Financial Analysis & Comparison

21

Running head: FINANCIAL ANALYSIS & COMPARISON 1 Financial Analysis & Comparison May 30, 2014

-

Upload

coloradotech -

Category

Documents

-

view

1 -

download

0

Transcript of Financial Analysis & Comparison

Running head: FINANCIAL ANALYSIS & COMPARISON 1

Financial Analysis & Comparison

May 30, 2014

FINANCIAL ANALYSIS & COMPARISON 2

Financial Analysis & Comparison

The manufacturing company chosen to be betrayed in this

financial analysis is Ford Motors. Ford Motors Co. is a major

distributor of vehicles worldwide. They specialize in

manufacturing everything from small cars, trucks and luxury brand

vehicles. The annual report will be reviewed to help give incite

on how this company ranks in sales and comparisons to its

competitors. Annual reports are accounting reports that are

issued to reveal performance, assess the success or failures of

the facility and inform shareholder’s exactly how the corporation

is doing. The annual report for 2013 Ford Motors Co. ranked

number ten in global revenues after dropping a notch from the

previous year from nine. Research has shown that it has declined

from its 2008 position of eight, (CNN Money, 2014).

Links to Ford Motors’ Financial Documents

Balance Sheet-http://finance.yahoo.com/q/bs?

s=F+Balance+Sheet&annual and Income

Statement-http://finance.yahoo.com/q/is?

s=F+Income+Statement&annual, (Yahoo Finance, 2014). Full Annual

FINANCIAL ANALYSIS & COMPARISON 3

report http://corporate.ford.com/doc/916/251/ar2013- 2013%20Ford

%20Annual%20Report%20MR.pdf , (Ford Motor Company, 2013).

FINANCIAL ANALYSIS & COMPARISON 4

FINANCIAL ANALYSIS & COMPARISON 5

FINANCIAL ANALYSIS & COMPARISON 6

Determining Financial Ratios

Financial ratios are relationships between different

accounts from financial statements. These ratios serve as

performance indicators because the reveal relative values and

allow for comparisons across time. The purpose of financial

ratios is to inform corporate heads on the best direction to lead

the firm and to inform investors on how well the company is doing

financially. This gives interested parties a chance to locate and

correct problems for performance improvement.

Return on Assets

Return on assets or ROAs measures how much the firm has earned from the use of its

total assets. The equation is Ford’s ROA= Total Income Average Total

Assets

Total income represents all revenue a business earns before

paying expenses, (Keythman, 2014). Assets represent anything

owned or owed to the company. Calculations for Ford Motors Co

return on assets are 1.48%. This information was gathered from

the December 31, 2013 income statement divided by the total

assets on the balance sheet.

