factors influencing knowledgeable consumers' level of - USM

229

FACTORS INFLUENCING KNOWLEDGEABLE CONSUMERS’ LEVEL OF ACCEPTANCE OF GOODS AND SERVICES TAX SHALENE KALYANASUNDARAM Research report in partial fulfilment of the requirements for the Degree of Master of Business Administration Universiti Sains Malaysia 2015

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of factors influencing knowledgeable consumers' level of - USM

FACTORS INFLUENCING KNOWLEDGEABLE CONSUMERS’ LEVEL OF

ACCEPTANCE OF GOODS AND SERVICES TAX

SHALENE KALYANASUNDARAM

Research report in partial fulfilment of the requirements for the

Degree of Master of Business Administration

Universiti Sains Malaysia

2015

This thesis is dedicated to my Papa, S.K. Sundaram who is my sturdiest pillar of

support and who inspired my interest in GST.

I can never thank you enough.

ii

ACKNOWLEDGEMENT

First and foremost, I am grateful to God for being able to conduct a research in an

area of much interest to me and for surrounding me with the best of people who have

supported me endlessly throughout this challenging journey. I am immensely indebted to my

mentor, Professor Dato’ Dr Hasnah Haron for her impeccable guidance, support, motivation,

approachability and constructive feedback without which this research would not have been

possible. Her diligence and dedication was highly inspiring and words cannot express the

honor and gratitude I feel to have worked with her.

I would also like to thank respected professors, namely Associate Professor Dr

Jayaraman and batch-mates who were so generous with their time and knowledge in assisting

me throughout the duration of this research paper. Their kind assistance and valuable

feedback enabled the successful completion of this paper. I would also like to take this

opportunity to thank my good friends; Bong-Arkya, Suria Chetta, Deepa, Thivagar and

Ameet from the bottom of my heart as they were my pillars of support and encouragement as

we travelled through this journey, spending days and nights together to finish this paper.

I would also like to thank my respondents who have participated in the study. I would

not have been able to contribute this study without their assistance. They have played a key

role in this research paper and I would like to pass my sincere gratitude to them.

Last but not at all least, I would like to thank my ever supporting parents, siblings,

employers, colleagues, friends, FREAKSisters and devoted fiancé for their constant show of

support, understanding, love and encouragement. Everyone played an important part in

easing the challenges I had to face throughout this period. Without this amazing support

system, this research paper would not have been a reality.

