FOREIGN VERSUS DOMESTIC CURRENCY D£BT FINANCING ...

177

FOREIGN VERSUS DOMESTIC CURRENCY D£BT FINANCING by KENNETH MOON, B.B.A., M.S. A DISSERTATION IN BUSINESS ADMINISTRATION Submitted to the Graduate Faculty of Texas Tech University in Partial Fulfillment of the Requirements for the Degree of DOCTOR OF PHILOSOPHY Approved December, 1997

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of FOREIGN VERSUS DOMESTIC CURRENCY D£BT FINANCING ...

FOREIGN VERSUS DOMESTIC CURRENCY

D£BT FINANCING

by

KENNETH MOON, B.B.A., M.S.

A DISSERTATION

IN

BUSINESS ADMINISTRATION

Submitted to the Graduate Faculty of Texas Tech University in

Partial Fulfillment of the Requirements for

the Degree of

DOCTOR OF PHILOSOPHY

Approved

December, 1997

^B

i c:

Copyright © 1994, Kenneth P. Moon

TABLE OF CONTENTS

LIST OF TABLES jv

LIST OF FIGURES xi

CHAPTER

I. INTRODUCTION I

II. DOMESTIC FIRM VALUE AND THE

DEBT DENOMINATION DECISION 8

Introduction 8

Reviewof Existing Literature 9

Summary and Motivation for Additional Research 24

III. THEORETICAL UNDERPINNINGS 27

Introduction 27

A Generalized Analysis 28

Intemational Equilibrium Redefined 38

Summary 42

IV. EMPIRICAL DESIGN AND DATA DESCRIPTION . . . . 44

Introduction 44

Event Methodology Test Statistic 45

Data Description and Empirical Design 49

Summary 56

11

V. SAMPLING PROCEDURES AND EMPIRICAL ANAI ^ SES . 57

Introduction ^7

Sampling Procedure X

Empirical Analysis 64

Data Evaluation 64

Event Methodology Results 68

One-Way AXOVA Results 72

Paired T-Test Results 78

Additional Empirical Analyses 81

Summary 90

VI. SUMMARY AND CONCLUSIONS 93

ENDNOTES 100

BIBLIOGRAPHY 103

APPENDICES

A. SUMMARY STATISTICS 106

B. EVENT METHODOLOGY RESULTS 120

C. ONE-WAY ANOVA RESULTS 126

D. PAIRED T-TEST RESULTS 134

E. MATURITY CONTROL ANALYSES 139

F. FOREIGN CURRENCY ANALYSES 159

111

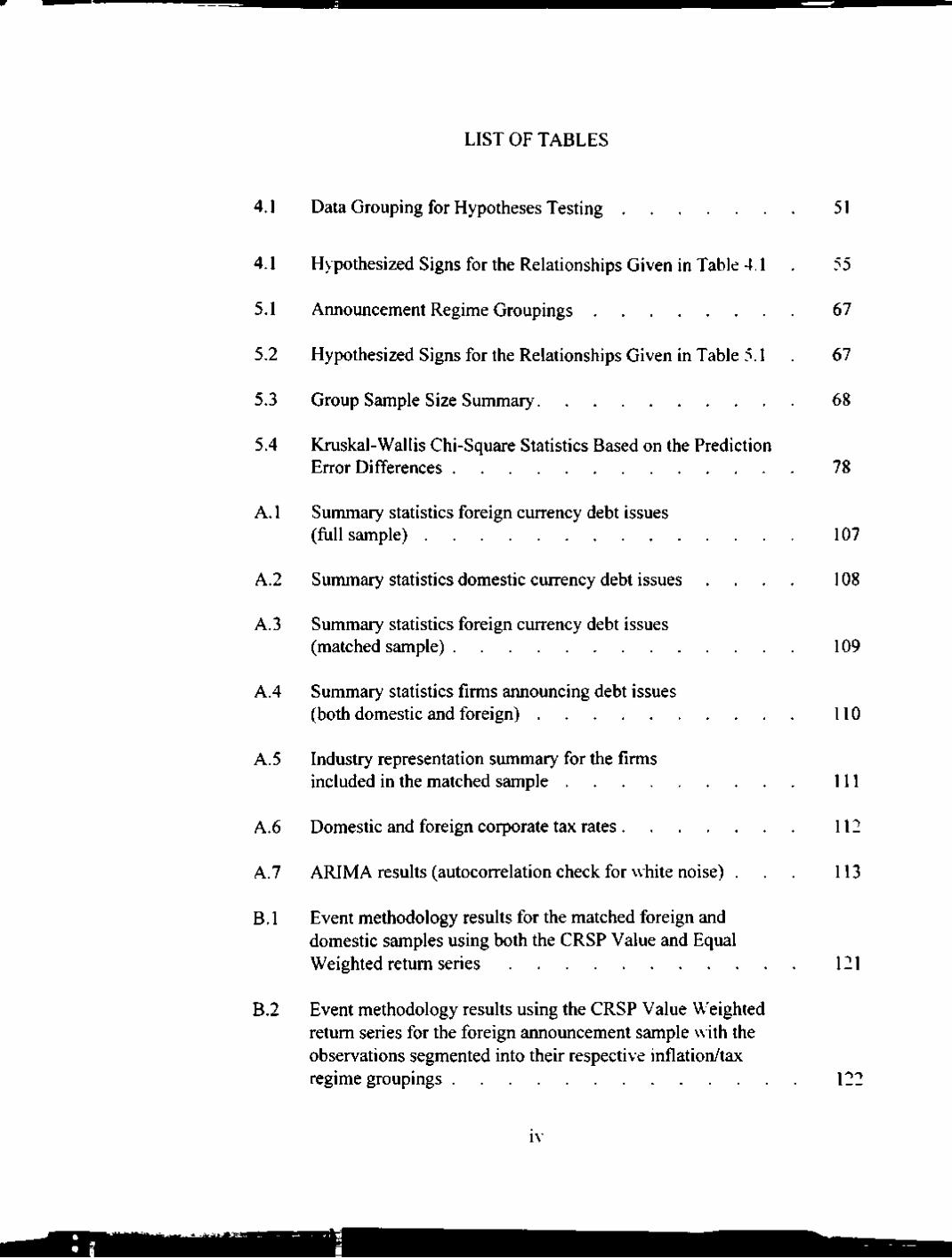

LIST OF TABLES

4.1 Data Grouping for Hypotheses Testing 51

4.1 Hypothesized Signs for the Relationships Given in Table 4.1 55

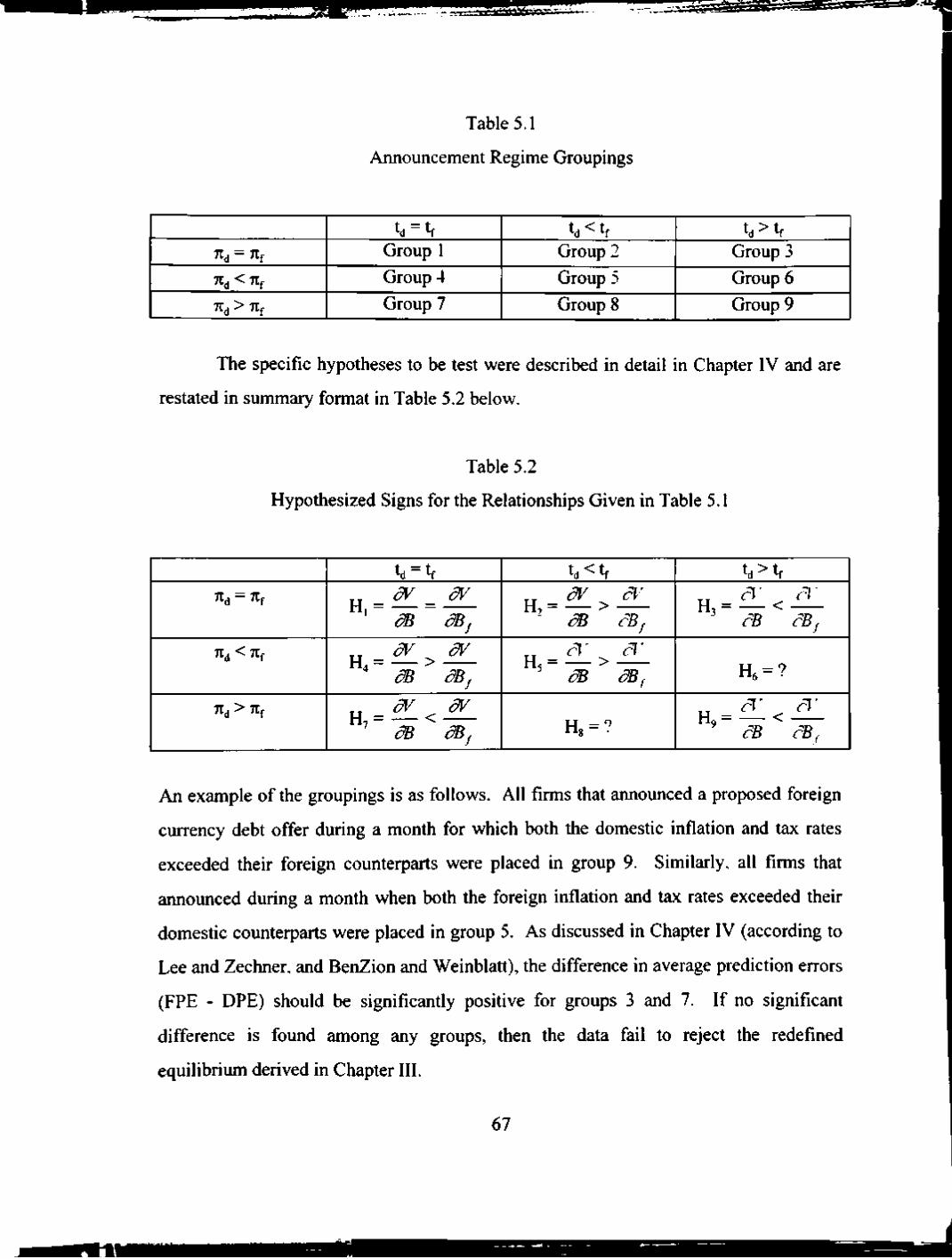

5.1 Announcement Regime Groupings 67

5.2 Hypothesized Signs for the Relationships Given in Table 5.1 . 67

5.3 Group Sample Size Summary 68

5.4 Kmskal-Wallis Chi-Square Statistics Based on the Prediction Error Differences 78

A.l Summary statistics foreign currency debt issues

(full sample) 107

A.2 Summary statistics domestic currency debt issues . . . . 108

A.3 Summary statistics foreign currency debt issues (matched sample) 109

A.4 Summary statistics firms announcing debt issues (both domestic and foreign) 110

