![Білий лелека [White Stork] (in Ukrainian)](https://static.fdokumen.com/doc/165x107/63343b8b7a687b71aa089820/bliy-leleka-white-stork-in-ukrainian.jpg)

EU Energy Policies and Ukrainian Crisis of 2014

10

Nikoloz Noniashvili Comparative Economic Systems EU Energy Policies and Geopolitical Consequences Essay To begin with, European Union imports Russia gas around 40% of total gas import and 30% of total oil import, which means that Russian gas and oil are significant sources for EU energy. In case of conflict in Ukraine EU will manage to buy Oil from other suppliers but Gas is very dependent on Russian supply, because Gas needs special transportation infrastructure for pipelines or for liquefied gas, transportation infrastructure for liquefied gas are not enough and well developed to substitute current pipeline natural gas, liquid gas first needs to liquefied in special facilities in exporting countries, then transported through ships and received through special terminals, which are generally expensive, includes transportation cost, needs time to develop and build ships and terminals and would be probably 2 times expensive than current natural gas from Russia. As former UK energy Minister says: American LNG, if and when it eventually arrives in Europe, will be priced at a good deal more than current US domestic levels and will carry $6-9 of transport and processing charges. Current Continental average prices are about $11 per million but (against $16+ in Asia). So LNG will be costlier, quite aside from the large capital costs of constructing new LNG import facilities. Domestic fracking in Europe may help, but is being strongly resisted in several countries and in the UK will take several years to get going - and may prove expensive stuff, both commercially and politically. (Howell 2014) Domestic fracking is now prohibited in France, Netherland and Luxemburg. Most of the imported natural Gas in EU is delivered through pipelines which go through Ukraine (16%) and other transit countries, as he says: In the very short term even the most Russia-reliant EU states can withstand a complete Ukraine cut-off (either as a result of physical damage or Ukrainian diversion of transit meant for EU customers). Only 16% of EU overall annual gas consumption flows through Ukraine (which represents some 50-60% total Russian exports to Europe - down from 75-80% in 2011 with Nordstream opening) (Howell 2014) According to him the most vulnerable countries like Baltic States, East and Central Europe, which depend on Russia the most, could ‘withstand’ complete cut-off from pipelines which goes through Ukraine, but the question is whether they can ‘withstand’ complete cut-off from Russian gas, meaning, if Russia cuts-off gas completely in response of EU’s sanctions for so called ‘annexation of Crimea’. (European Council 2014)

Transcript of EU Energy Policies and Ukrainian Crisis of 2014

Nikoloz Noniashvili

Comparative Economic Systems

EU Energy Policies and Geopolitical Consequences

Essay

To begin with, European Union imports Russia gas around 40% of total gas import and 30% of total oil

import, which means that Russian gas and oil are significant sources for EU energy.

In case of conflict in Ukraine EU will manage to buy Oil from other suppliers but Gas is very dependent on

Russian supply, because Gas needs special transportation infrastructure for pipelines or for liquefied gas,

transportation infrastructure for liquefied gas are not enough and well developed to substitute current

pipeline natural gas, liquid gas first needs to liquefied in special facilities in exporting countries, then

transported through ships and received through special terminals, which are generally expensive, includes

transportation cost, needs time to develop and build ships and terminals and would be probably 2 times

expensive than current natural gas from Russia. As former UK energy Minister says:

American LNG, if and when it eventually arrives in Europe, will be priced at a good deal more than current US domestic

levels and will carry $6-9 of transport and processing charges. Current Continental average prices are about $11 per

million but (against $16+ in Asia). So LNG will be costlier, quite aside from the large capital costs of constructing new LNG

import facilities. Domestic fracking in Europe may help, but is being strongly resisted in several countries and in the UK will

take several years to get going - and may prove expensive stuff, both commercially and politically. (Howell 2014)

Domestic fracking is now prohibited in France, Netherland and Luxemburg. Most of the imported natural

