Why Focus? A Study Of Intra-Industry Focus Effects

44

University of Pennsylvania University of Pennsylvania ScholarlyCommons ScholarlyCommons Management Papers Wharton Faculty Research 6-2003 Why Focus? A Study Of Intra-Industry Focus Effects Why Focus? A Study Of Intra-Industry Focus Effects Nicolaj Siggelkow University of Pennsylvania Follow this and additional works at: https://repository.upenn.edu/mgmt_papers Part of the Business Administration, Management, and Operations Commons Recommended Citation Recommended Citation Siggelkow, N. (2003). Why Focus? A Study Of Intra-Industry Focus Effects. The Journal of Industrial Economics, 51 (2), 121-150. http://dx.doi.org/10.1111/1467-6451.00195 This paper is posted at ScholarlyCommons. https://repository.upenn.edu/mgmt_papers/50 For more information, please contact [email protected].

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Why Focus? A Study Of Intra-Industry Focus Effects

University of Pennsylvania University of Pennsylvania

ScholarlyCommons ScholarlyCommons

Management Papers Wharton Faculty Research

6-2003

Why Focus? A Study Of Intra-Industry Focus Effects Why Focus? A Study Of Intra-Industry Focus Effects

Nicolaj Siggelkow University of Pennsylvania

Follow this and additional works at: https://repository.upenn.edu/mgmt_papers

Part of the Business Administration, Management, and Operations Commons

Recommended Citation Recommended Citation Siggelkow, N. (2003). Why Focus? A Study Of Intra-Industry Focus Effects. The Journal of Industrial Economics, 51 (2), 121-150. http://dx.doi.org/10.1111/1467-6451.00195

This paper is posted at ScholarlyCommons. https://repository.upenn.edu/mgmt_papers/50 For more information, please contact [email protected].

Why Focus? A Study Of Intra-Industry Focus Effects Why Focus? A Study Of Intra-Industry Focus Effects

Abstract Abstract In an intra-industry setting, firm-focus is found to be positively correlated with the ability of firms to produce high-value products, while the overall effect of focus on firm performance is negative due to missed demand externalities generated by a broad product offering. In particular, it is shown that U.S. mutual funds that belong to more focused fund providers outperform similar funds offered by more diversified providers. An explanation based on alignment among a provider's activities is consistent with this result. Cash inflows into fund providers—a measure related to fund provider profitability—is, however, negatively correlated with focus in fund offerings.

Disciplines Disciplines Business Administration, Management, and Operations

This journal article is available at ScholarlyCommons: https://repository.upenn.edu/mgmt_papers/50

Why Focus?A Study of Intra-Industry Focus Effects

Nicolaj Siggelkow

Management DepartmentWharton School

2017 Steinberg Hall – Dietrich HallUniversity of Pennsylvania

Philadelphia, PA 19104

[email protected]: (215) 573-7137

Abstract: While the effects of focus have been studied primarily in the context of diversificationacross industries, a study of focus within one industry can further our understanding of thedrivers that underlie focus effects. In particular, we study the effects of focus in the mutual fundindustry. We find that funds belonging to more focused fund families outperform similar funds inmore diversified families. Moreover, it is the relatedness among funds within a family, ratherthan the mere narrowness of product offering, which is responsible for this positive focus effect.Total cash inflows into fund families are, however, negatively affected by family focus. Sincefocus boosts the return of individual funds but reduces the scale of the total fund family, andthereby the fees that fund families receive, the interests of fund shareholders and the incentives ofthe owners of mutual fund families are potentially in conflict.

Draft Date: December 11, 1998

I would like to thank George Baker, Richard Caves, Pankaj Ghemawat, Tarun Khanna, CynthiaMontgomery, Michael Porter, Jan Rivkin, and Peter Tufano for helpful comments. All remaining errorsare mine. I am grateful to the Division of Research of the Harvard Business School for financial support.

1

Introduction

The relationship between diversification and the performance of firms has received

ample attention in both the industrial organization and finance literature (e.g., Wernerfelt

and Montgomery 1988, Lang and Stulz 1994). Almost exclusively, however, existing

research has studied firms which diversify across industries. In contrast, we explore the

effect of firm focus within an industry. Thus, we move the discussion and analysis of firm

focus from the corporate to the business unit level. This move allows us to explore

empirically the drivers of a focus effect. Moreover, by restricting the analysis to one

industry, we gain a deeper understanding of how firms operate within this industry,

allowing us to provide richer explanations of our findings.

In particular, we examine the effects of focus within the mutual fund industry over the

period 1985–1996. We explore whether a mutual fund that belongs to a focused fund

family has higher returns than similar funds that belong to more diversified families.

Furthermore, to analyze the drivers of the focus effect, we test whether a mutual fund

(e.g., a conservative corporate bond fund) benefits from belonging to a family which

specializes on that particular type of fund, or whether funds benefit from merely belonging

to a family with a narrow product portfolio, regardless of whether the family specializes

on that particular type of fund or not. In other words, we test whether the focus effect is

driven by relatedness or by narrowness of the product portfolio.

While the relationship between fund performance and family focus is of particular

interest to fund shareholders, the relationship between cash inflows into fund families and

family focus is of interest to the owners of the fund families (i.e., the owners of the

investment management company offering the funds). Therefore, to assess whether the

2

interests of fund shareholders and the incentives of fund family owners are aligned with

respect to family focus, we study how cash inflows into families are affected by the focus

of fund families.

The mutual fund industry is particularly attractive for a study of intra-industry focus

effects for three reasons. First, to disentangle the drivers of a focus effect it is essential to

have performance data at the sub-business unit level. In most industries, this data is

difficult to obtain.1 In the mutual fund industry, however, firms are required to disclose

the performance of each individual fund, i.e., each product in the offering of a mutual fund

family. Second, the performance measure is relatively precise in contrast to, for instance,

accounting returns for business units, or quality measures for individual products. Third,

all funds have basically the same access to the main input in this industry, i.e., securities

from which fund managers select their portfolios. Thus, in this setting, focus effects cannot

arise from some firms’ having cornered a part of the input market. Moreover, there are

strong forces at work to make this input market efficient. In sum, the mutual fund industry

is a particularly demanding setting for a test of the effects of focus.

Apart from its virtues as an arena to conduct a focus study, the mutual fund industry

deserves the attention not only of the finance profession, but also of strategy scholars,

industrial organization economists, and policy makers. Following enormous growth over

the past decade, by the end of 1996, the mutual fund industry managed more than $3.5

trillion in assets, making it the second largest financial intermediary in the U.S. behind

commercial banks. By 1996, more than 30 million households had invested in mutual

funds, either through an individual investment account or through a retirement account.

3

Thus, understanding the determinants of mutual fund performance and inquiring into

potential agency problems in this industry have become important undertakings.

This paper is organized as follows: Section I briefly reviews the related literature. In

Section II, we describe the organization of mutual fund families and discuss possible

sources of a focus effect in this industry. Section III describes a classification scheme for

mutual funds, and the focus-, performance-, and flow-measures which are used in the

analysis. Section IV reports the relationship between focus and fund performance and

analyzes the drivers of the focus effect. In Section V we explore the relationship between

focus and cash flows into fund families. Section VI concludes.

I. Brief literature review

The literature on diversification is so voluminous that even a brief review would

require an extraordinary amount of space. As a result, the following overview is at best

impressionistic.

Most of the industrial organization literature on diversification analyzes the

relationship between the performance of firms and a general, one-dimensional measure of

diversification. Studies use Herfindahl-like measures (e.g., Montgomery 1985, Scherer and

Ravenscraft 1987), entropy measures (e.g., Palepu 1985), or measures based on a

concentric index introduced by Caves et al. (1980) which takes into account the

relatedness among business units (e.g., Montgomery and Wernerfelt 1988). These studies

find either a neutral or a slightly negative relationship between the degree of diversification

and performance (for a survey, see Montgomery 1994).

4

Within the industrial organization literature, the study closest in structure to the one

presented in this paper is conducted by Lichtenberg (1992), who tests for the effect of

diversification on plant productivity. Lichtenberg finds that the larger the number of

industries in which a parent firm operates, the lower the productivity of its plants (holding

constant the number of parent-firm plants).

With respect to diversification, the finance literature has analyzed the impact of

acquisition and divestitures on firm performance. For instance, Morck, Shleifer, and

Vishny (1990) find that in the 1980s more bidders in related acquisitions had positive

returns than bidders in unrelated acquisitions. Similarly, Comment and Jarrell (1995) and

John and Ofek (1995) find that divesting unrelated divisions leads to increased

performance, while Daley, Mehotra, and Sivakumar (1997) find that cross-industry

spinoffs create more value than own-industry spinoffs.2

Given these results, it is natural to ask why focus should yield higher returns than

broad diversification. Explanations can be divided into two groups, using as a criterion

whether the proposed benefit accrues only to units the firm is focusing on (but not to

“lone stragglers” within the firm), or whether the benefit accrues to all units. Explanations

of the first kind are based on arguments of “relatedness” whereas explanations of the

second kind are based on arguments of “narrowness.”

