General Aspects of “Tax Residence” - EJTN

39

General Aspects of “Tax Residence” Maria Papadopoulou LL.M, Administrative Judge First Instance Administrative Court of Thessaloniki With financial support from the Justice Programme of the European Union

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of General Aspects of “Tax Residence” - EJTN

General Aspects of “Tax Residence”

Maria Papadopoulou LL.M, Administrative JudgeFirst Instance Administrative Court of Thessaloniki

With financial support from the Justice

Programme of the European Union

Outline

2

Α) Introduction

A1) Underlying principles

-Fiscal sovereignty – Jurisdiction to tax

A2) Why is defining tax residence important

- Double taxation issues

- Discrimination issues

- Double non taxation issues - tax avoidance issues

B) Legal rules for the determination of tax residence of individuals

B1) National rules

B2) International Agreements OECD Model Tax Convention

B3) Bilateral treaties

B4) EU legislation

Outline

C) Proving tax residence

-Burden of proof

-Necessary documentation and other means of proof

-The transfer of tax residence

D) Non dom

Definition and arising issues

E) Poll questions

3

A. Underlying principles – The fiscal sovereignty principle

• Fiscal sovereignty is defined as the authority of each State to tax

certain persons or activities with a link to a specific territory mainly

either personal (residence or citizenship) or territorial (source).

• Authority means that States are free to decide the tax rate, tax

base, the extent they wish to relieve double taxation.

• This principle constitutes the basis for the legal right to impose

taxes or jurisdiction to tax.

4

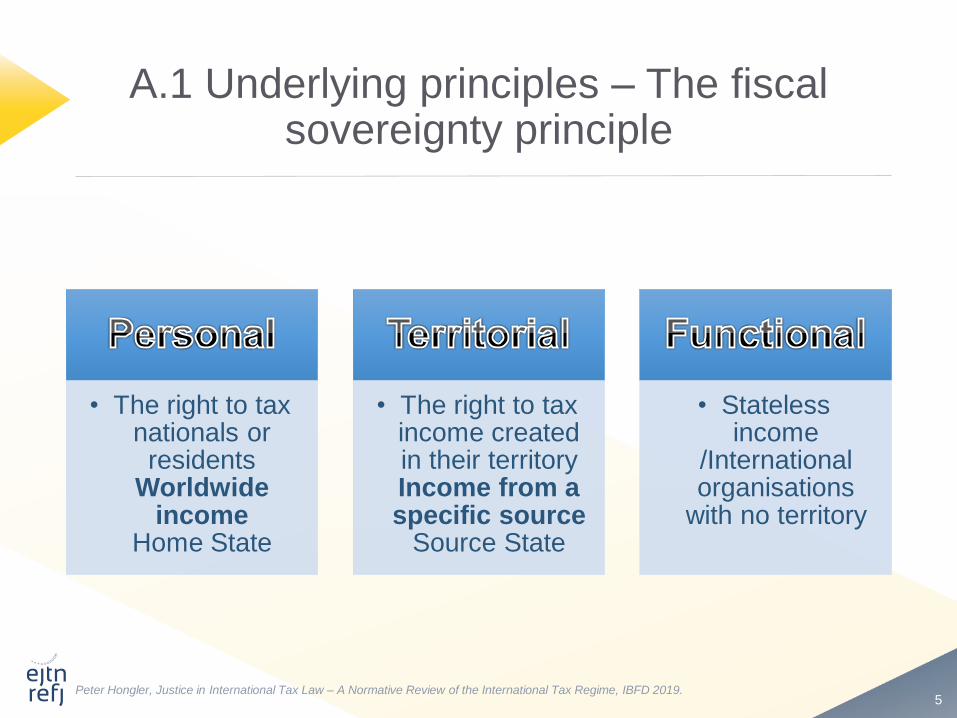

A.1 Underlying principles – The fiscal sovereignty principle

• The right to tax nationals or

residents Worldwide

income Home State

• The right to tax income created in their territory Income from a specific source

Source State

• Stateless income

/International organisations

with no territory

Peter Hongler, Justice in International Tax Law – A Normative Review of the International Tax Regime, IBFD 2019.5

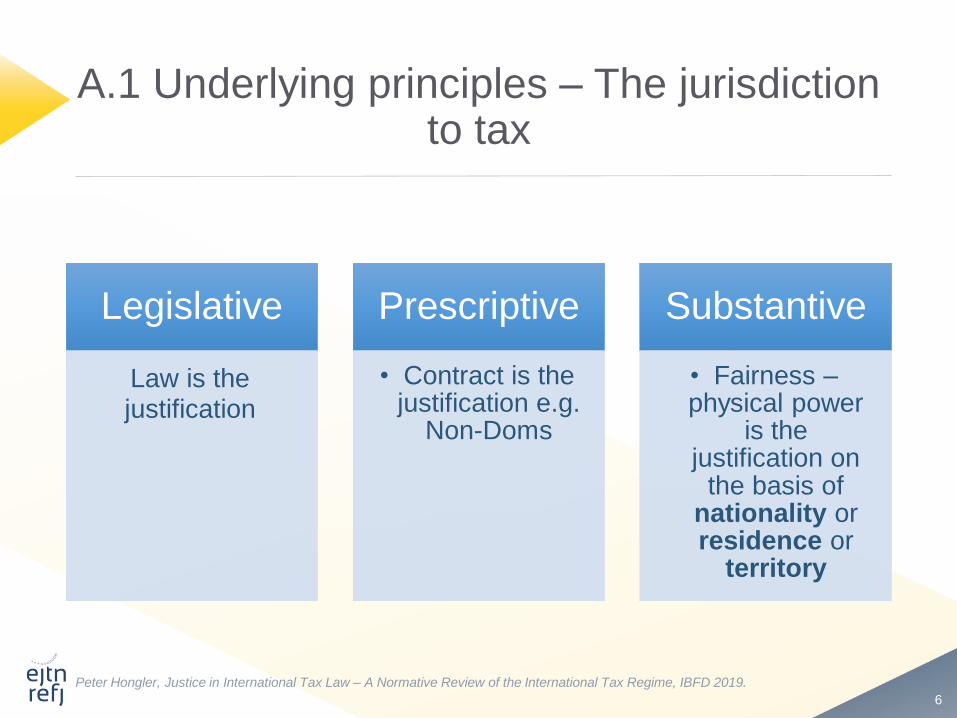

A.1 Underlying principles – The jurisdiction to tax

Legislative

Law is the justification

Prescriptive

• Contract is the justification e.g.

