Home Away From Home: Economic Relevance and Local Investors

76

Electronic copy available at: http://ssrn.com/abstract=1711653 Home Away From Home: Economic Relevance and Local Investors * Gennaro Bernile, University of Miami Alok Kumar, University of Miami Johan Sulaeman, Southern Methodist University March 25, 2012 Abstract – We identify states that are economically relevant for a firm through textual analysis of the firm’s annual financial (10-K) reports and show that institutional investors overweight firms with strong local economic presence and generate superior returns from those investments. This evidence of local over-weighting and superior local performance in economically relevant regions are stronger than those around corporate headquarters, even when those regions are far from the headquarters location. Our results are stronger among more sophisticated institutions and for firms that have speculative features or are harder-to-value. Overall, we demonstrate that economic relevance rather than physical presence has a stronger impact on institutional preferences for local stocks and their local informational advantage. * Please address all correspondence to Alok Kumar, Department of Finance, School of Busi- ness Administration, 514 Jenkins Building, University of Miami, Coral Gables, FL 33124; Phone: 305-284-1882; email: [email protected]. Gennaro Bernile can be reached at 305- 284-6690 or [email protected]. Johan Sulaeman can be reached at 214-768-8284 or [email protected]. We thank an anonymous referee, Brad Barber, Josh Coval, Doug Emery, Robin Greenwood, Michael Halling, Zoran Ivkovich, George Korniotis, Kelvin Law, Toby Moskowitz, Jeremy Page, Bill Schwert (the editor), Sophie Shive, Kumar Venkataraman, Scott Yonker, and seminar participants at the 2011 FEA Meetings, 2012 AFA Meetings, Southern Methodist University and University of Miami for helpful comments and valuable suggestions. We are responsible for all remaining errors and omissions.

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of Home Away From Home: Economic Relevance and Local Investors

Electronic copy available at: http://ssrn.com/abstract=1711653

Home Away From Home:

Economic Relevance and Local Investors∗

Gennaro Bernile, University of Miami

Alok Kumar, University of Miami

Johan Sulaeman, Southern Methodist University

March 25, 2012

Abstract – We identify states that are economically relevant for a firm through textual analysis

of the firm’s annual financial (10-K) reports and show that institutional investors overweight

firms with strong local economic presence and generate superior returns from those investments.

This evidence of local over-weighting and superior local performance in economically relevant

regions are stronger than those around corporate headquarters, even when those regions are far

from the headquarters location. Our results are stronger among more sophisticated institutions

and for firms that have speculative features or are harder-to-value. Overall, we demonstrate

that economic relevance rather than physical presence has a stronger impact on institutional

preferences for local stocks and their local informational advantage.

∗Please address all correspondence to Alok Kumar, Department of Finance, School of Busi-ness Administration, 514 Jenkins Building, University of Miami, Coral Gables, FL 33124;Phone: 305-284-1882; email: [email protected]. Gennaro Bernile can be reached at 305-284-6690 or [email protected]. Johan Sulaeman can be reached at 214-768-8284 [email protected]. We thank an anonymous referee, Brad Barber, Josh Coval, DougEmery, Robin Greenwood, Michael Halling, Zoran Ivkovich, George Korniotis, Kelvin Law, TobyMoskowitz, Jeremy Page, Bill Schwert (the editor), Sophie Shive, Kumar Venkataraman, ScottYonker, and seminar participants at the 2011 FEA Meetings, 2012 AFA Meetings, SouthernMethodist University and University of Miami for helpful comments and valuable suggestions.We are responsible for all remaining errors and omissions.

Electronic copy available at: http://ssrn.com/abstract=1711653

Home Away From Home:Economic Relevance and Local Investors

Abstract – We identify states that are economically relevant for a firm through textual analysis

of the firm’s annual financial (10-K) reports and show that institutional investors overweight

firms with strong local economic presence and generate superior returns from those investments.

This evidence of local over-weighting and superior local performance in economically relevant

regions are stronger than those around corporate headquarters, even when those regions are far

from the headquarters location. Our results are stronger among more sophisticated institutions

and for firms that have speculative features or are harder-to-value. Overall, we demonstrate

that economic relevance rather than physical presence has a stronger impact on institutional

preferences for local stocks and their local informational advantage.

Electronic copy available at: http://ssrn.com/abstract=1711653

I. Introduction

The recent local bias literature has shown that institutional investors around corporate head-

quarters overweight local firms and earn higher returns from those investments.1 Most of these

studies use corporate headquarters to identify firm location.2 However, although the typical

U.S. publicly traded firm has physical presence in only a few locations, it has economic presence

in nine U.S. states (median is six) and often in several international locations. Further, the

economically relevant regions of a typical firm are often located far away from its corporate

headquarters. On average, the economically relevant states are about 1,000 miles away from the

headquarters location.3

The finance literature recognizes the importance of economic location of a firm. However,

for simplicity, the recent local bias literature uses the headquarters location to proxy for firm

location.4 In this paper, we use a firm’s physical location of corporate headquarters and its

economic presence in other U.S. regions to define its geographical location. Using this multi-

dimensional firm location measure, we study the investment behavior of institutional investors

during the 1996 to 2008 period.5 We first examine whether, compared to local preferences

of institutions around corporate headquarters, institutional investors in economically relevant

regions exhibit a stronger preference for firms with local economic presence.

Next, we identify which investor, firm, and local factors influence the overweighting of local

stocks. The main objective of this analysis is to investigate whether there are systematic differ-

ences in the local clientele characteristics of investors in headquarters and economically relevant

states. We also want to examine whether the local ownership levels are higher for stocks with

certain characteristics.

Last, we investigate whether institutional investors in economically relevant regions are able

to exploit local information more effectively than institutions around corporate headquarters,

1We do not use the term “local bias” to strictly imply that the local stock preference is “irrational”. The“bias” towards local investments could be induced by a familiarity bias or may arise from informational reasons.

2For example, see Coval and Moskowitz (1999, 2001), Huberman (2001), Ivkovic and Weisbenner (2005),Loughran and Schultz (2005), Pirinsky and Wang (2006), Hong, Kubik, and Stein (2008), Baik, Kang, and Kim(2010), and Seasholes and Zhu (2010).

3These firm location statistics are based on our new firm location data described later. The mean of 1,000miles is obtained after excluding international locations.

4One exception is the study of Swedish investors by Massa and Simonov (2006). In addition to distance tocorporate headquarters, they use the distance to the closest branch or subsidiary to define “local”. However, theirproximity measures based on headquarters and subsidiary locations are strongly correlated, while our measuresof physical and economic proximity are distinct.

5Although our focus is on the investment behavior of institutional investors, in the Internet Appendix, weuse a shorter sample period covering the 1993 to 1996 period and compare the local ownership patterns ofinstitutional and retail investors.

1

especially if those stocks have speculative features or are harder-to-value.

There are several reasons why the local bias mechanisms around firm headquarters and in

economically relevant regions could differ. If a firm’s headquarters location is the primary source

of value-relevant information, investors around corporate headquarters may earn superior returns

from their local investments. And in contrast, investors away from corporate headquarters may

hold stocks that have local economic presence but would not necessarily earn superior returns

from those local investments. In this scenario, their local stock preference would reflect a

familiarity bias.

However, it is also likely that useful “soft” information about future profitability and per-

formance of a firm is geographically distributed and resides away from firm headquarters. In a

recent study, Giroud (2010) demonstrates that information asymmetry between firm headquar-

ters and plant locations decreases when airline routes are introduced between headquarters and

plant locations. If this information asymmetry is economically significant, investors around these

non-headquarters locations may have better information and may acquire the information faster

than investors around firm headquarters. Consequently, investors away from firm headquarters

may exhibit a preference for stocks that have local economic presence and those investors on av-

erage may have superior value-relevant information about local firms than investors around firm

headquarters. In this scenario, investors in economically relevant states would overweight local

stocks due to an informational advantage and earn higher returns from those local investments.