Explanations based on relatedness include the following: Montgomery (1985) argues

that broad diversification is associated with low market power in the individual markets in

which a firm operates. Thus, only units on which a firm is focusing (i.e., where a firm has

sufficient market share to exercise market power) should generate higher profitability.

5

A second reason is given by Montgomery and Wernerfelt (1988), who argue that as

firms employ excess capacity of less-than-perfectly marketable resources (Penrose 1959,

Teece 1982), the marginal return of these resources declines (see also Schmalensee 1985).

Hence, we would expect a negative correlation between the distance of a business unit

from the core of the firm and the profitability of this business unit.

A third explanation emphasizes the fit and complementarities among various choices a

firm makes (Milgrom and Roberts 1990, 1995; Porter 1996). Focus can enable a firm to

align its activities in a very specific manner, thereby enabling it to generate either a better

product or a product at a lower cost than a less focused firm. Following this line of

reasoning, we will describe in Section II.2 some particular misalignments that can arise

when a mutual fund family attempts to satisfy too many customer demands with respect to

fund types.3

Explanations that are based on the narrowness of a firm’s strategy include Meyer,

Milgrom, and Roberts (1992), who show that a reduction of the number of businesses a

firm is engaged in can reduce influence costs within a firm.4 Using an agency-theoretic

set-up, Rotemberg and Saloner (1994) show how the narrowness of business strategies

can facilitate the provision of incentives. These explanations imply that even units within a

firm that do not belong to a group of businesses on which the firm is focusing would still

benefit from the narrowness of the firm’s strategy. By using variables that distinguish

between relatedness and narrowness, we will be able to shed some empirical light on the

impact of these two sources of a focus effect.

In the literature on mutual funds, the effect of focus on fund performance and on cash

inflows into families has not been studied previously. However, we benefit from the

6

substantial research analyzing the performance of mutual funds as compared to market

indices in constructing performance measures and identifying relevant control variables

(e.g., Jensen 1968, Blake, Elton, and Gruber 1992, Gruber 1996).

One further study that is related to the present analysis is conducted by Makadok and

Walker (1996). While these authors pursue a very different goal in their paper—to analyze

whether search behavior within a specified stochastic growth system affects fund family

exit in the money market mutual fund industry—they estimate a performance regression

which includes a focus-like variable. In their model, focus is measured by the number of

money market funds a family is offering. They find that fund performance and product

breadth are negatively correlated.

To motivate our choice of variables which measure focus in this industry, the

following section provides a brief description of the organization of mutual fund families

and describes possible sources of a focus effect.

II.1. The organization of mutual fund families

In broad terms, a mutual fund is a company that invests on behalf of individual

investors who share a similar investment goal. Each mutual fund consists of a board of

directors and the capital paid in by fund shareholders (see Figure 1). Formally, the board

of directors hires an investment management company to operate the fund.5 In practice,

however, the investment management company decides to create a new fund, assigns a

fund manager to the fund, and then selects a board of directors to monitor the handling of

the fund’s assets. Throughout the rest of the paper, we will refer to an investment

management company which offers more than one fund as a “mutual fund family.”

7

To state it in terms of the diversification literature, the mutual fund family corresponds

to a corporation, the fund managers to business unit presidents, and the shares in

individual funds to the products that the corporation offers.

< FIGURE 1 ABOUT HERE >

The investment management company itself is a publicly or privately held firm. As a

result, fund managers not only have a fiduciary duty vis-à-vis fund shareholders but are

also financially accountable to the owners of the investment management company. Thus,

an agency problem can arise, since the incentives of the fund family owners are not

necessarily congruent with the interests of the fund shareholders. Recent research has

started to explore empirically these potentially divergent interests. For instance, Tufano

and Sevick (1997) find that the composition of the fund board affects the level of fees

investment management companies charge funds for providing their services, while

Chevalier and Ellison (1997) find that fund managers increase the riskiness of their fund

portfolios in the later months of the year if they have experienced low performance early in

the year.6

II.2. Possible sources of a focus effect

What are potential sources of a focus effect in the mutual fund industry? In particular,

what effects could focus have on fund performance (an internal “production” effect) and

on cash inflows (an external “demand” effect)? We will consider the production effect

first.

8

One possible way for family focus to influence fund performance is via the alignment

of investment styles and fund types. The investment and research styles that guide the

selection of securities for a mutual fund portfolio fall into very different categories, e.g.,

fundamental investing and investing using quantitative analysis. While the former involves

in-depth analysis of each individual security the fund manager decides to invest in, the

latter involves strict quantitative, often computerized, screening and analysis of security

prices. Each family acquires a distinctive investment style that permeates the entire

institution.7 For instance, Fidelity is imbued with a fundamental investment style, as it has

been preached and practiced by Edward Johnson II, Fidelity’s owner and CEO, and by

Peter Lynch, Fidelity’s most prominent former fund manager. Each style, in turn, has many

ramifications for how investment analysis is conducted, how performance is evaluated, and

how internal reputations are created.

The investment culture within a fund family can influence the focus-profitability

relationship, because different types of funds can warrant different investment styles. A

family offering a broad array of diverse funds may encounter difficulties either because

investment styles and fund characteristics match poorly, or because the family tries to

accommodate different styles within the same investment management company. For

instance, Fidelity has established itself as a “playground” for equity managers.

Fundamental research is encouraged, and fund managers pride themselves on being able to

find good bargains and to trade quickly in order to earn higher returns than the market. It

was these “gunslingers” who were held in highest esteem within the Fidelity hierarchy. As

a result, Fidelity’s bond fund managers tried to emulate this style. There was, however,

much less room for this kind of investment style in the fixed-income arena, where in

9

general low expenses, and not clever security selections, drive returns. The problems

caused by this mismatch climaxed in 1994, when aggressive investing in the U.S. bond

market and moves into risky derivatives and Latin American debt led to huge losses. A

New York Times article covering this incidence concluded: “The Fidelity story also reveals

some dirty little secrets that the mutual fund industry, busy selling Americans on the idea

of one-stop shopping, would rather investors not know: the very things that make a

company good at managing some kinds of investments may make them bad at running

others” (Eaton 1995).

A further example of internal problems generated by frictions between different

investment and research styles comes from a large Canadian mutual fund provider.8 Funds

that invest mainly in blue-chip stocks and funds that invest in small-cap stocks differ

greatly in the amount of additional analysis that a fund manager has to undertake. Blue-

chip stocks are already under such scrutiny by investment bank- and broker analysts that

often very little additional analysis is required. On the other hand, for small-cap stock

funds, fundamental analysis by the fund managers themselves, which might include road

trips, is needed. In the case of this Canadian mutual fund family, the Director of Canadian

Investments was managing a blue-chip stock fund and oversaw a small-cap stock fund.

She could not understand the high expenses incurred from road trips of the small-cap

stock fund managers and demanded that expenses be cut. As a result, research was

hindered and returns suffered.

In Section IV, we will test for the internal effects of focus by analyzing the relationship

between fund performance and the degree of fund family focus.

10

While the internal effect of focus corresponds to returns to specialization in the

“production” of particular types of mutual funds, the external, or demand, effect relates to

possible benefits or detriments of focus in the marketplace. For instance, fund families that

offer only a few categories of funds may have a clear corporate image in the minds of

customers. They stand for particular types of funds, and whenever the need arises for

investors to allocate assets to these types of funds, the investors know where to turn.

Contrary to this, a family which offers a broad variety of funds may attract assets because

investors might find it convenient to use only one fund family for all their investment

needs. Clearly, there exist many factors besides focus that influence the purchase decisions

of investors. As a result, our goal is not to explain consumer behavior. Rather, we explore

whether one possible factor influencing the purchase decision, i.e., focus, has an impact on

the cash inflows into fund families. Moreover, the main reason for studying the

relationship between focus and total inflows into families is to reveal the incentives family

owners face with respect to focus. Since costs of operating funds are fairly fixed and fund

management fees are proportional to assets under management, a main concern of fund

family owners is to increase fund inflows.9

III.1. Different types of funds

As discussed in the previous section, a fund family that focuses on particular fund

categories is able to align its activities and to design its policies and organizational

structure more appropriately than a family which offers a wide variety of funds. Thus, a

useful focus measure can be based on the various types of funds offered by a fund family.10

In general, funds fall into three categories: money market funds, equity funds, and bond

11

funds. Since differences in investment styles are particularly acute among and between

bond and equity funds, this study concentrates on these two types of funds.