Non-Doms

Substantive

• Fairness –physical power

is the justification on

the basis of nationality or residence or

territory

Peter Hongler, Justice in International Tax Law – A Normative Review of the International Tax Regime, IBFD 2019.

6

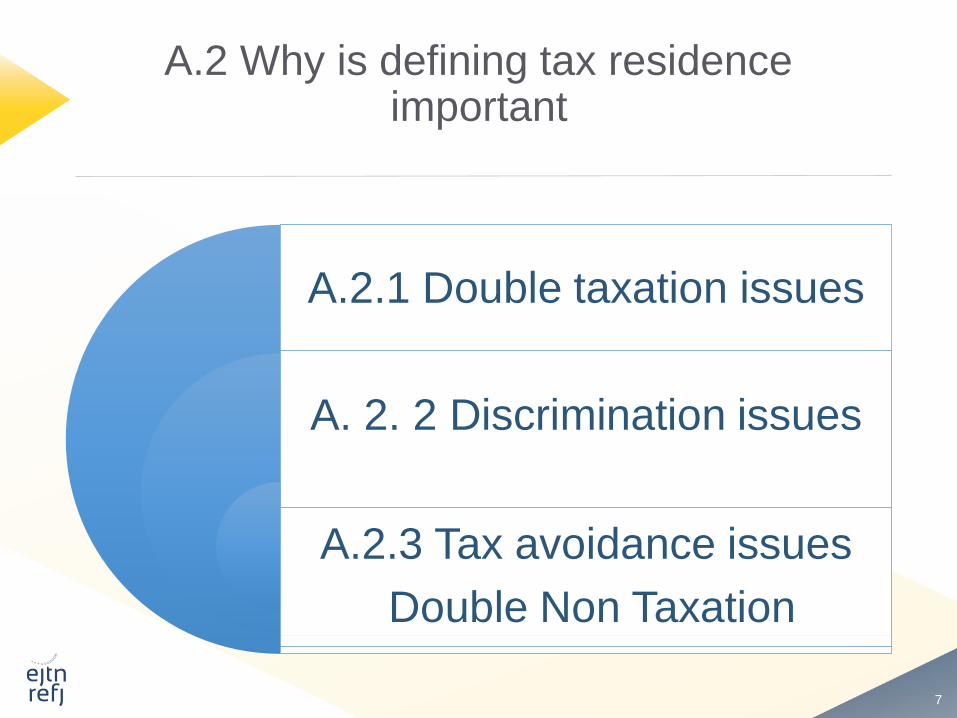

A.2 Why is defining tax residence important

A.2.1 Double taxation issues

A. 2. 2 Discrimination issues

A.2.3 Tax avoidance issues

Double Non Taxation

7

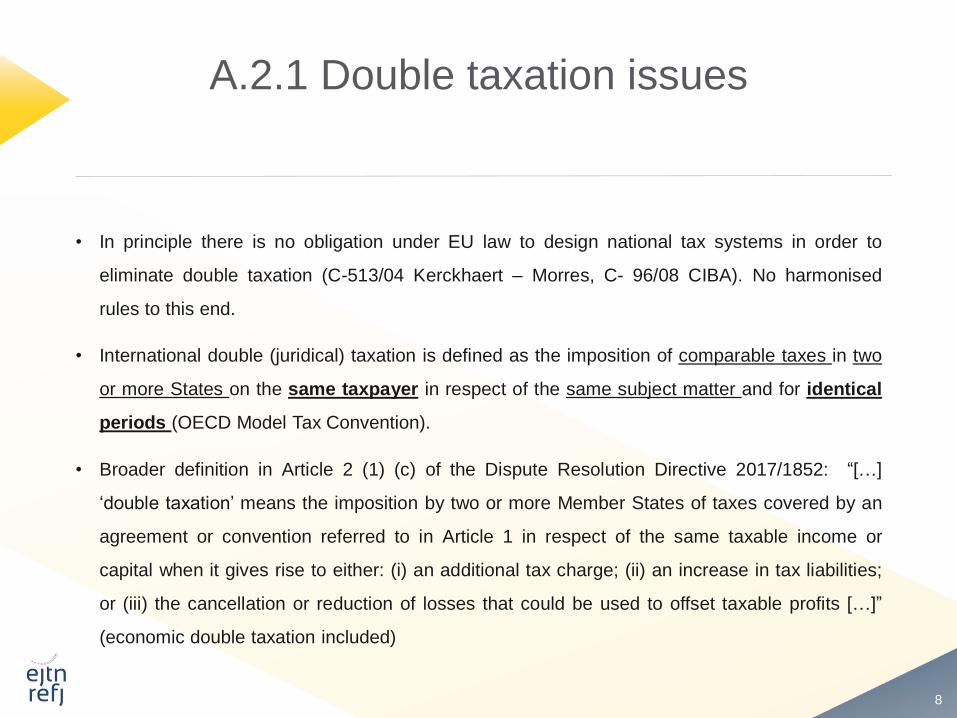

A.2.1 Double taxation issues

• In principle there is no obligation under EU law to design national tax systems in order to

eliminate double taxation (C-513/04 Kerckhaert – Morres, C- 96/08 CIBA). No harmonised

rules to this end.

• International double (juridical) taxation is defined as the imposition of comparable taxes in two

or more States on the same taxpayer in respect of the same subject matter and for identical

periods (OECD Model Tax Convention).

• Broader definition in Article 2 (1) (c) of the Dispute Resolution Directive 2017/1852: “[…]

‘double taxation’ means the imposition by two or more Member States of taxes covered by an

agreement or convention referred to in Article 1 in respect of the same taxable income or

capital when it gives rise to either: (i) an additional tax charge; (ii) an increase in tax liabilities;

or (iii) the cancellation or reduction of losses that could be used to offset taxable profits […]”

(economic double taxation included)

8

A.2.1 Double taxation issues

• Possible forms-reasons: (a) Application of diverging substantive criteria by different countries to

establish their jurisdiction to tax (nationality-residence), (b) Application of diverging criteria by

different countries to establish tax residence per se, (c) Worldwide income taxation of residents

v. taxation at the source state, (d) Transfer of residence within the same fiscal year, (e) different

interpretation by various jurisdictions of the same terms.

• It is a breach of tax fairness, proportionality, it deters investments, it consists a breach of the

right to Property (Article 1 of the First Additional Protocol of ECHR, see relevant ECHR case

law James & Others v. UK 1986, Neftyanaya Kompaniya Yukos v. Russia 2012, Gall v.

