Are there long-run diversification gains from the Dow Jones Islamic finance index?

Upload

independentCategory

view

1download

0

Copyright

by

Mohammed El Youssofi Oulad Ibrahim

August, 2014

Funding Social Business: a recognition of Islamic Finance

by

Mohammed El Youssofi Oulad Ibrahim

MSc Thesis

Presented to the Faculty of the Graduate School of Economics

Utrecht University

in Partial Fulfilment

of the Requirements

for the Degree of

Master of Science in International Economics and Business

Utrecht University

August 2014

Dedication

To my mother, Malika

iv

ACKNOWLEDGEMENTS

I would like to thank my supervisor Prof. Niels Bosma for his support and

flexibility when I was having problems in getting to the right direction. I also would

like to thank Fundació Parera, Dr. Hassan Hussein, Dr. Kabir Hassan, Ms. Rachida

Talal, Ms. Ermira Kamberi and everyone who helped me along the way.

My special consideration to all professors and tutors I had since I started

school in Morocco and then when I moved to Spain, Belgium and now here in The

Netherlands.

Thank you mother and father.

v

FUNDING SOCIAL BUSINESS: A RECOGNITION OF ISLAMIC FINANCE

Mohammed El Youssofi Oulad Ibrahim

MSc International Economics and Business

Track IV, International Ventures and Entrepreneurship

Utrecht University School of Economics, 2014

1st Supervisor: Prof. Dr. Niels Bosma

2nd Supervisor: Prof. Dr. Erik Stam

ABSTRACT

Islamic finance and Social Business have been two of the most rapidly growing

business areas over the last two decades. Both fields are distinguished by their

inherent ethical values. Therefore, the purpose of this paper is to explore financial

sources for Social Business and later present Islamic finance as valid funding

instrument and how both could gain from each other. Islamic finance outline is

similar to ethical investing sources, but yet being differently framed. Based on the

literature review and research analysis, the findings of this study reveal a lack of

perception and recognition of Islamic finance. This is probably the first attempt to

associate Islamic finance and Social Business.

Keywords: Islamic Finance, Social Business, Social Entrepreneurship,

vi

TABLE OF CONTENTS

1. Introduction 1 1.1. Social Enterprises 1 1.2. Islamic Finance 2 1.3. Research 3

2. Social Entrepreneurship and Social Business 4

3. Financing Social Business 7 3.1. Conventional financial sources. 8 3.2. Financial instruments with mission alignment. 9 3.3. New financial mechanisms 12

4. Islamic Finance 13 4.1. Sharia’a Law and Ethics 13 4.1. Principles 14 4.2.1. Riba 14 4.2.2. Gharar 15 4.2.3. Impermissible activities. 15 4.3. Instruments 17 4.3.1. Musharakah 17 4.3.2. Mudarabah 21 4.3.3. Murabaha 23 4.3.4. Ijarah 25 4.3.5. Sukuk 26 4.3.6. Qard al Hasan and Zakah 26 4.4. Funding Social Ventures through Islamic Finance 27

5. Research 29

5.1. Methodology 29 5.2. Results 29 5.3. Discussion 31 5.4. Strengths and limitations 33

6. Conclusion 34 REFERENCES 35 APPENDIX. Survey questionnaire 39 GLOSSARY. 43

vii

This page intentionally left blank

1

1. Introduction

During the last century, the result of globalization has become palpable. The

rapid economic growth and further development of welfare system has led to an

unfriendly trade-off: social and environmental damage. According to Oxfam (2014)

about half of the world’s wealth is now held by one percent of the world’s

population. Moreover, one of the main points on the United Nations agenda is to

“provide economic transformation and opportunity to lift people out of poverty,

advancing social justice and protecting the environment” (UN, 2014). This

statement well represents the actual unsustainable economic growth. Global

business practices fall into growth pattern vector and financial profits

maximization with no consideration of the negative social externalities. Contrary

to this trend, recently, moral and ethical values have become driving forces for

social claims. With regard to business practices, social awareness and social value

creation have become central drivers for social entrepreneurship which

experienced a surprising growth (Austin et, al. 2006). Furthermore, other means of

ethical based financial services, such as Islamic Finance (IF), have grown in

attraction over the last three decades. Therefore, it is important to review what

makes Social Enterprises (SEs) and IF such relevant phenomena.

1.1. Social Enterprises

SEs are changing the business framework in which the conventional business

mechanisms and instruments seem not to be generally admitted anymore. Thomas

Dean (2014) argues that “SB’s mission is to create social value and prioritization of

social value creation over the generation of personal or organizational financial

wealth” (p.52). This statement conflicts the values which underlie the foundation

of conventional business. The traditional purpose of business ventures has been

narrowed down to financial values optimization in short-term ignoring broader

repercussion that their activities would have both in space and time. Business

ventures and financial organizations cannot be considered as separate

2

components. They are both part of the same machinery that provides goods and

services to society. An environment where business sponsors steadfastly stick to

the money vector does not seem sustainable. In the same line, Porter and Kramer

(2013) propose the concept of “shared value”, a framework where economic and

social benefits are simultaneously addressed.

1.2. Islamic Finance

IF has become a popular topic in writing and conferences (e.g. Harvard

University Forum on Islamic Finance within the Islamic Finance Project)

attributing its shape to the religio-ethical foundation. Thus, IF rests on Sharia’a-

Compliance and Islamic Ethics principles from teaching of Islam (Taqi Usmani,

2007). The main literature about IF argues that Islam does not consider business

to be something that is impious or damaging to society. According to Islamic

Economics (IE), money does not create wealth beforehand, but it only does when it

is combined with other resources/assets. The most important feature of IF is that

it promotes risk sharing between the investor on one side and the intermediary

and entrepreneurs on the other side.

Since its origins in 1970’s with the establishment of Dubai Islamic Bank as a

private institution and Islamic Development Bank as a multilateral organization,

the growth of the Islamic Finance Market has been determined by the increasing

liquidity in the Gulf region due to high oil revenues, combination of political,

economical and demographic factors (Sayyid Tahir, 2011). The most recent

indicators from different reports estimate a yearly growth of 15 to 20 percent

since 1990 (Ernest & Young, 2014; IFSB, 2013) thus, achieving US$1.7 trillion

assets globally. Even several Western banks, e.g. ABN Amro, Bank of America,

HSBC, either started introducing Islamic Banking branches or even launching IF

products and services to their customers. Islamic Finance Institutions (hereafter

IFI) are still insignificant compared to conventional banking, the US’s 10 largest

banks alone hold over US $4.3 trillion in assets (Khan, 2010). Therefore, it is clear

that IF is willing to become an important player in the future development of the

global financial market.

3

1.3. Research

Considering these two parallel and ethically based practices, this paper aims to

answer the following questions:

- Is IF an appropriate financial instrument for SB?

- Is IF recognized by actors in the SB framework?

Hence, the paper is organized as follows. First, there is a literature review on

Social Entrepreneurship and SB. Second, we review different financial sources for

funding social ventures. Third, IF is analyzed and considered as financial source for

SB. Fourth, we present the research analysis as well as the main results. Fifth, this

section puts together the main findings on the literature review and drawn

research while discussing the research questions. Lastly, we present the

concluding remarks.

4

2. Social Entrepreneurship and Social Business

During the last few decades, Social Entrepreneurship (SE) has made a

significant step in becoming a world phenomenon attracting activists, business

managers, philanthropists and investors worldwide. These new alternative means

of doing business have introduced social purpose and ethical values into the

conventional methods of delivering products or services. Besides, SE as a field of

research is also a relatively recent and active study field. For instance, Thomas J.

Dean (2014) argues that “SE is distinguished by the entrepreneur’s mission to

create social value, and the prioritization of social value creation over the

generation of personal or organizational financial wealth” (p.52).

A prevailing conception of SE is that it is distinguished by business purpose is

to create social value and giving priority to social value creation over financial

profits. However, this variance in conceptualization of SE revels that there is a

