cost volume profit analysis and financial forecast

66

i COST VOLUME PROFIT ANALYSIS AND FINANCIAL FORECAST OF WATER AND SANITATION CORPORATION RWANDA IMANISHIMWE CLEMENTINE MBA/3926/13 A Research Project Submitted in Partial Fulfilment for the Award of the Degree of Master of Business Administration (Accounting and Finance Option) of Mount Kenya University OCTOBER 2016

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of cost volume profit analysis and financial forecast

i

COST VOLUME PROFIT ANALYSIS AND FINANCIAL FORECAST

OF WATER AND SANITATION CORPORATION RWANDA

IMANISHIMWE CLEMENTINE

MBA/3926/13

A Research Project Submitted in Partial Fulfilment for the Award of the

Degree of Master of Business Administration (Accounting and Finance

Option) of Mount Kenya University

OCTOBER 2016

ii

DECLARATION

This research thesis is my original work and has not been presented to any other Institution.

No part of this research proposal should be reproduced without the authors’ consent or that of

Mount Kenya University.

Student Names: Imanishimwe Clementine

Registration Number: MBA/3926/13

Sign ____________________ Date _____________

This research has been submitted with my approval as the Mount Kenya University

Supervisor.

Name: Osiemo Kengere

Sign ____________________ Date _____________

iii

DEDICATION

I dedicate this research project to my daughter Etia.

iv

ACKNOWLEDGEMENTS

This study has been influenced by the inputs of more people than it is possible to list. I do,

however want to express my sincere thanks to those who played the most significant roles

during the course of this study.

I owe a special debt of thanks to my family. Without his assistance, advices and support, this

research could not reach to the desired end.

I would like to thank my supervisor Osiemo Kengere for his guidance, corrections and advice

without which this work could not be a success.

My gratitude is also addressed to Mount Kenya University lecturers. Without the knowledge

gained from them this project could not reach its result.

v

ABSTRACT

The business profitability is related to the costs and revenue. Managers need to estimate

future revenues, costs, and profits to help them plan and monitor operations. They use cost-

volume-profit (CVP) analysis to identify the levels of operating activity needed to avoid

losses, achieve targeted profits, plan future operations, and monitor organizational

performance. This study applied a cost volume profit analysis of water for financial forecast

of Water and Sanitation Corporation (WASAC). WASAC is a limited liability wholly owned

by the Government of Rwanda with mandate to contribute to the national goal of 100%

access to water and sanitation by 2018 under Economic Development and Poverty Reduction

Strategy II (EDPRS). However the aim of the corporation in business is not to make profit

rather to break- even and achieve its goal faster. The study CVP analysis and financial

forecast of WASAC is a descriptive research design using quantitative analysis specifically

aimed to determine the sales volume required to break-even, to examine the effects of

changes in revenue and costs on profit, and to evaluate the importance of CVP analysis in

financial forecast at WASAC. The target population was composed of 155 members of

WASAC staff directly involved in production, spending and distribution activities of water.

From which purposive sampling technique was used to select 61 respondents. Primary data

were obtained through self-administered questionnaire and were presented using tables and

charts, and analysed using descriptive statistics (frequencies and percentages). CVP analysis

was performed using financial statements of the utility for the year ended 30th

June 2015 as

secondary data source. The findings revealed that the sales volume required to break-even is

equal to Rwf 24,171,593,698 that is to increase the sales by 106.10%. The examination of

effects of changes in revenue and costs on profit revealed that any increase in costs exercises

a negative effect on profit while an increase in either quantity or unit selling price leads to an

increase in revenue and contributes positively to operating income. The findings also

revealed a paramount importance of using the CVP analysis in financial forecasts of the

corporation. From the findings, the research made some recommendations to the management

of WASAC such as minimization of costs of production and distribution of water, the use of

the CVP analysis as a managerial tool for decision making in line of financial forecast, and to

increase the volume of water produced and distributed.

vi

TABLE OF CONTENTS

DECLARATION..................................................................................................................... ii

DEDICATION........................................................................................................................ iii

ACKNOWLEDGEMENT ..................................................................................................... iv

ABSTRACT ..............................................................................................................................v

TABLE OF CONTENTS ...................................................................................................... vi

LIST OF TABLES ...................................................................................................................x

LIST OF FIGURES ............................................................................................................... xi

LIST OF ACRONYMS AND ABBREVIATIONS ............................................................ xii

OPERATIONAL DEFINITION OF KEY TERMS ......................................................... xiii

CHAPTER ONE: INTRODUCTION ....................................................................................1

1.0. Introduction .........................................................................................................................1

1.1. Background of the Study ....................................................................................................1

1.2. Problem Statement ..............................................................................................................2

1.3Objectives of Study ...............................................................................................................3

1.3.1General Objective ..............................................................................................................3

1.3.2 Specific Objectives ...........................................................................................................3

1.4Research Questions ...............................................................................................................3

1.5Significance of the Study ......................................................................................................4

1.6 Limitation of the Study ........................................................................................................4

1.7 Scope of the Study ...............................................................................................................5

vii

1.7.1 The content scope .............................................................................................................5

1.7.2 Geographical scope ...........................................................................................................5

1.7.3 Time scope ........................................................................................................................5

1.8Organization of the Study .....................................................................................................5

CHAPTER TWO: REVIEW OF RELATED LITERATURE ............................................6

2.0 Introduction ..........................................................................................................................6

2.1 Theoretical Literature ...........................................................................................................6

2.1.1 Overview of Cost ..............................................................................................................6

2.1.2 CVP Analysis and Its Importance in Decision Making ....................................................7

2.1.3 CVP Analysis Indicators ...................................................................................................8

2.1.4 CVP Analysis Techniques ................................................................................................9

2.2 Empirical Literature ...........................................................................................................10

2.4 Theoretical Framework ......................................................................................................12

2.5 Conceptual Framework ......................................................................................................13

2.6 Summary ............................................................................................................................14

CHAPTER THREE: RESEARCH METHODOLOGY ....................................................15

3.0 Introduction ........................................................................................................................15

3.1 Research Design.................................................................................................................15

3.2 Target Population ...............................................................................................................15

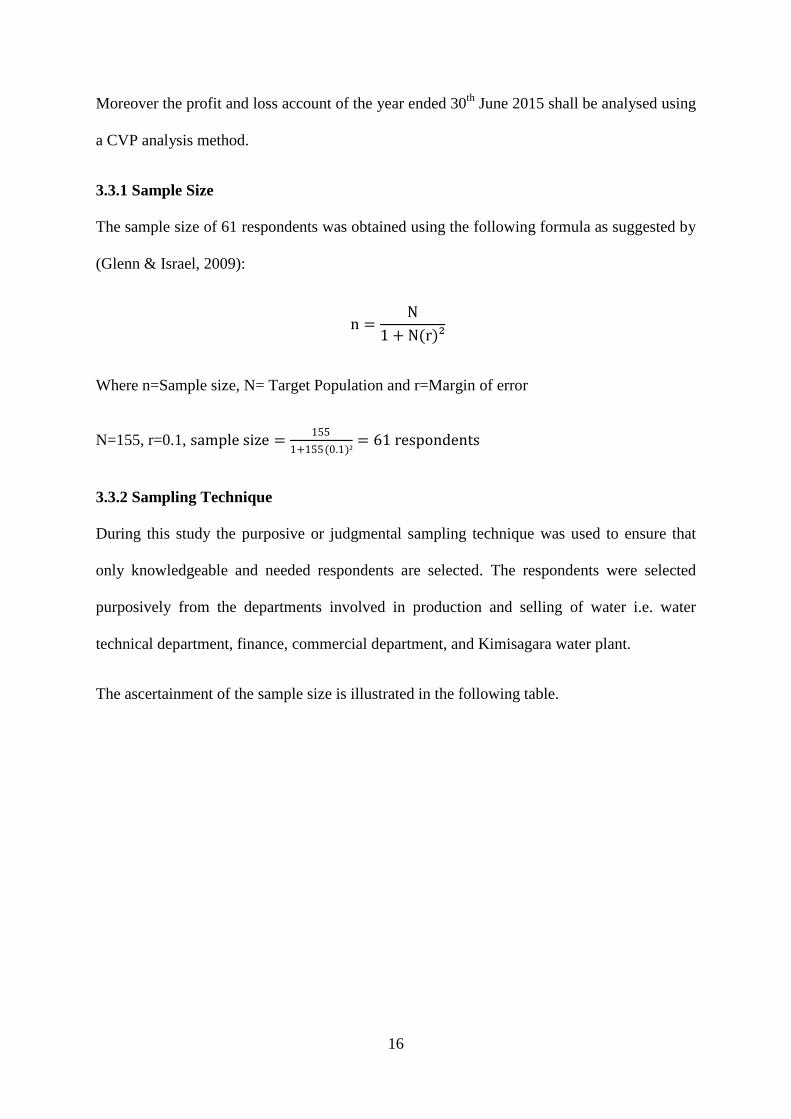

3.3 Sample Design ...................................................................................................................15

3.3.1 Sample Size .....................................................................................................................16

viii

3.3.2 Sampling Technique .......................................................................................................16

3.4 Data Collection Methods ...................................................................................................17

3.4.1 Data Collection Instrument .............................................................................................17

3.4.2 Administration of Data Collection Instruments ..............................................................18

3.4.3 Reliability and Validity ...................................................................................................18

3.5

3.6 Ethical Consideration .........................................................................................................19

CHAPTER FOUR: RESEARCH FINDINGS AND DISCUSSION .................................20

4.0 Introduction ........................................................................................................................20

4.1Demographic Characteristics of Respondents ....................................................................20

4.2Presentation of Findings .....................................................................................................23

4.2.1 To determine the sales volume (in Frw) required to break-even and evaluate possible

alternatives to breakeven..........................................................................................................23

4.2.2 To examine the effect of changes in revenue and costs on profit at Water and Sanitation

Corporation. .............................................................................................................................26

4.2.3 To evaluate the importance of use of CVP analysis in financial forecast at Water and

Sanitation Corporation. ............................................................................................................29

CHAPTER FIVE: SUMMARY, CONCLUSIONS AND RECOMMENDATIONS .......31

5.0 Introduction ........................................................................................................................31

5.1 Summary of Findings .........................................................................................................31

5.1.1 To determine the sales volume required to break-even and to evaluate alternatives to

break-even at Water and Sanitation Corporation .....................................................................31

ix

5.1.2 To examine the effect of changes in revenue and costs on profit at Water and Sanitation

Corporation. .............................................................................................................................32

5.1.3 To evaluate the importance of use of CVP analysis in financial forecast at Water and

Sanitation Corporation. ............................................................................................................32

5.2 Conclusion .........................................................................................................................33

5.3 Recommendations ..............................................................................................................34

5.4 Suggestions for further study .............................................................................................34

REFERENCES .......................................................................................................................35

APPENDICES ........................................................................................................................39

APPENDIX ONE: AUTHORIZATION LETTER .............................................................40

APPENDIX TWO: DATA COLLECTION ........................................................................41

APPENDIX THREE: WASAC INCOME STATEMENT FOR THE YEAR ENDED 30

JUNE 2015 ..............................................................................................................................42

APPENDIX FOUR: QUESTIONNAIRE FOR WASAC STAFF AND MANAGEMENT

..................................................................................................................................................50

x

LIST OF TABLES

Table3.1: Population and sample size ..................................................................................... 17

Table 4.2: Respondents by Department ................................................................................... 21

Table 4.3 Respondents by Position .......................................................................................... 21

Table 4.4: Respondents by Education Level............................................................................ 22

Table 4.5: Marginal Income Statement .................................................................................... 23

Table 4.6: Calculation of CVP indicators ................................................................................ 24

Table 4.7 Alternatives to break-even ....................................................................................... 25

Table 4.8: Effect of increase in unit selling price of water on profit ....................................... 26

Table 4.9: An increase in sales results into an increase in total revenue and contributes

positively to operating income ................................................................................................. 26

Table 4.10 A decrease in variable costs has a positive effect while their increase exercises a

negative effect on operating income ........................................................................................ 27

Table 4.11 An increase in fixed costs can contribute to increase the sales and thereby exercise

a positive effect on operating income ...................................................................................... 28

