Acctg policies

49

Accounting Policies and Procedures

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of Acctg policies

Accounting Policies andProcedures

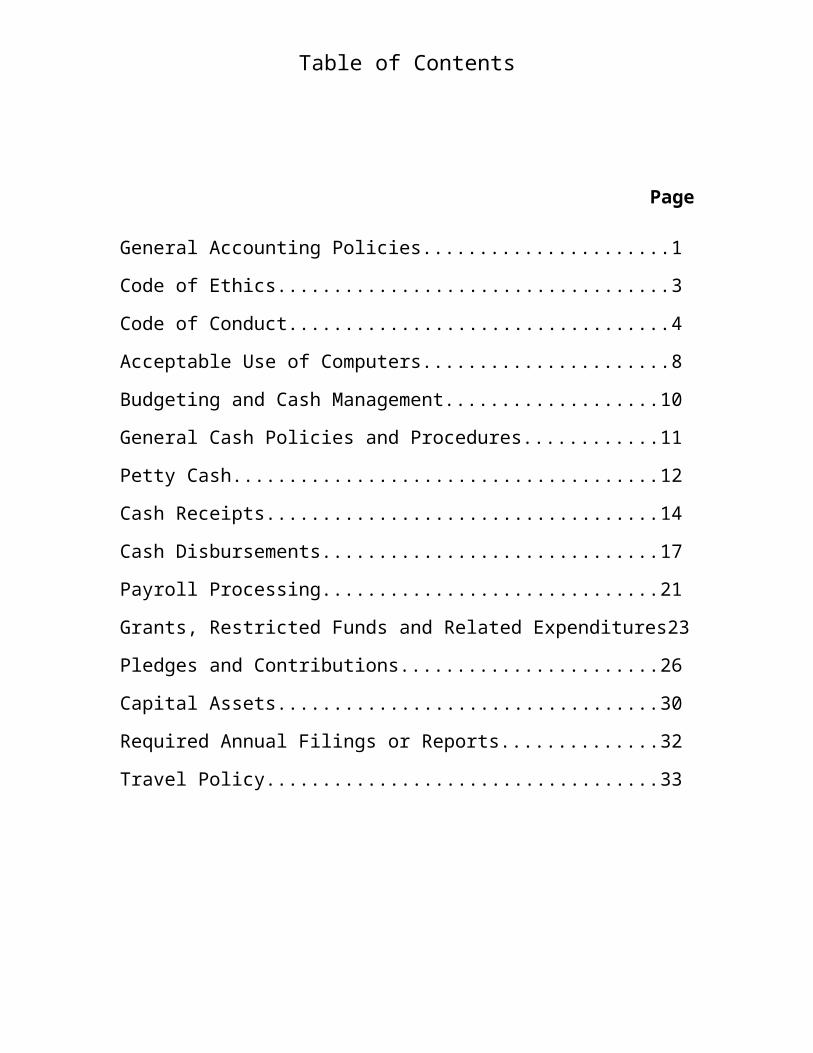

Table of Contents

Page

General Accounting Policies......................1

Code of Ethics...................................3

Code of Conduct..................................4

Acceptable Use of Computers......................8

Budgeting and Cash Management...................10

General Cash Policies and Procedures............11

Petty Cash......................................12

Cash Receipts...................................14

Cash Disbursements..............................17

Payroll Processing..............................21

Grants, Restricted Funds and Related Expenditures23

Pledges and Contributions.......................26

Capital Assets..................................30

Required Annual Filings or Reports..............32

Travel Policy...................................33

Table of Contents

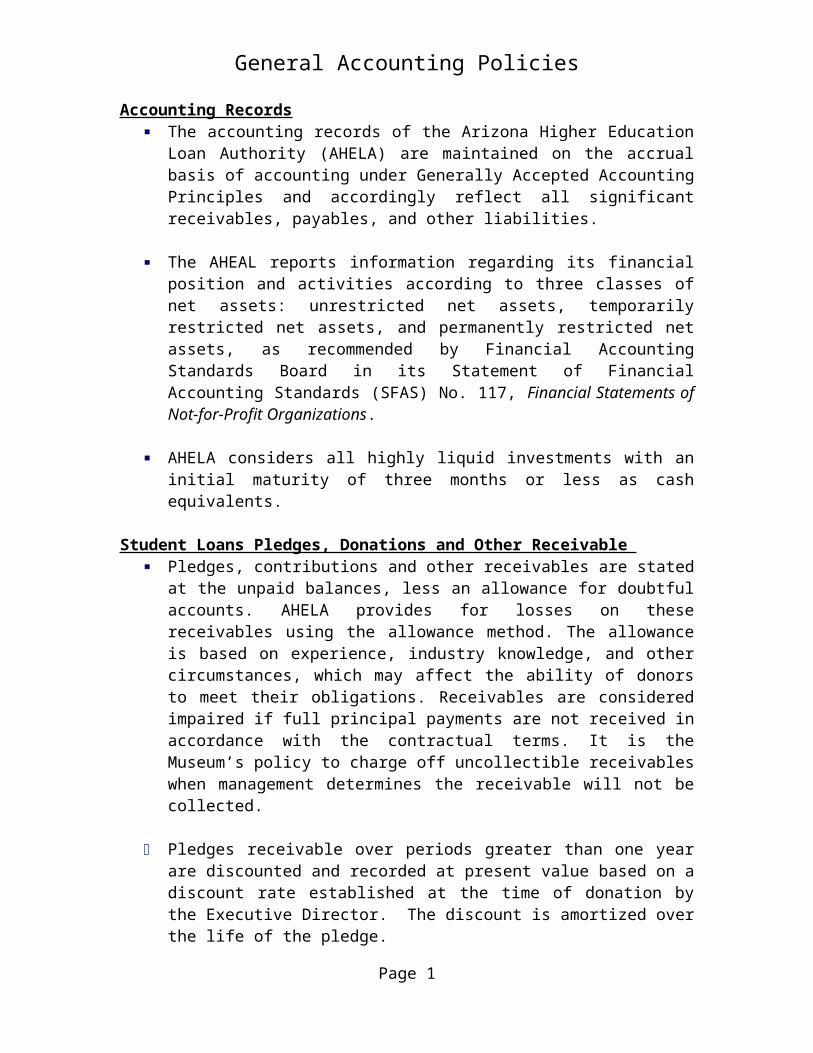

General Accounting Policies

Accounting Records The accounting records of the Arizona Higher Education

Loan Authority (AHELA) are maintained on the accrualbasis of accounting under Generally Accepted AccountingPrinciples and accordingly reflect all significantreceivables, payables, and other liabilities.

The AHEAL reports information regarding its financialposition and activities according to three classes ofnet assets: unrestricted net assets, temporarilyrestricted net assets, and permanently restricted netassets, as recommended by Financial AccountingStandards Board in its Statement of FinancialAccounting Standards (SFAS) No. 117, Financial Statements ofNot-for-Profit Organizations.

AHELA considers all highly liquid investments with aninitial maturity of three months or less as cashequivalents.