fragmented framework and there is a need for a multidimensional model for social

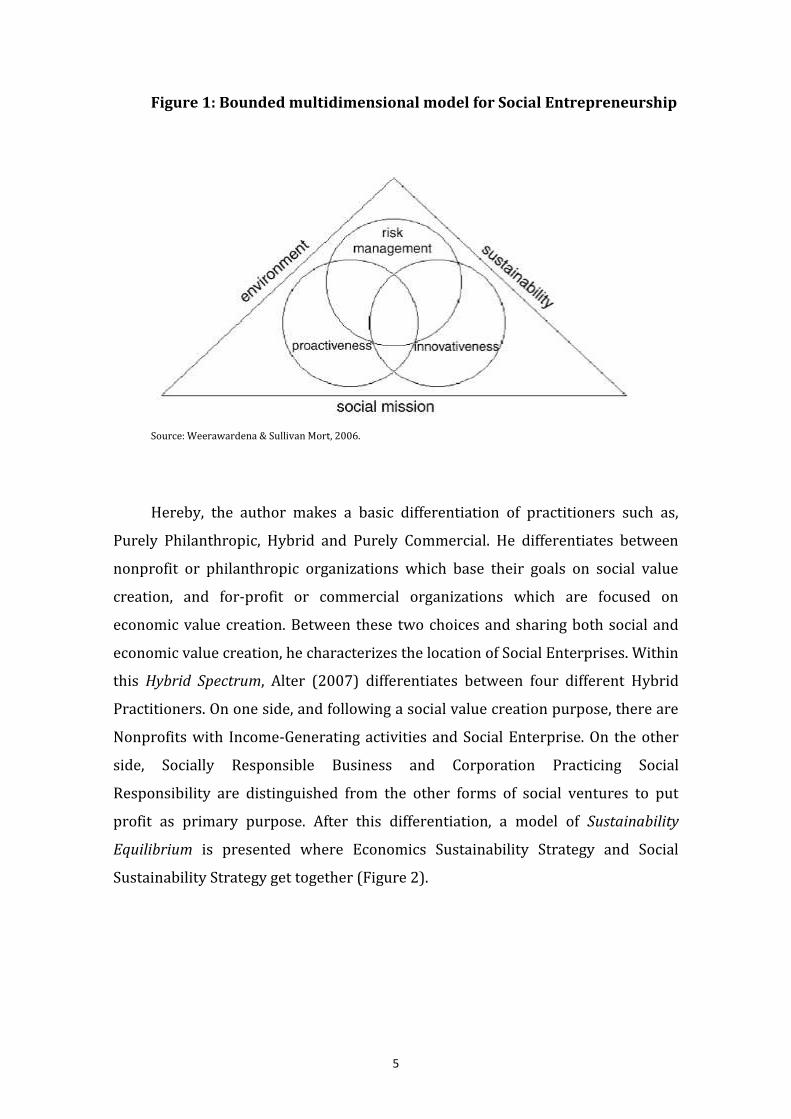

entrepreneurs in which they must operate (Weerawardena & Sullivan Mort, 2006).

In their paper, Weerawardena and Sullivan Mort propose that SE is understood

within a bounded multidimensional figure (Figure 1) that contains innovation,

proactiveness and risk management as three individually allied dimensions.

Together, these characteristics are contextualized under other constraints such

environment, sustainability and social mission. This model is proposed as a

response to opportunities and threats that social entrepreneurs are facing from the

marketplace. Different researches attempted to explain the “marketization” of

social entrepreneurial organizations (Austin, Stevenson & Wei-Skillem, 2006;

Peredo & McLean, 2006; Uygur & Marcoux, 2013) and most of them subscribed the

notion of Spectrum of Practitioners developed by Alter (2007).

5

Figure 1: Bounded multidimensional model for Social Entrepreneurship

Source: Weerawardena & Sullivan Mort, 2006.

Hereby, the author makes a basic differentiation of practitioners such as,

Purely Philanthropic, Hybrid and Purely Commercial. He differentiates between

nonprofit or philanthropic organizations which base their goals on social value

creation, and for-profit or commercial organizations which are focused on

economic value creation. Between these two choices and sharing both social and

economic value creation, he characterizes the location of Social Enterprises. Within

this Hybrid Spectrum, Alter (2007) differentiates between four different Hybrid

Practitioners. On one side, and following a social value creation purpose, there are

Nonprofits with Income-Generating activities and Social Enterprise. On the other

side, Socially Responsible Business and Corporation Practicing Social

Responsibility are distinguished from the other forms of social ventures to put

profit as primary purpose. After this differentiation, a model of Sustainability

Equilibrium is presented where Economics Sustainability Strategy and Social

Sustainability Strategy get together (Figure 2).

6

Figure 2: Sustainability Equilibrium

Source: Alter, 2007.

Peredo and McLean (2006) also argue that clear distinction between for-

profit and non-for-profit enterprises in the case of SE becomes attenuated.

Furthermore, Johnson (2000) adds a new dimension of public-private when he

mentions “Socially entrepreneurial activities blur the traditional boundaries

between the public, private and non-profit sector, and emphasize hybrid models of

for-profit and non-profit activities” (p.1). Above all, the range of Social Enterprises

can vary from community organizations to a global-scale corporation. They could

be shown as innovative not-for-profit to hybrid for profit organizations. The

inherent obligation to provide social value is what creates the gap between social

and other forms of entrepreneurship (Peredo & McLean, 2006).

In this sense, the specific business model of SE is explicitly addressed to a

particular source of funding based on capacity to generate income/profits and

intensity of providing a social value.

7

3. Financing Social Business

From the Hybrid Spectrum presented by Alter (2007), it has been shown that

Social Enterprises might be characterized differently according to their social and

economic strategy. Depending on what economic and social values the enterprises

create, social entrepreneurs may face more difficulties in mobilizing financial

resources (Certo & Miller, 2008). Peredo and Mclean (2006) criticize the notion of

social entrepreneurship when social goals are subordinated to profit seeking.

Considering the non-profit branch of Social Enterprises (Alter, 2007), there is a

discussion among scholars about the revenue contribution of earned-income

(Anderson & Dees, 2002; Austin et al., 2006; Forster & Bradach, 2005). Firstly,

Anderson and Dees (2002) disclaim that earned income generation, result of a

commercial exchange, is indispensable for social entrepreneurship. They argue

that “Social entrepreneurship is about finding new and better ways to create and

sustain social value” (p.192). In the same way of thinking, Foster and Bradach

(2005) propose that pursuit of earned income might conflict with the

organization’s mission. Notwithstanding, others argue that social and commercial

entrepreneurship have similarities regarding resource mobilization (Austin et al.

2006). What essentially differentiates their ability to mobilize financial resources

are the inherent strategic rigidities and the organization’s ambitious goals. This

paradox of “money or mission” has been addressed by Weerawardena and Sullivan

Mort (2006) concluding that the demands of the marketplace cause a direct

competition between organizations maximizing profits and those maximizing

social value creation.

Given these constraints, social entrepreneurs could not afford to pay market

rates for traditional funding (e.g. Angels, Venture Capitalists or Banks) depending

on the constitution of the Social Venture (see Hybrid Spectrum). Consequently, a

social entrepreneur requires seeking for financial sources that are, before all else,

interested in creating social value/impact and also aligned with the organization’s

pursue of earned income. This is, some funding instruments could better favor

non-profit forms of social ventures while others would better opt for commercial

social ventures with a more complex earned income structure. The following

paragraphs will introduce the financial instruments spectrum for social ventures,

8

some of which have emerged relatively recently, yet experiencing a rapid

development and raising the chance for financing organizations with greater social

and environmental impact.

3.1. Conventional financial sources.

Dean (2014) and Tulchin and Yi-Han Lin (2012) agree with these four

different traditional financing outlets: bootstrapping, financing from cash flow (or

internal financing), financing from debt and financing from equity. These financing

instruments do not differ between social and conventional businesses. Firstly,

bootstrapping refers to those tools that help to decrease, postpone or even

eliminate financial needs, such as, cooperation with other organizations to

exchange services/products or free of charge provisions looking for a future

contract. Also, some organizations tend to offer free advice or consultancy to

social ventures willing to create a partnership aligned with their Social Corporate

Responsibility (CSR) strategy. Secondly, cash flow financing is related to the

treasury department of the business. It has much to do with the capacity of the

venture to generate earned income. The faster the clients pay what is owed, the

better for the financial capacity. Payment on delivery, pre-sell or discounts are

some incentives for cash flow financing. The inverse tactic is used for accounts

payables. Thirdly, banks and credit unions provide debt financing requiring a

monthly payment of principal and interests. It requires a relationship to be built

and a track record. Therefore, in case of social entrepreneurs, it may be expensive

and difficult to get, unless the founders have collateral to offer. Finally, equity

financing implies a sell of part of the company to equity investors. This does not

require regular payments but ownership. The investors gain some voting rights

and board positions in the organizations. This fact may put the venture’s mission in

risk since investors may protect their investments. On the other hand, investors

might bring skills, network or even other sources which could become a valuable

asset. This mode of financing may conflict with the leadership approach of social

ventures. Strategic investors (corporations), angel investors, venture capitalists

and friends or family are considered equity investment (Dean, 2014).

9

Except of bootstrapping financing, the rest of the conventional sources

mentioned above hardly match with the business model of social venture. Unless

the purpose of for-profit social ventures with high capacity is to generate earned

incomes, conventional funding may be financially difficult to reconcile with the

cost structure of the organization due to the inherent social mission. Moreover,

both debt and equity financing imply a capital pressure which goes against SB

singularity (Peredo & McLean, 2006).

3.2. Financial instruments with mission alignment.

Besides conventional funds, other finance providers have developed

specialized instruments and financial services that address the particular needs of

social entrepreneurs. Social ventures face the same finance challenges that

traditional for profit enterprises struggle with, along with the added value of social

mission. Wuttunee et. al (2008) point out that “Balancing the demands of the

market place against the demand of the social goals is a big challenge. If small

business is risky (and it is, especially in the start-up stages), then social enterprise

is more so” (p.1). Therefore, mission financing fills the gap that conventional

financing suffer harmonizing with organization’s social and economical values. The

appropriate fund will vary, depending on the SB model and stage of development.

Finance providers with mission alignment and better understanding of social

enterprises include: Microfinance, Ethical Banks, Social Investors and

Philanthropic grants.

