Adaptive kinetic model for coal devolatilization in oxy-coal combustion conditions

Energy Policy 32 (2004) 151–163

Energy rent and public policy: an analysis of theCanadian coal industry

Thomas Gunton*

School of Resource and Environmental Management, Simon Fraser University, Burnaby, BC V5A 1S6, Canada

Abstract

This paper analyses issues in resource rent through a case study of the Canadian coal industry. A model of the coal industry is

constructed to estimate the magnitude of rent and distribution of coal rent between government and industry over the 30-year period

from 1970 to 2000. Disaggregation of results by coal sector shows that rent varied widely, with one sector generating substantial rent

and other sectors incurring large losses. The pattern of development of the coal sector followed what can be termed a ‘‘rent

dissipation cycle’’ in which the generation of rent in the profitable sector created excessively optimistic expectations that encouraged

new entrants to dissipate rent by developing uneconomic capacity. The analysis also shows that the system used to collect rent was

ineffective. The public owner collected only one-third of the rent on the profitable mines and collected royalty revenue from the

unprofitable mines even though no rent was generated. The case study illustrates that improvements in private sector planning based

on a better appreciation of resource market fundamentals, elimination of government subsidies that encourage uneconomic

expansion and more effective rent collection are all needed to avoid rent dissipation and increase the benefits of energy development

in producing jurisdictions. The study also illustrates that estimates of rent in the resource sector should disaggregate results by sector

and make adjustments for market imperfections to accurately assess the magnitude of potential rent.

r 2002 Elsevier Ltd. All rights reserved.

1. Introduction

The rapid rise in energy prices precipitated by thecreation of OPEC in the early 1970s stimulated agrowing interest in the concept of resource rent by bothacademics and policy practitioners. The magnitude ofrent, its distribution between competing stakeholdersand the impact of alternative mechanisms for collectingrent were all thrust to the forefront of the policy agenda.Much of this policy debate occurred in the midst of thetwo major petroleum commodity booms in the early1970s and again in the early 1980s. Now that energyprices are more stable, the timing is opportune toundertake a longer term analysis of rent to assess policylessons from several decades of experimentation withrent collection regimes. As Kemp (1992) and Rutledgeand Wright (1998) note in recent issues of Energy Policy,rent collection remains one of the key issues for energyproducing countries.

The purpose of this paper is to assess issues in rentgeneration and distribution through a case study of theCanadian coal industry over the last three decades. Thepaper will commence with an overview of the coalindustry and its evolution in British Columbia, Canada.This will be followed by an empirical estimate of coalrents based on a model of the regional coal sector. Theimpact of policy on the generation and distribution ofcoal rents will be assessed and policy lessons from thecase study identified.

2. Coal markets

Coal is a ubiquitous resource with a wide range ofcharacteristics and quality. Two basic categories of coalare coking coal used in the making of steel and thermalcoal used for power generation (IEA, 1997; Ellerman,1995). Thermal coal is more abundant and its valuevaries with factors such as heating value, ash content,sulphur content and moisture. Coking or metallurgicalcoal is less abundant and commands a premium overthermal coal by virtue of its more restricted supply andlack of substitutes in the steel making process. Coking

ARTICLE IN PRESS

*Corresponding author. Tel.: +1-604-291-4659; fax: +1-604-291-

4968.

E-mail address: [email protected] (T. Gunton).

0301-4215/04/$ - see front matter r 2002 Elsevier Ltd. All rights reserved.

PII: S 0 3 0 1 - 4 2 1 5 ( 0 2 ) 0 0 2 4 7 - 1

coal varies in value based on factors such as fluidity,swelling and strength which all affect its efficiency inmaking steel. There is also a range of coals referred to assoft coals that can be used as either coking coal in themaking of steel or as thermal coal for power generation.Currently thermal coal accounts for 84% of world coalproduction and coking coal 16% of world production(IEA, 2000: p. 11.30).The market structure of the coal industry has changed

significantly over the last several decades. Prior to 1960,coal markets were not well integrated. Internationaltrade was a small proportion of world production and

consisted largely of high cost land based trade betweenneighboring countries. International trade began togrow rapidly after 1960 when the growth in steelproduction in Pacific Rim countries such as Japanstimulated coal imports to meet domestic requirements.The rise in oil prices in 1973 and again in 1979 alsoincreased trade in coal as a substitute for oil in powerproduction. The result of these changes has been theemergence of an integrated international coal market(IEA, 1997). Ellerman (1995) estimates that one-third toone-half of world production is now part of a single,unified market connected by seaborne trade. Theinternational trade market remains relatively concen-trated on both the supply side and the demand side withfew countries accounting for the major proportion oftraded coal, particularly in the coking coal market(Table 1). Chang (1997), Ellerman (1995) and IEA(1997) all conclude, however, that the coal market showsincreasing signs of being a well functioning competitivemarket characterized by large numbers of buyers andsellers, good information and competitive pricingbehavior within the coal market and between energysubstitutes.Within this international market there is a wide