Student Loans Pledges, Donations and Other Receivable Pledges, contributions and other receivables are stated

at the unpaid balances, less an allowance for doubtfulaccounts. AHELA provides for losses on thesereceivables using the allowance method. The allowanceis based on experience, industry knowledge, and othercircumstances, which may affect the ability of donorsto meet their obligations. Receivables are consideredimpaired if full principal payments are not received inaccordance with the contractual terms. It is theMuseum’s policy to charge off uncollectible receivableswhen management determines the receivable will not becollected.

Pledges receivable over periods greater than one yearare discounted and recorded at present value based on adiscount rate established at the time of donation bythe Executive Director. The discount is amortized overthe life of the pledge.

Page 1

General Accounting Policies

Donated marketable securities and other noncashdonations are recorded as contributions at theirestimated fair values at the date of donation. Unlessotherwise directed by the Board of Directors, theMuseum will sell any donated marketable securities assoon as practical.

Donations are reported as increases in unrestricted netassets unless the donor has restricted the donation toa specific purpose. Assets donated with explicitrestrictions regarding their use and contributions ofcash that must be used to acquire property andequipment are reported as restricted contributions.Absent donor stipulations regarding how long thosedonated assets must be maintained, the Museum reportsexpirations of donor restrictions when the donated oracquired assets are placed in service as instructed bythe donor. The Museum reclassifies temporarilyrestricted net assets to unrestricted net assets atthat time.

Contributions that are restricted by the donor arereported as increases in unrestricted net assets if therestrictions expire (that is, when a stipulated timerestriction ends or purpose restriction isaccomplished) in the reporting period in which therevenue is recognized. The reporting period is theMuseum’s fiscal year beginning September 1 and endingAugust 31. All other donor-restricted contributionsare reported as increases in temporarily or permanentlyrestricted net assets, depending on the nature of therestrictions. When a restriction expires, temporarilyrestricted net assets are reclassified to unrestrictednet assets and reported in the Statement of Activitiesas net assets released from restrictions.

Page 2

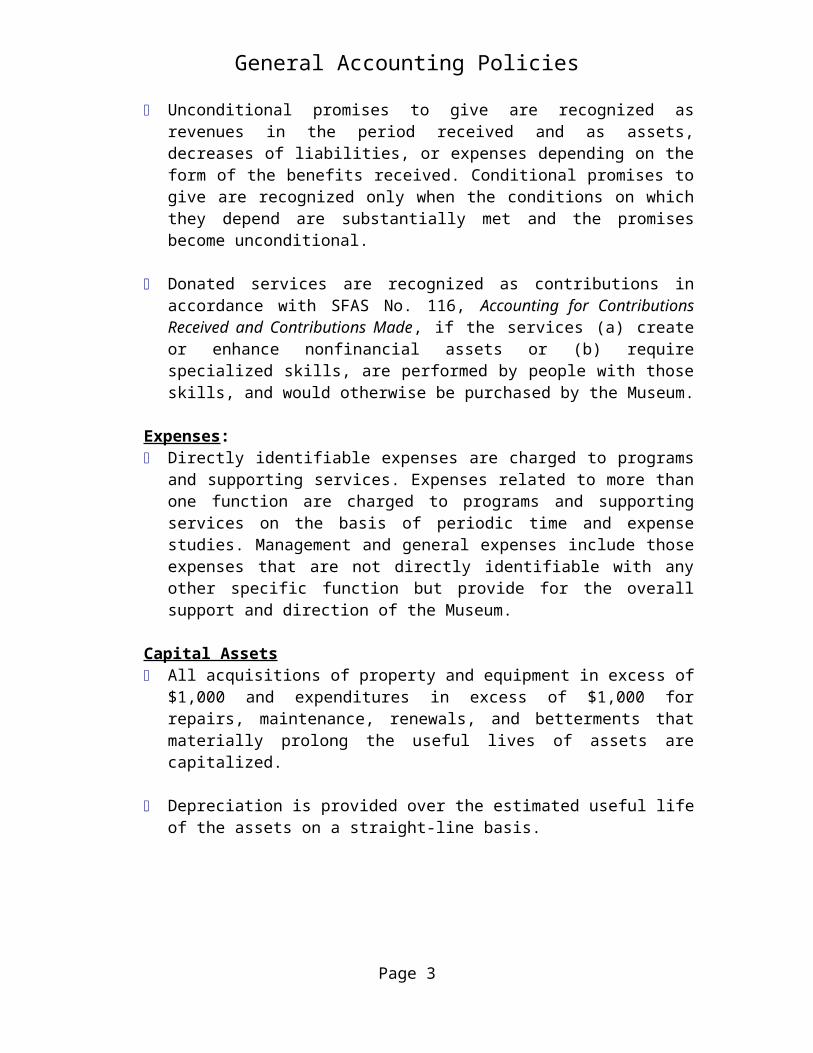

General Accounting Policies

Unconditional promises to give are recognized asrevenues in the period received and as assets,decreases of liabilities, or expenses depending on theform of the benefits received. Conditional promises togive are recognized only when the conditions on whichthey depend are substantially met and the promisesbecome unconditional.

Donated services are recognized as contributions inaccordance with SFAS No. 116, Accounting for ContributionsReceived and Contributions Made, if the services (a) createor enhance nonfinancial assets or (b) requirespecialized skills, are performed by people with thoseskills, and would otherwise be purchased by the Museum.

Expenses: Directly identifiable expenses are charged to programs

and supporting services. Expenses related to more thanone function are charged to programs and supportingservices on the basis of periodic time and expensestudies. Management and general expenses include thoseexpenses that are not directly identifiable with anyother specific function but provide for the overallsupport and direction of the Museum.

Capital Assets All acquisitions of property and equipment in excess of

$1,000 and expenditures in excess of $1,000 forrepairs, maintenance, renewals, and betterments thatmaterially prolong the useful lives of assets arecapitalized.

Depreciation is provided over the estimated useful lifeof the assets on a straight-line basis.

Page 3

Code of Ethics

The employees and Board of Directors of the Phoenix FamilyMuseum will:

Act with honesty and integrity, avoiding actual orapparent conflicts of interest in personal andprofessional relationships.

Provide information that is accurate, complete,objective, relevant, timely and understandable.

Comply with rules and regulations of federal, state,local governments and other appropriate private andpublic regulatory agencies.

Act in good faith; responsibly; and with due care,competence, and diligence, without misrepresentingmaterial facts or allowing one’s independent judgmentto be subordinated.

Respect the confidentiality of information acquired inthe course of one’s work except when authorized orotherwise legally obligated to disclose. Confidentialinformation acquired in the course of one’s work willnot be used for personal advantage.

Share knowledge and maintain skills important andrelevant to other Museum employee’s and director’sneeds.

Proactively promote ethical behavior as a responsiblepartner among peers, in the work environment, and inthe community.

Achieve responsible use of and control over all assetsand resources employed or entrusted.

