Hong Kong Monetary Authority

160

ANNUAL REPORT ANNUAL REPORT

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Hong Kong Monetary Authority

A N N U A L R E P O R TA N N U A L R E P O R T

Established in April 1993, the Hong KongMonetary Authority (HKMA) is the governmentauthority in Hong Kong responsible formaintaining monetary and banking stability.The HKMA’s policy objectives are

• to maintain currency stability, within the framework of

the Linked Exchange Rate system, through sound

management of the Exchange Fund, monetary policy

operations and other means deemed necessary

• to promote the safety and stability of the banking system

through the regulation of banking business and the

business of taking deposits, and the supervision of

authorized institutions

• to enhance the efficiency, integrity and development of

the financial system, particularly payment and

settlement arrangements.

THE HONG KONG MONETARY AUTHORITY

The photographs

The first half of 2003 was a time of difficulty and challenge for people in HongKong. The second half brought new confidence and optimism. The theme forthe photographs in this year’s Annual Report is the Spirit of Hong Kong. Thephotographs show Hong Kong people working together, as individuals andin teams, often under pressure, to overcome challenges.

Contents

This Annual Report makes reference to documentsand other materials available on the HKMA websitewww.hkma.gov.hk. These references appear as in the relevant parts of the Report, followed bynavigation guidance from the HKMA homepage.

The full text of this Report is available on the HKMAwebsite in interactive form and on PDF files.

A summary version of this Report is also available.

All amounts in this Report are in Hong Kong dollarsunless otherwise stated.

2 Highlights of 2003

4 Chief Executive’s Statement

10 About The HKMA

14 Advisory Committees

20 Chief Executive’s Committee

24 The HKMA: The First 10 Years

33 Economic and Banking Environment

51 Monetary Stability

57 Banking Stability

75 Market Infrastructure

83 International Financial Centre

87 Reserves Management

92 The Exchange Fund

123 Professional and Corporate Services

132 Calendar of Events 2003

134 Annex and Tables

157 Abbreviations used in this Report

158 Reference Resources

The chapter on Banking Stability in this Annual Report is the reporton the working of the Banking Ordinance and the activities of theoffice of the Monetary Authority during 2003 submitted by theMonetary Authority to the Financial Secretary in accordance withSection 9 of the Banking Ordinance.

> www

2 ABOUT THE HKMA

HIGHLIGHTS OF 2003

The Hong Kong dollar is largely stable, despite a marked shift in marketsentiment from extreme pessimism in the second quarter to optimismlater in the year.

The HKMA completes the implementation of the risk-based supervisoryapproach.

Progress is made in preparing the legislation for the Deposit ProtectionScheme Bill and the establishment of a Commercial Credit ReferenceAgency in Hong Kong.

The economy contracts in the second quarter because of the SARSoutbreak, but rebounds sharply in the second half. Real GDP grows by3.3% in 2003.

With improved economic conditions in the second half, the bankingsector ends the year with a modest growth in profitability.

New $100 and $500 Hong Kong banknotes with advanced securityfeatures are issued in December.

ECONOMIC AND BANKING ENVIRONMENT

MONETARY STABILITY

BANKING STABILITY

3ANNUAL REPORT 2003HONG KONG MONETARY AUTHORITY

A euro clearing system is launched in April.

A Clearing and Settlement Systems Bill is introduced to the LegislativeCouncil in December to establish a statutory oversight regime andprovide for finality of settlement.

The first phase of the Asian Bond Fund is launched in June with anissue size of about US$1 billion.

In November the People’s Bank of China agrees to provide clearingarrangements for personal renminbi business in Hong Kong.

The Exchange Fund achieves a 10.2% investment return in 2003, 70 basispoints above the investment benchmark.

Hong Kong’s foreign currency reserve assets stand at US$118.4 billionat the end of 2003.

A permanent HKMA Information Centre, consisting of an exhibition areaand a library, is open to the public in December.

MARKET INFRASTRUCTURE

INTERNATIONAL FINANCIAL CENTRE

RESERVES MANAGEMENT

PROFESSIONAL AND CORPORATE SERVICES

CHIEF EXECUTIVE’S STATEMENT

After six years of difficulty and uncertainty, Hong Kong’s economyexperienced a strong rebound in the second half of 2003. Helped by amore benign global environment, and by measures to strengtheneconomic ties between Hong Kong and the Mainland, this reboundcontinued its momentum into 2004. A broad and sustained economicrecovery now appears to be in progress.

The rebound came after one of the most distressing episodes in HongKong’s recent history: the outbreak between March and June of SARS(severe acute respiratory syndrome), which infected 1,755 people in HongKong, of whom 299 died. The people of Hong Kong faced this epidemicwith courage and resilience, but the anxieties created by a new andvirulent disease inevitably had their effects on daily life, on economicactivity, and on confidence in the future. The difficulties in Hong Kongcame against the background of the spread of SARS on the Mainlandand in other parts of the world, uncertainties about the impact of thewar in Iraq, and concerns about the performance of some of the majorworld economies.

recovery in the secondhalf of 2003

5ANNUAL REPORT 2003HONG KONG MONETARY AUTHORITY

Economic indicators for the second quarter of 2003 dramaticallyreflected the sharp decline in activity and confidence. Tourist arrivalsplunged by 58% from a year earlier. Private consumption, already weak,continued to decline. The unemployment rate rose to a record high of8.7% in the middle of the year. Deflation deepened. Residential propertyprices continued to decline, and by July had dropped to about a third oftheir value when the property market peaked in 1997. The number ofresidential mortgages in negative equity rose to around 106,000 in June,which was around 22% of all residential mortgages.

These were indeed troubled times. But the economic impact of SARSwas short-lived, and some important sectors of the economy, such asmerchandise trade, were hardly affected at all. The rebound in thesecond half of the year was sufficient not only to cancel the negativeeconomic impact of SARS but also to propel Hong Kong into whatappears by all signs to be a robust recovery.

This rebound has been boosted by measures taken by the authorities inHong Kong and the Mainland to strengthen economic ties through theCloser Economic Partnership Arrangement (CEPA) and by the relaxationof restrictions on travel by individuals to Hong Kong. With the sharpturnaround in tourist visits in the third quarter, a marked revival inprivate consumption, and continued buoyancy in exports, Hong Kong’sreal GDP grew by 3.3% for the year as a whole, compared with 2.3% in2002 and 0.5% in 2001. Asset markets stabilised in the second half of theyear, and the number of residential mortgages in negative equitydeclined by 36% to around 67,600 by the end of the year. Deflation,if measured month on month, appears to have come to an end in aroundAugust 2003. The unemployment rate, though still high by historicalstandards, declined to 7.3% in the fourth quarter of 2003.

During this eventful and turbulent year the Hong Kong MonetaryAuthority achieved its objectives of maintaining currency stability,promoting the safety and stability of the banking system, and enhancingthe efficiency, integrity and development of the financial system. HongKong’s Exchange Fund, which is managed by the HKMA, produced aninvestment return of 10.2%: this was 70 basis points above the return onthe benchmark set by the Financial Secretary on the advice of theExchange Fund Advisory Committee.

