IMPACT OF KEY INTERNAL DETERMINANTS ON PROFITABILITY AND SHARE PRICE PERFORMANCE OF A LARGE PUBLIC...

13

IJBER Volume 1, Issue 1 (January, 2013) International center of Science Education and Academic Research for Scholars www.isearchscholars.com 183 INTERNATIONAL JOURNAL OF BUSINESS AND ECONOMIC RESEARCH A Journal of IMPACT OF KEY INTERNAL DETERMINANTS ON PROFITABILITY AND SHARE PRICE PERFORMANCE OF A LARGE PUBLIC SECTOR BANK IN INDIA Rajveer Rawlin Research Scholar, Bharathiar University, India Email: [email protected] Cell: (+) 91-9480217380 Dr. Ramaswamy Shanmugam Professor, Department of Management Studies, Bharathiar University, India Abstract Banking sector reforms have changed the profile and functioning of the Indian banking industry in a significant manner. The reforms have led to the increase in resource productivity, increasing level of deposits and credits, increase in profitability and decrease in non-performing assets (NPAs). Profitability of banks is impacted by both internal and external factors. Profitability eventually drives stock price performance. Accordingly this paper attempts to study the determinants of profitability of a leading public sector bank in India and the relationship between the bank’s profitability and share price. The key performance indicators chosen were: deposits, advances, net NPAs, business-per -employee, profit-per-employee, capital adequacy ratio and return on assets. The impact of these indicators on net profit and the share price

Transcript of IMPACT OF KEY INTERNAL DETERMINANTS ON PROFITABILITY AND SHARE PRICE PERFORMANCE OF A LARGE PUBLIC...

IJBER Volume 1, Issue 1 (January, 2013)

International center of Science Education and Academic Research for Scholars

www.isearchscholars.com

183

INTERNATIONAL JOURNAL

OF BUSINESS AND ECONOMIC RESEARCH

A Journal of

IMPACT OF KEY INTERNAL DETERMINANTS ON

PROFITABILITY AND SHARE PRICE PERFORMANCE OF A

LARGE PUBLIC SECTOR BANK IN INDIA

Rajveer Rawlin

Research Scholar, Bharathiar University, India

Email: [email protected]

Cell: (+) 91-9480217380

Dr. Ramaswamy Shanmugam Professor, Department of Management Studies, Bharathiar University, India

Abstract

Banking sector reforms have changed the profile and functioning of the Indian banking

industry in a significant manner. The reforms have led to the increase in resource

productivity, increasing level of deposits and credits, increase in profitability and

decrease in non-performing assets (NPAs). Profitability of banks is impacted by both

internal and external factors. Profitability eventually drives stock price performance.

Accordingly this paper attempts to study the determinants of profitability of a leading

public sector bank in India and the relationship between the bank’s profitability and share

price. The key performance indicators chosen were: deposits, advances, net NPAs, business-per -employee, profit-per-employee, capital adequacy ratio and return on assets. The impact of these indicators on net profit and the share price

IJBER Volume 1, Issue 1 (January, 2013)

International center of Science Education and Academic Research for Scholars

www.isearchscholars.com

184

were studied in the period 2002-2011 through a multi-variate regression analysis. A strong correlation was observed between net profit and individual performance indicators such as deposits, advances, net NPAs and business-per-employee. A strong correlation was also observed between the stock price and individual performance indicators namely deposits, advances, net NPAs, business-per-employee and profit-per-employee. The correlation of the performance indicators with both the net income and the share price increased when all the indicators were taken together in a multi-variate regression. This suggests that the chosen indicators have a synergistic effect on profitability and the stock price.

Keywords: Net Profit, Stock Price, Key Performance Indicators, Indian Public Bank, Multiple Regression, Synergy.

1. Introduction

Introduction of banking sector reforms have changed the face of the entire Indian banking

scenario. The national, institutional and international boundaries are becoming less

important. Globalization of operations and development of new technologies are taking

place at a rapid pace. A shift in marketing philosophy of banks is visible from the rising

focus on quality of service offered to customers. However, banks are now facing a

number of challenges such as frequent changes in technology required for modern

banking, stringent prudential norms, increasing competition, worrying level of NPA’s,

rising customer expectations, increasing pressure on profitability, rising operating

expenditure and shrinking levels of spreads. The reforms in banking sector have also

brought margins under pressure. The Reserve Bank of India’s (RBI) efforts to adopt

international banking norms have further forced banks to adopt measures to control and

maintain margins.