Gas in EU is delivered through pipelines which go through Ukraine (16%) and other transit countries, as he

says:

In the very short term even the most Russia-reliant EU states can withstand a complete Ukraine cut-off (either as a result

of physical damage or Ukrainian diversion of transit meant for EU customers). Only 16% of EU overall annual gas

consumption flows through Ukraine (which represents some 50-60% total Russian exports to Europe - down from 75-80%

in 2011 with Nordstream opening) (Howell 2014)

According to him the most vulnerable countries like Baltic States, East and Central Europe, which depend on

Russia the most, could ‘withstand’ complete cut-off from pipelines which goes through Ukraine, but the

question is whether they can ‘withstand’ complete cut-off from Russian gas, meaning, if Russia cuts-off gas

completely in response of EU’s sanctions for so called ‘annexation of Crimea’. (European Council 2014)

These sanctions (according to European Council meeting in May 2014) include (a) individual Visa ban on

certain individuals, (b) asset freeze on certain companies and individuals and (c) cancelled of the next EU-

Russia summit. (European Council 2014)

According to Lord Howell financial sanctions “can cause Russia real pain,” but it is not possible to solve

Ukraine and gas problem without Russia’s cooperation. Therefore EU has to carefully choose what it is

doing. (Howell 2014) Many European countries called Russia’s annexation of Crimea ‘illegal action’.

(European Council 2014)

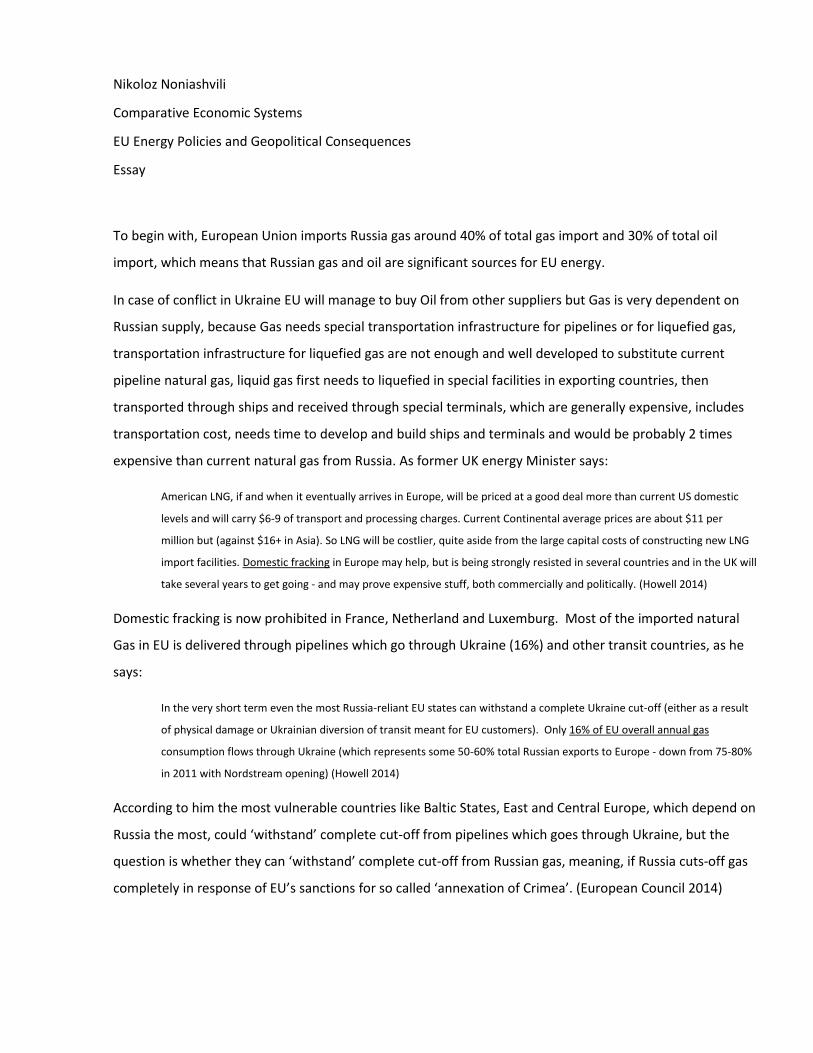

This graph shows current gas supplied by Russia published on Economist.