the economic impactof SARS

sharp rebound supportedby deepening economicintegration with theMainland

strong investment returnon the Exchange Fund

6 CHIEF EXECUTIVE’S STATEMENT

a robust and effectivebanking system

a stable Hong Kongdollar against volatileworld markets

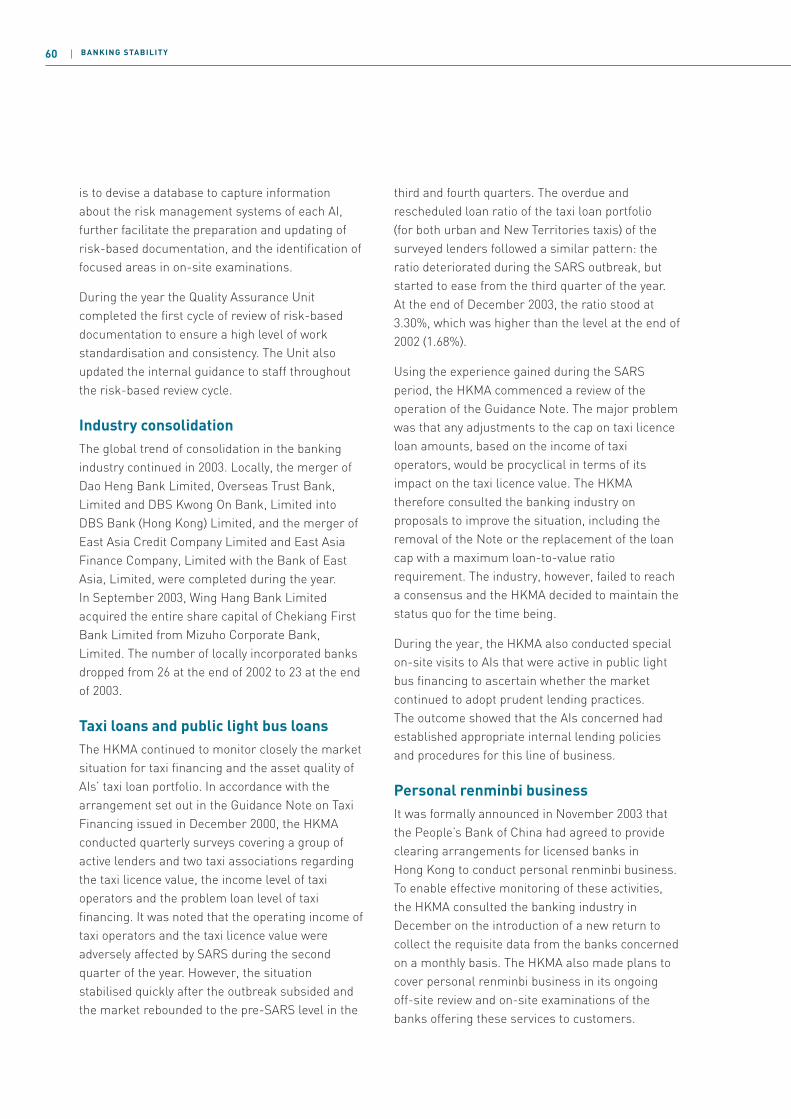

Hong Kong’s banking sector withstood the stresses and strains of thesecond quarter and came out stronger. Banks had to manage acombination of challenges brought on by persistent economic difficultyand exacerbated by SARS: sluggish loan growth, pressure on lendingmargins, negative equity, and a high bankruptcy rate. Like many otherorganisations, they also had to cope with the challenge of maintainingessential services and staff morale during a time of crisis. Not only didHong Kong’s banking system remain stable and effective: the bankingsector as a whole managed to show an increase in profits for the year asa whole, thanks to the markedly improved economic conditions in thesecond half of the year and to their own efforts to diversify business.The HKMA continued to work with the banking sector on the plannedimplementation of a Commercial Credit Reference Agency in 2004, andwith the Legislative Council on the bill for establishing a DepositProtection Scheme. Since August 2003 banks have been able to sharepositive consumer credit data. This will help nurture a healthier creditenvironment and provide more competitive products for borrowers withgood credit standing.

Despite the difficult second quarter and considerable volatility in theworld’s main currencies, the Hong Kong dollar continued to be stableunder the Linked Exchange Rate system. There was a moderate rise in12-month Hong Kong dollar forward points in April, reflecting concernsabout the effects of SARS. But the most striking event of the year wasthe sharp strengthening of the Hong Kong dollar in late September.Forward points went into discount, and the Aggregate Balance – themost sensitive component of the Monetary Base – grew to historicallyhigh levels as the HKMA sold Hong Kong dollars to banks in response tothe increased demand for Hong Kong dollar assets. Almost overnight,longstanding concerns about downward pressure on the Link gave wayto complaints from some that the Hong Kong dollar was being allowed tostrengthen too much.

This episode of strengthening is gradually playing itself out throughthe normal operation of the Currency Board arrangements, throughwhich the Linked Exchange Rate is maintained. The causes of thestrengthening were complex, but there were three main elements.Economic recovery and a rapid revival in confidence attracted a stronginflow of funds into the Hong Kong dollar. The sharp decline in the valueof the US dollar against other major currencies pulled the Hong Kongdollar down with it – unjustifiably in the view of the market. Politicalpressure from outside for a revaluation of the renminbi encouraged theview that, if the renminbi were to be revalued, the Hong Kong dollar

7ANNUAL REPORT 2003HONG KONG MONETARY AUTHORITY

developing Hong Kong asan international financialcentre

introduction of renminbibanking in Hong Kong

would be pulled up with it. The strong inflow of funds is a matter of fact.The other two elements are an interesting example of how suddenlymarket sentiment can change.

A strengthening Hong Kong dollar is a much more straightforwardproblem than a weakening Hong Kong dollar. In addition to normalCurrency Board operations, the HKMA has a range of tools – all of themconsistent with Currency Board principles – that can be deployed todampen excessive volatility in the Hong Kong dollar. Together with theSub-Committee on Currency Board Operations of the Exchange FundAdvisory Committee, we shall continue to watch the situation carefully.

The excitement over the short-term movements of markets in the lastquarter of 2003 may perhaps have obscured the longer-term view. Theweakness of the US dollar has had the benign effect of moderating thepain of structural adjustment arising from the increasing economicintegration between the Mainland and Hong Kong. It has helped lessenthe extent of deflation necessary as part of that structural adjustment.Along with deflation, it has contributed to a decline in Hong Kong’s realeffective exchange rate – the true measure of an economy’scompetitiveness – of as much as 26% between its peak in August 1998and the end of 2003.

Hong Kong’s competitiveness as an international city has beenstrengthened considerably by the reductions in the cost of doingbusiness here. But competitiveness is not just a matter of low costs.An international city must have the institutions, the talent, and theinfrastructure to attract business. An important, though largely invisible,part of this infrastructure is the machinery for clearing and settlingfinancial transactions and for linking the financial system with otherfinancial systems.

Hong Kong has one of the world’s most advanced financialinfrastructures. We introduced real time gross settlement for the HongKong dollar in 1996 and extended this to the US dollar in 2000. In April2003 we launched a euro clearing system, and in November, followingapproval from the State Council, the People’s Bank of China agreed toprovide clearing arrangements for personal renminbi business in HongKong. In February 2004, 35 banks in Hong Kong began to providepersonal renminbi deposit, remittance and exchange services. Thesenew arrangements are made on the principle of cautious and gradualchange, taking into account the fact that the renminbi is not yet a fullyconvertible currency. Renminbi services in Hong Kong will facilitate the

8 CHIEF EXECUTIVE’S STATEMENT

new Hong Kongbanknotes

international standards

operational autonomyof the HKMA

growing economic integration between Hong Kong and the Mainland.Looking further ahead, they will also help place Hong Kong in anexcellent position as a centre for China’s international financialtransactions with the gradual liberalisation of the Mainland’s monetaryand financial systems in the future.

Other developments in Hong Kong’s financial infrastructure in 2003included the introduction in June of cheque imaging and truncation,which greatly reduces the need for physically delivering cheques forclearance, and the launch by the note-issuing banks in December of new$100 and $500 banknotes. These are the first of a new series of HongKong banknotes with fresh designs and improved security features: theremaining denominations in the new series will be issued later in 2004.

One of the aims of the HKMA is to ensure that Hong Kong’s banking andmonetary systems comply with international codes and standards.For this reason, the groundwork continued in 2003 for implementing theNew Basel Capital Accord, which is targeted for implementation in late2006. In June 2003 the joint IMF-World Bank mission under the FinancialSector Assessment Programme (FSAP) delivered its comprehensivereport on Hong Kong. The report confirmed that Hong Kongcomplies with key international standards, that its financial systemis fundamentally sound, and that its market infrastructure is robustand efficient.

The FSAP mission made a number of recommendations for improvingthe regulation and transparency of Hong Kong’s financial system.The great majority of these have been swiftly implemented. One of therecommendations was that the legal foundation of the HKMA should beclarified and the operational autonomy of the HKMA for theimplementation of monetary policy should be explicitly recognised in aformal document. On 25 June the Financial Secretary and I, as MonetaryAuthority, exchanged a series of letters setting out the division betweenthe two of us of functions and responsibilities in monetary and financialaffairs. These letters, which are public documents, summarisegovernance and other provisions, under the Exchange Fund and BankingOrdinances, that have been in place for some years, and as such theymake no change to existing arrangements.

Two aspects of this Exchange of Letters are, however, worth drawingparticular attention to for the emphasis they place on the operationalindependence of the HKMA. First, disclosure is made in the letters, forthe first time, of the details of the delegation of statutory powers from

9ANNUAL REPORT 2003HONG KONG MONETARY AUTHORITY

20th anniversary of theLink, 10th anniversaryof the HKMA

the Financial Secretary to the Monetary Authority. The FinancialSecretary makes an undertaking to disclose publicly, within threemonths and giving reasons, any exercise by himself of those delegatedpowers or any overriding of the Monetary Authority in his exercise of thedelegated powers. Secondly, the Financial Secretary formally lays down,for the first time, the monetary policy objective and the structure of HongKong’s monetary system: a stable exchange value of the Hong Kongdollar in terms of its exchange rate against the US dollar at aroundHK$7.80 to US$1 maintained by Currency Board arrangements.

These are, of course, the monetary arrangements that have been inplace in Hong Kong for 20 years, and it is perhaps appropriate that, as itcomes of age, the Linked Exchange Rate system, which was introducedon 17 October 1983, should be formally enunciated in this way. In April2003 we also marked the 10th anniversary of the foundation of theHKMA. This has been a momentous decade for Hong Kong, and a time ofgreat difficulty and anxiety. I believe, however, that the HKMA can lookback on its achievements during these years with some satisfaction. Inits contributions to maintaining monetary and financial stability, theHKMA has relied heavily upon its greatest asset – an excellent staff –and I pay tribute to them for their unfailing dedication and determinationover the years. The HKMA has also received skilled guidance fromsuccessive Financial Secretaries and Members of the Exchange FundAdvisory Committee. And, most important of all, we have enjoyed thesupport and confidence of the people of Hong Kong: without this, andwithout the co-operation from their representatives on the LegislativeCouncil, we could not fulfil our objectives.

Ten challenging years have taught us that there are few certainties andmany surprises in this rapidly changing world. It would be unwise to tryto predict what might happen in the next decade, although the prospectsfor Hong Kong in the coming year at least seem to be brighter than theyhave been for some time. The HKMA will, however, continue to do itsbest to ensure that Hong Kong’s monetary and financial systems havethe stability, the infrastructure, and the resources to manage whateverchallenges, opportunities and crises that may lie ahead.

