Harmonisation of the Balkans in the field of electricity - Past achievments and future prospects

176

focus on— Energy karanovic/nikolic

Transcript of Harmonisation of the Balkans in the field of electricity - Past achievments and future prospects

focus on— Energy

karanovic/nikolic

A Global Issue

focus on—Energy

2013, Karanović & Nikolić

Contents

—2

/Intro01 — Entry word by the Energy Community’s Deputy Director 1002 — The Region–Current

situation, trends and cooperation 14

/Oil & Gas03 — Regulatory framework

and EU harmonisation 2604 — Who are the players –

biggest companies in the region 36

05 — The ‘South Stream’ project 40

/Electricity & Renewables06 — Regulatory Framework and EU

Harmonisation 5407 — The Grid Connection – problems and

solutions from throughout the region 62

08 — Transmission Networks Unbundling 68

09 — EFT Group: Current Developments in the Electricity Market in the Region 72

10 — Concessions for Hydro Projects in the Republic of Srpska – Miscalculation? 78

11 — Wind energy in Montenegro – The (un) success of 2010 wind concessions? 82

12 — Supporting renewable power generation in the Western Balkans 88

13 — Overview of the Feed-in Tariffs in the Region 100

/Harmonisation with The EU19 — Harmonisation of the

Balkans in the field of electricity – Past Achievements and Future Prospects 144

20 — Unpacking the ‘Third Package’ – The Croatian Story and the Region 154

21 — Cooperation between USA and Serbia – current situation and future prospects 162

—1 This designation is without prejudice to positions on status, and is in line with UNSC 1244 and the ICJ Opinion on the Kosovo* Declaration of Independence.

—4

/Energy, Environment and New Solutions14 — Environment vs. Energy

needs 11015 — Unconventional Energy

Resources – Shale: the Game Changer 116

16 — Environmental Transition in Practice – Curious case of Kosovo1 124

17 — Energy Efficiency In Macedonia 130

18 — Energy Trends in Africa 134

Foreword

—6

milestone in the integration process of the Balkans. We monitor the on-going changes that ought to prepare the energy sector and entire economies for the challenges ahead. Our Croatian team have provided this perspective through the prism of EU integration, providing their experiences and expectations, as the first Western Balkan country to obtain full membership into the Union. I can only hope that you’ll enjoy reading these articles as much as we enjoyed preparing them for you. Whether you are an energy lawyer or an executive, an electricity broker or a regulator – I am certain that you will find some topics of interest. I also hope that the perspectives presented here will give you a hint of some of the future developments in the region, as well as facts and figures concerning the regional energy sectors that may be of use to you.

Miloš VučkovićPartner

contributors helped us to delve into the African energy sector’s thrilling new developments to see how these emerging markets are managing their energy requirements.

We also had the future in mind while preparing this year’s edition. What should we expect on the energy horizon in the years to come? Which resources to watch for in the next decade or two? Which projects are a must for the Balkan countries and how can we make them happen? Our energy team believes these questions are crucial; therefore we tried to open up these subjects and create a platform for their discussion and consideration.

The current challenging situation in the region is the topic for several articles. The harmonisation of the regulatory frameworks and energy markets are a

On behalf of the Karanović & Nikolić energy team, I am proud to present the new 2013 edition of our Focus on Energy publication.

In the pages ahead, we have done our best to bring you the most up-to-date developments and hottest topics in the energy sectors throughout the region and beyond.

This year, we invited a number of our friends, colleagues, experts and clients to help us and to share their experiences and practices. This has enabled us to present you with first-hand articles on the regulatory tendencies and energy strategies in the Balkans, an analysis of the reform of the electricity markets, and the role of the Energy Community in these processes. Furthermore as a comparative our external

/Intro — Energy 2013, Karanović & Nikolić

01Entry word by the Energy Community’s Deputy DirectorBy Dr Dirk BuschleDeputy Director and LegalCounsel Energy Community Secretariat

—10

Implementing change obviously requires strong and persistent politicians at the helm. But it also requires individuals and companies in and around the energy sectors endorsing the ideas behind the Energy Community and ready to involve themselves. From experience I can tell that they do exist, and their number is growing. It gives me particular pleasure to see law firms becoming active and seizing the opportunities the Treaty establishing the Energy Community offers them. Like in the European Union, the vision informing the Energy Community is spelt out in the legal language of articles and paragraphs. European energy law is still a rather young discipline. It is quickly evolving, many legal questions are yet to be answered and there is only little precedence available. For smart, creative and proactive lawyers this is a big chance, a chance not only to advise their clients well but to become agents of the change needed in Europe’s, and in particular in South East Europe’s energy sectors.

The Energy Community may have been conceived in Brussels but it was born in South East Europe. It was, and remains to be, guided by a vision. The vision is to fundamentally change the governance of the energy sectors in each participating country, to make them transparent, efficient and competitive, and to attract the investment needed to revive the economies and increase the welfare of our citizens. This vision, translated into a Treaty, necessitates deep reforms in each country. To create a regional market moreover presupposes trust in the partners from across the borders, and governments giving up control to some extent. The path towards this vision is not always straight and is sometimes painful, as we have recently witnessed in Albania and Bulgaria. But ever since I have been working for the Energy Community I have never heard anybody claiming that the vision itself is wrong, and change is not needed.

—12

In carrying out this work, they need to rely on domestic institutions and courts which, for their part, need to adapt and reform. Companies and their counsel should also not be shy in seeking the assistance of the Secretariat which, under Article 90 of the Treaty, may institute proceedings for non-compliance with the Treaty. Over the past years, the Secretariat established this procedure as a tool for protecting investors and domestic companies alike, and to involve itself actively in the reform process throughout South East Europe. The procedure, but also the rule of law in the Energy Community in general, can largely benefit from the contribution made by professional lawyers knowing European energy law as well as they know the intricacies of region. This book constitutes an important element in this process.

The Energy Community continuously incorporates European legislation which needs to be implemented by and in the South East European countries. Recently, the Ministerial Council adopted the Third Package requiring far-reaching structural reforms of energy companies. The Network Codes which will be taken over by the Energy Community by and by will have a profound influence on the way the electricity and gas grids are operated. European legislation on renewable energy and energy efficiency will determine future generation mix and consumption patterns in our countries. At the same time, the environmental legislation is still to be effectively implemented. And the potential of competition and state aid law for opening up the energy sectors still remains to be tapped. There can be no doubt that much work lies ahead of companies and law firms in the region.

02The Region–Current situation, trends and cooperationby Petar MitrovićAssociate, Karanović & Nikolić

—14

fossil fuel reserves have been explored in the Western Balkans and Moldova. Ukraine, on the other hand is a large market, larger than all of the other Energy Community markets together, with nuclear energy being the most important type of energy that it uses.

Another common feature of these markets is that the main elements of energy infrastructure (primarily generation facilities) were developed in the 1960’s and 1970’s, primarily using technology from the Eastern Europe, which was even then well behind the level of technology that was available in the more developed Western European countries. The Balkan conflicts in the ‘90s resulted in the significant deterioration of the energy infrastructure, primarily in Bosnia and Herzegovina, Kosovo* and Croatia. Also, the infrastructure was generally very poorly maintained. Due to its age, the type of technology and inadequate maintenance, as well as war damage, there is a general need for the rehabilitation and replacement of infrastructure.

Aware of the necessity for cooperation and solidarity in the field of energy, in October 2005 the European Union and nine Contracting Parties (Albania, Bosnia and Herzegovina, Bulgaria, Croatia, Kosovo*, Macedonia, Montenegro, Romania and Serbia) took the decisive step of founding the Energy Community. In 2007, Bulgaria and Romania joined the European Union, and in line with the Treaty Establishing the Energy Community changed their status from Contracting Parties to Participants. In 2011, Moldova and Ukraine became full members of the Energy Community.

Overview of marketsCurrent situationThe Contracting Parties, save for Ukraine, have small and fragmented energy markets. The most striking common feature of these markets is import dependency. Specifically, the main energy sources are fossil fuels, which are predominantly imported, seeing as no significant

Natural gas In 2009, the total domestic natural gas production in the Contracting Parties was approximately 24.2 Bcm4, and imports were approximately 37.4 Bcm.

