Foreign Direct - Philippine Statistics Authority

57

~ ••.•..•. A .•.• NATIONAL STATISTiCAL COORDINATION BOARD ARCHIVES Foreign Direct INVESTMENTS SECOND QUARTER 2006 Republika ng Piltpinas PAMBANSANG LUPON SA UGNAYANG PANG-ESTADISTIKA (NATIONAL STATISTICAL COORDINATION BOARD) http://www.nscb.gov.ph

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Foreign Direct - Philippine Statistics Authority

~ ••.•..•. A .•.•

NATIONAL STATISTiCAL COORDINATION BOARDARCHIVES

Foreign DirectINVESTMENTS

SECOND QUARTER 2006

Republika ng PiltpinasPAMBANSANG LUPON SA UGNAYANG PANG-ESTADISTIKA

(NATIONAL STATISTICAL COORDINATION BOARD)http://www.nscb.gov.ph

•

Foreign Djrect Investment in the PhilippinesSecond Quane.- 2006

is s qu.srraly pubJiclIion pr<p:=d bythe Economic Indicators and S2.tdlitt: AccountS Dmsion (ElSAD)

of the NATIONAL STATISTICAL COORDINATION BOARD (NSC ).For technical inquiries, please contact us at: (632) (896-7981) or email us at !:' •."ii 'l (+...' 1\ ": ••

TERMS OF USE OF NSCB PUBLICATIONSThe NSCB reserves its exclush-e right to reproduce all of it..•• publications in whatever form .•An~-pan of this publication should not be reproduced, recopied, lend or repackage~ for otherparries for any commerciaJ purposes without written pamission from the NSCB. • Any pan ofthis publication may onJy be reproduced fOr mrcm21 use of the reapiem/cusrorner <!ompany .•Should any portion of the data are to be included in a n::pon/arride, the source of the darn or thetitle of the publication and the NSCB ~ publisher should always be cited .• Any i ormationderi\'"cd from the manipulation of data contained in the publication will no longer be the

responsibility of NSCB. '

ISSN 1655-S928

Publis hed by the~ational Statistical Coordination Board

Midland Buendia Building403 Sen. Gil Puyat A'\-enue

Makati City 1200Philippines.

4 September 2006

The Foreign Direct In\'estmOlts in the Philippines Second Qw.ner2006 is av:ubhle in prima:i and decrronic formats

(Excel/Word/PDF in CDRom).Bad issues of this public2tion att a'\"'li.iIablefor purchase.For details, please contact us 2t (632) 890-R456 or at

1:1:0:" n'C!: .•••,., .""'1: •.

••

NSCB Publications

, ....

Regular Publications

Economic and Social Statistics and Indicators (National)• Philippine Statistical Yearbook• Economic and Social Indicators• StatWatch• Compendium of Philippine Social Statistics• Economic Indicators

o Economic Indicatorso Quarterly Economic Indiceso Foreign Direct Investmentso Food Balance Sheet of the Philippines

• Socia/Indicatorso Women and Men in the Philippineso Statistical Report on Children and Womeno Report on the Philippine Human

Development Indexo Philippine Poverty Statisticso Philippine Provincial Poverty Statistics

National Accounts of the Philippines (NAP)• Quarterly, Semestral and Annual NAP• Gross Regional Domestic Product• Gross Regional Domestic Expenditure• Input-Output Accounts• Philippine National Health Accounts• Philippine Education Accounts

Sut>-nalional Statistics• The Countryside in Figures

(Philippines, Western Visayas Region,Province of Guimaras)

• Regional Social and Economic Trends (RSEn(CAR, I , IV, V, VI, VIII, IX ,XII)

• Southern Mindanao Statistical Yearbook• Statistical Handbook on Women and Men

(Philippines, I, V, VI, VIII, IX, XI, XII)Serial Publications

• Factsheets• NSCB Statistics series

o Metro Manila: A Gateway to thePhilippines

o The International Revenue Allotment (IRA)as a Source of Funds for LocalGovernance

o Statistical Capacity Building in thePhilippine Statistical System

o Reported Rape Cases in the Philippines• NSCB Technical Papers

o Environmental Accounting in thePhilippines

o Poverty Assessment in the Philippineso Rebasing, Unking and Constant Price

Estimation of the National Accounts of thePhilippines

o Recent Initiatives of the NSCB inImproving Official Statistics in thePhilippines

o Measuring the Contribution of the InfonnalSector in the Philippines

o Enhancing the Relevance of the PSNAo Challenges in the Compilation of Official

Poverty Statistieso NSCB Techndl Paper on The NSCB: Our

Products and services

Others

Standard Classifications• Philippine Standard Industrial Classification

(PSIC)o PSIC Ammendment 1997

• Philippine Standard Commodity Classification(PSCC), Rev, 21993o PSCC Ammendment 1999

• Phiippine Standard Classification for Education(PSCEd)

• Philippine Standard OCcupational Classification(PSOC)o PSOC Update 2003

• Philippine Central pAJductClassification(PC PC)

Proceedings of Conventions• National Convention on Statistics• Asian Regional Section, International

Conference on Statistical ComputingReference Materials

• Inventory of Airports• Inventory of Ports• Philippine Statistical pevelopment Program,

1999-2004 I• Profile of Censuses and Surveys• Directory of Statistical Services in the

Philippines• Catalogue of Philippine Statistical Publications• Directory of selectd Statistical Tenms• Manual on the Preparation of Statistical Project

Proposals I• A Guide to Statistics for Business Planning• Framework for the Development of

Environment Statistics• Registry of Top Forel9n Direct Investment

Enterprises in the Philippines• Compendium of Philippine Environment

Statistics• State of the Philippine Land and Soil

Resources I• Statistics for Entrepreneurs

Other NSCB Products and Services

Products

1. Statistical policies and measures to resolve specifIC issues and provide policydirections in the Philippine Statistical System I

2. The Philippine Statistical Development Program (PSDP) to serve as blueprint ofpriority programs and activities to be undertaken to improve the Philippine StatisticalSystem in the Medium Term .' I

3. National Accounts and related economic accounts to assess the economicperformance of the country thru the following:

• National AccountsRegional Accounts

• Input-Output (1-0) Accounts• National Heatth Accounts• National Education Accounts

4. Other social and economic indicators• Poverty statistics• Environment statistics• Food balance sheet

Indicators on children and womenGender and development statisticsQuarterty economic indicesForeign investments

• Leading economic indicatorsEconomic and social impact analysis indicators

• Human development index

5. Standards and dassification systems to prescribe uniform standards in governmentstatistics

Philippine Standard Occupational Classification (PSOC)• Philippine Standard Commodity Classification (PSCC)

Philippine Standard Industrial Classification (PSIC)• Philippine Standard Geographic Code (PSGC)• Philippine Standard Classification of Education (PSCED)• Philippine Classification of Commodities by Broad Economic Categories

(PCCBEC)Philippine Central Product Classification (PCPC)

6. Statistical publications to disseminate the most relevant information produced by thePSS and to make statistics more accessible to the public

Services

1. Maintenance of a one-stop statistical information center2. Monitoring of designated statistics3. Coordination of subnational statistical system4. Coordination of inter-agency concerns on statistics5. Survey review and dearance6. On-line statistical service through the internet (:.wv. ",0'.' oc': 0-)7. Servicing data requests8. Technical services9. Advocacy for statistical awareness

National Statistics Month• National Convention on Statistics• Government Statistics Accessibility Program• Hosting of international conferences in statistics

• .I. .. . •

Republlka ng PlliplnasPAMBANSANG LUPON SA UGNAYANG PANG-ESTADISTIKA

(NATIONAL STATISTICALCOORDINATION BOARD)1",2""" 5'" FIoon MlcIand Buendia BuUdIng

403 Sen. Gi J. Puyal Avenue, Makall City 1200

MEMORANDUM

FOR Her ExcellencyPresident GLORIA MACAPAGAL ARROYO

FOREIGN DIRECT INVESTM TS IN THE PHILIPPINESSecond Quarter 2006

The Honorable ROMULO L.Secretary of Socio-Economic Pia gand Chairman of the Nation tatistical Coordination Board

h. . The H~ET B. F~VILA,I -,. Secretary of the Department of Tra .

FROM:

RE

DATE 4 September 2006

1.

2.

3.

We are pleased to submit the Second Quarter 2006 Report dn Foreign DirectInvestments (FDI) in the Philippines as compiled by the Technical Staff of theNational Statistical Coordination Board (NSCB), in collaboration with the memberagencies of the NSCB Inter-Agency Committee on Foreign Direct InvestmentStatistics (IACFDIS). IThe NSCB IACFDIS is composed of the: NSCBas Chair, the Board of Investments(BOI) as Co-Chair, and the Bangko Sentral ng Pilipinas (BSP), the Securities andExchange' Commission (SEC), the Bureau of Trade Regulation and ConsumerProtection (BTRCP), the Philippine Economic Zone Authority (PEZA), the Subic BayMetropolitan Authority (SBMA), the Clark Development Corporation (CDC), theNational Economic and Development Authority (NEDA) and the National StatisticsOffice (NSO), as members. IThis report is based on the consolidated administrative data of the investmentpromotion agencies, namely, the BOI, PEZA, CDC and SBMA, and the BSP withsupplementary data on registered foreign investments through the SECand BTRCP.

4. The highlights of the report are as follows:

Approved foreign direct investments

Second Quarter 2006

4.1 Total approved foreign direct investments (FDIs) totaled PhP 52.7 billion in thesecond quarter of 2006, 348.5 percent higher than the PhP 11.7 billionapproved in the same quarter a year ago. The second quarter saw a hike ininvestment pledges to the manufacturing sector, a sustained level for theservices sector, and a notable increase in investment pledges to the tradesector. The manufacturing sector is the top recipient of investment pledges forthe second quarter, retaining its rank in the first quarter of 2006 when pledgesto the sector reached a high PhP 59.6 billion.

leI. Nos. 895-2395 897.2171 896-4665896-1787 896-1796 896-7975

Fax Nos. 895-2765 890-8456

URL:http://www.nscb.gov.phE-mail address:[email protected]

. . 1. J.

4.2 Among countries, the United States of America (U.S.A.) waslthe leading sourceof approved FDIs in the second quarter of 2006, registering PhP 16.6 billionworth of pledges mainly to the trade sector. China followed closely with itspledge to inject PhP 16.3 billion, practically all or 99.9 percent of which iscommitted to the manufacturing sector. Other significant contributors duringthe period included Netherlands and Japan.

4.3 FDI pledges to the manufacturing sector grew by 167.6 percent, from PhP 9.3billion in the second quarter of 2005 to PhP 24.8 bill"on a year later,contributing 47.0 percent to the total approved FDIs in the second quarter of2006. The growth in pledges was propelled by the SBMA-approved project toengage in the manufacture of glass products, worth PhP 16.2 billion whichcomprised 65.5 percent of the FDIs pledged to the sector in the second quarterof 2006. IApproved FDIs in the services sector, meanwhile, rose by 32.8 percent to PhP2.9 billion in the second quarter of 2006, increasing from its PhP 2.2 billionlevel in the same period in 2005.

4.4 The trade sector is seen to be boosted by a BOI-approved project in wholesale& retail trading activities of a fast food chain in the country, which is expectedto infuse PhP 9.8 billion worth of investments, constituting 50.1 percent of thetotal FDIs in the trade sector in the quarter. I

4.5 Significant investment commitments to the communications sector and thefinance and real estate sector, posted at PhP 2.67 billion and PhP 2.70 billion,respectively, likewise pushed the levels of FDIs in the quarter, with combinedvalues contributing 10.2 percent or PhP 5.4 billion of the total FDIs in thequarter. I

4.6 Investment projects with foreign interest, approved in the second quarter of2006, was estimated to generate 39,459 jobs, up 76.3 percent from the 22,380jobs expected from projects approved in the same period in 2005. Anestimated 22,482 jobs, representing 57.0 percent of total jotls from approvedinvestments with foreign interest were expected to come from PEZA-approvedinvestment projects.

