"Flexibility and solution-driven work – two of our distinguishing ...

8

"Flexibility and solution-driven work – two of our distinguishing key strengths" The international transport markets – by sea, by land and in the air – are distinctly heterogeneous, both in terms of the economic environment and regarding the trans- port assets used. Martin Metz, who has headed DVB's Land Transport Finance divi- sion since 1999, comments on current macro-economic trends, on the Bank's unique business model, and on future challenges and opportunities. The interview was conducted by Elisabeth Winter, Head of Group Corporate Communications, Frankfurt. Besides the already mentioned heterogeneity of the transport sector, what is common to all these segments is the cyclicality of markets. Martin, would you agree to this, and if so, how would you describe the current cyclical en- vironment for rail and road transport? Cyclicality is a pattern of mature markets. Based on this, we can easily agree that our rail and land transport markets Europe, Australia, and North America are obviously mature mar- kets. The North American market is characterised by pronounced economic cycles – and additionally by sector-specific waves overlaying those cycles – while Australia basically fol- lows the up- and downswings of the mining or natural resources industry – and ultimately those of the Chinese economy. In Europe, we are far beyond the time when political cycles dominated the movements of the market, and now the sector follows the more moderate flow of economic cycles. Due to the excellent input from our Land Transport Research team, to which we have meanwhile added an additional expert, we believe we know where we are in any of these cyclical trends, and we are well positioned to take our decisions accordingly. What key macro-economic trends do you see in rail transport at present, and to what extent is rail transport affected by technological progress? Our markets grow long-term, and overall annual investments are immense – also in new rol- ling stock. Besides the economic cycles just described, we have identified some overarching trends which influence rail markets but – again – vary between the three regions: (i) regula- tion, (ii) political influence and governmental efforts to regain control over specific players and market segments, and (iii) dynamics between different transport modes, in particular the relationship between rail and road transport. These trends interconnect and overlap. Technological change is less a natural driving factor in our business and sometimes more dri- ven by political influence than by economic needs.

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of "Flexibility and solution-driven work – two of our distinguishing ...

Investor Relations Newslet ter 1/ 2015

"Flexibility and solution-driven work – two of our distinguishing key strengths"The international transport markets – by sea, by land and in the air – are distinctly heterogeneous, both in terms of the economic environment and regarding the trans-port assets used. Martin Metz, who has headed DVB's Land Transport Finance divi-sion since 1999, comments on current macro-economic trends, on the Bank's unique business model, and on future challenges and opportunities.

The interview was conducted by Elisabeth Winter, Head of Group Corporate Communications, Frankfurt.

Besides the already mentioned heterogeneity of the transport sector, what is common to all these segments is the cyclicality of markets. Martin, would you agree to this, and if so, how would you describe the current cyclical en-vironment for rail and road transport?

Cyclicality is a pattern of mature markets. Based on this, we can easily agree that our rail and land transport markets Europe, Australia, and North America are obviously mature mar-kets. The North American market is characterised by pronounced economic cycles – and additionally by sector-specific waves overlaying those cycles – while Australia basically fol-lows the up- and downswings of the mining or natural resources industry – and ultimately those of the Chinese economy. In Europe, we are far beyond the time when political cycles dominated the movements of the market, and now the sector follows the more moderate flow of economic cycles. Due to the excellent input from our Land Transport Research team, to which we have meanwhile added an additional expert, we believe we know where we are in any of these cyclical trends, and we are well positioned to take our decisions accordingly.

What key macro-economic trends do you see in rail transport at present, and to what extent is rail transport affected by technological progress?

Our markets grow long-term, and overall annual investments are immense – also in new rol-ling stock. Besides the economic cycles just described, we have identified some overarching trends which influence rail markets but – again – vary between the three regions: (i) regula-tion, (ii) political influence and governmental efforts to regain control over specific players and market segments, and (iii) dynamics between different transport modes, in particular the relationship between rail and road transport. These trends interconnect and overlap.

Technological change is less a natural driving factor in our business and sometimes more dri-ven by political influence than by economic needs.

2

Good examples are:

• therequirementtoinvestintolow-noisebrakingsystemsforfreighttrainsinEurope;• significantlychangedspecificationsforcrudeoiltankcarsaftertheLacMégantiquetrain disasterinCanadain2013andotherincidents;or• certainchangesinprimemoversofself-propelledequipment,suchasthedevelopmentof e.g. hybrid locomotives.