iii

TABLE OF CONTENTS

Page

ACKNOWLEDGEMENT…………………………………………………………….ii

TABLE OF CONTENTS……………………………………………………………..iii

LIST OF TABLES………………………………………………………………….....ix

LIST OF FIGURES…………………………………………………………….……..xi

ABSTRAK……………………………………………………………………….......xiii

ABSTRACT…………………………………………………………………………..xiv

LIST OF ABBREVIATION………………..…………………………………………xv

CHAPTER 1 INTRODUCTION………………………………………………………1

1.0 Introduction…………………………………………………………………........1

1.1 Background of the Study…………………………………………………………1

1.2 Problem Statement………………………………………………………………..3

1.3 Research Objectives ……………………………………………………………...7

1.4 Research Question……………………………………………………………......7

1.5 Definition of Key Terms …………………………………………………………8

1.6 Significance of the Study………………………………………………..………..9

1.6.1 Practical Implication…..………………………………………………...……..9

1.6.2 Theoretical Implication……………………………………………………….11

1.7 Organization of the Remaining Chapters……………………………………….12

iv

CHAPTER 2 LITERATURE REVIEW………………………………………..…….13

2.0 Introduction……………………………………………………………………13

2.1 Malaysian Taxation……………………………….……………………………13

2.2 Consumers………………………..……………………………………………14

2.3 GST…………………………………………………………………………….16

2.3.1 Reasons for Implementing GST……………………………………………..16

2.3.2 Significance of GST…………………………………………………………18

2.3.3 Mechanism of GST……………………………………………………….....19

2.3.4 GST rate in the ASEAN countries…………………………………………..24

2.3.5 Implementation of GST……………………………………………………..25

2.4 Theory…………………………………………………………………………26

2.4.1 Theory of Planned Behavior (TPB)………………..……………………….26

2.5 Dependent Variable……………………………………………………………28

2.6 Antecedent and Independent variables ………………………………………..29

2.6.1 Attitude………………………………………………………………………29

2.6.2 Rule Observance Behavior……………………………………………..…....31

2.6.3 Perception of fairness of GST…………………………………………..…...32

2.6.4 Subjective Norm……………………………………………………………..34

2.6.5 Perceived behavioral control (PBC)…………………………………………35

2.6.6 Level of GST Knowledge………………………………………………...….36

2.6.7 Self-Efficacy…………………………………………………………………37

2.7 Theoretical Framework………………………………………………………...39

2.8 Factors Affecting Level of Acceptance of GST………………………………..41

2.8.1 Studies on Goods & Services Tax…………………………………………...44

2.8.2 Studies on Tax compliance……………………………………………….….44

v

2.8.3 Studies on Intention to Accept…………………………………………….....44

2.8.4 Other Studies……………………………………………………………..…..45

2.9 Hypotheses Development………………………………………………………46

2.9.1 Rule observance behavior and attitude ………………………………………46

2.9.2 Perception of Fairness of GST and attitude…………………………………..46

2.9.3 Level of GST Knowledge and Perceived Behavioral Control………………..47

2.9.4 Self-efficacy and Perceived Behavior Control ……………………………….48

2.9.5 Attitude and Level of Acceptance…………………………………………….50

2.9.6 Subjective Norms and Level of Acceptance………………….……………….51

2.9.7 Perceived Behavioral Control and Level of Acceptance……………………...52

2.10 Summary……………..………………………………………………………..53

CHAPTER 3 RESEARCH METHODOLOGY………………………………………55

3.0 Introduction……………………………………………………………………...55

3.1 Research Design………………………………….……………………………...55

3.1.1 Type of Study……………………………………………………………..…..55

3.1.2 Population and Unit of Analysis……………………………………………...56

3.1.3 Sample Size…………………………………………………………………..58

3.1.4 Sampling Method…………………………………………………………….59

3.1.5 Data Collection Techniques………………………………………………….59

3.1.6 Survey Instrument…………………………………………………………....60

3.1.7 Questionnaire Design………………………………………………………...61

3.2 Measurements of Variables…………………………………………..…….…..63

3.2.1 Measurements of Antecedent Variables and Independent Variables………..63

3.2.2 Level of Tax of Knowledge Scoring………………………………………...64

3.2.3 Measurement of Dependent Variable………………………………………..65

vi

3.3 Pre Test…………………………………………………………………...……67

3.4 Pilot Test….……………………………………………………………………68

3.5 Data Analysis………………………………………………………….……….71

3.5.1 Structured Equation Modeling (SEM)………………………………………71

3.5.2 Covariance-based SEM (CBSEM) against Variance-based SEM

with Partial Least Squares (PLS)……………………………………………72

3.5.3 Statistical Analysis…………………………………………………………..74

3.5.4 Demographic Analysis………………………………………………………74

3.5.5 Common Method Bias………………………………………………………74

3.5.6 Descriptive Analysis………………………………………………………...75

3.5.7 Goodness of Data Test………………………………………………………76

3.5.8 Factor Analysis……………………………………………………………....76

3.5.9 Validity Analysis…………………………………………………………….77

3.5.10 Reliability Analysis………………………………………………………….78

3.5.11 Goodness-of-Fit (GoF)………………………………………………………79

3.6 Summary……………………………………………………………………….79

CHAPTER 4 RESULTS…………………………………………………………….81

4.0 Introduction……………………………………………………………………81

4.1 Response Rate…………………………………………………………………82

4.2 Profile of Respondents…………………………………………………….…..83

4.3 Descriptive Statistics and Multicollinearity ………………………………..…86

4.4 Common Method Bias using Principal Component Analysis ……...…………90

4.5 Data analysis and results ………………………………………………….…..91

4.5.1 Goodness of measures……………………………….………………….......91

4.5.2 Pathway of Each Model Construct………………………………………….92

vii

4.5.3 Construct validity…………………………………………………………...93

4.5.4 Convergent validity…………………………………………………………93

4.5.5 β value and R Square………………………………………………………..94

4.5.6 Discriminant validity………………………………………………………..95

4.5.7 SEM Model…………………………………………………………………95

4.5.8 Results of each model………………………………………………………96

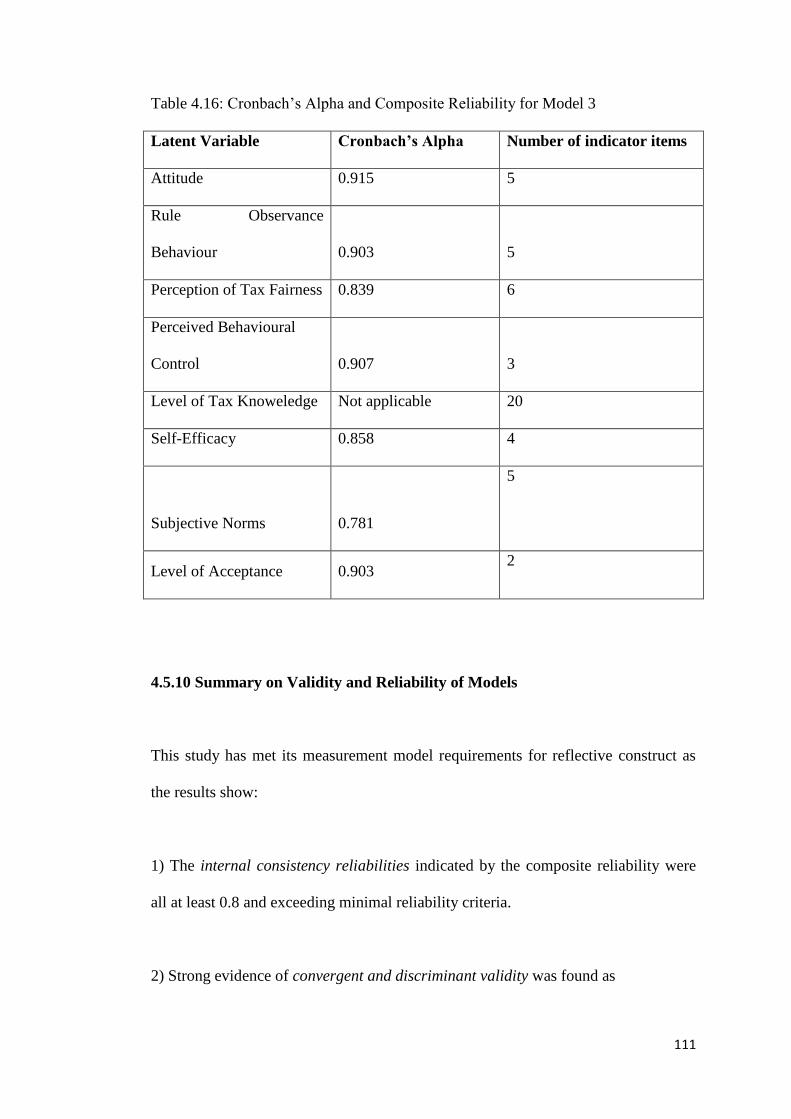

4.5.9 Reliability Analysis………………………………………………………..110

4.5.10 Summary on Validity and Reliability of Models………………………….111

4.5.11 Summary of Hypothesis Testing…………………………………………..113

4.5.12 Goodness-of-Fit……………………………………………………………114

4.6 Summary……………………………………………….…………………….115

CHAPTER 5 DISCUSSIONS AND CONCLUSIONS……………………………116

5.0 Introduction…………………………………………………………………..116

5.1 Recapitulation of the Study Findings………………………………………...116

5.2 Discussion…………………………………………………………………….119

5.2.1 What is the GST acceptance level amongst Malaysians?.............................120

5.2.2 What is the relationship of rule observance behavior and perceptions

of tax fairness with attitude of consumer?...........................................................123

5.2.3 What is the relationship of Self – Efficacy and Level of Tax Knowledge

with Perceived Behavior Control?.........................................................................125

5.2.4 What is the relationship of Attitude, Subjective Norms and

Perceived Behavioral Control with Level of Acceptance? .............................128

5.3 Summary and findings…….……………………………………………………130

5.4 Implications...……………………………………………………………….….131

5.4.1 Theoretical Implication……………………………………………………...131

viii

5.4.2 Practical Implication………………………………………………………...133

5.5 Limitation………………………………………………………….…………...138

5.6 Suggestion for Future Research ………………………………………………..138

5.7 Conclusion……………………………………………………………………...140

REFERENCES……………………………………………………………………….142

APPENDIX A – ECONOMIC REPORT 2010-2014- FEDERAL GOVERNMENT

REVENUE ……………………………………………..................167

APPENDIX B – ECONOMIC REPORT 2010-2014- FEDERAL GOVERNMENT

FINANCE ……………………………………………..................168

APPENDIX C – RESULTS OF MERDEKA CENTRE SURVEY ON GST....……169

APPENDIX D – QUESTIONNAIRE……………………………………………….176

APPENDIX E – PLS ALGORITHM REPORT (PILOT STUDY)………………….187

APPENDIX F – PLS ALGORITHM REPORT……………………………………..188

APPENDIX G – BOOTSTRAPPING PLS REPORT……………………………….199

APPENDIX H – IBM SPSS STATISTICS REPORT……………………………….203

ix

LIST OF TABLES

Page

Table 2.1 Key Studies on Malaysian Goods and Services Tax 42

Table 3.1 Profile of Contacts 60

Table 3.2 Summary of Questionnaire Sections 63

Table 3.3 Sources of measurement of variables 66

Table 3.4 Details of Models for analysis 69

Table 3.5 Cronbach’s Alpha for pilot study 70

Table 4.1 Summary on the Response Rate 82

Table 4.2 Socio-Demographic table – Respondent’s profile 83

Table 4.3 Descriptive Statistics and Correlation Matrix (n=228) 86

Table 4.4 Total Variance Explained 91

Table 4.5 Measurement model of VB-SEM- Model 1 97

Table 4.6 Discriminant Validity- Model 1 98

Table 4.7 Summary of PLS Results – Direct Effects- Model 1 99

Table 4.8 Measurement model of VB-SEM-Model 2 101

x

Table 4.9 Discriminant Validity- Model 2 101

Table 4.10 Summary of PLS Results – Direct Effects-Model 2 103

Table 4.11 Measurement model of VB-SEM-Model 3 105

Table 4.12 Discriminant Validity-Model 3 107

Table 4.13 Summary of PLS Results – Direct Effects- Model 3 109

Table 4.14 Cronbach’s Alpha and Composite Reliability for Model 1 110

Table 4.15 Cronbach’s Alpha and Composite Reliability for Model 2 110

Table 4.16 Cronbach’s Alpha and Composite Reliability for Model 3 111

Table 4.17

Summary of Hypotheses Testing

113

Table 5.1

Summary on t-test for Gender and Mode of Study

121

Table 5.2

Descriptive Table on Institutes and Level of Acceptance of GST

121

Table 5.3

ANOVA table of results for institution groups

122

Table 5.4

Descriptive Table on Income Level and Level of Acceptance of GST

122

Table5.5

ANOVA table of results for income level groups

122

xi

LIST OF FIGURES

Page

Figure 2.1 Cascading effect -Sales & Service tax 17

Figure 2.2 Cascading effect - Service tax 17

Figure 2.3 Input and output tax 20

Figure 2.4 Standard rated supply 21

Figure 2.5 Zero-rated supply 21

Figure 2.6 Exempt supply 22

Figure 2.7 GST Mechanism- standard rated 22

Figure 2.8 GST rates in the ASEAN countries 25

Figure 2.9 Theoretical Framework 40

Figure 4.1 PLS Pathway for Model 1 92

Figure 4.2 PLS Pathway for Model 2 92

Figure 4.3 PLS Pathway for Model 3 93

Figure 4.4 PLS output for Beta-value and R square value(Model 1) 98

xii

Figure 4.5 PLS output for testing population regression coefficients 100

Figure 4.6 PLS output for Beta-value and R square value – Model 2 102

Figure 4.7 PLS Output for testing population regression coefficients 103

Figure 4.8 PLS output for Beta-value and R square value-Model 3 108

Figure 4.9 PLS Output for testing population regression coefficients 109

xiii

ABSTRAK

Pelaksanaan Cukai Barangan dan Perkhidmatan (GST) pada 1 April 2015 adalah satu

kejayaan bagi Malaysia. Pelaksanaan GST adalah amat penting untuk menyokong

pembangunan negara. Kajian ini telah dibangunkan untuk mengenal pasti faktor-faktor yang

mempengaruhi tahap penerimaan GST oleh pengguna menggunakan’Theory of Planned

Behavior’. Faktor-faktor yang dikaji termasuk Peraturan kelakuan pematuhan, Persepsi

keadilan GST, Aras pengetahuan GST, ‘Self-efficacy’, Sikap, ‘Subjective Norm’ dan

‘Perceived Behavorial Control’. Borang soal selidik telah diedarkan kepada pelajar-pelajar

dalam talian MBA daripada Universiti Sains Malaysia, Universiti KebangsaanMalaysia,

Universiti Malaya dan Universiti Putra Malaysia pada Februari 2015. 228 MBA pelajar

mengambil bahagian dalam kajian ini dan Smart PLS telah digunakan untuk menguji kesahan

dan kebolehpercayaan data dan hipotesis.. Hasil kajian membuat kesimpulan bahawa 6

hipotesis daripada 7 disokong. Tahap penerimaan GST rendah dengan Sikap dan Persepsi

Kawalan Tingkahlaku menjadi pengaruh yang penting. Pematuhan Peraturan Kelakuan dan

Persepsi GST keadilan adalah ‘ántecedent’ yang penting kepada Sikap. Self-efficacy dan

Tahap pengetahuan GST adalah ántecedent’ yang penting kepada ‘Perceived Behavorial

Control’. Kajian menunjukkan bahawa walaupun tahap pengetahuan GST dipertingkatkan di

kalangan pengguna, tahap penerimaan tidak akan bertambah baik tanpa langkah-langkah

berkesan yang diambil untuk meningkatkan persepsi mereka terhadap keadilan GST. Di

samping itu, pemahaman GST tidak akan mencukupi untuk mempengaruhi penerimaan GST.