January - June 2006

4.7 The cumulative January to June approved foreign direct investments (FDIs)totaled PhP 116.2 billion, up 168.7 percent from the PhP 43.3 billion reported in2005. It is worth noting that the cumulative January to June 2006 figure ofapproved FDIs constitutes the fourth highest semester value of investmentpledges since the start of the compilation of the FDIs statistics in 1996.

4.8 Potential investments to the manufacturing sector reached PhP.84.4 billion, up190.9 percent from its previous year's level of PhP 29.0 billion. Investmentpledges to the trade sector was posted at PhP 19.5 billion which was asignificant improvement over the PhP 33.2 million worth of investmentscommitted in the first semester of 2005. The services sector on the other handregistered PhP 6.6 billion worth of investment pledges, growing by 119.3percent from PhP 3.0 billion in the same period a year ago. The first semester

level of approved FDIs was boosted by a huge pledge to the manufacturingsector by South Korea, which was worth PhP 51.7 billion or M.5 percent of thetotal approved FDIs in the first semester of 2006.

4.9 South Korea topped the list of countries with the most investment pledges inthe first six months of 2006 at PhP 52.1 billion. The U.S.A., likewise, cut a bigchunk of the pie at 19.8 percent of total approved investments, outpacingChina for the number two spot with its PhP 23.0 billion worth of investmentcommitments in the first semester of 2006. China pledgee PhP 16.7 billionworth of investments, representing 14.4 percent of total FDI pledges in theperiod. The cumulative investment pledges from South Korea, the U.S.A. andChina brought in 79.0 percent of the total potential FDIs in the first semester of2006.

4.10 The total projected number of jObs from approved projects with foreigninterest from January to June 2006 was estimated to reach 72,051 new jobswhich was 85.7 percent higher than the 38,795 expected jobs from theprevious year's approved FDI projects.

Approved investments, foreign and Filipino nationals

Second Quarter 2006

4.11 The combined investment pledges of foreign and Filipino nationals expandedto PhP 101.5 billion in the second quarter of 2006, a 68.3 percent increasefrom the PhP 60.3 billion worth of commitments a year ago

4.12 Total investments approved by BOI and SBMA valued at PhP 68.7 billion andPhP 17.8 billion, respectively, constituted 85.2 percent of the total approvedinvestments in the second quarter of 2006. The rest of the investmentpledges comprising 14.8 percent were made through PEZA and CDC.

4.13 The combined foreign and Filipino investment projects lapproved in thesecond quarter of 2006 are expected to generate 41,977 new jobs, a 59.9percent improvement over the 26,258 projected jobs from projects approvedin the second quarter of 2005. PEZA and BOI-approvedl investments areexpected to produce 82.4 percent or 34,584 of the total jobs from approvedprojects in the second quarter of 2006. The sizeable 76.4 percent of theexpected new jobs are intended for the manufacturing and servicesindustries, each standing to get 53.1 percent and 23.3 percent, respectively,of the total projected employment.

January - June 2006

4.14 Total approved investments by foreign and Filipino nationals stood at PhP174.6 billion in the first semester of 2006 which was 38.1 percent higher thanthe PhP 126.4 billion reported in the same period in 2005.

4.15 Approved Filipino investments comprised 33.4 percent of the total investmentspledged during the period while FDIs comprised 66.6 percent. In the firstsemester of 2005, the sharing was 65.8 percent Filipino and 34.2 percent

J. "

foreign. Investment pledges from Filipino investors was boosted in the firstsemester of 2006 by the approval of investments in the communicationssector, valued at PhP 36.3 billion or 62.2 percent of total Filipino investmentsin the first half of 2006.

4.16 The projected cumulative number of jobs from investment pledges in the firstsemester of 2006 is seen to reach 80,134, a 70.0 percent increase from the47,135 jObs estimated to be generated from last year's investment pledges inthe same period. PEZA-approved investments stand to generate a total of45,772 jobs representing 57.1 percent of the total projected jobs fromprojects approved in the first six months of 2006.

Approved investments in the Information and Communications Technology(ICT) Industry

Second Quarter 2006

4.17 Potential FDIs in the Ief industry increased by 27.6 percent in the secondquarter of 2006, posting PhP 2.7 billion worth of inyestment pledgescompared to the previous year's level of PhP 2.1 billion. Filipino nationals,meanwhile, pledged less investments in the Ief industrv in the secondquarter with PhP 604.1 million, 72.3 percent less than its previous year'spledges of PhP 2.2 billion.

4.18 Seventy percent of the approved FDIs in Ief were coursed t;hrough PEZAandmore than 91.8 percent, or PhP 2.5 billion worth of FDIs in Ief wereintended for the IT services sector. I

4.19 The ref industry is expected to create 23.3 percent of the total number ofjobs from all approved investments in the quarter or 9,796 new jobs.

January - June 2006

4.20 On a semestral basis, a drop of 33.8 percent in approved investments in theIef industry was observed, decreasing from PhP 10.3 billion in 2005 to PhP6.8 billion this year. Pledges from both Filipino and foreign nationals dropped,the former by 64.8 percent and the latter by 23.7 percent. I

4.21 The approved Ief projects of both Filipino and foreign investors in the firstsemester of 2006 are expected to generate 27,223 new jobs, 25,684 of whichare for IT services.

A ..•. Z..

Actual foreign direct investments in the Balance of Payments

First Quarter 2006

4.22 Actual FDIs as compiled by the Bangko Sentral ng Pilipinas in the Balance ofPayments (BOP) posted a 5.0 percent year-on-year increase in the firstquarter of 2005, from PhP 21.2 billion in the first quarter of 2005 to PhP 22.3billion in 2005. I

4.23 Net equity capital reached PhP 9.5 billion during the quarter, down by 54.7percent from the PhP 21.0 billion reported in the same Reriod a year ago.Reinvested earnings, meanwhile, posted a net inflow of PhP 1.1 billion fromlast year's PhP 935.5 million. Other capital posted a turn around from a netoutflow of PhP 770.5 million in the first quarter of 2005 to a net inflow of PhP11.5 billion in the first quarter of 2005.

5. For Her Excellency's information.

.L •. ....1. ..E!. , e--

Foreign Direct Investments in the PhilippinesSecond Quarter 2006 and First Semester 2006

Total approved foreign direct investments (FDls) totaled PhP 52.7 billion in the secondquarter of 2006, 348.5 percent higher than the PhP 11.7 billion approved in the same quartera year ago. (Part I, FigureA and Part II - Table 1a and Figure 1). The second Cjuarter saw a hikein investment pledges to the manufacturing sector, a sustained level for t~e services sector,and a notable increase in investment pledges to the trade sector (Part II -Table 3a and Figure3). The manufacturing sector is the top recipient of investment pledges for the secondquarter, retaining its rank in the first quarter of 2006 when pledges to the. sector reached ahigh PhP 59.6 billion.

Figure AApproved investments by Filipino and Foreign Nationals:

Second Quarter 2005and 2006

Q2 2006

50.048.6

140.0

"-.c"- 30.0mcg

20.0:c-" 11.7

10.0

Q2 2005

52.7 48.8

I!I FDI o Filipino investments

The combined approved investments of Filipino and foreign nationals, meanwhile, expandedin the second quarter of 2006, reaching PhP 101.5 billion, up 68.3 percent from the PhP 60.3billion reported in same period in 2005 (Part II • Table 7a and Figure 7). bringing the totalapproved investments for the first semester 2006 to PhP 174.6 billion which is 38.1 percentmore than previous year's level of PhP 126.4 billion (Part 11- Table 6b).

Aboul this reportthiS repor1 IS II'le tnirty seventh of a senes on quarterty statlS1/CSon foreign drrectInvestments (FO!s) tn the Philippines, integ'"allng ttle quarterly statIStical reports on FDtssuomrned by the governments mvestments promollon, admmstrallon and regUlationagellCles as of 8 Augvs12006 It provides an analysis of the:

la) tOl"elfln dlrec:f UlVestmsnfS and mvestments by Flllp,nos approVfJd by theBoard of In..-estments (BOI), Philippine Economic: Zone Autnortty (PEZAl.ClarK Devdooment CorporatIOn (CDC), and SUbic Bay MetropolitanAuthOnty(SBMA) for tne first qool1er 01200510 the second quarter at 2006;

(D) BCfua! fOf6IfJn dIrect mvestments as presenled in the B8/ance of Payments(BOP) by the Depanment of EcxmomiCResearCh of tne BanglW Sentral ngPillpinas (BSP) tor the first qu3f1er 012005 10the first quaner of 2006

Also featured are data on fClfe1gndlred Investments reglS1ered thfOl.I;;lh too SecuntleSaM Exchange ConYnISSlOn(SEC) and the Bureau of Trade RegUiallon and ConsumerProlectlOn (BTRCP) of the Oepartmenl at Trade and Industry (011). Annex A presentsthe 1eehnical noles on the data and compilation mell1odology ...mIleAnnex B Qlves abrlef badl;ground on the FOreign Investment Intonnahon System (FilS) thai generalesthe FDI stabsllCSpresented In thIS report

InsidePart I • Analysis IA..ApproveOforeign direcl

Investments..................... 2

B.ApproveO investments by FilipinoaM foreign nationals............... 4

C.Ap'proved investments in theInformation and CommunicationsTechnology............................ 6

D.Actual foreign direct investmentsin the Balance of Payments....... 8

Part 11- Statistical Tables

Annexes I

-=.....=="-""""_..z::.=il::... •.•••""'i~=':.l.~'.",';;':';ID,;=4!..

IForeign Direct Invest ents, Q2 2006

Meanwhile, actual foreign direct investments (FDls) or the net non-residents' investments ascompiled in the Balance of Payments (BOP) increased by 5.0 percent, from PhP 21.2 billionin the first quarter of 2005 to PhP 22.3 billion in the first quarter of 2006 (Part I - Figure 0 andPart II - Table 9a).

Part IAnalysis

A. Approved foreign direct investments

1. Second Quarter 2006

Table AApproved foreign direct investments

Second Quarter 2005 and 2006(in million pesos)

Investment Promotion Q22005 Q22006 PencentchangeAgency I

BOI 5,793.0 24,033.6 314.9PEZA 5,857.1 8,575.9 46.4SBMA 1.5 16.718.0 1,131,111.2CDC 95.4 3,360.3 3,423.6

Total 11,746.9 52,687,9 348.5

Total approved foreign direct investments (FDls) swelled in the second tuarter of 2006,increasing by 348.5 percent from PhP 11.7 billion in the second quarter of 2005 to PhP 52.7billion in the second quarter of 2006 (Part I - Table A and Part II - Table 1 and Figure 1). Thequarter in review saw a considerable increase in pledges to the trade, cO"lmunication and,finance and real sectors, contributing a cumulative PhP 24.9 billion worth of investmentpledges for the quarter (Part II - Table 3a and Figure3). IFDI pledges to the manufacturing sector grew by 167.6 percent, from PhP 9.3 billion in thesecond quarter of 2005 to PhP 24.8 billion a year later, contributing 47.0 percent to the totalapproved FDls in the second quarter of 2006. The growth in pledges was propelled by theSBMA-approved project to engage in the manufacture of glass products, worth PhP 16.2billion which comprised 65.5 percent of the FDls pledged to the sector in the second quarterof 2006.

Approved FDls in the services sector, meanwhile, rose by 32.8 percent to PhP 2.9 billion inthe second quarter of 2006, increasing from its PhP 2.2 billion level in the same period in2005 (Part II - Table 3a),

The trade sector is seen to be boosted by a BOI-approved project in wholesale & retailtrading activities of a fast food chain in the country, which is expected to linfuse PhP 9.8billion worth of investments, constituting 50.1 percent of the total FDls in the trade sector inthe quarter. ISignificant investment commitments to the communications sector and the finance and realestate sector, posted at PhP 2.67 billion and PhP 2.10 billion, respectively, likewise pushedthe levels of FDls in the quarter, with combined values contributing 10.2 percent or PhP 5.4billion of the total FDls in the quarter.