Theconsequencesofthesechangesaredrivingadjustmentcostsandtechnologicalchangesmuch more than consistent research and development in our markets. This is different to other DVB industry segments, e.g. the aviation world.

Talking about regulation or deregulation of land transport markets: do you expect further burdens to fall upon the sector, especially in Europe? What opportunities do you see in this context for private-sector operators, in freight and passenger transport?

Thisisawonderfulquestionwithafairlysober response: we would love seeing further technical and operational barriers falling, but it somehow seems to us that Europe currently has a couple of other, more stringent topics on the agenda so that the momentum in trying to even further deregulate our markets seems to have somewhat reduced. Undoubtedly, the rail sector has dramatically changed after libe-ralisation during the 1990s. While there are efficient and pragmatic solutions and trends now with which technical barriers can be largely reduced that have blocked international rail operations during 19th and most of the 20th century, the political barriers have not softened to levels expec-ted. But we remain to be optimists, and continue working on deals that are driving forward asset finance in European rail and that are supporting an open and liberalised rail market.

Despite this set-up, there are always good opportunities for private-sector players in our rail markets. We very much like those initiatives as they make the difference – opportunities whichneedquickdecisions,bringmomentum,drivechangesintechnologyandrisktaking,and inspire. It pretty much relates to one of the slogans which the Bank printed once on the JPMorganChaseChallengeshirts:“It'sNottheBigthatEattheSmall...It'stheFastthatEattheSlow”.Andwearehappytobepartofit.

A nice example in this context is a new start-up locomotive operating lessor which started business last year, currently ramping up a fleet of 50 modern electric locomotives, in a mar-ketalreadywellservedbycompetitors.EquitysponsorisKKR,andthesignificantdebtpiecehasbeenarrangedandfundedbyDVBtogetherwithSiemensBank.Thisisjustonecase, and there are many more examples where private initiatives are pursued and push the market dynamically forward, also on the operator or railroad side.

Issue1/September2015

"Flexibilityandsolution-drivenwork– two of our distinguishing key strengths"

MartinMetz,HeadofDVB'sLandTransportFinancedivision

3

Martin, where do you see the specific strengths of your market presence and business model?

Continuously, we discuss this topic amongst us, and very recently again at our last team meeting. Dominant drivers of our success are:

• therealisationthatourclientsandthemarketunderstandandappreciateourfocus,our railfinanceexpertise,andtheauthenticityofourapproach;• ourflexibilityandsolution-drivenwork;• thecommunicationof,andouractinginaccordancewithourclearstrategy;• ourcapacitytoexecute,tounderstandourcustomers,andtopursueastrategicdialogue with our core clients, along with• ourinspiration–theentireLandTransportplatformcontinuouslytriestoachievebetter resultsandbetterbusiness,whichisverymuchrootedinthequalityofourteams.

That’sit.ThesuccessofDVB’sLandTransportFinancedivisionoverthelastyears–whichhas led us to a peak year in basically all performance criteria by the end of 2014, including growing our loan book to €2.0 billion – gives sufficient evidence of it, as we believe.

From a regional perspective, you are currently active in North America and Europe and, since 2012, also in Australia. What exactly makes these markets attractive?

Very early in our efforts to define our strategy, we have understood that financing rail and rail-relatedassetsisdifferenttofundingassetsflyinginopenskiesorcruisinginbluewater.Mostor all of the rolling stock which we are financing is much more subject to specific national inte-rests and sovereign insolvency rules than ships and aircraft. Once this was clear, we decided that we should only work in regions with

• alargelyreducedlevelofpoliticalrisk;• aquitefirmregulatoryframework;and• anassoundandreliableaspossiblelegalsystem.

Theseparametersalsoultimatelyimplythatthereisasecondarymarketfortheequipmentwefinance – a natural element and necessary aspect of our asset finance work in rail. This has led us to limit our business so far to the three regions that you mentioned.

Sofar,wehavebeenquitepleasedwiththisset-up;volume-wise,ourregionsaredynamicandgenerate on average investment volumes of roughly €20 billion in rolling stock per annum, a sizeablenumberthatgivesamplespacetodobusiness.

Numerous competitor banks withdrew from financing and advisory services during the global economic crisis. At the same time, DVB continued to support its land transport clients with financial advice and asset-based financings. What was that down to?