As an important route for the transport of Russian natural gas to the Western Europe, Ukraine transported almost 96 Bcm of natural gas from Russia to Europe.

Ukraine is also the single biggest producer of natural gas in the Energy Community with an annual production of 21.2 Bcm in 2009. The remaining Contracting Parties are positioned well behind then with Croatia being the second positioned producer with 2.71 Bcm in the same year.

The most developed gas markets are those in Ukraine, Croatia and Serbia. Gas markets are small in Bosnia and Herzegovina and Moldova. Albania, Kosovo* and Montenegro still do not have access to gas.

—4 Billion cubic meters

Electricity In 2009, the total electricity supply (domestic generation increased for net import) amounted to 273TWh. Approximately 62% of these quantities were supplied in Ukraine and 38% in the remaining Contracting Parties. The diversity in the electricity mix is notable, with the domination of coal and lignite in the mix at 42% (when calculated only for the Western Balkans and Moldova the participation of coal/lignite is even higher – 52%) at aggregate level. Even though it is present only in Ukraine, nuclear power has the second highest participation in the fuel mix on an aggregated level with a 30% share. These sources are followed by hydro generation at 18%, natural gas at 7% and oil at 2%.

Renewable energyRenewable energy (including large hydropower plants) has a notable presence in the total energy supply in several Contracting Parties - Montenegro 52%, Albania 43%, Croatia 39%, Serbia 29%, and Bosnia and Herzegovina 24%. Its contribution is smaller in Macedonia at 12%, whereas it is almost negligible in Kosovo* , Moldova and Ukraine.

Regardless of these common features, when it comes to the structure of the energy mix, this is completely diverse in the Contracting Parties. Whilst some of them have a balanced portfolio of energy sources (Serbia, Macedonia, Croatia); others are dependent on a few types of sources (Albania, Bosnia and Herzegovina, Kosovo*, Montenegro).

In 20092, the total primary energy supplied in the Contracting Parties was 155,878.68 ktoe3. 74% of this quantity was supplied in Ukraine, while the remaining 26% was supplied in the Western Balkans and Moldova. Domestic coal and lignite dominate the mix, primarily in Serbia and Macedonia. The following Contracting Parties have the highest share of coal and lignite in their energy supply:

- Serbia – 52%,- Macedonia – 50%, - Montenegro and Kosovo* – 48%, respectively, - Bosnia – 33%.

—2 Reference year3 Kilo tons of oil equivalent

—16

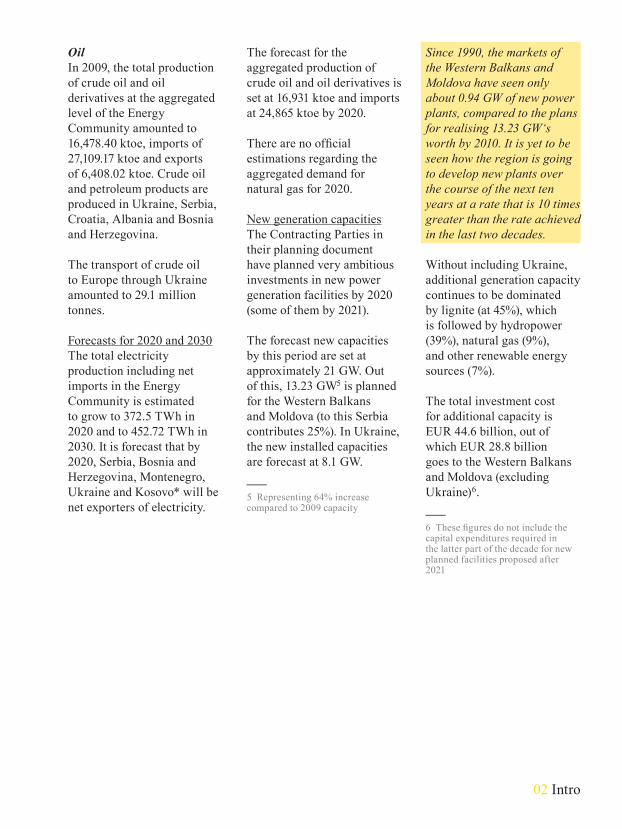

Since 1990, the markets of the Western Balkans and Moldova have seen only about 0.94 GW of new power plants, compared to the plans for realising 13.23 GW‘s worth by 2010. It is yet to be seen how the region is going to develop new plants over the course of the next ten years at a rate that is 10 times greater than the rate achieved in the last two decades.

Without including Ukraine, additional generation capacity continues to be dominated by lignite (at 45%), which is followed by hydropower (39%), natural gas (9%), and other renewable energy sources (7%).

The total investment cost for additional capacity is EUR 44.6 billion, out of which EUR 28.8 billion goes to the Western Balkans and Moldova (excluding Ukraine)6.

—6 These figures do not include the capital expenditures required in the latter part of the decade for new planned facilities proposed after 2021

The forecast for the aggregated production of crude oil and oil derivatives is set at 16,931 ktoe and imports at 24,865 ktoe by 2020.

There are no official estimations regarding the aggregated demand for natural gas for 2020.

New generation capacitiesThe Contracting Parties in their planning document have planned very ambitious investments in new power generation facilities by 2020 (some of them by 2021).

The forecast new capacities by this period are set at approximately 21 GW. Out of this, 13.23 GW5 is planned for the Western Balkans and Moldova (to this Serbia contributes 25%). In Ukraine, the new installed capacities are forecast at 8.1 GW.

—5 Representing 64% increase compared to 2009 capacity

OilIn 2009, the total production of crude oil and oil derivatives at the aggregated level of the Energy Community amounted to 16,478.40 ktoe, imports of 27,109.17 ktoe and exports of 6,408.02 ktoe. Crude oil and petroleum products are produced in Ukraine, Serbia, Croatia, Albania and Bosnia and Herzegovina.

The transport of crude oil to Europe through Ukraine amounted to 29.1 million tonnes.

Forecasts for 2020 and 2030The total electricity production including net imports in the Energy Community is estimated to grow to 372.5 TWh in 2020 and to 452.72 TWh in 2030. It is forecast that by 2020, Serbia, Bosnia and Herzegovina, Montenegro, Ukraine and Kosovo* will be net exporters of electricity.

02 Intro

Regional Energy Strategy“If necessity is the mother of invention, it is also the father of cooperation.”-John David Ashcroft,legal expert

As noted in the report of the European Commission (COM(2011) 105 final), the “Energy Community is about investments, economic development, security of energy supply and social stability; but – more than this – the Energy Community is also about solidarity, mutual trust and peace. The very existence of the Energy Community, only ten years after the end of the Balkan conflict, is a success in itself, as it stands as the first common institutional project undertaken by the non-European Union countries of South East Europe.”

Regional cooperation and solidarity have been the backbone of the Energy Community from the very beginning. Faced with new, very similar obstacles and

Council in October 2011 and the Task Force for the preparation of the Energy Strategy was established. The members of the Energy Strategy Task Force included representatives from each of the Contracting Parties, the European Union, the Donors Community and the Investors’ Advisory Panel.

It was decided that the Strategy would be prepared in two stages – first being the preparation and adoption of the text of Energy Strategy summarizing the main objectives of the Strategy and actions necessary to meet them. The second stage is related to the preparation the list of energy projects of regional interest.

In July 2012, the Energy Community Secretariat circulated the draft Strategy to the representatives of the Contracting Parties. The ministers subsequently adopted the draft Strategy at the 10th Ministerial Council in Montenegro, on 18 October 2012 and the first stage of the preparation of the Strategy was completed.

—18

challenges, the Contracting Parties decided to deepen their cooperation and to prepare the First Regional Energy Strategy.

The preparation of the regional energy strategy was proposed by the Serbian minister for energy and mining at the 8th Ministerial Council, held in Skopje in 2010. The remaining ministers welcomed the idea and instructed the Energy Community Secretariat to develop a more concrete proposal for deeper discussion and analyses.

