Impact of micro finance on grassroot business

32

Page | 1 Title Impact of micro-finance in grass root development BAIDOO TAWIAH WILLIAM A dissertation submitted in partial fulfillment of the requirement of Chartered of Financial and Investment Analysts, at the Chartered Institute of Financial and Investment Analysts, Ghana April, 2014

-

Upload

independent -

Category

Documents

-

view

2 -

download

0

Transcript of Impact of micro finance on grassroot business

Page | 1

Title

Impact of micro-finance in grass root development

BAIDOO TAWIAH WILLIAM

A dissertation submitted in partial fulfillment of the

requirement of

Chartered of Financial and Investment Analysts,

at the

Chartered Institute of Financial and Investment Analysts,

Ghana

April, 2014

Page | 2

ABSTRACT

To improve the socio-economic conditions of rural communities in Ghana, the Rural

and Community banks were established in 1976 with the first rural bank in central

region of Ghana. These banks play very important role in microfinance in the

country. They were established specifically to advance loans to small enterprises,

farmers, individuals and others within their catchment areas and also provide

opportunity for people to save their excess monies.

This research work looks at the impact of micro-finance in grass root development.

The study points out perceptions of grass root business on the need for microfinance

institutions in providing funds in their start-up needs and working capital

requirements for further expansion and development.

Page | 3

DEDICATION

This thesis is dedicated to God, my Parents, Siblings, Sons, family members and my

friends who always inspired me in every step to accomplish this study.

Page | 4

ACKNOWLEDGEMENT

Glory is to God for his protection and guidance throughout my educational life.

I am very thankful to all persons whose divers contributions in no small way, have

contributed to the success of this work.

My first and immeasurably gratitude goes to Kitch Mensah Bonsu, for his efforts to

ensure the successful completion of this work. My special thanks also go to Michael

Kofi Baidoo and Joseph Osei Baidoo for thier time, care, support and assistance in

organizing this work. May you receive the divine favors of Our Lord, Jesus Christ

Thanks goes to my mother, Mrs. Lydia Baidoo, and my brothers and sister for their

moral, spaniel and physical support during difficult times.

Page | 5

TABLE OF CONTENTS

Title page 1

Abstract 2

Dedication 3

Acknowledgment 4

Table of content 5-6

CHAPTER ONE

Introduction

1.1 Background of study

1.2 Statement of problem

1.3 Objectives

1.4 Research questions

1.5 Significance

1.6 Limitations

1.7 Delimitations

1.8 Organization

7-10

7

8

8

8

9

9

10

10

CHAPTER TWO

Theoretical perspective:

2.0 Introduction

2.1 Concept of Microfinance

2.2 Approaches to Microfinance

2.2.1 Welfarist Approach

2.2.2 Institutionalist Approach

2.3 Rotation Saving and Credit

2.4 The Grameen Solidarity group model

11- 13

11

11

11

11

12

13

13

CHAPTER THREE

Methodology:

3.0 Introduction

3.1 Research design

3.2 Population

14-17

14

14

15

Page | 6

3.3 Sample and sampling procedure

3.4 Data collection techniques and procedures

3.5 Data analysis

3.6 Data used

15

15

16

16-17

CHAPTER FOUR

Data collected, coding, analysis and discussion

4.0 Introduction

4.1 Coding

4.2 Analysis of data, Questionnaires responses

18-24

18

18

18-24

CHAPTER FIVE

Findings, recommendation and conclusion

5.0 Introduction

5.1 Findings

5.2 Summary of findings

5.3 Recommendation

5.4 Conclusion

25-28

25

25

27

28

28

REFERENCE 29

APPENDIX A 30-32

Page | 7

CHAPTER – I

INTRODUCTION

Background of study

Economic development is caused by many factors and indicators which generally is

the source and application of resources. The effective and efficient use of economic

resources has seen many countries grow and developed from third (3rd) class

country to a first (1st) class country like United Arab Emirates, Brunei Darussalam,

Singapore, and others. The sources and application of economic resources is

regulated by a financial system in any economy. This system determines how much

can be saved from surplus consumption as the sources and can be reinvested into

economic activities as the application. The tool for the regulation of the financial

system is the financial intermediaries or institutions that mobilize savings and

facilitate the allocation of funds in an efficient manner. Financial institutions can be

classified as banking and non banking financial institutions. Banking institutions are

creators of credit while non-banking financial institutions are purveyors of credit.

Examples of financial institutions in Ghana are savings and loans, rural banks,

commercial banks, merchant banks, micro-finance, etc.

The impact of micro-finance is a subject of much controversy. Proponents state that

it reduces poverty through higher employment and higher incomes. This is expected

to lead to improved nutrition and improved education of the borrowers' children.

Some argue that micro-finance empowers women. In the US and Canada, it is

argued that micro-finance helps recipients to graduate from welfare programs.

Critics say that micro-finance has not increased incomes, but has driven poor

households into a debt trap, in some cases even leading to suicide. They add that the

money from loans is often used for durable consumer goods or consumption instead

of being used for productive investments, that it fails to empower women, and that it

has not improved health or education.

Page | 8

To improve the socio-economic conditions of rural communities in Ghana, the Rural

and Community banks were established in 1976 with the first rural bank in central

region of Ghana. These banks play very important role in microfinance in the

country. They were established specifically to advance loans to small enterprises,

farmers, individuals and others within their catchment areas and also provide

opportunity for people to save their excess monies.

This research work looks at the impact of micro-finance in grass root development.

STATEMENT OF PROBLEM

The efficiency of a financial system is measured by the accurate link of savings to

investments. Microfinance Institutions as a financial intermediary assists in the

reallocation of saving to grass root businesses. Despite a multitude of studies

devoted to the topic, the impact of microfinance programs on the poor in developing

countries remains an intensely debated issue. This study is to identify the impact of

microfinance institutions on grass root businesses in Ghana.

OBJECTIVES

The objectives of this study are;

To examine accessibility to micro-credit by grass root businesses

To assess the impact of microfinance services in developing grass root

businesses

Assess the factors influencing the attitude of Ghanaians to savings with

financial institutions and banks.

Identify strategies that can be employed to improve the impact of

microfinance institutions in Ghana.