A.5 Industry representation summary for the firms

included in the matched sample I l l

A.6 Domestic and foreign corporate tax rates 112

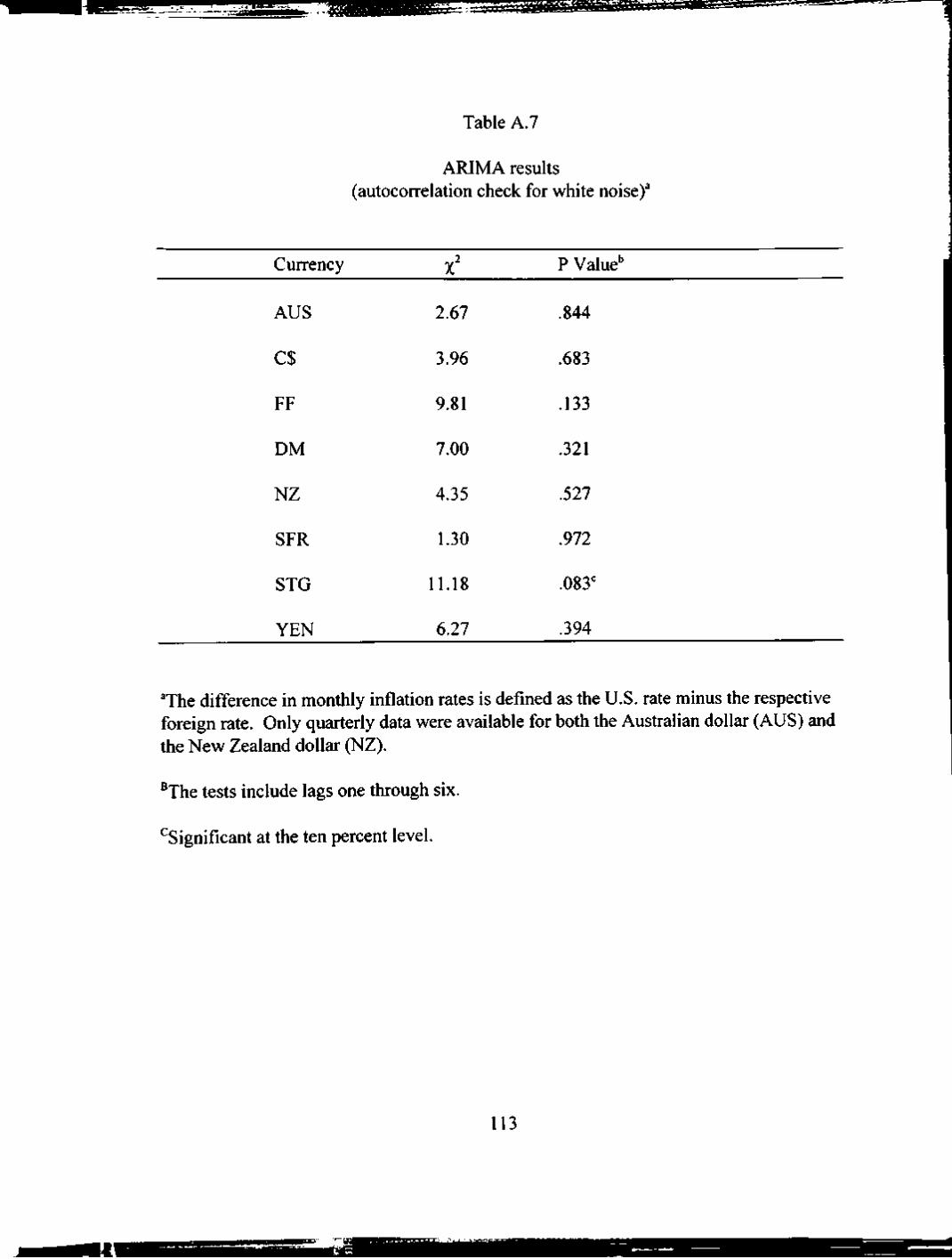

A.7 ARIMA results (autocorrelation check for white noise) . . 113

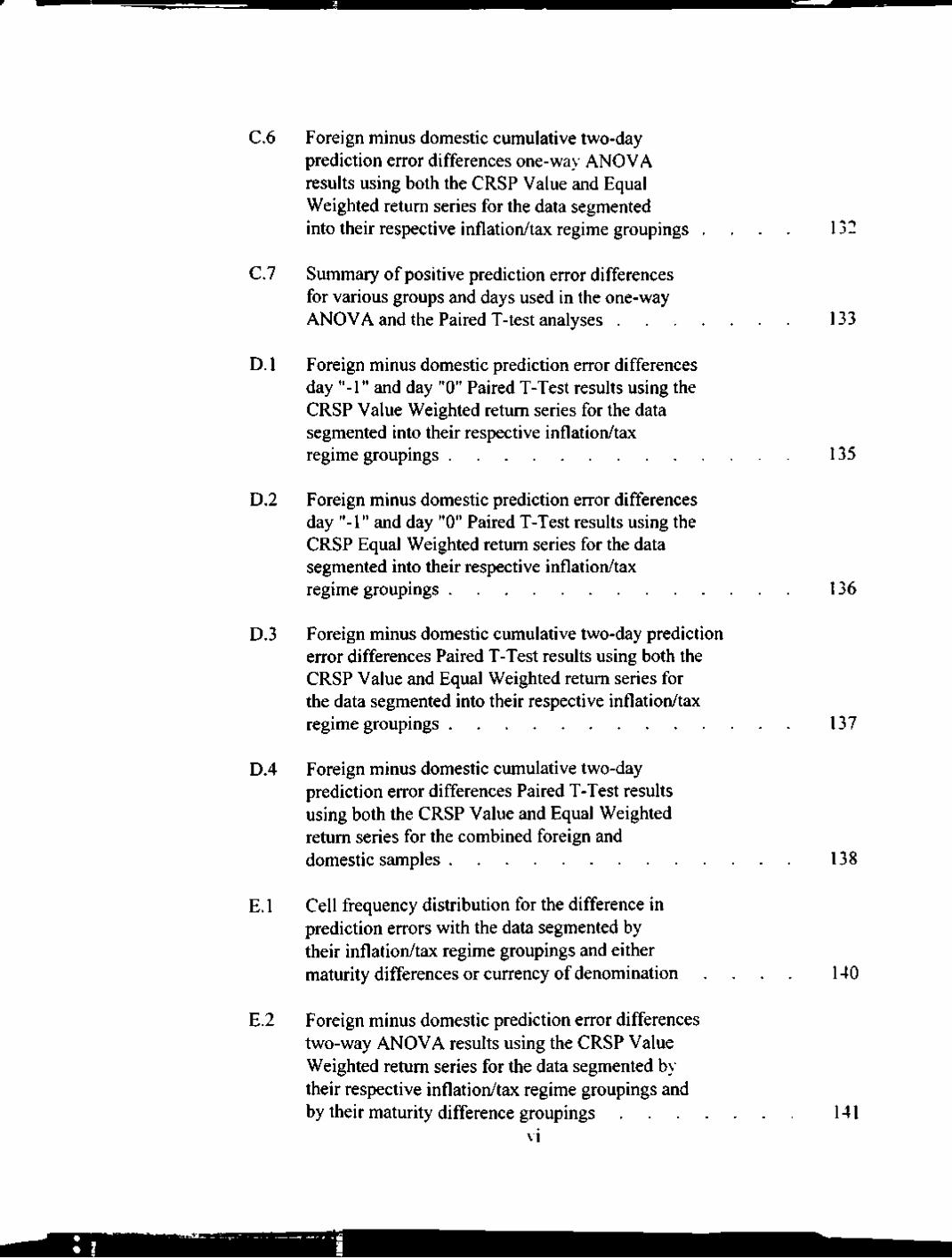

B. 1 Event methodology results for the matched foreign and domestic samples using both the CRSP Value and Equal Weighted return series 121

B.2 Event methodology results using the CRSP Value Weighted return series for the foreign announcement sample with the observations segmented into their respective inflation/tax regime groupings 122

i \

B.3

B.4

B.5

C.l

C.2

C.3

Event methodology results using the CRSP Equal Weighted return series for the foreign announcement sample with the observations segmented into their respecti\ e inflation/tax regime groupings

Non-parametric event methodology results using the CRSP Value and Equal Weighted return series for the foreign announcement sample with the observations segmented into their respective inflation/tax regime groupings .

Small sample non-parametric event methodology results using the CRSP Value and Equal Weighted return series for the foreign announcement sample with the observations segmented into their respective inflation/tax regime groupings

Day "-1" and day "0" prediction error one-way ANOVA results using the CRSP Value Weighted return series for the data segmented into their respective inflation/tax regime groupings

Day "-1" and day "0" prediction error one-way ANOVA results using the CRSP Equal Weighted return series for the data segmented into their respective inflation/tax regime groupings

Cumulative two-day prediction error one-way ANOVA results using both the CRSP Value and Equal Weighted return series for the data segmented into their respective inflation/tax regime groupings

12 J

124

125

127

128

129

C.4 Foreign minus domestic prediction error differences day "-1" and day "0" one-way ANOVA resuhs using the CRSP Value Weighted return series for the data segmented into their respective inflation/tax regime groupings 130

C.5 Foreign minus domestic prediction error differences day "-1" and day "0" one-way ANOVA results using the CRSP Equal Weighted return series for the data segmented into their respective inflation/tax regime groupings 131

C.6 Foreign minus domestic cumulative two-day prediction error differences one-way ANOVA results using both the CRSP Value and Equal Weighted return series for the data segmented into their respective inflation/tax regime groupings . . . 132

C.7 Summary of positive prediction error differences for various groups and days used in the one-way ANOVA and the Paired T-test analyses 133

D. 1 Foreign minus domestic prediction error differences day "-1" and day "0" Paired T-Test results using the CRSP Value Weighted return series for the data segmented into their respective inflation/tax regime groupings 135

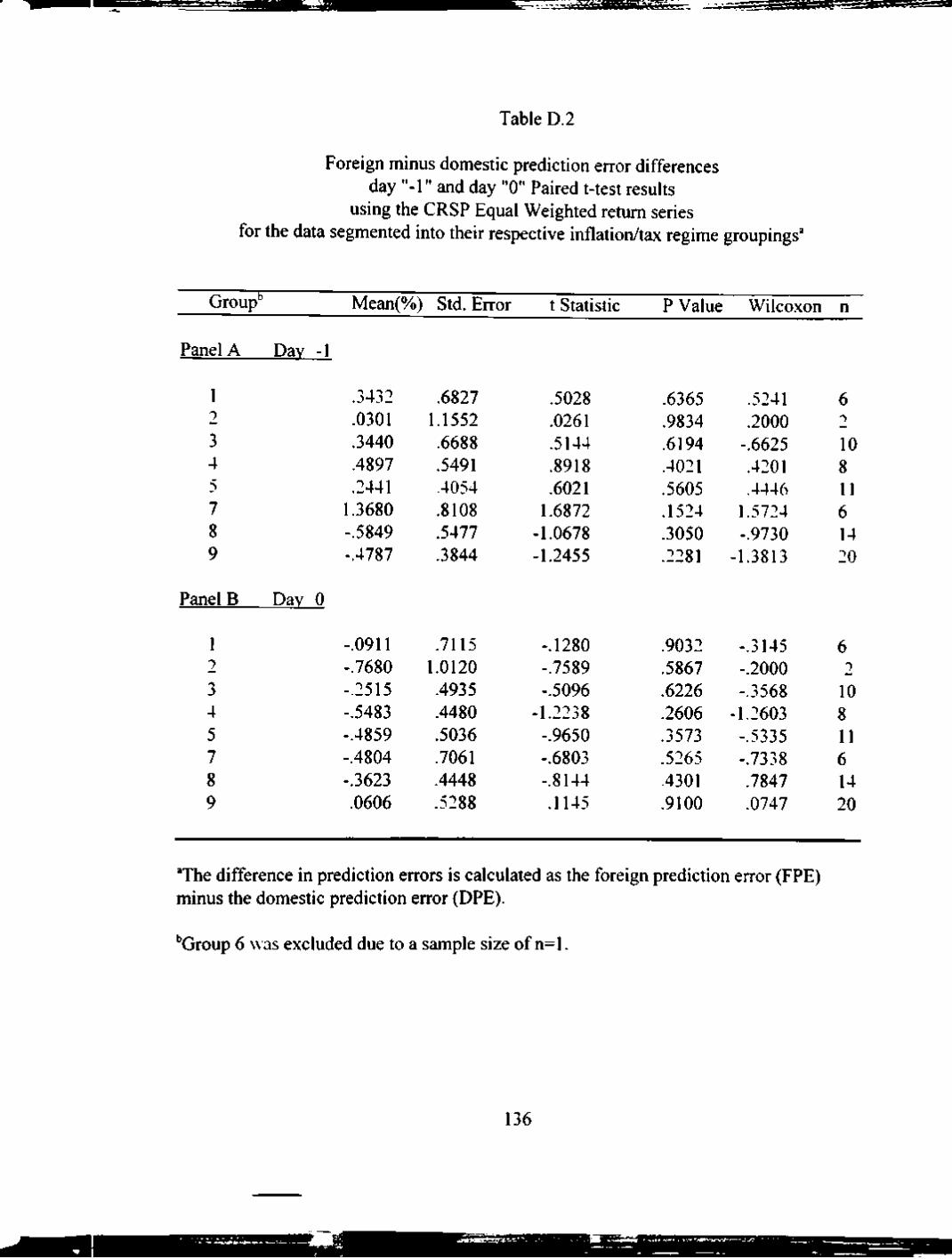

D.2 Foreign minus domestic prediction error differences day "-1" and day "0" Paired T-Test results using the CRSP Equal Weighted return series for the data segmented into their respective inflation/tax regime groupings 136

D.3 Foreign minus domestic cumulative two-day prediction error differences Paired T-Test results using both the CRSP Value and Equal Weighted return series for the data segmented into their respective inflation/tax regime groupings 137

D.4 Foreign minus domestic cumulative two-day prediction error differences Paired T-Test results using both the CRSP Value and Equal Weighted return series for the combined foreign and domestic samples 138

E. 1 Cell frequency distribution for the difference in prediction errors with the data segmented by their inflation/tax regime groupings and either maturity differences or currency of denomination . . . . 140

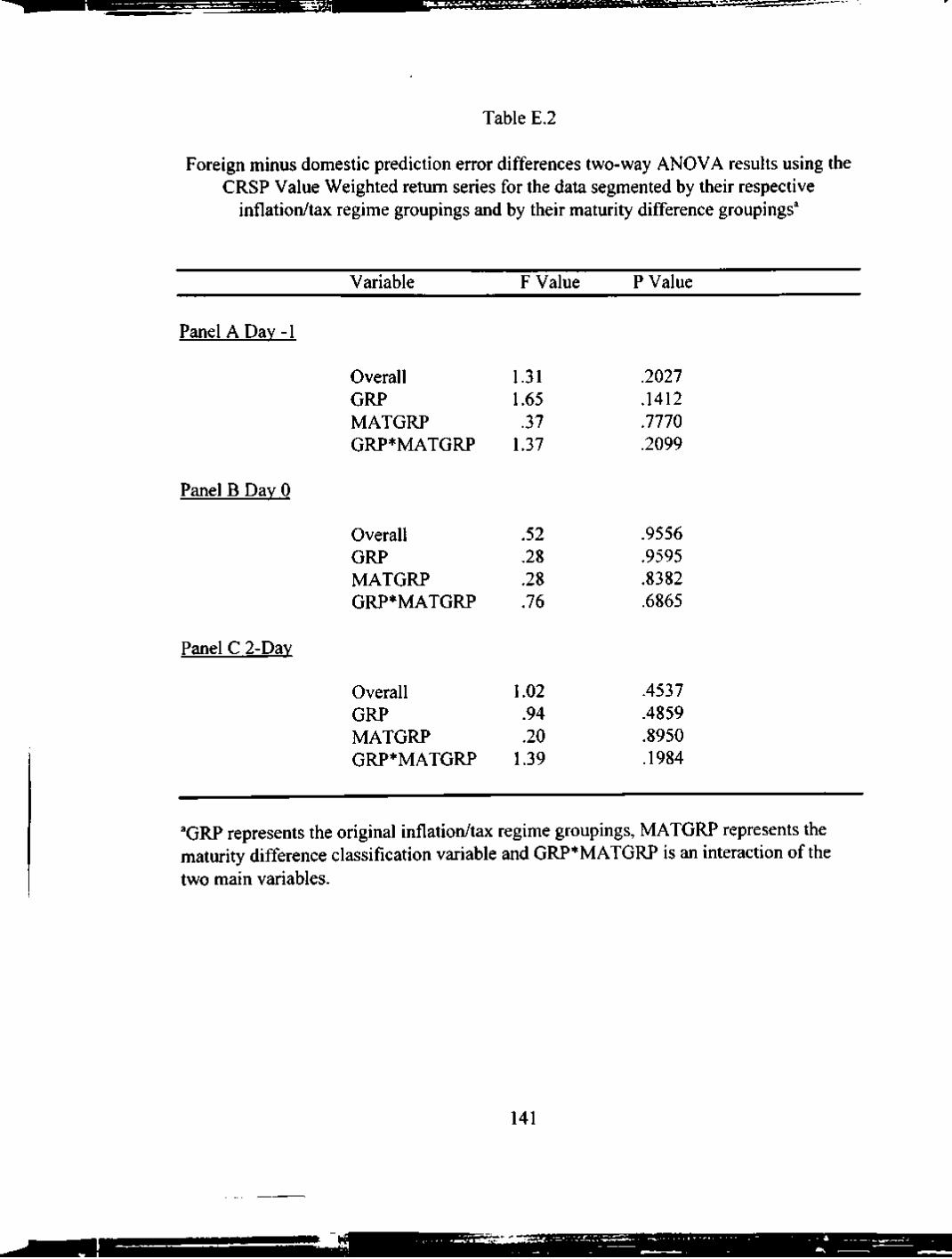

E.2 Foreign minus domestic prediction error differences two-way ANOVA resuhs using the CRSP Value Weighted return series for the data segmented b>' their respective inflation/tax regime groupings and by their maturity difference groupings 141

vi

E.3

E.4

E.5

E.6

Foreign minus domestic prediction error differences two-way ANOVA results using the CRSP Equal Weighted return series for the data segmented by their respective inflation/tax regime groupings and by their maturity difference groupings