The concept document “A Ten Year Strategy for the Energy Community 2011-2021”, was presented at the 21st Permanent High Level Group (PHLG) in June 2011. The PHLG agreed that the Strategy should contain the main development goals and actions required to meet them, priority projects and the mechanisms for the development of those projects. The PHLG also agreed that a task force should be set up to clarify the Strategy. The proposal of the PHLG was accepted by the 9th Ministerial

The Harmonization of VAT rules

One of the significant barriers to the creation of an integrated market is the inconsistency of VAT applicable to energy amongst the Contracting Parties in comparison with the VAT system applicable in the EU. Unlike the EU rules, the VAT laws and regulations in the Contracting Parties do not differentiate between the situation where the recipient of electricity is a wholesaler/reseller (“taxable dealer”) and where the recipient is a final consumer, i.e. between non-consumptive supply (trading) and consumptive supply of electricity (supply of final consumers of electricity). This inappropriate treatment is often the source of significant confusion as to how supplies involving a cross-border element should be treated for VAT purposes.

On the eve of the accession to the EU, Croatia proposed amendments to its VAT Law to align the rules with those applicable in the EU, including those related to the place of supply of electricity.

Activities necessary to create a competitive integrated energy marketIn order to reform the energy markets of the Contracting Parties and to create an integrated one, the following actions have to be taken:

— Removal of barriers at the interfaces between the Contracting Parties and EU Member States.

— Introduction of coordinated auctions for capacity allocation7, Establishment of one or more power exchanges that cover all Contracting Parties and the implementation of prices based on coupling.

— Adoption of regulatory balancing rules and balancing responsibilities for market participants.

— Removal of remaining barriers (regulatory, institutional and legal) to energy trade by January 2015.

—7 Serbia already organises coordinated auctions for capacity allocation with Hungary and Romania.

The Task Force is currently working on the second stage of the Strategy – projects of regional interest. The work on the list should be finalised over the course of 2013 and ready for the endorsement of the 11th Ministerial Council in October 2013.

Objectives of the Energy Community StrategyThe Strategy defined 3 key objectives, which, naturally, correspond to the main goals and tasks of the Energy Community itself. These objectives include the following:

— Creating a competitive integrated energy market,

— Attracting investments in energy, and

— Providing a secure and sustainable supply to customers.

Activities necessary to meet the objectivesThe Strategy defines the actions which need to be taken by the Contracting Parties (in addition to the implementation of the EU acquis) in order to achieve the set objectives.

02 Intro

It is expected that the new rules will become applicable by 1 July 2013. The remaining Contracting Parties have to harmonise their rules governing the VAT treatment for energy with those in the EU by 1 January 2015.

Actions necessary to attract new investmentsIn order to attract new investments in the energy sector, the Contracting Parties will need to take action in relation to price (de)regulation, infrastructure and the removal of administrative barriers in the authorization process.

Activities in relation to price (de)regulation include the following: phasing out of price regulation for large consumers, the adoption of cost reflective energy network tariffs and the adoption of prices that reflect the full cost of supply for tariff consumers.

As for the actions to be taken in relation to energy infrastructure, the precise set of measures should be proposed by the Energy Strategy Task Force by mid-2013. These may generally include accelerated and

The share of gross final energy consumption established by the Ministerial Council in October 2012 should be achieved through the adoption and implementation of the National Renewable Energy Action Plans, the simplification of authorization procedures for renewable projects and the introduction or improvement of existing support schemes for such projects.

On the environmental protection front, the Contracting Parties have to prepare the national road maps for the implementation of the large Combustion Plants Directive by the end of July 2013 and national road maps for GHG emissions reduction/limitation by the end of 2013.

Finally, in relation to the protection of consumers, it is necessary to ensure the protection of vulnerable customers and to create a clear and transparent regulatory framework, to set standards for the quality of services and to provide clear guidelines for when one wishes to switch energy supplier.

coordinated permit granting procedures, coordinated regulatory authorizations and support from relevant EU funds.

Finally, the Contracting Parties should introduce harmonised licensing regimes in line with the applicable EU regime by 1 January 2015.

Actions related to providing secure and sustainable energy supplies to consumersA number of measures in relation to security of supply, energy efficiency, renewable energy, environmental protection and protection of consumers are defined.

Security of supply will be accomplished through the establishment of an appropriate internal framework for security of supply, enhancement of preparedness to secure gas supply and the diversification of gas imports.

The Contracting Parties should increase the efficient use of energy by achieving a minimum 9% energy saving target by 2018.

—20

full list of projects envisaged in this category, as well as in other categories by the Regional Energy Study (electricity transmission, gas and oil) is available on the web page of the Energy Community - http://www.energy-community.org/portal/page/portal/ENC_HOME/AREAS_OF_WORK/Regional_Energy_Strategy/PECIs .

Power generation projectsHydro Power System of the Upper Drina (Bosnia and Herzegovina)The project includes the construction of 3 hydro power plants (HPP Buk Bijela, HPP Foca and HPP Paunci) on the Drina River and one HPP Sutjeska on the Sutjeska River, a tributary of the Drina River. The estimated value of the project is EUR 474.17 million. It should be finalized between 2019 and 2021.

ProjectsIn the second phase for the preparation of the Energy Strategy, the Energy Strategy Task Force will be working on identifying energy projects of regional importance, with the goal that financing and regulatory procedures take place in a coordinated manner.

The Regional Energy Strategy provided the methodology and criteria for the identification of projects of regional importance, as well as categories of projects which could be considered projects of regional importance.

The Task Force will identify the projects of regional importance in the course of 2013 on the basis of applications submitted to it by project promoters.

The most significant projects in the area of power generation submitted to the Regional Strategy Task Force are summarised below. The

HPPs on Lower Drina (Bosnia and Herzegovina and Serbia)Donja Drina HPP is a system of four run off river facilities located downstream of Zvornik HPP on the Drina River: Kozluk HPP, Drina I HPP, Drina II HPP and Drina III HPP. The hydro power potential is being divided in a ratio of 50:50% between Serbia and BiH. The total installed capacity of the planned hydro power plants is 365 MW while the average annual generation amounts to 1,588 GWh of electricity. The estimated value of the project is EUR 1.35 billion.

HPPs on Middle Drina (Bosnia and Herzegovina and Serbia)The Middle Drina HPP is a system of run off river facilities located between Bajina Basta and Zvornik HPPs on the Drina River. It will consist of three plants: Tegare HPP, Rogacica HPP and Dubravica HPP. The total installed capacity of planned hydro power plants is 321 MW. The estimated value of the project is EUR 870 million.

02 Intro

8.5 MW and 12 MW each) on the Ibar River. The project should be developed by EPS in cooperation with Italian Seci Energia S.p.A. The realization of the project should start in 2014 and end gradually in phases between 2016 and 2021. The estimated value of this project is EUR 300 million.

Kolubara B TPP (Serbia)The project includes the development of 2 lignite fired units with an installed capacity of 375 MW each. The lignite fired in the plant will come from the Kolubara Mining Basin. The investments in the project are estimated at EUR 1.3 billion. The project should be completed by 2019.

Nikola Tesla B3 TPP (Serbia)The project includes the construction of a third unit of the very important TPP Nikola Tesla. The installed capacity of the unit is set at up to 800 MW. The project, which has an estimated value of EUR 1.1 billion, should be completed by 2020.

HPPs on the River Lim (Montenegro) Montenegro plans the construction of small hydro power plants system on the River Lim, including the following SHPPs: ‘’Plav’’, ’’Murino’’, ’’Kruševo”, ’’Mostine’’, ‘’Jagnjilo’’, ‘’Andrijevica’’, ‘’Lukin Vir’’, ’’Berane 1’’, ’’Berane 2’’, ‘’Poda’’, “Bijelo Polje 1’’ and “Bijelo Polje 2’’. The estimated investments amount to approximately EUR 167 million. The project should be finalized by 2017.

HPPs on the Velika Morava River (Serbia)The project includes the development of 5 HPPs (installed capacity between 28.9 MW and 30.6 MW each) on the Velika Morava River. The project should be developed by the public company EPS in cooperation with RWE. The realization of the project should start in 2016 and end in 2021. The value is estimated at EUR 250 million.

HPPs on the Ibar River (Serbia)The project includes the development of 10 HPPs (installed capacity between

HPP Dubrovnik II (Croatia and Bosnia and Herzegovina)The planned installed capacity of HPP Dubrovnik II is set at 300 MW. The electricity output should be divided 50-50 between Croatia and Bosnia and Herzegovina. The estimated value of the project is EUR 170 million. It is planned that the project will be finalised by 2017.