2

, .- .L - .•., --

Foreign Direct Investments, 02 2006

All investment promotion agencies showed vigor in their investment approvals in the secondquarter of 2006_ Investment applications approved by the Board of Investments (BOI)accounted for PhP 24.0 billion or 45.6 percent of total FDls in the second quarter of 2006, upby 314.9 percent from the previous year's level for the same period (Part II - Table 1a)_Notable increases in investment approvals were observed for SBMA and CDC, withcombined approvals a=unling for 38-1 percent or PhP 20.0 billion worth of the totalapprovals in the second quarter of 2006 compared to the PhP 96_8 million tumout in thesame period a year ago. _' IAmong countries, the United States of America (U_SA) was the leading source of approvedFDls in the second quarter of 2006, registering PhP 16_6billion worth of pledges mainly tothe trade sector (Part II - Table 2a & Figure 2). China followed dosely with its pledge to injectPhP 16_3 billion, practically all or 99.9 percent of which is commil1ed to the manufacturingsector. Other significant contributors during the period included Netherlands and Japan_

Investment projects with foreign interest, approved in the second quarter of 2006, wasestimated to generate 39,459 jobs, up 76.3 percent from the 22,380 jobs expected fromprojects approved in the same period in 2005 (Part 11- Table 4b). An estimated 22,482 jobs,representing 57.0 percent of total jobs from approved investments with for~ign interest wereexpected to come from PEZA-approved investment projects.

2. January to June 2006

The cumulative January to June approved foreign direct investments (F.Dls) totaled PhP116.2 billion, up 168.7 percent from the PhP 43.3 billion reported in 2005. (Part 1- Figure Band Part II - Table 1b). It is worth noting that the cumulative January to June 2006 figure ofapproved FDls constitutes the fourth highest semester value of investment pledges since thestart of the compilation of the FDls statistics in 1996.

Figure BApproved foreign direct investments:

First Semester 2005 and 2006

120.0

1100.0 1

80.0 I"- ]-"Co

~ 60.0 43.3:.c I.£ 40.0 1I

20.0 J

Isem 1 2005

1162

sem 12006

A total of PhP 110.5 billion or 95.1 percent of the total value of approved FDls in the first sixmonths of 2006 (Part II - Table 3b) was intended for the manufacturing, trade and servicessectors. IPotential investments to the manufacturing sector reached PhP 84.4 billion, up 190.9 percentfrom its previous year's level of PhP 29.0 billion. Investment pledges to the trade sector wasposted at PhP 19.5 billion which was a significant improvement over the PhP 33.2 million

3

Jo. •• , . ' .=. _ _ .IIt;=i,="""" •.•-'"",,"""IIlII!:II!li:t.l.:=_~ll<.il~~Y'!!'

Foreign Direct Investients, 02 2006

Iworth of investments committed in the first semester of 2005. The services sector on theother hand registered PhP 6.6 billion worth of investment pledges, growing by 119.3 percentfrom PhP 3.0 billion in the same period a year ago. The first semeste~ level of approvedFDls was boosted by a huge pledge to the manufacturing sector by South Korea, which wasworth PhP 51.7 billion or 44.5 percent of th~ total approved FDls in the first semester of2006. IAmong the country's four investment promotion agencies, SBMA came on top as the biggestsource of FDls, approving FDI applications valued at PhP 68,1 !lillian or 58.6 percent of totalFDls approved in the first semester of 2006. BOI followed with an estimated approval of PhP26.4 billion which represented 22.8 percent of the period's total FDls. The combinedapprovals of PEZA and CDC comprised 18.6 percent of total FDls for the year (Part 11- Table1b),

South Korea topped the list of countries with the most investment pledges in the first sixmonths of 2006 at PhP 52.1 billion (Part II - Table2b). The U.S.A., likewise, cut a big chunk ofthe pie at 19,8 percent of total approved investments, outpacing China for the number twospot with its PhP 23.0 billion worth of investment commitments in the first semester of 2006,China pledged PhP 16.7 billion worth of investments, representing 14,4 percent of total FDIpledges in the period, The cumulative investment pledges from South Korea, the U.S.A. andChina brought in 79.0 percent of the total potential FDls in the first semester of 2006,

The total projected number of jobs from approved projects with foreign interest from Januaryto June 2006 was estimated to reach 72,051 new jobs which was 85.7 percent higher thanthe 38,795 expected jobs from the previous year's approved FDI projects (Part 11- Table 4d),

B. Approved investments by foreign and Filipino nationalsby promotion agency

1. Second Quarter 2005

The combined investment pledges of foreign and Filipino nationals expanded to PhP 101,5billion in the second quarter of 2006, a 68.3 percent increase from the PhP 60.3 billion worthof commitments a year ago (Part 1- FigureC and Part 11-Table 6a and Figure7).

Figure CApproved Investments, Foreign and Filipino Nationals:

Second Quarter 2005and 2006

55.0

1 48.848,6 52,745,0 -,

I

35.0 I"- 1

IE I

I~25,0

,~15.0 1 11.7

5,0I"

(5,0) J Q2 2005 Q2 2006

.FDI OFili ino investments

4

Foreign Direct Investlents, 02 2006

Investment pledges from Filipino investors reached PhP 48.8 billion du~ng the quarter, aslight 0.6 percent increase over the PhP 48.6 billion worth of approvals in the second quarterof 2005. The level of investment pledges from Filipino nationals was improved by the BOI-approved pledge to the communication sector, particularly in activities in the mobiletelephone system, valued at PhP 33.2 billion which represents 67.91 percent of totalinvestment pledges from Filipino nationals in the quarter.

Total investments approved by BOI and SBMA valued at PhP 68.7 billion and PhP 17.8billion, respectively, constituted 85.2 percent of the total approved investments in the secondquarter of 2006 (Part II - Table 7a). The rest of the investment pledges comprising 14.8percent were made through PEZA and CDC.. IThe combined foreign and Filipino investment projects approved in the second quarter of2006 are expected to generate 41,977 new jobs, a 59.9 percent improvement over the26,258 projected jobs from projects approved in the second quarter of 2005 (Part II - Table 4a& Figure 4). PEZA and BOI-approved investments are expected to produce 82.4 percent or34,584 of the total jobs from approved projects in the second quarter of 2006. The sizeable76.4 percent of the expected new jobs are intended for the manufacturing and servicesindustries, each standing to get 53.1 percent and 23.3 percent, respectIVely, of the totalprojected employment (Part I • TableB).

Table BProjected employment on approved investments by industry:

Second Quarter 2005and 2006

Industry Q2 2005 Q22006 Percent to total Q2 Percent to total2006 Q22006

Agriculture 41 183 0.2 0.4Communication 300 494 1.14 1.2Construction 86 274 0.3 0.7ElectricityFinance& Real Estate 308 1,238 1.2 2.9GasManu1acturing 15,351 22,305 58.5 53.1Mining 445 85 1.7 0.2Services 9,618 9,787 36.6 23.3Storage 21 0.1Trade 39 7,316 0.1 17.4Transportation 70 274 0.3 0.7

Total 26,258 41,9n 100.0 100.0

2. January to June 2006

Total approved investments by foreign and Fifipino nationals stood at PhP 174.6 billion in thefirst semester of 2006 which was 38.1 percent higher than the PhP 126.4 billion reported inthe same periiod in 2005 (Part II - Tables 6b and 7b). IBOI was the top source of project approvals for the combined investments of Filipino andforeign nationals, with a total value of PhP 74.3 billion representing 42.6\percent of totalvalue of investment pledges in the first six months of 2006.

Approved Filipino investments comprised 33.4 percent of the total investments pledgedduring the period while FDls comprised 66.6 percent. In the first semester of 2005, thesharing was 65.8 percent Filipino and 34.2 percent foreign (Part II - Tables 7b). Investment

5

• .•...

IForeign Direct Investrents, 02 2006

pledges from Filipino investors was boosted in the first semester of 2006 by the approval ofinvestments in the communications sector, valued at PhP 36.3 billion or 62.2 percent of totalFilipino investments in the first half of 2006.

The projected cumulative number of jobs from investment pledges in tHe first semester of2006 is seen to reach 80,134, a 70.0 percent increase from the 47,135 jobs estimated to begenerated from last year's investment pledges in the same period (Part II -Table 4c). PEZA-approved investments stand to generate a total of 45,772 jobs representing 57.1 percent ofthe total projected jobs from projects approved in the first six months of 2006.

C. Approved investments in the Information and commUniCatiJns Technology(ICT) Industry

1. Second Quarter 2006

Potential FDls in the ICT industry increased by 27.6 percent in the second quarter of 2006,posting PhP 2.7 billion worth of investment pledges compared to the previous year's level ofPhP 2.1 billion (Part I - Table C and Part II - Table Sa). Filipino nationals, meanwhile, pledgedless investments in the ICT industry in the second quarter with PhP 604.1 million, 72.3percent less than its previous year's pledges of PhP 2.2 billion.

Table CApproved investments in ICT by ICTsub-industry;

Filipino and Foreign: Second Quarter 2006(in million pesos)

Sub-industry Foreign Filipino Total Percent to Total

Manufacturing 218.2 90.3 308.5 9.4Trade 3.0 3.0 0.1Telecomm. 327.6 327.6 10.0IT services 2,466.9 186.2 2,653.1 80.6Total 2.688.1 604.1 3,292.2 100.0

Percent Share 81.6 18.4 100.0

Seventy percent of the approved FDls in leT were coursed through PEZA (Part II - Table Sa)and more than 91.8 percent, or PhP 2.5 billion worth of FDls in ICT were intended for the ITservices sector (Part I - Table C and Part II - Table 5b.1). IThe ICT industry is expected to create 23.3 percent of the total number. of jobs from allapproved investments in the quarter or 9,796 new jobs (Part 1- Table D & Part 11-Table 4a).

6

Table DPrDjected emplDyment in ICT by ICT sub-industry

SecDnd Quarter 2006

Industry

ManufacturingTradeIT ServicesTelecomm.

TDtal

2. January to June 2006

ProjectedemplDyment

6313

9.14319

9,796

PercenttDtDtal

6.40.0

93.30.2

100.0

On a semestral basis, a drop of 33.8 percent in approved investments in the ICT industrywas observed, decreasing from PhP 10.3 billion in 2005 to PhP 6.8 billion this year (Part I -Table E & Part II - Table 5a.2). Pledges from both Filipino and foreign nationals dropped, theformer by 64.8 percent and the latter by 23.7 percent.

Table EApprDved investments in ICT by ICT sub-industry

First Semester 2005 and 2006(In million Pesos)

Sub-industry sem 1 2005 sem 1 2006Percent tototal sem

IT Services 3,156.9 5,426.1 79.2Manufacturing 5,170.1 1,090.5 15.9Telecomm. 2,019.5 327.6 4.8Trade 3.0 0.0

Total 10,346.5 6,847.2 100.0

IT services, growing by 71.9 percent in the first half of 2006. stand to receive the lion's shareof 79.2 percent of investment pledges in ICT for the semester with PhP 5,4 billion.Investments intended for the manufacturing sector, meanwhile, was estimated at PhP 1.0billion, down 78.9 percent from the PhP 5.2 billion pledged in the first six months of 2005(Part I - Table E and Part II - Table 5b.2).

The approved ICT projects of both Filipino and foreign investors in the first semester of 2006are expected to generate 27,223 new jobs, 25,684 of which are for IT services (Part I - TableF).

Table FProjected emplDyment in ICT by ICT sub-industry:

Sem 1 2005 and Sem 1 2006

Sub-industry sem 12005 sem 1 2006Percent tDtDtal sem

IT Services 14,024 25.684 94.3Manufacturing 1,906 1,517 5.6Telecomm. 300 19 0.1Trade 3 0.0

Total 16,230 27,223 100.0

7

=oreign Direct Investments, 02 2006

D. Actual Foreign direct investments in the Balance of Payments 1

1. First Quarter 2006

Actual FDls as compiled by the Bangko Senlra! ng Pilipinas in the Balance of Payments(BOP) posted a 5.0 percent year-on-year increase in the first quarter of 2006, from PhP 21.2billion in the first quarter of 2005 to PhP 22.3 billion in 2006 (Part II - Table 9a)

In dollar terms, non-resident's investments increased by 11.4 'percent, tolUS$ 430 millionfrom US$ 386 million a year ago (Part II - Table9b).