Page 4

Code of Conduct

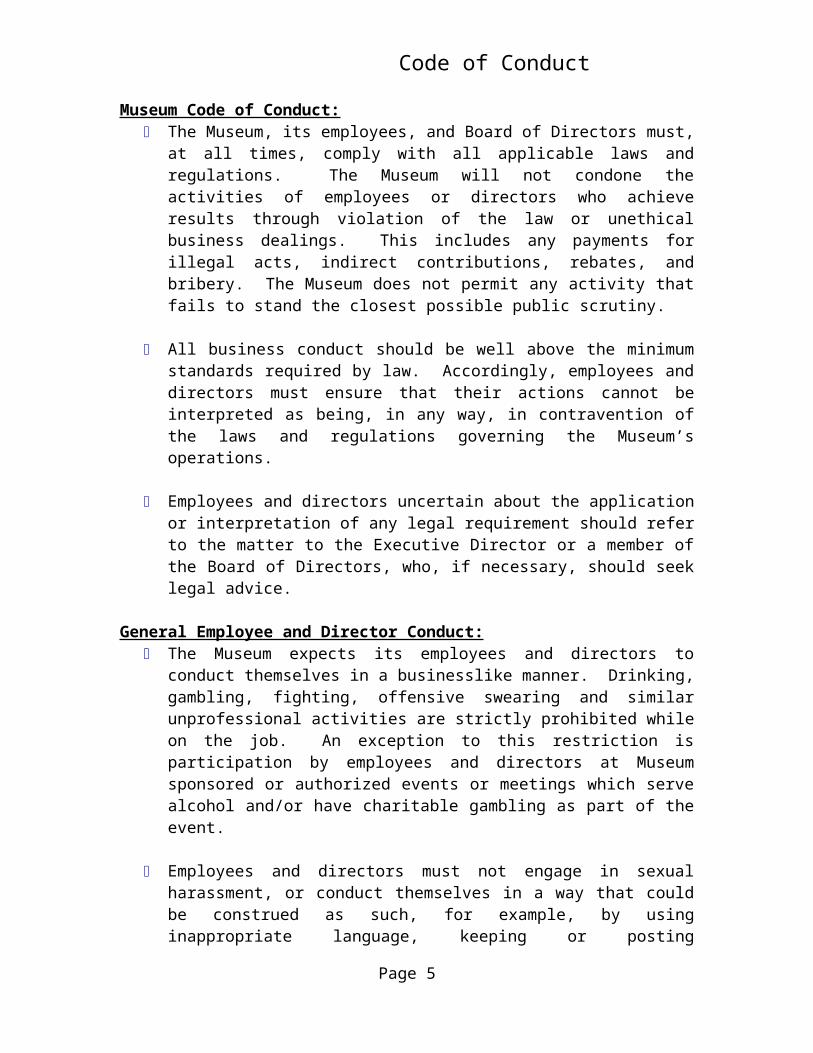

Museum Code of Conduct: The Museum, its employees, and Board of Directors must,

at all times, comply with all applicable laws andregulations. The Museum will not condone theactivities of employees or directors who achieveresults through violation of the law or unethicalbusiness dealings. This includes any payments forillegal acts, indirect contributions, rebates, andbribery. The Museum does not permit any activity thatfails to stand the closest possible public scrutiny.

All business conduct should be well above the minimumstandards required by law. Accordingly, employees anddirectors must ensure that their actions cannot beinterpreted as being, in any way, in contravention ofthe laws and regulations governing the Museum’soperations.

Employees and directors uncertain about the applicationor interpretation of any legal requirement should referto the matter to the Executive Director or a member ofthe Board of Directors, who, if necessary, should seeklegal advice.

General Employee and Director Conduct: The Museum expects its employees and directors to

conduct themselves in a businesslike manner. Drinking,gambling, fighting, offensive swearing and similarunprofessional activities are strictly prohibited whileon the job. An exception to this restriction isparticipation by employees and directors at Museumsponsored or authorized events or meetings which servealcohol and/or have charitable gambling as part of theevent.

Employees and directors must not engage in sexualharassment, or conduct themselves in a way that couldbe construed as such, for example, by usinginappropriate language, keeping or posting

Page 5

Code of Conduct

inappropriate materials in their work area, oraccessing inappropriate materials on their computer.

Conflicts of Interest: The Museum expects that employees and directors will

perform their duties conscientiously, honestly, and inaccordance with the best interests of the Museum.Employees and directors must not use their position orthe knowledge gained as a result of their position forprivate or personal advantage. Regardless of thecircumstances, if employees or directors sense that acourse of action they have pursued, are presentlypursuing, or contemplating pursing may involve them ina conflict of interest with the Museum, they shouldimmediately communicate all of facts to the ExecutiveDirector or a member of the Board of Directors.

Outside Activities, Employment and Directorships: All employees and directors share serious

responsibility for the Museum’s good public relations,especially at the community level. Their readiness tohelp with religious, charitable, educational, and civicactivities brings credit to the Museum and isencouraged. Employees and directors must, however,avoid acquiring any business interest or participatingin any other activity outside the Museum that would, orappear to:

Create an excessive demand upon their time andattention, thus depriving the Museum of their bestefforts.

Create a conflict of interest – an obligation,interest, or distraction – that may interfere with

Page 6

Code of Conduct

the independent exercise of judgment in theMuseum’s best interest.

Relationships with Contributors, Clients, and Suppliers: Employees and directors should avoid investing in or

acquiring a financial interest for their own benefit inany business organization that has a contractualrelationship with the Museum, or that provides goods orservices, or both to the Museum, if such investment orinterest could influence or create the impression ofinfluencing their decisions in the performance of theirduties on behalf of the Museum. This is not to preventrelationships with contributors, clients, or suppliesthat are beneficial to the Museum, but all suchrelationships should be fully disclosed to theExecutive Director and the Board of Directors.

Gifts, Entertainment, and Favors: Employees and directors must not accept entertainment,

gifts, or personal favors that could influence, orappear to influence, business decisions in favor of anyperson or organization. This includes people ororganizations that currently, or are likely to, havebusiness dealings with the Museum.

Kickbacks and Secret Commissions:

Regarding the Museum’s activities, employees anddirectors may not receive payment or compensation ofany kind, except as authorized under the Museum’sremuneration policies. In particular, the Museumstrictly prohibits the acceptance of kickbacks andsecret commissions from suppliers or others. Anybreach of this rule will result in immediatetermination and prosecution to the fullest extent ofthe law.

Museum Funds and Other Assets: Employees and directors who have access to Museum funds

in any form must follow the prescribed procedures for

Page 7

Code of Conduct

recording, handling and protecting these funds asdetailed in the Museum’s Policies and Procedures orother explanatory materials. The Museum imposes strictstandards to prevent fraud and dishonesty. Ifemployees or directors become aware of any evidence offraud and/or dishonesty, they should immediately advisethe Executive Director or a member of the Board ofDirectors so that the Museum can promptly investigatefurther.

When an employee’s or director’s position requiresspending Museum funds or incurring any reimbursablepersonal expenses, that individual must use goodjudgment on the Museum’s behalf to ensure that goodvalue is received for all expenditures.

