Focus Your Thinking

144

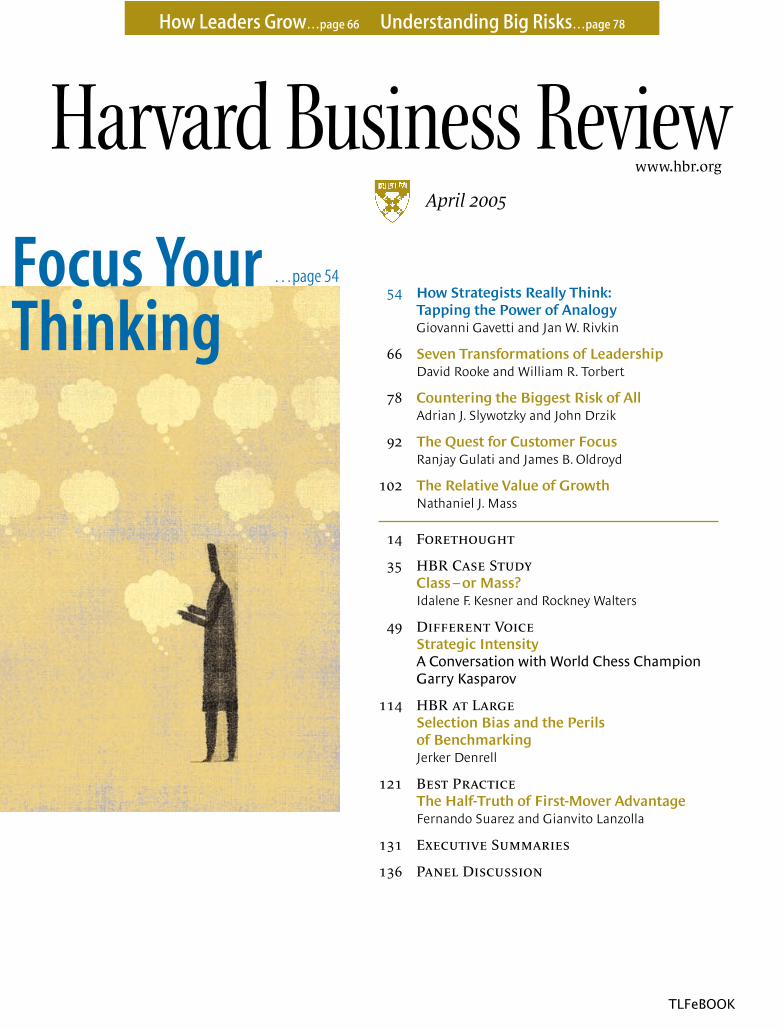

How Leaders Grow…page 66 Understanding Big Risks…page 78 54 How Strategists Really Think: Tapping the Power of Analogy Giovanni Gavetti and Jan W. Rivkin 66 Seven Transformations of Leadership David Rooke and William R. Torbert 78 Countering the Biggest Risk of All Adrian J. Slywotzky and John Drzik 92 The Quest for Customer Focus Ranjay Gulati and James B. Oldroyd 102 The Relative Value of Growth Nathaniel J. Mass 14 Forethought 35 HBR Case Study Class – or Mass? Idalene F. Kesner and Rockney Walters 49 Different Voice Strategic Intensity A Conversation with World Chess Champion Garry Kasparov 114 HBR at Large Selection Bias and the Perils of Benchmarking Jerker Denrell 121 Best Practice The Half-Truth of First-Mover Advantage Fernando Suarez and Gianvito Lanzolla 131 Executive Summaries 136 Panel Discussion Focus Your Thinking April 2005 www.hbr.org …page 54 TLFeBOOK

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Focus Your Thinking

How Leaders Grow…page 66 Understanding Big Risks…page 78

54 How Strategists Really Think:Tapping the Power of AnalogyGiovanni Gavetti and Jan W. Rivkin

66 Seven Transformations of LeadershipDavid Rooke and William R. Torbert

78 Countering the Biggest Risk of AllAdrian J. Slywotzky and John Drzik

92 The Quest for Customer FocusRanjay Gulati and James B. Oldroyd

102 The Relative Value of GrowthNathaniel J. Mass

14 Forethought

35 HBR Case StudyClass – or Mass?Idalene F. Kesner and Rockney Walters

49 Different Voice Strategic Intensity A Conversation with World Chess ChampionGarry Kasparov

114 HBR at LargeSelection Bias and the Perils of Benchmarking Jerker Denrell

121 Best Practice The Half-Truth of First-Mover Advantage Fernando Suarez and Gianvito Lanzolla

131 Executive Summaries

136 Panel Discussion

Focus YourThinking

April 2005

www.hbr.org

…page 54

TLFeBOOK

TLFeBOOK

N E W YO R K L O N D O N PA R I S M I L A N TO K YO C H I C AG O T R OY DA L L A S B E V E R LY H I L L S PA L M B E AC H B O S TO N

TLFeBOOK

TLFeBOOK

TLFeBOOK

6 harvard business review

CO

VE

R A

RT:

JIM

FRA

ZIE

R

F e a t u r e s

92 The Quest for Customer FocusRanjay Gulati and James B. Oldroyd

What do customers really want? What does your com-pany really need to know about them? You won’t find out simply by conducting a survey or installing a CRMsystem. The road to enlightenment is much longer andharder than that – but those who go the distance have the profits to show for it.

102 The Relative Value of GrowthNathaniel J. Mass

You might be surprised at how much more valuable itcan be to grow than to cut costs. Now you can determinewhich of your corporate strategies are working to delivervalue and whether you are pulling the most powerfullevers for value creation.

continued on page 8

66

54 How Strategists Really Think:Tapping the Power of AnalogyGiovanni Gavetti and Jan W. Rivkin

The exhilarating feeling of “I’ve seen this situation before!” leads sometimes to strategic breakthroughs,sometimes to disaster. Here’s how to make sure your analogical reasoning is on the money.

66 Seven Transformations of LeadershipDavid Rooke and William R. Torbert

Few leaders try to understand their leadership styles.They should, because those who undertake a voyage of personal understanding and development can trans-form not only their own capabilities but those of theircompanies.

78 Countering the Biggest Risk of AllAdrian J. Slywotzky and John Drzik

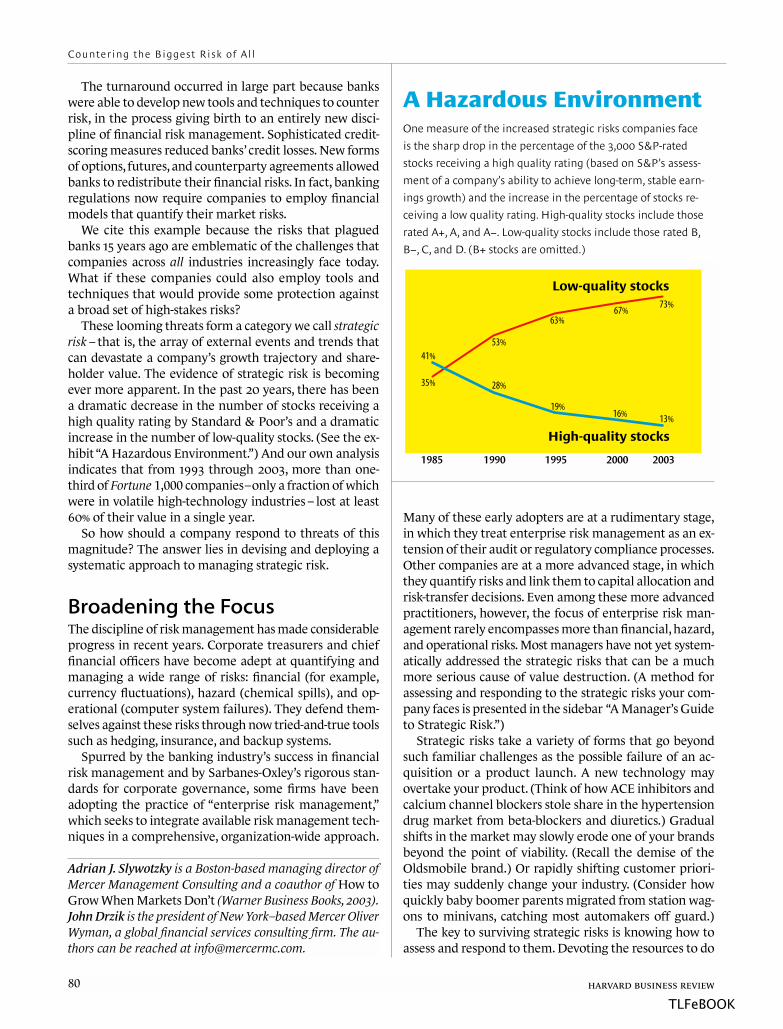

You can hedge, but you can’t hide from “strategicrisks”– the events and trends that can devastate yourcompany’s growth trajectory and shareholder value.Learn to anticipate and manage these threats system-atically. (You may even be able to turn some of them into growth opportunities.)

HBRApril 2005

54

78

92

102

TLFeBOOK

©2005 Merrill Lynch & Co., Inc.

Merrill Lynch provides fi nancial advice and

strategic insight to position both issuers and

investors for success in achieving their objectives.

Our integrated teams working across multiple

disciplines bring the full strength of our resources

together on behalf of our clients. We leverage

rigorous analysis, knowledge of the markets and

structuring expertise to help our clients identify

opportunities and realize their goals. This is how

Merrill Lynch develops and delivers exceptional

fi nancial solutions for exceptional clients.

UPHOLD YOUR GROWTH

PROJECTIONS.

UPHOLD YOUR BOND OBLIGATIONS. UPHOLD YOUR SHARE VALUE.

JUST DON’T UPHOLD THE STATUS QUO.

TLFeBOOK

8 harvard business review

10 F R O M T H E E D I T O R

When Businesspeople Think As several articles in this issue makeclear, understanding how managers’minds churn is often more importantthan knowing what they’re thinking.

