative Analysis of Market Risk . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 288Capital Expenditures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 291Critical Accounting Policies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 291Recent Accounting Pronouncements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 297Indebtedness . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 297Rules 13.11 to 13.19 of the Hong Kong Listing Rules . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 298Profit Forecast for the Year Ending December 31, 2006 . . . . . . . . . . . . . . . . . . . . . . . . . . . . 298Dividend Policy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 298Unaudited Pro Forma Adjusted Consolidated Net Tangible Assets . . . . . . . . . . . . . . . . . . . . 301No Material Adverse Change . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 302Working Capital . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 302

Future Plans and Use of Proceeds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 303

Underwriting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 304

Structure of the Global Offering . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 311

A Share Offering . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 317

How to Apply for Hong Kong Offer Shares . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 320

Further Terms and Conditions of the Hong Kong Public Offering . . . . . . . . . . . . . . . . . . . . . 334

Appendix I—Accountants’ Report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Appendix I-1

Appendix II—Unaudited Supplementary Financial Information . . . . . . . . . . . . . . . . . . . . . . Appendix II-1

Appendix III—Unaudited Pro Forma Financial Information . . . . . . . . . . . . . . . . . . . . . . . . . Appendix III-1

iii

Global Reports LLC

CONTENTS

Page

Appendix IV—Profit Forecast . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Appendix IV-1

Appendix V—Property Valuation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Appendix V-1

Appendix VI—Taxation and Foreign Exchange . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Appendix VI-1

Appendix VII—Summary of Principal Legal and Regulatory Provisions . . . . . . . . . . . . . . Appendix VII-1

Appendix VIII—Summary of Articles of Association . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Appendix VIII-1

Appendix IX—Statutory and General Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Appendix IX-1

Appendix X—Documents Delivered to the Registrar of Companies and Available forInspection . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Appendix X-1

iv

Global Reports LLC

SUMMARY

This summary aims to give you an overview of the information contained in thisprospectus. As this is a summary, it does not contain all the information that may be important toyou. You should read this prospectus in its entirety before you decide to invest in our shares.

There are risks associated with any investment. Some of the particular risks in investing inour shares are set out in the section headed “Risk Factors.” You should read that sectioncarefully before you decide to invest in our shares.

The market share and industry data in this prospectus were derived from data prepared inaccordance with PRC GAAP or other applicable local GAAP, which may differ from IFRS incertain significant respects.

OVERVIEW

We are the largest commercial bank in China in terms of total assets, loans and deposits. AtDecember 31, 2005, we had RMB6,456.1 billion (US$816.8 billion) in total assets, RMB3,289.6billion (US$416.2 billion) in total loans, RMB5,736.9 billion (US$725.8 billion) in total deposits, andour total operating income in 2005 was RMB171.6 billion (US$21.7 billion). Our assets, loans anddeposits represented 16.8%, 15.4% and 19.4% of the total assets, total loans and total deposits,respectively, of all banking institutions in China, and 31.4%, 30.4% and 32.6% of the total assets, totalloans and total deposits, respectively, of the Big Four commercial banks at December 31, 2005, basedon PRC GAAP statistical data published by the PBOC.

We primarily operate in China and provide an extensive range of commercial banking productsand services. According to the PBOC, we were:

Š the largest corporate bank in China in terms of outstanding corporate loans, discountedbills and corporate deposits at December 31, 2005;

Š the largest personal bank in China in terms of outstanding personal loans and personaldeposits at December 31, 2005; and

Š the leading service provider in credit card, quasi-credit card and debit card businesses inChina in terms of the aggregate transaction volume in 2005.

At June 30, 2006, we had more than 2.5 million corporate customers and more than 150 millionpersonal customers. We serve our customers through our traditional branch network, which, at June 30,2006, comprised 18,038 domestic branches, outlets and other establishments (including our headoffice), and through our electronic banking network, which, at June 30, 2006, comprised a range ofInternet and telephone banking services, 1,610 self-service banking centers and 19,026 ATMs.

We are headquartered in Beijing and, at June 30, 2006, had 98 overseas branches, subsidiaries,representative offices and outlets. We currently maintain branches in Hong Kong, Macau, Singapore,Tokyo, Seoul, Busan, Frankfurt and Luxembourg and representative offices in New York, Moscow andSydney. In addition, we have subsidiaries in Hong Kong, London and Almaty. ICBC (Asia), which iscontrolled by us, was the sixth largest Hong Kong-incorporated bank listed, or controlled by acompany that is listed, on the Hong Kong Stock Exchange in terms of total assets at December 31,2005.

1

Global Reports LLC

SUMMARY

We believe that “Industrial and Commercial Bank of China” ( ) is one of the mostrecognized financial services brands in China. We were named “Bank of the Year in 2004 (China)” byThe Banker, “Best Bank Award” for China in 2005 by Global Finance, “Best Bank in China” in 2004by EuroMoney, “Best Domestic Commercial Bank in China” in 2004 and 2005 by Asiamoney, “BestRetail Bank in China” in 2004 and 2005 and “Best Retail Bank (State-owned) in China” in 2006 byThe Asian Banker, “Best Consumer Internet Bank” in China in 2004, 2005 and 2006 by GlobalFinance, “Bank with Best Investment Management Services in Corporate Internet Banking” in AsiaPacific in 2006 by Global Finance, “Best Local Bank in China” in 2003 and 2004 by FinanceAsia,“Best Custodian Bank in China” in 2005 by The Asset, “Best Custodian Bank in China” in 2004 and2005 by Global Custodian, and “Best Sub-Custodian in China” in 2004 by Asiamoney. We receivedthe worldwide “Networking Initiative of the Year” award in 2006 from The Banker, the “Best BankingTechnology Development Award” in 2004 from the PBOC, the First Prize of “China Internet IndustrySurvey Report for Internet Banking” in 2005 from the Internet Society of China, the “Gold Award forCustomer Care and Public Service in China” in 2005 from the Ministry of Information Industry, “TheMost-Used Bank by Consumers in China” in 2003 from AC Nielsen and the title of “Best Finance,Economics and Securities Website in China” in 2005 from Securities Times.