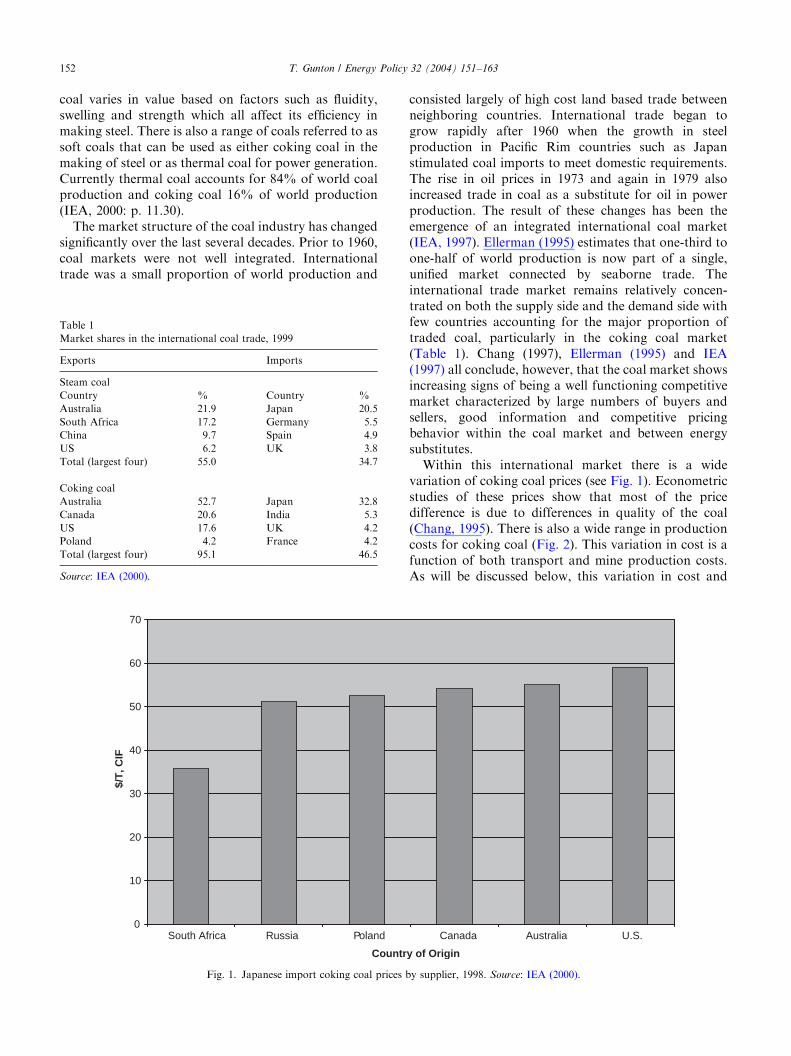

variation of coking coal prices (see Fig. 1). Econometricstudies of these prices show that most of the pricedifference is due to differences in quality of the coal(Chang, 1995). There is also a wide range in productioncosts for coking coal (Fig. 2). This variation in cost is afunction of both transport and mine production costs.As will be discussed below, this variation in cost and

ARTICLE IN PRESS

Table 1

Market shares in the international coal trade, 1999

Exports Imports

Steam coal

Country % Country %

Australia 21.9 Japan 20.5

South Africa 17.2 Germany 5.5

China 9.7 Spain 4.9

US 6.2 UK 3.8

Total (largest four) 55.0 34.7

Coking coal

Australia 52.7 Japan 32.8

Canada 20.6 India 5.3

US 17.6 UK 4.2

Poland 4.2 France 4.2

Total (largest four) 95.1 46.5

Source: IEA (2000).

0

10

20

30

40

50

60

70

South Africa Russia Poland Canada Australia U.S.

Country of Origin

$/T

, CIF

Fig. 1. Japanese import coking coal prices by supplier, 1998. Source: IEA (2000).

T. Gunton / Energy Policy 32 (2004) 151–163152

quality is a major factor in generating economic rent inthe coal sector.

3. Development of the BC coal industry

The emergence of the BC coal industry was stimulatedby the demand for coking coal by the Japanese SteelIndustry (JSI), which wanted to diversify its coalpurchases by contracting with new suppliers in costcompetitive regions. The JSI concluded contracts withtwo BC mining companies in the late 1960s to supplyabout 8MMT/year of coking coal. With the develop-ment of these two mines, BC became a major exporter ofcoking coal, supplying 18% of the JSI requirements by1975 (IEA, 1999).The dramatic rise in oil prices in 1973 and 1979 caused

a concurrent rise in coal prices (Fig. 3). This stimulatedinterest in further expansion of coal production in BC inthe existing southeast mines and the development of anew coal producing region in northeast British Colum-bia. The expansion in the northeast began with thesigning of a 20-year contract with the JSI to purchase6.7MMT/year of coal. The northeast coal project(NECP) was completed in 1983 at a cost of $4.6 billion(2000 Can $) to construct two new mines, a major newrail line, a new port, a new town and upgrade existinginfrastructure. Overall, the government contributedapproximately $1.7 billion of the total cost. With aconcurrent expansion of about 7.0MMT/year in thesoutheast, total BC capacity increased from 9.0MM/year in 1980 to 24MT/year in 1983. With this increase,

BC displaced the United States as the second largestsupplier to the JSI.This period of expansion in the BC coal industry was

characterized by several key factors. First, as Fig. 4indicates, the rates of return in the coal industry in the1970s and early 1980s were well in excess of the averagereturns in the private sector.1 These high rates of returngenerated excessive optimism about the future of theindustry, which persisted despite cautions in government

ARTICLE IN PRESS

0

10

20

30

40

50

60

BC low Aust low SA low SA high US low BC high US high Aus high

Mine

US

$/t

, FO

B P

ort

Fig. 2. Costs of coking coal production, 1999. Source: IEA (2000).

1Unfortunately there is no consistent time series of rates of return in

the BC coal sector. Therefore the time series in Fig. 4 has been based

on several sources. The rate of return for the years 1970 to 1979 are

based on the annual reports of Kaiser Resources (1969–1979) which

accounted for 63% of BC production during this period. The cost

structure of Kaiser was similar to the other major producer, Fording

Coal and is therefore representative of the profitability of the BC coal

sector during this period. For the years 1980 and 1981 the rate of

return for all Canadian coal mines is used based on the Statistics

Canada series #61-207. For the years 1982 to 1991 the Coal

Association of Canada (1987, 1990) annual review of the BC Coal

industry is used. For the years 1992 to 1999 the coal sector net earnings

from the BC Mining Association annual review of the BC mining

industry (PricewaterhouseCoopers, 1992–1999) are used. In all years

except 1990 and 1991, the rate of return is calculated as after tax net

earnings as a percentage of the year end shareholders equity. For 1990

and 1991 the after tax return on capital employed is used because the

negative value of shareholders equity in the coal sector prohibited the

calculation of a return of shareholder’s equity. The average rate of

return for Canadian industry is based for the years 1972 to 1987 on the

Statistics Canada publication Corporation Financial Statistics, Cat #

61-207. This series was discontinued in 1987 and replaced with a new

series #61-219, which was used for the period 1988 to 2000. Again, the

rate of return is the after tax net earnings as a percentage of year-end

shareholders equity for the manufacturing sector from 1972 to 1987

and for all non-financial industries in the new series for 1988 to 2000.

T. Gunton / Energy Policy 32 (2004) 151–163 153

and private sector studies that high prices that existed inthe post-OPEC era would fall as new supply wasdeveloped. (Siverston and Clancy, 1976; Jones andSiverston, 1979; Halvorson, 1980).The second feature of this period was that the lure of

high profits drew in new firms with little experience inthe coal industry that financed their expansion with highratios of debt as opposed to equity capital. The high costNECP was built by two mining companies that werewell established but had no previous experience incoking coal production. The expansion in the southeastwas undertaken by the two existing operators, one ofwhich was subsequently purchased by a new companythat had no experience in mining. By 1983 five majorcompanies were involved in BC coal production, four ofwhich had no previous experience in BC coal productionand overall debt levels in the industry increased fromalmost nil to a relatively high debt to equity ratio of 1.3(Coal Association of Canada, 1987).The final feature of this period was an increasing role

for government in financing the expansion. Governmenthad virtually no role in the development of the originalsoutheast mines or the new southeast mines built in theearly 1980s. But the industry was moving up the costcurve, with the NECP project incurring a per tonne

capital cost more than double the cost of the originalsoutheast mines and substantially higher than theconcurrent expansion in the southeast (BC, 1986). Thehigher costs required government to make a significantinvestment in infrastructure comprising 37% of totalNECP costs in order for the project to go ahead.The BC coal industry encountered major problems as

soon as these new mines were completed. Capital andoperating costs on the NECP mines were well abovebudget and coal prices declined, forcing the principalNECP and the major southeast operator, which hadpurchased existing capacity at the peak of the marketcycle, to declare bankruptcy in the early 1990s. Thebankrupt mines were purchased by two other estab-lished coal mine operators who wrote down the debtsand reopened the bankrupt mines. As illustrated in Fig.4, the two remaining mining companies, which nowcontrolled over 90% of BC coal production after theirpurchase of the bankrupt mines, were able to achievedramatic increases in productivity. This resulted in adecline in employment in the coal sector of almost 50%between 1990 and 2000. Although this employmentdecline caused substantial economic instability in thecoal producing regions of BC, the lowering of cost andthe closure of the high cost NECP in 2000 helped

ARTICLE IN PRESS

0

10

20

30

40

50

60

70

80

90

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

Year

U.S

. $/t

FO

BT

NECP Quintette MineSoutheast Elkview Mine

Fig. 3. British Columbia coking coal prices, 1970–1999. Source: IEA (2000).