For example, the Boeing Company is headquartered in Chicago but most of its operations

are around Seattle. Due to their potentially greater ability to observe manufacturing and oper-

ations, it is likely that investors in the state of Washington have better information about the

overall financial health of Boeing than investors in Illinois. Similarly, Whole Foods Market is

headquartered in Austin, but investors in other states in which Whole Foods Market has large

number of stores and significant economic presence (e.g., Massachusetts, Florida, Colorado) may

have the same or even greater degree of awareness about Whole Foods Market than investors

in Texas. Another example is Xerox Corporation, which is perceived by many as a Rochester

company due to its major operations there but the firm is headquartered in Stamford, Con-

necticut. It is possible that investors around the operations of Xerox in Rochester, New York

possess better short-term information about Xerox than investors in Connecticut.

In addition to differences in information environments, the investor clientele characteristics

could differ between firm headquarters and other regions in which the firm has an economic

presence. The local investor clientele at headquarters location may be relatively less sophisti-

cated than local investors in economically relevant regions. Specifically, being aware of a firm

2

with local economic presence may require a higher level of sophistication than identifying a firm

that merely has a physical local presence.6 Consequently, a more sophisticated clientele may

emerge in non-headquarters locations where firms have economic rather than physical presence.

Those local investors away from headquarters locations may be able to earn higher risk-adjusted

returns from their local investments.

In contrast, investors around headquarters may exhibit greater awareness about a firm merely

because that firm has a local physical presence. Those investors need not possess superior

information about local firms. In this scenario, short-term demand shifts of local investors

would contain less information about future returns of local firms.

To test our conjectures, we identify U.S. states that are economically relevant for a firm

through a textual analysis of its annual financial (10-K) reports. This economic relevance

measure of a U.S. state for a given firm is based on the citation share of the state in the firm’s

annual financial reports. The citation share of a firm-state pair is defined as the number of times

the U.S. state is cited in the relevant sections of the firm’s annual financial statement divided

by the total number of citations of all U.S. locations. Thus, a firm can be present in multiple

locations within the U.S. and we are also able to quantify the strength of a firm’s presence

in each of the states in the U.S. This multi-dimensional location measure allows us to better

identify the geographical regions in which value-relevant information about a firm is likely to be

produced.

According to the citation-based location measure, in many instances, a firm’s headquarters

state is not its most economically relevant region. We find that in about 37 percent of cases,

another state is at least as economically relevant as the headquarters state. And in 29 percent of

cases, there is at least one other state that is economically more relevant than the headquarters

state.7 The average citation share of the most economically-relevant state away from firm

headquarters is large (= 0.244), although it is lower than the average citation share of 0.383 for

the headquarters state. These citation share statistics indicate that many firms have significant

economic presence and visibility even in non-headquarters states, which could induce investors

in those states to overweight firms with local economic presence.

In our main empirical tests, we estimate the local ownership levels and local informational

advantage of institutional investors during the 1996 to 2008 sample period. We compare the

6This argument has limitations and does not apply to all types of firms. For example, firms with retail outletsmay be familiar even to investors located far away from corporate headquarters location.

7For example, Connecticut is never the most relevant state for Xerox Corporation even though it is head-quartered in Stamford, Connecticut. Similarly, Washington continues to be Boeing’s most economically relevantstate even after the relocation of its headquarters to Chicago.

3

local ownership and performance levels of investors around headquarters and those located in

economically relevant states. Similar to several previous local bias studies, we perform the

analysis at both the institution- and the firm-level.

Our results indicate that investors allocate disproportionately large fractions of their port-

folios to firms for which the investor’s state is economically relevant. For example, a typical

institution around corporate headquarters overweights local firms by 1.78%, while the mean

institutional local bias for economically relevant firms is 4.70%, which is 2.92% higher than the

mean local bias for locally headquartered firms. Similarly, the average excess local ownership

is 6.17 percent in non-headquarters states with high economic relevance, only 0.99 percent in

low economic relevance states, and significantly negative in states that are not mentioned in the

annual reports. The average excess local ownership in high economic relevance states remain

high even when the economically relevant state is far from the firm headquarters.

Even in headquarters states, the average excess local ownership is strongly dependent upon

the degree of economic relevance. The average excess local ownership is 14.58 percent in head-

quarters states with high economic relevance but only 3.02 percent in less economically relevant

headquarters states. And when the headquarters state is not economically relevant for a firm,

there is no local bias as institutions located within the state under-weight local stocks by an

average of 1.81%. Overall, the institution-level and firm-level local ownership estimates portray

a consistent picture and suggest that economic relevance affects local ownership levels more than

physical proximity.

To investigate whether there are differences in the underlying mechanisms that induce high

levels of local ownership around headquarters and in economically relevant states, we identify

the characteristics of regions in which local ownership levels are high. We also identify the stock

attributes that are associated with higher levels of local ownership. The goal of this analysis is

to examine whether institutional local bias is stronger in regions where local investors are more

sophisticated and local stocks have greater information asymmetry or are harder-to-value.

Our results indicate that local ownership levels are high in conservative Republican states as

well as regions with low population density, and these effects are more pronounced in headquar-

ters states. Further, the local ownership levels around headquarters are higher in states with

lower education levels, while the excess local ownership levels in economically relevant states

exhibit an opposite pattern. Examining the impact of firm attributes on local ownership levels,

we find that local investors exhibit a stronger propensity to overweight smaller and younger

firms, recent losers, value stocks, and firms that have higher volatility. Taken together, the lo-

cal ownership regression estimates indicate that the local institutional clientele in economically

4

relevant states is likely to be more sophisticated.

To examine whether sophisticated investors in economically relevant states are able to exploit

their potential local informational advantage more effectively, we compare the degree of infor-

mational advantage of investors around firm headquarters and economically relevant regions.

We find that, irrespective of the performance measure, institutions in economically relevant re-

gions outperform nonlocal investors and investors around corporate headquarters by 1-2% on

an annualized basis.

The results are similar when we perform firm-level tests to account for potential cross-

sectional dependence in institutional performance. When we measure the performance of local

ownership sorted portfolios, consistent with the recent evidence in Baik, Kang, and Kim (2010),

we find that firms with higher local ownership levels earn higher risk-adjusted returns and

the local ownership-performance relation is strong in headquarters states. However, when we

measure the performance of portfolios sorted on quarterly changes in local ownership levels, we

find that changes in local ownership levels of firms in economically relevant states have a greater

ability to predict the returns of local firms in the following quarter.

Even when changes in ownership levels in headquarters states are low or negative, increases

in ownership levels in economically relevant states are associated with higher local returns in

the next quarter. When the quarterly demand shifts are high in both headquarters states and

economically relevant states, their impact on next quarter returns is the strongest. These effects

are especially pronounced among the types of stocks that have strong local investor clienteles in

economically relevant states (i.e., low priced and high volatility firms, lottery-type stocks). The

annualized risk-adjusted performance differentials are economically significant and range from

two percent to about eight percent for smaller firms.

These empirical findings make several important contributions to the local bias literature. A

recurring criticism of local bias studies is that firm headquarters may not capture the location of a

firm. Our study overcomes this criticism. We use a multi-dimensional measure of geographical

location of a firm based on both economic and physical local presence. To our knowledge,

this is the first paper that uses a broader measure of firm location to quantify the local stock

preferences and informational advantage of institutional investors. In a related study, Garcıa

and Norli (2012) use citation shares to obtain geographic dispersion levels of firms and show

that more dispersed firms earn lower returns. But they do not study investors’ local bias around

headquarters and economically relevant regions, which is the main focus of our study.

