Hang Seng Bank Limited - 2006 Annual Report - HSBC Group

204

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of Hang Seng Bank Limited - 2006 Annual Report - HSBC Group

������ ���� ���

����

����

���

��� �

����������� ����

���� ���

����

#

��

$

#��

�!��

�

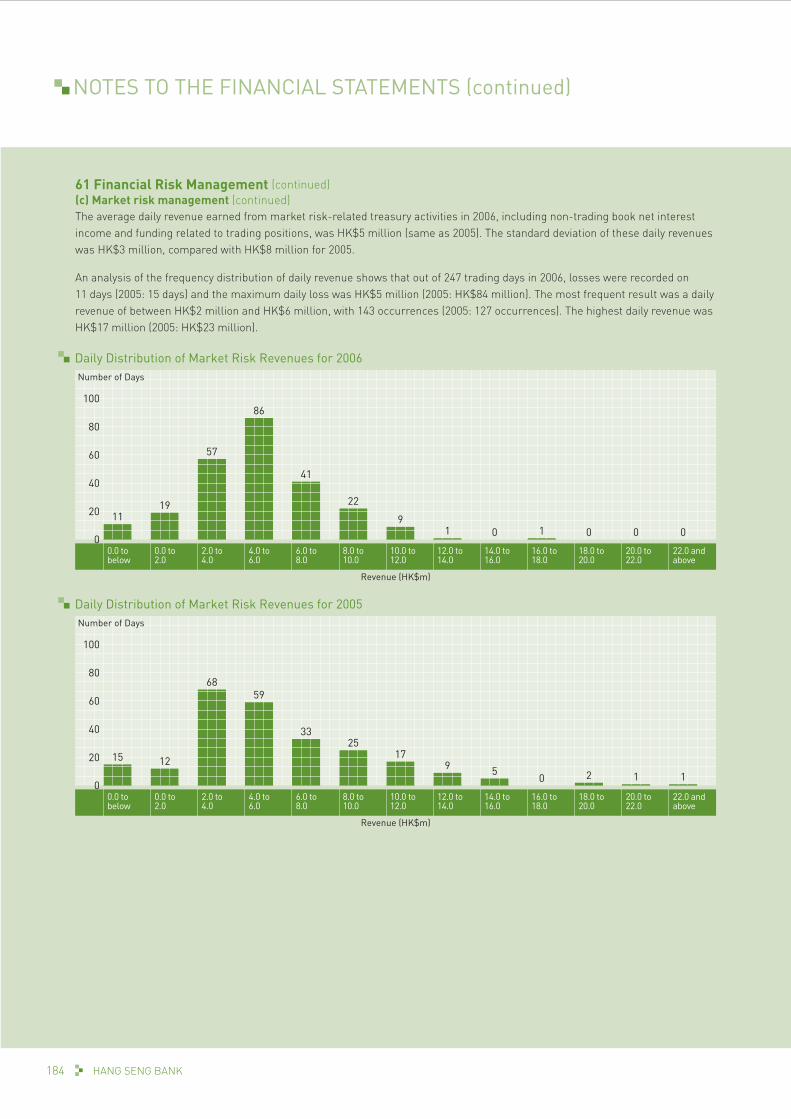

���$�� ����� ���� ������ ��� ���������� ������ ��� ��� ������ !��� "��� #��������$ ����%�� &�� �#�����#�%

'� ���������� �� �������� �� � ��� ��� &����#������������� �� (������ ������ ���� $��� )� ����*����� �� ��� +�� &�� ���)�� , ������� ��������# ����� ��

��%� �� *������ &��)�� %-

'��� $����� ����� ������ ���+� , .� �#���� , ��&��#���� ���������%�� $��+�# ����� � ��)�� � �������������� ����� �� �#�� ��� #���+�� ���#�������%-

���)��� &#����*����)���+���� �����%� ������+�+&����#��� ���%�#��� ��#������� %��� &�� �������� ����� #�����*���� �� �� #�++���$% �)��� #�������� ��� �����%�� �� ���#� ��) �������%

$'()*()+, $'-.'-/)* �-'012*

3 �*+42)+ 1( �-1*0

5 617*89*/- 61(/(:1/2 �4;;/-9

< �/='- �12*+)'(*+

>? �*:'@(1)1'(

>A $B/1-;/(C+ �)/)*;*()

>< $B1*0 �D*:4)17*C+ �*.'-)

,3 $'-.'-/)* �'7*-(/(:* /(E )B*- �(0'-;/)1'(

F< �4+1(*++ .*-/)1'(+

"������ �� ���� ����

"������ �� ��� /������

G, �/(@ �*(@ �(E*D*+

G3 $'-.'-/)* �*+.'(+1H121)9

3? 61(/(:1/2 �*71*I

5A �1'@-/.B1:/2 �*)/12+ '0 �1-*:)'-+

5< �1'@-/.B1:/2 �*)/12+ '0 �*(1'- �/(/@*;*()

<? �*.'-) '0 )B* �1-*:)'-+

<5 !""# 61(/(:1/2 �)/)*;*()+

>J5 �(E*.*(E*() �4E1)'-K+ �*.'-)

>J< �(/29+1+ '0 �B/-*B'2E*-+

>JJ �4H+1E1/-1*+

,?? $'-.'-/)* �(0'-;/)1'( /(E $/2*(E/-

CORPORATE PROFILE

Established in 1933, Hang Seng Bank is a world-class financial institution and one of Hong Kong’s largest listed companies in terms of market capitalisation (HK$203.2 billion as at the end of December 2006).

In Hong Kong, we serve over one-third of the population through around 150 branches and automated banking centres. Our mainland China network includes 16 outlets – seven branches (in Beijing, Dongguan, Fuzhou, Guangzhou, Nanjing, Shanghai and Shenzhen); eight sub-branches (one in Shenzhen, two in Guangzhou and five in Shanghai); and a representative office in Xiamen. We also have a branch in Macau and a representative office in Taipei.

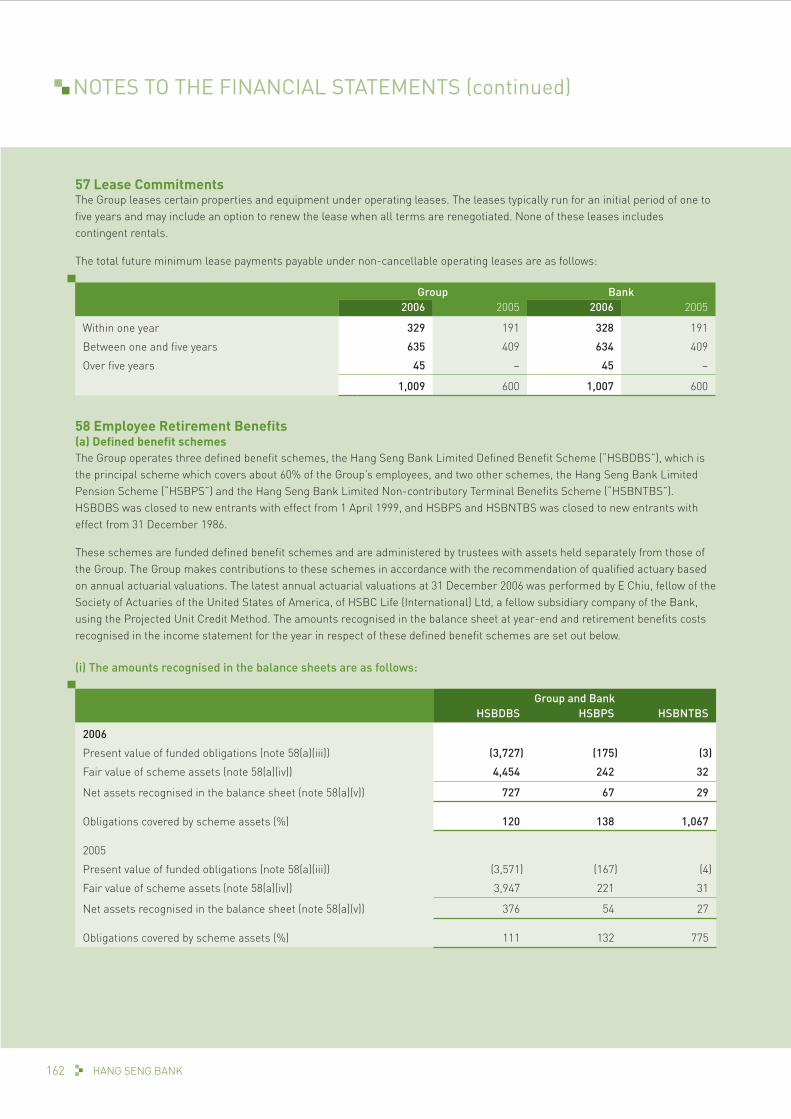

Hang Seng is a principal member of the HSBC Group, one of the world’s largest banking and financial services organisations.

A World-Class

BANK2 HANG SENG BANK2 HANG SENG BANK

EMPLOYEES

Our employees are our most valuable asset. That’s why we work hard to create an environment in which they are engaged and inspired. In turn, their professional, pragmatic and thoughtful approach to business helps us stand out from our competitors.

CUSTOMERS

As reflected in our corporate tagline ‘Managing wealth for you, with you’, helping customers plan for the future and achieve their financial goals lies at the heart of everything we do.

SHAREHOLDERS

We generate returns for our shareholders by achieving sustainable growth over the long term and enhancing our position as a leading financial institution in Greater China.

COMMUNITY

Our corporate responsibility programmes reflect our commitment to improving the well-being of the communities that help to create our success as well as promoting sustainable practices.