T. Gunton / Energy Policy 32 (2004) 151–163154

stabilize the industry. Given its current competitiveposition, the BC industry should remain stable over thenext decade.

4. Coal rent

Natural resource rent is normally defined as theincome generated by the sale of a natural resource abovethat required to compensate the factors of productionused in extraction and refining. Natural resource renthas been disaggregated into conceptually distinctcategories including differential rent, monopoly rent,user cost rent and windfall rent (Gunton and Richards,1987).Differential rent in the coal sector is generated by the

difference in cost between the marginal mine, which justcovers the cost of labor and capital required to extractthe coal and the intramarginal mine, which generates asurplus above that required to cover cost of labor andcapital. The magnitude of this surplus for the intramar-ginal mine is equivalent to the cost advantage over themarginal mine. The difference in cost can be due to anumber of factors including the quality of the coal, thedifficulty in extracting the coal and the transport costs tomarket.

Coal market data from the International EnergyAgency (IEA) summarized in Fig. 2 illustrates that thedifference in production costs between coking coalmines varies up to $20 per tonne (1999 US $).Differences in coking coal quality result in a furthervariation of up to $13 per tonne (Fig. 1). Thecombination of production cost and quality differenceshas the potential for generating substantial differentialrent for the intramarginal coal mines.Monopoly resource rent is generated by the ability of

resource producers to increase price above competitivelevels by having sufficient market power to restrictsupply. The market analysis of the coal sector bySchwindt (1989), Ellerman (1995) and the IEA (1997),however, suggests that monopoly rent is not significantin the coal sector due to the increasingly competitivestructure of international coal markets.User cost rent is generated by the increase in current

resource prices in anticipation of future resourceexhaustion. There is no evidence to suggest that usercost in a factor in a sector such as coal, which hasextensive reserves. Windfall rent or windfall loss isgenerated by unanticipated changes in markets that cancause short-term mismatches between supply anddemand. In capital intensive industries such as coal thatrequire long lead times to adjust supply capacity to

ARTICLE IN PRESS

-15

-10

-5

0

5

10

15

20

25

30

35

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

year

An

nu

al %

Ch

ang

e (3

yea

r m

mo

vin

g a

vera

ge)

change in output/employee

rate of return

Fig. 4. Rate of return and productivity change in coal sector, 1971–1999. Source: BC (2000).

T. Gunton / Energy Policy 32 (2004) 151–163 155

changes in demand, windfall rents and windfall lossescan be an important factor, particularly over the shortrun. Over the longer run market cycle windfall gains andlosses tend to offset each other.Although these different types of rent are easy to

distinguish conceptually, they are difficult to estimateseparately. Consequently, British Columbia coal rent isinitially estimated as an aggregate rent based on thestandard method used in other research studies on rentin the resource sector (Helliwell, 1978; Hughes andSingh, 1978; Copithorne, 1979; Bradley et al., 1981,Cairns, 1982; Gunton and Richards, 1987). Revenue isestimated by year. Costs, including capital costs, areestimated by year and deducted from revenue togenerate a net income stream. The net income streamis then capitalized as a net present value by using adiscount rate that represents the opportunity cost ofprivate capital. This definition of rent can be moreformally summarized as follows:

Resource rent ¼Xn

t¼0

Rt � Ct

ð1þ rÞt

Where R is the revenue, C the cost of production(including capital), r the opportunity cost capital, t theyear and n the number of years.The model used to estimate rent for the British

Columbia coal industry divides the industry into threesectors: the original southeast mines built in the early1970s, the new southeast mines built in the early 1980sand the NECP built in the early 1980s. Revenue is basedon the minehead value of the coal and costs are based onthe operating and capital costs of the mines. The datasources for the model are summarized.2 The model

calculates the results in $2000 Canadian dollars usingthe Canadian Gross National Expenditure price defla-tor. The net revenue stream is estimated for the threecoal sectors for the years 1970 to 2000 and is capitalizedas a net present value in 1970.Although the method for estimating coal rent is

conceptually straightforward, there are a number ofpractical difficulties. One major issue is defining theopportunity cost of private capital invested in mining,which is key to distinguishing between ‘‘normal’’ profitsnecessary to compensate private investors and rent. Theproblem is that there is no consensus on whatconstitutes a normal profit. Many factors such as riskcan result in the opportunity cost of capital varying bysector and by time period (Cairns, 1982). To deal withthis uncertainty over the opportunity cost of capital, theestimate of coal rent is based on a sensitivity analysisusing a range of opportunity costs of private capital.The base case estimate uses a real before tax opportunitycost of 10%. This is the estimate of the private sectoropportunity cost by Jenkins (1977) and is the base caseestimate used in many of the feasibility studies of themining sector (BC, 1982; Barnett, 1985, 1987; Richards,1987; Anderson, 1987a, b, 1990). A sensitivity analysis isalso reported using real before tax opportunity costs of8% and 12%.A second problem is that profits will vary over the

market cycle as high returns during market upturnscompensate for low returns during market downturns.High returns or windfalls above the long run opportu-nity cost of private capital during strong markets can bemisinterpreted as rent instead of compensation for lowreturns during weak markets. This was a deficiency, forexample, in the first major study of rent in the Canadianmining industry by Kierans (1973), who based hisestimate of rent over a short-term peak in the mineralmarket. The estimate of rent in the coal sector avoidsthis problem by estimating rent over a thirty-year cycle.A third issue identified by Cairns (1982) is that the

cost of exploration for any specific project must beaveraged over a large number of projects to fullyincorporate the risk of exploration. Taking the explora-tion costs of only the successful projects that aredeveloped would therefore understate the real cost ofmine development and overstate the quantity of rent.This problem is mitigated in the estimate of coal rent intwo ways. First, the capital cost numbers include thepurchase price of ore reserves, which includes thecapitalized supply costs of exploration for the industry.Second, the coal model is based on the financial data forintegrated operators, which includes exploration expen-ditures for undeveloped sites. Consequently, the capitaland operating cost data used in the model include animputed cost for unsuccessful exploration investment.Although this is a crude indicator that may overestimateor underestimate exploration costs, it helps offset the

ARTICLE IN PRESS

2Capital cost for the mines was obtained from BC (1986). Value of

production was obtained from the BC government coal statistics series.