Pengguna perlu dididik bagaimana untuk menguruskan penggunaan dan kewangan mereka

serta diberikan sokongan yang mencukupi dalam tempoh peralihan ini.

xiv

ABSTRACT

The implementation of Goods and Services tax (GST) on the 1st of April 2015 is a milestone

for Malaysia. The implementation of GST is of vital importance in order to support the

development of the nation. This study was developed in order to identify the factors that

influence knowledgeable consumers’ level of acceptance of GST using the Theory of Planned

Behaviour. Factors examined include Rule observance behavior, Perception of fairness of

GST, Level of GST knowledge, Self-efficacy, Attitude, Subjective Norm and Perceived

Behavioral Control. Questionnaires were distributed online to MBA students of Universiti

Sains Malaysia, Universiti Kebangsaan Malaysia, Universiti Malaya and Universiti Putra

Malaysia in February 2015. 228 MBA students participated in the study and Smart PLS was

used to test the validity and reliability of the data as well as the hypotheses developed.

Findings of the study concluded that 6 hypotheses out of 7 were supported. The acceptance

level of GST was slightly low with Attitude and Perceived Behavioural Control being

significant influencers of the acceptance level. Rule Observance Behaviour and Perception of

GST fairness were significant antecedents to Attitude with perception of fairness being the

variable with higher weightage. Self-efficacy and Level of GST knowledge were acceptable

antecedents to Perceived Behavioral Control with Self-Efficacy carrying the higher

weightage of significance. This implies that although the level of GST knowledge is

enhanced amongst consumers, level of acceptance will not improve without effective

measures taken to enhance their perception of GST fairness. Besides that, the mere

understanding of GST will not be sufficient to influence acceptance of GST. Consumers need

to be educated on how to manage their consumption and finances as well as be given ample

support during this transition period.

xv

LIST OF ABBREVIATIONS

ATT Attitude

AVE Average Variance Extracted

BR1M Bantuan Rakyat 1 Malaysia

CBSEM Covariance-based Structural Equation Modelling

CFA Confirmatory Factor Analysis

CMB Common Method Bias

FAQ Frequently Asked Questions

GST Goods & Services Tax

ITA Income Tax Act

LA Level of Acceptance

LTK Level of Tax Knowledge

PBC Perceived Behavorial Control

PLS Partial Least Squares

PTF Perception of Tax Fairness

RMCD Royal Malaysian Customs Department

ROB Rule Observance Behavior

SE Self Efficacy

SEM Structural Equation Modelling

SN Subjective Norms

SST Sales & Services Tax

TPB Theory of Planned Behavior

xvi

UM Universiti Malaya

UKM Universiti Kebangsaan Malaysia

UPM Universiti Putra Malaysia

USM Universiti Sains Malaysia

VAT Value-Added Tax

VBSEM Variance-based Structural Equation Modelling

1

CHAPTER 1

INTRODUCTION

1.0 Introduction

This chapter presents the research framework of the study. It begins with discussing

the background of the study and the problem statement followed by research

objectives and research question. Definition of key terms of major variables will also

be included to enhance understanding of the concepts. The significance of the study

is the contribution of the scope of study to both practical and theoretical

implications. The scope of study focuses on consumers as the Goods and Services

tax being studied is a consumption tax. Manufacturers, retailers and distributors are

able to set off the tax they pay against the tax charged to their customers but

consumers are unable to claim the GST they pay on their consumption. Towards the

end, the chapter will give a brief overview of the remaining chapters in the thesis.

1.1 Background

Malaysian taxation system is divided into two; direct and indirect taxes. Indirect

taxes are controlled by the Royal Malaysian Customs Department (RMCD) and

consist of four parts; customs duties, excise duty, sales tax and service tax. Direct

taxes are administered by the Inland Revenue Board of Malaysia (IRBM). This

comprises individual income taxes, corporate taxes, petroleum income taxes, real

property gains taxes and stamp duty.

2

According to Jeyapalan Kasipillai(2005), taxation is a vital economic tool for

governments to regulate the economy, to revitalize economic growth through the

granting of fiscal incentives and to provide funds for development projects.

Attached in Appendix A is a table which provides information on the federal

government revenue obtained from the Economic Report 2013/2014 of Ministry of

Finance. According to the report, in 2013, 57.6% of the revenue was in the form of

direct taxes while 16.6% was in the form of indirect taxes.

With reference to the second table in the Appendix B, the Economic Report

2013/2014 reports an overall deficit yet again. From the table, it can be seen that

Malaysia faces deficits even from 2010. This has accentuated the desperate need for

Malaysia to develop a more efficient, effective taxation system which will be able to

provide Malaysia with a stable source of revenue.

Since the Sales and Service tax had inherent weaknesses in its system in terms of

generating stable revenue, Malaysia was forced to look into the implementation of

GST. GST is a broader consumption-based tax which is proven to be able to generate

stable revenue for the nation's financial needs. GST is levied on all goods and

services except for essential ones which are exempted from tax, or those which are at

zero-rated tax for now (Palil & Ibrahim, 2011).

Sales tax is an indirect tax levied on certain imported and locally manufactured

goods introduced in 1972. It is also known as manufacturer's tax. It is a single stage

3

tax and 10% sales tax is charged to manufacturers of locally manufactured goods

when goods are sold or for imported goods, at the time when goods are cleared at

Customs. Service tax of 6% was introduced in 1975 and is levied on taxable services

which include prescribed goods, i.e tobacco as well as professional and consultancy

services (Palil & Ibrahim, 2011). The Goods and Services Tax will replace both

these taxes at a rate of 6%. It is also categorized into standard-rated, zero-rated and

tax-exempt items. It is mandatory and involves all Malaysians nationwide as it is a

consumption based tax.

1.2 Problem Statement

Budget 2014 was a milestone budget as the Honourable Prime Minister Dato’ Seri

Najib Tun Razak announced the implementation of Goods and services tax (GST) on

the 1st of April 2015. According to The Star newspaper the Prime Minister in his

budget speech stated that the Government had to take bold measures to overcome the

weaknesses of the current sales and service tax in order to strengthen the fiscal

position of the nation. Thus, after years of detailed and comprehensive studies as

well as views of all segments of society including chambers of commerce, investors,

economists, academicians, consumer associations and NGOs, the government has

decided to implement a fair tax system that benefits all Malaysians, Goods and

Services Tax (GST). The GST was publicized at a rate of 6%, higher than what was

promised in earlier proposals (Singh 2013). However, this rate is the lowest amongst

the ASEAN countries compared with 10% in Indonesia, Vietnam, Cambodia, the

Philippines, and Laos and 7% in Singapore and Thailand.

4

Amongst the main highlights associated with the implementation of GST was that

GST will not be implemented on approximately 40 essential goods and services, the

Government will be assisting the Rakyat with the GST transition period by providing

them with one off cash allowance and a reduction of 1% in individual income tax

rates. The Prime Minister also iterated that the GST is vital in assisting the

Government to generate revenues in an effective way in order to invest in the

development of the country (Lai 2014; New Strait Times, 2014).

Despite the implementation of GST being a topic already put forth many years ago,

the acceptance level amongst Malaysians is poor as represented by the massive rally

organized by a coalition of 89 various parties on May 1 2014. The rally with the

theme “GST: Protest Till It’s Dropped’ was aimed at displaying the protest of

citizens against the implementation of GST and enforced the need of the

Government to first resolve the issue on the high personal debt level of the nation

and minimum wage as well as that the people are currently still adjusting to the hike

in petrol prices and other essential goods. (Star Online, 2014)

Moreover, a survey conducted by the Merdeka Centre in May 2014 of 1009

registered voters comprising 60% Malay, 31% Chinese and 9% Indian concluded

that 62% of Malaysians are not in favour of GST. The respondents were selected on

the basis of random stratified sampling along ethnicity, gender and state of residence

in order to obtain results which are generalizable. At the same time, 64% of the

respondents indicated that they are not aware of the working of the national

economy. To add on, 72% of those with household income less than RM1, 500 and

56% of those with household income between RM1, 501 and RM3,000 do not

5

understand GST. More than half of those who earn between RM3, 000 and RM5,

000 and 67% of those who have a household income of over RM5, 000 understand

the issue.(MerdekaCenter,2015).