Joseph YamChief Executive

ABOUT THE HKMA

The Hong Kong Monetary Authority is Hong Kong’s central bankinginstitution. The HKMA has four main functions: maintaining the stabilityof the Hong Kong dollar; promoting the safety of Hong Kong’s bankingsystem; managing Hong Kong’s official reserves; and maintaining anddeveloping Hong Kong’s financial infrastructure.

THE HKMA’S LEGAL MANDATEThe HKMA was established on 1 April 1993 bymerging the Office of the Exchange Fund with theOffice of the Commissioner of Banking. To facilitatethe establishment of the HKMA, the LegislativeCouncil passed amendments to the Exchange FundOrdinance in 1992 empowering the FinancialSecretary to appoint a Monetary Authority.

The powers, functions and responsibilities of theMonetary Authority are set out in the ExchangeFund Ordinance, the Banking Ordinance and otherrelevant Ordinances. The division of functions andresponsibilities in monetary and financial affairsbetween the Financial Secretary and the MonetaryAuthority is set out in an Exchange of Lettersbetween the two dated 25 June 2003. ThisExchange of Letters also discloses the delegationsmade by the Financial Secretary to the MonetaryAuthority under these Ordinances. The letters arepublic documents: copies of them may be found onthe HKMA website.

The Exchange Fund Ordinance establishes theExchange Fund under the control of the FinancialSecretary. According to the Ordinance, the Fundshall be used primarily for affecting the exchangevalue of the Hong Kong dollar. It may also be usedfor maintaining the stability and integrity of themonetary and financial systems of Hong Kong,with a view to maintaining Hong Kong as aninternational financial centre.

The Monetary Authority is appointed under theExchange Fund Ordinance to assist the Financial

Secretary in performing his functions under theExchange Fund Ordinance and to perform such otherfunctions as are assigned by other Ordinances or bythe Financial Secretary. The office of the MonetaryAuthority is known as the HKMA and the MonetaryAuthority as the Chief Executive of the HKMA.

The Banking Ordinance provides the MonetaryAuthority with the responsibility and powers forregulating and supervising banking business andthe business of taking deposits. Under theOrdinance, the Monetary Authority is responsible,among other things, for the authorization oflicensed banks, restricted licence banks, anddeposit-taking institutions in Hong Kong.

> About the HKMA > The HKMA > Who we arewww

THE HKMA AND THE HONG KONGSAR GOVERNMENTThe HKMA is an integral part of the Hong Kong SARGovernment, but is able to employ staff on termsdifferent from those of the civil service in order toattract personnel of the right experience andexpertise. The Chief Executive of the HKMAremains a public officer, as do his staff. In itsday-to-day work the HKMA operates with a highdegree of autonomy within the relevant statutorypowers conferred upon, or delegated to, theMonetary Authority.

The Financial Secretary is responsible fordetermining the monetary policy objective and thestructure of the monetary system of Hong Kong:A letter from the Financial Secretary to the

11ANNUAL REPORT 2003HONG KONG MONETARY AUTHORITY

Monetary Authority dated 25 June 2003 specifiesthat these should be currency stability defined asa stable exchange value at around HK$7.80 toone US dollar maintained by Currency Boardarrangements. The Monetary Authority is on hisown responsible for achieving the monetary policyobjective, including determining the strategy,instruments and operational means for doing so.He is also responsible for maintaining the stabilityand integrity of the monetary system of Hong Kong.

The Financial Secretary, assisted by the Secretaryfor Financial Services and the Treasury, hasresponsibility for policies for maintaining thestability and integrity of Hong Kong’s financialsystem and the status of Hong Kong as aninternational financial centre. In support of thesepolicies, the Monetary Authority is responsible,among other things, for

• promoting the general stability and effectiveworking of the banking system

• promoting the development of the debt market,in co-operation with other relevant bodies

• matters relating to the issuance and circulation oflegal tender notes and coins

• promoting the safety and efficiency of thefinancial infrastructure through the developmentof payment, clearing and settlement systemsand, where appropriate, the operation ofthese systems

• seeking to promote, in co-operation with otherrelevant bodies, confidence in Hong Kong’smonetary and financial systems, and appropriatemarket development initiatives to help strengthenthe international competitiveness of Hong Kong’sfinancial services.

The Exchange Fund is under the control of theFinancial Secretary. The Monetary Authority, underdelegation from the Financial Secretary, isresponsible to the Financial Secretary for the use ofthe Exchange Fund, and for the investmentmanagement of the Fund.

> About the HKMA > The HKMA > Who we arewww

ACCOUNTABILITY ANDTRANSPARENCYThe autonomy given to the HKMA in its day-to-dayoperations, and in the methods it uses to pursuepolicy objectives determined by the Government,is complemented by a high degree of accountabilityand transparency.

The HKMA serves Hong Kong by promotingmonetary and banking stability, by managing theofficial reserves effectively, and by developing arobust and diverse financial infrastructure. Theseprocesses help to strengthen Hong Kong’s role asan international financial centre and to foster HongKong’s economic well-being. The HKMA must havethe confidence of the community if it is to performits duties well. The HKMA therefore takes seriouslythe duty of explaining its policies and work to thegeneral public and makes every effort to addressany concerns within the community relevant to theHKMA’s responsibilities.

The HKMA is accountable to the people of HongKong through the Financial Secretary, whoappoints the Monetary Authority, and through thelaws passed by the Legislative Council that setout the Monetary Authority’s powers andresponsibilities. The HKMA also recognises abroader responsibility to promote a betterunderstanding of its roles and objectives and tokeep itself informed of community concerns. In itsday-to-day operations and in its wider contactswith the community, the HKMA pursues a policy oftransparency and accessibility. This policy has twomain objectives:

• to keep the financial industry and the public asfully informed about the work of the HKMA aspossible, subject to considerations of marketsensitivity, commercial confidentiality andstatutory restrictions on disclosure ofconfidential information

• to ensure that the HKMA is in touch with, andresponsive to, the community it serves.

The HKMA seeks to follow international bestpractices in its transparency arrangements. Itmaintains extensive relations with the mass media

12 ABOUT THE HKMA

and produces a range of regular and specialpublications in both English and Chinese.The HKMA’s bilingual website (www.hkma.gov.hk)carries all HKMA’s publications, press releases,speeches and presentations, in addition to specialsections on research, statistics, consumerinformation and other topics. The HKMA maintainsan Information Centre at its offices, consisting of alibrary and an exhibition area, which is open to thepublic six days a week. The HKMA also organises anannual public education programme, which seeksto inform the public, and in particular students,about the work of the HKMA through seminars andguided tours at the Information Centre. The HKMA’sweekly Viewpoint column, carried on the HKMAwebsite and in about ten Hong Kong newspapers,informs the public about aspects of the HKMA’swork. Further information on the HKMA’s mediawork, publications and public educationprogrammes is contained in the Chapter onProfessional and Corporate Services on page 123.

> Viewpointwww

> HKMA Information Centrewww

Over the years the HKMA has progressivelyincreased the detail and frequency of its disclosureof information on the Exchange Fund and CurrencyBoard Accounts. Since 1999 the HKMA hasparticipated in the International Monetary Fund’sSpecial Data Dissemination Standard project forcentral banks. The HKMA publishes records ofmeetings of the Exchange Fund AdvisoryCommittee’s Sub-Committee on Currency BoardOperations, along with the monthly reports onCurrency Board operations. The supervisorypolicies and guidelines on banking have beenpublished on the website since 1996.

> Information Centre > Press Releases > The Exchange Fund categorywww

> Policy Areas > Supervisory Policy Manualwww

The relations between the HKMA and theLegislative Council play an important part in theprocess of accountability and transparency. There isa formal commitment from the Chief Executive ofthe HKMA to appear before the Legislative CouncilPanel on Financial Affairs three times a year to briefMembers and to answer questions on the HKMA’s

work. At one of these briefings, usually in May, theHKMA’s Annual Report is presented. In addition,staff from the HKMA attend Legislative CouncilPanel meetings to explain and discuss particularissues, and Committee meetings to assistMembers in their scrutiny of draft legislation.

> Information Centre > Legislative Council Issueswww

ADVISORY AND OTHERCOMMITTEESExchange Fund Advisory CommitteeIn his control of the Exchange Fund, the FinancialSecretary is advised by the Exchange Fund AdvisoryCommittee (EFAC). EFAC is established underSection 3(1) of the Exchange Fund Ordinance,which requires the Financial Secretary to consultthe Committee in his exercise of control of theExchange Fund. The Financial Secretary isex officio chairman of EFAC. Other members,including the Monetary Authority, are appointed ina personal capacity by the Financial Secretaryunder the delegated authority of the ChiefExecutive of the Hong Kong SAR. Members of EFACare appointed for the expertise and experience thatthey can bring to the committee. Such expertiseand experience includes knowledge of monetary,financial and economic affairs and of investmentissues, as well as of accounting, management,business and legal matters.

EFAC advises the Financial Secretary oninvestment policies and strategies for the Fund andon projects, such as the development of financialinfrastructure, that are charged to the Fund. Sincethe operating and staff costs of the HKMA are alsochargeable to the Exchange Fund, EFAC advisesthe Financial Secretary on the HKMA’s annualadministration budget and on the terms andconditions of service of HKMA staff. EFAC meetsregularly and on other occasions when particularadvice is being sought.

