Financial analysis

24

CONTENTS 1 INTRODUCTION.............................................. 2 2 OVERVIEW OF BELLWAY....................................... 2 3 RATIO ANALYSIS............................................ 2 3.1 Profitability Ratio.........................................2 3.1.1 Return on Capital Employed................................3 3.1.2 Gross Profit Margin.......................................3 3.1.3 Net Profit Margin.........................................3 3.2 Working Capital Position....................................4 3.2.1 Inventory Days............................................4 3.2.2 Receivable Days...........................................4 3.2.3 Payable Days..............................................5 3.3 Liquidity Ratio.............................................5 3.3.1 Current Ratio.............................................5 3.3.2 Acid-Test Ratio...........................................6 3.4 Long-Term Solvency Ratio....................................6 3.4.1 Gearing Ratio.............................................6 3.4.2 Interest Cover Ratio......................................7 4 CRITICAL ANALYSIS OF CORPORATE GOVERNANCE STATEMENT.......7 4.1 Audit committee.............................................8 4.2 Remuneration Committee......................................8 4.3 Nominations Committee.......................................8 5 CONCLUSION................................................ 8 6 APPENDIX.................................................. 9 6.1 Reflective Journal..........................................9

-

Upload

independent -

Category

Documents

-

view

3 -

download

0

Transcript of Financial analysis

CONTENTS

1 INTRODUCTION..............................................2

2 OVERVIEW OF BELLWAY.......................................2

3 RATIO ANALYSIS............................................2

3.1 Profitability Ratio.........................................2

3.1.1 Return on Capital Employed................................3

3.1.2 Gross Profit Margin.......................................3

3.1.3 Net Profit Margin.........................................3

3.2 Working Capital Position....................................4

3.2.1 Inventory Days............................................4

3.2.2 Receivable Days...........................................4

3.2.3 Payable Days..............................................5

3.3 Liquidity Ratio.............................................5

3.3.1 Current Ratio.............................................5

3.3.2 Acid-Test Ratio...........................................6

3.4 Long-Term Solvency Ratio....................................6

3.4.1 Gearing Ratio.............................................6

3.4.2 Interest Cover Ratio......................................7

4 CRITICAL ANALYSIS OF CORPORATE GOVERNANCE STATEMENT.......7

4.1 Audit committee.............................................8

4.2 Remuneration Committee......................................8

4.3 Nominations Committee.......................................8

5 CONCLUSION................................................8

6 APPENDIX..................................................9

6.1 Reflective Journal..........................................9

6.2 Ratio Calculations.........................................10

7 REFERENCES...............................................19

1 INTRODUCTIONThe objective of this assignment is to do a critical analysisof the annual report 2009 and accounts of Bellway Plc. Duringthe analysis, the values of 2009 report are compared to thevalues of 2008. The ratios used are profitability ratios,working capital ratios, liquidity ratios and long-termsolvency ratios. It is followed by a critical assessment ofthe corporate governance of the company and a reflectivejournal.

2 OVERVIEW OF BELLWAYThe Bellway Group was formed in 1946 and was started by JohnThomas Bell. It is sixty four years old and one of the largesthouse builder companies in the United Kingdom. They design andbuild homes which are in turn marketed by their respectiveregional offices who sell to people in highly populated areas.The Bellway Group has strength of 2000 employees which coverdifferent disciplines with their expertise. Bellway claimsitself as the 4th biggest house builder in the country(Bellway).

3 RATIO ANALYSISRatio analysis is the process of comparing the ratios of acompany which are derived from the company’s income statementand balance sheet, which helps us to define whether a businessis in profitable condition. The following are the ratios wecalculate,

1) Profitability Ratio2) Working Capital Position ratio3) Liquidity Ratio4) Long-term Solvency Ratio

2

3.1 Profitability RatioThe ratios used to evaluate the profitability of abusiness are,

1) Return on Capital Employed2) Gross Profit Ratio3) Net Profit Ratio

Below are the profitability ratios of Bellway Plc for theyear 2009 and 2008.