Net equity capital reached PhP 9.5 billion during the quarter, down by 54.7i percent from thePhP 21.0 billion reported in the same period a year ago. Reinvested earnings, meanwhile,posted a net inflow of PhP 1.1 billion from last year's PhP 935.6 million. Other capital posteda turn around from a net outflow of PhP 770.5 million in the first quarter of 2005 to a netinflow of PhP 11.6 billion in the first quarter of 2006 (Part1-Figure D and Part II - Table 9a).

Figure DBalance of Payments: First Quarter 200S and 2006

25.0

] 22.3 m 01 200520.0 01 2006

I IIe.. 15.0 J

11.6'" I,e..Ie 10.0i~ Ji~ 5.0

I 0.9 1.1I

I(0.8)

(5.0) jNon ~ Net Equity Reinwsted Other Capital

Residents' Capital EarningsIn'vestments

Ball:::"'<'S::ntr.~; II':: f'ihrm:l:-' ,:omniIJIIOn II; Balan •...•.(If !'J~:1l'':1lt''I fH IP j 1:- j quan •..., h.:hllld the.' <:nmnilatlllll (I!"

:\pprll\cu rtlr..:igll Dir..:c! In\..;QJ1l\:m •..

8

PART II

STATISTICAL TABLES

- - . .•

Symbols Used

Symbolspr*

MeaningPreliminaryRevisedLess than half the unit employedZeroNot applicable

Table A

Table 8

Table C

Table D

Table E

Table F

Table 1a

Table 1b

Table 2a

Table 2b

Table 3a

Table 3b

Table 4a

Table 4b

Table 4c

Table 4d

Table 5a.1

LIST OF TABLES

Total Approved Foreign Direct InvestmentsSecond Quarter 2005 and 2006

Projected Employment on Total Approved Investments by Industry,Second Quarter 2005 and 2006

Total Approved Investments in Information and Communications TeChnolOgy(ICT) Industryby ICT Sub-industry, Foreign and Filpino Nationals I .Second Quarter 2006

Projected Employment on Total Approved ICT Investments, by ICT sUb-ildustrySecond Quarter 2006

Total Approved Investments in Information and Communications Technology (ICT) Industryby ICT Sub-industry, Foreign and Filpino NationalsFirst Semester 2005 and 2006

Projected Employment on Total Approved ICT Investments, by ICT Sub-inaustryFirst Semester 2005 and 2006

Total Approved Foreign Direct Investments by Promotion AgencyFirst Quarter 2005 to Second Quarter 2006

Total Approved Foreign Direct Investments by Promotion AgencyFirst Semester 2005 to First Semester 2006

Total Approved Foreign Direct Investments by Country of InvestorFirst Quarter 2005 to Second Quarter 2006

Total Approved Foreign Direct Investments by Country of InvestorFirst Semester 2005 to First Semester 2006

Total Approved Foreign Direct Investments by IndustryFirst Quarter 2005 to Second Quarter 2006

Total Approved Foreign Direct Investments by IndustryFirst Semester 2005 to First Semester 2006

Projected Employment on Approved InvestmentsFirst Quarter 2005 to Second Quarter 2006

Projected Employment on Foreign Direct Investments(Approved Projects with Foreign Interest)First Quarter 2005 to Second Quarter 2006

Projected Employment on Approved InvestmentsFirst Semester 2005 to First Semester 2006

Projected Employment on Approved Projects with Foreign Interest,First Semester 2005 to First Semester 2006

Total Approved Investments in the Information andCommunication Technology (lCT) Sector by Promotion AgencyFirst Quarter 2005 to Second Quarter 2006

Page

2

5

6

7

7

7

9

10

11

12

13

14

15

16

17

18

19

.•

PageTable 5a.2 Total Approved Investments in the Information and

Communication Technology (ICT) Sector by Promotion AgencyFirst Semester 2005 to First Semester 2006 20

Table 5b.1 Total Approved Investments in the Information andCommunication Technology (ICT) Sector by Sub-IndustryFirst Quarter 2005 to Second Quarter 2006 21

Table 5b.2 Total Approved Investments in the Information andCommunication Technology (ICT) Sector by Sub-IndustryFirst Semester 2005 to First Semester 2006 22

Table 6a Total Approved Investments by Promotion AgencyFirst Quarter 2005 to Second Quarter 2006 23

Table 6b Total Approved Investments by Promotion AgencyFirst Semester 2005 to First Semester 2006 24

Table 7a Total Approved Investments by Nationality (Filipino and Foreign) andby Promotion Agency, First Quarter 2005 to Second Quarter 2006 25

Table 7b Total Approved Investments by Nationality (Filipino and Foreign) andby Promotion Agency, First Semester 2005 to First Semester 2006 26

Table 8a Total Approved Investments (Filipino and Foreign) by IndustryFirst Quarter 2005 to Second Quarter 2006 27

Table 8b Total Approved Investments (Filipino and Foreign) by IndustryFirst Semester 2005 to First Semester 2006 28

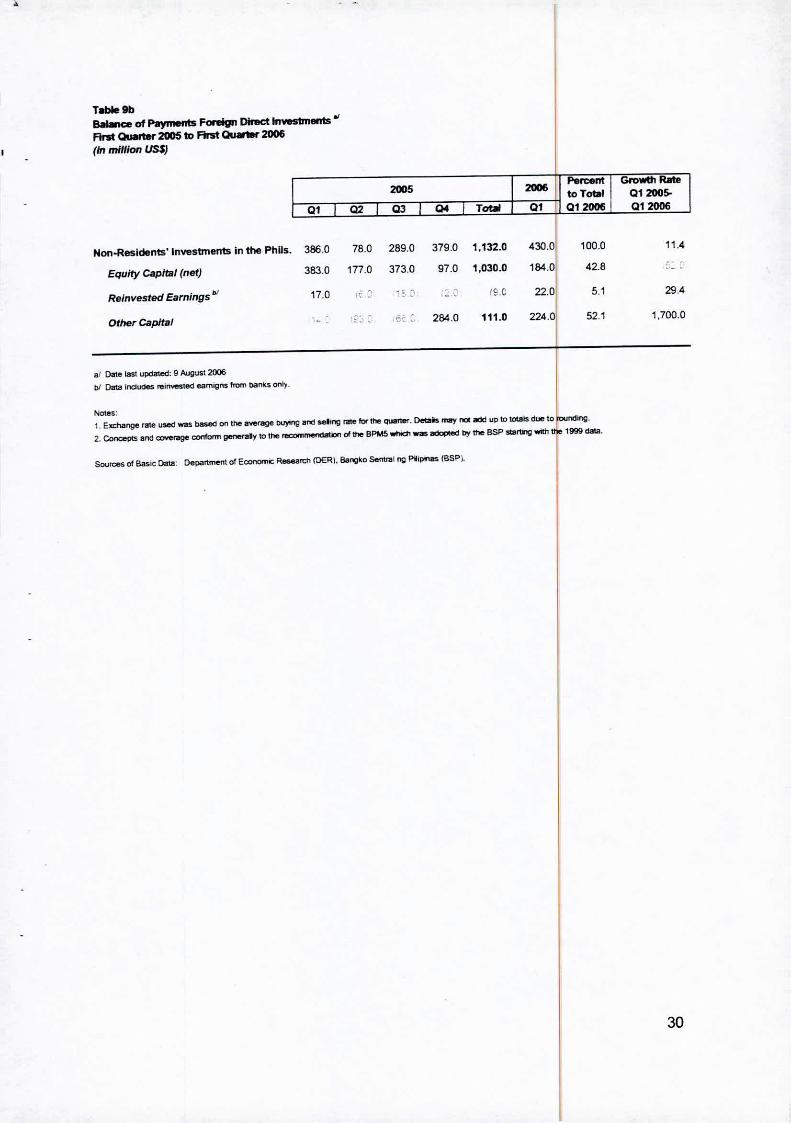

Table 9a Balance of Payments Foreign Direct InvestmentsFirst Quarter 2005 to First Quarter 2006 (in million Pesos) 29

Table 9b Balance of Payments Foreign Direct InvestmentsFirst Quarter 2005 to First Quarter 2006 (in million US $) 30

Table 10 Registered Foreign Direct Investments (SEC and BTRCP)by Country of Investor, First Semester 2002 to Second Semester 2002 31

Table 11 Registered Foreign Direct Investments (SEC and BTRCP)by Country of Investor, by Type of Investment,First Semester 2002 to Second Semester 2002 32

Table 12a Registered Foreign Direct Investments of BSP FDI Firms by Countryof Investor, First Quarter 2005 to Second Quarter 2006 33

Table 12b Registered Foreign Direct Investments of BSP FDI Firms by Countryof Investor, First Semester 2005 to First Semester 2006 34

Table 13a Registered Foreign Direct Investments of BSP FDI Firms byIndustry, First Quarter 2005 to Second Quarter 2006 35

Table 13b Registered Foreign Direct Investments of BSP FDI Firms byIndustry, First Semester 2005 to First Semester 2006 36

.!L •. 1E!-ll...ll.!!III! IIl.::l!l!lll!l!l.m!l!.MIl:.l!l!MI' ~.•!!

LIST OF FIGURESPage

Figure A Total Approved Foreign Direct InvestmentsSecond Quarter 2005 and 2006

Figure B Total Approved Foreign Direct InvestmentsFirst Semester 2005 and 2006 3

Figure C Total Approved Investments, Foreign and Filipino NationalsSecond Quarter 2005 and 2006 4

Figure 0 Balance of Payments, FDIFirst Quarter 2005 and 2006 8

Figure 1 Total Approved Foreign Direct Investments, by Country of Investor.Second Quarter 2005 and 2006 9

Figure 2 Total Approved Foreign Direct Investments, by Country of Investor.Second Quarter2006 11

Figure 3 Total Approved Foreign Direct Investments by IndustrySecond Quarter 2006 13

Figure 4 Projected Employment on Approved Investments,Second Quarter 2005 and 2006 15

Figure 5 Percent Share of ICT Sector in the Total Approved FDls 19Second Quarter 2006

Figure 6 Percent Share of ICT Sector in the Total Approved FDlsby Sub-Industry, Second Quarter 2006 21

Figure 7 Total Approved Investments (Filipino and Foreign),Second Quarter 2005 and 2006 23

Figure 8 Percent Share of Total Approved Investments, by Nationality (Filipino anForeign), Second Quarter 2005 and 2006 25

Figure 9 Total Approved Investments (Filipino and Foreign), by Industry,Second Quarter 2006 18

Figure 10 Balance of Payments FDIFirst Quarter 2005 and 2006 19

."

314.946.4

1,131,111.23,423.6

346.5

'.

45.616.331.76.4

100.0

24,033.68,575.

16,718.03,360.352,687.9

2,413,58,829.7

51.385.89012

63,530.1

43,796.949,842.2

836.71,329.0

95,806.8

12,824.322.276.1

103.71,147.236,351.3

6,064.59.717.8

366.154.8

16,203.3

5,793.05,857.1

1.595.4

11,746.9

19.115.111.9912

367.331.6

31,505.2

BOIPEZASBMACDC

Total

-

Table la.Total Approved Foreign Direct Investments by Promotion Agenc)First Quarter 2005 to Second Quarter 2006(in million pesos)

Approved FDI Percent to Growth RateAgency 2005 I 2006 I Total 02 02 2005-

Ql I 02 f Q3 I Q4 I Total I Ql. I 021 2006 02 2006

I

af ReVISed tor 01 2006 801 figures

Noles:

1. Approved Investments refer to the pro,ed cost cy committed rnvestments by RI!PlOOand tor'elgn if1"leStors

2. Details may nol add up 10CalaISBJe to mooci'ng

SOIJrces of B3Slc DB'S' Board Of InvesJments (801). Phihpptne EttJnO'nIC Zone Ault"Iotify (pEZAl. Subic Bay Metropolital Aumonty (SBMA)

arid Ciai'll; Oevelopmenl CorPcr.IIoo (CDC).

