Indonesia Media

52

ed: CK / sa:MA, PY, CS Seizing the opportunity Current share price has yet to price in potential upside from higher advertising expenditure (adex) growth We forecast 10% adex growth in FY18F from potential consumption pick-up in pre-election year, and two major sporting events (World Cup and Asian Games) Initiate Indonesia Media Sector with OVERWEIGHT We prefer SCMA as a potential beneficiary of adex recovery, while MNCN is our second pick for its cheap valuation Laggard sector with potential upside. The Indonesian media sector has notably underperformed the JCI in FY17 on the back of muted advertising spending (ad spend) by FMCG companies due to political uncertainties and stagnant private consumption. We think that the current share price level has not priced in the potential higher adex growth in FY18F due to (i) potential pick-up in household consumption in a pre-election year which would help boost advertising spending (ad spend), and (ii) two major sporting events that would boost adex growth. Currently, both SCMA and MNCN are trading at - 1SD/-2SD of their historical 8-year average), which provides a good entry point in the event of a pick-up in adex growth. Election year is coming. Two major election events will take place in June 2018 and April 2019, i.e. the regional PILKADA and Presidential elections respectively. We think that both events will help boost private household consumption. In the past, household expenditure has increased by 300-400bps in the year prior to Indonesian elections. This is because the government needs to deliver economic growth to increase the electability of the incumbent or ruling party. The pre-election consumption boost will also bode well for consumer stocks; which will directly translate into a better performance for media companies from higher advertising spending by FMCG companies. SCMA is our top pick in the sector. Even though we have BUY calls on SCMA and MNCN, we prefer the former to the latter. Under our base-case scenario of higher adex growth for this year at 10%, we believe that SCMA is better positioned to monetise higher adex growth due to its improvement in audience share (in prime time (PT) and all time (AT)). Furthermore, SCMA will also broadcast the Asian Games which would enable it to have a high audience share number and additional revenue streams from sponsorships. JCI : 5,821.81 Analyst David Arie Hartono +62 2130034936 [email protected] Surya Citra Media : Surya Citra Media (SCMA) focusses on national free to air (FTA) TV broadcasting. Through its station SCTV and Indosiar. SCMA controls c. 31.0% of Indonesia's FTA TV audience shares (all time) as of April 2018 and ranked first on the metric. Media Nusantara Citra : Media Nusantara Citra (MNCN) is one of South East Asia's largest and most integrated media companies, controlled by media mogul, Hary Tanoesoedibjo, with a focus on national free to air (FTA) television broadcasting. MNCN controlled 32.8% of all time MNCN and SCMA share price movement Source: Bloomberg Finance L.P. 0 1,000 2,000 3,000 4,000 5,000 2/1/2013 5/1/2013 8/1/2013 11/1/2013 2/1/2014 5/1/2014 8/1/2014 11/1/2014 2/1/2015 5/1/2015 8/1/2015 11/1/2015 2/1/2016 5/1/2016 8/1/2016 11/1/2016 2/1/2017 5/1/2017 8/1/2017 11/1/2017 2/1/2018 5/1/2018 MNCN SCMA 25 Jun 2018 Indonesia Industry Focus Indonesia Media Refer to important disclosures at the end of this report STOCKS 12-mth Price Mkt Cap Target Price Performance (%) Rp US$m Rp 3 mth 12 mth Rating Surya Citra Media 2,100 2,181 2,600 (22.5) (19.2) BUY Media Nusantara 975 954 1,300 (28.6) (48.6) BUY Source: DBSVI, Bloomberg Finance L.P. Closing price as of 22 Jun 2018

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Indonesia Media

ed: CK / sa:MA, PY, CS

Seizing the opportunity

Current share price has yet to price in potential upside from higher advertising expenditure (adex) growth

We forecast 10% adex growth in FY18F from potential consumption pick-up in pre-election year, and two major sporting events (World Cup and Asian Games)

Initiate Indonesia Media Sector with OVERWEIGHT

We prefer SCMA as a potential beneficiary of adex recovery, while MNCN is our second pick for its cheap valuation

Laggard sector with potential upside. The Indonesian media sector has notably underperformed the JCI in FY17 on the back of muted advertising spending (ad spend) by FMCG companies due to political uncertainties and stagnant private consumption. We think that the current share price level has not priced in the potential higher adex growth in FY18F due to (i) potential pick-up in household consumption in a pre-election year which would help boost advertising spending (ad spend), and (ii) two major sporting events that would boost adex growth. Currently, both SCMA and MNCN are trading at -1SD/-2SD of their historical 8-year average), which provides a good entry point in the event of a pick-up in adex growth. Election year is coming. Two major election events will take place in June 2018 and April 2019, i.e. the regional PILKADA and Presidential elections respectively. We think that both events will help boost private household consumption. In the past, household expenditure has increased by 300-400bps in the year prior to Indonesian elections. This is because the government needs to deliver economic growth to increase the electability of the incumbent or ruling party. The pre-election consumption boost will also bode well for consumer stocks; which will directly translate into a better performance for media companies from higher advertising spending by FMCG companies. SCMA is our top pick in the sector. Even though we have BUY calls on SCMA and MNCN, we prefer the former to the latter. Under our base-case scenario of higher adex growth for this year at 10%, we believe that SCMA is better positioned to monetise higher adex growth due to its improvement in audience share (in prime time (PT) and all time (AT)). Furthermore, SCMA will also broadcast the Asian Games which would enable it to have a high audience share number and additional revenue streams from sponsorships.

JCI : 5,821.81

Analyst David Arie Hartono +62 2130034936 [email protected]

Surya Citra Media : Surya Citra Media (SCMA) focusses on national free to air (FTA) TV broadcasting. Through its station SCTV and Indosiar. SCMA controls c. 31.0% of Indonesia's FTA TV audience shares (all time) as of April 2018 and ranked first on the metric.

Media Nusantara Citra : Media Nusantara Citra (MNCN) is one of South East Asia's largest and most integrated media companies, controlled by media mogul, Hary Tanoesoedibjo, with a focus on national free to air (FTA) television broadcasting. MNCN controlled 32.8% of all time

MNCN and SCMA share price movement

Source: Bloomberg Finance L.P.

0

1,000

2,000

3,000

4,000

5,000

2/1

/20

13

5/1

/20

13

8/1

/20

13

11

/1/2

01

3

2/1

/20

14

5/1

/20

14

8/1

/20

14

11

/1/2

01

4

2/1

/20

15

5/1

/20

15

8/1

/20

15

11

/1/2

01

5

2/1

/20

16

5/1

/20

16

8/1

/20

16

11

/1/2

01

6

2/1

/20

17

5/1

/20

17

8/1

/20

17

11

/1/2

01

7

2/1

/20

18

5/1

/20

18

MNCN SCMA

25 Jun 2018

Indonesia Industry Focus

Indonesia Media

Refer to important disclosures at the end of this report

STOCKS

12-mth

Price Mkt Cap Target Price Performance (%)

Rp US$m Rp 3 mth 12 mth Rating

Surya Citra Media 2,100 2,181 2,600 (22.5) (19.2) BUY Media Nusantara 975 954 1,300 (28.6) (48.6) BUY

Source: DBSVI, Bloomberg Finance L.P. Closing price as of 22 Jun 2018

Industry Focus

Indonesia Media

Page 2

Table of Contents

Investment Thesis 3

Advertising revenue is positively correlated with economic conditions 5

Growth is driven by FMCG advertising budget, and audience share which 6

Special events to support adex growth in FY18F 11

Company Guide – Initiation 13

Surya Citra Media 14

Media Nusantara Citra 31

Industry Focus

Indonesia Media

Page 3

Investment Thesis

We initiate the media sector with an Overweight call, and we prefer Surya Citra Media (SCMA) to Media Nusantara Citra (MNCN). Our Overweight call on the sector is premised on the following:

- We expect a recovery in advertising expenditure (adex) growth in FY18F. We estimate a 10% adex growth in FY18F which is based on (i) rate card improvement, (ii) potential higher advertising spending by FMCG companies and also technology companies, and (iii) two major sports events this year which could boost adex this year

- The sector has been underperformed the JCI in FY17 due to weak adex growth. But we think that the current share prices of SCMA and MNCN have only priced in adex growth of 4-5% and the market has yet to really price in the potential recovery of adex growth

- The media sector’s PE is now at a huge discount to consumer names – higher than the historical average discount

- Undemanding valuations – As SCMA/MNCN are trading at -1SD/-2SD of their 8-year means at the moment, we believe that their valuations are attractive

Laggard sector, with potential recovery in FY18F. Total adex growth in Indonesia decelerated to 8% y-o-y (bringing adex value to Rp145.5tr) in FY17 vs. 14% y-o-y in the previous year. The softer adex growth was due to: (i) stagnant private consumption which resulted in a decrease in the sales volume of FMCG companies and thus prompting FMCG companies cut their adex budget in 2017, and (ii) political instability in 2H17. Total advertising spending on TV and print (Rptr)

Source: Nielsen Note: Commercial product ad spending on TV and print based on gross rate card (does not include discount, promo, and bonus)

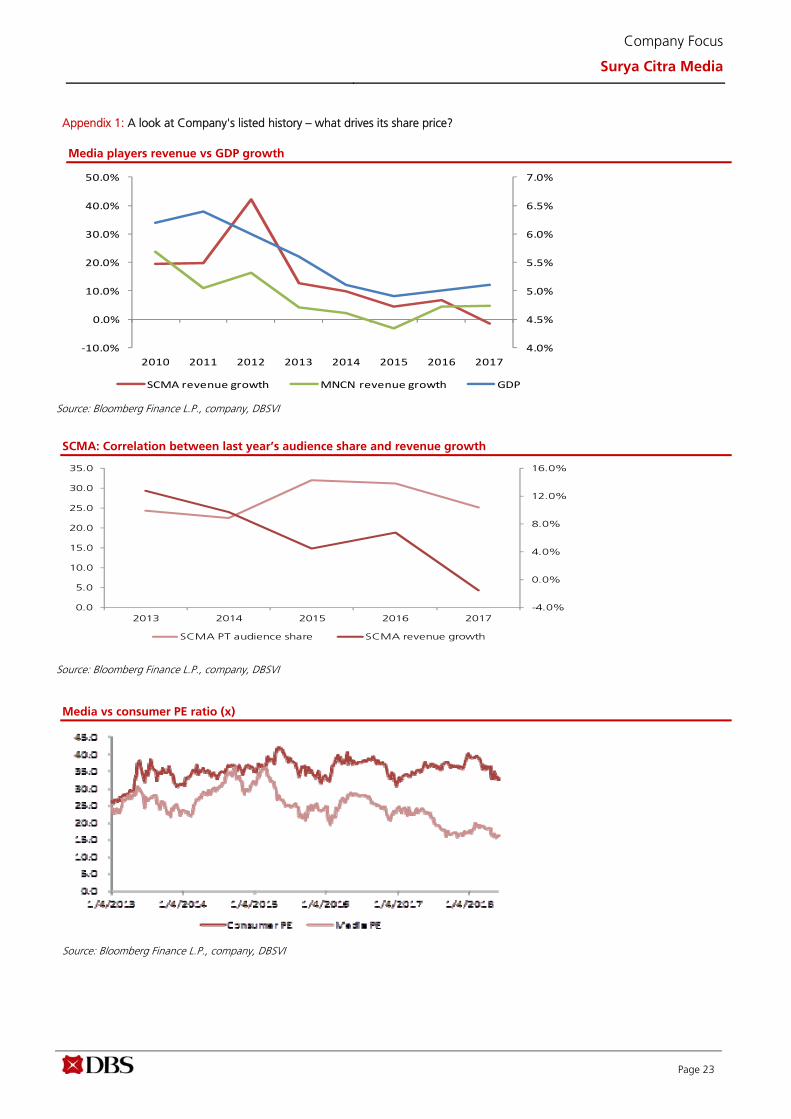

As the media sector is at a discount to consumer names, expect the discount to narrow on the back of potential adex recovery. The underperformance was due to company-specific problems. SCMA’s underperformance can be attributed to (i) weak topline performance due to soft audience share numbers in FY17, (ii) higher cost of programming from the acquisition of a production house, Sinemart in early FY17 – which resulted in a weaker EBITDA margin, and (iii) weak net income in FY17. Meanwhile, MNCN’s underperformance was due to (i) the fact that higher audience share number did not translate into a very strong topline growth in FY17, and (ii) some overhangs arising from debt refinancing at the parent level. Thus, currently the media stock is trading at a 37% discount to consumer PE multiple (the historical 3-year mean discount is at 28%). Media vs consumer PE ratio (x)

Source: Bloomberg Finance L.P.

Note: Media companies average only include MNCN and SCMA Consumer companies are UNVR, INDF, ICBP, MYOR, KLBF, HMSP, GGRM

101.7 109.8

118.0

134.8 145.5

8.0%7.5%

14.2%

7.9%

0%

2%

4%

6%

8%

10%

12%

14%

16%

-

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

2013 2014 2015 2016 2017

Advertising spending (Rptn) y-o-y growth (%)

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

2/1/20

13

7/1/20

13

12/1/201

3

5/1/20

14

10/1/201

4

3/1/20

15

8/1/20

15

1/1/20

16

6/1/20

16

11/1/201

6

4/1/20

17

9/1/20

17

2/1/20

18

Media PE Consumer PE

Industry Focus

Indonesia Media

Page 4

Relative PE between media and consumer is currently trading at -1SD. Revenue for most Indonesian media companies is highly correlated to spending on advertising and promotion by FMCG (more than 70%). We believe that the investors could view media stocks as a cheaper play on an improving domestic consumption story than consumer names. Relative PE between media and consumer sectors are currently trading at -1SD below the historical 3-year mean of 0.72x. With our positive view on TV adex growth, we believe that current valuations offer an attractive entry point into the media sector. Media PE relative to consumer PE

Source: Bloomberg Finance L.P.