We employ a classification scheme developed by Morningstar, one of the leading

mutual fund rating agencies, which categorizes funds using the characteristics of the

security portfolio held by the funds. For instance, a domestic equity fund is classified as

“Large Value” if the mean market capitalization of the companies in its portfolio is greater

than $5 billion and the mean price-to-earnings ratio of the portfolio is significantly below

the P/E ratio of the S&P 500. Domestic bond funds are classified along the dimensions of

average maturity and average risk rating (for exact definitions see Appendix 1).

International funds are classified by the countries of which the fund is holding securities,

e.g., “Japan fund.” In total, there are 44 Morningstar categories (see Appendix 2). Please

note that whenever the term “categories” is used in this paper, we are referring to these

Morningstar categories. Since index funds alleviate the problems of misalignments as

described in the previous section, we introduce a further “index fund” category for the

sole purpose of computing focus measures (see next section).11 The performance of an

index fund is still compared, however, to its peers as defined by its Morningstar category.

III.2. Focus, performance, and flow measures

Given the discussion in Section II.2 on internal focus effects, we would expect that

funds which belong to focused families perform better than funds which belong to more

diversified fund families. Moreover, we want to explore whether any potential focus effect

is driven by “relatedness” or by “narrowness.” We would receive evidence for a

relatedness effect if we were to find that funds which belong to categories that a fund

12

family is specializing in are performing better than funds which do not belong to such a

category. Likewise, a negative effect of the breadth of product offering on fund

performance would provide evidence of a narrowness effect. In other words, we want to

distinguish between benefits for a fund that arise from being a fund in a family which offers

many similar funds, and benefits for a fund that arise from being a fund in a family that

offers funds in only a few categories (regardless of whether the fund belongs to a category

the family specializes in).

Thus, in the first step, we will test for the effect of focus by analyzing the following

relationship:

“fund performance” = ƒ(“family focus,” other controls)

In the second step, we will attempt to shed light on the sources of a potential focus

effect by exploring the relationship:

“fund performance” = ƒ(“narrowness measure,” “relatedness measure,” other controls)

Lastly, to explore the incentives of fund family owners with respect to focus, we will

analyze the relationship between family focus and cash inflows into fund families:

“flows into fund families” = ƒ(“family focus,” other controls)

In the following paragraphs, we will define more precisely the measures of family focus,

relatedness, narrowness, fund performance, and cash inflows.

13

III.2.1. Measures of focus, relatedness, and narrowness

We follow the diversification literature in employing a Herfindahl-like measure as an

indicator of family focus. For family k at time t we define

2

∑

=

jkt ttimeatkfamilyofassetstotal

ttimeatjcategoryinkfamilyofassetsfocus

where the sum is taken over all categories j of family k at time t.

In our exploration of the sources of the focus effect, we want to include measures of

relatedness and narrowness rather than an overall focus measure. For the relatedness

measure, we construct a variable for each fund that measures the degree to which its fund

family has focused on similar funds. Let fund i be in category j and a member of family k at

time t. Then variable relatedit is defined as: assets of family k in category j at time t,

divided by total assets of family k at time t. One should note that this relatedness measure

is not the same for all funds within a family (unless all the funds happen to be in the same

category). Thus, this measure allows us to differentiate between funds that belong to a

family’s core group(s) and funds that are lone stragglers within a family.

As narrowness-of-strategy measure we use the number of categories a family is

engaged in at time t (variable narrowkt). By including both relatedit and narrowkt in the

later performance regressions, we will be able to distinguish between a narrowness effect

from which all funds within a family benefit, and a relatedness benefit, which accrues only

to funds that belong to a core group of a family.

14

III.2.2. Measures of fund performance

Since no single “perfect” performance measure for mutual funds exists—and for the

sake of robustness—we construct four different performance measures. All measures have

as their starting point the total annual return of each fund which includes dividends paid.

In order to make total returns comparable across funds, we adjust total returns to

account for the fact that some funds charge a sales fee (called a “load”).12 We will refer to

these returns as “adjusted total returns.” Morningstar also reports the average returns for

each of its 44 categories. These averages are computed over the entire population

Morningstar tracks (in total over 7,500 funds, comprising essentially all industry

participants).

For the first performance measure used in the analysis, we subtract from each fund’s

adjusted return the mean of its category. The resulting variable is called dcret (difference

from category return).

Second, since the total return is net of expenses charged to the fund, we measure the

“gross return” achieved by a fund’s security portfolio by adding the expense ratio to the

total annual return.13 Subtracting from these gross returns the respective mean category

performance and the mean category expense ratio yields variable dgret (difference in gross

returns).

The third performance measure is based on “Jensen’s alpha,” which is derived from the

standard capital asset pricing model (Jensen 1968). By this measure, the excess return of

fund i in period t is given by:

alphait = (Rit – Rft) – βi(Rmt – Rft) (1)

15

where Rit is the total return of fund i, Rft the risk-free rate (90-day T-Bill), and Rmt the

return of an appropriate market benchmark.

The risk measure βi, in turn, is computed by running for each fund the standard CAPM

regression: 14

(Rit – Rft) = αi + βi(Rmt – Rft) (2)

As Elton et al. (1993) point out, the choice of an appropriate market benchmark is

crucial in the computation of Jensen’s alpha (see below). Consequently, rather than

assigning to each equity fund the S&P 500 index as benchmark and to each bond fund a

broad bond index, we assign to each category the index that is used by Morningstar to

benchmark the performance of that particular category (see Appendix 2).

Lastly, the fourth performance variable, malpha, is an excess return measure which

uses monthly performance data obtained from Morningstar’s Principia Plus database.

Whereas in the construction of alpha we implicitly assumed a constant βi over time, we

are now able to relax this assumption. The variable malpha is based on multi-index models

suggested by Gruber (1996), and Blake, Elton, Gruber (1993). To understand the

underlying idea of multi-index models, assume that over a period of time small-cap stocks

outperform large-cap stocks. Then, using a total market index to compute beta would

result in a positive alpha for a fund that held small-cap stocks. The question is, should we

attribute this excess return to the skill of the fund manager, or not? In most cases, the

choice to invest in small-cap stocks was not made by the fund manager, but the manager

was charged to manage a small-cap stock fund. Hence, a more appropriate market

benchmark for judging the manager’s performance is a small-cap index. This is the

rationale for matching funds to different market benchmarks in the computation of alpha

16

above. To control for the fact that many funds invest in more than one type of security,

Gruber (1996) suggests to regress the returns of funds on several indices and to compute a

set of relevant betas. More precisely, for domestic equity funds we run the following

regression:15

(Rit – Rft) = αi + β1i(Rmt – Rft) + β2i(Rst – Rlt) + β3i(Rgt – Rvt) + β4i(Rdt – Rft)(3)

where Rit = the return of fund i in month t

Rft = the 30-day T-Bill rate in month t

Rmt = the return on the S&P 500 index in month t

Rst = the return on a small-cap portfolio in month t (average return on the Wilshire Small CapIndex and the Wilshire Small Value Index)

Rlt = the return on a large-cap portfolio in month t (average return on the Wilshire Large CapIndex and the Wilshire Large Value Index)

Rgt = the return on a growth portfolio in month t (average return on the Wilshire Small Cap,Mid Cap, and Large Cap Growth Indices)

Rvt = the return on a value portfolio in month t (average return on the Wilshire Small Cap,Mid Cap, and Large Cap Value Indices)

Rdt = the return on the Lehman Brothers (LB) Aggregate Bond Index in month t

We then compute our new excess return measure as

malphait = (Rit – Rft) – β1i(Rmt – Rft) – β2i(Rst – Rlt) – β3i(Rgt – Rvt) – β4i(Rdt – Rft) (4)

To take into account that betas might change over time, regression (3) is run using

three years of (rolling) monthly performance data. Thus, to obtain malpha for fund i in

month t, we use the performance of fund i in the 35 months prior to and including month t

to find β1i, … , β4i from (3). These betas are then used in (4) to compute malpha for

month t. Lastly, the malpha’s are annualized over each calendar year.