We use the citation-based firm location measure to document the key result that institutional

investors need not be located near a firm’s headquarters to exhibit a preference for local stocks

5

and possess local informational advantage. The aggregate excess ownership levels of investors

that are local to firms but are located away from firm headquarters are more than the excess

ownership levels of investors in headquarters states. Our estimates of higher local ownership

levels compared to the estimates reported in previous local bias studies further highlights the

importance of local investors for asset pricing. In particular, our findings suggest that the impact

of local investors on the asset prices of local stocks may be considerably stronger than reported

in recent studies (e.g., Hong, Kubik, and Stein (2008), Korniotis and Kumar (2011)).

We also demonstrate that, compared to institutions around corporate headquarter, investors

in economically relevant states have better short-term information about local firms, especially

if those firms have speculative features or are harder-to-value. This evidence is consistent with

Giroud (2010) who finds that useful information about a firm may be located away from firm

headquarters.8 These performance results extend the recent evidence of superior local informa-

tion among a large sample of institutional investors reported in Baik, Kang, and Kim (2010).

Similar to their study, we find that local institutions have superior information about local firms.

However, we show that unlike institutions around corporate headquarters, institutions located

in regions where firms have economic presence possess superior information about local firms.

The rest of the paper is organized as follows. In the next section, we summarize the main

data sources and explain the citation-based measure of firm location. We present our main

empirical results in Sections III, IV, and V. We conclude in Section VI with a brief discussion.

The Appendix provides additional information about the construction of citation-based firm

location measure and reports additional results.

II. Data Sources and Summary Statistics

In this section, we summarize our main data sources. Table I provides a brief description of the

main variables used in the empirical analysis.

II.A. Citation-Based Firm Location Data

Our first main data source is the annual financial reports stored on the Electronic Data Gath-

ering, Analysis, and Retrieval system (EDGAR) of U.S. Securities and Exchange Commission

(SEC). All U.S.-based companies are required to file Form 10-K with the SEC. This is a stan-

dardized form with a fixed structure and a pre-determined number of sections. It contains

8We are not suggesting that firms intentionally choose to pick headquarters locations in regions with unso-phisticated investors. While the choice of the headquarters location is an important corporate decision, in thecurrent context it is more likely that a relatively less sophisticated investor clientele emerges around headquarterswhile more sophisticated clienteles develop in regions where firms have economic presence.

6

details about a firm’s organizational structure, executive compensation, competition, and regu-

latory issues. For our purposes, more importantly, the form contains information about a firm’s

physical assets, including factories, warehouses, and sales offices. In addition, the form contains

a comprehensive summary of a company’s performance and operations, including information

about changes in firm’s operations during a certain year.

We use a computer-based parsing method to count the number of times references to 50

U.S. states and Washington D.C. appear in annual 10-K filings stored on EDGAR.9 The sample

period is from 1996 to 2008. For each annual filing, we count the occurrence of geographic

locations in sections “Item 1: Business”, “Item 2: Properties”, “Item 6: Consolidated Financial

Data”, and “Item 7: Management’s Discussion and Analysis.” These citation counts provide a

measure of the geographic locations of a firm’s economic interests. This includes information

about a firm’s plant and store locations, office spaces, acquisition activities, and other means

through which a firm can have an economic presence in a state.

Specifically, we compute the citation share of each state in the firm’s annual financial reports.

The citation share of a firm-state pair is defined as the number of times a U.S. state is cited in

the relevant sections of the annual financial statement of a firm divided by the total number of

citations of all U.S. locations. Internet Appendix A provides a brief summary of the information

contained in these four sections of the annual financial reports, while Appendix B provides

excerpts from a few actual 10-K forms filed during the 1996 to 2008 sample period.

Table II provides the summary of the citation share estimates. We find that a typical U.S.

firm has economic presence in nine U.S. states (median is six).10 The average citation share

is 0.205 (median is 0.167) and, as expected, the headquarters states have a higher citation

share (mean = 0.383, median = 0.333). The average citation share of the most economically-

relevant state away from headquarters is also economically significant (= 0.244). These citation

share statistics suggest that many firms are likely to have economic presence and visibility

even in non-headquarters states. These economically relevant states are often located far from

its headquarters. Even though we exclude international locations, the states with economic

presence are on average about 1,000 miles away from the headquarters location.

Although the economic presence of a firm across the U.S. states can vary over time, it is

9Our parsing algorithm would miss instances where the 10-K report mentions the city but not the state. Wewould also be unable to capture cases in which the 10-K reports use state abbreviations. Manual inspection of afew randomly chosen 10-K reports indicates that both cases are rare. Further, there is no reason to believe thatcertain types of firms or firms located in certain states are more likely to abbreviate states or mention only citynames in their reports. Thus, the citation share estimates may be downward biased but the relative rankings offirms would not be affected systematic bias due to these exclusions.

10We present the histogram of this distribution in Figure A.1 of the Internet Appendix.

7

unlikely to change significantly from year-to-year. Consistent with this expectation, we find

that the citation share estimates are quite persistent. In about two-third of cases, the most

economically-relevant state in a certain year is one of the top three economically-relevant states

in each of the past three years. And in more than 90% of cases, the most economically-relevant

state in a certain year is one of the top three economically-relevant states at least once in the

past three years.

II.B. Other Data Sources

Our second main data set is the quarterly common stock holdings of 13(f) institutions compiled

by Thomson Reuters. The sample period is from 1996 to 2008. We identify the institutional

location (zip code) using the Nelson’s Directory of Investment Managers and by searching the

SEC documents and web sites of institutional managers.

In addition to these main data sources, we use several other standard data sets. We obtain

price, volume, return, and industry membership data from the Center for Research on Security

Prices (CRSP). The firm headquarters location data are from the CRSP-Compustat merged

(CCM) file. We obtain monthly time series of the market (RMRF), size (SMB), value (HML),

and momentum (UMD) factors from Kenneth French’s web site.11 We obtain the performance

benchmarks for computing characteristic-adjusted stock returns from Russell Wermers’ web

site.12 The quarterly data on state economic activity index are from Korniotis and Kumar

(2011). The index is defined as the equal weighted average of the standardized values of state

income growth, state housing collateral (Lustig and van Nieuwerburgh (2005, 2010)), and the

negative value of standardized relative state unemployment.

To match the citation-based firm location data with CRSP and Compustat, we use the

Central Index Key (CIK). All entities registered with the SEC are uniquely identified by CIK.

Specifically, we use the firm CIK and link file from the CRSP-Compustat Merged database

to match the annual citation-based location data with data on stock returns and various firm

characteristics.

We use state-level Presidential elections data to identify the political preferences of all U.S.

states.13 We obtain additional state-level demographic characteristics from the U.S. Census

Bureau. Specifically, we consider state population density and the state education level (the

proportion of state population above age 25 that has completed a bachelor’s degree or higher) in

our local ownership regressions. Further, using the religious adherence data from the “Churches

11The web site is http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data library.html.12The web site is http://www.smith.umd.edu/faculty/rwermers/ftpsite/Dgtw/coverpage.htm.13The election data are obtained from David Leip’s web site: www.uselectionatlas.org.

8

and Church Membership” files available through the American Religion Data Archive (ARDA),

we compute the proportion of Catholics (CATH) and the proportion of Protestants in a state

(PROT). Using the two religion variables, we define the Catholic-Protestant ratio (CPRATIO)

to capture the relative proportions of Catholics and Protestants in a state. We also measure the

overall religiosity of all U.S. states.

Table I provides a brief definition of all variables. Table II provides the summary statistics

for the firm-level economic relevance measure, while Table III report those statistics for other

key variables used in the empirical analysis.

III. Economic Presence and Local Ownership

We begin our main empirical analysis by quantifying the local ownership levels in headquarters

states and in states that are economically relevant for a firm. Our main objective is to assess

the extent to which investors display a preference for investing in firms that have an economic

presence in their state even when the investor is located far away from the firm’s headquarters

location. We provide estimates of local stock preferences of institutions using both institutional-

level and firm-level measures.