DVB benefited from a couple of aspects which have helped us to support our clients even duringthepeakofthefinancialcrisis.Obviously,withDZBANKasourparentcompany,DVBhashadastronganchorpartnerwhichwaswillingtoprovideliquidityandfundingtouswhenotherbanksfalteredorfailedtobeavailabletoclients’needsandlendingrequests.Thisliquiditywasvitalforthemarket,and–withnosurprise–webookedarecordvolumeof new transactions at that time. Our clients appreciated our continuous availability during these crisis times. We can still feel today – and value enormously – the positive feedback that many of the market participants are mirroring back to us. We have firmly positioned us

Issue1/September2015

"Flexibilityandsolution-drivenwork– two of our distinguishing key strengths"

4

in their mind as the expert asset finance lender which not only deeply understands the needs foradequatestructuresandlendingbasedontheassetvaluesoftheunderlyingequipment,but which is also willing to partner with them even during tough times. This was only possi-ble as DVB has never been a corporate lender, but a significant player in the international asset finance arena.

On this basis, we have also successfully expanded our product range into the DVB Corporate Financeworld,withanexcellentco-operationwiththeteamsinLondonandNewYork.Thenumber of projects done with them is pleasantly high, and has delivered significant contribu-tions to our income statement, across the board from advisory services and capital markets activities, both in Europe and North America. At the end, it is clear that we will not be cross-sellers at large, but be able to capitalise on our client relationships to earn not insignificantly outside our asset-based lending area.

How would you describe the development of the land transport finance sector?

Thisquestionisoneofthemostvalidonestoberaisedatthemoment.Obviously,thenatureof banking is changing, and also the nature of debt markets in general. Biggest drivers for changearetheglutofliquidity(nosurpriseofcourse),increasedregulationofbanks,newfundingpartnersarrivinganddesperatelyseekingwaystodeployequityanddebtcapitalinto our sector (entities like insurance companies, funds, etc.), changing financing schemes in certain segments (like public finance arrangements), and pressure from – and on – manage-mentboardstodomore“safe”railbusiness.Allofwhichcurrentlyleadstopatternsandattitudes which we believe we have seen already between 2006 and 2008.

Inmoredetail:increasedliquidityallowsandforcesbankstooffercheapfundingsothatdealscanbebooked;banksandplayerswhichweconsidertobe“sunshine”or“touristbanks”–anicknamewithwhichpeopletaggedthosethatweregonewhentheskywascloudy during financial market crisis – are back, actively seeking business in sectors they have not been working in for years. Investors are keen to deploy capital, leading to a situa-tion where capital markets are open to absorb transactions which were typical bank debt deals in the past, at terms that many bank lenders can only dream of. Also, investors start takingoutexistingbankdebtdealsassingleinvestortransactions.Privateequityismoreactivethaneverinourmarkets,allowingpricetagsforacquisitionstojumpup;also,transac-tionsarebeingchurnedmorefrequentlythanwhatastrategicplayerwoulddo.

Lastly, it is worth mentioning that export credit agency (ECA) structures only play a marginal roleinourrailworld.Moneyissocheapthatpeopleshyawayfromundertakingtheextraeffort to structure such deals as a valuable alternative, which basically tells us in turn that ECA schemes have mostly been done historically rather for pricing than for risk reasons. Funnyenough,theonlyECAstructureswehaveseenoverthelastyearswerefordealsinOECD countries.

Don’t get me wrong: we so highly appreciate that rail gets much more attention in the financeworld,whichiswelldeserved.However,themainquestionismoreintowhatdirec-tionthefinancingworldwithalltheliquiditywilltakeourdeals.

"Land transport financings are less prone to risk than transactions in other transport sectors" – Martin, would you agree with this statement, and how do you deal with the risk?

It would be naive to believe that rail markets are risk free. Our approach is driven by always remindingourselvesofthe“3Rs”principleduringevaluation,whichmeans“risk-risk-risk”.

Issue1/September2015

"Flexibilityandsolution-drivenwork– two of our distinguishing key strengths"

5

Nojoking,thoughraildealsenjoythelowestcapitalcostwithinDVB,dealsrequirealotofdue diligence and internal discussion. Our Land Transport Research team plays a vital role, as muchasourEarlyWarningSystem,thedialoguewithourcreditcolleagues,generalmarketintelligence, and our capability to early understand signals, e.g. as part of security and admi-nistrative agent roles, which we take more often than ever. Even in rail, there is no free lunch, and we understand the clear signal from the market to become even more careful when we see lenders and investors joining the sector who cannot be considered experts.