Hungary 2013 etc.), it distorts the internal market.

• It may be eliminated or reduced either by unilateral measures (tax exemptions or credits) and

(or) by allocation rules found in bilateral tax treaties.

9

A. 2. 2 Discrimination issues

➢ Distinction between residents and non residents is essential in international tax law - Non discrimination

clause in DTTs following Article 24 of the OECD MTC.

➢ Extensive ECJ case law exists on the comparability of those two categories, on the difference in treatment

and possible justifications of different treatment.

➢ Normally there is no comparability. However, if comparable, then “equal treatment” has to be granted meaning

no “less favourable treatment” (not even a minor disadvantage (C- 270/83 Avoir Fiscal). Otherwise, indirect

discrimination on the basis of nationality, as non residents are usually nationals of other MS (C- 175/88 Biehl).

➢ The comparability is either decided on the legal situation (C- 270/83 Avoir Fiscal) or on facts (C-279/93

Schumacker) by equating non residents who receive all or almost all of their income in one MS with residents.

Further ECJ case law on discrimination: C-81/87 Daily Mail, C- 80/94 Wielockx, C-336/96 Gilly, C-330/91

Commerzbank, C-397/98 Metallgesellschaft, C-307/97 Saint Gobain, C-391/97 Geschwind, C- 152/03 Ritter

Coulais, C- 520/04 Turpeinen, C-182/06 Lakebrink, C- 527/06 Renneberg etc.

10

A. 2. 2 Discrimination issues

• Broader scope of restriction based case law concerning non discriminative measures capable of hindering

Treaty freedoms without being justified, whereby the comparability test is skipped (indicatively Case 18/84

Commission v. France, C- 250/95 Futura, C-264/96 ICI, C- 439/97 Sandoz, C-385/00 De Groot, C- 436/00 X&

Y, C- 234/01 Gerritse, C-168/01 Bosal, C- 39/04 Laboratoires Fournier).

• Also, discrimination between residents on the ground of exercising Treaty freedoms. For instance upon transfer

of their residence in another State (C- 9/02 Lasteyrie). Also, relevant C-204/90 Bachmann, C- 152/03 Ritter

Coulais, C-31/2011 Marianne Scheunemann.

• Nationals- tax residents may invoke discrimination against foreign nationals (reverse discrimination-purely

domestic situation- Case C-112/91 Hans Werner). For instance, against expatriates benefiting from special

non-dom regimes.

11

A.2.3 Tax avoidance issues - Double Non Taxation

➢ Already in the Preamble of the OECD MTC

“Intending to conclude a Convention for the elimination of double taxation with respect to taxes on income and on capital

without creating opportunities for non-taxation or reduced taxation through tax evasion or avoidance (including through

treaty-shopping arrangements aimed at obtaining reliefs provided in this Convention for the indirect benefit of residents of

third States)”

➢ Double non taxation means the non taxation or unduly low taxation of cross border activities. It may result from the

application of tax treaties, when each contracting state considers that the treaty does not allow it to tax. It is considered to

be as unfair as double taxation.

➢ Ways to address the issue: (a) Application of general principles of rule of law, proportionality and non discrimination while

drafting and interpreting relevant domestic law and DTTs (Article 3 par. 2 and Article 23A par. 4 of the OECD MTC), (b)

application of domestic anti-abuse clauses either by virtue of a relevant clause included in the DTT or unilaterally (without

prejudice to treaty override practices), (c) “limitation on benefits” clauses (LOB) or “subject to tax clauses” included in

DTTs, (d) beneficial ownership (substance over form), (e) G20 Framework on BEPS (Base Erosion and Profit Shifting)

applying as of 1.7.2018, (f) EU Directive 2016/1164 on tax avoidance.

12

B. Definition of Resident for tax purposes

B.1 National rules

-Not all countries have a set legal definition.

-Most countries have been affected by the definition of the OECD Model Tax

Convention, however they don’t share strictly the same internal criteria for

determining residence.

-Each country has an interest to expand its jurisdiction to tax by exercising its

sovereignty over its entire territory.

-Domicile = corpus + animus or Habitual Abode.

-Same general principles apply such as the obligation to have a domicile and the

exclusivity of domicile.

13

B. Definition of Resident for tax purposes

B.2. Bilateral Treaties DTTs

-International Treaties ➔ Domestic Law after ratification.

-Apply only between the two Contracting States under the

condition of reciprocity – Each country has its own network.

-They allocate the jurisdiction to levy tax (double taxation) and

encourage the exchange of information between contracting

states (double non taxation). They do NOT impose taxes.

14

B. Definition of Resident for tax purposes

-They are drafted following mostly the OECD Model Tax Convention.

Contracting States are free to choose among all the various available links

(C-241/14 Bukovansky, C-168/19, C-169/19 HB and IC etc.)

-For their interpretation the Vienna Convention Treaty on the Law of

Treaties 1969 applies (mainly Articles 31-33).

https://legal.un.org/ilc/texts/instruments/english/conventions/1_1_1969.pdf

15

B. Definition of Resident for tax purposes

B.3. OECD Model Tax Convention (MTC) on Income & Capital (as read on 21.11.2017)

and Commentary

-OECD is an international Organisation – 38 Members /developed countries– Founded in

Paris in 1960.

-Its predecessor was the Organisation for European Economic Cooperation founded in

1948.

-Enhance financial relations between MS and promote international trade.

-MTC introduced in 1963 as a Draft – revised in 1977 under the name MTC- loose leaf

format in 1992- constant updates – Not legally binding (maybe customary law /Soft law

instrument)-Impact national / EU law.