Since 1999, we have implemented a series of reform measures that we believe havesignificantly transformed our business, operations and corporate culture. In particular, we have focusedon developing comprehensive risk management systems and rationalizing our business structure andorganization. Our business focus and structure have evolved to meet our customers’ demand for abroad range of banking products and services. We have focused on expanding our personal bankingoperations, particularly in high-growth fee- and commission-based segments, and we have establishedourselves as a leading electronic banking service provider. Through significant investments ininformation technology, we have established centralized information systems designed to enable us toanalyze the activities of our customer base, target attractive client segments and enhance our riskmanagement and other internal control capabilities. We believe that, as a result of our reforms, ourbusiness structure and processes, corporate governance practices and internal controls are among themost advanced of PRC commercial banks. Our financial restructuring in 2005 has significantlystrengthened our capital base, and we believe that we are currently well-positioned to pursue our nextphase of growth.

OUR COMPETITIVE STRENGTHS

Our principal competitive strengths include:

Š Largest PRC Commercial Bank with a Leading Market Position in Major BusinessSegments. We are the largest PRC commercial bank in terms of total loans and deposits. Inaddition, we have also established leading positions in numerous corporate banking,personal banking and treasury business lines.

Š Large High-Quality Corporate and Personal Banking Customer Base. We believe that wehave the largest corporate banking customer base in China with more than 2.5 millioncorporate banking customers, including approximately 57,710 borrowers at June 30, 2006.We have established banking relationships with many leading business conglomerates andcorporations, including 492 out of the 500 top domestic companies in terms of revenuesand 238 of the Fortune 500 companies at June 30, 2006. We believe that we have thelargest personal banking customer base in China with more than 150 million personalbanking customers. At June 30, 2006, we had more than 50 million customers maintaining

2

Global Reports LLC

SUMMARY

a financial asset balance in the range of RMB5,000 to RMB50,000 each with us. At thesame date, we had over 16 million customers maintaining a financial asset balance of overRMB50,000 each with us. The average financial asset balance of these customers was overRMB150,000.

Š Extensive Distribution Network and Largest Electronic Banking Service Provider. Wehave a nationwide presence, with 18,038 branches, outlets and other establishments(including head office) in China at June 30, 2006. Our traditional branch network issupported by a large sales force in both corporate and personal banking and supplementedby our convenient electronic banking network.

Š Leading Information Technology Capabilities. We believe that we have the most advancedinformation technology platform among PRC commercial banks. We were the first BigFour commercial bank to complete a bank-wide data consolidation project, which enablescentralized real-time processing of operational data from all of our domestic branchoffices. We received the worldwide “Networking Initiative of the Year” award in June2006 from The Banker, the “Best Banking Technology Development Award” in 2004from the PBOC for our bank-wide data consolidation project, the “Best Consumer InternetBank” in China award in 2004, 2005 and 2006 from Global Finance, the First Prize of“China Internet Industry Survey Report for Internet Banking” in 2005 from the InternetSociety of China, the “Gold Award for Customer Care and Public Service in China” in2005 from the Ministry of Information Industry and the “Bank with Best InvestmentManagement Services in Corporate Internet Banking” in Asia Pacific award in 2006 fromGlobal Finance. Our leading technology infrastructure provides comprehensive support toour operations and facilitates the growth of our revenues.

Š Fast Growing Fee and Commission Income. We have experienced fast growth in our feeand commission income, as a result of our strategic focus on developing our non-interestbased businesses. In 2005, our net fee and commission income was the highest among theBig Four commercial banks. Our net fee and commission income increased fromRMB5,624 million in 2003 to RMB10,546 million in 2005, representing a compoundannual growth rate of 36.9%. As we plan to focus on and expand our leadership in non-interest based businesses, we believe that we will be able to further increase our fee andcommission income.

Š Comprehensive Risk Management and Internal Controls. We have a risk managementframework covering credit, liquidity, market and operational risks. This framework, whichis supported by our advanced risk management information technology, enables us tobetter manage our risks and has contributed to the improvement of our asset quality.

Š Stable and Experienced Management Team. Our senior management team has extensiveindustry and leadership experience in China’s commercial banking industry. Our seniormanagement team has a track record of successfully implementing innovative andindustry-leading business initiatives.

OUR STRATEGY

We aim to strengthen our market leadership in China’s banking industry and focus ontransforming our bank into a world-class financial institution. Our overall goal is to maximizeshareholder value and achieve sustainable growth. We believe we have distinguished ourselves through

3

Global Reports LLC

SUMMARY

our innovative business approach and market leading initiatives. We led the market in investing incentralized information technology, introducing new products and services, establishingcomprehensive risk management systems and developing electronic banking networks. We intend tocontinue this innovative approach and differentiate ourselves through the following strategies:

Š Diversify Our Revenue and Asset Mix by Expanding into Higher Growth Non-CreditBusinesses. We plan to diversify our revenue sources by continuing to develop ournon-credit businesses. We believe that many fee- and commission-based products andservices will experience strong growth over the next few years as China’s economycontinues to grow, the financial services sector in China further liberalizes and ourcustomers’ banking needs become more sophisticated.

Š Prudently Grow Our Credit Businesses and Actively Enhance Our Credit Portfolio. Weseek to leverage our market leadership in corporate and personal lending to prudentlygrow our credit businesses and improve our risk-adjusted return by actively managing thesector, geographical, customer and product composition of our credit portfolio.

Š Continue to Improve Our Customer Mix and Profitability through Increased CustomerSegmentation, Targeted Marketing and Enhanced Customer Service. We will continue toleverage our extensive customer base and database to identify and retain profitablecustomers in both our corporate banking and personal banking businesses. By betterunderstanding the characteristics, needs and preferences of our customers, we can designnew products, attract more customers and actively cross-sell our financial products andservices.

Š Strategically Expand Our Traditional Branch Network and Enhance Our Sales andMarketing Capabilities through Strengthening Our Electronic Banking Operations. Weintend to fully leverage our advanced information technology platform and customerrelationship management systems. In order to provide our customers with convenientaccess to our products and services, we also intend to expand our electronic bankingoperations and improve the productivity of our traditional branch network throughstreamlining the operations of our branch network. In addition, to take advantage of therapid growth in foreign trade and better serve our multinational clients, we intend tofurther expand our network by establishing additional overseas branches and outlets.

Š Continue to Strengthen Our Risk Management and Internal Control Capabilities. We planto continue to align our risk management and internal control capabilities withinternational best practices.

Š Leverage Our Partnerships with Strategic Investors. We are cooperating with our overseasstrategic investors to improve our corporate governance, strengthen our new productdevelopment capabilities and diversify our product and service offerings.