The value of production was disaggregated by sector as follows.

Northeast production values were estimated by year based on the price

and production data contained in the Tex Coal Manuals (Horie, 1985–

1999) for the northeast mines. Southeast production and values were

estimated by deducting the northeast values from BC total values. Old

southeast and new southeast were estimated by prorating southeast

production values on the basis of the relative production output of the

old mines to the new mines. Operating cost and ongoing capital

maintenance costs were estimated for the years 1970 to 1979 based on

Kaiser Resources Annual Reports (Kaiser Resources, 1969–1979).

This cost data was used for all old southeast production based on the

assumption of a similar cost structure of the Kaiser and Fording coal

mines. Cost data for southeast mines for 1985 was obtained from BC

(1986) and for 1987 from Barnett (1987). Southeast mine cost data for

1989 to 1995 for southeast mines was obtained from IEA data

published in the annual series Coal Information (IEA, 1986–2000).

Cost data for the southeast mines for the years 1996 to 2000 was

obtained from Teck Annual reports for the Elkview mine (Teck

Corporation, 1980–2000). Southeast production costs for the years

1980 to 1985 were based on the 1979 operating cost data derived from

the Kaiser Annual Report inflated at the rate of inflation based on the

GNE price deflator. Northeast mine operating costs were taken from

the Annual Reports of Quintette (Quintette Coal Ltd., 1980–1991,

1991, 1996) and Teck for the respective years.

T. Gunton / Energy Policy 32 (2004) 151–163156

upward bias in rent estimates of including explorationcosts for only successful deposits.A fourth issue is that market imperfections can cause

observed estimates of rent to deviate from the potentialrent that would exist in a well functioning market. Onepotential market imperfection is that market power ofbuyers or sellers may result in the observed selling priceof coal deviating from its actual value. A study of rent inthe mineral sector by Hughes and Singh (1978), forexample, concludes that the purchasing power ofresource consuming nations may drive the mineralexport price below its competitive level. In effect, thepurchaser extracts some of the rent in the form of belowmarket purchase price. According to several studies, thismay also be a problem in the British Columbia coalindustry where the exercise of market purchasing powerby the JSI could result in the export price of coal beingsuppressed below competitive levels (Anderson, 1987;Parker, 1997).The issue of market power in the coal sector was

examined in several comprehensive studies. One studyby Schwindt (1989) used three common tests of marketstructure to assess competition: market concentrationratios, barriers to entry and market performance. Theresults showed that market concentration ratios weretoo low to allow the JSI to exert market power. Further,freedom of exit and entry exhibited in the coal marketby buyers and sellers indicated the absence of barriers toentry and market performance data were consistent withcompetitive market conditions. Based on these findings,Scwindt concluded that coal markets were competitiveand that the JSI was not able to affect coal prices. Asimilar conclusion that coal markets were competitivewas reached in a major study by the Australiangovernment (Industry Commission, 1990).Studies by Kittredge and Sivertson (1979), Kittredge

(1982), Gunton (1989) specifically examined pricing inthe coal market to determine if there was any evidenceof the JSI using market buying power to imposedifferential pricing by coal producer. Regression analy-sis of coal prices demonstrated that price differenceswere do exclusively to quality differences in the coal andthere was no evidence of distortions caused by marketpower. In similar studies of coal prices, Koerner (1993)and Chang (1995) found evidence that JSI buying powercould have resulted in Australian coal being under-priced and/or the Canadian coals marginally overpricedby a relatively small margin, although the evidence wasinconclusive.Overall, therefore, there is no evidence to suggest that

coal prices are affected by market power. However, thereview of price data in the studies did reveal a significantanomaly. The price paid for NECP coal was well abovecompetitive levels due to the structure of the NECP coalcontract (Fig. 3). In the NECP contract the price was seton the basis of a formula for the period 1980 to 1987 for

the largest NECP mine and to 1989 for the smaller mine.This price certainty provided by the contracts wasintended to reduce risk for the project developers. Afterthe price formula provision terminated, prices were setby negotiation on the basis of the then prevailingcompetitive market price. An arbitration process set theprice if negotiations were unsuccessful. This contractstructure was very different from the standard approachin JSI coking coal contracts, which determine pricesannually by negotiation between buyers and sellers(Horie, 1985).As Fig. 3 shows, the price for NECP coal remained

well above the competitive price for the duration of thecontract. During the first years of the contract thisexcess price paid for NECP coal was caused by the priceformula in the contract, which escalated the NECP pricewhile the market determined price for coal declined.After the expiry of the price provision, the above marketprice for NECP was due to the decision of thearbitration process. The result was that the transactionprice for NECP coal exceeded the market value for theduration of the contract. Therefore the estimate of coalrent includes a sensitivity analysis that uses thecompetitively determined market price of comparablecoal in place of the NECP transaction price to illustratethe impact of this market imperfectionA second potential market imperfection is that the

dependence of British Columbia coal mines on onerailway system creates the potential for transport costsbeing set above competitive levels. Some of the rent maytherefore show up as excess returns in the transportationsector. Barnett (1985), for example, found evidence ofthis is the Australian coal industry. Unfortunately thereis insufficient data to evaluate transport rates todetermine whether this is the case in BC. Therefore asensitivity analysis was done using an arbitrary 10%reduction in transport costs from the minehead to FOBat the port to demonstrate the impact of changes intransport costs on coal rent.A third potential market imperfection is that

production costs could be higher than necessary due topoor management. One common theory of the firmposits that instead of maximizing profits, firms earnsuboptimal returns by engaging in ‘‘satisficingbehavior’’ in the pursuit of non-pecuniary goalssuch as growth and remuneration within a profitconstraint. (Leibenstein, 1966; Baumol, 1966; William-son, 1974). Gunton and Richards (1987) found that thisproblem of ‘‘x-inefficiency’’ is especially acute inresource industries where rent acts as a cushion allowingfirms to achieve competitive rates of return whiledissipating a share of the rent in non-profit maximizingbehavior. Ellerman (1995) and Humphries (1995) alsofound evidence consistent with this theory in anexamination of productivity trends in the US coalindustry.