III.A. Institutional-Level Local Bias Estimates

Similar to previous local bias studies (e.g., Coval and Moskowitz (2001), Ivkovic and Weisbenner

(2005)), we use the following equation to measure the local bias of institution i around firm

headquarters:

HQ Local Biasi = Weight allocated to firms with headquarters in the state

− Market portfolio weight of firms headquartered in the state. (1)

Here, “weight allocated to firms with headquarters in the state” is the dollar value of the

institutional holdings in firms that are headquartered in the state in which institution i is

located divided by the total dollar value of all of holdings of institution i. The second term is

the benchmark weight and is defined as the total market value of firms headquartered in the

state in which institution i is located divided by the aggregate market value of all firms in the

market portfolio. If institution i follows the prescriptions of the traditional portfolio theory and

holds the well-diversified market portfolio, the HQ local bias measure would be zero.

A similar measure of institutional “local” bias can be defined with respect to firms that

have economic rather than physical presence in the state in which an institution is located.

9

Specifically, the local bias of institution i for firms with local economic presence is defined as:

ER Local Biasi = Weight allocated to firms with economic presence in the state

− Weight of economically relevant firms in the market portfolio. (2)

In this equation, “weight allocated to firms with economic presence in the state” is the dollar

value of the institutional holdings in firms that have strong economic presence in the state in

which institution i is located divided by the total dollar value of all of holdings of institution i.

We define the set of firms with strong economic presence as those for which the state is one of

the top five most economically relevant states based on the citation share scores. If institution

i follows the prescriptions of the traditional portfolio theory, the weight allocated to firms with

economic presence in the state would be the same as the weight of those firms in the market

portfolio, and the ER local bias measure would be zero.

Table IV reports the mean HQ and ER local bias estimates for all institutions (Panel A) and

various subgroups of institutions (Panels B to E). Consistent with the prior evidence, we find

that institutional investors exhibit a stronger preference for firms that have headquarters in the

state where the institution is located. The mean HQ local bias is 1.78%. More interestingly, we

find that the institutional local bias is stronger if the state in which the institution is located is

one of the top five economically relevant state for the firm. The mean ER local bias is 4.70%,

which is 2.92% higher than the mean HQ bias.

The strong institutional preference for firms with local economic presence is not restricted

to economically relevant states that are close to corporate headquarters. In fact, the evidence

in Panel A indicates that ER local bias is stronger in economically relevant states that are far

away from headquarters state. The ER−HQ local bias differentials are 1.29%, 2.88%, and 4.17%

for close, medium-distance, and far away ER states, respectively.

When we decompose the total ER bias based on the magnitude of economic relevance, we

find that the local bias for first, second, third, fourth, and fifth most economically relevant

firms are 1.84%, 0.96%, 0.84%, 0.60%, and 0.46%, respectively. The value-weighted estimates

exhibit a similar monotonically declining trend.14 This evidence indicates that the extent of

institutional local bias is strongly dependent upon the strength of local economic relevance of

firms.

When we use the size of the institutional portfolio to weight the institution-level local bias

14Using the value-weighted measures, the local bias for first, second, third, fourth, and fifth most economicallyrelevant firms are 1.50%, 0.83%, 0.78%, 0.59%, and 0.63%, respectively.

10

measures, we find that the HQ local bias measure is weakly negative (= −0.61%). This evidence

indicates that large institutions do not exhibit a stronger preference for locally headquartered

firms. However, they do exhibit a stronger preference for firms with local economic presence as

the mean ER local bias is positive (= 4.32%) and significantly higher than the mean HQ local

bias estimate.

To ensure that our results are not concentrated in any particular geographical region, we

compute the mean institutional local bias estimate for each U.S. state. These results are reported

in Appendix Table A.I. We find that institutional local bias in economically relevant states is

larger in magnitude than HQ local bias in 31 states.

We find similar results when we examine the excess local holdings of institutional subsamples

based on the institution type, trading frequency, portfolio size, and the number of stocks in the

portfolio. In particular, motivated by the evidence of heterogeneity in the informational advan-

tage across institutional types presented in Baik, Kang, and Kim (2010), we examine whether

local stock preferences in economically relevant states vary across institutional categories.

We use two methods to identify institutional types. Bushee (1998) distinguishes institutional

investors by the levels and changes of their past holdings into three different categories: quasi-

indexers, transient (i.e., short-term investors), and dedicated (i.e., long-term, non-indexers).

Another approach to categorize institutional investors is by examining their 13(f) institutional

types. Specifically, we consider investment advisers (including investment companies and inde-

pendent investment advisers), banks (including bank trusts), and other institutions (including

pension funds and university endowments).

In all instances, with the exception of dedicated investors, the ER local bias is significantly

higher than the HQ local bias. Further, while the local HQ bias estimates are weaker for large

institutional investors or those with large number of stocks in their portfolios, the ER−HQ bias

differential is significantly positive in those cases. These differences are also stronger when we

examine the value-weighted institution-level local bias estimates.

III.B. Firm-Level Excess Local Ownership Estimates

To provide an alternative perspective on the local stock preferences of institutional investors,

we report firm-level local ownership estimates. This aggregated measure avoids several pitfalls

associated with portfolio-level analysis highlighted in Seasholes and Zhu (2010). In particular,

the firm-level measure allows us to effectively account for potential cross-sectional dependence

in the performance of institutional portfolios.

Similar to the institution-level analysis, we estimate the abnormal local ownership level of

11

each firm in the headquarters state as well as in economically relevant states. Our measure

is similar to the firm-level local ownership measures used in previous studies (e.g., Coval and

Moskowitz (1999), Baik, Kang, and Kim (2010), Korniotis and Kumar (2011)). Specifically, we

measure the quarterly local institutional ownership for each firm-state pair as the ratio of the

number of firm shares held by institutions located within the state and the total institutional

ownership in the firm at the end of that quarter.

We also calculate the percentage weight of local institutions in the aggregate institutional

portfolio, which provides a benchmark for comparison. The aggregate portfolio weight represents

the expected level of ownership by local institutions when they follow the prescriptions of the

traditional portfolio theory and do not exhibit an abnormal preference for firms with physical

or economic presence in their state. The expected local ownership measure also accounts for

the non-uniform geographical distribution of institutions across the U.S. It is higher for regions

with greater concentration of institutional investors.

Using the two measures, we define each firm-state pair’s excess local institutional ownership

level as the difference between the quarterly local institutional ownership level of that firm-state

pair and the percentage weight of the state’s institutional investors in the aggregate institutional

portfolio:

Excess State-j Ownershipi =Ownership of state-j institutions in firm i

Total institutional ownership in firm i

−Value of portfolios of institutions located in state j

Value of the aggregate institutional portfolio(3)

For each firm, we compute the average excess state ownership levels for headquarters states

as well as five of its economically relevant (ER) states. For many firms, the HQ state is also

economically most relevant. To better distinguish between the effects of physical and economic

presence on local ownership levels and performance, we only consider ER states after excluding

the HQ state.

We aggregate the firm-level excess state ownership estimates to obtain state-level ownership

levels. For each state, we compute the excess HQ-state ownership and obtain estimates of excess

ERk-state ownership levels (k = 1, . . . , 5).15 Specifically, we compute the excess HQ-state own-

ership for a given state using the equal-weighted average of the firm-level excess state ownership

measures of firms whose headquarters are located in that state. Similarly, to compute the excess

ERk-state ownership for a given state, we aggregate the firm-level excess state ownership esti-

15For brevity, we consider only the five most economically relevant states. This choice is motivated by themedian number of economically relevant states, which is six.

12

mates of all firms for which the state is the kth most economically relevant states. For example,

the excess ER1-state ownership for a certain state is the equal-weighted average of firm-level

excess state ownership levels of firms for which that state is economically most relevant.