Museum funds and all other assets of the Museum are forMuseum purposes only and not for personal benefit.This includes the personal use of organizationalassets, such as computers.

Museum Records and Communications:

Accurate and reliable records of many kinds arenecessary to meet the Museum’s legal and financialobligations and to manage the affairs of the Museum.The Museum’s books and records must reflect in anaccurate and timely manner all business transactions.The employees and directors responsible for accountingand record keeping must fully disclose and records allassets, liabilities, or both, and must exercisediligence in enforcing these requirements.

Employees must not make or engage in any false recordor communication of any kind, whether internal orexternal, including but not limited to:

False expense, attendance, production, financial,or similar reports and statements.

False advertising, deceptive marketing practices,or other misleading representations.

Page 8

Code of Conduct

Prompt Communications: In all matters relevant to donors, suppliers,

government authorities, the public and others regardingthe Museum, all employees and directors must make everyeffort to achieve complete, accurate and timelycommunications – responding promptly and courteously toall proper requests for information and to allcomplaints.

Privacy and Confidentiality: When handling financial and personal information about

donors, grantors, customers, suppliers or others withwhom the Museum has dealings, observe the followingprinciples:

Collect, use, and retain only the personalinformation necessary for the Museum’s business.When ever possible, obtain any relevantinformation directly from the person concerned.Use only reputable and reliable sources tosupplement this information.

Retain information only for as long as necessaryor as required by law. Protect the physicalsecurity of this information.

Limit internal access to personal information tothose with a legitimate business reason forseeking that information. Use personalinformation only for the purposes for which it wasoriginally obtained. Obtain the consent of theperson concerned before externally disclosing anypersonal information, unless legal process orcontractual obligations provides otherwise.

Page 9

Code of Conduct

Page 10

Acceptable Use of Computers

The polices for use of the Museum’s computers are asfollows:

The Executive Director, or other employee designated bythe Executive Director, is in charge of InformationTechnology for the Museum.

Use of the Museum’s computers is limited to businessuse to limit exposure of the system to threats andviruses.

Employees may not display inappropriate images orwords, such as sexually explicit materials, ethnicslurs or racial epithets, or retain such information ontheir computers.

Employees may not access Internet games, radios, moviesand other forms of electronic entertainment as theseuse considerable bandwidth and may contain spyware andadware.

Only software licensed by the Museum may be installedand used on the Museum’s computers. Installation mayonly be performed by personnel or suppliers authorizedby the Executive Director.

Employees are advised that no electronic information isprivate and all information on the Museum’s computers,or accessed through the computers, is available to theMuseum’s management and under court order.

Instant messenger services are prohibited as anunnecessary security risk that may carry viruses.

The Executive Director, or an employee designated bythe Executive Director, must authorize who can serviceor work on computers and who can purchase computersoftware and hardware.

Page 11

Acceptable Use of Computers

The Museum’s computer system must perform a dailyupdate of antivirus software. This can be accomplishedautomatically or by an employee designated by theExecutive Director performing the daily task.

Employees are restricted from changing computersettings or overriding security features.

Employees will not sign up for junk or group e-mailswith permission from the Executive Director. Thispermission may be given for the type of allowable groupe-mail and does not need to be provided on anindividual sign-up basis.

Employees may not connect with the Museum’s computersystem from a remote location without prior approval ofthe Executive Director.

Employees must use computers is limited to legalactivities and use only.

Employees may not store private or personal informationon Museum computers.

Page 12

Budgeting and Cash Management

Control Objective: To provide a tool to assist management in meeting shortrange operational goals, long range capital goals, and plansfor specific projects or programs. Cash managementprocedures are integral to the budgeting process.

Responsible Parties:Executive Director and Board of Directors, or theirauthorized committee – prepare an annual Museum budget andbudgets for identified projects or fundraising events.

Procedures: The Executive Director and the Board of Directors, or

their designated committee, are responsible forpreparing and adopting an annual budget by_______________ of each year. Revisions to this budgetgreater than 10% for an individual expense require theapproval of the Board of Directors, or their designatedcommittee.

Develop written guidelines for the preparation ofbudgets for the Museum as a whole, individualdepartments or areas, and specific projects.

The Executive Director and the Board of Directors usethe budgets as an analytical tool to compare actualresults to budgeted expectations. Significantdifferences should be explained.

Cash Management Procedures: The Executive Director and Board of Directors, or their

designated committee, will establish an investment andspending policy (see policy at _____________).

Page 13

General Cash Policies andProcedures

Control Objective: To ensure cash is properly safeguarded, deposited to thebank timely, disbursements are properly authorized andcontrolled, and cash transactions are recorded accuratelyand timely in the accounting records.

Responsible Parties:See employees designated in the cash receipts or cashdisbursements procedures.

Procedures: All responsible parties are required to take vacations.

During these vacations, the Executive Director or otherassigned staff person will perform all aspects of thevacationing employee’s job. If a part-time employeedoes not receive and take vacation time, the ExecutiveDirector or other assigned staff person willperiodically perform all aspects of the job as a crosstraining exercise.

Bank statement reconciliations are performed timelywithin two weeks of receiving the bank statements. Allunopened bank statements will be given to the outsideaccountant for reconciliation. The following arecompleted in conjunction with the bank statementreconciliation:

Comparison of deposit dates and amounts in theaccounting records to the dates and amounts on thebank statement.

Review of bank transfers between accounts todetermine that both bank account transactions wereproperly posted.

Investigation of items rejected by the bank, forexample, deposited checks or collection items

Page 14

General Cash Policies andProcedures

charged back by the bank because of insufficientfunds.

Comparison of checks numbers, dates, payees, andamounts to the information recorded in theaccounting records.

Check number sequences are reviewed and anymissing check numbers are investigated.

Review of canceled checks for authorizedsignatures.

Review of canceled checks for irregularendorsements.

Checks outstanding over 60 days are researched andstop payments are issued after 90 days.

Review and reconciliation of bank statement isnoted by the outside accountant by dating andsigning the reconciliation.

The Board of Directors will approve both an annual andspecific event budgets. Actual contributions and eventor other revenues will be compared to budgetedexpectations. Variances will be reviewed to understandany significant differences from budget.

All employees who handle cash are bonded or otherwiseinsured.

Page 15

Petty Cash

Control Objective: To ensure petty cash disbursements and replenishments areauthorized and properly recorded in the accounting records.

Responsible Parties:Petty cash custodian – maintains petty cash accounting andsafeguards and controls disbursement of funds.

Executive Director – oversight of procedures and directsperiodic surprise counts of the petty cash.

Procedures: Management has established a maximum petty cash amount

of $200 based on the needs of the Museum for smallpayments or reimbursements.

The original distribution to set up the petty cashaccount is recorded as petty cash on the generalledger.

Petty cash should not be used in place of properplanning and requests for known upcoming expense. Thefollowing list is the expected use of petty cash; anyexceptions require approval of the Executive Director.Petty cash is authorized for the following expenses:

food purchases for office events or meetings, payment of bus drivers, and small emergency office supply purchases.