14 F O R E T H O U G H T

Professional service firms may no longerbe the best role models for corpora-tions…HR? A launching pad?…A sys-tem for scripting successful TV ads…Think twice before trimming HQ staff…Knowledge work is (basically) here tostay…Consumers do know the differencebetween “tall” and “medium”…The “bro-ken windows” crime-prevention theoryapplies to business as well…Earnings inmiddle-wage countries are stagnating…What your logo font says about you…HR needs to segment talent strategi-cally…Avoid an overload of meetings…The coming of femtosecond lasers.

31 2 0 0 4 M C K I N S E Y AWA R D S

35 H B R C A S E ST U D Y

Class – or Mass? Idalene F. Kesner and Rockney Walters

Neptune Gourmet Seafood has a vastamount of excess inventory. If the com-pany slashes prices or creates a low-priced brand to get rid of the surplus, itcould trigger a price war, cannibalizesales of its other products, and destroyits premium image.

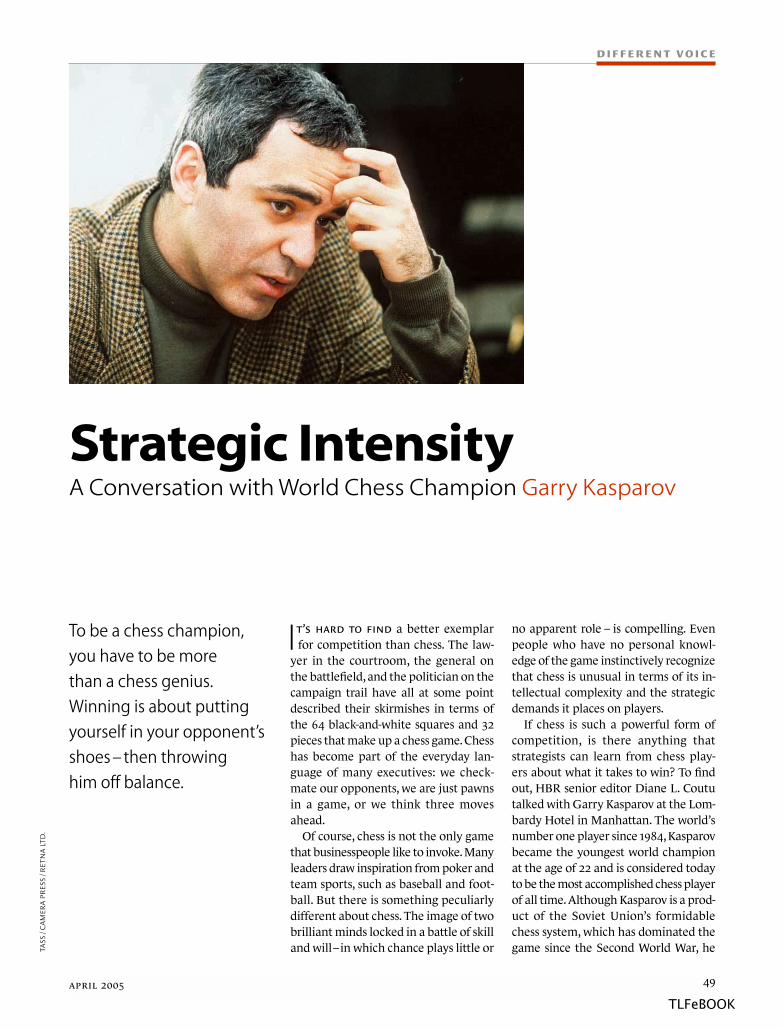

49 D I F F E R E N T V O I C E

Strategic Intensity:A Conversation with World ChessChampion Garry Kasparov

The greatest challenge for highly suc-cessful people is to stay passionateabout being at the top, says the world’snumber one chess player. The secret tolasting triumph? You must be lucky inyour enemies.

D e pa r t m e n t s

10

April 2005

90 ST R AT E G I C H U M O R

114 H B R AT L A R G E

Selection Bias and the Perils of Benchmarking Jerker Denrell

Looking to successful companies forbest practices may seem like a no-brainer, but it’s an approach that’sdoomed to failure.

121 B E ST P R A C T I C E

The Half-Truth of First-MoverAdvantage Fernando Suarez and Gianvito Lanzolla

Sometimes the first company to moveinto a new product category is simplythe first to get clobbered. To improve theodds of success, a first mover needs toanalyze the technological and market-place environments it will be entering.

128 L E T T E R S T O T H E E D I T O R

Matching commitments with convic-tions is important for personal and professional fulfillment. It’s also at theheart of good leadership.

131 E X E C U T I V E S U M M A R I E S

136 PA N E L D I S C U S S I O N

Evil Unnecessaries Don Moyer

It’s one thing to improve or differenti-ate a product by adding functions. It’sanother thing entirely to complicate aproduct beyond users’ comprehension.

HBR

14

49

114

121

TLFeBOOK

The Power of Ideas At WorkNow Available in Digital Format!

!"#$send me a 12 issue digital subscription ($118) to the ✓ .

Click Here To Order Now!

TLFeBOOK

The Power of Ideas At WorkNow Available in Digital Format!

!"#$send me a 12 issue digital subscription ($118) to the ✓ .

Click Here To Order Now!

TLFeBOOK

We’re Siemens, a global innovation company helping the needs of businessesand communities right here in the US. One of our specialties is providing

integrated services and solutions to enhance operational efficiency and strengthen theintegrity of airport security. From check-in through take-off to landing, we deliver solutions toincrease passenger comfort, baggage and cargo security, and airfield safety. We are the largestmanufacturer of baggage handling systems, and we maintain passenger and baggage screeningequipment at virtually all US commercial airports. And soon we’ll deliver the largest airport-wide100% in-line baggage security screening system in the US. We also provide airfield lighting controlsystems for sixty-five of the nation’s busiest airports. But unless you’re one of the 70,000Americans that we currently employ, you may not have heard of us. We’re Siemens.

Who is improving efficiency and security

We are.at airports all across the US?

automation & control • building technologies • energy & power • financial services • hearing solutions • home appliances • information & communicationlighting • material handling • medical solutions • transportation • water technologies usa.siemens.com

TLFeBOOK

RO

BE

RT

ME

GA

NC

K

F R O M T H E E D I T O R

When Businesspeople Think

usiness is always in a hurry.“History is more or less bunk,”

Henry Ford proclaimed. Speed is asource of competitive advantage. An ineffective businessperson is all talkand no action, while a successful busi-nessperson gets things done. Indeed, theeminent psychologist Karl Weick advisesleaders to leap before they look.

But spend some time with this issueof HBR first.

Start with “How Strategists Really Think: Tapping thePower of Analogy,” by two rising stars in Harvard BusinessSchool’s strategy unit, Giovanni Gavetti and Jan Rivkin.They’ve been studying executives’ reasoning processes.They’ve found that more often than not, executives developand test their strategic ideas by means of analogies. For example, Toys R Us was founded when Charles Lazarus figured that toy stores could be run like supermarkets.

Reasoning by analogy is highly efficient. It’s faster than de-veloping and sifting through mountains of data, it’s less riskythan trial and error, and it’s highly persuasive. But analogiesare perilous precisely because they are shortcuts and be-cause they are powerful. If you know what you’re doing, ana-logical thinking is a fabulous tool; Gavetti and Rivkin canshow you how to know what you’re doing. Not only will theirarticle make you think, it will help you think better.

Another threat to clear thinking is selection bias, whichoccurs when people draw conclusions from a set of datawithout examining the sample itself to see if it is represen-tative. Someone who has visited London only in the sum-mer might believe it has a delectable climate, for example.In his article “Selection Bias and the Perils of Benchmark-ing,” Stanford’s Jerker Denrell points out that business re-search is riddled with selection bias – starting with the factthat almost none of it is performed on firms that no longerexist. It’s interesting to know that a management practicesuch as empowerment is found in winning companies, butit could be that losers practice it, too.

Understanding how selection bias afflicts business re-search will make you a smarter consumer of business ideas.Take, for instance, the conventional wisdom about first-mover advantage. Conventional wisdoms, I should say, be-cause there are two: that it is a great thing to be first to a market and that first-mover advantage is a will-o’-the-wisp.Both are hasty generalizations that obscure useful detail.In “The Half-Truth of First-Mover Advantage,” Fernando

Suarez and Gianvito Lanzolla, fromBoston University and London BusinessSchool respectively, reveal the circum-stances under which first-mover advan-tage is very real – and the instances inwhich only a fool would pursue it.

Consultant Nathaniel Mass digs intoanother piece of conventional wis-dom in “The Relative Value of Growth.”Among executives, there’s an unspokenassumption that companies have to

choose between managing for value and managing forgrowth. Mass disagrees. Profitable growth, he argues, is a grossly underestimated lever for creating value. His re-search ought to make you think twice about how you reachyour strategic decisions.

In their eagerness for action, businesspeople commonlymake two other kinds of mistakes. First, they let the urgentdrive out the important. Nowhere is this more dangerousthan in the area of risk. As consultants Adrian Slywotzky andJohn Drzik argue in “Countering the Biggest Risk of All,”riskoperates at the strategic level as well as at the tactical onewhere executives are used to meeting it. Second, business-people race through processes that can’t be hurried. Two articles in this issue explore the theme of impetuosity. TheKellogg School’s Ranjay Gulati has been curious about howcompanies become customer focused. His research led himto the surprising conclusion that all of the companies thatsucceed in this quest go through the same four stages in thesame order. It’s not a process you can leapfrog, Gulati andhis coauthor James Oldroyd say in “The Quest for CustomerFocus”– it’s a journey you must complete one leg at a time.Something analogous happens with the development ofleaders, the topic of “Seven Transformations of Leadership”by consultant David Rooke and professor William Torbert.As our adult minds and characters mature, we developgreater capacities for leadership. Often, though, a talentedleader is promoted ahead of his or her maturation. The re-sult can be disastrous – for the company and for the leader.

Business is, indeed, about action–but it ought to be aboutintelligence, too. We hope this issue will make you smarter.