F~tml1Total approved foreign direct Investments:

Q2 2005 .nd Q2 2006

60.0

45,0•£•~c

30.0g~E

15.0 11.7

52.7

Q2 2005 Q2 2Oll6

9

... -

Table 1b.Total Approved Foreign Direct Invesbnents by Promotion AgencyFirst Semester 2005 to First Semester 2006(in million pesos)

Approved FDI Percent to I Growth RateAgency 2005 r 2006 Total sem 1 sem 12005-

sem 1 I sem2 I Total I sem 1 2006 sem 12006

BOI 24,908.1 18,888.8 43,796.9 26,447.0 22.8 6.2PEZA 17,848.3 31,993.9 49,842.2 17,405.6 15.0 (2.5)SBMA 368.8 469.8 838.7 68,103.8 58.6 18,365.2CDC 127.0 1,202.0 1,329.0 4,261.5 3.7 3,255.9

Total 43,252,1 52,554.6 95,806.8 116,218.0 100.0 168.7

Notes; I1. Approved Investments refer to the project cost or committed investments by Filipino and foretgn investors.

2. Details may not add up to lotals due 10 ",undlng. ISources of Bask; Data: Board of Investments (BOl), Philippfne Econom;c Zone Authority (PEZA), Subic Bay MelTopolttan

Aurtlortty (SBMA) and Clark Development Corpocahon (CDC).

10

J. .I,J.

52. .963,5JO.Total 31,505.2 11,746.9 16.203.3 36,351.3 95.806

a/ Revrsed for 01 2006 BOI flglJl"e$.

Notes:1. Approved 1nvestrne1G reter to tne pro,ecl o:JSt ry oommitted rwestmeot!..

2. Details may not add up to totals dlR to rW"ldlno-

..

Table 2.a.Total Approved Foreign Direct Invesbnenls by Country of InvestorFirst Quarter 2005 to Second Quarter 2006

(In million pesos)

ApproYed FDl Pen:ent1D GrowtII Ram

Country 2005 I 2006 TotalQ2 Q2 2005-Ql I Q2 I Q3 I Q4 I Total I Ql" I Q2 '2006 Q22006

Australia . 466.7 92.2 4.1 563.0 n.6 10.6 0.0 (97.7)

8r. Virgin la. 175.5 60.4 173.2 249.0 658.0 39.7 . 1.0 0.0 /9£.3}

FranCtl . 22.5 0.0 23.0 45.5 . 35.2 0.1 56.6Gennany 166.2 231.5 0.7 19.1 417.5 1.0 90.0 0.2 (6"11

Hong Kong . 2.7 11.3 78.6 92.6 34.9 275.1 0.5 10,001.2Indonesia . . . . . 2.7 84 0.0 ...•• ty 2.7 4.9 . . 7.7 2.7 15.7 0.0 217.4

J8~n 14.203.4 3.065.8 6,234.4 4,035.4 27,538.9 2,862.3 5.651.5 10.7 84.3Korea 9,574.8 172.3 769.0 312.3 10,828.4 51,680.5 423.5 0.8 145.7

MalaysIa 18.0 0.2 14 49.9 69.4 55.3 0.0 0.0 (8~.5'

Netherlands 3,009.6 4,029.8 551.5 11.616.9 19,207.6 258.6 6,135.0 11.6 52.2

PROC 14 49.9 31.0 112.3 194.6 464.6 16,281.6 30.9 32,535.6

Slng.para 26.7 884 151.5 622.9 889.5 1,370.6 2,239.0 4.2 2,433.9

Sweden . . . 0.4 0.4 . . . _.Swttzerland . 0.0 817.2 . 817.2 4.7 520.0 1.0 24,185,946.5

Taiwan 354.5 764.5 33.0 241.5 1,393.5 2294 371.9 0.7 (5~.':

Thailand 1.533.5 - . 1.5 1,535.1 . - . ...UK 11.4 25.2 65.7 92.8 195.1 1.8 2,784.0 5.3 10,946.7

USA 2,175.2 1,759.3 6.302.7 4,675.5 14,912.7 6,380.1 16,615.6 31.5 844.5

Manx . . . . . . . . ...Nauru . . . . . . . . ...Cayman lslands . . . 13.817.2 13,817.2 . . . ,..Oth ••• 252.3 1.002.9 968.6 398.8 2,622.7 63.8 1,229.9 2.3 22.6

•• 1 687 1000 348.5

$oUn::es of BasiC Data Board c1lr\'VeStJ'1'leO{ (801). Ptiipplne Ea:nol'Tllt: ZCne AJ.nDrrry {PEZA}, Sl.IIx Bay MeuoooIrtlln

Autt1Ol'ty (SBMA) and Ct<m. Oeveloprrel1t CorponItlon (CDC).

Figure 2Totallllpproved FDts by c::om1t:ry of

investor. Second Quarter 2006

11

••••

Table 2b.Total Approved Foreign Direct Invesbnents by Country of InvestorFirst Semester 2005 to First Semester 2006 I(in million pesos)

Hong Kong 2.7 89.8 92.6 310.0 0.3 11,283.9Indonesia 110 0.0Italy 7.7 7.7 18 .• 0.0 140.1Japan 17,269.2 10,269.7 27,538.9 8,513.8 7.3 iSC.7,

Korea 9,747.1 1,081,3 10,828.4 52,104.0 44.8 434.6

Ma'aysla 18.1 51.3 69.4 55.3 0,0 205.3

Nether1ands 7,039.2 12,168.4 19,207.6 6,393.5 5.5 (£.2:

PROC 51.3 143.3 194.6 16,746.2 14.4 32,537.1

Singapore 115.0 774.4 889.5 3,609.6 3.1 3,038.1

SwedGn 0.4 0.4 0.0 ISwitzerland 0.0 817,2 817.2 524,7 0.5

24"T~~:~'illtw3n 1,119.0 274.5 1,393.5 601.3 0.5Thailand 1,533.5 1.5 1,535.1 0.0 ...UK 36,6 158.5 195.1 2,785.8 2,4 7,516.4

USA 3,934.5 10,978.2 14,912.7 22,995.6 19.8 484.5

Manx 0.0

Nauru 0,0

Cayman Islands 13,817.2 13,817.2 0.0

Othe •• 1,255.3 1,367.5 2,622.7 1,293.6 1.1 3.1

''''''' 43,252.1 52.554.6 95,806.8 '16,218.0 100.0 168,7

""OI:es:1. AfJproved InvestmefG reterto the proed rostor lX:I"I"tffitt l"loreS1J,e,lS.

2. Details may nol add up to lotaIs cb? to t'ClI..Fdng.

Sources of Basic Data: Board of Investmertts (8011. PIti~oPlI'le EaJnoITlC Zooe AutflOnty (PEZA), Sut*: Bay Metrooolitan

AutI\ol1l'y(S8MA) 8rd Oarit Ol!'Yelopmel1t CorporaJOO {CDq

Approved FDI Percent to GrowlI1 RlIt2

Country 2005 T Total sem,

2006 sem 1 2005-,sem 1 I sem 2 -1 Total f sem 1 12006 sem 12006

Australia 466.7 96.3 563.0 88.2 0.1 ItL1,

Br. Virgin 15. 235.8 422.2 658.0 40.7 0.0 18:.01France 22.5 23.0 45.5 35.2 0.0 56.6Genn_ny 397.7 19.8 417.5 91.0 0.1 :-;-7.1,

12

•• " ".

33,810.232.8

348.5

(8£.2)167.6

254.458,728.3

88.0

Mining 225.3 7.087.6 7,312.9 31.1 0.1Manufacturing 19.759.1 9.258.3 11,226 .• 27.486.5 67,730.• 59.641.5 24.776.5 47.0Elaclriclty 10.863.5 10,863.5 0.0Gas 90.2 90.2 0.0Wate, 0.0Construction 20.1 13.9 33.9 71.1 0.1Trade 0.0 33.2 50.7 23.3 107.3 1.5 19,539.7 37.1Transportation 254 14.4 299.8 51.9 391.4 3.0 27.0 0.1Storage 0.1 0.4 0.5 8.9 0.0Communication 2.669.7 5.1

Finance & Real Estate'" 8.3 8.0 1 1 1.7 75.1 203.1 161.0 2,700.7 5.1Services 848.9 2,154.5 4.410.4 1,369.4 8,783.1 3,723.1 2, 1.9 5.4

T_I 31,505.2 11,746.9 16,203.3 36,351.3 95,806.8 63.530.1 52,687.9 100.0

Table 3a.Total Approved Foreign Direct Investments by IndustryAm Quam, 2005 to Second Qua_ 2006(In million pesos)

Approved FDI I Percent to GrowtI1RateIndustry 2005 I 2006 I r_lQ2 Q2 2005-

01 I 02 I 03 I Q4 I Total , 01~ I 02 200S 022006

Agriculture . 33.2 . 257.2 290.5 . !12 0.0 (9£.3)

a' Includes Eoooonuc Zone [)eveIopmen[ and Ird.JstT181 Park..

W Revrsed tor 01 2006 801 41ure!>.

Nates:,. Approved Irrvestmel1ts reter to ttle pro,ea cost or conwnined ~ts.

2.":::::;=:'""'':':=::~':::::=--.= ===-- ""'",i",ngSources of BasIc Data" 80arel of In\leSlmeMS (BOIl. Philippine Ec:orDJTK ZOne AultDity (P'EZA). Soble Bay Metropolitan AJ1nonty (S8MA)

8M Clark Dewtopment Co!'poratJon (COCI.

Figure 3Total approved FOls by

industry, Second Quarter 2006

T••••37.1%

Others Sefvlce-r.

0.3% (Fnanoe & Reai..••%Comm. Estate5.1% 5.1%

13

•

Table 3b.Total Approved Foreign Direct Investments by IndustryRrst Semester 2005 IDRm Semester 2006(In million pesos)

Approved FDl Percent to GrowthRalI!

Industry 2005 I 2006 Total sem sem 12005-

sem 1 I sem 2 I Total I sem 1 12006 sem 1 2006

Agriculture 33.2 257.2 290.5 1.2 0.0 (96.3i

Mining 225.3 7,087,6 7,312.9 31.1 . 0,0 186.2\

Manufacturing 29,017.4 38,712.9 67,730,4 84,418.0 72.6 190.9

Elec1riclty 10,863,5 . 10.863.5 - 0.0 ...Gas - 90,2 90.2 - 0.0 ...W•••• , - - . - 0.0 ...Construction 20.1 13.9 33.9 71,1 0.1 254.4

Trade 33.2 74.0 107.3 19,541.2 16.8 58,678,3

Transportation 39,8 351,7 391,4 30,1 0.0 (24.l1

Storage - 0.5 0.5 8,9 0.0 ...Communication . - . 2,669.7 2.3 ...Finance & Real Estate ~ 16.3 186,8 203.1 2.861.7 2.5 17,448.2

Services 3,003.3 5,n9.8 8,783.1 6,585,0 5.7 119.3

Total 43.252.1 52,554.6 95806.8 116.218.0 100.0 168.7

a/ Includes Eamomic Zone ~ 8M 1rd.Jstnal Pin..

Nares:,. Aporcwed Investments refer to the pro,ed cosl 01"committed' ~ts_2. The set'Vlces .ndusty includes hcteVrestalnnl: busnesses. CXJI'T"CuteI'" scttware ~ •• heaItn C8~ p1"OQI'8msetVices.

rer«lng and Ieasng of ~er sport equIPment, trall'llflg se'fVKleS. procec:t1clno's tt9lning c:ourse.college edueaton

and other services. ISourt:eSof BasicData: Boardof In~ (BOl). PhiliPQine Eccn:m'IC ZoneAutnaTty (PEZA).SubIC BayMetropolrtan

AulhorIY (SBMAI8lld Clarlt t::)evelopment Corpof8tlOO (CDC).