Foreign minus domestic prediction error differences two-way ANOVA results using the CRSP Value Weighted return series for the collapsed data segmented by their respective inflation/tax regime groupings and by their maturity difference groupings

Foreign minus domestic prediction error differences two-way ANOVA results using the CRSP Equal Weighted return series for the collapsed data segmented by their respective inflation/tax regime groupings and by their maturity difference groupings

Foreign minus domestic prediction error differences two-way ANOVA results using the CRSP Value Weighted return series for the data segmented by their respective inflation/tax regime groupings and by their maturity difference groupings (Groups 4, 5, 8. 9 and Maturity Groups 1 & 4)

142

143

144

145

E.7 Foreign minus domestic prediction error differences two-way ANOVA results using the CRSP Equal Weighted return series for the data segmented by their respective inflation/tax regime groupings and by their maturity difference groupings (Groups 4. 5. 8, 9 and Maturity Groups 1 & 4) 146

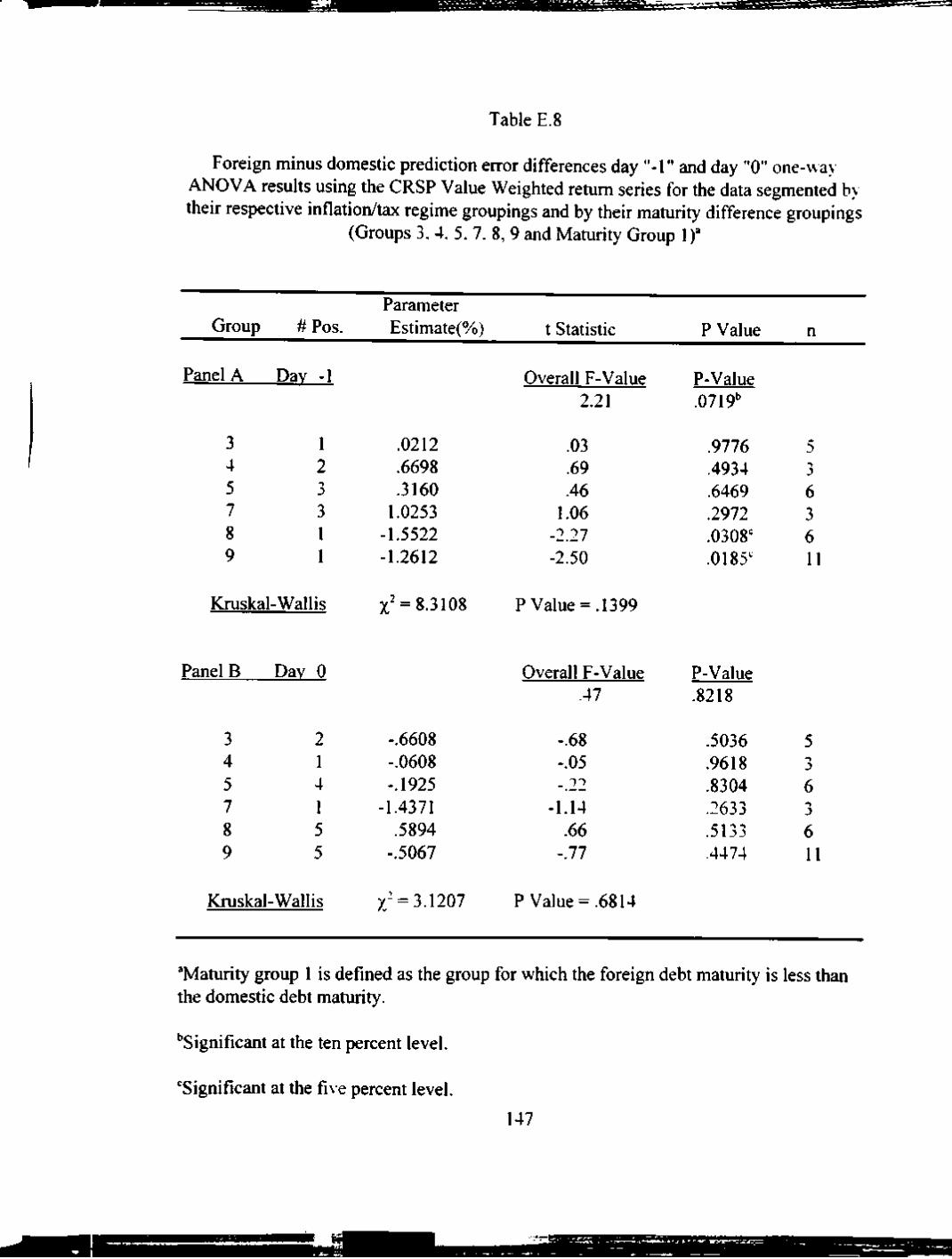

E.8 Foreign minus domestic prediction error differences day "-1" and day "0" one-way ANOVA results using the CRSP Value Weighted return series for the data segmented by their respective inflation/tax regime groupings and by their maturity difference groupings (Groups 3. 4, 5, 7. 8, 9 and Maturity Group 1) 147

vii

E.9

E.IO

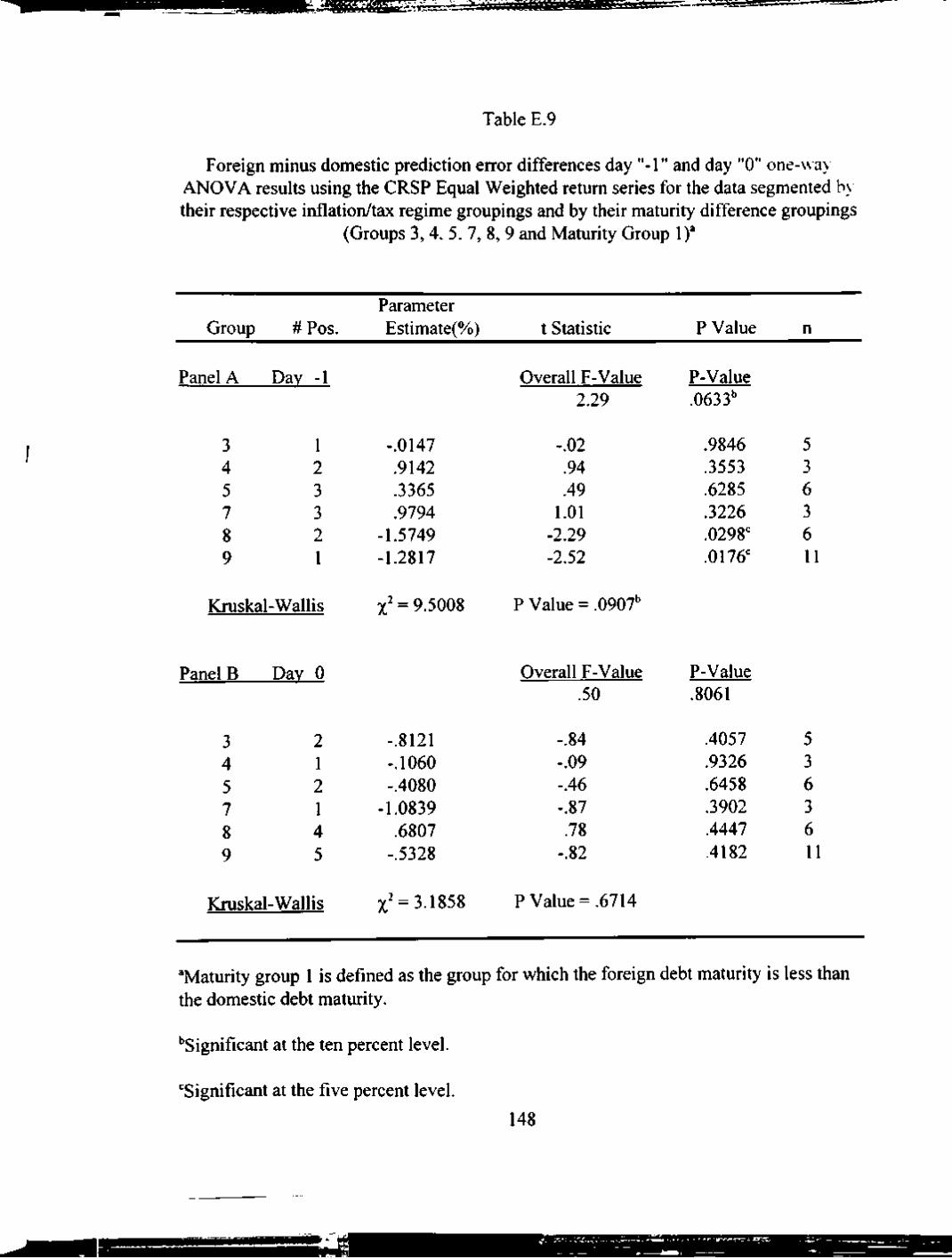

Foreign minus domestic prediction error differences day "-1" and day "0" one-way ANOVA results using the CRSP Equal Weighted return series for the data segmented by their respectiv e inflation/tax regime groupings and by their maturity difference groupings (Groups 3, 4. 5.1, 8, 9 and Maturity Group 1)

Foreign minus domestic cumulativ e two-day prediction error differences one-way ANOVA results using both the CRSP Value and Equal Weighted return series for the data segmented by their respectiv e inflationytax regime groupings and by their maturity difference groupings (Groups 3. 4, 5. 7. 8, 9 and Maturity Group 1)

148

149

E. 11 Foreign minus domestic prediction error differences day "-1" and day "0" one-way ANOVA results using the CRSP Value Weighted return series for the data segmented by their respective inflation/tax regime groupings and by their maturity difference groupings (Groups 1. 4. 5, 8, 9 and Maturity' Group 4) . 150

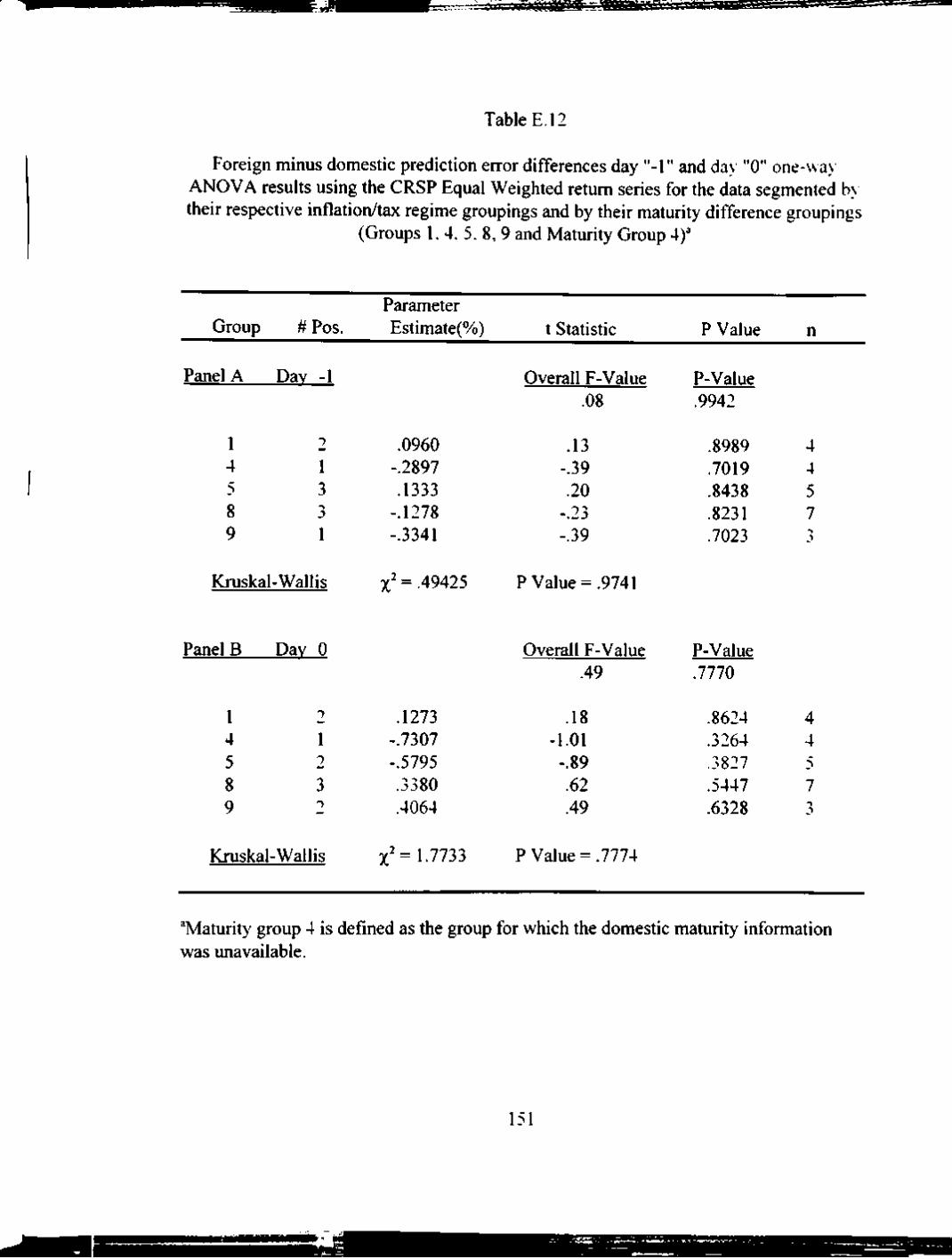

E. 12 Foreign minus domestic prediction error differences day "-1" and day "0" one-way ANOVA results using the CRSP Equal Weighted return series for the data segmented by their respective inflation/tax regime groupings and by their maturity difference groupings (Groups 1. 4. 5, 8, 9 and Maturity Group 4) . 151

E.13 Foreign minus domestic cumulative two-day prediction error differences one-way ANOVA results using both the CRSP Value and Equal Weighted return series for the data segmented by their respectiv e inflation/tax regime groupings and by their maturitv difference grouping (Groups 1. 4. 5. 8. 9 and Maturity Group 4) 152

E. 14 Foreign minus domestic prediction error differences day "-1" and day "0" one-way ANOV.A. results using the CRSP Value \\ eighted return series for the inflation/tax regime group 9 across all maturitv difference groupings 53

