Analysis of performance of cost volume profit (CVP) analysis ...

128

The University of Dodoma University of Dodoma Institutional Repository http://repository.udom.ac.tz Business Master Dissertations 2013 Analysis of performance of cost volume profit (CVP) analysis in manufacturing companies in Tanzania: a case of Tanzania Portland Cement Company (TPCC) Ndongolo, Rahabu P The University of Dodoma Ndongolo, R.P. (2013). Analysis of performance of cost volume profit (CVP) analysis in manufacturing companies in Tanzania: a case of Tanzania Portland Cement Company (TPCC). Dodoma: The University of Dodoma http://hdl.handle.net/20.500.12661/1751 Downloaded from UDOM Institutional Repository at The University of Dodoma, an open access institutional repository.

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Analysis of performance of cost volume profit (CVP) analysis ...

The University of Dodoma

University of Dodoma Institutional Repository http://repository.udom.ac.tz

Business Master Dissertations

2013

Analysis of performance of cost volume

profit (CVP) analysis in manufacturing

companies in Tanzania: a case of

Tanzania Portland Cement Company (TPCC)

Ndongolo, Rahabu P

The University of Dodoma

Ndongolo, R.P. (2013). Analysis of performance of cost volume profit (CVP) analysis in

manufacturing companies in Tanzania: a case of Tanzania Portland Cement Company (TPCC).

Dodoma: The University of Dodoma

http://hdl.handle.net/20.500.12661/1751

Downloaded from UDOM Institutional Repository at The University of Dodoma, an open access institutional repository.

ANALYSIS OF PERFORMANCE OF COST VOLUME PROFIT (CVP)

ANALYSIS IN MANUFACTURING COMPANIES IN TANZANIA - A CASE

OF TANZANIA PORTLAND CEMENT COMPANY (TPCC))

Rahabu Philip Ndongolo

Dissertation Submitted in Partial Fulfillment of the Requirements for the Degree of

Master of Business Administration of the University of Dodoma

The University of Dodoma

October, 2013

i

CERTIFICATION

The undersigned certification that I have read and hereby recommend to the senate

for acceptance, a dissertation entitled; Analysis of Performance of Cost Volume

Profit (CVP) Analysis in Manufacturing Companies in Tanzania - a Case Of

Tanzania Portland Cement Company (TPCC)) in a partial fulfillment of the

requirement for the degree of Masters of Business Administration (MBA) of the

University of Dodoma.

…………………………………………

Professor Inderjeet Singh Sodhi

(SUPERVISOR)

Date………………………….

ii

DECLARATION AND COPYRIGHT

I, Rahabu Philip Ndongolo hereby proclaim that this dissertation is an outcome of

my personal research work with the exception of the literature acted, which served as

a source of information. This work is in no way a duplicate in any party or in whole

of a work ever presented for the award of a degree or publication. I further confirm

that works by other authors, which were used as references and resource material

have been acknowledged.

Signature ……………………………….

(HD/UDOM/169/T.2010)

This dissertation is a copyrighted material under the author, the copyright Act of

1999 and other national and international acting. In that behalf, none of the material

of this work may be reproduced in full or part, stored in any retrieval system, or

transmitted in any form or by any means without prior written permission of the

Directorate of Post Graduate Studies on behalf of both the author and the University

of Dodoma.

iii

ACKNOWLEDGEMENT

Magnificence, respect, brilliance, perfectibility, sovereignty and celebrity are

credited unto the Almighty God who in his immeasurable affection steered me to the

successful completion of this study. Wholeheartedly, I am in meagreness of the

words to express my indebtedness to him.

This dissertation would not have been possible without the guidance and the help of

several individuals who in one way or another contributed and extended their

valuable assistance in the preparation and completion of this study.

First and foremost, I would like to reveal my utmost gratitude to Professor

INDERJEET SIGH SODHI for his tireless, perfectly, sincerity and encouraging

supervision. I also admirably express my gratitude to Dr. AME for his

encouragement and guides on the preparation of and completion of this report

together with the management and all staff of the University of Dodoma (UDOM). I

am thankful to management and other staff of TPCC for consenting me to collect

data at their company.

More specifically, to my lovely husband Wilbert Fabian for his delightful support

and encouragement and lovely sons Dickson and David for keeping me busy but

pleased. To my parents Mr. and Mrs. Kalugira for their prayers and encouragement,

may God bless them! Finally, is the heartfelt thanks to all my wonderful friends

Sylvestry January, Annastanzia Majenga, Khalid Karabaki and Frank Mkomochi for

their contribution in my studies.

iv

DEDICATION

This study is dedicated to my cherished husband Mr. Wilbert and my children

Dickson and David for their endless love, encouragement and support for

accomplishment of this work.

v

ABSTRACT

This paper presents the study on the subject of the analysis of performance of Cost

Volume Profit (CVP) analysis in manufacturing companies in Tanzania, a case of

Tanzania Portland Cement Company. Cost volume profit analysis is a model which

is used to plan profit. The general objective of this study was to determine if CVP

can assist management in formulating pricing policies by projecting the effect of

different price structures on cost and profit and to highlight the usefulness of CVP

analysis in manufacturing companies in Tanzania. Specifically, this study desired to

understand the relevancy and efficiency of Cost Volume Profit analysis as a

decisions model in helping manufacturing business to face the challenges caused by

the ever changing business environment predominantly in Tanzania, as policy

makers in making relevant policies.

A case study survey type of research was used in which a sample from the target

population was selected as a source of information needed to achieve researcher‟s

objectives. Consequently, random probability sampling and non-random sampling

were selected. This study included both qualitative and quantitative data. Thus, the

researcher collected data by administering a questionnaire along with interviews to

pave the way for easy analysis of data. Focus group discussion was also conducted

for top management team and employees who are working in management

accounting unit as well as production manager.

The analysis showed that, CVP analysis, though it is a very useful tool for decision

making, is based upon certain assumptions which can rarely be completely realized

vi

in practice. This leads managers and policy makers to forget about the usefulness of

the model and conclude that CVP is not effective and efficient technique for decision

making. In presented enterprise, CVP analysis seemed to be not well known and

hence not applied for managers to find out and decide what to do to improve business

and get planned values of certain indicators.

Due to competition and complexity of the structure of production, traditional

management accounting techniques are not giving the fruitful result to response to

the keen competition. Thus, manufacturing organizations have to adopt advanced

management accounting techniques. Therefore, policy makers should pave the way

for policy implanters to select the model for decision making and test the sensitivity

of the model with alternative scenarios and judge which outcome best describes their

beliefs about the future. To help managers make better decisions, accountants should

evaluate the quality of the techniques they use, given the organizational setting and

decisions to be made.