Undemanding valuations, especially if adex rebounds. Trading at -1SD and -2SD or below relative to the historical level, we believe that SCMA and MNCN’s valuations are attractive, especially if advertising spending recovers. We think at the current share price levels for SCMA and MNCN, the market is pricing at 4-5% TV adex growth in FY18F (vs. our estimate of 10%). We believe that both stocks offer an attractive risk-reward profile at current valuations. Thus, we initiate the media sector with an Overweight call, and BUY calls on SCMA and MNCN. Even though we have BUY calls on SCMA and MNCN, we prefer the former to the latter. Under our base-case scenario of higher adex growth for this year at 10%, we believe that SCMA is better positioned to monetise higher adex growth due to its improvement in audience share (in prime time (PT) and all time (AT)). Furthermore, SCMA will also broadcast the Asian Games which would enable it to have a high audience share number and additional revenue streams from sponsorships. Meanwhile, we think that MNCN will see a slower multiple expansion, as it is facing weaker audience share in YTD 2018.

Peers comparison

Source: Bloomberg Finance L.P., and DBSVI

0.40

0.50

0.60

0.70

0.80

0.90

1.00

PE Average +1SDEV -1SDEV +2SDEV -2SDEV

FY2017 FY2018 FY2019 FY2017 FY2018 FY2019 FY2017 FY2018 FY2019 FY2017 FY2018 FY2019 FY2017 FY2018 FY2019

Indonesia Media

Surya Citra Media SCMA IJ EQUITY 24.4x 21.9x 19.8x 16.6x 14.8x 13.1x 91.1 101.5 112.2 266.81 317.62 372.48 8.3x 7.0x 6.0x

Media Nusantara Citra MNCN IJ EQUITY 10.5x 9.4x 7.9x 6.1x 5.6x 4.8x 101.8 113.5 135.2 632.15 703.57 793.34 1.7x 1.5x 1.3x

Regional Media

BEC World PCL BEC TB Equity nm nm 77.0x nm 15.1x 7.4x (0.6) (0.0) 0.0 0.69 0.67 0.67 0.7x 0.8x 0.8x

Astro Malaysia ASTRO MK EQUITY 13.9x 11.3x 13.4x 7.0x 7.8x 6.7x 0.1 0.1 0.1 0.12 0.13 0.15 13.9x 13.3x 11.5x

Media Prima MPR MK Equity nm nm 77.0x nm 15.1x 7.4x (0.6) (0.0) 0.0 0.69 0.67 0.67 0.7x 0.8x 0.8x

Sun TV SUNTV IN Equity nm nm 77.0x nm 15.1x 7.4x (0.6) (0.0) 0.0 0.69 0.67 0.67 0.7x 0.8x 0.8x

TV18 TV18 IN Equity nm nm 77.0x nm 15.1x 7.4x (0.6) (0.0) 0.0 0.69 0.67 0.67 0.7x 0.8x 0.8x

Indonesia Consumer

Unilever Indonesia UNVR IJ EQUITY 48.2x 43.1x 39.2x 33.8x 30.1x 27.4x 918.0 1,027.0 1,129.9 678.03 787.02 889.95 65.3x 56.3x 49.8x

Indofood Sukses Makmur INDF IJ EQUITY 14.1x 13.5x 12.7x 7.4x 7.1x 6.9x 474.7 497.4 528.4 3,550.95 3,810.93 4,075.13 1.9x 1.8x 1.6x

Indofood CBP Sukses Makmur ICBP IJ Equity 26.4x 22.7x 20.6x 15.6x 13.8x 12.4x 325.6 378.1 418.2 1,677.57 1,892.89 2,122.05 5.1x 4.5x 4.1x

Mayora Indah MYOR IJ EQUITY 50.2x 42.5x 37.0x 25.2x 22.1x 19.6x 59.2 69.8 80.3 311.95 360.83 417.06 9.8x 8.5x 7.3x

Kalbe Farma KLBF IJ EQUITY 25.5x 23.1x 20.9x 16.2x 14.7x 13.1x 51.6 56.8 63.0 287.90 319.14 353.81 4.6x 4.1x 3.7x

Indonesia Retail

Ace Hardware Indonesia ACES IJ EQUITY 33.0x 32.8x 32.5x 21.6x 21.0x 20.6x 39.1 39.3 39.7 211.84 239.01 266.47 6.1x 5.4x 4.8x

Matahari Department Store LPPF IJ EQUITY 13.5x 12.4x 11.5x 9.1x 8.0x 7.1x 653.6 710.9 768.7 797.82 1,051.26 1,322.28 11.1x 8.4x 6.7x

Matahari Putra Prima MPPA IJ EQUITY nm 103.0x 43.3x nm 4.5x 3.5x (231.2) 2.6 6.3 218.32 272.08 278.36 1.2x 1.0x 1.0x

Ramayana Lestari RALS IJ EQUITY 24.4x 21.9x 19.8x 16.6x 14.8x 13.1x 91.1 101.5 112.2 266.81 317.62 372.48 8.3x 7.0x 6.0x

Price/ BVPS (X)P/E (X) EV/ EBITDA (X) EPS (Fully Diluted) BVPS

Industry Focus

Indonesia Media

Page 5

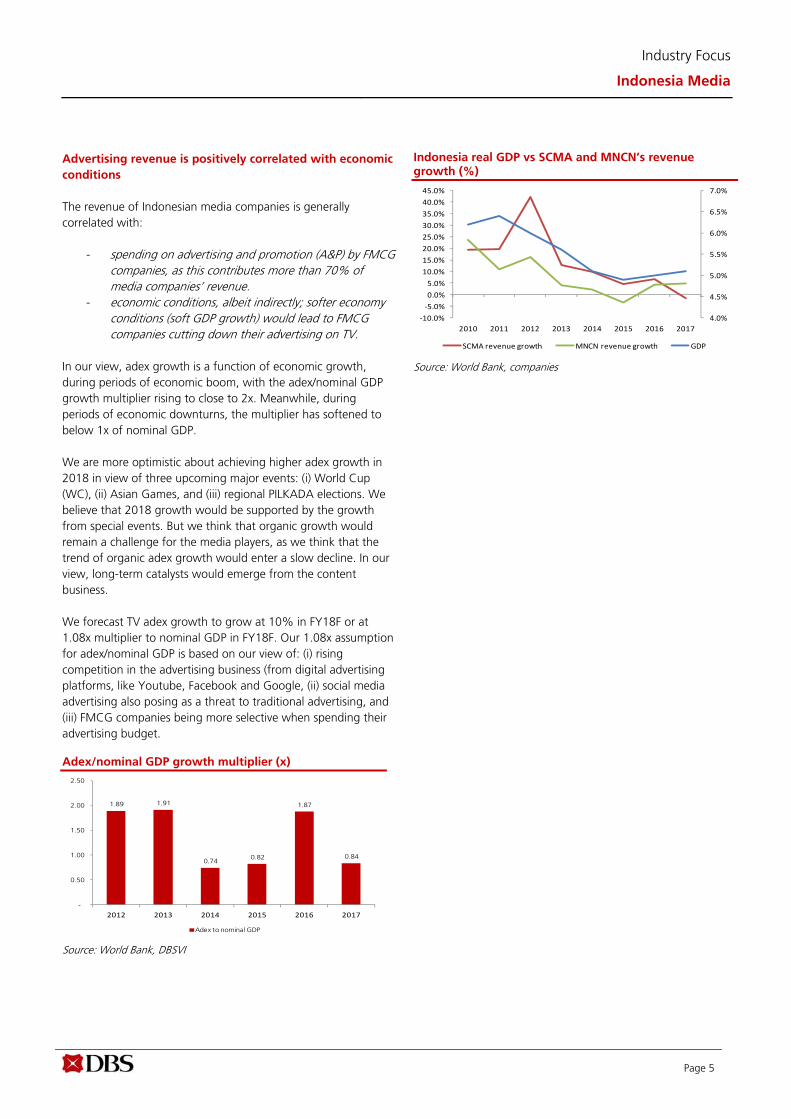

Advertising revenue is positively correlated with economic

conditions

The revenue of Indonesian media companies is generally correlated with:

- spending on advertising and promotion (A&P) by FMCG companies, as this contributes more than 70% of media companies’ revenue.

- economic conditions, albeit indirectly; softer economy conditions (soft GDP growth) would lead to FMCG companies cutting down their advertising on TV.

In our view, adex growth is a function of economic growth, during periods of economic boom, with the adex/nominal GDP growth multiplier rising to close to 2x. Meanwhile, during periods of economic downturns, the multiplier has softened to below 1x of nominal GDP. We are more optimistic about achieving higher adex growth in 2018 in view of three upcoming major events: (i) World Cup (WC), (ii) Asian Games, and (iii) regional PILKADA elections. We believe that 2018 growth would be supported by the growth from special events. But we think that organic growth would remain a challenge for the media players, as we think that the trend of organic adex growth would enter a slow decline. In our view, long-term catalysts would emerge from the content business. We forecast TV adex growth to grow at 10% in FY18F or at 1.08x multiplier to nominal GDP in FY18F. Our 1.08x assumption for adex/nominal GDP is based on our view of: (i) rising competition in the advertising business (from digital advertising platforms, like Youtube, Facebook and Google, (ii) social media advertising also posing as a threat to traditional advertising, and (iii) FMCG companies being more selective when spending their advertising budget. Adex/nominal GDP growth multiplier (x)

Source: World Bank, DBSVI

Indonesia real GDP vs SCMA and MNCN’s revenue growth (%)

Source: World Bank, companies

1.89 1.91

0.74 0.82

1.87

0.84

-

0.50

1.00

1.50

2.00

2.50

2012 2013 2014 2015 2016 2017

Adex to nominal GDP

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

‐10.0%

‐5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

2010 2011 2012 2013 2014 2015 2016 2017

SCMA revenue growth MNCN revenue growth GDP

Industry Focus

Indonesia Media

Page 6

TV still dominates ad spend. Based on MPA estimates, Indonesia has approximately 42m TV households (TVHHs) wherein ~80% have access to FTA. FTA channels are the most viewed on all platforms, with an estimated total TV audience share in excess of 90% Thus, FTA advertising remains strong with a total advertising market share of ~60%, dominated primarily by popular local content, such as dramas and sinetrons. FTA advertising is projected to grow to US$1.5bn at a CAGR of 3.1% over 2017-2022. MPA estimates Internet advertising to post growth of up to 35% in 2017. This specific media platform has shown a remarkably steep growth curve, driven primarily by online videos as well as the surging popularity of e-commerce and digital services. Among online video platforms, YouTube still dominates despite last year’s launch of several legal video platforms and sites offering ads-supported videos. Internet advertising is expected to expand from US$368m to US$848m over a five-year period starting 2017. Indonesia advertising share by media (2017)

Source: Media Partner Asia Indonesia advertising share by media (2022F)

Source: Media Partner Asia

Growth is driven by (i) FMCG advertising budget, and (ii)

audience share which translates into higher rate card

FMCG companies’ advertising spending will be higher in FY18F, thus supporting the growth. The market will likely regain some confidence in 2018, as major advertisers have indicated their intention to increase their total budgets for TV advertising spending in 2018 by up to 7-8%. Based on the 1Q18 data for consumer and cigarette companies’ advertising and promotion expenses, we gather that Unilever, Mayora, and Indofood have increased their advertising spending budget. On the other hand, tobacco players have not increased their advertising spending budget for this year. We noticed that cigarette companies have allocated more advertising spending to music events. However, we expect an increase in their advertising spending in 2H18 due to the World Cup and Asian Games events. Quarterly consumer advertising spending (Rpbn)

Source: companies Quarterly cigarette advertising spending (Rpbn)

Source: companies Technology companies will continue to rely on TV advertising. Technology companies are still trying to establish a foothold in the Indonesian market and are now advertising heavily on

61.1%17.5%

18.0%

1.8% 1.2% 0.4%

TV Internet Print OOH Radio Cinema

54.1%30.7%

12.3%

1.6% 1.0% 0.3%

TV Internet Print OOH Radio Cinema

‐200.0

0.0

200.0

400.0

600.0

800.0

1,000.0

1,200.0

1,400.0

UNVR INDF ICBP KLBF MYOR

1Q17 2Q17 3Q17 4Q17 1Q18

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

900.0

1,000.0

GGRM HMSP RMBA

1Q17 2Q17 3Q17 4Q17 1Q18

Industry Focus

Indonesia Media

Page 7

traditional media, like TV. Based on the data from Nielsen, technology companies consistently rank among the top 10 advertisers on the main TV channels. Top 10 product adex (Rpbn)

Source: Nielsen Audience share is key for rate card improvement. For FMCG companies that would like to advertise their products on TV stations, they would like to see high and stable audience share numbers. A higher audience share number means that the probability of their products become well-known would be higher. The audience share is calculated by dividing the average number of audience by total TV audience share. The average rate card in the Indonesian media industry stands at US$5,000/30seconds and it could go higher, subject to the audience share number. MNCN regained its pole position in May 2018 audience share number. Based on Nielsen data for May audience share numbers, MNCN has successfully won back its first position in all time (AT) audience share by 32.8% (+2.1ppts m-o-m), and prime time (PT) audience share by 33.9% (+1.7ppts m-o-m). We think the increase of audience share in May 2018 was due to its strong Ramadhan programme line-up. RCTI has secured a leading audience share (23.7%) in Suhoor prime time between 2am and 6am. In the Ramadhan festive period, there were other prime time slots being allocated in the morning; while under normal circumstances, these will be considered as non-prime time slots. VIVA group occupies the third position with 19.7% share (+0.2ppt m-o-m) of prime time (PT) and 21.3% share (+0.9ppt m-o-m) of all time (AT) as of May 2018.