3ANNUAL REPORT 2006

4 HANG SENG BANK

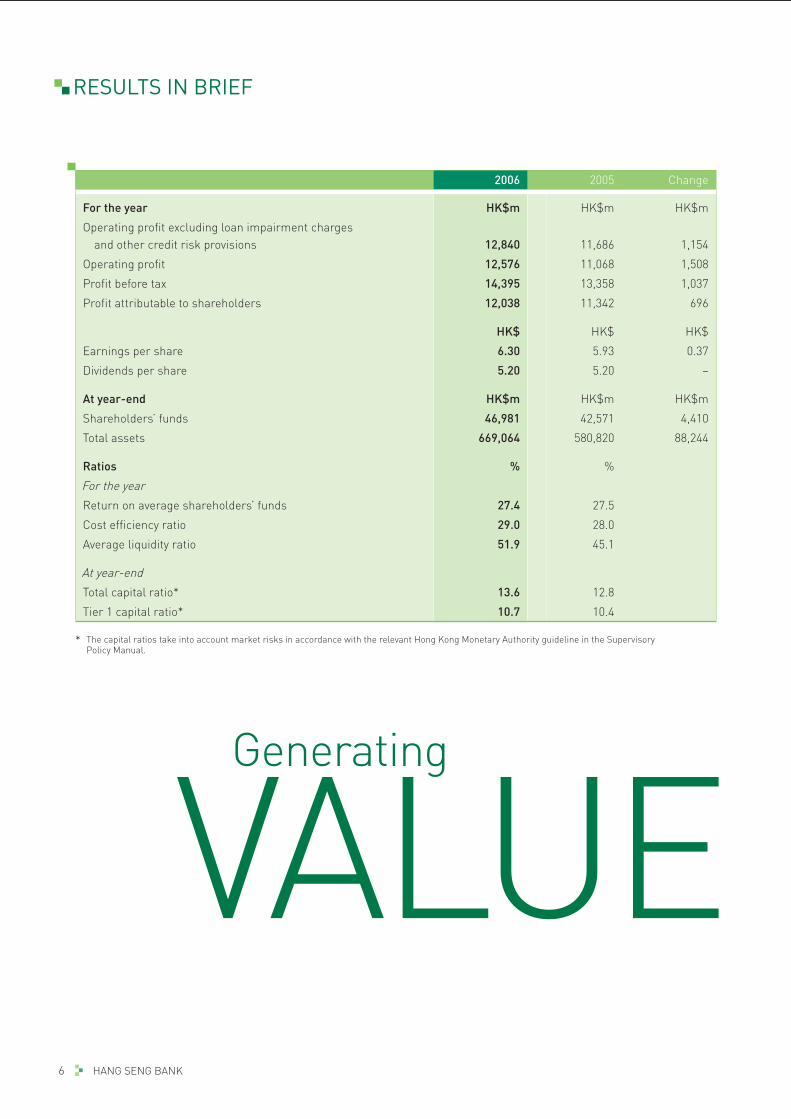

RESULTS IN BRIEF

5ANNUAL REPORT 2006

FIVE-YEAR FINANCIAL SUMMARY

DELIVERINGFocusing on our strategic plan for business success, we are increasing value for shareholders.

Results

6 HANG SENG BANK

RESULTS IN BRIEF

2006 2005 Change

For the year HK$m HK$m HK$m

Operating profit excluding loan impairment charges and other credit risk provisions 12,840 11,686 1,154

Operating profit 12,576 11,068 1,508

Profit before tax 14,395 13,358 1,037

Profit attributable to shareholders 12,038 11,342 696

HK$ HK$ HK$

Earnings per share 6.30 5.93 0.37

Dividends per share 5.20 5.20 –

At year-end HK$m HK$m HK$m

Shareholders’ funds 46,981 42,571 4,410

Total assets 669,064 580,820 88,244

Ratios % %

For the year

Return on average shareholders’ funds 27.4 27.5

Cost efficiency ratio 29.0 28.0

Average liquidity ratio 51.9 45.1

At year-end

Total capital ratio* 13.6 12.8

Tier 1 capital ratio* 10.7 10.4

* The capital ratios take into account market risks in accordance with the relevant Hong Kong Monetary Authority guideline in the SupervisoryPolicy Manual.

Generating

VALUE

7ANNUAL REPORT 2006

FIVE-YEAR FINANCIAL SUMMARY

Results

Attributable Profit

Operating Profit Shareholders’ Funds

Post-Tax return onAverage Shareholders’ Funds

Total Assets

Special Interim Dividend per Share

Earnings per Share

Dividends per Share

Total Assets andShareholders’ Funds

Per Share Earnings and Dividends

2

10

8

6

4

0

HK$

30

5

10

15

20

25

0

%

400

800

700

600

100

200

300

500

0

HK$bnHK$bn

02 0603 0504 02 0603 0504 02 0603 0504

14

12

10

2

4

6

8

0

2002 2003 2004 2005 2006

For the year HK$bn HK$bn HK$bn HK$bn HK$bn

Operating profit 10.7 10.7 12.6 11.1 12.6

Profit before tax 11.2 11.1 13.3 13.4 14.4

Profit attributable to shareholders 9.9 9.5 11.4 11.3 12.0

At year-end HK$bn HK$bn HK$bn HK$bn HK$bn

Shareholders’ funds 43.1 39.6 40.9 42.6 47.0

Issued and paid up capital 9.6 9.6 9.6 9.6 9.6

Total assets 474.7 503.0 546.9 580.8 669.1

Per share HK$ HK$ HK$ HK$ HK$

Earnings per share 5.19 4.99 5.94 5.93 6.30

Dividends per share 5.40# 4.90 5.20 5.20 5.20

Ratios % % % % %

Post-tax return on average shareholders’ funds 23.1 23.4 28.5 27.5 27.4

Post-tax return on average total assets 2.1 2.0 2.2 2.0 1.9

Capital ratios

– Total ratio* 14.2 13.2 12.0 12.8 13.6

– Tier 1 ratio* 11.9 11.3 10.8 10.4 10.7

Cost efficiency ratio 25.4 25.4 26.4 28.0 29.0

# Including special interim dividend of HK$0.50 per share for 2002.

* The capital ratios take into account market risks in accordance with the relevant Hong Kong Monetary Authority guideline in the SupervisoryPolicy Manual.

8 HANG SENG BANK

MAJOR MILESTONES

JanuaryHang Seng launches China Equity Fund.

FebruaryHang Seng introduces two new cards – alpha card, a payment card for young people, and a commercial card for members of the New Territories General Chamber of Commerce.

Hang Seng begins offering insurance agency service at its Shanghai and Shenzhen branches and sub-branches.

HSI Services announces that mainland China H-share companies are eligible for inclusion in Hang Seng Index.

MarchHang Seng introduces Index-linked Capital Protected Investment product on the Mainland.

AprilHang Seng launches 24-hour Personal Loan application hotline.

MayHang Seng launches integrated brand revitalisation programme and introduces new corporate tagline –‘Managing wealth for you, with you’.

Hang Seng sells its property at 77 Des Voeux Road Central for HK$2.26 billion.

Hang Seng signs an agreement with Kerry Properties to lease 262,000 square feet of office space in Enterprise Square Five in Kowloon Bay, with occupancy planned for late 2007.

Hang Seng opens fourth Shanghai sub-branch.

Hang Seng launches VISA Infinite, an invitation-only prestige credit card.

Hang Seng extends Mainland insurance agency service to Guangzhou branch.

Hang Seng announces first interim dividend of HK$1.10 per share.

JuneHang Seng announces its debut US dollar subordinated notes offering amounting to US$450 million.

Hang Seng opens Business Banking Centre in Chai Wan to further expand network of outlets serving SMEs.

Hang Seng receives approval to provide RMB services and extend foreign currency services at Nanjing branch.

9ANNUAL REPORT 2006

JulyHang Seng introduces MediCash Lifetime Insurance Plan.

Hang Seng announces second interim dividend of HK$1.10 per share.

AugustHang Seng opens first Guangzhou sub-branch.

Hang Seng extends Mainland insurance agency service to Beijing branch.

SeptemberHang Seng relocates Macau branch to accommodate expansion of services and new Prestige Banking Centre.

Hang Seng receives approval for Qualified Domestic Institutional Investor (QDII) licence.

Hang Seng holds Board of Directors meeting on the Mainland for the first time.

Hang Seng opens fifth Shanghai sub-branch.

First H-share company enters Hang Seng Index.

OctoberHang Seng receives approval for US$300 million foreign exchange conversion quota under QDII licence.

Hang Seng becomes first foreign bank to open a branch in Dongguan.

NovemberHang Seng announces third interim dividend of HK$1.10 per share.

HSI Services launches Hang Seng China H-Financials Index to track performance of Mainland financial companies listed in Hong Kong.

DecemberHang Seng launches its first QDII investment product through Mainland branches and sub-branches.

Hang Seng becomes first bank to offer Octopus merchant services to retailers.

Hang Seng receives approval to prepare for the establishment of Mainland subsidiary bank.

10 HANG SENG BANK

RECOGNITION

2006 Awards

Best Retail Bank in Asia, Best Retail Bank in Hong Kong and Excellence in Wealth Management Awards, The Asian Banker.

Best Domestic Bank in Hong Kong, The Asset.

No. 1 for Financial Soundness and No. 7 Overall in Hong Kong category, Wall Street Journal Asia, 200 Most Admired Companies survey.

Trusted Brands Gold Awards in the Banking and Investment Funds categories, Reader’s Digest, Trusted Brands Awards.

Best Wealth Management Bank and No. 2 for Overall Competitiveness, 21st Century Business Herald, Asian Banks Competition.

Best Banking Service Award, Hong Kong Chamber of Small and Medium Business.

Highly Commended in Best Overall Investor Relations at a Hong Kong Company (large cap), Best Annual Report and Other Corporate Literature, and Best Corporate Governance categories, IR Magazine, Hong Kong & Taiwan Awards.

No. 85 in Top 100 Financial Institution Brands Worldwide and Brand Rating of A, The Banker.

290th Largest Listed Company in the World in terms of Market Capitalisation, Financial Times, FT Global 500.

No. 2 Local Cash Management Bank (Small Corporations) and No. 2 Local Cash Management Bank (Medium-sized Corporations), Asiamoney.

Green Enterprise of the Year, Federation of Hong Kong Industries.

Gold Award in the Community Relations category, China International Public Relations Association, China Golden Awards for Excellence in Public Relations.

Caring Company, Hong Kong Council of Social Service.

Bronze Award and Certificate of Excellence, Hong Kong Management Association, Awards for Excellence in Training.

China Top 10 Growing Financial Organisation (Hang Seng Shanghai Branch), China Council for the Promotion of International Trade and the Shanghai Committee of the Chinese People’s Political Consultative Conference, China International Financial Forum.

Silver Award for Photography, Bronze Award for Cover Design/Photo and Honors Award for Interior Design (Hang Seng 2005 Annual Report), International ARC Awards Competition.

Bronze Award, Hong Kong Management Association, Best Annual Reports Awards.