Also, 45% of the respondents have indicated that GST is not a fair tax system when

in fact more than 160 countries have successfully implemented GST. According to

the poll, 62% Malays do not understand GST, while less than half of the Chinese

(41%) and Indian (35%) respondents do not understand the issue

(MerdekaCenter,2015).The results of the survey are attached in Appendix C. To

further corroborate this phenomenon, some of the riot participants who were

interviewed by the Star newspaper displayed the same lack of knowledge in the

system and high level of uncertainty in its impact to their daily lives.

Previous studies (Nordiana, 2012; Bidin & Shamsudin, 2013; Ramalingam et al.,

2014) were focused on the compliance of organizations with GST and their adoption

of the GST application systems. Previous studies have also explored the awareness

and acceptance levels of consumers (Saira et al., 2010; Palil & Ibrahim, 2011;

Shamsuddin et al., 2014; Moomal & Zakarian, 2014). However, in the nation’s

current scenario, it is vital for the government to understand the causes of the low

levels of acceptance. In line with that, this study will delve deeper into factors that

are influencing consumers’ acceptance of GST using the well-established Theory of

Planned Behavior. In order to further understand the factors influencing the

consumers’ acceptance of GST, antecedent variables to the attitude and perceived

behavorial control are examined. The antecedent variables determined were Rule

Observance Behaviour, Perception of GST Fairness, Level of GST knowledge and

6

Self-Efficacy. If these antecedent variables together with the other variables

examined in the study (attitude, subjective norm and perceived behavioral control)

proved significant, recommendations can be suggested to ensure a more efficient and

smooth implementation of GST. This is because the relevant authorities can now

identify specific areas for improvement in order to address any acceptance issues

amongst the consumers.

The focus of this study is knowledgeable consumers who are currently pursuing their

Masters in Business Administration. This is because the Merdeka Center survey had

portrayed that there was a higher level of unacceptance amongst private sector

employees, self-employed individuals and those involved in business. Moreover, the

age groups comprising of those in their twenties and thirties showed a higher level of

unacceptance (Merdeka Center, 2015). MBA students will be able to represent the

demographics of the Merdeka Center survey who are not accepting GST. MBA

students are normally within the above-mentioned age group and majority are

employed (Tay, 2001) Moreover, lack of GST acceptance has been associated with

lack of knowledge (Borneo Post Online, 2015; Jalil, 2015; GST Malaysia Info,2014)

and by choosing MBA students we will be able to put that assumption to test as

MBA students are expected to have the required basic knowledge on GST. Thus, for

this study, MBA students will represent the consumers in Malaysia.

7

1.3 Research Objectives

1) To examine the level of acceptance of Goods and Service Tax (GST)

amongst consumers.

2) To examine the relationship between the existence of rule observance

behavior and attitude of consumer.

3) To examine the relationship between perception of GST fairness and attitude

of consumer.

4) To examine the relationship between level of GST knowledge and perceived

behavioral control of consumer.

5) To examine the relationship between self-efficacy and the perceived

behavioral control of consumer.

6) To examine the relationship between attitude of consumers and their level of

acceptance of GST

7) To examine the relationship between subjective norms of consumers and

their level of acceptance of GST

8) To examine the relationship between perceived behavioral controls of

consumers and their level of acceptance of GST

1.4 Research Questions

1) What is the level of acceptance of GST amongst consumers?

2) What is the relationship between rule observance behavior and attitude of

consumer?

8

3) What is the relationship between perception of GST fairness and attitude of

consumer?

4) What is the relationship between the level of GST knowledge of consumers

and perceived behavioral control?

5) What is the relationship between self-efficacy of a consumer and perceived

behavioral control?

6) What is the relationship between attitude of consumers and their level of

acceptance of GST?

7) What is the relationship between subjective norms of consumers and their

level of acceptance of GST?

8) What is the relationship between perceived behavioral control of consumers

and their level of acceptance of GST?

1.5 Definition of Key Terms

1. Level of Acceptance refers to the level of intention to accept (Shamsuddin et al.,

2014).

2. Attitude is an individual’s positive and negative feelings about performing a

target behavior. The feelings are brought about after evaluations conducted based on

beliefs (Fishbein & Ajzen, 1975).

3. Subjective Norm is the individual’s opinion that those who are important to

him/her think that he/she should not perform the behavior in question

(Fishbein&Ajzen, 1975).

9

4. Perceived behavioral control is the perceived internal and external constraints on

behavior or intention to behave (Taylor & Todd, 1995).

5. Rule observance behavior relates to obedience to authority (Trevino, 1986).

6. Perception of fairness is the judgement of individuals that something or someone

is free of biasness and injustice (Saad, 2010).

7. Self-efficacy is an individual’s perception of his/her capability to organize and

execute courses of action required to accomplish selected types of performances

(Bandura, 1986).

8. Level of GST knowledge is an individual’s technical and general knowledge on

the subject matter of GST. (Saad, 2010)

1.6 Significance of Study

Both theoretical and practical implications of the study will be discussed.

1.6.1 Practical Implication

With the Goods and Services Tax finally being implemented, a study of this nature

would be imperative for the government in identifying areas at which they should

improve in and allocate resources to. This is very crucial especially since according

to Deputy Finance Minister Datuk Ahmad Maslan, there is RM250 million budget

10

allocation to educate the public about GST and to facilitate its implementation (Ian,

2014 ; Malaysian Insider, 2014).

This will therefore enable the Royal Malaysian Customs Department to undertake

measures for a smooth and effective transition to the GST system for consumers and

the Government as a whole. This includes enhancing their current support system

and enforcement measures (Kasipillai, 2013; Tan, 2009; Tan, 2014; Choo, 2014).

Previous studies (Saira et al., 2010; Palil & Ibrahim, 2011) have been conducted on

an exploratory mode as the GST implementation was not finalized. Other studies

Shamsuddin et al. (2014) and Moomal & Zakarian (2014) studied on the correlation

between awareness and acceptance. However, all these studies were not backed up

by a theory. Nordiana (2012), Bidin & Shamsudin (2013) and Ramalingam et al.

(2014), conducted a study on the compliance with GST and adoption of GST

application system of corporate tax collectors. Thus, this study would be the first

study to examine the factors that influence the acceptance level of consumers at large

amidst the announcement of the confirmed implementation of GST on 1 April 2015.

The key idea to understand here is that with corporate tax payers, their compliance is

harped on because under the GST implementation they are required to file in taxes to

the Royal Customs on a monthly or quarterly basis. Although they bear expenses on

preparing infrastructure and staff to ensure compliance to GST, which is usually a

one-off expenditure, it is the consumers who bear the tax burden of GST and

corresponding price hikes. The findings of this study will ultimately provide insight

11

to the Consumers’ association on the information they can disseminate to the

consumers in order to assist them to accept and adapt to the implementation of GST.

1.6.2 Theoretical Implication

Although the implementation of GST has been decided upon-1 April 2015, however,

the acceptance level of consumers is still low. As such, the only issue at hand now is

to handle the transition process as smoothly as possible.

For this to be a success, the theory of planned behavior comes in handy to explain

the various possible factors to be addressed in order to enhance the acceptance of

GST amongst consumers. Previously this theory has been used to study corporate tax

payers’ compliance to GST (Nordiana, 2012; Bidin & Shamsudin, 2013) but through

this research, the theory will be extended to understand the factors that contribute

towards the acceptance of GST by consumers. Consumers do not need to comply

with the GST but rather just accept it as the tax will already be embedded in prices of

goods and service. In this case, the study will examine the consumers’ level of

acceptance of GST by determining their intention to accept GST because at the time

of data collection GST has not been implemented yet.

Hence, this study will test the theory’s rigidity in instances where the intention to not

behave in a certain way does not enable the respondent to escape from the behavior

itself.

12

Antecedent variables are also used in this study to enhance the explanatory power of

the Theory of Planned Behavior. With these antecedent variables, the research will

be able to demonstrate very specific key areas for improvement that the government

should allocate resources to. The antecedents were Rule Observance Behavior,

Perception of GST Fairness, Self-Efficacy and Level of GST Knowledge.

1.7 Organization of the remaining chapters

This research is made up of a total of five chapters in order to present the study in a

systematic manner. The next chapter, Chapter two presents an overview of previous

literature on the variables put forth. This then leads to the development of the

theoretical framework and hypotheses for this study.

Chapter three consists of the research methodology, research design, data collection

methods and data measurement methods that will be employed for this study.

Chapter four presents the findings of this study where the goodness of the data used

is confirmed and the hypotheses developed are tested.