Prime time (PT) audience share as of May 2018 per TV station

Source: Nielsen

Prime time (PT) audience share as of May 2018 per group

Source: NIelsen

All time (AT) audience share as of May 2018 per TV station

Source: NIelsen

RCT I SCTV IV M T RA NS MNCTV T RA NS7 GTV A NTV TV ONE METRO TV RM

Jan-17 26.9 11.4 12.5 6.9 10.1 6.0 4.6 14.7 3.5 2.0 1.1Feb-17 24.9 16.0 13.7 5.2 7.9 5.9 5.2 14.2 3.4 2.1 1.1Mar-17 23.8 22.9 11.2 5.6 7.6 5.6 5.3 12.1 2.8 1.8 1.1Apr-17 21.7 21.4 12.6 4.6 8.7 6.1 7.3 9.5 4.9 1.9 1.0May-17 23.0 17.9 12.4 4.4 9.2 6.8 6.8 9.6 6.5 2.1 0.9Jun-17 24.0 15.9 9.9 4.1 9.4 5.7 7.7 14.4 5.9 1.8 0.9Jul-17 20.9 14.5 13.4 4.7 10.7 5.3 5.4 16.9 5.7 1.5 0.7Aug-17 21.6 14.5 12.2 3.9 10.4 6.5 5.8 16.0 6.0 1.7 1.2Sep-17 20.6 12.7 12.7 4.0 12.7 6.8 5.2 16.0 6.5 1.6 0.9Oct-17 19.2 13.2 12.3 4.6 11.4 6.5 5.6 18.6 6.1 1.4 0.9Nov-17 18.6 16.1 14.0 4.8 9.2 7.3 4.8 17.0 5.4 1.4 1.0Dec-17 16.8 18.8 17.6 5.2 9.3 6.3 5.2 15.0 3.4 1.3 0.9Jan-18 15.3 20.4 15.6 4.4 11.3 5.3 6.5 16.3 2.6 1.2 0.8Feb-18 14.5 20.5 15.0 4.6 11.2 5.5 7.4 16.3 2.8 1.2 0.7Mar-18 15.6 20.2 14.1 4.7 10.3 5.9 7.3 17.2 2.5 1.1 0.7Apr-18 15.2 21.0 14.2 5.6 9.8 5.4 7.2 16.9 2.6 1.1 0.7May-18 16.4 17.9 15.1 4.6 10.8 6.1 6.7 16.8 2.9 1.4 1.1

MNCN SCMA TRA NS V IV A

Jan-17 41.6 23.9 12.9 18.2

Feb-17 38.0 29.7 11.1 17.6Mar-17 36.7 34.1 11.2 14.9

Apr-17 37.7 34.0 10.7 14.4May-17 39.0 30.3 11.2 16.1

Jun-17 41.1 25.8 9.8 20.3Jul-17 37.0 27.9 10.0 22.6

Aug-17 37.8 26.7 10.4 22.0Sep-17 38.5 25.4 10.8 22.5

Oct-17 36.2 25.5 11.1 24.7Nov-17 32.6 30.1 12.1 22.4

Dec-17 31.3 36.4 11.5 18.4Jan-18 33.1 36.0 9.7 18.9

Feb-18 33.1 35.5 10.1 19.1Mar-18 33.2 34.3 10.6 19.7

Apr-18 32.2 35.2 11.0 19.5May-18 33.9 33.0 10.7 19.7

R C TI SC TV IV M TR A N S M N C T V T R A N S7 GTV A N TV T V ON E M ET R O TV R I1 LocalT V

Jan-17 19.3 12.6 11.4 6.9 11.2 7.1 5.0 19.4 3.7 2.0 1.2 0.2Feb-17 17.8 14.6 12.7 6.3 9.6 7.1 5.2 19.4 3.7 2.2 1.2 0.2Mar-17 17.2 18.1 11.0 6.7 10.3 7.6 5.7 16.9 3.3 1.8 1.2 0.2Apr-17 16.4 17.4 12.4 6.6 10.6 8.0 6.5 14.5 4.3 2.0 1.0 0.3May-17 17.7 16.0 12.1 6.2 11.1 8.4 6.7 13.4 4.9 2.1 1.1 0.3Jun-17 18.9 14.5 11.0 5.6 10.9 7.5 7.1 17.5 4.0 1.7 1.0 0.3Jul-17 16.2 13.3 13.6 6.5 12.0 7.6 5.5 17.9 4.5 1.6 0.9 0.1Aug-17 16.6 13.2 13.5 5.9 11.4 7.9 5.6 17.6 5.2 1.8 1.2 0.1Sep-17 15.7 12.6 15.0 6.2 12.4 8.2 5.3 16.3 5.5 1.7 1.1 0.0Oct-17 15.3 13.1 14.9 6.8 11.4 7.9 5.4 17.2 5.2 1.5 1.0 0.3Nov-17 15.3 13.9 15.2 7.0 10.4 8.5 5.2 16.7 4.9 1.6 1.0 0.9Dec-17 14.5 15.5 16.3 7.1 10.3 7.3 6.7 16.2 3.6 1.4 0.9 0.2Jan-18 13.1 17.2 15.6 6.6 11.5 6.6 7.3 16.8 2.9 1.3 0.9 0.2Feb-18 12.1 17.5 15.2 6.7 11.6 6.6 8.1 16.7 3.1 1.3 0.8 0.3Mar-18 12.7 17.8 14.6 6.5 10.7 6.7 7.7 18.5 2.7 1.1 0.8 0.2Apr-18 13.0 18.7 14.7 7.0 10.0 6.4 7.7 17.5 2.9 1.2 0.8 0.1May-18 15.1 16.5 14.5 6.1 10.3 6.2 7.4 18.1 3.2 1.4 1.1 0.1

Top 10 product TV and print Adex 2017 Adex 2016Meikarta 1,539.5 -Trave loka.com 1,136.7 65%Indomie 981.5 25%Vivo s martphone 823.5 577%Clear shampoo 795.5 40%SGM exksplor 769.9 38%Kementrian Kesehatan 702.2 23%Sams ung s martphone 640.0 28%Dove 610.3 788%Cap bango 589.7 36%

Industry Focus

Indonesia Media

Page 8

All time (AT) audience share as of May 2018 per group

Source: NIelsen

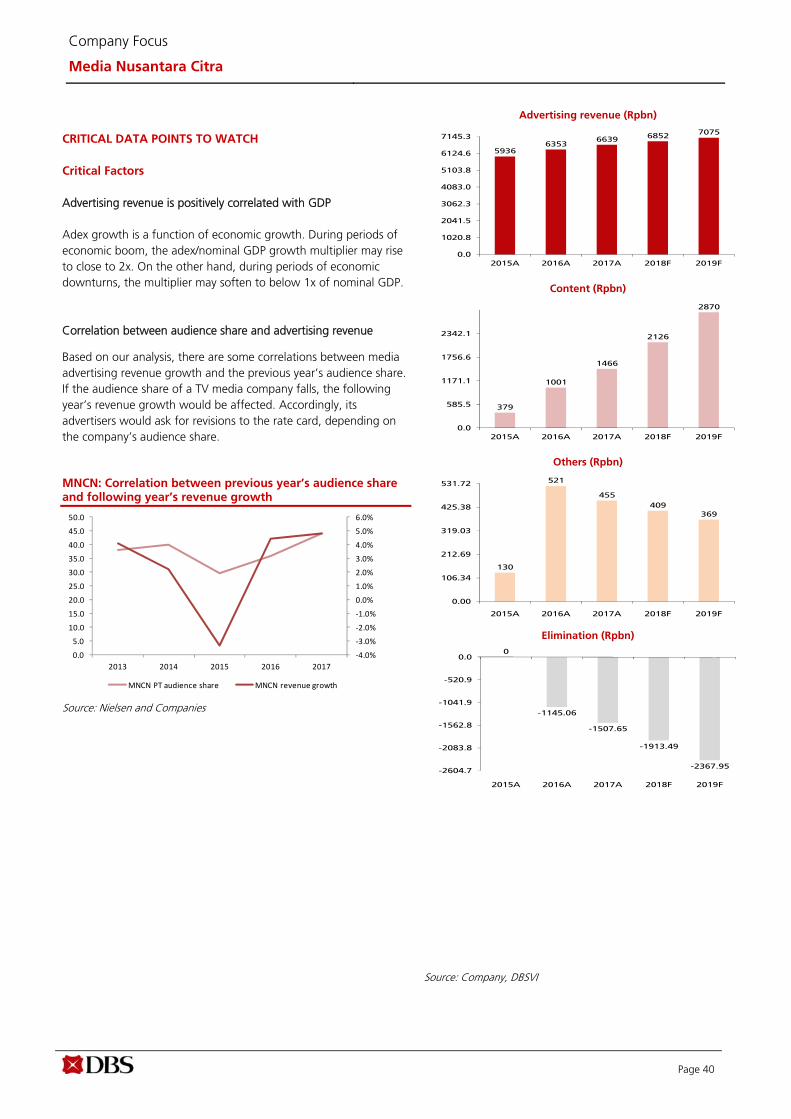

Correlation between audience share and advertising revenue of each TV player. Based on our analysis, we gather that there is some correlation between media advertising revenue growth and last year’s audience share number. This indicates that, if the audience share of one TV media company fell – it would have an impact on next year’s revenue growth. We believe that the advertisers will ask for adjustments in the rate card, depending on the audience share.

SCMA: Correlation between last year’s audience share and revenue growth

Source: Nielsen, companies

MNCN: Correlation between last year’s audience share and revenue growth

Source: Nielsen, companies

MNCN SCMA TRA NS V IV AJan-17 35.5 24.0 14.0 23.1Feb-17 32.6 27.3 13.4 23.1Mar-17 33.2 29.1 14.3 20.2Apr-17 33.5 29.8 14.6 18.8May-17 35.5 28.1 14.6 18.3Jun-17 36.9 25.5 13.1 21.5Jul-17 33.7 26.9 14.1 22.4Aug-17 33.6 26.7 13.8 22.8Sep-17 33.4 27.6 14.4 21.8Oct-17 32.1 28.0 14.7 22.4Nov-17 30.9 29.1 15.5 21.6Dec-17 31.5 31.8 14.4 19.8Jan-18 31.9 32.8 13.2 19.7Feb-18 31.8 32.7 13.3 19.8Mar-18 31.1 32.4 13.2 21.2Apr-18 30.7 33.4 13.4 20.4May-18 32.8 31.0 12.3 21.3

‐4.0%

‐2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2013 2014 2015 2016 2017

SCMA PT audience share SCMA revenue growth

‐4.0%

‐3.0%

‐2.0%

‐1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

2013 2014 2015 2016 2017

MNCN PT audience share MNCN revenue growth

Industry Focus

Indonesia Media

Page 9

Who are the players in Indonesia’s media industry? There are some groups that owned a number of national free to air TV stations in Indonesia:

- MNC Group, which is owned by Hary Tanoesoedibjo, has three national TV stations (RCTI, MNCTV, and GTV) and regional TV stations under i-News TV

- Emtek Group, which is owned by Eddy Sariaatmadja, has two national TV stations (SCTV and Indosiar)

- VIVA Group, which is owned by Bakrie group, has two national TV stations (ANTV and TV One)

- Trans Group, which is owned by Chairul Tanjung, has two national TV stations (Trans TV and Trans 7)

- Media Group, which is owned by Surya Paloh, has one TV station (Metro TV)

- Government of Indonesia also owns one national TV station (TVRI)

