european journal of economics and business studies

300

EJES EUROPEAN JOURNAL OF ECONOMICS AND BUSINESS STUDIES January-April 2018 Volume 4, Issue 1 ISSN 2411-9571 (Print) ISSN 2411-4073 (online)

-

Upload

khangminh22 -

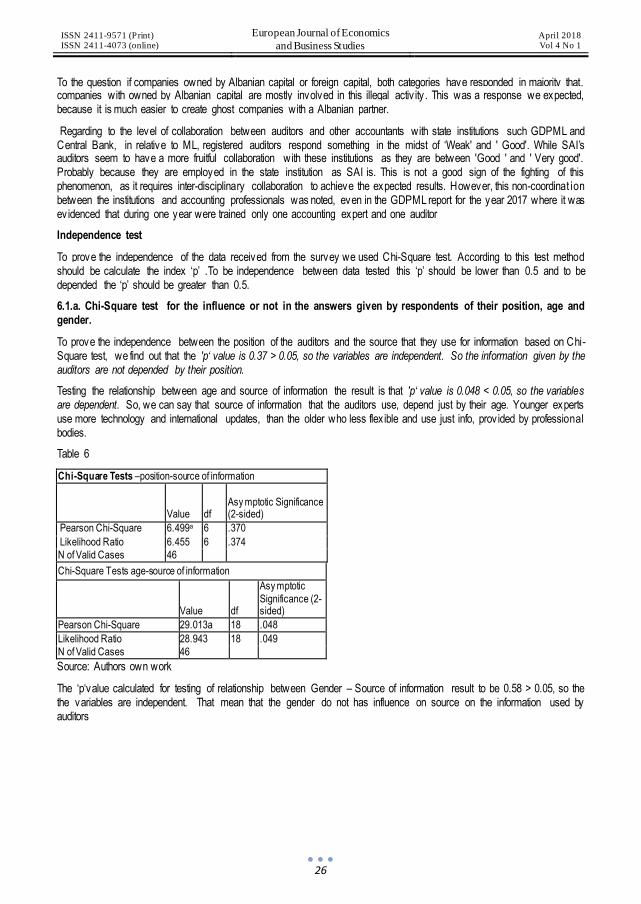

Category

Documents

-

view

0 -

download

0

Transcript of european journal of economics and business studies

EJES

EUROPEAN JOURNAL OF ECONOMICS

AND BUSINESS STUDIES

January-April 2018

Volume 4, Issue 1

ISSN 2411-9571 (Print)

ISSN 2411-4073 (online)

REVISTIA

PUBLISHING AND RESEARCH

EUROPEAN JOURNAL OF ECONOMICS

AND BUSINESS STUDIES

January-April 2018

Volume 4, Issue 1

Every reasonable effort has been made to ensure that the material in this book is true, correct, complete, and appropriate at the time of writing. Nevertheless, the publishers,

the editors and the authors do not accept responsibility for any omission or error, or for any injury, damage, loss, or financial consequences arising from the use of the book. The

views expressed by contributors do not necessarily reflect those of Revistia.

Typeset by Revistia

Copyright © Revistia. All rights reserved. No part of this book may be reproduced in any form or by any electronic or mechanical means, including information storage and

retrieval systems, without written permission from the publisher or author, except in the case of a reviewer, who may quote brief passages embodied in critical articles or in a

review.

Address: 11, Portland Road, London, SE25 4UF, United Kingdom

Tel: +44 2080680407

E-Mail: office@revistia. com

Web: https://ejes.revistia.com

ISSN 2411-9571 (Print)

ISSN 2411-4073 (online)

Indexed in Elsevier’s Mendeley, WorldCat, RePEc & Ideas, Google Scholar, Crossref

Editorial & International Scientific Advisory Board

Ahmet Ecirli, PhD - Institute of Sociology, Bucharest, Romania

Nicos Rodosthenous, PhD - Aristotle University of Thessaloniki, Greece

Irene Salmaso, PhD - University of Florence, Italy

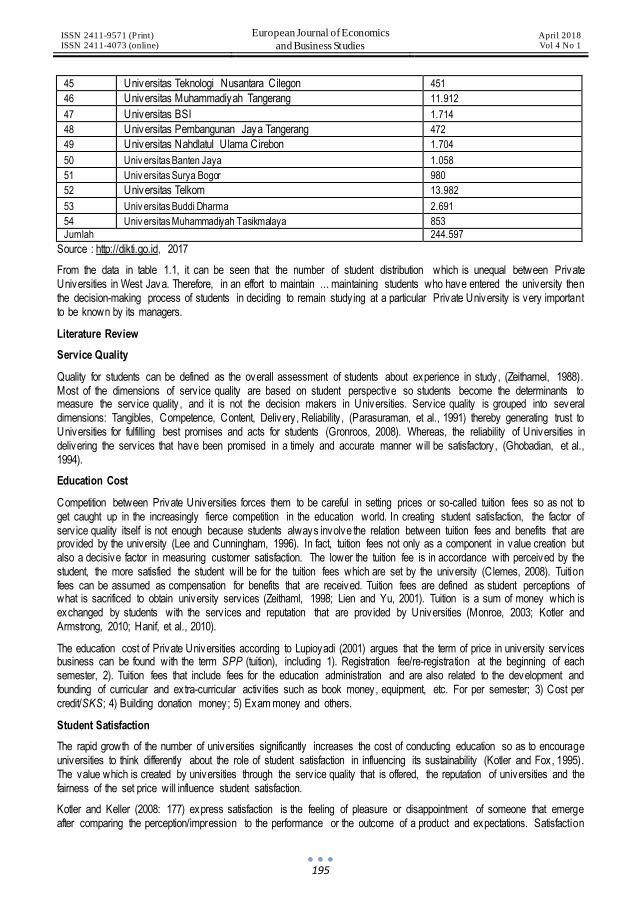

Nino Orjonikidze, PhD - Gori State Teaching University, Georgia

Javier Cachón Zagalaz, PhD - Universidad de Jaén, Spain

Gonca Atıcı, PhD - Istanbul University, School of Business, Turkey

Enkhtuya Dandar - University of Science and Technology, Mongolia

Basira Azizaliyeva, PhD - National Academy of Sciences, Azerbaijan

Natalia Kharadze, PhD - Ivane Javakhishvili Tbilisi State University, Georgia

Federica Roccisano, PhD -

Tatiana Pischina, PhD - Academy of Economic Studies, Moldova

Irina Golitsyna, PhD - Kazan (Volga) Federal University, Russia

Ekaterine Gulua, PhD - Ivane Javakhishvili Tbilisi State University, Georgia

Mariam Gersamia, PhD - Ivane Javakhishvili Tbilisi State University, Georgia

Jean d'Amour - Åbo Akademi University, Finland

Ornela Bilali, PhD - “Aleksander Xhuvani” University, Albania

Niyazi Berk, PhD - Bahcesehir University, Istanbul, Turkey

Jesus Francisco Gutierrez Ocampo, PhD - Tecnologico Nacional de Mexico

Chandrasekaran Nagarajan, PhD - IFMR Graduate School of Business, India

Carmen Cecilia Espinoza Melo, PhD - Universidad Católica de la Santísima Concepción in Chile

Fouzi Abderzag, PhD

Valentinas Navickas, PhD - Kaunas University of Technology, Lithuania

Elenita Velikova, PhD - University of National and World Economy, Bulgaria

Agnieszka Huterska, PhD - Nicolaus Copernicus University in Toruń

Ewa Badzińska, PhD - Poznan University of Technology, Poland

Khaled Salah, PhD - Faculty of Education - Alexandria University, Egypt

Maria João Mimoso, PhD - Portucalense University Oporto, Portugal

Nastaran Norouzi Richards-Carpenter, PhD - Richmond Business School, London, UK

Sajitha Lakmali Hewapathirana, PhD - University of Colombo, Sri Lanka

Habib Kocak, PhD - Marmara University, Turkey

Amel Alić, PhD - University of Zenica, Bosnia and Herzegovina

Eugenia Strano - University Magna Graecia of Catanzaro, Italy

Asta Savaneviciene, PhD - Kaunas University of Technology, Lithuania

Nino Liparteliani, PhD - Gori State Teaching University, Georgia

Jadvyga Ciburiene, PhD - Kaunas University of Technology, Lithuania

Mirela Ujkani Miti, PhD - University of Tirana Albania

Vania Ivanova, PhD - University of National and World Economy, Bulgaria

Wawan Lulus Setiawan - Institute of Cooperative Management, Indonesia

Wan Kamal Mujani, PhD - The National Universiti of Malaysia

Maria Irma Botero Ospina, PhD - Universidad Militar Nueva Granada, Colombia

Mohd Aderi Che Noh, PhD - National University of Malaysia

Francisco Javier Blanco-Encomienda, PhD - University of Granada, Spain

Driss Harizi, PhD - Hassan University of Settat, Morocco

Maleerat Ka-Kan-Dee, PhD

Ana Paula Marques, PhD - University of Minho, Portugal

Smaragda Papadopoulou, PhD - Universityof Ioannina - Greece

Maia Chania, PhD - Davit Agmashenebeli University of Georgia

Besik Bolkvadze, PhD - Batumi Shota Rustaveli State University, Georgia

Adebayo Emmanuel, PhD - Federal University of Technology, Akure, Nigeria

Marwan Al Qur’an, PhD - International Business & Strategy, Abu Dhabi University, UAE

Manasi Gore, PhD - Pune University, Maharashtra, India

Dominika Pazder, PhD - Poznań University of Technology, Poland

Copyright © Revistia

ISSN 2411-9571 (Print) ISSN 2411-4073 (online)

European Journal of Economics

and Business Studies April 2018 Vol 4 No 1

5

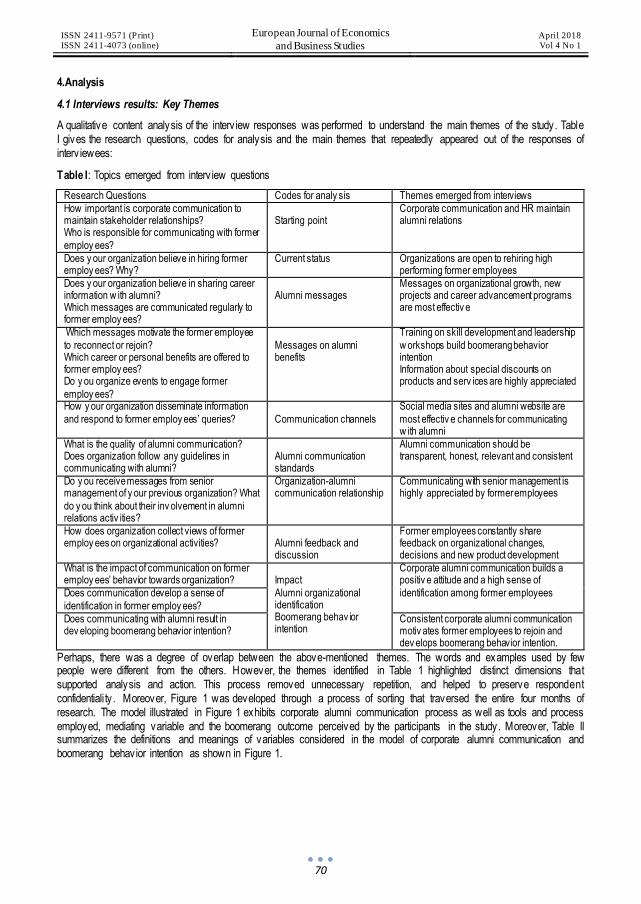

TABLE OF CONTENTS

INNOVATIVE PRACTICES AS A KEY FOR A BETTER MANAGEMENT IN TOURISM INDUSTRY ............................. 8

NIKOLAY TSONEV

SVETOSLAV KALEYCHEV

THE ROLE OF AUDITORS AGAINST MONEY LAUNDERING - ALBANIA CASE .....................................................17

NERTILA CIKA SOTIRAQ DHAMO

IGLI TOLA

ORGANIZATIONAL CONFLICT MANAGEMENT CHALLENGES .............................................................................30