16

B. Definition of Resident for tax purposes

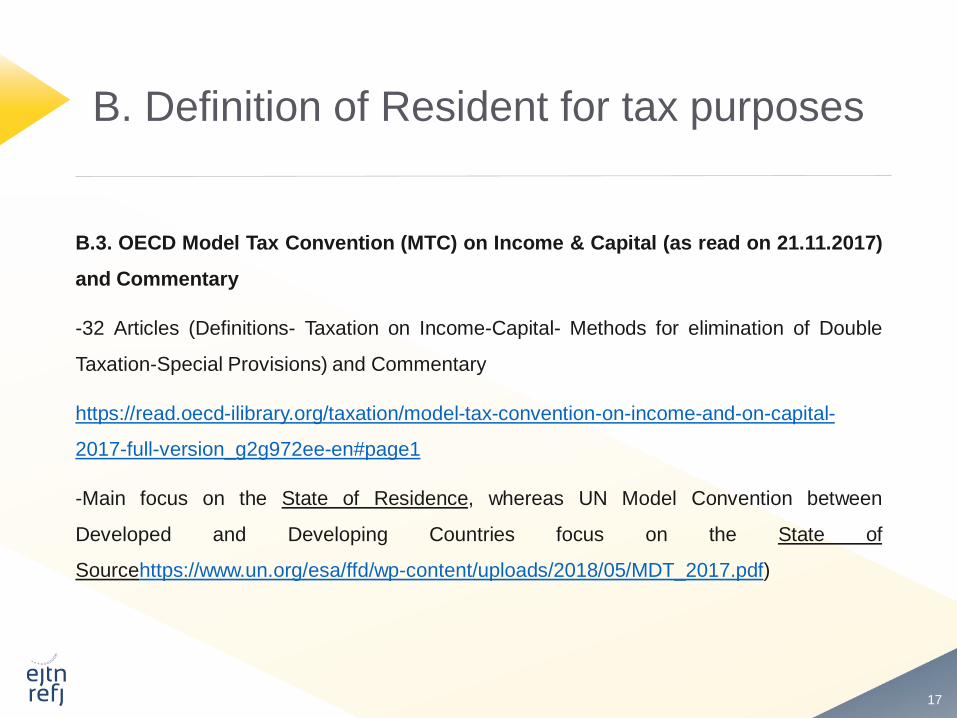

B.3. OECD Model Tax Convention (MTC) on Income & Capital (as read on 21.11.2017)

and Commentary

-32 Articles (Definitions- Taxation on Income-Capital- Methods for elimination of Double

Taxation-Special Provisions) and Commentary

https://read.oecd-ilibrary.org/taxation/model-tax-convention-on-income-and-on-capital-

2017-full-version_g2g972ee-en#page1

-Main focus on the State of Residence, whereas UN Model Convention between

Developed and Developing Countries focus on the State of

Sourcehttps://www.un.org/esa/ffd/wp-content/uploads/2018/05/MDT_2017.pdf)

17

B. Definition of Resident for tax purposes

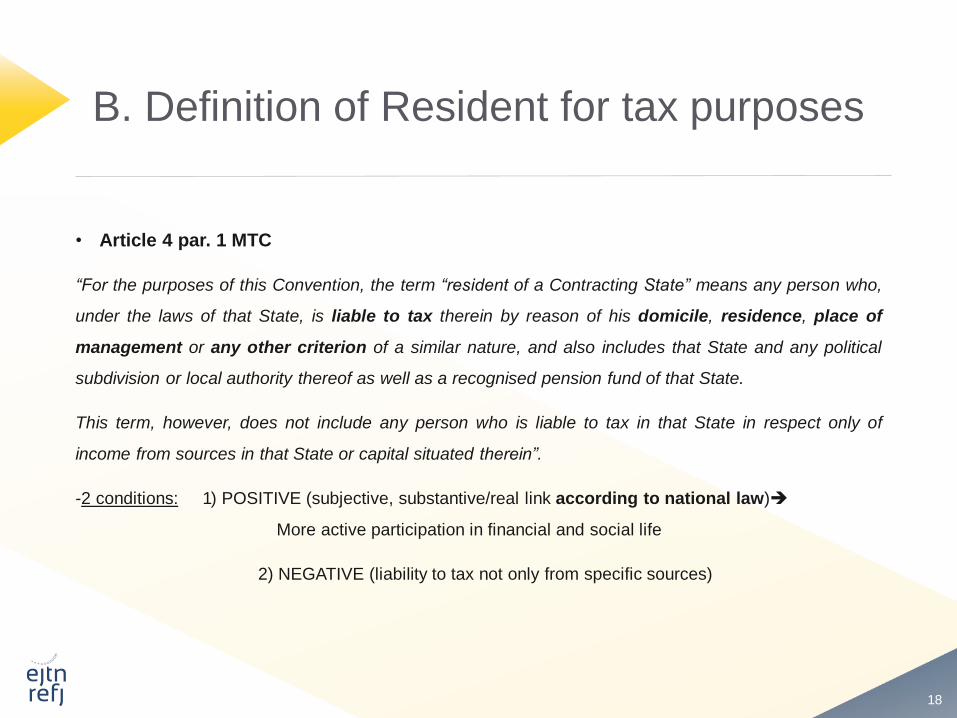

• Article 4 par. 1 MTC

“For the purposes of this Convention, the term “resident of a Contracting State” means any person who,

under the laws of that State, is liable to tax therein by reason of his domicile, residence, place of

management or any other criterion of a similar nature, and also includes that State and any political

subdivision or local authority thereof as well as a recognised pension fund of that State.

This term, however, does not include any person who is liable to tax in that State in respect only of

income from sources in that State or capital situated therein”.

-2 conditions: 1) POSITIVE (subjective, substantive/real link according to national law)➔

More active participation in financial and social life

2) NEGATIVE (liability to tax not only from specific sources)

18

B. Definition of Resident for tax purposes

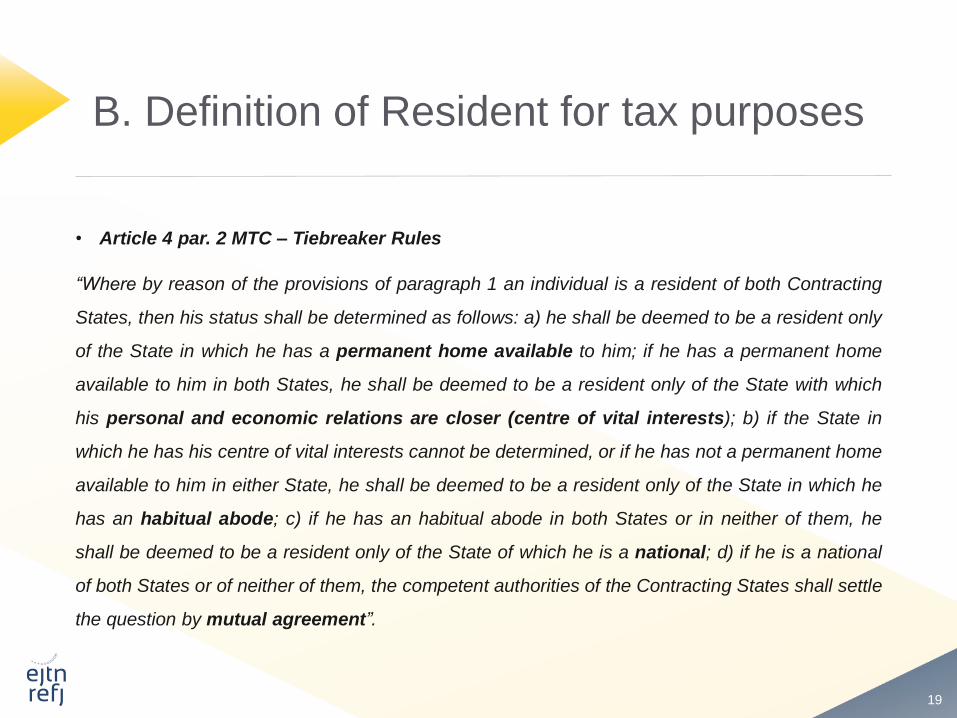

• Article 4 par. 2 MTC – Tiebreaker Rules

“Where by reason of the provisions of paragraph 1 an individual is a resident of both Contracting