vii

TABLE OF CONTENTS

Title ……………………………………………………………………………. i

Certification …………………………………………………………………… ii

Declaration and Copyright…………………………………………………….. iii

Acknowledgement……………………………………………………………… iv

Dedication ……………………………………………………………………… v

Abstract ………………………………………………………………………… vi

Table of Contents …………………………………………………………......... viii

List of Table …………………………………………………………………… xiv

List of Figure …………………………………………………………………. xv

List of Abbreviations ………………………………………………………… xvi

CHAPTER ONE: GENERAL INTRODUCTION…………………………… 1

1.0 Introduction…………………………………………………………………. 1

1.1 Background to the Study ………………………………………………….. 1

1.1.1 CVP Analysis; an Overview……………………………………………… 1

1.1.2 Economists versus Accountants view of CVP Analysis…………………. 2

1.2 Statement of the Problem ………………………………………………… 4

1.3 Objectives of the Study…………………………………………………… 8

1.3.1 General Objective ………………………………………………………. 8

1.3.2 Specific Objectives ……………………………………………………… 8

1.4 Research Questions ……………………………………………………….. 8

1.5 Significance of the Study …………………………………………………. 9

1.6 Scope of the Study ………………………………………………………… 9

1.7 Limitations of the Study …………………………………………………… 11

viii

1.8 Conclusion ………………………………………………………………… 12

CHAPTER TWO: LITERTURE REVIEW ………………………………. 13

2.0 Introduction ………………………………………………………………. 13

2.1 Theoretical Review of Literature………………………………………… 14

2.1.1 The Concept of Cost Volume Profit (CVP) Analysis ……………….... 14

2.1.2 Definitions of Key Terms ……………………………………………… 15

2.1.2.1 Cost…………………………………………………………………… 15

2.1.2.2 Volume ………………………………………………………………. 15

2.1.2.3 Profit ………………………………………………………………….. 16

2.1.2.4 Break-Even Point ……………………………………………………... 16

2.1.2.5 Margin of Safety ……………………………………………………… 17

2.1.2.6 Degree of Operating Leverage ………………………………………… 17

2.1.3 Cost Volume Profit Chart ……………………………………………… 18

2.1.4 Theories Related to CVP ……………………………………………….. 19

2.1.4.1 Theory of Cost………………………………………………………… 20

2.1.4.2 Theory of Production …………………………………………………. 22

2.1.4.3 Pricing Theory ………………………………………………………… 23

2.1.4.4 Theory of the Firm …………………………………………………… 23

2.1.4.5 Theory of Constraints …………………………………………………. 24

2.1.5 Factors Affecting Cost Volume Profit Analysis ………………………… 26

2.1.5.1 Basic Constituents ……………………………………………………… 26

2.1.5.2 Income Statement ………………………………………………………. 27

2.1.5.3 Contribution Margin …………………………………………………… 28

2.1.5.4 Fixed Costs …………………………………………………………… 28

ix

2.1.6 Challenges Facing Manufacturing Companies When Using CVP Analysis for

Decision Making ……………………………………………………………… 29

2.1.6.1 Linearity of Total Revenue and Total Cost Schedule ……………….. 29

2.1.6.2 Similarities to Standard Economic Model ……………………………. 29

2.1.6.3 Focus on Revenue and Operating Expenses ………………………….. 30

2.1.6.4 Wealth Impacts of CVP Decisions ……………………………………. 31

2.1.7 CVP Analysis and the Modern Manufacturing Firms …………………… 31

2.1.7.1 Cost Structure ………………………………………………………….. 31

2.1.7.2 Technology and Competition ………………………………………….. 32

2.1.7.3 Strategic Planning ……………………………………………………… 32

2.1.8 Budgeting and CVP Analysis …………………………………………… 33

2.1.9 CVP as Performance Evaluation Tool …………………………………… 34

2.2 Empirical Literature Review ………………………………………………. 35

2.3 Knowledge Gap ……………………………………………………………. 40

2.4 Critical Review of Literature………………………………………………. 40

2.4.1 Criticisms of Studies by Researchers …………………………………… 40

2.4.2 Criticisms of CVP ……………………………………………………….. 42

2.5 Conceptual Framework of the Study ………………………………………. 44

2.6 Relevance of Literature …………………………………………………….. 47

2.7 Conclusion …………………………………………………………………. 50

CHAPTER THREE: RESEARCH METHODOLOGY…………………… 51

3.0 Introduction ……………………………………………………………….. 51

3.1 Research Design ………………………………………………………….. 51

3.2 Population ……………………………………………………………… 52

3.3 Sampling and Sampling Techniques …………………………………… 52

x

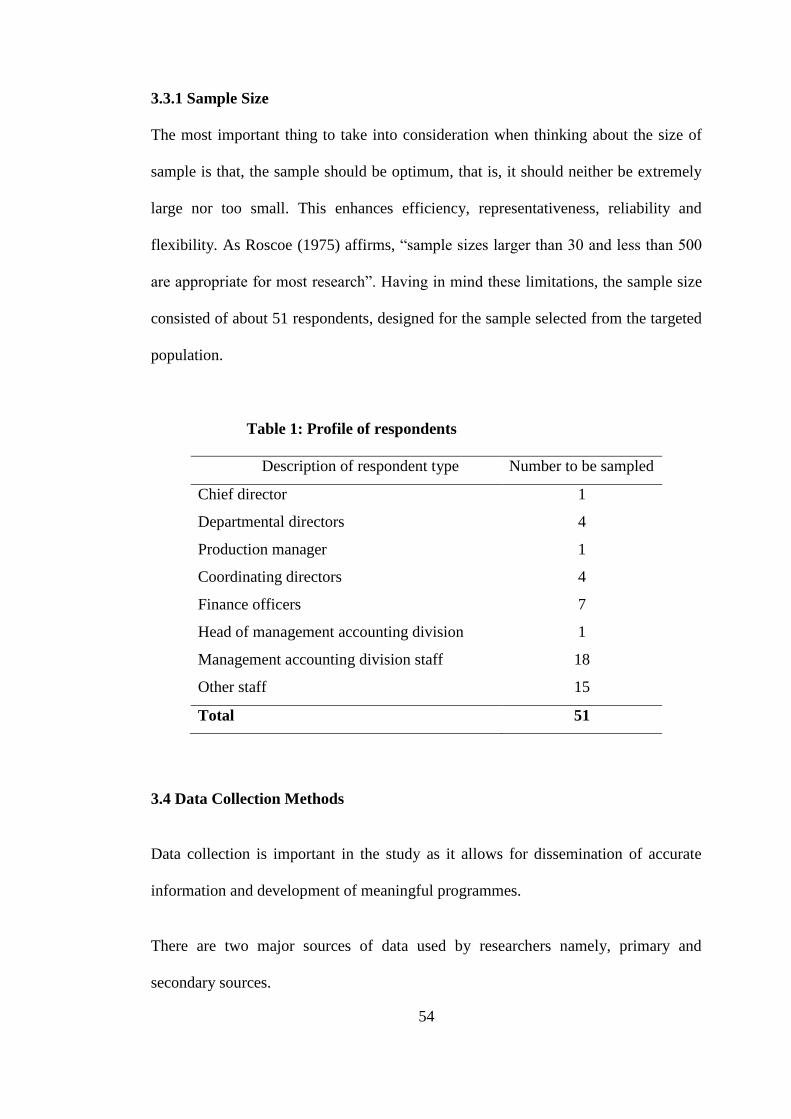

3.3.1 Sample Size …………………………………………………………… 54

3.4 Data Collection Methods ………………………………………………… 55