NATALIA KHARADZE

EKATERINE GULUA

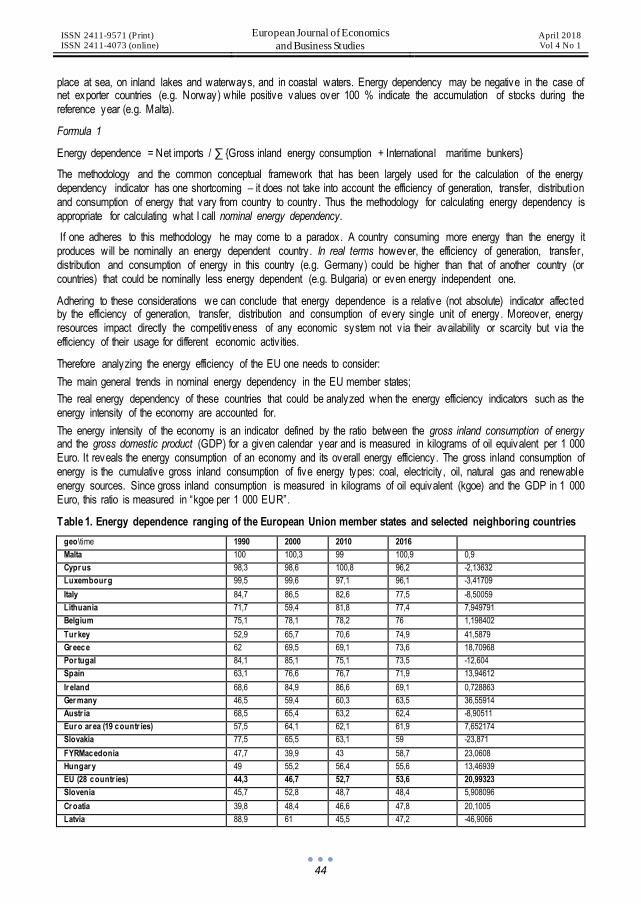

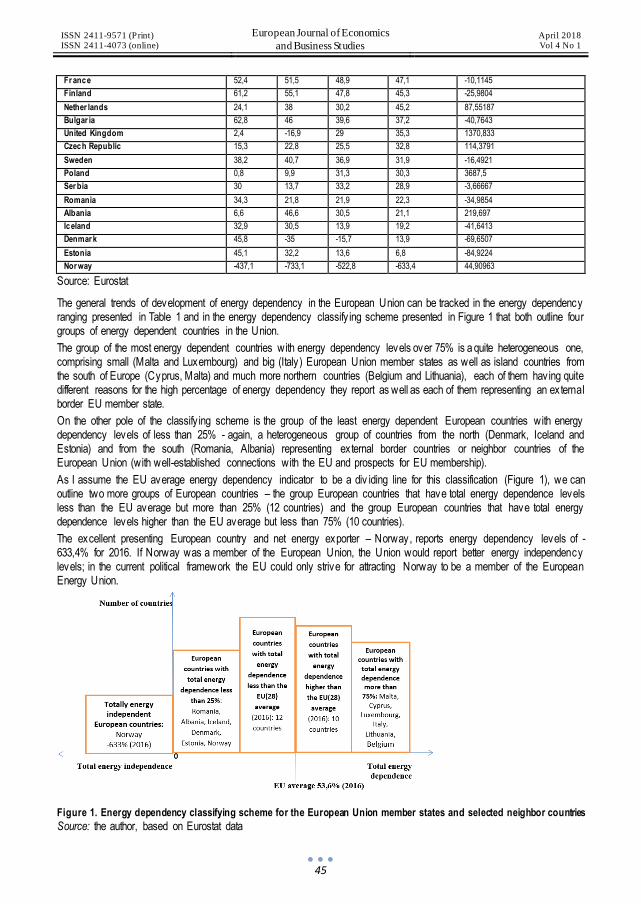

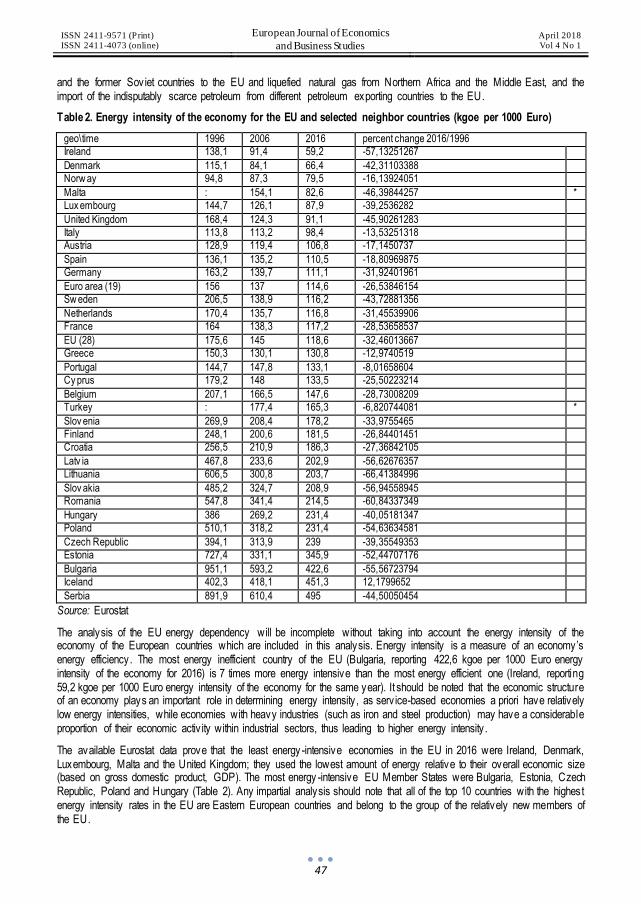

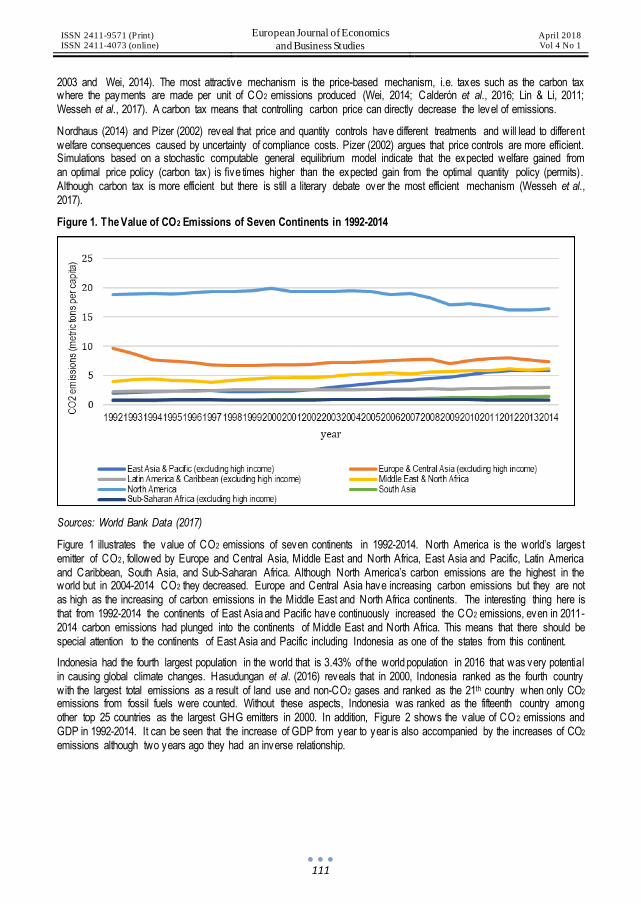

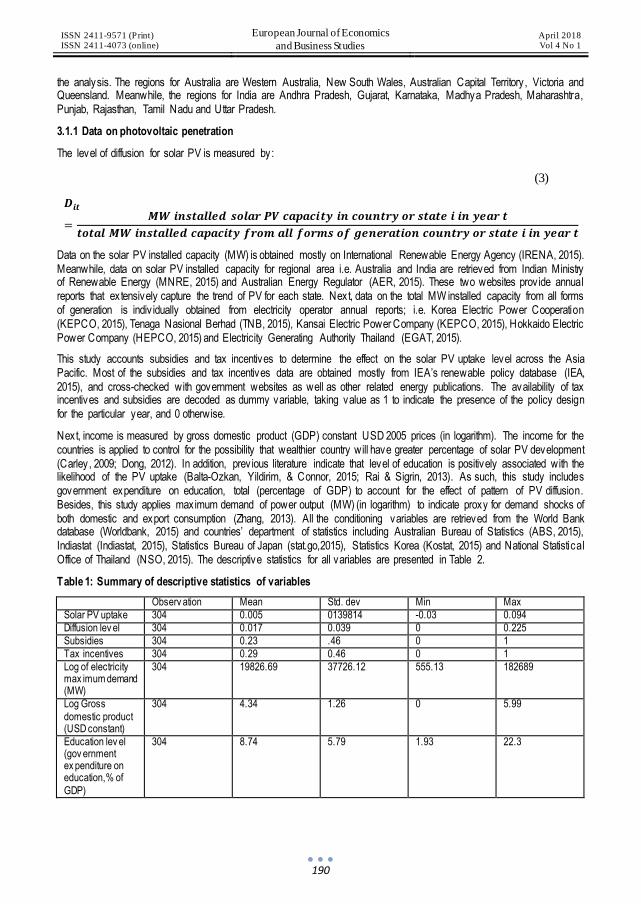

ANALYSIS OF THE ENERGY DEPENDENCE OF THE EUROPEAN UNION.............................................................42

SVETLA BONEVA

PUBLIC SERVICE EMPLOYEE MOTIVATION ISSUES IN GEORGIA .......................................................................49

SALOME SAKVARELIDZE

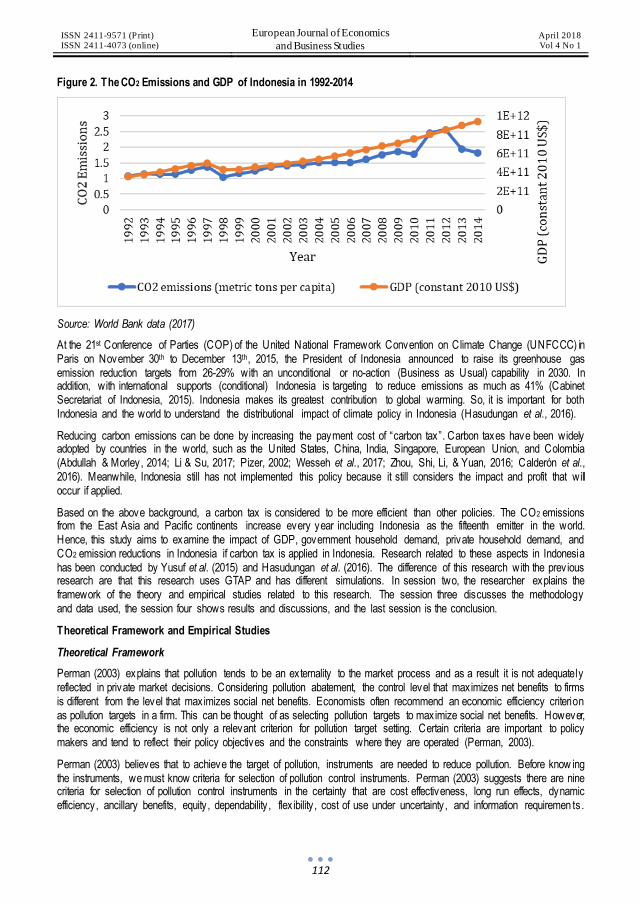

THE WAYS OF CREATING NEW PATHS FOR FINANCIAL ORGANIZATIONS WITHIN THE FRAMEWORK OF SPATIAL DEPENDENCY .......................................................................................................................................56

EMEL ALTIN

MURAT KASIMOĞLU

ALI KÜÇÜKÇOLAK

ROLE OF CORPORATE COMMUNICATION IN BOOMERANG................................................................................66

NEHA SHARMA

AUDIT TESTS AND THEIR IMPACT ON FRAUD DETECTION-CASE OF ALBANIA .................................................79

MIRELA UJKANI MITI

ELENA MYFTARAJ (TOMORI)

TRACKING THE NEW DEMAND FOR JUSTICE IN THE BIG DATA ECOSYSTEM ...................................................89

CARMEN VARGAS PÉREZ

JUAN LUIS PEÑALOZA FIGUEROA

IMPACT EVALUATION OF INDONESIA CONDITIONAL CASH TRANSFER PROGRAM (BSM) ON STUDENT ACHIEVEMENT.....................................................................................................................................................98

ROSINTA HOTMAIDA FEBRIANTI PURBA

THE IMPACT OF CARBON TAX APPLICATION ON THE ECONOMY AND ENVIRONMENT OF INDONESIA .......... 110

PUTRI AYU

THE IMPORTANCE OF RESOURCE ASSESSMENT FOR ENTREPRENEURSHIP AND LOCAL ECONOMIC DEVELOPMENT IN KOSOVO .............................................................................................................................. 121

SEJDI REXHEPI MJELLMA KADRIU

CREATIVE ACCOUNTING – SOME ASPECTS OF KNOWLEDGE AND IMPLEMENTATION IN ALBANIA............... 134

MIRELA UJKANI MITI

ISSN 2411-9571 (Print) ISSN 2411-4073 (online)

European Journal of Economics

and Business Studies April 2018 Vol 4 No 1

6

ELENA MYFTARAJ (TOMORI) BRISEJDA RAMAJ ZENUNI

STATE PROCUREMENT ELECTRONIC SYSTEM EFFICIENCY IN GEORGIA........................................................ 146

TINATIN MEDZMARIASHVILI

ECONOMIC GROWTH THOUGH COMPETITIVE ADVANTAGE AND SPECIALIZATION: THE EXAMPLE OF WINEMAKING IN MOLDOVA ............................................................................................................................... 150

PROF. DR. TATIANA PÎŞCHINA

ROMEO FORTUNA

ORIENTAL CULTURAL VALUES DEPICTED IN ADVERTISING; WITH SPECIAL REFERENCE TO SRI LANKAN CONTEXT ........................................................................................................................................................... 156