Financial year 2009 2008

Return On CapitalEmployed (1.94%) 4.18%

Gross Profit Margin 3.04% 9.82%

Net Profit Margin (3.03%) 4.7%

3.1.1 Return on Capital Employed“Return on capital employed expresses the relationship between the net profit generated during a period and the average long term capital invested in the business duringthat period (Peter Atrill and Eddie McLaney, 2006, p175).”

ROCE = (Net profit before interest and taxation / (ShareCapital + long term loans)) x 100

ROCE has decreased when compared to the previous year. Itwas 4.18% in 2008 where as in 2009 it is -1.94%. Therehas been a decrease in sales of the company by 33.1% inthe year 2009. This was because there was a decrease inthe mortgage approval rates in the start of the year 2009which dropped to 33,000 which is the lowest recorded

3

value since 1993. As a result the customer had no moneyto invest or buy new properties. This was due to thefinancial down turn which can also be called as theperiod of reduced economy.

3.1.2 Gross Profit Margin“The gross profit margin ration relates the gross profit of the business to the sales revenue generated for the same period (Peter Atrill and Eddie McLaney, 2006, p 176)”.

Gross Profit Margin = (Gross Profit / Sales Revenue) x100

Gross profit = Sales Revenue – Cost of Sales

This ratio helps us to know whether the business hadsuccess with the amount of sales they made in a year.Gross profit margin for the year 2008 was 9.82% which hasdrastically decreased to 3.04%. The sales revenue hasdecreased to GBP 683mn in 2009 which was GBP 1.1bn in theyear 2008. This occurred as the average selling price wasdecreased by 9.2%. The reservations of homes was 50% lessthan what it was in the previous year (p45). Bellwayclaims that its sales have dropped to 50 to 60 new housesa week in the year 2008 which is 50% less than theprevious year’s sales (timesonline, 2008).This is againdue to the credit crunch which hit the UK economy.

3.1.3 Net Profit Margin“The net profit margin ratio relates the net profit for the period to the sales revenue during that period (PeterAtrill and Eddie McLaney, 2006, p 178)”.

Net Profit Margin = (Net profit before interest andtaxation / Sales Revenue) x 100

4

If the net profit margin of a company is high, it impliesthat the company effectively converting its revenue intoprofits.

The company’s net profit margin was 4.7% in the year2008, where as in 2009 it is -3.03%. The various reasonsfor the loss calculated include less sales, lower averageselling price and operating loss. There was a significantincrease in the administrative expenses when compared tothe gross profit in the year 2009 (Bellway annualreport). The review of inventories has been done due tothe recession and the land, exchange properties andoption costs and fees have been written down to GBP66.3mn, which brought a loss in the value of itsinventories. This resulted in poor sales revenue.

3.2 Working Capital PositionThe working capital position of Bellway is as follows,

Financial year 2009 2008

Inventory Days 666.89 529.52

Receivable Days 5.9 4.3

Payable Days 29 26

3.2.1 Inventory DaysInventory days can be defined as the number of days acompany takes to convert its inventory into sales.

Inventory Days = (Inventory / Cost of Sales) x 365

The inventory days in 2008 were 529.52 which haveincreased to 666.89 in the year 2009. Bellway used itsland as security for land payables which was worth GBP

5

63.6mn. The write down amount on inventories in the year2009 was GBP 66.3 mn which has decreased the total valueof the inventories (Bellway annual report). The cost ofsales was also decreased in the year 2009 which resultedin the company holding its inventory for a long period.The land values have decreased due to global recessionwhich decreased the sales revenue.

3.2.2 Receivable DaysReceivable days are the number of days a company takes tocollect its money from its debtors.

Receivable days = (Trade receivables / cost of sales) x365

Receivable days in 2008 were 4.3 and in 2009 it is 5.9days. According to the annual report, none of the tradereceivables have crossed their due dates (Bellway annualreport). The trade receivables in 2008 were 13mn, whereas in 2009 it is 11mn. The difference between thereceivable days has not changed much when compared to2008. Therefore it can be said that the receivable daysor recovery period is normal.