EFAC is assisted in its work by three specialisedsub-committees, which monitor specific areas ofthe HKMA’s work and report and makerecommendations to EFAC.

13ANNUAL REPORT 2003HONG KONG MONETARY AUTHORITY

The Sub-Committee on Currency Board Operationsmonitors and reports on the Currency Boardarrangements that underpin Hong Kong’s LinkedExchange Rate system. It is responsible, amongother things, for ensuring that Currency Boardoperations are in accordance with establishedpolicy, recommending improvements to theCurrency Board system, and ensuring a high degreeof transparency in the operation of the system. TheSub-Committee is composed of members of EFAC,a representative of the Hong Kong Association ofBanks, additional members with expertise on theCurrency Board system, and senior HKMA staff.Records of the Sub-Committee’s meetings and thereports on Currency Board operations submittedmonthly to the Sub-Committee are published.

> Information Centre > Press Releases > Monetary Policy categorywww

The Remuneration and Finance Sub-Committeemakes recommendations to EFAC on pay andconditions of service, human resources policy,and budgetary and administrative issues. TheSub-Committee is composed of six non-officialnon-banking Members of EFAC.

The Audit Sub-Committee reviews and reports toEFAC on the HKMA’s financial reporting processand the adequacy and effectiveness of the internalcontrol systems of the HKMA. The Sub-Committeereviews the HKMA’s financial statements, and thecomposition and accounting principles adopted insuch statements. It also examines and reviews withboth the external and internal auditors the scopeand results of their audits. The Sub-Committeeconsists of four non-executive, non-officialmembers of EFAC. It held three meetings in 2003.

The Banking Advisory CommitteeThe Banking Advisory Committee is establishedunder Section 4(1) of the Banking Ordinance toadvise the Chief Executive of the Hong Kong SARon matters relating to the Banking Ordinance,in particular matters relating to banks and thecarrying on of banking business. The Committeeconsists of the Financial Secretary, who is the

chairman, the Monetary Authority, and otherpersons appointed by the Financial Secretary underthe delegated authority of the Chief Executive of theHong Kong SAR.

The Deposit-Taking CompaniesAdvisory CommitteeThe Deposit-Taking Companies Advisory Committeeis established under Section 5(1) of the BankingOrdinance to advise the Chief Executive of the HongKong SAR on matters relating to the BankingOrdinance, in particular matters relating to deposit-taking companies and restricted licence banks andthe carrying on of a business of taking deposits bythem. The Committee consists of the FinancialSecretary, who is the chairman, the MonetaryAuthority, and other persons appointed by theFinancial Secretary under the delegated authority ofthe Chief Executive of the Hong Kong SAR.

Chief Executive’s CommitteeThe Chief Executive’s Committee is chaired by theChief Executive of the HKMA and consists of theDeputy Chief Executives and the ExecutiveDirectors of the HKMA. The Committee meetsweekly to report to the Chief Executive on theprogress of major tasks being undertaken by thevarious departments of the HKMA and to advisehim on policy matters relating to the operations ofthe HKMA.

The membership lists of the various Committees andSub-Committees are given on pages 14 to 22. Briefbiographies and the Code of Conduct for EFACMembers can be found on the HKMA website.A Register of Members’ Interests, which contains thedeclarations of interests by Members of EFAC, isavailable for public inspection during office hours(9:00 a.m. to 5:00 p.m. Monday to Friday and 9.00 a.m.to 12 noon Saturday) at the HKMA, 55th Floor,Two International Finance Centre, 8 Finance Street,Central, Hong Kong.

> About the HKMA > Advisory Committeeswww

ADVISORY COMMITTEES

Chairman

The Hon. Henry Tang Ying Yen, GBS, JP

The Financial Secretary

(from 4 August 2003)

The Hon. Antony Leung, GBS, JP

The Financial Secretary

(until 16 July 2003)

THE EXCHANGE FUND ADVISORY COMMITTEE

Members

Mr Joseph Yam, GBS, JP

The Monetary Authority

Dr The Hon. David Li Kwok Po, LLD, GBS, JP

Chairman and Chief Executive

The Bank of East Asia Limited

Mr Marvin Cheung Kin Tung, DBA Hon., SBS, JP

Mr David Eldon, JP

Chairman

The Hongkong and Shanghai Banking Corporation Limited

Mr Patrick Wang Mr Victor Lo Professor Richard Wong Mr Marvin Cheung Mr Joseph YamMr Mervyn Davies

15ANNUAL REPORT 2003HONG KONG MONETARY AUTHORITY

Mr E Mervyn DaviesGroup Chief Executive

Standard Chartered PLC

Dr James Z M Kung, GBS

Chairman

Chekiang First Bank Limited

Professor Richard Y C Wong, SBS, JP

Dean, Faculty of Business and Economics

The University of Hong Kong

Mr Christopher Cheng Wai Chee, JP

Chairman

USI Holdings Limited

Mr Victor Lo Chung Wing, GBS, JP

Chairman and Chief Executive

Gold Peak Industries (Holdings) Limited

Mr Robert C Tang, SC, JP

Barrister-at-Law

Mr Patrick Wang Shui Chung, JP

Chairman and Chief Executive Officer

Johnson Electric Holdings Limited

Mr He GuangbeiVice Chairman & Chief Executive

Bank of China (Hong Kong) Limited

(from 26 June 2003)

Dr Liu JinbaoVice Chairman & Chief Executive

Bank of China (Hong Kong) Limited

(until 28 May 2003)

Secretary

Mr Christopher Munn

Mr Henry Tang Dr David Li Mr David Eldon Mr Robert TangMr Christopher Cheng Mr He GuangbeiDr James Kung

16 ADVISORY COMMITTEES

THE EXCHANGE FUND ADVISORY COMMITTEESUB-COMMITTEE ON CURRENCY BOARD OPERATIONS

Chairman

Mr Joseph Yam, GBS, JP

The Monetary Authority

Members

Mr Norman Chan, SBS, JP

Deputy Chief Executive

Hong Kong Monetary Authority

Mr William RybackDeputy Chief Executive

Hong Kong Monetary Authority

(from 27 August 2003)

Mr David Carse, SBS, JP

Deputy Chief Executive

Hong Kong Monetary Authority

(until 30 September 2003)

Dr The Hon. David Li Kwok Po, LLD, GBS, JP

Chairman and Chief Executive

The Bank of East Asia Limited

Mr Marvin Cheung Kin Tung, DBA Hon., SBS, JP

Professor Richard Y C Wong, SBS, JP

Dean, Faculty of Business and Economics

The University of Hong Kong

Mr John GreenwoodGroup Chief Economist

INVESCO Asset Management Limited

Professor Tsang Shu KiDepartment of Economics

Hong Kong Baptist University

Mr Raymond C F OrChairman

The Hong Kong Association of Banks

Secretary

Mr Christopher Munn

17ANNUAL REPORT 2003HONG KONG MONETARY AUTHORITY

THE EXCHANGE FUNDADVISORY COMMITTEEREMUNERATION AND FINANCESUB-COMMITTEE

Chairman

Mr Marvin Cheung Kin Tung, DBA Hon., SBS, JP

Members

Professor Richard Y C Wong, SBS, JP

Dean, Faculty of Business and Economics

The University of Hong Kong

Mr Christopher Cheng Wai Chee, JP

Chairman

USI Holdings Limited

Mr Victor Lo Chung Wing, GBS, JP

Chairman and Chief Executive

Gold Peak Industries (Holdings) Limited

Mr Robert C Tang, SC, JP

Barrister-at-Law

Mr Patrick Wang Shui Chung, JP

Chairman and Chief Executive Officer

Johnson Electric Holdings Limited

Secretary

Mr Christopher Munn

THE EXCHANGE FUNDADVISORY COMMITTEEAUDIT SUB-COMMITTEE

Chairman

Mr Marvin Cheung Kin Tung, DBA Hon., SBS, JP

Members

Mr David Eldon, JP

Chairman

The Hongkong and Shanghai Banking Corporation Limited

Mr E Mervyn DaviesGroup Chief Executive

Standard Chartered PLC

Mr He GuangbeiVice Chairman & Chief Executive

Bank of China (Hong Kong) Limited

(from 26 June 2003)

Dr Liu JinbaoVice Chairman & Chief Executive

Bank of China (Hong Kong) Limited

(until 28 May 2003)

Secretary

Mr Christopher Munn

18 ADVISORY COMMITTEES

THE BANKING ADVISORY COMMITTEE

Chairman

The Hon. Henry Tang Ying Yen, GBS, JP

The Financial Secretary

(from 4 August 2003)

The Hon. Antony Leung, GBS, JP

The Financial Secretary

(until 16 July 2003)

Ex Officio Member

Mr Joseph Yam, GBS, JP

The Monetary Authority

Members

The Hon. Frederick Ma Si Hang, JP

Secretary for Financial Services and the Treasury

Mr He GuangbeiVice Chairman & Chief Executive

Bank of China (Hong Kong) Limited

Representing Bank of China (Hong Kong) Limited

(from 29 May 2003)

Mr Raymond C F OrGeneral Manager

The Hongkong and Shanghai Banking Corporation Limited

Representing The Hongkong and Shanghai Banking

Corporation Limited

Mr Peter T S Wong, JP

Director

Standard Chartered Bank

Representing Standard Chartered Bank

Mr Didier BalmeHead of North & East Asia

BNP Paribas

Mrs Chan Hui Dor Lam DoreenPresident & Chief Executive Officer

Citic Ka Wah Bank Limited

Mrs Angelina P L Lee, JP

Partner

Woo, Kwan, Lee & Lo

Solicitors and Notaries

Dr The Hon. David Li Kwok Po, LLD, GBS, JP

Chairman and Chief Executive

The Bank of East Asia Limited

Mr Tatsuo TanakaDirector and Chief Executive Officer for China

The Bank of Tokyo-Mitsubishi, Ltd.