The firm-level local ownership estimates are reported in Table V. Panel A reports the average

excess state ownership levels for HQ and non-HQ states. We further sort HQ states using their

economic relevance, as captured by the citation share scores. We also sort non-HQ states using

economic relevance and distance from firm headquarters. Consistent with the institution-level

local bias estimates, we find that, the average excess local ownership in the HQ state is 4.86

percent and it varies significantly with economic relevance. The excess HQ-state ownership

increases monotonically with the citation share of the HQ state (see the “HQ State” column

in Panel A). The average excess HQ-state ownership levels for high economic relevance (i.e.,

citation share above 0.50) and low economic relevance (i.e., citation share below 0.05) HQ states

are 14.58 and 3.02 percent, respectively.

For firms whose HQ states are not mentioned in the 10-K reports (i.e., the citation share is

zero), the average excess local HQ ownership is negative (= −1.81 percent). This evidence indi-

cates that economic presence is an important determinant of high local institutional ownership

levels. Institutional investors do not overweight locally headquartered firms if those firms have

no economic presence in their respective HQ states.

To further quantify the relation between economic relevance and ownership, we examine the

ownership patterns in non-HQ states. We find that in non-HQ states the excess local ownership

level is also a monotonically increasing function of the state’s economic relevance for the firm

(see the second column of Panel A). The average excess local ownership levels for the most

and the least economically relevant non-HQ states are 6.17 and 0.99 percent, respectively. And

similar to the evidence in HQ states, the average excess local ownership level is negative in states

that are not mentioned in the 10-K reports (i.e., the citation share is zero).

For robustness, we use an alternative method to create economic relevance based firm-state

categories. This method does not use pre-defined citation share cutoffs. Rather, for each firm, we

rank all non-HQ states based on their citation share scores and identify its five most economically

relevant states. We designate the top five states as ER1, ER2, . . . ER5. We report the average

excess local ownership for these states in “All Non-HQ” column of Table V, Panel B. The results

are consistent with the evidence in Panel A. The excess local ownership is a monotonically

increasing function of the state’s economic relevance for the firm.

We find that these results are not driven by geographical concentration of firms and insti-

tutions in certain dominant states such as California and New York. Firms are economically

13

present throughout the U.S. and the citation share estimates of firms in economically relevant

states are comparable to the citation share estimates of firms headquartered in those states.

Figure 1 shows that the average proportion of economically relevant firms in a state is 0.660

(median is 0.667), while the average ER to HQ citation share ratio is 0.658 (median is 0.573).

These estimates are based on data for the year 2008 but the results are qualitatively similar in

other years.

To further ensure that our results are not concentrated in any particular geographical region,

Appendix Table A.II reports the mean state-level excess institutional ownership of firms whose

headquarters are located in the state. We also list the most economically relevant state and

provide local ownership estimates when the state is one of the five most economically relevant

states. Even in large states such as California and New York, local ownership levels for firms

with economic presence are comparable to the local ownership levels for firms with physical

presence in those states. And in several states, economic presence affects local ownership more

than the physical presence of firm headquarters.16

Figure 2 summarizes the mean local state-level ownership levels for the HQ state and ER

states. To highlight the importance of economic relevance, we report the mean local ownership

levels for ER1, ER2, ER3, ER4, and ER5 states separately. As expected, the level of excess

ownership declines as the economic relevance of a state declines. However, investors in even the

fifth most economically relevant state overweight local firms by an average of 1.32 percent. The

average local ownership in the five most economically relevant states is 8.73 percent, which is

considerably higher than the headquarters state average of 5.02 percent. These results are very

similar when we focus only on the subsample of states with highest institutional ownership levels.

Overall, the state-level local ownership estimates indicate that the institutional preference for

firms with local economic presence is not concentrated in any particular geographical region of

the U.S.

III.C. Distance From HQ, Economic Relevance, and Local Ownership

In the next set of tests, we examine whether the distance between headquarters location and

economically relevant states affect the local institutional ownership patterns. If the observed

impact of economic relevance on local ownership is concentrated in states that are closer to HQ

16To address the potential concern that our citation measure captures the economic relevance of a region ratherthan a state, we compare the state-level excess holdings of cited and non-cited states located in the same Censusregion or division. The results of this supplemental analysis are reported in Internet Appendix Table A.IV. Theevidence indicates that states with explicit citations are associated with larger local excess holdings than statesin the same Census region/division that are not cited explicitly in firms’ 10-K filings.

14

states, the high local ownership levels in economically relevant states may simply reflect the

proximity of economically relevant states to corporate headquarters.

We double-sort firm-state pairs based on the degree of economic relevance and distance from

headquarters and measure the mean excess local ownership levels. These results are reported in

the last four columns of Table V, Panels A and B. We find that local ownership levels are high

even when an economically relevant state is very far from the headquarters state. For example,

the results in Panel A indicate that the average excess local ownership is 5.97% for economically

relevant states that are close to the headquarters state (i.e., less than 500 kilometers away).

And the average local ownership level is higher (= 6.92%) for economically relevant states that

are located far from the headquarters state (i.e., at least 2,000 kilometers away).17

Even when we use an alternative method to create economic relevance based firm-state cat-

egories (see Panel B), we find that local ownership is a monotonically increasing function of the

state’s economic relevance, irrespective of the distance between firm headquarters and econom-

ically relevant states. These double sorting results indicate that the relation between economic

relevance and local institutional ownership does not merely reflect the physical proximity be-

tween economically relevant states and firm headquarters. Overall, economic presence rather

than physical proximity is a stronger determinant of local institutional ownership.

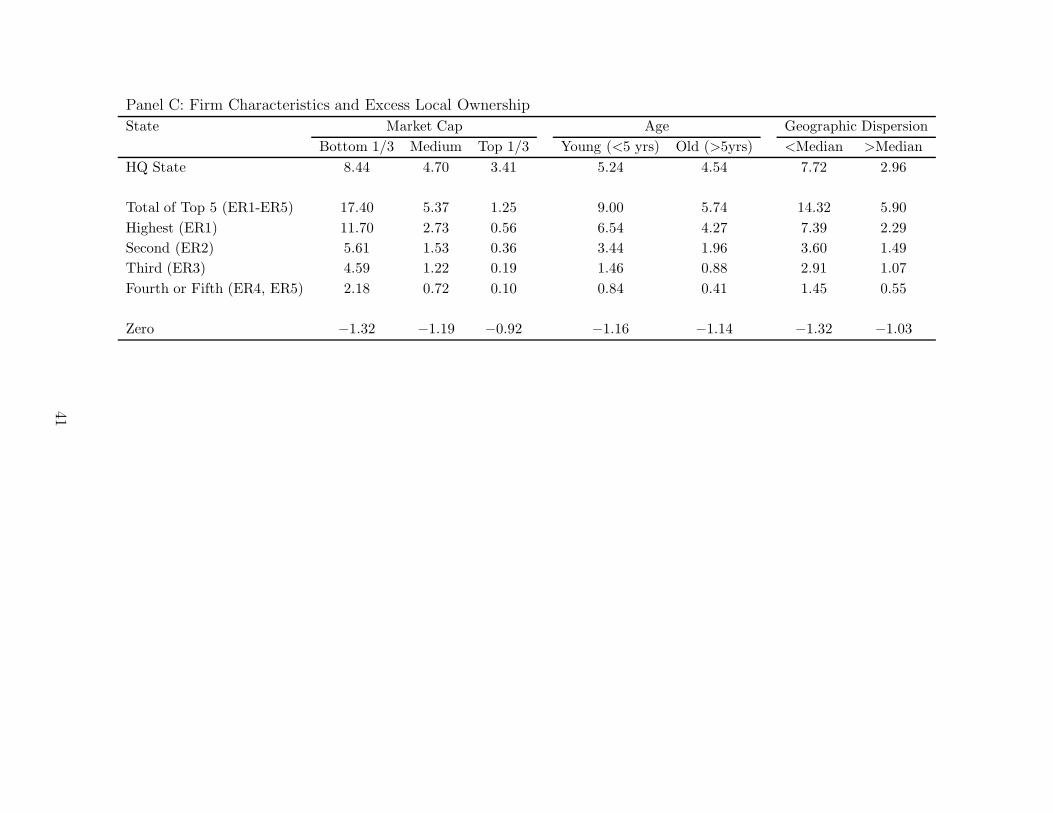

III.D. Firm Attributes, Economic Relevance, and Local Ownership

In this section, we examine whether firm attributes determine the impact of economic or physical

local presence on institutional ownership. We consider three firm attributes: size, age, and

geographic dispersion. These results are reported in Table V, Panel C. We find that local

ownership levels are higher for smaller firms, both in HQ and non-HQ economically relevant

states. However, in all three size-based categories, local ownership decreases monotonically with

economic relevance. Examining the firm age-based categories, we find that local ownership levels

are higher for younger firms, but again, we find a monotonic relation between local ownership

and economic relevance within each firm age category.