States, then his status shall be determined as follows: a) he shall be deemed to be a resident only

of the State in which he has a permanent home available to him; if he has a permanent home

available to him in both States, he shall be deemed to be a resident only of the State with which

his personal and economic relations are closer (centre of vital interests); b) if the State in

which he has his centre of vital interests cannot be determined, or if he has not a permanent home

available to him in either State, he shall be deemed to be a resident only of the State in which he

has an habitual abode; c) if he has an habitual abode in both States or in neither of them, he

shall be deemed to be a resident only of the State of which he is a national; d) if he is a national

of both States or of neither of them, the competent authorities of the Contracting States shall settle

the question by mutual agreement”.

19

B. Definition of Resident for tax purposes

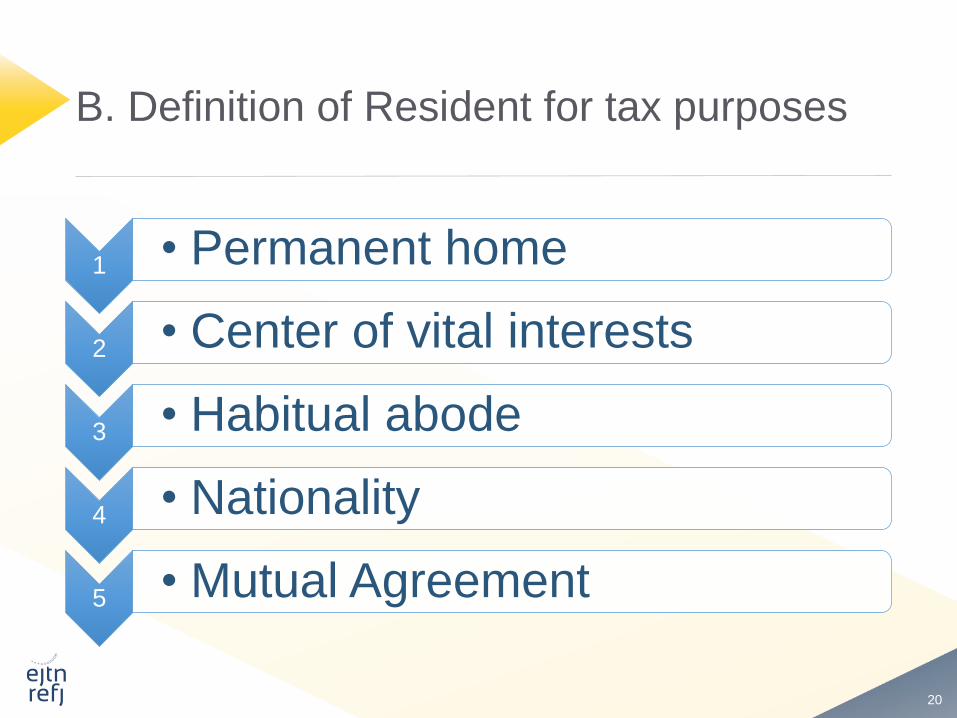

1 • Permanent home

2 • Center of vital interests

3 • Habitual abode

4 • Nationality

5 • Mutual Agreement

20

B. Definition of Resident for tax purposes

- All criteria apply hierarchically not alternatively.

- Permanent home (or domicile): any type of home / availability/ animus.

- Center of vital interests: all factors have to be examined.

- Habitual abode: physical presence of 183 days (see Article 15 of the MTC) – not only

physical presence (e.g. covid restrictions) – not necessarily consecutively.

- Mutual agreement Procedure (Article 25 of the MTC) – 3 stages (unilateral, bilateral,

arbitration).

- Exchange of information (Article of 26 of the MTC) –Also, relevant Council Directive

2011/16/EU of 15 February 2011 on administrative cooperation in the field of taxation (C-

682/15 Berlioz).

21

B. Definition of Resident for tax purposes

• B.4 EU law

-No consensus for a multilateral treaty concerning the avoidance of double taxation – A Draft in 1968 (EC Commission

Document 11.414/WIV/68) was never adopted.

-In Article 293 of the EC Treaty (Official Journal C 325 ,24/12/2002) MS were urged to negotiate in view of the abolition of

double taxation, but this provision was later repealed by the Treaty of Lisbon (no direct applicability to the benefit of

taxpayers).

-“Community law, in its current state and in a situation such as that in the main proceedings, does not lay down any general

criteria for the attribution of areas of competence between the Member States in relation to the elimination of double taxation

within the Community. Apart from Council Directive 90/435/EEC of 23 July 1990 on the common system of taxation

applicable in the case of parent companies and subsidiaries of different Member States (OJ 1990 L 225, p. 6), the

Convention of 23 July 1990 on the elimination of double taxation in connection with the adjustment of profits of associated

enterprises (OJ 1990 L 225, p. 10) and Council Directive 2003/48/EC of 3 June 2003 on taxation of savings income in the

form of interest payments (OJ 2003 L 157, p. 38), no uniform or harmonisation measure designed to eliminate double

taxation has as yet been adopted at Community law level.” (C-513/04 Kerckhaert – Morres par. 22, also relevant C-540/11

Levy & Sebbag etc.)

22

B. Definition of Resident for tax purposes

➢ C-262/99 Louloudakis

“[…] must be interpreted as meaning that, where a person has both personal and occupational ties in two Member States, his normal

residence, determined in the context of an overall assessment by reference to all the relevant facts, is that where the permanent centre of

interests of that person is located; in the event that such an overall assessment does not result in its determination, primacy must be given

to personal ties.”