14

Table4a.Projected Employment on Approved InvesbllentsFIrst au_ 2005 to second au•••••.2006

a _

2005 2006Percent to Growll1Rate

Agency TotalQ2 Q2200S-Ql I Q2 I Q3 I Q4 J Tobtl Ql" Q2 2006 Q2 2006

BOI 6,017 5,161 15,310 19,861 46.349 5,637 11,851 28.2 129.6

PEZA 12,722 20,366 23,525 15,179 71.792 23,039 22,733 54.2 11.6

SBMA 1,892 139 2,333 1,752 6.116 7.731 4,631 11.0 3.231.7

CDC 246 592 2,184 4.764 7.786 1.750 2,762 6,6 366,6

Total 20.877 26.258 43.352 41.556 132.043 38.157 41.977 100,0 59.9

a' Revised for 01 2006 BOI 1QLnS.

N"",,'1. Approved Investments refer to the Pf1Jled c:os1 (ll' commrtted ~ by Fitpino and Ioreign Investors..

2. Details may not edd up to 1WlIs due to f'()l.nkJg.

Sources of BasiC Data: Board of tl1V'e5tmefU (BOIl. PhihpPlne EconomIC Zone ALato1fy (PEZA). Subte Bay Metropolrta

Au!Tk:lrtty (SBMA) and Can:. ~ Corporcmn (COC~

Figure 4Projected employment:Q2 2005 and Q2 2006

50,000

140,000 ,I

30,000I

20,000

10.000

Q22005

o on Total approved investments

[lon Total approved investtnentswith foreign interest I

41,m 38,458

Q22006

15

- .

Table 4b.Projected Employment on Approved Projects with Foreign InterestArst Quarter 2005 to Second Cumer 2006

2005 2006 Percent to Growth RateAgency Tota' Q2 Q2 2005.

Ql I Q2 I Q3 I Q4 I T_' Q1.' I Q2 2006 Q22006

BOI 3.558 2,497 12,208 8.249 26.512 3,286 .. 10.816 27.4 333.2

PEZA 10.976 19.192 20,662 12.190 63,020 20.171 22,462 57.0 17.1

SBMA 1.732 114 2,176 1,394 5,416 7,701 4,410 11.2 3,768.4

CDC 149 577 2,033 2.635 5,394 1.434 1,751 4.4 203.5

Total 16,415 22,380 37,079 24,468 100,342 32,592 39.459 100.0 76.3

al ReVIsed fOf 01 2006 801 ligUfeS.

Notes:

1. Approved In¥eStments remr 10 the ~ rost Of comrrwftDd 1f'lves1ments by FihOtrlo and b91gn InV'9!iiors.

2. Details may rot add up 10lotals due to J'OI.Ildmg.

Sources of BasICData: Board cJ Investm9llts (BOl). Pttihppne EccnorntC lone AultKlnty (PEZA). Subtc Bay Metroool n

Aurtlonty (SBMA) and Ciani. [)awIopme11l CorporatIOn (CDC).

16

._ Jr.lA. _ • .J. -

T_4c.Projec1Ied Employment on Approved Inves_First SeliiE'stef 2005 to First Set.»est&i 2006

2005 2006 Percontto GrowtIl RlrI8

A9"ncy ToDI ,..", 1 ,..", 1 2005-sem 1 I sem2 I TollI' sem 1 2006 sem 12006

BOI 11,178 35,171 46,349 17,488 .21.8 56.5

PEZA 33.088 38,704 71,792 45.772 57.1 38.3

SBMA 2,031 4,085 6,116 12,362 15.4 508.7

CDC 838 6,!l48 7,786 4,512 5.6 438.4

Total 47,135 84,908 132,043 80,134 100.0 70.0

N_ I1. Approved IIlYeStmel'1t5 rete' 10 the Pl"O,ed cost or committed IlWe5tl'T'ents tIy F~rPlno and foreign lIWestoT5.

2. Details may nol a:td up to tttais dUe 10 1'lJU1d1lQ. ISoun::es of Basic Data: Boerd ollrwestmefts (801). PtihPPlne Eoooomic Ztne Authaty (PEZA). $ubic Bay

Metropolrtan Aulhonty (SBMA) and Clal1l Developmen: CorporatiOn (CDC).

.I. !!.!

17

, .•••••• .IL

Table 4d.Projec1ed Employment on AppI oved Projects wilh Foreign InterestFIrst $etnester 2005 to FIrst SeiiNiSbtl 2006

I Agency I 2005 2006 IT~mll=r=1oem 1 I ••••••2 Total •••••• 1

IBOI 6,055 20,457 26.512 14,102 19,6 r2

•9

PEZA 30,168 32,852 63.020 42,653 59.2 4U

SBMA 1.846 3.570 5,416 12,111 16.8 556.1

CDC 726 4,668 5.394 3,185 4.4 338.7

Total 38.795 61.547 100.342 72.051 100.0 85.7

'- I1. AppraYoed Investments refertD the pmfeClcost CJ( romrm:ted 1f'M!'Strrents. by FltlplflO 8fd betgn irwestors.

2. Details may not add up 10 teUts d..Ie to 1'(II.ndng. ISources of Basic Data: Boerd of lth'astI1Wl,iItS (801), Philippine EttlronicZone Ad.horty (PEZA). Subie 8a)I

MetropolltBn Authority (SBMA) and Clat1t Dewtopmerf. Corporation (CDC).

18

• ....Table 50.1Total Approved Investments in the Information and Communication Technology(ICT) Sector by Promotion Agency

"FIrst Quarter 2005 to Second Quarter 2006

(In million pesos)

2005 ,Agency 1at Qu."..r 2nd Quarter T 3rd Q\ul'tllr I 4tt\Quarte"'"

T_ I FUIplno" I F••• 1gn T_ I •••••••" I F",1gn T T_ '_"I F....." T_ I FlII"'no" I F",1gn

BOI 239.7 231.4 8.3 2,047.2 2.036.5 10.7 887.8 209.6 678.2 471.4 249.3 =.2

PEZA 5.789.9 137.0 5,652.9 2.210.1 128.9 2,0812 3,860.5 234.0 3.626.5 6,340.4 742.1 5.598.2

SBMA 0.7 0.7 . 0.3 0.1 0.1 61.0 46.9 14.1 5.5 5.5 .

CDC 26.4 0.4 26.0 32.2 17.5 14.7 . - - 566.4 73.0 493.4

Total% Shareto Total

6.056.7

100 0

369.5

6.1

5.687.2

93.9

4.289.8 2.183.0 2,106.8 4.809.3

100.0 50.9 49.1 100.0

490.5 4,318.8 7,383.7 1.069.8

10.2 89.8 100.0 14.5

6,313.9

85.5

a' Includes 81 comrrmed investmel"lS d Filonos In whoIty lind pamaty owned ~.

l>'R2vised04 2005forTetec::omml~,

N,•• ",. Approved IllYeStments reCefto the pl"ClIed. cost or commttted in-..estments,

2. Details rngy not a:kj up to tot8ls due to roundlOQ

Sources 01 BasiC Da!8: Board of Il'M'!StI'TlE!flts (B()(~ PI'1i'ppne ~ Zore Al1honty (PEZA)., Slbc Bay MetropoIrtarl Althor'ly (SBMA).

and the Oao:.l:leve!oPment ~ (COC).

2006 Growtn Ratf

Agency 1at Quartsr I 2nd Quarter 0:: 2004.Q2 200::.

'_1 I F111"lno" I Fcnrlgn I lot.1 I Flllplno-' I F",1gn T_' I Filipino ""'on

B01 156.7 156.1 0.6 102.9 37.0 65.9 .~\:~ . ~~2 :. 514.0

PEZA 2,411.3 IK2 2,327.1 2,015.4 137.0 1.878.4 6.3

SBMA 89.5 0.4 89.0 3-45.5 329.6 15.9 125.545.1 239_" 11.485.7

CDC 895.5 52.7 842.8 828.4 100.5 727.9 2,475.7 475.8 4.850.3

Total 3,555.0 295.5 3.259.5 3,292.2 604.1 2.688.1 , 27.6'-" .% Shareto Total 100.0 8.3 91.7 100.0 18.4 81.6

Fig,," 5Percent snare of ICT MCIOr In the total appn:Hed FDtI. by

promotlon apency, SeeoncI Qual1lltr ~

"' ..".••..,./J

OCT3.2%

PEZA2.0%

SBMA0.3%

CDC0.8".4

19

• JIi:. __ 1..Jr::l~ ••1l..:'t'd _II.

Tobie 50..2.

Total Approved Investments in the Information and Communication Technology(ICT) Sector by Promotion AgencyFim Semester 2005 to FI<st Semester 2006(In million pesos)

2005 2006 II Growth Rat!?

Agency SAm 1 I SAm 211' ••m' II sem'! 2005.sem2 200f

Tota' J Flllpinoa! I Foreign I Tota' Filipino. I Foreign Tota' T Fillplno" I Foreign I I Tota' I FI"pino I Forelgn

BOI 2,286.9 2.267.9 19.0 1,359.2 458.9 9004 261.6 195.1 66J ,fiE. 6 .S'~.: 249.4I

PEZA 8,000.0 265.9 7.734.1 10,200.9 976.1 9.224.8 4,426.8 221.2 4.205'1 ,-- ,1';: E I':: 6

SBMA 1.0 0.9 0.1 66.5 52.3 14.1 435.0 330.0 105.0 42.650.4 37,403.0 76,233.8

CDC 58.6 17.9 40.7 566.4 73.0 493.4 1,723.9 1532 1,570. 2.842.4 757.1 3,758.3I

Total 10,346.5 2,552.5 7,794.0 12,193.0 1,560.3 10,632.7 6,847.2 899.6 5,947.6 I';'';' ::. 10:'':.£ "'. -% Share to ITotal 100.0 24.7 75.3 100.0 12.8 87.2 100.0 13.1 86.9

Ii InduOes aR oommitled ilN'eStmeIXS of Filrpnos In wt10Ity aoo partial)' owned c::omparI'8S.

bI Revised 04 2005 tor Teleoomm 1fNeStmet1tS

No",,,1. Approved Investments re4erto the ~Cl cost cy rornrrmed nvestrnents.

2. OeIails may ncr. add 1lOto tota5 due to I'Oln::l!ng

SooItleS of Basic Data. Board of Investmems (SOl). Phi.ppne Econo~ Zone AlI1'Onty (PEZA). Subtc Bay MetrooolItBT'l AlJolorty (SBMAl.

and trle Ciano:. DevelQprT'er4 Corpcrabon (COC~

20

.1

. 2005 i

Subsector 1st Qu.l'tar I 2nd QuIIrter I 3rd Quart8r I, 4th Quarter

T•••• T FUlplno" I Foretgn-l T•••• I F1Ilptno.' •••••••• I T•••• m_. I •••••••• II Tota' I Filipino" I Foreign

Table 51>.1.Total Approved Investments in the Information and Communication Technology

(ICl) Sector by sub sectorFirst Quarter 2005 to Second Quart8f 2006

(In million pesos)

M.nur.cturtng 5,152.9 121.9 5.031.0 17.2 17.1 0.1 5,871.1 645.6 5.225.4

Trade

Telecomm•b1 2,019.5 2.019.5

60.0 60.0

IT Services 903.8 247.6 6562 2,253.1 146.4 2.106.7 4,809.3 490.5 4.318.8 1,452.6 364.2 1.088.4

Total 6.056.7 369.5 5.687.2 4,289.8 2.183.0 2,106.8 4,809.3 490.5 4.318.8 7.383.7 1,069.8 6,313.9

.". Share toTotal 100.0 6.1 93.9 100.0 50.9 49.1 100.0 10.2 89.8 100.0 14.5 85.5

at 1nc\ldeS 8ft cornmrtted investmentS 01 FillplOOS 10wtdty and parnally 0fI'T1E!d~.

tY Revtsed 04 2005 tor TeiecOmm investrnerts.