FINANCIAL ANALYSIS & COMPARISON 7

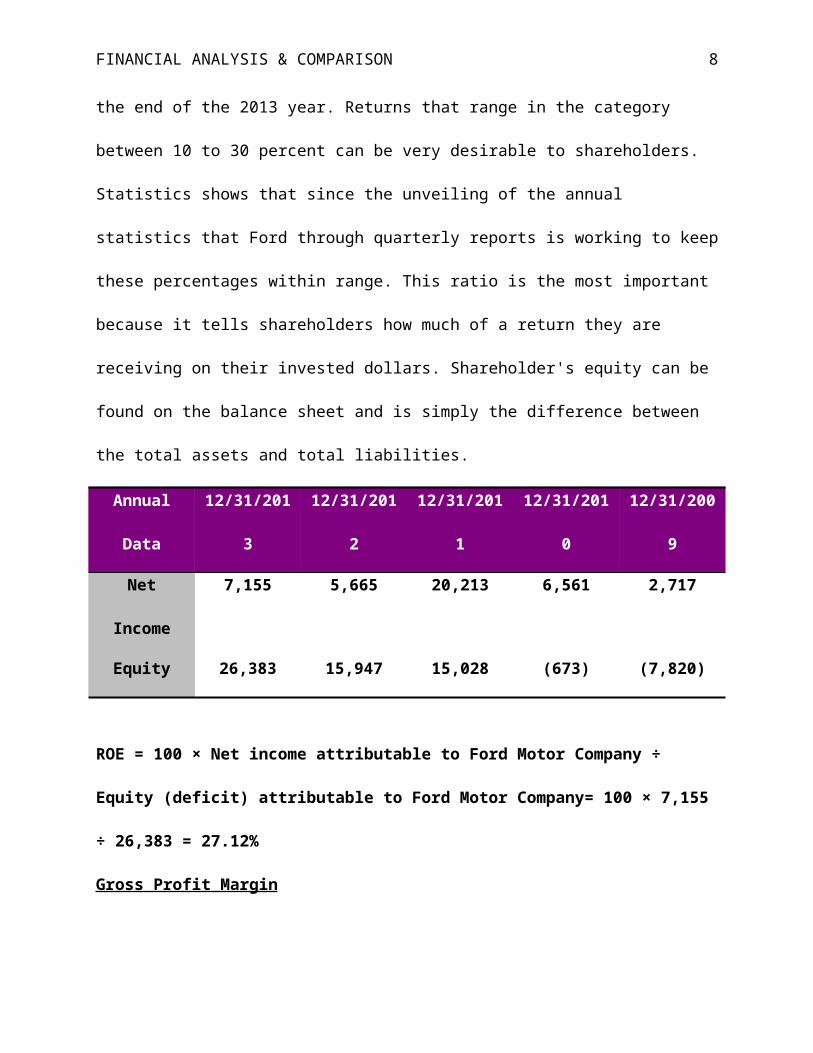

Return on Equity

Return on equity measures how much the firm earned as a

percentage of the investments

made by shareholders. Return on Equity can be figured by finding the shareholder's equity on the

balance sheet and is simply the difference between the total assets and total liabilities. The

equation is calculated Ford’s ROE= Profit (Net Income) Average Shareholders’

Equity

Return on equity is important because it helps a company

determine if they consume cash or create assets. Ford Motors ROE

was 27.12% on December 31, 2013. Quarterly reports for March 31,

2014 ranked ROE for the company at 29.59% which shows it has had

a significant drop from

FINANCIAL ANALYSIS & COMPARISON 8

the end of the 2013 year. Returns that range in the category

between 10 to 30 percent can be very desirable to shareholders.

Statistics shows that since the unveiling of the annual

statistics that Ford through quarterly reports is working to keep

these percentages within range. This ratio is the most important

because it tells shareholders how much of a return they are

receiving on their invested dollars. Shareholder's equity can be

found on the balance sheet and is simply the difference between

the total assets and total liabilities.

Annual

Data

12/31/201

3

12/31/201

2

12/31/201

1

12/31/201

0

12/31/200

9

Net

Income

7,155 5,665 20,213 6,561 2,717

Equity 26,383 15,947 15,028 (673) (7,820)