SAJITHA LAKMALI HEWAPATHIRANA

R.I.BATUWANGALA

FACTORS OF FAILURE OF THE IRAQI BANKING SYSTEM IN THE IMPLEMENTATION OF THE DECISIONS OF THE BASEL COMMITTEE ................................................................................................................................... 161

JASIM MOHAMMED MUSHIB JANABI

ZAINAB HUSHAM QASIM AL-RIKABI

PROFESSIONAL ETHICS IN ACCOUNTING AS ASSESSED BY MANAGERS OF ENTITIES.................................. 167

GRAŻYNA VOSS

THE REFLECTION OF THE CONSUMERS’ SPIRITUAL PERSPECTIVE TO THE MATERIALISM: A CASE FROM TURKEY ............................................................................................................................................................. 176

SÜREYYA KARSU DILŞAD ÇOKNAZ

MEFTUNE ÖZBAKIR UMUT

MELTEM NURTANIŞ VELIOĞLU

THE ROLE OF POLICY INSTRUMENTS ON THE PATTERN OF DIFFUSION: THE CASE OF SOLAR PHOTOVOLTAIC IN ASIA PACIFIC...................................................................................................................... 186

FARAH ROSLAN

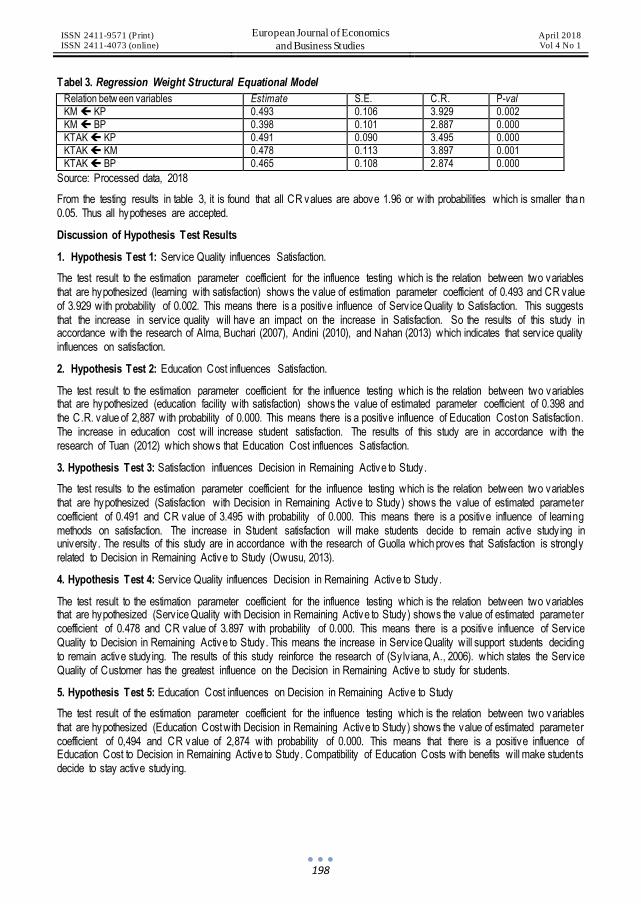

SERVICE QUALITY AND EDUCATION COST IMPLICATION THE DECISION TO STAY ACTIVE RE-STUDY MEDIATED BY STUDENT SATISFACTION – A STUDY AT PRIVATE UNIVERSITY IN WEST JAVA ....................... 193

YENNY MAYA DORA

COLLECTIVE INTELLIGENCE: A NEW MODEL OF BUSINESS MANAGEMENT IN THE BIG-DATA ECOSYSTEM . 201

JUAN LUIS PEÑALOZA FIGUEROA

CARMEN VARGAS PÉREZ

TAX STRUCTURE AND DEVELOPING COUNTRIES ............................................................................................ 213

LUMNIJE THAÇI

ARBNORA GËRXHALIU

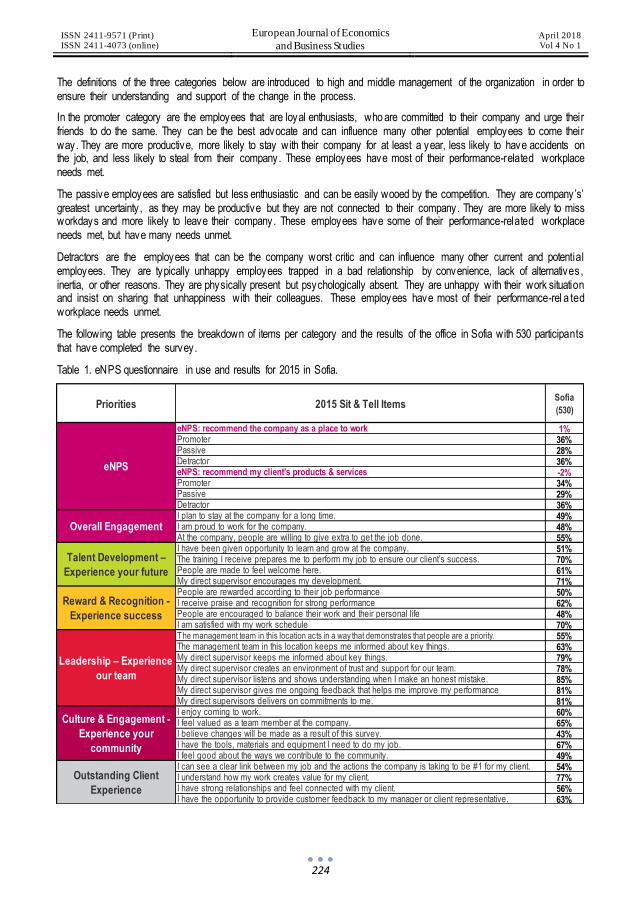

EMPLOYEE SATISFACTION VS. EMPLOYEE ENGAGEMENT VS. EMPLOYEE NPS ............................................ 221

MAYA YANEVA

THE SHARING ECONOMY AT TOURIST TOURS AND ITS IMPACT ON THE TOURIST BUSINESS (TRAVEL AGENCIES) IN BULGARIA .................................................................................................................................. 228

ISSN 2411-9571 (Print) ISSN 2411-4073 (online)

European Journal of Economics

and Business Studies April 2018 Vol 4 No 1

7

MARIANA IANEVA

THE IMPACT OF PRODUCT EXPOSURE AS A KEY ELEMENT OF SALES PROMOTION ..................................... 235

SHAIP BYTYÇI

IMPORTANCE OF QUALITY CONTROL IMPLEMENTATION IN THE PRODUCTION PROCESS OF A COMPANY .......................................................................................................................................................... 240