For domestic bond funds, we employ a six-index model suggested by Blake, Elton,

and Gruber (1993):

17

(Rit – Rft) = αi + β1i(Rgt – Rft) + β2i(Rlgt – Rft) + β3i(Rct – Rft)

+ β4i(Rlct – Rft) + β5i(Rmot – Rft) + β6i(Rhyt – Rft) (5)

where Rit = the return of fund i in month t

Rft = the 30-day T-Bill rate in month t

Rgt = the return on the LB Intermediate-Term Government Bond Index in month t

Rlgt = the return on the LB Long-Term Government Bond Index in month t

Rct = the return on the LB Intermediate-Term Corporate Bond Index in month t

Rlct = the return on the LB Long-Term Corporate Bond Index in month t

Rmot = the return on the LB Mortgage Backed Bond Index in month t

Rhyt = the return on the First Boston High Yield Bond Index in month t

We then compute our new excess return measure for bond funds as

malphait = (Rit – Rft) – β1i(Rgt – Rft) – β2i(Rlgt – Rft) – β3i(Rct – Rft)

– β4i(Rlct – Rft) – β5i(Rmot – Rft) – β6i(Rhyt – Rft) (6)

Lastly, we need a measure of cash flows into each fund family. Cash flows at the level

of the fund can be estimated by the difference in fund size after adjusting for appreciation

(or depreciation) of the existing asset stock. Cash flows at the level of the family are then

obtained by summing over all funds within one family:

famflowkt = Σnetassit – (1 + totretit)netassi(t-1) (7)

where netassit are the total assets of fund i at the end of year t, totretit is the total

return of fund i in year t, and the sum is taken over all funds i within family k.

III.3. Data and methods

Data was collected on all bond and equity funds covered by Morningstar in its

Morningstar Mutual Funds publication as of December 1996. The database consists of a

18

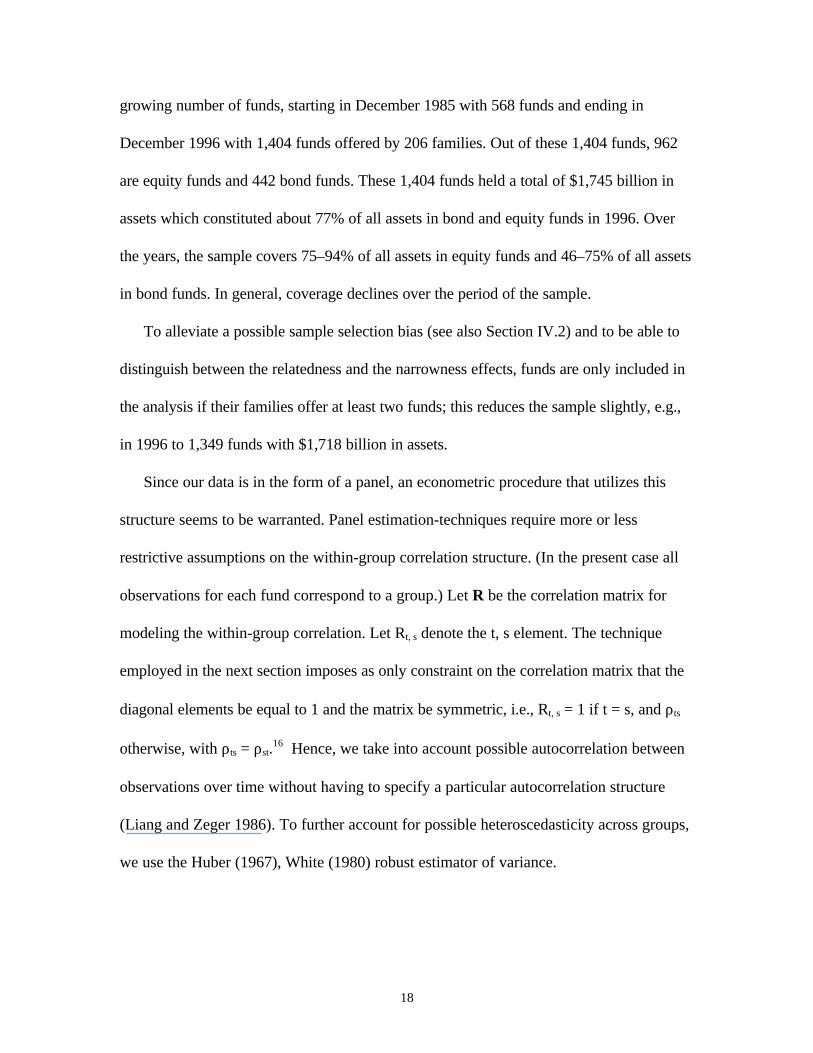

growing number of funds, starting in December 1985 with 568 funds and ending in

December 1996 with 1,404 funds offered by 206 families. Out of these 1,404 funds, 962

are equity funds and 442 bond funds. These 1,404 funds held a total of $1,745 billion in

assets which constituted about 77% of all assets in bond and equity funds in 1996. Over

the years, the sample covers 75–94% of all assets in equity funds and 46–75% of all assets

in bond funds. In general, coverage declines over the period of the sample.

To alleviate a possible sample selection bias (see also Section IV.2) and to be able to

distinguish between the relatedness and the narrowness effects, funds are only included in

the analysis if their families offer at least two funds; this reduces the sample slightly, e.g.,

in 1996 to 1,349 funds with $1,718 billion in assets.

Since our data is in the form of a panel, an econometric procedure that utilizes this

structure seems to be warranted. Panel estimation-techniques require more or less

restrictive assumptions on the within-group correlation structure. (In the present case all

observations for each fund correspond to a group.) Let R be the correlation matrix for

modeling the within-group correlation. Let Rt, s denote the t, s element. The technique

employed in the next section imposes as only constraint on the correlation matrix that the

diagonal elements be equal to 1 and the matrix be symmetric, i.e., Rt, s = 1 if t = s, and ρts

otherwise, with ρts = ρst.16 Hence, we take into account possible autocorrelation between

observations over time without having to specify a particular autocorrelation structure

(Liang and Zeger 1986). To further account for possible heteroscedasticity across groups,

we use the Huber (1967), White (1980) robust estimator of variance.

19

IV.1. Relationship between performance and focus

In exploring the effect of family focus on fund performance, we will proceed in two

steps. In the first step, following the diversification literature, we will test whether overall

family focus has an impact on fund performance. In the second step, we will analyze

whether it is relatedness or narrowness which drives the focus effect. Studies which have

tested whether funds outperform passive market indices suggest to include variables which

control for differences in (portfolio) turnover, expense ratio, sales loads, and fund size.

Accordingly, we include variables diffturn, which measures the difference between a

fund’s turnover and the average turnover of its category, variable diffexpense, which

measures the difference between a fund’s expense ratio and the average expense ratio of

its category, and variable loaddum, a dummy equal to one if the fund charged a front- or a

back-end load. Since the measures of focus and relatedness both involve non-linear size

terms, we include a fairly flexible size specification in our model to avoid misspecification.

As a result, rather than including, for instance, the logarithm of size, which would force

upon the estimation decreasing (or increasing) returns over the entire range of values, we

include linear, quadratic, and cubic terms of fund- and family size.

Further variables at the level of the fund include the age and the square of the age of

the fund, the market share of the fund within its category, and the standard deviation of its

monthly returns over the year. Given potential sample selection bias in the data (see

discussion in Section IV.2), we would expect a negative coefficient on the linear age term.

The fund’s market share was included, because on one hand a manager with a large share

within a category might receive preferential treatment by industry analysts, while on the

20

other hand the manager might find it increasingly more difficult to find attractive

securities.

Further control variables at the level of the family include the sum of assets of the

family within the category and the number of funds of the family within the category (of

the particular fund). Families which have large categories might be able to avoid the

problems of misalignment as discussed in Section II.2.

Lastly, we include the number of funds that exist in the category as a measure of

general competition, for instance, for mis-priced securities.17

Thus, our regression model is specified as follows:

Performance of fund i belonging to family k and category j at time t =

constant

+ α1 focus [t – 1] Herfindahl index of family k

+ α 2 diffturnover [t] (turnover of i) – (mean turnover of category j)

+ α 3 diffexpense [t] (expense ratio of i) – (mean expense ratio of cat. j)

+ α 4 loaddum [t] dummy = 1 when i had a load in 1996

+ α 5 age [t] age of fund i

+ α 6 age2 [t] square of fund i’s age

+ α 7 assets [t – 1] net assets of fund i

+ α 8 assets2 [t – 1] squared net assets of fund i

+ α 9 assets3 [t – 1] cubed net assets of fund i

+ α 10 fund mshare [t – 1] market share of fund i in category j

+ α11 stdv [t] stdv of fund i’s monthly returns over year t

+ α 12 family assets [t – 1] net assets of family k

+ α 13 family assets2 [t – 1] squared net assets of family k

+ α 14 family assets3 [t – 1] cubed net assets of family k

+ α15 family assets in cat [t – 1] sum of assets of family k in category j

+ α 16 family funds in cat [t – 1] number of funds of family k in category j

+ α17 funds in cat [t] total number of funds in category j

where [t] means the variable is taken at the end of year t, and [t – 1] that the variable is takenat the end of year t – 1.