ROE = 100 × Net income attributable to Ford Motor Company ÷

Equity (deficit) attributable to Ford Motor Company= 100 × 7,155

÷ 26,383 = 27.12%

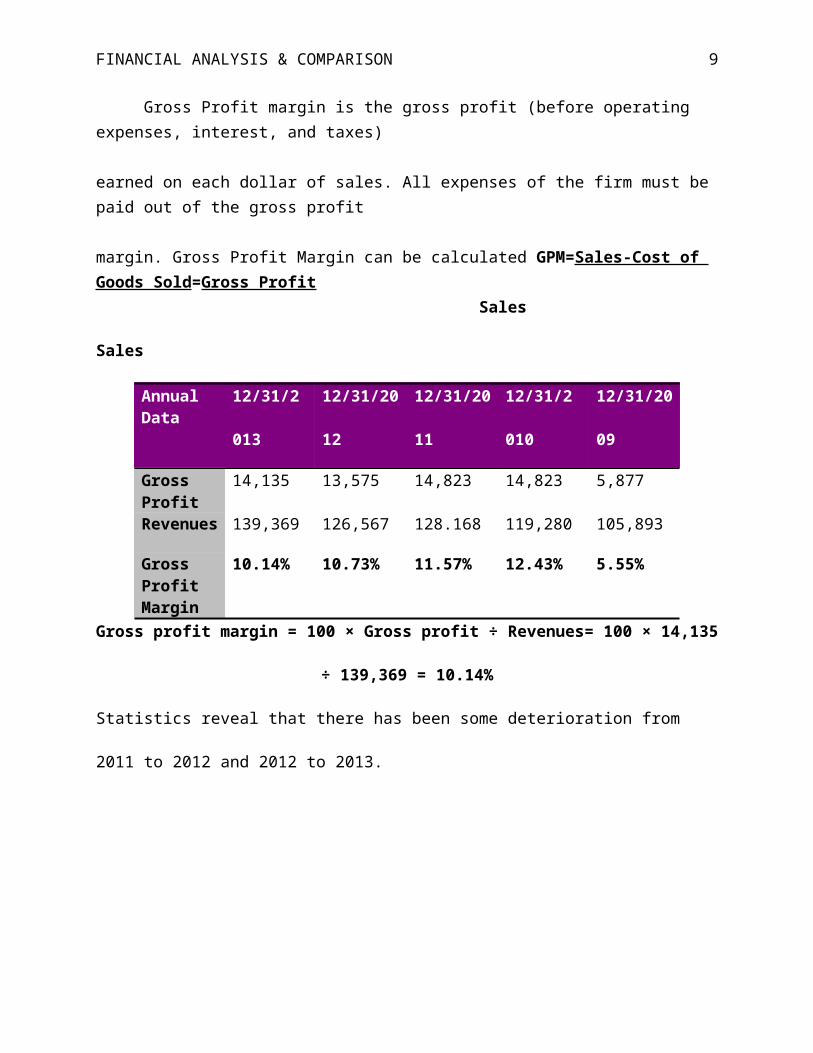

Gross Profit Margin

FINANCIAL ANALYSIS & COMPARISON 9

Gross Profit margin is the gross profit (before operating expenses, interest, and taxes)

earned on each dollar of sales. All expenses of the firm must be paid out of the gross profit

margin. Gross Profit Margin can be calculated GPM=Sales-Cost of Goods Sold=Gross Profit

Sales

Sales

AnnualData

12/31/2

013

12/31/20

12

12/31/20

11

12/31/2

010

12/31/20

09

Gross Profit

14,135 13,575 14,823 14,823 5,877

Revenues 139,369 126,567 128.168 119,280 105,893

Gross Profit Margin

10.14% 10.73% 11.57% 12.43% 5.55%

Gross profit margin = 100 × Gross profit ÷ Revenues= 100 × 14,135

÷ 139,369 = 10.14%

Statistics reveal that there has been some deterioration from

2011 to 2012 and 2012 to 2013.

FINANCIAL ANALYSIS & COMPARISON 10

Debt to Equity Ratio

Debt to Equity Ratio shows the relationship between the suppliers of credit and equity.

The ratio can be calculated by using the equation Debt-Equity Ratio= Total Liabilities

TotalEquity

AnnualData

12/31/2013

12/31/2012

12/31/2011

12/31/2010

12/31/2009

Debt/Payable1yr

1,257 1,386 1,033 2,049 2,095

LTD/Payable

1yr

14,426 12,870 12,061 17,028 32,321

TotalDebt

15,683 14,256 13,094 19,077 34,416

Equity(deficit)

26,383 15,947 15,028 (673) (7,820)

Debt to equity = Total debt ÷ Equity (deficit) attributable to Ford Motor Company

= 15,683 ÷ 26,383 = 0.59

Statistics reveal that there indeed was a decline from 2012 to 2013.