11ANNUAL REPORT 2006

Moody’s Investors Service

Short-term foreign currency deposit rating Prime 1

Short-term local currency deposit rating Prime 1

Long-term foreign currency deposit rating Aa3

Long-term local currency deposit rating Aa2

Bank financial strength rating B+

Local currency subordinated debt rating Aa3

US$450 million subordinated debt issue in June 2006 Aa3

A.M. Best

Hang Seng Insurance Co. Ltd – financial strength rating A+ (Superior)

Hang Seng Insurance Co. Ltd – solicited issuer credit rating aa-

Hang Seng Life Ltd –financial strength rating A+ (Superior)

Fitch

Bank individual rating A/B

Ratings

Standard and Poor’s

Short-term local currency counterparty rating A-1+

Short-term foreign currency counterparty rating A-1+

Long-term local currency corporate credit rating AA

Long-term foreign currency corporate credit rating AA

Bank fundamental strength rating B+

US$450 million subordinated debt issue in June 2006 A+

Hang Seng Insurance Co. Ltd – insurer financial strength A+

Hang Seng Insurance Co. Ltd – counterparty credit rating A+

Hang Seng Life Ltd – insurer financial strength A+

Hang Seng Life Ltd – counterparty credit rating A+

12 HANG SENG BANK

CHAIRMAN’S STATEMENT

LEADING“Hang Seng will continue to drive its business forward, flying the flag for premium customer service, sustainable growth and increasing value for shareholders.”

for Growth

13ANNUAL REPORT 2006

Mr Michael SmithChairman

14 HANG SENG BANK

CHAIRMAN’S STATEMENT

A sharp focus on our vision for long-term business growth along with good economic conditions helped Hang Seng achieve positive results in 2006.

Our personal wealth management business recorded significant rises in income from investment services, insurance and Private Banking. Commercial Banking performed strongly, underpinned by increases in customer advances and the development of corporate wealth management services. Additional investments in our mainland China operations yielded encouraging growth.

Operating profit rose by 13.6 per cent to HK$12,576 million, reflecting good growth of primary business drivers as well as a drop in loan impairment allowances. Operating profit excluding loan impairment charges and other credit risk provisions grew by 9.9 per cent to HK$12,840 million.

Attributable profit increased 6.1 per cent to a record HK$12,038 million. Earnings per share were up 6.2 per cent at HK$6.30.

The Directors have announced a fourth interim dividend of HK$1.90 per share. In light of capital requirements for future business expansion, particularly on the Mainland, total distribution for 2006 is HK$5.20 per share, the same as in 2005.

Operating expenses increased by 15.3 per cent to HK$5,241 million with further investments in human resources, IT, marketing and branding to support business growth in Hong Kong and on the Mainland.

Our return on average shareholders’ funds was 27.4 per cent.

Our total capital ratio was 13.6 per cent at year-end, up 0.8 percentage point compared with 31 December 2005. Our tier 1 ratio was up 0.3 percentage point at 10.7 per cent.

Personal Financial Services’ operating profit excluding loan impairment charges grew by 5.4 per cent to HK$7,840 million. Wealth management income was up 22.7 per cent at HK$4,281 million, reflecting record investment product sales, a high level of stock market activity and a 17.5 per cent rise in life insurance income. We also benefited from high levels of consumer confidence, recording increases in our credit card base and cardholder spending as well as in personal lending.

Commercial Banking’s operating profit excluding loan impairment charges rose 21.5 per cent to HK$2,001 million. Customer

advances grew by 22.2 per cent with trade finance gaining market share. Lending to the manufacturing industry and wholesale and retail sector outpaced the market average as a result of refined segmentation and deepened relationships.

Intensified marketing saw a 34.7 per cent increase in the number of new small and medium-sized enterprise accounts acquired in the second half of 2006 compared with the first half. Good progress with corporate wealth management services and card acquiring business underpinned growth in net fees and commissions and net trading income.

With keen competition continuing to put pressure on lending margins, Corporate Banking focused on asset yield. We further diversified our customer base, grew deposits by 32.5 per cent and took advantage of cross-selling opportunities. The strong growth of our targeted business segments helped to compensate for the decline in operating profit before loan impairment charges from lending to large corporates. Net operating income increased by 11.8 per cent. Net operating income excluding loan impairment charges rose 2.3 per cent. Operating profit excluding loan

15ANNUAL REPORT 2006

in market segments with high growth potential and growing our Mainland business more rapidly.

We have taken significant strides in the past year, but there is still much to do. Focusing on our strategic plan for growth, Hang Seng will continue to drive its business forward, flying the flag for premium customer service, sustainable growth and increasing value for shareholders.

Michael SmithChairmanHong Kong, 5 March 2007

impairment charges was HK$543 million, down 2 per cent compared with 2005.

Treasury’s operating profit excluding loan impairment charges declined 25 per cent to HK$887 million. Efforts to expand proprietary trading and customer-driven business helped trading income grow by 66.1 per cent to HK$628 million. However, net interest income fell by HK$514 million, or 51.7 per cent, as the balance sheet management portfolio continued to be challenged by rising funding costs and flattened yield curves.

Our Mainland business recorded good growth in advances, deposits, customer base and profit contribution. Operating profit excluding loan impairment charges at our Mainland branches rose by 211.9 per cent. We upgraded a representative office to a branch and opened three new sub-branches during the year. In December, we were granted permission to begin preparations for the establishment of a Mainland subsidiary. Our subsidiary bank will be named Hang Seng Bank (China) Limited and will be headquartered in Shanghai.

To demonstrate our strong commitment to this exciting market, in September we held a Board of Directors’ meeting on the Mainland for the first time.

Our PeopleBusiness success relies on the teamwork and talents of our staff. We work to bring out the best in our employees and they continue to

exceed our expectations. In 2006, putting our roadmap for growth strategy into action and ensuring that our comprehensive brand strengthening programme moved full steam ahead were just two of the tasks enthusiastically embraced by staff at all levels. That Hang Seng remains a standard-bearer for superior customer service is a testament to their commitment and professionalism.

In recognition of this dedication to excellence, the Directors approved performance-related salary increases of up to 8.75 per cent, which took effect in January 2007.

I also wish to convey the Board’s thanks to our customers and shareholders for their continued support of Hang Seng and for providing both inspiration and incentive as we work to enhance our position as a leading financial institution in Greater China.

Moving AheadHong Kong is likely to experience above-trend growth in 2007. Economic uncertainty in the US generated by weaknesses in the housing market may result in a slowing of export and re-export trade activity. However, sustained economic momentum, the

stabilisation of interest rates and the improving labour market will continue to drive domestic demand. The positive economic outlook for the Mainland also augurs well.

Against this backdrop, we will build on the good momentum generated in 2006 by making greater use of our competitive advantages, further developing our core business areas, strengthening our service capabilities

Business success relies on the teamwork and talents of our staff. We work to bring out the best in our employees and they continue to exceed our expectations.

16 HANG SENG BANK

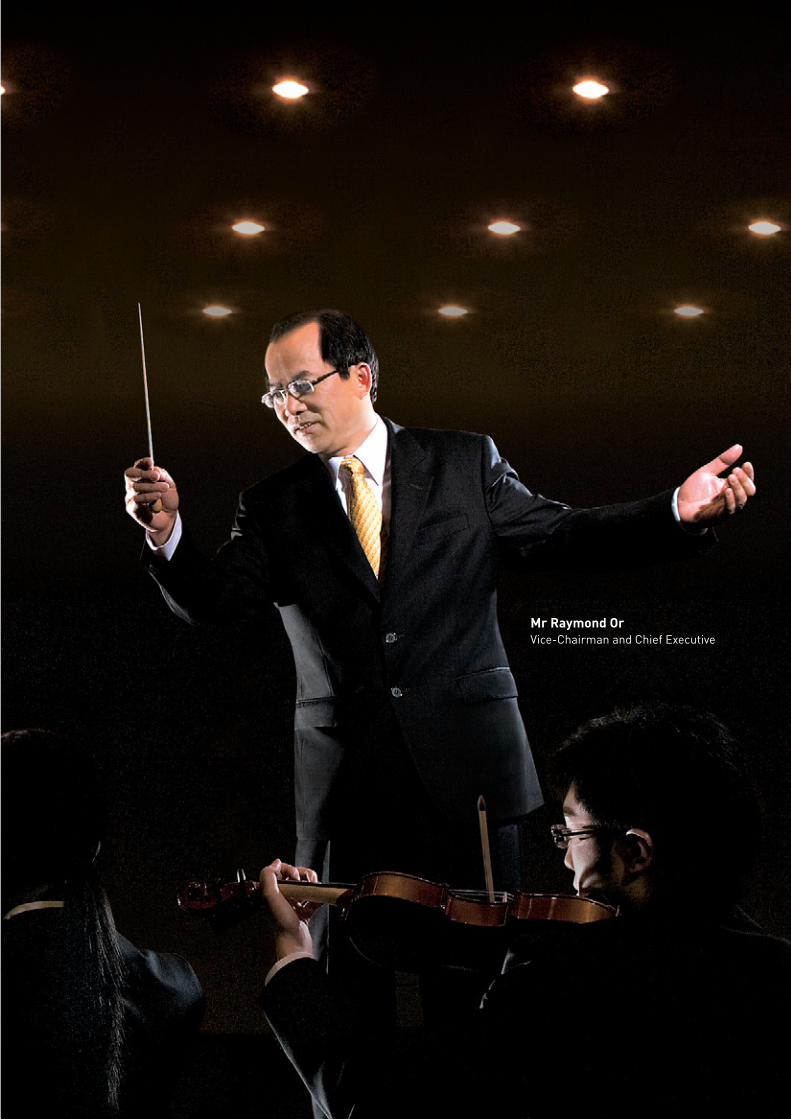

CHIEF EXECUTIVE’S REPORT

SUCCESS“No one person can perform a symphony – it takes the efforts of an entire orchestra.”

Conducting

17ANNUAL REPORT 2006

Mr Raymond OrVice-Chairman and Chief Executive

18 HANG SENG BANK

CHIEF EXECUTIVE’S REPORT

I am pleased to report that Hang Seng gave an upbeat performance in 2006.

During our 2005 results announcement, we set out our roadmap for growth – a strategic plan to help us achieve our vision for future business success. Our hard work over the past year to put this strategy into action has yielded encouraging results.

From Vision To ActionSupported by the buoyant economic environment, we grew wealth management income by 22.7 per cent by further harmonising our service and product offerings with the investment and insurance needs of our customers.