The final chapter, Chapter 5 will discuss the implications of the findings, practical

and theoretical applications of this study, limitations of the study, future research

suggestions and the conclusion.

13

CHAPTER 2

LITERATURE REVIEW

2.0 Introduction

This chapter aims to examine all existing literature on the content, theory and latent

variables of this study as well as the relationships being examined in relation to

Goods and Services Tax which will be implemented come 1st April 2015.This will

then lead to the formation of the theoretical framework and the development of the

hypotheses.

2.1 Malaysian Taxation

The British colonialism introduced taxes into the Federation of Malaya in 1947

which has resulted in the taxation system in Malaysia today (Singh, 1999). At first,

the Income Tax Ordinance 1947 was gazetted as the fundamental act yet this was

accordingly changed and replaced by Income Tax Act 1967 (ITA) with effect from

January 1, 1968. At that time, ITA combined the three acts of income taxation in

particular Sabah Income Ordinance 195633, Sarawak Inland Revenue Ordinance

196034 and Income Tax Ordinance 194735. As of now, ITA 1967 is the fundamental

act to administer direct taxes in Malaysia including individual and corporate income

tax (Palil, 2010).

14

The Lembaga Hasil Dalam Negeri or the Inland Revenue Board (IRB) is the tax

authority which oversees the operationalization of direct taxes in Malaysia. Other

than ITA, the IRB are also accountable for supervision, assessment, collection and

enforcement of petroleum taxes, real property gain taxes and stamp duties. The

indirect taxation system is controlled by the Royal Malaysian Customs (RMC). This

includes customs duties, excise duty, sales tax and service tax (Palil, 2010).

2.2 Consumers

In previous research, (Nordiana, 2012; Bidin & Shamsudin, 2013; Ramalingam et

al., 2014) their scope of study was on industrial taxpayers such as manufacturers,

retailers and distributors. The focus was on businesses that were registered under

GST compliance. In this study, the scope of study is on consumers, individuals who

consume goods with taxes already embedded in the pricing. Thus, the matter of non-

compliance or evasion does not exist in this context. In this study, MBA students

will be representing the consumers as majority of them are within the age group and

employment status highlighted in the Merdeka Center Survey of those who had a

higher percentage of not accepting GST.

An in-depth discussion of GST in the following component will highlight the very

fact that although GST will be charged at different stages, in the end the burden will

be on the consumer (Voon, 2013). The implementation of GST will have quite a

significant impact on consumers especially since according to the Report on

Household Expenditure by the Department of Statistics Malaysia, average monthly

expenditure per household has increased from RM 1,161 in 2004 up to RM 2,190 in

15

2010. Even without GST implemented, consumers are facing an increase in

expenditure by 89% over 6 years. Thus, it is vital to study the perceptions and

acceptance of GST by these Malaysian consumers and the factors that are

influencing their perceptions.

Moreover, according to Bank Negara, Personal/Household Debt is standing at an

alarming rate of 83% of Gross Domestic Product of the nation compared to a 70% in

2009 and the debt to household income ratio is standing at an alarming 140%

(Joseph, 2013). Additional statistics creates more concern over this implementation

of GST. The increase in GDP of 5.1% in 2012 is less than half of the growth of

household debt of 12% in 2012, indicating severe unsustainability (Joseph, 2013).

Consumers are already high in debt pre-GST and it is worrying to imagine the

impact on consumers’ post-GST, where prices of goods and services are expected to

increase.

Hence, with the undertaking of this study, the reasons for knowledgeable consumers

accepting or not accepting GST can be determined and consequently influence the

channeling of resources towards customizing assistance and support for the

consumers in the most effective way.

16

2.3 GST

Goods and Services Tax or GST is a tax on consumption based on a value-added

concept. In a nutshell, the more you consume the more tax you pay. Unlike the

present sales tax or service tax which is a single stage tax, GST is a multi-stage tax.

The tax is not a cost to the intermediaries since they are able to claim back GST

incurred in their business operations. GST is imposed on goods and services at every

stage in the supply chain including situations in which the good or service is

imported. It is not a new tax but instead is a tax to replace the current Sales Tax and

Service Tax (SST). GST is also known as VAT, Value-Added Tax in certain

countries (RMCD, 2013)

2.3.1 Reasons for implementing GST

The key reason for many countries adopting GST/VAT is the inefficiency of the

current tax system in financially supporting the development of the nation’s

economy. The same scenario occurred here in Malaysia and the Ministry of Finance

has studied and confirmed that the implementation of GST can overcome the various

weaknesses under the current Sales & Service Tax system. These weaknesses

include tax compounding and cascading, transfer pricing and reliefs on certain goods

(RMCD, 2013).

17

Figure 2.1: Cascading effect -Sales & Service tax (RMCD, 2013)

Figure 2.2: Cascading effect - Service tax (RMCD, 2013)

In 1990, direct taxes contributed to 35.2% of the nation’s revenue whilst indirect

taxes contribute to 36.7%. The contributions of both categories of taxes were equal

but trade liberalization policies were amended causing major inequality in the

contribution of direct and indirect taxes. This was clearly depicted in 2012 when the

contribution from direct tax was 56.4% and indirect tax 17.2%. At this point of time,

Malaysia relies profoundly on direct taxes and petroleum revenues, a situation which

economic experts do not recommend. According to these experts, over-dependence

on only certain taxes will have an adverse effect on the nation’s financial position.

Hence, to eliminate these adverse effects this is an appropriate time for the

Government to engage in an overall tax reform and implement GST. (RMCD, 2013)

18

2.3.2 Significance of GST

GST was introduced by the government in the 2005 budget but postponed to a later

date. Following that, the GST Bill was tabled for the First Reading in the Dewan

Rakyat in December 2009 but in 2010 the implementation was postponed again.

However, the implementation of GST is inevitable to support the nation’s long term

economic growth and the pressure was on the government to ensure a smooth

transition to GST. In order to do this, the Government has to take into account the

welfare and concerns of the society as a whole so that it is well-received (RMCD,

2013).

With this in mind, the Government had undertaken social impact studies of the

implementation of GST. To ease the tax burden on the consumers, certain goods and

services which are indispensable to the low and middle income group have been

proposed not to be subjected to GST. To add on, basic items such as poultry, rice,

flour, meat, vegetable, sugar, flour, cooking oil, residential and agricultural

properties, health services and education will not be subjected to GST (RMCD,

2013).

GST is a more transparent, competent, effective and less bureaucratic taxation

system. The double taxation phenomenon under the Sales & Services Tax regime is

eliminated with GST in place. From a business point of view, they are able to reduce

costs as they now can claim back the GST incurred which was not possible under the

SST regime. A company which back then had to absorb the sales and service taxes

19

2.3.3 Mechanism of GST

The mechanism of GST can be examined from the consumers’ and businesses’ point

of view.

(a) Business

GST is charged on the supply of goods and services made in Malaysia and on the

imports of goods and services into Malaysia. GST is charged on the selling price of

the goods or services and only the GST amount will be forwarded to the

Government. The GST value is representative of the value added to the goods or

services at each level of the supply chain. The value added is the value added to a

raw material or purchases before selling the new or improved product or service. To

operationalize this, GST adopts a credit offset mechanism whereby GST charged

on the output of the business is offset against the GST paid on the goods or services

acquired as inputs by the business. Along these lines, a company will be charged

GST by its suppliers and simultaneously, the company will charge GST to its

paid can now claim the GST paid from the Customs. The net effect is definitely a

reduction in costs for these companies (RMCD, 2013).

Exportation of goods and services are not subjected to GST which will in return

ensure Malaysian exports are competitive in the global market. Consequently, this

will improve the Gross Domestic Product of the nation (News Strait Times, 2015)

With GST in place, shadow economy activities such as illegal trading, black money

and tax evasion can be curbed. (Schneider & Frey, 2000 ; MalayMail Online, 2015)

20

customers. GST charged on output is called output tax and GST incurred on

purchase is called input tax. This offsetting mechanism is to guarantee GST paid by

businesses are recoverable leading to a reduction is cost. Most importantly, this

ensures there’s no double taxation and the net tax effect on the end consumer is only

6%. (RMCD, 2013)

Diagram 2.3: Input and output tax (RMCD, 2013)

(b) Consumers

GST-registered businesses will collect GST from consumers on the goods and

services purchased. There are three types of supplies listed under GST which

are(Examples are derived from Royal Malaysian Customs Guide on Supply

under GST):

(i) Standard rated supplies are taxable supplies of goods and services which are

subject to a positive rate of 6%. Examples of these supplies are sales of

commercial properties, vehicles, accessories and packaged food items.

(ii) Zero rated supplies are taxable supplies which are subject to a zero rate.

21

Examples of zero-rated supply are fresh vegetables, live animals, books and

exports of goods and services. Businesses dealing with zero-rated supplies are

still able to claim the input taxes incurred.