21

For results, see Table 1. The dependent variable in regression (1) is dcret, the

difference between the fund’s adjusted total returns and the average adjusted total returns

of its category. In regressions (2) – (4) we use dgret, alpha, and malpha as performance

measures. In all four regressions the (lagged) focus variable is positive and highly

significant. The p-value for the coefficient on the focus variable across the regressions is

0.006, 0.012, 0.027, and 0.002, respectively. The effect is not only statistically significant,

but economically relevant as well. Comparing families at the 20th and 80th percentile of the

focus measure, the coefficients imply a size of the effect of 43, 40, 61, and 59 basis points

per year.

< TABLE 1 ABOUT HERE >

Due to space constraints and our primary concern with the focus variable, we will

discuss the coefficients of the control variables only briefly. Turnover appears to have a

neutral effect on fund performance, while we find some evidence that higher expenses

decrease performance. The variable diffexpense is negative and strongly significant in

regression (4) and significantly less than one in regression (2). Recall that variable dgret

increases one-to-one with the expense ratio. Thus, a coefficient less than 1 on the

diffexpense variable in regression (2) implies that net performance suffers when expenses

are increased.

For the interpretation of the coefficient on the load dummy, we need to recall that

dcret is adjusted for sales loads, while the other three performance measures are not. The

22

general result is that the performance of funds (taking loads into account) is negatively

affected by sales loads.18

The market share of a fund appears to have a negative effect on performance. Using

the coefficient from regression (1) and comparing funds at the 20th and 80th percentile of

fund mshare, the effect is about 25 basis points.

Lastly we note that at least for regressions (3) and (4) there is a negative impact of the

number of funds within the category on fund performance.

Having documented the existence of a focus effect on fund performance, we will now

turn to the question of the sources of this focus effect. Is the focus effect driven by

relatedness or by narrowness? To provide an answer, we will use the above regression

model but replace the focus variable with the related and the narrow variables. Results of

this regression model can be found in Table 2. Again, for the sake of robustness, we use

all four different performance measures as independent variables.

<TABLE 2 ABOUT HERE>

The measure of relatedness is positive in all four regressions and significant at the 1%

level in regression (3), at the 5% level in regressions (1) and (2), and at the 10% level in

regression (4). In contrast, the measure of narrowness is insignificant in all four

regressions. Thus, the benefit of focus appears to accrue only to funds that belong to a

category of funds the fund family is concentrating on. Mere membership in a focused

family does not generate a performance benefit for a fund.

23

What is the magnitude of the relatedness effect? Comparing two funds at the 20th and

80th percentile of related in 1996, the effect is, depending on the performance measure, 30,

27, 62, and 25 basis points per year.

One objection to the results between performance and family focus could involve the

possible reverse direction of causality. Perhaps fund families which have poorly

performing funds start to diversify. There exists some evidence in the finance and

industrial organization literature that poorly performing firms start to diversify broadly

(Morck, Shleifer, and Vishny 1990, Lang and Stulz 1994) and that low-value mergers are

more likely to be undertaken by firms with poor prospects for increasing their profit

streams from their existing activities (You et al. 1986). To determine whether fund

families which perform poorly start to increase their product portfolio, we construct a new

variable, ∆focuskt, which measures the change in focus of family k between years t and t –

1, and regress it on various past average performance measures of families, controlling for

family size, average fund age, average flows into categories, and average expense levels

(see Section V. for definitions of variables at the family level). For all performance

measures the coefficient on the past performance variable is insignificant, thus throwing

doubt on the reverse-causality explanation in this case (detailed results available from the

author).

IV.2. Sample selection bias

We need to be concerned about the following possible sample selection bias:

Morningstar may cover in its publication only those small families (and funds) which are

successful. Since there exists a negative correlation between focus and family size, the

24

focus measure could pick up a size effect caused by the selection bias. Similarly, small

families might be covered less completely than large families. If only hot performing funds

of small families are covered, it could again induce a negative relationship between family

size and performance.

To alleviate this selection bias problem, linear and non-linear terms for both the size of

the fund and the size of the family are included in the performance regressions. An age

variable, which presumably picks up some of the selection bias effect as well, is also

included. Moreover, since lagged variables are used in the regression, the performance in

the first year of each new fund is excluded. Thus, first-year blips in performance, which

could have caused Morningstar to cover a fund, do not influence the results. In addition,

once Morningstar begins to cover a fund, it is not dropped very quickly.

Lastly, we exclude from the analysis all families that have only one fund (in year t).

Clearly, for these funds the focus measure would be equal to 1, yet the inclusion of these

funds could be driven by high past performance. We would potentially detect a very strong

focus effect for these funds (which truly might exist), but which might be overstated since

we do not include all other one-fund families with similarly high focus.

To see whether there exists a strong small family-size or fund-size effect in the data,

we compute the unconditional correlation coefficients between the four performance

variables and family- and fund size. While the correlation coefficients between fund size

and the performance measures are insignificant, the correlation coefficients between family

size and the performance measures are (weakly) significant. However, the correlation is

positive, i.e., the reverse of what we would expect in the presence of a strong sample bias

of the kind described above.19

25

V. The impact of focus on cash inflows at the family level

In the last section, we found that funds belonging to families which are focused have

higher returns, ceteris paribus, than funds belonging to broadly diversified families. Given

the intuitive—and empirically validated—positive relationship between past performance

and inflows at the fund level (e.g., Chevalier and Ellison 1997, Sirri and Tufano 1998) and

the fact that fund families’ payoffs are proportional to fund inflows, the question arises

why are all fund families not highly focused? To answer this question, we should note that

even though owners of fund families care about inflows into individual funds, they are

ultimately concerned with the total flows into all funds they are offering. Thus, to gauge

the incentives of family owners with respect to focus, we need to analyze how focus

affects total inflows into fund families.

With the help of the above-cited studies of the relationship between performance and

inflows at the fund level, we identify several relevant control variables. First of all, we

control for the size of the family. To allow for potential non-linearities we again include

linear, square, and cubic terms of the lagged net assets of the family.20 Second, we control

for the past performance of the funds in each family. For sake of robustness, we employ

several average performance measures. Whenever we average at the family level, we

weight by individual fund asset size. The first performance measure is the average of dcret.

The second performance measure is the average of malpha. A third and fourth

performance measure are the percentile ranks of each fund, where each fund was ranked

within its category using either adjusted total returns or malpha. These ranks were then

averaged over all funds within each family.

26

Following Sirri and Tufano (1998), who show that prior performance does not have a

linear effect on cash flows into individual funds, we include in some regressions not a

single family performance measure but rather piecewise ranks as defined by:

average low performancekt = Min(Rankkt , 0.2)

average medium performancekt = Min(0.6, Rankkt – average low performancekt)

average high performancekt = Rankkt – (average low performancekt + average

medium performancekt)

where Rankkt is the asset-weighted average of the percentile ranks of all funds within

family k in year t and ranking for each fund is conducted within the fund’s respective

category using either adjusted total returns or malpha.

These piecewise linear regressors pick up the relationship between flows and past

performance, contingent upon whether the family’s overall performance (as compared to

all other families) fell in the lowest quintile, in the middle 60%, or in the upper quintile. In

other words, these regressors allow us to estimate three different slope parameters for the

past-performance-flow relationship, depending on how well the family performed in the

previous year.

Next, we control for the average age of funds within each family. Again, there might

be a non-linear relationship, because new funds might receive a lot of marketing support

while very old funds have reputation effects which could help increase inflows. We further

control for the expenses charged, by including an average of the variable diffexpense. To

control for a potential dislike of investors for volatility, we include the average of the

funds’ standard deviation of monthly returns.

27

We include two further control variables which measure industry-wide effects. We

compute the total flows into each category, and weight the flows for each family by the

percentage of assets that the family has in each category. Thus, we control for sector

flows into particular categories, which may have been en vogue in a particular year.

Secondly, to assess how many competitors the funds of a family face within their

categories, we multiply the number of funds in each category by the percentage of assets

that the family has in each category.

There are possibly other family-specific variables which could influence the total cash

inflows into families, such as the amount spent on advertising. Unfortunately, such data is

difficult to obtain for the 151 families which we track over 13 years. To take into account

family-specific differences, we employ a fixed-effect regression model which controls for

(constant) family differences.