To ensure that our results are not driven by geographically dispersed firms that are present

in almost every state, we examine the level of excess local ownership in geographical dispersion

based subsamples. In particular, we examine the local ownership patterns in subsamples of

firms for which the number of states mentioned in the 10-K reports are below and above the

median number of states. We find stronger excess local ownership levels at both HQ and

17Our results are not very sensitive to the distance and economic relevance cutoffs. The results are qualitativelysimilar when we use other cutoffs to define these categories.

15

economically relevant locations for firms that are less dispersed geographically. And yet again, in

both subsamples, we find a monotonic relation between local ownership and economic relevance.

This evidence indicates that the observed local ownership patterns are not driven by firms

that are present in most states and are not really local to any particular set of investors. Overall,

the firm attributes based subsample results indicate that while firm attributes influence local

ownership patterns, economic relevance has an additional impact on local institutional ownership

levels.

IV. Determinants of Local Ownership

Our next battery of tests focuses on identifying the characteristics of regions and stocks that

are associated with stronger local clienteles. The goal of this analysis is to investigate whether

there are systematic differences in the local clientele characteristics of investors in headquarters

and economically relevant states. We also want to examine whether the local ownership levels

are higher when stocks are more difficult to value. For this exercise, we use several proxies for

investor sophistication (e.g., local education level, local religiosity, etc.) and the difficulty in

stock valuation (e.g., idiosyncratic volatility, firm size, etc.).

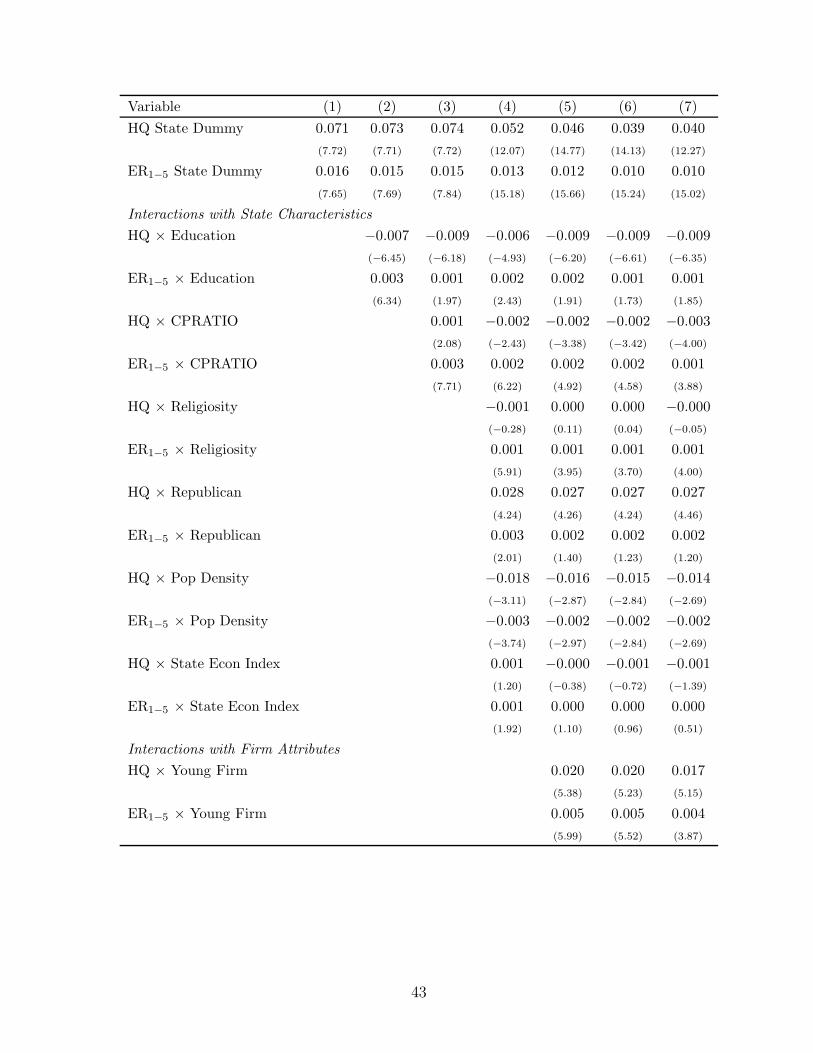

IV.A. Baseline Estimates

We estimate a set of Fama and MacBeth (1973) style regressions in which the dependent variable

is the local ownership of a given firm in a certain state (LocalOwni,j). It is defined as firm j’s

total share ownership of institutional investors located in state i as a fraction of the aggregate

institutional ownership in firm j. Among the independent variables, our primary focus is on

the following two location-based indicator variables: HQ state dummy for the headquarters

state and ER1−5 state dummy for the top five most economically relevant states excluding the

headquarters state. We also interact the two indicator variables with various state characteristics

and stock attributes to measure their incremental effects on local stock ownership. We include

state fixed effects in each quarterly cross-sectional regression to account for the expected level

of state ownership based on the size of a state’s institutional investor base in that quarter.

We report the time-series average of the coefficient estimates from quarterly cross-sectional

regressions in Table VI, where the t-statistics are calculated using the time series of these

coefficient estimates. In Model (1), we include only the two location indicator variables. The

first indicator variable is the HQ state dummy, which is set to one for firm-state pair when the

state is the firm’s headquarter location. The second indicator variable is the ER1−5 dummy,

16

which is defined using the economic relevance rank of a state for a given firm-year. This indicator

variable is set to one for a firm-state pair when the state has one of the five highest citation

shares for that firm-year.

Consistent with our sorting results, we find strong evidence of excess local ownership among

investors in both the headquarters states and economically relevant non-headquarters states.

Specifically, institutions in headquarters state overweight local firms by 7.1 percent, while the

average excess local ownership of institutions in the top five economically relevant states is 1.6

percent.

We also estimate the local ownership baseline regressions separately for subsamples based

on firm size. Small, medium, and large stock categories contain stocks in the bottom, middle,

and top terciles defined on the basis of the market capitalization measure. In these regressions,

instead of using one dummy variable for the five most economically relevant states, we use five

distinct dummies for those five states. The local ownership regression estimates for subsamples

based on firm size are summarized in Figure 3.

We find that the coefficient estimate is highest for the HQ state indicator variable. Examin-

ing the estimates of the five state economic relevance indicator variables, we find that across all

size groups the coefficient estimates decline monotonically as the degree of economic relevance

decreases. In addition, we find that the local ownership levels vary inversely with firm size,

independent of the location type (HQ or ER) and state economic relevance rank. This evidence

shows that the link between economic relevance of a firm’s location and local investors’ propen-

sity to hold disproportionately large fractions of the firm’s stocks is not exclusively a “small firm

phenomenon”. Both the strength of a firm’s presence as well as its size independently affect the

level of local ownership.