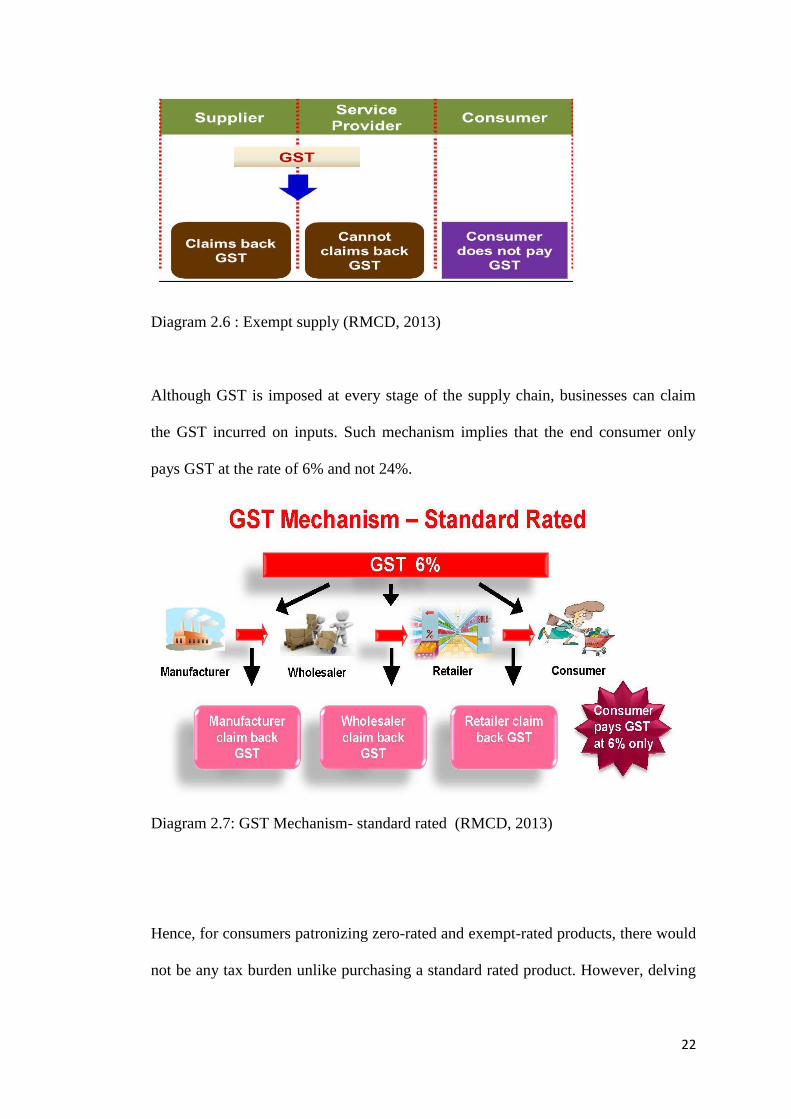

(iii) Exempt supplies are non-taxable supplies which are not subject to GST.

However, the GST paid on input by the businesses cannot be claimed as tax

credit. Examples of exempt supply of services are domestic transportation of

passengers for mass public transports, private education and private health

services. Examples of exempt supplies of goods are residential properties, land

for agricultural and land for general use.

Below is an illustration showing how GST works:

Diagram 2.4: Standard rated supply (RMCD, 2013)

Diagram 2.5: Zero-rated supply (RMCD, 2013)

22

Diagram 2.6 : Exempt supply (RMCD, 2013)

Although GST is imposed at every stage of the supply chain, businesses can claim

the GST incurred on inputs. Such mechanism implies that the end consumer only

pays GST at the rate of 6% and not 24%.

Diagram 2.7: GST Mechanism- standard rated (RMCD, 2013)

Hence, for consumers patronizing zero-rated and exempt-rated products, there would

not be any tax burden unlike purchasing a standard rated product. However, delving

23

deeper, the consumer should understand that producers of exempt rated goods and

services cannot claim back their incurred input GST and will have no choice but to

channel the cost to the consumers by increasing prices. For example, a private

education institute will have to pay their suppliers GST for purchases of

infrastructure and maintenance services but will not be able to claim this GST

expense from the customs as their service is considered an exempt rated service.

However, the institute is now incurring higher costs than pre-GST implementation

and will have to increase their selling prices as well to cover the costs incurred.

An equally important point to understand is that GST, if well-implemented

should not result in increase of prices of all standard-rated products and

services. With the discussions below, an understanding can be obtained on the

three main implications of standard-rated GST on consumers.

Scenario 1:

10% SALES TAX abolished, 6% GST implemented

The sales tax of 10% is a business to business transaction and this tax burden is

usually embedded in the final pricing to end consumers. With the

implementation of GST, consumers should end up paying less because a

product manufactured or imported now is subject to 6% GST rather than 10%

Sales Tax.

24

Scenario 2:

6% SERVICE TAX abolished, 6% GST implemented

While most consumers don’t experience the direct effect of the 10% Sales Tax,

most of them would have paid for the 6% Service Tax. In the scenario of

consumers engaging in service for which they were previously charged 6%, the

implementation of GST will not impose any price increase on items.

Consumers will be paying the same.

Scenario 3:

No Service or Sales Tax previously, GST 6% implemented

As GST is a broad-based taxation system, more sectors of the economy are

covered as compared to under the SST regime such as the paper and printing

industry, food preparation industry, medical and educational equipment

industry as well as repackaging industry. (Customs Guide Book,2003) Unless

the goods or services are zero-rated, prices of goods not previously covered

under SST will now be affected. Consumers will have to pay a higher price.

2.3.4 GST rates in the ASEAN countries

The GST rate of 6% suggested is the lowest in comparison to our neighboring

countries. Although Singapore initially introduced GST at 3% but the current GST

rate is 7%.

25

The following are the GST rates among the ASEAN countries:

Figure 2.8: GST rates in the ASEAN countries (RMCD, 2013)

2.3.5 Implementation of GST

Budget 2014 has announced the confirmed implementation of GST on 1st April

2015. Many steps are undertaken to ensure the smooth implementation of GST.

Currently the Ministry of Finance is conducting a series of awareness program on

GST to the public and businesses. The aim of this awareness program is to help the

public and business to have a better understanding on the proposed GST model in

Malaysia, the mechanism and steps taken by the Government to overcome issues

raised concerning GST. (RMCD, 2013)

The people need to know that GST is charged and collected on all taxable goods and

services produced in the country including imports. Only businesses registered under

GST can charge and collect GST. GST collected on output must be remitted to the

26

Government. However, businesses are allowed to claim the input tax credit.

From the nation’s point of view, Minister in the Prime Minister's Department, Datuk

Seri Idris Jala stated that GST implementation is projected to result in additional

revenue of RM20 billion to RM27 billion, at maturity. At maturity refers to the point

in time when every Malaysian starts to contribute towards the GST. The additional

revenue thus can be used to enhance the well-being of Malaysians as a whole

(Xavier, 2013).

2.4 Theory

A theory in essence is a tested general proposal, universally regarded as correct,

that can be used as a principle of explanation and prediction for a scenario (Oxford

Dictionary, 2015). This study employs the Theory of Planned Behavior to determine

the consumers’ acceptance behavior of GST. The theory is used to support the

framework of this study. Antecedent variables are added in to enable better

explanation of the components of TPB. Detailed discussion will be done in following

sections.

2.4.1 Theory of Planned Behavior (TPB)

Through his article "From intentions to actions: A theory of planned behavior", Icek

Ajzen put forth the Theory of Planned Behavior in 1985. This theory was expanded

from the theory of reasoned action proposed by Martin Fishbein together with Icek

Ajzen in 1975. (Azjen 1991) The theory of reasoned action portrays behavioral

27

intention as antecedent to actual behavior. Behavioral Intention is determined by two

independent variables; attitude and subjective norms.

In the Theory of planned behavior, to take into account conditions of variable

control, an additional construct was included- Perceived Behavioral Control. This

particular component reflects the respondent’s perception of how much control they

have over the behavior. (Taylor & Todd, 1995) Therefore, according to TPB,

intention to behave in a certain way is determined by the attitude towards the

behavior, subjective norms and perceived behavioral control. The TPB is highly

valuable due to the fact that it can be used in numerous applications and has a more

powerful predictive framework compared to TRA (Ajzen, 1991)

Predicting behavior is the ultimate objective of TPB thus it does not explain the

behavior (Conner & Sparks, 2005). The TPB model is not restricted to predicting

behaviors in information systems (Davis et al., 1989) and other human behaviors

(Paris &Broucke, 2008; Guo et al., 2007; and Chang, 1998), but is also useful in

explaining tax compliance behavior (Saad, 2010; Palil & Ibrahim 2011). Research on

tax compliance has tried to prove this theory in a number of countries. Trivedi &

Shehata (2005) proved the Theory of Planned Behavior in Canada, Bobek and

Hatfield (2003) proved it in the USA, Damayanti (2012) proved it in Indonesia and

this study aims at proving the applicability of this theory in the context of Malaysian

Goods and Services Tax.