3.2.3 Payable DaysPayable days are defined as the time the company takes topay its vendors.

Payable days = (Trade payable / cost of sales) x 365

The payable days in the year 2008 was 26, where as in theyear 2009 it has increased to 29 days. The trade payablesin 2009 are GBP 52.6mn. The debt of the company has beencleared from the inventories and hence the payable daysincreased in 2009. The average selling price has beendecreased by 9.2%, which brought down the sales as well.

6

3.3 Liquidity RatioLiquidity ratios are calculated to see if a company canmeet its short-term financial obligations. It is done asfollows,

1) Current Ratio2) Acid Test Ratio

The following are the liquidity ratios for the year 2009and 2008.

3.3.1 Current Ratio“The current ratio compares the liquid assets of the business with the current liabilities (Peter Atrill and Eddie McLaney, 2006, p187)”.

Current Ratio = current assets / current liabilities.

Current assets = cash and the assets that will be soonconverted into cash.

Ideally the current ratio should be 2:1, but argumentssay that the type of business has to be considered tofollow this. The current ratio in the year 2008 was 4.9 :1 where as in the year 2009 it is 5.3 : 1, which is arecovery. The company has made significant investments inits inventories. The current liabilities in the year 2008were GBP 52mn. In this case the inventories can beconsidered as the vacant land or houses which were notsold during the year. The company had poor sales duringthe year 2009. There was also a write down on inventoriesin the year 2009 of GBP 66.3mn and land having GBP 63.6mn

7

Financial year 2009 2008

Current Ratio 5.3 : 1 4.9 : 1

Acid-Test Ratio 0.38 : 1 0.48 : 1

worth has been used as a security for land payables(Bellway annual report). There were no interest bearingloans and borrowings in the year 2009 which results ingreater solvency in the company’s future projects(Bellway annual report).

3.3.2 Acid-Test Ratio“The acid-test ratio is a variation of the current ratio,but excluding inventories (Peter Atrill and Eddie McLaney, 2006, p188)”.

Acid-Test Ratio = Current Assets (excludinginventories) / Current liabilities

In most of the businesses inventory cannot be convertedinto cash immediately. Some companies have a difficultyin turning their inventory into cash so the acid testratio is calculated using current assets excluding theinventories. This ratio gives more accurate ratio of theliquidity. The ratio of Bellway in 2008 was 0.48:1, andthe ratio in 2009 is 0.38:1. This implies that thecompany’s position is deteriorating in terms ofliquidity. The value of the current assets has beendecreased. The average selling price has been decreasedby 9%. Bellway claimed that it would escape the writedown on land that affected its competitors, and itsoperating margins were forecasted to be 3% less than theprevious year (timesonline, 2008). However the write-downin lands alone was GBP 58.881mn in the year 2009 whichhas decreased the value of its assets (Bellway annualreport). The land which was used for security had acarrying value of GBP 57.354mn when compared to GBP36.831mn in 2008. Considering the above conditions theaverage in 2009 has decreased (Bellway annual report).

8

3.4 Long-Term Solvency RatioLong term solvency ratios help us to know if a company canservice its debt obligations immediately and in the nearfuture. There are two long term solvency ratios namely,

1) Gearing Ratio2) Interest Cover Ratio

Financial year 2009 2008

Gearing Ratio 9.38 22.76

Interest CoverRatio (1.31) 2.84

3.4.1 Gearing Ratio“The gearing ratio measures the contribution of long termlenders to the long term capital structure of a business

(Peter Atrill and Eddie McLaney, 2006, p192)”.

Gearing Ratio = ((Long term liabilities (non-current)) /(share capital + Reserves + Long-termliabilities (non current))) x 100

The gearing ratio of Bellway in 2008 has been 22.76% andit has decreased to 9.38% in 2009. The long term (noncurrent) liabilities like bank loans in 2009 had beenless when compared to 2008. It means that long termborrowing has been less in the year 2009. Bellway hascleared its debts from GBP 180mn to GBP 37mn in the year2009 (guardian, 2009). The company runs on equity ifthere is no borrowing which is a good sign for thecompany.