FRANCISCO JAVIER BLANCO-ENCOMIENDA ELENA ROSILLO-DÍAZ

JUAN FRANCISCO MUÑOZ-ROSAS

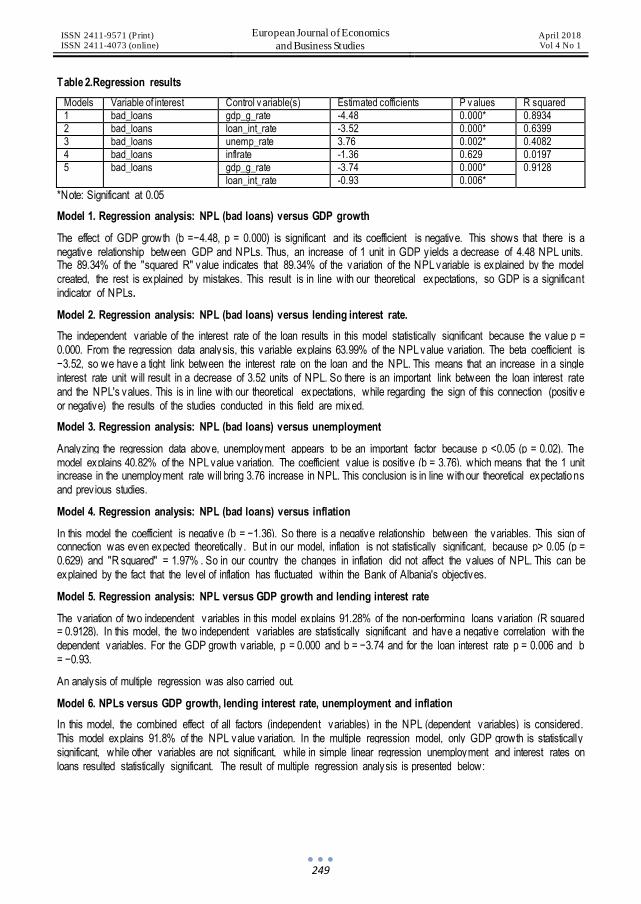

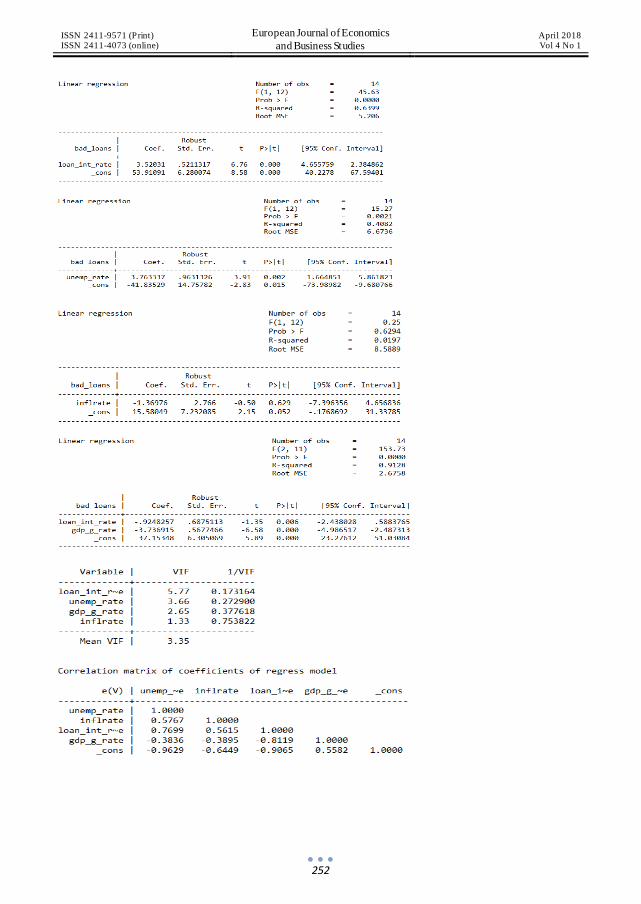

RELATIONSHIP BETWEEN ECONOMIC FACTORS AND NON-PERFORMING LOANS- THE CASE OF ALBANIA.. 245

VALBONA GJINI

LUCIANA KOPRENCKA

CONSULTANCY SERVICES AND THEIR IMPACT IN FINANCIAL REPORTING - CASE OF ALBANIA ................... 253

BRISEJDA ZENUNI RAMAJ MIRELA UJKANI MITI

COMMON CHARACTERISTICS AND DIFFERENCES IN EXTERNAL AND INTERNAL AUDITING .......................... 261

FATMIR MEHMETI

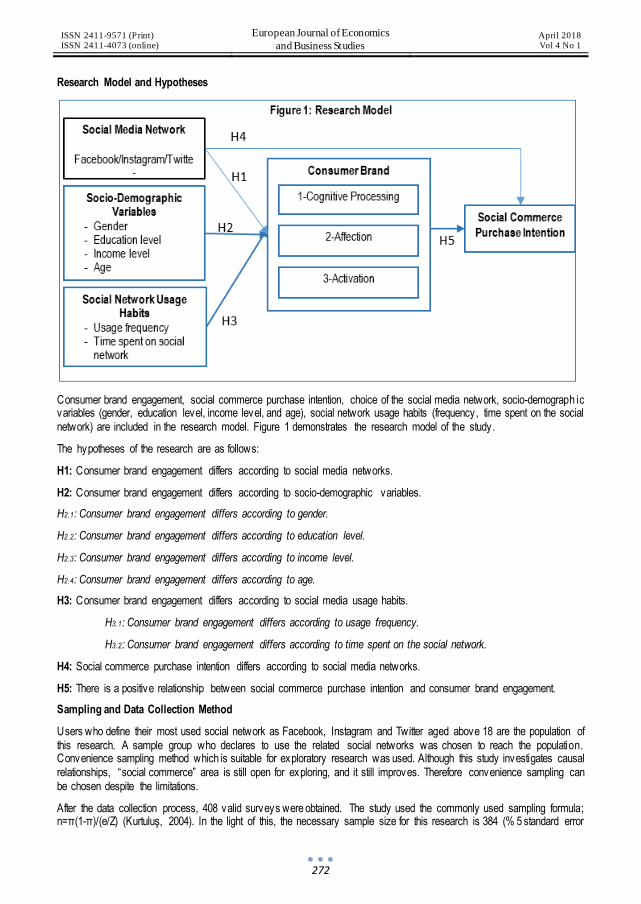

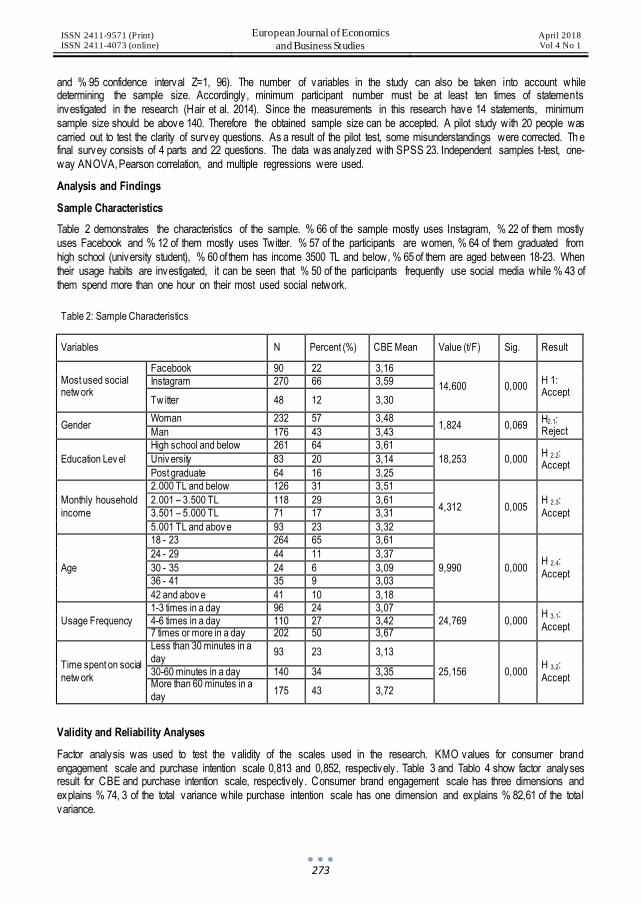

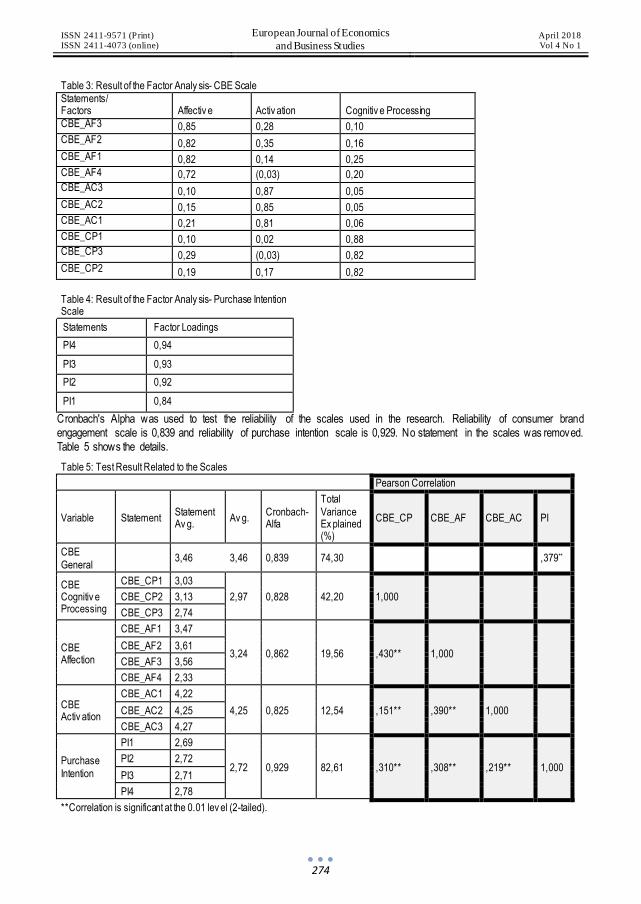

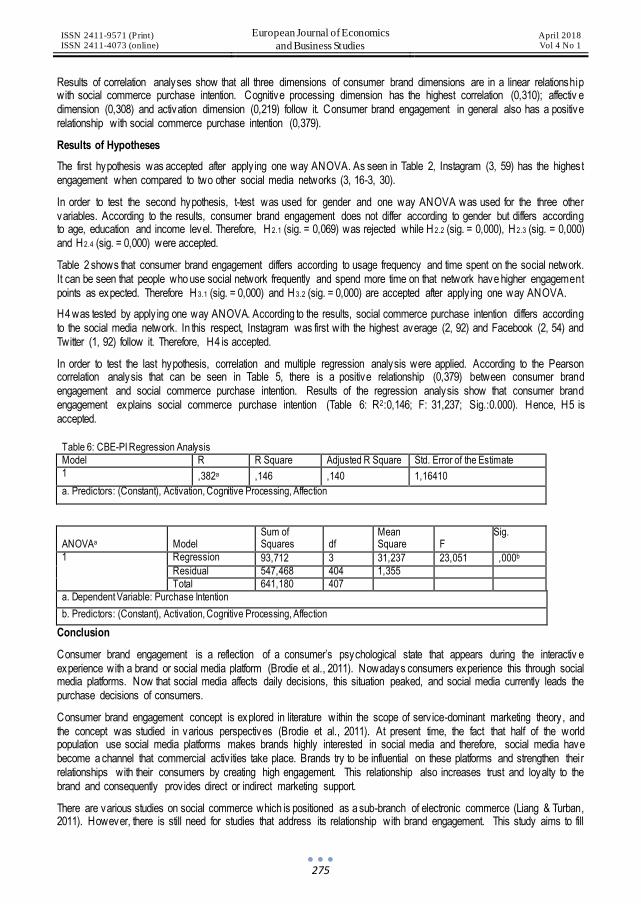

INSTAGRAM, FACEBOOK OR TWITTER: WHICH ENGAGES BEST? A COMPARATIVE STUDY OF CONSUMER BRAND ENGAGEMENT AND SOCIAL COMMERCE PURCHASE INTENTION....................................................... 268

İBRAHIM KIRCOVA

YILMAZ YAMAN

ŞIRIN GIZEM KÖSE

GLOBAL FINANCIAL CRISES: THE IMPACT ON ALBANIAN ECONOMIC GROWTH ............................................ 279

ÇELJETA SHERIFI

GÜNGÖR TURAN

RENEWABLE ENERGY AND SOLAR BUSINESS IN THE EUROPEAN UNION ...................................................... 295

NONCHO DIMITROV

ISSN 2411-9571 (Print) ISSN 2411-4073 (online)

European Journal of Economics

and Business Studies April 2018 Vol 4 No 1

8

DOI: 10.26417/ejes.v4i1.p8-16

Open Access. © 2018 Nikolay Tsonev and Svetoslav Kaleychev.

This is an open access article licensed under the

Creative Commons Attribution-NonCommercial-NoDerivs 4.0 License

Innovative Practices as a Key for a Better Management in Tourism Industry

Nikolay Tsonev

Assoc. Prof. Dr. University of National and World Economy, Bulgaria

Svetoslav Kaleychev

Assist. PhD, University of National and World Economy, Bulgaria

Abstract:

The dynamics in socio-economic life raises the need of new organizational and managerial solutions that meet the requirements of contemporary society . Innovative technologies, as part of these solutions, have a major impact on all areas of life and determine the direction of social development. Modern managers and leaders in the economic industry strive to implement the best innovation practices that will be the key for achiev ing of the maximum results and ultimate goals. In this respect, tourism as a sector of global economic and social importance is aware of the need to implement innovative practices in all tourism activ ities. International tourism market show specific changes in the actual and potential tourist behavior. These changes are significant and affect all of the participants in the process of formation and realization of the tourism products, producers and distributors. The main goal is connected with the achiev ing of a more personal experience, inner satisfaction and maximum recovery as expression of the global contemporary trends in the tourism business. In a more dynamic competitive environment, participants in the tourism market must increasingly rely on the implementation and use of innovative technologies that improve management, organizational structure, economic policy and contributing for the success of the tourism companies.

Keywords: tourism, innovation, management

1. Introduction

Today 's society lives in an extremely dynamic, comprehensive, full of information and opportunities world. This is due to the growing and determining role of digitization in an increasing number of industrial sectors of the world economy. It shoul d be noted the fact that the modern economy, especially in its practical and applied part, is directing its efforts towards introducing new and innovative practices of production process, organization of business, positioning of production and serv ices and their market consumption. In today 's global society , these practices are enormous and the rate at which they change and evolve is extremely large. This remarkably dynamic environment in which the world economy develops also has an impact on the tourism industry . It must be said that travel and tourism industry is one of the world’s largest industries with a global economic contribution of over 7.6 trillion U.S. dollars in 2016, which is 10,2% of world GDP. The sector now supports 292 million people in enviroment – that’s 1 of 10 jobs on the planet and it developing is under the strategic impact of modern innovations in all directions of its activ ities. Due to the broad access of information and the opportunity for global and fast communication, the tourism industry is shaping under conditions of a strong and highly changing competitiv e environment. These conditions determined the need of implement and use of new and innovative practices and technologies to identify the difference and contribute to success of indiv idual tourism enterprises. It is the extremely complex and highly competitive environment in which modern tourism enterprises develop their activ ities and it determines the need for creation of a better management and organizational standards, leading for the best management decisions that will be the key to maximizing efficiency. They also lead the introduction of new and innovative practices, which are a direct expression of the contemporary requirements of tourists, regarding used tourist products and serv ices. At this stage, it may

ISSN 2411-9571 (Print) ISSN 2411-4073 (online)

European Journal of Economics

and Business Studies April 2018 Vol 4 No 1

9

be necessary to conclude that modern tourism enterprises are directing their efforts towards for the use of innovative practices that will lead to implementation of better managerial decisions at all stages of management actions.

At a global level, innovation policy is becoming a key factor and a key tool for achiev ing competitiveness in tourism. Changes in tourism supply as a result of globalization processes lead to new challenges for the tourism business in Bulgaria as well. The short and long-term development policies should be rethought by the market participants, regarding the new conditions.

World tourism trends pose to the state policy in Bulgaria the need to stimulate the development of innovations and the adoption of the relevant regulations, which direct the business towards to implementation of innovation policy. Innovation takes central place at the EU's growth and jobs strategy. A key feature of the economics of knowledge is the creation, conservation, dissemination and use of knowledge as a way to achieve accelerated growth rates and greater competitiveness.1

It can reasonably be argued that, to a large extent, the management of the tourist enterprise or destination determines and guides the choice of tourists seeking new and fulfilling tourist experiences. The technological prov ision and the better organizational structure of serv ices, following the introduction of innovative practices and technologies, create positive impressions, comfort and personal satisfaction during the tourist stay and the various tourist activ ities that accompany it.

2. Method

Based on the information prov ided and according to the purpose of the present study, to reveal the manifestations and the effects of the better management in tourism as a result of the application of innovative practices, a method of study was chosen. Taking into account the nature of the matter under consideration, the "questionnaire" methodology is applied as a comprehensive and in-depth approach to innovation focusing on consumer experiences and experiences as the basis for choosing solutions. The questionnaire surveys are a very traditional way of conducting research. They are particularly useful for non experimental descriptive designs that seek to describe reality . Likewise, the questionnaire survey approach is frequently used to collect information on attitudes and behavior2.

The advantages of questionnaires are as follow: practical; large amounts of information can be collected from a large number of people in a short period of time and in a relatively cost effective way; can be carried out by the researcher or by any number of people with limited affect to its validity and reliability ; the results of the questionnaires can usually be quickly and easily quantified by either a researcher or through the use of a software package; can be analyzed more 'scientifically ' and objectively than other forms of research; when data has been quantified, it can be used to compare and contrast other research and may be used to measure change and positiv ists believe that quantitative data can be used to create new theories and / or test ex isting hypotheses3.

The focus of attention is on studying a specific innovative hotel practice with an innovative character based on the study of the better results achieved by managers of the hotel complexes, to highlight and present the usefulness of introducing innovative technology in the tourism industry .

A basic principle of design as a "way of thinking" is to create a harmony between the function of the product / serv ice and the shape and environment in which it is used so that the user remains with positive impressions4

3. Analysis

Creating better management in tourism companies is an extremely complex and dynamic process related to the change and restructuring of business models, activ ities, processes and competencies in order to better exploit the opportuniti es created by the implemented innovative technologies, taking into account their strategic and future influence of the enterprise. The development of new management models and activ ities is a key factor of creating conditions through which tourist preferences will be more flex ible, market oriented and innovative, effective and responsive to current and future changes in economic reality and in the minds of today’s and future tourists. The goal of a better management of tourism

1Ianev a, M., Georgieva, R.,"Innovations of the MICE tourism: Opportunities in Bulgaria", 3rd International Scientific Business Conference on Leadership and Management: Integrated Politics of Research and Innovations – LIMEN 2017, Belgrade, Serbia 2 Mathers. M., Fox, N., A. Hunn, “Surveys and questionnaires”, NIHR RDS for the East Midlands / Yorkshire & Humber 2009 3http://libw eb.surrey.ac.uk/library/skills/Introduction%20to%20Research%20and%20Managing%20Information%20Leicester/page_51.htm 4 Stankov a.M, Kaleychev.S., 2017, “ The trajectory of creativity and innovation in tourism” XIII International Scientific Conference -

Modern Science, Business and Education, Dobrich, Bulgaria

ISSN 2411-9571 (Print) ISSN 2411-4073 (online)

European Journal of Economics

and Business Studies April 2018 Vol 4 No 1

10

companies is to create conditions and environment for faster entry of a new and innovative technological solutions, increasing their reliance on the company's activ ity in order to achieve more efficient, higher quality results, as well as creating serv ices and products that meet the interests and demands of a wider range of real and potential consumers1. The best management is the key that enables modern tourists to have more control over their personal experiences and emotions during the tourist experience. Reality shows that a better organization in a tourist enterprise is not related for example, only to a certain type of interface or IT program, or a certain type of new digital product that is offered to tourists . Rather, it expresses how the tourist company operates and how it offers its products and serv ices, allowing tourists to get the most out of any tourist activ ity during their stay.