Our Private Banking business built on its good growth momentum to achieve a 46.3 per cent increase in pre-tax profit. Given the progress made in the past year, we are confident of achieving our roadmap goal of doubling Private Banking’s pre-tax profit by 2008, two years ahead of schedule.

We capitalised on strong consumer demand to expand higher-yield lending, recording significant rises of

46.4 per cent in personal loans and 22.1 per cent in card receivables. Cards in issue reached 1.4 million.

Continued fine-tuning of relationships with Commercial Banking customers, especially small and medium-sized enterprises (SMEs), drove growth in trade finance, net fees and commissions, and net trading income. We gained market share in lending to the manufacturing industry and the wholesale and retail sector. Commercial Banking’s contribution to total pre-tax profit was 16.4 per cent, up from 8.8 per cent in 2005, putting us on track to achieve our five-year target of 20 per cent.

We further diversified our Treasury income base and promoted closer cooperation with other customer groups. This led to a 66.1 per cent increase in trading income, helping to offset the adverse effects of rising funding costs and flattened yield curves on the balance sheet management portfolio.

We picked up the pace of expansion in mainland China. Our number of full-time equivalent staff increased

by 284 to reach 661. We became the first foreign bank to have a branch in Dongguan and opened three new sub-branches in key cities. Including a Guangzhou sub-branch opened early this year, we now have 16 outlets on the Mainland.

This expansion in service capabilities helped us achieve strong growth in Mainland deposits and advances, which rose by 51.1 per cent and 50.9 per cent respectively.

In the second half of 2006, we obtained a licence and foreign exchange conversion quota under the Qualified Domestic Institutional Investors scheme. We finished the year on a high note by receiving approval to begin preparations to establish a Mainland subsidiary bank.

We stepped up mutually beneficial cooperation with our strategic partner Industrial Bank in areas such as customer referrals, accelerated remittance services and secondment of staff. We also actively explored possibilities for working together to enhance note delivery, cash deposit and other services.

19ANNUAL REPORT 2006

Including our share of profits from Industrial Bank, our Mainland business contributed 6.1 per cent of total pre-tax profit, up from 4.5 per cent in 2005, bringing us closer to our objective of 10 per cent by 2010.

We embarked on an integrated brand revitalisation programme designed to enhance our brand equity.

Emphasizing our progressive, pragmatic and thoughtful approach to service, this programme is helping us strengthen partnerships with existing customers and build relationships with new ones.

In May, we further rationalised our property portfolio with the sale of 77 Des Voeux Road Central for HK$2.26 billion. We also signed an agreement to lease 262,000 square feet of office space in Enterprise Square Five in Kowloon Bay. With occupancy planned for late 2007, moving some of our back office functions to this new site will help enhance our operating and cost efficiency.

Financial HighlightsGood growth in our core businesses and improved credit conditions saw operating profit grow 13.6 per cent to HK$12,576 million. Operating profit excluding loan impairment

Attributable profit reached a new high of HK$12,038 million.

charges was HK$12,840 million, up 9.9 per cent.

Pre-tax profit rose 7.8 per cent to HK$14,395 million, affected by a significant drop in property revaluation gains. Attributable profit reached a new high of HK$12,038 million, an increase of 6.1 per cent compared with 2005.

Increases in lending and contribution from net free funds helped net interest income grow by 8.3 per cent to HK$11,694 million. Average interest-earning assets were up 10.6 per cent at HK$578.6 billion.

The ratio of non-interest income to net operating income excluding loan impairment charges rose to 35.3 per cent, up from 33.5 per cent a year earlier.

Net interest income rose by HK$898 million, or 8.3 per cent. The loan portfolio expanded by 7.2 per cent driven by growth in consumer finance, trade finance and Mainland lending, contributing HK$419 million. Spreads on best lending rate-based loans improved, although strong market competition continued to exert downward pressure on mortgage and corporate loan pricing. Net free funds

+13.6%

Operating Profit

20 HANG SENG BANK

CHIEF EXECUTIVE’S REPORT (continued)

and the debt securities portfolio of life insurance fund investments contributed HK$867 million and HK$264 million respectively to the rise in net interest income.

These increases more than offset the HK$514 million decline in net interest income from the Treasury balance sheet management portfolio and the fall of HK$138 million due to the narrowing of spreads on Hong Kong dollar savings accounts and the change in deposit mix from savings to structured deposits.

Benefiting from the active stock market and positive investor sentiment, investment services income grew by 29.6 per cent. We offered new investment funds to capture growth on the Mainland and in other emerging markets, achieving a 40.6 per cent rise in retail fund sales. Income from structured products grew by 48.1 per cent.

The introduction of new products, the recruitment of more relationship managers and a continued emphasis on personalised advice saw Private

We embarked on an integrated brand revitalisation programme designed to enhance our brand equity.

+22.7%

Wealth Management income

Net fee income grew by 18.3 per cent to HK$3,497 million. Securities-related income rose 63.3 per cent, reflecting increases in turnover, customer base and market share. Card services income was up 22 per cent at HK$860 million, driven by rises of 10.5 per cent in the number of cards in issue and 11.7 per cent in cardholder spending.

Trading income grew by HK$445 million to HK$1,330 million, attributable mainly to a 50.1 per cent growth in foreign exchange income on the back of increased customer activity and improved trading results.

Income from wealth management rose by HK$793 million to HK$4,281 million.

Banking’s investment services income rise by 83.5 per cent. Assets under management increased 39.6 per cent.

Life insurance income grew by 17.5 per cent to HK$1,476 million as we further tapped the high-potential retirement and medical insurance markets.

Operating expenses rose by HK$695 million, or 15.3 percent. We made investments in staff, IT, marketing and branding to better position our Hong Kong business for continued growth and better prepare our Mainland business to take greater advantage of the growing opportunities.

Our cost efficiency ratio rose1 percentage point to 29 per cent, but

21ANNUAL REPORT 2006

remains among the lowest in the banking industry.

Underpinned by a HK$2,992 million rise in retained profits and an increase in the available-for-sale investment reserves, shareholders’ funds (excluding proposed dividends) grew by HK$4,410 million to HK$43,348 million. Return on average shareholders’ funds was 27.4 per cent.

As at 31 December 2006, our total and tier 1 capital ratios stood at 13.6 per cent and 10.7 per cent respectively, up from 12.8 per cent and 10.4 per cent a year earlier.

Our average liquidity ratio for 2006 was 51.9 per cent, up from 45.1 per cent in 2005.

Increases in both lending and deposits saw total assets grow by 15.2 per cent to HK$669.1 billion. At year-end, our advances-to-deposits ratio was 51.7 per cent, compared with 54.4 per cent at the end of 2005.

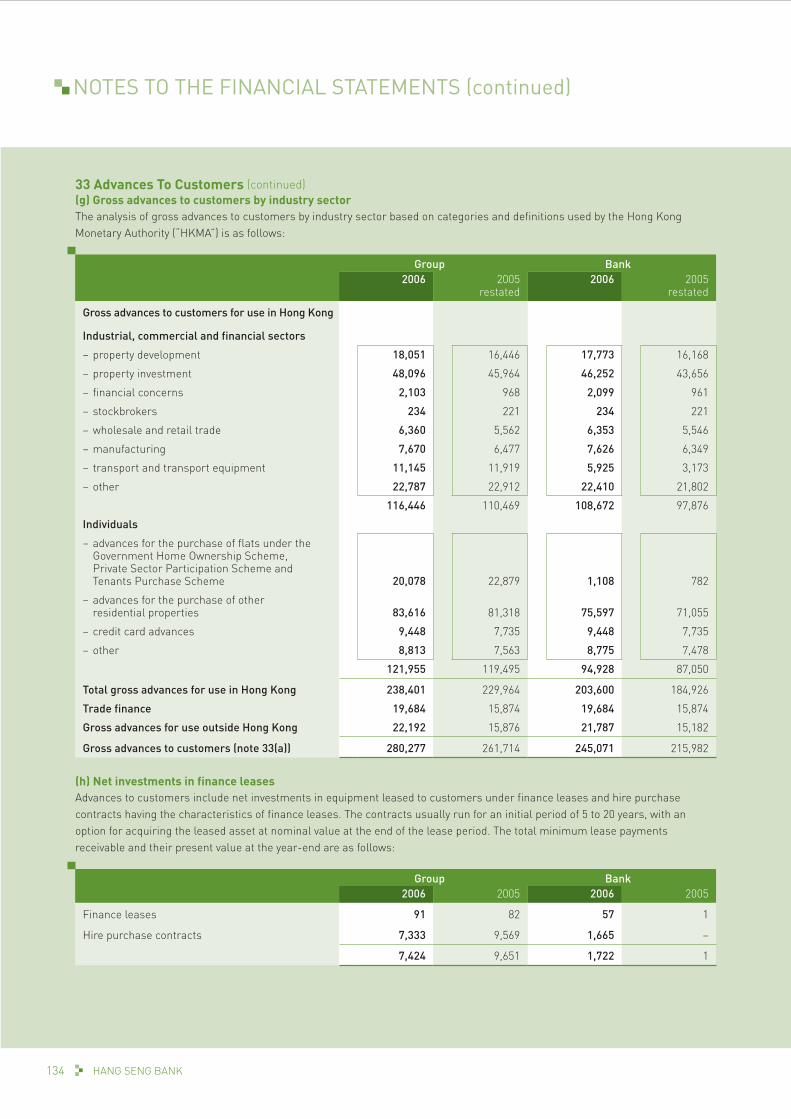

Gross advances to customers rose by 7.1 per cent to HK$280.3 billion.

The good investment climate helped us grow lending to the property

development sector by 9.8 per cent. Success with strengthening our Commercial Banking relationships was reflected in rises of 14.3 per cent and 18.4 per cent in lending to the wholesale and retail trade and the manufacturing sector respectively, as well as strong growth of 24 per cent in trade finance.

Lending to individuals rose 5.4 per cent (excluding the fall in Government Home Ownership Scheme mortgages) with improvement in the employment market underpinning demand. Strategic marketing, new credit card offerings and improved efficiency contributed to good growth in consumer finance. Our credit card business gained market share in terms of card base, spending and receivables.

Despite intense market competition, we increased residential mortgage lending by 5.9 per cent.

Loans for use outside Hong Kong increased by 39.8 per cent to HK$22,192 million, due largely to the 50.9 per cent rise in lending by our Mainland branches. Corporate lending on the Mainland enjoyed

good growth, driven by higher-margin RMB loans. Closer collaboration between our Mainland and Hong Kong teams led to a significant increase in Mainland trade finance.