Microfinance. There is no common definition of microfinance, but is well

known as financial services for lower-income people who lack access to capital

(Mckee, 2008). Back in the 1970s, The Nobel laureate Muhammad Yunus, broadly

known as one of the founders of microfinance, started providing small loans to

woman in rural areas in Bangladesh. After a significant growth and success, Yunus

found the Grameen Bank to scale impact and reach more women in need of small

loans for starting micro-enterprises. This financing model has been replicated by

others to make an impact worldwide (e.g. Kiva). Without an accurate impact,

different sources estimate that microfinance could have reached between 100 and

10

500 people (Christen et al., 2004; Sample, 2011). However, Mersland and Oystein

Strom (2007) concluded that corporate governance in microfinance institutions

requires improvements to achieve greater impact.

Sustainable and social/ethical Banks. According to the Institute for Social

Banking, “Social Banking describes a provision of banking and financial services

that consequently pursue, as their main objective, a positive contribution to the

potential of all human beings to develop, today and in the future”. Also, the global

financial crisis has triggered a growing level of awareness among banking

customers. These banks differ from mainstream banks in social purpose, being less

speculative, more responsible, ethical, and community oriented (Goyal and Joshi,

2011).

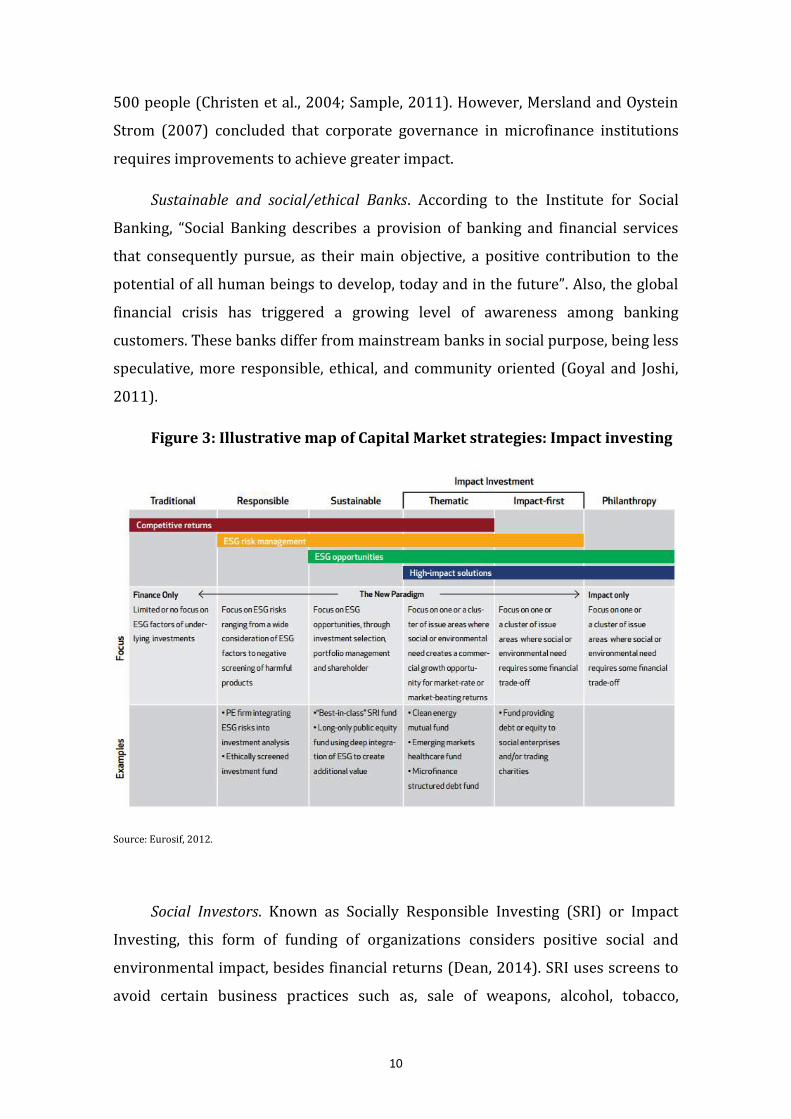

Figure 3: Illustrative map of Capital Market strategies: Impact investing

Source: Eurosif, 2012.

Social Investors. Known as Socially Responsible Investing (SRI) or Impact

Investing, this form of funding of organizations considers positive social and

environmental impact, besides financial returns (Dean, 2014). SRI uses screens to

avoid certain business practices such as, sale of weapons, alcohol, tobacco,

11

gambling or nuclear energy, encouraging investment for positive change including

protection of human rights, environmental stewardship or fair trade. The

difference between impact investment and other strategies are illustrated in

Figure 3. The range of impact investors vary from investment funds, foundations, to

even banks and corporations providing funds for social ventures (Tulchin and Yi-

Han Lin, 2012).

Philanthropic grants. Mainly focusing on non-profit forms of social ventures,

different organizations and individuals provide money contributing greatly to

social and environmental causes. For grant donors, the value proposition is the key

point. Therefore, being able to track and measure impact is critical (Dean, 2014).

Nicholls (2009) presents a fluid, contingent and dynamic reporting approach:

Blended Value Accounting. This landscape of social impact reporting could be

important for winning and maintaining donor contributions over the long term.

Social investment bonds (SIBs). This emerging innovative idea is gaining

attraction in USA and the UK. It brings the private investment funds to the field of

policy making. In essence, Warner (2013) describes SIB’s as “a form of outcome-

based contract between public or non-profit service provider and private

investors, in which private financiers provide upfront funding for interventions to

improve specific targeted social outcomes”(p.303). The notion behind SIBs is that

it could avoid future high social costs (e.g. offender rehabilitation) through

anticipating investments and undertaking prevention programs with performance

measurement. Liebman (2011) argues that SIBs only works for projects with the

following features: (1) high net benefits and short term payout, (2) excellent

performance measures, (3) clearly defined treatment population to avoid cream

skimming and encourage integrated programs that meet multiple needs, and (4)

credible impact assessment – randomized and quasi-experimental with a neutral

authority.

Crowdfunding. Crowdfunding, an emerging and dynamic new channel to

access capital, refers to a collective cooperation, participation and trust by people

who network and pool money and/or other resources, usually through internet, to

support a project or venture (Tulchin and Yi-Han Lin, 2012). The potential of

internet makes available capital affordable for individuals, ventures and

12

communities. Therefore, crowdfunding activities are also demonstrated to have a

global scope through internet and social media platforms. In this domain, Agrawal

et al. (2011) state that “crowdfunding platform eliminates most distance-related

economics frictions normally associated with financing early state projects, such as

acquiring information, monitoring progress, and providing input” (p.3). Therefore,

crowdfunding appears to well fit social enterprises, which are also widely

dispersed (Lehner, 2013). In addition, Lehner (2013) advocates that

crowdfunding brings together people’s values and alternative reward systems with

social entrepreneurs. Hence, in theory crowdfunding should match social

entrepreneurial initiatives (Dart, 2004) because it offers a solution to financial

needs of social enterprises, as the crowd does not look at collaterals but at the core

values and legitimacy of the firm (Lehner, 213).

3.4. Islamic Finance

Several scholars have already discussed the similarities and relationship

between IF and Socially Investing, and therefore, Social Entrepreneurship.

Novethic (2009) argues that ethical principles in Islam strongly fit with the values

behind SRI. For others, it is not evident that Muslims act more socially responsible

(e.g. regarding the environment) because of the religious duty (Brugnoni, 2009).

Considering the teachings of Koran (Holy book of Islam), Islam preaches ecological

behavior, kindness, labor rights, social justice and sustainability (Jaufeerally,

2011). In spite of the gaps and perplexity in IF , this should not obscure the fact

that it could achieve an important performance in SB. The following section

deepens the phenomenon of IF as a mean for social entrepreneurship.

13

4. Islamic Finance

The IF industry is one of the fastest growing segments of the global Financial

Industry attracting considerable interest and participation from governments and

financial institutions from both the Islamic World and beyond (IFSI, 2013; EY,

2014). Several countries are actually starting to embrace the industry by making

the necessary adaptations to their regulatory and fiscal frameworks. The former

Chief Executive of TheCityUk, the organization supporting the financial industry in

the UK, claims that the pre-eminent position as the leading Western center for IF

can be seen not only in business but also in London’s position at the heart of the

market (Maslakovic, 2013).

IF represents a way of conducting financial transactions that are complained

with Sharia’a or Islamic Law. However, Jaufeerally (2011) mentions that “Islamic

Banking is obsessed with the idea of Riba and (conveniently?) ignores the social

objectives of Sharia’a”(p.163).

4.1. Sharia Law and Ethics

The Sharia’a or Islamic Law is essentially derived from four different sources

(Kamali, 1991). The first source is the Qur’an or The Holly Book of Islam

understood as the literal words of Allah (God). The second source comes from

Sunnah, the sayings, actions and approvals of the Prophet Mohammad (PBUH).