(from 8 July 2003)

Mr Samuel N TsienPresident and Chief Executive Officer

Bank of America (Asia) Limited

Mr David S Y Wong, JP

Chairman

Dah Sing Bank Limited

Ms Maria XuerebFinancial Services Partner

Deloitte Touche Tohmatsu

Mr Tomonori KobayashiExecutive Officer and General Manager

Hong Kong Branch

Mizuho Corporate Bank, Ltd

(until 1 April 2003)

Dr Liu JinbaoVice Chairman & Chief Executive

Bank of China (Hong Kong) Limited

Representing Bank of China (Hong Kong) Limited

(until 28 May 2003)

Secretary

Ms Carman Chiu

19ANNUAL REPORT 2003HONG KONG MONETARY AUTHORITY

THE DEPOSIT-TAKING COMPANIES ADVISORY COMMITTEE

Chairman

The Hon. Henry Tang Ying Yen, GBS, JP

The Financial Secretary

(from 4 August 2003)

The Hon. Antony Leung, GBS, JP

The Financial Secretary

(until 16 July 2003)

Ex Officio Member

Mr Joseph Yam, GBS, JP

The Monetary Authority

Members

The Hon. Frederick Ma Si Hang, JP

Secretary for Financial Services and the Treasury

Mr Andrew Sheng, SBS, JP

Chairman

Securities and Futures Commission

Representing The Securities and Futures Commission

Mrs Pamela Chan Wong Shui, BBS, JP

Chief Executive

Consumer Council

Representing The Consumer Council

(from 1 June 2003)

Mr Clifford ForsterChairman

Hong Kong Association of Restricted Licence Banks and

Deposit-Taking Companies (The DTC Association)

Representing The DTC Association

Mr Mohan KohliPartner

Financial Services Division

PricewaterhouseCoopers

Mr Andrew KuoManaging Director

J.P. Morgan Securities (Asia Pacific) Limited

(from 1 June 2003)

The Hon. Eric K C Li, GBS, JP

Senior Partner

Li, Tang, Chen & Co

Certified Public Accountants

Mr Geoffrey J. MansfieldDirector and Chief Executive

PrimeCredit Limited

(from 1 June 2003)

Mr Mok Wai-kinDirector

Hang Seng Finance Limited

Mr Poon Kwok YuenPresident & Chief Executive Officer

AIG Finance (Hong Kong) Limited

(from 9 December 2003)

Mr Tan Yoke KongGeneral Manager

JCG Finance Company, Limited

Mr Frank J. WangDeputy Chief Executive

Wing Hang Finance Company Limited

(from 1 June 2003)

Mr Jackson CheungChief Executive

Société Générale Asia Limited

(until 31 May 2003)

Mr Randolph SullivanManaging Director

Dao Heng Finance Limited

(until 31 May 2003)

Mr Kotaro TakamoriManaging Director

ORIX Asia Limited

(until 1 September 2003)

Secretary

Ms Carman Chiu

CHIEF EXECUTIVE’S COMMITTEE

DEPUTY CHIEF EXECUTIVE

William RybackWilliam Ryback is in charge ofthe full range of banking policy,development and supervisionissues. Prior to joining the HKMA inAugust 2003, Mr Ryback was SeniorAssociate Director of the Division ofBank Supervision at the Board ofGovernors of the Federal ReserveSystem in Washington, D.C. He wasalso Chairman of the Board ofDirectors of the Association ofBank Supervisors of the Americas.He was the Board of Governorsrepresentative on the BaselCommittee on Banking Supervisionfrom 1986 to 1994.

CHIEF EXECUTIVE

Joseph Yam, GBS, JP

Joseph Yam has served as Chief Executive of the HKMA since itsestablishment in April 1993. Mr Yam began his civil service career inHong Kong as a Statistician in 1971, and became an Economist in 1976.His involvement in monetary affairs in Hong Kong started when he wasappointed as Principal Assistant Secretary for Monetary Affairs in 1982.He helped put together Hong Kong’s Linked Exchange Rate system in1983. He was subsequently appointed Deputy Secretary for MonetaryAffairs in 1985 and Director of the Office of the Exchange Fund in 1991.

DEPUTY CHIEF EXECUTIVE

David Carse, SBS, JP

David Carse joined the HKMA in1993 as Deputy Chief Executive withresponsibilities for banking policy,development and supervisionissues. He left the HKMA inSeptember 2003.

DEPUTY CHIEF EXECUTIVE

Norman Chan, SBS, JP

Norman Chan has responsibility formonetary management, financialinfrastructure, research, reservesmanagement and internationalfinance. He has been with the HKMAsince its establishment in 1993.Mr Chan joined the Hong KongGovernment as an AdministrativeOfficer in 1976. In 1991 he wasappointed Deputy Director(Monetary Management) of theOffice of the Exchange Fund. Hebecame an Executive Director of theHKMA when it was established in1993 and was made a Deputy ChiefExecutive in 1996.

21ANNUAL REPORT 2003HONG KONG MONETARY AUTHORITY

GENERAL COUNSEL

Stefan Gannon, JP

Stefan Gannon has been GeneralCounsel of the HKMA since itsestablishment in 1993. A barrister,Mr Gannon was the Legal Adviserto the Monetary Affairs Branch ofthe Hong Kong Government from1987 to 1993.

EXECUTIVE DIRECTOR(MONETARY MANAGEMENT ANDINFRASTRUCTURE)

James H Lau Jr, JP

James Lau is responsible formonetary management and marketinfrastructure. He was appointedHead (Monetary Policy) on theestablishment of the HKMA in 1993and became Executive Director(External) in 1994. Mr Lau joinedthe Hong Kong Government as anAdministrative Officer in 1979. Hewas Hong Kong’s Deputy PermanentRepresentative to the GATT inGeneva from 1986 to 1990 beforejoining the Office of the ExchangeFund as Assistant Director(Monetary Management) in 1991.

EXECUTIVE DIRECTOR(BANKING SUPERVISION)

Y K Choi, JP

Y K Choi is responsible for bankingsupervision. He has been with theHKMA since 1993. Mr Choi joinedthe Office of the Commissioner ofBanking in 1974 and becameAssistant Commissioner ofBanking in 1990 after a one-yearsecondment to the Bank ofEngland. In 1990 he was secondedto the Office of the Exchange Fundfor three years and was appointedHead (Banking Policy) at theHKMA in 1993. He became theHKMA’s Head (Administration) in1994 and was appointed to hispresent position in 1995.

EXECUTIVE DIRECTOR(BANKING DEVELOPMENT)

Raymond Li, JP

Raymond Li is responsible forbanking reform and developmentissues as well as licensing andspecialised supervision such ase-banking. Mr Li joined the HongKong Government as anAdministrative Officer in 1982 andbecame Principal AssistantSecretary (Monetary Affairs) in 1990.He was appointed Head (BankingDevelopment) at the HKMA in 1993and took up the post of Head(Administration) in 1995. He waspromoted to Executive Director(Banking Policy) in 1996 andappointed Executive Director(Corporate Services) in September2000. Mr Li was appointed to hispresent position in June 2001.

EXECUTIVE DIRECTOR(RESERVES MANAGEMENT)

Amy Yip, BBS, JP

Amy Yip is responsible for theinvestment management of theExchange Fund. Prior to joiningthe HKMA in 1996, Ms Yip workedat JP Morgan, Rothschild AssetManagement and Citibank.

EXECUTIVE DIRECTOR(EXTERNAL)

Julia Leung, JP

Julia Leung is responsible forinternational affairs relating tomultilateral agencies and centralbank co-operation, the HKMAoverseas offices, and Chinaresearch and relations. Ms Leungjoined the HKMA in 1994 as SeniorManager in charge of press andpublications matters. She waspromoted to Division Head in 1996,and appointed to her presentposition in April 2000.

22 CHIEF EXECUTIVE’S COMMITTEE

EXECUTIVE DIRECTOR(BANKING POLICY)

Simon Topping, JP

Simon Topping is responsible forthe development of bankingsupervisory policies. He joined theHKMA in 1995 as a Division Headin the Banking SupervisionDepartment and was appointed tohis present position in September2000. Prior to joining the HKMAhe worked for the Bank ofEngland and the InternationalMonetary Fund.

EXECUTIVE DIRECTOR(RESEARCH)

Stefan GerlachStefan Gerlach is in charge ofresearch matters. He is alsoDirector of the Hong Kong Institutefor Monetary Research. Dr Gerlachjoined the HKMA in 2001. He hasextensive experience in the researchand policy fields. Prior to joining theHKMA, he worked in the Bank forInternational Settlements since1992, where he was the Head ofMonetary Policy and ExchangeRates, Research and Policy AnalysisGroup of the Monetary andEconomic Department.