Debt Ratio

The debt ratio measures the proportion of assets financed by

the debt. The greater the total debt ratio, the more leveraged

and risky things can become for the firm. The key is to always

FINANCIAL ANALYSIS & COMPARISON 11

ensure that the total assets outweigh liabilities. Companies need

to be aware of their abilities to pay back long term debt and if

that debt will cloud or overwhelm the assets and profits that are

made. The Equation for measuring the debt ratio is

Total Debt Ratio=Total LiabilitiesAssets

AnnualData

12/31/2013

12/31/2012

12/31/2011

12/31/2010

12/31/2009

Liabilities

177,005 176,055 164,177 166,435 204,405

Assets 203,752 192,366 179,248 165,793 197,890TotalDebtRatio

0.869 0.915 0.914 1.004 1.032

Ford did manage in 2011 to drastically decrease their debt ratio from the all-time high they had

in 2009 but it has been steadily increasing from 2011 to 2013.

FINANCIAL ANALYSIS & COMPARISON 12

Current Ratio

Creditors are particularly interested in the widely reported

current ratio of businesses. Analyzing this ratio ensure the

firm’s ability to meet its short-term obligations. Assets can be

converted into cash within a year and the firm will be able to

pay current liabilities. This ratio in general helps to give an

effective measure of the firm’s liquidity. The goal is to ensure

a ratio of one but to ensure financial cushioning firms will want

to maintain well over that allotment. The Equation is Current

ratio = Current assets ÷ Current liabilities.

This ratio accounts for all inventories that the company

currently possesses.

AnnualData

12/31/2013

12/31/2012

12/31/2011

12/31/2010

12/31/2009

CurrentAssets

42,547 43,175 38,147 34,368 40,560

CurrentLiabiliti

es

37,003 35,228 32,825 34,516 37,037

CurrentRatio

1.15 1.23 1.16 1.00 1.10

Current ratio = Current assets ÷ Current liabilities= 42,457 ÷

37,003 = 1.15.

FINANCIAL ANALYSIS & COMPARISON 13

The five year table reveals that at one particular point

between 2011 the current ratio showed improved but has dropped

significantly from 2012-2013. Even though Ford has dropped this

ratio ensures that Ford has enough to cover liabilities.

Quick Ratio

Quick ratio is described a calculating the cash plus short-

term marketable investments plus receivables divided by the

current liabilities. It does not include all inventories as

current ratio requires. The equation for Quick ratio = (cash +

marketable securities + net receivables) / current liabilities.

FINANCIAL ANALYSIS & COMPARISON 14

AnnualData

12/31/2013

12/31/2012

12/31/2011

12/31/2010

12/31/2009

Cash &CashEquiv.

4,959 6,247 7,965 6,301 10,309

Marketable

Securities

20,157 18,178 14,984 14,207 15,169

Receivables, LessAllowance

s

5,641 5,361 4,219 3,992 3,708

TotalQuickAssets

30,757 29,786 27,168 24,500 29,186

CurrentLiabiliti

es

37,003 35,228 32,825 34,516 37,037

Ford’sQuickRatio

0.83 0.85 0.83 0.71 0.79

Quick ratio = Total quick assets ÷ Current liabilities= 30,757 ÷

37,003 = 0.83.

Ford’s quick ratio improved from 2011 to 2012 but then slightly

deteriorated from 2012 to 2013 not reaching 2011 level, (Stock

Analysis on the net, 2014).

Inventory Asset Turnover

Inventory Asset Turnover is the number of times the value of

inventory assets turns over in a period. The equation is IAT=Cost

of Goods Sold/Average Inventory.

