Financial Development and Crises: What Lessons for Emerging Economies?

16

Financial Development and Crises: What Lessons for Emerging Economies? XI National and VIII International Finance Experts Symposium: "Financial management and capital markets in emerging countries" Bogotá, September 16-17, 2014. Faruk ÜLGEN Centre de Recherche en Economie de Grenoble (CREG) - University of Grenoble Alpes [email protected] ; [email protected] ; [email protected] 1 Faruk ÜLGEN, “Financial Development and Crises”, Bogotá, September 16-17, 2014

-

Upload

univ-grenoble-alpes -

Category

Documents

-

view

7 -

download

0

Transcript of Financial Development and Crises: What Lessons for Emerging Economies?

Financial Development and Crises: What Lessons for Emerging Economies?

XI National and VIII International Finance Experts Symposium: "Financial management and capital markets in emerging countries"

Bogotá, September 16-17, 2014.

Faruk ÜLGEN Centre de Recherche en Economie de Grenoble (CREG) -

University of Grenoble [email protected]; [email protected]; [email protected]

1Faruk ÜLGEN, “Financial Development and Crises”, Bogotá, September 16-17, 2014

Abstract Aim:To assess the relevance/consistency of liberal regulatory - institutional environment with regard to financial (in)stability of market economies. Means:Studying the links between the process of FinDev and EMEs crises in light of the 2007-08 crisis of financialized capitalism. Result:Monetary/financial problems do not lie only in the economic fragilities (due to underdevelopment) but rather in the way liberalized economies work. Statement:Fin. Instabilities: result of endogenous problems of financialized economy (not natural outcome of difficulties of transition of some EMEs toward an efficient market.

2Faruk ÜLGEN, “Financial Development and Crises”, Bogotá, September 16-17, 2014

Standard assertion (Washington Consensus and after-crisis avatars) vs. disappointment (or deception?)

• Open/free/liberalized markets: necessary structural transformation for financial development (FD) and THEN for economic development (e.g. neo/new classical statements).

• Unfortunately: recurrence of EMEs crises AND the developed financial markets crisis of 2007-08 ⇒ doubt about the relevance of liberal assertions.

Faruk ÜLGEN, “Financial Development and Crises”, Bogotá, September 16-17, 2014 3

Work plan1.Observations about the conceptual foundations of financial liberalization reforms.

2.Links between the financial market development process and the EMEs and advanced economies crisis.

3.Lessons for EMEs in light of the 2007-08 crisis.

Faruk ÜLGEN, “Financial Development and Crises”, Bogotá, September 16-17, 2014 4

1. Financial development: from liberalization to (in)efficiency

Statement:•Crises in EMEs regarded as transition issues of underdeveloped financial systems toward free-market system (Washington Consensus N°1).•Conceptual foundations: Competitive (Pareto-optimal) equilibrium & Financial repression models(Subsequent) Cure:•To enforce mechanisms of open/free markets•Financial development

Faruk ÜLGEN, “Financial Development and Crises”, Bogotá, September 16-17, 2014 5

Well-known works

Finance stimulates growth (efficiency of market allocation mechanisms and increase of productive capital accumulation: saving-I equilibrium, low i, flexibility. See the 1st year undergraduate textbooks). Legal environment (market-friendly) and economic development (modernization: openness, competition): major determinants of sound finance.