At year-end, total loan impairment allowances as a percentage of gross advances to customers were 0.33 per cent, down from 0.39 per cent at the end of 2005. Gross impaired advances as a percentage of gross advances to customers were unchanged at 0.5 per cent.

Customer deposits, including certificates of deposit and other debt securities in issue, grew by 12.8 per cent. Hong Kong and US dollar savings accounts rose, reflecting a preference for liquidity in an active investment market. Additions to our range of structured products helped drive a 31.2 per cent increase in structured deposits, structured certificates of deposit and other debt securities in issue.

BrandingIn May 2006, we launched an integrated branding programme that covers advertising and key points of customer contact and is designed to establish us as the financial institution of choice for personal and commercial banking.

COMMERCIALStrong growth in

Banking

22 HANG SENG BANK

CHIEF EXECUTIVE’S REPORT (continued)

23ANNUAL REPORT 2006

The professionalism and dynamic attitude of our staff help define the Hang Seng spirit. When it comes to service, every member of our team is ready to jump into action to exceed ever-increasing customer expectations.

NEW HEIGHTSReaching

24 HANG SENG BANK

CHIEF EXECUTIVE’S REPORT (continued)

We launched a series of testimonial-style television commercials covering our SME, wealth management and insurance businesses. We also unveiled a fresh corporate look that uses a vibrant green to reflect our progressive and proactive attitude. All branches have adopted our new bulkhead and we are steadily rolling out our new branch design.

To engage all staff in the brand-building initiative, we have developed an internal branding framework comprising seven ‘Beliefs’ that ensure an excellent customer experience and strengthen our corporate value. In August we kicked-off ‘Live The Brand, Start With Me’, a Bank-wide communication and education campaign which is helping staff move from awareness to practical application of the seven ‘Beliefs’.

Focused On The FutureEfforts to reach our roadmap objectives are continuing to help us refine our business focus, putting us in a position to take better advantage of growth opportunities.

The economic outlook for the year ahead remains positive. Developments in the US housing sector may slow the pace of external trade, but increasing confidence in the local economy, the buoyant labour market and sustained growth on the Mainland should underpin domestic demand.

Supported by our revitalised brand, we are deepening relationships with existing customers and increasing our appeal among key customer groups.

Personal Financial Services will step up cross-selling efforts and expand

its customer base by leveraging its well-developed, all-weather portfolio of investment products. Private Banking’s growing service capabilities and open architecture will enable us to further tap the affluent customer segment by offering personalised financial solutions.

We have had notable success with our annuity and healthcare insurance plans and will continue to develop new products to complement our existing range.

We will capitalise on positive consumer sentiment to further grow personal lending.

On the Mainland, we will continue with our two-pronged approach of organic growth and close collaboration with Industrial Bank.

ExcellentCustomer

Experience

Engaged and Inspired Employee

Progressive Pragmatic Thoughtful

Cour

tesy

with

Pas

sion

Pro

fess

iona

lism

InnovationCorp

orat

e Re

spon

sibi

lity Execution Excellence

Corporate Governance

Our Seven ‘Beliefs’

25ANNUAL REPORT 2006

in the year ahead. We will work to identify more cross-selling opportunities and expand corporate treasury services. We will step up efforts to acquire new customers to grow our Corporate Banking deposit base.

We will further strengthen cooperation and communication between all customer groups.

No one person can perform a symphony – it takes the efforts of an entire orchestra. I am delighted to be working with a world-class ensemble whose members are in tune with each other and with our customers’ needs. Together we will continue to enhance our position as a leading financial institution in Greater China to the long-term benefit of our customers and shareholders.

Raymond OrVice-Chairman and Chief ExecutiveHong Kong, 5 March 2007

The establishment of our Mainland subsidiary bank, planned for the second quarter of this year, will mark a new phase of business expansion. We will take good advantage of the opportunities generated by the opening up of the retail RMB market and work to increase RMB deposits to support lending growth.

We will expand our Mainland customer base through setting up new outlets in high-growth areas,

I am delighted to be working with a world-class ensemble whose members are in tune with each other and with our customers’ needs.

By 2010, we aim to grow our Mainland business to more than 2,000 staff and over 50 outlets.

We will capitalise on our growing capabilities in southern China by offering a greater range of services to Commercial Banking customers with operations in Hong Kong and on the Mainland. Our closer partnerships with SME customers will help us grow trade finance and our corporate wealth management business.

increased marketing and more promotion of our strong brand, including leveraging our role as the compiler of the Hang Seng Index series.

In January this year we added a second Guangzhou sub-branch. We will soon open our sixth Shanghai sub-branch and have a further two planned for later in the year, giving us one of the largest networks among foreign banks in this strategic city. Other openings in the pipeline for 2007 include a branch in Hangzhou and a total of six sub-branches in Beijing, Guangzhou and Shenzhen.

Treasury will explore gapping opportunities while maintaining a prudent attitude towards growth in risk-weighted assets. We will further strengthen our customer-driven business and expand the scope of our proprietary trading. We will broaden our product range to include new commodity-linked, credit derivatives and hybrid instruments, and deepen our coverage in foreign exchange, interest rates and equity-linked structured products.

In a highly competitive market for corporate lending, Corporate Banking will continue to target asset yield

26 HANG SENG BANK

CORPORATE GOVERNANCE AND OTHER INFORMATION

In addition to the module on “Corporate Governance of Locally Incorporated Authorised Institutions” under the Supervisory Policy Manual issued by the Hong Kong Monetary Authority (“HKMA”) in September 2001, the Bank also follows all the code provisions set out in the Code on Corporate Governance Practices (the “Code”) contained in Appendix 14 of the Rules Governing the Listing of Securities on The Stock Exchange of Hong Kong Limited (the “Listing Rules”) throughout the year.

Board Of DirectorsThe BoardAt 5 March 2007, the Bank’s Board consisted of 15 Directors. The Board has collective responsibility for leadership and control of, and for promoting the success of, the Bank by directing and supervising the Bank’s affairs.

The types of decisions which are to be taken by the Board include those relating to :

– Annual plans and performance targets;

– Specified senior appointments;

– Acquisitions and disposals above predetermined thresholds; and

– Any substantial change in balance sheet management policy.

Chairman And Chief ExecutiveThe roles of Chairman of the Board and Chief Executive of the Bank are segregated, with a clear division of responsibilities. The Chairman of the Board is anon-executive Director who is responsible for the

leadership and effective running of the Board. The Chief Executive of the Bank is an executive Director who exercises all the powers, authorities and discretions of the Executive Committee as may be delegated to him in respect of the Bank and its subsidiaries.

Board Composition The Board comprises three executive Directors and 12 non-executive Directors. Of the 12 non-executive Directors, eight are independent non-executive Directors. All the independent non-executive Directors meet the guidelines for assessment of independence as set out in Rule 3.13 of the Listing Rules.

Members of the Board of the Bank, who come from a variety of different backgrounds, have a diverse range of business, banking and professional expertise. Brief biographical particulars of all Hang Seng Directors, together with information relating to the relationship among them, are set out in the “Biographical Details of Directors” section under the Bank’s 2006 Annual Report.

Board ProcessRegular Board/Committee meeting schedules for each year are made available to all Directors/Committee members at the beginning of the year. In addition, notice of meetings will be given to all Directors prior to each Board meeting, normally at least 14 days in advance.

Other than regular Board meetings, in 2006, the Chairman also met with non-executive Directors, including independent non-executive Directors, without the presence of executive Directors to discuss matters of particular interest.

Hang Seng is committed to high standards of corporate governance.

27ANNUAL REPORT 2006

All Directors have access to the Company Secretary who is responsible for ensuring that the Board procedures, and related rules and regulations, are followed.

Under the Articles of Association of the Bank, a Director shall not vote or be counted in the quorum in respect of any contract, arrangement, transaction or other proposal in which he or his associate(s), is/are materially interested.

Minutes of Board/Committee meetings are kept by the Company Secretary and are open for inspection by Directors.

Appointments, Re-election And Removal The Bank’s Articles of Association provide that each Director is required to retire by rotation once every three years and that one-third (or the number nearest to one-third) of the Directors shall retire from office every year during the Bank’s Annual General Meeting. A Director’s specific term of appointment, therefore, cannot exceed three years. Retiring Directors shall be eligible for re-election at the Annual General Meeting of the Bank.

Hang Seng uses a formal, considered and transparent procedure for the appointment of new Directors. Before a prospective Director’s name is formally proposed, the opinions of the existing Directors (including the independent non-executive Directors) are sought. After considering the proposal for the appointment of a new Director, the Executive Committee will make its recommendation to the Board for further decision. In accordance with the requirement under the Banking Ordinance, approval from the HKMA will also be obtained. All new Directors are subject to election by shareholders of the Bank at the next scheduled Annual General Meeting after their appointments become effective.

In 2006, Mr Edgar D Ancona was appointed a non-executive Director of the Bank. The appointment was approved by the Board at a meeting held on 27 April 2006. All Directors, except Mr John C C Chan, attended the meeting.

Responsibilities Of DirectorsThe Bank regularly reminds all Directors of their functions and responsibilities. Through regular Board meetings, all Directors are kept abreast of the conduct, business activities and development of the Bank.

Induction programmes are arranged for newly appointed Directors. All Directors are given opportunities to update and develop their skills and knowledge.

All Directors have full and timely access to all relevant information about the Bank so that they can discharge their duties and responsibilities as Directors. There are established procedures for Directors to seek independent professional advice on Bank-related matters where appropriate. All costs associated with obtaining such advice will be borne by the Bank. In addition, each Director has separate and independent access to the Bank’s senior management.

The Bank has adopted a Code for Securities Transactions by Directors on terms no less exacting than the required standards set out in the Model Code for Securities Transactions by Directors of Listed Issuers (set out in Appendix 10 to the Listing Rules). Specific enquiries have been made with all Directors (including those who have ceased to be Directors or who have become Directors during the year ended 31 December 2006) who have confirmed that they complied with the Bank’s Code for Securities Transactions by Directors at all the applicable times for the period from 1 January 2006 to 31 December 2006 (both dates inclusive).

The interests in Group securities, including HSBC Holdings plc and the Bank, held by Directors as at 31 December 2006 are disclosed in the Directors’ Report attached to the Bank’s 2006 Annual Report.