RESEARCH QUESTIONS

The following research questions come in mind about the impact of micro finance on

grass root businesses in Ghana;

Page | 9

Does access to micro-credit facility impact on the grass root businesses?

What role does Microfinance Institution play in developing grass root

business?

What is the effect of interest on loans granted by micro finance to grass root

business?

SIGNIFICANCE

With grass root businesses constituting nearly half of the businesses in the Ashanti

Region, the development of these business can catapult the general economic growth

and development of the country. It is necessary that the impact of microfinance

institutions be identified and possible assistance be given to these grass root

business. This study is to assist in the better evaluation of the general effect of micro

financial institutions on the fundamental development of businesses in the country.

LIMITATIONS

The following were the limitations on the result of the research:

The correlations figures used in analyzing the data could not absolutely prove

that the relations were only or mainly caused by the occurrence of the other

variable.

Respondent would not totally disclose information concerning their finances

and limited the research in terms of the access of information about

respondents‟ financial capabilities.

The language barrier encountered was not to be underestimated either. The

researcher had to translate the questions on the questionnaires to respondents

who could not read. Hence, it is likely that pieces of information got lost in

translation.

Finally the sample size comes with its own limitations. With the sample of ten

(10) businesses from Kumasi in the Ashanti Region of Ghana. None the less,

when looking at the sample size often becomes rather small.

Page | 10

DELIMITATIONS

For the purpose of a detailed research the study was:

Carried out in Ghana, more specifically in Kumasi the regional capital of

Ashanti region.

Limited grass root business in Kumasi.

Conducted using questionnaire, interview and observation and analyzed the

data using Statistical Program for Social Sciences software (SPSS 17.0).

THE STUDY

The study is presented in five chapters. Chapter one shows briefly, background and

general introduction to the study, the problem statement and objectives of the study.

The second chapter looks at the theoretical framework and reviews related literature

concerning the study. Chapter three explain the research process and the methods

adopted for collecting and analyzing data. Chapter four deals with analysis of the

data and the final chapter presents a summary as well as conclusions and

recommendations of the study.

Page | 11

CHAPTER – II

THEORETICAL PERSPECTIVE:

INTRODUCTION

This chapter talks about the theories that informed the conduct of the research.

2.1 Concepts of Microfinance

Microfinance is the provision of financial services to low income poor and very poor

self-employed people (Otero, 1999). These financial services according to

Ledgerwood (1999) generally include savings and credit but can also include other

financial services such as insurance and payment services. Schreiner, (2001) support

this view by defining microfinance as “the attempt to improve access to small

deposits and small loans for poor households neglected by banks.” Therefore,

microfinance involves the provision of financial services such as savings, loans and

insurance to poor people living in both urban and rural settings who are unable to

obtain such services from the formal financial sector.

2.2 Approaches of Microfinance

There are two main diverse approaches of microfinance in the literature. These are

the welfarist approach, also called the direct credit approach, and the institutionalist

approach also called financial market approach (Morduch, 1999).

2.2.1 Welfarist Approach

The welfarist approach focuses on the demand side, which is to say on the clients.

This approach support the idea of subsidizing microcredit programmes in order to

lower the cost for the microfinance institutions so they can offer low interest rates on

their loans (Morduch, 1999). Welfarist argues that Microfinance Institution can

achieve sustainability without the institutionalist definition of self-sufficiency

(Woller, Dunfield, & Woodworth, 1999). They further argue that gifts, for instance

subsidies, from donors serve as a form of equity, and as such the donors can be

viewed as investors. Unlike investors who purchase equity in a publicly traded firm,

Page | 12

Microfinance Institution donors do not expect to earn monetary returns. Instead,

these donor-investors realize an intrinsic return. These donors can be compared to

equity investors who invest in socially responsible funds, even if the expected risk-

adjusted return of the socially responsible fund is below that of an index fund. These

socially responsible fund investors are willing to accept a lower expected return

because they also receive the intrinsic return of not investing in firms that they find

offensive.

2.2.2 Institutionalist Approach

The institutionalist view of microfinance argues that a Microfinance Institution

should be able to cover its costs with its revenues. Institutionalists feel self-

sufficiency leads to long-term sustainability for Microfinance Institution, which will

facilitate greater poverty alleviation in the long-term. The institutionalist argument is

consistent with Congo (2002) who discusses historical cases in an attempt to identify

the institutional designs that facilitated success and sustainability for 19th century

loan funds in the UK, Germany, and Italy.

The Institutionalist view of self-sufficiency as a requirement for Microfinance

Institution sustainability seems untenable until one realizes that there appears to be

a trade-off between self-sufficiency and targeting. Most Microfinance Institution

which has proven self-sufficient has tended to loan borrowers who were either

slightly above or below the poverty line in their respective countries (Morduch,

1999).

2.3 Rotating Savings and Credit Associations

These are formed when a group of people come together to make regular cyclical

contributions to a common fund, which is then given as a lump sum to one member

of the group in each cycle (Grameen Bank, 2000). According to Harper (2002), this

model is a very common form of savings and credit. He states that the members of

the group are usually neighbours and friends, and the group provides an

Page | 13

opportunity for social interaction and is very popular with women. They are also

called merry-go-rounds or Self-Help Groups (Yunus, 1999).

2.4 The Grameen Solidarity Group model

This model is based on group peer pressure whereby loans are made to individuals

in groups of four to seven (Yunus, 1999). Group members collectively guarantee loan

repayment, and access to subsequent loans is dependent on successful repayment by

all group members. Payments are usually made weekly (Ledgerwood, 1999).

According to Berenbach & Guzman (1994), solidarity groups have proved effective

in deterring defaults as evidenced by loan repayment rates attained by organisations

such as the Grameen Bank, who use this type of microfinance model. They also

highlight the fact that this model has contributed to broader social benefits because

of the mutual trust arrangement at the heart of the group guarantee system. The

group itself often becomes the building block to a broader social network (Yunus,

1999).

2.5 Village Banking Model

Village banks are community-managed credit and savings associations established

by NGOs to provide access to financial services, build community self-help groups,

and help members accumulate savings (Hulme, 1999). They have been in existence

since the mid-1980s. They usually have 25 to 50 members who are low-income

individuals seeking to improve their lives through self-employment activities. These

members run the bank, elect their own officers, establish their own by-laws,

distribute loans to individuals and collect payments and services (Grameen Bank,

2000). The loans are backed by moral collateral thus the promise that the group

stands behind each loan (Global Development Research Centre, 2005).