Modern innovative technologies, developed specific business models and types of management, revolutionized the process of making and creating the management solutions offered by the tourism industry . Examples of such innovations are the use of personal smart phones such as key card for hotel rooms; hotel accommodation using personal mobile phone; mobile reservations; electronic media in the hotel lobby; electronic luggage stickers carry ing their own information platforms; use on-board smart phones; hotel search optimization systems; Internet Protocol Voice Phones that are linked to the hotel's internal system ( in-room telephones, through which v isitors can order a room serv ice directly from the touch screen) using system communicates directly with the relevant hotel departments; portable identify guests tablet menus and reservation systems table in restaurants; an electronic device that can track every action of the cook and his team, and the customer can even give him a comment or talk about the recipe; cyber-mirror that allows you to get weather information, read the news, or define a route while looking around, wondering what to wear and many others.

On the basis of the information prov ided so far, the report will present innovative practice in tourism, aimed to create a better organization in the hotel industry in order to achieve the most efficient management decisions, improv e the working process and maximize the satisfaction of the tourists. The essence of this innovative practice is bracelet chip serv ice introduced in the 2014 season in Bulgarian hotel complexes and subsequently distributed in a large number of hotels operating on the Bulgarian Black Sea coast. At present 50 hotels use this device.

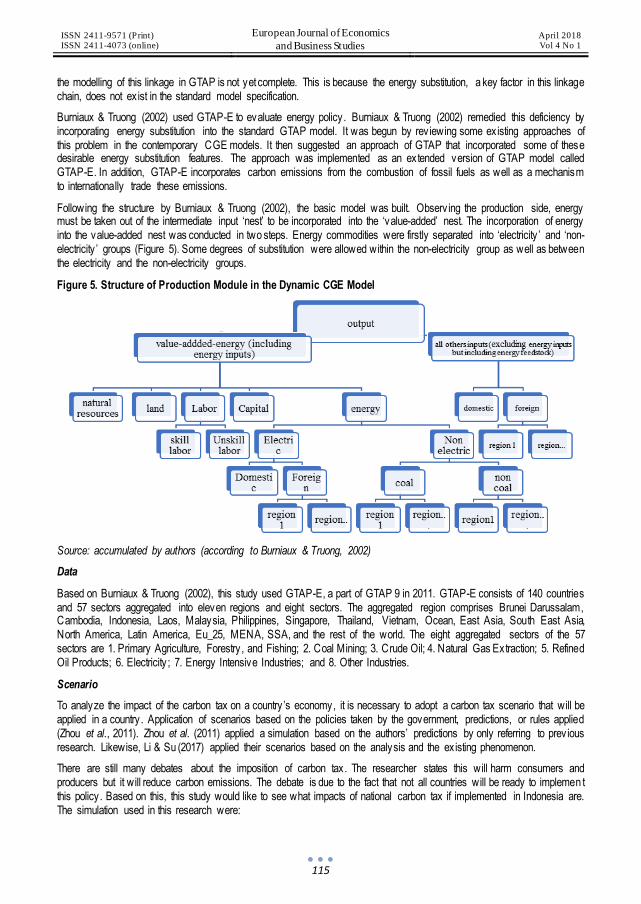

Chip bracelet is an innovative and modern solution designed to improve the overall tourist experience during rest, recreation or entertainment. The hotel complexes in Bulgaria, which have implemented it in their business, aim to offer complex serv ice, using the chip bracelet such as a room key or a multipurpose payment device. With it help, guests do not wear a wallet or room key because the intelligent bracelet allows the opening of the personal room or the payment of different purchases to be done with just one touch of the bracelet to the specific touchscreen.

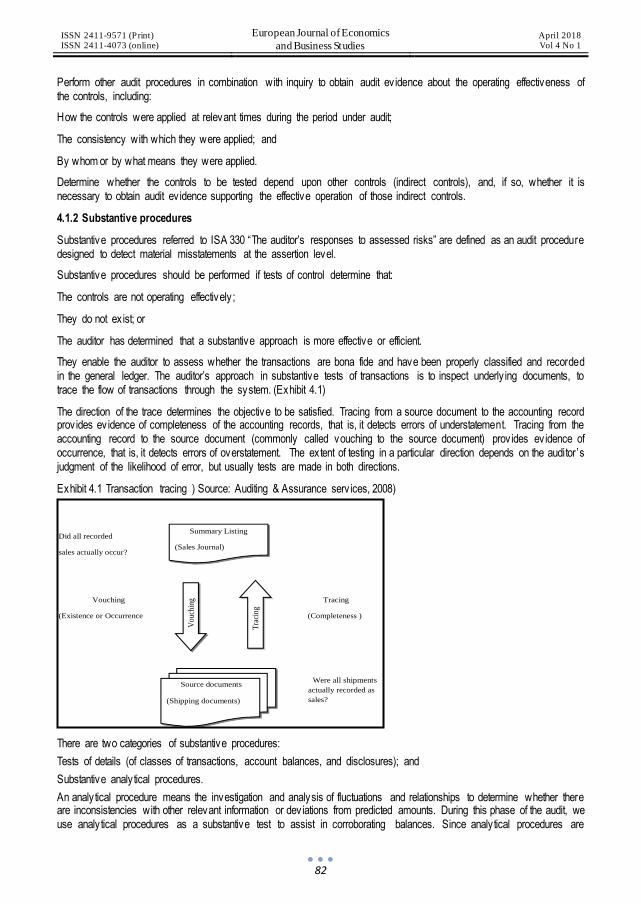

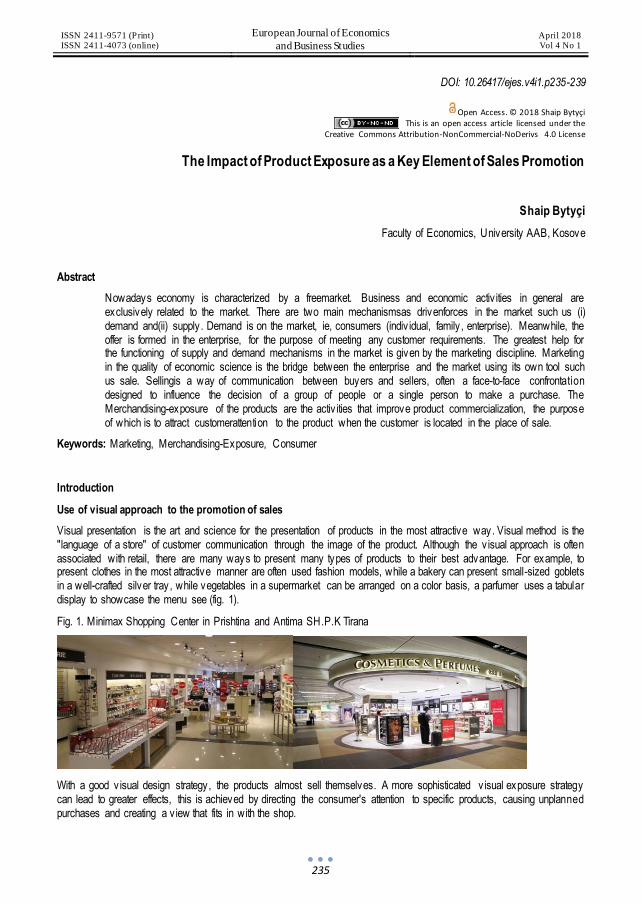

Figure 1. Example of an all-inclusive access control bracelet with non-contact tag

Source:https://www.tripadvisor.com.au/LocationPhotoDirectLink-g8766716-d8762779-i280667790-Melia_Braco_Village-Rio_Bueno_Trelawny_Parish_Jamaica.html

In technical terms, the chip bracelet consists of two parts (Figure 1). One part is a colored strap with a buckle that allows adjustment of the width when placing the hand of the tourist. It is made of water-resistant, impact-resistant, sun-resistant

1 Stankov a, M. & S. Kirilov, S. Kaleichev, I. Vasenska (2015), “Innovation and tourism – Getting sustainability trough good practices”. Sustainable mountain regions: make them work, International Scientific conference, Proceedings 14-16 May 2015, Borovets, Bulgaria.

ISBN 978-954-411-220-2, p. 175.

ISSN 2411-9571 (Print) ISSN 2411-4073 (online)

European Journal of Economics

and Business Studies April 2018 Vol 4 No 1

11

materials, allowing it to be used in various conditions without disturbing its integrity . The shape and color combinations of the bracelet are tailored to the feeling of wear and tear. The second part consists of a chip a non-contact PVC tag attached to the bracelet. The tag allows multiple use with rewriting and reading. It is a major component of the so-called “Chip Bracelet” because it brings all the information about the tourist who uses it. It can reasonably said that is collection of an electronic identity card with tourist data and an electronic debit card that holds some of its financial resources.

The conceptual innovation in chip bracelet serv ice is related to the ability to improve and optimize the organization of work, serv ice and by the statistics from bracelet data to take the best management decisions for the overall functioning of a hotel complex. Every tourist can charge their bracelet chip electronically on each of the receptions or areas designated for this activ ity , with a sum determined by him / her, and then dispose and pay with his / her means at each of the commercial premises designated by the hotel complex. On this way, a tourist without physical money can use a variety of serv ices. On the other hand, the chip bracelet promptly informs the holder for any financial transaction, the type of purchased products or serv ices and the available financial amount at its disposal at any point of its stay.

Whether the hotel guest is in the pool, sports or collects sun rays, the bracelet chip allows secure, fast and easy access to any serv ice or product offered in the complex. It frees it from the necessity of wearing cash currency, from worry ing about its security , while enabling him / her to quickly and easily make a payment, with just one hand movement and touching the bracelet chip to a corresponding sensor device.

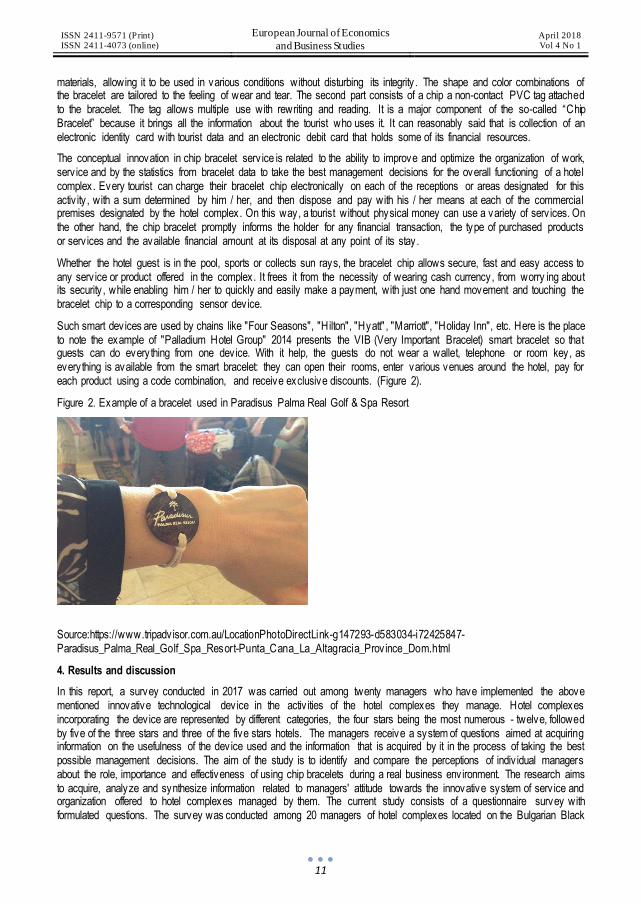

Such smart dev ices are used by chains like "Four Seasons", "Hilton", "Hyatt" , "Marriott", "Holiday Inn", etc. Here is the place to note the example of "Palladium Hotel Group" 2014 presents the VIB (Very Important Bracelet) smart bracelet so that guests can do everything from one device. With it help, the guests do not wear a wallet, telephone or room key, as everything is available from the smart bracelet: they can open their rooms, enter various venues around the hotel, pay for each product using a code combination, and receive exclusive discounts. (Figure 2).