Hydro Power Plants on Crna River (Macedonia)HPP Cebren (installed capacity targeted between 315 MW and 333 MW) and HPP Galiste (installed capacity between 185 MW and 197 MW) should be constructed and operated by the concessionaire for a period of 52 years. The concession should also include a right to operate and maintain the existing TPP Tikves (with installed capacity of 116 MW). The concessionaire will be an SPV incorporated by ELEM and a third-party investor. The value of project is estimated at EUR 600 million. The HPP Cebren is planned to be developed by 2020 and the HPP Galiste by 2026.

—22

/Oil & Gas — Energy 2013, Karanović & Nikolić

03Regulatory framework andEU harmonisationBy Jadranka Jerković, Ivana Vragović, Petar Mitrović, Veton Qoku Associates, Karanović & Nikolićand Josip Marohnić Attorney at Law/Odvjetnik in association with Karanović & Nikolić

—26

— The Law on the Pipeline Transport of Gaseous and Liquid Hydrocarbons and the Distribution of Gaseous Hydrocarbons. This regulates the pipeline transport of gaseous and liquid hydrocarbons, the distribution of gaseous hydrocarbons, as well as construction and maintenance.

— The Law on Mining and Geology Explorations. This regulates mineral policy, the conditions for the exploration and production of minerals (including oil and gas), the construction and maintenance of mining related premises and their subsequent decommissioning.

The key laws, in particular the Energy Law, are largely in line with the Second Energy Package (as in the

All members of the Energy Community undertook to implement the EU acquis on energy into their respective national legislation. In line with the requirements of the Energy Community Treaty, the national legislation of such member countries is more or less based on the rules comprising of the EU Second Energy Package. Croatia, who are on the cusp of joining the EU have gone a step further and implemented the EU Third Energy Package.

SerbiaThe regulatory framework for oil and gas is set out by primarily by the Energy Law. The Energy Law, being the umbrella law for the entire energy sector, also regulates the oil and gas sector, including the aims of the energy policy, conditions for the performance of energy activities, the functioning of the gas and oil activities, and the protection of consumers.

In addition, the oil and gas sector is also governed by the following laws:

—28

MacedoniaThe regulatory framework for the oil and natural gas sectors in the Republic of Macedonia is primarily set out by the Energy Law 2011. The Energy Law takes the form of an “umbrella” law, covering all significant energy related areas including inter alia the oil and gas activities and markets.

The other key regulatory acts that apply to the oil and gas sectors are:— The Law on Mineral

Resources. This regulates the conditions and procedures for the geological exploration and the exploitation and processing of mineral resources.

— The Law on Concessions and Public Private Partnership. This regulates the manner in which concessions of common interest (such as oil and gas) are granted and the manner in which public-private partnership agreements are established.

— A number of other laws and bylaws regulating different aspects of environment protection, construction, trade etc.

As for the oil market, it has already been fully liberalized, and Serbia for quite some time does not impose any restrictions on imports and the processing of oil and oil derivatives.

The authorities in charge of the regulation of the gas sector include:— The Serbian Government,

which has a primarily policy-making function in the sector.

— The Ministry of Energy, Development and Environmental Protection, which is in charge of the implementation of the policy documents and laws, and performs various administrative, regulatory and supervisory functions.

— The Energy Agency, an independent regulatory body that decides on the issuance of licences, tariff methodologies and regulated tariffs.

case of electricity, in Serbia, the regulator cannot impose fines for a breach of the law because this falls under the exclusive competence of the courts).

The Energy Law provides for the full liberalization of the gas market by 1 January 2015, when households will be able to choose their supplier. It is expected that the liberalization of the market will finally lead to the stronger participation of private companies in the supply sector.

The 2011 Energy Law provides a framework for the legal unbundling of distribution from the public supply of gas. Even though the deadline for the unbundling of distribution and supply was 1 October 2012, it has not yet been implemented in practice.

In addition, Serbia has gone a step further with the implementation of acquis and it also implemented the requirement for the preparation of crisis-prevention plans.

03 Oil & Gas

exploration and production of oil and gas. The exploration and production of oil and gas was previously governed by the Law on Geology Explorations and the Law on Mining. However, these regulations treated the exploration and production of oil and gas like any other mineral resources, not recognising the specifics related to oil and gas. The Law on the Exploration and Production of Hydrocarbons explicitly states that the Concession Law, the Law on Geology Explorations and the Law on Mining will not apply to the exploration and production of oil and gas.

According to the Law on Exploration and the Production of Hydrocarbons, a special administration authority will be responsible for hydrocarbons. However, the said authority has not yet been established. Until the establishment of this authority, the Ministry of Economy, Sector for Mining and Geological Research will be responsible.

Macedonia already has an unbundled natural gas sector. Namely, different entities are in charge of: (i) the transmission of natural gas; (ii) the distribution of natural gas; as well as (iii) the end supply of natural gas. However, although the liberalisation of the gas market was primarily planned for June of 2012, such liberalization is yet to be achieved.

Тhe oil market in Macedonia is already fully liberalized, however in practice a handful of entities still dominate the sector.

MontenegroAside from strategic and policy documents, i.e. the Energy Policy of Montenegro until 2030 and Energy Development Strategy until 2025, the regulatory framework for oil and gas in Montenegro is regulated by two main pieces of legislation, the Law on Exploration and Production of Hydrocarbons and the Energy Law.

The Law on Exploration and Production of Hydrocarbons was enacted in 2010 and this is the key law for the

The key laws, in particular the Energy Law, are largely in line with the Second Energy Package. However, changes in the legal and regulatory framework are expected in the near future under the Programme for the Realisation of the Strategy for Energy Development for the Period 2012 to 2016. The Macedonian Government plans to adopt by 1 January 2015 the Third Energy Package of the European Union.

The proposed timetable for this envisaged legal and regulatory framework change is as follows:— A platform and an action

plan for a new energy law will be adopted by mid-2013.

— The new energy law will be drafted by mid-2014.

— The bye-laws, which under the new energy law will be drafted by the end of 2014.

—30

and harmonized, liberated markets. Along the lines of the Directive 2009/73/EC concerning common rules for the internal market in natural gas, the 2012 Energy Act introduces a category of vulnerable customers and respective safeguards to protect such final customers. The government passed considerable authority to the regulating agency, such as passing the supply terms and conditions, quality of service and even setting the tariff items that affect the final price of gas. The technical implementation of bylaws are yet to be enacted in the first half of 2013.

The 2013 Gas Market Act further promotes the non-discrimination, effective competition, efficient market functioning and open third-party access, especially cross-border interconnection. The Act leaves until the end of first quarter of 2014 for participants to align their business with the new regulation. The subsidiary of INA (a leading national, recently privatized oil company) maintains the status of public service, home consumers and balancing supplier by that date. Existing gas distribution concessions

CroatiaFollowing the initial modern energy regulation in 2001 and the 2004 to 2008 period of legislative overhaul that was part of the EU acquis implementation in the accession negotiations, the most recent legislative changes finally implemented the Gas and Electricity Directives of the third package for an internal EU gas and electricity market. The implementation commenced with the all-new framework Energy Law that was enacted in the last quarter of the 2012. The new Gas Market Act followed in the first quarter of the 2013. Oil regulation may not follow, as the latest accession requirements have been fulfilled by the 2011 Oil Market Act amendments.

By ensuring greater security of supply and fewer interruptions in gas supply, by setting clear conditions for investing in power plants and transmission networks, the latest set of gas-related laws is expected to achieve more secure, competitive and sustainable energy,

It is expected that the Government of Montenegro will grant its first concession under the Law on Exploration and Production of Hydrocarbons in 2013.

The Energy Law regulates the transport, distribution, storage, retail and wholesale and supply of oil products and gas. Under the Energy Act, the Montenegrin oil and gas market are fully liberalized and the key players are private entities.

The authorities in charge of the regulation of the oil and gas sector include:— The Montenegrin

Government, which has a primarily policy-making function in the sector.