3.4.1 Primary Data …………………………………………………………… 55

3.4.2 Secondary Data ………………………………………………………… 55

3.4.3 Data collection Instruments ……………………………………………. 55

3.4.3.1 Questionnaire …………………………………………………………. 56

3.4.3.2 Interview ……………………………………………………………… 57

3.5 Data Analysis …………………………………………………………….. 58

3.6 Reliability and Validity of the Study …………………………………….. 58

3.6.1 Reliability ………………………………………………………………. 58

3.6.2 Validity …………………………………………………………………. 59

3.6.3 Achieving Validity and Reliability ……………………………………. 59

CHAPTER FOUR: STUDY FINDINGS, ANALYSIS AND DISCUSSION 61

4.0 Introduction ……………………………………………………………….. 61

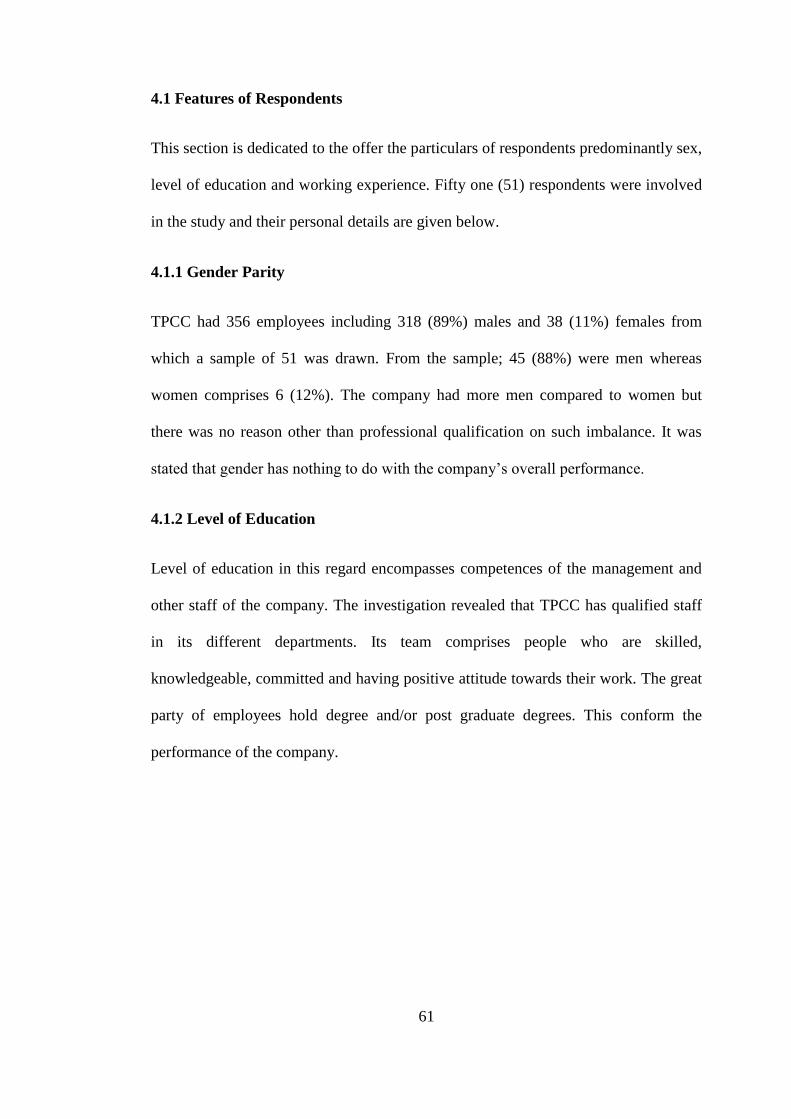

4.1 Features of Respondents …………………………………………………… 62

4.1.1 Gender Parity ……………………………………………………………. 62

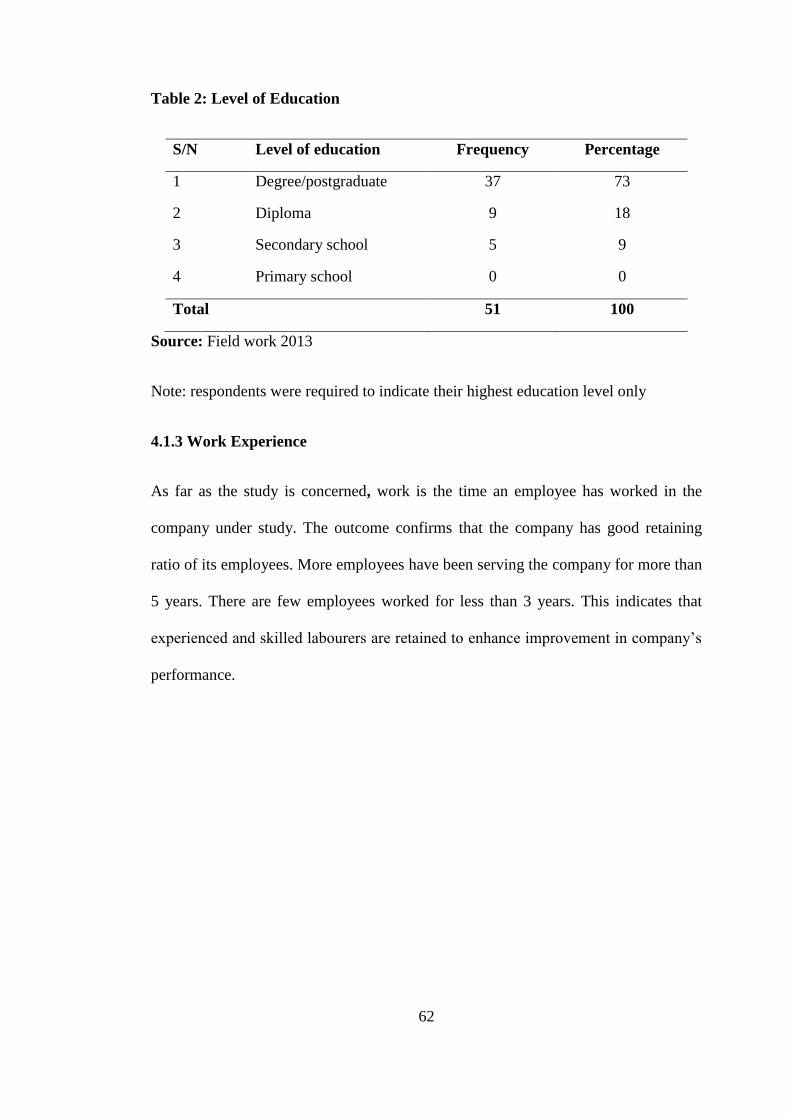

4.1.2 Level of Education ………………………………………………………. 62

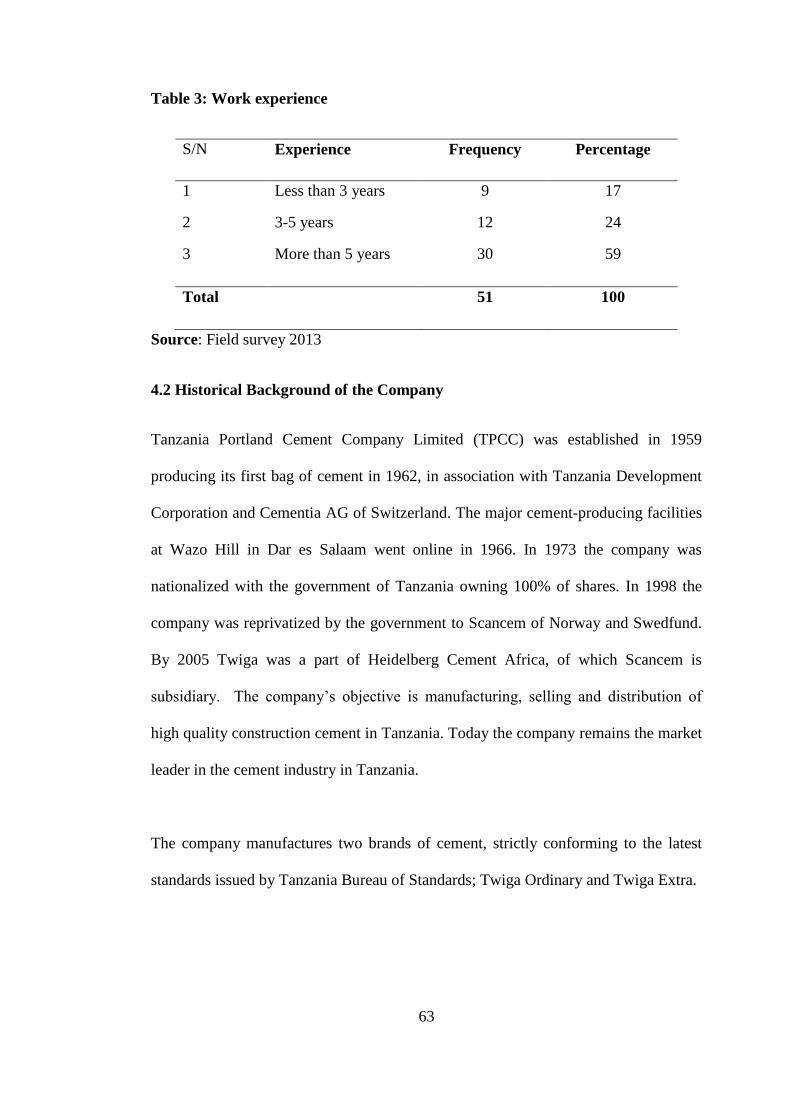

4.1.3 Work Experience ………………………………………………………… 63

4.2 Historical Background of the Company …………………………………… 64

4.3 Objective One: General Understanding of Cost Volume Profit Analysis … 65

4.3.1 CVP Analysis Awareness ……………………………………………….. 65

4.3.2 Linearity of Costs and Revenue ………………………………………… 65

xi

4.3.3 Drivers of Costs …………………………………………………………. 66

4.3.4 Separation of Costs into Fixed and Variable Categories ………………… 67

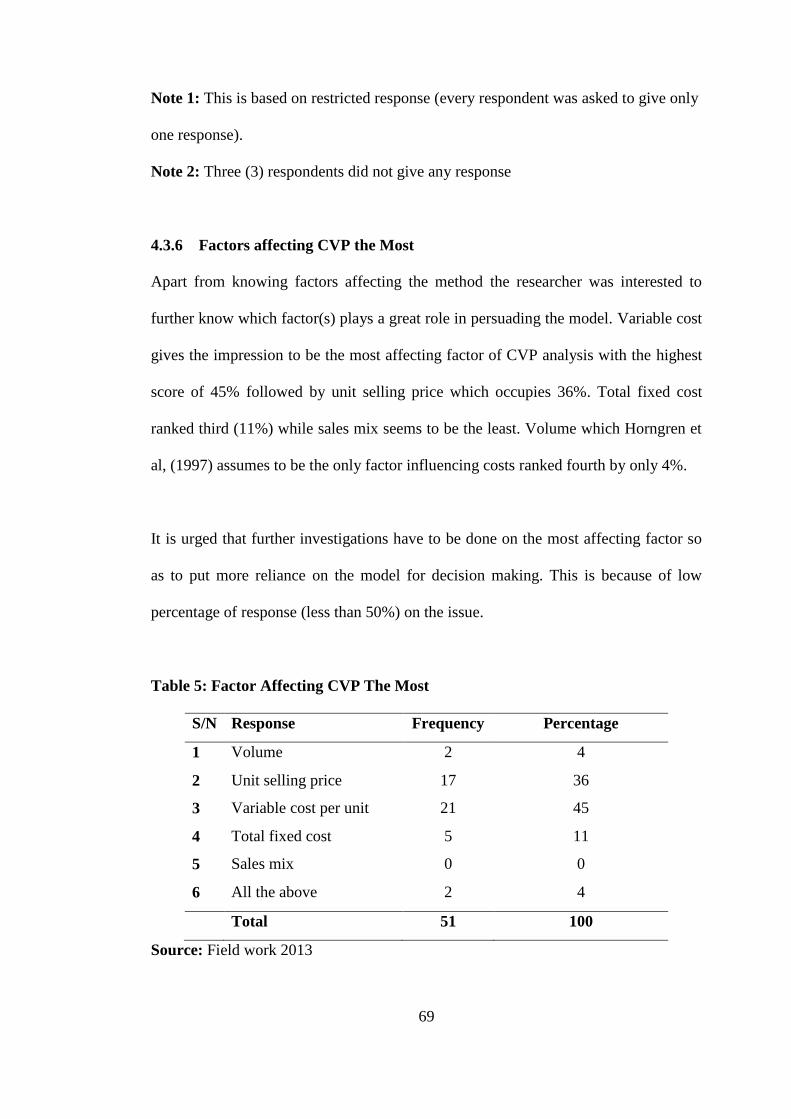

4.3.5 Factors Affecting CVP Analysis ………………………………………… 69

4.3.6 Factors affecting CVP the Most ………………………………………. 70

4.4 Second Objective: CVP Analysis and Related Challenges ……………… 71

4.4.1 The Use of CVP Analysis in Planning and Control …………………….. 71

4.4.2 Planning and Control Problems ………………………………………… 71

4.4.3 CVP Analysis in Long-Term Planning …………………………………. 73

4.5 Third Objective: Applicability of Breakeven Analysis in Modern Manufacturing

Firms……………………………………………………………………………. 73

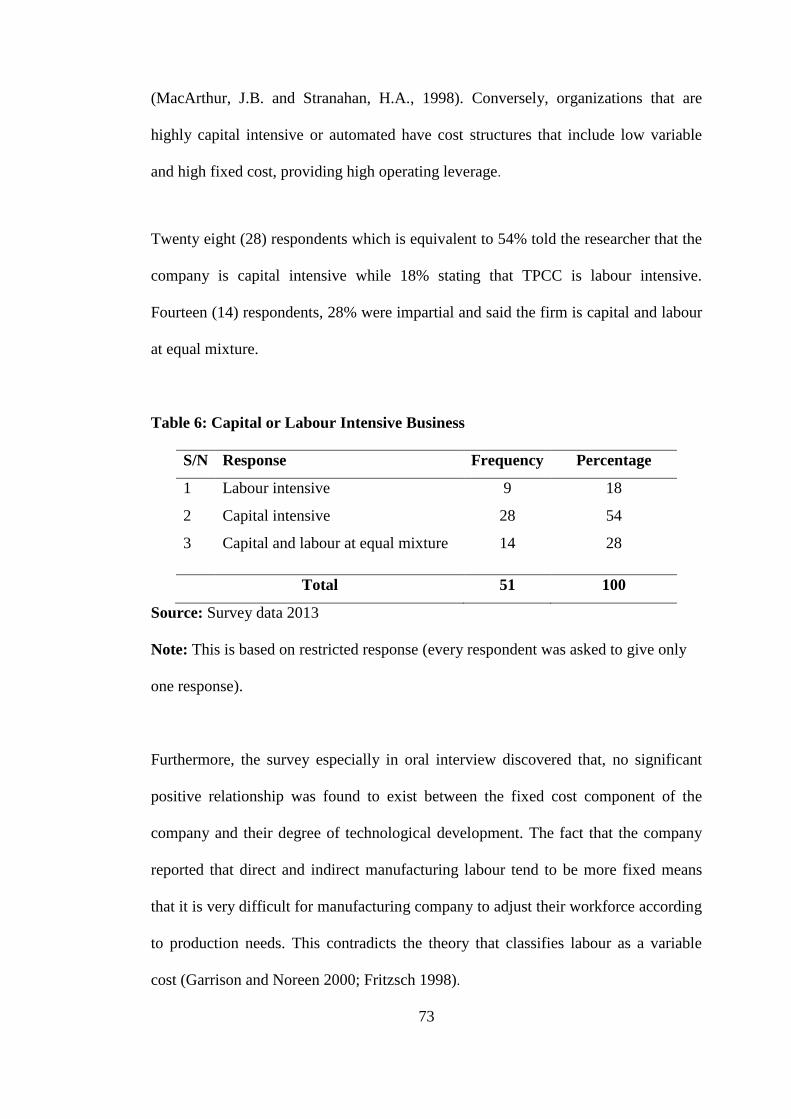

4.5.1 Capital or Labour Intensive Business …………………………………….. 74

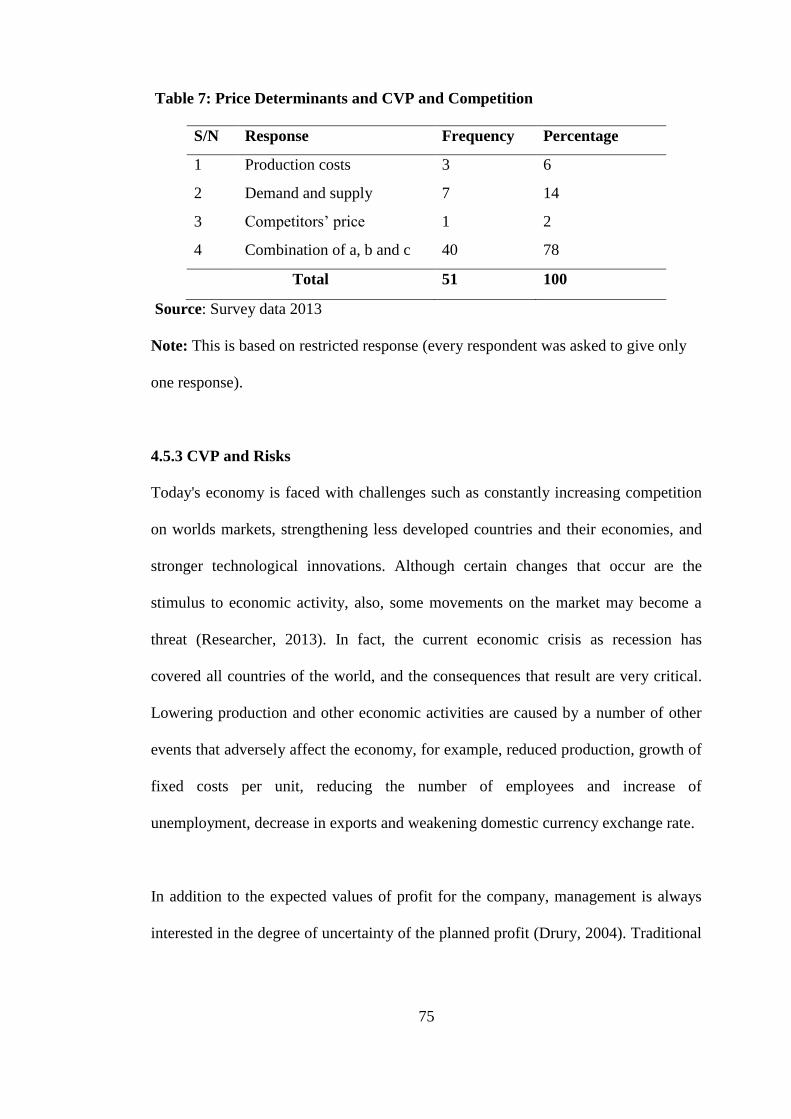

4.5.2 Price Determinants and CVP and Competition ………………………..... 75

4.5.3 CVP and Risks …………………………………………………………... 76

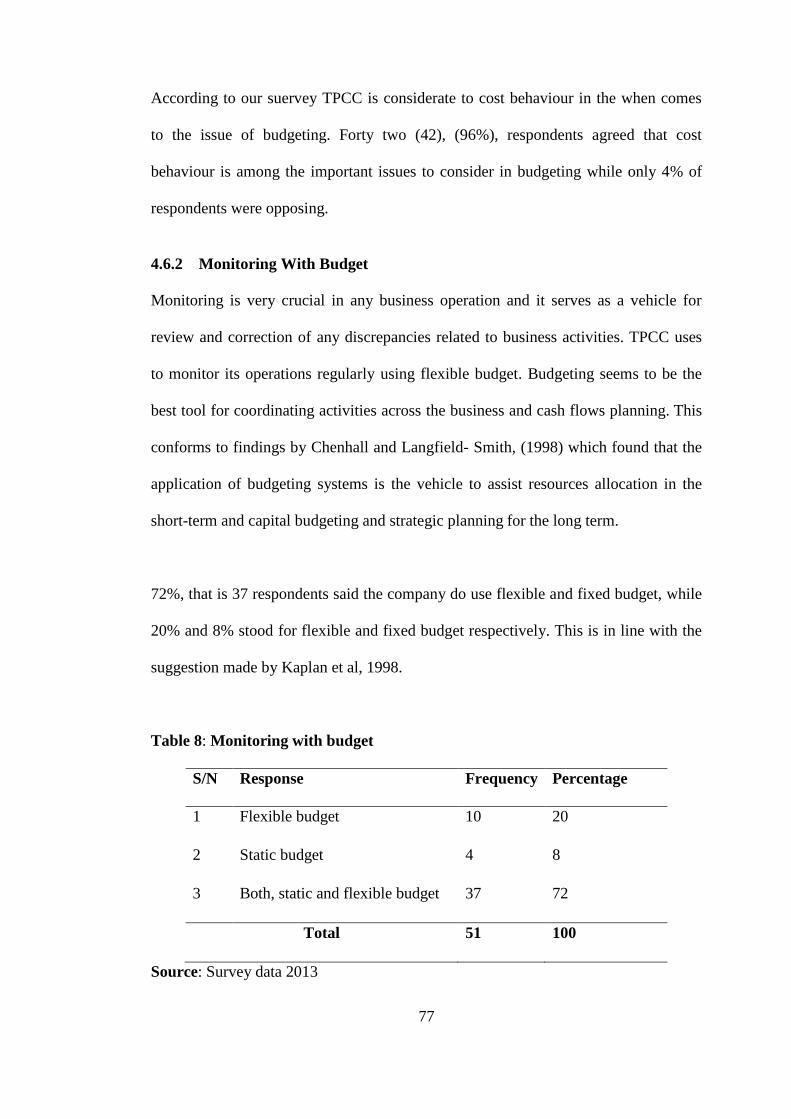

4.6 Objective Four: Budgeting and CVP Analysis ………………………….. 77

4.6.1 Cost Behaviour in Budgeting ………………………………………… 77

4.6.2 Monitoring With Budget ……………………………………………...... 78

4.6.3 Budgeting and the Company‟s Business Pattern …………………….... 79

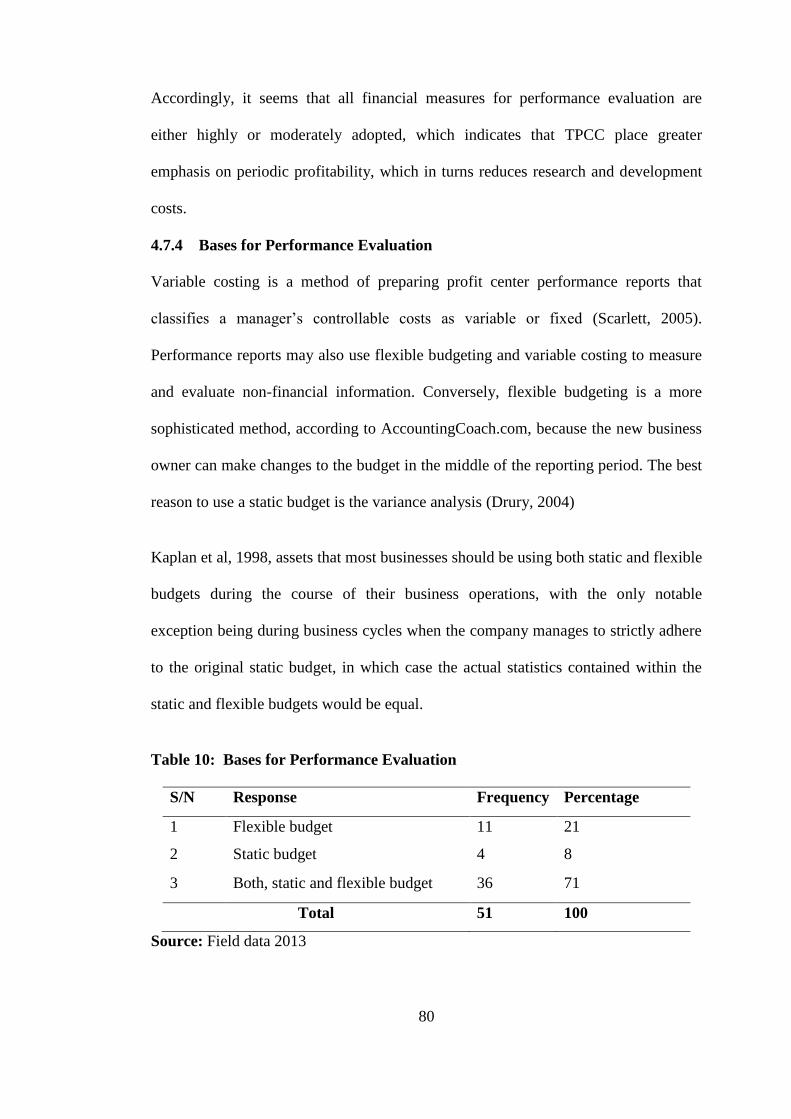

4.7 Objective Five: Performance Evaluation With CVP Analysis…………… 80

4.7.1 Performance Evaluation …………………………………………………. 80

4.7.2 Bases for Performance Evaluation ………………………………….. 81

4.7.3 Effectiveness and Efficiency of CVP ………………………………. 82

4.8 Summary of Data analysis ……………………………………………...... 83

CHAPTER FIVE: SUMMARY, CONCLUSION AND RECOMMENDATIONS

………………………………………………………………………………. 84

xii

5.0 Introduction ……………………………………………………………… 84

5.1 Summary …………………………………………………………………. 84

5.2 Conclusion ……………………………………………………………….. 86

5.3 Recommendations ………………………………………………………... 88

5.3.1 Recommendations to Policy Makers …………………………………. 88

5.3.2 Recommendations to Managers ……………………………………….. 89

5.4 Areas for Future Studies ………………………………………………… 93

REFERENCES …………………………………………………………… .. 94

APPENDIX I: QUESTIONNAIRE ……………………………………… 103

xiii

LIST OF TABLES

Table 1: Profile of respondents …………………………………………….. 54

Table 2: Level of Education ………………………………………………. 62

Table 3: Work experience ………………………………………………… 64

Table 4: Factors Influencing CVP ……………………………………………. 68

Table 5: Factor Affecting CVP The Most ………………………………….. 69

Table 6: Capital or Labour Intensive Business ……………………………. .. 74

Table 7: Price Determinants and CVP and Competition …………………. 76

Table 8: Monitoring with budget …………………………………………… 78

Table 9: Performance Valuation Methods …………………………………… 80

Table 10: Bases for Performance Evaluation ………………………………… 81

xiv

LIST OF FIGURES

Figure 1: CVP Analysis Chart ……………………………………………… 18

Figure 2: Profit Volume Chart …………………………………………….. 19