B

10 harvard business review

Thomas A. Stewart

TLFeBOOK

New York Beverly Hills Chicago Boston Bal Harbour South Coast Plaza Vancouver Las Vegas 888.880.3462 zegna.com

Peter Cincotti

ABC

TLFeBOOK

senior editorsLeigh BuchananDavid ChampionDiane L. CoutuBronwyn Fryer

Ben Gerson Paul HempJulia Kirby

Gardiner MorseM. Ellen PeeblesAnand P. Raman

associate editor

Eileen Roche

consulting editor

Louise O’Brien

manuscripteditors

Christina BortzLisa Burrell

Roberta A. FusaroMargaret K. Hanshaw

Andrew O’ConnellAndrea Ovans

editor forbusiness

developmentJohn T. Landry

executive editorand director of derivative

productsJane Heifetz

seniorproduction

managerDana Lissy

editorialproduction

managerChristine Wilder

senior designersKaajal S. Asher

Jill MancaAnnette Trivette

productioncoordinatorsJosette Akresh-

GonzalesTisha Clifford

communicationsmanager

Cathy Olofson

editorialcoordinator

Kassandra Duane

editorialassistant

Siobhan C. Ford

contributingstaff

Lilith Z.C. Fondulas Amy L. HallidaySusan McCabe

Amy N. MonaghanAnnie NoonanKristin Murphy

Romano

editor-at-largeharvard business school publishing

Walter Kiechel

a note to readersThe views expressed in articles are

the authors’ and not necessarily those ofHarvard Business Review, Harvard Business

School, or Harvard University. Authors may have consulting or other business relationships

with the companies they discuss.

submissionsWe encourage prospective authors

to follow HBR’s “Guidelines for Authors”before submitting manuscripts. To obtain a

copy, please go to our Web site at www.hbr.org;write to The Editor, Harvard Business Review,60 Harvard Way, Boston, MA 02163; or send e-mail to [email protected] manuscripts will be returned only if accompanied by a self-addressed

stamped envelope.

editorial offices60 Harvard Way, Boston, MA 02163

617-783-7410; fax: 617-783-7493www.harvardbusinessonline.org

Volume 83, Number 4April 2005

Printed in the U.S.A.

editorThomas A. Stewart

deputy editorKaren Dillon

executive editorSarah Cliffe

art directorKaren Player

TLFeBOOK

publisherCathryn Cronin Cranston

worldwide advertising offices

advertising director – worldwideTrish Henry212-872-9283

New York Maria A. Beacom Michael J. CarrollJames H. Patten509 Madison Avenue15th FloorNew York, NY 10022212-872-9280; fax: 212-838-9659

Atlanta 404-256-3800Boston 978-287-5400

Chicago 312-575-1100Dallas 214-521-6116

Detroit 248-524-9000Los Angeles 323-467-5906

San Francisco 415-986-7762

Australia 612-9252-3476Brazil 5511-3285-2754

France 33-01-4643-0066Hong Kong 852-237-52311

India 912-2287-5717Latin America 562-738-4033

Mexico 5255-5081-6838Sweden 48-8-541-318-37

United Kingdom 44-20-7833-3733

For all other inquiries,please call 212-872-9280.

For advertising contact information,please visit our Web site at

www.hbradsales.com.

subscription service information

u.s. and canada800-274-3214; fax: 902-563-4807

Rates per year: U.S., $129; Canada, u.s.$128

international44-1858-438868; fax: 44-1858-468969

Rates per year: u.s.$165; Mexico, u.s.$128

subscribe onlinewww.hbr.org

reproductionCopyright © 2005 Harvard Business SchoolPublishing Corporation. All rights reserved.

No part of this publication may be reproducedor transmitted in any form or by any means,

electronic or mechanical, including photocopy,recording, or any information storage and

retrieval system, without written permission.

consumermarketingdirectorJohn Titus

manager,marketing and

operationsMarisa Maurer

advertisingproduction

managerCatharine-Mary

Donovan

circulationfulfillment

managerGreg Daly

fulfillmentcoordinatorDanielle Weber

business director

Edward D. Crowley

circulationdirector

Bruce W. Rhodes

business manager

Adrienne M. Spelker

associatemarketingmanager

Nicole Costa

assistantadvertising

managerAshley C. Hartmann STANFORD

GRADUATE SCHOOL OF BUSINESSEXECUTIVE EDUCATION

CHANGE LIVES. CHANGE ORGANIZATIONS. CHANGE THE WORLD.

CHOOSE STANFORD EXECUTIVE EDUCATION FOR PROGRAMS IN:General Management • Financial Management • Leadership and Strategy

Marketing • Negotiation • Technology and Operations • Nonprofit and Philanthropy • Custom Programs

Executive Program in Strategyand OrganizationJuly 17 – 29

Mergers and AcquisitionsAugust 14 – 19

Strategic Marketing ManagementAugust 14 – 24

Corporate Governance ProgramMay 31 – June 3

Managing Teams for Innovationand SuccessJune 5 – 10

Executive Program in Leadership:The Effective Use of PowerJuly 10 – 15

Our Executive Education programs reflect the vibrant andentrepreneurial culture of Stanford. They are fast paced andinteractive. They engage you professionally and personally, andemphasize both the economic and social responsibilities ofmanaging business.

We are confident that you will enjoy every aspect of the Stanford Executive Education experience, and that you willleave our programs a better manager, leader, and innovator.

Please visit our Web site to apply online.

www.gsb.stanford.edu/exed866.542.2205 (toll free, U.S. and Canada only) or 650.723.3341

Stanford, California

LEADERSHIP AND STRATEGY PROGRAMS 2005

TLFeBOOK

ME

LIN

DA

BE

CK

Less remarked upon is the reverse. Sixyears ago, a book by Tom Peters exhortedmanagers to “Transform Your ‘Depart-ment’ into a Professional Service FirmWhose Trademarks Are Passion and Inno-vation!”But traditional businesses havelong been adapting PSFs’ approaches tocustomers, talent, and knowledge. Makersof things, such as General Electric andIBM, have been methodically turningthemselves into providers of services –and in the service category, PSFs add themost value and thus command the high-est margins. They also possess few depre-

Over the past 20 years, professional ser-vice firms (PSFs) have come to look a lotlike their clients. Many, now corporationsthemselves, operate in multiple countriesand have hundreds – even thousands – ofemployees. A small cadre of principals setsdirection, while professional administra-tors impose budgets and other financialcontrols. Functions that were once deemedintegral, such as research, are outsourcedor delegated to paraprofessionals. Thefirms’ proprietors, meanwhile, have over-come their qualms about advertising theirservices, not to mention themselves.

grist

The Limits of Professional Behavior

John W. Boudreau ([email protected])is a management professor at theUniversity of Southern California’sMarshall School of Business and theresearch director at USC’s Center for Effective Organizations.

James Goodnight ([email protected]) is the CEO of SAS Institute.

Michael Goold ([email protected]) is a director of theAshridge Strategic Management Center.

Pamela W. Henderson ([email protected]) is an associateprofessor of marketing at Washing-ton State University and the CEO ofNewEdge.

John Kastenholz is the vice president of consumer insights at Unilever.

Aradhna Krishna ([email protected])is the Isadore and Leon WinkelmanProfessor of Retail Marketing at theUniversity of Michigan’s Ross Schoolof Business.

Peter M. Ramstad ([email protected]) is the execu-tive vice president for strategy and finance at Personnel Decisions International.

Robert B. Reich ([email protected])is University Professor at BrandeisUniversity and the Maurice B. HexterProfessor of Social and Economic Policy at Brandeis’s Heller School for Social Policy and Management. He is a former U.S. secretary of labor.

Amy Salzhauer ([email protected]) is the founder and CEO of Igni-tion Ventures.

Peter K. Schott ([email protected])is an associate professor of economicsat the Yale School of Management.

David Young ([email protected]) is an associate at AshridgeStrategic Management Center andan independent consultant.

14 harvard business review

A survey of ideas, trends, people, and practices on the business horizon.

TLFeBOOK

ciating hard assets, while being enviablyrich in knowledge workers who are contin-ually upgrading their mental equipment.

In fact, the primacy of knowledge workmay be the salient common feature ofmost progressive corporations. Thesecompanies wage wars for talented em-ployees, from whom they increasingly expect mature managerial judgment.To encourage these knowledge workersto think like owners, progressive com-panies award options and grant stock;traditional professional service firms, ofcourse, are owned and run by their part-ners. And these companies, like PSFs,are adept at knowledge codification andsharing: Law firms’ file drawers, and nowdatabases, are crammed with modelpleadings that young associates regularlyconsult. What’s more, forward-lookingcompanies are committed to becomingcustomer-centric, an unmistakable echoof PSFs’ sworn subservience to theirclients’ interests.

With so much talent at hand, profes-sional service firms have always felt a responsibility to develop their own lead-ers. That’s why they’ve been such prolificsources of executives, having launchedthe careers of Delta Air Lines’ formerCEO Leo Mullin, Morgan Stanley CEOPhilip Purcell, and Citigroup CEOCharles O. Prince, among many others.The best-governed corporations do thesame. Procter & Gamble has become sogood at executive development, for othercompanies as well as itself, that it has es-tablished an alumni network along thelines of those maintained by up-and-outconsulting and law firms. Inevitably, a bitof the service firm clings to these trans-plants, who prefer to hire people withMBAs – a degree that, like the JD and the MD, is supposed to bespeak masteryof a complex body of knowledge and adherence to strict ethical standards.Trained to be corporate managers, thetop business-school graduates under-standably gravitate instead to invest-ment banks and consulting firms, the

two most lucrative varieties of profes-sional service firms.

Convergence in some areas is un-imaginable, however. For example, ser-vice firms are supposed to offer a singlestandard of care to all their clients, re-gardless of their ability to pay, while cor-porations use dynamic pricing and cus-tomer relationship management to varyservice quality according to spendingpower. But in general, the traits compa-nies share with PSFs attest to those com-panies’ health.

Still, organizations must take carewhen consulting a model that is itselfchanging – and not for the better. In fact,there is evidence that companies havelearned about as much as they can fromtoday’s professional service firms. Truepartnerships remain “effective mecha-

nisms for managing and motivatinghighly intelligent, highly autonomousknowledge workers,” according to LauraEmpson at the Clifford Chance Center forthe Management of Professional ServiceFirms at Oxford University’s Saïd Busi-ness School. But the larger PSFs that hirelaterally instead of investing in home-grown talent; that favor ever-higher ra-tios of associates to proprietors; and thatshow greater concern for shareholdersthan for clients may no longer be worthyof emulation.