9

3.4.2 Interest Cover Ratio“The interest cover ratio measures the amount of profit available to cover interest payable (Peter Atrill and Eddie McLaney, 2006, p193)”.

Interest Cover Ratio = Profit before interest andtaxation / Interest Payable

The interest cover ratio in 2008 was 2.84 and in 2009 theratio is reduced to -1.31%. If the profit leverage isless, then the chance of debt climbs. Bellway hasannounced for a scheme in which it sold new houses inexchange to old ones. This resulted in increase ofmaintenance costs due to part exchange properties. Thenet value of part exchange properties was written down toGBP 1mn in 2009 which resulted in high maintenance cost.As a result more money was spent on operation costs whichresulted in an operating loss in the year 2009. Thedecrease in sales has also affected the profits ofBellway. The profits available to cover the interest thathas to be payable is in negatives.

4 CRITICAL ANALYSIS OF CORPORATE GOVERNANCE STATEMENT“Corporate Governance can be defined as the way a company is controlled and directed (Peter Atrill and Eddie McLaney,2006, p107)”.

Corporate governance relates to the relationship betweenthe management of a company, the board of directors, shareholders and other stake holders (ifc, 2005). The numbers ofexecutive and non-executive directors are similar in theboard. So, it can be said that the combine code wasfollowed by Bellway.

10

The share holders have voted against a bill passed by theboard of directors in January 2009, regarding acontroversial pay and bonus announced by Bellway. If thebill was approved, it gave a 55% bonus on salary to JohnWatson who is the chief executive director. There was a 40-60 vote percentage between the directors and share holdersand the bill was not through. This is an example of Bellwayfollowing corporate governance (timesline, 2009). Bellwayis dedicated to its terms and abides by corporategovernance.

The board consists of an audit committee, remunerationcommittee and a nominations committee.

4.1 Audit committeeThe audit committee of Bellway consists of threeindependent non-executive directors. Mr. Toms is thechairman of Bellway. The other two directors are Mr.Johnson and Mr. Perry. Bellway claims that the auditcommittee meets at least three times in a year, where asit met four times in the year 2009. Some of the functionsof auditing committee are, to select external auditors,to check manually if an external audit is required,checking the effectiveness if internal financial auditsystem, financial reporting and risk management(Bellwayannual report). From the above said information it can besaid that Bellway has abided by all the rules andregulations.

4.2 Remuneration CommitteeThe remuneration committee of Bellway consists of Mr Tomsas its chairman, Mr Johnson and Mr. Perry as its membersof committee. This committee has a meeting twice in everyyear. The functions of remuneration committee arerecommending basic salaries, performance incentives, longterm incentive schemes, other benefits and the terms and

11

conditions of employment to chairman, executive directorsand non executive directors. The increase in salaries ofthe board is also monitored by shareholders who canappeal if they disagree.

4.3 Nominations CommitteeThe nomination committee of Bellway consists of Mr. Perrywho is the chairman of the committee, Mr. Toms, Mr.Johnson and Mr. Dave. This board meets two times in everyyear. The company has met for three times in the previousyear. Some of the functions of the nominations committeeare to formulate plans for the Chairman, Chief Executiveand directors (executive and non executive). The boardrequested the committee to find a replacement for thevacancy that has created by Mr Perry leaving the companyin Jan 2010. Mr Cuthbert was then recommended by thenominations committee to the board, and the board hasapproved it (Bellway Annual report).

5 CONCLUSIONBellway Plc’s performance for the year 2009 has been poor,although it had performed well in a few areas. Fewachievements in the year were clearing the bank loans anddebts, from GBP 187mn to GBP 57mn during the year, buthowever the sales were low. The write down of inventories,land, option costs and other fees has decreased the valueof assets of Bellway. The average selling price wasdecreased by 9.2% compared to the previous year. The salesof the company had affect when compared to the previousyear. Other external factors which affected the sales werethe low mortgage approval rate in the FY 2009. The mortgageapproval rate went low due to the affect of globalrecession on the banking sector. Bellway has abidedcorporate governance and has all the committees required.It has been in compliance with combine code.