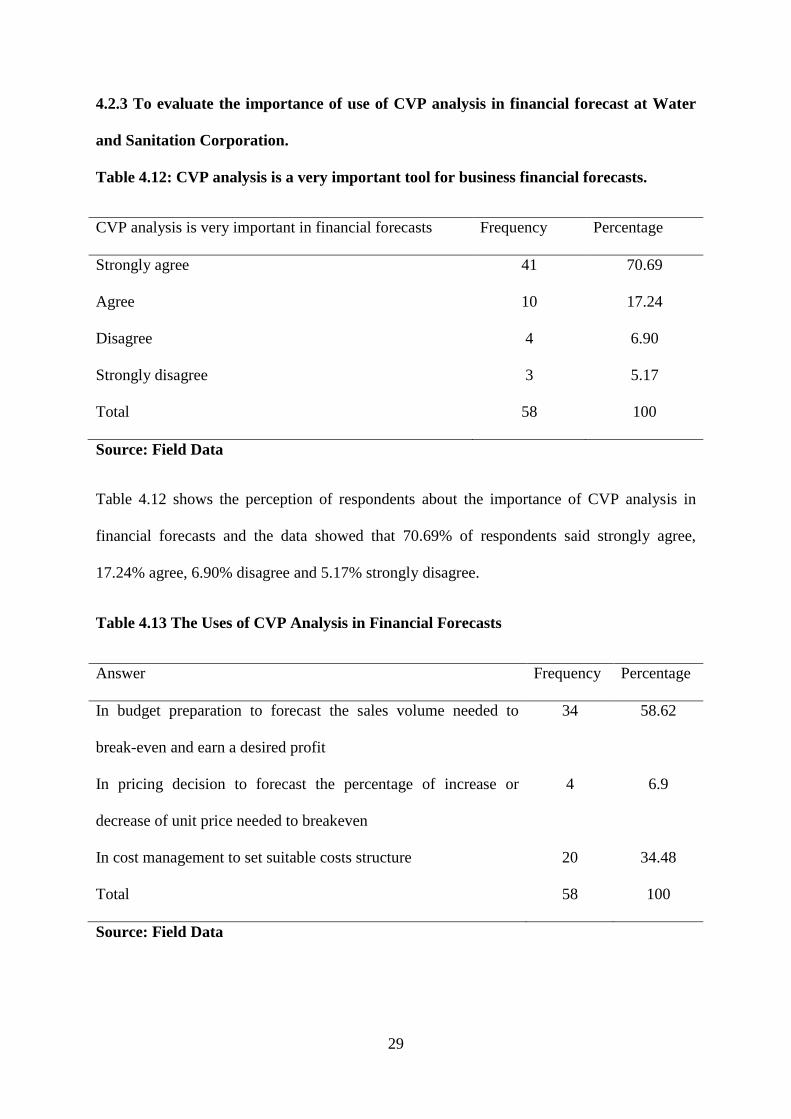

Table 4.12: CVP analysis is a very important tool for business financial forecasts. ............... 29

Table 4.13 The Uses of CVP Analysis in Financial Forecasts ................................................ 29

xi

LIST OF FIGURES

Figure 2.1: C-V-P Analysis Indicators................................................................................. 8

Figure2.2: Conceptual Framework .................................................................................... 13

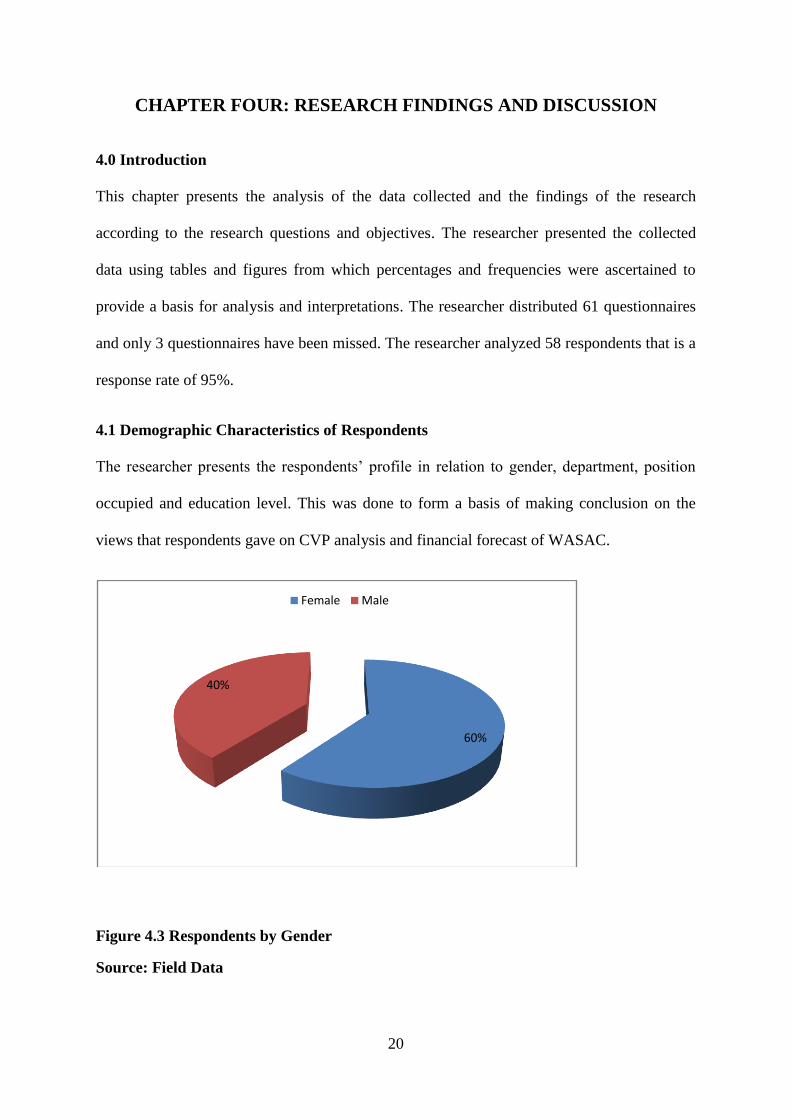

Figure 4.3 Respondents by Gender .................................................................................... 20

xii

LIST OF ACRONYMS AND ABBREVIATIONS

BEP : Break Even Point

CM : Contribution Margin

CVP : Cost Volume Profit

EDPRS : Economic Development and Poverty Reduction Strategy

ELECTROGAZ : Etablissement Rwandais de Distribution de l’Eau, de l’Electricité et

de Gaz (Water, Electricity, and Gaz Distribution Company)

EWSA : Energy, Water and Sanitation Authority

RECO : Rwanda Electricity Corporation

REG : Rwanda Energy Group

REGIDESO : Régie des Eaux (Water Company)

RURA : Rwanda Utility Regulation Agency

RWASCO : Rwanda Water and Sanitation Corporation

WASAC : Water and Sanitation Corporation

xiii

OPERATIONAL DEFINITION OF KEY TERMS

CVP Analysis: is a systematic examination of the relationships among selling prices, sales

and production volume, costs, expenses and profits. Cost-volume-profit analysis provides

management with useful information for decision making. One relationship among cost,

volume and profit is contribution margin.

Contribution Margin: The contribution margin (CM) is the excess of sales over the variable

costs of the product or service. It is the amount of money available to cover fixed costs and to

generate profit. The contribution margin is especially useful in business forecast because it

gives insight into the profit potential of a firm

Financial Forecasts: Future prediction of the business finances.

1

CHAPTER ONE: INTRODUCTION

1.0 Introduction

This chapter covers the background of the study, the problem statement, general and specific

objectives, the research questions, the significance of the study, the limitation of the study,

the scope and the organization of the study.

1.1 Background of the Study

Managers continuously strive to achieve a variety of company objectives such as

maximization of profit, maintenance of or increase in market share and generation of

customer goodwill and loyalty. However to accomplish the organization objectives, managers

must be effective by continually monitoring the costs and the selling prices of their products

(Rainborn, 2009)

Some sectors tend to have a high level of fixed costs and this means high losses will result if

revenue is significantly reduced below the breakeven point. In this regard, most companies

make a tremendous effort to analyze their costs and prices.

While many researchers have used the CVP analysis to help managers in decision making

(e.g. Rainborn, 2009; Choudhary, 2013), not much has been said about the use of CVP

analysis in financial forecast of an organization.

In Rwanda Vision 2020, the Government of Rwanda is committed to continue to invest in

protection and management of water resources, as well as water infrastructure development

to ensure that by 2020 all Rwandans have access to clean water. It is therefore obvious that

the efficiency should be observed in water production and distribution in order to achieve this

goal. The research used a case study of WASAC which is a national utility that distributes

water in Rwanda.

2

WASAC has been in existence as ELECTROGAZ. And ELECTROGAZ was founded in

1939 as REGIDESO by the colonial masters supplying water, electricity and gas to Rwanda-

URUNDI. The company was later divided into REGIDESO Rwanda and REGIDESO

Burundi in 1963. In 1976 REGIDESO Rwanda became ELECTROGAZ and was granted the

monopoly for the production and distribution of water and electricity in the country

(WASAC, 2015)

On 09/09/2008, ELECTROGAZ was split into two parastatals; one charged with electricity

RECO and another with water RWASCO. Based on the law no 43/2000 of 07/12/2010,

RECO and RWASCO have been merged and became EWSA (Office of Prime Minister,

2011)

EWSA was replaced by two independent companies REG and WASAC as the Prime

Minister’s Order no 87/03 of 16/0 8/2014 (Office of Prime Minister, 2014)

WASAC is a private company wholly owned by Government of Rwanda. The core business

of the company is production, distribution and sale of water and sanitation services as well as

development and operation of water and sanitation facilities (WASAC, 2015)

To accomplish its mission WASAC has to incur a high level of fixed costs and this

sometimes results into high losses.

Given that all reforms known by the company were done for to seek the improvement of its

performance, it is also of a paramount importance to carry out a CVP analysis for water to

enable the company to avoid future losses.

1.2 Problem Statement

Given that before generating profit, a company must first reach its break-even point which

means that it must generate sufficient sales revenue to cover all costs (Brock, Herrington, &

Ramey 2009)

3

Water production sector is one of the sectors which tend to have a high level of fixed costs.

This means high losses will result if revenue is significantly reduced below the breakeven

point. Previous operating losses known by WASAC have been greatly associated with a high

level of fixed costs not covered by revenue generated by the utility. With such trend, it is

important for any company to ask and try to answer the question of how costs incurred should

be covered by revenue. The intention of this research was to answer that question by carrying

out a cost volume profit analysis of water for the year ended 30th

June 2015.

1.3 Objectives of Study

The study was conducted to achieve the general and specific objectives as follows;

1.3.1 General Objective

The general objective of this study was to analyse costs, volume and profit for financial

forecast of Water Sanitation Corporation.

1.3.2 Specific Objectives

The study specific objectives are:

i) To determine the sales volume required to break-even and alternatives to break-even at

Water and Sanitation Corporation.

ii) To examine the effects of changes in revenue and costs on profit at Water and Sanitation

Corporation.

iii) To evaluate the importance of use of Costs Volume Profit analysis in financial forecast at

Water and Sanitation Corporation.

1.4 Research Questions

i) What sales volume is required to break-even and what are alternatives to break-even at

Water and Sanitation Corporation?

4

ii) What are the effects of changes in revenue and costs on profit at Water and Sanitation

Corporation?

iii) How important is the use of Cost Volume Profit analysis in the financial forecasts at

Water and Sanitation Corporation?

1.5 Significance of the Study

This study is of great significance. To the researcher, the main purpose of the present

research is to award the Master’s degree in Business Administration of Mount Kenya

University. The study familiarized the researcher to the research techniques and added up on

her knowledge in the research conducting.

To the case study; the findings of this research enabled the management of WASAC to know

the sales volume required to break-even and will contribute to make informed decisions

regarding financial forecasts of the company.

To the Mount Kenya University, this study is very significant as it contributes to existing

literature.

1.6 Limitation of the Study

Organization’s size is a challenge that the researcher faced during the study; WASAC is a big

organization operating in all Provinces of Rwanda and it was not easy for the researcher to

cover all water treatment plants of WASAC.

To overcome this challenge Kimisagara Water Treatment Plant as the main water treatment

plant was used as sample.

The restructure is another challenge that hindered the research as some needed respondents

were not yet have been recruited.

To overcome this challenge the researcher distributed the questionnaires to staff in place.