28 HANG SENG BANK

CORPORATE GOVERNANCE AND OTHER INFORMATION (continued)

Board Members’ Attendance

Name

Number of Board meetings held during the Director’s term of

office in 2006Number of

meetings attended

Mr Michael R P Smith# (Chairman) 7 7

Mr Raymond C F Or (Vice-Chairman and Chief Executive) 7 7

Mr Edgar D Ancona# (Appointed as Director on 4 September 2006) 2 2

Mr John C C Chan* 7 5

Mr Patrick K W Chan (Executive Director and Chief Financial Officer) 7 7

Dr Y T Cheng* 7 7

Dr Marvin K T Cheung* (Note) 7 3

Mr S J Glass# (Resigned as Director on 24 March 2006) 2 2

Mr Jenkin Hui* 7 6

Mr Peter T C Lee* 7 5

Dr Eric K C Li* 7 6

Dr Vincent H S Lo# 7 4

Mr Joseph C Y Poon (Managing Director and Deputy Chief Executive) 7 7

Dr David W K Sin* 7 7

Mr Richard Y S Tang* 7 6

Mr Peter T S Wong# 7 6

* Independent non-executive Director

# Non-executive Director

(Note: Dr Marvin K T Cheung has been indisposed since 20 July 2006, and will resume duty on 11 March 2007.)

Executive Committee

Members: Mr Raymond C F Or (Chairman) Mr Peter T S Wong Mr Joseph C Y Poon Mr Patrick K W Chan Mr William W LeungØ

Mrs Dorothy K Y P SitØ

(ØGeneral Manager)

Audit Committee

Members: Dr Eric K C Li (Chairman) Mr Richard Y S Tang Dr Marvin K T Cheung

Remuneration Committee

Members: Mr John C C Chan (Chairman) Mr Jenkin Hui Mr Peter T C Lee

Board

Delegation By The BoardManagement Functions And Board CommitteesThe Board has set up three committees: the Executive Committee, the Audit Committee and the Remuneration Committee.

Each of these committees has specific written terms of reference which deal clearly with their authority and duties. All committees, except the Executive Committee, are comprised solely of independent non-executive Directors.

29ANNUAL REPORT 2006

The Executive Committee meets each month and operates as a general management committee under the direct authority of the Board. It exercises the powers, authorities and discretions of the Board in so far as they concern the management and day-to-day running of the Bank in accordance with its terms of reference and such other policies and directives as the Board may determine from time to time. The Executive Committee also sub-delegates credit, investment and capital expenditure authorities to its members.

The Audit Committee meets regularly, normally four times a year, with the senior financial, internal audit and compliance management and the external auditors to consider the Bank’s financial reporting, the nature and

scope of audit reviews and the effectiveness of the systems of internal control and compliance. It is also responsible for the appointment, reappointment, removal and remuneration of external auditors. The Audit Committee reports to the Board following each Audit Committee meeting, drawing the Board’s attention to salient points that the Board should be aware of, identifying any matters in respect of which it considers that action or improvement is needed and making relevant recommendations.

The Remuneration Committee considers human resource issues and makes recommendations to the Board on the Bank’s policy and structure for remuneration of Directors and senior management. It meets at least twice a year.

Committee Members’ Attendance

Number of meetings attended during 2006

Name Executive Committee Audit CommitteeRemuneration

Committee

Mr Raymond C F Or 12 out of 12 – –

Mr John C C Chan* – – 2 out of 2

Mr Patrick K W Chan 12 out of 12 – –

Dr Marvin K T Cheung* (Note 1) – 2 out of 5 –

Mr Jenkin Hui* – – 2 out of 2

Mr Peter T C Lee* – – 2 out of 2

Dr Eric K C Li* – 5 out of 5 –

Mr Joseph C Y Poon 9 out of 12 – –

Mr Richard Y S Tang* – 5 out of 5 –

Mr Peter T S Wong# (Note 2) 12 out of 12 – –

Mr William W Leungø 11 out of 12 – –

Mrs Dorothy K Y P Sitø 10 out of 12 – –

* Independent non-executive Director

# Non-executive Director

ø General Manager

(Notes: 1. Dr Marvin K T Cheung has been indisposed since 20 July 2006, and will resume duty on 11 March 2007.

2. Seven meetings were attended by Mr Peter T S Wong’s alternates.)

30 HANG SENG BANK

CORPORATE GOVERNANCE AND OTHER INFORMATION (continued)

Business needs

General economic situation, including GDP growth and local inflation rates

Changes in appropriate markets, e.g. supply/demand fluctuations and changes in competitive conditions

Individual contributions to results as confirmed in the performance appraisal process

Retention considerations and individual potential

Remuneration packages of Executive Directors

The Remuneration Committee held two meetings in 2006. The work performed by the Committee during 2006 included:

– Reviewing the fees payable to the Directors and the members of the Board’s Committees;

– Reviewing the policy for the remuneration of the executive Directors of the Bank and the Directors of the Bank’s subsidiaries;

– Reviewing the remuneration of the executive Directors and senior management of the Bank;

– Determining the remuneration packages of a newly appointed senior executive of the Bank and the fees payable to members of a newly established Audit Committee of a subsidiary of the Bank; and

– Reviewing general and special salary increases of the Bank’s staff for 2007.

During the process of consideration, no individual Director was involved in decisions relating to his/her own remuneration.

The present scale of Director’s fees, and additional fees for membership on the Audit Committee and Remuneration Committee, is outlined below:

Amount

Board of Directors:Director’s annual fees

Chairman HK$230,000

Vice-Chairman HK$150,000

Other directors HK$150,000

Audit Committee:Additional annual fees

Chairman HK$120,000

Other members HK$80,000

Remuneration Committee:Additional annual fees

Chairman HK$60,000

Other members HK$40,000

Remuneration of Directors and Senior ManagementThe Level And Make-up Of Remuneration and Disclosure The Remuneration Committee is responsible for the policy on remuneration of Directors and senior management.

The Bank’s policy on remuneration is to maintain fair and competitive packages based on business needs and industry practice. For determining the level of fees paid to members of the Board of Directors, market rates and factors such as each Director’s workload and required commitment will be taken into account. The following factors are considered when determining the remuneration packages of Executive Directors:

31ANNUAL REPORT 2006

Board

– to approve risk management policies and major risk control limits

– to oversee the monitoring and control of various types of risks

Executive Committee / Audit Committee / Asset and Liability Management Committee / Credit Committee

– to review risk management reporting by business and functional units

Business and functional units

– to assess individual types of risk arising under their areas of responsibility

– to manage the risks in accordance with risk management procedures

– to report on risk management

The Bank’s internal control system comprises a well-established organisational structure and comprehensive policies and standards. Areas of responsibilities for each business and operational unit are clearly defined to ensure effective checks and balances.

Procedures have been designed for safeguarding assets against unauthorised use or disposition; for maintaining proper accounting records; and for ensuring the reliability of financial information used within the business or for publication. The procedures provide reasonable but not absolute assurance against material errors, losses or fraud. Procedures have also been designed to ensure compliance with applicable laws, rules and regulations.

Systems and procedures are in place in the Bank to identify, control and report on the major types of risks the Bank faces. In particular, the Bank has developed comprehensive procedures (ranging from a money laundering deterrence programme to health and safety rules) to manage reputational risks that may arise as a consequence of its daily operations. The Bank’s general risk management control procedures are also illustrated below:

Information relating to the remuneration of each Director for 2006 is set out in Note 18 to the Bank’s 2006 Financial Statements.

Accountability And AuditFinancial Reporting The Board aims at making a balanced, clear and comprehensive assessment of the Bank’s performance, position and prospects. An annual operating plan is reviewed and approved by the Board on a yearly basis. Reports on monthly financial results, business performance and variances against the approved annual operating plan are submitted to the Board at each Board meeting for regular monitoring.

Strategic planning cycles are generally from three to five years. The HSBC Group Strategic Plan for 2004 to 2008, Managing for Growth, was adopted by Hang Seng’s Board in January 2004.

The annual and interim results of the Bank are announced in a timely manner within the limits of three months and two months respectively after the end of the relevant periods.

The Directors acknowledge their responsibility for preparing the accounts of the Bank. As at 31 December 2006, the Directors are not aware of any material uncertainties relating to events or conditions which may cast significant doubt upon the Bank’s ability to continue as a going concern. Accordingly, the Directors have prepared the financial statements of the Bank on a going-concern basis.

The responsibilities of the external auditors with respect to financial reporting are set out in the report of the auditors attached to the Bank’s 2006 Financial Statements.

Internal ControlsSystem And ProceduresThe Directors are responsible for internal control at the Bank and its subsidiaries and for reviewing its effectiveness.

32 HANG SENG BANK

CORPORATE GOVERNANCE AND OTHER INFORMATION (continued)

More detailed discussions on the policies and procedures for management of each of the major types of risk the Bank faces, including credit, market, liquidity and operational risks, are included in the risk management section of the “Financial Review” section under the Bank’s 2006 Annual Report, and in Note 61 to the Bank’s 2006 Financial Statements.

Annual AssessmentA review of the effectiveness of the Bank’s internal control system covering all controls, including financial, operational and compliance and risk management controls, is conducted annually. The review at the end of 2006 was conducted with reference to the COSO (The Committee of Sponsoring Organisations) internal control framework, which assesses the Bank’s internal control system against the five elements of control environment, risk assessment, control activities, communication and monitoring. The result has been reported to the Audit Committee and the Board.

Internal AuditInternal audit plays an important role in the Bank’s internal control framework. It monitors the effectiveness of internal control procedures and compliance with policies and standards across all business and operational units. All management letters from external auditors and reports from regulatory authorities will be reviewed by the Audit Committee and all recommendations will be implemented. Management is required to annually provide the internal audit function with written confirmation that it has acted fully on all recommendations made by external auditors and regulatory authorities. The internal audit function also advises management on operational efficiency and other risk management issues. The work of the internal audit function is focused on areas of greatest risk to the Bank as determined by risk assessment. The head of internal audit of the Bank reports to the Chairman and the Audit Committee.

External AuditorsThe Bank’s external auditor is KPMG. The Audit Committee is responsible for making recommendations to the Board on the appointment, reappointment, removal and remuneration of the external auditor. The external auditor’s independence and objectivities are also reviewed and monitored by the Audit Committee.