— The Ministry of Economy, Sector for Mining and Geological Exploration which is in charge of the implementation of the policy documents and laws, and performs various administrative, regulatory and supervisory functions.

— The Regulatory Energy Agency, an independent regulatory body that decides on the issuance of licences, tariff methodologies and regulated tariffs.

issuance of license for the production, the license for transport and the license for the storage of oil and oil derivatives.

— In the FBH, the law governing the oil sector has not been adopted. The Draft Law on Oil Derivatives was produced in October 2012, but there is no official information as to when the adoption of the law could be expected. For now, the following secondary legislation is in force: the Decision on the Obligation of a Merchant to Create and Maintain a Minimum Stock of Oil Derivatives; Rules on Conditions for the Minimum Technical Equipment of Business Premises for the Performance of Trade; Rules on the Method of Registering and Controlling the Turnover of Oil Derivatives and other Products and Services at Petrol Stations via Installed Equipment in FBH. Additionally, the Law on Domestic Trade governs the wholesale and importation of oil.

Bosnia and HerzegovinaBosnia and Herzegovina (“BH”) has several levels of political structuring under the overall federal government. The most important of these is the division of the country into two entities these being the Republic of Srpska (“RS”) and the Federation of Bosnia and Herzegovina (“FBH”). In addition to these, the Brcko District (“BD”) as a specific unit of local government was created in 2000. The energy sector in BH essentially reflects the constitutional organization of the country - the regulatory powers in the sector are divided between the central government and the entities, while the BD does not have authority in the energy sector.

The regulatory framework in the oil sector is set by the regulations on the level of the entities, including the following:— In the RS, the legal

framework is defined by the Law on Energy, while the Law on Oil and Oil Derivatives governs the production of oil derivatives, market functioning and safe supply. The Rulebook on the Issuance of Licenses regulates, inter alia, the

must be aligned in terms of duration (20 to 30 years) and the concession fee (turnover percentage in accordance with a government bylaw that has not yet been passed). The regulator is given authority to foster market competition, by imposing measures upon market participants that include the forced sale of gas at public auctions.

The 2006 Oil regulation needed significant amendment as recently as 2011, principally to comply with accession negotiation requirements on maintaining a minimum stock of crude oil and petroleum products and the 2009 Council Directive on the matter. The investment cycle that was to be launched with the law had still not occurred.

Traditional petroleum products had seen new regulation with the 2009 regulation on transport biofuel. That was already at a time that the EU realised the effect that it had on the price of food. Therefore, the 2010 changes introduced second-generation renewable fuel concepts from the latest EU directives.

03 Oil & Gas

—32

The new RES Decree on the Security of Supply and Delivery of Natural Gas regulates the measures that are to be taken to secure the long-term stability in the supply of gas; measures in the case of disruption to the supply and delivery of gas; an obligation to supply and deliver gas to certain special categories of consumers; priorities in the supply of gas in the event of the termination of supply; and the content of the report on security in the supply of gas. Moreover, the Law on the Pipeline Transport of Gaseous and Liquid Hydrocarbons and Distribution of Gaseous Hydrocarbons, (which was adopted in 2012) regulates the requirements for the safe and undisturbed pipeline transport of gaseous and liquid hydrocarbons and the distribution of gaseous hydrocarbons, and the design, construction and maintenance and use of pipelines.

The regulatory framework in the natural gas sector is set by the regulations enacted at entity level, including the following8:— In the RS, the Gas Law

governs the terms and conditions for the supply, transportation and distribution of natural gas, including the construction of gas facilities and the licensing system for the performance of gas activities. Also, the General Conditions for the Supply of Natural Gas regulate the supply of natural gas to customers, the rights and obligations of the suppliers and the conditions under which a discontinued or limited supply of natural gas can be applied to certain customers.

—8 BH has still not properly implemented Directive 2003/55, Directive 2004/67 and Regulation 1775/2005 as was required by the Energy Community Treaty. Pursuant to the obligations under the signed Treaty on the development of gas regulation on the national level and the transposition of EU Directive 2003/55/EC on the internal gas market, the Ministry of Foreign Trade and Economic Relations of BiH has established an Expert Team in order to reach a fully compliant and harmonized legal framework in BH.

The institutional framework of the oil and gas sector in BH consists of the national Ministry of Foreign Trade and Economic Relations and following two entity ministries:— In the RS, the Ministry

of Industry, Energy and Mining;

— In the FBH, the Federal Ministry of Energy, Mining and Industry.

Key authorities in the oil and oil derivatives sector:— In the RS, The Regulatory

Commission of the RS (the “RCERS”) has jurisdiction over the regulation of activities, such as the determination of the methodology for the calculation of costs of oil and oil derivatives transport, tariff system, approving prices for the use of oil, issuing licenses, etc.

— In the FBH, the Federal Ministry of Energy, Mining and Industry has jurisdiction over such activities.

decree once this law is enacted. The draft law governs the organization and functioning of the natural gas sector, rules and conditions for carrying out energy activities in this sector, planning and development of the natural gas market, market regulation, “unbundling” of activities, third party access to natural gas systems, construction and reconstruction of infrastructure facilities, technical rules, supervision of the enforcement of the laws, related principles, procedures, rights and obligations of natural persons and legal entities and other issues relevant to the gas sector in the FBH. This draft law stipulates the establishment of the Regulatory Commission, which will take over all the responsibilities, competences and powers of the gas regulator in the FBH.

— In the FBH, the Decree on the Organisation and Regulation of the Gas Sector Economy sets out the general legal and institutional framework for the supply and distribution of natural gas in the FBH.

The key authorities in charge of the regulation of gas include:— In the RS, the RCERS, an

independent regulatory body that decides on the issuance of licences, the issuance of general conditions for the supply of natural gas, the tariff methodologies and regulated tariffs.

— In the FBH, supply and distribution of natural gas is currently regulated by the Decree on the Organization and Regulation of the Gas Industry Sector of the FBH. However, in May 2013 the Federal Government adopted the Draft Law on Gas, which will supersede the current

03 Oil & Gas

exploit

exploit

04Who are the players – biggest companies in the regionBy Ivana VragovićAssociate, Karanović & Nikolić

—36

companies are present, inter alia, in Sarajevo, Belgrade and Podgorica. One of the partly owned INA’s companies is Jadranski naftovod JSC (“Janaf”), which owns and operates the Adria pipeline system. The company cooperates with its neighbouring countries. Specifically, Janaf and the Serbian subsidiary of Gazprom, Naftna industrija Srbije a.d. (“NIS”) have signed an Agreement on the Transport of 1.8 mill tons of oil from Janaf that it needs during 2013. In BH, Janaf has its presence through the daughter company “Janaf – Terminal Brod LTD”. Additionally, “Oil Refinery” in Brod (in Bosnian: „Rafinerija nafte“ a.d. Brod) imports crude oil via the Adriatic oil pipeline Janaf, its length being around 13 km in BH/Republic of Srpska.

Another important player in the oil and gas market is Hrvatska Elektroprivreda (HEP). HEP is a national electricity company, which is, in the last two decades, also engaged in the heat supply and gas distribution.

For many years the Croatian INA-Industrija Nafte (“INA”) has occupied second position in the Southeast Europe 100 Company rankings, which makes it the biggest oil company in the Balkan region and deservingly puts INA at the top of our list. INA is a joint stock company, with Hungarian MOL and the Republic of Croatia as its biggest shareholders. It was established through the merger of Naftaplin (a company for oil and gas exploration and production) with the refineries in Rijeka and Sisak. INA manages a regional network of 454 petrol stations in Croatia and in the neighbouring countries of Bosnia and Herzegovina (BH), Slovenia and Montenegro. In 2011, INA had total revenue of 3.6 billion euro.

The INA Group has a leading role in the Croatian oil business and a strong position in the region in the oil and gas sector activities. The Group is comprised of several affiliated companies that are wholly or partially owned by INA. Such

—38

During the past 15 years or so, the oil derivatives market in BH has been mostly dependant on oil derivatives import. The re-launch of production in the “Oil Refinery” in Brod and its continuous operation has had a significant impact on the decrease in oil derivative imports during the past three years. Oil derivatives are mostly imported from Croatia, Italy, Hungary, Slovenia and Austria. The majority owner of the only two Bosnian oil refineries (the one in Brod and the “Oil Refinery” in Modrica, as well as of the company Petrol Banja Luka), is the company NeftegazInKor. NeftegazInKor is also the founder of the “OPTIMA Group” LTD Banja Luka for trading of oils and oil derivatives. OPTIMA Group business operations entail the supply of raw materials for the production of oil derivatives from the two BH refineries, the processing of raw materials and launching oil derivatives on the BH and the international market.

second biggest share belongs to the Republic of Serbia, while the remaining portion is held by a handful of small shareholders.