Faruk ÜLGEN, “Financial Development and Crises”, Bogotá, September 16-17, 2014

6

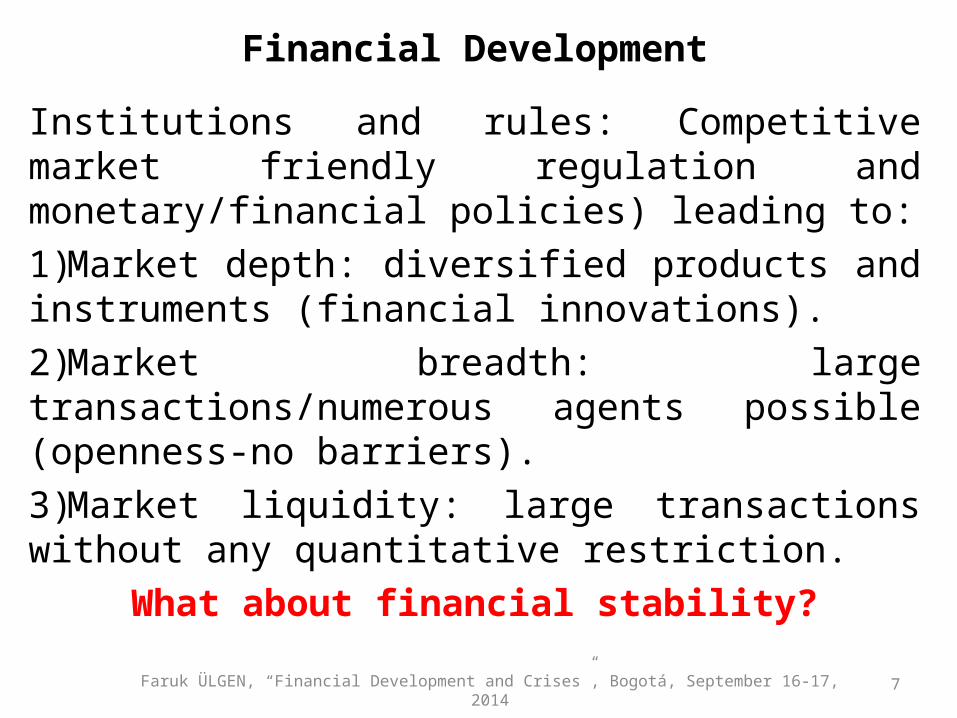

Financial DevelopmentInstitutions and rules: Competitive market friendly regulation and monetary/financial policies) leading to:1)Market depth: diversified products and instruments (financial innovations).2)Market breadth: large transactions/numerous agents possible (openness-no barriers). 3)Market liquidity: large transactions without any quantitative restriction.

What about financial stability?Faruk ÜLGEN, “Financial Development and Crises”, Bogotá, September 16-17,

20147

2. Financial development and difficulties: emerging economies

and the ongoing crisis• Two opposite approaches:1) Shock therapy: “let it be”, stabilization-liberalization-privatization triptych: markets can do.

2) Gradual approach: There is no market magic. Voluntary and conscious policies to guide/supervise market transformations.

The practice: mix of the two, eclectic implementation but tight ideological liberal

lineFaruk ÜLGEN, “Financial Development and Crises”, Bogotá, September 16-

17, 2014 8

• As a matter of logic from the hypothesis of complete and efficient (developed) financial markets, problems of illiquidity and insolvency are only thought as individual risks related concerns.

• It is supposed that free markets have self-regulatory mechanisms that rest on market prices which would produce sufficient information to direct effectively the behavior of decentralized actors through (socially) optimal strategies.

• Macro-prudential supervision (resting on public authorities) replaced by micro-prudential/self-regulation (assessing risks at individual level, no systemic view).

Faruk ÜLGEN, “Financial Development and Crises”, Bogotá, September 16-17, 2014

9

System development:•Financial liberalization related innovations crowd out traditional long-run and stable personal (non-market) relations between banks and enterprises. •Traditional banking replaced by transactional banking (financial investment funds management) •Market expansion: off-balance sheet activities –securitization-, increasing access of a large number of agents (low-income households).•Increase of market allocative efficiency but also of complex and immediate interconnectedness.

Faruk ÜLGEN, “Financial Development and Crises”, Bogotá, September 16-17, 2014 10

But:Blindness and cognitive dissonance phenomena in a euphoric and very flexible environment.This fuels expectations to realize substantial speculative gains while agents believe that they could easily cope with reversal in trend without much difficulty. Complex interconnections among different institutions, products and processes contribute to financial expansion and give the impression of a greater efficiency in the use of loanable funds. But at the same time this contains the seeds of a contagion at systemic level, contagion that is out of individuals and financial institutions reach.