Figure 2. Example of a bracelet used in Paradisus Palma Real Golf & Spa Resort

Source:https://www.tripadvisor.com.au/LocationPhotoDirectLink-g147293-d583034-i72425847-Paradisus_Palma_Real_Golf_Spa_Resort-Punta_Cana_La_Altagracia_Province_Dom.html

4. Results and discussion

In this report, a survey conducted in 2017 was carried out among twenty managers who have implemented the above mentioned innovative technological dev ice in the activ ities of the hotel complexes they manage. Hotel complexes incorporating the device are represented by different categories, the four stars being the most numerous - twelve, followed by five of the three stars and three of the five stars hotels. The managers receive a system of questions aimed at acquiring information on the usefulness of the device used and the information that is acquired by it in the process of taking the best possible management decisions. The aim of the study is to identify and compare the perceptions of indiv idual managers about the role, importance and effectiveness of using chip bracelets during a real business environment. The research aims to acquire, analyze and synthesize information related to managers' attitude towards the innovative system of serv ice and organization offered to hotel complexes managed by them. The current study consists of a questionnaire survey with formulated questions. The survey was conducted among 20 managers of hotel complexes located on the Bulgarian Black

ISSN 2411-9571 (Print) ISSN 2411-4073 (online)

European Journal of Economics

and Business Studies April 2018 Vol 4 No 1

12

Sea coast. They manage hotels with different sizes, mode of operation and type of the offered tourist products and serv ices. All of that implies differences and specifics in the choice of answers determined by the essence of their activ ity , way of work and management capabilities.

A system of questions has been set up for managers in the following form:

1. What is your nationality?

Bulgarian other ...........................................

2. What is your age?

26- 35 years 36 - 45 years

46-55 years over 55 years old

3 Are you support the implementation of innovative practices to optimize the activ ities of hotel complexes?

yes no I have no opinion

4. Do you think that the serv ice in the complex is much faster using a bracelet chip?

(Yes) (Maybe) (No) (I have no opinion)

5. Is the statistical information obtained by using a bracelet chip in the complex improv ing your management decisions?

(Yes) (Maybe) (No) (I have no opinion)

6. Does the accounting organization of the complex improve after the implementation of the bracelet chip as the primary payment instrument?

(Yes) (Maybe) (No) (I have no opinion)

7. Is the efficiency of the staff in the work process increased due to the use of a bracelet chip by the guests of the complex?

(Yes) (Maybe) (No) (I have no opinion)

8. Do you receive a faster information about each serv ice that is paid in the various venues around the hotel complex?

(Yes) (Maybe) (No) (I have no opinion)

9. Do you think the process of activating and charging the bracelet chips is fast enough?

(Yes) (Maybe) (No) (I have no opinion)

10. Do you think that turists used bracelet chip as a serv ice method in the complex, are satisfied with it?

(Yes) (Maybe) (No) (I have no opinion)

11. Do you think that the use of bracelet chip in the future will find a wider manifestation in the tourism industry?

(Yes) (Maybe) (No) (I have no opinion)

The answers to the questions were analyzed and presented in graphs, the results being presented in a quantitative and proportional ratio. For the purpose of this report an analysis of the information obtained from the survey will be presented in graphical form.

ISSN 2411-9571 (Print) ISSN 2411-4073 (online)

European Journal of Economics

and Business Studies April 2018 Vol 4 No 1

13

Figure 3: Nationality of the tourists involved in the survey

Source: own survey

From the information presented in (Figure 3), it is clear that the managers who participated in the survey are only bulgarians. This fact is due to the successful tourism business in Bulgaria and the favorable opportunities for building professional bulgarian managers to meet the contemporary requirements of the dynamic tourism industry .

Figure 4: Age range of participants in the study

Source: own survey

In the analysis of the obtained data in (Figure 4), it is clear that the largest number of participants in the survey are in the age range of 36-45 years old, accounting for more than half of the total number of all respondents. This fact is due to the preference of hotel owners to hire already established managers with experience but also with knowledge of new technologies, products and serv ices in the hotel industry . The second most important group involved in the survey is between the ages of 26-35. The representatives of this group being the young wave of managers who are less experienced but familiar with all new trends of modern tourism and are digitally oriented, hav ing the skills to deal with the latest and innovative technologies and methods of serv ice and business. The third age group by number of respondents in the study ranged from 46-55 years. Here we can find mainly managers with very wide practical experience but can be said that they belong to the older generation that is not technologically oriented in terms of processes related to the implementation and operation with innovative technologies and products in hotel industry . Managers of the age range over 55 years were not identified during the survey, perhaps due to the fact that they could very hardly use new and innovative technologies during their management duties. Which determines and sets the hotel owners who want to implement such technologies to orient themselves to other types of managers.

Nationality0

20

Bulgarians

Others

Bulgarians, 20

Others, 0

0

5

10

15

26- 35 years36 - 45years

46 - 55years +55 years

26- 35 years, 5

36 - 45 years, 12

46 - 55 years, 3

+55 years, 0

ISSN 2411-9571 (Print) ISSN 2411-4073 (online)

European Journal of Economics

and Business Studies April 2018 Vol 4 No 1

14

Figure 5: Are you support the implementation of innovative practices to optimize the activ ities of hotel complexes?

Source: own survey

In the survey (Figure 5) presents the answers of third question asked to all participants, which aimed at establishing the attitudes and preferences of managers towards the introduction and use of optimization practices in tourist serv ices. As the results show, 100% of all respondents are optimization supporters It can reasonably be concluded that modern managers in the tourism industry have a positive attitude towards the optimization of the stay in the hotel complexes managed by them.

Figure 6: Summarized results of the study of the attitude towards the optimization of the serv ice in selected hotel complexes.

Source: own survey

Figure 6 shows the value attitude in the answers to the questions received in the study. A specific point in the survey is the systematisation of questions from the fourth to eleventh in a way that addresses questions that combine four types of answers: "Yes", "Maybe", "No" and " I have no opinion"

20

00%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Yes No No opinion

Question 4

Question 5

Question 6

Question 7

Question 8

Question 9

Question 10

Question 11

Yes 18 19 16 18 20 15 17 17

Maybe 2 2 2 2 2 2

No 2

No opinion 1 2 1 1 1

0

5

10

15

20

25

ISSN 2411-9571 (Print) ISSN 2411-4073 (online)

European Journal of Economics

and Business Studies April 2018 Vol 4 No 1

15

Regarding the fourth question from the survey, it is clear that the choice of the “Yes” answer is a leading one and takes into account the personal and direct experience of the managers regarding the innovative approach in the serv ice. Followed by the answer "Maybe," with notably small amounts of background of the overall opinion on the asked question. The specific moment in the analysis of the information on the given question is related to the fact that the answer "No" does’t ex ist in the selection of the interv iewed managers, which itself is a testimonial for the positive impact of an innovative approach. The fifth question also integrates almost absolute values of the “Yes” response. Followed from the "I have no opinion" response that was noted with only one participant in the surveyed group. The preferred answer is in values from which it can be accepted as dominating and shows the direct experience of managers regarding the usefulness of using chips bracelets in the overall activ ity of the complex. On the six th question, the analysis of the information shows extremely high values of the "Yes" answer, the second and the third choice of the respondents being the answers "Maybe" and " I have no opinion " with two preferences. It is noteworthy that the answer "No" is missing as it is a direct expression of the additional efficiency in accounting that comes from the introduction of the innovative product. The leading answer to the seventh question is related to the choice of "Yes", which is extremely dominant. Only two people chose the "Maybe" response during the study. The other two responses were not preferred by any of the study participants. This question shows the overall positive result of the introduction of the chip bracelet, with better management decisions affecting all levels and structures in the hotel complex. The eighth question is extremely interesting from an informational point of v iew as it shows the effectiveness of the innovative product implementation. 100% of all managers have chosen the "Yes" answer, confirming the high levels of creativ ity and innovativeness embedded in the innovative approach of this kind of tourist serv ice. The ninth question also addresses the tangible leading role of the "Yes” answer, but must be noticed that this is the only question that contains the four types of answers selected in the study. The second most important answers are "Maybe" and "No" with 2 preferences, while the third choice is the " I have no opinion " option, preferred by only one of the managers surveyed. The tenth question combine together three of the possible answers, div iding their number into similar amount in the study so far. A leading choice is the “Yes” answer chosen by seventeen managers involved in the study, followed by the answer "Maybe" with two preferences, and the third is the "I have no opinion" with only one answer. These magnitudes of our responses are due to the fact that still in the Bulgarian hotel serv ices are some specifics regarding the management priorities. Some of them sometimes do not take into account the values of satisfaction of their tourists in contrast to other leading world and European hotel industry . The last eleventh question takes into account the leading role of the "Yes" response as the main choice of surveyed managers. Followed by the answer "Maybe," while the " I have no opinion" answer takes the third position. It should be noted that the answer "No" is not preferred by any of the survey participants. The answer to this question clearly reflects the v iews and opinions of the interv iewed managers about the future of the hotel serv ice and draws attention to the use of creative and innovative approaches in it.

5. Conclusion

The data obtained from this study show that innovative practices impacting on better management decisions, consequently improv ing organizational structure in tourism serv ices and they are increasingly important in the activ ity of each touris t enterprise. It can be argued that the innovative products and serv ices offered by the tourist companies, modeling and predetermine the choice of a specific tourist destination in the conditions of an extremely dynamic competitive environment. Modern tourists orient their preferences to destinations that prov ide them with comfortt, security , fast and quality serv ice as well as technological solutions that contribute to a more complete personal satisfaction and memorable holiday. Undoubtedly , the innovative products and serv ices offered by tourism companies are one of the most important factors in the contemporary tourism business, they allow modern managers to make decisions that are based on a large practical information and which are aimed at maximally satisfy ing all the requirements of tourists. The 21st century tourist is extremely knowledgeable and has a variety of modern methods and technologies to modeling his preferences and ways to achieve a full tourist experience and satisfaction. That is why it can reasonably be argued that tourism innovations are the key to better management in tourism, being one of the most important prerequisites for creating a better organizational structure in hotel complexes and one of the main factors, which determine the preferences and motivation of modern tourists.

ISSN 2411-9571 (Print) ISSN 2411-4073 (online)

European Journal of Economics

and Business Studies April 2018 Vol 4 No 1

16

References

[1] Ianeva, M., Georgieva, R.,"Innovations of the MICE tourism: Opportunities in Bulgaria", 3rd International Scientific Business Conference on Leadership and Management: Integrated Politics of Research and Innovations – LIMEN 2017, Belgrade, Serbia

[2] Kaleychev.S., 2017, “ Influence of technological transformations on innovative practices in tourism ”, XXV Symposium "Quality , Competitiveness, Sustainable Development" - "The Challenges of the New Technological Transformation", Sofia, Bulgaria

[3] Mathers. M., Fox, N., A. Hunn, “SURVEYS AND QUESTIONNAIRES”, NIHR RDS for the East Midlands / Yorkshire & Humber 2009

[4] Stankova.M, Kaleychev.S., 2017, “The trajectory of creativity and innovation in tourism” XIII International Scientific Conference - Modern Science, Business and Education, Dobrich, Bulgaria

[5] Stankova, M. & S. Kirilov , S. Kaleichev, I. Vasenska (2015), “ Innovation and tourism – Getting sustainability trough good practices”. Sustainable mountain regions: make them work, International Scientific conference, Proceedings 14-16 May 2015, Borovets, Bulgaria. ISBN 978-954-411-220-2, p. 175.

[6] Tsonev, N., Kaleychev, S., Innovative practices as a premise for creating a better organization in tourism companies”, 3rd International Scientific Business Conference on Leadership and Management: Integrated Politics of Research and Innovations – LIMEN 2017 , Belgrade, Serbia

[7] http://libweb.surrey.ac.uk/library/skills/Introduction% 20to% 20Research% 20and% 20Managing% 20Information% 20Leicester/page_51.htm

ISSN 2411-9571 (Print) ISSN 2411-4073 (online)

European Journal of Economics

and Business Studies April 2018 Vol 4 No 1

17

DOI: 10.26417/ejes.v4i1.p17-29

Open Access. © 2018 Nertila Cika et al..

This is an open access article licensed under the

Creative Commons Attribution-NonCommercial-NoDerivs 4.0 License

The Role of Auditors against Money Laundering - Albania Case

Nertila Cika

PhD Cand., Faculty of Economy, University of Tirana, Albania

Sotiraq Dhamo

Prof. Dr. , Faculty of Economy, University of Tirana, Albania

Igli Tola

Faculty of Economy, University of Tirana, Albania

Abstract

In the process of the globalization of the economy one of the biggest challenges is combating and preventing criminal activ ities such as the money laundering. This phenomenon affects the failure of many sectors, such as monetary and banking system, the loss of public confidence in the financial system, the problem in calculating GDP in the affected countries. Albania has been considered a 'paradise' for investing and money laundering from suspicious or illegal activ ities, for more than 20 years. To prevent Money Laundering is necessary to make proper legislation and the involvement of several parties, including also the accounting professionals. The purpose of this paper is to estimate the role and function performed by Albanian Chartered Auditors (CAA –EKR) and auditors of State High Control Institution against Money Laundering. We try to give answer to the main research questions as: Are the Albanian auditors involved in fighting Money Laundering? Which is the level of legislation of Albania regulated against Money Laundering? What is the role of professional body of the auditors in preventing Money Laundering? The conclusions of this paper are based on literature rev iew and data analysis through the independent test, Chi-Square test, gathered from questionnaires designed and intended for Albanian auditors to understand practically how they face this phenomenon in Albania. We find out a negligence of the auditors in reporting ML.Typically the construction companies with Albanian capital are involved in the money laundry transactions and further research studies are recommended to be made.