During 2006, fees paid to the Bank’s external auditor for audit services totalled HK$11.2 million, compared with HK$10.8 million in 2005. For non-audit services, the fees paid amounted to HK$2.9 million, compared with HK$7.3 million in 2005. The significant non-audit service assignments covered by these fees include the following:

Nature of service Fees paid (HK$m)

Review of regulatory returns and interim review 1.9

Tax services 0.8

Other services 0.2

2.9

Audit CommitteeThe Audit Committee assists the Board in meeting its responsibilities for ensuring an effective system of internal control and compliance, and in meeting its external financial reporting obligations.

The Audit Committee held five meetings in 2006. The work performed by the Committee during 2006 included:

– Reviewing the Directors’ Report and Full-year Accounts for the year ended 31 December 2005 and the annual results announcement;

– Reviewing the Interim Accounts for the six months ended 30 June 2006 and the interim results announcement;

– Reviewing the recently issued accounting standards, and the progress of implementation work relating to the Sarbanes-Oxley Act and Basel II;

– Developing and implementing a policy on the employment of former employees of the external auditors;

33ANNUAL REPORT 2006

– Reviewing the preliminary internal audit and compliance framework for the establishment of a mainland China-incorporated foreign bank;

– Reviewing the internal audit plan for 2007;

– Reviewing essential matters or high-level reports relating to financial control, internal audit, credit and compliance, and the system of internal control, and discussing these with management;

– Reviewing regular risk management reports and the business continuity planning for avian influenza crisis; and

– Monitoring the staffing and resources of the Bank’s Internal Audit Department.

Communication With ShareholdersEffective CommunicationThe Bank attaches great importance to communications with shareholders and a number of means are used to promote greater understanding and dialogue with investment audiences. The Bank holds group meetings with analysts to announce its annual and interim results. The results announcements are also broadcast live via webcast. Apart from the above, designated senior executives maintain regular dialogue with institutional investors and analysts to keep them abreast of the Bank’s development. Including the two results announcements, a total of 77 meetings with 332 analysts and fund managers from 258 companies were held in 2006. The Bank’s Chief Executive and Chief Financial Officer made presentation at major investor forums held in Hong Kong and overseas. The Bank’s website www.hangseng.com contains an investor relations section which offers timely access to the Bank’s press releases and other business information.

The Annual General Meeting provides a useful forum for shareholders to exchange views with the Board. The Bank’s Chairman, executive Directors, Chairman of the Audit Committee and non-executive Directors are available atthe Annual General Meeting to answer questions from shareholders. Separate resolutions are proposed at general meetings for each substantial issue, including the

election of individual Directors. Procedures for voting by poll, which comply with the Listing Rules and the Articles of Association of the Bank, are set out in the circular to shareholders dispatched together with the Annual Report.

The Bank’s last Annual General Meeting of shareholders was held on Wednesday, 26 April 2006 at 3:30pm at the Penthouse of Hang Seng Bank Headquarters, 83 Des Voeux Road Central, Level 24, Hong Kong. All the resolutions proposed at that meeting were approved by shareholders of the Bank by poll voting. Details of the poll results are available under the investor relations section of the Bank’s website www.hangseng.com.

The next Annual General Meeting of shareholders will be held on Wednesday, 2 May 2007. Shareholders may refer to the “Corporate Information and Calendar” section under the Bank’s 2006 Annual Report for a calendar of other important dates for shareholders in the financial year 2007.

Other InformationThe Annual and Interim Reports contain comprehensive information on business strategies and developments. Discussions and analyses of the Bank’s performance during 2006 and the material factors underlying its results and financial position can be found in the Chairman’s Statement, the Chief Executive’s Report and the Financial Review in the Bank’s 2006 Annual Report.

Material Related Party Transactions And Contracts Of SignificanceThe Bank’s material related party transactions are set out in Note 60 to the 2006 Financial Statements. These transactions include those that the Bank has entered into with its immediate holding company and fellow subsidiary companies in the ordinary course of its interbank activities, including the acceptance and placement of interbank deposits, correspondent banking transactions, off-balance sheet transactions, and the provision of other banking and financial services.

34 HANG SENG BANK

CORPORATE GOVERNANCE AND OTHER INFORMATION (continued)

The Bank uses the IT services of, and shares an automated teller machine network with, The Hongkong and Shanghai Banking Corporation Limited, its immediate holding company. The Bank also shares IT and certain processing services with fellow subsidiaries on a cost recovery basis. For 2006, the Bank’s share of the costs include HK$174 million for system development services, HK$24 million for printing and stationery, HK$109 million for data processing, and HK$44 million for administrative services.

The Bank maintains a staff retirement benefit scheme for which a fellow subsidiary company acts as insurer and administrator. As part of its ordinary course of business with other financial institutions, the Bank also markets Mandatory Provident Fund products and distributes retail investment funds for fellow subsidiaries, with a fee income of HK$61 million and HK$77 million respectively in 2006. Hang Seng Investment Management Limited, a wholly owned subsidiary of the Bank, manages in the ordinary course of its business a fund administered by a fellow subsidiary, to whom management fee rebates were made. The rebate for 2006 amounted to HK$59 million.

The Bank also sells life insurance products issued byHang Seng Life Limited, which is a 50% subsidiary of the Bank (the remaining 50% is indirectly owned by the Bank’s controlling shareholder, The Hongkong and Shanghai Banking Corporation Limited). Hang Seng Life Limited subscribes to management services provided by a fellow subsidiary on a cost recovery basis and, for 2006,Hang Seng Life Limited’s share of the costs amounted to HK$72 million. Hang Seng Life Limited also uses the investment management services of a fellow subsidiary, and fees paid in 2006 amounted to HK$30 million.

These transactions were entered into by the Bank in the ordinary and usual course of business on normal commercial terms, and in relation to those which constitute connected transactions under the Listing Rules, they also comply with applicable requirements under the Listing Rules. The Bank regards its usage of the IT services of The Hongkong and Shanghai Banking Corporation Limited (amount of IT services cost incurred for 2006: HK$399 million), and the sale of life insurance products issued by Hang Seng Life Limited (amount of commission income for 2006: HK$697 million), as contracts of significance for 2006.

Human ResourcesThe human resources policies of the Bank are designed to attract people of the highest calibre and to motivate them to excel in their careers, as well as uphold the Bank’s culture of service quality.

Employee StatisticsAs at 31 December 2006, the Bank’s total headcount was 8,498, reflecting an increase of 610, or 7.73 per cent, compared with a year earlier. The total comprised 864 executives, 3,085 staff officers and 4,549 clerical and non-clerical staff.

Employee RemunerationCompensation packages take into account levels and composition of pay in the markets in which the Bank operates. Salaries are reviewed annually in the context of individual and business performance, market practice, internal relativities and competitive market pressures.

Under appropriate circumstances, performance-related variable pay is provided as an incentive for staff. In 2006, incentive payments were made to staff members who had chosen to join the Bank’s 12-month Pay Scheme with variable bonus under performance-based remuneration strategy.

Since 1999, the Bank has participated in the HSBC Holdings Savings-related Share Option Plan (Sharesave), which enables staff members to make monthly savings for the purchase of HSBC Group shares after a specified period. For Sharesave 2006, 2,666 staff members had subscribed to the plan.

Other incentive awards were also made. More than 1,300 staff were rewarded with HSBC Group shares or cash in 2006 for outstanding performance or displaying good potential.

Employee Involvement Communication with staff is a key aspect of the Bank’s policies. Information relating to employment matters, the Bank’s business direction, and strategies and factors affecting the Bank’s performance are conveyed to staff via different channels, including interchange sessions, focus group meetings, an intranet site, in-house magazines, morning broadcasts and training programmes. Employees are encouraged to contribute their ideas during work improvement programmes, cross-team projects and suggestion schemes.

35ANNUAL REPORT 2006

Staff DevelopmentIn order to fully develop staff members’ potential, the Bank offers a wide range of training programmes that help them fulfil their personal career goals or professional training requirements, including those for regulated businesses and activities, while equipping them to meet future challenges. Two training programmes respectively won The Bronze Award and Certificate of Excellence in the 2006 Award for Excellence in Training competition organised by Hong Kong Management Association. These programmes were also awarded American Society for Training and Development (ASTD) Excellence in Practice citations.

New staff joining the Bank attend an induction programme that provides them with a better understanding of the history, culture and values of the Bank. In 2006, the staff integration programme was delivered to facilitate the integration of new executives to familiarise them with the culture and strategies of the Bank. Continuous educational development is provided to staff through the Bank’s Learning Resource Centre, multi-media programmes, an intranet site and videos. Staff members are also encouraged to pursue professional or academic qualifications through the Bank’s Education and Professional Qualification Award System.

An in-branch pre-placement training scheme, comprising self-learning material, learning guide, training videos and online exercises as well as workplace coaching, was launched for new sales staff at Mainland branches to equip them with the necessary skills upon joining the Bank.

To foster the Bank’s ‘can-do’ spirit and ‘listening and speaking up’ culture, a new series of ‘Driving the Change’ programmes were launched. In support of the Bank’s Six Sigma initiatives, a seminar was organised for certain officers and executives in 2006.

The average number of training days per staff member in 2006 was 6.5 days.

Recruitment And RetentionThe employment market continued to be active in 2006. Various resourcing measures, including a number of employer branding and staff retention initiatives, were implemented to attract and retain high-quality staff.

The Bank in 2006 participated in the Financial Services Career Exhibition organised by the FinMan Committee and the Hong Kong Polytechnic University and the Career Expos organised by the Hong Kong Trade Development Council, the Hong Kong Federation of Youth Groups and the Labour Department of the Hong Kong government.

As part of the Bank’s staff retention programme, packages and career paths for certain job positions have been reviewed to increase career advancement opportunities and ensure market competitiveness. Trainee programmes have also been developed for jobs in selected functional areas.

Code Of ConductTo ensure the Bank operates according to the highest standards of ethical conduct and professional competence, all staff are required to strictly follow the Code of Conduct contained in the Staff Handbook. Following the relevant regulatory guidelines and other industry best practices, the Code sets out ethical standards and values to which staff are required to adhere and covers various legal, regulatory and ethical issues. These include topics such as prevention of bribery, dealing in securities, personal benefits, outside employment and anti-discrimination policies.

The Bank uses various communication channels to periodically remind staff of the requirement to adhere to the rules and ethical standards set out in the Code.

Health And SafetyThe Bank recognises the need for effective management of health and safety in order to provide a safe working environment. The Bank focuses on identifying health, safety and fire risks in advance, taking any measures necessary to remove, reduce or control material risks of fires and of accidents or injuries to employees and visitors.