ARTICLE IN PRESST. Gunton / Energy Policy 32 (2004) 151–163 157

The trends in the BC coal industry appear to supportthis theory. The data on productivity and rates of returnin Fig. 4 show that during the period of high returns inthe 1970s, productivity gains were minimal. When ratesof return fell in the period 1984 to 2000, productivitybegan to improve, as the coal industry had to cut coststo maintain viability. The correlation coefficient be-tween rates of return and productivity growth over theperiod 1971 to 2000 is �0.54. Although more detailedanalysis is required to confirm this hypothesis, the trendin productivity provides strong circumstantial evidencethat production costs could have been lower throughoutthe period with more assiduous management. Conse-quently, a sensitivity analysis was done using anarbitrary 10% downward adjustment to costs toillustrate the magnitude of the impact of cost changeson coal rent.A fourth potential market imperfection is that coal

production could generate external costs such asenvironmental degradation that need to be included inthe cost function in order to provide an accuratemeasure of rent. A detailed estimate of external costsof NECP coal production was completed by the BritishColumbia government (BC, 1982). The results of thisstudy were used to estimate a per tonne environmentalcost of coal production. This was then applied to theentire BC coal sector in a sensitivity analysis to estimaterent net of environmental cost.The results summarized in Table 2 show that under

base case assumptions the British Columbia coal minesgenerated rent of $371.5 million (2000 Canadian $). Therent estimate under alternative assumptions variedbetween a high of $975.6 under the lower productioncost scenario to a negative value of $(80.5) using thecompetitive price for the NECP. The variation betweensectors was substantial. The old southeast minesgenerated a rent of $1108.1 million under the base caseassumptions while the new southeast and NECPincurred losses of $(140.3) million and $(596.4) million,respectively. It is also interesting to note while much ofthe rent was generated during the period of high coalprices in the 1970s, the old southeast mines continued togenerate rent throughout the entire period due to their

low cost structure. The sensitivity analysis on factorinput costs, discount rates and environmental costs donot significantly alter the findings. Under all scenarios,the old southeast mines generated large rents and thenew southeast and northeast mines incurred net costs.The next step in the rent estimate was to measure the

proportion of British Columbia coal rent that can becategorized as differential rent. Theoretically, differen-tial can be estimated by measuring the cost advantageenjoyed by intramarginal British Columbia minesrelative to the marginal coal mine. The challenge in thistype of estimate is that it is difficult to identify themarginal mine that just covers long run costs becausethe marginal mine will change over time and someoperating mines may be beyond the margin because theydo not cover long run costs. For example, comparingthe cost of intramarginal mines to mines such as theNECP mines that are beyond the economic marginwould over estimate differential rent. A second problemis that there is no accurate comparative cost time seriesthat can be used to estimate cost differences betweenoperating coking coal mines over the thirty-year periodunder review.Nonetheless, it is possible to provide an order of

magnitude estimate of differential rent in the BritishColumbia coal industry. For the purposes of thisestimate, the marginal producer in the coking coalmarket is defined as the United States, which Ellerman(1995) identifies as the swing or marginal supplier in theinternational export market. The cost advantage perunit of output of the British Columbia producers overthe United States producers is estimated by year basedon the data sources summarized.3 The cost advantage

ARTICLE IN PRESS

Table 2

Coal rents by sector, 1970–2000 (millions of 2000 Canadian $)

Sector

Old southeast New southeast Northeast Total

Base case 1108.1 (140.3) (596.4) 371.5

12% Discount rate 824.9 (118.2) (499.8) 206.8

8% Discount rate 1467.7 (162.5) (705.9) 599.3

Competitive price for NECP 1108.1 (140.3) (1048.4) (80.5)

Lower production cost (10%) 1503.8 (70.2) (458.0) (975.6)

Lower transport cost (10%) 1369.4 (98.3) (539.2) 731.9

Environmental cost included 999.0 (141.9) (598.0) 259.1

Differential rent estimate 1129.7 na na na

3The comparative cost data for the British Columbia and United

States coal mines is obtained from Barnett (1987) for the years 1983 to

1986 and from the IEA (1992–2000) for the years 1992 to 2000. The US

mine cost data is for the upper end cost for Appalachia surface mines.

Cost data is FOB at port and includes operating costs, capital costs

and transportation and port costs. Comparative costs for other years

from 1970 to 2000 is estimated by using the average for the years for

which data is available (1983 to 1986 and 1992 to 2000), adjusted each

year for changes in the Canadian/United States exchange rate. All

calculations were done in 2000 Canadian $.

T. Gunton / Energy Policy 32 (2004) 151–163158

per unit of output is then multiplied by production andcalculated as a net present value in year 2000 Canadian$ so that it is comparable to the rent estimates (Table 2).More formally the estimate of differential rent can besummarized as follows.

Differential rent ¼Xn

t¼0

ðCmt � CimtÞQt

ð1þ rÞt

Where Cmt is the cost of production per tonne in year t

for marginal mine, Cimt the cost of production per tonnein year t for the intramarginal mine, Q the quantity ofproduction in tonnes for year t, r the opportunity costcapital, t the year and n the number of years.The results summarized in Table 2 show that

differential rent for the original southeast producers is$1129.7 million (2000 Canadian $), which is almostidentical to the total rent estimate of $1108.1 (2000Canadian $). Although this is a rough estimate due tothe limitations cited above, it suggests that virtually allof the rent generated in British Columbia can becategorized as differential rent based on the costadvantage enjoyed by the original southeast producers.

5. Distribution of coal rent

The distribution of rents between competing stake-holders has been one of the principal public policy issuesin the energy sector. The coal model analyzes rentdistribution by disaggregating rent payments by threemajor recipients: the coal industry that receives rent inthe form of profits, the federal government that receivesrent in the form of corporate income tax payments andthe provincial government that receives rent in the formof corporate income taxes and coal royalties. Thefederal government corporate income tax is a relativelyconventional profit based tax based on an accountingprofits defined in the tax legislation. Brewer et al. (1999)provides details on the tax and its comparison tocorporate income taxes in other jurisdictions. The onesignificant feature of the Canadian corporate income taxsystem for the resource sector is the provision of aspecial resource allowance that exempts 25% ofcorporate profits from taxation as an implicit deductionfor royalties levied by provincial governments, which arenot explicitly deductible as an expense.Provincial corporate income taxes in BC are levied on

the same basis as the federal corporate income tax.Provincial coal mining taxes have gone through severalstages. Up until 1993, the mining taxes on coal consistedof two levies. One was a special royalty that initially wasdefined as a volumetric per tonne charge and later as anad valorem royalty calculated as 3.5% of the mineheadvalue of coal. The second tax was a mining taxcalculated as a percent of accounting profit as defined

in the tax legislation. In 1993, these mining taxes werereplaced with a new two-tier tax. The first tier was basedon a percentage of net income and the second tierapplied to only net income earned above a specified rateof return on the project. The second tier, therefore, wasdesigned to apply to only the rent proportion of theincome stream. The first tier was set at 2% and thesecond tier at 13%. These taxes were in addition tothe combined federal and provincial corporate incometax rates of 45%.The distribution of rents is shown in Table 3. For the

aggregate coal industry, the provincial and federalgovernments both earned rents while the private sectorlost $596 million. The disaggregated results show widevariations. For the original southeast mines, theprovince, which is the owner of the resource, received34% of the rent while the private mining companiesretained 43% as extra profit. The residual 23% accruedto the federal government as corporate income taxpayments. The payments from the original southeastmines to the federal government and the externallyowned producers, which comprised 66% of the rent,were leaked from the provincial economy. The resultsfor the NECP show that the JSI and the coal producersincurred 85% of the losses. The private sector losseswere almost evenly distributed between the JSI purcha-sers and the mining companies. The losses of JSIpurchasers largely consisted of payments for NECPcoal that were well above the competitive price. Thelong-term contract for NECP effectively transferredincome from JIS purchasers to coal producersThe data show that the rent collection regime for the