The leader in the gas market in Serbia is Srbijagas, the company that performs transport, distribution and storage of natural gas. It was established back in 2005 by the Republic of Serbia in the process of the restructuring of NIS. Worth mentioning is - YugoRosGaz JSC, with pipeline construction and the distribution of natural gas as its business activity. The company is a Gazprom subsidiary in Serbia, owned by Gazprom, Srbijagas and Central ME Energy & Gas AG.

In BH, the gas market is small, with integrated supplies from integrated companies owned by state-owned companies. BH Gas is the single wholesale gas supplier in the country. BH Gas, in cooperation with the Energoinvest Company, has signed long-term contracts on the transit of natural gas with foreign partners, including: The company Mol – through a transport system in Hungary until 2018, and with Srbijagas - through a transport system in Serbia until 2017.

It is organized in the form of a holding company with a number of daughter companies. Within HEP operates HEP Proizvodnja LTD, whose daughter-company Pump station Busko blato LTD is situated in BH.

The Serbian company NIS is also one of the biggest oil companies in South East Europe with two refineries – in Pancevo and in Novi Sad. Its business activities include oil and natural gas exploration, production and refining, as well as the sale of a wide range of oil products. Apart from Serbia, NIS operates in the territory of Angola (where it has concessions for the exploration and exploitation of oil) and in BH. In Republic of Srpska, NIS owns the company Jadran-Naftagas, established as a joint-venture with the Russian company called NeftegazInKor. The majority owner of NIS is the Russian Open JSC Gazprom Neft (“Gazprom”), while the

The company performs the exploration, exploitation and trade of petroleum products in Montenegro. Since 2002, it has been a member of the large Hellenic Petroleum Group. After the SP Agreement had been signed, Hellenic Petroleum became the majority shareholder of Jugopetrol AD Kotor. Since then, the retail network of the Company operates under the commercial brand “EKO”. Jugopetrol AD Kotor has a network of 38 petrol stations in Montenegro and 3 petrol stations in BH.

The company “Euro Pact” is also one of the most successful in the oil industry of Montenegro. Oil and oil related products represent the main business operation. The successful cooperation of the Company was established with large number of significant business partners from Serbia, Albania, Kosovo*, BH, Croatia and the European Union.

products in Macedonia. Its core business is the retail and wholesale of oil, oil products, natural gas and biodiesel. Makpetrol Group has its own affiliates, four of which are located in Macedonia, while on an international level the Company owns affiliated companies in Greece, Petrolmak and in the Republic of Serbia, Makpetrol-Beograd.

Another important company in the gas sector in Macedonia is a joint stock company GA-MA for the transmission of natural gas and for the management of the natural gas transmission system. It was formed by an agreement between Makpetrol a.d. and the Government of the Republic of Macedonia.

In Montenegro however, there is no gas distribution infrastructure, which is why the consumption of gas is negligible. The largest petrol firm is Jugopetrol JSC Kotor.

The majority owner of the Russian NeftegazInKor is Zarubezhneft Moscow which does business under the trademark Nestro. Under this trademark all of the Bosnian oil companies: OPTIMA Group, Petrol, “Oil Refinery” Brod and “Oil Refinery” Modrica, are conducting business. Affiliated companies of the Nestro Group are: Nestro Dunav and Nestro Petrol Serbia, both in Belgrade; and Nestro Adria and Nestro Adria Slavonski Brod in Zagreb.

In Macedonia, OKTA is the only oil refinery. It is situated outside the capital city of Skopje. The company was acquired in 1999 by the well-known Greek oil Company Hellenic Petroleum. With an annual capacity of 4 million tonnes, OKTA is well able to meet Macedonia’s own need for 1.25 million tonnes of refined products per annum. The oil is supplied to neighbouring areas such as Kosovo*.

Makpetrol JSC is the largest private company for distribution and sale of oil

04 Oil & Gas

05The ‘South Stream’ project By Veton QokuAssociate, Karanović & Nikolić

—40

at risk because of on-going gas disputes between Moscow and Kiev (bearing in mind that Europe gets 80% of its imported gas from Russia, through Ukraine), both the European countries and Russia are looking for new routes to get the gas from point A (gas sources in Russia, the Caspian Sea and the Middle East regions) to point B (European countries). An obvious solution as a new route is the Balkan region. Russia, as the world’s biggest gas producer, and the European Union, as one of the world’s largest importers of natural gas, agree up to this point, but they have very different ideas when it comes to which gas should pass through this new route. Namely, while Russia wants to continue its domination in the European energy market, the EU wants to reduce European dependence on Russian energy. Therefore, these two powers have planned two different gas pipeline projects that are intended to pass through the Balkan region.

Experts share the opinion that in the medium to long term, the demand for gas in the European Union as well as in other European countries that are not members of the European Union will grow significantly. Countries that used to consume moderate amounts of gas for industrial purposes are likely to guide their economies towards increased utilization, as coal, fuel oil and nuclear power are less environmentally-friendly and more expensive if compared to natural gas. According to the consensus forecast by the world’s leading forecast centres, Europe’s annual demand for additional gas imports (on top of the current 420 billion cubic meters) may increase by an additional 80 billion cubic meters by 2020 and surpass this figure by another 60 to 140 billion cubic meters by 2030.

However, at a time when natural gas is gaining momentum in the race for energy resources, the supply of gas to Europe is constantly

—42

Operator, as well as (x) MVM Group, the largest Hungarian energy company. The South Stream is expected to be operational by 2015.

However, the initial plan has substantially changed and now the South Stream pipeline route is planned to pass through Russia through the Black Sea to Bulgaria, Serbia, Hungary and Slovenia The pipeline is now planned to end at Tarvisio, Italy, instead of Austria. Moreover, two cul-de-sac branches are envisaged to be built in order to provide connection of Bosnia and Croatia to the pipeline.

Although it is not yet officially included in the project publically available documents, a cul-de-sac branch could also be built in order to connect Macedonia to the pipeline. In this respect, according to Macedonian vice-prime minister’s statement the agreement for the joining of Macedonia to the South Stream pipeline is the final stages, i.e. such agreement is soon expected to be ratified by the Russian side, and thereafter by the Macedonian side.

continue through Hungary to Austria ending at the Baumgarten gas hub. Another branch would run through Hungary and Slovenia to Arnoldstein in Austria near the Italian border to supply northern Italy. An option to re-route this branch through Croatia instead of Hungary was also being considered. This proposed gas pipeline will exclusively transport Russian natural gas. The South Stream pipeline was projected and will be implemented by the following companies in the energy sector: (i) the Russian (government controlled) energy giant Gazprom, (ii) the Italian Eni, (iii) the French EDF, also government controlled, (iv) the largest crude oil and natural gas producer in Germany, Wintershall AG, (v) Bulgarian Energy Holding EAD, (vi) state-owned natural gas provider in Serbia, Srbijagas, (vii) Austrian based OMV, (viii) Plinovodi, the Slovenian company managing the national natural gas transmission network, (ix) Greek DESFA, the Greek National Natural Gas System

The European Union, as a major player on the international gas market, is planning to build the Nabucco-West pipeline. This 3,300 kilometres long pipeline will run from Turkey via Bulgaria, Romania, and Hungary to the Baumgarten gas hub in Austria. Nabucco-West will have gas from Iraq, Azerbaijan, Turkmenistan, and possibly Egypt passing through it. Six companies (Austrian OMV, Hungarian MOL, Romanian Transgaz, Bulgarian Bulgargaz, Turkish BOTAŞ and German RWE) have teamed up for the purpose of its successful realization. If built, the Nabucco-West pipeline is expected to be operational by 2017.