EXECUTIVE DIRECTOR(CORPORATE SERVICES)

Eddie Yue, JP

Eddie Yue is responsible formatters relating to corporatedevelopment, human resources,administration, finance andinformation technology.Mr Yue began his career as anAdministrative Officer in theHong Kong Government in 1986.He joined the HKMA in 1993 asa Senior Manager, and wassubsequently promoted to DivisionHead in 1994. He has worked in anumber of divisions, includingMonetary Management, ExternalRelations, and BankingDevelopment, and has served asAdministrative Assistant to theChief Executive of the HKMA.Mr Yue was appointed to hispresent position in June 2001.

CHIEF EXECUTIVE OFFICER(HONG KONG MORTGAGECORPORATION)

Peter Pang, JP

Peter Pang has been the ChiefExecutive Officer of the Hong KongMortgage Corporation sinceDecember 1997. Mr Pang joined theHKMA as Executive Director(Banking Policy) in 1994 and wasappointed as Executive Director(Monetary Policy and Markets) in1996. He started his civil servicecareer as an Administrative Officerin 1979 and served as AssistantDirector General of Trade andAssistant Commissioner of Bankingbefore joining the HKMA.

23ANNUAL REPORT 2003HONG KONG MONETARY AUTHORITY

HKMA ORGANISATION CHARTDecember 2003

Banking Development Division ARaymond Chan

Banking DevelopmentDepartmentExecutive DirectorRaymond Li

Deputy ChiefExecutiveWilliam Ryback

Banking Development Division BDanny LeungBanking Development Division CS P Li

Banking Policy Division ARita YeungBanking Policy Division BMichelle Quek

Banking Supervision Division IArthur YuenBanking Supervision Division IINelson ManBanking Supervision Division IIIFrederic LauBanking Supervision Division IVRose Luk

Support Services DivisionLydia Chan

Deputy General CounselMeena DatwaniDeputy General CounselFeliciana CheungDeputy General CounselKaren Kemp

Internal Audit DivisionPont Chiu

External Division (1)Francis LauExternal Division (2)Brenda TaoLondon OfficePriscilla ChiuNew York OfficeFrancis Chu

Market Systems DivisionEsmond LeeMonetary Operations DivisionJosie Wong

Economic Research DivisionPeng WenshengMarket Research DivisionGrace Lau

Direct Investment DivisionKen ChengExternal Managers DivisionMartin MatsuiRisk Management & Compliance DivisionClement Ho

Human Resources DivisionJennie WongFinance and Administration DivisionThomas YipInformation Technology DivisionY W TanCorporate Development DivisionChristopher Munn

Banking PolicyDepartmentExecutive DirectorSimon Topping

Banking SupervisionDepartmentExecutive DirectorY K Choi

Office of the GeneralCounselGeneral CounselStefan Gannon

ResearchDepartmentExecutive DirectorStefan Gerlach

Reserves ManagementDepartmentExecutive DirectorAmy Yip

Corporate ServicesDepartmentExecutive DirectorEddie Yue

External DepartmentExecutive DirectorJulia Leung

Monetary Management & Infrastructure Department Executive DirectorJames H Lau Jr

Deputy ChiefExecutiveNorman Chan

Chief ExecutiveJoseph Yam

The current organisation chart of the HKMA may be found on the HKMA website.

> About the HKMA > The HKMA > Organisation Chartwww

The Hong Kong Monetary Authority marked its

10th anniversary on 1 April 2003. The decade

between 1993 and 2003 was a period of political

transition, culminating in Hong Kong’s

establishment as a Special Administrative

Region of the People’s Republic of China on

1 July 1997. This was also a decade of economic

change and stress. Hong Kong’s economy

became more closely integrated with that of

the Mainland of China. Following the Asian

financial crisis in 1997, Hong Kong experienced

a period of prolonged economic difficulty.

The HKMA was formed with the aim of placing

under one authority the official responsibilities

for maintaining monetary and financial stability

and for developing an efficient and robust

financial infrastructure. The decision to

establish the HKMA in 1993 took into account

the growing importance of Hong Kong as an

international financial centre, the need to

ensure monetary stability during a period of

political and economic transition, and the

increasing risks posed by the globalisation

of finance.

• to maintain currency stability,

within the framework of the Linked

Exchange Rate system, through sound

management of the Exchange Fund,

monetary policy operations and other

means deemed necessary

• to promote the safety and stability

of the banking system through

the regulation of banking business

and the business of taking deposits,

and the supervision of authorized

institutions

• to enhance the efficiency, integrity and

development of the financial system,

particularly payment and settlement

arrangements.

THE HKMA’S POLICY OBJECTIVES

THE HKMA :THE FIRST 10 YEARS

12

10

8

6

4

2

0

-2

-4

-6

9

8

7

6

5

4

3

2

1

0

a

b

a

b

CPI inflation(Left-hand scale)

a Unemployment rate(Right-hand scale)

b

Source: Census and Statistics Department.

1993 199919981997199619951994 20012000 20032002

(% yoy) (%)

Real GDP growth (Left-hand scale)

ECONOMIC DEVELOPMENT

25ANNUAL REPORT 2003HONG KONG MONETARY AUTHORITY

Hong Kong’s economy developed between 1993and 2003. Over the decade

• real gross domestic product grew by anaverage rate of 3.3% per year, while nominalgross domestic product increased fromUS$118 billion to US$159 billion

• per capita gross national product rose fromHK$157,000 to HK$187,000

• the workforce expanded from 2.9 millionto 3.5 million

• real private consumption increased by one-fifth,recording an average annual increase of 1.9%

• real exports of goods and services almostdoubled, increasing by an average of 6.6% a year

• broad money, in terms of Hong Kong dollarM3, grew by an average of 8.5% a year, fromHK$939 billion to HK$2,123 billion

• the share of the value-added of the servicesector in gross domestic product rose from81% to 88% between 1993 and 2002.

These positive figures must, however, be setagainst indicators that reflect the difficulties ofthe second half of the decade:

• the unemployment rate rose from 2.4% inJanuary 1998 to 7.3% in December 2003

• the Composite Consumer Price Indexdeclined by about 16% from its peak inMay 1998

• residential property prices declined by abouttwo-thirds from their peak in October 1997.

The charts on this page illustrate the stressesand volatilities during these years.

Residential property pricea Hang Seng Indexb

Source: Rating and Valuation Department and Reuters.

350

300

250

200

150

100

50

0

ab

a

b

1993 199919981997199619951994 20012000 20032002

(Jan 93=100)

ASSET PRICES

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 Compoundedannual

investmentreturn

(1994-2003)

Compoundedannual

Hong KongCPI-A

(1994-2003#)

14

12

10

8

6

4

2

0

* Investment return computed in accordance with AIMR Global Investment Performance Standards.# Hong Kong CPI-A at end-November 2003.

2.4%

10.8%

5.1%

6.1%

12.1%

10.8%

4.8%

0.7%

5.1%

10.2%

6.7%

1.3%

INVESTMENT RETURN* OF THE EXCHANGE FUND

(%)

Economic distress and financial crisis placed

strains and burdens on the whole community of

Hong Kong. Extreme conditions and speculative

attacks presented challenges that tested the

HKMA’s ability to achieve its aims and which,

in retrospect, amply justified the decision to

establish the HKMA in 1993.

During its first decade the HKMA fully delivered

on its policy objectives and was able to promote

development in the financial sector and in Hong

Kong’s financial infrastructure. In the process,

the HKMA became more transparent in the

information it makes available to the markets

and in its accountability to the community.

Currency stability

• the market exchange rate of the Hong Kongdollar stayed close to the official LinkedExchange Rate of HK$7.80 to one US dollarthroughout the decade

• following the Asian financial crisis a series ofreforms and refinements were made to theCurrency Board system to ensure smoothfunctioning in periods of stress.

Exchange Fund

• between January 1994 and December 2003the Exchange Fund achieved an annualcompounded rate of return of 6.7%, whichwas consistently higher than the investmentbenchmark and the Consumer Price Index

• the Accumulated Surplus of the ExchangeFund increased from about HK$127.5 billionat the end of 1993 to over HK$380 billion atthe end of 2003.

26 THE HKMA: THE FIRST 10 YEARS

27ANNUAL REPORT 2003HONG KONG MONETARY AUTHORITY

Banking stability

• the total assets of the banking sector grew by7.3% between 1993 and 2003

• the total capital adequacy ratio of HongKong’s banking sector remained above 15%throughout the decade

• the supervisory framework for the bankingsector was brought into line with internationalstandards, and reforms were made toincrease competitiveness while maintainingsafety and stability.

Financial infrastructure

• real time gross settlement was introducedfor the Hong Kong dollar in 1996, for theUS dollar in 2000 and for the euro in 2003

• Exchange Fund paper was further developedto facilitate liquidity management and thegrowth of the debt market

• linkages for clearing and settling securitieswere established with five jurisdictionsoutside of Hong Kong

• Hong Kong dollar and US dollar clearing andsettlement arrangements were extended toGuangdong Province.

International financial centre

• the HKMA became a member of the Bank forInternational Settlements in 1996

• Hong Kong hosted the World Bank/IMFAnnual Meetings in 1997

• Hong Kong played a prominent role inregional and international initiatives forpromoting financial stability and developingthe regional and domestic bond markets

• approval was given in 2003 for banks in HongKong to conduct personal renminbi business.