The profitability of a bank is predominantly driven by a series of internal and external

factors. The internal determinants of bank profitability include but are not limited to bank size, capital, risk management procedures adopted, expenses, and diversification adopted (Molyneux and Thornton, (1992); Goddard et al., (2004); Bodla

and Verma, (2006)). External determinants of bank profitability include both industry structural determinants such as market concentration, industry size and ownership, and macroeconomic determinants such as inflation, interest rates, money supply and Gross Domestic Product (GDP) (Athanasoglou et al., (2008);

Chirwa, (2003)). In the current study we focus primarily on the impact of internal factors closely

monitored by the RBI on bank profitability and share price performance These factors

include deposits, advances, net NPAs, return on assets, the capital adequacy ratio, business-per-employee and profit-per-employee. The effect of these factors on bank profitability and share price performance was examined over a 10 year period spanning from 2002-2011 through a multi-variate regression analysis.

IJBER Volume 1, Issue 1 (January, 2013)

International center of Science Education and Academic Research for Scholars

www.isearchscholars.com

185

Objectives: The following are the specific objectives of this study:

a) To assess the impact of key internal factors namely deposits, advances, net NPAs,

return on assets, the capital adequacy ratio, business-per-employee and profit-per-

employee on profitability.

b) To assess the impact of the above factors on the share price.

c) To study the combined effect of all the above factors on both profitability and the

share price.

2. Literature Review

The banking sector plays a pivotal role in fostering economic development. By

mobilizing savings from the public and channeling them through advances, banking

activities support developmental activities across the nation. Thus, a stable banking

system is mandatory for a nations overall financial health and prosperity. An

understanding of factors instrumental in driving bank profitability can throw light not

only in identifying profitable banking strategies but also will help uncover operational

inefficiencies which can be eliminated.

There are several factors that impact the profitability of banks (Sufian and

Habibullah, (2010); Dietrich and Wanzenried, (2011)). These factors can be broadly

classified as either internal determinants that originate within the firm such as bank size, capital, risk management, expenses management, and diversification (Molyneux

and Thornton, (1992); Goddard et al., (2004); Bodla and Verma, (2006)) or external

determinants that are outside the firm like market concentration, industry size and ownership, inflation, interest rates, money supply and Gross Domestic Product (GDP) (Athanasoglou et al., (2008); Chirwa, (2003)).

Several studies have examined the impact of key internal factors on profitability.

Smirlock & Brown, (1986) studied the impact of demand deposits as a function of total

deposits on profitability. Their findings suggest that demand deposits had a significant

positive relationship with profits. Miller and Noulas, (1997) found that loan loss

provision and net charge offs had a significant negative effect on the profitability of large

banks. These results indicated that net charge offs were further affected by asset and

liability composition. Thus, the asset liability portfolio decisions of commercial banks

can be expected to affect the profitability of these institutions via net charge offs. It was

also observed that higher salaries and benefits per employee were consistently associated

with higher net charge offs to total assets. This suggested that banks with higher salaries

and benefits would require higher net interest margins to maintain profitability.

Ganesan, (2001) examined the profitability of public sector banks in India and

found that interest costs, interest income, other income, deposits per branch, credit to

total assets and proportion of priority sector advances were key determinants of

IJBER Volume 1, Issue 1 (January, 2013)

International center of Science Education and Academic Research for Scholars

www.isearchscholars.com

186

profitability of these banks. Holden and El-Bannany, (2004) investigated whether

investment in information technology systems affects bank profitability in UK. The

results showed that, when the other factors used in the literature are included, the number

of automated teller machines installed by a bank has a positive impact on bank

profitability. Bodla and Verma, (2006) made an attempt to identify the key determinants

of profitability of public sector banks in India and their study indicated that the variables

such as non-interest income, operating expenses, provision and contingencies and spread

have significant relationship with net profits.