Š Enhance Employee Performance through Performance-linked Incentive Schemes andContinuous Training and Development. We will continue to develop our human resourcesthrough various initiatives in order to support our business strategies. We believe thatthrough adopting an economic value-added (EVA)-based incentive scheme and enhancingthe training and development of our employees, we can attract, retain, motivate anddevelop a high quality workforce.

4

Global Reports LLC

SUMMARY

OUR RESTRUCTURING AND INCORPORATION

We were converted from a state-owned commercial bank to a joint-stock limited company onOctober 28, 2005, with the MOF and Huijin as our promoters, and our legal name was changed toIndustrial and Commercial Bank of China Limited. All of the businesses, assets and liabilities ofIndustrial and Commercial Bank of China were assumed by Industrial and Commercial Bank of ChinaLimited upon the conversion.

As part of our financial restructuring in 2005 (i) the MOF retained RMB124.0 billion of ourthen existing capital, (ii) Huijin made a capital contribution of US$15.0 billion to us, (iii) we disposedof certain non-performing assets in an aggregate amount of RMB705.0 billion at book value, (iv) thegovernment contributed certain land use rights to us, and (v) the MOF amended the terms of a specialgovernment bond issued by it to us.

To further accelerate our corporate governance reform and business development, we haveestablished non-exclusive strategic cooperations with The Goldman Sachs Group, Inc., Allianz Groupand American Express Company. In addition, the National Council for Social Security Fund has madean investment in us.

5

Global Reports LLC

SUMMARY

SUMMARY FINANCIAL INFORMATION

The summary historical consolidated income statement data for the years ended December 31,2003, 2004, 2005, and the six months ended June 30, 2005 and 2006 and the summary historicalconsolidated balance sheet data at December 31, 2003, 2004, 2005, and June 30, 2006 set forth belowhave been derived from the Accountants’ Report issued by Ernst & Young, Certified PublicAccountants, Hong Kong, which has been prepared in accordance with IFRS and is included inAppendix I to this prospectus. You should read the summary historical financial information below inconjunction with Appendix I “Accountants’ Report”.

Summary Historical Consolidated Income Statement DataFor the year ended

December 31,For the six months ended

June 30,

2003 2004 2005 2005 (unaudited) 2006

(in millions of RMB, except per share data)

Interest income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 189,069 204,889 240,202 112,283 129,038Interest expense . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (66,361) (70,161) (86,599) (40,558) (52,530)

Net interest income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 122,708 134,728 153,603 71,725 76,508

Fee and commission income . . . . . . . . . . . . . . . . . . . . . . . 7,059 9,780 12,376 5,502 8,761Fee and commission expense . . . . . . . . . . . . . . . . . . . . . . (1,435) (1,572) (1,830) (635) (895)

Net fee and commission income . . . . . . . . . . . . . . . . . . . 5,624 8,208 10,546 4,867 7,866

Other operating income . . . . . . . . . . . . . . . . . . . . . . . . . . . 4,452 5,023 7,471 4,500 1,376

Operating income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 132,784 147,959 171,620 81,092 85,750

Operating expenses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (62,575) (62,639) (81,585) (33,964) (34,696)

Provisions for impairment losses on—Loans and advances to customers . . . . . . . . . . . . . (34,914) (30,511) (26,589) (11,558) (11,645)—Others . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (1,379) (348) (425) (165) (573)

Operating profit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33,916 54,461 63,021 35,405 38,836

Share of profits and losses of associates . . . . . . . . . . . . . . (32) (50) 5 — 5

Profit before tax . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33,884 54,411 63,026 35,405 38,841

Income tax expense . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (11,292) (23,193) (25,007) (9,957) (13,199)

Profit for the year/period . . . . . . . . . . . . . . . . . . . . . . . . 22,592 31,218 38,019 25,448 25,642

Attributable to:Equity holders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22,472 30,863 37,555 25,161 25,399Minority interests . . . . . . . . . . . . . . . . . . . . . . . . . . . 120 355 464 287 243

22,592 31,218 38,019 25,448 25,642

Earnings per share attributable to equity holders—Basic and diluted (RMB) . . . . . . . . . . . . . . . . . . . . 0.09 0.12 0.15 0.10 0.10

6

Global Reports LLC

SUMMARY

Summary Historical Consolidated Balance Sheet DataAt December 31, At June 30,

2003 2004 2005 2006

(in millions of RMB)

AssetsCash and balances with central banks . . . . . . . . . . . . . . . . . . . . . . . 457,816 508,616 553,873 598,269Due from banks and other financial institutions . . . . . . . . . . . . . . . 66,009 69,430 132,162 131,133Reverse repurchase agreements . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71,239 21,764 89,235 105,542Loans and advances to customers . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,766,055 3,109,191 3,205,861 3,375,342Investment securities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,044,730 1,230,416 2,305,689 2,657,819Income tax recoverable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 427 — — —Investments in associates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 274 117 120 125Property and equipment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77,767 75,579 92,984 88,709Deferred income tax assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27,381 8,805 — —Other assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45,253 45,406 76,207 97,686

Total assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4,556,951 5,069,324 6,456,131 7,054,625

LiabilitiesDue to a central bank . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32,383 28,402 — —Due to banks and other financial institutions . . . . . . . . . . . . . . . . . . 219,009 205,695 232,910 367,218Repurchase agreements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16,253 26,339 32,301 11,622Certificates of deposit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,376 3,680 5,704 6,991Due to customers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4,706,861 5,176,282 5,736,866 6,119,038Income tax payable . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 84 2,792 14,641 12,812Deferred income tax liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . — — 1,418 270Debt issued . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . — 3,294 38,076 37,987Other liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 118,119 130,885 134,339 169,222

Total liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5,096,085 5,577,369 6,196,255 6,725,160

EQUITYIssued share capital/paid-up capital . . . . . . . . . . . . . . . . . . . . . . . . . 160,671 160,669 248,000 286,509Reserves . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17,151 15,334 2,559 19,681Retained profits/(accumulated losses) . . . . . . . . . . . . . . . . . . . . . . . (718,571) (687,716) 5,280 19,183

Equity attributable to equity holders . . . . . . . . . . . . . . . . . . . . . . . . (540,749) (511,713) 255,839 325,373Minority interests . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,615 3,668 4,037 4,092

Total equity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (539,134) (508,045) 259,876 329,465

Total equity and liabilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4,556,951 5,069,324 6,456,131 7,054,625

7

Global Reports LLC

SUMMARY

Selected Financial Ratios

For the year endedDecember 31,

For thesix months ended

June 30,

2003 2004 20052005

(unaudited) 2006

(in percentages)