The leaders of today’s large profes-sional service firms, unlike their contem-poraries running corporations,“are moreconcerned about their book of businessthan how the group does,” asserts DavidMaister, a Boston-based consultant. Suchfirms resist accountability, refuse to stick

april 2005 15

l e a d e r s h i p

Those Fertile HR FieldsTheoretically, generalist CEOs are better equipped than specialists to navigate

the myriad functions inside, and the complex world outside, their compa-

nies’ walls. In Japan, one of the best sources of generalists is human resource

departments.

In his new book The Embedded Corporation: Corporate Governance and

Employment Relations in Japan and the United States (Princeton, 2004), UCLA

management professor Sanford M. Jacoby reports that in Japan HR departments

have often been springboards to top executive postings – including CEO – as well

as to board membership. Studies from the 1990s showed Japanese CEOs emerg-

ing from HR more frequently than from R&D, engineering, or overseas jobs. In

addition, one-fifth of directors in Japanese manufacturing firms and one-third

of those from other industries claimed past stints in HR.

HR managers in the United States become CEOs or directors only very rarely;

so why have they reached the top of the charts in Japan? For one thing, the Japa-

nese consider HR a good place to get to know leaders and managers throughout

the organization. But more important, Jacoby explains, Japanese HR managers

are often generalists who spend much of their careers in other functions, includ-

ing accounting, finance, strategic planning, production, and sales. In other words,

they are well-rounded, Jacoby says. Perceived as a narrow specialty in the United

States, HR in Japan is a place to go to get ahead. – Leigh Buchanan

Reprint F0504B

TLFeBOOK

to their stated strategies, and lack vision,drive, and commitment, he says.

In short, if companies have anythingmore to learn from professional servicefirms, it will be from those that operatedin the era before PSFs attached Inc. orLLP to their names and developed thefear of clients’ lawsuits that those lettersbetray. That means the era before PSFsbecame, in essence, profit-seeking com-panies themselves. – Ben Gerson

Reprint F0504A

how we do it

The Spielberg Variablesby john kastenholzCompanies want to believe that all advertising ideas – like the children ofLake Wobegone – are above average.But the bell curve dictates that only 30out of every 100 television ads we test atconsumer-products giant Unilever willbe superior. Forty out of 100 will be justaverage, and, understandably, we don’twant to put average ads on the air.

TV commercial effectiveness is hugelyimportant at Unilever; last year, we spent $3.3 billion globally advertising our brands. Each year, we work with ouragencies to produce a multitude of 30-second spots for the U.S. market at a costof about $400,000 each, not includingairtime. Many of those ads aren’t abso-lute failures but still score low enough–consumers rate them as B players inquantitative research – that we wouldrather not entrust them with our brands.For the past few years, however, we’vebeen using a diagnostic technique thatallows us to reedit just-passable ads intogreat ones.

Working with Albuquerque, New Mexico–based Ameritest/CY Research,one of our two principal testing compa-nies in the United States, we ask targetaudiences the usual questions about our ads: Do they stand out? Are they wellbranded? Do they motivate consumers to act? For the ads with mediocre scores,we then judge whether the problem lieswith the concept (the ad looks great, butthe idea isn’t exciting enough) or withthe execution (the idea is potentially

wonderful, but somethingabout the way the ad was puttogether is holding it back). Ifwe determine that we have abig idea hobbled by flawed ex-ecution, we put “the Spielbergvariables” to work.

That is, we ensure that eachof our ads employs the samestyle and storytelling tech-niques used in feature films.Good movies win viewers’ at-tention, propel the audienceforward emotionally, and con-vey meaning. Good movies arealso often born in the editingroom. We believe the same is true ofgood ads, so our goal is to diagnose problems and then fix them with a newdirector’s cut, as it were. That requiresidentifying flaws at each ad’s narrativeinflection points.

As a part of the process, each ad is de-constructed into frames that represent a change in tone or action – a cut to anew scene, for instance, or different bodylanguage displayed by a character in the ad. These images are randomized andshown to consumers, who have alreadyviewed the ad in its entirety, as part of anonline interview. The consumers providethree levels of feedback. First, they pointout which frames they recall and whichthey don’t. Second, the consumers de-scribe how they felt emotionally (Mildlypositive? Strongly negative? Neutral?)about the images they recall. And finally,they talk about the values (Convenience?Taste? Nutrition?) each image conveys.

The frames give us a visual vocabularyfor probing how viewers respond to dis-crete elements of an ad. When those data are plotted in a “flow of attention”or “flow of emotion” graph we begin tosee where things go wrong. We can tell if the ad hooks viewers right away. If itdoesn’t, we can pinpoint where theirimage recall–and hence their attention–starts to decline. Or we can see exactlywhere viewers shifted from a weak posi-tive feeling to a strong one. If importantinformation – particularly about thebrand – does not appear at those pointsof peak attention, we are missing theboat. If viewers take away the message

16 harvard business review

“cleans” when we are trying to sell themon “beauty,” we can identify exactly whichimages aren’t doing their jobs. Armedwith this precise definition of the prob-lem, our ad folks can make creativechanges to achieve the desired effects.

Over the past two years, 60 ads fromone of our health and beauty productsunits were approved for airing; 25 ofthem started out as average performers.After recutting on the basis of the Spiel-berg variables, those 25 ads tested in thesuperior range. This ability to optimizeour advertising helps Unilever maximizeROI in what has traditionally been a neb-ulous and difficult area to measure.

Reprint F0504C

headquarters

When Lean Isn’t Meanby michael goold and david youngMost executives believe that corporationswith large headquarters are bureaucratic,out of touch with customers, and slow tomake decisions – and, so, perform poorly.That’s why CEOs slash headquarters staffwhenever they try to cut costs or improveperformance. But do lean headquartersreally perform better?

In collaboration with research partnersaround the world, we studied the sizeand financial performance of the head-quarters of 600 companies in Europe,the United States, Japan, and Chile. Wefound a wide range of HQ sizes and com-position. For instance, for companieswith 10,000 employees, headquarters size

continued on page 18

TLFeBOOK

who knows the market better

than I do and understands my

risk preferences and financial

needs. Searching for profits,

IBM progressed from hardware

to software to services as each

of those offerings in turn be-

came commoditized. Today, the

company’s focus is on special-

ized solutions, consulting, and

custom applications – the next points along the sophisti-

cation arc.

In sum, topflight research communities, and increas-

ingly demanding American customers and their growing

appetite for ever more sophisticated products and ser-

vices, all spell more knowledge work in the United States,

not less. Between 1999 and 2003 (the latest year for which

we have data), the number of IT-related white-collar jobs

in the United States actually increased. IT wages are ris-

ing, too (adjusted for inflation and the business cycle).

The earnings of college graduates continue to outpace

the earnings of those with only high school diplomas; the

earnings of people with graduate and professional degrees

are rising even faster. If demand for knowledge work

were dropping, we’d expect the opposite.

This isn’t a brief for complacency. Unless the United

States invests large sums in education and in basic re-

search and development – and invests wisely – it won’t

have enough knowledge workers to meet future demand.

It won’t even have the majority of the world’s richest and

most sophisticated customers. Decades from now, China

and India may have surpassed the United States in high-

value knowledge work.

A related challenge is to reverse the slide of Americans

without college degrees, most of whom fall into the local

service economy, with its low wages and vanishing bene-

fits. The widening earnings gap between this group and

America’s knowledge workers undermines social solidar-

ity and threatens democracy. Not every American can be-

come a world-class knowledge worker, of course. But mil-

lions more can get the skills they need to be prosperous

members of the world’s wealthiest nation.

Reprint F0504E

Plenty of Knowledge Work to Go Around

april 2005 17

Anxiety over outsourcing mounts as the jobs trekking

overseas increasingly involve intellectual heavy lifting.

Relatively modest knowledge work – back-office support,

customer service, and data entry – was followed by more

sophisticated tasks such as computer coding, insurance un-

derwriting, claims processing, and medical transcription.

Recently, we have been exporting jobs in X-ray diagnos-

tics, software programming, software engineering, and

even some research and development.

At this rate, won’t most of the cerebral work American

companies do be farmed out to lower-cost labor offshore?

The short answer: Not a chance. The slightly longer – and

even more upbeat – answer is that there is far more knowl-

edge work in the United States today than there was a de-

cade ago. In ten years, we can expect to see more.

Some of that work will even come from foreign-based

corporations offshoring to the United States. Global com-

panies deciding where to locate consider first where they

can tap into the highest level of skill they need at the

lowest cost. For that reason, the quality of America’s top

research institutions is a huge boon to the nation’s knowl-

edge workers. A mile from my home in Cambridge, Massa-

chusetts, for example, a research and development zone

plays host to loads of non-U.S. software and biotech firms

eager to absorb some brainpower from Harvard and MIT.

I assume those companies are paying a high price for such

skills, and they’re worth every penny.

At the same time, Siemens, Nokia, and General Elec-

tric, among others, are conducting manufacturing-related

R&D in China, at a much lower cost. That work doesn’t

require a Harvard or an MIT, and it needs to be done close

to where it will be implemented – in this case, China’s

sprawling manufacturing centers.

Yes, proximity to customers matters. And here’s an-

other big advantage for America’s knowledge workers:

They live near some of the richest and most sophisti-

cated customers in the world. Furthermore, as more prod-

ucts become low-cost commodities, those customers are

demanding – and paying more for – additional customiza-

tion, special applications, and new designs and ideas. In

other words, knowledge work. Because I can trade over

the Internet, for example, I no longer rely on a stock-

broker. But I do need advice from a financial consultant

by robert b. reich

TLFeBOOK

varied from a low of ten staff members to a high of well over 1,000 people.

Most surprising, we found no evidencethat a lean and mean headquarters is associated with superior financial perfor-mance. On the contrary, the companiesthat reported above-average profitability(measured by both the return on capitalemployed and total shareholder returns)had headquarters that were, on average,20% larger than the headquarters of com-panies of similar size (in terms of totalemployees) and with similar influenceover business decisions.