A petty cash distribution to an employee to cash apersonal check or as a temporary distribution of funds(secured by the employee’s check) is prohibited.

Cash on hand is assigned to a responsible staff memberand kept in a locked, fire resistant box.

Page 16

Petty Cash

Responsible party: AdministrativeAssistant

All petty cash disbursements will be made only with thesubmission of purchase receipts (if a receipt exists)and a signed request form.

All receipts submitted should be cancelled ormarked as paid.

Disbursements from petty cash are recorded by thecustodian on a petty cash reconciliation form (seeexample at ).

Disbursement from petty cash should comply withcontrols established for cash disbursements (seeadditional procedures at cash disbursements).

Before the petty cash fund is exhausted, theresponsible party will submit a petty cashreconciliation form and all receipts and reimbursementrequest forms for replenishment of funds. The pettycash account should be reimbursed at least monthly totimely record expenses in the accounting records. Thepetty cash funds on hand should not be less thanapproximately $40.

A check written payable to petty cash is used toreplenish funds. All disbursements from petty cash arerecorded in the accounting records (Quick Books) whenthe check is written to replenish the petty cash. Noamounts are posted to the petty cash account unless thetotal amount of the petty cash fund is increased ordecreased.

Surprise counts of the petty cash funds should beconducted periodically, as directed by the ExecutiveDirector.

Page 17

Petty Cash

Segregation of duties:Due to the limited number of staff, the petty cash custodianalso posts entries to the accounting records. The small ofamount of petty cash on hand and the associated entries arenot material to the operations of the Museum and there islimited risk associated with these conflicting duties.Management understands this risk and feels the risk to theMuseum is limited.

Additional controls are achieved in this area as follows: review and approval procedures established in the cash

disbursements process for reimbursements to petty cash, oversight by the Executive Director, periodic surprise cash counts, and monthly review of all accounting entries by an outside

accountant.

Page 18

Cash Receipts

Control Objective: To ensure cash receipts are properly safeguarded, depositedin the bank timely, and recorded accurately and timely inthe accounting records. To prevent loss or theft of Museumassets, to minimize the opportunity for loss of assets, andto detect if a loss has occurred.

Responsible Parties:Administrative Assistant – receives, opens, and processesmail; makes deposits and records deposits in the accountingrecords (Quick Books).

Pledges/Receivables Manager – maintains records of donationsand pledges received and receivable and updates donor database (Blackbaud). Sends pledge notices and receipts todonors.

Community Liaison/Fundraising Manager – maintains records ofamounts receivable and received on individual grants andrestricted contributions.

Executive Director – oversight of procedures and analysisand review of monthly financial statements

Board of Directors – oversight of procedures throughanalysis and review of monthly financial statements

Procedures: Cash and checks received in the mail are opened and

processed by the Administrative Assistant. Thefollowing steps are completed in this process:

checks are stamped “for deposit only” whenreceived, and

checks are photocopied with a copy maintained withthe deposit documentation, a copy given to thePledges/Receivables Manager to record in the donor

Page 19

Cash Receipts

data base, and a copy of any grant or restricteddonation checks to the CommunityLiaison/Fundraising Manager.

Maintain a master file or binder of the following: Quick Books print out of the deposit detail, check photocopies, copy of the deposit slip, and bank deposit receipt.

Deposit checks on a daily basis, if possible, or at aminimum twice weekly. Any checks held and notdeposited should be secured in a locked, fire resistantfile.

The Community Liaison/Fundraising Manager will maintaina record of all grant funds received, by individualgrant, including date funds are received, amount, andany remaining funds receivable.

A thank you letter or other receipt will be provided tothe donor for all donations and pledges received. Seeprocedures in Pledges Receivable and other Donationsfor any additional procedures performed byPledges/Receivables Manager for cash receipts.

Record the deposit in the accounting records (QuickBooks).

List individual checks and/or cash by the donorand amount.

Determine whether the amount received is a newdonation or a payment toward a prior commitmentalready recorded in the accounting records.

Donor restrictions are noted and properlydocumented by the responsible employee.

Access to cash receipts records is limited to thosewith approval for logical access to the information.

Page 20

Cash Receipts

Administrative Assistant Executive Director Outside accountant

Complaints from donors or granters will be resolved bythe Executive Director, Community Liaison/FundraisingManager or Pledges/Receivables Manager as they are notpart of the direct processing and recording of cashreceipts.

See additional procedures in the General CashProcedures and Policies Section.

Segregation of duties:Due to the limited number of staff, the AdministrativeAssistant opens the mail and posts cash receipts to theaccounting records. The controls listed below are adequateto compensate for these conflicting duties and to reduce therisk of incompatible duties to an acceptable level.Management understands this risk and feels the risk to theMuseum is limited.

Additional controls are achieved in this area as follows: oversight by the Executive Director; unopened bank statements are opened and reconciled by

the outside accountant; the Pledges/Receivables Manager reconciles the donation

revenues and amounts receivable recorded in theaccounting records to the information recorded in thedonor data base on a monthly basis;

the Community Liaison/Fundraising Manager reconcilesthe grant revenues and amounts receivable recorded inthe accounting records to the information recorded ingranter files and records on a monthly basis;

complaints from donors or granters are resolved by theExecutive Director, Community Liaison/FundraisingManager or Pledges/Receivables Manager as they are not

Page 21

Cash Receipts

part of the direct processing and recording of cashreceipts;

comparison and analytical review of cash receipts tobudget expectations by the Executive Director and theBoard of Directors; and the

monthly review of all accounting entries and the bankaccount reconciliations by an outside accountant.

Page 22

Cash Disbursements

Control Objective: To ensure cash disbursements are properly authorized andrecorded accurately and timely in the accounting records.To prevent loss or theft of Museum assets, to minimize theopportunity for loss of assets, and to detect if a loss hasoccurred.

Responsible Parties:Administrative Assistant – prepares invoice packages andchecks for approval and signature.

Executive Director – oversight of procedures; review ofinvoice packages and authorization for disbursements;analysis and review of monthly financial statements; andcomparison of actual expenses to budgeted expenses.

Board of Directors – specific Board of Directors members aredesignated with signing authority, review of invoice packageand authorization for disbursements. The Board ofDirectors provides oversight through analysis and review ofmonthly financial statements and comparison of actual tobudgeted expenses.

Procedures: All disbursements are made by check, including payroll,

except for those allowed through petty cash. Any wiretransfers or other electronic payments are made by theExecutive Director. The same approval procedures usedfor cash disbursements by check should be followed orelectronic payments to venders.

Access to cash disbursement records is limited to thosewith approval and logical access to the information.

Administrative Assistant Executive Director Outside accountant

Page 23

Cash Disbursements

The following is performed for safeguarding checks: prenumbered checks are used (in numerical order), checks printed in error are voided on the face of

the check and saved with other canceled checks, the Administrative Assistant stores unused checks

in a secure locked space, and any missing checks will be researched by the

Administrative Assistant and resolution will becommunicated to the Executive Director.Resolution will be reviewed by outside accountant.