28

2.5 Dependent Variable

In this study, level of acceptance of Goods & Services Tax has been identified as the

dependent variable of the study. Level of acceptance of GST is measured by the

individual’s intention to accept GST. Intention is defined as being mentally

determined to accept GST (Hung, Chang & Yu, 2005). Level of acceptance is simply

the level of agreement of the individual with the implementation of GST. The TPB

advocates that the intention to behave in a certain manner is highly influenced by the

attitude towards the behavior in question, whether or not those who are influential to

the respondents have the behavioral intention-subjective norm and perceived

behavioral control- the ease or difficulty of performing the behavior caused by

internal and external constraints (Ajzen, 1991; Sommer, 2011).

The type of behavior impacts the degree of intention-behavior uniformity. Findings

confirmed that intentions are significant predictors of an action. The intention to

behave in a certain way is a sufficient proxy measure of behavior. Previous studies

have concurred that intention to comply with tax obligations explains an individual’s

decision to comply with tax obligations (Bidin & Shamsudin 2013; Saad, 2010;

Trivedi et al.,2005; Palil & Ibrahim,2011). Cheng, Lam & Yeung (2006) also argued

that for a survey-based research design, measurement of behavioral intention is more

appropriate than actual behavior.

29

2.6 Antecedent and Independent variables

Independent variables of this study consist of attitude, subjective norm and perceived

behavioral control. Antecedent variables consist of rule observance behavior,

perception of GST fairness, level of GST knowledge and self-efficacy.

2.6.1 Attitude

Attitude is an individual’s assessment of performing a behavior. The evaluation can

be either positive or negative (Fishbein & Ajzen, 1975). Attitude towards behavior is

defined as a function of an individual’s beliefs towards a behavior and a subjective

evaluation of that behavior (Fishbein & Ajzen, 1975). The belief component captures

a person’s perceptions about a certain behaviour. Many studies confirmed the

correlation between attitudes and behavioral intention. (Wan et al., 2012) It is highly

related to behavioral intention because individuals form intentions to perform

behaviors towards which they have positive feelings. Ajzen (1991) specifies that

attitudes towards compliance reflect feelings of favour and disfavour towards

behavior, in this case level of acceptance of GST.

Any attitude is a hypothetical or latent variable rather than an immediately

observable variable. It is, in other words, an abstraction. The concept of attitude does

not refer to any one specific act or response of an individual, but it is an abstraction

from a large number of related acts or responses. When we state that a certain

individual, A, has a less favorable attitude towards GST than another individual, B,

30

we mean that A's words and actions are consistently less favorable to GST than B's

words and deeds (Jones, 1970).

There are a number of functional approaches to attitude and the approach applicable

to this study would be the adjustive function. This function of attitude has relevance

in the realm of behavioral theory. It follows from the nature of the adjustive function

of attitudes that the clarity, consistency and nearness of rewards and punishments are

important factors in the acquiring of new attitudes. In this case, the possible rewards

and benefits from GST could be an important factor in consumers acquiring a

positive attitude towards GST (Jones, 1970)

Social psychologists agree that an attitude involves at least three things

(Culbertson,1986):

1. An attitude object which may be physical or an abstraction. In this context, it

is the GST.

2. A set of beliefs that the object is either good or bad. Hence in this case it

would be the belief of whether GST is good or bad.

3. A tendency to behave towards the object so as to keep or eliminate it. This

refers to the acceptance of GST.

Using belief-based attitudes measurements in a taxation context will result in

attitudes explaining compliance behavior (Bobek, 1997). Thus, it is anticipated in

this study that a positive attitude towards the GST tax system would encourage

31

consumers to be accepting of it. In this study, we have considered two antecedents to

attitude, namely Rule Observance Behaviour and Fairness Perception.

Attitude is operationalized in previous studies (Loo et al.,2007 & Bobek 1997) by

determining the individual’s positive or negative feeling towards the behavioral

intention. The same concept is applied here to determine the beliefs and perspectives

that these consumers have on GST.

2.6.2 Rule Observance Behavior

Rule Observance Behaviour is an act or instance of following a rule. Trevino (1986)

discussed a model of ethical decision making wherein situational and individual

moderators interact with an individual’s cognitions to determine ethical or unethical

behavior.

One situational moderator included in the framework is “obedience to authority”.

Obedience is a form of social influence where an individual acts in response to a

direct order from another individual, who is usually an authority figure. (McLeod,

2007) Rule Observance Behavior is studied as an antecedent to attitude in this study.

Previous study (Sarina et al., 2007) measured the obedience of auditors to authority

and rules whilst another previous study (Jeffrey &Weatherholt, 1996) measured the

rule observance behavior amongst corporate accountants. This study will undertake

32

the same operationalization of this variable as it is a straightforward and simple

variable.

2.6.3 Perception of fairness of GST

The term fairness relates to the justification and validity a consumer assigns to

the burden of the GST. The term perception of fairness is used here because each

individual has a different perspective of the fairness of the taxation system which

does not conclude on the ultimate fairness of the system (Jones, 2009).

Previous studies indicate that fairness perceptions can take various forms. The first

dimension that can be looked at is the vertical fairness, which stresses that different

tax rates should be enforced for taxpayers with different economic situations (Erich

et al., 2006). This would result in higher income earners paying tax at higher rates

than low-income earners. The next dimension is horizontal fairness, defined as ‘the

equal treatment of equally circumstanced individuals’ (Michael, 1978). In this

horizontal fairness dimension, taxpayers of similar economic positions should pay

the same amount of tax. Horizontal and vertical fairness are derived from the

Distributive Justice Theory (DJT) which argues that individuals in similar

circumstances must be treated in an equivalent manner without compromising their

individual needs.

Besides vertical and horizontal fairness, a study on the US tax system brought forth

the concept of procedural fairness and policy fairness (Bobek, 1997). Procedural

33

fairness relates to the procedure engaged to reach distribution outcomes while policy

fairness deals with the content of the tax law. Moving on, exchange fairness is a very

significant dimension (Gilligan & Richardson, 2005; Gerbing, 1988), which

represents the exchange of contribution and benefit between taxpayers and

government. In simple terms, the exchange fairness dimension highlights that

taxpayers will have fair perceptions of the tax system if the benefits received from

the government are justifiable compared to their tax contributions. Other dimensions

of fairness include a preference for either progressive or proportional taxation

(Turman, 1995), personal fairness, tax rate fairness, special provisions and general

fairness (Gilligan & Richardson, 2005; Richardson, 2005a; Christensen &

Weichrich, 1996; Christensen et al., 1994; Gerbing, 1988). The above review on

studies of tax fairness suggests approximately ten dimensions of fairness.

However, in this study, only two dimensions are identified to be important in

assessing the fairness of the GST system; general fairness, exchange fairness (Saad,

2010) General fairness simply measures individuals’ judgments whether the GST tax

system is generally fair or not while exchange fairness is concerned with a mutual

exchange between taxpayers and the government. The rest of the dimensions would

not be applicable as GST is a tax on consumption and not income. Perception of

fairness of GST is studied as an antecedent to attitude.

In general, equity theory is engaged when studying tax fairness. Equity

theory explains relational satisfaction in terms of fairness perceptions of distributions

of resources within interpersonal relationships (Jones, 2009).

34

2.6.4 Subjective Norm

Subjective norm reflects the level of influence significant referents have on

individuals. In this case, the influence would be in reference to accept or not accept

the implementation of GST. Ajzen (1991) describes subjective norm as ‘the

perceived social pressure to perform or not to perform the behaviour’ or ‘an

individual’s perception that important others would approve or disapprove of his or

her performing a behaviour’ Subjective norm addresses the individual’s belief that

others in their support network want them to support or oppose GST, and their

motivation to comply with the views of those persons. This is simply known as the

social influence component of decision making.

According to the theory of planned behavior, the support of significant others will

influence consumer’s acceptance of GST. The opinions of peers are critical in

shaping the views of individuals due to the necessity for interpersonal support during

a time of change (Gerpott, 1990) and the effects of information processing on

socialization (Salancik and Pfeffer, 1978) In this context, subjective norms in

intention to accept GST refer to how other consumers feel about the subject matter.

As subjective norm is related to significant referents, peers and family members are

taken up as the influential referents (Damayanti, 2012).

No antecedents were identified for the subjective norm as influences from peers and

family members would have the same impact and thus would not provide additional

insight. The same measurements used in Bhattacherjee (2000) were used for this

35

study as the two main areas of peers and family members have to be covered in order

to have a valid measurement.