BC coal industry was not effective in meeting the threecriteria of equity, economic development and efficiency.For the highly profitable southeast sector, the owner ofthe resource, provincial government received only 34%of the in situ resource value. The leakage of theremaining 66% of the rent to the federal governmentand private sector constrained regional economicgrowth. The magnitude of employment loss associatedwith this leakage is estimated on the basis of employ-ment multipliers for the BC economy.4 The estimated

ARTICLE IN PRESS

Table 3

Distribution of coal rents by sector, 1970–2000 (millions of 2000

Canadian $)

Sector Province Federal Private sector

% $ % $ % $

Old southeast 34% $376 23% $255 43% $476

New southeast — — — — 100% $(140)

Northeast 15% $(174) — — 85% $(932)

Total $202 $255 $(596)

4The estimate of the employment impact of rent is based on

employment multipliers for government fiscal policy published in BC

T. Gunton / Energy Policy 32 (2004) 151–163 159

loss was 1400 jobs, which compares to direct employ-ment in the coal industry of 2400 jobs. Obviously, theeconomic impact of rent can be a significant andsometimes neglected factor.It is interesting to note that some of the economic loss

associated with the leakage of rent on the southeastmines was offset by the transfer of income from the JSIto the NECP producers in the form of payments for coalabove the international competitive price due to theterms of the long term coal contract. The payment of ahigher price reduced the losses of the NECP and keptthe uneconomic project in operation. This illustratesthat long term contracts can be an important factorreducing risk and instability for resource supplyingregions.The rent collection regime also had a negative impact

on efficiency in several ways. First, the method of rentcollection based on volumetric and ad valorem royaltiesincreased costs at the marginal mines, particularly in theNECP. Theoretically, this had the potential to imposean efficiency loss by reducing output below optimallevels. The empirical evidence on the impact of this typeof tax suggests that the efficiency loss at low rates of taxis small, however (Helliwell, 1978; Bradley et al., 1981;Rowse, 1997; Dahlhy, 1999). Second, to the extent thatother taxes in the economy may have been higher thanthey would have been if more rent was collected, theremay have been an efficiency loss equivalent to thedifference between the economic welfare cost of othertaxes and a less distorting rent collection tax (Dahlhy,1999).Third, the retention of rent by the private sector could

have reduced efficiency by acting as a subsidy thatallowed firms to earn competitive rates of return whileincurring higher than necessary production costs. Thehigher profits resulting from rent retention may alsohave increased the probability of uneconomic expansionas the lure of high profits generated excessivelyoptimistic expectations that encouraged both existingand new firms to expand production beyond theeconomic margin.The impact of dissipation of rent through higher

production costs on the regional economy is complex.To the extent that the dissipation is in the form of excesspayments to regional factors of production, the dissipa-tion of rent could actually increase aggregate regionaleconomic growth by reducing leakage of rent. On theother hand, the higher cost structure could reduceregional productivity and per capita income by ineffi-cient utilization of factors of production in the regionaleconomy. A higher cost structure could also increase

instability as coal firms shed excess employment duringdownturns to lower per unit costs. This shedding ofinefficiently utilized labor is in addition to laborreductions due to reduced production. In sum, a moreefficient coal sector would have employed fewer people,but would have been better able to withstand marketdownturns without requiring the same level of down-sizing.

6. Rent collection policy

The findings in the case study show that the BC coalindustry had the potential to generate up to $1.1 billionin rents. The study shows that most of this rent wasdissipated through investment in uneconomic capacityand higher than necessary production costs. In additionto dissipating rents, poor management of the coal sectoralso increased community instability by the closure ofuneconomic capacity in the NECP and the dramaticdownsizing of the labor force in the southeast mines tolower costs in the face of declining coal prices. If theNECP had not been built and if the southeast mines hadnot dissipated rent through higher than necessaryproduction costs, the industry would have been smallerbut the rent generated would have been significantlyhigher and the employment trends more stable.What are the policy lessons from this experience?

First, the owner of coal needs to implement moreeffective rent collection regimes. The failure to effec-tively collect rent in the profitable southeast coalindustry reduced regional economic income and con-tributed to overly optimistic expectations that encour-aged investment in uneconomic new capacity, purchaseof existing capacity at inflated prices and higherproduction costs. The attempt to collect rent onunprofitable high cost mines helped undermine theviability of the marginal mines and contributed toinstability.Methods for rent collection have been well canvassed

in the literature (Helliwell, 1978; Bradley et al., 1981;Rowse, 1997; Dahlhy, 1999; Garnaut and Clunies Ross,1983; Gunton and Richards, 1987; Otto, 1995; Byrne,1997; Figuerao, 1999). The consensus is that an effectiverent collection regime must distinguish between normalprofit and rent and apply to only the rent proportion ofthe income stream. The royalty must be sensitive tomarket cycles and leave a sufficient proportion of rentwith the private sector to ensure adequate incentives forefficiency.Volumetric and ad valorem royalties, such as the

3.5% coal royalty used in BC. are a poor techniquebecause they are insensitive to the rent generated byindividual mines. Ad valorem and volumetric royaltiescollected the same amount per tonne on the unprofitableNECP mines as on the highly profitable original

ARTICLE IN PRESS

(footnote continued)

(1999). The rent NPV is translated into an annual flow and the

employment multipliers are then applied to the annual flow to estimate

an average annual employment impact.

T. Gunton / Energy Policy 32 (2004) 151–163160

southeast mines. Consequently, they forego rent on theintramarginal mines and encourage high grading onmarginal mines by reducing production below optimallevels.Income taxes based on a proportion of accounting

profits, which were also used in the BC coal industry aretheoretically superior to ad valorem and volumetricroyalties because they are more sensitive to relativeprofitability of different mines. However, income basedtaxes can also cause distortions because they do notdistinguish between normal profits and rent.The preferred technique is a rate of return royalty,

which is levied on profits above a specified rate of returnrequired to compensate capital. The rate of returnroyalty is therefore applied to only rent. The two tiermineral royalty applied in 1990 is a hybrid rate of returnapproach. Although it is the preferred technique, thereare challenges that policy makers must address in thedesign of rate of return systems. Rate of return royaltiesrequire more detailed information and are thereforeharder to administer and enforce. Revenue is also lessstable than other kinds of resource taxes. The specifica-tion of the ‘‘normal’ risk adjusted rate of return and therate of taxation are also problematic. If the rate ofreturn is set too high, excess capital will be invested andif it is set too low, marginal investments will bediscouraged. If the rate of taxation on rent is set highthere is little incentive for efficiency by private firmsafter the normal profits have been earned and if the rateis too low, the royalty will forgo rent for the publicowner.An equally challenging policy issue is the allocation of