Keywords: money laundering, auditors, accounting professionals, procedure, financial statements

Introduction

For many years the world faces a very delicate and negative phenomenon that is money laundering. With the development of the world's economies, with the increase of controls over the use of money and their source, the efforts of certain person s or groups have been increased to "clean" their money earned by criminal activ ity , corruption and tax evasion. Globalization of the economy has caused this phenomenon from a national phenomenon to become an international phenomenon because the efforts of criminal groups to “clean” money actually extend to other countries where the opportunities evaluated by them are greater. According to INCSR (2017, Volume 2, March 2017, pg 6) as in past years, money laundering continues to be a serious global threat. As transnational criminal organizations, terrorist groups, and other bad actors increasingly draw upon new technologies and criminal techniques to fund their illegal activ ities and generate and launder their considerable proceeds, the challenges faced by the financial, law enforcement, superv isory, legal, and intelligence communities are exacerbated. Jurisdictions flooded with illicit funds remain vulnerable to the breakdown of the rule of law, the corruption of public officials, and destabilization of their economies.

ISSN 2411-9571 (Print) ISSN 2411-4073 (online)

European Journal of Economics

and Business Studies April 2018 Vol 4 No 1

18

Money laundering (ML) is the process of concealing the criminal origin of activ ities and investments or the unlawful nature of financial transactions. Money laundering (World Bank Guide to AML 2011) is: "Concealing or disguising the true nature, source, location, disposition, movement, real rights in relation to property , knowing that such property is derived from a criminal offense ...” It is a criminal activ ity through which crime proceeds integrate into legitimate activ ities, making it easier to use them further. Paul Byron (2005), the representative of the United States Department of Justice, states that: "Money laundering has to do with gaining wealth from illegal activ ities and efforts to put these benefits into banking systems in such a way as to erase origin of money or even continue criminal activ ity , using the financial system". Actually money laundering activ ity has moved beyond traditional financial institutions to other non-financial businesses and professions and alternativ e money value transfer systems

The phenomenon of ML becomes a problem even for Albania after years 90’ when the market economy has been placed in Albania. For more than 20 years Albania has been considered a 'paradise' for investing and clearing money from suspicious or illegal activ ities. The general belief of experts is that this phenomenon finds 'free land' in our country as a result of many economic, historical and cultural factors. Among them, we can mention: the culture of ‘cash’ transfers; According to IFM (2011)cash-based informal economy (which facilitates the laundering and integration of proceeds of crime, especially in the real estate sector and in commercial undertakings) and the cross border transportation of cash and its further assimilation into the economy and A lbania‘s financial system; the lack of a financial and tax system for more than 45 years; the unstable economic situation, characterized by the 'boom' of the construction industry ; high level of corruption and of informal economy, non-complete legal framework and administrative structures non fully functional up to year 2000, for preventing and combating this phenomenon, etc. Albania (USA State Department, March 2017) remains at significant risk for money laundering due to rampant corruption and weak legal and government institutions. Albania has a large cash economy and informal sector, with significant money inflows from abroad in the form of remittances. Major proceeds -generating crimes in Albania include drug trafficking, tax evasion, smuggling, and human trafficking. Albania has a substantial black market for smuggled goods, and smuggling is facilitated by weak border controls and customs enforcement.. According to the Basel Anti-Money Laundering (AML) Index 2017, Albania is the top of high-risk risk countries in Europe and Central Asia. Albanian scored 5.75 points in the index, and is ranked 85th out of 146 or is the 10-th within European countries. Te methods actually used by criminal organizations for ML, as revealed by investigations are: transactions within the financial sector; Opening of bank accounts in the name of social and family ties; Purchasing or entering into partnerships in legal businesses (commercial companies, construction, serv ices, transportation etc); Opening of offshore companies; Purchasing immovable properties (land, apartments, hotels, restaurants, gas stations etc); Commission of criminal activ ity outside of the territory of Albania, and laundering some of the proceeds obtained from this activ ity in Albania (IFM 2011)

Actually the ML now is a global 'gangrene' it is not any more a national phenomenon. Referring to United Nations Office on Drugs and Crimes's report of 2014, money laundering turnover in the world can reach up to $ 2 trillion, or about 2.5-5% of the global GDP. In the process of ML are involved several parties such as lawyers, bankers, financial organizations, accountants, tax employees, ecct. Various important national and international organizations such as Financial Action Task Force (FATF), OECD, UN, IMF, EU, etc have devised different arrangements or guidelines to combat and prevention money laundering. The governments have prepared the legislation against ML. Professional organizations, including those of accountants; have also devised different guidelines for their actions in the fight against Money Laundering.

The objective of this paper is to highlight the factors and actors that play a role in promoting and preventing the phenomeno n of money laundering in the world and in Albania, and the role that the Albanian Registered Auditors (ARA –EKR) and auditors of State High Control Institution have in particular in this regard. The research questions of this paper are: which is the regulation level of legislation in Albania against Money Laundering? What is the role of professional body of the auditors in preventing Money Laundering? : Are the Albanian auditors involved in fighting Money Laundering? Do Albanian auditors the proper qualification and action to combat money laundering? Which is the role of professional bodies of auditors? To give answers to these questions has been done an international and Albanian literature rev iew. To understand practically how they face this phenomenon in Albania we have use and the data analyses based on the questionnair es prepared and sent to Chartered Auditors (CAA –EKR) and auditors of State High Control Institution. Based on the results of the study of the legislation regulation in Albania against ML and the role of the auditors in combating and preventing this phenomenon we have draw some conclusion and some recommendations.

Methodology

The main purpose of this paper is to estimate the role and function performed by Albanian Registered Auditors (ARA –EKR) and auditors of State High Control Institution against Money Laundering.

ISSN 2411-9571 (Print) ISSN 2411-4073 (online)

European Journal of Economics

and Business Studies April 2018 Vol 4 No 1

19

To achive the objective of the paper, the methodology used is a combination of primary and secondary data. The primary method used is the survey (questionnaire), which enables quantification because it measures the facts objectively . This method enables many cases to be studied with many subjects, and this gives us the ability to use statistical analysis and is more reliable than quality research. Questionnaires were addressed to 212 member of the Institute of Chartered Auditors of Albania (ICAA -IEKA) and to 20 auditors of Supreme Audit Institute (SAI-KLSH). The survey was conducted in Albanian language and the questionnaires are distributed during 2017 by e-mail using Google form. In total we get 46 responses. At first glance, this seems a small number of responses, but knowing that our target champion was no more than 232 indiv iduals, we can say that we have reached about 20 percent. So, this is a good percentage to take survey for this population.

In the survey, most of the questions (9) are closed because they are easier to get an answer from the auditor, and it's easier to make their encryption because they are converted more quickly into statistical data. Only one question of the questionnaire was open questions so that respondents were free to express their opinion regarding the improvement of the procedures against ML. Searching was designed in such a way as to facilitate data collection and at the same time to achieve satisfactory results that would draw conclusions as close to reality

Among the secondary data used, an important place has had the literature on the ML in Albanian and foreign language, especially the Albanian legislation on ML, reports published by specialized national and international institutions, the various guide of international organization on ML and other studies and materials published in this filed. It helps to present a v iew on the ML as a phenomenon and its effects in economy and the necessity to combat it by all the parties involved, to analize the level of legislation on AML and the relative insituttions in Albania, particulary the requirements for companies and auditors and for comaprision with interenatioanl practice.

Reivew of Literature and Theoretical framework

There is important to understand what ML is, what is the role and the consequences in the national and global economy, why the parties are involved in this phenomenon and the role of the governments and vary professional bodies.

3.1 Money laundering as phenomenon

Any amount of money that is either directly or indirectly circulated, re-translated or transferred; transformed or allied to products and property derived from criminal or illegal activ ities and criminal offenses constitutes "dirty" (Bank Of Albania 2017) ”. Money Laundering is the process used to hide the source of money or assets arising from the activ ity criminal. Crime is motivated by profits and involves a variety of illegal activ ities from drug trafficking and smuggling to fraud, robbery and corruption.(GDPML 2015) Money laundering (Duhaime. C . 2014) is a process whereby the proceeds of crime are transformed into apparently legitimate money or other assets. It is said that the term ‘money laundering’ was coined from the practice of the American mafia who, at one time, channelled the cash proceeds of crime through launderettes to legitimize the cash. Whether this is true or not, the term ‘money laundering’ is now widely used. According to wikipedia definition Money laundering is the process of transforming the profits of crime and corruption into ostensibly "legitimate" assets (https://en.wikipedia.org/wiki/Money_laundering-30.01.2018). Anti-money laundering (AML) is a term mainly used in the financial and legal industries to describe the legal controls that require financial institutions and other regulated entities to prevent, detect, and report money laundering activ ities. Many countries have drafted their legislation to combat and prevent money laundering. Many international organizations have also been set up to combat money laundering.Anti-money laundering guidelines came into prominence globally as a result of the formation of the Financial Action Task Force (FATF) and the promulgation of an international framework of anti-money laundering standards. An effective AML program (AMF/CFT 2017) requires a jurisdiction to criminalise money laundering, giv ing the relevant regulators and police the powers and tools to investigate; be able to share information with other countries as appropriate; and require financial institutions to identify their customers, establish risk-based controls, keep records, and report suspicious activ ities. Money laundering (IFAC 2004) is the funneling of cash or other funds generated from illegal activ ities through legitimate financial institutions and businesses to conceal the source of the fund. Money laundering involves the manipulation of large quantities of illicit funds to distance them from their source quickly and in as undetectable a manner as possible. Because money -laundering activ ities may, however, have indirect effects on an entity ’s financial statements, they are of concern to externa l auditors

3.2. Albanian regulation AML

The regulation on AML in Albania has been started to prepare from the year 1995 and after. Albanian regulation and the relevant institution on AML is based on the international and European standards and legislation. Clearing money by

ISSN 2411-9571 (Print) ISSN 2411-4073 (online)

European Journal of Economics

and Business Studies April 2018 Vol 4 No 1

20

investing personally or through third parties is considered a criminal offense, sanctioned by Law: No. 9086, dated 19.06.2003 "On some amendments to Law no. 7895, dated 27.01.1995 "Penal Code of the Republic of Albania"; Law: No. 9085, dated 19.06.2003 "On some additions and amendments to Law no. 7905, dated 21.03.1995 "The Criminal Procedure Code of the Republic of Albania"; Law: No. 9084, dated 19.06.2003 "On some additions and amendments to Law no. 8610, dated May 17, 2000 "On the prevention of money laundering". As explained above, the prov ision of direct or indirect assistance, criminal or even extrajudicial activ ities deriv ing from good, movable or non-property and income, is also punishable. This is because you qualify as a Participant in this process.

Albanian AML legislation (Law No.9917, dated 19.5.2008/2011 Article no 3) define and the subjects involved in Money Laundering Prevention and legal obligation. Law no. 9084, dated 19.06.2003 states that subjects that should be v igilant and active participants in preventing and combating this phenomenon are besides the Banks and entities performing banking and financial activ ities, licensed by the Bank of Albania, other institutions or entities such Notaries, Lawyers, Registered Auditors, Consultancy Offices and Certified Chartered Accountants. This AML legislation considers as very important institution on fighting and prevention ML the Bank of Albania (BOA) and other commercial banks. The Bank of Albania, as well as its other counterparty banks in other countries, exercises a superv isory and controlling role over the entities licensed by it (Second Level Banks, Currency Exchange Points, etc). In exercising this function, it creates legal obligations for the prevention of the money laundering phenomenon.. In addition to the rigorous control of these units, the BOA also compiles mandatory enforceable regulatory policies for these vulnerable entities (Law No.9917, dated 19.5.2008 article 3). The law requires that any suspicious cases ev idencing during the oversight exercise be reported to the GDPML. In the event of confirmation of its suspicions, the BOA continues with monetary sanctions, the removal or suspension of licenses of the entities involved in the ML until the criminal offense of the responsible persons.

The main structure monitoring and directing the AML in Albania is General Directory for Prevention of Money Laundering (GDPML). The law no. 8610, dated 17.05.2000 establishment of the Albanian Financial Intelligence Unit (FIU). The unit was then baptized under the designation of the GDPML. This structure is empowered by the AML legislation (against money laundering and the fight against terrorism financing) to collect, manage and analyze reports submitted by enforcers to prevent and combat money laundering and terrorist financing. Apart from supply ing data to the prosecution and court, GDPML cooperates closely with other Financial Intelligence Units around the world. This is because nowadays money can be invested anywhere within a few minutes.

3.3 The AML regulation for Auditors and Accountants.

Albanian AML regulation involve in the fighting ML and the accounting profession and professional bodies which are e very important part of the entities and their business transaction. In particular it involve the registered auditors member of AIRA – IEKA) and the auditors of Supreme Audit Institution (High State Control). In order to assess whether the company has maintained an effective and AML compliance framework, the Inspection Procedure guided by the GDPML advises also to follow the Independent Testing of the Unit. The main purpose of independent testing is usually to determine the adequacy of the company's AML program, including whether it operates in accordance with the requirements of the AML Law and the policies pursued by society itself. Beside that in Albania GDPML has not the direct oversight on the professional auditors and accountants bodies, the legislation require from the company accountants to deal with the Internal Control System and their v iability to prov ide links to: Care should be shown to the documentation needed to identify the customer and his / her background; Categorize the risk from customers and the transactions carried out with them to identify customers potentially involved in local or international Money Laundering Schemes and to these clients should be shown Growth Care, not allowing to be overlooked without any transaction being scanned with them; As soon as their doubts come to their attention, public or anti criminal authorities should be contacted to report the case. Reporting also implies the filing of all the proofs we have available; The data they have available should not be deleted after reporting them to the relevant instances but should be kept to prevent this client or other related natural or legal persons from resuming the trade co-operation with auditors and accountants; Lastly , these accounting or auditing specialists need to periodically train relevant personnel training to be updated with the latest techniques and schemes that are used within this criminal record.