➢ C- 392/05 Alevizos

“[…] All of the relevant facts must be taken into consideration in determining normal residence as the permanent centre of interests of the

person concerned (see Ryborg paragraph 20), namely, in particular, the actual presence of the person concerned and of the members of

his family, the availability of accommodation, the place where the children actually attend school, the place where business is conducted,

the place where property interests are situated, that of administrative links to public services and social services, inasmuch as those

factors express the intention of that person to confer a certain stability on the place of connection, by reason of the continuity arising from

a way of life and the development of normal social and occupational relationships (see Louloudakis, paragraph 55).”

23

B. Definition of Resident for tax purposes

-Finally, another relevant EU legal instrument implying the notion of resident is Council Directive

2017/1852 on resolution on tax disputes by mutual arrangements (Dispute Resolution Directive),

which applies on all kinds of income tax disputes (individual – business) as of 1.7.2019. Already

since 1990 the Multilateral Arbitration Convention 90/463 on the elimination of double taxation in

connection with the adjustment of profits of associated enterprises.

-MS may not invoke DTTs’ provisions to override EU law (C-170/05 Denkavit, C-265/04

Bouanich)- There are currently DTTs in force for almost all MS with each other – a network of

around 300 Treaties (exceptions are Cyprus-Croatia, Cyprus –Netherlands, Denmark-France).

-MS may agree on the ECJ as Arbitration Court for disputes under DTTs in combination to Article

273 TFEU (Case C-648/15 Austria v. Germany par. 39)

-Indirect impact of non discrimination principle in relation to fundamental freedoms.

24

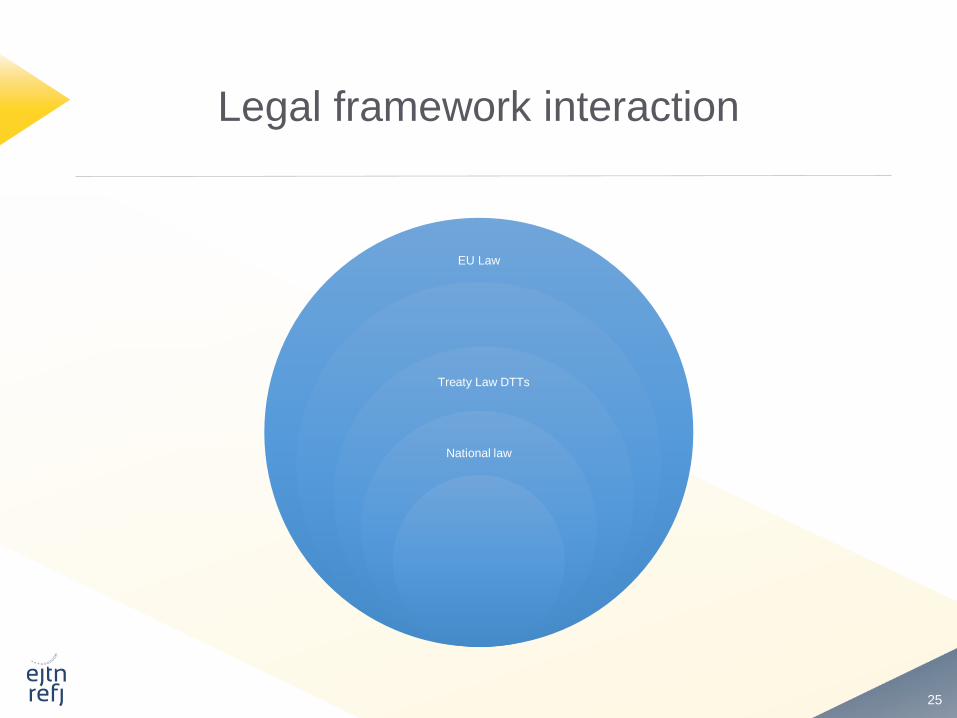

Legal framework interaction

EU Law

Treaty Law DTTs

National law

25

Examples

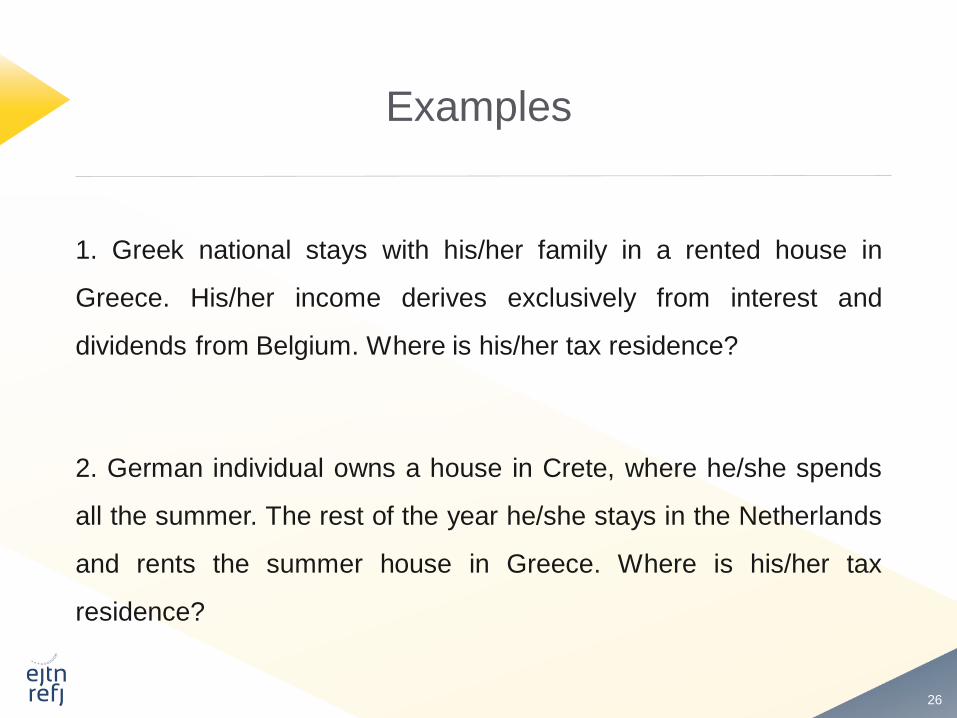

1. Greek national stays with his/her family in a rented house in

Greece. His/her income derives exclusively from interest and

dividends from Belgium. Where is his/her tax residence?

2. German individual owns a house in Crete, where he/she spends

all the summer. The rest of the year he/she stays in the Netherlands

and rents the summer house in Greece. Where is his/her tax

residence?