V l l l

E.15

E.16

E.17

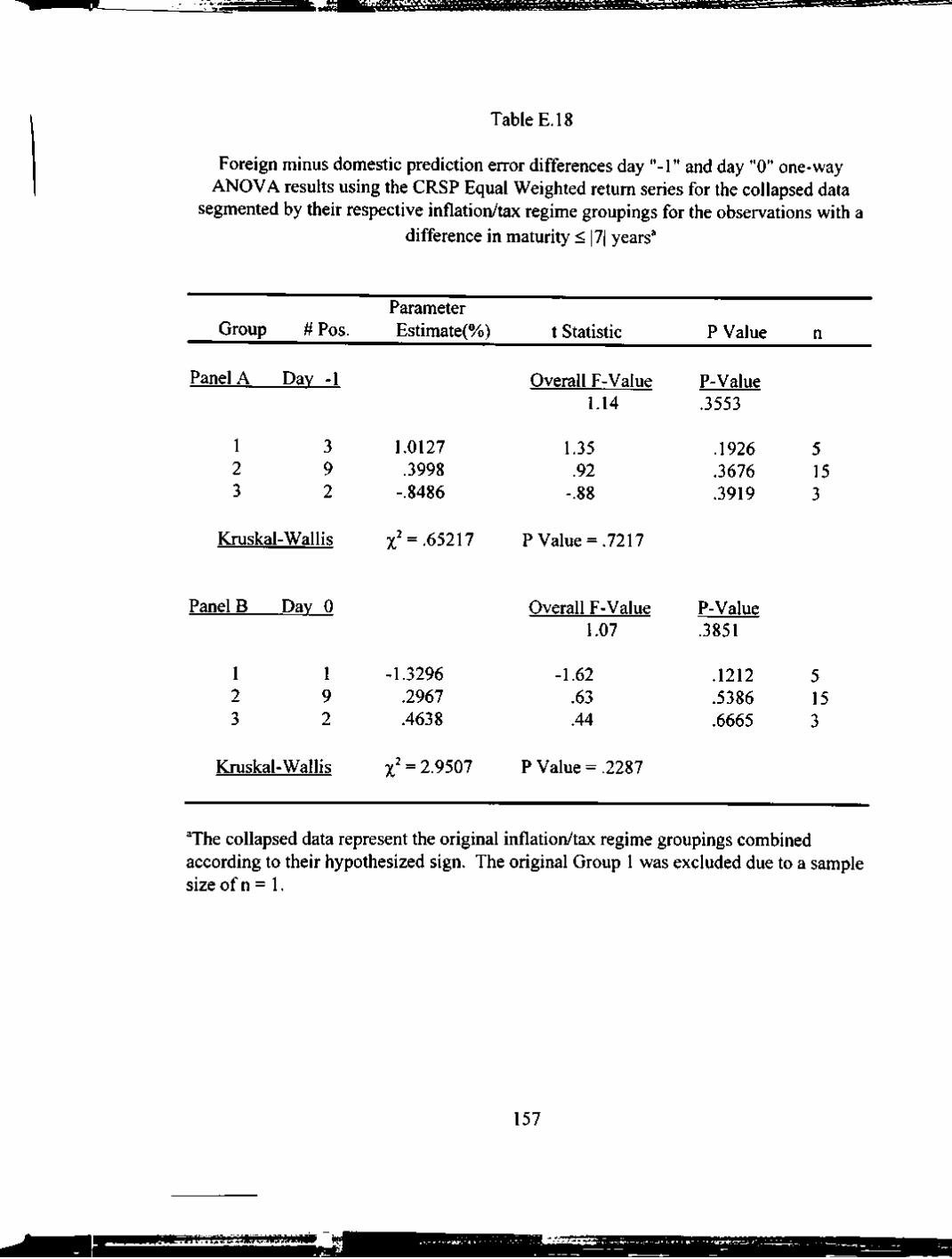

E.18

E.19

F.l

Foreign minus domestic prediction error differences day "-1" and day "0" one-way ANOVA results using the CRSP Equal Weighted retum series for the inflation/tax regime group 9 across all maturity difference groupings

Foreign minus domestic cumulative two-day prediction error differences one-way ANOVA results using both the CRSP Value and Equal Weighted retum series for the inflation/tax regime group 9 across all maturity difference groupings

Foreign minus domestic prediction error differences day " - 1 " and day "0" one-way ANOVA results using the CRSP Value Weighted retum series for the collapsed data segmented by their respective inflation/tax regime groupings for the observations with a difference in maturity < 17| years

Foreign minus domestic prediction error differences day " - 1 " and day "0" one-way ANOVA results using the CRSP Equal Weighted retum series for the collapsed data segmented by their respective inflation/tax regime groupings for the observations with a difference in maturity < |7| years

Foreign minus domestic cumulative two-day prediction error differences one-way ANOVA results using both the CRSP Value and Equal Weighted retum series for the collapsed data segmented by their respective inflation/tax regime groupings for the observations with a difference in maturity < |7| years

Foreign minus domestic prediction error differences day "-1" and cumulative two-day one-way ANOVA resuhs using the CRSP Value Weighted retum series for the data segmented by their currency of denomination (Currency Groups AUS C$ DM SFR STG YEN) . .

154

155

156

157

158

160

IX

wHfaiig

m

F.2 Foreign minus domestic prediction error differences day "-1" and cumulative two-day one-way ANOV.A results using the CRSP Equal Weighted retum series for the data segmented b\ their currencv of denomination (Currency Groups AUS CS DM SFR STG YEN) . .

F.3 Foreign minus domestic prediction error differences day "-1" and cumulative two-day one-way ANOVA results using the CRSP Value Weighted retum series for the data segmented by their inflation/tax regime groups and currency of denomination (Inflation/Tax Regime Groups 1, 3. 4. 7. 9 and Currency Group SFR)

161

162

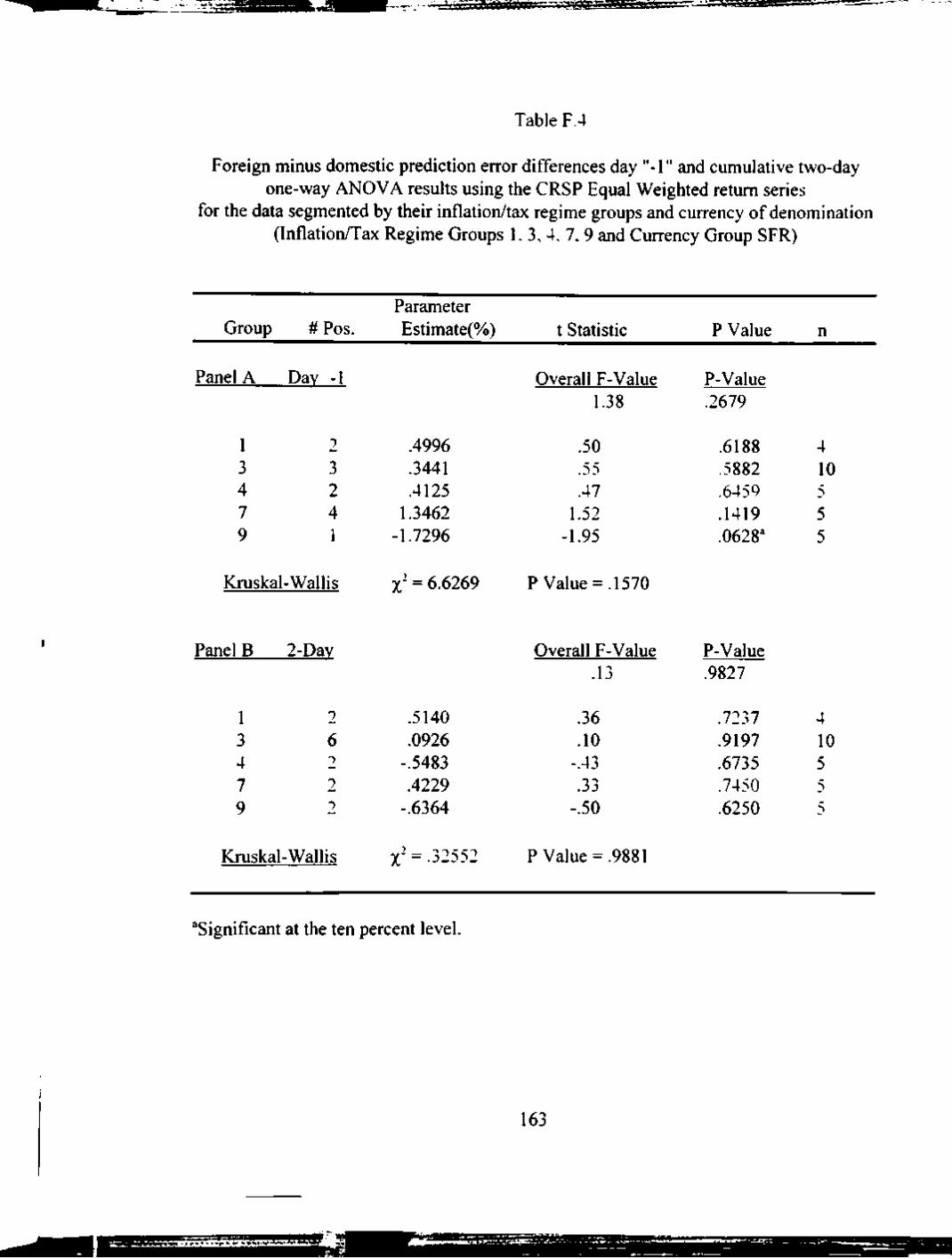

F.4 Foreign minus domestic prediction error differences day "-1" and cumulative two-day one-vvav ANOVA results using the CRSP Equal Weighted retum series for the data segmented by their inflation/tax regime groups and currency of denomination (Inflation/Tax Regime Groups 1, 3. 4. 7, 9 and Currency Group SFR) 163

F.5 Foreign minus domestic prediction error differences day "-1" and cumulative two-day one-way ANOVA results using the CRSP Value Weighted retum series for the data segmented by their inflation/tax regime groups and currency of denomination (Inflation/Tax Regime Group 9 and Currency Groups SFR & YEN) 164

F.6 Foreign minus domestic prediction error differences day "-1" and cumulative two-day one-way ANOV.A. results using the CRSP Equal Weighted retum series for the data segmented bv- their inflation/tax regime groups and currencv of denomination (Inflation/Tax Regime Group 9 and Currency Groups SFR & YEN) 165

X

LIST OF FIGURES

3.1 Exchange Adjusted After-Tax Retum Differential . . . . 33

3.2 Generalized Exchange Adjusted After-Tax Retum Differential . 34

A.l Monthly Inflation Rates U.S. Versus Canada 114

A.2 Monthly Inflation Rates U.S. Versus France 115

A.3 Monthly Inflation Rates U.S. Versus Germany 116

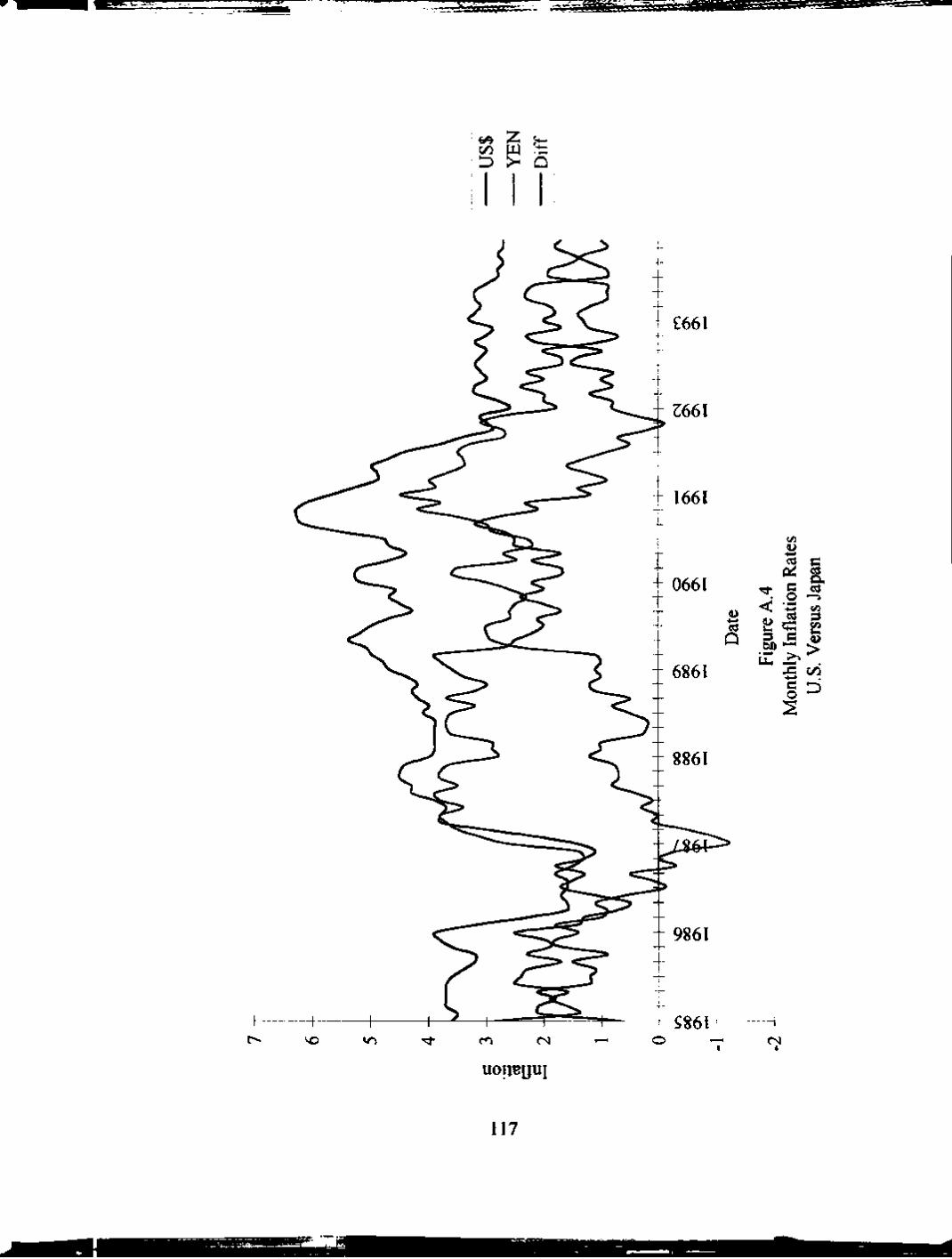

A.4 Monthly Inflation Rates U.S. Versus Japan 117

A.5 Monthly Inflation Rates U.S. Versus Switzerland . . 118

A.6 Monthlv Inflation Rates U.S. Versus U.K 119

XI

CHAPTER I

INTRODUCTION

The issue concerning the use of foreign versus domestic currency denominated

debt in a firm's capital stmcture is unresolved. Specifically, there exist in the literature

conflicting conclusions regarding whether a domestic firm may enhance its value by

using foreign currency debt, rather than domestic currency debt. Further, no attempt has

yet been made to empirically evaluate the problem.