Russia on the other hand is planning to build the South Stream pipeline. This pipeline is planned to pass from Russia through the Black Sea to Bulgaria. The initial plan was that from there, the south-western route would continue through Greece and the Ionian Sea to southern Italy, while the north-western pipeline would run from Bulgaria to Serbia. From there one branch would

one (1) is in Russia, three (3) are in Bulgaria, two (2) are in Serbia, one (1) is in Hungary and two (2) in Slovenia.Moreover, at least two gas storage facilities are planned to be constructed as part of the pipeline project, out of which one would be an underground storage facility in Hungary with a capacity of 1 billion cubic metres and the other in Banatski Dvor in Serbia with a capacity of 3.2 billion cubic metres.It is estimated that the offshore section of the pipeline would cost approximately EUR 10 billion, while the onshore pipeline along with the eight new compressor stations and the two gas storage facilities which are planned to be constructed are expected to cost around EUR 6 billion. Thus the entire project is envisaged to cost approximately EUR 16 billion.

The offshore part of the pipeline is routed through the exclusive economic zones of Russia, Turkey and Bulgaria in the Black Sea, in order to avoid the exclusive economic zone of Ukraine, due to on-going Russia–Ukraine gas disputes. The offshore section (which will be around 900 kilometres long) will run from the Russkaya compressor station in Russia through the Black Sea to Bulgaria’s city of Varna.The South Stream pipeline’s planned annual capacity is up to 63 billion cubic meters per annum. The total length of the pipeline is planned to amount to approximately 2,380 km and the pipeline is planned to have 9 (nine) compressor stations (if we include the existing Russkaya compressor station as part of the pipeline), out of which

It should also be mentioned that Montenegro is interested in a connection to the said pipeline. In that sense, the Montenegrin Government and Gazprom have launched a feasibility study, in order to determine whether Montenegro could be included in the South Stream gas pipeline project.

Furthermore, having in mind the fact that the south-western route of the South Stream pipeline does not appear in the publically available official documentation for the project, it seems that the pipeline will definitively bypass Greece and Southern Italy. According to some reports, Gazprom will continue supplying gas to Greece using the existing pipeline system due to the fact that demand in Greece and Southern Italy markets cannot cover the cost of the investment.

05 Oil & Gas

RU

UAMO

RO

BG

TR

GRMK

SR

MN

BH

HRSL

HUAU

SV

IT

CH

DE

AL

SOUTH STREAMPIPELINE ROUTE OPTIONS

PIPELINE BRANCHES

RUSSIA-BULGARIA-SERBIA-HUNGARY-SLOVENIA-ITALY

TO CROTIA FROM SERBIATO REPUBLIC OF SRPSKA FROM SERBIA

sure more will follow by the end of the year (the interview took place on 27 December 2012, a/n). The projects deal with both electricity and natural gas, perhaps one or two will have to do with oil.One of the very interesting actions that will be taken not only within the Energy Community, but the entire EU, is streamlining permit granting procedures for energy infrastructure projects of common interest. This measure aims at reducing the duration of, at times, very lengthy permit granting procedures, which in some instances have resulted in project failure. This new measure, which I hope the parties to the Energy Community will adopt before the end of 2013, is a particularly important challenge for me, because spatial planning had long been my area of work. I will strive for the Energy Community to outdo the European Union in this regard.

South East Europe, Moldova and Ukraine. This will be the focus of mag. Kopač’s activi-ties in his new role, but the focus of this interview was the future development of the regional energy industry.

How would you describe the regional energy industry today?— The regional energy

industry has still not been integrated to a sufficient degree, so it is still not regional enough. This is why in 2012 the Energy Community adopted a regional strategy, and will prepare a concrete set of project of regional importance in 2013 to put this strategy to practice. This is scheduled to take place in the October meeting of the Ministerial Council of the Energy Community. In the process, we will use the methodology also employed by the EU. About 70 proposals for such projects had already been submitted by Christmas, and I am

—44

When South Stream complies with the principles of the Third EU Energy Package in all the countries it crosses, it will make a most welcome project

By Mag. Janez KopačDate: January 14th 2013 Author: Alenka Žumbar Source: www.energetika.net/see

1 December 2012 marked the beginning for mag. Janez Kopač’s appointment as the Director of the Energy Com-munity Secretariat, after he had earlier been in charge of the Slovenian energy industry as the energy minister in the governments led by dr. Janez Drnovšek and Anton Rop, and later during Prime Minister Pahor’s govern-ment as head of the Energy Directorate at the Slovenian Ministry of the Economy. The biggest challenge in his new position, Kopač says, is to take the past achievements of the Energy Community one step further. The main goals of this organisation are to achieve implementation of the Third Energy Package by 2015, and create a welcoming environment for energy in-vestments in the countries of

First successful market entries then trigger an avalanche. The Energy Community will do everything in its power to assist in the process. I am sure the concern about liberalisation in the region will gradually subside, and that countries in the region will follow the lead of the EU member states.

How do you see the development of the regional sector in South East Europe during your term of office over the coming three years? Traditionally, the energy industry is a rather “rigid” sector, but sudden changes now seem to be on the way.— True, there was not

much change over the last twenty years, but this was also a time of the decline of old mechanisms and strategic planning mechanisms. New systems which would include the market component have not been developed, and this is where the Secretariat sees its key mission.

In Serbia, people are very concerned how market opening will affect large industrial users, the closing of which could lead to a social catastrophe.— I can understand this

concern, but we can always address this concern by underlining positive experience from other countries, including, again, Slovenia. The Ruše nitrogen plant in Slovenia shut down after finding itself in the liberalised market, but as it turned out later on, its terribly dated technology would inevitably result in its closing down. On the other hand, producers of aluminium, glass, paper, steel, etc., handled the open market well. They are even calling on the government to open the gas market, where monopolistic long-term supply contracts are stifling competition from exporters. The ultimate protection against fear is the knowhow in energy trade, which users can most easily get from chambers of commerce and other similar institutions.

It is no secret that in a big part of the region energy prices are still far below market prices. How do you think this will change?Serbia, for instance, announced it would open its market to large consumers on 1 January 2013. — Yes, and the same holds

true for Macedonia. There is bound to be some problems at first, just like in the EU member states, including Slovenia. As regards other countries in the region, we keep encouraging them to open their markets as soon as possible. On the other hand, I can understand the ministers who are concerned about liberalisation, saying it could affect the users who are already underprivileged. To help stakeholders take a stand in this dilemma, the Secretariat decided to try and make a definition of underprivileged users during the next Social Forum, which will take place in Belgrade in April 2013. On the other hand, it is ministers who should know that big energy investments are just impossible without market prices.

05 Oil & Gas

—46

according to its claims free of charge. But despite this argument, the fact is that refusal to pay for interconnection is a breach of the acquis communautaire, so EMS and Serbia are in the dock. If no agreement is reached in this matter in the near future, the Secretariat will propose further action by referring the matter to the Ministerial Council. This is not the same as a decision by the European Court, as the Energy Community has no real court, but it would by no means be very unpleasant for a contracting party to the Energy Community if the existence of a breach was established.

In addition to this dispute, there is another one that is close to being referred to the Ministerial Council: a gas dispute in Bosnia and Herzegovina. The problem is that the national regulator only has power for the electricity sector, not the gas sector. As a result, the gas sector remains unresolved and in the domain of the entities, with Republika Srpska

Another good example of cooperation was the adoption of the regional energy strategy in 2012.

The Secretariat has the power not only to persuade, but also to resolve disputes, correct?— Correct. The Secretariat

is actually servicing the judicial function of the Energy Community. This function is not very clearly defined, but still envisages certain steps in settling disputes between contracting parties to the Community or their energy companies. Currently, the biggest issue is the dispute between the Kosovo* transmission system operator KOSTT and the Serbian operator Elektromreža Srbije (EMS), which refuses to pay transit fees for cross-border electricity transmission. EMS justifies this by taking care of secondary and tertiary regulation,

In his last interview for Energetika.NET, your predecessor said that countries in the region had learned to work together. Can you give a good practice example of such cooperation in the energy industry?