5

1.7 Scope of the Study

The study covers:

1.7.1 The content scope

The content scope of the study is Cost-Volume-Profit and Financial Forecast

1.7.2 Geographical scope

Geographical scope of this study is WASAC Rwanda, as the monopolistic utility engaged in

water production one of the sectors which tends to have high level of fixed costs.

1.7.3 Time scope

The study covered the year ended 30th

June 2015, the first year of operations of WASAC

after its separation from REG.

1.8 Organization of the Study

This study is composed of five chapters organised as follows: the first chapter covers the

introduction of the study, the background of the study, the problem statement, objectives of

the study; general and specific, research questions, significance of the study, limitation of the

study, scope of the study, and the organization of the study. The second chapter covers the

literature review both theoretical and empirical literature, critical review and research gap

identification, theoretical framework, conceptual framework and the summary of the

literature review. The third chapter deals with research methodology, the research design,

target population, sample design, sample size, sampling technique, data collection methods

and instruments and their administration, reliability and validity, data analysis procedures and

ethical consideration. The fourth chapter contains research findings and discussions. The fifth

chapter deals with summary of findings, conclusions and recommendations.

6

CHAPTER TWO: REVIEW OF RELATED LITERATURE

2.0 Introduction

This chapter involves the systematic identification, location and analysis of documents

containing information related to the research problem being investigated.

In this chapter, the researcher considers the previous studies, works, publications and theories

arrived at by other scholars. Information provided in this chapter was gathered from existing

literature.

2.1 Theoretical Literature

2.1.1 Overview of Cost

According to Ashiq (1997) the cost is defined as resources foregone or sacrificed so as to

achieve a given objective. However Rainborn (2009) suggests that cost reflects the monetary

measure of resources expended to attain an objective such as making a good or delivering a

service.

The costs are either direct or indirect. This classification concerns whether costs have a direct

or indirect relationship to a particular cost object. Direct costs are costs that are related to the

particular cost object and can be traced to it in an economically feasible (cost effective) way.

Whereas indirect costs are costs that are related to the particular cost object but cannot be

traced to it in an economically feasible (cost-effective) way (Horngren, Datar, & Rajan,

2008). Costs can be variable or fixed. This implies how costs behave in relation with activity

level. Variable cost is the cost that changes in total in proportion to changes in the related

level of total activity or volume. And fixed cost as a cost that does not change in total despite

changes in the related level of total activity or volume (Bhimani, Horngren, Datar & Foster,

2008)

7

2.1.2 CVP Analysis and Its Importance in Decision Making

Cost-volume-profit (CVP) analysis is a technique that examines changes in profits in

response to changes in sales volumes, costs, and prices (Hansen & Mowen, 2000).

The CVP analysis is an examination of the cost behaviour patterns that underlie the

relationship among cost, volume of output and profit (Crosson & Needles, 2008).

The CVP analysis examines the behaviour of total revenues, total costs, and operating income

as changes occur in output level, selling price, variable costs, or fixed cost (Horngren, Foster,

Datar & Teall, 2004).

It is very important for managers, account officers and planners to have knowledge of the

relationship between cost and volume of sales as well as the scale with which they impact

profit (Hilton, 2000). Managers use CVP analysis to measure the effect of alternative courses

of action, such as changing variable or fixed costs, expanding or contracting sales volume,

and increasing or decreasing selling price (Crosson & Needles, 2008). It establishes a

relationship between revenues and costs with respect to volumes. It indicates the level of

sales at which costs and revenue are in equilibrium. This equilibrium point is commonly

known as break-even point. Managers also use CVP analysis to make different choices that

can affect selling price, variable cost per unit, fixed costs, units sold and operating income

(Horngren, Datar, and Rajan, 2013) Accountants often perform CVP analysis to plan future

levels of operating activity and provide information about which products or services to

emphasize, the volume of sales needed to achieve a targeted level of profit, the amount of

revenue required to avoid losses, whether to increase fixed costs, how much to budget for

discretionary expenditures and whether fixed costs expose the organization to an

unacceptable level of risk (Horngren, Datar, & Rajan, 2003). By breaking down costs into

fixed versus variable, CVP analysis gives companies strong insight into the profitability of

8

their products or services (Hilton, 2000). With CVP analysis, managers have the ability to

choose the levels of fixed costs in their cost structures (Hinterhuber, 2004). CVP analysis is

useful for pricing, cost control and other financial decisions and the major benefit to using

CVP analysis is that it indicates the lowest amount of business activity necessary to prevent

losses. CVP analysis is a simple tool for financial analysis so as to make a right decision in

business proposals when more than one alternative are available (Choudhary, Patnaik, et al,

2013). Managers can also use CVP relationship to conduct sensitivity analysis to know what

results are likely if selling prices or costs change, or if an underlying assumption changes

(Horngren, Harrison, & Oliver, 2009). CVP analysis plays a larger role in managerial

accounting than in financing accounting. Managerial accounting focuses on helping managers

or those tasked with running businesses make smart, cost effective moves. Financial

accounting, by contrast, focuses more on painting an economic picture of a company so that

outside parties, such as banks or investors, can determine how financially healthy it is

(Martins, 2003).

2.1.3 CVP Analysis Indicators

During the analysis of costs, volume and profit, managers must take into considerations the

following three indicators: contribution margin, break-even point and margin of safety

(Martins, 2003).

Figure 2.1: CVP Analysis Indicators

Source: Martins (2003)

Cost-Volume-Profit Analysis

Contribution Margin Margin of Safety Break Even Point

9

The contribution margin as the difference between total revenues and total variable costs

indicates why operating income changes as the number of units sold changes. The break-even

point is an indicator that tells managers how much they must sell to avoid a loss.

The break-even point is that quantity of output sold at which total revenues equal total costs.

The margin of safety is a risk indicator that stipulates the amount by which sales may decline

before losses are experienced, i.e. the access of actual sales over breakeven sales (Garrison &

Noreen, 2003) Once you've determined your breakeven point, you can use it to examine the

effects of increasing or decreasing the role of fixed costs in your operating structure (Proctor,

2009).

2.1.4 CVP Analysis Techniques

Hansen and Mowen (2000) suggest the three methods used to make CVP analysis as follows:

The equation method;

Revenues − Variable costs − Fixed costs = Operating income

Revenues = Selling price × Quantity of unit sold

Variable Costs = (Variable cost per unit × Quantity of units sold)

The contribution margin method;

Contribution margin per unit × Quantity of units sold − Fixed costs

= Operating income

Contribution margin per unit = Selling price − Variable cost per unit

CM ratio =Unit contribution margin

Unit selling price

At breakeven, operating income is zero

10

$0 = Q × Unit Price − Unit Variable Cost − Fixed Cost

The graph method: In a CVP graph or the break-even chart, unit volume is commonly

represented on the horizontal axis (X) and dollars on the vertical axis (Y). The break-even

point is where total revenue and total expenses lines cross.

2.2 Empirical Literature

In the study called break even analysis in healthcare setup carried out by Choudhary, Patnaik,

et al, (2013) with aim to find out the BEP of health services provided by hospitals and clinics.

The findings of this study revealed that a decline in the output of services cause a shortfall of

revenue that throws the facility left of BEP and into deficit. And recommend the hospital to

close the gap either by increasing price or reducing costs.

The study by Choudhary, Patnaik, et al, (2013) relates to the study of cost volume profit

analysis and financial forecast of WASAC Rwanda as it aimed to find out the BEP of health

services by hospitals and clinics which is the prime specific objective of the study. It also

takes into consideration both effects of increasing prices or reducing costs on operating profit,

and this being the second specific objective of the study. However it differs from the study

due to the fact that the analysis was about health services while this study is about water.

Hinterhuber (2008) carried out a study called value delivery and value-based pricing in

industrial market- an integrative framework for decision making. The aim of the study was to

analyze the extent to which pricing, revenue growth and cost reduction strategy impact on

earnings before interest and tax (EBIT). The study used a sample of fortune 500 companies in

America and showed the pricing as a key profit driver where an increase in selling price of

5% increases EBIT by an average of 22 % while other activities such as revenue growth or

cost reduction tend to have a much smaller impact. Andreas Hinterhuber’s extensive research

11

shows that business effort to increase prices result in higher profitability than those to reduce

costs.

Ericson (2010) detected the effects of changes in prices on contribution margin and realized

that if the selling price increases, it increases the CM ratio and the rate of fixed costs recovery

is increased. The break-even point declines, profit beyond the breakeven point increases and

loss below the break-even point decreases. A decrease in selling price results in decrease in

CM ratio and the rate of fixed costs recovery declines. The break-even point increases.

In the study entitled improving the profitability and reducing costs in retailers by Walker

(2008), the findings revealed that you can improve your profit performance through your

ability to reduce costs, adjust selling price. Where a 1% uplift in pricing, with no loss of sales

volume, creates a 10.5 % uplift net profit and a 1% reduction in variable cost creates an 8.5%

increase in net profit.

The studies by Hinterhuber (2008), Ericson (2010), and Walker (2008), emphasized on

increasing price as the best way to faster the breakeven point, and they ignored the fact that

price is one thing most that a business cannot control. And there are several factors

influencing the managers while making pricing decision such as legal requirements,

competitors’ actions and customer demand (Horngren, et. Al, 2008)

2.3 Critical Review and Research Gap Identification

Given that previous studies have been carried out to find out the ways to improve your profit

through costs reduction and price adjustment, the literature still lacks empirical researches

extended on the relationship between cost and volume of sales as well as the scale with which

they impact profit. Also the costs-volume-profit analysis and financial forecasts literature is

still lacking especially for WASAC Rwanda. And due to lack of such analysis, most

12

companies fail to plan for their future levels of operating activity, the volume of sales needed

to achieve a targeted level of profit, and the amount of revenue required to avoid losses.

In order to solve the problem created by the above situations; cost control, sales projections

and profit planning require an understanding of the relationship between cost and volume of

sales as well as the scale with which they impact profit. To bridge that gap it is necessary to

carry out a CVP analysis as one of the most important tools developed by accountants to

assist management in meeting these challenges, in order to determine the amount of revenue

required to avoid loss (Break-Even Point). This is the intention of this research entitled: “cost

volume profit analysis and financial forecasts of Water and Sanitation Corporation Rwanda”.

Using the CVP analysis the research determines the amount of revenue required to avoid

losses at WASAC. The research also detects the effects of changes in price and changes in

costs on profits, and evaluates the importance of cost volume profit analysis in financial

forecasts of WASAC Rwanda.

2.4 Theoretical Framework

This study was guided by the management accounting theory of cost behaviour, and

according to Horngren, Datar, and Rajan (2013) the CVP analysis is based on the following

assumptions: Change in the level of revenues and costs arise only because of the number of

product units sold, total costs can be divided into a fixed component and a component that is

variable with respect to level of output, the behaviour of total revenues and costs is linear

(straight line) in relation to output unit within relevant range, the unit selling price, unit

variable costs and fixed costs are known. The analysis either covers a single product or

assumes that a given revenue mix of products will remain constant as the level of total units

sold changes. All revenues and costs can be added and compared without taking into account

the time value of money.