The question is first addressed in a no tax environment where Senbet [1979]

concludes that foreign currency debt offers no advantage relative to domestic currency

debt, assuming Interest Rate Parity (IRP) and Relative Purchasing Power Paritv (RPPP)

hold. Next, taxes are introduced into the analysis. Here, Lee and Zechner [1984]

conclude that a domestic firm may enhance its value by issuing foreign currency debt,

even when IRP and RPPP hold. Contrary to this conclusion, Hodder and Senbet [1990]

argue that the presence of intemational tax arbitrage by multinational firms will render

the currency of denomination decision irrelevant.

Three primary areas of concern are identified based on the theories examined in

Chapter II. First, the models put forth thus far only consider situations where the

domestic inflation rate is positive while assuming the foreign inflation rate is equal to

zero, given that there is no difference in national tax rates, or where national tax rates

differ while the national inflation rates are assumed to equal zero. Accordingly, the

analysis needs to be extended to consider whether the simultaneous presence of both

differential positive inflation rates and differential national tax rates alter the conclusions

drawn thus far. Second, it is assumed throughout the existing literature that the

introduction of taxes only affects how national interest rates are defined, but does not

alter the traditional RPPP mechanism. This assumption leads to an inherent

inconsistency among the IRP condition, the RPPP mechanism and the Modified Fisher

Effect. Hence, h is argued that international, as well as national, conditions must be

modified to incorporate taxes such that a stable equilibrium may be achieved. Finally,

1

because no specific empirical test related to the stock price reaction for foreign currencv

debt offers (relative to domestic debt offers) exists, it is deemed necessarv that such an

analysis be conducted to determine which (if any) of the theoretical arguments are

supported by the data.

Chapter III begins by extending the analyses reviewed in Chapter II into a more

general setting. The primary concern discussed in Chapter III is whether the conclusions

drawn are altered by the simultaneous existence of both differential national inflation

rates and differential national tax rates. Specifically, Lee and Zechner conclude that a

domestic firm may enhance its value by issuing foreign currency debt when either the

domestic tax rate exceeds the foreign tax rate in the absence of differential inflation rates

or when the domestic inflation rate is positive given equal national tax rates. In contrast,

Hodder and Senbet conclude that the presence of intemational tax arbitrage by

multinational firms will render the currency of denomination decision irrelevant for

domestic non-multinational firms under the scenarios explored by Lee and Zechner. Will

these results be materially altered when both differential inflation and tax rates are present

in the analysis?

Based on the concern discussed above, it is shown that once all factors are

incorporated into the analysis, the national tax rate differential must be proportional to the

national inflation rate differential for an equilibrium to be achieved. In other words, for

there to be no difference in the exchange adjusted real after-tax cost of foreign borrowing

relative to domestic borrowing, the inflation rate differential must be proportionally offset

by the tax rate differential. This result leads to the conclusion that the intemational parity

conditions should be modified such that a stable equilibrium may be achieved.

The counter-intuitive result that tax rate differentials must be proportional to

inflation rate differentials leads to a re-examination of the traditional intemational parity

conditions in the presence of taxes. It is argued that, if national interest rates equilibrate

on a real after-tax basis as defined according to Darby [1975], then an intemational parity

should also be established on a real after-tax basis rather than the traditional real before-

tax equilibrium setting. The resuhs of this analysis imply that the Modified Fisher Effect

(which incorporates taxes within countries, but still invokes the traditional Relative

Purchasing Power Parity) according to Darby is inconsistent with the traditional

Intemational Fisher Effect. The inconsistency stems from the fact that national markets

are assumed to equilibrate on a real after-tax basis, while the intemational market is

assumed to equilibrate on a real before-tax basis. Accordingly, a new intemational

equilibrium, referred to as the Intemational Darby Effect, is derived where all markets

equilibrate on a real after-tax basis. The chapter concludes with a summary of the

analyses explored, and highlights the need for an empirical investigation of the issues at

hand.

Chapter IV begins with a description of the methodology that will be emploved in

the empirical analysis of the issues explored. The primary theoretical argument of

concem centers on how firm value will change with respect to a change in debt.

Specifically, is the value-debt relationship significantly different for a foreign versus a

domestic currency debt offer? To this end, it is deemed appropriate to employ an ev ent

study methodology that measures a firm's abnormal stock price as it relates to the

announcement of a debt offer. This type of methodology will provide the necessarv

information to compare stock price reactions for foreign debt offers relativ e to domestic

debt offers.

Next, the hypotheses implied by the research previously discussed will be

developed. In this section of the chapter, the null hypothesis for each scenario will be

that there is no significant differential effect on stock price for foreign debt offers relafive

to domestic debt offers. This debt denomination irrelev ancv proposition is based on the

Intemational Darby Effect (IDE) developed in Chapter 111. In the development of the

IDE h was assumed that the real after-tax costs of debt were equal across countries.

Based on this assumption, there should be no observable difference in stock price

reactions for foreign debt offers relative to domestic debt offers. Several altemative

hypotheses will be constmcted based on the scenario in quesfion. For example (as argued

by Lee and Zechner). there should be a positive relationship between firm value and

foreign debt offers under certain circumstances.

D

A brief description of the data to be used in this study is combined with the

discussions regarding the methodological design and the dev elopment of the testable

hypotheses. In addition, several areas of concem related to other factors that may lead to

an observable difference between debt offers are addressed. For instance, previous

research by Kidwell, Marr and Thompson [1985, 1986] argues that there may be an

advantage to borrowing in the Eurobond market relative to the U.S. domestic market.

This possible advantage stems from the observation by these authors that there exists a

persistent lower cost of borrowing in the Eurobond market relative to the U.S. domestic

debt market. In a similar vein, another area of concem deals with the Relative Purchasing

Power Parity assumpfion invoked in the arguments discussed in Chapters II and III.

Specifically, should debt offer announcements be categorized according to inflation

differentials, or according to expected currency movements as reflected in the exchange

rate markets? Finally, the chapter concludes with a summary of the issues discussed.

The discussion regarding the data collection process, the empirical design and test

results appears in Chapter V. As explained in Chapter IV. the main empirical tests

employ an event study methodology. Given the new intemational equilibrium condition

derived in Chapter III, the null hypothesis is defined as no statistical difference in stock

price reaction for a foreign debt offer versus a domestic debt offer.

The initial step in the data collection process involved identifying domestic firms

announcing a proposed foreign currency debt offer. The data for this initial step is

provided by the Securities Data Company for the years 1985 through 1993. After

screening the data following standard event study techniques, 115 foreign debt offers by

56 domestic based firms remained. These offers are then matched with domestic debt

offers in an effort to provide a control sample. The final samples consist of 78 foreign

and 78 domestic debt offers by 45 and 65 firms, respectiv ely.

Following the debt announcement identification phase, data are collected relating

to national inflation and tax rates for the countries in question. As described above, Lee

and Zechner posit foreign debt and firm value relationships only for specific inflation and

tax rate regimes. Therefore, it is necessary to categorize each foreign debt announcement

4

•.^^^iset

into its respective inflation and tax differential setting. Data related to national inflation

rates are from the International Financial Statistics Yearbook, and tax rate information

from the Prentice Hall publication Corporate Taxes a Worldwide Summary.

The empirical phase of the analysis has three primarv tests based on an ev ent

study methodology following Brown and Wamer [1985]. The first set of tests examine

whether any observable significance exists for either sample overall. The second set of

tests evaluates the foreign announcements after accounting for the inflation and tax rate

regime categorizations. The final primary empirical results attempt to discem an>

observable significant difference in stock price reaction for foreign debt offers relativ e to

domestic offers. Additionally, a fourth set of tests examines the relativ e difference in

stock price reactions after accounfing for differences in maturity for the "matched"

foreign and domestic offers. This analysis is deemed necessarv due to a lack of data that

would have enabled an initial control for this variable. In general, there is no conclusiv e

evidence to contradict the notion that firms should be indifferent to the currency

denomination decision as implied by the newly derived Intemational Darby Effect.

Once all data were collected and organized, an event methodology following

Brown and Wamer was used to compute the prediction errors associated with each debt

offer announcement. This segment of the analysis produced a negativ ely significant

result for the firms in group nine, in contrast to Lee and Zechner's theory. Group nine

relates to the foreign debt offer announcements under the inflation/tax regime where the

domestic tax and inflation rates exceed their foreign counterpart. According to Lee and

Zechner, this group should produce a positive sign due to an added tax shield benefit

from borrowing in an appreciating foreign currency. A potential rational for the result

found related to an increase in firm risk via the foreign currency exposure.

The second level of tests employed the prediction errors as the response variables

in a one-way ANOVA analysis. These tests were performed in an effort to increase the

efficiency of the results given the small sample sizes. Here, the results were similar to

those of the event methodology in that only group nine was found to be negativ ely

significant. The final phase of the primary empirical analysis focused on identifying anv

observable difference in prediction errors for the foreign announcements relative to the

domestic announcements.

In this last set of primary empirical tests, an ANOVA procedure and a matched

pairs t-test procedure were used, where the difference in prediction errors (for each group)

was the response variable. Further, the comparable non-parametric Kmskal-Wallis and

Wilcoxon Signed-Ranks tests were also employed in this analv sis. Overall, only the

difference in prediction errors for group seven on day "-1" appeared as significantly

positiv e. Group seven refers to those foreign debt announcements for which the domestic

inflation rate exceed its foreign counterpart, assuming no difference in tax rates. This

was one of the specific groups Lee and Zechner argued would be positive due to an added

tax shield benefit associated with borrowing in an appreciating foreign currencv.

Howev er, it was proposed that a negatively significant result related to the domestic

announcements might be behind the apparent positively significant difference in

prediction errors. This argument is based on the fact that this group was not significant

when the foreign prediction errors were examined independentlv of the domestic

prediction errors.

The empirical analyses also included a section related to an examination

controlling for differences in maturity between the foreign and domestic debt

announcements. This analysis was included because such a control was not possible in

the original sampling procedures given the limited amount of data available. Controlling

for differences in maturity did not provide any significant change in the results reported

in the prior sections. It was found, as before, that only group nine persisted as a

significant result. One possible explanation for this result was that a large sub-categorv'

of group nine related to observ ations for which the domestic maturity exceed the foreign

maturity. However, there were no other major changes in significance for the other

groups related to this maturity difference classification. The fact that only group nine

showed persistent significance may indicate that this significance was the result of three

outliers contained in this group. Unfortunately, no logical reason related to these outliers

could be identified.

In conclusion, there are a few significant results based on the analyses related

solely to the examination of prediction errors for foreign debt offer announcements and

based on the analyses comparing the foreign and domestic prediction errors. Further, an

additional analysis controlling for differences in maturity between the foreign and

domestic sample provided no new information. The overall results provide little ev idence

to reject (if at all) the null hypotheses based on the newly derived intemational

equilibrium given in Chapter III.

This dissertation constitutes an examination of the theoretical arguments

presented in the literature related to the issue concerning whether domestic firm value

may be enhanced via the use of foreign currency debt. Additionally, this research adds to

the existing literature in three ways. First, the existing literature is extended into a more

generalized (and perhaps more realistic) setting. Second, a new intemational debt market

equilibrium condition is derived, where all markets are assumed to equilibrate on a real

after-tax basis. And finally, an event study methodology is employed to empirically

examine the theoretical issues explored herein.

-9 y*?^^5i| mm

CHAPTER II

DOMESTIC FIRM VALUE AND THE DEBT

DENOMINATION DECISION

Introduction

This chapter examines the existing literature that explores the impact of using

foreign versus domestic currency denominated debt on firm value. The issue conceming

the use of foreign versus domestic currency denominated debt in a firm's capital stmcture

is unresolved. Specifically, the issue centers on conflicting conclusions regarding

whether a domestic firm may enhance its value by using foreign currency debt rather than

domestic currency debt.

The question is first addressed in a no tax environment where Senbet [1979]

concludes that foreign currency debt offers no advantage relative to domestic currency

debt, assuming Interest Rate Parity (IRP) and Relative Purchasing Power Parit> (RPPP)

hold. Next, taxes are introduced into the analysis. Here, Lee and Zechner [1984]

conclude that a domestic firm may enhance its value by issuing foreign currency debt,

even when IRP and RPPP hold. Contrary to this conclusion, Hodder and Senbet [1990]

argue that the presence of intemational tax arbitrage by multinational firms will render

the currency of denomination decision irrelevant.

This chapter concludes with a discussion highlighting the need for additional

research in this area. Three primary areas of concem are identified. First, the models put

forth thus far only consider situations where the domestic inflation rate is positiv e. while

assuming the foreign inflation rate is equal to zero and there is no difference in national

tax rates, or where national tax rates differ while the national inflation rates are assumed

to equal zero. Accordingly, the analysis needs to be extended to consider whether the

simultaneous presence of both differential positive inflation rates and differential national

tax rates alter the conclusions drawn thus far. Second, it is assumed throughout the

existing literature that the introduction of taxes onlv affects how national interest rates are

defined, but does not alter the traditional RPPP mechanism. This assumption leads to an

8

inherent inconsistency among the IRP condition, the RPPP mechanism and the .Modified

Fisher Effect. Hence, it is argued that national, as well as intemational. conditions must

be modified to incorporate taxes such that a stable equilibrium may be achieved. Finall>.

because no empirical analysis exists regarding the questions at hand, it is deemed

necessary that such an analysis be conducted to determine which (if any) of the

theoretical arguments are supported by the data.