FIGURE 1: GAS SUPPLIED BY RUSSIA, 2012

SOURCE 1 THE ECONOMIST 2014

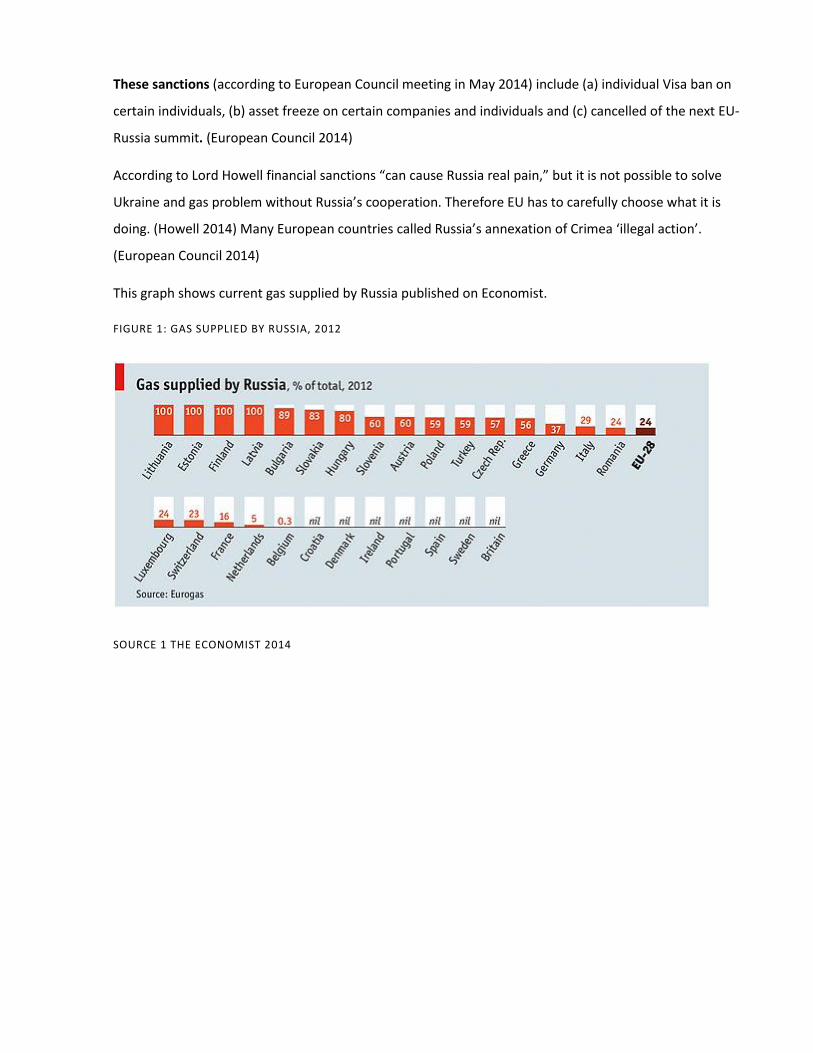

And this is the Preventive Action Plan (PAP) developed by European Commission to decrease energy

dependency.

FIGURE 2: SUPPLY-SIDE PREVENTIVE ACTION PLAN (PAP)

SOURCE 2: EUROPEAN COMMISSION STAFF WORKING DOCUMENT (2014)

This chart shows Supply-side measures proposed by EU Commission in case of problems on gas supply.

Commission says that the most of the preventive measures are related to infrastructure (building and

improving both domestic and transit country energy infrastructure) and significant attention is paid on

building new infrastructure to bring gas from Caspian basin, Middle-east and even from North Americas.