13

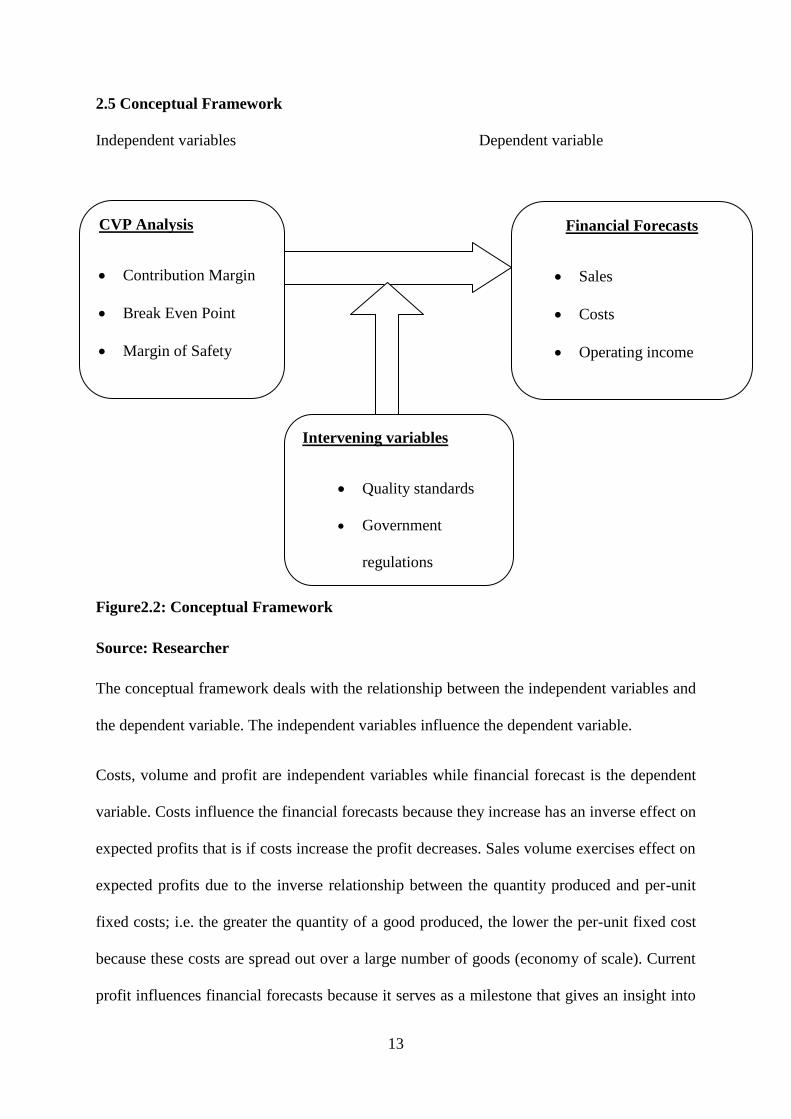

2.5 Conceptual Framework

Independent variables Dependent variable

Figure2.2: Conceptual Framework

Source: Researcher

The conceptual framework deals with the relationship between the independent variables and

the dependent variable. The independent variables influence the dependent variable.

Costs, volume and profit are independent variables while financial forecast is the dependent

variable. Costs influence the financial forecasts because they increase has an inverse effect on

expected profits that is if costs increase the profit decreases. Sales volume exercises effect on

expected profits due to the inverse relationship between the quantity produced and per-unit

fixed costs; i.e. the greater the quantity of a good produced, the lower the per-unit fixed cost

because these costs are spread out over a large number of goods (economy of scale). Current

profit influences financial forecasts because it serves as a milestone that gives an insight into

CVP Analysis

Contribution Margin

Break Even Point

Margin of Safety

Financial Forecasts

Sales

Costs

Operating income

Net Profit

Intervening variables

Quality standards

Government

regulations

14

the profit potential of the firm and enables the firm to adjust their cost structure and unit

selling price in order to achieve a target profit.

However some moderating factors influence the relationship between costs-volume- profit

and financial forecast of WASAC Rwanda. Those factors include water quality standards and

Government regulations. On one hand, for water to be useful, it must be clean and fulfil all

quality standards. This implies that there are costs attached with those standards which cannot

be removed or reduced. On another hand, there are Government regulations in setting prices

for water.

2.6 Summary

The CVP analysis is an important analytical technique used to study relations among costs,

revenues and profits because it allows the business to consider the effect on profits of various

changes in operating costs and revenues such as a reduction in selling price or an increase in

fixed costs; to determine the sales volume required to achieve a specific profit level and to

establish the amount by which the current sales level can decrease before losses are incurred

(Kelly, 2013)

Before generating profit, a company must first reach its break-even point, which means that it

must generate sufficient sales revenues to cover all costs (Rainborn, 2009) The break-even

point is the lower limit of profit when prices are set and margins are determined. And the

lower the break-even point, the higher the surplus and the less the operating risk (Choudhary,

Patnaik, et al, 2013)

It is evident that actual business profitability depends on costs and revenues. Analysis and a

comparison of those two elements with the resultant profit is of great importance in financial

forecasts of the company. In this chapter a number of theories on CVP analysis explaining the

relationship between costs, revenues and the resultant profit have been identified.

15

CHAPTER THREE: RESEARCH METHODOLOGY

3.0 Introduction

This section describes the research methods used in the study and demonstrates where

necessary reasons why certain methods were not be used. These methods were used to collect

data upon which interpretations of findings, conclusions and recommendation were made.

This section covers research design, target population, sample design, data collection

methods, data analysis and ethical consideration.

3.1 Research Design

According to Sekaran and Bougie (2010), after identifying the variables in a problem

situation and developed the theoretical framework, the next step is to design the research in

such a way that the requisite data can be gathered and analyzed to arrive at a solution.

To achieve the study objectives, a descriptive approach was used that is both qualitative and

quantitative methods were used. Quantitative data to be collected through questionnaires was

complemented by the views, opinions and perception of the company staff and management.

3.2 Target Population

The target population was composed of 155 staff of WASAC working in departments directly

involved in production and selling of water (WASAC, 2016)

3.3 Sample Design

The essential requirement of any sample is that it should be as representative as possible of

the population from which is drawn. A sample is said to be representative if the analyses

made on its sampling units produce results similar to those that would be obtained as had the

entire population analyzed (Nachimias & Nachimias, 1987)

16

Moreover the profit and loss account of the year ended 30th

June 2015 shall be analysed using

a CVP analysis method.

3.3.1 Sample Size

The sample size of 61 respondents was obtained using the following formula as suggested by

(Glenn & Israel, 2009):

n =N

1 + N(r)²

Where n=Sample size, N= Target Population and r=Margin of error

N=155, r=0.1, sample size =155

1+155(0.1)²= 61 respondents

3.3.2 Sampling Technique

During this study the purposive or judgmental sampling technique was used to ensure that

only knowledgeable and needed respondents are selected. The respondents were selected

purposively from the departments involved in production and selling of water i.e. water

technical department, finance, commercial department, and Kimisagara water plant.

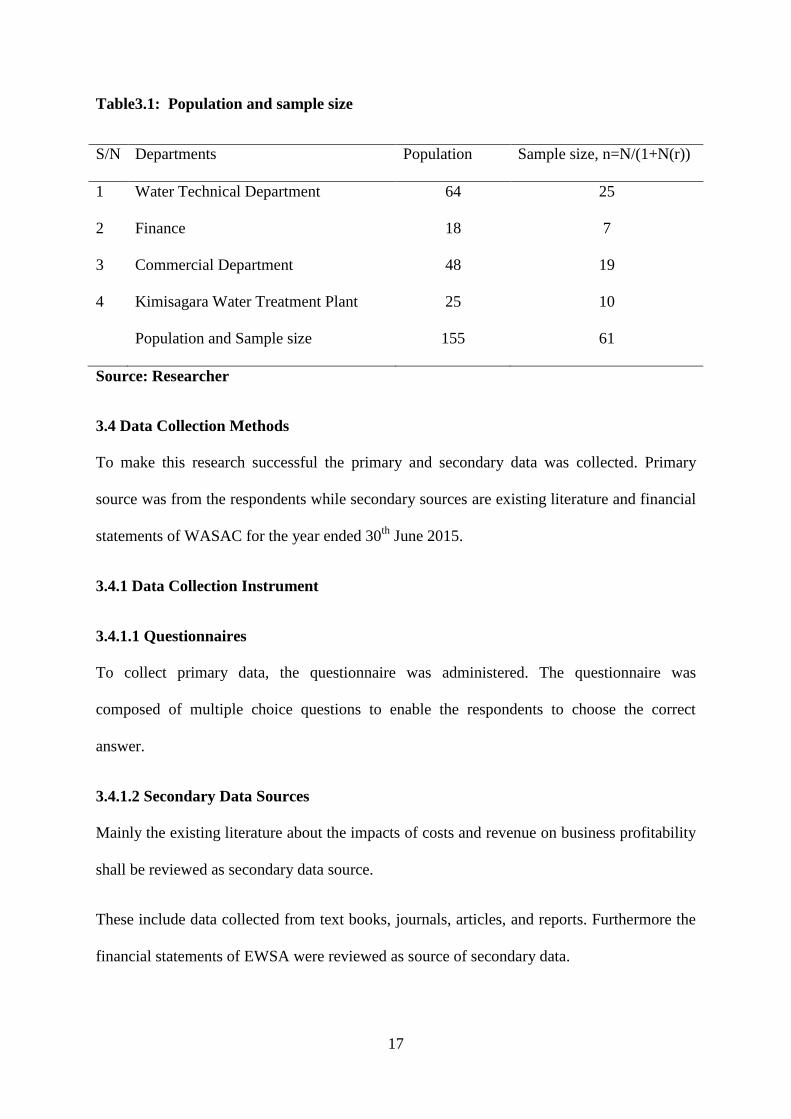

The ascertainment of the sample size is illustrated in the following table.

17

Table3.1: Population and sample size

S/N Departments Population Sample size, n=N/(1+N(r))

1 Water Technical Department 64 25

2 Finance 18 7

3 Commercial Department 48 19

4 Kimisagara Water Treatment Plant 25 10

Population and Sample size 155 61

Source: Researcher

3.4 Data Collection Methods

To make this research successful the primary and secondary data was collected. Primary

source was from the respondents while secondary sources are existing literature and financial

statements of WASAC for the year ended 30th

June 2015.

3.4.1 Data Collection Instrument

3.4.1.1 Questionnaires

To collect primary data, the questionnaire was administered. The questionnaire was

composed of multiple choice questions to enable the respondents to choose the correct

answer.

3.4.1.2 Secondary Data Sources

Mainly the existing literature about the impacts of costs and revenue on business profitability

shall be reviewed as secondary data source.

These include data collected from text books, journals, articles, and reports. Furthermore the

financial statements of EWSA were reviewed as source of secondary data.

18

3.4.2 Administration of Data Collection Instruments

The questionnaires were given to chosen respondents and left for being collected after one

week when they were completed.

3.4.3 Reliability and Validity

According to Ochieng (2009), for a study to be of real meaning, it ought to apply a valid and

reliable instrument. The questionnaire was measured and tested for reliability and validity

before being administered.

The reliability focused on the degree to which the instrument was given similar results over a

number of repeated trials. In this regards, a Test-Retest reliability measure was done to

ascertain reliability. The pilot research of 10 respondents selected among the population of

the study was undertaken. The data from pilot research were tested using Cronbach’s Alpha

Coefficient. After this, unclear questions were removed.

The validity of questionnaire was measured using the following formula:

CVI = n/N

Where,

CVI=Content Validity Index

N=Total number of items in questionnaire

n=Number of relevant item in questionnaire.

𝐶𝑉𝐼 =8

11= 0.73

The interval is from 0 to 1. The closer the value to 1, the more valid the instrument is. Since

the CVI calculated was 0.73, the questionnaire was valid.

19

3.5 Data Analysis

During this study data collected was systematically entered into the computer for further

analysis.

At the end of this study, the collected data have been carefully edited and the work cleaned

from errors that have occurred during data collection and recording such as; incompleteness,

omission, non response or inconsistencies. Then the data were classified, coded and checked

for accuracy and relevancy. To analyse variables, information was obtained using excel

spread sheet and SPSS programme. Data was presented using different statistic tools such as

tables, frequency, charts and graphs. Data has been qualitatively and quantitatively analysed

with statistical procedures.

3.6 Ethical Consideration

The ethical guidelines observed during this study are: honesty, general care, and diligence.

For data collection, the University provided a letter of introduction that was used to request

access to information. After WASAC consent, the introduction of the researcher was made

and the purpose of the study was clearly explained to the respondents. All rights of

respondents were respected. The protection of the research subject privacy is combined with

the confidentiality of the research data.

20

CHAPTER FOUR: RESEARCH FINDINGS AND DISCUSSION

4.0 Introduction

This chapter presents the analysis of the data collected and the findings of the research

according to the research questions and objectives. The researcher presented the collected

data using tables and figures from which percentages and frequencies were ascertained to

provide a basis for analysis and interpretations. The researcher distributed 61 questionnaires

and only 3 questionnaires have been missed. The researcher analyzed 58 respondents that is a

response rate of 95%.

4.1 Demographic Characteristics of Respondents

The researcher presents the respondents’ profile in relation to gender, department, position

occupied and education level. This was done to form a basis of making conclusion on the

views that respondents gave on CVP analysis and financial forecast of WASAC.

Figure 4.3 Respondents by Gender

Source: Field Data

60%

40%

Female Male

21

On distribution of data according to gender, majority of respondents were female that is 35

out of 58 and 23 out of 58 were male corresponding to 60% and 40% respectively.