HONG KONG INTERBANKCLEARING LIMITED

1993 1994 1995

MAJOR EVENTS 1993–2003

July 1993Hong Kong becomes the firstcity in the world to have acompletely digital telephonenetwork.

May 1994The Bank of China issues itsfirst Hong Kong banknotes.

June 1994The Government announces apackage of measures to dampenproperty speculation.

August 1994The Hang Seng China EnterprisesIndex is launched to serve asan indicator of the overallperformance of Hong Kong-listed,state owned enterprises of thePeople’s Republic of China.

September 1994The first issue of five-yearExchange Fund Notes is launched.The issue helps extend thebenchmark yield curve for HongKong dollar debt to the fiveyear area.

October 1994The interest rate cap on timedeposits is lifted in phases. Thismarks the beginning of a relaxationof Interest Rate Rules in Hong Kong.

November 1994Hong Kong issues itsfirst bimetallic coin –the bauhinia $10 coin.

January 1995In the aftermath of the Mexican pesocrisis, the Hong Kong dollar comesunder selling pressure along withother Asian currencies.

May 1995Hong Kong InterbankClearing Limited isestablished to provideinterbank clearingfunctions in Hong Kong.

April 1993The Hong Kong Monetary Authorityis established with responsibilityfor monetary and banking stability,reserves management, andfinancial infrastructure.

May 1993The Government startsto replace the Queen’sHead coins with the newbauhinia design.

July 1993The Government announces thesale of Overseas Trust Bank forHK$4,457 million. The sale of thebank, taken over in June 1985,marks the end of the Government’sefforts to rescue banks in the 1980s.

June 1995The HKMA becomes the licensing authority ofthree types of authorized institutions,following the enactment of the Banking(Amendment) Ordinance 1995.

July 1995The Companies Ordinance is amended so thatdepositors are entitled to receive prioritypayment in the liquidation of banks.

November 1995The Government decides to publish the size ofHong Kong’s foreign exchange reserves (i.e.foreign currency assets of the Exchange Fund)every quarter instead of every six months.

November 1995The first issue of seven-year Exchange FundNotes is launched.

1,000

800

600

400

200

0

Source: Datastream.12-month forward points

January 1995 February 1995

(pips)

Hong Kong dollar forward exchange rate

29ANNUAL REPORT 2003HONG KONG MONETARY AUTHORITY

1996 1997

January 1996The Exchange Fund acquiresthe De La Rue banknoteprinting plant in Tai Po, whichis renamed “Hong Kong NotePrinting Limited”.

July 1997The assets of the Land Fund arehanded over to Hong Kong SARGovernment with a net value ofHK$197 billion. From July 1997 toOctober 1998 these assets aremanaged by the HKMA as a separatefund within the fiscal reserves. On1 November 1998 the assets of theLand Fund are merged with theExchange Fund and managed as partof the investment portfolio of theExchange Fund.

March 1997The Hong Kong Mortgage Corporation isestablished. It will buy mortgage loans for itsown portfolio and issue mortgage-backedsecurities.

September 1997World Bank/IMF Annual Meetings areheld in Hong Kong. Central bank andfinance ministry officials from some180 countries attend the meetings.

July 1997Hong Kong becomes aSpecial AdministrativeRegion of the People’sRepublic of China.

September 1996The HKMA is invited to join theBank for InternationalSettlements, the Swiss-basedforum promoting co-operationamong central banks.

October 1996The first issue of ten-yearExchange Fund Notesis launched.

December 1996Real Time Gross Settlementis launched in Hong Kong,enabling interbank paymentsto be settled real time.

September 1997The Octopus card appears in HongKong. This contact-free stored valuecard is used for transport fares andretail purchases. By 2003, there arearound nine million Octopus cards incirculation in Hong Kong (or 1.3 forevery resident) and over sevenmillion daily Octopus transactions.

1997 – 1998Financial crisis in several Asian countries includingSouth Korea, Indonesia and Thailand.

July 1997The Code of BankingPractice is issuedto improve thetransparency andquality of bankingservices inHong Kong.

1997 – 2003Economic Downturn in Hong Kong. After the Asian financial crisis Hong Kongexperiences a period of prolonged economic difficulty, relieved only by a briefrecovery in 2000. A series of external shocks, coupled with sharp declines inasset prices, result in high unemployment, deflation and fiscal deficits.

1998 1999 2000

30 MAJOR EVENTS 1993-2003

July 1998The Bank for International Settlementsopens its representative office for Asia andthe Pacific in Hong Kong.

August 1998Using HK$118 billion out of the ExchangeFund, the Hong Kong SAR Governmentlaunches a stock market operation tofrustrate manipulation of the money andstock markets.

September 1998The HKMA introduces seven technicalmeasures to strengthen the CurrencyBoard arrangements.

July 1998Hong Kong International Airport opensat Chek Lap Kok.

January 1999The foreign currency assetsand the balance sheet data ofthe Exchange Fund arepublished monthly, in linewith the standard set by theInternational Monetary Fund.

August 1999Exchange Fund Notescommence listing on theHong Kong Stock Exchange.

August 1999The Hong KongInstitute forMonetary Researchis established.

November 1999The Tracker Fund of HongKong is established as avehicle for graduallydisposing of the majority ofthe stocks acquired by theExchange Fund in the 1998market operation.

August 2000Hong Kong processes itsfirst transaction throughthe new US dollarclearing system.

October 2000Hong Kong is selectedas President for 2001-2002 of the FinancialAction Task Force onMoney Laundering, aninternational body.

December 2000Hong Kong’s MandatoryProvident Fund Systemcomes into full operationafter years ofpreparation.

October 1998Exchange Fund Investment Limited isestablished to manage the portfolio ofHang Seng Index constituent stocksacquired by the Exchange Fund in themarket operation of August.

31ANNUAL REPORT 2003HONG KONG MONETARY AUTHORITY

2001 2002 2003

January 2001The InternationalMonetary Fund opens asub-office in Hong Kong.

April 2001The Governmentapproves in principle theproposal to introduce adeposit protectionscheme in Hong Kong.

July 2001Interest Rate Rules arecompletely deregulated.Banks are free to setinterest rates for alltypes of deposits.

November 2001All restrictions on thenumber of branches offoreign banks are lifted.

December 2001China enters the WorldTrade Organisation.

November 2003Following approval from the State Council, the People’sBank of China agrees to provide clearing arrangements forbanks in Hong Kong to conduct personal renminbibusiness on a trial basis. The scope of the business to beconducted includes deposit-taking, exchange, remittancesand debit and credit cards.

December 2003The three note-issuingbanks issue new $100and $500 notes withadditional securityfeatures.

June 2003The Mainland and Hong Kong signthe Closer Economic PartnershipArrangement (CEPA).

November 2003The HKMA moves its offices topermanent premises at TwoInternational Finance Centre.

March to June 2003Outbreak of Severe AcuteRespiratory Syndrome(SARS). 1,755 people inHong Kong are infectedand 299 people die.

June 2003Exchange of letters betweenthe Financial Secretary andthe Monetary Authority onfunctions and responsibilitiesin monetary and financialaffairs.

March 2002The Securities andFutures Ordinance ispassed by the LegislativeCouncil. The Ordinanceconsolidates andmodernises 10 existingordinances into a singlepiece of legislation togovern financial andinvestment products,regulate the securitiesand futures markets, andprotect investors.

May 2002The Governmentendorses the HKMA’sproposals to relax certainmarket entry criteria forthe banking sector.

September 2002The Government issuesnew $10 currency notes.

April 2003Hong Kong processes its firsttransaction through its new euroclearing system.

More than 2,000 swimmers brave chilly waters to takepart in the 27th International New Year WinterSwimming Championships held on the south side ofHong Kong Island to welcome the New Year in 2003.

33ANNUAL REPORT 2003HONG KONG MONETARY AUTHORITY

TABLE 1 Contributions to GDP growth by components (%)

20021 20032

Q1 Q2 Q3 Q4 Overall Q1 Q2 Q3 Q4 Overall

Private Consumption Expenditure 0.0 -1.5 -0.5 -0.7 -0.7 -1.1 -2.1 0.9 2.0 0.0

Government Consumption Expenditure 0.2 0.3 0.3 0.1 0.2 0.1 0.0 0.1 0.5 0.2

Gross Domestic Fixed Capital Formation -3.4 0.0 -1.2 -0.2 -1.2 0.9 -1.5 -0.1 0.6 0.0

Change in Inventories -1.2 -0.1 1.3 2.3 0.6 1.8 0.1 -1.0 1.0 0.5

Net Exports of Goods 2.2 -0.5 0.3 -0.5 0.3 -1.0 3.3 2.1 -1.9 0.6

Net Exports of Services 1.6 2.8 3.3 4.2 3.0 3.9 -0.3 2.1 2.8 2.1

GDP -0.6 0.8 3.4 5.1 2.3 4.5 -0.5 4.0 5.0 3.3

1 Revised figures2 Preliminary figures

ECONOMIC AND BANKINGENVIRONMENT

After the severe disruption by the outbreak of SARS (severe acuterespiratory syndrome) in the second quarter of 2003, Hong Kong’seconomy rebounded sharply in the second half of the year. The overallasset quality of the banking sector improved. With improved economicconditions in the second half, the banking sector ended the year witha modest growth in profitability.