Nates:

1. ApproYed Investmeft'..s reterto the project cost or committed investment!.,

2. [)etaits may net. add up to totals due to rounding_

Soun::esof BasK:Data: Board ollnvestmems (SOl). Ptnppne Econo~ ZMI'! A1DlO1ity(PEZA)..Stbc Bay MetropOIrtlltl AlihOnty (SBMA)'

and the Dark [)ewIkIpmef'l: eorporatJon (ctX:).

I..ManufactUrtng 782.0 48.8 733.3 308.5 90.3 218.2 1.694.3 429.5 158.592.6

Trade3.0 3.0 1

Teleeomm.327.8 327.6 s: :: rf,2,.t.

IT services 2,773.0 246.7 2.526.3 2,653.1 186.2 2,466.9 17.8 27.2 17.

Total 3.555.0 295.5 3,259.5 3,292.2 604.1 2.688.1 -:: 27.8

-;. Share to ITotal 100.0 8.3 91.7 100.0 18.4 81.6

2006Gro .•••'tn Rau

Subseetor 1st Quarter I 2nd Quar1Qr a: 200"'.02 2005

Tota' I FIIlp4no" I F_9'l I T•••• I F,"pino.' I FOR9l T•••• I FiUplno 1 Foreign

""'~'Percent share of ICT s.ectDr In the total approved ft)ts byindustry. Second QuM'I'" 2006

Tnod.0.003%

/bl""-~ 26%

tel Mtg3.2% 0.3%

\Telecomm.0.3%

21

T_5b.2.Total Approved Investments in the Information and Communication Technology(ICT) Sector by sub sectorFirst Semester 2005 '" First _ 2006(in minion pesos)

80.7

IM.nuflleturtng 5,170.1 139.0 5.031.1 5,871.1 645.6 5.225.4 1,090.5 139.1 951.5 -~~ 0.1

ITrade

3.0 3.0

Telecomm.b! 2,019.5 2.019.5 60.0 60.0 327.6 327.6 - I IS::; E ;~:: f.

IT services 3,156.9 394.0 2.762.9 6,262.0 854.7 5,407.3 5,426.1 433.0 4.993. 71.9 9.9

Total 10,346.5 2,552.5 7,794.0 12,193.0 1,560.3 10,632.7 6,847.2 899.6 5.947.6 ::'::. ~ f~'::~

% Share to 86!9Total 100.0 24.7 75.3 100.0 12.8 87.2 100.0 13.1

2005 2006 , Growth Rau-

Subsector •• m 1 I sem 2 •• m 1 I sem1 2005-sem2 200f.

T_' I FIIlDtno.' I FClf'8lgn Toml I Flllolno.' I F"'1gn To1>' t FlIIDlno" I Forelgnl T"" I Filipino Foreign

aJ Includes 8~ commmed Irwestme!W:S of Fil.,nos in wtnlly aOO partJaty owned c;:oroane!>.

bI ReviSed 04 2005 tor TeIoc:Omm i~ .

.••...,1. App«roIed Il"\'Y'eStI'T'Iemsreler to the pro,ect oost or committed investments.

2. Details may no: add up to totals. due to rounding.

Sourcesof BasicData: Boardof Investmel'lts(801).Phi~ppne Eco'lo~Zone ~my (PEZA),SltJIc Bay~ ALIhorty (SBMA).

and the ~ ~nl: (;orpaabon (CDC).

22

I ._.

T_6a.Tolal Approved Invesbnents by Promotion AgencyAm Quar18r 2005 to Second Quat1sl"2006(In million pesos)

Approved Investmenls Percent to Growlt1RateAgency 2005 2006 TotolQ2 Q2 2005-

Ql Q2 I Q3 I Q4 I Toto' Qf. Q2 2006 Q22OO6

BOI 52,604.8 52,278.7 8,357.8 50,839.4 f63,878.7 5,600.~ 68,737.1 67.7 31.5

PEZA 13,006.6 7,824.5 14,809.1 27,121.0 62,761.2 14,519.2 11,397.3 11.2 45.7

SBMA 436.3 3.1 592.7 452.3 1,_.4 51,711.6 17.799.7 17.5 572,766.0

CDC 57.4 210,1 167.2 2,675.5 3,11D.1 1,243.0 3,603.4 3.5 1,615.4

Total 66 f05.1 60 314.4 23926.7 8ll888.3 231 34.5 73 074.4 101,537.5 100.0 68.3

a' RevtSedfor Q1 2006 801 figures.

Notes:1. ApprovedInvestmentsrder to tneprDfedCDS!orcomrmted~ts tJyF~lprnoam begn Irwestors..

2. Details.may not add up to ~81$ due 10tcU'ldlr'lg-

Soun::es of BasIC Data: Board of 1rwestrnef'lS (BOI). ~llpprne Ec:oI'lCWT'llCZone ~ (PEZA). SubIc Bay Metropolrtarl

Authonly (SBMA) and Clatt. DeYeloornent CorpOlilbOn (COC}.

••••••• 7Total iIIpptV'+'ed i,.w6Atl ••elib ~.wi Filipino):

Q2 2005 and Q2 2006

101.5105.0

90.0

• 75.00••0- 60.0c~ 45.0:is.S 30.0

15.0

-!i 60.3

1i,Ji

Q2 2005 Q2 2006

23

I

..s!!I!B. _ .•..••. .•.

Table 61>.Total Approved Investments by Promotion AgencyAm Semester 2005 10Am Semester 2006(In million pesos)

Approved Investments Pon:ent 10 Growth R••••Agency 2005 I 2006 Totalsem sem12OOSo

semI I sem2 I TobIl I sem 1 12006 S8m 1 2006

BOI 104,881,5 58,997.2 163.878.7 74,337,7 42.6.. :2~,1)

PEZA 20,831,1 41,930.1 62.761.2 25,916.5 14.8 24.4I

SBMA 439.4 1,045.0 1.484.4 69,511,3 39,8 15.718.8I

CDC 267.4 2,842,6 3.110.1 4,846.4 2.8 1.712.2I

Total 126,419.5 104,815.0 231,234.5 174.612.0 100.0 38.1

NOles:

1. Approved Investments refer to the l)\"01eCt cost ~ rommmad '"vestments by Filipol'lCl and toreipn inVestors.

2. Details. may Mt add up to totals due to ran:lng

Sourcesof BasicData: Boatdof I~ (BOt).PtjhppmeEmncrnic Zone~ (PEZA). SUDtcBayMetropolitan

Aul:horlty (SBMA) 8rd ClaTt. DeveIoPl'T'ent CorponltlOn (CDC).

.1. .II. ••.

24

.1. •.

Tab4e 7a.

Total Approved Investments by Nationality (Filipino and Foreign) and by Promotion AgencyArst Quarter 2005 to Second Quarter 2006 I

-(In minion pesos)

BOI 52.604.8 33.489.7 19.115.1 52,276.7 46.483.7 5.793.0 8.357.8 2.293.3 I 50,639.4 37.815.16Jl64,5 12.824.3

PEZA 13,006.6 1.015.4 11.991.2 7,82(,5 1.967.4 5.857.1 14,809.1 5.091.2 9.717.8 27,121.0 4,844.9 22.276.1

SBMA 436.3 69.0 367.3 3.1 1.6 1.5 592.7 226.5 366" 4S2.3 348.6 103.7

CDC 57.4 25.8 31.6 210.1 114.7 95.4 167.2 112.4 54,8 2.675.5 1.528.3 1.147.2

Total 66,105.1 34,599.9 31,505.2 6O,3H ..4 48,567.5 11,7Ui.9 23.926.7 7,n3." 16,203.3 80,888.3 ".537.0 36.351.3

% Shareto Total 100.0 52.3 47.7 100.0 80.5 19.5 100.0 32.3 67.7 100,0 55.1 44.9

aI Indudes all (rImmrtted ~~ d mpnos. 11\wtolly and pert.l3lly (JIIIItI-:I COT08r-s.

IIIR:II'Med!'o'"012006 SOl figu~.N,,..,,1. Approved lmoestments refer to 1tIe prtIIeCl. oost Of committed rnvestmen1S.

2. Details may rot add UP to tcxBlS ClLe to round.,g.

2005 !

Agency 1st Quane, 1 2nd Qlgrwr 1 3rd Quan.r I 4th Quarter

Tota' I Fdipino- _I T_ I _"I - I T_ . J _. 1 •••••••• T_ J Fflipfr-.)- I -"

SoufCeS d Base Data" Board d I~ (BOf). Ph'pp:oe Ec:onomc lJ:rrt:Aul/'Iot.y lPEZAl. SOOoc Bay MemXXlhlal'1 Autnonty {SBMA~

and tne Dan. [)eo.oelooml!l!Tl CorpcJr;IfDn (CDCi.

2006 Growth Rate IAgency 1st Quarter~ I 2nd Quarter Q2 2005-Q2 2006

T"",' I Ffliotno. I ~'9n I Toorl 1 FJliplno" I Foreign Tatlll I Filipino I F0r8ign

IB01 5.600.6 3.187.2 2,413.5 68,737.1 44.703.5 2~.O33.6 31.5 •.~ 2 314~9

PEZA 14.519.2 5.689.5 8.829.7 11.397.3 2.821.3 8.575.9 45.7 43.4 4J.

16.718.0 66.293.2I

SBMA 51,711.6 325.8 51.385.8 17.799.7 1.081.7 Sn.766.0 1.131.11,.2

-CDC 1,243.0 341.8 901.2 3,603.04 243.1 3.360.3 1.615.4 111.9 3,423.6

Total 73.074.4 9,S44.3 63,530.1 101,537.5 48,849.7 52,687.9 68.3 0.6 348.5

% Share Ito Total 100.0 13.1 86.9 100.0 48.1 51.9

Figure 8Percent share of total approved Investments,

foreign and Filipino nationaisa2 2005 and Q2 2006

Q~ 200~ a: 2001.

25

'" J. i I _ I .

Table 7b.Total Approved Investments by Nationality (Filipino and Foreign) and by Promotion AgencyFirst Semester 2005 to F1Bt Semester 2006 I(In million pesos)

2005 2006 •Agency 1stSemnt~r 2nd_ , at s.mestar •

Total I Rllplno" Fonolgn r_ I ••• ,.,.," I Fonoign r_ I flftplno" I FCW'IlIgn

BOI 104,881.5 79,973.4 24,908.1 58.997.2 40.1084 18,888.8 74.337.7 .. 47,890.7 26,447.0

PEZA 20.831.1 2,982.9 17,848.3 41,930.1 9.936.1 31,993.9 25,916.5 8,510.9 17,405.6

SBMA 439.4 70.6 368.8 1,045.0 575.2 469.8 69,511.3 1.407.5 68.103.8

CDC 267.4 140.4 127.0 2,842.6 1.640.7 1,202.0 4,846.4 584.9 4.261.5

Total 126.419.5 83.167.3 43,252.1 104.815.0 52,260.4 52.554.6 174,612.0 58.394.0 116,218.0% Share Ito Total 100.0 65.8 34.2 100.0 49.9 50.1 100.0 33.4 66.6

a! InclLrles 81 oomrnrtted trl'Wl5trTlercs d FiIIPRJS in wtdly and pa'1Jaolly owned~.

Notes:

1. Approved Investments relerto the pl"OJed cost O~committed Investments.

2. Details may not IIdd up to totals dlJe to roundll"lQ

Sources 01BasIC Data: Board of Investments (BOI). Phitppne EealomIC Zone At.tt'Ionty (PEZA). SlDc sa.,. Metropolitan Al.fOOrty (S8MA).

and the Clan; QreveIopmenl CorportItlOn (CDC).

Growth R_ Q2 2005-02 2006Agency

Total I Atip;no I Fomgn

BOI ,2£. ~} 14(;.1 J 6.2

PEZA 24.4 185.3 " ,'_ ..'SBMA 15,718.8 1,893.7 18,365.2

CDC 1,712.2 316.5 3,255.9

Total 38.1 :2S.~ 168.7

26

.J.