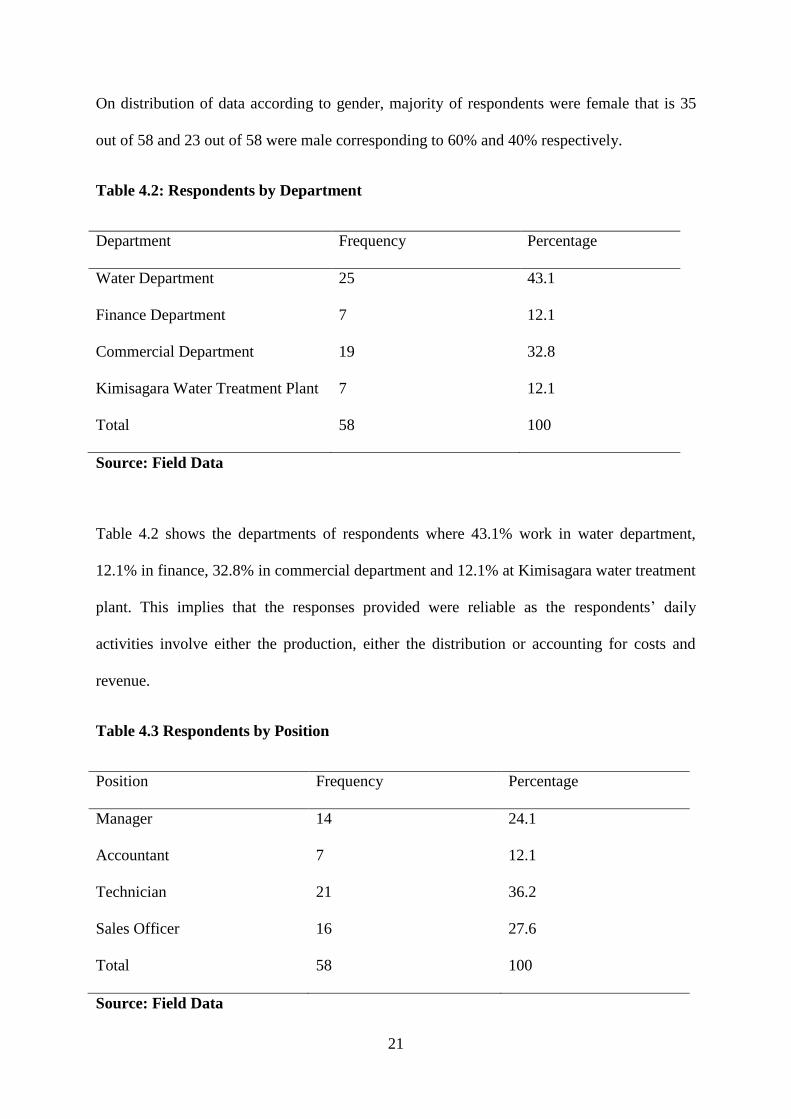

Table 4.2: Respondents by Department

Department Frequency Percentage

Water Department 25 43.1

Finance Department 7 12.1

Commercial Department 19 32.8

Kimisagara Water Treatment Plant 7 12.1

Total 58 100

Source: Field Data

Table 4.2 shows the departments of respondents where 43.1% work in water department,

12.1% in finance, 32.8% in commercial department and 12.1% at Kimisagara water treatment

plant. This implies that the responses provided were reliable as the respondents’ daily

activities involve either the production, either the distribution or accounting for costs and

revenue.

Table 4.3 Respondents by Position

Position Frequency Percentage

Manager 14 24.1

Accountant 7 12.1

Technician 21 36.2

Sales Officer 16 27.6

Total 58 100

Source: Field Data

22

According to the position of respondents, 24.1 % of respondent were managers, 12.1%

accountants, 36.2% technicians and 27.6% were sales officers. This implies that respondents

were in good position to provide the needed information regarding the cost, volume and

profit of the corporation.

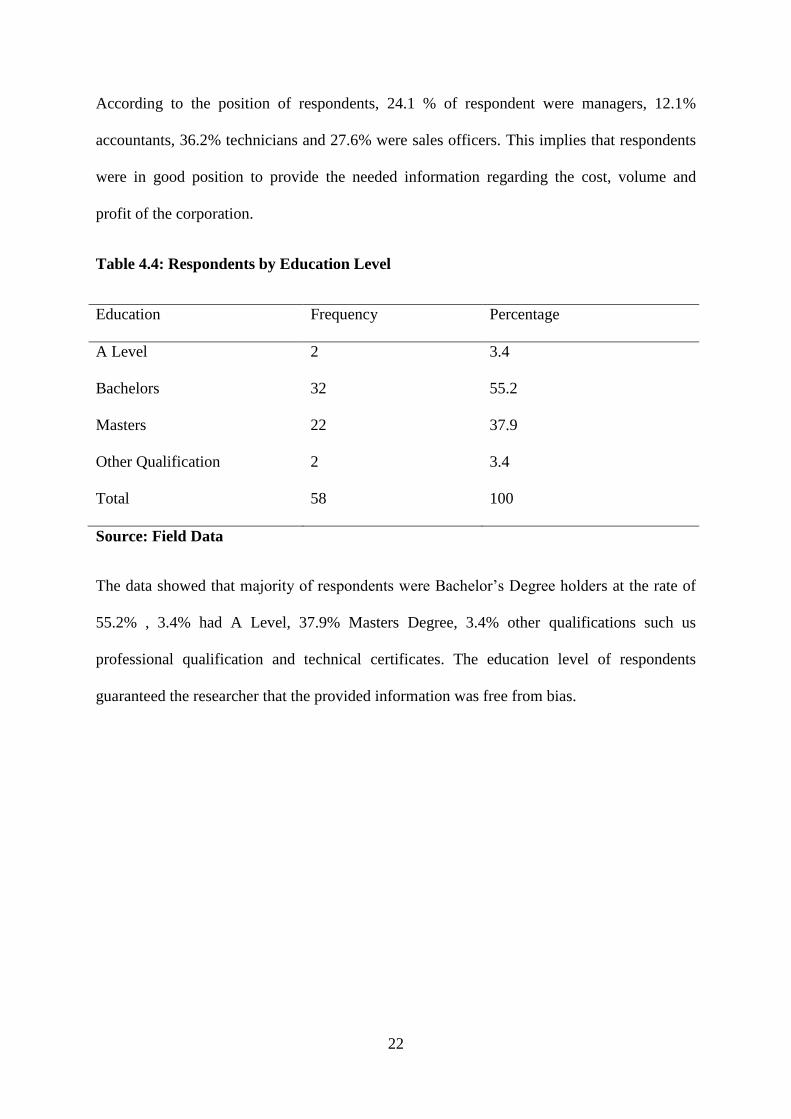

Table 4.4: Respondents by Education Level

Education Frequency Percentage

A Level 2 3.4

Bachelors 32 55.2

Masters 22 37.9

Other Qualification 2 3.4

Total 58 100

Source: Field Data

The data showed that majority of respondents were Bachelor’s Degree holders at the rate of

55.2% , 3.4% had A Level, 37.9% Masters Degree, 3.4% other qualifications such us

professional qualification and technical certificates. The education level of respondents

guaranteed the researcher that the provided information was free from bias.

23

4.2 Presentation of Findings

4.2.1 To determine the sales volume (in Frw) required to break-even and evaluate

possible alternatives to breakeven.

Table 4.5: Marginal Income Statement

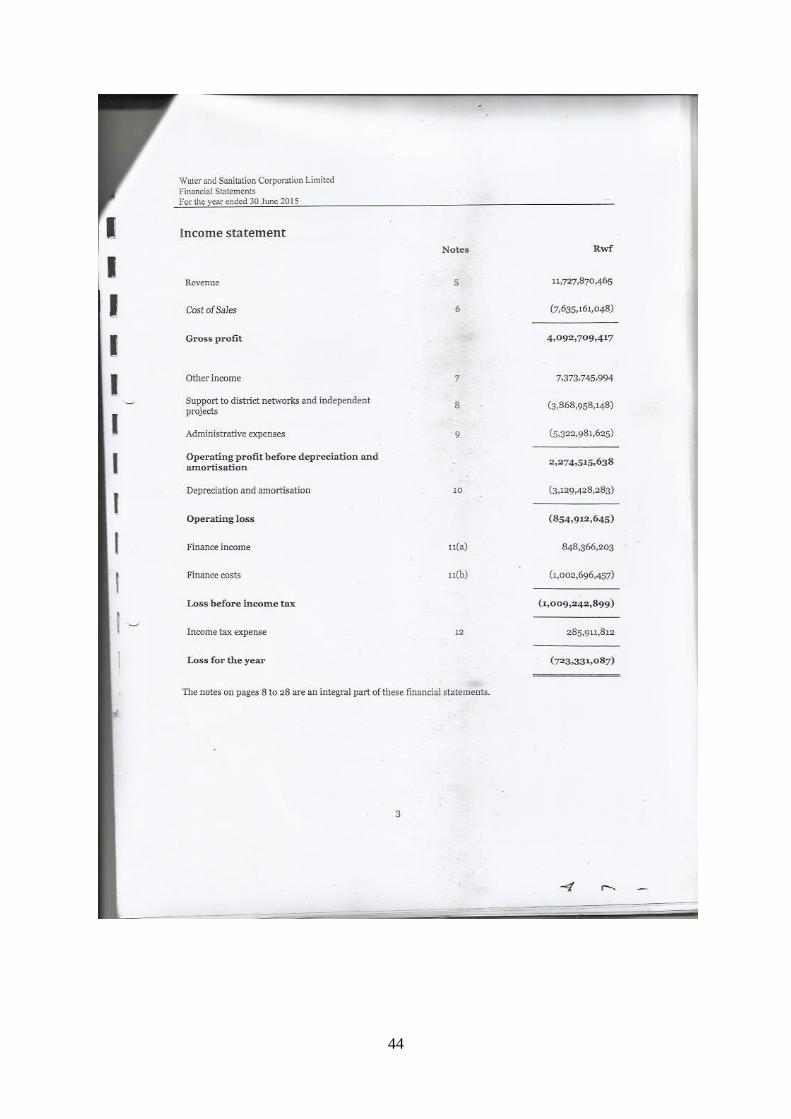

Source: WASAC Financial Statement, 2015

From income statement of WASAC, marginal income statement was prepared and showed a

contribution margin ratio of 67%, an operating loss of Frw (8,382,988,894), the break-even