Indonesia’s TV stations

Source: company

Owner Group TV stat ion

Wishnutama and A gus Lasmono

Indika Group

Gov ernment of Indonesia

Gov ernment of Indonesia

Rajawali Corpora Rajawali Corpora

Chairul Tanjung T rans Group

Sury a Paloh Media Group

Kompas Gramedia Kompas Gramedia

Hary Tanoesoedibjo MNC Group

Eddy Sariaatmadja Emtek Group

Bak rie Group Bak rie Group

Industry Focus

Indonesia Media

Page 10

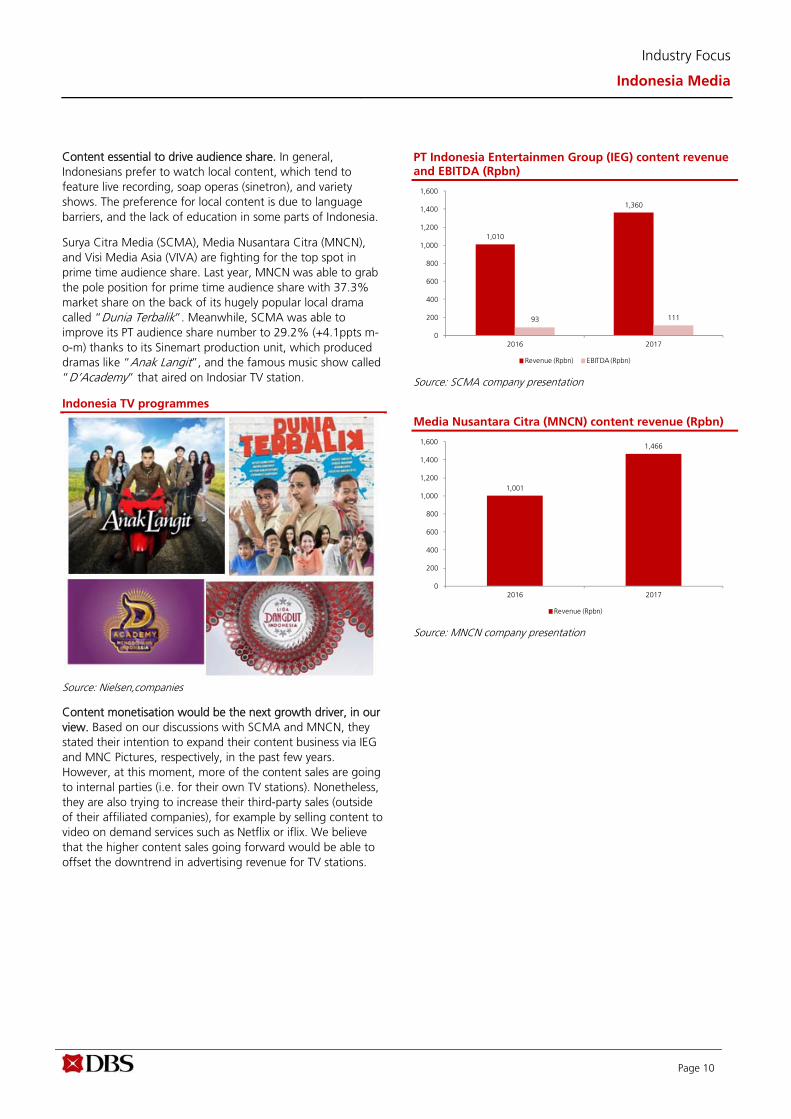

Content essential to drive audience share. In general, Indonesians prefer to watch local content, which tend to feature live recording, soap operas (sinetron), and variety shows. The preference for local content is due to language barriers, and the lack of education in some parts of Indonesia.

Surya Citra Media (SCMA), Media Nusantara Citra (MNCN), and Visi Media Asia (VIVA) are fighting for the top spot in prime time audience share. Last year, MNCN was able to grab the pole position for prime time audience share with 37.3% market share on the back of its hugely popular local drama called “Dunia Terbalik”. Meanwhile, SCMA was able to improve its PT audience share number to 29.2% (+4.1ppts m-o-m) thanks to its Sinemart production unit, which produced dramas like “Anak Langit”, and the famous music show called “D’Academy” that aired on Indosiar TV station.

Indonesia TV programmes

Source: Nielsen,companies

Content monetisation would be the next growth driver, in our view. Based on our discussions with SCMA and MNCN, they stated their intention to expand their content business via IEG and MNC Pictures, respectively, in the past few years. However, at this moment, more of the content sales are going to internal parties (i.e. for their own TV stations). Nonetheless, they are also trying to increase their third-party sales (outside of their affiliated companies), for example by selling content to video on demand services such as Netflix or iflix. We believe that the higher content sales going forward would be able to offset the downtrend in advertising revenue for TV stations.

PT Indonesia Entertainmen Group (IEG) content revenue and EBITDA (Rpbn)

Source: SCMA company presentation

Media Nusantara Citra (MNCN) content revenue (Rpbn)

Source: MNCN company presentation

1,010

1,360

93 111

0

200

400

600

800

1,000

1,200

1,400

1,600

2016 2017

Revenue (Rpbn) EBITDA (Rpbn)

1,001

1,466

0

200

400

600

800

1,000

1,200

1,400

1,600

2016 2017

Revenue (Rpbn)

Industry Focus

Indonesia Media

Page 11

Special events to support adex growth in FY18F Special events to support adex growth in FY18F. In 2018, there are a few major events that we believe could help boost the adex growth of media players. The events are: (i) World Cup (WC), and (ii) Asian Games. For WC, based on the past experience, cigarette, telecommunication, and health drink players will spend a substantial part of their advertising budgets on TV by sponsoring WC-related programmes. Top product category for TV advertisements during WC 2010

Source: Nielsen Top products that were advertised during WC 2010

Source: Nielsen About 3,000 spots were aired during WC. During WC events, audience share will typically surge and this will lead to media players increasing their rate card. Besides a higher rate card, we believe the TV programmes that are aired prior to WC games would benefit as well. If we assume that there are 3,000 available spots for WC events and a rate card of Rp70m/30seconds, we believe that WC could generate advertising revenue of at least Rp200bn over one month. With the World Cup being broadcasted by Trans Group, will this have an impact on SCMA and MNCN? Trans Group (privately owned) and the 4th largest TV group in Indonesia has secured the broadcast rights for WC 2018, which will start on 14 June 2018 and end on 15 July 2018. WC 2018 will be hosted in Russia (whose time zone is four hours ahead of Indonesia’s) and the matches will be broadcast at 7pm to 1am in Indonesia. We

believe it would directly compete with the prime time shows offered by SCMA and MNCN, and also VIVA. If we look back at the previous WC in 2014 that was broadcasted by the VIVA group, the event helped it gain at least 8% of audience share during that time (from a rough average share of 6% in the first five months of 2014 to 13%-15% during WC 2014). We think that the audience share of MNCN, SCMA, and VIVA will decline in June and July 2018, and Trans Group will benefit from improving audience share numbers. Will Trans Group be able to monetise the WC momentum to create some pressure on the Big 3? In our view, the strategy to broadcast WC 2018 would enable it to significantly improve its audience share numbers. But most importantly, there are also opportunities for TV programmes preceding WC 2018 matches to shine and grab the attention of a huge audience. If we look back at VIVA group via ANTV, prior to the screening of WC 2014 matches, its audience share in prime time (PT) slots was actually quite low. Post WC 2014, ANTV managed to successfully monetise its association with the event by clinching higher viewership for its drama series as well as improving its long-term audience share. ANTV’s audience share pre- and post-WC 2014

Source: Nielsen Regional PILKADA election in 2H18 and Presidential election next year will improve private consumption – leading to higher advertising spending by FMCG companies. We believe that two major election events will happen in June 2018 and April 2019. We are of the opinion that such events will help boost private household consumption. In the past, household expenditure has increased by 300-400bps in the year prior to Indonesian elections. This is because the government needs to deliver economic growth to increase the electability of the incumbent or ruling party. The pre-election consumption boost will also bode well for consumer stocks; which will directly translate into a better performance for media companies from higher advertising spending by FMCG companies.

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

World Cup 2014 boostANTV audience share

Pre World Cup 2014,the audience share was quite low

Post World Cup 2014, ANTV has been able to improve the audience share. Since the other programs also been sh ining and able to post a good audience share number up to now

Industry Focus

Indonesia Media

Page 12

Household expenditure growth (%)

Source: World Bank

3.2%

5.0%5.3%

4.9% 4.7%5.1%

5.5% 5.4%5.1% 5.0% 5.0% 4.9%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Household consumption

Industry Focus

Indonesia Media

Page 13

Company Initiations

ed: CK / MA, PY, CS

BUY (Initiating Coverage) Last Traded Price ( 22 Jun 2018): Rp2,100 (JCI : 5,821.81) Price Target 12-mth: Rp2,600 (24% upside) Potential Catalyst: Asian Games could further spur revenue growth this year, Ramadhan, and acceleration of Media adex to benefit SCMA Analyst David Arie Hartono +62 2130034936 [email protected]

Price Relative

Forecasts and Valuation FY Dec (Rpbn) 2016A 2017A 2018F 2019F Revenue 4,524 4,454 4,854 5,222 EBITDA 2,140 1,970 2,184 2,411 Pre-tax Profit 2,024 1,782 1,999 2,210 Net Profit 1,501 1,331 1,484 1,641 Net Pft (Pre Ex.) 1,501 1,331 1,484 1,641 EPS (Rp) 103 91.1 101 112 EPS Pre Ex. (Rp) 103 91.1 101 112 EPS Gth (%) (1) (11) 11 11 EPS Gth Pre Ex (%) (1) (11) 11 11 Diluted EPS (Rp) 103 91.1 101 112 Net DPS (Rp) 0.0 0.0 0.0 0.0 BV Per Share (Rp) 234 267 318 372 PE (X) 20.5 23.1 20.7 18.7 PE Pre Ex. (X) 20.5 23.1 20.7 18.7 P/Cash Flow (X) 22.2 24.6 20.2 18.1 EV/EBITDA (X) 14.3 15.7 13.9 12.4 Net Div Yield (%) 0.0 0.0 0.0 0.0 P/Book Value (X) 9.0 7.9 6.6 5.6 Net Debt/Equity (X) CASH CASH CASH CASH ROAE (%) 45.7 36.3 34.7 32.5 Consensus EPS (Rp): N/A N/A N/A Other Broker Recs: B: 13 S: 0 H: 3 ICB Industry : Consumer Services ICB Sector: Media Principal Business: Surya Citra Media (SCMA) focusses on national free to air (FTA) TV broadcasting. Through its station SCTV and Indosiar. SCMA controls c. 31.0% of Indonesia's FTA TV audience shares (all time) as of April 2018 and ranked first on the metric.

Source of all data on this page: Company, DBSVI, Bloomberg Finance L.P.

At A Glance Issued Capital (m shrs) 14,622

Mkt. Cap (Rpbn/US$m) 30,705 / 2,181

Major Shareholders (%)

PT Elang Mahkota Teknologi 60.83%

Free Float (%) 39.1%

3m Avg. Daily Val (US$m) 1.9

DBS Group Research . Equity 25 Jun 2018

Indonesia Company Focus

Surya Citra Media Bloomberg: SCMA IJ | Reuters: SCMA.IJ Refer to important disclosures at the end of this report

More exciting outlook Revenue growth driven by higher rate card due to audience

share improvement and Asian Games

The acquisition of another TV station would make SCMA the biggest TV station, thus boosting its revenue growth

Higher content sold to third parties would be the next growth catalyst

Initiate SCMA with BUY call and TP of Rp2,600/share

Promising outlook. We estimate SCMA to post 9% y-o-y growth in FY18F (vs. -1.6% y-o-y in FY17), due to (i) better ad spend outlook in FY18F, (ii) recovery in audience share, which translates into a higher rate card, and (iii) additional revenue streams from Asian Games events in August 2018. We assume earnings CAGR of 10.8% over FY17-20F on the back of higher gross margin of 59.8% in FY18F (vs. 58.6% in FY17).

Are M&As on the table? SCMA has received the approval for its rights issue of 1.46bn new shares at Rp2,446/share that will raise Rp3.6tr. The company plans to use the proceeds (currently unused) for working capital and business expansion. In our view, the proceeds could be used to expand its business by either (i) acquiring another TV station, or (ii) venturing into online/digital media platforms. The acquisition of another TV station would be positive for SCMA, thus making it the biggest TV player in Indonesia and boosting its revenue growth.

Where we differ. We are more conservative than consensus as we assume lower media industry adex of 10% in FY18F and as a result, our revenue growth is 5% below consensus. Furthermore, we assume a higher cost of programming, which will lead to a lower GPM. Thus, our FY18 earnings forecast is 14% below consensus. At the end of the day, we have a lower TP vs consensus. Valuation:

Our DCF-based TP of Rp2,600/share for SCMA assumes a WACC of 9% and terminal growth of 3%. Our TP implies 25.6x FY18F PE. Currently, the stock is trading at 17.9x FY18F PE, which is -1SD of its 8-year mean.

Key Risks to Our View:

Slower ad spend by FMCG companies, decline in audience share, competition from digital advertising, and digitalisation of transmission.