Review of Existing Literature

de Faro and Jucker [1973] are among the first to explore a relafionship enabling

one to compare the effecfive nominal cost of domestic currency borrowing versus that of

foreign currency borrowing. They explore this relationship in a restrictive environment

in which they ignore the impact of taxes and assume a one period certainty model. In this

setting, the effecfive nominal cost of domesfic borrowing should equal the exchange

adjusted cost of foreign currency borrowing. This relationship is expressed as:

i,={l + i,)(l + e)-l (2.1)

Where i is the effective nominal cost of domestic currency borrowing. The effective

nominal cost of foreign borrowing in foreign currency terms is if. And, e is the change in

the value of the foreign currency e = 5, SQ

\

(SQ and s, represent the domestic currency

per unit of foreign currency exchange rates at the beginning and end of period,

respectively). The relationship expressed in equation (2.1) may be referred to as an

Interest Rate Parity (IRP) condition, in that any difference in the stated nominal interest

rates should be offset by the change in relative currency values.' Specifically, the change

in the exchange rate, e, should equal the geometric difference in the effective nominal

interest rates between the two countries defined as:

-\ = e (2.2)

de Faro and Jucker use the condition given in equation (2.1) or equation (2.2) to

show that a firm should borrow domestically if / - (1 + / )(l + ) ~ 1 • and vice versa.

Thus, if the change in the exchange rate did not offset the difference between the two

stated nominal interest rates, then it would be beneficial to borrow in the foreign

currency. For example, if i = if and e was negative, then (on an exchange adjusted basis)

foreign currency borrowing by a domestic firm would be less costly than domestic

currency borrowing. Hence, in the absence of taxes there could be a cost advantage for a

domestic firm to borrow in a weakening currency. This type of formulation for

evaluating effective borrowing costs establishes the basis for further examination once

other factors such as differential inflation rates, differential tax rates, and exchange risks

are introduced into the model.

Recognizing that s, is not known with certainty at the beginning of the period,

Senbet [1979] expands on this basic relationship by developing an intemational asset

pricing model that allows for this exchange rate uncertainty. Assuming that Relative

Purchasing Power Parity (RPPP) and that Interest Rate Parity hold, Senbet argues that

when taxes are equal to zero the value of a purely domestic firm will be unaffected bv the

use of foreign currency leverage in its capital structure." Further, he shows that the firm

value relationship for a purely domestic firm using foreign currency debt compared to a

purely domestic unlevered firm collapses to the traditional Modigliani and Miller [1958.

1963] setting.

10

Senbet's conclusions can be demonstrated using the following analysis.

For a given firm define:

X = the firm's domestic currency cash flow before payments to debt holders and

before corporate tax at (t = 1).

B = the face value of domestic currency debt.

Bf = the face value of foreign currency debt,

ij = the nominal retum on domestic currency debt,

r = the nominal^ retum on equity in the domestic country,

if = the nominal retum on foreign currency debt,

r f = the nominal retum on equity in the foreign country,

tj = the domestic corporate tax rate,

tf = the foreign corporate tax rate.

The value of a domestic firm at (t = 0) may then be expressed as:

V = B

1 + r + S X-B-t. X-B + B

1 + /., l + r. (2.3)

Following DeAngelo and Masulis [1980b], if the first derivative of V with respect

to B in equation (2.3) is positive, then firms would supply only debt; if the derivative is

negativ e, firms would supply only equity. An interior equilibrium can be achieved only

if there are positive suppliers of both debt and equity. This will be the case if the first

derivative of V with respect to B in equation (2.3) is zero. Differentiating equation (2.3)

with respect to B and setting this equal to zero giv es:

\

rl' _ 1

rB~ \ + i.

l-t. 1-1 + / dJ

1 + /-, = 0 (2.4:

11

Solving equation (2.4) for i gives:

h = 1 - / . (2.5)

If the equilibrium relationship for retums on debt and equity holds according to

equation (2.5), then the value of the firm (V) is unaffected by the use of debt (B). This

irrelevancy proposition holds for t > 0. If t = 0 then i = r„ and (V) is still unaffected by

the use of leverage (B). The issue of concem is whether the introduction of foreign

currency leverage in the presence of currency exchange rates or differential national tax

rates materially alters the proposifion set forth in equation (2.5). This issue is first

explored in a one-period no-tax setting following Senbet.

Following Senbet, let the current time zero (t = 0) domestic price of foreign

currency exchange rate equal one, and assume the domestic country has an inflation rate

(TTJ) for the coming period, while the foreign inflation rate (TTJ) is zero. If Relativ e

Purchasing Power Parity holds, the exchange rate at (t = 1) will be (1 + TT ). Combining

the IRP relationship and the RPPP relationship (and assuming equal real retums on equity

in both countries) results in what has been termed the Intemational Fisher Effect (IFE),

see for example Hodder and Senbet [1990]. Thus, an intemational equilibrium condition

for nominal equity retums may be defined as:

h = hl^ +7rd) + 7rd- (2.6)

Consider now a domestic firm that issues debt denominated in a foreign currency

to investors in the foreign country, and assume that t = tf = 0. National equilibrium in the

foreign country implies that / c/

/ \-t if = r^j so that the value of a domestic firm

may be written as:

12

«LUH

V = 5 \ + r e/

+ \X- B. (1 + .T, )} —-^—^ . (2 .7)

The first term on the right-hand side of equation (2.7) is the present value of

foreign debt. The terms within the outer brackets denote the end of period (t = 1) amount

paid to the firm's equity holders denominated in domestic currency terms. The last term

is the equilibrium discount rate for equity income.^

Differentiating (2.7) for V with respect to Bf giv es:

3' cB,

(1 + ^ .)

l+'-e/ ^+^e/{^ + ^'^d)+^'^c = 0. (2.8)

and the value of the firm is unaffected by the use of foreign currency lev erage. In the

absence of taxes (assuming RPPP and IRP hold) the value of a domestic firm is

unaffected bv the use of either domestic or foreign currency debt.

The leverage irrelevancy argument demonstrated above may also be explored

using a format following deFaro and Jucker. The assumption of IRP for equity retums,

and the RPPP assumption are defined as. respectivelv:

^e={'^ + ^vf )(1 + ) - 1. and (2.9)

e = {\ + 7ij) (2.10)

Combining (2.9) and (2.10) gives:

fe=[^ + r^f\^^^d)-^ = r,f{\ + ^,) + ^j (2.11)

13

With tj = tf = 0, national equilibria imply that i = r and that if = r f. These conditions

imply that the following condition holds for the relative costs of debt:

i,=if(\ + ;r,) + 7rj=[\ + if){\-^e)~\ (2.12)

Accordingly, there is no cost advantage for a domestic firm to issue foreign

currency debt because any difference in the stated nominal interest rates is offset by the

change in the exchange rate. This intemational irrelevancy proposition is feasible in the

absence of taxes because Interest Rate Parity. Relative Purchasing Power Parity and the

Intemational Fisher Effect are shown to be consistent with one another. The following

discussion explores literature that attempts to incorporate taxes into this analysis.

Lee and Zechner extend the above analysis to include domestic and foreign

corporate taxes. Their arguments center on the scenarios where t = tf > 0 and TTJ > Tif = 0,

and where t 9 tf and TI = 7if > 0. They conclude that with equal corporate taxes between

countries there may be an advantage to issuing foreign debt when TTJ > Tif = 0, and that

there may be an advantage to issuing foreign debt with TT = TTf = 0 when t > tf. Hence, in

the presence of either differential national inflation rates or differential national tax rates,

a Miller [1977] equilibrium cannot be attained for a domestic firm that issues foreign

currency debt. This result is obtained even though a Miller equilibrium exists within each

country for firms that issue home currency debt.

Lee and Zechner's first conclusion can be demonstrated by incorporating taxes in

equations (2.7) and (2.8). For TI > Tif = 0 and t = tf > 0 equafions (2.7) and (2.8) may be

rewritten as:

14

.-giiBiLi

(2.7)

V = B,

1 + ef

1-r.

+ < X-B,{\-^7r,)-t^ X-B,{\ + .T,) + B,

1 + /L_ l - r

l + r.,(l + .Tj + .T

and

cB. 1 + '<t/^

(l + .T,)( l-r , ) + /, / \

ef 1 +

l + ''./(l + ^J+^. 1- / .

(2.8')

Lee and Zechner argue that for TTJ > 0 the value of equation (2.8') will alwav s be

positive. The advantage of foreign debt in this case is because the firm can deduct from

its taxable income the foreign exchange loss on the foreign debt principal repayment. If

Relativ e Purchasing Power Parity holds and t = tf > 0, then a situation where TIJ is greater

than Tif = 0 will result in a tax deductible foreign exchange loss for a domestic firm that

issues foreign currency debt. In other words, higher domestic inflation relativ e to foreign

inflation results in an appreciation of the foreign currency, which leads to a tax deductible

foreign exchange loss for the firm upon repayment of Bf.

To see this result more clearly, the total deductible debt expense of foreign debt in

domestic terms may be decomposed as follows:

5,(1+ ;r,) B.

1 + 1-r

B. -B,

1 + \-t.

+ KjBf (2.13)

15

The term within brackets represents a tax-deductible interest expense to the firm but

taxable income to the foreign lender. The last term (Ti Bf) is a compensation for the

inflation in the domestic country. Assuming RPPP holds, this term will be documented

as a tax deductible foreign exchange loss for the firm. This compensation for domestic

inflation will not be taxed on a personal level in the foreign countr>' because the foreign

investors' required interest income is equal to the bracketed terms in equation (2.13).

Since foreign investors (in this setting) are lending in their home country currency for

which there is no inflation or exchange exposure, the\ do not require any compensation

for inflation or foreign exchange. Hence, foreign investors only require a real rate of

retum grossed-up for their tax liability.

To examine Lee and Zechner's second conclusion thev ignore anv inflation

differential between countries (or that n^ = iif = 0). This helps to isolate the affect of

different tax rates across countries. It is assumed bv Lee and Zechner that real rates of

retum on equity are initiallv equal across countries (r . = r f). and that national equilibria

imply that i = TJ{\ - t j and if = TJ{\ - tf). The value of a domestic firm issuing foreign

currency debt may be expressed as:

V = B.

+ s 1 +

1 - ^

X-B.-t. X-Bf + B /

1 + \-t

\ + r. (2.14)

Differenfiafing (2.14) with respect to Bf gives:

cB, 1 +

1-r

1-0+^. 1

1+ '^ i-t f

l + r„ (2.15)

16

If tj = tf, then equation (2.15) reduces to equation (2.4). and the gain from foreign

currency leverage is equal to that of domestic currency leverage. Further, if t ^ i. = 0.

then — = = 0. cB cBf

On the other hand, when t > tf the value of equation (2.15) is positive, and the

domestic firm can increase its value by issuing foreign currency debt even in the absence

of changes m the exchange rate. For example, when t > tf = 0 equafion (2.15) reduces to:

r l '

cB f {'' 1 U+/-J

r 0 ] 1(1+'-,)'J

>0. (2.15')

In this simplified situafion the foreign equilibrium interest rate is not grossed up b> (1 - tf)

since tf = 0; however, domestic firms can still offset their interest expense against the

positive domestic tax rate, t . Hence, domestic firms would gain by issuing foreign debt

versus domestic debt.

The arguments bv Lee and Zechner can also be demonstrated using an analysis

following work by BenZion and Weinblatt [1984]. BenZion and Weinblatt examine the

relationship among the Relative Purchasing Power Parity, Interest Rate Parity, and what

they refer to as the Modified Fisher Effect in the presence of taxes. Thev argue that, in the

presence of taxes, the simultaneous coexistence of these three phenomena is inconsistent.'

BenZion and Weinblatt's analvsis compares these relationships in a "no-tax"

world to that of a more realistic setting that allows for taxation of interest income. In a

taxless world (assuming a constant before-tax real rate in the domestic and foreign

country equal to r^' and r*'. respectively), IRP, RPPP, and the simple (within countr>')

Fisher Effects are defined (respectivelv) as:^

0 + ' . ) - ( i + ^ ) ^ - (2.16)

17

^ = ( 1 + ^ . ) (2.17)

/• f =r)', and • / ' /

(2.18a)

i d = 0 * ' ( l + ^ d ) + ^d- (2.18b)

By substituting (2.17), (2.18a) and (2.18b) into (2.16). BenZion and Weinblatt

show that IRP, RPPP and the within country Fisher Effects are consistent in the sense that

before-tax real rates of retum are equal across countries. This substitution results in:

+{'-i'(i+^.)+'^<'}]=[i+{'-/'(i+'^.)+'^^}]'°'-ht hi (2.16')

BenZion and Weinblatt assume that the introduction of taxes into the analysis will not

affect the RPPP mechanism, but that taxes will modify the relationships in the other

equations.

With the introduction of taxes, the simple Fisher Effect no longer holds, and must

be modified as suggested by Darby [1975], Fedlstein [1976], or Tanzi [1976]. Assuming

constant real after-tax domestic and foreign interest rates {rf and r^', respectively), the

nominal foreign and domestic interest rates may be defined as, respectively:

'/ = ^f' (l + ;r ,) + /r /

( ' - ' . )

and (2.18'a)

."'

h = 0 + .) + 7r.

O-o) (2.18'b)

18

BenZion and Weinblatt set % = 0, and argue that the capital market equilibrium is

affected by the existence of taxes. Thus, the Modified Interest Rate Parity condition in

after-tax terms may be defined as:

•^3Rn

^.(1-^) = (1-V 1 - 1 (1-^.) (2.16")

Under IRP, the difference between these retums should be equal to zero, defined as:

' . ( i -o)- (->©-' 0-o)=o (2.16'")

BenZion and Weinblatt argue that the equality in (2.16'"), which held under IRP,

may not necessarily hold once RPPP is invoked because it is assumed that taxes do not

affect the RPPP mechanism. Invoking RPPP, and substituting equations (2.17), (2.18'a)

with TTf = 0 and (2.18'b) into the left-hand side of (2.16'") results in:

(1-0-.al \

1 + 7

( • - ' . ) .

( i + ^ . ) - i (i-o)<o (2.19)

Assuming r" = r"' = f", and re-arranging terms yields:

al (' + ' </)-

(1 + J(1-^.) > (2.19')

Since equation (2.19') is not necessarily equal to zero as suggested by equation

(2.16'"), BenZion and Weinblatt conclude that the Interest Rate Parity condition is not

19

,.fi^ i ^ » a w *•<

compatible with the revised Fisher Effect and/or the Relative Purchasing Power Parity

mechanism.