What are the criteria you use to plan and manage your business at present? And in which lines of business do you see the biggest potential for success-ful cooperation between your clients and DVB, in 2015 and beyond?

We firmly believe we understand the market dynamics in principle, the exchange with our cli-ents is excellent, our platform benefits from great teams and an outstanding internal research database. We can therefore identify trends, spot orders and opportunities, and know about deals fairly early.

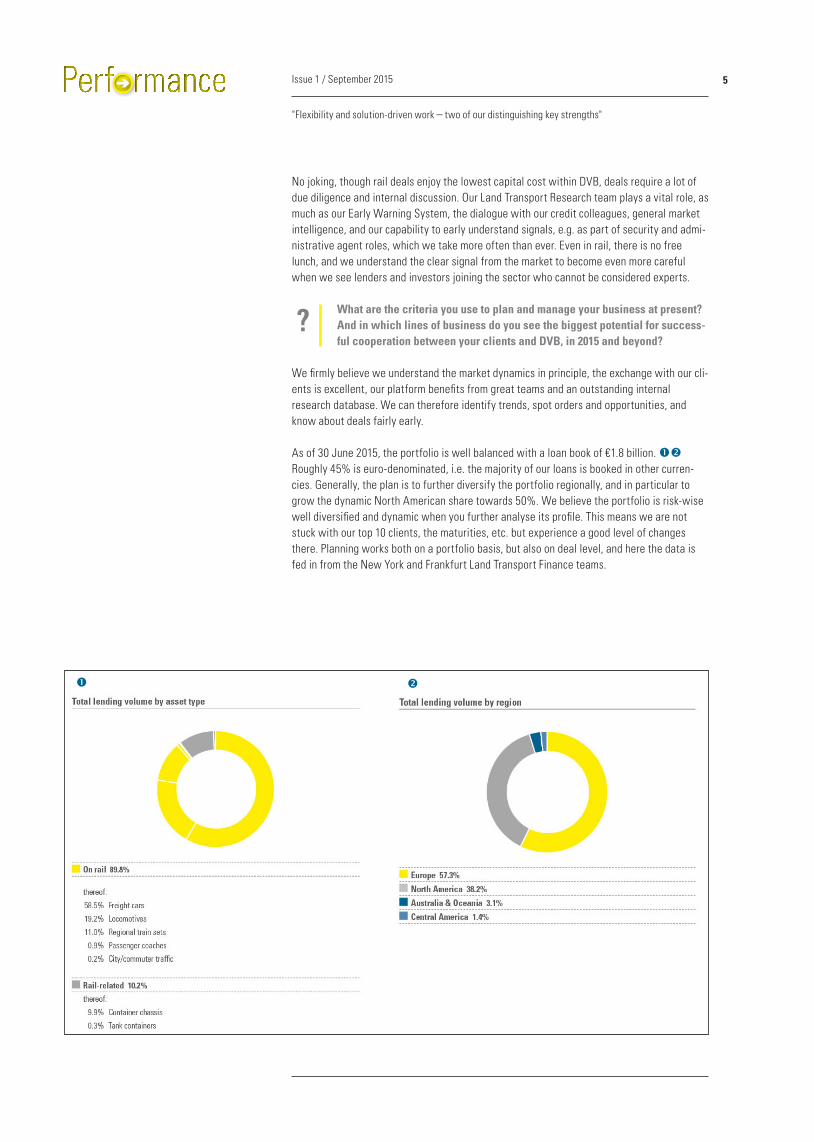

As of 30 June 2015, the portfolio is well balanced with a loan book of €1.8 billion. Roughly 45% is euro-denominated, i.e. the majority of our loans is booked in other curren-cies. Generally, the plan is to further diversify the portfolio regionally, and in particular to grow the dynamic North American share towards 50%. We believe the portfolio is risk-wise well diversified and dynamic when you further analyse its profile. This means we are not stuck with our top 10 clients, the maturities, etc. but experience a good level of changes there. Planning works both on a portfolio basis, but also on deal level, and here the data is fedinfromtheNewYorkandFrankfurtLandTransportFinanceteams.