12

6 APPENDIX

6.1 Student Guidance Reflective Journal(a) During my research, I came across a lot of

analytical thinking. The assignment pattern is different from the usual studying methodology used inIndia. It brought me entirely a different approach towork on the assignment which is very challenging and interesting as well. My research during the analysis included a thorough insight of the Bellway Plc annualreport 2009, research from articles and news papers, news sources like financial times, BBC and business times. Time management and planning is an important factor in completing these assignments. Starting early helped me to go through minor elements of Bellway which helped me in the research.

(b) The problems encountered during my work were minimal. With reference to books, articles and news, there were more possibilities of finding information.The class work and sessions helped me a lot, as in how to approach a given problem. The methods taught in the sessions, and the guidance from the tutors wasvery helpful.

(c) The experience in doing a assignment helps in learning a lot, like critical thinking, analysis, academic writing, analysis, being analytical and descriptive where necessary etc., All the experience gained here would be of definite help in the future assignments.

(d) Writing the assignment in a format, continuing the flow was easy. The analysis part was also good. Analysing the company is a great task and is interesting.

13

(e) Nothing in particular. But there is always a high chance of misconception and some analysis is tricky. Getting into the right groove is a challenging task. I would say I was comfortable in doing so.

(f) I honestly believe that I have performed to the bestof my ability. It was a wonderful experience overall.

6.2 Ratio Calculations

RATIOS FOR THE YEAR 2008

Profitability Ratios

Gross Profit Margin:

Gross Profit x 100

Sales revenue

= 112,891 x100

1,149,541

= 9.82 %

Net Profit Margin:

14

Operating Profit x 100

Sales revenue

= 54,130 _ x100

1,149,541

= 4.7 %

Return on capital employed (ROCE):

Operating Profit (PBIT) x 100

Capital employed

(Shareholder’s funds + Long term liabilities)

= _54,130 x100

1,296,084

= 4.17%

15

Working Capital Management Ratio:

Inventory days:

Inventories x 365

Cost of sales

= 1,503,936 x365

1,036,650

= 529.52 days

Receivable days:

Trade receivables x 365

Credit sales

= 13,644x365

1,149,541

= 4.3 days

16

Payable days:

Trade payables x 365

Credit purchases

= 75075 x365

1,036.650

=26.43 days

Liquidity Ratio:

Current Ratio:

Current Assets

Current Liabilities

= 1,667,745

336,901

= 4.9

Acid Test (Quick) Ratio:

Current Assets - Inventories

17

Current Liabilities

= 163809

336901

= 0.48

Long-term solvency ratios:

Gearing:

Long-term liability x 100

Capital employed

= 295,000 x100

1,296,084

= 22.76%

Interest cover:

Operating profit

18

Interest (Finance cost)

= 54130

19052

= 2.84

RATIOS FOR THE YEAR 2009

Profitability Ratios

Gross Profit Margin:

Gross Profit x 100

Sales revenue

= 20,821 x100

683,813

= 3.03 %

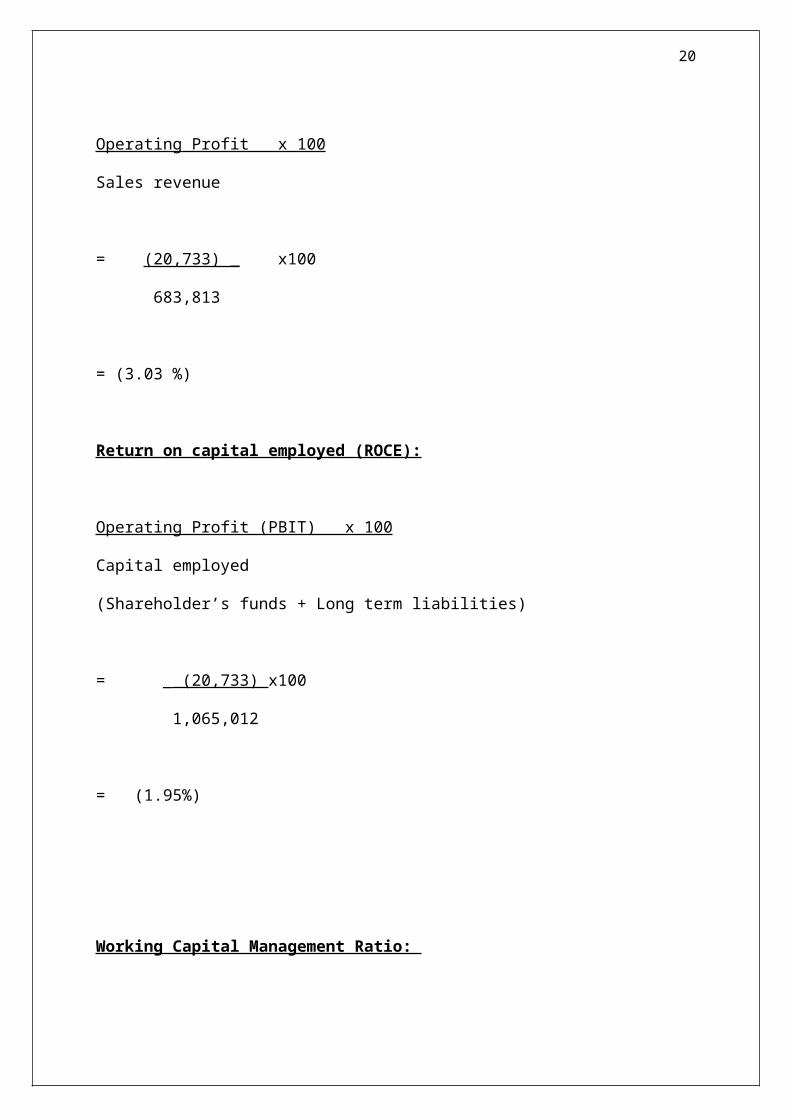

Net Profit Margin:

19

Operating Profit x 100

Sales revenue

= (20,733) _ x100

683,813

= (3.03 %)

Return on capital employed (ROCE):

Operating Profit (PBIT) x 100

Capital employed

(Shareholder’s funds + Long term liabilities)

= _ (20,733) x100

1,065,012

= (1.95%)

Working Capital Management Ratio:

20

Inventory days:

Inventories x 365

Cost of sales

= 1,211,351 x365

662,992

= 666.89 days

Receivable days:

Trade receivables x 365

Credit sales

= 11032 x365

683,813

= 5.88days

Payable days:

21

Trade payables x 365

Credit purchases

= 52610 x365

662,992

= 28.96 days

Liquidity Ratio:

Current Ratio:

Current Assets

Current Liabilities

= 1,306,157

246,147

= 5.3

Acid Test (Quick) Ratio:

Current Assets - Inventories

Current Liabilities

22

= 94,806

246,147

= 0.38

Long-term solvency ratios:

Gearing:

Long-term liability x 100

Capital employed

= 100,000 x100

1,065,012

= 9.38%

Interest cover:

Operating profit

Interest (Finance cost)

23

= (20733)

15818

= (1.31)

7 REFERENCES

1) PETER ATRILL and EDDIE MCLANEY, 2006, Accounting and finance for non-specialists, 5th edn, USA, PrenticeHall.

2) [WWW].http://business.timesonline.co.uk/tol/business/industry_sectors/construction_and_property/article5285065.ece.(9th April, 2010)

3) [WWW].http://business.timesonline.co.uk/tol/business/industry_sectors/construction_and_property/article4528803.ece.(11th April, 2010)

4) [WWW]. http://www.guardian.co.uk/business/2009/oct/13/bellway-housing-construction-loss.(6th April, 2010)

5) [WWW].http://www.ifc.org/ifcext/corporategovernance.nsf/AttachmentsByTitle/WhyCG_PrintFriendly/$FILE/WhyCG.pdf.(10th April, 2010)

6) [WWW].http://business.timesonline.co.uk/tol/business/industry_sectors/construction_and_property/article5531567.ece.(18th April, 2010)

7) Bellway Plc Annual Report, 2009.

24