42

62

82

102

122

142

162

182

202

222

1,755.0

2,255.0

2,755.0

3,255.0

3,755.0

4,255.0

Jun-14 Jun-15 Jun-16 Jun-17 Jun-18

Relative IndexRp

Surya Citra Media (LHS) Relative JCI (RHS)

Page 15

Company Focus

Surya Citra Media

Table of Contents

SWOT analysis 16

Investment summary 17

Company background 19

Key management team 19

Competitive strengths 20

Growth strategies 20

Key risks 21

Critical data points to watch 22

Key assumption 25

Income statement 26

Quarterly/interim income statement 27

Balance sheet 28

Cash flow statement 29

Valuation 30

Page 16

Company Focus

Surya Citra Media

SWOT Analysis

Strengths Weakness

SCMA has solid prime time and non-prime time audience share numbers Strong production house Healthy balance sheet and minimum USD exposure Higher FCF vis-à-vis peers Has the highest net margin in the industry of 29.9% and ROE of 36.3% as of 2017

Highly dependent on FMCG companies (70% of revenue), since they contribute the bulk of the company’s revenue

Opportunities Threats

Potential higher revenue growth in FY18F from the Asian Games event, whose broadcasting licence is owned by SCTV Potential acquisition of another TV station. Such move would make SCMA the largest TV company in terms of audience share in Indonesia

Softer advertising spending (ad spend) by FMCG companies would impact its revenue growth Fierce competition in audience share will also pose a threat to the company Competition from digital advertising Switch to digital from analog

Source: DBSVI

Page 17

Company Focus

Surya Citra Media

Investment Summary Initiate coverage of SCMA with BUY call and TP of Rp2,600/share. Our optimism is based on the following:

- Improvement in SCTV audience share in YTD 2018, which enables the company to increase its rate card in FY18F

- Asian Games would give another boost to the company’s revenue stream in FY18F

- Indosiar’s audience share remains stable and at a high level, which we believe it would enable a higher sponsorship payment

- We estimate a stabilisation of SCMA’s margin in FY18F to 59.8%. In FY17, gross margin fell significantly to 58.6% due to higher cost of programming after acquiring SinemArt

- Healthy balance sheet with minimum USD exposure, and the company offers a good ROE of 34.7% in FY18F – which is the highest among the media industry

- SCMA is currently trading at 17.9x PE FY18F, -1SD of its historical 8-year mean of 21.2x. We believe that the current share price has priced in the bad news, coupled with the failure to reflect any potential upside

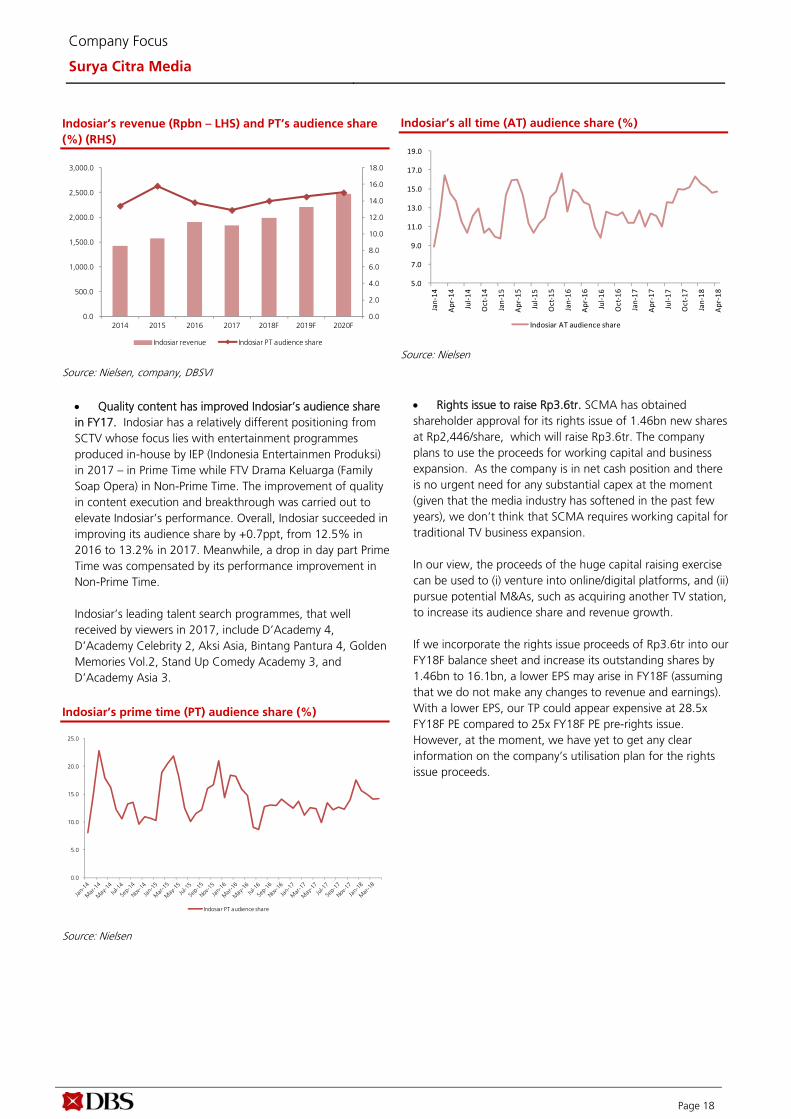

SCTV’s improvement in audience share to drive revenue growth in FY18F. In the past three years, SCTV has been under pressure to deliver a strong and stable audience share number, which resulted in soft revenue growth. However, we foresee that SCTV’s audience share has shown a recovery since end of 2017, and it has continued to improve up till April 2018. We believe the improvement in audience share would boost its rate card in FY18F. Furthermore, we also see additional revenue streams for SCTV from Asian Games, as SCTV owns the broadcasting licence for Asian Games. We estimate an additional revenue of at least Rp200bn (assuming 3,000 time slots available for Asian Games and a rate card between of Rp65m and Rp70m per 30seconds).

SCTV prime time (PT) audience share (%) (RHS) and SCTV

revenue (Rpbn) (LHS)

Source: Nielsen, company

Forecast SCTV revenue CAGR of 5% over FY17-20F. We assume that SCTV’s prime time audience share to remain in the range of 18.5-19.5% over FY18F-20F and assume 5% rate card improvement p.a. As a result, we assume revenue to grow at a CAGR of 5% over FY17-20F. This has already pencilled in softer advertising expenditure (adex) going forward due to more competition from digital advertising.

SCTV revenue (Rpbn – LHS) and PT audience share (% -

RHS)

Source: Nielsen, company, DBSVI Indosiar to continue delivering good growth. Indosiar has successfully transformed its programming since 2012, with the TV station now delivering good audience share numbers – thanks to its music shows like D’Academy. Indosiar’s revenue grew at a CAGR of 9% in FY14-17 due to the improvement in audience share number. We forecast 10% revenue CAGR over FY17-20F for Indosiar TV station on the back of potentially stable audience share numbers. Several new programmes have emerged to maintain its audience share number in FY18F, e.g. LIDA (Liga Dangdut Indonesia). The show has received more sponsorship revenue from FMCG companies but it entails higher programming costs.

Indosiar’s revenue (Rpbn – LHS) and PT’s audience share

(%) (RHS)

Source: Nielsen, company

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

2,540.0

2,560.0

2,580.0

2,600.0

2,620.0

2,640.0

2,660.0

2,680.0

2,700.0

2,720.0

2,740.0

2014 2015 2016 2017

SCTV revenue SCTV PT audience share

0.0

5.0

10.0

15.0

20.0

25.0

2,400.0

2,500.0

2,600.0

2,700.0

2,800.0

2,900.0

3,000.0

3,100.0

2014 2015 2016 2017 2018F 2019F 2020F

SCTV revenue SCTV PT audience share

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

0.0

200.0

400.0

600.0

800.0

1,000.0

1,200.0

1,400.0

1,600.0

1,800.0

2,000.0

2014 2015 2016 2017

Indosiar revenue Indosiar PT audience share

Page 18

Company Focus

Surya Citra Media

Indosiar’s revenue (Rpbn – LHS) and PT’s audience share

(%) (RHS)

Source: Nielsen, company, DBSVI Quality content has improved Indosiar’s audience share in FY17. Indosiar has a relatively different positioning from SCTV whose focus lies with entertainment programmes produced in-house by IEP (Indonesia Entertainmen Produksi) in 2017 – in Prime Time while FTV Drama Keluarga (Family Soap Opera) in Non-Prime Time. The improvement of quality in content execution and breakthrough was carried out to elevate Indosiar’s performance. Overall, Indosiar succeeded in improving its audience share by +0.7ppt, from 12.5% in 2016 to 13.2% in 2017. Meanwhile, a drop in day part Prime Time was compensated by its performance improvement in Non-Prime Time. Indosiar’s leading talent search programmes, that well received by viewers in 2017, include D’Academy 4, D’Academy Celebrity 2, Aksi Asia, Bintang Pantura 4, Golden Memories Vol.2, Stand Up Comedy Academy 3, and D’Academy Asia 3.

Indosiar’s prime time (PT) audience share (%)

Source: Nielsen

Indosiar’s all time (AT) audience share (%)

Source: Nielsen

Rights issue to raise Rp3.6tr. SCMA has obtained shareholder approval for its rights issue of 1.46bn new shares at Rp2,446/share, which will raise Rp3.6tr. The company plans to use the proceeds for working capital and business expansion. As the company is in net cash position and there is no urgent need for any substantial capex at the moment (given that the media industry has softened in the past few years), we don’t think that SCMA requires working capital for traditional TV business expansion.

In our view, the proceeds of the huge capital raising exercise can be used to (i) venture into online/digital platforms, and (ii) pursue potential M&As, such as acquiring another TV station, to increase its audience share and revenue growth. If we incorporate the rights issue proceeds of Rp3.6tr into our FY18F balance sheet and increase its outstanding shares by 1.46bn to 16.1bn, a lower EPS may arise in FY18F (assuming that we do not make any changes to revenue and earnings). With a lower EPS, our TP could appear expensive at 28.5x FY18F PE compared to 25x FY18F PE pre-rights issue. However, at the moment, we have yet to get any clear information on the company’s utilisation plan for the rights issue proceeds.

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

0.0

500.0

1,000.0

1,500.0

2,000.0

2,500.0

3,000.0

2014 2015 2016 2017 2018F 2019F 2020F

Indosiar revenue Indosiar PT audience share

0.0

5.0

10.0

15.0

20.0

25.0

Indosiar PT audience share

5.0

7.0

9.0

11.0

13.0

15.0

17.0

19.0

Jan‐14

Apr‐14

Jul‐14

Oct‐14

Jan‐15

Apr‐15

Jul‐15

Oct‐15

Jan‐16

Apr‐16

Jul‐16

Oct‐16

Jan‐17

Apr‐17

Jul‐17

Oct‐17

Jan‐18

Apr‐18

Indosiar AT audience share

Page 19

Company Focus

Surya Citra Media

Company Background

Corporate History. Surya Citra Media (SCMA) was established on 29 January 1999 to focus on national free to air (FTA) TV broadcasting. SCMA owns two national FTA TV stations, i.e. SCTV and Indosiar (IVM). SCTV commenced its commercial broadcast in 1990, covering the city of Surabaya, and began operating nationwide in 1993. In early 2013, PT Indosiar Karya Media Tbk merged into SCMA. And at the end

of December 2016, SCMA took over SinemArt (production house company). SCMA’s parent company is the Emtek Group, which is controlled by the Sariaatmadja family. Currently, SCMA controls c.31.0% of Indonesia FTA TV audience share (all time) as of May 2018 and ranked second on the metric.

Sales Trend Profitability Trend

Source: Company, DBSVI

Key Management Team

Source: Company

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

0

1,000

2,000

3,000

4,000

5,000

2015A 2016A 2017A 2018F 2019F

Rp bn

Total Revenue Revenue Growth (%) (YoY)

1,331

1,431

1,531

1,631

1,731

1,831

1,931

2,031

2,131

2015A 2016A 2017A 2018F 2019F

Rp bn

Operating EBIT Pre tax Profit Net Profit

Sutanto Hartono President Director

Mr Sutanto Hartono was born in 1967. He was appointed as a President Director of the company in 2013. Prior to this appointment from 2011-2013, he served as the President Director of SCTV, a role which he was re-apointed in 2015. Previously, he was the Country General Manager of PT Microsoft Indonesia. He hold MBA from University of California, Berkeley.

Harsiwi Achmad Director

Mrs Harsiwi Achmad was born in 1966. She was appointed as a Director of the company since 2013. Previously, she held the position of Programming Director of PT Surya Citra Telev isi (SCTV) from 2010-2013, and Director of PT Rajawali Citra Telev isi (RCTI) from 2006-2010. She hold Master Degree from Monash University .

Imam Sudjarwo Director

Mr Imam Sudjarwo was born in 1955. He was appointed as a Director of the company since 2015 and he still serves as the President Director of PT Indosiar V isual Mandiri since 2014. Previously, he was the Head of Security Intelligence of National Police. He hold Master of Science Degree from University of Indonesia.

Rusmiyati Djajaseputra Director

Mrs Rusmiyati Djajaseputra was born in 1978. She was appointed as a Director of the company since 2015. Previously, she served as F inance Director at PT Surya Citra Telev isi (SCTV) and PT Indosiar V isual Mandiri. She graduated from Tarumanegara University with a Bachelor Degree of Accounting and possessed CPA Indonesia Certificate.

Mutia Nandika Independent Director

Mrs Mutia Nandika was born in 1980. She was appointed as an Independent Director of the company since 2016. Previously, she served as Country Industry Head of Google Indonesia since March 2013-October 2015. She obtained her Bachelor Degree in Politic and Social Sciences from Catholic University of Parahyangan.

Page 20

Company Focus

Surya Citra Media

Competitive Strengths One of the leaders in prime time (PT) and all time (AT) audience share. As of May 2018, SCMA controls market shares of 33.0% and 31.0% of PT and AT, respectively. In YTD 2018, SCMA has showed a significant improvement in terms of audience share for both TV stations, SCTV and Indosiar; through their new programs in both TV stations. Currently, SCMA is the second largest market share behind MNCN.