Issue1/September2015

"Flexibilityandsolution-drivenwork– two of our distinguishing key strengths"

6Issue1/September2015

"Flexibilityandsolution-drivenwork– two of our distinguishing key strengths"

At the end, all that counts is reacting flexibly to market changes. We intensify our activities in those market segments where we see open windows for asset investments, see chances for markets to develop further, or when clients start being interested in procuring rolling stock, etc. Lots of information comes directly from our customers. Once an opportunity is identified, we go very early into our Deal Committee. Once a transaction idea crosses that committee line, we are going to strictly allocate resources to the deals we want to pursue.

Currently,weseeprimarilygoodopportunitiesforDVB’sLandTransportFinanceDivisioninthefreight sector, both for locomotive and railcar fleet deals. The passenger rail market is more a European market, and there we see a lot of political influence on the market. Otherwise, we are open for all types of business in our three regions, Europe, North America and Australia. The markets are sound and produce enough pipeline of investments into new rolling stock every year, or refurbishment of older assets. By far not all of our assets are brand new when we finance them. We enjoy the stability and lower cyclicality of our markets, appreciate the creditqualityofourclientsandtransactions,andvaluethefeedbackfromthemarketsfromwhich we hear that we are still a reference bank for rail asset finance deals.

Martin, thank you very much for the interview.!

7

Prezi – A step towards the world of business entertainmentby Elisabeth Winter, Head of Group Corporate Communications, and Simone Sacherer,

Manager Corporate Design, Frankfurt

In early May 2015 we presented our new “baby”: a Prezi presentation. Now we would like to zoom in on this new product, outline the challenges we have to take up and explain how users benefit.

As Group Corporate Communications, it is our everyday challenge to tell DVB’s success story to a wide variety of target groups (clients, business partners, investors, analysts, journalists, employees and many more) using different communication tools – storytelling is the new buzzwordinthecommunicationmarkets.

Prezi – Target groupStakeholders’informationbehaviourhaschangedaswell.Itisnolongeraboutcontentandtopics, but also about entertainment. Communication as a process should be fun.

“Businessentertainment”reliesevermoreheavilyonvisualstimuli–likecorporatevideos,corporatephotography,acaptivatingwebsite,aswellassocialmedia.WithourPrezi,wewanttopresent“hard”bankingtopicssuchasDVB’svision,ourcolleagues’expertiseandtheDVB’sstrengthsprofileina“fresh”way.

The presentation was designed with the growing number of younger decision makers in mind, those who primarily turn to social media platforms for private communication. That is why we want DVB content to be

• easilyandquicklyaccessiblefromoneplace;• presentedvisuallyinanentertainingwayasthepowerofvisualsattractsattentionand helpspeoplerememberinformation;• visuallyfacilitatedasitbecomeseasierforpeopletofollowandconcentrate.

Issue1/September2015

8

Imprint

Performance –Investor Relations NewsletterDVB Bank SEPlatz der Republik 660325 Frankfurt/Main, Germany

Editing & layout:

Elisabeth WinterHead of Group Corporate CommunicationsManaging Director+49 69 9750 [email protected]

Simone SachererManager Corporate Design+ 49 69 9750 [email protected]

Photos:

Prezi logo (page 7) –Prezi Inc., San Francisco, USAAll other photos –DVB Bank SE, Frankfurt/Main, Germany

After scanning this QR code with your smartphone, you will have direct access to our website.

Issue1/September2015

Prezi–Asteptowardstheworldofbuisnessentertainment

The target groups we aim for with this approach include journalists working under deadline pressures, and potential job applicants, who are interested in DVB and would like to get to know us. Last but not least, we also hope to engage clients who would like to learn more about our business divisions and product range.