Page | 14

Chapter – III

Methodology

Introduction

This chapter talks about the research design used in conducting the research, the

population and sampling technique, the techniques used in data collection and

procedures and also to analyze the data.

RESEARCH DESIGN

The research designs used for the study were descriptive and historical research.

The descriptive research involves describing, recording, analyzing and interpreting

conditions as they exist. Descriptive research, also known as statistical research,

describes data and characteristics about the population or phenomenon being

studied. Descriptive research answers the questions who, what, where, when,

and how. Although the data description is factual, accurate and systematic, the

research cannot describe what caused a situation. They do not make accurate

predictions, and determine cause and effect. There are three main types of

descriptive methods: observational methods, case-study methods and survey

methods. This type of research enables the researcher to identify the possible

impacts of microfinance institutions on grass root businesses.

The historical research also deals with studying, understanding and explaining past

events. It helps the researcher in providing historical data in support of current and

possible future trends on the impact of microfinance on grass root businesses. This

type of research describes what was happening in the past through the collection of

data on past occurrences, recording, analyzing and interpreting the facts on the past

events. This type of research assisted the researcher to conclude on the causes of the

existing problems. Historical research also helped in explaining present events and

also anticipates future events.

Page | 15

Notwithstanding the benefits stated above, the limitation of historical research is

that, it does not experiment to know how effective the strategies that would be used

in solving the existing problem.

POPULATION

The population for the study was made up of small and medium enterprises (SME)

in Kumasi, the capital of Ashanti Region. The region is has the many small and

medium enterprises. However the main target group is grass root businesses that

require an amount of financial assistance, the source and impact of the financial

assistance gain from microfinance institutions. These are businesses that are

operating and intend to expand its operations.

SAMPLE AND SAMPLING PROCEDURE

The sampling method the researcher used is the simple random selection which

helped in selecting respondents that would represent a fair view of the case study.

The sample consisted of ten (10) respondents. The sample for the study was picked

from Kumasi in the Ashanti Region of Ghana. This type of sampling enables the

researcher to have a proper generalization of results. In sampling, different views

from the respondents at different points in time will be evident.

DATA COLLECTION TECHNIQUES AND PROCEDURES

The following set of instruments were used in collecting data; questionnaires,

interviews and observation. Observation is studying respondents from a distance to

know what they are doing; questionnaires is a set of detailed questions that are

printed to be answered by respondents to know the facts concerning an existing

problem and interviewing is interacting with respondents to know their personal

views on an existing problem. These instruments are appropriate in collecting useful

and meaningful data because of their flexibility.

Through observation, the researcher watched how people reacted to savings and

investment as representatives of financial institutions talked about savings. Through

Page | 16

questionnaires were designed questions that sought to reveal the facts about the

existing problem. These questions were carefully arranged and printed. It was then

given to respondents for them to answer them on the printed paper and in the case

of respondents that were not literate the researcher assisted them in answering the

questions in the questionnaires.

The interview conducted was between the respondent and the researcher. The

respondents were selected randomly and they were asked questions concerning

their attitude towards savings and investment. The questionnaires were used as the

interview guide in trying to collect data in connections to the research problem.

DATA ANALYSIS

The data collected were arranged systematically and also analyzed using simple

frequency tables and other statistical tools in analyzing and assessing the frequency

of responses to the questions and that of facts collected about the problem to be

solved.

The researcher arranged collected data carefully and accurately and encoded them

into a computer using Statistical Program for Social Sciences 16.0 (SPSS 16.0)

software. After recording it, the researcher used the frequency tables to analyze the

data so as to know the highest responses to the questions and highest facts collected

about the problems, this can effectively solve it with the selected strategies. The uses

of statistical formulas were used for further analyses.

DATA USED

The researcher used primary and secondary data in conducting the study. The

primary data was collected by the researcher in relations to the research objectives

and questions. Questionnaires, interviews and observations were the means of

gathering primary data.

Page | 17

The secondary data were mainly collect from the World Bank database and Ghana

statistical services database. These data were collected in relations to other or similar

research topics and would not absolutely predict the outcome of this study. The data

was collected by these institutions for different purposes and only the portions that

are relevant to this study was used in the research work.

Page | 18

Chapter - IV

Data collected, coding, analysis and discussion

INTRODUCTION

This chapter talks about the responses given to questions asked in terms of the

research instruments. This chapter also deals with discussions and analyses of data

which ties together the findings in relation to the theory, literature review and issues

relevant to the study. Here the researcher discussed the results obtained through the

questionnaires and interviews.

4.1 Coding

In order to analyze questionnaires and interview results references were made to

questionnaires as appendix A and the questionnaires were used as the interview

guide. Equally, tables representing responses were labeled as table 1, table 2, etc.

Responses were scale from high to low values, that is, the first alternative response

in the in the questionnaire to a question is ranked with one (1) then follows the order

to the last alternative responds for that same question.

4.2 Analysis of Data, Questionnaires Responses

Through the administration of the questionnaire, a lot of factors contributing to

people‟s attitude towards savings and investments were exposed.

Frequency Tables of variety of responses from Respondents

What is (are) the source(s) of your business start-up capital?

Frequency Percent Valid Percent

Cumulative

Percent

Valid 1.00 2 20.0 20.0 20.0

2.00 2 20.0 20.0 40.0

3.00 2 20.0 20.0 60.0

4.00 4 40.0 40.0 100.0

Total 10 100.0 100.0

Note: 1= self, 2= friends & relatives, 3= partnership, 4= loan from microfinance

Page | 19

Accessing the sources of finance for grass root business in starting up their

businesses forty percent (40%) responded that their source of finance was through

loans from microfinance institutions, and twenty percent (20%) each responded as

their source being self, friends and relatives, and partnership. The responses

indicated a high and positive impact of microfinance institutions assisting

entrepreneurs in setting up their businesses to assist in economic development.

Do you have adequate capital for your business growth?