When tj = tf > 0 and TT > % = 0 equation (2.19') reduces to the following

inequality:

^dtd > 0. (2.19")

The term given in (2.19") represents the after-tax cost differential for domestic versus

foreign currency borrowing by a domestic firm. In other words, the after-tax cost of

domestic borrowing exceeds its foreign counterpart by the term given in (2.19"). This

result is consistent with that derived by Lee and Zechner shown in equation (2.13). As in

Lee and Zechner's analysis, a domestic firm benefits from issuing foreign currency debt

because foreign investors do not require compensation for exchange rate gains or losses.

Accordingly, the firm derives the full benefit of the exchange loss tax shield given in

(2.19").

When Tij = Tif = 0 and t tf equation (2.19') reduces to:

.«' 1- ( 1 - 0 ) > 0

< (2.19'")

From (2.19'"), it is clear that when t > tf the after-tax cost of domestic borrowing by a

domestic firm exceeds the after-tax domestic cost of foreign currency borrowing. Again,

this result is consistent with that derived by Lee and Zechner.

Thus far, the analyses explored have resulted in an opposite conclusion regarding

the use of foreign currency debt with or without the presence of taxes. Specifically, de

Faro and Jucker, and Senbet, would argue that (ignoring taxes) there is no gain from

issuing foreign currency debt assuming that Interest Rate Parity and/or Relative

purchasing Power Parity hold. Further, if IRP and/or RPPP did not hold, then it could be

20

beneficial to borrow in a weakening foreign currency. Contrary to this result, Lee and

Zechner (and BenZion and Weinblatt) would argue that a firm should borrow in a

strengthening foreign currency in the presence of taxes. This result is obtained e\ en

when IRP and RPPP are assumed to hold. In addhion to the above analv ses. the issue

conceming the possible incremental affect of foreign versus domestic currency borrowing

on firm value is examined by Hodder and Senbet.

Hodder and Senbet re-examine the scenarios discussed by Lee and Zechner, and

they conclude that an intemational equilibrium that renders capital stmcture irrelevant

will prevail in the presence of intemational tax arbitrage. Hodder and Senbet first

examine the case where TT = Tif = 0 and t ^ tf. Specifically, they argue that when t > t,

the solution implied by Lee and Zechner is for domestic firms to be entirelv foreign

levered. However, this solution ignores the ability of firms to engage in a tax arbitrage.

The argument put forth by Hodder and Senbet supposes a domestic based

multinational that owns a foreign levered subsidiary. In this setting, it would be to the

domestic parents" advantage to issue domestic debt and give the foreign subsidiary an

equity infusion used to repay its debt, which results in a firm-wide tax savings due to the

higher domestic tax shield. Alternatively, a foreign parent that owns a domestic

subsidiary may engage in a similar capital restmcturing so as to realign its debt stmcture

into the country that offers a higher tax shield. These types of tax shield realignments

would result in an intemational equilibrium rendering foreign leverage irrelevant for ev en

non-multinational domestic firms.

The capital realignment process described by Hodder and Senbet is supported by

Madura and Fosberg [1990]. Madura and Fosberg examine the effect of differing

national tax rates on the net present v alue of foreign investments and conclude that the

firm should borrow in the country that offers the highest tax shield adv antage. How ev er.

Liu and Hsueh [1993] point out that previous conclusions regarding the effect of taxes on

the currency of denomination decision for multinationals ignore the impact of foreign tax

credits (FTCs) for repatriated foreign earnings. They argue that when a domestic parent

has full utilization of FTCs or is able to use excess FTCs to offset other foreign source

21 ^

income (as long as the domestic tax rate is greater than zero) foreign financing ah\avs

ensures a higher expected net present value. Apparently, the issue conceming

multinational tax shield realignments that render foreign leverage irrelevant for domestic

non-multinationals is an empirical issue, which may be discemed by examining the

incremental effect of foreign versus domestic debt announcements on firm value.

Hodder and Senbet move on to re-examine the case where t = tf and TTJ > Tif = 0.

Here, the analysis focuses on whether the IFE holds for both equity and debt retums

simultaneously. As before, they assume real retums on equity are equal across countries

and define the nominal equity retum relationship according to the IFE as:

r, = r,f(l +7rd) + 7rd. (2.20)

Next, they consider whether an intemational analog of the "Darby Effect" dismpts

the IFE for interest rates on debt. They begin by examining the after-tax receipts to a

marginal investor in the foreign country. The after-tax receipts from a foreign and

domestic currency loan are defined as. respectively:

ij(l-tf), and (2.21)

lilA 1 0-/) (2.22)

Equating (2.21) and (2.22) yields:

if(l-tf) = (1 + ^ . )

(1-0 (2.23)

11

Hodder and Senbet argue that when we allow for progressive income taxes on debt

retums and do not restrict investors to lending only in their home currency, equation

(2.23) may be re-written as:

i, =if{l + 7Cj) + 7r,. (2.23')

The resuh derived in (2.23') stems from the assumption that the (1 - tf) term on either side

of equation (2.23) simply cancel each other out. Thus, they conclude that the IFE

relationship holds for both equity and debt retums simultaneously, even with the

introduction of taxes. This conclusion is obviously in direct contrast to the result derived

following Lee and Zechner, and BenZion and Weinblatt.

Hodder and Senbet do point out that even when IFE holds in both markets, the

existence of taxes leads to a difference in what they term the "effective real tax rate" for

each country. They define the nominal tax shield for a domestic firm borrowing in the

domestic currency as t^ij, or in real terms as X^\J{\ + n^). Further, the real interest rate on

domestic debt is equal to (i - n^l{\ + TT ). Thus they derive an effective real tax rate

(7^^) for domestic borrowing by a domestic firm by equating the following:

^d

( :

V l + TT^

tdh

l + TT, (2.24)

Hence,

T'^ =t ^d 'd

\K,-^dJ (2.25)

Similarly, the effective real tax rate for foreign borrowing bv a domestic firm is

shown to equal the expression given in equation (2.25). Since 7if = 0, the effectiv e real

23

tax rate in the foreign country for local or domestic currency borrowing equals tf. Hence,

the supply side conditions for domestic firms and foreign firms issuing debt in either

currency is expressed as. respectively:

h = l-Tf , and (2.26)

h = ef

\-t (2.27)

Obviously, (when TIJ > 0 and t = tf) equations (2.26) and (2.27) cannot hold

simultaneously. Hodder and Senbet argue that the existence of equal nominal tax rates

across countries combined with the introduction of differential inflation rates between

countries does not dismpt the IFE. Instead, this setting results in a difference between the

effective real tax rates, which reduces to the no inflation different tax rate scenario, except

that the difference in tax rates is in real terms rather than nominal. Accordingly, a similar

type of tax shield realignment renders foreign leverage decisions irrelevant for non-

multinational domestic firms. Again, this is an empirical issue.

Summarv and Motivation for Additional Research

The literature reviewed in this chapter has focused on the theoretical implications

of introducing taxes into an intemational equilibrium setting with and without the

existence of domestic inflation. The arguments begin in a no tax regime following

deFaro and Jucker, where the prescription is to borrow in the weakening currency in order

to gain a possible cost advantage. Next. Senbet invokes Interest Rate and Relative

Purchasing Power Parity, and concludes that the v alue of a purely domesfic firm will be

unaffected by the use of foreign leverage in its capital stmcture assuming taxes are

ignored. The introduction of taxes by Lee and Zechner. and BenZion and Weinblatt.

leads to the following conclusions: (1) ignoring the impact of exchange rate changes

24

(i.e.. 71 = %= 0), domestic firms can benefit from the issuance of foreign currencv debt

when the domestic tax rate exceeds the foreign tax rate; and (2) assuming national tax

rates are equal, domestic firms can benefit from the issuance of foreign currencv debt

when the domestic inflation rate exceeds the foreign inflation rate (i.e.. TT > Ttf = 0).

The arguments developed by these latter two papers is contradicted in the work bv

Hodder and Senbet. Here h is argued that the presence of intemational tax arbitrage bv

multinational firms renders foreign currency borrowing decisions irrelevant for non-

multinational domestic firms. This tax shield realignment process is supported bv

Madura and Fosberg in that firms should borrow in the country that offers the highest tax

shield advantage in order to maximize foreign projects' net present values. However. Liu

and Hsueh point out that these conclusions ignore the foreign tax credit provisions. Once

these provisions are recognized, the firm should always borrow in the foreign currency in

order to maximize foreign projects' net present values.

The need for additional research stems from three areas of concem that are not

adequately addressed in the existing literature. First, none of the arguments put forth thus

far have attempted to analyze the situation where both positive differential national

inflation rates and differential national tax rates exist simultaneously. Do the conclusions

drawn in each of the restricted settings examined thus far extend into a more generalized

setting where all variables are considered simultaneously? This issue is further explored

in the following chapter. Second, the cmx of the existing arguments centers on how the

introduction of taxes will alter within country retum relationships and/or how taxes will

alter traditional intemational parity conditions. In general, it is assumed that taxes affect

the interest rate relationships w ithin each country, but do not alter the traditional Relativ e

Purchasing Power Parity mechanism. Following these conditions, two primary

conclusions are drawn. The simultaneous existence of RPPP, IRP and the Modified

Fisher Effect is found to be inconsistent. This result leads Lee and Zechner, and BenZion

and Weinblatt, to conclude that domestic firm value may be enhanced bv the use of

foreign currency debt. Second, the simultaneous existence of RPPP, IRP and the

Modified Fisher Effect is found to be consistent. From this, Hodder and Senbet argue

25

that domestic firms will be indifferent between the use of foreign currency debt and

domestic currency debt in the presence of intemational tax arbitrage opportunities.

The next chapter of this dissertation re-examines how the introduction of taxes

affects national interest rates and traditional intemational parity conditions. An

intemational equilibrium is derived assuming national interest rates are defined according

to Darby. This revised equilibrium condition is termed the Intemational Darby Effect

(IDE). It is argued that under the IDE setting the tax shield advantage from foreign

exchange gains for domestic firms vanishes. This result is derived by recognizing that

differential inflation rates as well as nominal interest rates are grossed-up for taxes. The

conclusions drawn from this setting support the view that the traditional RPPP is

inconsistent with the Modified Fisher Effect as defined by Darby, which is in contrast to

the argument put forth by Hodder and Senbet.

The final area of concem regards the fact that the existing literature has examined

the issues of concem at the theoretical level, but not in an empirical setting. Further, the

existence of competing theories clearly sets the stage for an empirical investigation.

Accordingly, the combination of competing theories and the lack of an empirical analysis

provide ample motivation for further research in this area.

This chapter has provided a review of the existing literature as it relates to the

impact of taxes on traditional intemational equilibrium settings. Further, it has

established a need for more investigation into this issue in the form of a theoretical as

well as an empirical analysis. The following chapter re-examines the theoretical

underpinnings that are cmcial to the analysis at hand. Chapter IV develops the empirical

methodology to be employed in this study, examines the relevant concems involved with

empirically tesfing the issue, and provides a brief descripfion of the data to be used.

26

m

CHAPTER 111

THEORETICAL UNDERPINNINGS

Introduction

This chapter begins by extending the analyses reviewed in the prev ious chapter

into a more general setting. Of primary concem is whether the conclusions drawn are

altered by the simultaneous existence of both differential national inflation rates and

differential national tax rates. Specifically, Lee and Zechner conclude that a domestic

firm may enhance its value by issuing foreign currency debt when either the domestic tax

rate exceeds the foreign tax rate in the absence of differential inflation rates, or when the

domestic inflation rate is positive given equal national tax rates. In contrast, Hodder and

Senbet conclude that the presence of intemational tax arbitrage by multinational firms

will render the currency of denomination decision irrelevant for domestic non-

multinational firms under the scenarios explored by Lee and Zechner. Will these results

be materially altered when both differential inflation and tax rates are present in the

analysis?

Based on the concem discussed above, it is shown that once all factors are

incorporated into the analysis the national tax rate differential must be proportional to the

national inflation rate differential for an equilibrium to be achieved. In other words, for

there to be no difference in the real after-tax cost of domestic borrowing relative to

foreign borrowing, the inflation rate differential must be proportionally offset by the tax

rate differential. This result leads to the conclusion that the intemational parity

conditions should be modified such that a stable equilibrium may be achieved.

The counter-intuitive result that tax rate differentials must be proportional to

inflation rate differentials leads to a re-examination of the traditional intemational paritv

conditions in the presence of taxes. It is argued that if national interest rates equilibrate

on a real after-tax basis as defined according to Darbv, then an intemational parity should

also be established on a real after-tax basis rather than the traditional real before-tax

equilibrium setting. The results of this analysis imply that the Modified Fisher Effect

27

according to Darby is inconsistent with the traditional Intemational Fisher Effect. The

inconsistency stems from the fact that national markets are assumed to equilibrate on a

real after-tax basis, while the intemational market is assumed to equilibrate on a real

before-tax basis. Accordingly, a new intemational equilibrium, referred to as the

Intemational Darby Effect, is derived where all markets equilibrate on a real after-tax

basis. The chapter concludes with a summary of the analyses explored, and highlights the

need for an empirical investigation of the issues at hand.

A Generalized Analvsis

The most tractable method to expand the analysis so that all factors may be

incorporated is to follow a simplified version of the analysis by BenZion and Weinblatt.

This approach basically involves comparing the real after-tax retum from a domestic debt

issue to that of a foreign debt issue from the perspective of a domestic investor. Based on

this analysis, inferences may be drawn regarding the relative real after-tax cost of

borrowing by a domestic firm. This analysis will be conducted following the

assumptions made by Lee and Zechner, and BenZion and Weinblatt, except that both

inflation differentials and tax differentials are present in the model.

As explained in the previous chapter. Interest Rate Parity (IRP), Relative

Purchasing Power Parity (RPPP), and the Modified (within country) Fisher Effects are

defined, respectively, as:

^d =^f + (3.1)

= TT.-TT., (3.2)

,^.!^:±^,and ^"(1-0

(3.3)

h = r;'^n,

(1-0 (3.4)

28

Where s, and SQ are the beginning and end-of-period exchange rates; ij and if are the

domestic and foreign before-tax nominal interest rates, respectively. TTJ and 7tf are the

domestic and foreign inflation rates, respectively, rj" and r^' are the domestic and

foreign real after-tax rates, respectively. And, the domestic tax rate is tj. while the

foreign tax rate is tf.