In a study done on Tunisian banks from 1980-2000, Ben Naceur and Goaied,

(2008) find that banks with relatively high amount of capital and overhead expenses tend

to exhibit higher net-interest margin and profitability levels. They also find that bank size

is negatively related to profitability. Additionally stock market development had a

positive impact on bank profitability. Further private banks were found to be relatively

more profitable than their state-owned counterparts.

Sufian, (2009) examined the determinants of Malaysian domestic and foreign commercial

bank profitability during the period 2000-2004. It was found that Malaysian banks with

higher credit risk and loan concentration exhibit lower profitability levels. On the other

hand, banks that have a higher level of capitalization, higher proportion of income from

non-interest sources, and high operational expenses proved to be relatively more

profitable.

External determinants of bank profitability encompasses the impact of

macroeconomic variables such as concentration, growth and inflation on bank

profitability (Rajan and Zingales (1998); Athanasoglou et al., (2008); Chirwa, (2003).

Chirwa, (2003) investigated the relationship between market structure

and profitability of commercial banks in Malawi using time series data between 1970

and 1994. The analysis shows a long-run relationship between bank performance and

concentration. Sufian, (2009) found that economic growth negatively impacts the

profitability of Malaysian banks. Higher inflation rates however positively impacted the

profitability of these banks. While studying a sample of eighteen European countries

Molyneux and Thornton, (1992) found a significant positive relationship between the

return on equity and the level of interest rates in each country, bank concentration, and

government ownership.

Kumar and Warne, (2009) have found that valuations in the stock market as

measured by the Price/Earnings (P/E) ratio are largely influenced by the size of the firm

and variations in the market price. The impact of both internal and external determinants

of profitability on share price performance is however not clearly understood.

3. Methodology

This study used historical data to study the impact of the independent

variables namely, deposits (D), advances (Adv), net non performing assets (NPA), business-per-employee (BPE), profit-per-employee (PPE), capital adequacy ratio (CAR) and return on assets (ROA), on the dependent variables

IJBER Volume 1, Issue 1 (January, 2013)