Following the SARS outbreak in 2003, the Bank prepared a Communicable Diseases Plan. This sets out the key issues to be addressed and the responses to be taken in the event of a similar occurrence involving a serious communicable disease. To get the Bank prepared for the outbreak of avian influenza, an Avian Influenza Contingency Manual was prepared jointly with various divisions with reference to the SARS experience. Staff have been made aware through various channels of the importance of personal hygiene and health, and informed of the contingency measures to adopt should there be an outbreak.

36 HANG SENG BANK

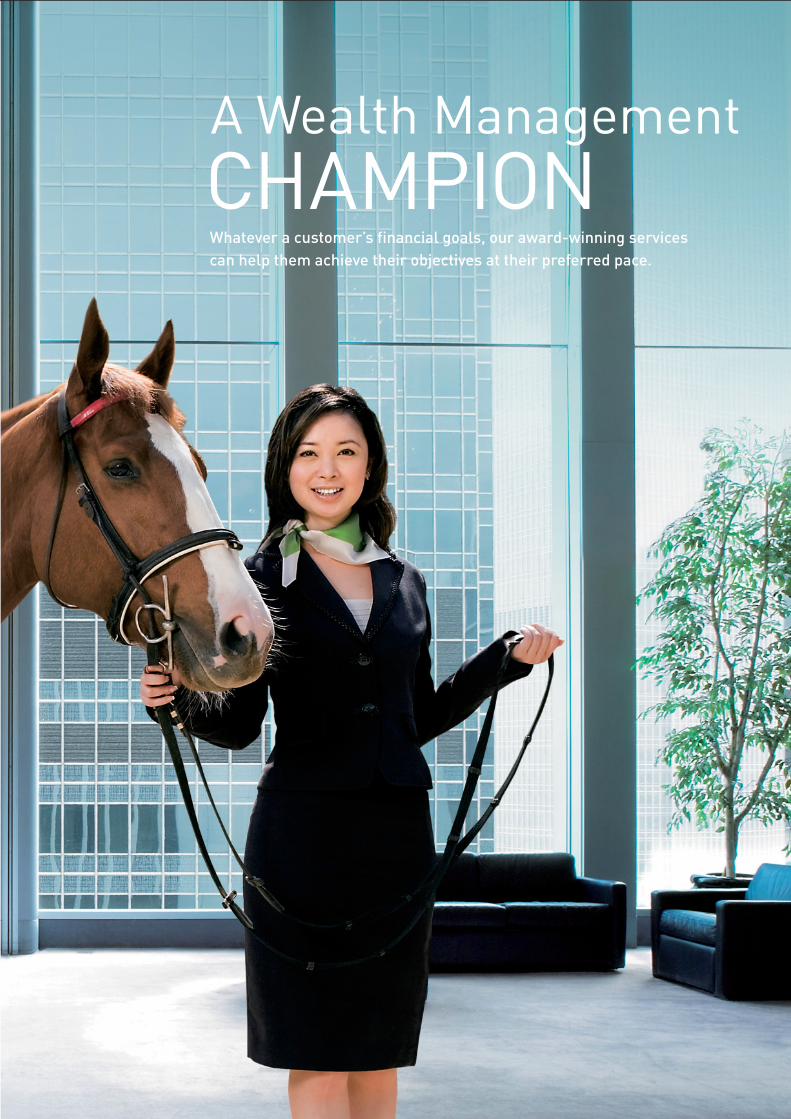

BUSINESS OPERATIONS – BUSINESS IN HONG KONG

37ANNUAL REPORT 2006

CHAMPIONWhatever a customer’s financial goals, our award-winning services can help them achieve their objectives at their preferred pace.

A Wealth Management

38 HANG SENG BANK

BUSINESS OPERATIONS – BUSINESS IN HONG KONG

In a competitive operating environment, Hang Seng differentiated itself through customer service excellence, driven by a progressive and pragmatic approach to business as well as product and service innovations.

Commercial Banking and wealth management business both achieved significant increases in income as we stepped up efforts to refine our relationship management strategy and further personalise financial solutions. The strong labour market supported good growth in consumer finance, particularly personal loans and card receivables.

Our comprehensive brand strengthening programme helped us deepen existing customer relationships and broaden our appeal in key market segments such as young people, affluent individuals and small and medium-sized enterprises (SMEs).

Customer deposits, including certificates of deposit and other debt securities in issue, grew by 12.8 per cent to HK$540.3 billion, largely reflecting increases in savings and structured deposits, which rose by 18.2 per cent and 31.2 per cent respectively.

We further expanded and diversified our loan portfolio. This resulted in an HK$18.6 billion, or 7.1 per cent, increase in gross advances to customers.

We continued with our property portfolio rationalisation strategy, realising HK$3.1 billion through the sale of several properties.

To support business expansion, we hired more staff in key areas such as Commercial Banking, wealth management and IT. We also continued to place strong emphasis on employee development through various training, coaching and mentoring programmes and talent management initiatives. In a buoyant employment market, we focused on staff retention through a combination of competitive compensation packages, incentive schemes and career development programmes.

Personal Financial ServicesPersonal Financial Services recorded pre-tax profit of HK$7,730 million, representing 52.9 per cent of total pre-tax profit.

Net interest income rose 4.7 per cent, benefiting from the improvement of spreads on best lending rate-based loans and growth in customer advances.

Wealth management income grew by 22.7 per cent. The strong stock market and the introduction of new investment products helped investment services income increase by HK$576 million to HK$2,519 million. Private Banking achieved a 51.1 per cent rise in total operating income to HK$731 million. Life insurance income was up 17.5 per cent at HK$1,476 million.

+46.3%

Private Banking pre-tax profit

39ANNUAL REPORT 2006

Investment ServicesWe worked to capitalise on the positive investment climate by expanding our product range to meet changing market demands and grow fee income. We used increased marketing and competitive pricing strategies to acquire new customers and boost turnover. Investment services income rose by 29.6 per cent.

We grew our securities services customer base by 20.1 per cent through special promotions and enhancing delivery channels for faster and easier completion of transactions. Securities services income increased 63.3 per cent, with growth of 86.6 per cent in stockbroking turnover.

A 40.6 per cent increase in retail investment fund sales was achieved by offering a wide range of funds to suit different needs, the timely provision of supporting services such as market and fund performance

commentaries, and taking action to strengthen our fund management business. The number of investment fund accounts rose by 7.8 per cent.

We received number one rankings from Morningstar Asia, S&P’s Fund Services and Lipper for the 2006 performance of five Hang Seng funds, with one-year returns in Hong Kong dollars ranging from 52.3 per cent for the Hang Seng Hong Kong Property Equity Fund to 161.1 per cent for the Hang Seng China H-Share Index Leveraged 150 Fund.

In January 2006, we launched the Hang Seng China Equity Fund to increase choice for retail customers looking to benefit from the high growth potential of the mainland China market.

We continued to enjoy an excellent customer response to funds offered under our Qualified Foreign Institutional Investor licence. We have

applied to the Mainland authorities to increase our current quota of US$100 million, which is now fully utilised.

The introduction of more structured deposits and instruments, particularly those with shorter tenors and callable features, helped structured products issue volume and income grow by 93 per cent and 48.1 per cent respectively.

Private Banking’s 10th anniversary year proved a successful one. Assets under management grew by 39.6 per cent and investment services income rose by 83.5 per cent, driven by increases in the number of relationship managers, cross-referrals and product offerings. Pre-tax profit was up 46.3 per cent at HK$556 million.

Total funds under management, including discretionary and advisory, increased by 10.3 per cent to HK$106.4 billion.

40 HANG SENG BANK

BUSINESS OPERATIONS – BUSINESS IN HONG KONG (continued)

Residential mortgage lending grew by 5.9 per cent.

InsuranceOur life insurance income grew with the launch of products targeting expanding market segments. The Monthly Income Retirement Plan helped strengthen our retirement planning portfolio and the MediCash Lifetime Insurance Plan extended our retirement offerings to include health protection.

Operating income rose by 17.5 per cent to HK$1,476 million. The number of policies in force increased 18.5 per cent.

Consumer LendingExcluding the fall in Government Home Ownership Scheme mortgages, lending to individuals rose by 5.4 per cent. Personal loans rose significantly by 46.4 per cent and we gained market share.

Enhancements to ‘Mortgage-Link’ accounts as well as the expansion of our online mortgage services enabled us to grow residential mortgage lending by 5.9 per cent.

New credit cards such as VISA Infinite, an invitation-only card for affluent customers, and increased collaboration with merchants contributed to an 11.7 per cent increase in card spending. Card services income grew by 22 per cent to HK$860 million.

The launch of alpha card, a debit card for 15 to 18 year olds, helped us capture new business among young people.

41ANNUAL REPORT 2006

Commercial BankingA 22.2 per cent increase in customer advances, encouraging progress with corporate wealth management services and closer relationships with commercial customers all contributed to a 21.5 per cent rise in Commercial Banking’s operating profit excluding loan impairment charges and other credit risk provisions.

Net interest income increased by 28.3 per cent. Trade finance jumped 24 per cent, gaining market share. Lending to the manufacturing industry and the wholesale and retail sector exceeded average market growth, rising by 18.4 per cent and 14.3 per cent respectively.

We strengthened our position as the preferred bank for SMEs. We rolled out more services, including a 24-hour manned hotline and the introduction of SME ambassadors at all branches. We became the first bank in Hong Kong to offer Octopus merchant services to retailers.

The expansion of our network of Business Banking Centres brought us closer to customers, facilitating our proactive approach to meeting their needs. With the addition of more marketing officers during the year, new SME accounts acquired in the second half of 2006 outpaced the first half by 34.7 per cent.

Refined customer group segmentation and deeper customer relationships generated greater

cross-selling opportunities. Increases in corporate wealth management and card acquiring business helped net trading income and net fees and commissions grow by 11.9 per cent and 13.5 per cent respectively.

In May, we won the ‘Best Banking Service Award’ at the SME’s Best Partner Awards organised by the Hong Kong Chamber of Small and Medium Business.

We invested additional resources in our Macau branch, which moved to new premises in September to accommodate its expansion. The broader service scope and product range saw encouraging growth in loans and deposits.

Including a significant reduction in loan impairment allowances, Commercial Banking’s pre-tax profit increased 109.8 per cent to HK$2,262 million, contributing 16.4 per cent to total pre-tax profit.

+21.5%

Commercial Banking operating profit excluding loan impairment charges

42 HANG SENG BANK