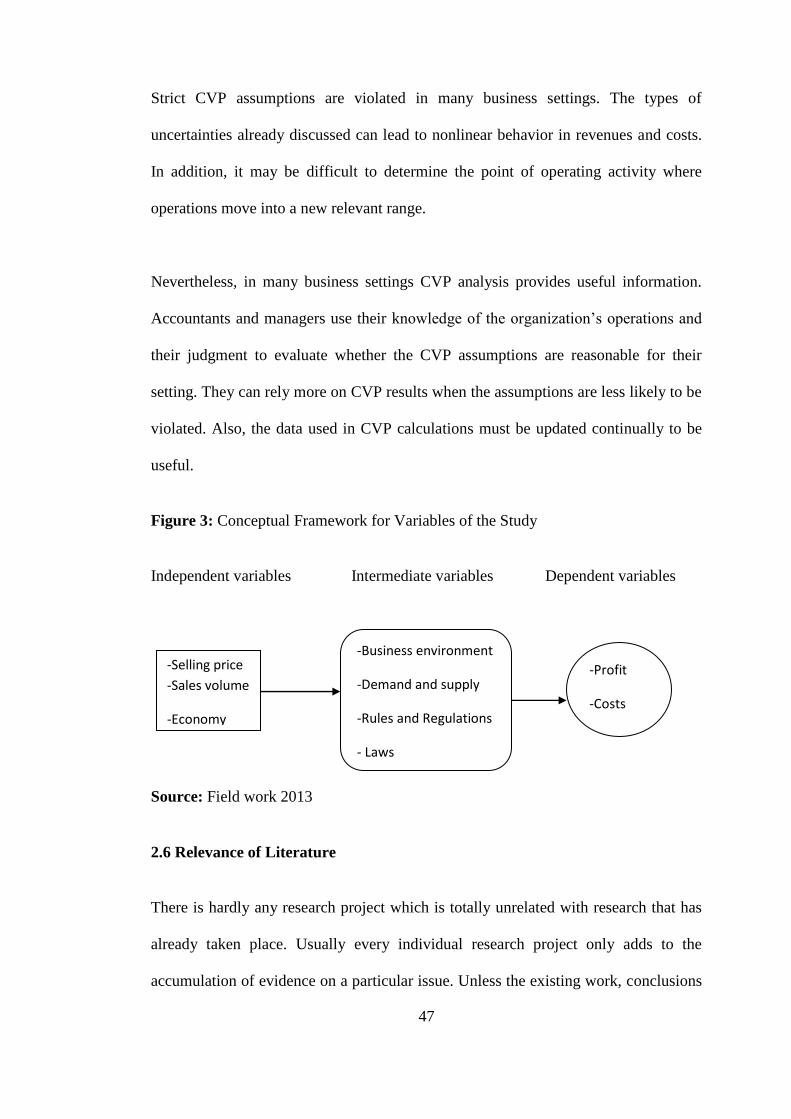

Figure 3: Conceptual Framework for Variables of the Study ………………. 47

xv

LIST OF ABBREVIATION

ABC – Activity Based Costing

BEP – Break Even Point

CVP – Cost Volume Profit

DOL – Degree of Operating Leverage

EAC - East African Community

EVA - Economic Value Added

JIT – Just-in-Time

NPV- Net Present Value

ROI – Return on Investment

SP – selling price

SPSS – Statistical Package for Service Solution

TFC – Total Fixed Costs

TOC - Theory of Constraints

TPCC – Tanzania Portland Cement Company

TQM – Total Quality Management

UCM – Unit Contribution Margin

VC – Variable Cost

1

CHAPTER ONE

GENERAL INTRODUCTION

1.0 Introduction

This chapter conveys the universal outline of the study on the subject of the analysis

of performance of Cost Volume Profit (CVP) analysis in manufacturing companies in

Tanzania, a case of Tanzania Portland Cement Company (TPCC). It commences by

depiction of the background to the study problem, followed by the statement of the

problem, subsequent to which it presents the research objectives and research

questions. The chapter also briefly explains the significance of the study, explaining

how important the study in knowledge is, managerial impact and contributions to

personal understanding of the researcher and scope of the study. It ends up by

presenting the limitations of the study.

1.1 Background to the Study

1.1.1 CVP Analysis; an Overview

Cost volume profit analysis is a model which is used to plan profit. The basic

assumption made is that, cost volume and profit has linear relationship. It is used to

measure the economic characteristics of manufacturing a proposed product. A critical

part of CVP analysis is the point where total revenue equals total costs (Duncan,

1996). At this break-even point (BEP), a company will experience no income or loss.

This BEP can be an initial examination that precedes more detailed CVP analysis.

Based on accounting data, the CVP model is used to determine the sales quantity

needed to break even, as well as the sales quantity required to earn a desired profit or

2

profit margin. Managers then compare a product's expected sales with the sales

quantities required to break even and/or earn a target profit margin to determine

whether the product should be produced (Duncan, 1996).

Cost-volume-profit, like all financial models, is based on a set of simplifying

assumptions that reduces the complexity of a resource allocation decision to make

decision making more tractable. These assumptions will be outlined in the literature

review chapter. To understand a financial model and its usefulness, its assumptions

and their role in a decision must be understood, that is, the reliability of the results

from CVP analysis depends on the reasonableness of the assumptions.

One of the features useful for decision making, is the ability to display the

information in different methods, one of these is the Margin of safety. This is the

difference between the expected sales and break even sales, expressed as a percentage

of the expected sales. It shows management the level that sales can fall by before the

company‟s revenue falls below the breakeven point (Researcher, 2013).

1.1.2 Economists versus Accountants view of CVP Analysis

There are many ways that CVP analysis can be useful for decision making. It is

important to distinguish between the different applications of the Economists and

Accountants interpretations, as well as other factors involved in decision making

(Lucey, 1996). The economist‟s interpretation of the CVP is based on two main

assumptions, which explain the shape of the cost and revenue curves.

The first assumption, which affects the revenue, is that the firm is competing on price

competition; this means that in order to increase sales, the firm must reduce the

3

marginal selling price of the product. This causes the firm‟s revenue curve to level

off, as the marginal revenue falls to zero (Drury, 2004).