Frequency Percent Valid Percent

Cumulative

Percent

Valid 1.00 2 20.0 20.0 20.0

2.00 8 80.0 80.0 100.0

Total 10 100.0 100.0

Note: 1= Yes, 2= No

The majority of the respondents indicate an insufficient capital requirement

representing eighty percent (80%) of the responses and twenty percent (20)%

responded they had sufficient capital. These responses call for a reliable source of

funding in assisting the grass root businesses access and keep on expanding.

If No, in what ways do you intend to acquire additional capital for your business?

Frequency Percent Valid Percent

Cumulative

Percent

Valid 1.00 1 10.0 11.1 11.1

2.00 2 20.0 22.2 33.3

3.00 1 10.0 11.1 44.4

4.00 5 50.0 55.6 100.0

Total 9 90.0 100.0

Missing System 1 10.0

Total 10 100.0

Page | 20

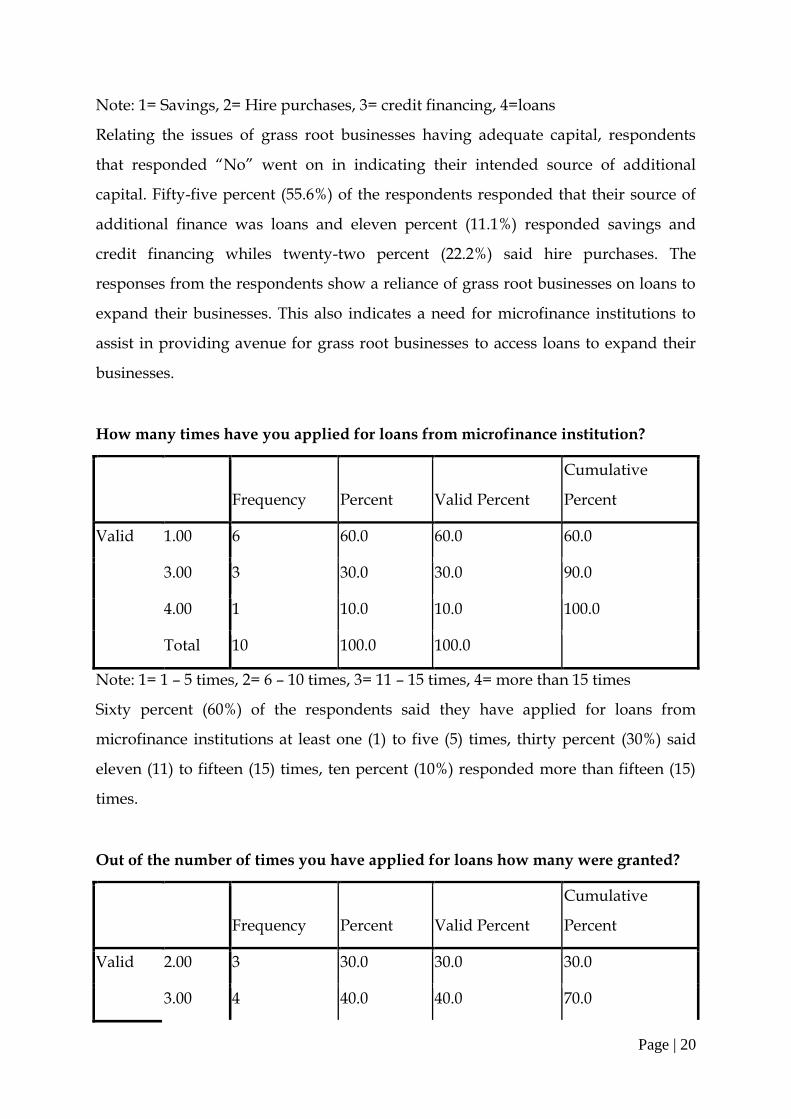

Note: 1= Savings, 2= Hire purchases, 3= credit financing, 4=loans

Relating the issues of grass root businesses having adequate capital, respondents

that responded “No” went on in indicating their intended source of additional

capital. Fifty-five percent (55.6%) of the respondents responded that their source of

additional finance was loans and eleven percent (11.1%) responded savings and

credit financing whiles twenty-two percent (22.2%) said hire purchases. The

responses from the respondents show a reliance of grass root businesses on loans to

expand their businesses. This also indicates a need for microfinance institutions to

assist in providing avenue for grass root businesses to access loans to expand their

businesses.

How many times have you applied for loans from microfinance institution?

Frequency Percent Valid Percent

Cumulative

Percent

Valid 1.00 6 60.0 60.0 60.0

3.00 3 30.0 30.0 90.0

4.00 1 10.0 10.0 100.0

Total 10 100.0 100.0

Note: 1= 1 – 5 times, 2= 6 – 10 times, 3= 11 – 15 times, 4= more than 15 times

Sixty percent (60%) of the respondents said they have applied for loans from

microfinance institutions at least one (1) to five (5) times, thirty percent (30%) said

eleven (11) to fifteen (15) times, ten percent (10%) responded more than fifteen (15)

times.