rent after it is collected. The case study of coal showsthat it is possible that retention of rent by the privatesector can reduce regional income and can encourageinefficient behavior that dissipates rent. In a series ofstudies of rent collection by the public sector, Auty(1998, 2001) showed that collection of rent by publicowners can also be dissipated by inefficient expendituresthat can lower income and restrain growth. Unstablerevenue flows can be overcommitted during boom timesto fund dubious projects or unsustainable programs thatcan not be cut when revenues decline. Resource richeconomies that capture rents can also become over-heated with factor prices and currency exchange ratesbeing bid up to a point where diversification in newinvestments is hampered.Several mechanisms have been proposed for mitigat-

ing these problems. One suggested by Auty (2001) is toplace resource revenues is a special stabilization fundand set the flow of expenditures based on a long-termaverage estimation of expected resource revenues. Thishelps avoid the tendency of overcommitting funds andoverheating the economy based on short-term windfalls.However, as Davis et al. (2001) argue, the managementof such funds is challenging due to the difficulty of

determining future average revenues and resisting shortterm political pressures to spend.A second mechanism is to distribute a proportion of

resource revenues directly to the citizenry in the form ofa resource dividend. Gunton and Richards (1987) arguethat this allows the market to determine the expenditureof the rent and creates a constituency to lobby foreffective rent collection. Without a strong constituencylobbying for rent collection, effective rent collectionregimes are difficult to maintain because the benefits ofrent collection are normally not transparent and the percapita perceived benefits are too small to motivate thegeneral public to lobby for more aggressive rentcollection. The pressure against effective rent collectionis usually stronger because the benefits of weak rentcollection often accrue to a small number of investorswho consequently have a strong motivation to lobbyagainst collecting rents. The high transparency of aresource dividend paid directly to the public helpsovercome this imbalance.The second and even more important policy lesson

from the coal experience is the need to maximize rentsby avoiding investments in uneconomic capacity andhigher than necessary production costs. Public policyneeds to be more risk averse by limiting infrastructureand other financial support for resource projects. If thegovernment did not help fund infrastructure for theNECP, the project would likely not have proceeded andthe dissipation of rent would have been avoided. Whenpublic infrastructure is required due to economies ofscale or external benefits, investments should only beprovided after independent reviews and based on theprinciples of full cost recovery.There also needs to be a better appreciation of market

fundamentals by both private sector investors andpublic planners. Resource commodity markets arenotoriously unstable with long lead times to developnew supply and absorb excess capacity. Resourcecommodity markets are therefore characterized by longbooms followed by long downturns as new supply isdeveloped in response to higher prices. As the develop-ment of the BC coal industry shows, the booms cancreate excessively optimistic expectations that encouragenew firms with limited experience to enter the industryand build surplus capacity. Given past experience,investors need to err on the side of pessimism to avoidmisinterpreting short-term windfall rents as permanentchanges in the market.

7. Conclusion

The analysis of the BC coal industry shows that thecoal sector is capable of generating significant rent.However, the pattern of development in the coal sectorfollowed what can be termed a ‘‘rent dissipation cycle’’

ARTICLE IN PRESST. Gunton / Energy Policy 32 (2004) 151–163 161

in which generation of rent in the profitable sectorduring a commodity boom created excessively optimisticexpectations that encouraged expansion beyond theeconomic margin to the point where most of the rentwas dissipated. The development of excess capacity lefta legacy of debt and high cost structure that resulted in acostly restructuring of the industry and communityinstability. If the industry had avoided this uneconomicexpansion, rent would have been substantially higherand employment more stable. A further problem wasthat the rent collection regime collected only one-thirdof the rent for the public owner on the highly profitablesoutheast mines and over taxed the high cost NECPmines where no rent was generated. The leakage ofuncollected rent from the province reduced economicgrowth and could have contributed to inefficiencies inthe industry.Better planning by both the private and public

sector is required to increase the benefits of resourcedevelopment and avoid the rent dissipation cycle.First, investors must have a better appreciation ofresource market fundamentals by avoiding the forma-tion of exuberant expectations based on the misinter-pretation of short-term commodity booms as apermanent structural change in industry funda-mentals. Given past experience, investors need to erron the side of pessimism. Second, governments mustresist fueling unrealistic expectations by providingfinancial incentives or subsidized infrastructure thatencourages uneconomic expansion. Finally, govern-ments need to use more effective rent collectiontechniques. More effective rent collection would haveincreased regional economic growth by reducing leakageand increased stability by avoiding over taxation of themarginal coal mines. It is also possible that moreeffective rent collection could have reduced the prob-ability of investing in uneconomic capacity by dampen-ing unrealistic investor expectations. To be successfulrent collection must be based on a rate of return systemthat is focused on rent instead of ‘‘normal profits’’, issensitive to market cycles and leaves sufficient incentivefor the private sector. Rent must also be distributed in away that avoids wasteful and unsustainable publicexpenditures.As a final methodological note, the case study

illustrates that it is essential to dissaggregate rentestimates by sector. If coal rent had been estimated onan aggregate basis for the BC coal sector, the conclusionwould have been that there was no rent and the benefitsof better management to avoid rent dissipation by theuneconomic expansion in the northeast would have goneunnoticed. Second, it is important to make adjustmentsfor market failure. The sensitivity analysis of alternativemarket assumptions illustrates that there can be a widevariation between observed rent and actual rent basedon mitigation of market failures.

Acknowledgements

I would like to thank Dr. Denny Ellerman, Centerfor Energy and Environmental Policy Research, MITfor helpful suggestions on an earlier draft of thisarticle.

References

Anderson, D.L., 1987a. An Analysis of Japanese Coking Coal

Procurement Policies: the Canadian and Australian Experience.

Centre for Resource Studies, Kingston, Ontario.

Anderson, D.L., 1987b. Innovation in Public Rent Capture: the

saskatchewan uranium industry. In: Gunton, T., Richards, J.

(Eds.), Resource Rents and Public Policy in Western Canada.

Institute for Research on Public Policy, Halifax, pp. 147–181.

Anderson, D.L., 1990. Subsidy measurement problems in new mining

projects. Resources Policy 16, 162–171.

Auty, R.M., 1998. Sustainable Development in Mineral Economies.

Oxford, Clarendon Press.

Auty, R.M., 2001. Resource Abundance and Economic Development.

Oxford, Oxford University Press.

Barnett, D.W., 1985. Export coal costs in Australia, Canada, South

Africa and the USA. Materials and Society 9, 461–478.

Barnett, D.W., 1987. Comparative Costs of Export Coal in Australia,

Canada, South Africa and the USA. In: Barnett, D.W., Calarco,

V.J., McCloskey, G. (Eds.), World Coal Outlook 87. Mcquarie

University, Sydney Australia, pp. 135–156.