International center of Science Education and Academic Research for Scholars

www.isearchscholars.com

187

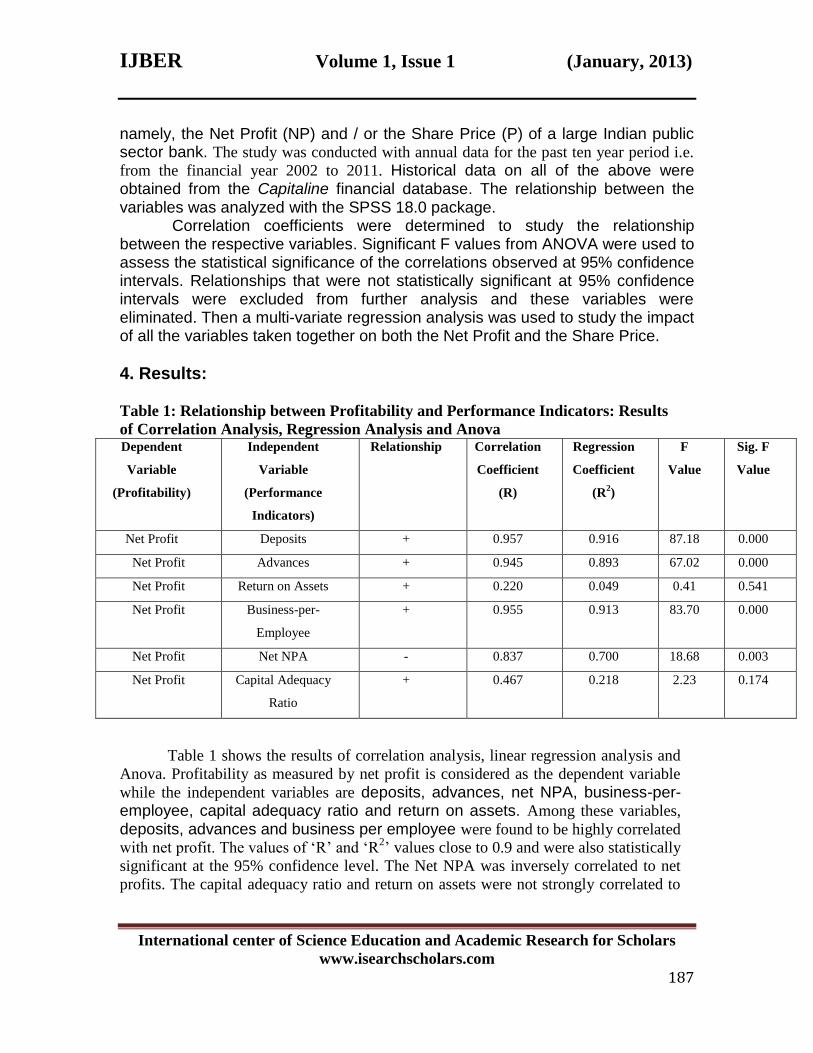

namely, the Net Profit (NP) and / or the Share Price (P) of a large Indian public sector bank. The study was conducted with annual data for the past ten year period i.e.

from the financial year 2002 to 2011. Historical data on all of the above were obtained from the Capitaline financial database. The relationship between the variables was analyzed with the SPSS 18.0 package.

Correlation coefficients were determined to study the relationship between the respective variables. Significant F values from ANOVA were used to assess the statistical significance of the correlations observed at 95% confidence intervals. Relationships that were not statistically significant at 95% confidence intervals were excluded from further analysis and these variables were eliminated. Then a multi-variate regression analysis was used to study the impact of all the variables taken together on both the Net Profit and the Share Price.

4. Results:

Table 1: Relationship between Profitability and Performance Indicators: Results

of Correlation Analysis, Regression Analysis and Anova Dependent

Variable

(Profitability)

Independent

Variable

(Performance

Indicators)

Relationship Correlation

Coefficient

(R)

Regression

Coefficient

(R2)

F

Value

Sig. F

Value

Net Profit Deposits + 0.957 0.916 87.18 0.000

Net Profit Advances + 0.945 0.893 67.02 0.000

Net Profit Return on Assets + 0.220 0.049 0.41 0.541

Net Profit Business-per-

Employee

+ 0.955 0.913 83.70 0.000

Net Profit Net NPA - 0.837 0.700 18.68 0.003

Net Profit Capital Adequacy

Ratio

+ 0.467 0.218 2.23 0.174

Table 1 shows the results of correlation analysis, linear regression analysis and

Anova. Profitability as measured by net profit is considered as the dependent variable

while the independent variables are deposits, advances, net NPA, business-per-employee, capital adequacy ratio and return on assets. Among these variables, deposits, advances and business per employee were found to be highly correlated

with net profit. The values of ‘R’ and ‘R2’ values close to 0.9 and were also statistically

significant at the 95% confidence level. The Net NPA was inversely correlated to net

profits. The capital adequacy ratio and return on assets were not strongly correlated to

IJBER Volume 1, Issue 1 (January, 2013)

International center of Science Education and Academic Research for Scholars

www.isearchscholars.com

188

net profit at the 95% confidence level and hence were excluded from subsequent

analysis.