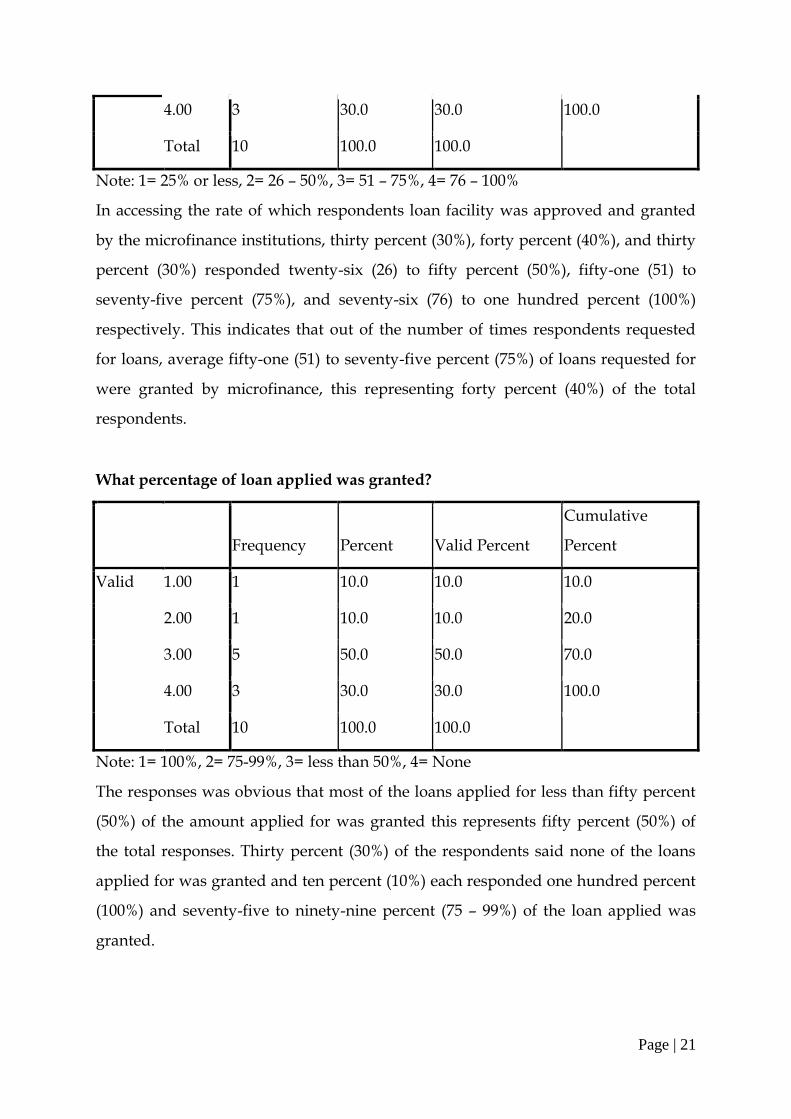

Out of the number of times you have applied for loans how many were granted?

Frequency Percent Valid Percent

Cumulative

Percent

Valid 2.00 3 30.0 30.0 30.0

3.00 4 40.0 40.0 70.0

Page | 21

4.00 3 30.0 30.0 100.0

Total 10 100.0 100.0

Note: 1= 25% or less, 2= 26 – 50%, 3= 51 – 75%, 4= 76 – 100%

In accessing the rate of which respondents loan facility was approved and granted

by the microfinance institutions, thirty percent (30%), forty percent (40%), and thirty

percent (30%) responded twenty-six (26) to fifty percent (50%), fifty-one (51) to

seventy-five percent (75%), and seventy-six (76) to one hundred percent (100%)

respectively. This indicates that out of the number of times respondents requested

for loans, average fifty-one (51) to seventy-five percent (75%) of loans requested for

were granted by microfinance, this representing forty percent (40%) of the total

respondents.

What percentage of loan applied was granted?

Frequency Percent Valid Percent

Cumulative

Percent

Valid 1.00 1 10.0 10.0 10.0

2.00 1 10.0 10.0 20.0

3.00 5 50.0 50.0 70.0

4.00 3 30.0 30.0 100.0

Total 10 100.0 100.0

Note: 1= 100%, 2= 75-99%, 3= less than 50%, 4= None

The responses was obvious that most of the loans applied for less than fifty percent

(50%) of the amount applied for was granted this represents fifty percent (50%) of

the total responses. Thirty percent (30%) of the respondents said none of the loans

applied for was granted and ten percent (10%) each responded one hundred percent

(100%) and seventy-five to ninety-nine percent (75 – 99%) of the loan applied was

granted.

Page | 22

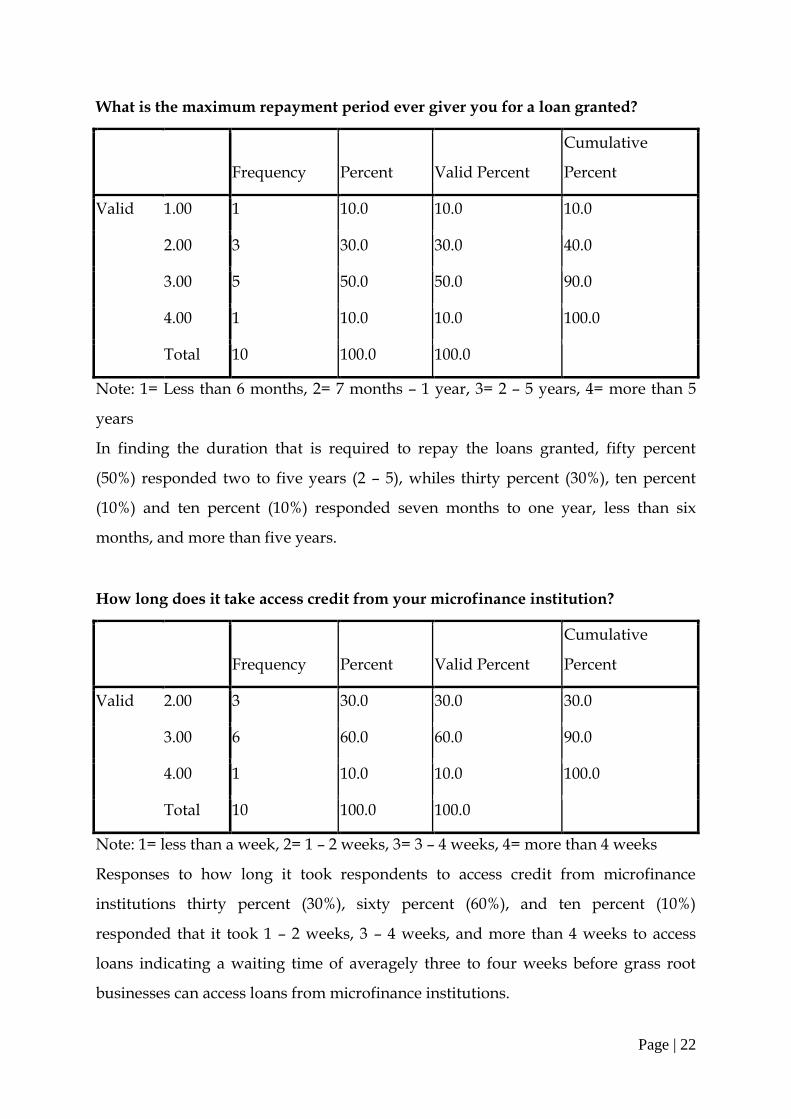

What is the maximum repayment period ever giver you for a loan granted?