Profitability indicatorsReturn on total assets(1) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.50% 0.62% 0.59% 0.83%(13) 0.73%(13)

Return on average total assets(2) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . N/A 0.65 0.66 0.91(13) 0.76(13)

Return on equity(3) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . N/A N/A 14.68 21.86(13) 15.61(13)

Net interest spread(4) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2.59 2.54 2.58 2.56(13) 2.30(13)

Net interest margin(5) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2.59 2.55 2.61 2.56(13) 2.35(13)

Non-interest income to operating income(6) . . . . . . . . . . . . . . . . . . . . . 7.59 8.94 10.50 11.55 10.78Operating expenses to operating income(7) . . . . . . . . . . . . . . . . . . . . . 47.1 42.3 47.5 41.9 40.5Operating expenses to operating income (excluding business tax and

surcharges and interest income and expenses in relation to aspecial government bond)(8) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38.8 34.0 40.1 34.0 34.2

At December 31,At

June 30,

2003 2004 2005 2006

(in percentages)

Capital adequacy indicatorsCore capital adequacy ratio(9) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . N/A N/A 8.11 8.97Capital adequacy ratio(9) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . N/A N/A 9.89 10.74Total equity to total assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . N/A N/A 4.03 4.67

Assets quality indicatorsNon-performing loan ratio(10) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24.24 21.16 4.69 4.10Allowance to non-performing loans(11) . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77.15 76.28 54.20 60.37Allowance to total loans(12) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18.70 16.14 2.54 2.48

(1) Represents the profit for the period (including profit attributable to minority interests) as a percentage of the period end balance of totalassets.

(2) Represents the profit for the period (including profit attributable to minority interests) as a percentage of the average balance of totalassets at the beginning and end of the period.

(3) Represents the profit attributable to equity holders as a percentage of the period end balance of total equity excluding minority interests.(4) Calculated as the difference between the average yield on average interest-earning assets and the average cost on average interest-bearing

liabilities.(5) Calculated by dividing net interest income by average interest-earning assets.(6) Calculated by dividing (i) net fee and commission income and other operating income, by (ii) operating income.(7) Calculated by dividing total operating expenses by operating income.(8) Calculated by dividing (i) total operating expenses minus business tax and surcharges and expenses in relation to the special government

bond, by (ii) operating income, which, for the years ended December 31, 2003, 2004 and 2005 and the six months ended June 30, 2005,is subtracted by interest income in relation to the special government bond (other than interest income accrued after December 1, 2005 inthe case of the year ended December 31, 2005).

(9) The ratios at December 31, 2005 are prepared in accordance with the statutory financial statements and do not reflect the impact ofCaikuai (2005) No. 14 “Provisional Guidelines on Recognition and Measurement of Financial Instruments” issued by the MOF. Theratios as at June 30, 2006 are prepared in accordance with the PRC GAAP. We had a capital deficit for each of 2003 and 2004.

(10) Calculated by dividing non-performing loans and advances to customers by total loans and advances to customers.(11) Calculated by dividing the allowance for impairment losses on total loans and advances by total non-performing loans and advances to

customers.(12) Calculated by dividing the allowance for impairment losses on total loans and advances by total loans and advances to customers.(13) Calculated by using annualized average rates.

8

Global Reports LLC

SUMMARY

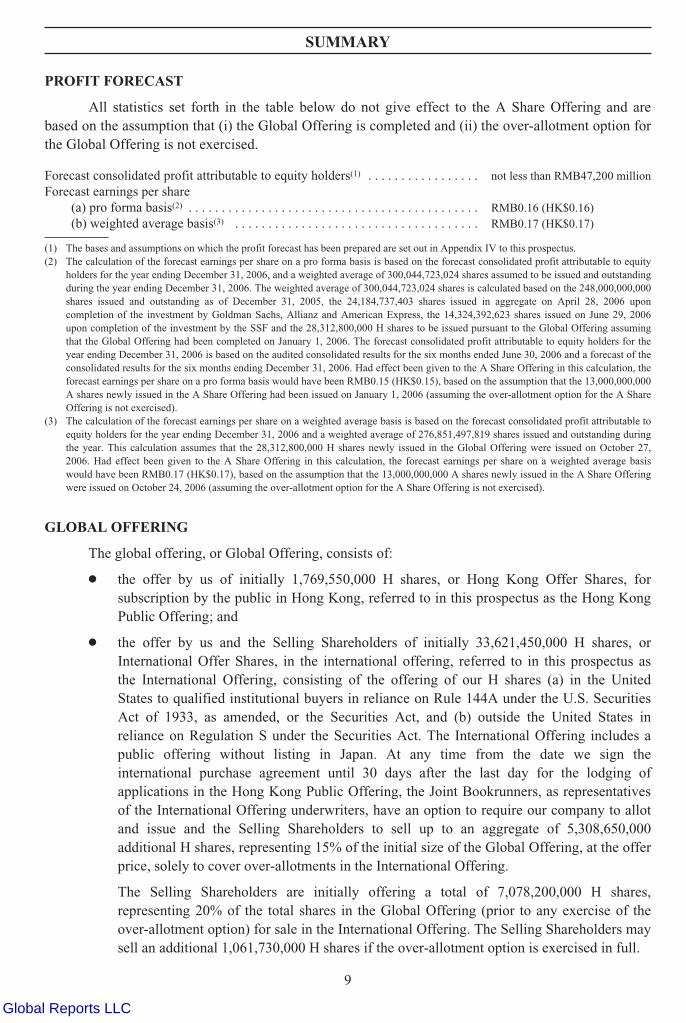

PROFIT FORECAST

All statistics set forth in the table below do not give effect to the A Share Offering and arebased on the assumption that (i) the Global Offering is completed and (ii) the over-allotment option forthe Global Offering is not exercised.