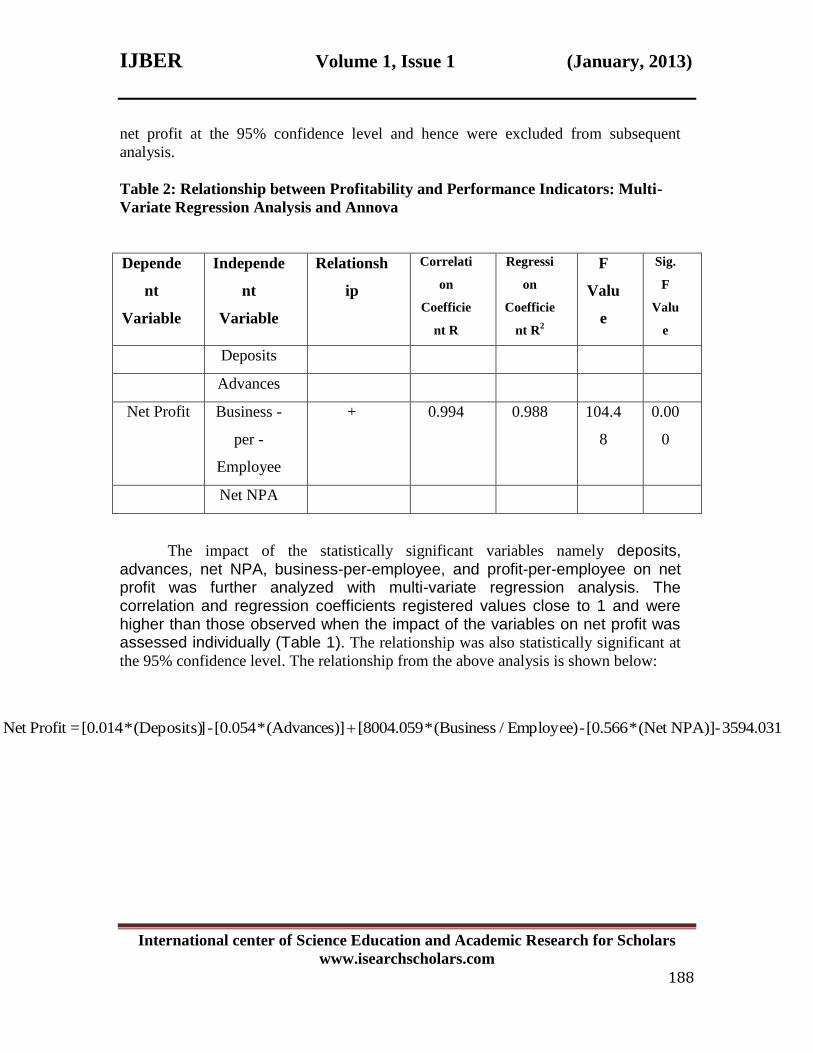

Table 2: Relationship between Profitability and Performance Indicators: Multi-

Variate Regression Analysis and Annova

Depende

nt

Variable

Independe

nt

Variable

Relationsh

ip

Correlati

on

Coefficie

nt R

Regressi

on

Coefficie

nt R2

F

Valu

e

Sig.

F

Valu

e

Deposits

Advances

Net Profit Business -

per -

Employee

+ 0.994 0.988 104.4

8

0.00

0

Net NPA

The impact of the statistically significant variables namely deposits, advances, net NPA, business-per-employee, and profit-per-employee on net profit was further analyzed with multi-variate regression analysis. The correlation and regression coefficients registered values close to 1 and were higher than those observed when the impact of the variables on net profit was assessed individually (Table 1). The relationship was also statistically significant at

the 95% confidence level. The relationship from the above analysis is shown below:

1) (Eqn. 3594.031-NPA)](Net *[0.566 - Employee) / (Business*[8004.059 ](Advances)*[0.054 - ](Deposits)*[0.014 =ProfitNet

IJBER Volume 1, Issue 1 (January, 2013)