Frequency Percent Valid Percent

Cumulative

Percent

Valid 1.00 1 10.0 10.0 10.0

2.00 3 30.0 30.0 40.0

3.00 5 50.0 50.0 90.0

4.00 1 10.0 10.0 100.0

Total 10 100.0 100.0

Note: 1= Less than 6 months, 2= 7 months – 1 year, 3= 2 – 5 years, 4= more than 5

years

In finding the duration that is required to repay the loans granted, fifty percent

(50%) responded two to five years (2 – 5), whiles thirty percent (30%), ten percent

(10%) and ten percent (10%) responded seven months to one year, less than six

months, and more than five years.

How long does it take access credit from your microfinance institution?

Frequency Percent Valid Percent

Cumulative

Percent

Valid 2.00 3 30.0 30.0 30.0

3.00 6 60.0 60.0 90.0

4.00 1 10.0 10.0 100.0

Total 10 100.0 100.0

Note: 1= less than a week, 2= 1 – 2 weeks, 3= 3 – 4 weeks, 4= more than 4 weeks

Responses to how long it took respondents to access credit from microfinance

institutions thirty percent (30%), sixty percent (60%), and ten percent (10%)

responded that it took 1 – 2 weeks, 3 – 4 weeks, and more than 4 weeks to access

loans indicating a waiting time of averagely three to four weeks before grass root

businesses can access loans from microfinance institutions.

Page | 23

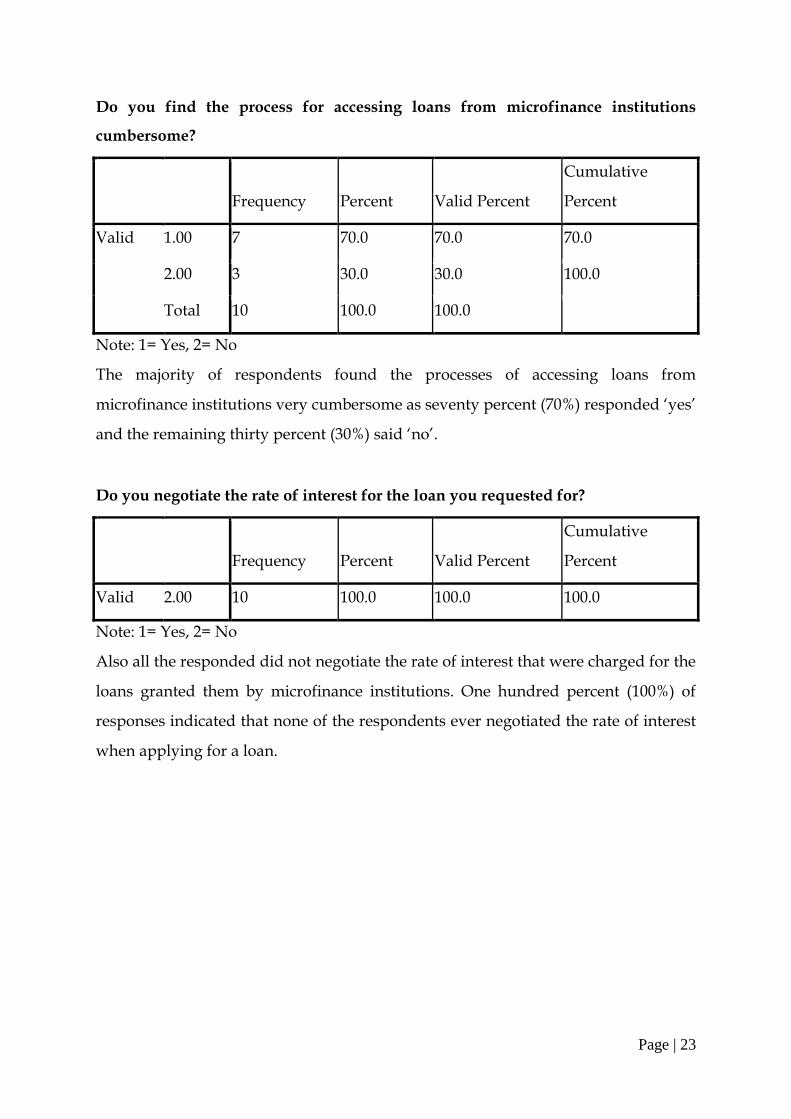

Do you find the process for accessing loans from microfinance institutions

cumbersome?

Frequency Percent Valid Percent

Cumulative

Percent

Valid 1.00 7 70.0 70.0 70.0

2.00 3 30.0 30.0 100.0

Total 10 100.0 100.0

Note: 1= Yes, 2= No

The majority of respondents found the processes of accessing loans from

microfinance institutions very cumbersome as seventy percent (70%) responded „yes‟

and the remaining thirty percent (30%) said „no‟.

Do you negotiate the rate of interest for the loan you requested for?

Frequency Percent Valid Percent

Cumulative

Percent

Valid 2.00 10 100.0 100.0 100.0

Note: 1= Yes, 2= No

Also all the responded did not negotiate the rate of interest that were charged for the

loans granted them by microfinance institutions. One hundred percent (100%) of

responses indicated that none of the respondents ever negotiated the rate of interest

when applying for a loan.