Following an analysis similar to that employed by BenZion and Weinblatt, the

Modified Interest Rate Parity condition in real after-tax terms may be defined as:

id{}-td)-^d = - 0

( l - ' . ) - ' ^ . (3.5)

Under IRP, the difference between these retums should be equal to zero. Substituting rj*

for the term on the left hand side of equation (3.5), and setting the difference equal to zero

yields:

.(" ^i

^0

{l-t,) + ;r,=0 (3.6)

Substituting the definition of if given in equation (3.4) and invoking RPPP (which is

assumed to be unaffected by taxes) gives:

al , _

+ 7ij-;r, ( l - 0 ) + ;r, =0

Assuming rj" = r"' = r ' and rearranging terms yields:

( r - + ; r , ) + h{^d-^f) = ^

(3.6')

(3.6")

29

Equations (3.6') and (3.6") represent the real after-tax retum (cost) from domestic debt

minus the exchange adjusted real after-tax retum (cost) from foreign debt, assuming

RPPP holds. In order for equafion (3.6') or (3.6") to equal zero, the following relationship

between the tax and inflation differentials must hold:

( l - r , ) ~ [r^'^^f] (3.7)

Based on the result derived in equation (3.7), it is evident that there must be some

type of relationship between national inflational rate differentials and national tax rate

differentials in order to achieve an equilibrium. Specifically, the intemational debt

market is in equilibrium when there is no difference in the exchange adjusted real after

tax cost of debt as given in equation (3.6"). An equilibrium condition will hold only

when the intemational tax rate relationship is proportionally offset by the intemational

inflation rate relationship. For example, when t = tf, it may be inferred from equation

(3.7) that Tij must equal Tif in equilibrium; or, when TT = 7if, t must equal tf. This result is

counter-intuitive in that national tax and inflation rates should be independent exogenous

variables, even in equilibrium. The conclusions inferred from the results derived in this

section lead to the argument that the intemational equilibrating process needs to be re

examined. The following section provides such an examination. Before the intemational

equilibrating process is re-examined, it may be helpful to further examine the above

analysis, since the altemative hypotheses for the subsequent empirical investigation will

be based on the above results.

From the result derived in equation (3.7), the relationship between domestic firm

value and the use of foreign leverage may be explored for several possible scenarios.

First, the simple scenarios explored in the previous chapter where either TT = Tif = 0 and tj

^ tf, or Tij 9 TTf = 0 and t = tf, will be re-affirmed. For equation (3.6") to be positive. which

30

- - % * . : •

implies that domestic borrowing is more costly than foreign borrowing in exchange

adjusted real after-tax terms, the following inequality must be true:

(3.8)

Altematively, for equation (3.6") to be negative, which implies that domestic

borrowing is cheaper than foreign borrowing in after-tax real terms, the following

inequality must be tme:

i^-'^) ^ I/"{''-'-"f) ( ' - ' / ) {'•"^-f)

(3.9)

Thus (as before) if n^ = Ttf, then it must be tme that (1-0) = 1 (which implies

that tj = tf) for there to be no advantage from the use of foreign debt. Clearlv. if TI = 7if =

0 and tj > tf (a situation explored by Lee and Zechner), then the inequality in (3.8) holds

and foreign borrowing will enhance firm value. Further, if t = tf and TI > 7tf = 0,

inequality (3.8) again holds tme. These results re-affirm the conclusions reached bv Lee

and Zechner.

The other scenarios that hav e determinant results are for the situations where t >

tf and Tij > TTf, and where t < tf and TT < % When t > tf and n^ > Uf. inequality (3.8) will

hold and equation (3.6") will be positive. Conversely, when t < tf and TT < Tif, inequality

(3.9) will hold and equation (3.6") will be negative. The situations where t > tf and n^ <

71,, or where t < tf and TI > Tif, are not necessarily determinant; however, the inequalities

given in (3.8) and (3.9) help to set boundary condhions for the effect of foreign leverage

on firm value. For example, if TIJ = .05, Tif = .03 and t = .3. then tf may be derived given

31

r '. Assuming r ' = .02, tf may be solved for as: (1-.3)

= 1 + (.05-.03)

such that tf ( l - r ^ ) " (.02- .03)

must equal .375 in order for the real after-tax costs of domestic and foreign debt to be

equal. For this same example, if tf < .375, equafion (3.6") would be poshive implying

that foreign borrowing would enhance firm value. Altematively, if tf > .375 the opposite

result would hold tme. Further, If TT increase to .07, then tf must be approximately equal

to -435. These simple examples demonstrate that in order to attain a real after-tax

equilibrium for the cost of domestic debt relative to the exchange adjusted cost of foreign

debt, there must be some type of relationship between national tax differentials and

national inflation differentials as defined in equation (3.7).

In an attempt to provide a more intuitive understanding of the relationship given

in equation (3.6") several scenarios are graphically depicted below. For all figures it is

assumed that r ' equals 3%. Figures (3.1a) and (3.1b) graph the retum relationship given

in equation (3.6") for a scenario explored by Lee and Zechner. It is assumed that TI = Tif,

td = 34%, and 19% < tf < 49%. Figure (3.1a) assumes that TI = Tif = 0. It is clear that the

relationship agmed by Lee and Zechner is supported by the graph depicted in Figure

(3.1a). However, the relationship depicted in Figure (3.1b) (with TT = 7if = 5%) is

opposite to the result argued by Lee and Zechner. Specifically, with equal negative

inflation differentials foreign borrowing becomes more expensive relative to domestic

borrowing when t > tf. It is clear that Lee and Zechner's analysis failed to account for

possible negative inflation rates.

32

r^rmsfs

(a)7id = 7Cf=0%

Grai* of Equation (3.6") with t j = 34% and 7td = JCf=0

0.60% T

15.00%

-1.00%

(b)7td = 7Cf=-5%

Graph of Equation (3.6") with U = 34% and Jtj = «f = - 5 %

15.00%

Figure 3.1 Exchange Adjusted After-Tax Retum Differential

33

^

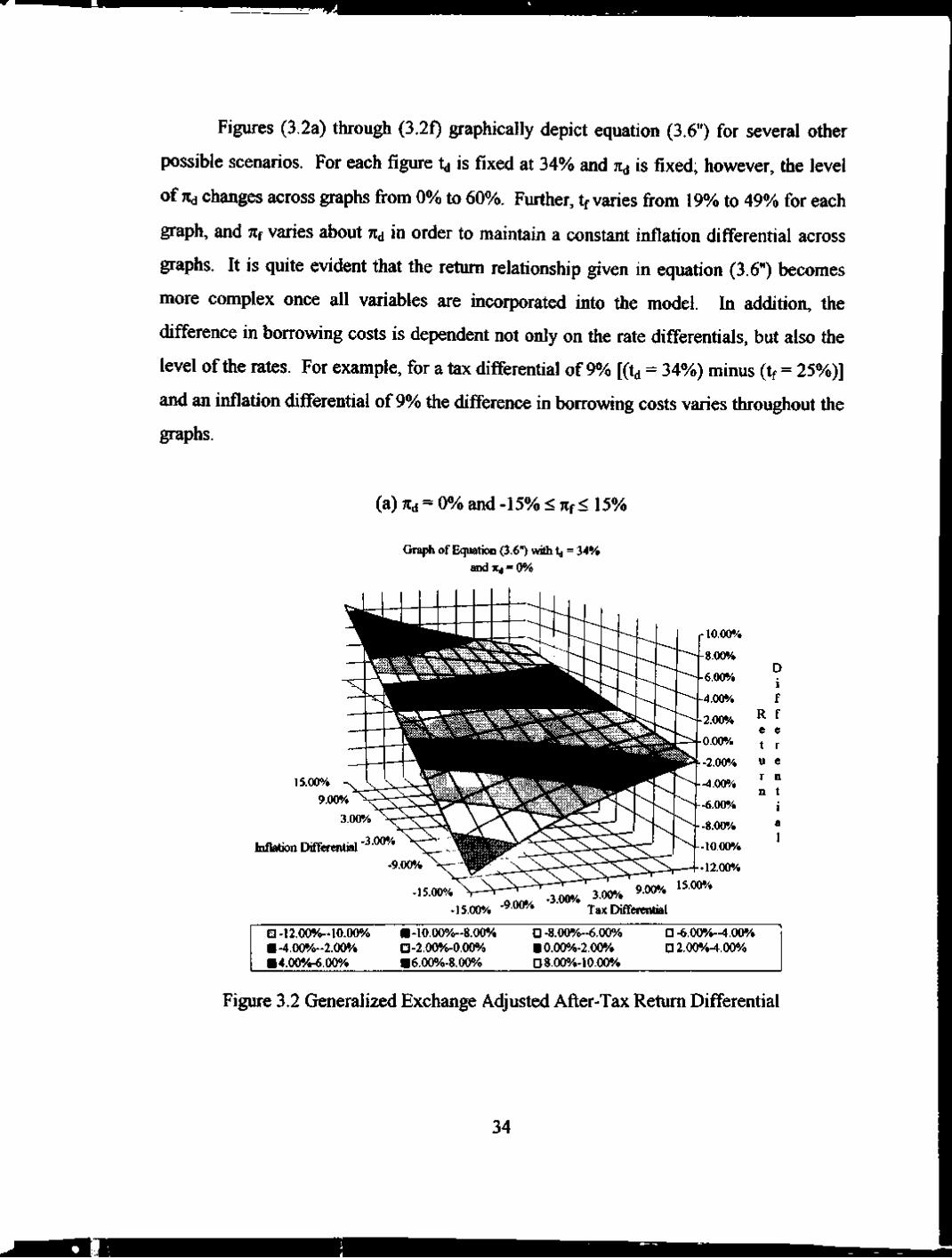

Figures (3.2a) through (3.2f) graphically depict equafion (3.6") for several other

possible scenarios. For each figure td is fixed at 34% and n^ is fixed; however, the level

of 7id changes across graphs from 0% to 60%. Further, tf varies from 19% to 49% for each

graph, and Tif varies about Tid in order to maintain a constant inflation differential across

graphs. It is quite evident that the retum relationship given in equation (3.6") becomes

more complex once all variables are mcorporated mto the model. In addition, the

difference in borrowing costs is dependent not only on the rate differentials, but also the

level of the rates. For example, for a tax differential of 9% [(td = 34%) minus (tf = 25%)]

and an inflation differential of 9% the difference in borrowing costs varies throughout the

graphs.

(a) TCd = 0% and -15% < Tif < 15%

Graph of Equation (3.6") with tj = 34% and JCd = 0%

Inflation Differential

• 15.00% -15.00% -9.00% 3.00% 3.00%

Tax Differential

ED-12.00%-10.00% • -4.00%~2.00% • 4.00%-6.00%

H-10.00%-8.00% D-2.00%-0.00% • 6.00%-8.00%

D -8.00%~6.00% • 0.00%-2.00% D8.00%-10.00%

n-6.00%-4,00% D2.00yo-4.00%

Figure 3.2 Generalized Exchange Adjusted After-Tax Retum Differential

34

(b) Tid = 2% and -13% < 7Cf < 17%

Graph of Equation (3.6") with tj = 34% and It J = 2%

Inflation Differential

-15.00% -9.00% 3.00% 3.00%

Tax Differential

13-12.00%-10.00% • -4.00%-2.00% • 4.00%-6.00%

H-10.00%-8.00% n-2.00%-0.00% • 6.00%-8.00%

n-8.00%"6.00% • 0.00%-2.00% D 8.00%-10.00%

n-6 .00%-4 .00% n2.00%-4.00%

D i f f e r e n t i a 1

(c) TCd = 5% and -10% < TCf < 20%

Graph of Equation (3.6") with U = 34% and Ttd = 5%

15.00% 9.00%

3.00%

Inflation Differential '

-9.00%

9.00% ^' .15.00% 'f-^^ .3.00% 3 00% -15.00% -9 00/ i Tax Differential

-12.00% 00%

D i f f e r e 0 t i a 1

Q-12.00%-10.00% B- lO.00%-8 .00% n-8.00%"6.00% a -6 .0 0%-4 .00% • - 4 . 0 0 % - 2 . 0 0 %

• -2.00%-0.00% •0 .00%-2 .00% a2.00%-4.00% •4 .00%-6 .00% •6 .00%-8 .00%

Figure 3.2 Continued

35

m

(d) jtd = 1 5 % and 0% < jtf < 30%

Graph of Equation (3.6") with U = 34% and ltd = 15%

Inflation Differential

10.00%

5.00%

0.00%

5.00%

-10.00%

D i f

R f e e t r u e r n n t

i a I

15.00%

-15.00% ~ : ^ c - - r - - — • ^^^^^^ 3.00O/. 9.00% 15.00%

-15.00% -9 00% Tax DifTercntial

E3-15.00%-10.00% a-10.00%-5.00% n-5.00%-0.00% nO.00%-5.00% •5.00%-10.00%

(e) TCd = 30% and 15% < TCf < 45%

Graph of Equation (3.6") with td = 34% and Xd = 30%

Inflation Differential

O-20.00%-! 5.00%

• -5.00%-0.00%

-15.00% -15.00%

on„,/ -3.00% 3.00% -9.00% j ^ x DifferenHal

l-15.00%-10.00<'o

l0.00%-5.00%

D-10.00%-5.00%

a5.00%-10.00%

Figure 3.2 Continued

36

m

(t) TCd = 60% and 4 5 % < TCf < 75%

Graph of Equation (3.6") with X^ = 34%

and ltd = 60%

15.00%

Inflation E)ifferential

-15.00% -15.00% -900*/-

-3.00% 3.00%

30.00%

9.00% 15.00%

Tax Ehfferential

El -30.00%-25.00% n-15.00%~10.00% • 0.00%-5.00%

H-25.00%-20.00% • -10.00%-5.00% • 5.00%-10.00%

n-20.0O%~15.00% • -5.00%-0.00% • 10.00%-] 5.00%

Figure 3.2 Continued

The conclusions inferred from the above analysis, which follows from the

assumptions by Lee and Zechner, and BenZion and Weinblatt, are counter-intuitive and

make very little economic sense. Specifically, there is no intuitive economic rationale for

why national tax rate differentials should be related to national inflation rate differentials

in order to achieve equilibrium. However, this result may be the reached via arbitrage

arguments. In any event, one would presume that tax rates as well as inflation rates

should be independent exogenous variables in defining equilibrium conditions. The

primary shortcoming of the above analysis is that it simultaneously assumes national

interest rates equilibrate on a real after-tax basis as per Darby, while an intemational

parity is achieved by equilibrating rates on a real before-tax basis. It is argued here that

these simultaneous assumptions lead to an inherent inconsistency that forces a