Ijmah is based on the consensus that has been reached on a particular issue by

Islamic Scholars and theologians through history. The last source is based on Qiyas

which is understood as analogy. These are rulings on issues where there is no

explicit guidance in the Qur’an or Sunnah and therefore, they are derived by

qualified scholars or reference to rulings related to similar issues. So, the scholar’s

role is to utilize all these sources to create a framework of Islamic Law collectively

known as Sharia’a. Furthermore, a critical analysis of the progress, growth and

operational tools of Islamic Banks warns about the use of Sharia’a as a reduction of

legal framework not related to human life (Asutay, 2012; Sarially, 2005; Khan,

2010; Tahir, 2011). For this, Asutay (2012) elude the Islamic Moral Economy as a

Sharia’a based framework in which Islamic Banking and Finance (IBF) should be

articulated in order to express the distinguishing nature of IBF as a valued

14

proposition. Therefore, ethical values are inherent in IF opening to interest of

rising number of investors and customers a seeking for socially responsible funds

(Elmelki & Ben Arab, 2009).

4.1. Principles

The principles begin on the premise that all contracts are permissible if the

Sharia’a violation is proved. This is demonstrated through the Prophet Mohammad

(PBUH) who either approved the practices which were already prevalent in his

lifetime or made changes in the prevailing contracts of that time by adding

additional conditions. A fundamental concept of Sharia’a is an idea that any

arrangement leading to prohibited practices is also prohibited. Overall, the

conclusion is that the focus is on identifying what should be avoided, rather than

which practices should be done.

In essence, Sharia’a has identified the minimum rights and responsibilities of

each party involved in a contract. This means that no party could contractually

bound to bear the responsibility of the other party and similarly no one can be

deprived of their minimum rights. If this is not adhered to, and there is a change in

the distribution of rights it will derive the contract impermissible. For instance, in

the lease agreement, all risks cannot be transferred to a lessee, or, in a partnership

agreement losses must be shared in accordance with the ratios of the capital

invested.

There are three key prohibitions: Riba (Interest), Gharar (Uncertainty) and

any kind of impermissible activity according to the Islamic Law (Usmani, 2007;

Iqbal & Mirahor, 2007; Vicary Abdullah & Chee, 2010; Bendjilali, 2000).

4.2.1. Riba

This feature is perhaps the most well known prohibition in IF. It refers to any

stipulated increase over and above the principle in a loan or debt transaction. It

should not be confused with a sale of an item on a deferred payment for a price

higher than the spot price which is allowed as long as the price is not linked with

the time for repayment. For instance, the following two scenarios given a car

15

purchasing show the main essence of Riba. On one side, the seller of a car gives the

buyer two options: one single payment now for €10k or separate payments over

12months for €12k. In this case the buyer chooses buying over 12months which

becomes contractually (legally) binding. On the other hand, the seller offers three

following payment schedule. The buyer could buy now for €10k. If he/she pays

over one year it would be €12k . However, if the payment is done in two years it

would increase to €14k. In this case, the buyer agrees to this arrangement without

being required to stipulate the chosen option. In this example, the first scenario

would be committed. However, the second scenario would not be a Sharia’a

compliant transaction as it would contain elements of uncertainty leading to Riba.

This example helps us to understand the economic consequences of transactions

that are not determinant of Sharia’a compliant. Two transactions may look the

same economically; however, the form in which transactions are taken would have

a direct impact on its Sharia’a compliant status.

4.2.2. Gharar

It is commonly translated as uncertainty and it has a broad meaning and

application. Gharar refers to situations and contractual arrangements that can be

viewed as unclear, deceitful or disproportionally risky. In the case of financial

transactions, Gharar can arise due to several reasons. First, the subject matter of

the sale transactions does not exist at the time the transaction is due to take place.

An example of this would be the sale of expected future crop of a specific field.

Second, the seller may not to be in a position to deliver the item upon sale. This

could be the case of selling an item before it is in one’s possession. Third, if the

terms of the sale contracts are not sufficiently defined and there is still space for

ambiguity. This is the case when conducting a sale on credit without specifying the

maturity date of the contract.

4.2.3. Impermissible activities.

The third prohibition stated earlier is engaging in financial transactions

which involve dealing with impermissible activities as defined by Sharia’a. This

16

includes all conventional insurers, banks or financial organizations whose

principle activity is conventional finance. Any company involved in any part of

alcohol supply chain including producers, distributors, and liquor stores.

Additional attention should focus on businesses deriving substantial income from

this area such hotels, bars and restaurants. Also, those companies involved in

production, distribution and sale of Non-Halal (prohibited according to Sharia’a)

products. And last, businesses involved in gambling, such hotels or casinos, and

adult entertainment (pornography) are totally banned from Sharia’a Law, and

therefore, not acceptable to be part of any kind if transaction with Islamic Banks.

The Sharia’a Law has defined some additional prohibitions that may be

avoided in financial transactions. Many of these derive from the fact that in Islamic

practices the seller has a degree of duty of care towards the ultimate purchaser.

These additional elements are conceived from deceiving or fraudulent practices

whatever form they may take. Selling something for an extra ordinarily high price

to an uninformed client or who relies on the sellers’ quotation. In addition, IF

prohibits practices or actions by parties to a transaction or any outside parties that

disturb the process of free negotiation. The is a specific prohibition regarding the

hoard basic needs such a food items for creating artificial shortage that can be

profited from.

In conclusion, IF provides a holistic set of principles from which one can

conduct financial affairs. Its overall aim can be seen to satisfy the following key

objectives:

Transparency. It is an important aspect of IF . As such, all parties must be

aware of all details of transitions that they are into.

Socially responsible. Many of the industries that are prohibited include those

which are known to have a detrimental societal impact.

Financing the real economy. All transactions in IF must be underpinned by

real assets.

Curbing speculation. IF seeks to curb speculative behaviour that may have a

detrimental impact on the economy and society at large.

17

4.3. Instruments

In accordance with the above mentioned principles and key objectives, IF

industry has been developing a diverse range of financial instruments (IIFM, 2012;

Usmani, 2007; Iqbal & Mirahor, 2007; Deloitte, 2014).

4.3.1. Musharakah

From a linguistic approach, the meaning of Musharakah is understood as

sharing or merging. With respect to IF, it represents the co-mingling of money,

work or obligations of two o more parties in order to earn a profit, yield or

appreciation in value. And, equally important, it implies a share in any losses that

are incurred according to their proportional ownership.

Figure 4: How does Musharaka work?

Source: Deloitte, 2014.

The case presented in Figure 4 illustrates how Musharakah agreement

works. In this case, Investor A and B decide to enter into a Musharakah business

venture. Both parties agree to contribute a specified amount of capital or other

18

assets in kinds towards this business venture. Subsequently, if the business is

successful and generates profits then this would be shared between the investors

in a pre agreed ratio. It is important to know that there are very specific rules

regarding to Musharakah arrangement that must be adhere to if the agreement is

deem to be valid. The rules are classified in five different categories: capital,

management, profit & loss, settlement and security.

Capital. The capital that can be used within the Musharakah can be liquid

form or can be goods in kind, for example, providing inventory to a venture.

Regardless of the form that the capital takes, it must be both quantified and

specified. In the case of cash or receivables, this will naturally be straightforward.

If fixed assets are contributed the value might be mutually agreed by all the

parties.

Management. The normal principle of Musharakah is that each parent is

entitled to take part of its management. However, the partner might agree that the

management should be carried out by only one or more of them by mutual

consent. Also, one or more partners may decide to be a silent partner and not

participate in the management scheme.

Profits & Loss. There are several rules regarding how profits and loss are

shared under Musharakah agreement. Firstly, prior to commencing the

Musharakah venture, all parties should agree amongst each other as the precise

sharing ration. The ratio of profits for each partner must be determined in

proportion of the actually profits accrued to the business and not in proportion to

the capital invested by them. In this case, if it is agreed that Investor A will get 5%

of its initial investment amount every year, then this is not valid according to

Sharia’a Law. Neither is valid to fix a lump sum amount for any of the partners. For

example, if Investor A is offered €1k as their share of profit with the rest going to

Investor B, this agreement would not be permitted. It is not necessary for the

shares to be in proportion of the capital contributed, unless the partners agree to

this. If the partner agrees not to work for the Musharakah venture and remains as

silent partner, then their share of profits cannot be more than the ratio of their

investments. The partners may, at the latest stage, agree to emend the percentages

19

of their profits and partners may surrender a part of their profits in favour of

another partner if they so wish.

Profit shares can be either fixed or variable and can be capped at a certain

amount of money. In any given year, the partners may decide not to distribute all

or a proportion of the profits retaining it instead within the venture. The final

allocation on profit should not be based on expected profit. However, it is

permissible to distribute a provisional profit, subject to final settlement.

All partners will have to share any losses in the exact amount of proportion to their

investment. Given this statement, if Investor A and B have invested half of the

capital each, they must suffer any losses in the exact proportion. If this condition is

not satisfied, the Musharakah contract will result being invalid. Furthermore, the

principle of Profits and Loss sharing can be summarized as “loss is distributed

exactly according to the ratio of investment and the profit is divided according to

the agreement of the partners”.