FRW Percentage

i. Water Sales (Frw 549×21,362,241.28) 11,727,870,465 100%

1 Chemical product 1,039,052,507

2 Repair and maintenance 173,233,916

3 Electricity cost 2,614,845,170

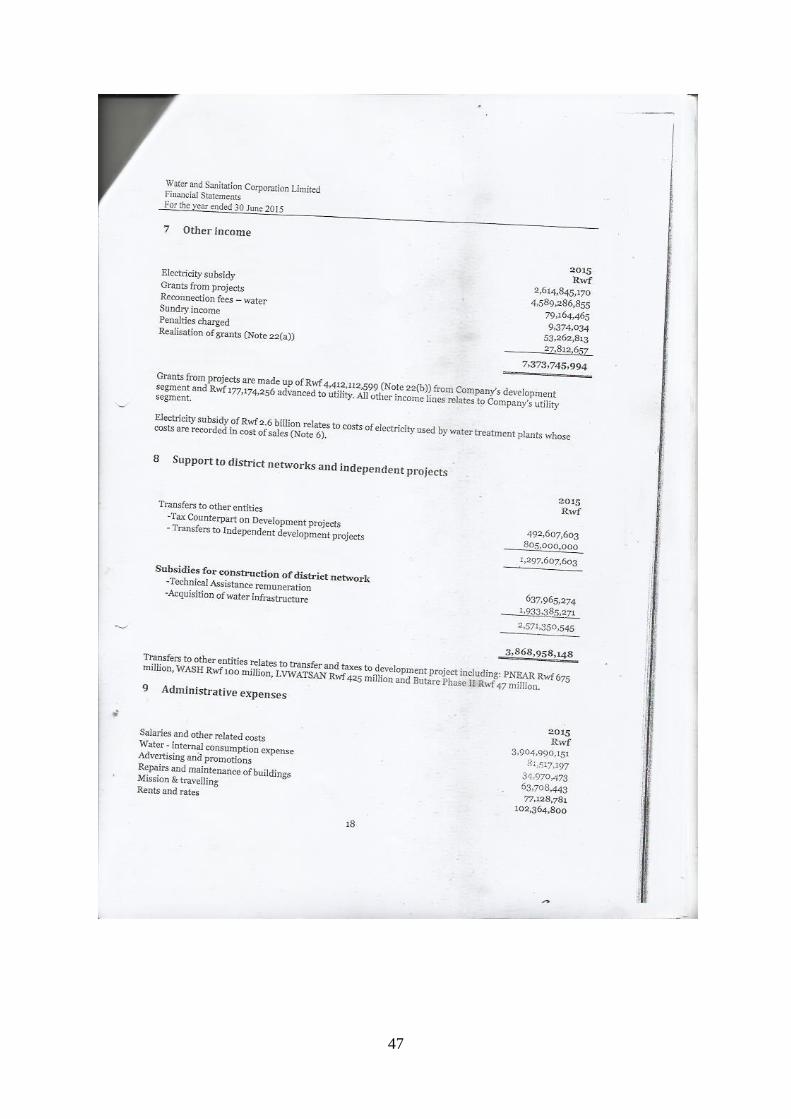

ii. Total Variable Costs/Generation Costs (1+2+3) 3,827,131,593

iii. Contribution Margin (i-ii) 7,900,738,872 67%

4 Distribution Cost 3,808,029,455

5 Support to district networks and independent

projects

3,868,958,148

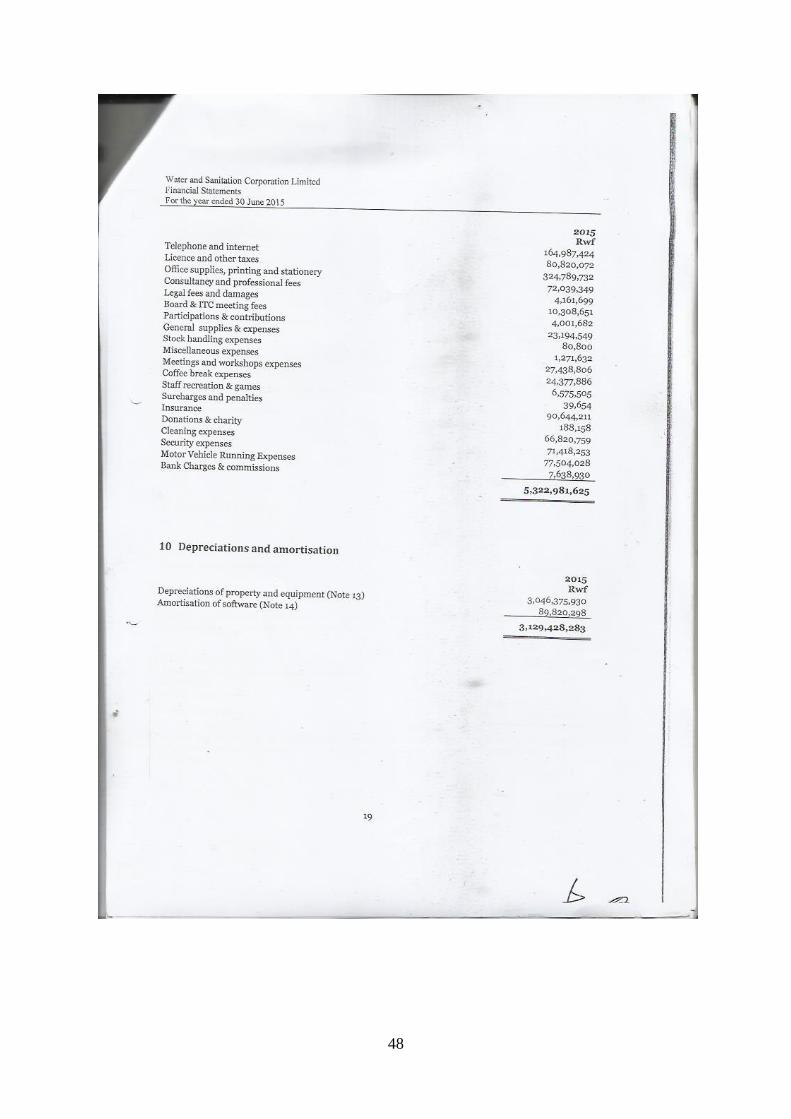

6 Administrative expenses 5,322,981,625

7 Depreciation and amortization 3,129,428,283

8 Finance Costs 154,330,255

iv. Total Fixed Costs (4+5+6+7+8) 16,283,727,766

v. Operating Income/(Loss) (iii-iv) (8,382,988,894 )

vi. Breakeven Point (iv/0.67) 24,171,593,698

vii. Margin of Safety (i-vi) (12,443,723,233)

-106.10%

24

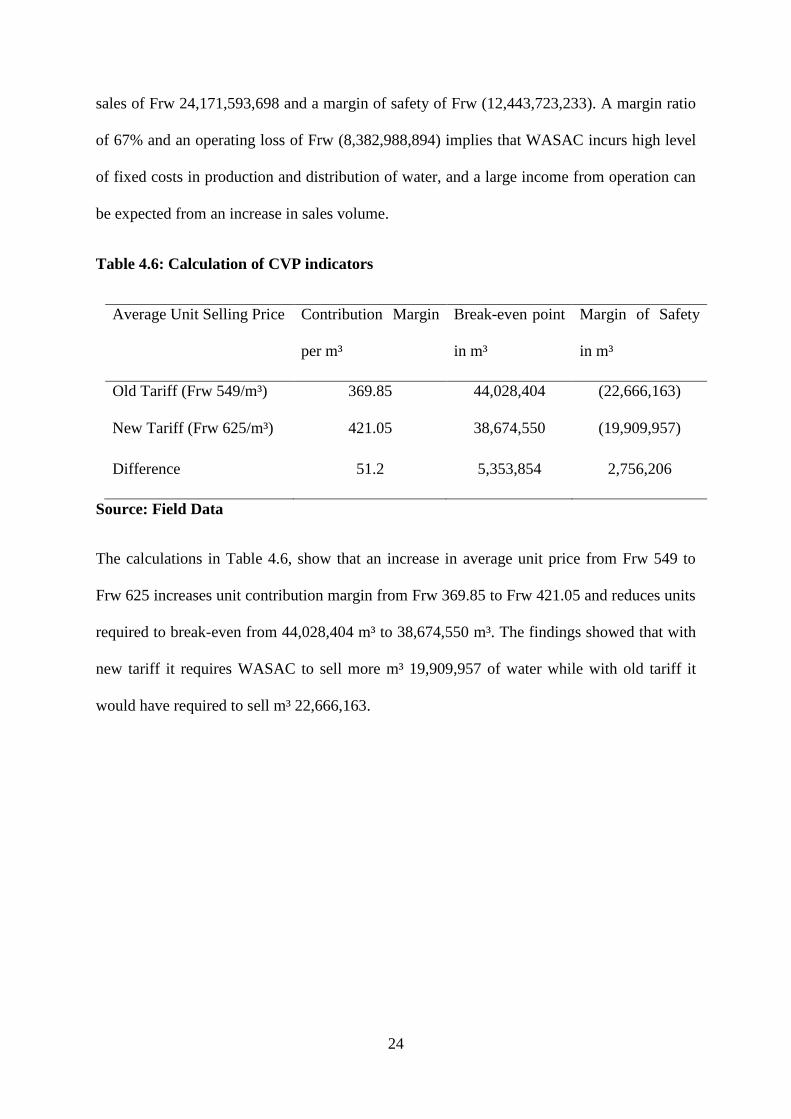

sales of Frw 24,171,593,698 and a margin of safety of Frw (12,443,723,233). A margin ratio

of 67% and an operating loss of Frw (8,382,988,894) implies that WASAC incurs high level

of fixed costs in production and distribution of water, and a large income from operation can

be expected from an increase in sales volume.

Table 4.6: Calculation of CVP indicators

Average Unit Selling Price Contribution Margin

per m³

Break-even point

in m³

Margin of Safety

in m³

Old Tariff (Frw 549/m³) 369.85 44,028,404 (22,666,163)

New Tariff (Frw 625/m³) 421.05 38,674,550 (19,909,957)

Difference 51.2 5,353,854 2,756,206

Source: Field Data

The calculations in Table 4.6, show that an increase in average unit price from Frw 549 to

Frw 625 increases unit contribution margin from Frw 369.85 to Frw 421.05 and reduces units

required to break-even from 44,028,404 m³ to 38,674,550 m³. The findings showed that with

new tariff it requires WASAC to sell more m³ 19,909,957 of water while with old tariff it

would have required to sell m³ 22,666,163.

25

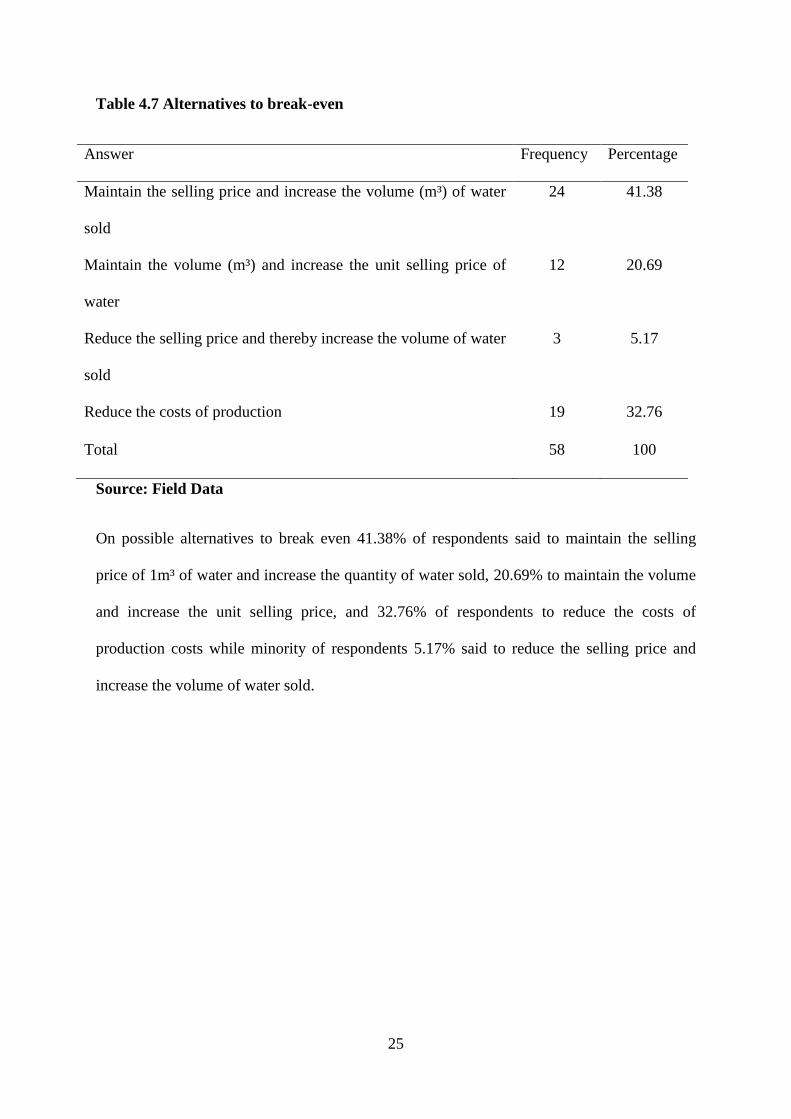

Table 4.7 Alternatives to break-even

Answer Frequency Percentage

Maintain the selling price and increase the volume (m³) of water

sold

24 41.38

Maintain the volume (m³) and increase the unit selling price of

water

12 20.69

Reduce the selling price and thereby increase the volume of water

sold

3 5.17

Reduce the costs of production 19 32.76

Total 58 100

Source: Field Data

On possible alternatives to break even 41.38% of respondents said to maintain the selling

price of 1m³ of water and increase the quantity of water sold, 20.69% to maintain the volume

and increase the unit selling price, and 32.76% of respondents to reduce the costs of

production costs while minority of respondents 5.17% said to reduce the selling price and

increase the volume of water sold.