2.6.5 Perceived behavioral control (PBC)

PBC is the latest and unique construct of the TPB and can be linked to behavior both

directly and indirectly through intentions. The direct impact is the actual control an

individual has over behavioral performance whilst indirect impact refers to the

motivational influence of control on behavior. In this case study, we are looking at

the indirect link of perceived behavioral control and behavior through the intention

to behave.

Perceived behavioural control reflects an individual’s perception on the ease or

difficulty in performing a particular behaviour. In a more detailed explanation, PBC

refers to an individual perception of accessibility of resources or opportunity

necessary for performing the behavior (Ajzen, 1985; Ajzen & Madden, 1986) Ajzen

(1991) stipulates that high perceived behavioural control results in a behaviour being

easy to perform, while one that is difficult to perform is low in perceived behavioural

control.

There are internal and external perceived behavioral controls. The internal factors

refer to individual’s disposition which includes the amount of information a person

has. The external factors determine the extent to which circumstances support or

inhibit the performance of behavior (Ajzen, 2001) PBC has to be customized to the

36

type of behavioral issues under study (Sparks et al., 1997). Perceived behavioral

control is the perception of the resources, knowledge and ability to perform the

behavior (Giantari, 2013). In this case, the two antecedents to PBC are level of tax

knowledge and self-efficacy. Both are internal perceived behavioral controls.

Previous studies (Sarina et al., 2007; Nordiana 2012) operationalized this variable by

examining the perceived internal and external constraints on behavior or intention to

behave. The same measurement is undertaken here in order to measure the

constraints or resources that individuals face or have in accepting GST.

2.6.6 Level of GST Knowledge

A voluntary tax compliance system is effectively functional only with tax knowledge

(Kasipillai, 2000). The tendency to not comply with tax whether intentionally or

unintentionally increases with the lack of knowledge. This was proposed by

McKerchar (1995) who studied small business taxpayers. She concluded that

taxpayers were not even aware of their tax knowledge deficit and this might lead to

unintentional non-compliance behavior.

An earlier study by Harris (1989) separated tax knowledge into fiscal awareness and

technical knowledge. Saad (2010) has divided tax knowledge into four categories but

only two are applicable here as we are not discussing compliance bur rather just

acceptance. The two are general knowledge and technical knowledge. Previous

37

studies have evidenced that general tax knowledge has a very close relationship with

taxpayers’ ability to understand and appreciate the laws and regulations of taxation.

(Singh, 2003). This can also be translated for the purpose of this case study, to the

fact that with the general and technical knowledge on GST, consumers will be able

to manage their consumption better in order to minimize the impact of the GST on

their expenses especially since many essentials are tax-exempt and zero-rated. Level

of tax knowledge is taken as an antecedent to perceived behavorial control in this

study.

This variable is measured both in a technical and practical way in this study and it is

customized to GST issues.

2.6.7 Self-Efficacy

Self-efficacy is associated with effective behavioral strategies and this has led to this

concept being studied as an influence to improved performance in various situations.

(Ben-Ami et al., 2014) Self-efficacy theory postulates that individuals judge their

ability to cope effectively with challenges when faced with environmental demands.

Based on this judgment, individuals initiate behavioral strategies to manage

challenges efficiently and attain desired outcomes (Bandura, 1997). Self-efficacy is

the confidence an individual has of his/her competence to perform specified tasks

(Bandura, 1997). It is a well-researched concept originating from the Social

Cognitive Theory (Bandura, 1986). Self-efficacy is comparable to self-confidence

however self-efficacy is more situational in nature. Self –confidence is more task-

38

specific whilst self-efficacy is a dynamic paradigm that changes over time depending

on new information and experiences (Schmidt & Karsten, 2015).

Previous studies (Schmidt &Karsten, 2015; Kraft et al.,2005; Kulviwat et al., 2014;

Ben-Ami et al., 2014;) had investigated this concept of self-efficacy in various

situations and have concluded that it is indeed a significant factor in those situations.

Thus, in this study, self-efficacy is in relation to the consumers’ judgement on how

well they will be able to cope with their lifestyles even with the implementation of

GST. This might include their perception of the costs and benefits involved as they

will have to set behavioral strategies. (Raghuram, 2003; Beauregard,2012) Self-

efficacy is studied as an antecedent to perceived behavioral control.

Self-efficacy was measured by previous research by enabling respondents to judge

their own capabilities to organize and execute their intention. (Kulviwat, 2014; Ben-

Ami, 2014) In this study, hence, this variable is measured by the individual’s

judgement of their ability to manage their lifestyles and finances with GST in place.

39

2.7 Theoretical Framework

In order to have a scientific and systematic research of this subject matter, a

theoretical framework has been formed. The theoretical framework is developed

using the Theory of Planned Behavior model as the underlying foundation. The

dependent variable of the framework is Level of Acceptance of GST. The

independent variables are based on the components of Theory of Planned Behavior

which are Attitude, Subjective Norms and Perceived Behavioral Control. Following

that, antecedent variables are determined and included to enhance the value of the

research. Antecedent variables are included only for Attitude and Perceived

Behavioral Control. The antecedent variables for attitude are Rule Observance

Behavior and Perception of GST Fairness whilst the antecedent variables to

perceived behavioral control are Level of GST knowledge and Self-efficacy.

40

Figure 2.9 Theoretical Framework

41

2.8 Factors Affecting Level of Acceptance of GST

Reading the literature, there are 3 main streams of literature that can be used for the

basis of this study. There are studies examining factors affecting compliance of GST,

factors affecting level of tax compliance and factors affecting level of acceptance of

products or systems, other than tax or GST. There are also a few other studies which

use the latent variables in this study in a different context. These studies have also

been used to support the hypotheses development involving the antecedent variables

and independent variables.

42

Table 2.1: Key Studies on Malaysian Goods and Services Tax

Author/Year Title Location Theory IV DV Methodology Findings

ZainolBidin and

FaridahwatiMohdSha

msudin/

2013

Using Theory of

Reasoned

Action to

Explain

Taxpayer

Intention to

Comply with

Goods and

Services Tax

(GST)

Malaysia Theory of

Reasoned

Action

1) Attitudes

2) Subjective

Norms

Compliance

with GST

Structured

questionnaires

that were

distributed to a

sample of 103

taxpayers

(corporates) with

the assistance of

the Department of

Royal Malaysian

Custom

Department in

Kedah and Perlis.

1) Subjective norms

and attitude

influenced the

manufacturers’

intention to

comply with

GST.

2) Subjective norm

was found to be

the strongest

factor for

successful GST

implementation

3) R square = 28%

NordianabintiRamli/

2012

The Perception

of Taxpayers

toward Goods

and Services

Tax (GST)

Implementation

Malaysia Theory of

Planned

behaviour

1) Attitude

2) Subjective

norm

3) Perceived

Behavioural

Control

4) Law &

enforcement

Intention to

comply with

GST

Structured

questionnaires

that were

distributed to a

sample of 150

with the

assistance of the

Department of

Royal Malaysian

Custom

Department in

Kedah and Perlis.

1) Subjective norms

and law &

enforcement

influence

intention.

2) Subjective Norm

is the strongest

factor.

3) R square = 28%

Mohd Rizal Palil and

MohdAdha Ibrahim /

2011

The Impacts Of

Goods And

Services Tax

(GST) On

Middle Income

Malaysia Theory of

Planned

behaviour

1) Demographics

2) Respondents’

readiness,

acceptance

Intention to

comply with

GST

Data was

collected through

a structured

survey among

middle income

1) This study

suggested that

many

respondents were

worried on their

43

Author/Year Title Location Theory IV DV Methodology Findings

Earners In

Malaysia

andperceptions.

3) Respondents’

behaviour

toward the

implementation

of GST

earners (RM

2000- RM 4000)

from various

organizations

including

government and

private sectors

from various

locations in Kuala

Lumpur,

Malaysia.

purchasing

power

particularly

among the

middle income

earners.

2) The study

provides the

government with

a number of

measures to be

undertaken for a

smooth process.

44

2.8.1. Studies on Goods & Services Tax

Table 2.1 shows the studies that have been conducted on GST which were referred to

in the hypothesis development of this study. As can be seen the studies conducted

are focusing on corporate tax payers who need to comply with the collection of GST

for the government. The Theory of Planned behavior is used in those studies and

hence can contribute significantly to the hypothesizing of latent variables’

relationships in this study.

2.8.2 Studies on Tax compliance

Studies on tax compliance have used Theory of Planned Behavior in the Western

context (Jones, 2009; Bobek & Hatfield, 2003) and Asian context (Damayanti, 2012;

Saad, 2010). Previous studies (Harris, 1989; Hanno &Violette, 1996; Bobek, 1997;

Tan & Chin Fatt, 2000; Richardson & Sawyer, 2001; Seidl & Traub, 2001; Loo et

al., 2007; Hai & See, 2011; Thomas, 2012; Devos, 2014; Boonyarat, 2014; Schmidt

& Karsten, 2015) all have dwelled in the various factors that affect tax compliance