This could mean that bigger headquar-ters are more effective than smaller onesand enable companies to perform better.Alternately, it might imply that betterperformance allows companies to sup-port bigger-than-average headquarters.While the latter is sometimes true, wefound that, in many companies, large cor-porate staffs improved performance bycreating value that more than paid fortheir costs. For example, pharmaceuticalcompanies such as Pfizer have big corpo-rate R&D departments, but this costly activity is central to the companies’ strate-gies and essential to their market perfor-mance. Other companies use large HRfunctions at the center to develop man-agement competencies that are especiallyvaluable to their businesses. Unilever’sHR function, for example, concentrates

on developing internationally mobilemanagers with superb marketing skills in the area of fast-moving consumergoods. Because corporate centers addvalue in different ways depending on acompany’s strategy and the businesses in which it competes, the appropriatesize and nature of staff functions arebound to differ, too.

The bottom line: There is no standardor ideal model or size for a successfulheadquarters. To achieve high perfor-mance, don’t reflexively cut staff. Focusinstead on matching headquarters’ sizeand roles with corporate strategy.

Reprint F0504D

marketing

How Big Is “Tall”?by aradhna krishna

To make their products stand out, orseem to deliver more value for their size,companies often invent evocative labelslike Super Size, Value Size, Double Gulp,and Whopper. To discourage consumersfrom making direct brand comparisons,businesses also create ambiguous por-tion sizes like Tall, Sixteen, and Power.The question is, do these labels mean the same thing to everyone?

My colleagues – Nilufer Aydinoglu andBrian Wansink – and I have found that

consumers do share acommon understandingof product labels, placingmany of the labels inunique and consistent po-sitions relative to one an-other. In an initial study,we looked at consumers’perceptions of productsizes in two food catego-ries. Within each cate-gory, we chose 14 com-mon labels, some ofwhich were conventional(such as small, medium,and large), others ofwhich were invented bymarketers (such as SuperQuencher and Big Kids).Study participants wereasked to arrange the

labels in each category on a scale fromsmallest to largest, left to right. For manylabels, the subjects’ perceptions aboutthe product sizes were significantly simi-lar. For example, consumers agreed that“petite” is smaller than “short,” that “sin-gle” falls between “small” and “medium,”and that “tall” is larger than “medium”or “double.” Super Quencher and Jumbotied in consumers’ minds (statistically)for sheer – apparent – size.

Because consumers form clear ideasabout product size on the basis of labels,we wondered whether their perceptions of serving size–regardless of actual size–

would affect how much of a product they ate. In a separate study, we served Rotary Club members individually packedeight-ounce portions of eggs, labeled either medium or large. Those givenmedium portions ate, on average, 35%

more than those whose portions were la-beled as large. The Rotarians’ perceptionshad obviously influenced their behavior.

Companies should test whether theirown views of their product labels matchtheir customers’ perceptions and whetherthe labels achieve what they’re supposedto. Do you want to convey that even yoursmall sizes are big? Then a label like “single” is better than a label like “petite.”Starbucks understood this when it labeledits smallest coffee “tall.” And don’t assumethat consumers think “extra large” is thebiggest. Finally, consider how your labelscan affect consumption: Would some

18 harvard business review

headquarters staff

total company employees

10,000 100,000 1M 1,000

10

100

1,000

10,000

1

100,000

A Corporate Head CountThe size of a company’s headquarters has little to do with howmany employees the firm has. Companies with 10,000 employees,for instance, have headquarters ranging in size from ten to severalthousand people.

continued on page 20

TLFeBOOK

6�W^\\Zg�bVg`Zi�^h�dji�i]ZgZ#�LZ�XVc�]Zae�ndj�XVeijgZ�

^i�l^i]�V�bdgZ�Z[[^X^Zci�hjeean�X]V^c#

^ÊÓääxÊ1��Ìi`Ê*>ÀVi�Ê-iÀÛ�ViÊ�vÊ��iÀ�V>]Ê��V°Ê1*-]ÊÌ�iÊ1*-ÊLÀ>�`�>À]Ê>�`ÊÌ�iÊV���ÀÊLÀ�Ü�Ê>ÀiÊÀi}�ÃÌiÀi`ÊÌÀ>`i�>ÀÃÊ�vÊ1��Ìi`Ê*>ÀVi�Ê-iÀÛ�ViÊ�vÊ��iÀ�V>]Ê��V°Ê���ÊÀ�}�ÌÃÊÀiÃiÀÛi`°

L]n�aZi�V�[Zl�i]^c\h�a^`Z�aVc\jV\Z�WVgg^Zgh!�Xjhidbh�gZ\jaVi^dch�VcY�kZcYdg�X]VaaZc\Zh�hiVcY�^c�i]Z�lVn�d[�ndjg�XdbeVcnÉh�\gdli]4�AZVkZ�^i�id�JEH�#�

I]gdj\]�djg�Hjeea^Zg�BVcV\ZbZci�hZgk^XZh!�lZÉaa�]Zae�ndj�ZhiVWa^h]�hjeea^Zg�VXXdjciVW^a^in�VcY�bV^ciV^c�hig^Xi�Xdbea^VcXZ�bVcV\ZbZci�Å�Vaa�id�ZchjgZ�i]Z�fjVa^in�d[�dgYZgh�VcY�dc"i^bZ�YZa^kZgn#�6cY�lZÉaa�egdk^YZ�dca^cZ�igVX`^c\�VcY�gZedgi^c\�XVeVW^a^i^Zh�i]Vi�]Zae�ndj�bV^ciV^c�Xdcigda�Vaa�Vadc\�i]Z�lVn#

LZ�Vahd�d[[Zg�i]Z�WZhi�igVchedgiVi^dc�hdaji^dch�[dg�ndjg�i^bZ�VcY�Xdhi�eVgVbZiZgh#�6cY�djg�Xjhidbh�Wgd`ZgV\Z�VcY�igVYZ�Xdchjai^c\�ZmeZgi^hZ�XVc�]Zae�ndj�Vkd^Y�YZaVnh�VcY�eZcVai^Zh#�

Ndj�iZaa�jh�i]Z�bVg`Zi0�lZÉaa�]Zae�ndj�gZVX]�^i#�L^i]�hjeean�X]V^c�Z[Ò�X^ZcXn�i]Vi�Wg^c\h�i]Z�ldgaY�id�ndj#

JEH#Xdb$hjeeanX]V^c���&"-%%",)'"*,',��

TLFeBOOK

of your customers buy two servings ofyour product if it were “regular” insteadof “large”?

Reprint F0504F

culture

Sweat the Small StuffIn 1982, James Q. Wilson introduced his“broken windows” theory of neighbor-hood decline in the pages of The Atlantic.

The criminologist famously argued thatby leaving litter, graffiti, and other urbandetritus unattended, authorities signal a lack of concern that tempts miscreantsto commit more serious violations.

Now a business author is suggestingthat companies are similarly vulnera-ble. A stained carpet in the office or aburned-out reading light on an airplanemay seem inconsequential. But whenmanagement ignores such trivial irrita-tions, it is effectively telling employeesor customers that they don’t matter.Such unconcern can depress morale or drive away business, says MichaelLevine, who interviewed criminologists,management experts, and ordinaryworkers and consumers about how tinyoffenses influence their perceptions ofcompanies.

An organization’s true priorities are re-vealed by the small stuff, explains Levine,whose book Broken Windows for Business

will be published by Warner in the fall.The corporate manual may trumpet themessage,“We are all one team,” but the rank and file know better when they see broken vending machines going un-repaired while the executive dining roomfunctions like a Michelin-starred restau-rant. “There’s a significant psychologi-cal impact to dingy surroundings – tostained carpets and broken toilets,” saysLevine, founder of a Los Angeles–basedpublic relations firm.“You can’t convinceemployees that you love and care aboutthem if you’re sending psychic signalsthat you don’t.”

Attention – or inattention – to detail affects service, too. Outsourcing, for ex-ample, is reviled for inflicting major painon workforces; but it also causes plenty of minor injuries to customers, Levine

20 harvard business review

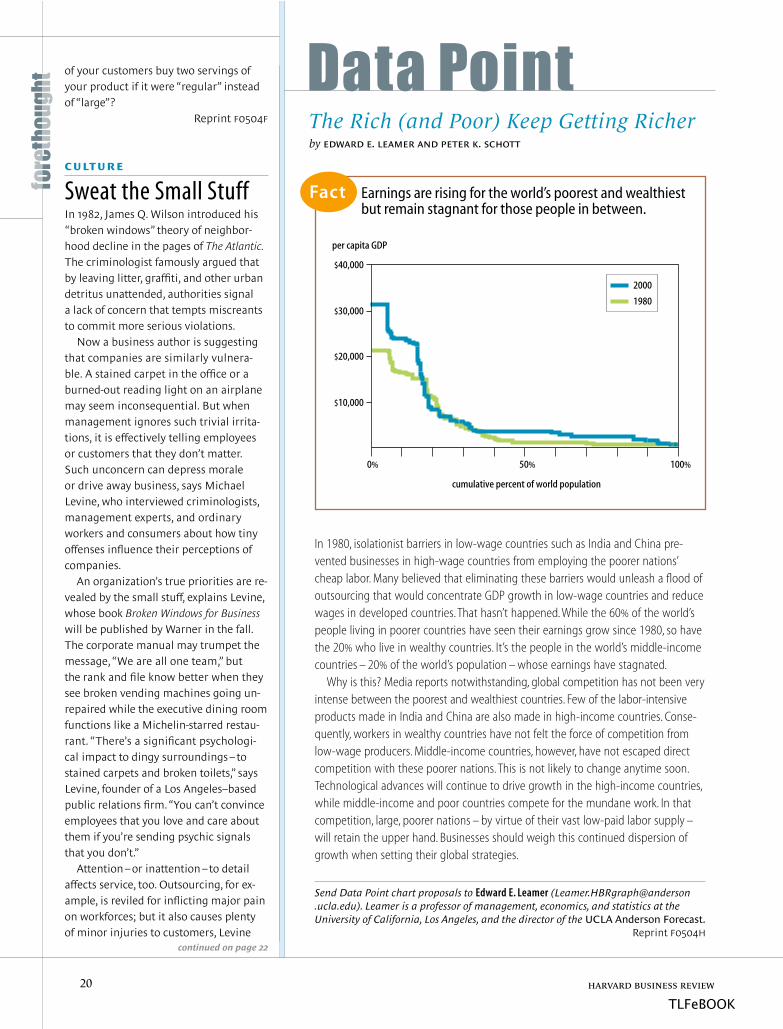

The Rich (and Poor) Keep Getting Richerby edward e. leamer and peter k. schott

Fact Earnings are rising for the world’s poorest and wealthiestbut remain stagnant for those people in between.