According to Burch (1994), the second assumption is based on the firms cost,

economies and diseconomies of scale. The firm‟s economies of scale cause the

variable cost per unit to decrease as production increases. This can be due to any of

the economies of scale, such as purchasing, where a discount for bulk buying is

received, managerial, where managers can become more specialised, financial where

the firm is offered lower interest rates as there is a lower risk of lending.

It is important to understand that Economists are trying to most accurately model real

world situations, rather than create a tool for management decision. Economists argue

that lowering selling price acts as a catalyst to increasing demand and thus as sales

volumes increase so will variable costs (Chesbrough, H. and Rosenbloom, R.S. 2002).

Proponents of the accounting model argue that it is not intended to provide a precise

representation of total revenue and cost functions throughout all levels of activity.

The objective of the accountant‟s CVP model is to represent an approximation of

revenue and cost behaviour over the relevant range in the short term.

Managers may wish to extend the CVP model to cover longer term decisions. This

needs them to be aware of the long term behaviour of fixed costs. In the long term,

firms will have a greater control over fixed costs, which will give the firm‟s fixed cost

line a step function. Meigs, (1998) states that, other factors will also affect the firm‟s

revenue and cost curves, such as advertising strategies, changes in political

environments, social, economic, and legal factors, such as a change in tax rate. These

factors cannot easily be planned for and are not easily shown in long term CVP

4

analysis, which is the main reason that CVP cannot accurately model long term

production.

In the real world, firms will be producing multi products, and spreading the overhead

costs across each of these products. A firm may wish to alter the CVP analysis to

reflect their product mix. This is done by grouping production into batches. The

batches revenue and variable costs will be defined as the total of the products in the

batch (Researcher, 2013). The values for the batch are then applied to the CVP in the

same way as a single product. The Accountant‟s interpretation of the CVP analysis, as

shown by the underlying assumptions, will allow managers to develop a more

relevant understanding of the information, so that it can be used more efficiently in

decision making. If managers tried to use the economists Cost Volume Profit model,

the cost of gathering and interpreting the data would be high, as well as making the

information more difficult to understand and less reliable (Kaplan, R. and Atkinson,

A., 1998).

Thus, Economists and accountants have diametrically opposite views of cost-volume

profit (CVP) behaviour but only accountants have a CVP model that is appropriate for

assisting management with decision making (Drury 2004).

1.2 Statement of the Problem

Running a successful business requires proficient navigation of the many choices

created by an ever changing market place (Meigs, 1998). This implies that, to have a

strong and successful business, managers need to have a clear understanding of the

financial impact that the most basic business decisions may have.

5

CVP analysis is a useful forecasting as well as managerial control tool. It is one of the

fundamental financial analysis tools for ascertaining the underlying profitability of a

business. Its primary value is in highlighting the effects of different levels of activity

on profit and, combinations of fixed and variable costs of production. The model not

only incorporates these admittedly important variables but recognizes the fixed and

variable nature of capital costs (Brigham, 1995). It includes a set of problem solving

techniques and procedures, based on understanding the characteristics of company

costs evolution models. In a general sense, it provides a comprehensive financial

overview of the planning process (Horngren, Datar, and Foster, 1994). That overview

allows managers to examine the possible impacts of a wide range of strategic

decisions. And such decisions can include crucial areas such as pricing policies,

product mixes, market expansions or contractions, outsourcing contracts, idle plant

usage, discretionary expense planning and a variety of other important considerations

in the planning process (Horngren et al, 1994).

The CVP analysis is useful in taking decisions related to installing manufacturing

capacity and selling prices taking in to consideration that different levels of

manufacturing capacity display different structure of fixed and variable components

of manufacturing cost, and the impact of difference between selling price and variable

cost on contribution for recovering the fixed costs and making profit (Drury, 2004).

However, the consequence of identifying and interpreting the underlying assumptions

of Cost Volume Profit (CVP) analysis rest on the practical application of it. When

CVP was developed, manufacturing firms had different cost structures than modern

manufacturing firms. Modern firms have a higher level of costs that remain constant

6

with changes in output, partly because modern firms are more capital intensive, and

partly because most of their labor cost is fixed (Johnson, H. Thomas, 1981). And cost

structures vary extensively among industries and between firms within an industry.

In addition, an organization‟s cost structure has a substantial effect on the sensitivity

of its profits to changes in volume. Operating leverage describes the extent to which

an organization‟s cost structure is made up of fixed costs. Operating leverage can

vary within an industry as well as between industries (Researcher, 2013).

Furthermore, as the manufacturing environment changes, business cost structure also

changes, the conventional cost behavior based on single action shows narrow-minded,

and the basic assumptions also limits the practical application of CVP analysis. CVP

is perceived to be a one-period model of a product's profitability, (Mc Waters et al,

2001) although the product may have an economic life of several years.

Likewise, there are factors that influence the changes in management accounting

practices within some organisations. Otley and Berry (1980) made reference to some

systems as open, that is, there is a continuous cycle of resources that are inputs which

moves from the external environment. It is a common belief that such changes will

have an influence on the selection of the appropriate management accounting

practices within any organisation. Some researchers have commented that such

changes may originate due to different settings of both economic and cultural

environments. Most of the research focused on changes in management accounting

practices, primarily in countries such as South Africa and Canada (e.g Luther &

Longden, 2001). Nevertheless, some researchers noted what is often taught in schools

is far different in the world of work and therefore creates a breach in knowledge

7

between the practical and the theory. Johnson and Kaplan (1987) argued that

management accounting has not changed over the past years. But, Libby and

Waterhouse (1996) were convinced that there were changes. Burns et al. (1999)

further argued that there is evidence that management accounting practices have

changed over the last decade in a developed country such as the United Kingdom.

There are some published reports in Africa such as “Cost Information and Strategic

Planning in the Egyptian Private Sector” written by Mohamed Elshahat in 2006. On

his report Mohamed (2006) explained a little on CVP as a tool for decision making

with its weaknesses and some more published in developed countries. But, currently

there is no any published report in Tanzania talking anything on CVP as a model for

decision making and there is no research study conducted on this issue. So

specifically, this study desires to understand how efficient Cost Volume Profit

analysis, in helping managers to is make decisions which, in turn, enable the

manufacturing business to face the challenges caused by the ever changing business

environment particularly in Tanzania, as well as it would help the policy makers to

make some relevant policies in this aspect.

1.3 Objectives of the Study

1.3.1 General Objective

Main purpose of this study is to determine if CVP can assist management in

formulating pricing policies by projecting the effect of different price structures on

cost and profit and to highlight the usefulness of CVP analysis in manufacturing

companies in Tanzania.

8

1.3.2 Specific Objectives

The specific objectives of this study are as follows:

1. To identify the factors affecting CVP analysis

2. To determine the challenges facing manufacturing companies when using

CVP analysis for decision making

3. To determine the relevance of CVP in modern manufacturing firm‟s decision

making.

4. To find out if CVP analysis is helpful in setting up flexible budget which

indicates cost at various levels of activities.

5. To find out if CVP analysis is useful in evaluating performance for the

purpose of control.

1.4 Research Questions

1. What are the factors affecting CVP analysis?

2. What are the challenges facing manufacturing companies when using CVP

analysis for decision making?

3. Is CVP analysis relevant to modern manufacturing firm‟s decision making?

4. What is the contribution of CVP in setting up flexible budget?

5. Can CVP assist in evaluating performance for the purpose of control?

1.5 Significance of the Study

CVP analysis is an important theory in modern management accounting. This

analysis provides useful information for decision-making in the management of a

company. But its conclusions are made in some strict assumptions, and we cannot be

sure that the conclusions are also set up in real environment. Those simplifications

9

and restrictions impinge on the reality and relevance of the analytical model, so

attempts to improve them will involve releasing some of their underlying assumptions

or broadening their scope.

Because in the modern environment of business, a business administration must act

and take decisions in a fast and accurate manner, gaining a better understanding of

costs and volume via CVP analysis can assist management in locating areas of

potential efficiency improvements. Thus studying whether the CVP conclusions are

justifiable in real environment will be worth for business policies formulation and

personal career improvement to researcher.

1.6 Scope of the Study

CVP is an important financial analysis that helps managers to deal with their routine

problems as well as strategic issues in the course of carrying out their business

activities. Such issues can come up when preparing company budgets, financial plans

or when new sales promotions and other functional decisions are taken. It evaluates

what-if situations that occur in the business.

CVP analysis has wider scope in various managerial decisions making. Various cost

accounting models have been developed within this broad decision framework such

as breakeven analysis, transfer pricing systems and mathematical programming

methods for choosing optimal sales mix and the optimal extend of processing joint

products. Initially all CVP models were deterministic, assuming demand and cost

structures to be known with certainty. However, following the significant

development in the area of economic decision making uncertainty, attempts have

been made to relax the certainty assumption of CVP models.

10

The following are the benefits (functions) of CVP in business;

It is helpful in setting up flexible budgets which indicates cost at various

levels of activities. It assists managers in determining the quantity of products

to be produced to attain desired profits, the quantity of products to be

produced at maximum threshold level, attaining desired profit under different

costs and volume relationship.

In order to ascertain profits accurately, it is essential to ascertain the

relationship between cost and profit on one hand and volume on the other.

CVP analysis helps the business to know its most profitable product(s) or

service(s) among various that the business offers in the market. This aids the

management to focus more on profitable products compared to others. It also

supports the form to know the impact of any variance, due to any reason, on

the profits.

CVP analysis assists in evaluating performance for the purpose of control. It

enables the firm to understand the level of fluctuations it can afford in its

selling price. Whenever firms increase their selling price to increase sales they

must know the new level of sales they have to meet to sustain the desired

profits. It is also essential for the firm to know the bare basic prices(s) that

must be charged for its products from its customer and how to cover any

increase in fixed costs that may arise.

1.7 Limitations of the Study

It is important to mention a few limitations of this study before any conclusion may

be drawn.

11

The study was subject to the normal limitations related with survey research. CVP

analysis is used to provide information for internal reporting purposes. This led to

response bias due to the unwillingness of the respondents to share the accurate

information on the ground of confidentiality. Some of the responses may have been

influenced by the problems of questions understanding and misinterpretation which

resulted in data analysis difficulties.

All research designs can be discussed in terms of their relative strengths and

limitations. The merits of a particular design are inherently related to the rationale for

selecting it as the most appropriate plan for addressing the research problem. The

researcher selected a case study design because of the nature of the research problem.

The case study is basically been faulted for its lack of representativeness and

therefore it involves problems on the issues of reliability, validity, and

generalizability. This is because a case study focuses on a single unit, a single

instance.

Time and budget were also among the limiting factors of this study. This was a self-

sponsored research; therefore the costs associated with the whole study were incurred

by the researcher. Thus the researcher was subject to financial constraints and time

for data collection and analysis.

1.8 Conclusion

This chapter has offered the broad preface of the whole study. It began by giving a

range of aspects with high regard to the idea Cost Volume Profit analysis, contracted

downward to the subject of applicability. Within the problem it has demonstrated how

the interpretation of strict assumptions of CVP analysis impinge on the application of

12

the model and, for this reason the purpose to discover the efficiency of the model in

manufacturing business. In winding up the chapter, the importance, scope and

limitations of the study are specified.

13

CHAPTER TWO

LITERTURE REVIEW

2.0 Introduction

This chapter is dedicated to a review of the most important theoretical, empirical and

critical literature related to the issues of CVP analysis as a planning and control tool

for mangers. Basically, CVP analysis is considered to be the powerful tool mangers

have at their hands for planning and control of the operations of their organizations.

There have been many studies on CVP for decision making as used in organizations a

long time ago. Nevertheless, these studies have not been telling us how competent is

the model in providing managers with the information they require particularly in the

changing business environment.

This chapter has five major parts. The first part discusses the theoretical framework of

CVP analysis. The key terms and assumptions underlying the study as well as its

pictorial presentations are also presented. The second party discusses the empirical

literature review of CVP analysis as used in the planning process in the changing

business environment and the recent tendencies of management thinking basing on

the objectives of the study followed by highlights the conceptual framework of the

study.