(European Commission 2014)

European Council said in March 2014, that EU has to “reduce energy dependency” and increase “bargaining

power and energy efficiency” in Europe (European Council 2014). Possible interpretation of this statement

is that EU cannot criticize Russia very much over Ukraine, due to energy dependency, and now she is trying

to get rid-of dependency to make strong action against Russia in near future for similar occasions, which is

contrary to EU’s basic argument for integration (Coal and Steel Community, European Union) that

interdependent economies decreases chances of War, which has been the case for Europe for decades.

Energy is a strategic resource, which EU imports mostly from Russia and other countries, and perhaps this

dependency decreases chances of conflict between EU and Russian Federations. But if EU is trying to find

diversification of supply and other energy sources perhaps this will make EU bolder to make decisive steps

in Ukrainian conflict.

According to EU Commission, EU imports most of its energy resources from ‘third countries’. Figure 3,

shows total EU energy imports.

FIGURE 3: EU TOTAL ENERGY IMPORTS (2012)

SOURCE 3: EUROPEAN COMMISSION, QUESTIONS AND ANSWERS ON ENERGY SECURITY, MEMO (2014)

According to the British Petroleum by 2035 81% of world energy supply would be of fossil fuel, (Howell

2014) Lord Howell says if EU wants to permanently

Gas

Cru

de

Oil

Solid

Fu

el

Ura

niu

m

Ren

ewab

les

95%

88%

66%

42%

4%

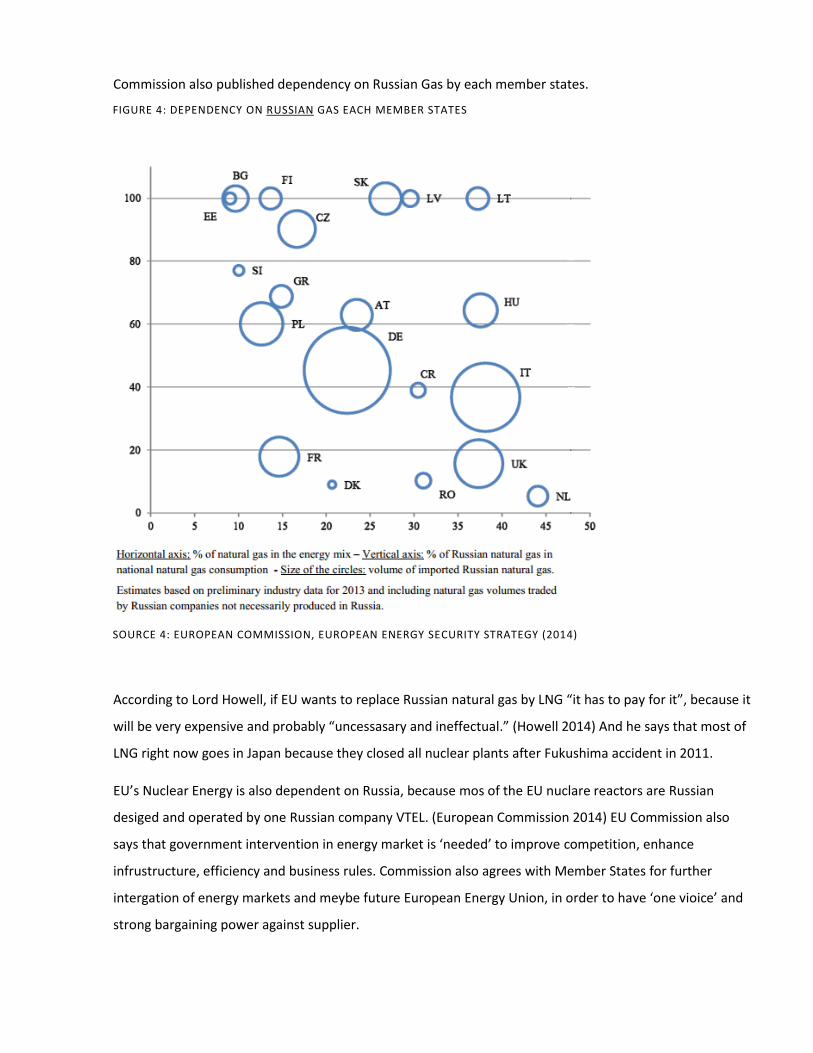

Commission also published dependency on Russian Gas by each member states.