All time (AT) audience share per group (%)

Source: Nielsen Prime time (PT) audience share per group (%)

Source: Nielsen

Growth Strategies SCTV’s audience share has improved. In 2017, SCTV prime time (PT) and all time (AT) audience share have improved significantly. SCTV AT and PT increased by 1.8ppts and 5.0ppts, respectively in 2017. The improvement of audience share was due to its soap opera (Sinetron) programmes that were produced by PT SinemArt Indonesia (which was acquired in FY17). Several programmes like “Siapa Takut Jatuh Cinta”, “Anak Langit”, “Berkah Cinta”, “Anak Sekolahan”, and “Boy” helped to improve SCTV’s PT audience share number in 2017.

SCTV’s PT audience share showed an improvement YTD

(%)

Source: Nielsen SCTV’s AT audience share showed an improvement YTD

(%)

Source: Nielsen

MNCN SCMA TRANS VIVAJan-17 35.5 24.0 14.0 23.1Feb-17 32.6 27.3 13.4 23.1Mar-17 33.2 29.1 14.3 20.2Apr-17 33.5 29.8 14.6 18.8May-17 35.5 28.1 14.6 18.3Jun-17 36.9 25.5 13.1 21.5Jul-17 33.7 26.9 14.1 22.4Aug-17 33.6 26.7 13.8 22.8Sep-17 33.4 27.6 14.4 21.8Oct-17 32.1 28.0 14.7 22.4Nov-17 30.9 29.1 15.5 21.6Dec-17 31.5 31.8 14.4 19.8Jan-18 31.9 32.8 13.2 19.7Feb-18 31.8 32.7 13.3 19.8Mar-18 31.1 32.4 13.2 21.2Apr-18 30.7 33.4 13.4 20.4May-18 32.8 31.0 12.3 21.3

MNCN SCMA TRANS VIVAJan-17 41.6 23.9 12.9 18.2Feb-17 38.0 29.7 11.1 17.6Mar-17 36.7 34.1 11.2 14.9Apr-17 37.7 34.0 10.7 14.4May-17 39.0 30.3 11.2 16.1Jun-17 41.1 25.8 9.8 20.3Jul-17 37.0 27.9 10.0 22.6Aug-17 37.8 26.7 10.4 22.0Sep-17 38.5 25.4 10.8 22.5Oct-17 36.2 25.5 11.1 24.7Nov-17 32.6 30.1 12.1 22.4Dec-17 31.3 36.4 11.5 18.4Jan-18 33.1 36.0 9.7 18.9Feb-18 33.1 35.5 10.1 19.1Mar-18 33.2 34.3 10.6 19.7Apr-18 32.2 35.2 11.0 19.5May-18 33.9 33.0 10.7 19.7

0.0

5.0

10.0

15.0

20.0

25.0

Jan-

14

Mar

-14

May

-14

Jul-1

4

Sep-

14

Nov

-14

Jan-

15

Mar

-15

May

-15

Jul-1

5

Sep-

15

Nov

-15

Jan-

16

Mar

-16

May

-16

Jul-1

6

Sep-

16

Nov

-16

Jan-

17

Mar

-17

May

-17

Jul-1

7

Sep-

17

Nov

-17

Jan-

18

Mar

-18

SCTV PT audience share

10.0

11.0

12.0

13.0

14.0

15.0

16.0

17.0

18.0

19.0

20.0

Jan‐14

Apr‐14

Jul‐14

Oct‐14

Jan‐15

Apr‐15

Jul‐15

Oct‐15

Jan‐16

Apr‐16

Jul‐16

Oct‐16

Jan‐17

Apr‐17

Jul‐17

Oct‐17

Jan‐18

Apr‐18

SCTV all time audience share

Page 21

Company Focus

Surya Citra Media

SCTV vs RCTI’s prime time audience share (%)

Source: Nielsen Asian Games will provide additional revenue for SCMA. The Asian Games, which will be held in Jakarta and Palembang, is expected to be a momentous national event that will grab the attention of Indonesians. All eyes will be on the second largest sporting event in the world, and the excitement is further underpinned by the fact it is the first time that Indonesia has hosted the Asian Games since 1962. The appointment of SCTV as the official media to cover the 2018 Asian Games in Jakarta and Palembang will certainly improve SCMA’s potential to boost its audience share.

Content is the next growth driver. Online video streaming platforms have been expanding into emerging markets like Indonesia with localised content. Falling smartphone prices and improved 4G coverage have also contributed to smartphone penetration rising to 43% and the proliferation of subscription video on demand (SVoD) services. Netflix, iflix and Hooq are a few examples of SVoD players in Indonesia. Most of the SVoD players provide localised content which they bought from SCMA or MNCN – thus providing a new revenue stream to offset the potential decline of advertising revenue in the future.

SCMA’s production house team and flow of content sales

Source: company

Key Risks

Soft advertising spending (ad spend) growth. Ad spend growth is positively correlated to the GDP of Indonesia. In our base case, we assume 1.08x multiplier between ad spend and nominal GDP. Our multiplier is based on the assumption of a household consumption recovery due to 2018 being an election year. However, if the household consumption recovery trails our expectation, then the risks of lower ad spend growth and lower revenue growth for TV players could emerge in FY18F.

Sensitivity analysis on advertising spending

Source: World Bank, Nielsen, companies, DBSVI Weaker audience share. Ad spend growth is one of the key drivers for the media industry’s growth. The other factor is audience share, which would impact the rate card of media players. Normally, advertisers prefer to advertise their products on TV stations that have a strong and stable audience share. If SCMAs fail to maintain its strong audience share, its rate card could head south and this could result in lower revenue growth in FY18F.

Rights issue to raise Rp3.6tr. SCMA has obtained shareholder approval for its rights issue of 1.46bn new shares at Rp2,446/share, which will raise Rp3.6tr. The company plans to use the proceeds for working capital and business expansion. We think that investors will wait for more clarity on the utilisation plan of its capital raising exercise ( which entails a potential dilution). The right investments could boost investor confidence. Massive growth of online media. The massive growth of online media remains a challenge for the media industry’s ad spend growth going forward.

Digitalisation regulation. Furthermore, the plan to introduce new broadcasting laws in relation to the migration of analogue to digital transmission, also poses another challenge for the media industry.

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

Jan-

14

Mar

-14

May

-14

Jul-1

4

Sep-

14

Nov-

14

Jan-

15

Mar

-15

May

-15

Jul-1

5

Sep-

15

Nov-

15

Jan-

16

Mar

-16

May

-16

Jul-1

6

Sep-

16

Nov-

16

Jan-

17

Mar

-17

May

-17

Jul-1

7

Sep-

17

Nov-

17

Jan-

18

Mar

-18

SCTV PT audience share RCTI PT audience share

VIP - Online Video Content production house

Content Distribution

TV shows (drama, FTV, variety show)Online (Iflix, Netflix, Vidio, Smartphones)Cinema (Indonesia Box Office)

2015 2016 2017 2018F BEA R BA SE BULL

SCMA 4.5% 6.8% -1.6% 9.0% 6.0% 9.0% 12.0%

MNCN -3.3% 4.4% 4.8% 6.0% 4.0% 6.0% 8.0%

Ads spend average growth 7.5% 14.2% 7.9% 10.0% 7.2% 10.0% 12.0%

Indonesia nominal GDP 9.1% 7.6% 9.5% 9.3% 9.0% 9.3% 10.0%

x GDP 0.82 1.87 0.84 1.08 0.80 1.08 1.20

Page 22

Company Focus

Surya Citra Media

CRITICAL DATA POINTS TO WATCH

Critical Factors Advertising revenue is positively correlated with GDP In our view, adex growth is a function of economic growth, during periods of economic boom, with the adex/nominal GDP growth multiplier rising to close to 2x. Meanwhile, during periods of economic downturns, the multiplier has softened to below 1x of nominal GDP. Media players are a proxy to consumer demand and trading at a discount Media player’s revenues are highly correlated to spending by FMCG companies on advertising and promotions. Currently, the media sector is trading at 16.2x FY18F PE vs. 32.7x FY18F PE for the consumer sector – we note that the media sector has been trading at a huge discount to consumer names. With the potential recovery of industry adex in FY18F, we believe that the media sector’s PE discount to consumer names will narrow going forward. Correlation between audience share and advertising revenue of each TV player

Based on our analysis, we gather that there is some correlation between media advertising revenue growth and last year’s audience share number. This indicates that, if the audience share of one TV media company fell – it would have an impact on next year’s revenue growth. We believe that the advertisers will ask for adjustments in the rate card, depending on the audience share.

SCTV Revenue (Rpbn)

Indosiar Revenue (Rpbn)

Others (content revenue -Rpbn)

Source: company, DBSVI

27052611 2600

27302860

0.0

412.7

825.4

1238.1

1650.8

2063.5

2476.2

2888.9

2015A 2016A 2017A 2018F 2019F

1485

18811731

1988

2213

0.0

451.4

902.9

1354.3

1805.8

2257.2

2015A 2016A 2017A 2018F 2019F

48.8

32.2

123

135

149

0.00

30.31

60.62

90.94

121.25

151.56

2015A 2016A 2017A 2018F 2019F

Page 23

Company Focus

Surya Citra Media

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

‐10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

2010 2011 2012 2013 2014 2015 2016 2017

SCMA revenue growth MNCN revenue growth GDP

Appendix 1: A look at Company's listed history – what drives its share price? Media players revenue vs GDP growth

Source: Bloomberg Finance L.P., company, DBSVI

SCMA: Correlation between last year’s audience share and revenue growth

Source: Bloomberg Finance L.P., company, DBSVI

Media vs consumer PE ratio (x)

Source: Bloomberg Finance L.P., company, DBSVI

-4.0%

0.0%

4.0%

8.0%

12.0%

16.0%

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2013 2014 2015 2016 2017

SCMA PT audience share SCMA revenue growth

Page 24

Company Focus

Surya Citra Media

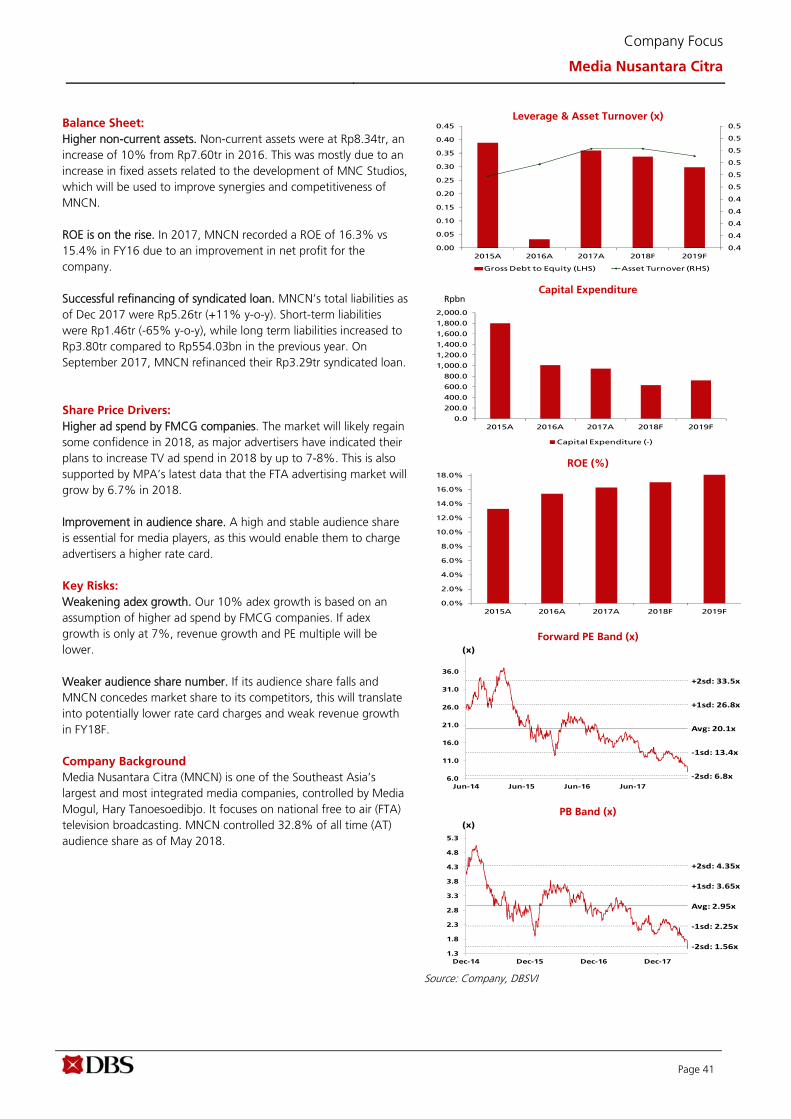

Balance Sheet:

Solid balance sheet. Surya Citra Media (SCMA) has a solid balance sheet. The company does not have any bank borrowings and has always been in a net cash position. As of end-December 2017, the company’s cash position stood at Rp233.5bn. ROA fell in 2017 due to acquisition of SinemArt. In the past three years, SCMA’s ROA stabilised at 32-33% between FY14 and FY16. However, in FY17, SCMA’s ROA fell to 26.1% due to higher intangible assets in the wake of the acquisition of SinemArt in 2017 that involved Rp716bn. Softer earnings lead to lower ROE. Due to the softer industry growth, SCMA faced a number of challenges in the past few years arising from (i) weak audience share number, and (ii) higher cost of programming incurred to quickly boost the audience share number. This has resulted in a lacklustre earnings performance in the past few years, with ROE falling to 36.3% in FY17 from 45.7% in FY16. Share Price Drivers:

Higher ad spend by FMCG companies. The market will likely regain some confidence in 2018, as major advertisers have indicated their plans to increase their total budgets on TV ad spend in 2018 by up to 7-8%. This is also supported by MPA’s latest data that the FTA advertising market will grow by 6.7% in 2018. Improvement in audience share. A high and stable audience share is essential for media players, as this would enable them to charge advertisers a higher rate card. Key Risks:

Weakening adex growth. Our 10% adex growth is based on our assumption of higher ad spend by FMCG companies. If adex growth is only at 7%, then our revenue growth and PE multiple will be lower. Weaker audience share number. If its audience share fall and SCMA concedes market share to its competitors, this will translate into potentially lower rate card charges and weak revenue growth in FY18F. Rights issue could become an overhang. SCMA has obtained shareholder approval at its EGM to raise new capital of Rp3.6tr (at Rp2,446/share). Based on the Indonesia’s securities regulations, the approval would be valid for two years, i.e. until 2020. In our view, this could present an overhang risk for SCMA’s share price, as investors could be concerned about the potential dilution effect. Company Background

Surya Citra Media (SCMA) focusses on national free to air (FTA) TV broadcasting. Through its station SCTV and Indosiar. SCMA controls c. 31.0% of Indonesia's FTA TV audience shares (all time) as of April 2018 and ranked first on the metric.