International center of Science Education and Academic Research for Scholars

www.isearchscholars.com

189

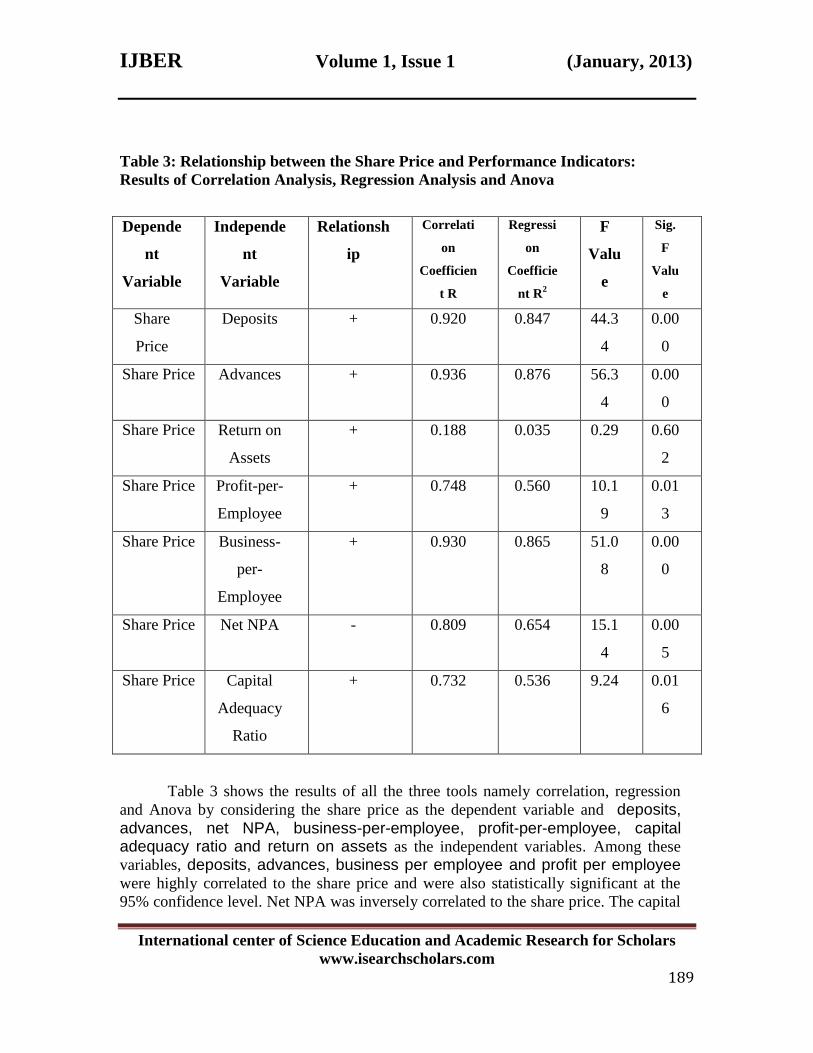

Table 3: Relationship between the Share Price and Performance Indicators:

Results of Correlation Analysis, Regression Analysis and Anova

Depende

nt

Variable

Independe

nt

Variable

Relationsh

ip

Correlati

on

Coefficien

t R

Regressi

on

Coefficie

nt R2

F

Valu

e

Sig.

F

Valu

e

Share

Price

Deposits + 0.920 0.847 44.3

4

0.00

0

Share Price Advances + 0.936 0.876 56.3

4

0.00

0

Share Price Return on

Assets

+ 0.188 0.035 0.29 0.60

2

Share Price Profit-per-

Employee

+ 0.748 0.560 10.1

9

0.01

3

Share Price Business-

per-

Employee

+ 0.930 0.865 51.0

8

0.00

0

Share Price Net NPA - 0.809 0.654 15.1

4

0.00

5

Share Price Capital

Adequacy

Ratio

+ 0.732 0.536 9.24 0.01

6

Table 3 shows the results of all the three tools namely correlation, regression

and Anova by considering the share price as the dependent variable and deposits, advances, net NPA, business-per-employee, profit-per-employee, capital adequacy ratio and return on assets as the independent variables. Among these

variables, deposits, advances, business per employee and profit per employee were highly correlated to the share price and were also statistically significant at the

95% confidence level. Net NPA was inversely correlated to the share price. The capital

IJBER Volume 1, Issue 1 (January, 2013)

International center of Science Education and Academic Research for Scholars

www.isearchscholars.com

190

adequacy ratio was correlated positively to the stock price. Return on assets was not

strongly correlated to the share price at the 95% confidence level and hence was

excluded from further analysis.

Table 4: Relationship between Profitability and Performance Indicators: Multi-

Variate Regression Analysis and Annova

Depende

nt

Variable

Independe

nt

Variable

Relationsh

ip

Correlati

on

Coefficien

t R

Regressi

on

Coefficie

nt R2

F

Valu

e

Sig.

F

Valu

e

Deposits

Advances

Net Profit Profit-per-

Employee

+ 0.959 0.919 5.66 0.09

Business-

per-

Employee

Net NPA

Capital

Adequacy

Ratio

The impact of the statistically significant variables namely deposits, advances, net NPA, business-per-employee, profit-per-employee and the capital adequacy ratio on the share price was further analyzed with a multi-variate regression. The correlation and regression coefficients registered values close to 1 and were higher than those observed when the impact of the variables on the share price was assessed individually. However it was not

statistically significant at the 95% confidence level and was significant only at the 90%

confidence level. The relationship from the above analysis given below:

IJBER Volume 1, Issue 1 (January, 2013)

International center of Science Education and Academic Research for Scholars

www.isearchscholars.com

191

5. Discussion and Analysis:

In the current study we focus exclusively on the impact of internal factors closely

monitored by the RBI on the profitability of one of India’s large public banks and also

its share price performance. These factors include deposits, advances, net NPA, return on assets, the capital adequacy ratio, business-per-employee and profit-per-employee. We find a strong positive correlation between deposits and net profit and also between deposits and the share price (Table1, 3). Deposits are often seen as a barometer of a bank’s financial health and stability. Similar results have been observed earlier by Smirlock & Brown (1986), who found a strong positive

relationship between demand deposits and bank profitability. Ganesan (2001) also

found a strong correlation between deposits and profitability for a group of public

sector banks in India.

We also find a strong positive correlation between advances and net profit and also between advances and the share price (Table1, 3). Banks generate significant profits from their margins on advances. Ganesan, (2001)

found a similar relationship between priority sector advances and profitability for a

group of Indian public sector banks.

We also find an inverse relationship between the net NPA and net profit and also between net NPA and the share price (Table1, 3). Nonperforming assets are charge off’s against profits and therefore negatively impact performance. In an earlier study Miller and Noulas, (1997) found that loan loss

provision and net charge offs had a significant negative effect on the profitability of

large banks. Bodla and Verma, (2006) have also indicated that provisioning for bad

loans significantly impacted profits of public sector banks in India.

We find a strong positive correlation between business generated-per-employee and net profit. Similarly a positive correlation is also observed between business and profit generated per employee and the share price (Table1, 3). These two indicators help in assessing the productivity of the work force

and the extent of their contribution to the operational efficiency of banks. Ben Naceur

and Goaied, (2001) found that the best performing Tunisian banks are those that

improve labor and capital productivity.

2) (Eqn. .3913233NPA)](Net *[246.288 NPA)](Net *[0.043 Employee) / (Business*[1056.537

Employee)](Profit / *[1152.459 -](Advances)*[0.0004 ](Deposits)*[-0.05 =Price Share

IJBER Volume 1, Issue 1 (January, 2013)

International center of Science Education and Academic Research for Scholars

www.isearchscholars.com

192

We don’t find a significant impact of the return on assets on profitability and the share price (Table1, 3). The return on assets ratio measures the asset usage efficiency. The capital adequacy ratio was found to be positively correlated to the stock price but had no effect on net profits (Table1, 3). The capital adequacy ratio can be used to gauge the credit risk of the bank. Sufian,

(2009) found that Malaysian banks with higher credit risk and loan concentration

exhibited lower profitability levels.

A multi-variate regression analysis (Table 2, 4) showing the combined effect of all the variables on net profit and the share price was carried out in the study. The results showed that impact of all the variables taken together on the net profit and share price was significantly higher than when assessed individually. The respective relationships are depicted in equations 1 and 2. This suggests that these variables synergistically impact both net profits and the share price. However Anova results suggest that the relationship of the variables with net profit was much stronger than with that of the share price (Table 2, 4). With a similar multi-variate analysis Bodla and Verma, (2006) found

that variables such as non-interest income, operating expenses, provisions ,

contingencies and spread have significant relationship with net profits.

Conclusion

In this paper, we study the impact of key internal determinants of profitability

namely deposits, advances, net NPA’s, business-per-employee, profit-per-employee, capital adequacy ratio and return on assets on both net income and the share price of a large Indian public bank. While deposits, advances, net NPA, business-per-employee and profit-per-employee positively influenced both net income and the share price net, the net NPA negatively impacted net income and the share price. The capital adequacy ratio influenced only the share price and did not

impact net income. Return on assets had no influence on either the net income or the

share price. A multi-variate regression analysis of the data indicated that the selected

variables synergistically impacted both net income and the share price. Thus interplay of

these and other factors drive profitability and share price performance.

IJBER Volume 1, Issue 1 (January, 2013)

International center of Science Education and Academic Research for Scholars

www.isearchscholars.com

193

References:

1. Athanasoglou, P.P., S.N. Brissimis, and M.D. Delis. (2008)”Bank-Specific,

Industry-Specific and Macroeconomic Determinants of Bank Profitability”.