In 1980, isolationist barriers in low-wage countries such as India and China pre-vented businesses in high-wage countries from employing the poorer nations’cheap labor. Many believed that eliminating these barriers would unleash a flood ofoutsourcing that would concentrate GDP growth in low-wage countries and reducewages in developed countries. That hasn’t happened. While the 60% of the world’speople living in poorer countries have seen their earnings grow since 1980, so havethe 20% who live in wealthy countries. It’s the people in the world’s middle-incomecountries – 20% of the world’s population – whose earnings have stagnated.

Why is this? Media reports notwithstanding, global competition has not been veryintense between the poorest and wealthiest countries. Few of the labor-intensiveproducts made in India and China are also made in high-income countries. Conse-quently, workers in wealthy countries have not felt the force of competition fromlow-wage producers. Middle-income countries, however, have not escaped directcompetition with these poorer nations. This is not likely to change anytime soon.Technological advances will continue to drive growth in the high-income countries,while middle-income and poor countries compete for the mundane work. In thatcompetition, large, poorer nations – by virtue of their vast low-paid labor supply –will retain the upper hand. Businesses should weigh this continued dispersion ofgrowth when setting their global strategies.

Send Data Point chart proposals to Edward E. Leamer ([email protected]). Leamer is a professor of management, economics, and statistics at the University of California, Los Angeles, and the director of the UCLA Anderson Forecast.

Reprint F0504H

$10,000

$20,000

$30,000

$40,000

0% 100%50%

per capita GDP

cumulative percent of world population

2000

1980

continued on page 22

TLFeBOOK

©UBS 2005. The key symbol and UBS are registered and unregistered trademarks of UBS. All rights reserved. Wealth Management services in theU.S. are provided by UBS Financial Services Inc., a registered broker dealer offering securities, trading, brokerage, and related product and services.UBS Financial Services Inc., Member SIPC.

You & Us

You and us. Bringing all the resources of one of the world’slargest wealth management firms to the table. Any table.

WealthManagement

Global AssetManagement

InvestmentBank

At UBS, we can offer our clients some of the world’s most powerful financial

resources. But, the most important resources of all are the ones your financial

advisor will bring to the table the very first time you meet. They’re called listening

and understanding. And they’re the first steps in the disciplined, on-going process

that we call Wealth Management at UBS.

We believe that the only wealth management plan worth having is the one

that’s specifically customized for your needs. So your financial advisor will always

begin the process by listening to the expert on your situation. You. It’s the key

to understanding where you are, where you want to be, and your risk tolerance

to get there.

We can then access all our resources as one of the world’s largest managers

of wealth, an award-winning investment bank and a global leader in asset

management. We can bring in expertise from asset allocation to estate planning

services. Together, we can design your financial plan.

Yet it’s not a plan set in stone. At UBS we recognize that as your life changes, so

your plan may need to change too. We’ll meet with you regularly to monitor your

portfolio and review strategies. Simply put, we’ll keep listening. Listening, and

understanding. It’s what we mean by a relationship we call ‘You & Us.’

TLFeBOOK

says.“You have a problem with your In-ternet provider, so you call the help lineand you get Bangladesh,” he says.“Theydon’t speak English well; you can barelyunderstand them. But call sales and youget a woman in Texas. That tells youwhat really matters to the company.”

In fact, the worst broken windows areoften broken people, Levine says. Cus-tomers who are ill-treated by a poorlytrained associate, or employees workingside by side with someone clearly in-competent, surmise that the businessdoesn’t respect them. And their angerspreads outward: from the unacceptableemployee to the manager who hiredhim, to the person who trained him,to the manager who hired the trainer,and so on.

Levine recommends that managerseject poor performers as quickly as possi-ble, letting everyone affected know theproblem has been dealt with. That mayprove unpopular among some employ-ees in the short run, but in time they willappreciate the improved environment.“When [former New York City mayorRudolph] Giuliani went after the squee-gee men and the turnstile jumpers, peo-ple called him a bully; they called himracist,” Levine says.“But his actions had a positive impact on the quality of life in New York City.”

Companies frying bigger fish –problems with earnings or ethics, for example – may be less sympathetic tosuch entreaties. But toilets and parkinglots and waiting times matter, Levine insists.“Leaders who don’t get that willnever build truly great companies,” hesays.“Companies need to do whatever ittakes to fix those bad little things beforethey become much, much bigger.”

– Leigh BuchananReprint F0504G

communication

Just My Typeby pamela w. henderson

The one-picture-to-a-thousand-wordsratio unjustly downplays the importanceof typestyles. Academics and marketershave long known that the choice of font

in logos and advertising copy greatly influences legibility, memorability, andpublic perception of the brand.

Companies need typestyles that suittheir images and reflect their inten-tions. To help them choose the rightfonts for their messages, my colleaguesat Washington State University – Joan L.Giese and Joseph A. Cote – and I roundedup 210 typefaces and identified a half-dozen discrete design components ineach. We then looked at how those com-ponents affect consumers’ responses toa brand. Specifically, we asked con-sumers to what degree the fonts con-veyed a message that was pleasing (lik-able, warm, attractive); engaging(interesting, emotional); reassuring(calm, honest, familiar); and prominent(strong, masculine).

The results should get marketersthinking about the messages their logosand ads are – perhaps inadvertently –sending and how they might better exploit typefaces to shape customers’perceptions.

Our research yielded six clusters offonts that produced similar effectsamong consumers.

The first group comprises fonts thatare considered likable, warm, attractive,interesting, emotional, feminine, and del-icate. But they are not especially strongor reassuring. Such fonts have consider-able aesthetic appeal but do not inspiregreat confidence. They include:

ScheherezadeInformal RomanAncientScriptEnviroPepita MT

The second group comprises fonts wedefined as interesting, emotional, excit-ing, and innovative. They are also unset-tling and unfamiliar. They could put offsome marketers but might be effective in edgier campaigns. These fonts include:

BaphometEddaChillerStonehengePaintbrush

The third group of fonts represents theworst of all worlds: disliked, cold, unattrac-tive, uninteresting, and unemotional. Butthese typefaces aren’t useless. Companiesmight, for example, use them to displaycharacteristics or claims of a counter-cultural or competing brand. They include:

PlaybillLoganOnyxIndustria InlineStencilSet

The fourth group of fonts is strong andmasculine. Their weighty lines suggest a forcefulness and solidity coveted bymany brands. They include:

NewYorkDeco BandstandSunSplashMiddle AgesFisherman

The fifth group gets high marks forbeing interesting, emotional, exciting, andinformal. But these fonts are also consid-ered dishonest, cold, and unattractive.They are good for conveying negative in-formation or for targeting such niche mar-kets as punk rock fans. These fonts include:

AluminumShredBigDaddyIntegrityRansomAmazon

The final group, which contains manycommon, highly readable fonts, makesup in comfort what it lacks in excitement.If you want to convey “stalwart of thecommunity,” these are your fonts:

GeorgiaVerdanaJanson TextCentury GothicTimes New RomanCentury Schoolbook

Most important, we demonstrate thetrade-offs corporations must accept inchoosing fonts. Not all the impressions

22 harvard business review

TLFeBOOK

april 2005 23

hen it comes to schedules,

James Goodnight hates being

fenced in. So the CEO of SAS

Institute, a $1.5 billion maker

of business software based in

Cary, North Carolina, attends as few formal meet-

ings as is humanly possible. He talked to us about

why useless meetings proliferate and what he

views as good alternatives.

Everyone hates meetings, but aren’t they a necessary evil?

Most of them aren’t necessary. Weekly meetings, in particular, in which you’re seeing

the same people and going over the same kinds of information are mostly a waste of

time. Managers and leaders should be constantly having casual interactions with peo-

ple at all levels, in elevators and hallways and just popping into one another’s offices.

The important thing is to be visible and accessible, which you’re not when you’re sit-

ting behind a closed door in a conference room for the better part of your days.

Why are so many meetings a waste of time?

There’s a tendency when you’re looking at an issue to want to cover yourself. So

you copy everyone on your e-mails or ask them to attend your meetings. And they

feel like if they don’t answer the e-mail or attend the meeting, that means they’re

not engaged or they’re out of the loop. How do you tell your boss,“I don’t need to

be part of that discussion,” without it sounding like you aren’t important or you

don’t care? But if you’re not part of it, and you spend that time doing something

that’s actually related to your job, your productivity goes way up.

We talk about the need for companies to be flexible, but what they’re often not

flexible about is people’s time. People tend to think that a full calendar means

they’re working hard. What it really means is that they haven’t given themselves

time to explore new ideas or just visit with folks. And if they have to respond

quickly to something, they have the additional headache of having to cancel a

bunch of meetings. My best days are ones when there is nothing on my calendar.

By the way, not all meetings are a waste of time. At certain levels of the organiza-

tion, it’s appropriate to meet with your team on a regular basis to keep them on

focus. Meetings can also be effective for brainstorming. But it’s important to contin-

ually question: Will this meeting boost or bust productivity? How long will it really

take to cover the issue? Who really needs to be there? Does every meeting need to

last an hour because that was the default appointment in the electronic calendar?

How do you keep meetings short?

I have left many meetings once I stopped getting anything out of them.

– Leigh Buchanan

Reprint F0504L

The Beauty of an Open Calendar

james goodnight on meetings

an organization may want to create canbe achieved at the same time. Some desirable traits – such as engaging and reassuring – are mutually exclusive. Butcompanies can use an understanding oftypestyle attributes to design their ownfonts and, consequently, exert maximumcontrol over their messages. That’s whatDisney and Hallmark did, and their fontshave become integral – and beloved –parts of their brands.

Reprint F0504J

human resources

Where’s Your PivotalTalent? by john w. boudreau and peter m. ramstad

As organizations increasingly competethrough talent, their investments inhuman capital will determine their com-petitive positions. Yet HR’s way of man-aging this key resource stands in sharpcontrast to how other organizationalfunctions operate. Marketing, finance,and most other functions have well-developed methodologies for generatingthe information managers need to makestrategic decisions. HR, however, often focuses principally on its own perfor-mance, carefully measuring cost per hire, the ROI on its programs, and howits initiatives affect skills and attitudes.It’s time for HR to shift its focus fromwhat it does to the quality of the talentdecisions it supports. HR needs to de-velop a systematic process for improvingdecisions, not just implementing them.