Thus, the regression we run is specified as follows:

Flows into fund family k at time t =

constant

+ α1 focus [t – 1] Herfindahl index of family k

+ α2 average performance [t – 1] average performance of funds in family k

{+ α2 average low performance [t – 1] for definition see above

+ α3 average medium performance [t – 1] for definition see above

+ α4 average high performance [t – 1] } for definition see above

+ α5 family assets [t – 1] net assets of family k

+ α6 family assets2 [t – 1] squared net assets of family k

+ α7 family assets3 [t – 1] cubed net assets of family k

+ α8 average age [t] average of age of all funds in family k

+ α9 average age2 [t] squared average of age

+ α10 average diffexpense [t] average of diffexpense of all funds in family k

+ α11 average stdv [t – 1] average of stdv of all funds in family k

+ α12 average category flow [t] average of inflows into categories

+ α13 average funds in cat [t] average of funds in cat

28

where we include either a single linear past performance measure or three piece-wise

linear past performance regressors, and all averages are asset-weighted.

For results of the cash flow regressions, see Table 3. Regressions (1) – (6) differ in the

way we control for past performance. In regression (1) the average past performance

measure is based on dcret, in regression (2) the measure is based on malpha, in

regressions (3) and (4) the measures are based on ranking using adjusted total returns, and

in regressions (5) and (6) the measures are based on ranking using malpha.

Across all six regressions we observe a negative and significant effect of family focus

on cash inflows into families. Moreover, the effect is substantial. Comparing two families

with a focus measure one standard deviation apart, regression (1), for instance, suggests

an effect of about $263 million more inflow for the less focused family—a large effect,

given that the mean inflow into families is $478 million. Thus, the owners of fund families

face strong incentives to increase the breadth of their product offering.

<TABLE 3 ABOUT HERE>

Given the results between individual fund performance and family focus, one may

point out that higher focus leads to better fund performance, which in turn should increase

inflows. To test the size of this indirect effect, we drop the past performance control

variable in regression (7), thereby attributing the positive externality of focus (on flows)

onto the focus measure. As can be seen in Table 3, the coefficient on the focus measure

remains basically unchanged. Thus, at the family level, the indirect negative effect of

diversification on cash inflows via reduced fund performance is only very small.

29

Using linear past performance measures, we see a positive, yet insignificant,

relationship between past family-wide performance and consequent cash inflow. The

piece-wise linear regressors allow us to paint a more differentiated picture. Similar to the

findings of Chevalier and Ellison (1997) and Sirri and Tufano (1998) at the fund level, we

find that at the family level, performance differences among very poor performing families

do not affect inflows. The surprising result is that among very well performing families

performance differences do not appear to affect inflows either. Only in the intermediate

range do performance differences play a role.

While the sector flows have a significant impact on inflows into families, differences in

expenses, volatility, and number of funds in the category do not affect inflows

significantly. Lastly, families with many young funds appear to gain extra inflows.

VI. Conclusion

This paper set out to analyze the effects of focus in an intra-industry setting. While

benefits of focus have been previously documented at the inter-industry level, the effects

of focus at the intra-industry level have not found much attention. Moreover, we

attempted to disentangle two different drivers of the focus effect: one based on relatedness

and one based on narrowness.

We find that the performance of a mutual fund improves with overall family focus, and

in particular with the fund family’s degree of focus on that fund’s category. Mere

narrowness does not suffice: funds that belong to focused families, yet are lone stragglers,

do not benefit with respect to performance from their membership in a focused family.

Thus, for the internal benefit of focus, relatedness matters. One explanation that is

30

consistent with these results, and consistent with field observations, is based upon fit

within a firm’s system of choices. A focused fund family is able to configure its activities,

to design its organizational structure, and to assemble its resources more appropriately

than a family that offers a broad array of different funds.

With respect to inflows into fund families—a measure of particular interest to fund

family owners—we observe a negative effect of focus. The finding that family focus

affects performance positively while reducing total inflows points towards a divergence of

interests between the owners of fund families and fund shareholders. Since higher fund

performance accrues to fund shareholders, shareholders would benefit from focused

families. On the other hand, the owners of fund families, who profit from larger inflows,

have an incentive to broaden a family’s offering. This finding resonates with research

examining the effects of direct marketing charges (12b-1 fees) levied by funds. Fund

managers argue that the additional business generated by advertising yields scale

economies which ultimately benefit the existing fund shareholders. Empirical research,

however, indicates that these charges are a dead-weight cost borne by shareholders, i.e.,

do not benefit existing shareholders (e.g., Ferris and Chance 1987).

In sum, we find that fund shareholders and the owners of fund families may arrive at

opposing answers to the question whether to focus. The results of the performance

regressions indicate that housing different production technologies within the same

organization can be difficult and lead to inferior product output. At the same time, in an

environment in which size confers profitability, and where focus restricts size, focus can be

detrimental from the point of view of the firm’s owners.

31

Figure 1: Organization of Mutual Fund Families

Fund Family (investment management company)

fund shareholders

owners/shareholdersFund

ManagerFund

ManagerFund

Manager

Mutual Fund 1

Board of Directors

Mutual Fund 2

Board of Directors

Mutual Fund 3

Board of Directors

32

Table 1: The effect of family focus on fund performance(t-values below coefficients)

(1) (2) (3) (4)performance measure dcret dgret alpha malpha

focus 1.356 1.233 1.906 1.8412.742 2.503 2.216 3.081

diffturn 0.002 0.002 0.000 0.0021.855 1.984 0.106 1.667

diffexpense -0.020 0.774 -0.476 -1.149-0.089 3.428 -1.200 -4.048

loaddum -0.705 -0.062 0.576 -0.115-4.935 -0.435 2.346 -0.659

age -0.030 -0.028 -0.093 -0.108-1.708 -1.603 -2.785 -6.140

age2 3.528E-04 3.159E-04 8.991E-04 1.267E-031.275 1.138 1.876 4.708

assets -1.356E-04 -1.360E-04 -6.150E-04 -4.001E-04-1.427 -1.440 -3.762 -3.456

assets2 2.750E-08 2.760E-08 5.410E-08 3.910E-083.642 3.711 3.527 3.706

assets3 -4.950E-13 -4.990E-13 -8.280E-13 -6.140E-13-4.171 -4.277 -3.282 -3.642

fund mshare -6.776 -6.741 -2.753 -3.764-5.457 -5.384 -1.642 -2.920

stdv 0.225 0.231 0.340 0.2502.889 2.915 3.685 3.816

family assets 2.540E-05 2.450E-05 3.400E-05 3.080E-052.243 2.158 1.666 2.444

family assets2 -1.170E-10 -1.130E-10 2.690E-11 -2.840E-10-0.967 -0.937 0.146 -2.135

family assets3 1.380E-16 1.340E-16 -5.670E-16 6.990E-160.421 0.407 -1.216 1.952

family assets in cat -9.250E-07 -6.190E-07 -4.570E-05 -8.640E-06-0.039 -0.026 -0.933 -0.332

family funds in cat -0.040 -0.044 0.117 0.005-0.966 -1.076 1.541 0.100

funds in cat 4.235E-04 3.312E-04 -3.444E-03 -2.506E-031.308 1.023 -6.577 -6.962

constant -0.016 -0.031 0.395 0.472-0.051 -0.099 0.722 1.356

Number of obs. 9980 9980 6471 8451χχ2

(14) 128.17 121.44 91.10 200.37Prob. >χχ2

(14) 0.0000 0.0000 0.0000 0.0000

33

Table 2: The effect of relatedness and narrowness on fund performance(t-values below coefficients)

(1) (2) (3) (4)performance measure dcret dgret alpha malpha

related 1.006 0.918 2.089 0.8242.309 2.124 2.620 1.667

narrow 0.018 0.018 0.038 -0.0170.989 0.958 1.277 -0.645

diffturn 0.001 0.002 -3.309E-04 0.0021.606 1.755 -0.273 1.591

diffexpense -0.005 0.786 -0.456 -1.094-0.024 3.480 -1.160 -3.926

loaddum -0.673 -0.031 0.611 -0.114-4.574 -0.212 2.425 -0.631

age -0.035 -0.032 -0.095 -0.113-1.976 -1.844 -2.830 -6.398

age2 4.217E-04 3.791E-04 9.101E-04 1.341E-031.521 1.359 1.908 4.962

assets -1.903E-04 -1.854E-04 -7.475E-04 -4.642E-04-1.888 -1.845 -4.092 -3.699

assets2 3.210E-08 3.180E-08 6.410E-08 4.380E-084.041 4.020 3.541 3.771

assets3 -5.660E-13 -5.640E-13 -9.750E-13 -6.810E-13-4.561 -4.564 -3.258 -3.657

fund mshare -7.042 -6.987 -3.229 -3.739-5.624 -5.539 -1.860 -2.888

stdv 0.2307 0.236 0.334 0.2592.998 3.017 3.652 3.983

family assets 1.380E-05 1.340E-05 2.240E-05 3.110E-051.086 1.057 1.028 2.022

family assets2 -3.060E-11 -3.110E-11 8.870E-11 -2.610E-10-0.253 -0.258 0.465 -1.856

family assets3 -5.520E-17 -5.060E-17 -6.780E-16 6.290E-16-0.170 -0.156 -1.413 1.702

family assets in cat -1.980E-06 -1.460E-06 -4.720E-05 -1.370E-05-0.081 -0.059 -0.966 -0.511

family funds in cat -0.066 -0.069 0.063 -0.007-1.513 -1.567 0.791 -0.124

funds in cat 4.294E-04 3.395E-04 -0.003 -0.0031.310 1.037 -6.594 -7.222

constant 0.217 0.175 0.436 1.1470.622 0.498 0.815 3.455

Number of obs. 9980 9980 6471 8451χχ2

(15) 119.89 104.98 90.08 191.56Prob. >χχ2

(15) 0.0000 0.0000 0.0000 0.0000

34

Table 3: The effect of focus on cash inflows into families(t-statistics below coefficients)