Forecast consolidated profit attributable to equity holders(1) . . . . . . . . . . . . . . . . . not less than RMB47,200 millionForecast earnings per share

(a) pro forma basis(2) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . RMB0.16 (HK$0.16)(b) weighted average basis(3) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . RMB0.17 (HK$0.17)

(1) The bases and assumptions on which the profit forecast has been prepared are set out in Appendix IV to this prospectus.(2) The calculation of the forecast earnings per share on a pro forma basis is based on the forecast consolidated profit attributable to equity

holders for the year ending December 31, 2006, and a weighted average of 300,044,723,024 shares assumed to be issued and outstandingduring the year ending December 31, 2006. The weighted average of 300,044,723,024 shares is calculated based on the 248,000,000,000shares issued and outstanding as of December 31, 2005, the 24,184,737,403 shares issued in aggregate on April 28, 2006 uponcompletion of the investment by Goldman Sachs, Allianz and American Express, the 14,324,392,623 shares issued on June 29, 2006upon completion of the investment by the SSF and the 28,312,800,000 H shares to be issued pursuant to the Global Offering assumingthat the Global Offering had been completed on January 1, 2006. The forecast consolidated profit attributable to equity holders for theyear ending December 31, 2006 is based on the audited consolidated results for the six months ended June 30, 2006 and a forecast of theconsolidated results for the six months ending December 31, 2006. Had effect been given to the A Share Offering in this calculation, theforecast earnings per share on a pro forma basis would have been RMB0.15 (HK$0.15), based on the assumption that the 13,000,000,000A shares newly issued in the A Share Offering had been issued on January 1, 2006 (assuming the over-allotment option for the A ShareOffering is not exercised).

(3) The calculation of the forecast earnings per share on a weighted average basis is based on the forecast consolidated profit attributable toequity holders for the year ending December 31, 2006 and a weighted average of 276,851,497,819 shares issued and outstanding duringthe year. This calculation assumes that the 28,312,800,000 H shares newly issued in the Global Offering were issued on October 27,2006. Had effect been given to the A Share Offering in this calculation, the forecast earnings per share on a weighted average basiswould have been RMB0.17 (HK$0.17), based on the assumption that the 13,000,000,000 A shares newly issued in the A Share Offeringwere issued on October 24, 2006 (assuming the over-allotment option for the A Share Offering is not exercised).

GLOBAL OFFERING

The global offering, or Global Offering, consists of:

Š the offer by us of initially 1,769,550,000 H shares, or Hong Kong Offer Shares, forsubscription by the public in Hong Kong, referred to in this prospectus as the Hong KongPublic Offering; and

Š the offer by us and the Selling Shareholders of initially 33,621,450,000 H shares, orInternational Offer Shares, in the international offering, referred to in this prospectus asthe International Offering, consisting of the offering of our H shares (a) in the UnitedStates to qualified institutional buyers in reliance on Rule 144A under the U.S. SecuritiesAct of 1933, as amended, or the Securities Act, and (b) outside the United States inreliance on Regulation S under the Securities Act. The International Offering includes apublic offering without listing in Japan. At any time from the date we sign theinternational purchase agreement until 30 days after the last day for the lodging ofapplications in the Hong Kong Public Offering, the Joint Bookrunners, as representativesof the International Offering underwriters, have an option to require our company to allotand issue and the Selling Shareholders to sell up to an aggregate of 5,308,650,000additional H shares, representing 15% of the initial size of the Global Offering, at the offerprice, solely to cover over-allotments in the International Offering.

The Selling Shareholders are initially offering a total of 7,078,200,000 H shares,representing 20% of the total shares in the Global Offering (prior to any exercise of theover-allotment option) for sale in the International Offering. The Selling Shareholders maysell an additional 1,061,730,000 H shares if the over-allotment option is exercised in full.

9

Global Reports LLC

SUMMARY

The number of Hong Kong Offer Shares and International Offer Shares, or together, OfferShares, is subject to adjustment and reallocation as described in “Structure of the Global Offering.”

A SHARE OFFERING

Concurrently with the Global Offering, we are undertaking a public offering of our A shares inthe PRC, which offering is referred to in this prospectus as our A Share Offering. Our A ShareOffering comprises an offering of initially 13,000,000,000 A shares (or 14,950,000,000 A shares if theover-allotment option for the A Share Offering is exercised in full) for subscription. Assuming an offerprice of RMB2.86 per A share, being the mid-point of the price range of the A Share Offering, weestimate that the net proceeds to us from the A Share Offering will be approximately RMB36.3 billion(HK$35.8 billion) if the over-allotment option is not exercised, or RMB41.8 billion (HK$41.1 billion)if the over-allotment option is exercised in full. Neither our Global Offering nor our A Share Offeringis conditional upon the other. See “A Share Offering.”

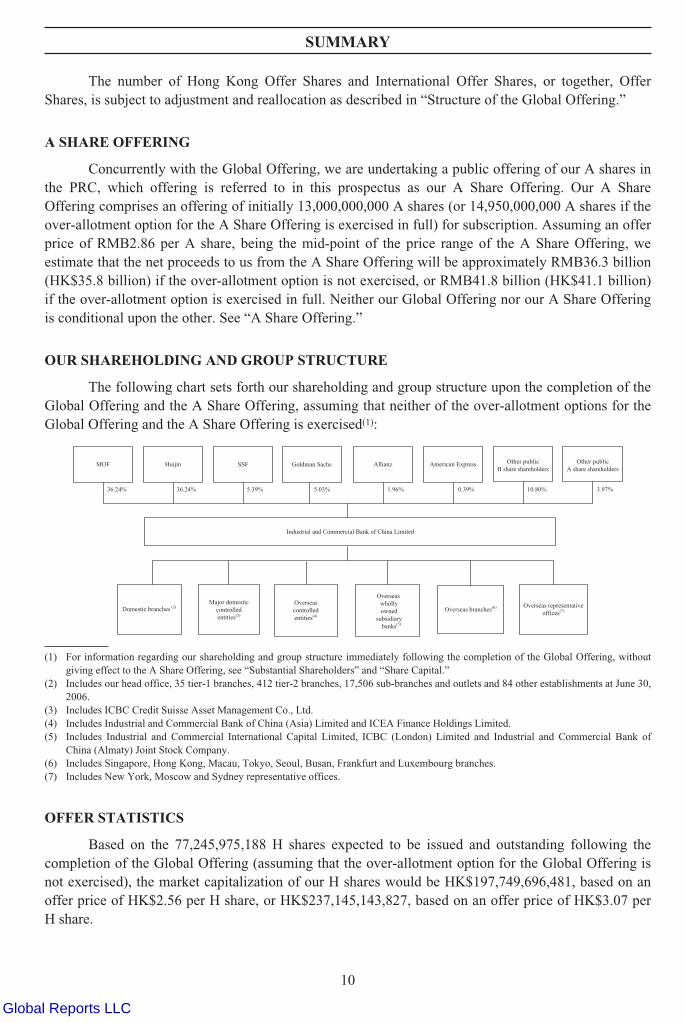

OUR SHAREHOLDING AND GROUP STRUCTURE

The following chart sets forth our shareholding and group structure upon the completion of theGlobal Offering and the A Share Offering, assuming that neither of the over-allotment options for theGlobal Offering and the A Share Offering is exercised(1):

Industrial and Commercial Bank of China Limited

Major domesticcontrolledentities(3)

Overseascontrolledentities(4)

Domestic branches (2)

Overseas whollyowned

subsidiarybanks

Overseas representativeoffices(7)Overseas branches(6)

(5)

MOF Huijin Goldman SachsSSF Allianz American Express

36.24% 36.24% 5.39% 5.03% 1.96% 0.39% 10.80%

Other publicH share shareholders

3.97%

Other publicA share shareholders

(1) For information regarding our shareholding and group structure immediately following the completion of the Global Offering, withoutgiving effect to the A Share Offering, see “Substantial Shareholders” and “Share Capital.”