The following signatures are required to authorizedistributions:

The Executive Director may sign checks less than$__________________.

Designated members of the Board of Directors maysign checks less than $______________.

Two signatures are required (either two members ofthe Board of Directors or the Executive Directorand one member of the Board of Directors) for alldisbursements greater than $1,000.

Check preparation procedures: A check request form is prepared for all disbursements

(see example of form). The form includes thefollowing information:

date requested date needed payee (vender) amount address of payee (if new or changed) telephone of payee (if new or changed) tax ID# of payee (if new or changed) – required

for 1099 reporting at year-end expense account to be charged, and classification of the expense (program, fund

raising, grant, etc.)

Page 24

Cash Disbursements

The Administrative Assistant prepares the invoicepackage for approval. The invoice package includes:

original invoice or purchase order request – allinvoices are marked as paid or otherwise noted asprocessed on the face of the invoice,

receiving documents, if purchase was shipped tothe Museum,

completed check request form, and the unsigned, printed check.

No late fees, interest charges or other additionalcharges will be paid without the approval of the checksigner(s).

The Administrative Assistant will review the invoiceand check the mathematical accuracy of the amounts onthe invoice and the total of the invoice.

Payments will be made from original invoices only, notfrom monthly statements, unless the statements arereconciled to the individual invoices. If the originalinvoice is missing, a copy should be requested from thevender.

A copy of any disbursements against restricted grantsor contributions is given to the CommunityLiaison/Fundraising Manager to be recorded on theindividual grant or restricted contributiondisbursement records.

An approved vender list should be established andapproved by the Executive Director. Payments should bemade only to approved venders. The Executive Directormust approve the addition of any new venders.

The Executive Director should review the approvedvender list twice a year and cancel any venders nolonger used.

Page 25

Cash Disbursements

All payments to employees must be approved by theExecutive Director. Payments to the Executive Directormust be approved by a member of the Board of Directors.

Check signers will review supporting documents, confirmvendor names and amounts printed on checks, and signchecks.

The invoice package is returned to the AdministrativeAssistant for processing and mailing payments.

All invoice packages are filed by vender in order ofthe date of payment.

The following are prohibited: checks signed in blank, without a payee or amount, checks signed that are payable to bearer or cash

(except for petty cash reimbursement checks), and checks countersigned in blank, without a payee or

amount.

The issuance of a manual (hand written) check is to beused only in rare situations and must be approved bythe Executive Director.

Complaints from venders will be resolved by theExecutive Director or another employee (other than theAdministrative Assistant) designated by the ExecutiveDirector.

The Board of Directors will approve both annual andevent budgets. Actual expenses will be compared tobudgeted expectations. Variances will be reviewed tounderstand any significant differences from budgeted.

See additional procedures in the General CashProcedures and Policies.

Page 26

Cash Disbursements

Segregation of duties:The controls listed above are adequate segregation of dutiesand there is limited risk in incompatible tasks completed bythe Administrative Assistant. Management understands thisrisk and feels the risk to the Museum is limited.

Additional controls are achieved in this area as follows: oversight by the Executive Director, unopened bank statements are opened and reconciled by

the outside accountant, the Community Liaison/Fundraising Manager reconciles

the grant and restricted contribution expense recordedin the accounting records to the information recordedin grant and restricted contribution files on a monthlybasis;

complaints from venders are resolved by the ExecutiveDirector.

comparison and analytical review of cash disbursementsto budget expectations by the Executive Director andthe Board of Directors, and the

monthly review of all accounting entries and the bankaccount reconciliations by an outside accountant.

Page 27

Payroll Processing

Control Objective: To ensure employees are paid appropriate, approved amountsfor actual work performed and salaries and related taxes orbenefits are properly calculated, recorded, and remitted ona timely basis

Responsible Parties:Executive Director – responsible for hiring, approval oftime sheets, employee review and advancement.

Administrative Assistant – responsible for calling in thehours worked to Paychex (outside payroll processing firm).

Procedures: Executive Director interviews and hires all staff.

Each employee completes the employee packet of formsincluding:

application/personal information sheetname and addresssocial security numberdate of birthproof of citizenshipdate of hire

Federal withholding form W-4 state withholding form A-4 proof of citizenship form I-9

Executive Director reviews all forms for completenessand notifies Paychex of the new employee, sendingcopies of forms to PayChex, as required.

Executive Director must authorize all changes topayroll or employee status and must personally notifyPayChex.

Page 28

Payroll Processing

All personal forms should be maintained in employeefiles, in the possession of the Executive Director.

Requests for vacation and/or sick/personnel time needapproval by the Executive Director.

Any unused vacation at fiscal year end will be accruedas a liability, based on the Museum’s policies for useand accumulation of vacation time.

For each time period (payroll is paid on the 15th and30th of the month), all employees will prepare and signa time sheet showing hours worked on a daily basis.

All time sheets will be reviewed and approved by theExecutive Director. Any overtime needs to be approvedin advance by the Executive Director.

The Administrative Assistant will check themathematical accuracy of the time sheets and call inthe payroll period hours to Paychex.

The Paychex reports for each payroll will be opened andreviewed by the outside accountant, then recorded inthe accounting system.

All required payroll reports are filed by Paychex.

Segregation of duties:The controls listed above are adequate segregation of dutiesand there is limited risk. Management understands this riskand feels the risk to the Museum is limited.

Additional control is achieved in this area as follows: oversight and approval of all areas by the Executive

Director, processing and oversight of legal requirements by a

professional payroll firm, and

Page 29

Payroll Processing

review and posting of all payrolls by the outsideaccountant.

Page 30

Grants, Restricted Funds andRelated Expenditures

Control Objective: To ensure grant funds and restricted contributions areproperly recorded, collected and monitored on a timelybasis. To ensure that restricted grant funds andcontributions are used for the purpose intended and anyreporting requirements for grants are met on a timely basis.

Responsible Parties:Community Liaison/Fundraising Manager – monitors all grantand restricted contribution transactions (receipt,collection, and expenses) and prepares required reports forgranting agencies.

Administrative Assistant – records entries in the accountingrecords and provides the Community Liaison/FundraisingManager with copies of all grant funds received and/orexpenditures against grant funds.

Executive Director – oversight of procedures and review ofproper recording and reporting for grant funds received andexpended.

Procedures: Community Liaison/Fundraising Manager informs the

Administrative Assistant when the Museum is notified ofthe award of grant funds or restricted contributions.

Community Liaison/Fundraising Manager maintains the

grant or restricted contribution documents inindividual files including:

grant application, budget submitted with application, grant or restricted contribution requirements,

Page 31

Grants, Restricted Funds andRelated Expenditures

summary sheet of grant/contribution cash receiptsand expenditures allocated against thegrant/contribution,

amounts and dates funds will be received on thegrant if all funds are not received in onedistribution prior to expenditures,

disbursement requests, if filed, with the grantingagency,

reports filed as required under thegrant/contribution.