14

2.1 Theoretical Review of Literature

2.1.1 The Concept of Cost Volume Profit (CVP) Analysis

CVP analysis is a systematic method of examining the relationship between changes

in activity (that is, output) and changes in total sales revenue, expenses and net profit

(Drury, 2004). It is a mathematical representation of the economics of producing a

product. The relationships between a product's revenue and cost functions expressed

within the CVP model are used to evaluate the financial implications of a wide range

of strategic and operational decisions. Cost-Volume-Profit analysis is a planning tool

which is extremely useful in predicting sales and profit levels given a certain cost

structure (Burch, 1994). Traditional CVP analysis has been applied largely to

manufacturing enterprises which have a tangible product base (for example,

furniture). However, the concept itself is applicable to service enterprises such as

banking, insurance and other financial service industries.

As mentioned earlier, Cost-Volume-Profit analysis, or breakeven analysis as it is

often commonly called, is used largely in the manufacturing sector. According to

Horngren et al (1997), the basic CVP model has the following underlying

assumptions:

1. The behavior of costs and revenues is linear.

2. Selling prices are constant.

3. All costs can be divided into their fixed and variable elements.

4. Total fixed costs remain constant.

15

5. Total variable costs are proportional to volume.

6. Prices of production inputs (for instance, materials) are constant.

7. Efficiency and productivity are constant.

8. The analysis covers a single product or a constant sales mix.

9. Volume is the only driver of costs.

2.1.2 Definitions of Key Terms

The main variables involved in the empirical study to the extent that our study is

concerned are as follows;

2.1.2.1 Cost

In business, cost is usually a monetary valuation of effort, material, resources, time

and utilities consumed, risks incurred, and opportunity forgone in production and

delivery of a good or service. Cost is a sacrifice of resources incurred for a future

benefit or objective (Kapil, 2011). The resources sacrificed are in form of cash or

cash equivalents. It is a resource sacrificed or forgone to achieve a specific objective

(Horngren et al., 1997).

2.1.2.2 Volume

The quantity or number of goods sold or services sold in the normal operations of a

company in a specified (Baumol, 1972). It is the level at which something is heard or

the amount of space that something takes up.

16

2.1.2.3 Profit

The word profit has different meaning to different people. In a general sense profit is

regarded as income accruing to the equity holders (Dwivedi, 2008). To an accountant,

profit means the excess of revenue over all paid-out costs including both

manufacturing and overhead expenses. Economists define profit as a return over and

above the opportunity cost, that is, the income which a businessman might expect

from the second best alternative use of his resources.

2.1.2.4 Break-Even Point (BEP)

The break-even point has its origins in the economic concept of the point of

indifference. From an economic perspective, this point indicates the quantity of some

good at which the decision maker would be indifferent (Dwivedi, 2008) (that is,

would be satisfied without reason to celebrate or to opine). At this quantity, the costs

and benefits are precisely balanced.

Break-even point is where both revenue and costs are equal (Duncan, 1996). It is a

starting point for planning purposes. If sales volume extends beyond break-even point

and if there is positive contribution, each additional unit sold will contribute to profit

at a rate which is equal to unit contribution margin. If sales volume will be below

break-even point, sales volume will not cover annual fixed costs.

BEP = Total fixed costs (TFC)

Unit contribution margin (UCM)

Unit contribution margin = Unit selling price (SP)-Variable cost per unit (VC)

17

2.1.2.5 Margin of Safety

A margin of safety is the difference between break even sales and planned sales. This

difference indicates the degree to which the business is safe from operating at a level

that will result in loss (Drury, 2004).

2.1.2.6 Degree of Operating Leverage

Managers decide how to structure the cost function for their organizations. Often,

potential trade-offs are made between fixed and variable costs. One of the major

disadvantages of fixed costs is that they may be difficult to reduce quickly if activity

levels fail to meet expectations, thereby increasing the organization‟s risk of incurring

losses.

The degree of operating leverage is the extent to which the cost function is made up

of fixed costs (Scarlett, 2005). Organizations with high operating leverage incur more

risk of loss when sales decline. Conversely, when operating leverage is high an

increase in sales (once fixed costs are covered) contributes quickly to profit.

A manager can use the DOL to quickly estimate what impact various percentage

changes in sales will have on profits, without the necessity of preparing detailed

income statements.

The formula for operating leverage is

Degree of operating leverage (DOL) = Contribution margin

Net operating income

18

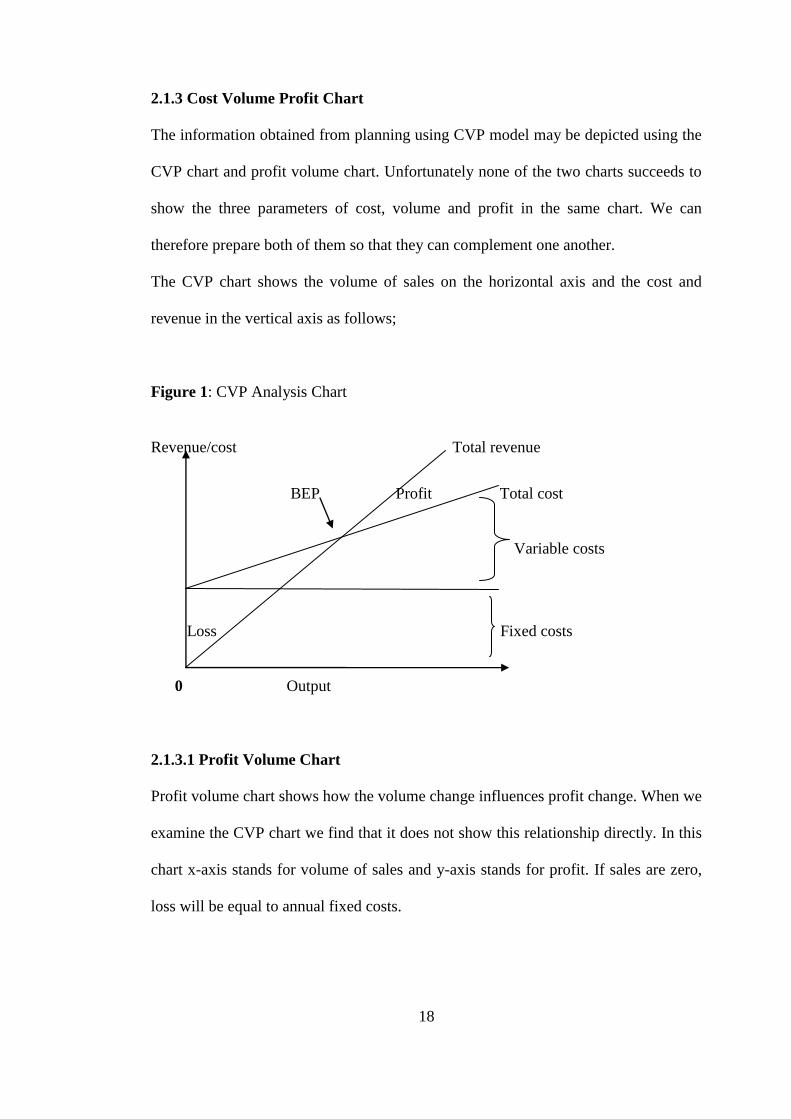

2.1.3 Cost Volume Profit Chart

The information obtained from planning using CVP model may be depicted using the

CVP chart and profit volume chart. Unfortunately none of the two charts succeeds to

show the three parameters of cost, volume and profit in the same chart. We can

therefore prepare both of them so that they can complement one another.

The CVP chart shows the volume of sales on the horizontal axis and the cost and

revenue in the vertical axis as follows;

Figure 1: CVP Analysis Chart

Revenue/cost Total revenue

BEP Profit Total cost

Variable costs

Loss Fixed costs

0 Output

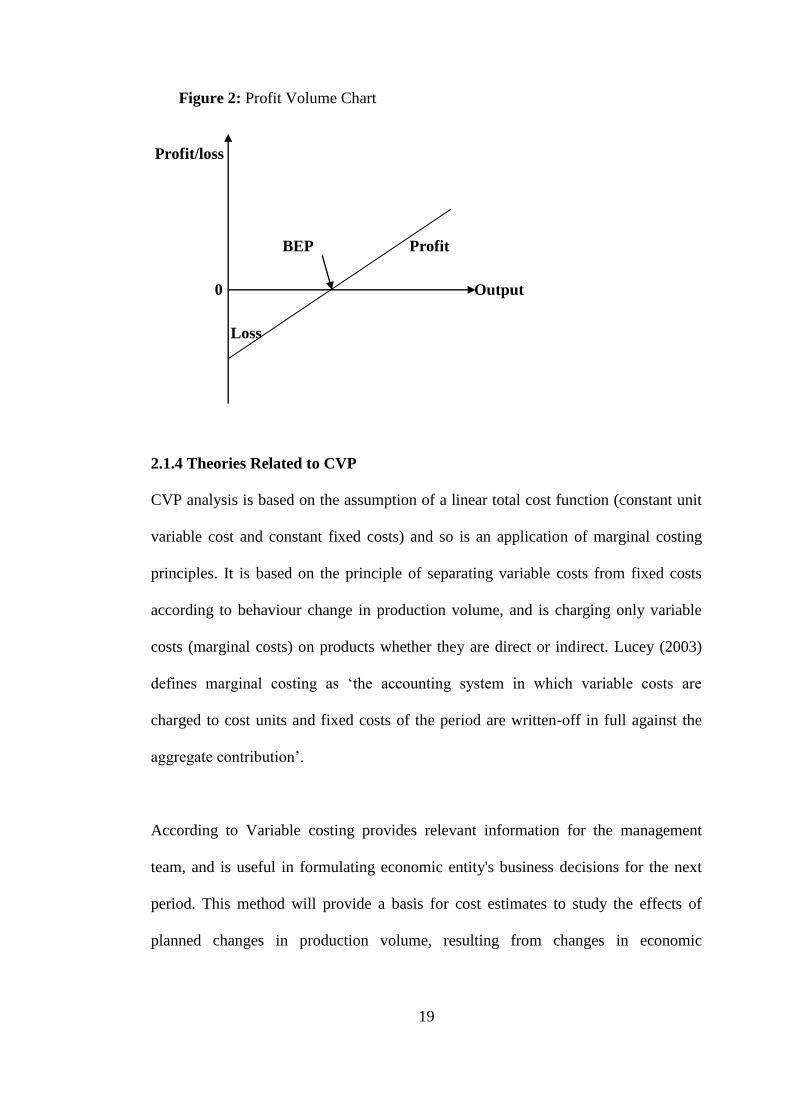

2.1.3.1 Profit Volume Chart

Profit volume chart shows how the volume change influences profit change. When we

examine the CVP chart we find that it does not show this relationship directly. In this

chart x-axis stands for volume of sales and y-axis stands for profit. If sales are zero,

loss will be equal to annual fixed costs.

19

Figure 2: Profit Volume Chart

Profit/loss

BEP Profit

0 Output

Loss

2.1.4 Theories Related to CVP

CVP analysis is based on the assumption of a linear total cost function (constant unit

variable cost and constant fixed costs) and so is an application of marginal costing

principles. It is based on the principle of separating variable costs from fixed costs

according to behaviour change in production volume, and is charging only variable

costs (marginal costs) on products whether they are direct or indirect. Lucey (2003)

defines marginal costing as „the accounting system in which variable costs are

charged to cost units and fixed costs of the period are written-off in full against the

aggregate contribution‟.

According to Variable costing provides relevant information for the management

team, and is useful in formulating economic entity's business decisions for the next

period. This method will provide a basis for cost estimates to study the effects of

planned changes in production volume, resulting from changes in economic

20

conditions or open some management actions such as price changes, increase or

decrease in stocks or special promotional activity.