According to Lord Howell, if EU wants to replace Russian natural gas by LNG “it has to pay for it”, because it

will be very expensive and probably “uncessasary and ineffectual.” (Howell 2014) And he says that most of

LNG right now goes in Japan because they closed all nuclear plants after Fukushima accident in 2011.

EU’s Nuclear Energy is also dependent on Russia, because mos of the EU nuclare reactors are Russian

desiged and operated by one Russian company VTEL. (European Commission 2014) EU Commission also

says that government intervention in energy market is ‘needed’ to improve competition, enhance

infrustructure, efficiency and business rules. Commission also agrees with Member States for further

intergation of energy markets and meybe future European Energy Union, in order to have ‘one vioice’ and

strong bargaining power against supplier.

FIGURE 4: DEPENDENCY ON RUSSIAN GAS EACH MEMBER STATES

SOURCE 4: EUROPEAN COMMISSION, EUROPEAN ENERGY SECURITY STRATEGY (2014)

Internal Energy Market, IEM

EU Internal Energy Market is a single market of all member states for one voice of the Union in negotiations

and dealing with the energy suppliers. The current situation is ‘self-sufficiency mind-set that most countries

still retain’ (Booz&Co. 2013) in the Union, and states deal individually to the major supplier like Russia that

decreases security dimensions of the European Union and the policies of the Union seek to diversify

suppliers so that Union could rely on various sources and the security concerns of the Europe would be

reduced.

The IEM is thought to be beneficial for consumers as well. The Diversification will bring more companies and

increases competition; and when the competition will be increased, companies will try to provide energy at

lower prices due to competition. Renewable energy industry includes development of Solar, Wind and Bio

fuels, which can potentially reduce energy dependency on fossil fuel in the future.

FIGURE 5: ENERGY DEMAND EU28

SOURCE 5: EUROPEAN COMMISSION, IN-DEPTH STUDY OF EU ENERGY SECURITY 2014

This can also decrease emission of harmful substances such as carbon dioxide into the nature that is part of

environmental issues and climate change. The fossil fuel consumption at household level is around 70%, and

EU looks forward to generate renewable energy to decrease dependency on fossil fuel. Moreover, fossil fuel

is imported and if EU develops local renewable energy market this will decrease trade deficit. Advantage of

the renewable energy is that it has low impact on environment, could be developed locally and will

potentially make EU self-sufficient in the future if the adequate infrastructure would be built.

The IEM Policy of the European Union identifies three goals to be accomplished (1) competitiveness, (2)

sustainability and (3) security of supply. (Council of European Energy Regulators 2013) Competitiveness will

be reached by integration of nations’ energy markets into a single EU energy market and by bringing more

business players. For this purpose EU adopted policies and projects for building infrastructure networks all

over the Europe for transmitting energy effectively to the various markets. (European Commission 2015)

This will foster competitions among suppliers and encourage price cuts and demand side responses as more

suppliers would be available and the consumers would have more opportunity to switch between suppliers

based on the best price offer.