(2) Includes our head office, 35 tier-1 branches, 412 tier-2 branches, 17,506 sub-branches and outlets and 84 other establishments at June 30,2006.

(3) Includes ICBC Credit Suisse Asset Management Co., Ltd.(4) Includes Industrial and Commercial Bank of China (Asia) Limited and ICEA Finance Holdings Limited.(5) Includes Industrial and Commercial International Capital Limited, ICBC (London) Limited and Industrial and Commercial Bank of

China (Almaty) Joint Stock Company.(6) Includes Singapore, Hong Kong, Macau, Tokyo, Seoul, Busan, Frankfurt and Luxembourg branches.(7) Includes New York, Moscow and Sydney representative offices.

OFFER STATISTICS

Based on the 77,245,975,188 H shares expected to be issued and outstanding following thecompletion of the Global Offering (assuming that the over-allotment option for the Global Offering isnot exercised), the market capitalization of our H shares would be HK$197,749,696,481, based on anoffer price of HK$2.56 per H share, or HK$237,145,143,827, based on an offer price of HK$3.07 perH share.

10

Global Reports LLC

SUMMARY

The statistics in the following table do not give effect to the A Share Offering and are based onthe assumptions that (i) the Global Offering is completed, (ii) 28,312,800,000 H shares are newlyissued in the Global Offering, (iii) the over-allotment option for the Global Offering is not exercised,and (iv) 314,821,930,026 shares are issued and outstanding following the completion of the GlobalOffering:

Based on an offerprice of

HK$2.56 per H share

Based on an offerprice of

HK$3.07 per H share

Prospective price/earnings multiple(a) pro forma basis(1) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16.0 times 19.2 times(b) weighted average basis(2) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15.1 times 18.1 times

Unaudited pro forma adjusted consolidated net tangible assets pershare(3) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . HK$1.23 HK$1.28

(1) The calculation of the prospective price/earnings multiple on a pro forma basis is based on the forecast earnings per share for the yearending December 31, 2006 on a pro forma basis at the respective offer prices of HK$2.56 per H share and HK$3.07 per H share. Hadeffect been given to the A Share Offering in this calculation, the prospective price/earnings multiple on a pro forma basis would havebeen 17.1 times based on an offer price of HK$2.56 per H share and 20.5 times based on an offer price of HK$3.07 per H share. Thiscalculation is based on the assumption that there were 13,000,000,000 A shares newly issued in the A Share Offering (assuming theover-allotment option for the A Share Offering is not exercised).

(2) The calculation of the prospective price/earnings multiple on a weighted average basis is based on the forecast earnings per share for theyear ending December 31, 2006 on a weighted average basis at the respective offer prices of HK$2.56 per H share and HK$3.07 perH share. Had effect been given to the A Share Offering in this calculation, the prospective price/earnings multiple on a weighted averagebasis would have been 15.1 times based on an offer price of HK$2.56 per H share and 18.1 times based on an offer price of HK$3.07 perH share. This calculation is based on the assumption that there were 13,000,000,000 A shares newly issued in the A Share Offering(assuming the over-allotment option for the A Share Offering is not exercised).

(3) The unaudited pro forma adjusted consolidated net tangible assets per share is calculated after making the adjustments referred to inAppendix III. Had effect been given to the A Share Offering in this calculation, our unaudited pro forma adjusted consolidated nettangible assets per share would have been HK$1.28 or RMB1.30 based on the offer prices of HK$2.56 per H share and RMB2.60 per Ashare and HK$1.35 or RMB1.37 based on the offer prices of HK$3.07 per H share and RMB3.12 per A share. This calculation is basedon the assumption that there were 13,000,000,000 newly issued A shares in the A Share Offering (assuming the over-allotment option forthe A Share Offering is not exercised) and the resulting net proceeds (after deduction of the estimated underwriting fees and other relatedexpenses payable by us) of RMB33.0 billion (based on the offer price of RMB2.60 per A share) and RMB39.6 billion (based on the offerprice of RMB3.12 per A share) from the A Share Offering.

If the over-allotment option for the Global Offering is exercised in full, the unaudited pro formaadjusted consolidated net tangible assets per H share will be approximately HK$1.25 (based on anoffer price of HK$2.56 per H share) or approximately HK$1.30 (based on an offer price of HK$3.07per H share), while the forecast earnings per H share on a pro forma basis and on a weighted averagebasis will be approximately HK$0.15 per H share and HK$0.17 per H share, respectively.

If the over-allotment options for both the Global Offering and the A Share Offering areexercised in full, the unaudited pro forma adjusted consolidated net tangible assets per H share will beapproximately HK$1.31 (based on offer prices of HK$2.56 per H share and RMB2.60 per A share) orapproximately HK$1.38 (based on an offer price of HK$3.07 per H share and RMB3.12 per A share),while the forecast earnings per H share on a pro forma basis and on a weighted average basis will beapproximately HK$0.15 per H share and HK$0.17 per H share, respectively.

USE OF PROCEEDS

After deducting the underwriting commission and our estimated offering expenses, we estimatethat the net proceeds to us from the Global Offering will be approximately HK$77.4 billion (RMB78.6billion) if the underwriters do not exercise their over-allotment option, or HK$89.1 billion (RMB90.5billion) if the underwriters exercise their over-allotment option in full, assuming an offer price of

11

Global Reports LLC

SUMMARY

HK$2.815 (RMB2.86) per H share, the midpoint of the range set forth on the cover page of thisprospectus. We will not receive any of the proceeds from the sale of shares by the Selling Shareholdersin the Global Offering. The Selling Shareholders will bear their proportional underwriting commissionand offering expenses.