Faruk ÜLGEN, “Financial Development and Crises”, Bogotá, September 16-17, 2014

11

3. What implications?

Faruk ÜLGEN, “Financial Development and Crises”, Bogotá, September 16-17, 2014 12

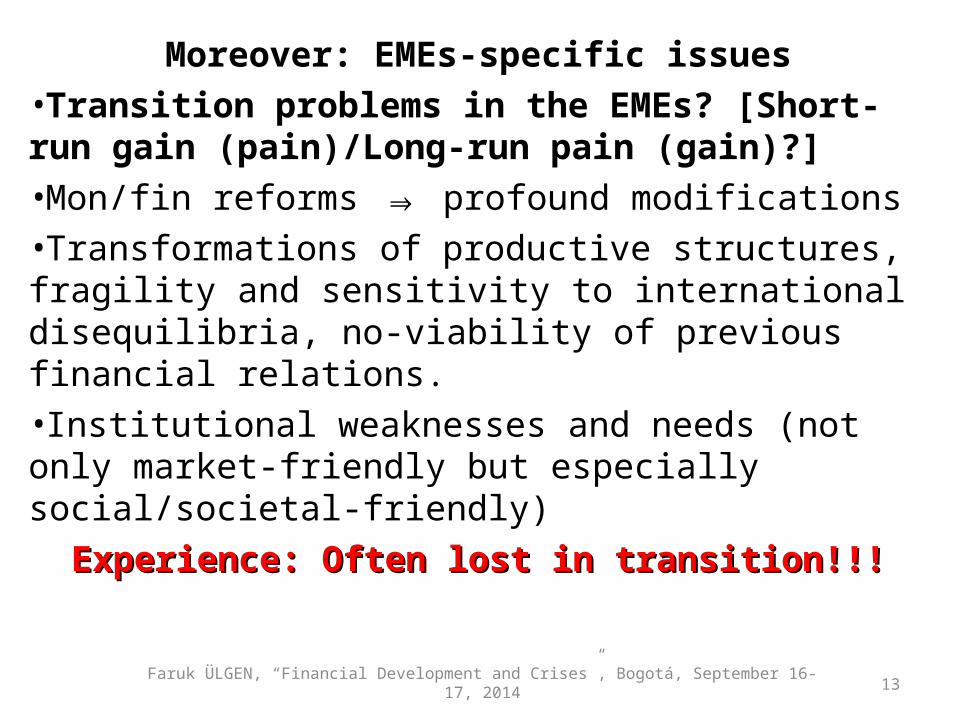

Moreover: EMEs-specific issues•Transition problems in the EMEs? [Short-run gain (pain)/Long-run pain (gain)?]•Mon/fin reforms ⇒ profound modifications •Transformations of productive structures, fragility and sensitivity to international disequilibria, no-viability of previous financial relations.•Institutional weaknesses and needs (not only market-friendly but especially social/societal-friendly)

Experience: Often lost in transition!!!Experience: Often lost in transition!!!

Faruk ÜLGEN, “Financial Development and Crises”, Bogotá, September 16-17, 2014 13

• Evolution of financial markets deteriorates financing conditions of entrepreneurial activities in favor of more financialized but fragile economic systems (endogenous financial instability).

• Thus development of macro-prudential framework consistent with the aim of enhancing the financing conditions of productive long-term economic activities.

• No automatic bridge between micro-prudential and macro-prudential supervision.

Faruk ÜLGEN, “Financial Development and Crises”, Bogotá, September 16-17, 2014 14

• Contrary to the hypotheses of shock therapy models, there is no spontaneous mechanism of competition which could incite market actors to adopt efficient behavior at macro level.

• Development is a process that must rest on a long-term sustainable objectives based program.

• These objectives must be structural objectives (choice of development strategy, improvement in the income distribution, sustainable productive system, structural approach to development, etc.).

Faruk ÜLGEN, “Financial Development and Crises”, Bogotá, September 16-17, 2014

15

Two recurrent problems require special attention:

•What advantages of RTAs as coordination devices to cope with the dependence of EMEs on exports (global demand remains sluggish and the problem of external imbalances can rise again and create the “mad waltz of FDIs” in EMEs)?; •What about the relevance of regional monetary/financial agreements to deal with capital outflows? At the moment, FDIs take an opportunistic position with regard to public and private debts in EMEs. But with persistent difficulties in European markets, the accumulation of global imbalances may have very strong impact on EMEs’ access to international financial markets.

Faruk ÜLGEN, “Financial Development and Crises”, Bogotá, September 16-17, 2014 16