Briefly, the following are the theories which provide the base or supports CVP

analysis:-

2.1.4.1 Theory of Cost

The theory of cost is the model which is most related to CVP. The theory of cost

deals with the behaviour of cost in relation to a change in output (cost-outputs

relation). The basic principle of the cost behaviour is that the total cost increases with

increase in output (Dwivedi, 2008). Such an unassuming statement of a witnessed

fact is of slight theoretical and practical importance. What is significant from a

theoretical and managerial idea of understanding is not the absolute increase in the

total cost but the direction of change in the average cost.

So the method focuses on boosting sales in that size does not allocate fixed costs on

inventory (unfinished products, finished products), but must be covered by the sales

of the period. Also the emphasis is on analysis and attribution of the fixed costs and

attributing the variable costs on the gross margin (Lucey, 1996).The manager has the

obligation to return and maximize margin on variable costs over which fixed costs

will be charged. The margin on variable costs, also called gross profit or contribution

limit is determined as the difference between gross turnover and variable costs

associated with the entire production sold (Vickers, 1997).

21

The margin of variable costs is also called the global margin and it is the sum total

margins on variable costs per product unit set multiplied by the associated production

sold. The unit margin can be determined as the difference between the selling price

and the unit variable cost of product (Scarlett, 2005).

CVP analysis is also predicated on the notion that, in the short run, a relationship

exists between volume, sales revenue, costs and profit. The “short run” in this regard

is a period of one year or less. And during this period, the organization's current

operating capacity becomes the main factor that restricts its output (Robert et al.,

2004). Though some of the organization's inputs can be increased in the short run,

others cannot. For example, it can take a long time to expand the capacity of the

organization's plant and machinery even though additional supplies of unskilled labor

and materials may be obtained on short notice (McWatters, et al., 2011).

Hence, given that the organization's plant facilities cannot be expanded in the short

run, its output will be limited in that period (Meigs, 1998). Furthermore,

organizations may be compelled to operate on relatively constant stock of production

resources in the short run because it also takes time to reduce capacity. In this regard,

sales volume becomes the major area of uncertainty for the affected organizations

because most of the costs and prices for their products will have already been

determined. The implication of this is that organizations‟ short-run profits are most

sensitive to sales volume. A CVP analysis reveals how this sales volume affects

short-run profits (Meigs, 1998).

22

The variation of the conventional CVP model provides more useful information to

management because it focuses on more than operating expenses and sales revenues.

Financial managers have long recognized the importance of including cost of capital

and business risk variables in capital budgeting decisions (Brigham, 1995). Our

model not only incorporates these admittedly significant variables but identifies the

fixed and variable character of capital costs.

The understanding of this theory led the researcher to develop the questions, which,

when responded helped her to conclude whether CVP analysis incorporates more than

costs and revenues when used in decision making (Researcher, 2013).

2.1.4.2 Theory of Production

This is the most basic theory in economics which was developed by Adam Smith and

David Ricardo in the late 18th century. Production theory is a theory which deals with

quantitative relationship, that is, technical and technological relations between input

and output. It also clarifies under what circumstances costs increases or decreases,

how total output behaves when all units of one factor (input) are increased keeping

other factors constant or when all factors are simultaneously changing. How can

output be maximized from a given quantity of resources and how can the optimum

size of output be determined are also the main concern of production theory

(Stewart, 1991).

An input is a good or service that goes into the process of production and output is

any good or service that comes out of production (Dwivedi, 2008). Production

process requires a wide variety of inputs depending on the nature of product. Inputs

23

are categorized as fixed inputs and variable inputs. Theoretically, a fixed factor is one

that remains constant (fixed) for a certain level of output. And a variable input is the

one that changes with the change in output.

This theory enabled the researcher, in the course of her study, try to find out and

come up with the proof of whether CVP analysis is applicable only for short-term

decisions or not (Researcher, 2013).

2.1.4.3Pricing Theory

This theory was developed by Alfred Marshall in the early 20th

century and was

supported by other economists such as David Ricardo and Adam Smith. Price theory

has always been at the heart of economic theory and profit maximization has been the

most important assumption on which economists have built price and production

theories. This assumption has however, been strongly questioned and alternative

hypothesis suggested. Price theory explains how price is determined under different

kinds of market conditions; when price discrimination is desirable, feasible and

profitable; and to what extend advertising can be helpful in expanding sales in a

competitive market (Dwivedi, 2008). Thus price theory can be supportive in

determining the price policy of the firm. Price and production theories together, in

fact assist in shaping the optimum size of the firm.

Therefore, this study also took into consideration the statement given by Kaplan and

Atkinson in 1998, stating that “If managers tried to use the economists Cost Volume

Profit model, the cost of gathering and interpreting the data would be high, as well as

making the information more difficult to understand and less reliable”.

24

2.1.4.4 Theory of the Firm

The economic question of the firm is old. Adam Smith discussed firms in The Wealth

of Nations (1776) and established that they, in the sense of "manufactures," were

more efficient in producing than individual, self-employed craftsmen and labour

workers. Managerial theories of the firm, as developed by William Baumol (1959 and

1962), is microeconomic concept founded in neoclassical economics that states that

firms (corporations) exist and make decisions in order to maximize profits.

Businesses interact with the market to determine pricing and demand and then

allocate resources according to models that look to maximize net profits (Baumol,

1959).

The concept of a business model facilitates analysis of the way in which a firm

derives economic value from a newly developed technology. Indeed Chesbrough and

Rosenbloom (2002) have argued that it is the business model adopted, more so than

the technology itself, which is critical to the success of the commercialisation of new

technology. The concept is concerned with how the firm defines its competitive

strategy through the design of the product or service it offers to its market, how it

charges for it and what it costs to produce. How it differentiates itself from other

firms by the nature of its value proposition. It also describes how the firm integrates

its own value chain with that of other firms in the industry‟s value networks.

The review of this theory assisted the researcher to impose questions which helped

her to determine whether CVP analysis is still relevant in this dynamic and

competitive world of business.

25

2.1.4.5 Theory of Constraints

The Theory of Constraints (TOC) is a series of decision making techniques first

created by Dr. Eliyahu M. Goldratt beginning around 1980 and later applied and

augmented by a number of others. An earlier propagator of the concept was Wolfgang

Mewes

in Germany with publications on power-oriented management theory

(Machtorientierte Führungstheorie, 1963). There are several works which provide

reviews of TOC's history and development its major components applications

(Noreen et al, 1995;), and published literature (Mabin and Balderstone, 1999).

The Theory of Constraints has been applied to production planning, production

control, project management, supply chain management, accounting and performance

measurement, and other areas of business as well as such not-for-profit facilities as

hospitals and military depots ((Goldratt, 2008). It has also been applied to decision

making in educational settings.

The Theory of Constraints states that constraints determine the performance of a

system. A constraint is anything that prevents a system from achieving a higher

performance relative to its goal (Schleier, 2010). The Theory of Constraints was first

applied to business systems. Dr. Goldratt defines the goal of a for-profit business as to

make more money now and in the future. This definition is in keeping with the

traditional definition of the goal of a business which is to maximize the owners‟ or

stockholders‟ wealth. Constraints may be resource constraints such as a person or

department that cannot keep up with market demand (Goldratt, 1995).

The Theory of Constraints is perhaps the most advanced operations management

philosophy in existence (Goldratt, 2008). Its usefulness has been widely proven. It has

26

been used in conjunction with Lean and Total Quality Management and may help to

focus these initiatives on the organization‟s constraints to increase their impact.

The importance of this theory is on finding out if CVP analysis can incorporate all

relevant factors which affect business in decision making.

2.1.5 Factors Affecting Cost Volume Profit Analysis

Cost-volume-profit analysis involves a study of various factors that affect profit and a

study of their interrelationship. It is a technique used for measuring the functional

relationships between the major factors affecting profits; and for determining the

profit structure of the firm. It is used to determine how changes in costs and volume

affect a company's operating income and net income (Saxena and Vashist, 2007).

Therefore the key factors that affect the profit of a business are the ones which affect

CVP analysis. Such factors are the selling price of the products, volume of sales and

cost of production.

2.1.5.1 Basic Constituents

CVP analysis consists of five basic constituents that include: volume or level of

activity, unit selling price, variable cost per unit, total fixed cost, and sales mix. Cost-

Volume-Profit Analysis also consists of the CVP income statement, break-even

analysis, margin of safety, target net income and changes in business environment.

These components are vital to determining the success of a company through profit

margins (Lecture notes).

The five basic components interdepend based on well thought out assumptions in a

CVP analysis. The level of activity shows the costs and revenues display relevance in

27

range in activity, activity levels are displayed as diverse dimension bases in a

company. The variable cost per unit is determined by dividing the change in total cost

by the high minus low activity level. Total fixed costs remain the same and do not

change as activity may change. The sales mix indicates a combination of products

sold in a CVP (Saxena et al., 2007). The five basic components help define profit in a

CVP analysis.

2.1.5.2 Income Statement

Aside from the five basic components of a CVP analysis, there are many other

important factors that display a company‟s success. A CVP income statement

evaluates costs and expenses in a period and also reports the contribution margin. In a

CVP analysis there is a break even analysis that determines a point where total

revenues equal total costs, also known as the break-even point. The break-even point

can be found using a mathematical equation, finding the point on a CVP graph or

simply by using the contribution margin technique (Scarlett, 2005).

A margin of safety is also displayed, which is the amount of sales at a break-even

point and the actual or expected sales for the company. According to Robert et al.,

(2004), the income is projected for certain products, this is known as the target net

income. The Cost-Volume-Profit Analysis then closes with reporting changes in the

business environment and revisits the CVP income statement to review profit analysis

and projections over a period of time.

28

2.1.5.3 Contribution Margin

Another important aspect of a Cost-Volume-Profit Analysis is the contribution

margin. The contribution margin is the revenue remaining after deducting variable

costs. McWatters, et al. (2011) states that if the unit selling price increases, the

contribution margin per unit will decrease provided the unit variable costs remain the

same and do not also rise. If the unit variable costs rise with the selling costs, the

contribution margin might remain the same or may not show as much of an increase.

Contribution margin ratios are sometimes more preferred in a CVP analysis. A

contribution margin ratio is a percentage of sales contributing to a company‟s net

income. The contribution margin per unit divided by the unit selling price gives out

the contribution margin ratio (Magee, 1975). If one of the components of the

contribution margin ratio changes, the company‟s net income will also change. If the

sales increase, then the net income will increase. By the sales increasing, the unit

selling price can be decreased and increase the contribution margin to the company.

The contribution margin can improve the net income of the company but is very

dependent on the sales of a company. There are many factors that determine the net

income of a company, and the main factors are all displayed in a Cost-Volume-Profit

Analysis income statement (Magee, 1975).

2.1.5.4 Fixed Costs

Fixed costs are another factor to consider in a Cost-Volume-Profit Analysis. Fixed

cost by itself does not increase or decrease, but a fixed cost per unit may show a

change in rates. If the fixed price per unit decreases then the items produced will

decrease, and the sales of the item will be lowered until there is no more of the

29

product to sale (Luther, et al., 1998). The decline in the production of candy canes

will eventually thin out to nothing. A change in fixed costs can alter the sale of a

product from any company.

2.1.6 Challenges Facing Manufacturing Companies When Using CVP Analysis

for Decision Making

The challenges facing decision makers in the practical application of CVP relate to its

basic underlying assumptions. Economists (Vickers, 1997; Machlup, 1955) have been

predominantly critical of those assumptions. Their disapprovals take various forms,

but they all arise from CVP's departures from the ordinary supply and demand models

in price theory economics.

2.1.6.1 Linearity of Total Revenue and Total Cost Schedule

Possibly the most basic dissimilarity between CVP analysis and price theory models

is that CVP disregards the curvilinear nature of total revenue and total cost schedules.