We expect to use the net proceeds from the Global Offering to strengthen our capital base tosupport the ongoing growth of our business as set forth in “Business—Our Strategy.”

RISK FACTORS

There are certain risks and considerations relating to an investment in our shares. These can becategorized into: (i) risks relating to our business; (ii) risks relating to the banking industry in China;(iii) risks relating to China; and (iv) risks relating to the Global Offering. These risks andconsiderations are further described in “Risk Factors” and are summarized below.

Risks Relating to Our Business

Š Our current results of operations and financial condition reflect a number of extraordinarydisposals of non-performing loans.

Š Actual losses on our loan portfolio may exceed our allowance for impairment losses in thefuture.

Š We have a concentration of exposures to certain industries.

Š The collateral or guarantees securing our loans may not fully protect us from the relatedcredit risks.

Š We may fail to satisfy the capital adequacy requirements established by the CBRC.

Š We cannot assure you that our risk management and internal control policies andprocedures can adequately control or protect us against all credit and other risks.

Š We face certain risks relating to our operational reform initiatives.

Š Our expanding range of products, services and business activities exposes us to new risks.

Š We may not be able to detect and prevent fraud or other misconduct committed by ouremployees or third parties.

Š We are subject to liquidity risk.

Š We are subject to risks relating to our information technology systems.

Š We are subject to credit risk with respect to certain off-balance sheet commitments.

Š We are required to meet PRC and overseas regulatory requirements and guidelines and ournon-compliance could result in fines, sanctions and other penalties.

Š We do not, and some of our lessors may not, possess the relevant title certificates or haveconsent from the owners to sublet some of the properties occupied by us.

Š We are subject to certain risks relating to the bonds issued by Huarong.

Š Our largest shareholders have the ability to exercise significant influence over us.

12

Global Reports LLC

SUMMARY

Risks Relating to the Banking Industry in China

Š Competition in the banking industry in China is increasing.

Š China’s banking regulatory environment is continually evolving and may change.

Š We are subject to changes in interest rates and other market risks, and our ability to hedgemarket risks is limited.

Š PRC regulations impose certain limitations on the types of investments we may make and,as a result, our ability to seek higher investment returns and our ability to diversify ourinvestment portfolio or hedge the risks relating to our Renminbi-denominated assets arelimited.

Š We face risks relating to the inspections and examinations carried out by PRC andoverseas regulatory authorities.

Š The effectiveness of our credit risk management is affected by the quality and scope ofinformation available in China.

Š Our loan classification and other policies are different in certain respects from thoseapplicable to banks in certain other countries or regions.

Š Future amendments to IAS39 and interpretive guidance on its application may require usto change our loan provisioning practice.

Š We cannot assure you of the accuracy or comparability of facts, forecasts and statisticscontained in this prospectus with respect to China, its economy or the PRC and globalbanking industries.

Š The ability of our shareholders to pledge their shares is limited by applicable PRC legaland regulatory requirements.

Š Any acquisition of 5% or more of our total outstanding shares will require the CBRC’sprior approval.

Risks Relating to China

Š China’s economic, political and social conditions, as well as government policies, couldaffect our business.

Š The legal protections available to you under the PRC legal system may be limited.

Š You may experience difficulties in effecting service of legal process and enforcingjudgments against us and our management.

Š Holders of H shares may be subject to PRC taxation.

Š Payment of dividends is subject to restrictions under PRC law.

Š We are subject to PRC government controls on currency conversion and future movementsin exchange rates.

Risks Relating to the Global Offering

Š An active trading market for our H shares may not develop, and their trading prices mayfluctuate significantly.

13

Global Reports LLC

SUMMARY

Š We are conducting a concurrent but separate A Share Offering; the characteristics of the Ashare and H share markets are different.

Š Future sales or perceived sales of a substantial number of our H shares or A shares inpublic markets could adversely affect the prevailing market price of our H shares.

Š Because the initial public offering price of the H shares is higher than the net tangibleasset value per share, you will incur immediate dilution.

Š Dividends declared in the past may not be indicative of our dividend policy in the future.

Š We strongly caution you not to place any reliance on any information contained in pressarticles or other media regarding our Global Offering or the A Share Offering orinformation released by us in connection with the A Share Offering.

DIVIDEND POLICY

Our shareholders’ general meeting decides whether to pay any dividends and in what amountbased on our results of operations, cash flow, financial condition, capital adequacy ratios, futureprospects, statutory and regulatory restrictions on the payment of dividends by us and other relevantfactors. Under the PRC Company Law and our articles of association, all of our shareholders haveequal rights to dividends and distributions.

Under PRC law, dividends may be paid only out of distributable profits. Distributable profitsmeans, as determined under PRC GAAP or IFRS, whichever is lower, the net profits for a period, plusthe distributable profits or net of the accumulated losses, if any, at the beginning of such period, lessappropriations to statutory surplus reserve (determined under PRC GAAP), general reserve, anddiscretionary surplus reserve (as approved by our shareholders meeting). Any distributable profits thatare not distributed in a given year are retained and available for distribution in subsequent years.

At an extraordinary general meeting of shareholders on April 28, 2006, our board of directorsrecommended and our shareholders approved a cash dividend to the MOF and Huijin in the amount ofRMB3,537 million for the year ended December 31, 2005.

At the extraordinary general meetings of shareholders on July 31, 2006 and September 22,2006, respectively, our board of directors recommended, and our shareholders approved, the dividenddistributions and policies for the period beginning on January 1, 2006 and ending on December 31,2008. See “Financial Information—Dividend Policy.”

14

Global Reports LLC

DEFINITIONS AND CONVENTIONS

In this prospectus, unless the context otherwise requires, the following terms shall have themeanings set out below.