Settlement. Each of the partners is entitled to terminate the partnership

with prior notice or when set conditions have been met. These include, if the

continuity of the partnership is compromised after the withdrawal of one of the

partners, when the partnership was set for a limited timeframe only, when the

purpose of forming the partnership has been achieved, in case of death of any of

the partners or in case of insolvency. For dissolving this partnership, if the assets

are liquidated, they should be distributed pro-rata between the partners. However,

the partners may choose to distribute the assets as they are. If a partner wants to

terminate while the other partners want to continue the partnership, then this is

only possible upon an agreement of all parties involved. The partners willing to

continue the business would be required to purchase the share of the leaving

partner at the price determined by mutual consents. If there is a dispute about the

valuation of the share, the leaving partner has the option to compel the other

partners to liquidate the business.

Security. In principle, a partner cannot demand that another partner

provides security in any form. This is because all the rights and obligations of all

the partners towards Musharakah agreement are the same. Consequently, in all

20

dealings they will act as agents for each other. In the case of Musharakah between

the bank and its client, the bank shall in its own right to obtain adequate security

from partners against misconduct and negligence to ensure the safety of the capital

invested.

Besides the above described form of Musharakah agreement, other common

form of the Musharakah contracts is Diminishing Musharakah. Under this

agreement, a financier and client agree to enter into a partnership agreement

whereby they assume a join partnership of a property, equipment or participate on

join commercial enterprise. The share of the financier is subsequently divided in

smaller number of units. It is there mutually agreed that the client would

periodically purchase these units. In doing so, the share would increase until all the

units from the financier are purchased. This would signify the end of the

Musharakah agreement. The timeline becomes a core difference in between the

Musharakah and Diminishing Musharakah agreements. One of the primary use of

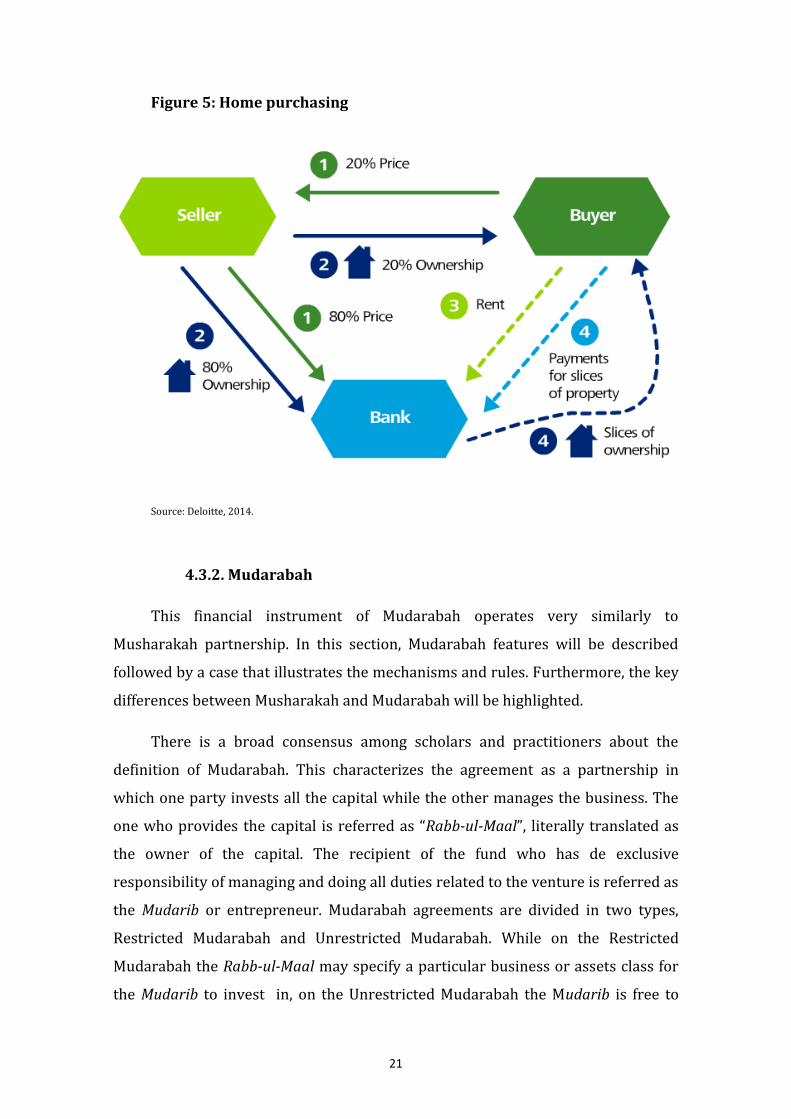

Diminishing Musharakah has been in real-estate financing. The example illustrated

on Figure 5 shows how this financing instrument works. The Buyer wishes to

purchase a property for which does not have funds. For doing so, he decides to

approach the Bank and both agree a Diminishing Musharakah agreement for

purchasing the property. At the beginning, the Buyer invests 20% of the value and

the 80% remaining are funded by the Bank. Thus, the bank will own 80% of the

asset and the Buyer the other 20% rest. After purchasing the asset jointly, the

Buyer pays a rental fee in exchange of using the 80% of the Bank property jointly

with the payments of slices of property in exchange of shared of the property. By

each time the Buyer buys a share from the Bank the ownership is transferred from

one to the other and subsequent the rent also decreases due to lower ownership of

the Bank in the property. This process will continue until the end of the stipulated

Diminishing Musharakah agreement period when the client has effectively

purchased the entire share from the Bank.

21

Figure 5: Home purchasing

Source: Deloitte, 2014.

4.3.2. Mudarabah

This financial instrument of Mudarabah operates very similarly to

Musharakah partnership. In this section, Mudarabah features will be described

followed by a case that illustrates the mechanisms and rules. Furthermore, the key

differences between Musharakah and Mudarabah will be highlighted.

There is a broad consensus among scholars and practitioners about the

definition of Mudarabah. This characterizes the agreement as a partnership in

which one party invests all the capital while the other manages the business. The

one who provides the capital is referred as “Rabb-ul-Maal”, literally translated as

the owner of the capital. The recipient of the fund who has de exclusive

responsibility of managing and doing all duties related to the venture is referred as

the Mudarib or entrepreneur. Mudarabah agreements are divided in two types,

Restricted Mudarabah and Unrestricted Mudarabah. While on the Restricted

Mudarabah the Rabb-ul-Maal may specify a particular business or assets class for

the Mudarib to invest in, on the Unrestricted Mudarabah the Mudarib is free to

22

undertake whatever business decision in order to maximize the value, always

according to Sharia’a Law principles. Subsequently, if the venture is successful and

generates profits (Figure 6), then this would be shared between both partners as

agreed on the outset of the venture.

Figure 6: How does Mudarabah works?

Source: Deloitte, 2014.

Many of the rules of Mudarabah are shared with the Musharakah partnership

as covered in the previous section. However, Mudarabah has specific rules relating

to how the parties can be remunerated or profits can be shared. (i) All parties must

agree on the definite proportion of the actual profit to which each one of them is

entitled to. In case of non explicit proportion was mentioned when the parties

entered the Mudarabah arrangement, then it presumed that each of the parties will

get exactly the same proportion of the profits. (ii) Incentives may be given to the

Mudarib as bonus to encourage positive behavior, such achieving targets. (iii) A

very important feature of Mudarabah settles in the idea of work remuneration is

not allowed. The Mudarib, apart from the agreed profit share, cannot claim any

periodical salary for the work done. (iv) The parties involved cannot allocate a

lump sum amount of profit for either of them neither can they determinate the

share of any party at a specific rate tied with the capital invested.

23

Although there are very similarities between Musharakah and Mudarabah, on

Figure 7 the main differences are described. From the investment side, in

Musharakah all parties are required to invest while in Mudarabah this is a sole

responsibility of the Rabb-ul-Maal. In Musharakah all partners can participate in

management of the business, however, the Rabb-ul-Maal has no right to

participate in Management on Mudarabah partnership. The liability of the parts is

normally unlimited in Musharakah agreement buy, in case of Mudarabah, the

Rabb-ul-Maal is liable to the extent of his investment. Generally the Rabb-ul-Maal

incurs all financial losses while Mudarib losses this efforts. Finally, in a

Musharakah all assets of the venture become jointly owned. Thus, all partners can

benefit from profit gained through appreciation in value of investment.

However, in this is not the case of Mudarabah where the assets and goods are

owned exclusively by the Rabb-ul-Maal. Therefore, any appreciation in the value of

the assets will be attributed to the Rab-ul-Maal.

Figure 7: Differences between Musharakah and Mudarabah

Source: Deloitte, 2014.

4.3.3. Murabaha

The financial instrument of Murabaha is a particular kind of sale where the

seller particularly discloses their own cost in acquiring the goods being sold when

24

selling to another entity. An agreed profit mark-up is added to this cost by the

seller. This type of transaction is based in different principles. First, the subject of

the sale must exist when the sale takes place. In addition, it must have some

intrinsic value. Secondly, transparency is vital. Therefore, not only the price should

be certain, but the goods sold must be acquired by a valid contract with the seller

disclosing and defects/faults of good. Third, any sale must be instant and absolute,

and involving the full transfer of all the rights and responsibilities associated with

the subject matter of the sale. If any of these above conditions are not met, the

buyer has the right to either proceed, cancel the contract or take a legal recurs

against the seller for any discrepancy.