Baumol, W.J., 1966. Business Behavior, Value and Growth. Harcourt

and Bruce, New York.

Bradley, P., Helliwell, J., Livernios, J., 1981. Efficient Taxation of

Resource Income, the Case of Copper Mining in British Columbia.

Resources Policy 7, 161–170.

Brewer, K., Bergeris, G., Araseneau, L., 1999. Mineral policy and

comparative and taxation regimes for mining. In: Figuero, B. (Ed.),

Economic Rents and Environmental Management in Mining and

Natural Resource Sectors. University of Alberta, Edmonton,

pp. 245–277.

BC, British Columbia. 1982. A Benefit–Cost Analysis of the North

East Coal Project. Ministry of Industry and Small Business

Development, Victoria.

BC, British Columbia. 1986. Coal in British Columbia. Ministry of

Energy, Mines and Resources, Victoria.

BC, British Columbia. 2000. Coal Statistics. Ministry of Energy and

Mines, Victoria.

Byrne, P. (Ed.), 1997. Global Mining Taxation Comparative Study.

Colorado School of Mines, Golden, Colorado.

Cairns, R.D., 1982. Measure of resource rent: an application to

canadian nickel. Resources Policy 8, 109–116.

Chang, H.S., 1995. Examining hard coking coal price differentials.

Resources Policy 21, 275–281.

Coal Association of Canada, 1987. 1990. British Columbia Coal

Industry in Review. Vancouver, BC.

Copithorne, L., 1979. Natural Resources and Regional Disparities.

Economic Council of Canada, Ottawa.

Dahlhy, B., 1999. Taxation of the Mining Sector in Canada. In:

Figuerao, B. (Ed.), Economic Rents and Environmental Manage-

ment in Mining and Natural Resource Sectors. University of

Alberta, Edmonton, pp. 273–299.

Davis, J., et al., 2001. Stabilization and Savings Funds for Non-

Renewable Resources. International Monetary Fund, Washington,

DC.

Ellerman, D., 1995. The world price of coal. Energy Policy 23,

499–506.

ARTICLE IN PRESST. Gunton / Energy Policy 32 (2004) 151–163162

Figuerao, B., (Ed.), 1999. Economic Rents and Environmental

Management in Mining and Natural Resource Sectors. University

of Alberta, Edmonton.

Garnaut, R.G., Clunies Ross, A.I., 1983. Taxation of Mineral Rents.

Clarendon Press, Oxford.

Gunton, T.I., Richards, J. (Eds.), 1987. Resource Rents and Public

Policy in Western Canada. Institute for Research on Public Policy,

Halifax.

Gunton, T.I., 1989. Critique of the JSI Conspiracy Allegation. Mimeo,

Vancouver.

Halvorson, H.N., 1980. New Coal Production from Southeastern B.C.

Compared with Proposed Northeastern B.C. Development. A

Study for the Council of Mayors of Southeastern B.C. Mimeo,

Vancouver.

Helliwell, J., 1978. Effects of Taxes and Royalties on Copper Mining

Investment in British Columbia. Resources Policy 4, 35–44.

Horie, H. (Ed.), 1985–1999. Coal Manual. Tex Report Ltd., Tokyo.

Humphries, D., 1995. Comment on the paper by denny ellerman.

Energy Policy 23, 507–509.

Hughes, H., Singh, S., 1978. Economic rent: incidence in selected

metals and minerals. Resources Policy 4, 135–145.

Industry Commission, 1990. Mining and Mineral Processing in

Australia. AGPS. Canberra, Australia.

IEA, International Energy Association, 1986–2000. Coal Information.

Paris: OECD.

IEA, International Energy Association. 1997. International Coal

Trade: the Evolution of a Global Market. Paris: IEA.

Jenkins, G., 1977. Capital in Canada: Its Social and Private

Performance. Discussion Paper no. 98, Economic Council of

Canada. Canada: Ministry of Supply and Services, Ottawa.

Jones, R.J., Sivertson, L.E., 1979. Pacific Rim Metallurgical Coal

Market Survey. Victoria: NECP Economic, Finance and Market-

ing Analysis Sub-Committee. Victoria, BC. Mimeo.

Kaiser Resources, 1969–1979. Annual Report. Vancouver, BC.

Kemp, A.G., 1992. Petroleum policy issues in developing countries.

Energy Policy 20, 104–115.

Kierans, E., 1973. Report on Natural Resources Policy in Manitoba.

Winnipeg, Government of Manitoba, Manitoba.

Kittredge, P., Sivertson, L., 1979. Competition and Canadian Coking

Coal Prices in the Japanese Market. Research Report No. 1. BC

Ministry of Economic Development, Victoria.

Kittredge, P., 1982. The Current Market Value of British Columbia

Coals. Ministry of Industry and Small Business, Victoria.

Koerner, R.J., 1993. The behavior of pacific metallurgical coal

markets: The impact of japan’s acquisition strategy on market

price. Resources Policy 19, 66–80.

Leibenstein, H., 1966. Allocative efficiency vs. X-inefficiency. Amer-

ican Economic Review 56, 392–415.

Otto, J. (Ed.), 1995. Taxation of Mineral Enterprises. Kluwer

Academic Publishers, Dordrecht.

Parker, P., 1997. Canada–Japan coal trade: an alternative form of the

staple production model. Canadian Geographer 41, 248–267.

PricewaterhouseCoopers, 1992–1999. Mining Industry in British

Columbia. Vancouver, BC.

Quintette Coal Ltd., 1980–1991. Annual Report. Vancouver, BC.

Quintette Coal Ltd., 1991. Quintette Development Plan Update.

Mimeo, Vancouver.

Quintette Coal Ltd., 1996. Economic Analysis Volume 3. Mimeo,

Vancouver.

Richards, J., 1987. The Saskatchewan Potash Industry. In: Gunton, T.,

Richards, J. (Eds.), Resource Rents and Public Policy in Western

Canada. Institute for Research on Public Policy, Halifax,

pp. 119–147.

Rowse, J., 1997. On ad valorem taxation of nonrenewable resource

production. Resource and Energy Economics 19, 221–239.

Rutledge, I., Wright, P., 1998. Profitability and taxation in he

ukcs oil and gas industry: analysing the distribution of

rewards between company and country. Energy Policy 26,

795–811.

Schwindt, R., 1989. Background Memorandum in the Matter of

Nippon Steel v. Quintette Coal. Mimeo, Vancouver.

Siverston, L.E., Clancy, J., 1976. Resource Depletion and Coking Coal

Prices. Institute for Economic Policy Analysis, Victoria.

Teck Corporation, 1980–2000. Annual Report. Vancouver.

Williamson, O.E., 1974. Managerial Objectives in a Theory of the

Firm. Kershaw, London.

ARTICLE IN PRESST. Gunton / Energy Policy 32 (2004) 151–163 163

Copyright © 2022 FDOKUMEN