The Community Liaison/Fundraising Manager will maintaina tickler file of due dates for payments and reports toensure payments are received and reports are filed on atimely basis.

The Community Liaison/Fundraising Manager will copy theAdministrative Assistant with any distribution requestsor notices of distribution from grants/restrictedcontributions.

The Administrative Assistant will record any amountsdue under grants when the grant is made or whendisbursement requests are filed with the grantingagency. These funds will be recorded in the accountingrecords as accounts receivable and grant orcontribution revenue. A classification will be set upfor individual grants and restricted contributions thatrequire tracking income and expense bygrant/contribution.

The Administrative Assistant will notify the CommunityLiaison/Fundraising Manager of any amounts recorded inthe accounting records as due and not received within15 days.

Page 32

Grants, Restricted Funds andRelated Expenditures

The Community Liaison/Fundraising Manager will followup with granting agencies within 30 days of the duedate on any amounts not received when due.

The Administrative Assistant will notify the CommunityLiaison/Fundraising Manager and the Executive Directorof any amounts more than 30 days overdue.

The Executive Director will review the grantsreceivable on a monthly basis and determine if anyallowance for doubtful collection is required on a pastdue grant. The Executive Director will notify theAdministrative Assistant to record any requiredallowance for doubtful collection.

Complaints from donors or granters will be resolved bythe Executive Director.

Grants and donors will be published in the Museum’sjournals, newsletters, programs, website, etc.

Records are kept by the Community Liaison/FundraisingManager of any gifts contingent on future events, suchas bequests, and periodically reviews these contingentcontributions to determine if they can be recorded inthe accounting records because the contingency has beenmet.

Restrictions that lapse at a specific time or at theoccurrence of a specific event are monitored by theCommunity Liaison/Fundraising Manager to ensure thatresources are appropriately used and accounted for inthe accounting records.

The Board of Directors will approve an annual budgetand budgets for specific events or grants. Actual

Page 33

Grants, Restricted Funds andRelated Expenditures

revenues and expenses will be compared to budgetedexpectations. Variances will be reviewed to understandany significant differences from budget.

Segregation of duties:The controls listed above are adequate segregation of dutiesand there is limited risk. Management understands this riskand feels the risk to the Museum is limited.

Additional control is achieved in this area as follows: oversight by the Executive Director, complaints from granting agencies are resolved by the

Executive Director, amounts receivable, received or expensed are recorded

in the accounting records and reconciled by theCommunity Liaison/Fundraising Manager to thegrant/contribution records, and

monthly review of all accounting entries by an outsideaccountant.

Page 34

Pledges and Contributions

Control Objective: To ensure contributions and fund raising event revenues areproperly recorded, collected and monitored on a timelybasis. To ensure that restricted contributions areidentified and used for the purpose intended.

Responsible Parties:Pledges/Receivables Manager – monitors all pledges,contributions, and fundraising event revenues; preparesrequired reports for the Board of Directors; and receives,solicits and acknowledges contributions.

Administrative Assistant – provides the Pledges/ReceivablesManager with copies of all funds received and deposited forreconciliation with the donor data base information; recordscontributions and pledges in the accounting records.

Community Liaison/Fundraising Manager – monitors and assurescompliance with restricted contributions.

Executive Director – oversight of procedures and review ofproper recording of contributions and fund raising eventrevenues.

Procedures: The Board of Directors, or their designated committee,

must approve any formal fund raising, capital campaign,or other solicitation activities. The ExecutiveDirector must review and approve the wording on anysolicitations, promotional information for events ordrives, or other formal fund raising materials toensure the wording meets the legal requirements and thepurpose of the contribution or pledge complies with theintent of the Board of Directors.

The Pledges/Receivables Manager will provide theamount, donor name, schedule of payments and otherrelevant information to the Administrative Assistant

Page 35

Pledges and Contributions

when the Museum is notified a pledge or contribution.The Manager will provide the same information to theCommunity Liaison/Fundraising Manager for restrictedcontributions. (See Grants, Restricted Funds andRelated Expenditures procedures)

If the contribution is restricted, the AdministrativeAssistant will set up a restricted classification whenthe contribution is recorded in the accounting recordsto document expenses processed under the terms of therestriction.

Pledges/Receivables Manager will write thank-youletters to donors for all contributions or eventparticipation. These acknowledgment letters willreflect all information required to conform to IRSrules. The following information must be included in adonor acknowledgment letter:

the amount of cash and a description of thecontribution or pledge,

description of any non-cash or other propertycontributed

a description is listed for non-cash contributionsbut not value of the contribution, except thevalue determined by the donor may be shown as thevaluation per the donor, if requested,

a statement about whether the Museum provided anygoods or services in return for the contribution,and

a description and an estimated value of the itemprovided if the Museum provided something inreturn for the contribution. Goods or serviceswith a nominal value can be ignored for thisdisclosure requirement.

Note: No disclosure is required if (a) the value ofthe portion that represents a benefit to the donoris not more than $80 or 2% of the payment, whichever

Page 36

Pledges and Contributions

is less, or (b) the benefit is a token item, such asa mug or tee shirt, bearing the nonprofit Museum’sname or logo, the contribution is $40 or more, andthe cost of all benefits to the donor in a year is$80 or less. As a best practice the Museum willshow the value of any items provided, since thetotal value to a donor may not be known until theend of the year.

The Pledges/Receivables Manager will maintain the donordata base and donor files (by donor name) including:

pledge and contribution documents, donor’s name, amount of pledge or contribution, any donor restrictions or designated use of the

contribution, amounts and dates funds will be received on the

pledge (if all funds are not received in onecontribution),

communication with donors regarding pledges andcontributions, and the

copy of the donor thank you letter or receipt.

The following information is required for any amountsreceived from donor’s and charged to a credit card:

credit card form signed by the donor (ifpossible),

if approval is verbal, document the person givingthe approval, who received the information for theMuseum, and the date and amount,

type of credit card, credit card number and expiration date, the donor’s name as shown on the credit card, and the donor’s billing address, including zip code,

for the credit card.

Page 37

Pledges and Contributions

Receipts or thank you letters are to be sent to donorsfor all credit card charges, whether it is for anongoing pledge or a one time contribution.

The Pledges/Receivables Manager will maintain a ticklerfile in the donor data base of pledge due dates toensure payments are received on a timely basis. Donorswill receive a notification of amounts due from thePledges/Receivables Manager no later than ten daysbefore the due date.

The Administrative Assistant will record any amountsdue under pledges or contributions receivable when thecommitment is made by the donor. These funds will berecorded in the accounting records as pledges oraccounts receivable and contribution revenue. If thecontributions are related to a specific fund raisingevent, a classification will be set up to track thecontributions by the event.

For pledges receivable, the Executive Director willestablish the discount rate for pledges payable overmore than one year. The Administrative Assistant willrecord the appropriate discount for new pledgesreceivable as computed by the Executive Director. TheExecutive Director may designate this task to theoutside accountant.

A schedule will be prepared and maintained of pledgesreceivable, the discount rate applied to the pledges,the applicable discount, and the annual adjustments tothe discount.