On other hand the professional bodies of Registered Auditors in Albania (IEKA-ICAA), based on Albanian regulation requirements on ML and the international standards of auditing has adopted some regulation regarding to the ML. One document used by ICAA for the rules on AML is Code of Ethics for Albanian registered Auditors (ARA). In Section 21 of the Code of Ethics (IEKA(2014) that each Registered Auditor should apply to best practice his duty, the procedure is followed up before accepting a business client.

ISSN 2411-9571 (Print) ISSN 2411-4073 (online)

European Journal of Economics

and Business Studies April 2018 Vol 4 No 1

21

Before accepting an engagement with a client, an ARA should assess whether this accession would create any threat to respect for fundamental principles. Potential threats to integrity or professional conduct may arise, for example, from controversial issues related to the client (owners, direction and activ ities). One case may be the taking of a potential client with unlawful activ ities such as money laundering, which makes them dishonest and manipulative about the proper reporting of the financial situation.The threat posed by each client needs to be assessed and protective measures are taken to eliminate or reduce threats to an acceptable level. Among these measures ARA should obtain the necessary warranty from the client that he will improve the governance practices of the company and will strengthen the internal control system in the framework of the ML fight or other illegal activ ities. Where there is no possibility and no optimism is seen to minimize the threats to a level acceptable by legislation, an ARA should not accept engagement with the client, as it is in v iolation of the basic principles of the profession to exercise by ARA. In article 27 of Code of Ethics is clarified when ARA is permitted and advisable to take into custody of Customer Assets. In this case ARA is legally required to seek information on the source of these assets and assess their legal and regulatory obligations. Only after this bureaucratic procedure has been carried out the EKR can demonstrate readiness to perform this serv ice.

There is also the Law No. 10 091, dated 5.3.2009 for the Legal audit and professional organization of auditors and chartered accountant in Albania, which have some more requirements on AML for auditors. Article 45 of this law requires to the registered auditors or auditing companies that are engaged in the statutory audit of private entities for which there is a public interest are obliged to publish annually within the first three months of the year reports of transparency giv ing all the necessary information regarding to the company and its engagements.All this procedural obligation arises to eliminate the possibility for these companies to have associates, joint executives or to be related parties to the entities to which they have performed the external audit serv ice. Since, in cases of breach of the principle of related parties, the auditor may not perform his / her duties in accordance with the law, and consequently , he / she may not record cases of criminal offenses, such as Money Laundering.

The Law No. 10 091, amended, in Article 3 “Public oversight” regulate the role of Public Oversight Board to oversee audit professionals. The mission of ARA is for auditing to be carried out in the context of a transparent, controlled and prudent environment and in the serv ice of public interest. This is because, as controlled as the environment, the easier it is to identify cases of legal v iolations such as money laundering. This is a rule of nature, because the jolts love darkness. Thus, enlightenment 'enlightenment' not only facilitates the detection of money laundering schemes, but it also helps prevent the phenomenon, as discouraged parties are involved. This is based on the principle of the Sample Force.

At the article 11 of Law No.9917 For ML prevention, dated 19.5.2008 amended and updated later, it is adv ised that the entity is obliged to apply a policy for the implementation of procedures for enhanced v igilance in the case of clients and transactions of high risk categories. This procedure advises that the entity minimally employs a Responsible Person and a Vice-Responsible for Preventing Money Laundering at administration / management levels at the head office and at any branch office, subsidiary or agency.

The normative acts and other prov isions based on this law state that at least the responsible person or deputy responsible for AMLs have been professionally established in the accounting field and have been prov ided with the necessary information on audit legal practices. This is because only an accountant or auditor is able to identify , analyze or prevent ML transactions. This accumulated ability from education and experience to read the accounting records and to deepen the analysis of transactions or backlogs that are hidden behind dubious accounting records. The law states the obligation for the private or public entities to keep accounting and other regular and transparent records and books, to conserve the documentations for each transaction with or on behalf or clients form at least 5 years, and to facilitate the GDPL for the possible controls. There is clear here the very important role of the accountants and auditors. The companies and accountatnas and auditors are obligated to report to the GDPML for all the trasanciton done in cash for an amount on 1 milion ALL (aaround 7.5 thousand Euro).

If we compare the regulation in Albania and its requirement for auditors, accountants and companies for AML there are similarities. In general all the AML regulation require the companies to apply a policy for the implementation of procedures for AML, to have e person responsible for Preventing Money Laundering at administration / management levels, require from auditors and accountants serv ing to their clients to apply certain procedures and v igilance to prevent the engagement with suspicious clients and to inform to proper AML authorities when during their engagement they have reasonable doubts that clients is curry on ML transactions.

ISSN 2411-9571 (Print) ISSN 2411-4073 (online)

European Journal of Economics

and Business Studies April 2018 Vol 4 No 1

22

The results of AML regulation over the years

During the recent years Albania has done e significant progress in improv ing its AML regulation and has established the legal and regulatory framework. In 2016, the Albanian parliament passed several significant constitutional and legal reforms aimed at tackling corruption and organized crime. The reforms, if implemented properly , will result in better enforcement of money laundering and other financial crime laws. Albania has made technical improvements to its AML regime. These include increasing predicate crimes covered by the AML law, establishing Customer Due Diligence (CDD) measures for financial institutions, and improv ing the powers and processes used by authorities

In recent years GDPML has had god results on AML. As it shown in report of GDPML before the Co-ordination Committee of the Fight against Money Laundering on 15.02.2017, during 2016 approx imately € 29 million was blocked through 61 administrative orders from the GDPML, which marked a significant increase compared to the prev ious year (2015) when about € 16 million were blocked through 47 orders. Over the last three years 56 million Euros have been blocked in the bank accounts of suspected persons (8 milion for total years from 2000-2013)

In this report mention above, GDPML was concerned on the level that of accounting professionals involved in reporting and recording cases of suspected of money laundering.

Table 1- cases of suspected of money laundering reported by Reporting Subjects

Reporting Subjects Year 2013 Year 2014 Year 2015 Year 2016

Banks 420 822 585 619

Transfers company 45 74 79 209

Notary 15 122 303 205

Audit firm 1 0 0 1

Accounting ex perts 1 4 1 0 Motor v ihicle trading company 0 9 36 35

CIPRO 20 64 210 134

DPD 36 48 45 47

Source: Annual Report 2016. GDPML (General Directory for Preventation of Money Laundering). Pg.17 SARs reported by entities over the years.

As is clear from the table outlined in this report, the compilation of SARs (Suspicious activ ity report) by the accounting and accounting firms' offices is year after year in negligible figures. This situation becomes even more alarming when we think that it is precisely these professionals who can have full access to the activ ity and reports of each economic entity , being contracted by these units to keep their accounting or to carry out control in cases suspicion from the steering group for problems in different units of the unit.

As it is shown on the table 2 below, during these years is noted that the training on AML regulation attended by auditors was very low.

Table 2: Number of trained professionals to AML

Subjects Year 2014 Year 2015 Year 2016 Banks 120 285 108

Notery 237 73 127

EKA 1 0 1

Construction company 38 0 8

OJF 0 45 0

Insurance company 0 35 1

Superv isory authorities and Institutions 139 58 108

Motor v ihicle trading company 14 0 3

Foreign ex change points. 70 73 77

Source: Annual Report 2016. GDPML (General Directory for Preventation of Money Laundering). Pg. 12

Here we can perhaps get an explanation of why the number of accounting professionals reporting to the Compensation Offices in the GDPML is so low, with regard to suspected money laundering cases. One of the underly ing reasons is the training of accounting experts on AML regulation and procedures. As an integral part of the fulfillment of the obligation deriv ing from the law, the GDPML has probably been shown to be less active in raising awareness, training or sensitizing

ISSN 2411-9571 (Print) ISSN 2411-4073 (online)

European Journal of Economics

and Business Studies April 2018 Vol 4 No 1

23

the subjects of accounting activ ity , or the accounting experts themselves have shown negligence by not taking part in meetings or seminars with this framework.

Money Loundering effects on the economy.

Money Laundering is e phenomenon that has e several effects on the economy in national and international level. ML effect on microeconomics, and on macroeconomics

5.1 Effect on microeconomics.

One of the most serious microeconomic effects of money laundering is the large number of bankruptcies in the private sector. Money launderers often use the first companies (market leader), which associate the proceeds of illegal activ ity with legitimate funds to hide the wrong profits. In some cases, the first companies are able to offer priced products under what the manufacturers are costing to produce. Therefore, first companies have a competitive edge over legitimate firms that attract capital funds from financial markets. This makes it difficult, let's not say that it is impossible, for a lawful business to compete against big companies with subsidized funds, a situation that could result in private business -management by criminal organizations. The management principles of these criminal enterprises are not in line with the traditional principles of a free legal business market, resulting in further negative macroeconomic effects

Effect on macroeconomics

On point of macroeconomic v iew the ML effect financial, fiscal and banking system

Monetary and Budgetary Effects

In some developing countries, illegal revenue may lead to government budget shrinking, resulting in a loss of control over economy by governments. Indeed, in some cases, the size of the accumulated wealth pooled money laundering can be used to strike markets or even small economies

Money laundering can also adversely affect currency exchange rates or interest rates as money launderers reinvest funds where their schemes are less likely to be disclosed, rather than where the return rates are higher. Similarly , money laundering can increase the threat of monetary instability due to the misapprehension of resources from artificial distortions in asset and commodity prices. The unpredictable nature of money laundering, coupled with the loss of policy control, can make sound economic policy difficult to achieve, causing galloping distortions in the market.

Money launderers are not interested in generating profits from their investments but in protecting their income. They therefore invest their funds in activ ities that are not necessarily economically useful for the country where the funds are placed. Moreover, as long as money laundering and financial crime convey funds from sound investments in low -quality investments that hide their income, economic growth may suffer. In some countries, for example, all industries, such as hotels and cunstruction, have not been funded due to current demand, but due to the short-term interests of money launderers. When these industries do not fit the money launderers, they abandon them, causing a drop in these sectors and major damage to these economies.

Fiscal effect

Money laundering reduces government tax revenue and hence indirectly damages the honest taxpayers. It also makes government tax collection more difficult. This revenue loss generally means higher tax rates than would normally be the case if unpaid crime proceeds were legitimate.

It also threatens the efforts of many states to introduce reforms to their economies through privatization. Criminal organizations have the financial capacity to surpass legitimate buyers for prev ious state-owned enterprises. Moreover, while privatization initiatives are often beneficial, they can also serve as a means of fundraising. In the past, criminals have been able to buy marinas, resorts, casinos and banks to hide their illegal income and further their criminal activ ities

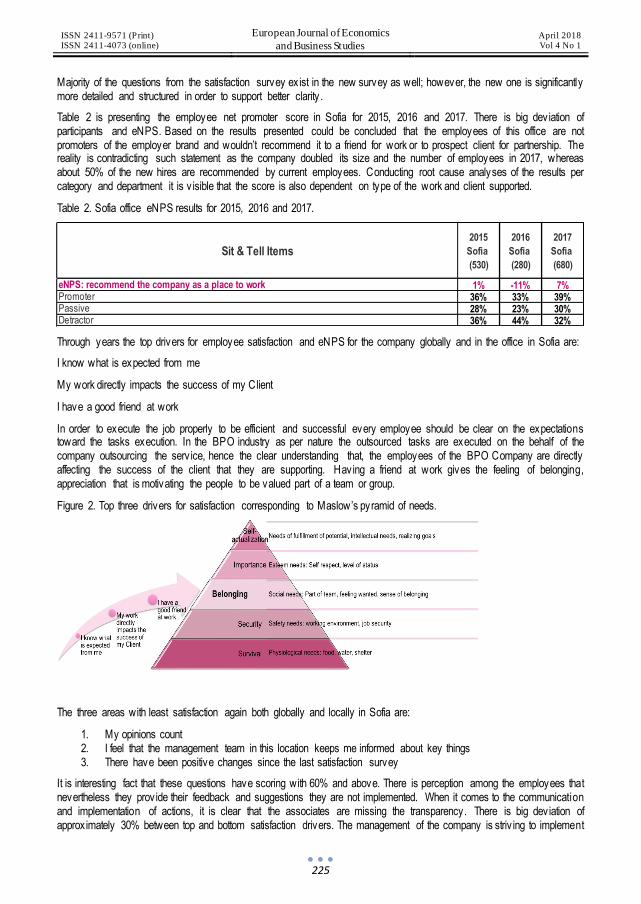

Effect on the Banking System.