26

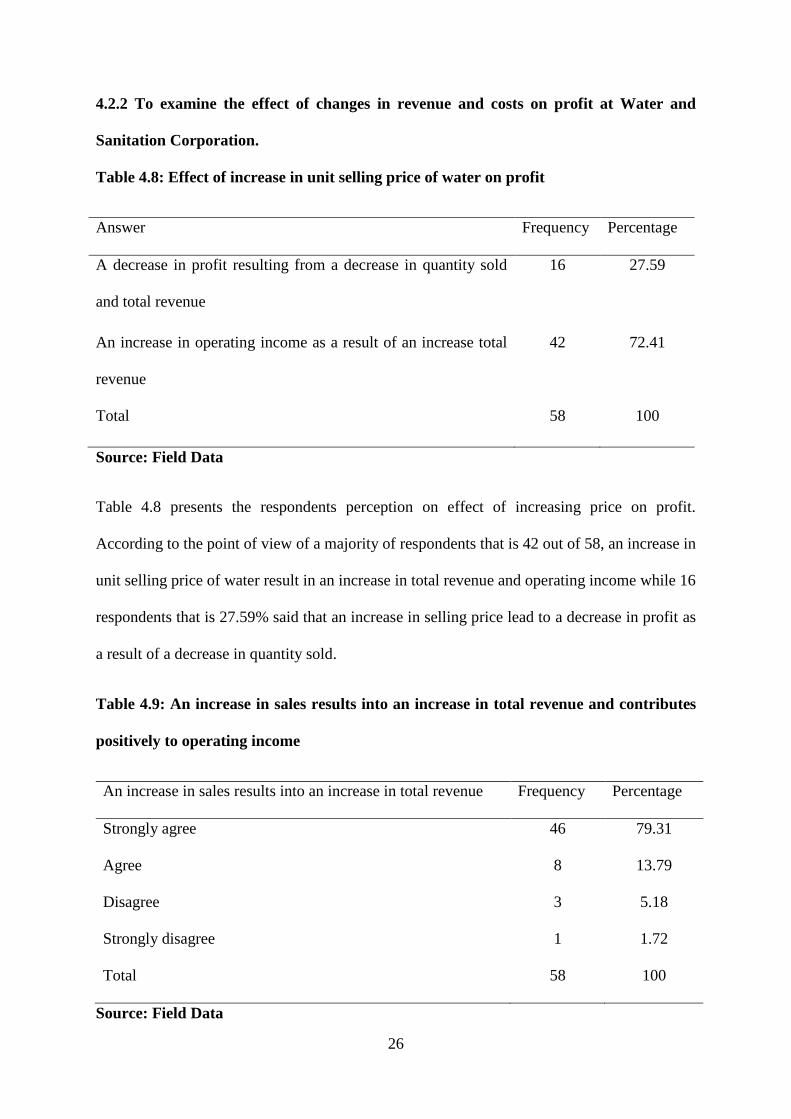

4.2.2 To examine the effect of changes in revenue and costs on profit at Water and

Sanitation Corporation.

Table 4.8: Effect of increase in unit selling price of water on profit

Answer Frequency Percentage

A decrease in profit resulting from a decrease in quantity sold

and total revenue

16 27.59

An increase in operating income as a result of an increase total

revenue

42 72.41

Total 58 100

Source: Field Data

Table 4.8 presents the respondents perception on effect of increasing price on profit.

According to the point of view of a majority of respondents that is 42 out of 58, an increase in

unit selling price of water result in an increase in total revenue and operating income while 16

respondents that is 27.59% said that an increase in selling price lead to a decrease in profit as

a result of a decrease in quantity sold.

Table 4.9: An increase in sales results into an increase in total revenue and contributes

positively to operating income

An increase in sales results into an increase in total revenue Frequency Percentage

Strongly agree 46 79.31

Agree 8 13.79

Disagree 3 5.18

Strongly disagree 1 1.72

Total 58 100

Source: Field Data

27

To evaluate whether an increase in unit sold result into an increase of total revenue and

contributes positively to operating income, the findings revealed that 79.31% of respondents

answered strongly agree, 13.79% agree, 5.18% disagree while 1.72% of respondent strongly

disagree.

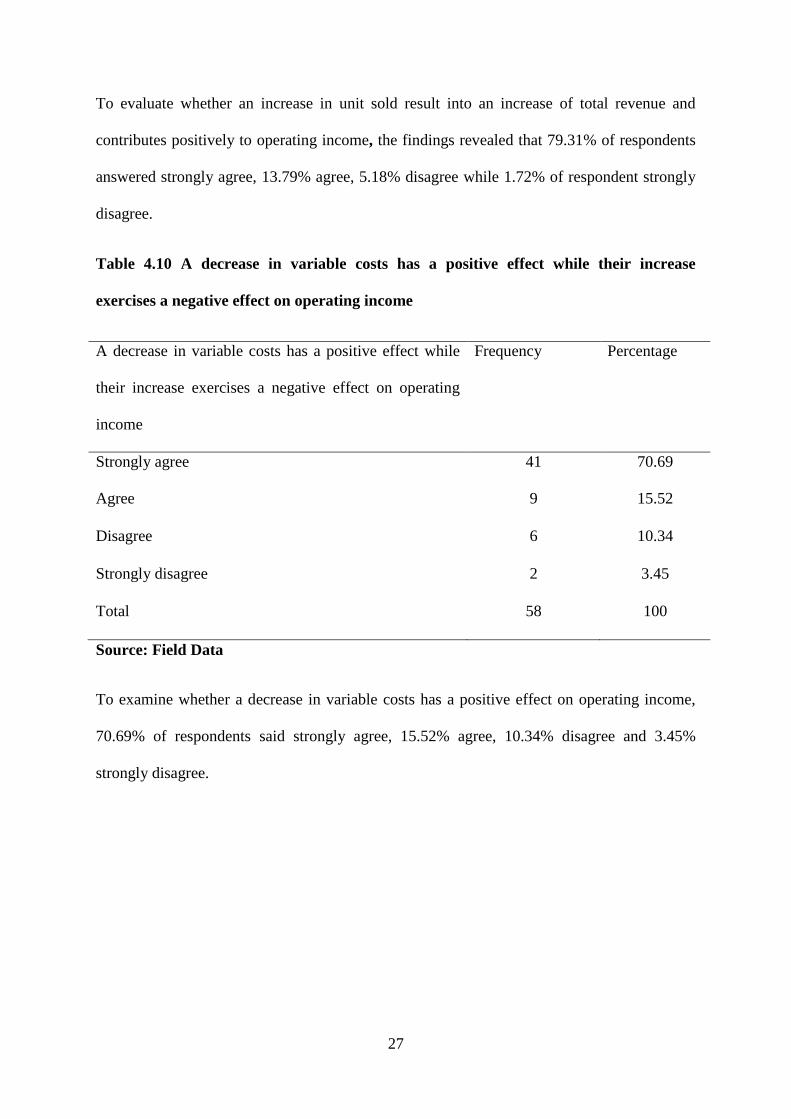

Table 4.10 A decrease in variable costs has a positive effect while their increase

exercises a negative effect on operating income

A decrease in variable costs has a positive effect while

their increase exercises a negative effect on operating

income

Frequency Percentage

Strongly agree 41 70.69

Agree 9 15.52

Disagree 6 10.34

Strongly disagree 2 3.45

Total 58 100

Source: Field Data

To examine whether a decrease in variable costs has a positive effect on operating income,

70.69% of respondents said strongly agree, 15.52% agree, 10.34% disagree and 3.45%

strongly disagree.

28

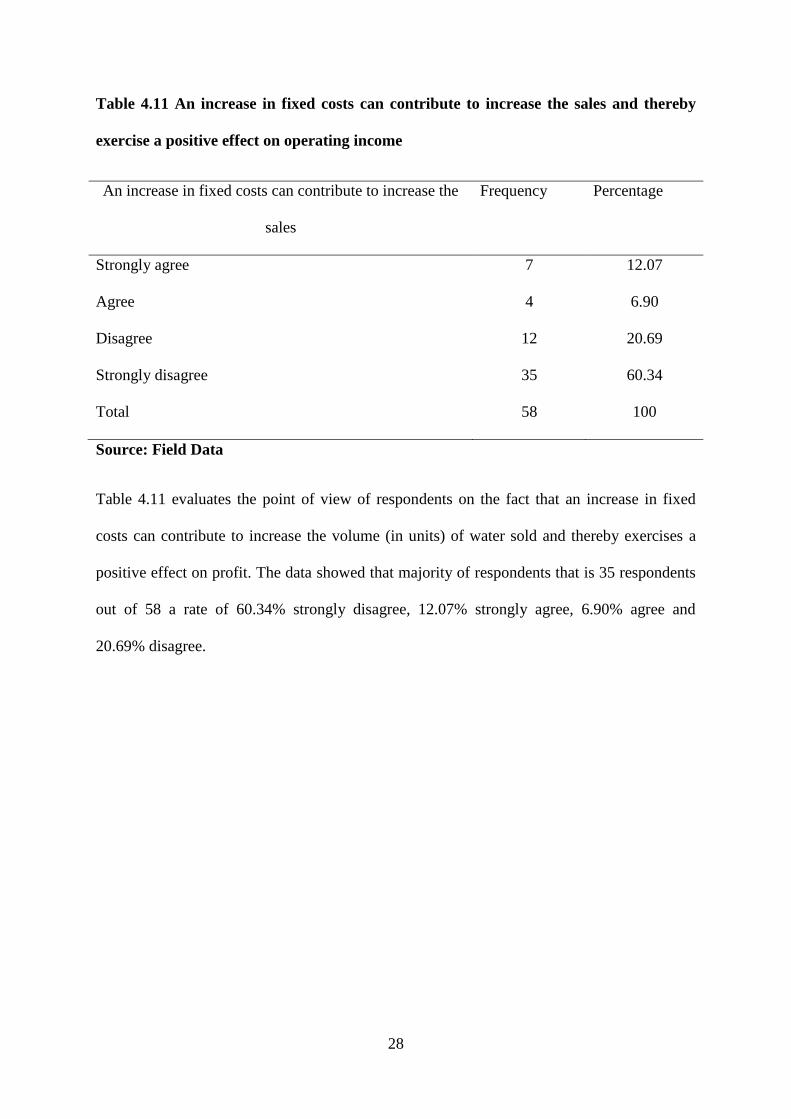

Table 4.11 An increase in fixed costs can contribute to increase the sales and thereby

exercise a positive effect on operating income

An increase in fixed costs can contribute to increase the

sales

Frequency Percentage

Strongly agree 7 12.07

Agree 4 6.90

Disagree 12 20.69

Strongly disagree 35 60.34

Total 58 100

Source: Field Data

Table 4.11 evaluates the point of view of respondents on the fact that an increase in fixed

costs can contribute to increase the volume (in units) of water sold and thereby exercises a

positive effect on profit. The data showed that majority of respondents that is 35 respondents

out of 58 a rate of 60.34% strongly disagree, 12.07% strongly agree, 6.90% agree and

20.69% disagree.

29

4.2.3 To evaluate the importance of use of CVP analysis in financial forecast at Water

and Sanitation Corporation.

Table 4.12: CVP analysis is a very important tool for business financial forecasts.

CVP analysis is very important in financial forecasts Frequency Percentage

Strongly agree 41 70.69

Agree 10 17.24

Disagree 4 6.90

Strongly disagree 3 5.17

Total 58 100

Source: Field Data

Table 4.12 shows the perception of respondents about the importance of CVP analysis in

financial forecasts and the data showed that 70.69% of respondents said strongly agree,

17.24% agree, 6.90% disagree and 5.17% strongly disagree.

Table 4.13 The Uses of CVP Analysis in Financial Forecasts

Answer Frequency Percentage

In budget preparation to forecast the sales volume needed to

break-even and earn a desired profit

34 58.62

In pricing decision to forecast the percentage of increase or

decrease of unit price needed to breakeven

4 6.9

In cost management to set suitable costs structure 20 34.48

Total 58 100

Source: Field Data

30

Table 4.13 shows where CVP analysis is used in financial forecasts, and 58.62% of

respondents selected that CVP analysis should be used in budget preparation to forecast the

sales volume needed to break-even and earn a desired profit, 6.9% of respondents selected

that it should be used in pricing decision to forecast the percentage of increase or decrease of

unit price needed to breakeven, while 34.48% of respondents said that it should be used in

cost management to set suitable costs structure.