IV.B. Role of Investor Sophistication

In Model (2) of Table 5, we interact the local indicator variables with each state’s average educa-

tion level. Since education does not vary within state-quarter, we do not include the education

variable itself in the regression. We use the level of education as a proxy for overall investor

sophistication as the level of education would be correlated with local or investor attributes that

affect investor sophistication. But we do not assume that institutions in more educated regions

would be more educated.

The negative coefficient estimate of the HQ × Education interaction term suggests that local

bias in the HQ state is stronger among states with lower education levels. In contrast, the local

bias in economically relevant states is positively correlated with the state’s education level. The

17

opposite signs of these interaction estimates suggest that the underlying mechanisms that induce

high local ownership around headquarters and in economically relevant states may be different.

For robustness, we provide another perspective on the relation between education and local

ownership. We sort states into quartiles based on the level of education in the state and compute

the average excess local ownership for the four state quartiles separately for headquarters states

and economically most relevant states. The results are reported in Figure 4. The evidence

indicates that the average excess local ownership around headquarters decreases with educa-

tion but the average excess local ownership levels in economically most relevant states exhibits

an opposite pattern. This evidence further supports the conjecture that investors in economi-

cally relevant states are likely to be more sophisticated than local investors around corporate

headquarters.

IV.C. Impact of State Attributes

To further examine the underlying mechanisms that induce higher levels of local ownerships, we

introduce additional state characteristics in local ownership regression specification. In Model

(3), we include interactions between location indicators and the ratio of Catholic adherents to

Protestant adherents in a state (CPRATIO). This specification is motivated by the evidence

in Kumar, Page, and Spalt (2011), who demonstrate that investors in high CPRATIO regions

have a higher tendency to invest in lottery-type stocks.18 It is likely that investors’ gambling

propensity is stronger among local stocks because investors perceive them as being less risky. The

regression estimates indicate that investors in high CPRATIO regions have a higher tendency to

invest in local firms, particularly for firms with local economic presence. This evidence indicates

that investors’ speculative tendencies influence their local stock preferences.

In Model (4), we include additional state characteristics, including state religiosity, political

orientation, population density, and state economic activity index, as defined in Korniotis and

Kumar (2011). The religiosity and political orientation measures are designed to capture the

level of local conservatism, which is likely to influence institutional investors’ propensity to hold

local stocks. Our premise is that conservatism would be positively correlated with local stock

preferences of institutional investors.

The estimates from this extended specification indicate that local ownership levels are high

in Republican states as well as regions with low population density, and these effects are more

pronounced in headquarters states. Further, once we account for these state attributes, local

18Motivated by the salient features of state lotteries (low price, low negative expected return, and risky as wellas skewed payoff) and the theoretical framework of Barberis and Huang (2008), Kumar (2009) defines stocksthat have low prices, high idiosyncratic volatility, and high idiosyncratic skewness as lottery-type stocks.

18

economic conditions do not have a significant impact on the local stock preferences of local

institutions. In this extended specification, we also find that institutional investors in high

CPRATIO regions no longer have a greater tendency to invest in firms with local headquarters,

but the local ownership levels remain high in economically relevant states with high CPRATIO.19

IV.D. Impact of Firm Attributes

In the next set of tests, we identify firms that are more difficult to value and examine the impact

of firm attributes on local ownership levels. We are particularly interested in identifying firms

that may be less visible and/or harder-to-value because familiarity- or information-driven local

bias should be most pronounced among these firms. Further, the effects of these characteristics

on local ownership could vary across location types (i.e., HQ vs ER) if investor clienteles are

indeed different, as our earlier evidence indicates.

Harder-to-value are typically younger, have highly volatile prices, and have lottery-type

features (e.g., Zhang (2006), Jiang, Lee, and Zhang (2005)). Models (5) and (6) include the

interactions of local indicator variables with these firm characteristics. We find that local in-

vestors exhibit a stronger propensity to overweight younger firms, firms with higher volatility,

and stocks with lottery features. Interestingly, the preference for harder-to-value firms and

stocks with lottery features, which are likely to have higher information asymmetry, is stronger

in economically relevant states. In Model (7), we include other firm characteristics, including

firm size, market-to-book equity ratio, past return, return skewness, and stock price. We find

that local investors also exhibit a stronger propensity to invest in smaller firms, value stocks,

and recent losers.20

Overall, the results from our local ownership regressions indicate that local institutional

clientele is likely to be sophisticated as they invest in local stocks that are more difficult to value.

In addition, the coefficient estimates of the interactions with state-level education suggest that

local investors in economically relevant states may be more sophisticated than local investors in

headquarters states.21

19We also estimate the full model without these variables and report the estimates in Table A.V of the InternetAppendix. Our inferences for the other variables remain very similar.

20For robustness, we estimate the full model on the subsample of large firms and geographically dispersedfirms. We report the estimates in Table A.V of the Internet Appendix. We find very similar results across thesesubsamples.

21Motivated by the evidence of heterogeneity in informational advantage across institutional types (Baik,Kang, and Kim (2010)), we also examine whether local stock preferences in economically relevant states varyacross institutional categories. We use both the Bushee (1998) classification and the 13(f) institutional types.We find that the evidence of local stock preference is quantitatively similar across all different types of insti-tutional investors. Thus, local stock preferences in economically relevant regions do not vary significantly withinstitutional type.

19

V. Local Ownership and Local Performance

Our analysis so far provides evidence of institutional local bias at the headquarters location

and in economically relevant states, where institutional preference for firms with local economic

presence is stronger than their preference for locally headquartered firms. Further, the local in-

stitutional clienteles in economically relevant states are likely to be relatively more sophisticated.

In this section, we examine whether those sophisticated investors have an informational advan-

tage that they are able exploit to earn superior returns from their local investments. Specifically,

we compare the performance of portfolios sorted by local ownership and trading levels at both

the headquarters location and in economically relevant states.

Our analysis is partially motivated by the emerging evidence in the recent finance literature,

which suggests that useful “soft” information about future profitability and performance of a firm

may be geographically distributed and could reside away from firm headquarters. Specifically,

Giroud (2010) shows that information asymmetry between firm headquarters and plant locations

decreases when airline routes are introduced between headquarters and plant locations. In

a similar manner, useful information about a firm’s future performance may reside at non-

headquarters locations where a firm has economic presence.

Further, due to their relatively higher sophistication, investors around these non-headquarters

locations may have better local information and/or a greater ability to interpret this informa-

tion than investors around firm headquarters. Those institutions may also be able acquire local

information faster than institutions located around corporate headquarters.

V.A. Demand Shift Correlations

Before presenting the performance results, we examine the correlation between the demand

shifts of institutional investors at the HQ and ER locations. If the two groups of investors

are responding to different information signals or if they are interpreting the same information

signals differently, their trades are less likely to be correlated. In contrast, if their information

sources and sophistication levels are similar, their trades would be strongly positively correlated.

We find that the trading correlation between local demand shifts at HQ and various ER

locations is essentially zero. The average cross-sectional correlations vary between −0.013 and

0.003 but none of these estimates is statistically different from zero. Examining the correlations

among the demand shifts from various economically relevant states (ER1, ER2, . . . ER5), we find

that these estimates are also very low and statistically indistinguishable from zero.

The lack of strong positive correlation between demand shifts at HQ and ER locations is

20

consistent with the conjecture that the mechanisms driving the local bias around HQ and ER

locations are different. In the remaining part of this section, we compare the performance levels

of HQ and ER investors to provide stronger and more direct evidence to support this conjecture.