THE ECONOMY IN REVIEWOverview

Hong Kong experienced very difficult economic

conditions in the first half of 2003 reflecting, in

particular, the effects of the outbreak of SARS in

the second quarter. Growth returned in the second

half of the year and Hong Kong emerged as a

strong-performing economy in the region. Real

GDP rose by 3.3% in 2003, compared with 2.3% in

2002. Exports of goods and trade-related services

were largely unaffected by the SARS outbreak.

Exports of tourism-related services showed a

sharp turnaround in the second half of 2003,

boosted by a relaxation of travel restrictions on

Mainland visitors to Hong Kong. Private

consumption also picked up markedly as consumer

confidence recovered. Investment spending on

machinery, equipment and computers started to

recover in the second half, but spending on

building and construction remained weak (Table 1).

Monetary conditions eased further during the year,

with declines in both Hong Kong dollar interest

rates and the real effective exchange rate. Broad

money growth picked up moderately alongside the

recovery in economic activity. Narrow money

growth was strong, owing to low interest rates and

an increase in transaction demand resulting,

in part, from robust stock market activity.

34 ECONOMIC AND BANKING ENVIRONMENT

1996 1997 1998 1999 2000 2001 2002 2003

a

c

b

Private consumptiona Public spendingcPrivate investmentb

ac

b

30

20

10

0

-10

-20

-30

CHART 1 Domestic demand (percentage change over a year ago in real terms)

Reviving domestic demand

Private consumption was weak in the early part of

2003 but recovered strongly in the second half of

the year. Consumer confidence rose, as a result of

improvements in the global economy and a decline

in unemployment and more stable asset markets at

home. One important source of optimism was the

policy initiatives designed to facilitate closer

economic integration between Hong Kong and the

Mainland. These include the Closer Economic

Partnership Arrangement (CEPA), the relaxation of

travel restrictions on Mainland visitors to Hong Kong,

and approval for Hong Kong banks to undertake

personal renminbi banking business on a trial basis.

Spending on durable goods and services registered

particularly strong growth in the second half. For the

year as a whole, private consumption expenditure

was little changed in 2003, after a decline of 1.2% in

2002 (Chart 1).

Despite the improvement in the economy in the

second half of 2003, investment remained weak.

Private investment continued to decline, by 0.3%,

largely owing to lower expenditure on building and

construction, although at a more moderate rate

than in the preceding year. Investment in

machinery, equipment and computer software

by the private sector recorded a rise of 6.9%.

Public investment rose slightly as a number of new

infrastructure projects came on stream in the

second half of the year (Chart 1).

Buoyant external trade

Exports of goods recorded double-digit growth

rates throughout the year, supported by robust

growth of Mainland exports, and improved

competitiveness as a result of the depreciation of

the US dollar (to which the Hong Kong dollar is

linked). The rush by Chinese exporters to ship

products ahead of the pre-announced reduction in

VAT rebates, due to be implemented on the

Mainland in January 2004, also contributed to

particularly strong growth of merchandise exports

in the fourth quarter of the year. Among the major

markets, exports to East Asia and to the European

Union grew strongly, while export performance to

35ANNUAL REPORT 2003HONG KONG MONETARY AUTHORITY

TABLE 2 Exports to major trading partners1

Share 2002 2003

% Q1 Q2 Q3 Q4 Overall Q1 Q2 Q3 Q4 Overall

Mainland China 43 3 8 13 25 12 27 21 16 21 21

United States 19 -15 1 6 9 1 7 -5 -7 -3 -3

European Union 13 -15 -7 1 7 -3 16 17 8 8 12

Japan 5 -14 -10 -2 7 -4 14 17 11 9 12

ASEAN52 + Korea 7 4 10 20 22 14 9 11 7 10 9

Taiwan 2 -10 -7 11 -2 -2 25 17 15 32 22

Others 10 -7 3 6 13 4 10 6 -2 6 5

Total 100 -6 3 8 16 5 18 12 7 11 12

1 Figures are percentage changes over a year ago except for major export markets’ shares in Hong Kong’s total exports.2 ASEAN5 includes the Philippines, Malaysia, Indonesia, Singapore and Thailand.

1996 1997 1998 1999 2000 2001 2002 2003

ab

b Export volume (Left-hand scale)

ab

Import volume (Left-hand scale)a

30

20

10

0

-10

-20

Percentage change over a year ago30

20

10

0

-10

-20

In % of GDP

Trade balance (Right-hand scale)

CHART 2 External merchandise trade

the United States was somewhat weak (Table 2).

Along with a buoyant re-export trade, imports of

goods rose by 13.1% in 2003 compared with 2002.

The merchandise trade deficit widened to

$45.0 billion in 2003, from $39.4 billion in 2002

(Chart 2), reflecting faster growth of goods exports

relative to imports.

Trade-related exports of services also grew

strongly, partly owing to vibrant merchandise

exports. By contrast, tourism-related earnings,

affected by the SARS outbreak, fell sharply in the

second quarter. Earnings bounced back very

sharply in the second half of the year helped by the

relaxation of travel restrictions on Mainland

visitors, making the tourism industry an important

driver of growth in the economy. The recovery in

imports of services was more modest. The overall

trade surplus, goods and services combined,

amounted to $116.1 billion, or 9.4% of GDP.

36 ECONOMIC AND BANKING ENVIRONMENT

1996 1997 1998 1999 2000 2001 2002 2003

a

c

b

Labour force (Right-hand scale)a Unemployment rate (Left-hand scale)cTotal employment (Right-hand scale)b

a

c

b

10

8

6

4

2

0

-2

-4

In % of labour force10

8

6

4

2

0

-2

-4

Percentage change over a year ago

CHART 3 Labour market

nominal index of payroll per person engaged was

2.1% lower in the first three quarters of the year

compared with the same period a year earlier, while

median household income fell by 6.1% in 2003.

Recovery in asset markets

The Hang Seng Index started the year on a weak

note in line with developments in other major

stock markets, which were affected by the

uncertainties surrounding the war in Iraq. The

Hong Kong stock market was also affected by

SARS, and fell sharply to a low of around 8,400 in

late April even as US and European markets

rallied. Market sentiment started to improve in

May, as SARS was progressively brought under

control. Investor confidence was also boosted by

the series of measures designed to facilitate

economic integration with the Mainland. These

measures are expected to help the structural

adjustment of the Hong Kong economy and develop

its competitiveness. They are thought to have

increased investors’ appetite for domestic assets,

especially for stocks likely to benefit directly. As a

result, the Hang Seng Index rebounded strongly to

close the year at 12,576, or 35% higher than at the

end of 2002.

Easing deflationary pressures

Deflationary pressures intensified in the first half of

2003, but eased markedly towards the year’s end.

The Composite Consumer Price Index (CCPI)

recorded the sharpest falls during May and July,

reflecting the impact of SARS. Since then, prices

appeared to stabilise, as economic growth

recovered, with the seasonally adjusted CCPI rising

slightly month on month since August. For 2003 as

a whole, the CCPI fell by 2.6% compared with 2002.

Import prices declined by 0.4%, less than the

3.9% fall in 2002, owing to a weaker US dollar and

firmer world commodity prices.

Improving labour market conditions

Labour market conditions lagged behind the

economic recovery but improved in the last quarter

of 2003 after a substantial deterioration in the first

half of the year. The unemployment rate reached a

record high of 8.7% in the three months to July,

partly owing to the impact of the outbreak of SARS,

but it subsequently fell to 7.3% in the three months

to December as growth recovered (Chart 3). The

improvement was broadly based, but consumption

and tourism-related sectors did particularly well.

Labour income, however, has yet to recover. The

37ANNUAL REPORT 2003HONG KONG MONETARY AUTHORITY

140,000

120,000

100,000

80,000

60,000

40,000

20,000

01999 20012000 20032002

Amount of issue

$ mn

118,195

99,265107,545

118,475

134,215

CHART 4 Banknotes in circulation at end of year

CHART 5 Distribution of banknotes in circulation at the end of 2003

(By value) (By pieces)

$10 3.1%$20 4.2%$50 2.4%$100 12.2%

$1,000 51.3%

$500 26.8%

$10 38.4%

$20 26.7%

$1,000 6.5%

$500 6.8%

$100 15.5%

$50 6.1%

Recovery of narrow and broadmoney growth

Monetary aggregates increased in 2003. Hong

Kong dollar narrow money (seasonally adjusted)

rose sharply during the year, by 35.8%, while broad

money growth recovered in mid-2003 and grew by

5.9% in the year to December 2003. The strong

growth of narrow money can be attributed to lower

interest rates and the significant rebound in stock

market activity during the second half of the year.

The growth of broad money reflected the revival in

economic activity more generally.

Notes and coins

At the end of 2003 the total value of banknotes in

circulation was $134,215 million, an increase of

13.3% on a year earlier (Charts 4, 5, 6). The total

value of Government-issued notes and coins in

The property market was also hit hard by SARS,

but the economic recovery, new supply restraint

measures introduced in November 2002, and an

associated rise in consumer optimism, coupled

with low funding costs, led to a revival of the

market in the last few months of 2003. The number

of transactions increased by 1.6% during the year.

Residential property prices rose by 10.3% between

their trough in July and the end of year, although

they were still lower in 2003 as a whole compared

with 2002.

MONETARY CONDITIONS

Monetary conditions continued to ease in 2003

as a result of further declines in interest rates

and in the effective exchange value of the Hong

Kong dollar. Hong Kong dollar interest rates

declined to almost zero per cent in the fourth