Leverage & Asset Turnover (x)

Capital Expenditure

ROE (%)

Forward PE Band (x)

PB Band (x)

Source: Company, DBSVI

0.7

0.8

0.8

0.9

0.9

1.0

1.0

0.00

0.01

0.01

0.02

0.02

0.03

0.03

0.04

0.04

0.05

0.05

2015A 2016A 2017A 2018F 2019F

Gross Debt to Equity (LHS) Asset Turnover (RHS)

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

2015A 2016A 2017A 2018F 2019F

Capital Expenditure (-)

Rpm

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

2015A 2016A 2017A 2018F 2019F

Avg: 29.2x

+1sd: 33.6x

+2sd: 38x

‐1sd: 24.9x

‐2sd: 20.5x

17.5

22.5

27.5

32.5

37.5

42.5

Jun-14 Jun-15 Jun-16 Jun-17

(x)

Avg: 11.93x

+1sd: 14.23x

+2sd: 16.53x

‐1sd: 9.63x

‐2sd: 7.33x6.4

8.4

10.4

12.4

14.4

16.4

18.4

Dec-14 Dec-15 Dec-16 Dec-17

(x)

Rpbn

Page 25

Company Focus

Surya Citra Media

Key Assumptions

FY Dec 2014A 2015A 2016A 2017A 2018F 2019F SCTV Revenue 2,717 2,705 2,611 2,600 2,730 2,860

Indosiar Revenue 1,319 1,485 1,881 1,731 1,988 2,213

Others (content revenue) 19.6 48.8 32.3 123 135 149

Segmental Breakdown

FY Dec 2014A 2015A 2016A 2017A 2018F 2019F Revenues (Rpbn)

Advertising Revenue 4,036 4,189 4,492 4,331 4,718 5,073

Others 19.6 48.8 32.3 123 135 149

Total 4,056 4,238 4,524 4,454 4,854 5,222

Source: company, DBSVI

Page 26

Company Focus

Surya Citra Media

Income Statement (Rpbn)

FY Dec 2014A 2015A 2016A 2017A 2018F 2019F Revenue 4,056 4,238 4,524 4,454 4,854 5,222

Cost of Goods Sold (1,475) (1,522) (1,782) (1,842) (1,950) (2,038)

Gross Profit 2,580 2,715 2,742 2,612 2,904 3,184

Other Opng (Exp)/Inc (664) (701) (738) (840) (915) (985)

Operating Profit 1,917 2,015 2,003 1,772 1,989 2,200

Other Non Opg (Exp)/Inc 0.0 0.0 0.0 0.0 0.0 0.0

Associates & JV Inc 0.0 (0.2) 1.85 11.0 0.0 0.0

Net Interest (Exp)/Inc 0.22 24.1 18.4 (1.1) 10.3 10.6

Exceptional Gain/(Loss) 0.0 0.0 0.0 0.0 0.0 0.0

Pre-tax Profit 1,917 2,038 2,024 1,782 1,999 2,210

Tax (469) (517) (512) (464) (500) (553)

Minority Interest 5.37 1.94 (10.2) 13.7 (15.4) (17.0)

Preference Dividend 0.0 0.0 0.0 0.0 0.0 0.0

Net Profit 1,454 1,524 1,501 1,331 1,484 1,641

Net Profit before Except. 1,454 1,524 1,501 1,331 1,484 1,641

EBITDA 2,026 2,142 2,140 1,970 2,184 2,411

Growth

Revenue Gth (%) 9.8 4.5 6.8 (1.6) 9.0 7.6

EBITDA Gth (%) 8.8 5.7 (0.1) (8.0) 10.9 10.4

Opg Profit Gth (%) 9.0 5.1 (0.6) (11.5) 12.2 10.6

Net Profit Gth (Pre-ex) (%) 13.6 4.8 (1.5) (11.3) 11.4 10.6

Margins & Ratio

Gross Margins (%) 63.6 64.1 60.6 58.6 59.8 61.0

Opg Profit Margin (%) 47.3 47.5 44.3 39.8 41.0 42.1

Net Profit Margin (%) 35.8 35.9 33.2 29.9 30.6 31.4

ROAE (%) N/A 46.2 45.7 36.3 34.7 32.5

ROA (%) N/A 32.8 32.0 26.1 25.7 25.0

ROCE (%) N/A 39.5 39.7 30.9 29.7 28.4

Div Payout Ratio (%) 51.3 120.0 80.9 63.7 50.7 51.1

Net Interest Cover (x) NM NM NM 1,652.8 NM NM Source: company, DBSVI

Margins Trend

28.0%

33.0%

38.0%

43.0%

48.0%

2015A 2016A 2017A 2018F 2019F

Operating Margin % Net Income Margin %

Page 27

Company Focus

Surya Citra Media

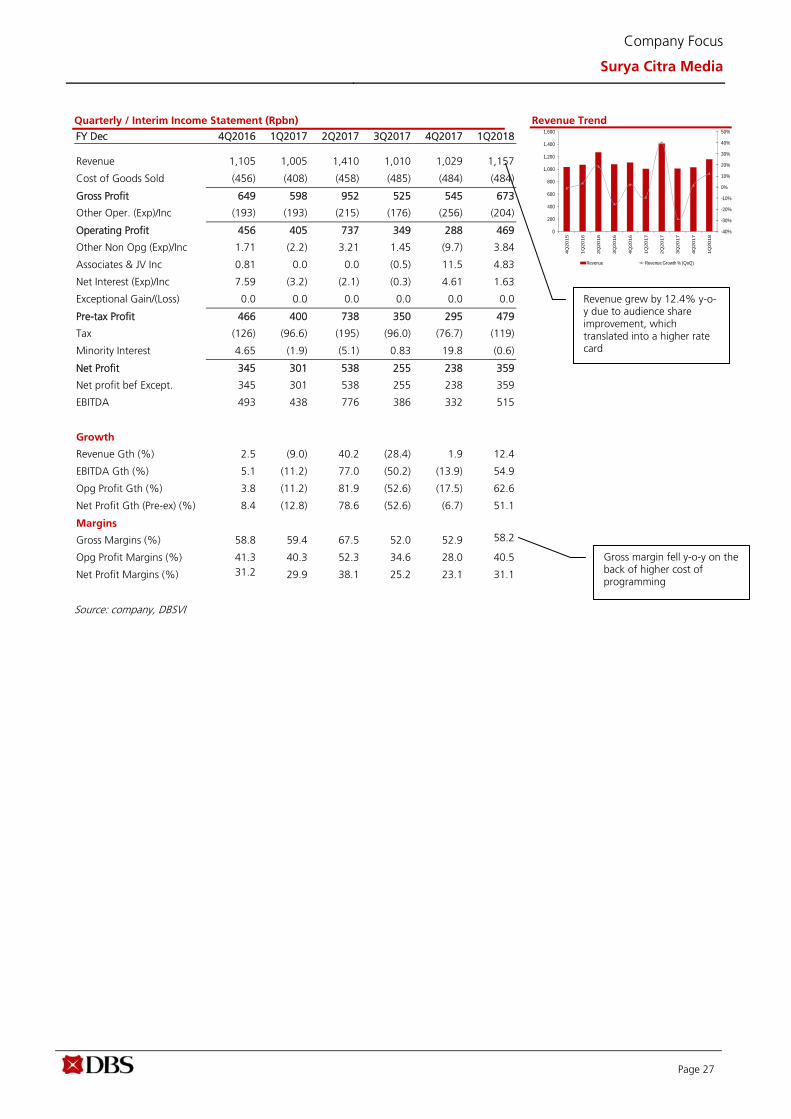

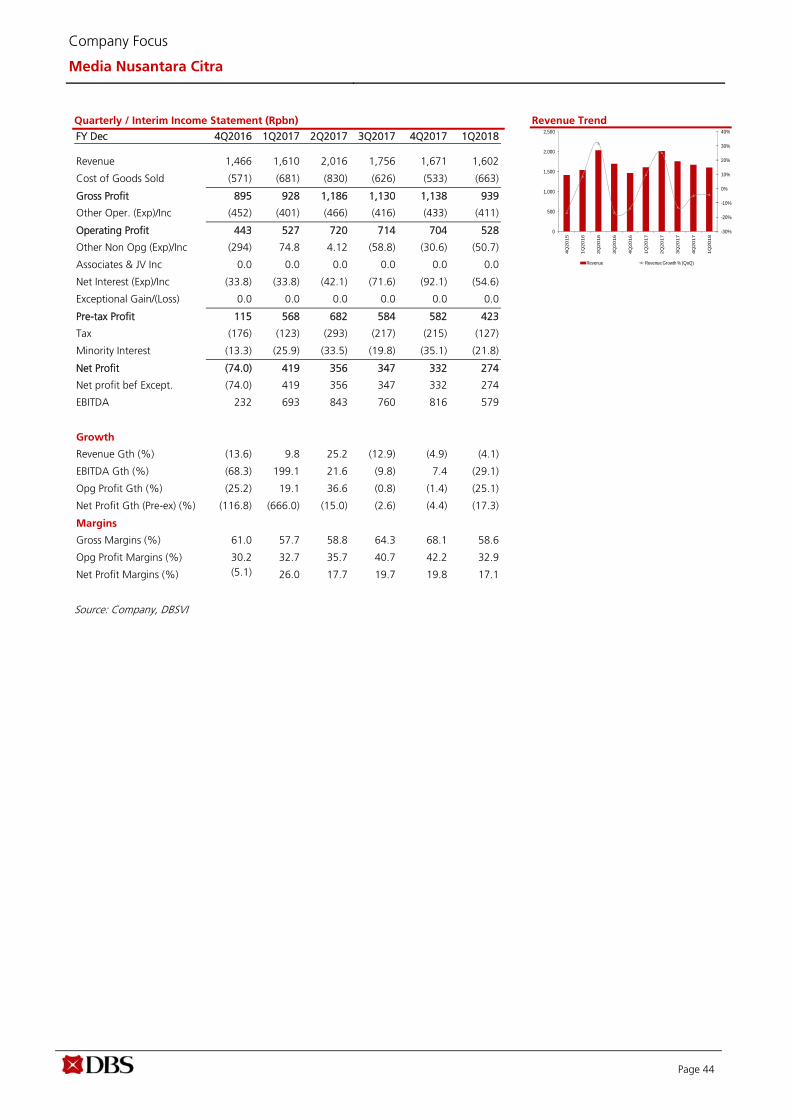

Quarterly / Interim Income Statement (Rpbn)

FY Dec 4Q2016 1Q2017 2Q2017 3Q2017 4Q2017 1Q2018 Revenue 1,105 1,005 1,410 1,010 1,029 1,157

Cost of Goods Sold (456) (408) (458) (485) (484) (484)

Gross Profit 649 598 952 525 545 673

Other Oper. (Exp)/Inc (193) (193) (215) (176) (256) (204)

Operating Profit 456 405 737 349 288 469

Other Non Opg (Exp)/Inc 1.71 (2.2) 3.21 1.45 (9.7) 3.84

Associates & JV Inc 0.81 0.0 0.0 (0.5) 11.5 4.83

Net Interest (Exp)/Inc 7.59 (3.2) (2.1) (0.3) 4.61 1.63

Exceptional Gain/(Loss) 0.0 0.0 0.0 0.0 0.0 0.0

Pre-tax Profit 466 400 738 350 295 479

Tax (126) (96.6) (195) (96.0) (76.7) (119)

Minority Interest 4.65 (1.9) (5.1) 0.83 19.8 (0.6)