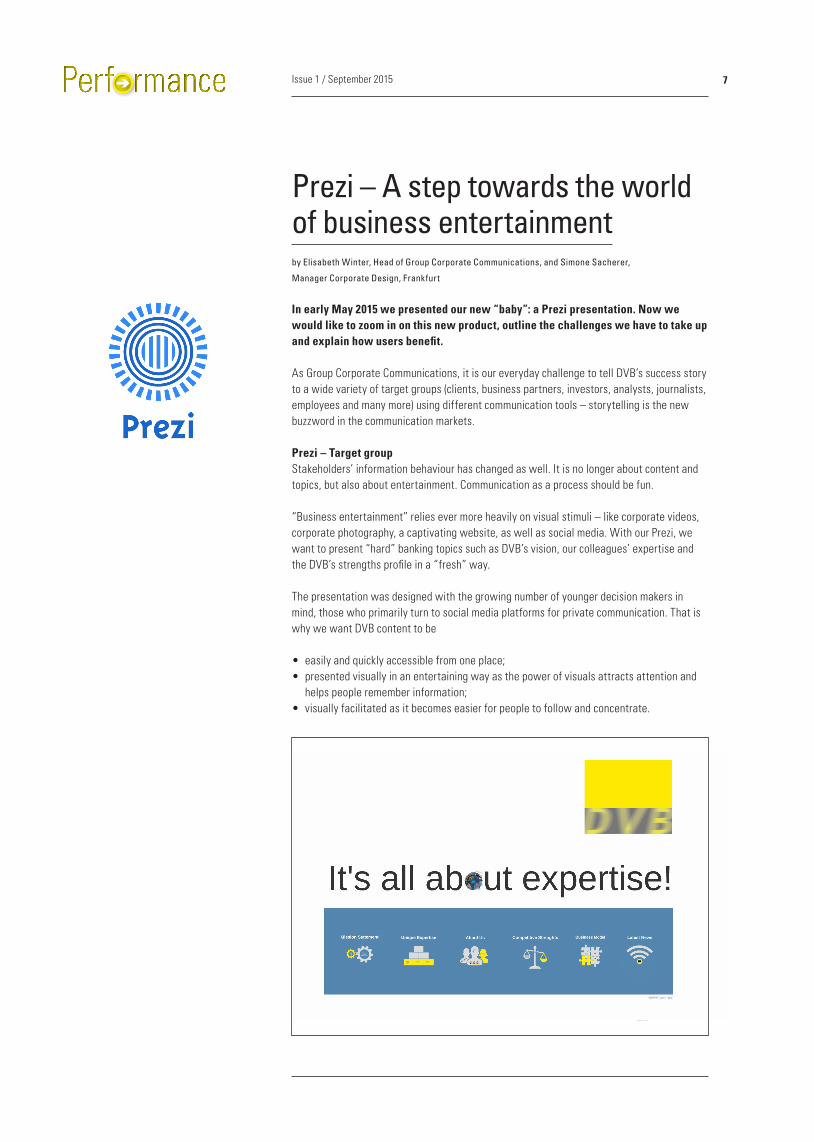

Prezi – StructureOurPreziiswell-structured:Inthelower,bluepartofthePrezicanvas,wepresentsixicons,oneforeachoftheBank’spillarsandcorecompetences:“MissionStatement”,“UniqueExpertise”,“AboutUs”,“Com-petitiveStrengths”and“BusinessModel”.Thepresentationfollowsapre-definedpath,gui-ding the viewer from one topic area to the next.

Then,theviewerdivesthroughtheheading“It’sallaboutexpertise!”intoourfourdivisions,andispresentedwithinformationonShipping,Aviation,OffshoreandLandTransport.Thispart of the presentation is designed as a globe, symbolic of the Bank’s global presence.

Thenextstopis“LatestNews”,withup-to-dateinformationonvarioustopics.Atthissec-tion is also the first opportunity for viewers to leave the presentation and access the web-site,shouldtheywishtodoso.“LegalInformation”,“Disclaimer”and“Contact”arealsolinked with the website.

Prezi – ProgrammeItwasanarchitectwhocameupwiththeoriginalideaforPrezi.Thisisreflectedinitsclearsetup: an empty canvas. Just as with a mind map, you can add text, pictures, videos, etc. to thecanvasandlinkthemtoeachother.Themostinterestingfeature,however,isthezoo-minginterface.Youmovefromoneelementtothenextasiffollowingacamera.

Thecamerazoomsinonanobject,thenoutagain,andontothenext.Adjustingthelayoutofeach“slide”workssimilartoPowerPoint,andisthuseasytounderstand.

Thepathaddsdynamism.ThepathistheorderinwhichPrezimovesfromoneelementtothenext,zoominginandoutofcontent.Thiswayofguidingpeoplethroughapresentationandletting them go back and forth between content means that you need neither presenter nor voice-overtoengagewithyouraudienceandensureaqualitypresentation.Viewersfindtheir way around on their own, navigating via mouse or arrow key.

Preziisaweb-basedsoftware,i.e.itisavailableeverywhere.Allyouneedisinternetaccess.

OutlookWearecurrentlyworkingonanotherPrezitouseatclientorsponsoringevents.Staytuned!

YoucanfindPrezionourwebsite'shomepagewww.dvbbank.com.