According to energy study prepared for the EU Commission, further integration and liberalization of

electricity markets can bring 10-16 billion benefit per year by 2015 and 30 billion per year for the gas

market. (Booz&Co. 2013) However, according to the study market integration can occur only if there would

be “sufficient infrastructure between markets” and also proper “regulatory and political conditions to foster

trade.” Truly integrated energy market can reduce dependency on a single supplier and improve “market’s

security of supply.” (Booz&Co. 2013)

To avoid monopoly prices and security dilemmas, and the dependency on Russian gas, EU turns to

alternative ways for bringing gas in Europe. EU Commission is discussing probability of importing gas from

Africa and Caspian Sea. Caspian Sea gas belongs to Azerbaijan where EU Commission President Mr. Barroso

and President of the European Council signed Memorandum with President of Azerbaijan Ilham Aliyev in

2013 on cooperation and partnership on supplying gas from Shah Deniz fields. The major shareholders of

the Shah Deniz consortium are British Petroleum, PB (28.8 %) and State Oil Company of Azerbaijan Republic

SOCAR (16.5%) and Norwegian Statoil ASA (15.5%). (British Petrolium 2015) It is interesting how BP invested

more than rest.

EU Energy Commissioner Gunther said that “the corridor will have potential to meet up to 20% of the EU’s

gas needs in the long term.” (European Commission 2013) The sales agreements have already been signed

and the initial investments have been made to extract gas from Caspian Sea and deliver to Europe via

Turkey by 2020.

The EU Commission is also studies other projects to link EU energy market with Middle East and African

suppliers and bring more business partners to the European Market. The official European Commission web

site says that the aims of EU is to “fully integrate national energy markets to give consumers and business

more and better products and services, more competition and more security supplies”. (European

Commission 2015) Union also tries to creation a new innovative technology for renewable energy, but

unfortunately there is no renewable energy infrastructure in the EU capable of supplying full energy

demand. By 2020 Union plans to have around 20% domestic supply of renewable energy and 20% supply of

natural gas from Caspian Sea, currently EU’s 40% gas comes from Russia.

Russia is often seen as an unpredictable business partner who can cut supplies at any time for the political

reasons. Examples are rampant, such as Ukraine gas disputes and cut offs in 2005-6 and 2008-9, Russia –

Belarus energy dispute in 2007, Baltic States in early 90s where Russian intention was to affect states’ policy

changes, (Wikipedia 2015) and Georgian –Russian disputes in 2003, where gas supply usually interrupts on

special occasions elections or bilateral negotiations. (Larsson 2007)

These examples I think are the basic arguments for the EU to seek alternative sources of energy supplies,

and in the future invest in domestic infrastructure to enhance renewable energy generation to be more self-

sufficient and decrease foreign energy reliance.

Sustainability is the second goal of the Internal Energy Market policy, which can potentially decrease

demand on fossil fuel in near future by renewable energy. Goal is to invest locally to build houses with solar

energy generators on top, wind energy plants in windy regions of the North and bio energy fuel plants in

central and Eastern Europe. The Concerto initiative was designed within the European Research Framework

Program to respond to the energy consumption by household buildings, because 40% of total energy is

consumed by residential buildings. (Concerto 2014) This initiative holds that each residential district should

have its access to the solar or wind energy plant in their neighborhood, which can provide energy locally to

domestic customers. The Concerto Project also says that the old building could be updated to meet new

energy requirements, such as upgrading windows, roof, walls, etc. (Concerto 2014)

As I noted above the major challenge for the IEM is that there is not enough physical connectivity of gas and

electricity markets to ensure efficient allocation of resources. That is to say, that there is not enough gas

pipeline and electricity networks across the continent to ensure effective allocation of resources.

Consequently customers are reluctant to choose their gas or electricity supplier, and they are mostly relied

on long term contracts with limited number of suppliers. Therefore, EU Commission has adopted new 248

energy infrastructure projects to build trans-European infrastructure for diversification and better access of

various market. (European Commission 2015) According to the Commission report in 2013, a full integration

of electricity markets could bring up to 40 billion annual cost savings. Commission also recognizes public

intervention in energy market as ‘necessity to correct market failures’ (European Commission 2013) but the

Guidance on Public Interventions says that the government shall not compensate loses or bed investment

decisions of the companies in the energy market. (Ibid) Document also says that the “energy markets,

renewables markets, and capacity markets need to be truly international if cost savings are to be achieved,”

government intervention should be minimized to allow price mechanism work better for energy allocations.