The following example helps to better understand the role of the Islamic

Bank in a Murabaha transaction. The Islamic Bank purchases a good from a

supplier in return of an agreed purchase price. Once the commodity is in position

of the bank, this sells the good to the customer for a predetermined sale price plus

the agreed profit mark-up. Then, the bank and the customer will agree to defer the

payment of the sale price, either to be paid in terms or at a fix point time of the

future. When the sale is concluded, as well as the risk, is transferred to the

customer.

Thus, a purchase order Murabaha is a sale transaction where a party asks the

other to purchase an asset on their behalf; and then sell it to him on an agreed

payment method. These types of transactions are meant to mitigate the risk of the

bank when buying and selling goods. They are normally conducted in three

different states. Prior to any transaction, the Islamic Bank will consider a request

from a customer who is seeking finance to buy an asset. Then, the asset is

purchased from the vendor by the bank through a sale contract. Finally, the

customer will be obliged to fulfil his promise to acquire the good as agreed in the

initial request. However, in case of dispute between the customer and the bank,

there are different tools to secure the transaction.

It is often compared Murabaha to a Short Term conventional lending (Figure

8) On one hand, it is true that, from an accounting point of view, they are both

considered as receivables (debt) on the bank books and also there is a collateral

agreement to secure the repayments. On the other hand, on the Murabaha

25

agreement there is a sale of a tangible asset when the conventional loan consists of

an advancement of money. Also, the Islamic Bank uses a profit margin tool in order

to charge for services but, the conventional bank uses interest rates. Another

important difference is that the lender has an option to charge a penalty if there is

a delay on repayment on conventional loans, which does not happen in Murabaha

transaction. Then, in terms of risk that the bank would be exposed to under either

Murabaha or conventional loan, both would be exposed to underlying credit risk.

However, is short term loan there is an additional interest risk to consider, which

is not applied in the case of Murabaha agreement.

Figure 8: Murabaha vs. Short Term Loan

Source: Deloitte, 2014.

The Murabaha financing it could also be performed in reverse. If an investor

wants to invest in a bank, this will purchase a commodity and sell it to the bank at

cost plus profit. Then, the bank will repay the agreed price over a period of time.

4.3.4. Ijarah

The popularity of Ijarah is due to its strong parallel to the conventional

leasing contracts, representing one of the most common modes of IF instrument,.

Similarly to leasing contracts, the Islamic Bank purchases a particular asset from a

26

supplier to transfer its usufruct to a customer in exchange of an agreed rental

payment. The transaction requires a transfer of rights over the asset at the end of

agreement. However, there are few principles that Ijarah contract needs to fulfil in

order to meet the requirements of Sharia’a Law. Considering the two parties, it is

possible for the lessee to sell the asset to the bank in the first transaction and then

lease the asset back on condition that both transactions need to be independent.

Also, it is allowed for the lessee to keep part of the ownership in the leased asset

with the lessor. The subject matter of the Ijarah contract must have some intrinsic

value and should be specifically identified and quantified to avoid any ambiguity in

the contract.

4.3.5. Sukuk

Sukuk is understood as the Arabic term of financial certificate and can be

regarded as equivalent instrument to conventional bonds, as it seeks to generate

predictable returns to the certificate holder. In its origins, a Suk (Sukuk in plural)

referred to a issuance of paper representing commodities for salary payments. The

modern concept of Sukuk it refers to certificates representing undivided shares in

ownership of tangible assets, usufruct or particular investments. Unlike

conventional bonds, based on interests, Sukuk offer participation rights in assets or

ventures.

4.3.6. Qard al Hasan and Zakah

With a peculiarity of profit free loan, Qard al Hasan aspires to assist those in

need of financial help for undesirable circumstances. In accordance with Sharia’a

the financial institution does not make financial gains by this providing this

service, but provide a social service. This kind of instrument is used also to provide

funding for healthcare, marriage or education. Likewise, Zakah relates to the

obligation of Muslim community to facilitate an equal and fair allocation of wealth.

Zakah is mentioned in the Holy Quran as one of the five cores believes of Islam.

Therefore, Islamic Banking might integrate promotion of Zakah and also be part of

the donors’ community contributing to individuals, organizations and businesses

with social purpose.

27

4.4. Funding Social Ventures through Islamic Finance

While SB is recognized as exogenous activity for conventional organizations

and financial institutions, we have seen that SB values are inherent in Islamic

Banking and Finance, since the Islamic Moral Economy principles and foundational

morals directly refer to ethical and SB activities. As Asutay (2012) concludes,

Islamic Ethics inherent in Islamic Finance Principles refer to a particular value

system distinct from conventional banking and similar to the mission based

financial instruments mentioned earlier.

The Islamic Finance Instruments outlined above seem to harmonize in line

with the model for SB proposed by Weerawardena and Sullivan Mort (2012). This

is, given the dimension of “risk management”, Islamic Finance Instruments

propose different range of funding where the risk is minimized. The system of risk-

sharing proposed by Islamic Finance relieves risk from the decision making

process of Social Ventures. Also, the constrains characterized within the bounded

multidimensional model – environment, sustainability and social mission – well fit

with value proposition of the Islamic Moral Economy, and so Islamic Finance

Instruments. For instance, Zakah financial instrument plays the same role as

Philanthropic grants, thereby, represents a central funding tool for non-profit

forms of Social Enterprises.

Several academics tend to explain the engagement of IF in Social

Entrepreneurship (About-Gabal et al., 2011, Sheng, 2013) applying to perception

and awareness by the SB spectrum. Abdullah (2011) proposes a allocation of social

capital as basis for mutual empowerment and overall (Ummah) benefit. Sheng

(2013) hypothesizes that “Taking IF to the next stage in terms of scale and market

demand requires a concerted effort to promote awareness about its merits,

especially in non-Islamic countries”(p.5). This brings to the claim that, despite the

remarkable growth, there remains significant unreached funding demand on SB

(About-Gabal et al., 2011). Therefore, we recognize that there is a gap between

both clusters in terms of recognition. Hence, we propose the following hypothesis:

social and ethical values inherent in IF are neither well perceived nor understood by

the actors in the field of SB. Therefore, the following section aims at gaining

28

additional clarifications on this aspect by conducting a survey analysis to identify

the recognition of Islamic Finance for sourcing Social Business (Figure 9).

Figure 9: Islamic Finance in Social Business Setting

Source: Own creation.

29

5. Research

From the previous sections, we stated that IF presents an appropriate setting

for funding SB. In order to test the hypothesis (section 4.4), this section attempts to

illustrate the recognition and understanding of the value proposition of Islamic

Moral Economy intrinsic in the Islamic Finance Instruments. Due to the limitation

of data available, it is not possible for us to run a regression analysis. Therefore,

we have chosen to carry out a qualitative analysis based on online survey.

5.1. Methodology

The survey was drawn with 7 different questions in order to scan recognition

of ethical and socially responsible elements inherent in IF system by the SB crowd.

Thus, we actively select the most productive sample to answer the research

question. The target sample here focuses on agents who are active in the broader

field of SB (including financial service, social entrepreneurs, SB employees, legal

services, consulting, academics and researchers, public institutions and students).

Furthermore, the survey was promoted only in Social Entrepreneurship events

and online social networks (e.g. LinkedIn) , and second, respondents were asked to

leave the survey if not fitting the requirements. Besides the individual control, a

geographical boundary is also applied to limit the group of respondents to agents

active in Western countries, independent on cultural background. Due to the

narrow nature of the target population, the sampling method was based on

snowball sampling (Heckarthorn, 2007), requiring respondents to forward the

survey to those people they know that could fit the selection criteria. This sampling

method

A total of 53 respondents filled in the survey, but only 37 completed all the

questions.

5.2. Results

The complete survey can be found in Appendix.

30

Q1: Please choose the category that best describes the nature of your profession. 53

answers.

The most predominant population is academia followed by social

entrepreneurs and consultants. This question is meant to frame the poll and better

interpret the other questions.

Q2: How familiar are you with the "ethical investment" movement (including socially

and environmentally "responsible" investment)? 48 answers.

We see that only few individuals never heard of it or either they did

participate in ethical finance (4 and 5, respectively). The majority (17) barely

know much about ethical investment while the rest are divided between those

familiar with it and those well informed.