Journal of International Financial Markets, Institutions & Money, Vol.18, Issue 2,

p121-136.

2. Balance sheet and Profit & Loss Account of a major public bank in India,

available from www.capitaline.com, accessed on 1/08/2011.

3. Barros, A. R. (2008). How to make bankers richer: The Brazilian financial market

with public and private banks. Quarterly Review of Economics & Finance, Vol.48

Issue 2, p217-236.

4. Ben Naceur S. and M. Goaied. (2001). The determinants of the Tunisian deposit

banks’

Performance. Applied Financial Economics, Vol.11:317-19.

5. Ben Naceur, S. and M. Goaied. (2008). The Determinants of Commercial Bank

Interest Margin and Profitability: Evidence from Tunisia. Frontiers in Finance and

Economics 5, no. 1 106-30.

6. Bodla, B.S. and R. Verma. (2006). Determinants of profitability of Banks in

India: A Multivariate Analysis. Journal of Services Research, Vol.6 Issue 2, p75-

89.

7. Boyd, J.H. and D.E. Runkle. (1993). Size and Performance of Banking Firms.

Testing the Predictions of Theory, Journal of Monetary Economics 31, 47-67.

IJBER Volume 1, Issue 1 (January, 2013)

International center of Science Education and Academic Research for Scholars

www.isearchscholars.com

194

8. Chirwa, E. W. (2003). Determinants of Commercial Banks Profitability in

Malawi: A Co Integration Approach. Applied Financial Economics, vol.13 Issue

8, p565-571.

9. Dietrich, A. and G. Wanzenried. (2011). Determinants of Bank Profitability

before and during the Crisis: Evidence from Switzerland. Journal of International

Financial Markets, Institutions &Money,Vol.21 Issue 3,p307-327.

10. Ganesan, P. (2001). Determination of profits and Profitability of Public Section

Banks in India: A Profit Function”. Journal of Financial Management & Analysis

& Analysis, Vol.14 Issue 1, p27-37.

11. Goddard, J., P. Molyneux, and J.O.S. Wilson. (2004). The Profitability of

European Banks: A Cross-Sectional and Dynamic Panel Analysis, Manchester

School, Vol. 72, No. 3, pp. 363-381.

12. Holden, K. and El-Bannany, Magdi. (2004). Investment in information

technology systems and other determinants of bank profitability in the UK.

Applied Financial Economics, Vol. 14 Issue 5, p361-365.

13. Kumar, S., & D. P. Warne. (2009). Parametric Determinants of Price-Earnings

Ratio in Indian Capital Markets. IUP Journal of Applied Finance, 15(9), 63-82.

14. Miller, S. M. and A. G. Noulas (1997). Portfolio Mix and Large-Bank

Profitability in the USA, Applied Economics, Vol. 29, No. 4, pp. 505-512.

15. Molyneux, P. and J. Thornton. (1992). Determinants of European bank

Profitability: A note. Journal of banking & Finance, Vol.16 Issue 6, p1173-1178.

IJBER Volume 1, Issue 1 (January, 2013)

International center of Science Education and Academic Research for Scholars

www.isearchscholars.com

195

16. Rajan R.G. and L. Zingales. (1998). Financial dependence and growth, American

Economic Review, 88:2, 559-586.

17. Report on The Trend and Progress of Banking in India 2010-2011, available from

http://rbidocs.rbi.org.in/rdocs/Publications/PDFs/0TPBI121111_FULL.pdf,

accessed on 2/10/ 2011.

18. Smirlock, M. and D. Brown. (1986). Collusion, Efficiency and Pricing Behavior:

Evidence From the Banking Industry, Economic Inquiry, vol. XXIV, no. 1, pp.85-

96.

19. Sufian, F and M.S. Habibullah. (2010). Accesing the Impact of Financial Crisis

on Bank Performance: Empirical Evidence from Indonesia". ASEAN Economic

Bulletin Vol. 27, No. 3 (2010), pp. 245-62.

20. Sufian, F. Factors Influencing Bank Profitability in a Developing Economy:

Empirical Evidence from Malaysia. Global Business Review 10, no. 2 (2009):

225-41.