“CBRC” China Banking Regulatory Commission

“CCASS” The Central Clearing and Settlement Systemestablished and operated by HKSCC

“CEPA” The Mainland and Hong Kong Closer EconomicPartnership Arrangement, and the Mainland andMacau Closer Economic Partnership Arrangement

“China,” “PRC” and “Mainland China” The People’s Republic of China, excluding, forpurposes of this prospectus, the Hong Kong SpecialAdministrative Region of the PRC, or Hong Kong, theMacau Special Administrative Region of the PRC, orMacau, and Taiwan

“CIRC” China Insurance Regulatory Commission

“COSO” The Committee of Sponsoring Organizations of theTreadway Commission

“CSRC” China Securities Regulatory Commission

“Hong Kong Listing Rules” The Rules Governing the Listing of Securities on TheStock Exchange of Hong Kong Limited

“Hong Kong Stock Exchange” The Stock Exchange of Hong Kong Limited

“Huarong” China Huarong Asset Management Corporation

“Huijin” Central SAFE Investments Limited, previously knownas China SAFE Investments Limited

“IAS” International Accounting Standards and theirinterpretations

“IFRS” International Financial Reporting Standardspromulgated by the International AccountingStandards Board (“IASB”), which include IAS

“MOF” Ministry of Finance of the PRC

“NAO” National Audit Office of the PRC

“NDRC” National Development and Reform Commission of thePRC

15

Global Reports LLC

DEFINITIONS AND CONVENTIONS

“Net Capital Base” Core capital and supplementary capital of a bank lessdeductions, in each case, as specified in the relevantCBRC regulations

“PBOC” People’s Bank of China

“PRC GAAP” The accounting rules and regulations in the PRC,currently consisting of the Accounting Standards forBusiness Enterprises, the Accounting System forFinancial Institutions (2001) and other relatedregulations, including Caikuai (2005) No. 14“Provisional Guidelines on Recognition andMeasurement of Financial Instruments”

“SAFE” State Administration of Foreign Exchange of the PRC

“SAIC” State Administration of Industry and Commerce of thePRC

“SAT” State Administration of Taxation of the PRC

“SSF” National Council for Social Security Fund of the PRC

“State Council” The PRC State Council

In this prospectus, the “Company,” “we,” “us,” “our,” “our bank” and “our company” refer toeither or both of Industrial and Commercial Bank of China Limited and our predecessor, Industrial andCommercial Bank of China, as applicable, and, except as the context may otherwise require, thesubsidiaries of Industrial and Commercial Bank of China Limited and of our predecessor, Industrialand Commercial Bank of China.

References to “controlling shareholder” mean any shareholder or other person or group ofpersons together entitled to exercise, or control the exercise of, 30% (or such other amount as mayfrom time to time be specified in applicable PRC law as being the level for triggering a mandatorygeneral offer or for otherwise establishing legal or management control over a business enterprise) ormore of the voting power at our general meetings or who is in a position to control the composition ofa majority of our board of directors.

For the purposes of this prospectus, we use the terms “impaired loans,” “non-performing loans”or “NPLs” synonymously to refer to the loans identified as “identified impaired loans and advances” inNote 16 to our financial information included in the Accountants’ Report in Appendix I to thisprospectus.

References to the “Selling Shareholders” mean (i) the MOF and (ii) Huijin.

References to the “Latest Practicable Date” mean October 3, 2006, which is the latestpracticable date for the purposes of ascertaining certain information for inclusion in this prospectus.

16

Global Reports LLC

DEFINITIONS AND CONVENTIONS

In this prospectus, we define the geographical regions of China to which we refer for thepurpose of describing our branch network and presenting certain results of operations and financialcondition as follows:

Geographical regions Tier-1 branches

“Yangtze River Delta” Š Shanghai Municipality Š Jiangsu ProvinceŠ Zhejiang Province Š City of Ningbo

“Pearl River Delta” Š Guangdong Province Š City of ShenzhenŠ Fujian Province Š City of Xiamen

“Bohai Rim” Š Beijing Municipality Š Tianjin MunicipalityŠ Hebei Province Š Shandong ProvinceŠ City of Qingdao

“Central China” Š Shanxi Province Š Henan ProvinceŠ Hubei Province Š Anhui ProvinceŠ Jiangxi Province Š Hainan ProvinceŠ Hunan Province

“Northeastern China” Š Liaoning Province Š Heilongjiang ProvinceŠ Jilin Province Š City of Dalian

“Western China” Š Sichuan Province Š Gansu ProvinceŠ Guizhou Province Š Qinghai ProvinceŠ Yunnan Province Š Chongqing MunicipalityŠ Ningxia Autonomous Region Š Xinjiang Autonomous RegionŠ Inner Mongolia Autonomous

RegionŠ Shaanxi Province

Š Guangxi Autonomous Region

Solely for your convenience, this prospectus contains translations of certain Renminbi amountsinto Hong Kong dollars, Renminbi amounts into U.S. dollars, and Hong Kong dollars into U.S. dollarsat specific rates. You should not construe these translations as representations that the Renminbiamounts could actually be converted into any Hong Kong dollar or U.S. dollar amounts (as the casemay be) at the rates indicated or at all. Unless we indicate otherwise, the translations of Renminbi intoHong Kong dollars, Renminbi into U.S. dollars and Hong Kong dollars into U.S. dollars have beenmade at the rates of RMB1.0154 to HK$1.00, the exchange rate set by the PBOC for foreign exchangetransactions prevailing on September 29, 2006, and RMB7.9040 to US$1.00 and HK$7.7907 toUS$1.00, the noon buying rates in New York City for cable transfers as certified for customs purposesby the Federal Reserve Bank of New York on October 3, 2006. Further information on exchange ratesis set forth in “Appendix VI—Taxation and Foreign Exchange.”

Any discrepancies in any table or chart between the total shown and the sum of the amountslisted are due to rounding.

17

Global Reports LLC

FORWARD-LOOKING STATEMENTS

We have included in this prospectus forward-looking statements regarding our plans,intentions, beliefs, expectations and predictions for the future, particularly under “Banking Industry inChina,” “Our Restructuring and Operational Reform,” “Our Strategic Investors and Other Investors,”“Business,” “Risk Management,” “Relationship with Our Promoters and Connected Transactions,”“Assets and Liabilities,” “Financial Information” and “Future Plans and Use of Proceeds.” By theirnature, these forward-looking statements are subject to significant risks and uncertainties.

The forward-looking statements in this prospectus include, without limitation, statementsrelating to:

Š future developments in the banking industry and our competitive environment in China;

Š our recently completed operational reforms, including our existing risk managementframework, our expectations regarding the effect of these reforms and our continuingefforts to enhance our risk management and internal controls;

Š our plans to continue to enhance our information technology capabilities and systems;

Š our plans to expand into new and high growth business areas and our product and servicedevelopment plans;

Š our business cooperation and relationship with our overseas strategic investors and theirability to assist our business development and corporate governance reforms;

Š the regulatory environment and general outlook for the banking industry in China;

Š the amount and nature of, and potential for, future development of our business;

Š our business strategy and plans to achieve this strategy; and

Š our dividend policy.