— Without doubt, the Energy Community itself is an example of good practice, bringing together ministers once a year, and other officials from the contracting parties up to four times a year, to meet and harmonize their energy policies, as of 2013 also projects. The latest regional project is the Central Auction Office (CAO), which was set up by transmission system operators for electricity (including Eles from Slovenia, a/n) in Macedonia. Unfortunately, Serbia and Bulgaria have not yet joined CAO, but we hope they can be persuaded to do so. The Energy Community Secretariat will work on this.

Energy Packages in a country that is actually like a miniature version of the world is a very positive thing. If Ukraine implements all the required rules in its energy market, it will be very effective not only inside its borders, but also on the outside. And this is what matters to the entire Energy Community, or even the entire Europe. In cooperation with the Energy Community Secretariat, Ukraine has so far put forward a draft law that regulates the electricity market and is fully in line with the Second and even the Third Energy Package. They now have a new government, so adoption of this legislation will be delayed by a couple of months, but I hope it will proceed as planned.

I should also mention Ukraine’s determined efforts in improving energy efficiency.

One of the full members, and thus an observer of the regional energy cooperation as practiced under the Secretariat, is Ukraine, the country which to some extent is “responsible” for the South Stream project and which the Russian gas supplier wants to avoid on its way to Europe. What can a country like Ukraine, which is relatively far from South East Europe, learn from these procedures and what contribution can it make as a contracting party?— Talks for full membership

of Ukraine in the Energy Community were actually more a matter of the European Union than they were of the Community. But the EU had a larger scope of issues that the Community would have had, which is why the process of Ukraine’s accession to the Energy Community took slightly more time. But to answer your question: we have to know that due to its size, Ukraine can develop a well functioning market even without outside connections. I am convinced the adoption of the Second and Third

insisting on keeping the sector on the entity level, while the Federation of Bosnia and Herzegovina wants to move it to the national level, which would be the right thing to do. All things considered, Bosnia and Herzegovina failed to regulate the field in line with the Second EU Energy Package.

How do you expect Croatia’s accession to the EU to be reflected in the energy industry?— Croatia more or less

functions as if it was already part of the EU, because it has already opened its energy market. In practice, there are still certain restrictions, but these are teething troubles. I believe that in the future, Croatia will strengthen its cooperation with its neighbours, and I remain absolutely optimistic as regards the development of its energy industry.

05 Oil & Gas

—48

Do you think electricity generated from gas will account for a bigger share in the regional energy mix in the future? How could this affect energy prices?— This depends not only on

future projects, but also on consumption trends with current users. The crisis has led to a decline in consumption and its volatility in South East Europe as well as the rest of the continent. So all of a sudden, we have surplus gas, the price of which on the spot market has dropped, and this is not a positive price signal for those who invest in large facilities. The truth is, I cannot give a very specific answer to this question.

For my last question, what could you say about the Slovenian energy industry, which you had been in charge of not that long ago, looking at it now “from outside”?— Unfortunately, the

Slovenian energy policy is not keeping pace with the energy reality in the EU. The Third Energy Package has not been transposed into the Slovenian legislation yet, even though my

to observe the principles of the Second and Third EU Energy Packages. Therefore, the rules are the same for everyone, Serbia or Slovenia.

Speaking of South Stream; how do you think South East Europe will benefit from the project? As we know, Serbia is very optimistic about it, Croatia did not want to be left out...— Any additional energy

route and energy source is good in terms of improving supply and increasing competition. On the other hand, no project should entirely wipe out its competitors. With any such project, you always have to balance two opposing public interests, security of supply on the one hand and best possible competition on the other. Here, the rules of the Third Energy Package play a decisive role. When South Stream complies with the principles of this Package, it will undoubtedly be a most welcome project.

Nowadays, its dependence on Russian energy is a terrible strain for the citizens, who used to pay for the country’s wasteful use of energy with lower living standards.

As regards South Stream, which you brought up, Ukraine is the one voicing concern at non-compliance of some intergovernmental agreements between the Russian Federation and the countries along the proposed route of the future pipeline with the Second and Third EU Energy Packages. Naturally, the Secretariat is well aware of this, and chances are the Energy Community will have to address this issue in terms of its judicial power.

Does EU membership make any difference for the countries that have signed an agreement with Gazprom on constructing the South Stream pipeline?— No, this plays to role,

because countries that are not EU member states, but are members of the Energy Community, have also obliged themselves

behind the Slovenian energy policy. On top of this, the second biggest driving force in its energy industry is Unit 6 of the Šoštanj thermal power plant. All things considered, the regulator should play a more important role in Slovenia’s energy industry, just like this is the case anywhere else in Europe. But as Slovenia has not yet transposed the Third Energy Package in its national law, this is not the case. As a result, the Slovenian energy industry is still under too much influence from top executives approved by the ruling parties, and trade unions.

former team had drafted the required law, and attached to it a broader ambition which included spatial planning. Sadly, my successor rejected the draft as it had my name on it. Something similar happened to our energy strategy, which we had more or less completed after years of work and which included, for the first time, final sites for energy infrastructure based on a comprehensive environmental impact assessment. In short, I would say the competent ministry is more occupied with itself than with what it should be doing. To many, the borders of Slovenia are the limits of the entire universe. This self-absorption is the principal driving force

05 Oil & Gas

renew

renew

/Electricity & Renewables — Energy 2013, Karanović & Nikolić

/Electricity & Renewables — Energy 2013, Karanović & Nikolić

06Regulatory Framework and EU HarmonisationBy Jadranka Jerković, Ivana Vragović, Petar Mitrović, Veton QokuAssociates, Karanović & Nikolić and Josip Marohnić Attorney at Law/Odvjetnik in association with Karanović & Nikolić

—54

electricity sector – licensing requirements, supply, distribution and transmission. The majority of secondary regulations that are necessary for the full implementation of the 2011 Energy Law have not yet been issued, leaving the electricity sector in a transitional phase. Until this happens, the old regulations issued on the basis of the 2004 Energy Law will remain in force.

The Energy Law is almost entirely in line with the Second Energy Package (although in Serbia the regulator cannot impose fines for a breach as only the courts are authorised to do so). It provides for the full liberalization of electricity market by 1 January 2015, when households will be authorized to choose their supplier. It is expected that the liberalization of the market will finally lead to the increased participation of private companies in the sector of supply.

The members of the Energy Community, all undertook to implement the EU acquis on energy into their respective national legislation. In line with the requirements of the Energy Community Treaty, the national legislation of such member countries is largely based on the EU Second Energy Package. The exception being Croatia, shortly due to join the EU, who have gone a step further and implemented the EU’s Third Energy Package.

SerbiaThe regulatory framework for the electricity sector is primarily set out by the 2011 Energy Law. The 2011 Energy Law is an umbrella law which provides the general rules governing the conduct of all energy activities in Serbia, including in the electricity sector.

The general rules prescribed by the law are further elaborated by a number of bylaws, governing separate areas within the

the electricity energy market by 1 January 2015. Currently only companies with large industrial capacities that are connected directly to the grid of the transmission system operator are eligible to choose their electricity supplier. Starting from 1 July 2013 approximately 140 middle sized companies will be able to purchase electricity at market prices from their chosen supplier, while starting from 1 January 2015 all households will also be authorized to choose their own supplier.

The Energy Law is entirely in line with the Second Energy Package. As detailed above, under 2.1. Regulatory framework and EU harmonization, by 1 January 2015 the Macedonian Government plans to adopt the Third Energy Package of the European Union by proposing to the Macedonian Parliament to enact a new law on energy along with new respective energy related bylaws which would be compliant with the Third Energy Package.

— The Energy Agency is an independent regulatory body that decides on the issuance of licences, tariff methodologies and regulated tariffs. Under the 2011 Energy Law the Energy Agency in place of the Government will be authorized to approve the prices of electricity for tariff consumers.

MacedoniaAs previously mentioned, the general energy sector law that regulates the energy industry and market in the Republic of Macedonia is the Energy Law. As stated above under 2.1. Regulatory framework and EU harmonization, the Energy Law takes the form of an “umbrella” law, i.e. it law covers all significant areas, amongst others electricity, renewable energy sources, as well as the regulation of the respective markets, licensing requirements, supply, distribution and the transmission of electricity. The Energy Law introduces a new regulatory framework aimed at opening up the energy market by allowing the new entry of competitors and the full liberalization of