(1) (2) (3) (4) (5) (6) (7)dependent variable forall regressions:famflow

pastperformance

based ondcret

past perf. based on malpha

past perf.based on

ranking on adj. total

returns

past perf.based on

ranking on adj. total returns

past perf.based on

ranking on malpha

past perf.based on

ranking on malpha

no past perf.

measureincluded

focus -1008.779 -991.246 -966.818 -986.613 -963.399 -1075.524 -996.085-2.513 -2.466 -2.408 -2.399 -2.396 -2.599 -2.479

average pastperformance

17.8711.886

5.4600.675

463.6972.034

397.2941.655

average lowperformance

-581.134-0353

-1440.007-1.299

average mediumperformance

613.8372.027

812.6322.470

average highperformance

-315.948-0.179

-2630.046-0/675

family assets -0.051 -0.051 -0.050 -0.050 -0.052 -0.053 -0.051-2.490 -2.501 -2.444 -2.442 -2.554 -2.601 -2.488

family assets2 2.17E-06 2.17E-06 2.16E-06 2.15E-06 2.18E-06 2.18E-06 2.17E-069.714 9.725 9.667 9.656 9.758 9.762 9.724

family assets3 -6.91E-12 -6.92E-12 -6.88E-12 -6.88E-12 -6.93E-12 -6.92E-12 -6.92E-12-10.824 -10.837 -10.781 -10.767 -10.859 -10.849 -10.840

average age -73.772 -73.096 -77.244 -74.201 -89.536 -75.783 -73.171-1.912 -1.892 -2.000 -1.907 -2.247 -1.851 -1.894

average age2 0.734 0.726 0.768 0.712 0.928 0.726 0.7271.181 1.166 1.235 1.137 1.465 1.119 1.168

average diffexpense -446.580 -461.467 -451.134 -452.275 -463.000 -453.458 -461.245-1.646 -1.699 -1.663 -1.664 -1.706 -1.672 -1.698

average stdv -33.300 -28.852 -43.103 -36.818 -35.818 -30.755 -24.847-0.876 -0.754 -1.111 -0.924 -0.934 -0.799 -0.657

av. category flow 1235.735 1224.479 1223.369 1229.771 1231.505 1213.881 1223.4238.603 8.522 8.528 8.514 8.574 8.438 8.517

average funds in cat -0.447 -0.414 -0.447 -0.421 -0.447 -0.426 -0.446-0.617 -0.570 -0.617 -0.581 -0.617 -0.589 -0.616

constant 1615.365 1590.912 1441.889 1565.017 1632.431 1786.837 1589.6593.380 3.326 2.985 2.904 3.411 3.664 3.324

obs. 1338 1338 1338 1338 1338 1338 1338R2 0.453 0.453 0.449 0.452 0.431 0.443 0.454

35

Appendix 1: Details on Morningstar categories and risk classification scheme

Equity fund investment style categories:

Funds are classified as follows:

Let IS = (average P/E ratio of fund / average P/E ratioof S&P 500) + (average P/book ratio of fund / averageP/book ratio of S&P 500)

If IS < 1.75, the fund is classified as Value.

If IS lies between 1.75 and 2.25, the fund is classifiedas Blend.

If IS > 2.25, the fund is classified as Growth.

Let MMC = median market capitalization = half of the fund’s assets are invested in stocks of companies larger than MMC

If MMC < $1 billion, the fund is classified as Small-Cap.If MMC lies between $1 billion and $5 billion, the fund is classified as Medium-Cap.If MMC > $5 billion, the fund is classified as Large-Cap.

For international equity funds, IS is defined on the basis of average price/cash flow and averageprice/book ratios relative to the MSCI EAFE index. The same cut-off points apply. The vertical axis isidentical.

Bond fund investment style categories:

Funds are classified as follows:

Let AEM = average effective maturity of a fund =weighted average of all bonds’ maturities, using assetsize as weight.

If AEM < 4 years, the fund is classified as Short-Term.

If AEM lies between 4 and 10 years, the fund isclassified as Intermediate-Term.

If AEM > 10 years, the fund is classified asLong-Term.

Funds that have an average credit rating of AAA or AA are classified as High Quality.Funds that have an average credit rating of A, BB, or BBB are classified as Medium Quality.Funds that have an average credit rating of less than BBB are classified as Low Quality.

source: Morningstar (1996)

Large-capValue

Large-capBlend

Mid-cap Value

Small-capValue

Mid-capBlend

Large-capGrowth

Small-capBlend

Mid-capGrowth

Small-capGrowth

Investment Style

Value Blend Growth

MedianMarketCapitalization

Large

Medium

Small

Short-termHighQuality

Interm-termHighQuality

Short-termMediumQuality

Short-termLowQuality

Interm-termMediumQuality

Long-term HighQuality

Interm-termLowQuality

Long-termMediumQuality

Long-termLowQuality

Investment Style

Short-term

Interm-term Quality

High

Medium

Low

Long-term

37

Appendix 2: Morningstar categories and associated market benchmarks

Morningstar Categories Market BenchmarkConvertible Bond 1985 Lehman Bros Agg, 1986-1996 Convertible Bond IndexDiversified Emerging Markets 1985-1988 MSCI Pacific; 1989-1996 MSCI Emerging MarketsDiversified Pacific Stock Morgan Stanley Country Index (MSCI) PacificDomestic Hybrid S&P 500Europe Stock 1985 MSCI World, 1986-1996 MSCI EuropeForeign Stock MSCI EAFEHigh Yield Bond 1985 Lehman Bros Agg, 1986-1996 First Boston High YieldIntermediate-Term Bond 1985-1988 Lehman Bros Agg, 89-96 Lehman Bros Int Govt/CorpIntermediate-Term Government Lehman Bros GovtInternational Bond Salomon Brothers World GovtInternational Hybrid MSCI WorldJapan Stock MSCI JapanLarge Blend S&P 500Large Growth Wilshire LGLarge Value Wilshire LVLatin America Stock MSCI Latin AmericaLong-Term Bond 1985 Lehman Bros Agg, 86-96 Lehman Bros LT Gov/CorpLong-Term Government 1985 Lehman Bros Agg, 86-96 Lehman Bros LT Gov/CorpMid-Cap Blend S&P Midcap 400Mid-Cap Growth Wilshire MGMid-Cap Value S&P Midcap 400Multisector Bond 1985 Lehman Bros Agg, 1986-1996 First Boston High YieldMuni National Intermediate Lehman Bros MuniMuni National Long-Term Lehman Bros MuniMuni Short Term Lehman Bros MuniMuni Single-State Intermediate Lehman Bros MuniMuni Single-State Long Lehman Bros MuniPacific ex-Japan Stock 1985-1987 MSCI Pacific; 1988-1996 MSCI FE ex JapanShort-Term Bond Lehman Bros 1-3 GovtShort-Term Government Lehman Bros 1-3 GovtSmall Blend Russell 2000Small Growth Russell 2000Small Value Russell 2000Specialty-Communications 1985 S&P 500, 1986-1996 Wilshire 5000Specialty-Financial S&P 500Specialty-Health Care 1985 S&P 500, 1986-1996 Wilshire 5000Specialty-Natural Resources 1985 S&P 500, 1986-1996 Wilshire 5000Specialty-Precious Metals 1985 S&P 500, 1986-1996 Wilshire 5000Specialty-Real Estate Wilshire REITSpecialty-Technology 1985 S&P 500, 1986-1996 Wilshire 5000Specialty-Unaligned 1985 S&P 500, 1986-1996 Wilshire 5000Specialty-Utilities Wilshire LVUltrashort Bond Lehman Bros 1-3 GovtWorld Stock MSCI World

38

References

Baumol, William J., Steven M. Goldfield, Lilli A. Gorden, and Michael F. Koehn. 1990. The Economicsof Mutual Fund Markets: Competition versus Regulation. Boston: Kluwer Academic.