HR should be able to help leaders answer critical questions such as, Wheredoes our strategy require talent that isbetter or more plentiful than our com-petitors’? In what new business ven-tures do we have a strategic advantagebecause of our talent? What talent gaps do we need to close in order to keep ourcompetitive advantage? And, most im-portant, Where would a change in theavailability or quality of talent have thegreatest impact?

HR should begin its transformation byapplying the tools of segmentation, theSA

S IN

STIT

UT

E

TLFeBOOK

widely accepted method for improvingdecisions in customer and financial markets. Do you use the same advertis-ing mix for every product line or investcapital equally across divisions? No.Yet when it comes to managing talent,your HR department probably appliesthe same processes and programs tonearly everyone. And even when HR investments are differentiated, they’reoften designed to meet generic bestpractices (“assign everyone a mentor,”for instance) or target broad groups ofindividuals (the top 20% of managers,for instance). Just as marketing system-atically segments customers to target investments strategically, HR needs tosegment talent to deploy human capitalstrategically.

Maybe you think you don’t need a de-cision science to figure out where to con-centrate your A-level talent. But our workwith large companies shows that’s not al-ways the case. Corning, for example, hastraditionally competed as an innovator.As the company expanded globally, itcontinued to invest its HR resourcesheavily in support of R&D scientists. Butwhen Corning’s HR leaders used talent-segmentation techniques to study thedistribution of human capital in the orga-nization, they discovered that the dearthof talent in manufacturing, not in prod-uct innovation, was slowing down thecompany’s expansion into markets insome developing countries.

On closer examination, HR and busi-ness leaders in the company’s DisplayTechnologies division found that, insome regions, there were only a few pro-duction engineers with one type of criti-cal manufacturing knowledge, a particu-lar skill set that takes years to develop.The division made the case for shiftingsome HR assets out of R&D and into hiring and retaining enough of these key production engineers to meet the division’s needs.

As Corning’s experience suggests, tal-ent decisions can be made with the samelevel of logic and rigor as decisions aboutmoney, customers, and technology – andthey can be logically linked to strategy.The ball is in HR’s court.

Reprint F0504K

frontiers

Way Faster than aSpeeding Bulletby amy salzhauer

Femtosecond lasers emit pulses of lightthat last just a millionth of a billionth of a second. These lasers enable surgery soprecise that a single mitochondrion canbe removed without harming the rest ofthe cell, and machining so controlled thatstructures can be micromachined withina piece of glass. Eric Mazur, a professor ofapplied physics at Harvard, likens thesefast flashes to “bullets of light.”

Once confined to phys-ics research laboratories,femtosecond lasers are justnow starting to be appliedby medicine and industry.They are poised to revo-lutionize processes as diverse as drug creationand the disassembly of nuclear weapons.

Tech Talk: Just how fastis a millionth of a billionthof a second? It takes lightonly about a second totravel from the moon to earth.“In afemtosecond,” Mazur says,“light travelsabout 300 nanometers”– or a fraction ofthe width of a human hair. That means a femtosecond laser lets users view phe-nomena previously impossible to observebecause they occur in so short a timeframe. It also means that while theamount of energy used to deliver the light is small, the intensity of light strik-ing the target is high because the pulse is so quick.“The peak power of our laserpulses–that is, the energy they deliver perunit time–is about the same as that of allpower plants in the United States com-bined,” Mazur explains.“Imagine all ofthat power concentrated into a micro-scopically small volume. Of course, thelaser pulse is very short, so we only deliverenergy for a very short amount of time.”

The brevity of femtosecond laser pulsesprevents them from transferring signifi-cant heat or shock. As the laser pulses,the material it hits becomes an ionized

plasma, while the surrounding materialstays cool. As a result, femtosecond lasersare much more precise and can be usedon much more fragile materials than canconventional lasers, diamond saws, watersaws, or other cutting tools. Femtosecondlasers produce a smooth, clean cut. Sowhile conventional lasers used in dentistrycan cause cracks and ragged holes in teeth,for example, femtosecond lasers drill pre-cise holes without collateral damage.

Why It Matters: Femtosecond laserscan remove material one atom at a timefrom substances as diverse as silicon,steel, and heart tissue; and they can ma-

chine very precise struc-tures that range in sizefrom a few microns to afew millimeters. They canalso change the refractiveproperties of transparentmaterials, so they can beused to manufacture inex-pensive optical devices,wave guides, and sensors.Chemical and drug manu-facturers are starting touse the lasers to observeimportant chemical andbiological reactions thatlast only femtoseconds,

such as the interaction of carbon monox-ide and myoglobin, which is critical forunderstanding how muscle cells carryoxygen. And the lasers “provide a muchhigher resolution for medical-imaging ap-plications,” says Melissa Love, of SanDiego–based laser manufacturer Del MarVentures. Taken together, these applica-tions will have a multibillion-dollar im-pact on a variety of industries.

In the Game: Invented at Bell Labora-tories in the 1980s and driven by ad-vances in fiber telecommunications,femtosecond lasers have long been usedin academic labs, where scientists haveoften built their own. A growing numberof small manufacturers have started tomake easy-to-use tabletop lasers that costonly $15,000 to $30,000. The number ofsuppliers should grow with demand, aslarge companies catch on to the lasers’ability to create better, cheaper, and en-tirely new drugs, devices, and products.

Reprint F0504M

24 harvard business review

TLFeBOOK

Welcome to our Swiss Business. Please take a bed.

We want to turn flying into an unforgettable experience. Forexample, by offering a business class designed to let yourelax even more. Lie down and relax in your spacious lie-flatseat for the ultimate in sleeping comfort. And enjoy theextra legroom and our attentive service. To find out whatelse SWISS has in store for discerning travellers like you,simply visit swiss.com

Service from 8 North American gateways to 70 destinations worldwide.

For information and reservations, call 1-877-FLY SWISS, contact your local travel agent or visit swiss.com

Partner in the American Airlines® program.

American Airlines® and AAdvantage are registered trademarks of American Airlines, Inc. American Airlines® is not responsible for products and services offered by other participating companies.TLFeBOOK

Hot Property The Stealing of Ideas in an Age of GlobalizationPat Choate(Alfred A. Knopf, 2005)

Innovation is not a pure act. Individuals and companies want to create, sure,

but they also want to get paid. If they’re not paid, then progress suffers, and

countries built on innovation tremble to their very foundations. That dire

situation is upon us, argues political economist Pat Choate in his book, Hot

Property. Global intellectual-property theft not only hurts Disney’s profits, it

“threatens America’s technological preeminence, its

economic well-being, and its national security.”

How great is the threat? Piracy, counterfeiting,

and theft cost the United States $200 billion a year,

Choate says, not including damage done to jobs,

innovation, and safety. (The book takes a largely

U.S.-centric view, although Choate acknowledges

the toll on other developed countries.) Hot Property

takes readers on a world tour of idea thievery:

Almost all music sales in Pakistan are of illegally

copied CDs. Cheap medicine flows across the bor-

der from Mexico, nearly 25% of it fake, contami-

nated, or even poisoned. That’s nothing compared to China, which Choate says

is “pursuing [a] national development strateg[y] based on the uncompensated,

unapproved stealing of other nations’ best ideas and technologies.”

Choate does a fine job explaining the evolution of intellectual-property

rights, a long-simmering issue that digital reproduction capabilities brought to

a public boil. Chapters dedicated to Germany, Japan, and China show how

each used – and abused – IP laws to catch up with cutting-edge technologies,

keep out external competition, and eventually dominate whole industries.

He is also persuasively critical of governments that sit by while their nation’s

intellectual wealth is plundered. Again the United States comes in for the

greatest scrutiny; the author cites case after case in which it failed to protect

the rights of companies and inventors. Only six employees in the Office of the

U.S. Trade Representative concentrate on intellectual property. The govern-

ment failed to pursue countless crimes for the sake of foreign relations. Indeed,

the country that fought hard for international laws that strengthen IP protec-

tions hasn’t filed a single case under those laws since 2000.

Unfortunately, Choate is less compelling when discussing solutions. Beyond

the obvious (hire more customs inspectors, FBI agents, and federal prosecutors;

educate the public) he suggests treating copyrights more like trademarks to

move knowledge into the public domain faster while protecting the creator’s

rights. Otherwise, he presents little more concrete than a demand that the gov-

ernment be resolute.“What is missing is the will of the U.S. political leaders to

confront those who are stealing U.S.-owned intellectual properties and with

them the future of the American people,” he pronounces. Yes, but are there

also opportunities to rethink the entire IP system to make it compatible with

new conditions? That would be innovative. And innovation, as Choate knows,

is always worth encouraging. – Eileen Roche

Blink: The Power of Thinking Without Thinking Malcolm Gladwell (Little, Brown, 2005)

We’re taught to be skeptical of first impres-sions, but journalist Gladwell argues thatthose split-second summations are wiserthan we know. Research has shown howstudying a subject in-depth can introduceextraneous information. That informationthen crowds out factors that our uncon-scious mind had pegged as key at the start.Sometimes the unconscious gets the keyfactors wrong, as with ethnic stereotyping,but Gladwell insists we’re better off teach-ing the brain to screen out these mistakesthan dismissing our instincts. This superbbook also offers insights on how serviceproviders can relate better to their clients.

China, Inc.: How the Rise of the Next Superpower Challenges Americaand the World Ted C. Fishman (Scribner, 2005)

You won’t find a more engagingly bullishbrief on China’s economic future. Fishman,a former commodities trader, explains howChina’s disciplined mastery of manufactur-ing has made it the Wal-Mart of world econ-omies, forcing everyone to respond to itslow-cost pressures. And with Chinese stu-dents and companies eagerly moving upto high tech, the country may soon com-pete and innovate along the entire valuechain. But you’ll have to go elsewhere foran in-depth look at the nation’s precariouspolitical and ecological situations.