Consequently, it assumes that changes in volume have no effect on elasticity of

demand or on the efficiency of production factors. Managerial accountants recognize

these economic critiques, but they believe nonetheless that CVP analysis is a very

useful initial analysis of strategic decisions (Horngren et al., 1994).

2.1.6.2 Similarities to Standard Economic Model

The supplementary condemnations of the underlying nature of CVP analysis stems

from its similarities to standard economic models, rather than its differences. Alike to

standard economic price theory models, basic CVP analysis usually assumes, among

other things, the following: single-stage, single-product manufacturing processes;

30

simple production functions with one causal variable; cost categories limited to only

variable or fixed; and data and production functions vulnerable to certainty

predictions (Chen et al, 2002). Further, CVP analysis is naturally restricted to one

time period in each case.

The shortcomings of CVP look like discouraging, but CVP is flexible enough to

overcome them all, if necessary and appropriate. Nonlinear and stochastic CVP

models involving multistage, multi-product, multivariate, or multi-period frameworks

are all possible, although a single model embracing all of those extensions would

appear a fundamental departure from the entire idea of CVP analysis, its basic

simplicity (Schneider, 1992). Universally, the durability and reputation of CVP

analysis definitely reflects the willingness of its users to "live with" the shortcomings

revealed by criticisms of its basic nature.

2.1.6.3 Focus on Revenue and Operating Expenses

The main concern lies on restricted focus of CVP on only sales revenue and operating

expenses. That drawback can leave some very significant aspects of strategic

decisions overlooked. Schneider (1992), for example, suggests that the scope of CVP

analysis ought to be widened to include the impact of managerial compensation

schemes on target profit levels. CVP does not measure the impact of the decision on

wealth, it does not incorporate the effect of asset structure changes required by the

decision and it does not acknowledge the risk created by the decision (Magee, 1975).

Some fairly simple extensions of the scope of the basic model can do much to

improve the shortcomings caused by those limitations.

31

2.1.6.4 Wealth Impacts of CVP Decisions

The first restriction of the basic CVP model that should be addressed is the

nonexistence of any dimension of a decision's impact on wealth. The existing CVP

model focuses on the total level of net profits produced by a decision, which may or

may not increase the wealth of the firm (Dwivedi, 2008). The decisive effect of a

specific decision upon wealth rests on the investment in assets necessary to

implement that decision. Though it would possibly be ideal to capture wealth effects

through present value analyses, the main improvement of CVP analysis, its relative

simplicity, would be lessened by the added complexities of present value techniques.

A simpler way to incorporate wealth effects in the CVP model would be to include

the firm's cost of capital in the analysis (Dwivedi, 2008).

2.1.7 CVP Analysis and the Modern Manufacturing Firms

2.1.7.1 Cost Structure

When CVP was developed, manufacturing firms had different cost structures than

modern manufacturing firms. Modern firms have a higher level of costs that remain

constant with changes in output, partly because modern firms are more capital

intensive, and partly because most of their labor cost is fixed. For example, the

supervisor of a machine is paid the same salary if the machine is running at 50% or

75%. Many authors (Kaplan et al., 1998) argue that traditional views of maximizing

contribution are no longer relevant.

32

2.1.7.2 Technology and Competition

In recent years particularly after the wide spread increase of technology in many

sectors, numerous firms have entered the market intending to take high percentage of

the market share. Consequently to compete more in the introduction market some

firms increase their sales regardless of the high price. They sell more at low price to

achieve progress in addition to reducing the inventory of some kinds of products.

According to Mc Watters et al., (2001), in most markets if you want to sell more, you

must lower your sale price. Assuming that one can sell very large quantity at a

constant price is unrealistic. CVP analysis has no explicit assumption of a constraint

in production or sales. The assumption of a constant sales price is probably accurate

only over a narrow range of output levels (Researcher, 2013).

Since its introduction in the 19th century, CVP analysis concept has been used,

enhanced, adjusted and extended in an attempt to reduce or correct for its limitations

and make it applicable to more and more business situations Vickers, (1997).

Hongren et al (2000) asserts that, inspite of its limitations and criticisms, cost-

volume-profit analysis continues to be considered as one of the best ways to focus on

the relationship between cost, volume and profitability.

2.1.7.3 Strategic Planning

Horngren et al. (2000) note that firms across a variety of industries have found the

simple CVP model to be helpful in both strategic and long-run planning decisions.

Furthermore, a survey of management accounting practices indicates that CVP

analysis is one of the most widely used techniques (Garg et al., 2003). However,

Horngren et al. (2000) warn that, in situations where revenue and cost are not

33

adequately represented by the simplifying assumption of CVP analysis, managers

should consider more sophisticated approaches to financial analysis.

2.1.8 Budgeting and CVP Analysis

Business prepares long-term plans and these are transformed into financial plans that

indicate what needs to be done and the financial resources required in accomplishing

it. Budgeting therefore transforms the plan of action into statistics. The budgeting

process is an important piece of the business planning process. It provides managers

with the opportunity to carefully match the goals of the organization with the

resources necessary to accomplish those goals. A well thought-out budget gives the

company a numeric picture of potential income, expenses and profitability (Scarlett,

2005).

According to Bhattacharyya (2011), Cost-volume-profit analysis is helpful in setting

up flexible budget which indicates cost at various levels of activities. A flexible

budget shows budgeted revenue, costs and profits for different levels of business

activity. Thus a flexible budget can be used to evaluate the efficiency of departments

throughout the business even if the actual level of business activity differs from

management's original estimates (McWatters, et al. (2011). The amounts included in a

flexible budget at any given level of activity are based on cost-volume-profit

relationships.

The flexible budget responds to changes in activity, and may provide a better tool for

performance evaluation. It is driven by the expected cost behavior. Fixed factory

34

overhead is the same no matter the activity level, and variable costs are a direct

function of observed activity.

A good financial model works in much the same fashion as flight simulator, allowing

an organization to test the interactions of decisions and economic variables in variety

settings (Hilton et al, 2003). He further argues that financial models should be

designed to have the following characteristics and objectives; (1) Usefulness for

decision making, (2) Accurate and reliable simulator of relevant factors and relations

and (3) Flexible and responsive analysis.

2.1.9 CVP as Performance Evaluation Tool

Performance evaluation has been identified as an important function of management

accounting (Emmanuel et al., 1990). Managers develop a group of measures that

identify changes in performance quality so that employees can determine what needs

to be done to improve performance

Cost management tools are essential to exert control over cost and to appraise

managerial performance in different segments of an organization particularly in

manufacturing organizations. Paulo, (2002) asserts that CVP analyses are useful for

planning and monitoring operations and for motivating employee performance.

Budgets are updated continuously to accommodate management‟s need for

performance evaluation in some settings such as just-in-time (JIT) or total quality

management (TQM) environments (Drury, 2004). This helps managers determine,

very specifically, what the future will hold if variables are altered. For instance,

35

transportation expenses and costs for materials can change. These variable costs can

affect the bottom line. CVP analysis allows the manager to plug in variable costs to

establish an idea of future performance, within a range of possibilities.

Profit analysis refers to the techniques used to generate an overall performance

evaluation from the financial perspective. It is a broader level of analysis than the

standard cost variance analysis for manufacturing costs and includes those variances

as well as several others. It is usually based on a comparison of the actual data with

the budget, but the actual data for the current period can also be compared with the

actual data from a previous period (Lucey, 1996).

Managers constantly monitor existing operations of their organizations to find out if

they would achieve the desired levels of profit. For this purpose, a number of tools are

available; one such tool is Cost-Volume-Profit (CVP) analysis (Emmanuel et al.,

1990).

When performance evaluation is based on a static budget, there is little incentive to

drive sales and production above anticipated levels because increases in volume tend

to produce more costs and unfavorable variances (Lucey, 1996). The flexible budget-

based performance evaluation provides a remedy for this phenomenon.

2.2 Empirical Literature Review

Countries with emerging economies suffer at times from the effects of political and

economic events which leave their businesses in a state of uncertainty. Within these

variables which are reflected in the price of the product or service and consequently

in the result, that is profit. To best administrate businesses in this scenario they must

36

be equipped with more efficient administrative controls which minimise the risk for

investment.

Magdy Abdel-Kader (University of Essex) and Robert Luther (University of the West

of England, Bristol) in their study on Management accounting practices in the UK

food and drinks industry in 2006 concluded that Cost Volume Profit analysis is most

frequently used in short-term decisions.

According to the study conducted by Syed Maqbool-ur-Rehman, (2011) entitled

“which management accounting techniques influence profitability in the

manufacturing sector of Pakistan?” it was found that Budgeting with a mean score of

4.42 (out of a maximum score value of 5) remained the most used and practiced

management accounting technique followed by Cost Volume Profit analysis. And An

Exploratory Study of Management Accounting Practices in Manufacturing

Companies in Barbados done by Philmore Alleyne in 2011 showed that the frequency

of use of CVP analysis is 67%.

These studies were most concerned with profitability influence and frequency of

usage, but they did not consider the limitations on applicability and relevancy of the

model in the rapid technological changing business environment (Researcher, 2013).

The Comparative Analysis of Management Accounting Practices in Australia and

Japan: An Empirical Investigation channelled in 1999 by H. Wijewardena and A. De

Zoysa, came out with results indicating that CVP analysis is the second important

technique in Japan and fifth in Australia. The ranking of importance indicates that the

37

Australian companies placed heavier emphasis on budgets, historical accounting

statements and standard costing while Japanese companies concentrated more heavily

on target costing, cost-volume-profit analysis and budgets.

Toomas Haldma and Kertu Lääts in their study on “Influencing contingencies on

management accounting practices in Estonian manufacturing companies” (2002)

asserted that Variable costing with the cost-volume-profit analysis offered a

convenient and more objective way to get an idea about the cost formation process in

manufacturing, to fix the price ranges and to realise an active pricing policy.

Manoj Anand, B.S. Sahay and Subhashish Saha 2005 in their empirical study on Cost

Management Practices in India found that The most widely used management tool is

cost-volume-profit analysis (77.3%) with reference to 65 percent adoption rate

finding of Joshi, 2001).

It was found that Break Even analysis could be applied in production planning and

control of manufacturing firms even where it is a multi-product firm. This is in line

with the studies of Ndaliman and Bala (2007) and the assertion of Nweze (1992).

These studies indicate that Break Even or CVP is applicable in many situations. The

other finding is that a relationship exists between the applications of break-even

analysis in production planning and control and the frequency with which due

dates/schedules are met by the firm.

In the study conducted in Nigeria by Ann I. Ogbo, Christopher Chukwudi Orga and

Adibe, T.N in 2012 with the title “Improving Production Planning and Control

38

through the Application of Breakeven Analysis in Manufacturing Firms in Nigeria”;

the results and findings suggest that multi- product firms can apply breakeven

analysis to great advantage. The single product firms can easily apply breakeven

analysis in production planning and control. Manufacturing firms in Enugu Urban

that apply breakeven analysis in production planning and control were more likely to

be profitable. Also such firms were more likely to meet due dates/schedules.

Manufacturing firms that apply breakeven analysis in production planning and control

were less likely to generate scraps. Most mass industries do not consciously engage in

breakeven analysis as a production planning and control tool.

Although it is nearly impossible to eliminate scrap and rework completely, they can

be reduced by optimizing the way product data are documented, reviewing

manufacturing processes and communicating manufacturing and engineering changes

throughout the supply chain. If priority is given to evaluating and improving

manufacturing processes, it becomes much easier to reduce the amount of scrap and

rework in the organization (Researcher, 2013).

It is clear to the company that understanding how costs behave is absolutely key to

making good decisions that affect market share analysis, annual budget preparation

and monitoring of results, sales volume and business mix decisions, pricing policies,

and cost management. According to the study done in Africa (Egypt) by Mohamed

(2006), as fixed costs in manufacturing organizations increase, and the economy

continues to shift more and more to service and e-commerce organizations, this fixed