Blake, Christopher R., Edwin J. Elton, and Martin Gruber. 1993. “The Performance of Bond Funds.”Journal of Business 66 (3): 371–403.

Brown, Keith C., W.V. Harlow, and Laura T. Starks. 1996. “Of Tournaments and Temptations: AnAnalysis of Managerial Incentives in the Mutual Fund Industry.” Journal of Finance 51 (1): 85–110.

Brown, Stephen J., and William N. Goetzman. 1995. “Performance Persistence.” Journal of Finance 50(2): 679–-698.

Brown, Stephen J., William N. Goetzman, Roger G. Ibbotson, and Stephen A. Ross. 1992. “SurvivorshipBias in Performance Studies.” Review of Financial Studies 5 (4): 553–580.

Brynjolfsson, Erik, and Lorin Hitt. 1996. “Information Technology and Organizational Architecture: AnExploratory Analysis.” (working paper).

Caves, Richard E., Michael E. Porter, A. Michael Spence, and J. T. Scott. 1980. Competition in the OpenEconomy. Cambridge: Harvard University Press.

Chevalier, Judith, and Glenn Ellison. 1997. “Risk Taking by Mutual Funds as a Response to Incentives.”Journal of Political Economy 105 (6): 1167–1200.

Comment, Robert, and Gregg A. Jarrell. 1995. “Corporate Focus and Stock Returns.” Journal ofFinancial Economics 37: 67–87.

Daley, Lane, Vikas Mehotra, and Ranjini Sivakumar. 1997. “Corporate Focus and Value Creation:Evidence from Spinoffs.” Journal of Financial Economics 45 (2): 257–281.

Eaton. Leslie. 1995. “A Bond Strategy Too Clever by Half; Fidelity Stumbles in an Attempt to Repeat ItsSuccess With Stock Funds.” New York Times, May 3.

Elton, Edwin J., Martin J. Gruber, Sanjiv Das, and Matthew Hlavka. 1993. “Efficiency with CostlyInformation: A Reinterpretation of Evidence from Managed Portfolios.” Review of FinancialStudies 6 (1): 1–22.

Ferris, Stephen P., and Don M. Chance. 1987. “The Effect of 12b-1 Plans on Mutual Fund ExpenseRatios: A Note.” Journal of Finance 62 (4): 1077–1082.

Gasparino, Charles. 1997. “Do Fund Mergers Hurt Small Investors?” Wall Street Journal, July 8: C1.

Gruber, Martin J. 1996. “Another Puzzle: The Growth in Actively Managed Mutual Funds.” Journal ofFinance 51 (3): 783–810.

Hoshi, Takeo, Anil Kashyap, and David Scharfstein. 1991. “Corporate Structure, Liquidity, andInvestment: Evidence from Japanese Industrial Groups.” Quarterly Journal of Economics 106: 33–60.

Huber, P. J. 1967. “The Behavior of Maximum Likelihood Estimates Under Non-Standard Conditions.” inProceedings of the Fifth Berkeley Symposium in Mathematical Statistics and Probability, 221–233.Berkeley: University of California Press.

39

Ichniowski, Casey, Kathryn Shaw, and Giovanno Prennushi. 1997. “The Effects of Human ResourceManagement Practices on Productivity: A Study of Steel Finishing Lines.” American EconomicReview 87 (3): 291–313.

Ippolito, Richard. A. 1989. “Efficiency with Costly Information: A Study of Mutual Fund Performance,1965–84.” Quarterly Journal of Economics 104: 1–23.

Jensen, Michael C. 1968. “The Performance of Mutual Funds in the Period 1945–1964.” Journal ofFinance 23: 389–416.

John, Kose, and Eli Ofek. 1995. “Asset Sales and Increase in Focus.” Journal of Financial Economics37:105–126.

Lang, Larry H. P., and René M. Stulz. 1994. “Tobin’s q, Corporate Diversification, and FirmPerformance.” Journal of Political Economy 102 (6): 1248–1280.

Liang, K.-Y., and S.L. Zeger. 1986. “Longitudinal Data Analysis Using Generalized Linear Models.”Biometrika 73: 13–22.

Lichtenberg, Frank R. 1992. “Industrial De-Diversification and its Consequences for Productivity.”Journal of Economic Behavior and Organization 18: 427–438.

Makadok, Richard, and Gordon Walker. 1996. “Search and Selection in the Money Market FundIndustry.” Strategic Management Journal 17: 39–54.

Malkiel, Burton G. 1995. “Returns from Investing in Equity Mutual Funds 1971–1991.” Journal ofFinance 50: 549–572.

Meyer, Margaret, Paul Milgrom, and John D. Roberts. “Organizational Prospects, Influence Costs, andOwnership Changes.” Journal of Economics and Management Strategy 1 (1): 10–35.

Milgrom, Paul, and John Roberts. 1990. “The Economics of Modern Manufacturing: Technology,Strategy, and Organization.” American Economic Review 80 (3): 511–528.

. 1995. “Complementarities and Fit: Strategy, Structure, and Organizational Change inManufacturing.” Journal of Accounting and Economics 19: 179–208.

Montgomery, Cynthia. 1985. “Product-Market Diversification and Market Power.” Academy ofManagement Journal 28: 789–798.

. 1994. “Corporate Diversification.” Journal of Economic Perspectives 8 (3): 163–178.

, and Birger Wernerfelt. 1988. “Diversification, Ricardian Rents, and Tobin’s q.” RAND Journalof Economics 19: 623–632.

Morck, Randall, Andrei Shleifer, and Robert W. Vishny. 1990. “Do Managerial Objectives Drive BadAcquisitions?” Journal of Finance 45 (1): 31–48.

Morningstar. 1996. User’s Guide to Morningstar Mutual Funds.

Palepu, Krishna. 1985. “Diversification Strategy, Profit Performance and the Entropy Measure.” StrategicManagement Journal 6: 239–255.

Penrose, Edith T. 1959. The Theory of the Growth of the Firm. Oxford: Basil Blackwell.

Porter, Michael E. 1996. “What is Strategy?” Harvard Business Review 74 (November-December): 61–78.

40

Rotemberg, Julio J., and Garth Saloner. 1994. “Benefits of Narrow Business Strategies.” AmericanEconomic Review 84 (5): 1330–1349.

Rumelt, Richard P. 1974. Strategy, Structure, and Economic Performance. Cambridge: HarvardUniversity Press.

. 1982. “Diversification Strategy and Profitability.” Strategic Management Journal 3: 359–369.

Scherer, Frederick M., and Ravenscraft, David J. 1987. Mergers, Sell-Offs, and Economic Efficiency.Washington, D.C.: The Brookings Institution.

Schmalensee, Richard. 1985. “Do Markets Differ Much?” American Economic Review 75: 341–351.

Sirri, Eric, and Peter Tufano. 1998. “Costly Search and Mutual Fund Flows.” Journal of Finance 53 (5):1589–1622.

Teece, David J. 1982. “Towards an Economic Theory of the Multiproduct Firm.” Journal of EconomicBehavior and Organization 3: 39–63.

Tufano, Peter, and Matthew Sevick. 1997. “Board Structure and Fee-Setting in the U.S. Mutual FundIndustry.” Journal of Financial Economics 46: 321–355.

Wernerfelt, Birger, and Cynthia A. Montgomery. 1988. “Tobin’s q and the Importance of Focus in FirmPerformance.” American Economic Review 78 (1): 246–250.

White, H. 1980. “A Heteroskedasticity-Consistent Covariance Matrix Estimator and a Direct Test forHeteroskedasticity.” Econometrica 48: 1–25.

You, Victor L., Richard E. Caves, James S. Henry, and Michael M. Smith. 1986. “Mergers and Bidders’Wealth: Managerial and Strategic Factors.” in The Economics of Strategic Planning, edited by L.G.Thomas, 201–221. Boston: Lexington Books.

v1.1

41

Footnotes

1 Within the context of studying inter-industry diversification, some authors have tackled this problem byanalyzing the effects of diversification at the level of business groups which are composed of individualfirms for which data is available (Hoshi, Kashyap, and Scharfstein 1991).2 In the strategic management literature, Rumelt (1974, 1982) further explores the relationship betweenthe type of diversification and firm performance. By adopting categorical measures of diversification,Rumelt extends the classification of firms beyond one-dimensional diversification measures. He finds thatfirms pursuing related diversification perform better than firms pursuing unrelated diversification.3 Related empirical work, which also uses the logic of complementarities, albeit on much more tightlydefined domains, includes Brynjolfsson and Hitt (1996), and Ichniowski, Shaw, and Prennushi (1997).