Page | 24

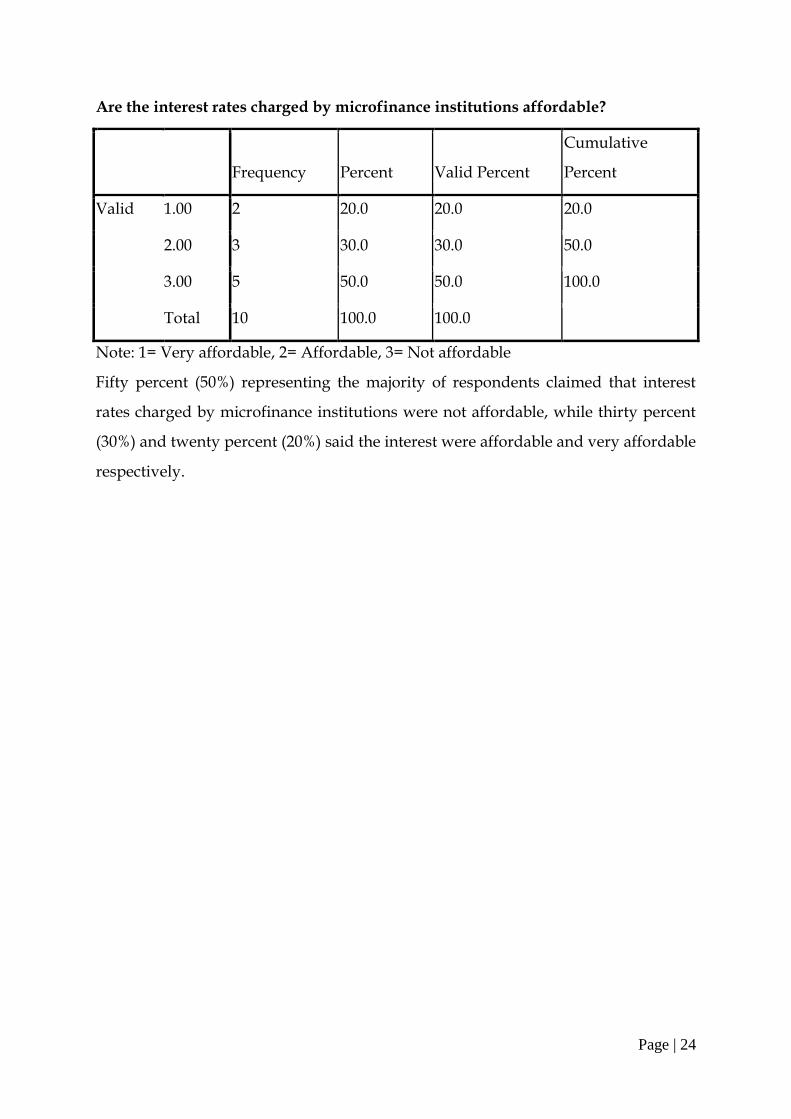

Are the interest rates charged by microfinance institutions affordable?

Frequency Percent Valid Percent

Cumulative

Percent

Valid 1.00 2 20.0 20.0 20.0

2.00 3 30.0 30.0 50.0

3.00 5 50.0 50.0 100.0

Total 10 100.0 100.0

Note: 1= Very affordable, 2= Affordable, 3= Not affordable

Fifty percent (50%) representing the majority of respondents claimed that interest

rates charged by microfinance institutions were not affordable, while thirty percent

(30%) and twenty percent (20%) said the interest were affordable and very affordable

respectively.

Page | 25

Chapter – V

Findings, Recommendations and Conclusion

5.0 INTRODUCTION

This chapter brings to light what the researcher has accomplished in the search for

the factors that influence people‟s attitude to savings and investments in Ghana. It

also provides recommendations to help improve the savings culture of Ghanaians.

Finally, the conclusion and summary of the research findings on the issue are also

outlined.

5.1 FINDINGS

There were numerous factors that contributed to the impact of microfinance

institutions on grass root businesses in Ghana. The study unveiled the following

factors contributing to the statement of the problem.

Microfinance institution as a financial intermediary responsible for reallocating

savings to investment was the main source of capital for the majority of grass root

businesses in Ghana specifically Kumasi in the Ashanti region. This makes the

activities of microfinance institutions critical to the development of these businesses

that needs capital to develop and keep growing. Forty percent (40%) of grass root

business source of capital for their businesses is from microfinance institutions.

These grass root businesses are found of not having adequate capital requirement for

rapid development and growth as eighty percent (80%) of the respondents said that

they did not have adequate capital for their business growth. Relating their capital

inadequacy to their source of financing their capital reveals an important impact of

microfinance institutions creating reliable and affordable funds to assist these grass

root businesses to have an adequate working capital that can grow their businesses

and the local economy.

Page | 26

The data collected also indicates that the majority of grass root businesses with

inadequate capital requirement intend to finance the capital deficiency through

loans. Fifty percent of the respondents responded that their way of getting

additional capital to supplement the working capital deficiency was through loans.

This implied that grass root businesses would fall on microfinance institutions to

give loans for their businesses expansions and developments.

Respondents made it clear that at least all of them had applied for loans from

microfinance institutions before. Sixty percent (60%) of the respondents being the

majority claimed that they had applied at least one to five times (1 – 5) for loans from

microfinance institutions. Ten percent (10%) of the total respondents also responded

that they had applied for loans more than fifteen times from microfinance

institutions.

Out of the number of times respondents applied for loans from microfinance

institutions fifty-one to seventy-five percent (51 – 75%) of the number of times

applied for loans were granted. This represent forty percent (40%) of the total

responses. also fifty percent (50%) of the respondents indicated that less than fifty

percent (50%) of the loans applied were granted. The number of times that loans are

applied for indicates the need for grass root businesses to access financial assistance

from microfinance institutions out of which less than fifty percent (50%) of the

amount of loans applied for are granted.

The loans granted by microfinance institutions are required to be repaid in a

maximum period of two to five (2 – 5) years as representing fifty percent (50%) of the

total responses to what is the maximum repayment period ever given for a loan

granted. This implies that the loans and interest are spread over a maximum period

of two to five years to be repaid by clients.

The lead time for grass root businesses to access loan facility from microfinance

institutions was three to five (3 – 5) weeks. This response represented sixty percent

of the total responses to how long does it takes to access credit from microfinance

Page | 27

institutions. The perception of respondents as to finding the process of accessing

loans from microfinance institutions being cumbersome, it was noted seventy

percent (70%) of respondents believed that the process was cumbersome. Relating

the waiting time in accessing loans and how cumbersome the process of applying for

loans from microfinance institutions creates a challenge for respondents to access

loans from microfinance.

The majority of respondents representing fifty percent (50%) indicated that the

interest rates charged by microfinance institutions were not affordable. Nonetheless,

all of the respondents had never negotiated the rate charged as interest by

microfinance institutions. This indicates clearly that these grass root businesses have

little or no knowledge of being able to negotiate the rate of interest to be charged on

loan facilities requested.

5.2 SUMMARY OF FINDINGS

The impact of microfinance institution has and is very critical in the grass root

development in Ghana. The impact of microfinance institution is not only the

development of the grass root businesses but a direct and indirect development of

the local economy and standard of living. The study unveiled the following impacts:

Well positioning of microfinance institutions would assist the grass root

businesses in raising additional capital requirement for the expansion and

development of their businesses.