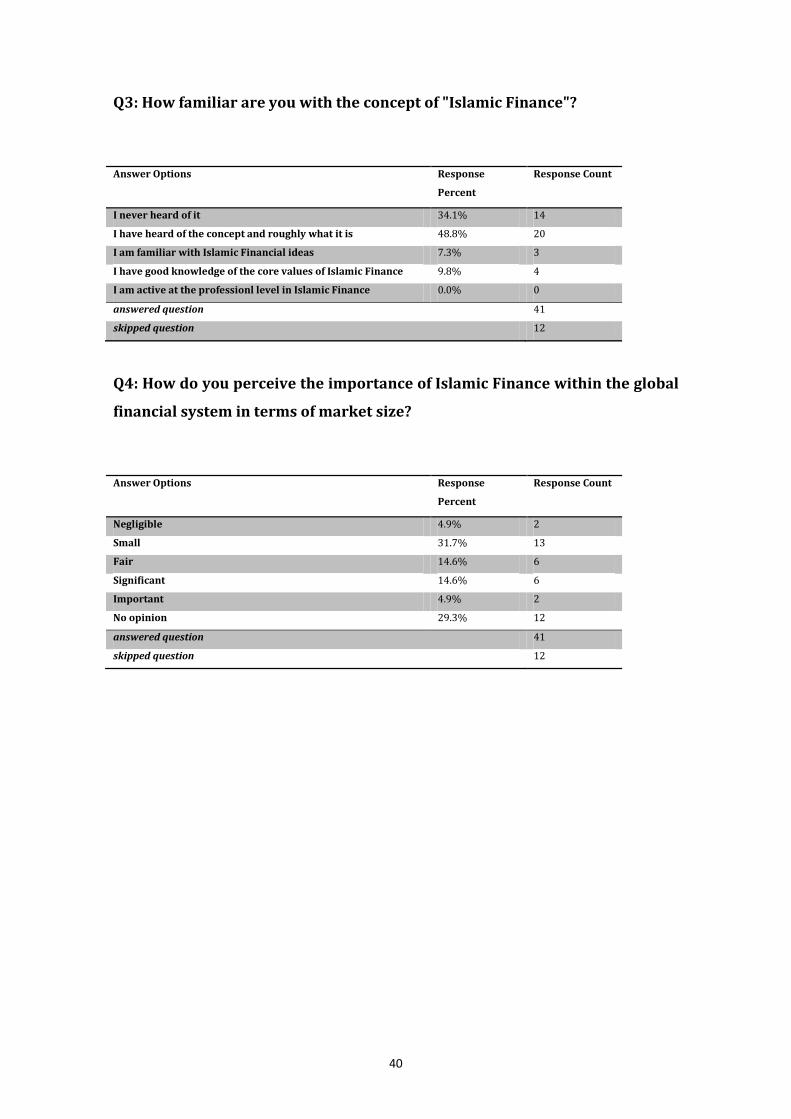

Q3: How familiar are you with the concept of "Islamic Finance"? 41 answers.

It is clear that there is rather a remote familiarity with IF or either no

recognition of the concept as all. Only few recognize familiarity and knowledge

with IF while none of the surveyed states being active with it.

Q4: How do you perceive the importance of IF within the global financial system in

terms of market size? 41 answers.

Generally, the recognition of IF as an important movement within the global

economy does not seem evident. However, the choice of “no opinion” could also

explain the ignorance of the potential of IF (12).

Q5: Regardless of your familiarity with IF, what words and/or ideas does the notion

of IF evoke you to? 3 boxes, 1 idea per box. 37 answers.

This questions was aimed to explore the chance that respondents would

mention concepts related to ethical value proposition in IF. Each individual was

asked to fill three different words or ideas. On a list of 111 different ideas, 29 were

associates with IF principles such as social, development, fairness or community

interest.

Q6: Do you agree with the following statements? 37 answers.

31

With a range of 1-5, where 1 means total disagreement and 5 total

agreement, the respondents jointly agree with prohibition of illicit activities and

also finance with social and ethical purpose. However, it is important to highlight

that prohibition of interest, yet being in the base of IF foundation it is not agreeably

considerate.

Q7: What are the points of divergence between the following Islamic Finance

principles and the Conventional Banks principles which you are familiar with? (you

may tick more than one answer). 37 answers.

There is a common acceptance of prohibition of interest and prohibition of

illicit activities (see section 4.2.3) as differentiator features (20 and 21,

respectively). But, only 5 respondents recognize asset based investments as a point

of divergence.

5.3. Discussion

An appropriate point to start this discussion is by characterizing the nature

of the respondents of the survey. It is remarkable that 37.7% of the respondents

belong to academic field in addition to social entrepreneurs (20.8%) and

consultants (15.1%). The relevance of this data is that the majority of the

population (73.6) is associated to the innovation and decision making process of

the Social Entrepreneurship.

An important number of respondents sustain familiarity with the notion of

ethical investment, even a few (8.3%) confirm having experience with ethical

finance (Table 2). Concerning to IF, there is an evident unfamiliarity in SB

environment (Table 3). Additionally, yet a significant number consider the Islamic

Finance Market as small in comparison to the Global Financial Market (31.8%),

there is no clear trend on the perception of the market size (Table 3), particularly,

because 29.3% of the population do not give any opinion on this matter.

Table 5 shows a list of concepts that IF evokes to the respondents. This

question is drawn to explore the relationship between the general notion of IF and

the values and principles introduces by the Islamic Finance Principles (section

32

4.2). The list shows that one third of the ideas mentioned go along with the

principles, a total of 36 out of 111 words. These findings go in line with what some

researchers claim (Haniffa & Hudaib, 2007; Sheng, 2013).

In Table 6, we present some features of IF to be evaluated. It is remarkable

that there is a general agreement on social purpose of finance and the prohibition of

illicit activities. These two features are considered closely related to SB value.

Further, the agreement on prohibition of interest is not very significant. The

reasoning behind it is that prohibition of interest is not an ethical or social value as

such, it is a process-based instrument used for applying risk-sharing principle

(Beck et al., 2013). Alongside, the same features are suggested to recognize the

perception of what principles distinct from conventional banks. There is a general

acceptance on the fact that all principles proposed differ from those in

conventional banking, particularly the prohibition of interest (70.3%). Only, there

is just little agreement on the idea that asset based investment differs from

conventional banks features, although this is a remarkable characteristic on IF.

In summary, several remarks can be drawn from this study on perception

and understanding of value proposition of IF. (1) Being ethical investment

accepted, there is not a clear awareness about the general notion of Islamic finance

in SB field. (2) The recognition of Islamic finance values is not well defined. (3)

Although there is consensus on differentiation in principles between conventional

banking and Islamic Finance, the respondents mostly support those principles

shared with SB value proposition. Therefore, the hypothesis is tested and

supported.

How, then, IF could be appropriate for SB? What seems important is that

much effort is being done from the supply side (Bennett & Iqbal, 2013; Fang &

Foucart, 2013; Haniffa & Hugaib, 2007). However, very little has been done on

demand recognition and product adjustment for SB and Social Entrepreneurship.

As contribution of this paper, we present IF as a valid alternative for SB funding,

and also, we raise and explore the recognition obstacle.

33

5.4. Strengths and limitations

First, due to lack of data this analysis has been limited to exploration of

theoretical sources together with a targeted survey. Since the investigation focuses

on IF acknowledge at the agent level of SB, the target sample represents strongly

the purpose of the research questions. The snowball methodology allows us to

reach the representative population that better fits with our research question.

However, sometimes representativeness of the sample is not guaranteed. A

sampling bias could be an issue when using this technique. Also, the sample is

geographically located in western countries where the presence of Islamic Finance

Institutions is very new or either nonexistent. This could logically lead to a lack of

knowledge and recognition of the Islamic Finance background. But, even if it might

weaken the empirical analysis, it also provides an overview for Islamic Finance

Institutions about the location of social business network.

34

6. Conclusion

Ethical and social values have been rising on interest during the last decade

due to social inequality and environmental degradation. These values have

strongly emerged also in business and financial sectors bringing about SB (or

Social Entrepreneurship) and ethical investment. As a chain reaction, one does not

exist as such without the other. While social entrepreneurs seek funding to provide

positive social and environmental impact, ethically investing must comply with

those business practices as well. As described in this paper, according to the

characteristic of the SB, besides other means of finance, the ethical investing sector

offers a particular solution (e.g. Philanthropy grants for non-profit organizations).

However, the purpose of this paper was to outline the Islamic Finance

phenomenon as an alternative finance source for SB. We have seen that the value

proposition and ethical value well fit with the need of SB, regardless its nature.

Also, we have seen that from the supply side of IF there is a wide range of financial

instruments that could fulfil the funding needs of Social Entrepreneurs. As

presented early in this paper (section 3), IF appears to be an alternative either for

conventional financial sources or those with mission alignment. The core research

findings support the hypothesis that there is lack of recognition and knowledge of

Islamic Finance among SB population.

We hope that the discussion and analysis in this paper stimulate more

research in this area since much work remains for future research. Firstly, data on

specific financial products and business industries are indispensable to better

understand differences in practice between conventional banks and Ethical

Banking on one side, and Islamic Finance, on the other side. Furthermore, also

qualitative analysis on extensive case studies can be use for future research. For

instance, a comparison between funding SB in eastern countries and western

countries can be accomplished to investigate the regulatory, accounting,

infrastructure or other impediments. At the same time, we expect an international

development of Islamic Finance following the current trends in order to reach the

SB sector in situ.

35

REFERENCES

Abdullah, M. A. and Hoetoro, A., (2011). Entrepreneurship as an Instrument to

Empowering Small and Medium Enterprises: An Islamic Perspective. International

Journal of Management Sciences and Business Research. 1 (1): 35-46.

Abou-Gabal, N., Ijaz Khwaja, A. and Klinger, B., (2011). Islamic Finance and

Entrepreneurship: Challenges and Opportunities Ahead. EFLRI Islamic Finance

Whitepaper. Harvard University, January 2011.

Agrawal, A. K., Catalini, C. and Goldfarb. A., (2011). The Geography of Crowdfunding. NBER

Working Paper No. w16820.

Alter, K., (2007). Social Enterprise Typology. Virtue Ventures LLc.