FINANCIAL ANALYSIS & COMPARISON 15

AnnualData

12/31/2013

12/31/2012

12/31/2011

12/31/2010

12/31/2009

Cost ofSales

125,234 112,992 113,345 104,451 100,016

Inventories

7,708 7,362 5,901 5,917 5,450

FordTurnoverRate

16.25 15.35 19.21 17.65 18.35

Inventory turnover = Cost of sales ÷ Inventories= 125,234 ÷ 7,708

= 16.25

Data reveals there was gradual deterioration for Ford Motor Co.

in the Inventory turnover from 2011 to 2013.

FINANCIAL ANALYSIS & COMPARISON 16

Price Earnings Ratio

Price Earnings Ratio is where the market price per share is

divided by earnings per share and indicates how any times

earnings. This can include years’ worth of earnings the market is

paying for the stock. It can be calculated by PE=Market price of

Stock/Earnings per Share.

This ratio is considered to be a stock market ratio because it

can be calculated from data associated with the stock market

performance. The P/E ratio informs analyst just exactly how much

an investor in common stock pays per dollar of current earnings.

AnnualData

12/31/2013

12/31/2012

12/31/2011

12/31/2010

12/31/2009

# Sharesof Com.Stock

Outstanding

3,943,822,377

3,922,247,667

3,800,746,841

3,782,710,935

3,368,265,681

NetIncome to

Ford

7,155 5,665 20,213 6,561 2,717

Shareprice

1.81 1.44 5.32 1.73 0.81

FordMotor Co.

8.48 8.99 2.36 8.68 14.60

Shows slight increase but then decreased in 2012-2013.

FINANCIAL ANALYSIS & COMPARISON 17

FINANCIAL ANALYSIS & COMPARISON 18

Memo

To: Jackie Russell, CEO

From: Stephanie Moore, Financial Analyst

RE: Ford Financial Summary

Date: June 1, 2014

Ford Motor Company Executive Summary

As requested I am submitting to you a financial summary of afive year comparison for Ford Motor Company. Ford Motor Company is a two sector corporation that manufactures vehicles under the Ford and Lincoln Brand. The other sector offers financial services by financing products by means of automotive dealers. This sector also encompasses retail installment sale contracts for new and used vehicles, lease for new vehicles to retail customers, government entities, daily rental car companies, and fleet customers. Ford Motor Company also offers the option to comprise loans to dealers to finance the purchase of vehicle inventory, loans to dealers to finance working capital, and to purchase dealership real estate, (Yahoo Finance, 2014).

Horizontal Analysis

This analysis is intended to discuss findings from the balance and income sheet which revealed over the five year time span for Ford Motor Company. In that time span the average total assets is with an average of about -----% increase. Assetsshowed an increase/decrease with a rise in -------and then a gradual decline during 20--.

FINANCIAL ANALYSIS & COMPARISON 19

Vertical Analysis

FINANCIAL ANALYSIS & COMPARISON 20

References

CNN Money (2014). Fortune 500 Annual Reports of Ford Motors. Retrieved

from:

http://money.cnn.com/magazines/fortune/fortune500/2013/snapshots/

160.html

Ford Motor Company (2013). 2013 Annual Report. Retrieved from:

http://corporate.ford.com/doc/916/251/ar2013-013%20Ford

%20Annual%20Report%20MR.pdf

Keythaman B., (2014). How to Calculate Total Revenue on a Financial Statement.

Hearst

Newspaper LLC: Retrieved from

http://smallbusiness.chron.com/calculate-total-revenue-

financial-statement-52111.html

Stock Analysis on Net (2014). Liquidity Analysis. Retrieved from:

http://www.stock-analysis-on.net/NYSE/Company/Ford-Motor-

Co/Ratios/Liquidity

Yahoo Finance (2014). Ford Company’s Balance Sheet. Retrieved from:

http://finance.yahoo.com/q/bs?s=F+Balance+Sheet&annual

Yahoo Finance (2014). Ford Company’s Income Statement. Retrieved from:

FINANCIAL ANALYSIS & COMPARISON 21

http://finance.yahoo.com/q/is?s=F+Income+Statement&annual