Grass root businesses reliance on microfinance was enormous that the

activities of microfinance affected the immediate expansion and growth as

their expansion would be financed by the loans granted by microfinance

institutions.

The duration taken by grass root businesses to access loan facility from

microfinance institutions also influenced their activities by slowing the

progress of expansion as respondents had to wait for an average of three to

four weeks before loans are granted.

Page | 28

Finally, the rate of interest charged by microfinance has been a stumbling

block for many grass root businesses to access loans.

5.3 RECOMMENDATION

In line with the findings of the study, the following recommendations could be made

in increasing and reducing all negative impacts of microfinance on grass root

businesses:

Microfinance institutions should take on financial education to the grass root

businesses on the requirements, documentations and all necessary details

needed to access loans.

Microfinance institutions should modify and reduce the cumbersome nature

of the documentations needed to access loan facilities by grass root

businesses.

Microfinance institutions should assist grass root businesses in enhancing

their managerial skills.

5.4 CONCLUSION

The study was to identify the impact of microfinance on grass root development in

Kumasi a suburb of Ashanti region. The findings therefore suggested microfinance

institutions has played many roles in the development of grass root businesses.

These impacts include the provisions of the start – up capital, working capital

inadequacies, and assisting in the general development of the businesses and

community as a whole. The conclusion that can be drawn about the impact of

microfinance in the development of grass root businesses as being necessary and

critical to the grass root businesses.

Page | 29

REFERENCES

Aguilar, V. G. (2006) “Is Micro-finance reaching the Poor? An Overview of Poverty

Targeting Methods” www.globalnet.org.

Ghana Statistical Service (GSS). Actions and attitudes towards use of financial

services and products,

http://statsghana.gov.gh/nada/index.php/ddibrowser/16/datafile/F4

Jose‟ Maria and Rohito Medhora, Finance and Competitiveness in Developing

Countries, International Development Research Centre, Canada

Aryertey, E. & Nissanke M. (1998) “Financial Integration, Development Libralisation

and Reform in Sub-Saharan Africa”, Routledge: London.

Ms Pallavi Kudal, Financial Systems, Amity University lecture note

Ricky W. Griffin, Management, Sixth Edition, Texas A& M University, Houghton Miffflin Company, Boston, New York

Aryeetey, E. (2008) “From Informal Financing to Formal Financing in Sub-Saharan

Africa”:

Zeller, M. (1994). .Determinants of credit rationing: A study of informal lenders and

formal credit groups in Madagascar,. World Development. 22:12, pp. 1895-1907.

World Bank (2000) World Development Report 2000/01: Attacking Poverty, World

Bank, Washington.

World Bank database, data.worldbank.org/country (accessed march 2014)

Page | 30

Appendix A

Impact of Microfinance on Grass root Businesses

These questions were designed to establish facts about the impact of microfinance on

grass root businesses. The researcher would be very grateful if you could spend

some time to respond to these questions. The result from this questionnaire will be

presented in a thesis. Your answers will be treated confidentially.

Please, tick { } or fill in as appropriate

A. DEMOGRAPHICS (To provide detailed profile of small and Medium Scale

Enterprises)

1. When did your business begin operations?

.........................................................................

2. What was the objective for establishing your business?

…………………………………………………………………………………………

…………………………………………………………………………………………

3. What is your line of Business?

Manufacturing [ ] Commerce [ ] Service [ ] Others (Please

specify)……………………………

4. What is the number of your employees?

Less than 6 people [ ] 6-9 people [ ] 10-29 people [ ] 30 and more [ ]

5. What is (are) the sources(s) of your business start-up capital?

Self [ ] Friends & Relatives [ ] Partnership [ ] Loans from

Microfinance institutions Others (Please specify)……………………….

6. Do you have adequate capital for your business growth?

Yes [ ] No [ ]

7. If NO, in what ways do you intend to acquire additional capital for your

business?

Savings [ ] hire purchase [ ] credit financing [ ] loans [ ]

IMPACT OF MICROFINANCE

8. How many microfinance institutions do you transact business with?

Page | 31

One 1 [ ] two 2 [ ] three 3 [ ] four 4 [ ] five 5 and more [

]

9. Has the availability of microfinance institutions contributed to your

enhancement?

Management skills [ ] financial management [ ] overall management [ ]

none [ ]

10. Have you ever applied for credit facility from more than one microfinance

institution?

Yes [ ] no [ ]

11. What percentage of loan applied was granted?

100 % [ ] 75 – 99% [ ] 50 – 74% [ ] less than 50% none

12. What reason was given for the grant of the percentage of loan applied for?

………………………………………………………………………………………………

………………………………………………………………………………………………

………………….

13. What is the maximum repayment period ever given you for a loan granted?

Less than 6 months [ ] 7 months – 1 year [ ] 2 – 5 years [ ]

more than 5 years [ ]

14. How many times have you applied for loans from microfinance institution?

1 - 5 times [ ] 6 – 10 times [ ] 11 – 15 times [ ] more than 15 times [ ]

15. Out of the number of times you have applied for loans how many were

granted?

25% or less [ ] 26 – 50% [ ] 51 – 75% [ ] 76 – 100% [ ]

16. How long does it take to access credit from your microfinance institution?

Less than a week [ ] 1 – 2 weeks [ ] 3 – 4 weeks [ ]

more than 4 weeks [ ]

Page | 32

17. Do fine the process for accessing loans from microfinance institutions

cumbersome?

Yes [ ] No [ ]

18. Do microfinance institutions always require collateral security (ies) before

granting loans?

Yes [ ] no [ ]

If no why,

…………………………………………………………………………………………..

19. What kind of collateral do they request?

Land [ ] house [ ] car [ ] shop [ ] others

…………………………

20. Do you negotiate the rate of interest for the loan you request for?

yes [ ] no [ ] sometimes [ ]

21. Are the interest rates charged by microfinance institutions affordable?

Very affordable [ ] affordable [ ] not affordable [ ]

22. What are the major challenges you face in accessing loans from microfinance

institutions?

………………………………………………………………………………………………

………………………………………………………………………………………………

………………………………………………………………………………………………

……………………….