If there would be a truly integrated market, power will flow from one market to the other if the prices in a

neighboring country would be higher, and conversely power will be imported if the domestic prices would

be higher. (Ibid)

Booze and Co. report for the Commission on the “Benefits of an Integrated European Energy Market” -

show that in electricity price volatility among France and Netherlands before integration was within EUR 1

/MWH for 10% of the time and EUR 10 for 39% of the time. After integration price remained within EUR 1

for 72% of the time and was more than EUR 10 only 14% of the time. (Booz&Co. 2013) This example shows

how price decreased after-market integrations among France and Netherlands and similar benefits can be

for other EU states.

Finally, communitarization EU energy market is on its way toward integration and will bring its benefits after

full integration. EU Commission has already assessed the benefits of single energy market, and now sets

goals to achieve it, there is no question whether it is necessary or brings enough benefits, but the issue is

when and how EU will represent Member states as a single voice at the international market for energy

procurement.

I think EU has already started communitarization process and there will be no concern whether it should be

implemented or not, as I noted above, each Member States are more obsessed with national energy supply

security, and sometimes do not take into account the EU interests. This individual approach gives Russia

advantage to negotiate individual prices for each Member State and sometimes sets monopoly prices as few

EU countries can diversify.

For the conclusion, communitarization will give EU a single voice over negotiation with Russia and other

energy suppliers, it will also improve efficiency and infrastructure, which in the future will bring more self-

sufficiency, but this is by and by. Currently EU Commission is looking for diversification of gas suppliers in

the light of Ukrainian Crisis, which is a national security issue as well and EU has a “wake up call” to better

organize their energy policies .

Works Cited Booz&Co. Benefits of an Integrated European Energy Market. Study, Amsterdam: Booz&Co., 2013.

British Petrolium. Shah Deniz. 1 5, 2015. http://www.bp.com/en_az/caspian/operationsprojects/Shahdeniz.html (accessed 1 5, 2015).

Concerto. The CONCERTO initiative. July 14, 2014. http://www.concerto.eu/concerto/about-concerto.html (accessed 1 10, 2015).

Council of European Energy Regulators. Annual Report. CEER, 2013.

European Commission. Energy Infrastructure, Projects of Common Interests (PCI). 1 5, 2015. http://ec.europa.eu/energy/infrastructure/pci/pci_en.htm (accessed 1 5, 2015).

European Commission. Gas from Azerbaijan: Commission welcomes final investment decision to extract gas pledged for Europe . Press Release, Brussels: EU Commission, 2013.

European Commission. Generation Adequacy in the internal - Guidance on Public Interventino. Working Document, Brussels: EU Commission, 2013.

European Commission. In-depth study of European Energy Security. Commission Staff Working Document, Brussels: EU Commission, 2014.

—. Single market for gas & electricity. 1 5, 2015. http://ec.europa.eu/energy/gas_electricity/index_en.htm (accessed 1 5, 2015).

European Council. Conclusions of European Council March 2014. Council Conclusions, Brussels: General Secretariat of the Council, 2014.

Howell, Lord. "Russian Gas is the Realistic Option for Europe." Journal of Energy Security, 2014.

Larsson, Robert L. Nord Stream, Sweden and Baltic Sea Security. Base date report, Stockholm: Swedish Defence Reasearch Agency, 2007.

The Economist. "Conscious uncoupling." Economist, 2014.

Wikipedia. Russia in the European energy sector. 1 5, 2015. http://en.wikipedia.org/wiki/Russia_in_the_European_energy_sector#cite_note-balticseasecurity-40 (accessed 1 5, 2015).

Appendix:

Shal Gas basins in Europe (Source: The Economist 2014)