Brand Sense: Build Powerful Brandsthrough Touch, Taste, Smell, Sight,and Sound Martin Lindstrom (Free Press, 2005)

The eyes are the windows to the pockets,marketers have long assumed, and so theyemphasize visual cues when packagingand promoting products. But Lindstrom,a consultant, urges companies to appeal to all the senses – especially when target-ing younger consumers, who have moresensory acuity then their elders. Smell, forexample, has a powerful influence on theunconscious, as McDonald’s discoveredwhen customers intrigued by its healthiermenu items were put off by the restaurants’continued oily odor. – John T. Landry

26 harvard business review

TLFeBOOK

haynesboone.com

We see no reason to behave like other law firms.

In 1970,

we set out to

build a law firm

unlike all others.

One that questions

the status quo.

Our goal?

To create smarter

ways to serve

our clients.

So far, so good.

Setting precedent.

haynesboone

Aus

tin

Dal

las

For

t Wor

th

Hou

ston

Mex

ico

City

N

ew Y

ork

Ric

hard

son

San

Ant

onio

W

ashi

ngto

n, D

.C.

© 2004 Haynes and Boone, LLP

TLFeBOOK

Safety bung courtesy of Justrite Manufacturing Company L.L.C. © 2004 - 2005 Factory Mutual Insurance Company. All rights reserved.

TLFeBOOK

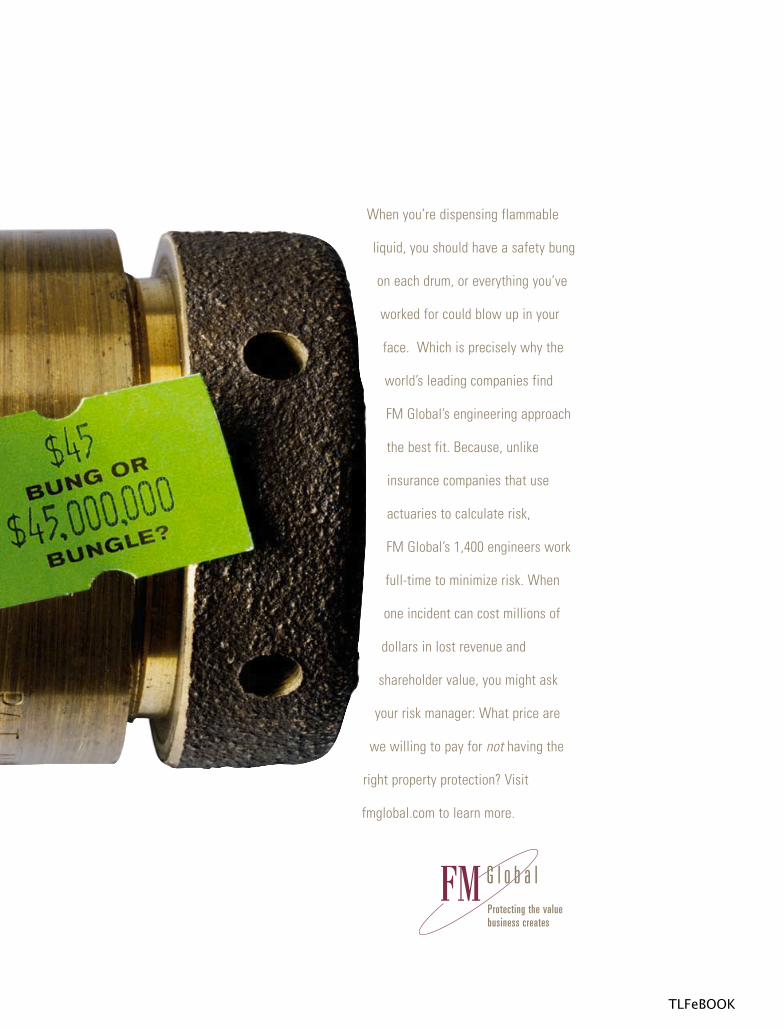

When you’re dispensing flammable

liquid, you should have a safety bung

on each drum, or everything you’ve

worked for could blow up in your

face. Which is precisely why the

world’s leading companies find

FM Global’s engineering approach

the best fit. Because, unlike

insurance companies that use

actuaries to calculate risk,

FM Global’s 1,400 engineers work

full-time to minimize risk. When

one incident can cost millions of

dollars in lost revenue and

shareholder value, you might ask

your risk manager: What price are

we willing to pay for not having the

right property protection? Visit

fmglobal.com to learn more.

Protecting the valuebusiness creates

TLFeBOOK

WI

NN

ER

S2

00

4

april 2005 31

THEODORE LEVITT. Henry Mintzberg. Abraham Zaleznik.

Michael E. Porter. Rosabeth Moss Kanter. Robert H. Hayes

and William J. Abernathy. John J. Gabarro and John P. Kotter.

Gary Hamel and C.K. Prahalad. John Seely Brown. Charles

Handy. John Hagel III and Marc Singer. All of these world-class

thinkers – and dozens more – have been singled out in the

past for McKinsey Awards. Harvard Business Review assembles

a distinguished group of judges from business, academia, and

consulting to evaluate every article the magazine has pub-

lished in the past year and select its two most significant. This

year’s winners are no exception to the tradition of excellence

in thought-provoking management theory.

T O L E A R N W H O T H I S Y E A R ’ S W I N N E R S A R E , T U R N T H E P A G E .

RECOGNIZING EXCELLENCE IN MANAGEMENT THINKING

T H E 4 6 T H A N N U A L

McKinseyAwards

][

TLFeBOOK

WI

NN

ER

S2

00

4

Harvard Business Review is pleased to

announce that Peter F. Drucker, the author

of “What Makes an Effective Executive,”

and Ken Dychtwald,Tamara Erickson, and

Bob Morison, the authors of “It’s Time to

Retire Retirement,” have tied for the first-

place 2004 McKinsey Award. The second-

place winner is Hau L. Lee for “The Triple-A

Supply Chain.”

Since 1959, the McKinsey Foundation

for Management Research has presented

awards recognizing the two best articles

published each year in Harvard Business

Review. The awards, judged by an indepen-

dent panel, commend outstanding works

that are likely to have a major influence

on executives worldwide.

32 harvard business review

What Makes an Effective ExecutivePeter F. Drucker

June 2004

Peter Drucker’s latest article for Harvard Business Review – and his seventhMcKinsey Award winner – ponders a mystery. Effective leaders come in all shapes and sizes. They may be charismatic or dull, number crunchers or visionaries, generous or tightfisted. But none of those traits necessarilyexplains leaders’ success. What does? According to Drucker, effective execu-tives all follow the same eight practices. Among them: Focus on oppor-tunities rather than problems. Run productive meetings. Think “we” ratherthan “I.” Take responsibility. In this concise and wonderfully written article,Drucker distills the lessons of his 65-year academic and consulting careerinto an indispensable guide from which managers and professionals at alllevels, and in all industries, can learn.

Peter F. Drucker is the Marie Rankin Clarke Professor of Social Science andManagement at the Peter F. Drucker and Masatoshi Ito Graduate School of Management at Claremont Graduate University in Claremont, California.He has written nearly two dozen articles for HBR.

F I R S T - P L A C E W I N N E R S[RECOGNIZING EXCELLENCE IN MANAGEMENT THINKING

T H E 4 6 T H A N N U A L

McKinseyAwards T I E

[ ]

TLFeBOOK

april 2005 33

It’s Time to Retire RetirementKen Dychtwald,Tamara Erickson,and Bob Morison

March 2004

Within half a dozen years, baby boomers – some 76 million people, morethan a quarter of all Americans – will start hitting their midsixties andcontemplate retirement. And why not? Long-standing human resourcepractice is to invest heavily in youth and push out older workers. But thismust change – and so must public policy – or companies will find them-selves running off a demographic cliff as baby boomers age.That’s theurgent message of this timely article, the result of a yearlong study of thebusiness implications of population change. Workplace environments;management styles; hiring, training, and promotion practices; outsourcing;and the use of part-time and contingent workers – nearly every aspect of the people side of running a business – will be affected by the agingworkforce. And companies don’t just face a shortage of labor as boomersleave. Skills, knowledge, experience, and relationships walk out the doorevery time somebody retires. Companies must gain the loyalty of olderworkers, the authors argue.They offer innovative recommendations forcreating a more flexible approach to retirement that allows people tocontinue contributing well into their sixties and seventies.

Ken Dychtwald is the founding president and CEO of Age Wave, a SanFrancisco–based consulting firm focused on the maturing marketplace andworkforce. Tamara Erickson is the executive officer and a board member,and Bob Morison is an executive vice president and the director of research,at the Concours Group, a management consulting firm based in Kingwood,Texas.They are all coauthors of a book about the impact of demographicshifts on the workplace forthcoming from the Harvard Business School Press in 2006.

The Triple-A Supply ChainHau L.Lee

October 2004

A strong supply chain is a strategic mandate for nearly every com-pany today. But many firms build their supply chain improvementson a false equation: faster plus cheaper equals competitive advan-tage. In fact, supply chains that focus on speed and costs tend todeteriorate over time.That’s the surprising insight of Hau L. Lee’sauthoritative article, based on his 15 years of studying the supplychains of more than 60 companies. Lee shows it’s the businessesthat create triple-A supply chains – those that are agile, adaptable,and aligned – that get ahead of their rivals.This article offers a rigor-ous look at the changes transforming modern supply chain man-agement, the best practices of triple-A leaders, and the steps compa-nies can take to build their own twenty-first-century supply chains.

Hau L. Lee is the Thoma Professor of Operations, Information, andTechnology at the Stanford Graduate School of Business in Stanford,California, and codirector of the Stanford Global Supply Chain Man-agement Forum. He is coeditor (with Terry P. Harrison and John J.Neale) of The Practice of Supply Chain Management:WhereTheory and Application Converge (Springer, 2003).

F I R S T - P L A C E W I N N E R S

T I E

]

S E C O N D - P L A C E W I N N E R

TLFeBOOK

2 0 0 4HBR wishes to thank this year’s esteemed panel of judges for all their work on behalf of the 2004 awards.

JU

DG

ES

34 harvard business review

Gurcharan DasAuthor Former Chief ExecutiveOfficerProcter & Gamble IndiaNew Delhi, India