Anderson, B. B., and Dees, J. G., (2002). Developing viable earned income strategies. In J. G.

Dees, J. Emerson,&P. Economy (Eds.), Strategic tools for social entrepreneurs:

Enhancing the performance of your enterprising nonprofit. New York: John Wiley &

Sons, Inc.

Asutay, M., (2012). Conceptualizing and Locating the Social Failure of Islamic Finance:

Aspirations of Islamic Moral Economy vs. the Realities of Islamic Finance. Asian and

African area Studies, 11 (2): 93-113,

Austin et al., (2006). Social and Commercial Entrepreneurship: Same, Different, or Both?.

Baylor University.

Barom, M. N., (2013). Social Responsibility Dimension in Islamic Investment: A Survey in

Investor’s Perspective in Malaysia. International Islamic University Malaysia.

Beck, T., Demirgüç-Kunt, A, and Merrouche, O., (2013). Islamic vs. conventional Banking:

Business model, efficiency and stability. Journal of Banking & Finance, 37: 433-447

Bendjilali, B., (2000). On the demand for customer credit: an Islamic setting. Islamic

Development Bank, 30. Jeddah

Bennett, M. S. and Iqbal, Z., (2013). How socially responsible investing can help bridge the

gap between Islamic and conventional financial markets. International Journal of

Islamic and Middle Eastern Finance and Management, 6. 211-225.

Brugnoni, A., (2009). Smoke signals. Islamic Banking and Finance 14: 22.

Certo, S. T. & Miller, T. (2008), Social Entrepreneurship: Key issues and concepts. Business

Horizons, 51. 267-271.

Christen, R. P., Rosenberg, R and Jayadeva, V., (2004). Financial institutions with a “double

bottom line”: Implications for the future of microfinance. Occasional Paper, C-Gap,

Washington.

36

Dart, R., (2004). The Legitimacy of Social Enterprise. Nonprofit Management and

Leadership 14 (4): 411–424.

Dean, T., (2014). Sustainable Venturing. Entrepreneurial Opportunity in the Transition to a

Sustainable Economy. Pearson.

Ernest & Young (2014). World Islamic Banking Competitiveness Report 2013-2014.

Elmelki, A. and Ben Arab, M., (2009). Ethical Investment and the Social Responsibilities of

the Islamic Banks. International Business Research. January 2009.

Fang, E. D. and Foucart, R., (2013). Western Financial Agents and Islamic Ethics. Journal of

Business Ethics.

Farook, S. Shikoh, R. (2011). Integration of Social Responsibility in Financial Communities.

Foster, W. and Bradach, J., (2005). Should Nonprofit Seek profits?. Harvard Business

Review. Vol, 83. 92-100.

Goyal, K. A. and Joshi,V., (2011). A study of social and ethical issues in banking industry.

International Journal of Economics and research.

Haniffa, R., Hudaib, M., (2007). Exploring the Ethical Identity of Islamic Banks via

Communication in Annual Reports. Journal of Business Ethics. 76: 97-116

Heckathorn, D. D., (2007). Extensions of respondent-driven sampling: analyzing

continuous variables and controlling for differential recruitment. Sociological

Methodology, 37: 151–207

IFSB (2013). Islamic Financial Services Industry. Stability Report.

Institute for Social Banking (2014). What is social Banking? 01-07-2014

Iqbal, Z. and Mirakhor, A. (2007), An Introduction to Islamic Finance: Theory and Practice.

Islamic Financial Services Industry (2013). Stability Report 2013. Kuala Lumpur. May

2013.

Jaufeerally, R. Z., (2011). Islamic Banking and Responsible Investment: Is a Fusion

Possible?. Issues in business Ethics, 31. 151-163.

Johnson, S. (2000). Literature review on social entrepreneurship. Canadian Centre for

Social Entrepreneurship, University of Alabama School of Business.

Kamali, M. H (1991). Principles of Islamic Jurisprudence. International Islamic University.

Malaysia. March 1991.

Kamla, R., (2009). Critical Insights into contemporary Islamic accounting. Critical

perspectives on accounting. 932-932

Khan, F., (2010). How “Islamic” is Islamic Banking?. Journal of Economics Behavior and

Organization.

KPMG & ALFI (2012): European Responsible Investing Fund Survey, Luxembourg: KPMG

& ALFI.

37

Lehner, O. M., (2013). Crowdfunding social ventures: a model and research agenda,

Venture Capital: An International Journal of Entrepreneurial Finance, 15:4, 289-311,

Liebman, J., (2011). Social Impact Bonds. Washington, DC: Center for American Progress.

Maslakovic, M., (2013). UK, the leasing western center for Islamic Finance. The UK Islamic

Finance Secretariat, TheCityUK. London.

Mckee, K., (2008). Microfinance: Climate change connections. World Bank.

Mersland, R. and Oystein S. R. (2007). Performance and corporate governance in

microfinance institutions.

Mildred E. W., (2013). Private finance for public goods: social impact bonds,

Journal of Economic Policy Reform, 16:4, 303-319

Nicholls, A., (2009). “We do good things, don’t we?”: Blended Value Accounting in Social

Entrepreneurship. Accounting, Organizations and Sociert, 34. 755-769.

Nimrah, K., Tarazi, M., and Reille, X. (2008). Islamic Microfinance: An Emerging Market

Niche. CGAP. No 49. August 2008

Novethic. (2009). Finance Islamique et ISR. Convergence Possible. Novethic working

paper.

Oxfam (2014). Working for the few. Political capture and economic inequality. Ozfam

briefing paper 178. January 2014.

Peredo, A. M. and McLean, M., (2006). Social Entrepreneurship: A critical review of the

concept.

Porter, E. M., and Kramer, R., (2013). Creating Shared Value. Harvard Business Review.

Rice, G., (1999). Islamic Ethics and the Implications for Business. Journal of Business

Ethics.

Sample, B., (2011). Moving 100 million families out of severe poverty: how can we do it?.

2011 Global Microcredit Summit. Auxiliary Session Paper, Valladolid.

Santos, F.M., (2012). A Positive Theory of Social Entrepreneurship.

Sarially, S., (2005). Evaluating the ‘Social Responsibility’ of Islamic Finance: Learning from

the Experiences of Socially Responsible Investment Funds, in the Proceedings of the

International Conference in Islamic Economics and Finance, Islamic Economics and

Banking in the 21st Century, 1. 433-472.

Sheng, A., (2012). Islamic Finance as Social Impact Investing. Fung Global Institute.

2013/08. December 2013.

Tahir, S. (2011) Challenges facing Islamic Finance: Research Areas. International Islamic

University. Islamabad.

Taqi Usmani, M., (2007). An Introduction to Islamic Finance. Brill.

38

Thulchin, D. and Yi-Han Lin, S., (2012). Capital Source for Social Enterprises. Social

Enterprise Associates, Working Paper 16.

UN (2014). Millenium development goals and beyond 2015. 05-07-2014

Uygur, U. and Marcoux, A. M. (2013). The Added Complexity of Social Entrepreneurship: A

knowledge-Based Approach. Loyola eCommons. Loyola University Chicago. April

2013.

Vicary Abdullah, D. and Chee, K. (2010). Islamic Finance: Why It Makes Sense –

Understanding Its Principles and Practices.

Warner, M.E., (2013). Private Finance for Public Goods: Social Impact Bonds. Journal of

Economic Policy Reform, 16:4. 303-319.

Warde, I,. (2000). Islamic Finance in the Global Economy. Edinburgh University press.

Weerawardena, J. and Mort, G. S., (2006). Investigating social entrepreneurship: A

multidimensional model. Journal of World Business, 41. 21-35.

Wuttunee, W., Chicilo, M., Rothney, R., and Gray, L., (2008). Financing Social Enterprise. An

enterprise perspective. Social Enterprises. Social Sciences and Humanities Research

Council of Canada. March 2008.

Wuttunee, W., Rothney, R., and Gray, L., (2008a). Financing Social Enterprise. A Scan of

Financing Providers in the Manitopa, Saskatchewan, and Northwestern Ontario

Region. Social Sciences and Humanities Research Council of Canada. January 2008.

39

APPENDIX. Survey questionnaire

Q1: Please choose the category that best describes the nature of your

profession.

Answer Options Response Per

cent

Response Count

Financial Services 1.9% 1

Social Enterpreneur (Founder) 20.8% 11

Social Business (Employee) 1.9% 1

Legal Services 1.9% 1

Business Consulting Services 15.1% 8

Academia/Research 37.7% 20

Public Institution (whether national or international) 1.9% 1

Still in education (College, University or higher education) 5.7% 3

Other. 13.2% 7

answered question 53

skipped question 0

Q2: How familiar are you with the "ethical investment" movement (including

socially and environmentally "responsible" investment)?

Answer Options Response

Percent

Response Count

I never heard of it 10.4% 5

I have heard of the concept and I know roughly what it is 35.4% 17

I am familiar with ethical finance 25.0% 12

I have a good knowledge of its core principles 20.8% 10

I have worked with ethical financial products/services 8.3% 4

answered question 48

skipped question 5

40

Q3: How familiar are you with the concept of "Islamic Finance"?

Answer Options Response

Percent

Response Count