The Administrative Assistant will notify thePledges/Receivables Manager of any amounts due but notreceived within 30 days.

Page 38

Pledges and Contributions

The Pledges/Receivables Manager will follow up withcontributors within 30 days of the due date for anyunpaid amounts.

The Administrative Assistant will notify thePledges/Receivables Manager and the Executive Directorany amounts more than 60 days overdue.

The Executive Director will review the pledges andcontributions receivable on a monthly basis anddetermine if any allowance for doubtful collection isrequired on past due commitments. The ExecutiveDirector will notify the Administrative Assistant ofany amounts to record to the allowance for doubtfulcollection.

Complaints from contributors will be resolved by theExecutive Director.

Contributions will be published in the Museum’sjournals, newsletters, programs, website, etc.

A monthly reconciliation will be performed by thePledges/Receivables Manager of the pledges andcontributions received and receivable in the accountingrecords to the amounts recorded in the donor data base.

The Executive Director (and the Board of Directors foramounts greater than $5,000) must approve theacceptance of any in-kind or other non-cash donationsbefore such donations are accepted by the Museum.Donations not considered appropriate or of value to theMuseum will not be accepted.

The Executive Director and/or the Board of Directorswill approve an annual budget and budgets for anyspecial events. Actual amounts will be compared to

Page 39

Pledges and Contributions

budgeted expectations. Variances will be reviewed tounderstand any significant differences from budget.

Segregation of duties:The controls listed above are adequate segregation of dutiesand there is limited risk. Management understands this riskand feels the risk to the Museum is limited.

Additional controls are achieved in this area as follows: oversight by the Executive Director and Board of

Directors, complaints from granting agencies are resolved by the

Executive Director, amounts receivable, received or expensed are recorded

in the accounting records and reconciled by theCommunity Liaison/Fundraising Manager and thePledges/Receivables Manager to independent records inthe donor data base and to grant/contribution records,and

monthly review of all accounting entries by an outsideaccountant.

Page 40

Capital Assets

Control Objective: To ensure the Museum’s capital assets are safeguarded andproperly recorded in the accounting records.

Responsible Parties:Administrative Assistant – records the purchase as a capitalasset addition in the accounting records.

Executive Director – approves capital purchases, providesoversight of procedures and reviews proper recording ofcapital assets.

Procedures: The Board of Directors will prepare a capital budget in

conjunction with other organizational budgeting.Inclusion of a capital item in the budget serves asapproval for the acquisition.

Asset acquisitions greater than $1,000 will be recordedin the accounting records as capitalized assets.Items less than $1,000 will be expenses as acquired.

The following procurement guidelines will be followed: procurements will be made from approved venders; bids or costs will be solicited from at least 2 to

3 venders for purchases greater than $5,000; the quality of the assets will be determined and

whether the assets selected are appropriate forthe intended purpose.

Prepare a purchase/check request for the asset (seecash disbursements procedures). Obtain approval of thepurchase from the Executive Director.

Attach a tag or sticker to the asset showing the nameof the Museum and the asset number of the item.

Page 41

Capital Assets

Maintain a list of all assets used in operations,whether capitalized or expensed, that includes thefollowing information:

description of the asset, serial/tag number, location of the asset, cost or value at time of acquisition, date acquired, funding source, if applicable, restrictions on use or disposal of the asset, date asset was retired or disposed, and the amount received from any sale of the asset.

The Executive Director, or a designated employee, willperform an annual inventory of major assets to assureall items are in use and held by the Museum. Anyassets not in use will be assessed to determine if thevalue of the assets needs to be written down or writtenoff in the accounting records.

The Executive Director will determine that all majorassets are safeguarded from loss and properly insured.

Any donations of capital assets greater than $5,000must be approved prior to acceptance by the ExecutiveDirector and the Board of Directors. See procedures inPledges, Contributions and Donations.

Use proper IRS guidelines to establish the estimateduseful lives for each asset and record depreciationbased on this determination. The Museum will consultwith the outside accountant to establish the estimateduseful life of an asset.

See procedures in Cash Disbursements that would alsoapply to purchases of Capital Assets.

Page 42

Capital Assets

Segregation of duties:The controls listed above are adequate segregation of dutiesand there is limited risk. Management understands this riskand feels the risk to the Museum is limited.

Additional controls are achieved in this area as follows: oversight by the Executive Director and Board of

Directors, annual inventory of major assets, cash disbursement procedures are following for any

purchases of assets, procurement guidelines for major purchases, and monthly review of all accounting entries by an outside

accountant.

Page 43

Required Annual Filings orReports

The Museum will prepare the following annual filings:

Arizona Corporation Commission ReportFiling is due annually on: December 20

Charitable Organization Financial Statement Report withthe Az. Secretary of StateFiling is due annually on: September 30

Federal and State of Arizona Income Tax ReturnsFiling is due annually on: February 15 (if notextended)

Note: All payroll reporting is completed for theMuseum by outside payroll company (Paychex).

Page 44

Travel Policy

Subject to approval of the Executive Director,employees are entitled to reimbursement for ordinaryand necessary business-related expenses. Reimbursementrequests should be submitted to the Executive Directoron an Employee Expense Report Form. Receiptsdocumenting expenditures for amounts of $25 and abovemust be attached to receive reimbursement. Receiptsfor items under $25 should be included if available.The Museum expects that you will apply the utmostdiscretion when incurring expenses on its behalf. Thespending philosophy applicable to expensereimbursements is to treat the Museum’s funds as ifthey were your own. All reimbursement requests must besubmitted within 60 days of the expense.

Mileage in excess of your normal commuting mileage toand from the office will be reimbursed at the maximumrate allowed by the Museum, which is the current IRSrate. For example, assume your normal drive to and fromthe office is 20 miles. On a particular day, you drivea total of 30 miles to attend a seminar without goingto the office. You will be reimbursed for only the 10miles over and above the commuting base mileage.

Overnight travel is reimbursable, if approved by theExecutive Director; your trip is essential; and ittakes you more than 60 miles from your home (120 milesfor the round trip). Deviations from this guideline maybe permitted in cases of inclement weather or otherunique circumstances, if approved in advance by theExecutive Director. Nonluxury lodging, reasonable mealcosts, and telephone calls will be reimbursed. Thelodging facility must be approved by the ExecutiveDirector. If a seminar or event is held at a specificfacility, lodging may be obtained at that facility inconjunction with the event. Expenses of a personalnature are typically not reimbursed.

Page 45

Travel Policy

If you fly on Museum business, you are expected to usethe most economical fare (first class travel isprohibited) available without creating an unreasonablepersonal hardship.

Rental cars are discouraged in favor of publictransportation, where available. If publictransportation (shuttle bus or other transportationfrom the airport to your lodging) is not available, arental car can be approved. You are expected to usethe most economical rental car agency without creatingan unreasonable personal hardship.

If a travel advance is needed, the request should bereceived by Accounting no later than seven days beforethe scheduled business trip.

Page 46