26

Examples

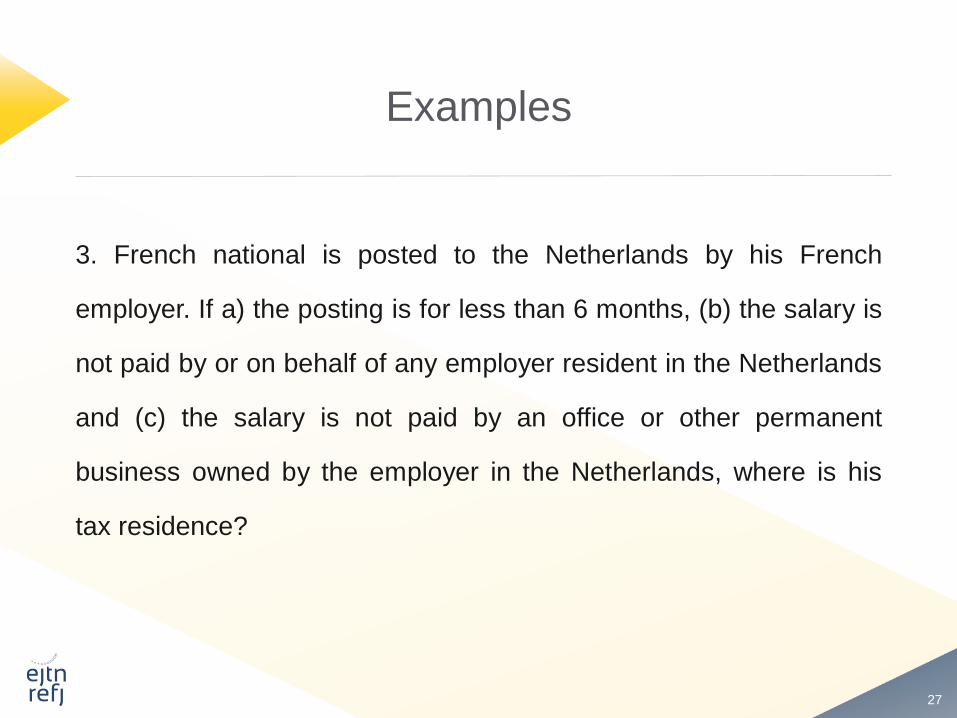

3. French national is posted to the Netherlands by his French

employer. If a) the posting is for less than 6 months, (b) the salary is

not paid by or on behalf of any employer resident in the Netherlands

and (c) the salary is not paid by an office or other permanent

business owned by the employer in the Netherlands, where is his

tax residence?

27

Examples

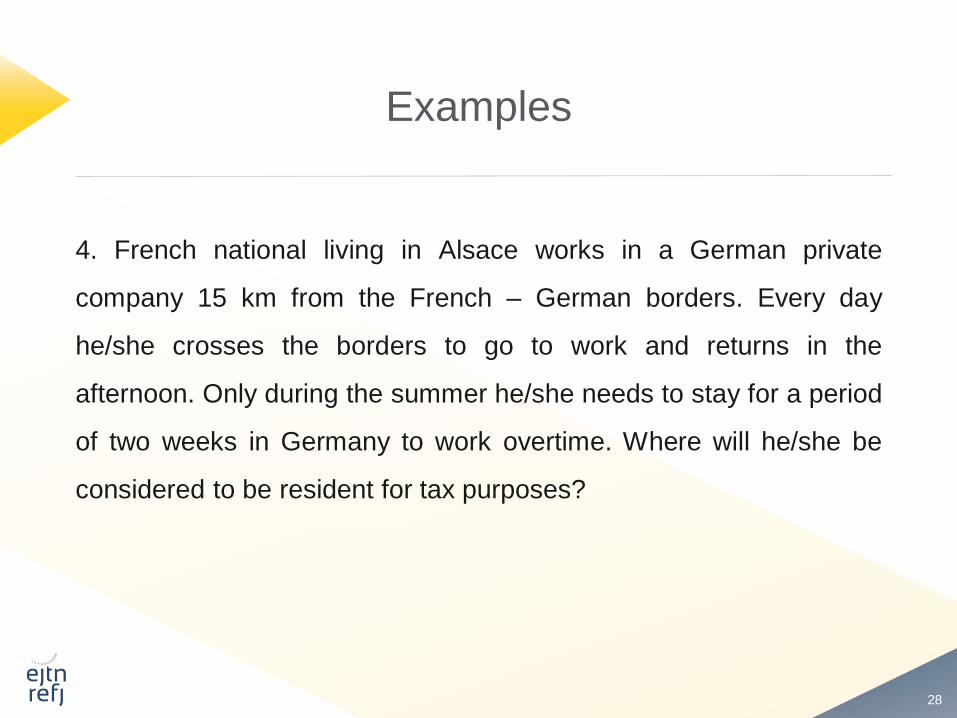

4. French national living in Alsace works in a German private

company 15 km from the French – German borders. Every day

he/she crosses the borders to go to work and returns in the

afternoon. Only during the summer he/she needs to stay for a period

of two weeks in Germany to work overtime. Where will he/she be

considered to be resident for tax purposes?

28

Examples

5. Danish national is married to a Dutch resident and national, with

whom she has two children, both Danish and Netherlands citizens.

The family lives in a house in the Netherlands, which they own. The

Danish individual used to work and live partly during the year in

Denmark. She is now working on a fulltime basis during the week in

Luxembourg under a permanent employment contract, and she has

bought an apartment to stay during the week and some weekends

during the year depending on her workload. Based on the facts and

circumstances, where is her tax residence?

29

C. Proving tax residence- The transfer of tax residence

-National tax authorities have to prove the existence of tax residence in order to

exercise their jurisdiction to tax and taxpayers have the right to counter prove.

-Respectively the transfer of residence has to be proved by taxpayers.

-Mostly important is the tax residence certificate (Apostille) or the Claim for the

Application of the existing DTT (tax residence certificate is embedded). Other

documentation: tax return or tax clearance form.

-Documentation required to prove the transfer of residence is more demanding. It

refers to the previous year. It usually includes certificate of employment, social

security contributions’ certificate, confirmation of abode by public-municipal

authorities, school certificates for the children, lease contracts, utility invoices etc. All

of them have to be Apostilled and if necessary translated.

30

C. Proving tax residence-The transfer of tax residence

-Spouses may have different residencies, notwithstanding their

obligation to file a common tax return (C-87/99 Patrick Zurstrassen).