31

CHAPTER FIVE: SUMMARY, CONCLUSIONS AND

RECOMMENDATIONS

5.0 Introduction

This chapter presents the summary of the findings, draws conclusion about CVP analysis and

financial forecasts and thereafter comes up with recommendations.

5.1 Summary of Findings

The following is the summary of the details concerning the information collected from the

field during the study.

5.1.1 To determine the sales volume required to break-even and to evaluate alternatives

to break-even at Water and Sanitation Corporation

The primary objective was to determine the sales volume required to break even and to

evaluate possible alternatives to break-even. An analysis of financial statement for the year

ended 30th

June 2015 revealed that for WASAC to break-even, the sales revenue of Frw

24,171,593,698 is required while the revenue of the year was Frw 11,727,870,465. This

implies that to start making profit, WASAC has to increase the revenue by more than

106.10%.

On evaluation of four alternatives available to faster break even, the findings revealed that

alternative quoted number one is that of maintaining the selling price of 1m³ of water and

increasing the quantity of water sold, alternative number two is to reduce the costs of

production costs, alternative number three is to maintain the volume and increase the unit

selling price, and to reduce the selling price and increase the volume of water sold was

quoted the last (see Table 4.7).

32

However there are intervening factors such as Government regulations regarding pricing of

utility services through the tariff established by RURA (Rwanda Utility Regulation Agency),

and water quality standards preventing the company from reducing some costs of production

such as chemicals.

5.1.2 To examine the effect of changes in revenue and costs on profit at Water and

Sanitation Corporation.

The findings showed that an increase in unit selling price of water result in an increase of

total revenue and operating income and does not affect the quantity of water sold (see Table

4.8). The research also found that an increase in units sold result into an increase of total

revenue and contributes positively to operating income (Table 4.9).

To examine whether a decrease in variable costs has a positive effect on operating income,

70.69% of respondents selected strongly agree, 15.52% agree, 10.34% disagree and 3.45%

strongly disagree. This leads to confirm that a decrease in variable costs has a positive effect

on operating income.

The findings lead to confirm that for water any increase in either fixed or variable cost

exercises a negative effect on profit. Hence costs should be reduced or minimized. However

the intervening variable of quality standards imposes on cost minimization.

5.1.3 To evaluate the importance of use of CVP analysis in financial forecast at Water

and Sanitation Corporation.

To evaluate the importance of CVP analysis in financial forecasts, the findings presented in

Table 4.9 showed that CVP analysis plays a virtual role in business financial forecasts. The

distribution of data revealed that it is most useful in budget preparation to forecast the sales

volume needed to break-even and earn a desired profit, and in cost management to set

suitable costs structure. This implies that at WASAC the use of CVP analysis in budget

33

preparation to forecast the sales volume needed to break-even and earn a desired profit out

weight other uses discussed in Table 4.13.

5.2 Conclusion

The study indicates that for WASAC to break-even, it requires to increase the sales revenue

by 106.10%. The research also revealed that an increase in unit selling price of water has a

positive effect on profit as a decrease in fixed and variable costs. As RURA adjusted water

tariff upward to an average of Frw 625/m³ from Frw 549/m³ with effect from September 01,

2015, it requires WASAC to produce m³ 38,674,550 instead of m³ 44,028,404 that would

have been produced if the price remained as it was before i.e. an average price of Frw

549/m³. This implies ceteris paribus, an increase in unit selling price help to faster the break-

even.

The research shows that CVP analysis is an important management tool that should be used

by WASAC to forecast the sales volume needed to break-even and earn a desired profit.

34

5.3 Recommendations

The research recommends the management of WASAC to use CVP analysis as a managerial

tool for financial forecast and such analysis should be performed while preparing budgets

especially sales budget and before cost commitment. The study also recommends the

management of WASAC to concentrate their effort on increase of sales volume and minimize

indirect costs especially administrative costs.

5.4 Suggestions for further study

During the study process the needs of further research were expressed. The cost benefit

analysis of water projects is suggested as further study to enable the management of WASAC

to evaluate the returns on investments made in various water projects.

35

REFERENCES

Ashiq, H. (1997). Cost accounting made easy. Nairobi: East Africa Publisher Ltd.

Bhimani, A., Horngren, C. T., & Foster, G. (2008). Management and cost accounting (Vol.

1). Pearson Education

Brock, H.R., Herrington, A.L., & Ramey, G.L. (2009). Cost accounting, principles and

applications, 7th

Edition. Toronto: Financial Times Prentice Hall.

Choudhary, PK., Patnalk, SK., Singh, MM., Kaushal, G. (2013), Break-even analysis in

healthcare setup. Int J Res Foundation Hosp Healthc Adm p29-32.

Colin, D. (1995). Management and cost accounting. London: Chapman & Hall.

Colin, D. (2007). Management and cost accounting. London: Cengage Learning EMEA.

Colin, D. (2008). Management and cost accounting, 7th

Edition. London: Pat Bond.

Crosson, V.S., & Needles. E.B. (2008). Managerial accounting, 8th

Edition. London:

Cengage Learning.

Ericson, R.N. (2010). The new standards for linking business performance and executive

incentive pay. New Jersey: John Wiley & Sons Inc. Hoboken.

Garrison, R.H., & Noreen, E.W. (2003).Managerial accounting. 10th

Edition. Boston:

McGraw-Hill Irwin.

Glenn, D., & Israel. (2009). Determining sample size. Gainesville: University of Florida.

Hansen, D. & Mowen, M. (2000). Cost management, accounting and control, 5th

Edition.

South Western College Publishing/Thomson Learning.

Hilton. W.R. (2000). Managerial accounting. creating value in a dynamic environment 5th

Edition. New York: McGraw-Hill Companies, Inc.

36

Hilton. W.R. (2009). Managerial accounting. creating value in a dynamic environment 8th

Edition. New York: McGraw-Hill Irwin.

Hinterhuber, A. (2008). Value delivery and value-based pricing in industrial markets.

Advances in Business Marketing and Purchasing, 14(1), 381-448.

Horngren, C.T., Datar, S.M., & Rajan, M.V. (2013). Cost accounting, a managerial

emphasis, 14th

Edition. Toronto: Paerson Prentice Hall.

Horngren, C.T., Datar, S.M., & Rajan, M.V. (2004). Cost accounting, a managerial

emphasis. Toronto: Paerson Prentice Hall.

Horngren C.T, Harrison W.T., & Oliver M.S. (2009). Accounting, 8th

Edition. London:

Paerson Education International

Horngren, C.T., Sundem, G.L. Stratton, W.o., Burgstahler, D., & Schatzberg, J. (2008).

Managerial accounting. 14th

Edition. Toronto: Paerson International Edition.

Horngren, Foster, Datar, & Teall. (2003). Cost accounting. 3rd

Edition. Toronto: Paerson

Prentice Hall.

Horngren, C. T., Foster, G., & Datar, S. (1994). Cost accounting: A managerial emphasis.

8th

Edition. New Jersey: Prentice-Hall.

Horngren, C. T., Sundem, G. L., Schatzberg, J. O., & Burgstahler, D. (2013). Introduction to

management accounting. Pearson Higher Ed.

Jiambalvo, J. (2001). Managerial accounting. New York: John Wiley & Sons, Inc.

Koltrer, P., Wong V., Saunders, J., Armstrong G. (2005). Principles of marketing, 4th

European Edition. Toronto: Paerson Prentice Hall.

37

Maher, M.W., & Deakin, E.B. (1994). Cost accounting, 4th

Edition. New York: McGraw-Hill

Irwin.

Martins, E. (2003). Cost accounting, 9th

Edition. New York: McGraw-Hill.

Nachimias, D., & Nachimias, C. (1987). Research methods in the social sciences 3rd

Edition.

New York: St. Martin’s Press.

Ochieng, F. (2009). Reasearch methodology, A simplified version to passing research

methods with model past paper questions. New York: McGraw-Hill.

Office of Prime Minister, (2011). Official gazette no. 4 bis of 24/01/2011

Office of Prime Minister, (2011). Prime Minister’s order no. 87/03 of 16/08/2014

Proctor, R. (2009). Managerial accounting for business decisions, 3rd

Edition. Toronto:

Paerson Education Limited.

Rainborn, K.(2009), Cost accounting: foundations and evolution. International Student

Edition. New York: McGraw-Hill Irwin

Rajeev, N. (2008). Inventory management performance in Indian machine tool SMEs: What

factors do influence them?.Thailand: Bank of Thailand.

Ronald, H.W. (2002). Managerial accounting, creating value in a dynamic environment 5th

Edition. New York: McGraw-Hill Companies, Inc.

Rosemarie K. (2013). Cost volume analysis. Management accounting, 3, 1-4.

Sekaran, U. & Bougie, R. (2010). Research methods for business A skill building approach,

5th

Edition. John Wiley & SonsLtd, West Susex, Po198Sq, United Kingdom.

38

Walker, D. (2008). Improving profitability and reducing costs in retailer, using activity based

costing. White paper, WP3111-A, Business objects an SAP Company, 1-32

39

APPENDICES

40

APPENDIX ONE: AUTHORIZATION LETTER

41

APPENDIX TWO: DATA COLLECTION

42

APPENDIX THREE: WASAC INCOME STATEMENT FOR THE YEAR

ENDED 30 JUNE 2015

43

44

45

46

47

48

49

50

APPENDIX FOUR: QUESTIONNAIRE FOR WASAC STAFF AND

MANAGEMENT

Dear Respondents,

My name is Clementine Imanishimwe, a student at Mount Kenya University pursuing a

Master’s Degree of Business Administration, option Accounting and Finance. I am currently

currying out a study for the purpose of writing a dissertation as a requirement for the award

of Master of Business Administration. The topic of the study is: “COST VOLUME PROFIT

ANALYSIS AND FINANCIAL FORECAST OF WATER AND SANITATION

CORPORATION RWANDA”.

You have been selected to participate in this study due to the importance of your information

in the study. I am humbly requesting you to assist me by sacrificing the part of your time and

respond the questions in this research instrument according to your opinion, knowledge and

judgement. The information you will provide will be highly valued, restricted to academic

purpose and treated with utmost confidentiality.

Thank you for your cooperation.

IMANISHIMWE Clementine

51

Instructions

a. Tick the box for the right answer

b. Chose only one best answer for each question

Section A: Respondents profile

1. Gender:

Female

Male

2. Department:

Water Technical Department

Finance

Commercial Department

Kimisagara Water Treatment Plant

3. Position occupied in WASAC:

Manager

Accountant

Technician

Sales officer

4. Education Level

A Level

Bachelors

Masters

PHD

Others qualifications (CPA, ACCA,...)

52

Section B: CVP Analysis and Financial Forecast of WASAC

i) To determine the sales volume in FRW required to break-even and evaluate

alternatives to break-even at Water and Sanitation Corporation.

5. To break even, the management of WASAC should:

1) Maintain the selling price and increase the volume (m³) of water sold

2) Maintain the volume (m³) and increase the selling price of water

3) Reduce the selling price and thereby increase volume

4) Reduce the costs of production

ii) To examine the effect of changes in revenue, variable costs, and fixed costs on profit

at Water and Sanitation Corporation.

6. An increase in selling price per unit of water may result into:

1) A decrease in sales volume (units) followed by a decrease in operating

income

2) An increase in total revenue, thereby an increase in operating income

7. An increase in total revenue result into an increase of operating income with the

same proportion

1) Strongly agree

2) Agree

3) Strongly Disagree

4) Disagree

8. A decrease in variable costs has a positive effect while their increase exercises a

negative effect on operating income

1) Strongly agree

2) Agree

3) Strongly Disagree

53

4) Disagree

9. An increase in fixed costs (such as advertising) may contribute to an increase of

volume (quantity) and thereby a positive effect on operating income

1) Strongly agree

2) Agree

3) Strongly Disagree

4) Disagree

iii) To evaluate the importance of CVP analysis in financial forecast at Water and

Sanitation Corporation.

10. The CVP analysis is a very important tool to use in business financial forecast.

1) Strongly agree

2) Agree

3) Strongly Disagree

4) Disagree

11. According to your perception how the CVP analysis is useful in financial forecast

of WASAC?

1) The CVP analysis can be used in sales budget preparation to forecast

the sales volume needed to break-even and earn a desired profit

2) The CVP analysis can be used in pricing decision to forecast the

percentage at which the selling price should be raised or reduced to

break-even and earn a desired profit

3) The CVP analysis can be used in cost management to set suitable

costs structure