Tobie 8lLTotal Approved Invesbnents (Filipino and Foreign) by IndustryArst Quarter 2005 to Second Quarter 2006(In million pesos)

/95.2118£.4',(49.51

1,830.3520.721.668.3

118.931,348.7

909.1

Approved Investments I Pen:ent1O GrowlI1 Ralo

Industry 2005 T 2006 I T_IQ2 02 2005-al I 02 I a3 I Q4 I Total I al'" I 021 2006 Q2 2006

IAgricutture 10.8 83.1 676.6 nO.5 55.5 ~.O 0.0Mining 573.2 29.1 7.691.5 8,293.8 71.8 0.1Manufacturing 46.157.1 53.236.7 12.415.8 38.351.0 150,160.6 61.967.8 26.882.8 26.5Eleclricl1y 17,473.5 4.185.8 21,659.4 0.0Ga. 90.2 178.4 268.6 0.0Walor 0.0Constl'\.lction 52.2 31.2 83.3 10.0 11 ,2 0.1Trade 117.8 82.9 103.3 53.1 357.0 16.5 26.084.3 25.7Transportation 531.0 16.8 393.7 21.230.7 22,172.2 100.8 169.5 0.2Storage 24.8 0.5 0.9 26.2 25.7 0.0Communication 2.019.5 60.0 2.079.5 38.982.1 38.4Finance & Real Estate •• 3n.8 811.5 4.334.3 4,495.9 10,019.5 5,426.6 5.036.7 5.0Services 1.412.5 3.438.5 6.528.6 3.964.3 15,343.9 5.497.3 4.180.3 4.1

Total 66.105.1 60,314.4 23,926.7 80,888.3 231,234.5 73.074.4 101,537.5 100.0

a' Includes Eamomc Zone ()eveiopr'oer( and Industrial Pa1l.

bI Re'Med for 01 2006BOI f9tre.

"""""1. Approved Investments refer to the PlO,eC cost Of committlld moestments..2 The seTVICe5industry indlrles ~lirestaLr.lnl busnesses. CQn'l)Ulef ~ oe- e coc,..,.,"(.1'l6aIm care program services. renting ar'd leasIng

of waler sport equipmer1l.. tranng ser'V'OI5. ~ trw1mg course. ooIlege educ8bon ard omer seMoeS.

Sources of BasICData" Boord of Irt....,;4iie.!s (801). PttIrppine Ec:onomcZOoe Authaity (PEZA). SubK:Bay Metropoh!MAlAhonty {SFWA;

snd Clan. Oe'o"e'kJpiiEi. Ccwpor8OOn (CDC).

Figure 9Total approved investments (foreign &

Filipino), Second Quorter 2006

Tradll26••••

27

"

...

Table 8b.Total Approved Invesbnenls (Filipino and Foreign) by IndustryFirst Semester 2005 to Antt Semester 2006(In million pesos)

.I.. • .!..!!I!II!l.L • ..!I!l

Approved Investments Pen:ent to Growltl RateIndustry 2005 2006 Totalsem r12005-

sem1 I sem 2 1 Total ,- S8m 1 12006 ,sem 1 2006

Agriculture 93.9 676.6 770.5 59.5 0.0Mining 573.2 7,720.7 8,293.8 77.8., 0.0Manufacturing 99,393.8 50,766.8 150.160.6 88.830.6 50.9EIeclricIly 17.473.5 4,185.8 21,659.4 0.0Gas 268.6 268.6 0.0Wate, 0.0Construction 52.2 31.2 83.3 124.2 0.1Trade 200.6 156.4 357.0 26.100.8 14.9Transportation 547.8 21,624' 22.172.2 270.4 0.2Storage 24.8 1.4 26.2 25.7 0.0Communication 2.019.5 60.0 2,079.5 38,982.1 22.3Fln.nee & Real Estate ., 1,189.3 8.830.2 10,019.5 10.463.3 6.0Services 4.851.0 10.492.9 15,343.9 9,677.5 5.5

Total 126.419.5 104.815.0 231,234.5 174.612.0 100.0

a' Indudes Economic: Zone Oevel(lptl'lel'll and lndustrl8l Pan..

;3£-.6'(8£.4\

I1C.6l

138.012,913.7

(50.6]4.0

1,830.3779.899.5

38.1

Notes:

1. Appruved Investments reter to the pro,eo: C051or corrrnitIed IWeSlmeots..2. The ser'tIICeS industry Includes hoteVrestBlnnt bUsnes~ CXlfT'(Uj[ef software ~ neatttI care program selVices. renting end,

Ieaslng of wale!' s;xxt eqUlprrent [J'Bl•..•ng ~ prtlle<%ctVsectrlY 1r.lInng c:o.nE!, college education and other SoeMCe$.

Sources of Basic Data. Board d Irr.oestJTeOts (BOt), PhiipPlfle EeonomK: zone ~ (PEZA). SUbIc Bay MetJ"opoirtan Almont)'

(SBMA)andCtar1tDe~ Corporabon (CDC;

28

Non-Residents' Investments In the Phlh;. 21,243,1 4.265.3 16.192.1 20.689.7

Equlry CIIpttal (net) 21,078.0 9.678.7 20,898 4 5.295.1

ReJnvestfK1 E8mJngs />I 935.6 ::2t • COE:: .('~::

Other cap'~1, ~ : ~ f:E:: ~ ::H,:'" f, 15.503.8

T.b" SalBalanc:eofP~nts FoN6gnDk.ct Ii•••• be.nta

lll

Arwt Quarmr 2DD5 to Ant Qu8rt:M 2006(In million Pesos)

Q'

81 [)IItB In!: u;dl1Bd: 9 N.IjjIVS! 200E

til t::lB18IllduOMre~ etrnogn&ttlm bents~'

Q2

2005

Q3

• I ••

2006 Pel"08nt to I GrowthTotal Q1 ••••• Q'

T_ Q' , 2006 2005-

62,390.1I22.305.3 100.0 50

56.950.2 9,544. 42.8 :....: -~51c::::; ,.141'1 5. , 22.0

5.950.2 11.619., 52.1 1.608.1

No<M1, EJx;flllnge rwMused wus ~ on thIl-ave ~ end....-,g nn k:r lne Q'IlWter DIMtiS rT&f nollldd U()to tl:Jtl'I*5~ torouKlong

2, Coflc:eptS.nd CIMI"1l(I'8corrtorm ge~ ~ tne •••••••'.'o&OOlIIDflof tne BPM5 ""l1ld1_1IdOl*Kl bytfl6 BSP nwtll'llil wen trte 1999 C111'le.

Figurw 10: Baanc:e d~ FDt: First q1art:er 2005 and 2OO4i

25.0

20.0

• 15.0i. 10.0~• 5.0,I

(5.0) J

22.3

Eepty Caonal (net)

[J Q' 2005

II Q' 2006

0.9 1.1

11.6

(0.8)

Other Capital

29

•

ents .,

2OIl5 2llO6 I Percent G",_ Rateto Total QI200>

Ql I Q2 I Q3 Q4 I T••••• Ql I Q12OO6 Q12OO6

T.bIo9bIllllmce of Payments FOf1lignDIrect Inws1mAm Quarter 200510 Am Quane< 2006(In million USS)

Non-Residents'lnvestments in the PhUs. 386.0 78.0 289.0 379.0 1.132.0 430.01 100.0

EquHy Capital (net) 383.0 1n.O 373.0 97.0 1.030.0 184.0 42.8

Reinvested Earnings IV 17.0 It- ::: "iE_ J i:::;:" (f.e 22.0 5.1

Other Capital I;~~. . ..,'.: " 284.0 111.0 224.0

1

52.1

11.4

29.4

1,700.0

aJ Date last upd8'led: 9 August 2006

bI Data includeS ltIimlll'Sted eamlgns from bank.s only.

Notes:1. Exchange nrte used was based on the BYel'llge buying and $eI'ng 1<l'Il!for the qulJI'lI!l'. Detaib may 001 cld UDto totals due to ling.

2. Concepts and ~ c:onfofmge:neotly to the rec:ommeodaton dtr.e BPM5 WhodT was adopted by the asp 5l:IIrmg...nn tne 1999 data.

5oun::es of BasIC Data: ~partment of Economc Rese<'Iteh COERl. Bangko Sentr.al ng PillptrUJS (SSP)..

30

A ••. '

T.bIe 10.RegIstenKI Foreign. Direct In,esb._ (SEC""" BTRCP) by CounlJy of Inves10r2002(In million pesos)

I Natlon.11Iy IAustraliaBelgiumBennudaBr Virgin IsCanadaFranceGennanyHKIndiaIndonesiaJapanKoreaMalaysiaNetherlandsPROCSingaporeSwTtzerlandTaiwanThailandUKUSAOthers

Total

HI

44.1

23.2150.7

1.278.8143.768.2

5.5133.410.538.5

54.7106.5386.9

2,«4.8

2002

H2

10.4

15.8

2.1

47.2143.4

2.3

19.4

72.426.565.2

405.0

Total

54.5

15.8

25.3150.7

1.326.0287.068.3

5.6135.710.657.9

127.1133.0452.2

2,849.8

aI Data tor 2OQ2are stil pr1!lmnary. ~ ~ tor 2003 to Q2 2006 alt! rD )"fl'tewiIable.

Note:

1. SEC data lI'ldudes new and addrtKmalllWes1J,lEilts In domestJc stadt c:orpolaoons and partnerships, by natlon81ily 01 investor2. Details may not add up to totals due to roundng. ISources of Basic Data: Sec:u'tJes arK! Exch9roe ComrnsSlOn lSEC~and BlIeeud Trade ~.., Catsumer P!UecllOn (BTRCP)

31

•

Table 11.Reg_red Fof1lIgn DinM:tInW>Sb._ (SEC and BlRCP) by Country a/ _. by Type at Investment

:;'/Ilion pes•••) I2002 ,

Country Hl I H2 , AnnualNew I AddllIonal I Total I New I Additional I Tolal New I Additional I Total

Australia 44.1 44.1 10.4 10.4 54.5 54.5BelgiumBermuda

ISr Virgin IsCanada 15.8 15.8 15.8 15.8FranceGennany 23.2 23.2 2.1 2.1 25.3 25.3HK 150.7 150.7 150.7 150.7IndiaIndonesiaJapan 1.278.8 1,278.8 47.2 47.2 1.326.0 1.326.0Korea 143.7 143.7 143.4 143.4 287.0 287.0Malaysia 68.2 68.2 68.3 68.3NethertandsPROC 5.5 5.5 5.6 5.6Singapore 133.4 133.4 2.3 2.3 135.7 135.7Switzerland 10.5 10.5 10.6 10.6Taiwan 38.5 38.5 19.4 19.4 57.9 57.9ThailandUK 54.7 54.7 72.4 72.4 127.1 127.1USA 106.5 106.5 26.5 26.5 133.0 133.0Others 386.9 386.9 65.2 65.2 452.2 452.2

Total 2.444.8 2.444.8 405.0 405.0 2.849.8 2.849.8

a! Oat. "" 2002.", ~iI pmImnwy. __ "" 200310 Q2 2006 ••• ""',... -- INote:

1. SEC data ndudes AeWarn:l.tdltJonBl trM!!StmerCs m ~sto<::ll. corporations and pitftrerstllps, Clynaoonatry of Il"NeStO"~. Details may not aQ:l uo to totals due to I'l:llXdng ISources of Basic Da18: ~ and Exchange CoITW'mSlOFl (SEC) and Ek¥eau a Trade ~ and CcnsuTer Ptoced:Dn (BTRcP)

32

Table 12a.Registered Foreign Direct Investments of SSP FDJArms by Country of InvestorFirst Quarter 2005 to First Quarter 2D06(In miUJon pesos)

.I. . .I.A .• ,lA •• A

200. 2006 Percent to Growth RateCountry Total Q2 Q2 :!ODS-

Q11 Q2 I Q3 Cl4 I T_ Q1 I Q2 2Oll6 Q2 2006