Additional documentation may be required.

-Case by case approach: membership in a listed company, ownership

of a private business, registration in professional registries, lease of

property via Airbnb or other similar platforms (have been considered not

to be unconditionally sufficient).

-Focus on the country with the strongest financial link with an individual

(holistic approach).

31

C. Proving tax residence

• Presumptions are used in various ways. In any case they should not be irrefutable, as the objective is to

establish real situations.

A. To establish tax residence

➢ Proof of physical presence of an individual in one country for more than 183 days in a year or

➢ Failure to prove tax residence in another State (within a deadline)

B. To reject applications for the transfer of tax residence

➢ When the transfer concerns a country with privileged tax rates. In this case, sticky or clinging rules may apply

providing for a certain period the levy of tax on worldwide income despite the transfer. The above may be

justified as an anti avoidance practice. However, no general presumption of tax avoidance or tax evasion

should apply (C-581/17 Martin Wächtler, C-9/02 Hughes de Lasteyrie du Saillant). There should always be the

possibility to prove that the transfer is real.

32

Examples

1. Greek national has transferred his/her tax residence in Switzerland, as he began working for a Swiss company

on 21/4. With his application he filed salary slips from the company he is working at in Switzerland, certificate for

the withholding tax imposed in his salary, social security contributions’ payment certificate, certificate from the

Municipality of the town he is living in Switzerland verifying that he is resident after moving there from Greece (for

a short period), certificate from the tax authorities of the Swiss canton that he is considered to be tax resident in

Switzerland as of 1/8 of the present year under the DTT between Greece and Switzerland meaning that he is

liable to pay tax for his worldwide income in Switzerland.

The Greek tax authorities rejected his application to transfer his tax residence on the basis that he is married and

his wife and minor children continued to stay in Greece until November of the current year considering that the

center of his vital interests was in Greece. The main reasoning of the Greek tax authorities’ decision was that in

this context family personal ties are deemed to be more important than professional ties.

There was an appeal before the Greek Council of State. What do think was its judgment?

33

Examples

2. Greek national and resident asked the transfer of her tax residence in 2019, in order to be considered as tax

resident in the UK from 2018 onwards. She was employed by a private bank in Greece from 2002 (dependent

employment), however since 2017 she was on unpaid leave ending in 2022. She submitted along with her

application: (a) UK tax residence certificate, covering the period between 2017-2019, (b) long term lease

agreement covering the period between 2018-2019, (c) certificate by the University of Lancaster attesting that she

has been working as a Lecturer from 2017 by virtue of a permanent contract. Her request was rejected by the

Greek tax authorities, as her employment, regardless of her leave, was considered to indicate that Greece

remained as the center of her vital interests. She appealed before the Greek Council of State. Additionally, she

submitted before the Court, among others: (a) social security contributions’ certificates attesting that her insurance

in Greece was interrupted in 2017 upon her leave and respectively commenced in the UK 2017, (b) payment slips

by the aforementioned University, (c) bank account statements from UK banks, (d) utility accounts (electricity,

telephone) and (e) municipal tax assessment act. What do think was Greek CoS judgment?

34

D. Non Dom individuals

• In principle tax residence has to correspond to a real situation and not purely artificial arrangements (C – 135/17 X

GmbH).

• However, some EU countries (Ireland, Italy, Portugal, Malta, Cyprus and since 2020 Greece), as well as the UK and

Switzerland grant privileges to high net worth individuals (or pensioners), resident in other countries for them to transfer

their tax residence (notwithstanding the fact that the relevant substantive conditions are not met), so that they will be

subject to tax for their worldwide income in a country other than the one of their actual residence (domicile of choice).

Certain conditions have to be met (e.g. no domicile in the respective country for the past years, investment in real estate

etc). Also, certain time – limits apply.

• The privileges usually consist in a flat tax rate (or flat tax amount) for all their income derived abroad with exhaustion of

tax the liability. Additionally, an exemption from inheritance/gift taxes abroad is provided. If any tax has been paid abroad,

it may not be credited in the state of the domicile of choice.

• Risk of harmful tax competition – Recently, the European Union Tax Observatory qualified Greece’s non-domicile

scheme as a particularly harmful form of tax competition, as it offers tax privileges for more than eight years (namely 15

years), appealing not only to “high net worth” individuals with the precondition to invest in Greece but also to pensioners,

without asking from them any activity in the local economy.

35

D. Non Dom individuals

• The main concerns are the following:

(a) Conflict with DTTs that normally have increased legal effect following their ratification in most jurisdictions. It

may not be excluded that those individuals continue to be considered as tax residents by the tax authorities in

the countries they actually maintain their tax residence under the relevant substantive criteria (double juridical

taxation). Could their choice establish an irrefutable presumption?

(b) Double taxation if there are provisions excluding the credit of tax paid in the country of actual residence (as in

Greece).

(c) What happens when the duration of this “special tax regime” has been completed. Does this situation qualify as

a transfer? Who bears the burden of proof? Exit taxation issues (Directive 2016/1164/EC)

(d) Discrimination issues raised by actual residents of the same State.

36

Example

• Italian national individual moved to the UK and established regular place of abode there. He/she

cancelled himself/herself from the register of Italian resident individuals in Italy and registered as an

Italian citizen, resident abroad (expatriate-non dom), in the Italian consulate in London. However, the

Italian tax authorities considered that he/she has remained resident for tax purposes in Italy and

imposed income taxes on his/her worldwide income following an audit. He/she appealed before the

Italian Supreme Court and invoked: (a) internal Italian tax law in relation to his/her habitual abode in

the UK and not Italy, meaning the place where somebody regularly lives with the intention to live there

indefinitely (other alternative tests in Italy are registration on the register of Italian resident individuals

for more than 6 months in a tax year or the individual’s main center of interest and affairs), (b) the UK-

Italian DTT (Article 4 par. 2) in relation to having a permanent home in the UK (and not in Italy), where

he/she maintains the most meaningful personal, family and social relations, as well as financial and

economic interests. What do you think was the Court’s decision about the right of the taxpayer to

invoke the UK-Italian DTT?

37

E. Poll Questions

1. Every State may set its own criteria to establish the existence of tax residence. True or false?

A. True

B. False

2. Non residents may always claim the same tax treatment as residents. True or false ?

A. True

B. False

3. Tax authorities in every state have to prove that a taxpayer is resident for tax purposes in its territory?

A. True

B. False

38

With financial support from the Justice

Programme of the European Union

Thank you!