Net Profit 345 301 538 255 238 359

Net profit bef Except. 345 301 538 255 238 359

EBITDA 493 438 776 386 332 515

Growth

Revenue Gth (%) 2.5 (9.0) 40.2 (28.4) 1.9 12.4

EBITDA Gth (%) 5.1 (11.2) 77.0 (50.2) (13.9) 54.9

Opg Profit Gth (%) 3.8 (11.2) 81.9 (52.6) (17.5) 62.6

Net Profit Gth (Pre-ex) (%) 8.4 (12.8) 78.6 (52.6) (6.7) 51.1

Margins

Gross Margins (%) 58.8 59.4 67.5 52.0 52.9 58.2

Opg Profit Margins (%) 41.3 40.3 52.3 34.6 28.0 40.5

Net Profit Margins (%) 31.2 29.9 38.1 25.2 23.1 31.1

Revenue Trend

Source: company, DBSVI

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

0

200

400

600

800

1,000

1,200

1,400

1,600

4Q

20

15

1Q

20

16

2Q

20

16

3Q

20

16

4Q

20

16

1Q

20

17

2Q

20

17

3Q

20

17

4Q

20

17

1Q

20

18

Revenue Revenue Growth % (QoQ)

Gross margin fell y-o-y on the back of higher cost of programming

Revenue grew by 12.4% y-o-y due to audience share improvement, which translated into a higher rate card

Page 28

Company Focus

Surya Citra Media

Balance Sheet (Rpbn)

FY Dec 2014A 2015A 2016A 2017A 2018F 2019F Net Fixed Assets 762 962 967 1,029 1,013 982

Invts in Associates & JVs 24.1 24.3 26.2 37.3 37.3 37.3

Other LT Assets 745 736 875 1,611 1,643 1,672

Cash & ST Invts 1,246 686 455 234 765 1,448

Inventory 462 533 689 766 770 805

Debtors 1,291 1,412 1,534 1,556 1,684 1,811

Other Current Assets 198 213 275 153 233 251

Total Assets 4,728 4,566 4,821 5,386 6,145 7,006

ST Debt

0.0 0.0 0.0 0.0 0.0 0.0

Creditor 335 260 385 437 435 455

Other Current Liab 484 601 605 306 304 322

LT Debt 0.0 0.0 0.0 0.0 0.0 0.0

Other LT Liabilities 431 292 125 237 241 245

Shareholder’s Equity 3,446 3,146 3,427 3,901 4,644 5,446

Minority Interests 32.4 267 279 504 520 537

Total Cap. & Liab. 4,728 4,566 4,821 5,386 6,145 7,006

Non-Cash Wkg. Capital 1,133 1,297 1,507 1,732 1,947 2,089

Net Cash/(Debt) 1,246 686 455 234 765 1,448

Debtors Turn (avg days) N/A 116.4 118.8 126.6 121.8 122.1

Creditors Turn (avg days) N/A 77.8 71.5 90.7 90.8 89.0

Inventory Turn (avg days) N/A 130.2 135.4 160.5 159.8 157.4

Asset Turnover (x) NM 0.9 1.0 0.9 0.8 0.8

Current Ratio (x) 3.9 3.3 3.0 3.6 4.7 5.6

Quick Ratio (x) 3.1 2.4 2.0 2.4 3.3 4.2

Net Debt/Equity (X) CASH CASH CASH CASH CASH CASH

Net Debt/Equity ex MI (X) CASH CASH CASH CASH CASH CASH

Capex to Debt (%) N/A N/A N/A N/A N/A N/A Source: company, DBSVI

Asset Breakdown

Net Fixed Assets -28.4%

Assocs'/JVs -1.0%

Bank, Cash and Liquid

Assets -6.4%

Inventory -21.1%

Debtors -43.0%

Other LT assets due to higher intangible assets from acquisition of SinemArt at Rp716bn

Page 29

Company Focus

Surya Citra Media

Cash Flow Statement (Rpbn)

FY Dec 2014A 2015A 2016A 2017A 2018F 2019F Pre-Tax Profit 1,917 2,038 2,024 1,782 1,999 2,210

Dep. & Amort. 109 127 135 187 195 212

Tax Paid (469) (517) (512) (464) (500) (553)

Assoc. & JV Inc/(loss) 0.0 0.0 0.0 0.0 0.0 0.0

Chg in Wkg.Cap. (384) (453) (434) (110) (120) (143)

Other Operating CF 4.89 311 172 (144) (50.8) (28.6)

Net Operating CF 1,179 1,507 1,385 1,251 1,524 1,698

Capital Exp.(net) (152) (322) (144) (253) (179) (180)

Other Invts.(net) 0.0 0.0 0.0 0.0 0.0 0.0

Invts in Assoc. & JV (24.1) (0.3) (1.9) (11.0) 0.0 0.0

Div from Assoc & JV 0.0 0.0 0.0 0.0 0.0 0.0

Other Investing CF (10.4) 210 (105) (263) 0.0 0.0

Net Investing CF (187) (112) (250) (526) (179) (180)

Div Paid (746) (1,828) (1,214) (848) (752) (838)

Chg in Gross Debt 37.1 84.5 35.5 (165) (65.0) 0.0

Capital Issues 0.0 (3.6) 0.33 0.0 0.0 0.0

Other Financing CF (80.5) (211) (188) 13.2 4.02 4.12

Net Financing CF (789) (1,958) (1,365) (1,000) (813) (834)

Currency Adjustments 0.0 0.0 0.0 0.0 0.0 0.0

Chg in Cash 203 (563) (231) (276) 531 683

Opg CFPS (Rp) 107 134 124 93.1 112 126

Free CFPS (Rp) 70.2 81.0 84.9 68.2 92.0 104 Source: Company, DBSVI

Capital Expenditure

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

2015A 2016A 2017A 2018F 2019F

Capital Expenditure (-)

Rpm

Page 30

Company Focus

Surya Citra Media

Valuation Initiate coverage: BUY, TP Rp2,600. Our DCF-based TP of Rp2,600/share for SCMA assumes a WACC of 9% and terminal growth of 3%, with cash flow discounted back from FY25F to the present. To arrive at our WACC of 9%, we assume a risk-free rate of 8%, market risk premium of

5%, and equity beta of 0.8. Our TP implies 25.6x FY18F PE which is above its historical 8-year mean. Currently, the stock is trading at 17.9x FY18F PE (-1SD of its historical 8-year mean of 21.2x).

SCMA’s forward PE band

Source: Bloomberg Finance LP Data as of 20 June 2018

‐

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

Jan‐10 Jan‐11 Jan‐12 Jan‐13 Jan‐14 Jan‐15 Jan‐16 Jan‐17 Jan‐18

P/E

MEAN

+1 STDEV

+2 STDEV

‐1 STDEV

‐2 STDEV

ed: KK / MA, PY, CS

BUY (Initiating Coverage) Last Traded Price ( 22 Jun 2018): Rp975 (JCI : 5,821.81) Price Target 12-mth: Rp1,300 (33% upside) Potential Catalyst: Acceleration of media advertising ependiture (adex), and Ramadhan season Analyst David Arie Hartono +62 2130034936 [email protected]

Price Relative

Forecasts and Valuation FY Dec (Rpbn) 2016A 2017A 2018F 2019F Revenue 6,730 7,053 7,474 7,945 EBITDA 2,582 3,113 3,293 3,612 Pre-tax Profit 2,153 2,416 2,482 2,746 Net Profit 1,369 1,453 1,620 1,930 Net Pft (Pre Ex.) 1,369 1,453 1,620 1,930 EPS (Rp) 95.9 102 113 135 EPS Pre Ex. (Rp) 95.9 102 113 135 EPS Gth (%) 15 6 11 19 EPS Gth Pre Ex (%) 15 6 11 19 Diluted EPS (Rp) 95.9 102 113 135 Net DPS (Rp) 0.0 0.0 0.0 0.0 BV Per Share (Rp) 618 632 704 793 PE (X) 10.2 9.6 8.6 7.2 PE Pre Ex. (X) 10.2 9.6 8.6 7.2 P/Cash Flow (X) 7.1 6.3 7.1 5.9 EV/EBITDA (X) 5.6 5.7 5.2 4.5 Net Div Yield (%) 0.0 0.0 0.0 0.0 P/Book Value (X) 1.6 1.5 1.4 1.2 Net Debt/Equity (X) CASH 0.3 0.2 0.1 ROAE (%) 15.4 16.3 17.0 18.1 Consensus EPS (Rp): N/A N/A N/A Other Broker Recs: B: S: H: ICB Industry : Consumer Services ICB Sector: Media Principal Business: Media Nusantara Citra (MNCN) is one of South East Asia's largest and most integrated media companies, controlled by media mogul, Hary Tanoesoedibjo, with a focus on national free to air (FTA) television broadcasting. MNCN controlled 32.8% of all time audience share. Source of all data on this page: company, DBSVI, Bloomberg Finance L.P.

At A Glance Issued Capital (m shrs)

Mkt. Cap (Rpbn/US$m) 17,488 / 954

Major Shareholders (%)

Global Mediacom Tbk 59.16%

Free Float (%) 40.8%

3m Avg. Daily Val (US$m) 1.6

DBS Group Research . Equity 25 Jun 2018

Indonesia Company Focus

Media Nusantara Citra Bloomberg: MNCN IJ | Reuters: MNCN.IJ Refer to important disclosures at the end of this report

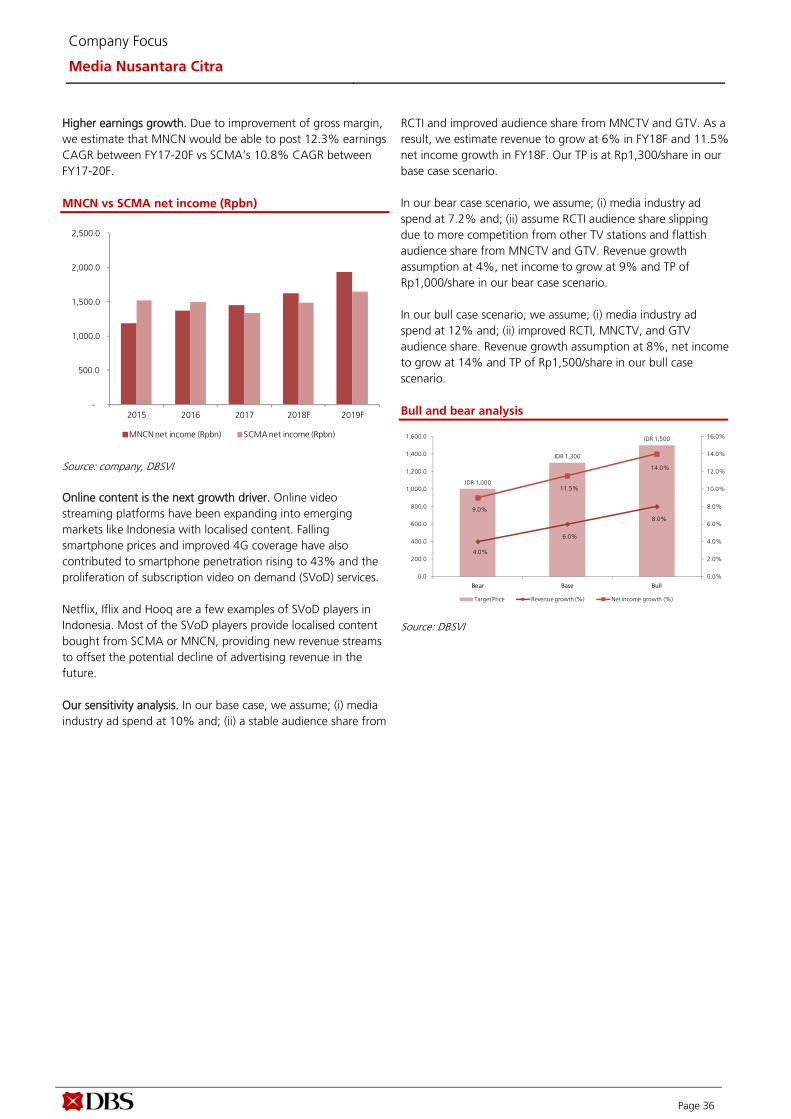

Too cheap to ignore Revenue growth driven by higher rate cards of MNCTV and

GTV Estimate 12.3% earnings CAGR between FY17-20F with

better gross margin Higher content sold to third parties would be the next

growth driver Initiate MNCN with a BUY call and TP of Rp1,300/share

Attractive entry point. Currently, the stock is trading at 8.8x FY18F PE or trading at -2SD (below its historical 8 years mean of 17.4x). We believe that the market has over punished the stock due to weak advertising expenditure (adex) growth environment in the past few years. However, we believe that the stock has not priced in the potential upsides from; (i) improvement in Media Nusantara Citra TV (MNCTV) and GTV (formerly Global TV) audience shares could be the growth drivers in FY18F; (ii) potential higher revenue contribution from its content business and; (iii) potential higher gross margin in FY18F of 62% vs SCMA of 59.8% in FY18F. Assume 12.3% earnings CAGR for FY17-20F. Even though MNCN did not have the rights to broadcast special events in FY18, we believe that MNCN would benefit from a potential acceleration of adex growth in 2H18 and the Lebaran season in 2Q18. We assume a revenue growth of 6%/6.3% in FY18F/19F respectively from higher rate card in MNCTV and GTV. Meanwhile, we assume a stable and high gross margin at 62% in FY18F due to more local content. Thus, we estimate an earnings growth of 23.9%/7.2% in FY18F/19F respectively.