V.B. Institution-Level Local Performance Estimates

In the first set of returns-based tests, we examine the local informational advantage of institu-

tions by comparing the performance of institutions in headquarters (HQ) states and economically

relevant (ER) states. We also compare the performance levels of institutions at HQ and ER

locations with the performance of nonlocal institutions. To get better insights into the source

of institutional local information, we measure institutional performance using both portfolio

holdings and quarterly changes in institutional holdings.

We start by separating each institution’s portfolio into three sub-portfolios:

• Local HQ portfolio, which comprises of stocks in the institutional portfolio whose head-

quarters are located in the investor’s state;

• Local ER1−5 portfolio, which comprises of stocks for which the investor’s state is one of

the five most economically relevant state for the firm but the firm is not headquartered in

the institution’s state; and

• Non-Local portfolio, which contains all other positions in the institutional portfolio.

We then use the Daniel, Grinblatt, Titman, and Wermers (1997) method to calculate the

monthly characteristic-adjusted returns of each investor’s local and non-local portfolios. We

compute the average of portfolio returns across all institutions each month, and then report the

time-series averages of those monthly averages. To obtain the monthly performance estimates,

we value-weight the institutional performance measures using the total dollar value of the in-

stitution’s holdings at the beginning of the quarter. For robustness, we also report the alphas

from the four-factor model.

Table VII, Panel A reports the average performance of local and non-local holdings of institu-

tional investors. We find that the average characteristic-adjusted returns or the alpha estimates

are positive for all three portfolios, but significantly so for only the Local ER1−5 portfolio (see

Columns (2) and (3), first three rows). In the last three rows, we report the performance dif-

ferentials among these portfolios. These performance differentials indicate that institutional

investors’ Local ER1−5 holdings outperform the other two portfolios by a significant margin.

21

Specifically, the evidence in Column (3) indicates that Local ER1−5 holdings outperform non-

local holdings by 15.3 basis points per month, which translates into an annual characteristic-

adjusted out-performance of about 1.84%. In contrast, Local HQ holdings outperform non-local

holdings only by 5.5 basis points per month or about 0.66% annually (t-statistic = 1.21) on a

characteristic-adjusted basis.22 The four-factor alpha estimates reported in Column (2) portray

a similar picture.

These comparisons suggest that institutions at ER locations have better local informa-

tion than institutions at HQ locations. When we directly compare the performance of local

institutions at HQ and ER locations, we find that Local ER1−5 holdings outperform Local

HQ holdings by 8.9 basis points per month, which translates into an annual characteristic-

adjusted out-performance of about 1.04% (t-statistic = 2.54). The performance differential is

0.143 × 12 = 1.72% when we use the risk-adjusted performance measure. These performance

differentials are not very large but this evidence is consistent with our conjecture that investors

in economically relevant states are relatively more sophisticated and earn higher returns on their

local investments.

In Columns (4) to (9) of Panel A, we report the portfolio performance estimates and per-

formance differentials for subsamples of institutional investors sorted by their type and their

trading characteristic as categorized by Bushee (1998). We find that the superior performance

of Local ER1−5 portfolio in the aggregate sample is driven by two (non-exclusive) investor types:

investment companies and advisors as identified in the 13(f) filings and institutions categorized

as transient investors using the Bushee (1998) classification method. In particular, the Local

ER1−5 holdings of institutions identified as investment companies and advisors outperform their

Local HQ holdings by 14.9 basis points per month, which translates into an annual characteristic-

adjusted out-performance of about 1.79% (t-statistic = 3.26).

To gain additional insights into the local informational advantage of institutional investors,

we measure the performance impact of “trading” activities of institutional investors in local

and non-local stocks. Given the quarterly structure of institutional investors’ holdings data,

we cannot measure their trading activities directly. Instead, we use the changes in portfolio

holdings between two quarterly snapshots to identify “trading”. Specifically, we estimate trading

performance as the difference in the monthly characteristics-adjusted returns of the holdings

snapshot at the end of the preceding quarter minus the holdings snapshot at the beginning of

the preceding quarter. This performance differential captures the incremental performance that

22This evidence suggests that the superior performance of local HQ portfolios documented for the mutual fundsample during the 1975-1994 period (Coval and Moskowitz (2001)) does not extend to the broader institutionalinvestor sample and our sample period.

22

is due to trades executed during a quarter.

Table VII, Panel B reports the average performance of local and non-local trading by insti-

tutional investors. Similar to the holdings-based analysis, we divide each institutional portfolio

into Local HQ, Local ER1−5, and Non-Local sub-portfolios and obtain the performance estimates

of each of these three components. Consistent with the holdings-based performance results, we

find that the average characteristic-adjusted “trading” returns are positive for all three portfo-

lios (see Column (3), first three rows), but significantly so only for the Local ER1−5 portfolio

(14.2 basis points per month or about 1.70% annually; t-statistic = 2.20).

Examining the performance differences between the local and non-local portfolios, we find

that trading in Local HQ stocks does not outperform trading in Non-Local stocks. However,

institutional investors’ trading in Local ER1−5 stocks outperform their trading in both Non-

Local and Local HQ stocks. The performance differentials are 9.6 and 10.5 basis points per

month and both estimates are statistically significant. The t-statistics for these two estimates

are 3.68 and 3.57, respectively. When we break-down the trading-based performance estimates

by institution type (see Columns (4) to (9)), we again find that the superior performance in

Local ER1−5 stocks is concentrated among investment companies and advisors and transient

investors.

Overall, these holdings- and trading-based institutional-level performance results are consis-

tent with our key conjecture, which posits that institutional investors in economically relevant

regions would have better information about firms with strong local presence than investors

around corporate headquarters and non-local regions.

V.C. Performance of Local Ownership Sorted Portfolios

In the next set of tests, we examine the performance of firm-level local ownership and trading

portfolios. These tests allow us to further quantity the local informational advantage of insti-

tutions around headquarters and in economically relevant states. Specifically, we compare the

future performance of location-based portfolios constructed using institutional investors’ portfo-

lio holdings as well as quarterly changes in their holdings. A key advantage of this portfolio-based

approach is that it is not sensitive to potential cross-sectional correlations in the performance

of institutional portfolios. Thus, we are able to avoid one of the main pitfalls common in local

bias studies, as identified in Seasholes and Zhu (2010).

In these tests, we aggregate the positions of each state’s institutional investors in each firm

into a firm-state level observation of state holdings. These firm-state holdings are then normal-

ized by the aggregate holdings of all institutional shareholders of the firm. To account for the

23

variation in the size of institutional investor population across states, we calculate the abnormal

level of firm-state holdings by subtracting the expected level of holdings for the firm-state pair.

The expected measure is the share of the state’s institutional investors in the aggregate portfolio

of institutional investors.

We form the first set of level-based portfolios by sorting stocks into quintiles using the

excess local ownership of investors located in the firm’s headquarters state. The second set of

level-based portfolios are defined using the excess local ownership of investors located in non-

headquarters states that are economically relevant for the firm. This analysis is similar in spirit

to the method used in Baik, Kang, and Kim (2010). However, to account for the variation in

the size of local institutional investor population across states, we use excess local ownership

levels of local institutions instead of their raw local holdings.

In addition to the level-based portfolios, we create two sets of change-based portfolios by cal-

culating the percentage change in the normalized firm-state holdings. The first set of portfolios is

formed by sorting stocks into quintiles using the change in the holdings of institutional investors

located in a firm’s headquarters state. The second set of portfolios is formed by sorting stocks

using ownership changes of investors located in non-headquarters states that are economically

relevant for a firm.

The performance of local ownership sorted portfolios are reported in Table VIII. Specifically,

we report the average return of each quintile portfolio in the quarter immediately following the

quarter in which we measure the excess local ownership levels and local ownership changes. Panel

A reports the average return of level-based quintile portfolios, while Panel B reports the average

return of change-based portfolios. For brevity, we only report the performance estimates using

characteristic-adjusted returns, but our results are very similar when we use raw or risk-adjusted