Enabling Responsible Banking through the Application ... - Cairn

34

ENABLING RESPONSIBLE BANKING THROUGH THE APPLICATION OF BLOCKCHAIN Paul David Richard Griffiths , Patricia Baudier De Boeck Supérieur | « Journal of Innovation Economics & Management » 2022/0 Prépublication | pages I à XXXIII Article disponible en ligne à l'adresse : -------------------------------------------------------------------------------------------------------------------- https://www.cairn.info/revue-journal-of-innovation-economics-2022-0-page-I.htm -------------------------------------------------------------------------------------------------------------------- Distribution électronique Cairn.info pour De Boeck Supérieur. © De Boeck Supérieur. Tous droits réservés pour tous pays. La reproduction ou représentation de cet article, notamment par photocopie, n'est autorisée que dans les limites des conditions générales d'utilisation du site ou, le cas échéant, des conditions générales de la licence souscrite par votre établissement. Toute autre reproduction ou représentation, en tout ou partie, sous quelque forme et de quelque manière que ce soit, est interdite sauf accord préalable et écrit de l'éditeur, en dehors des cas prévus par la législation en vigueur en France. Il est précisé que son stockage dans une base de données est également interdit. Powered by TCPDF (www.tcpdf.org) © De Boeck Supérieur | Téléchargé le 25/08/2022 sur www.cairn.info (IP: 65.21.229.84) © De Boeck Supérieur | Téléchargé le 25/08/2022 sur www.cairn.info (IP: 65.21.229.84)

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Enabling Responsible Banking through the Application ... - Cairn

ENABLING RESPONSIBLE BANKING THROUGH THE APPLICATION OFBLOCKCHAIN

Paul David Richard Griffiths, Patricia Baudier

De Boeck Supérieur | « Journal of Innovation Economics & Management »

2022/0 Prépublication | pages I à XXXIII

Article disponible en ligne à l'adresse :--------------------------------------------------------------------------------------------------------------------https://www.cairn.info/revue-journal-of-innovation-economics-2022-0-page-I.htm--------------------------------------------------------------------------------------------------------------------

Distribution électronique Cairn.info pour De Boeck Supérieur.© De Boeck Supérieur. Tous droits réservés pour tous pays. La reproduction ou représentation de cet article, notamment par photocopie, n'est autorisée que dans leslimites des conditions générales d'utilisation du site ou, le cas échéant, des conditions générales de lalicence souscrite par votre établissement. Toute autre reproduction ou représentation, en tout ou partie,sous quelque forme et de quelque manière que ce soit, est interdite sauf accord préalable et écrit del'éditeur, en dehors des cas prévus par la législation en vigueur en France. Il est précisé que son stockagedans une base de données est également interdit.

Powered by TCPDF (www.tcpdf.org)

© D

e B

oeck

Sup

érie

ur |

Tél

écha

rgé

le 2

5/08

/202

2 su

r w

ww

.cai

rn.in

fo (

IP: 6

5.21

.229

.84)

© D

e Boeck S

upérieur | Téléchargé le 25/08/2022 sur w

ww

.cairn.info (IP: 65.21.229.84)

Enabling Responsible Banking through the

Application of Blockchain

Paul David Richard GRIFFITHSEM Normandie Business School

Metis Lab, Francepgriffiths@ em -normandie .co .uk

Patricia BAUDIEREM Normandie Business School

Metis Lab, Francepbaudier@ em -normandie .fr

ABSTRACTBehaving responsibly is a priority for all businesses including, of course, the banking sector. The United Nations Principles for Responsible Banking (PRB), launched in 2019, pursue six internal and external objectives. The aim of this paper is to give an overview of the PRB and to investigate how an innovation such as the blockchain could contribute to achieving the UN objectives. Our research uses a qualitative method, based on the Knowledge Café as a data collection tool, enabling us to draw on the experience of ten experts in the banking and/or blockchain domains. Our data analysis iden-tifies a series of nine key concepts that cut across the six PRB. The main findings of our study shed light on the importance of transparency, trust, and the involvement of all stakeholders in the implementation of blockchain solutions within banks. However, there are some barriers to implementation, such as the energy consumption of blockchain, misunderstanding and a need for education on this disruptive technology, and the quality of data. We con-clude by presenting the theoretical and managerial implications of our study, including their impact on the funding of SMEs. KEYWORDS: Responsible Banking, Blockchain, Traceability, Fintech, Sustainability, Transparency, Technological Innovation, Innovation, Financial Services

JEL CODES: G21, M48, N20, O33

The UN-promoted Principles for Responsible Banking (PRB) were launched by 132 banks from 49 countries, representing more than US$-47

pre-published – Journal of Innovation Economics & Management 2022 I

© D

e B

oeck

Sup

érie

ur |

Tél

écha

rgé

le 2

5/08

/202

2 su

r w

ww

.cai

rn.in

fo (

IP: 6

5.21

.229

.84)

© D

e Boeck S

upérieur | Téléchargé le 25/08/2022 sur w

ww

.cairn.info (IP: 65.21.229.84)

trillion in assets, on September 22nd and 23rd 2019, during the annual United Nations General Assembly held in New York City. The PRB, largely aimed at combatting the climate crisis by persuading banks to shift their loan books away from fossil fuels as sources of energy1, were drawn up by UN officials and representatives from 30 banks. It took over eighteen months for the task-force, headed up by Simone Dettling of the Geneva-based United Nations Environmental Protection-Financial Initiative (UNEP-FI), to arrive at a final proposal. It is illustrative of the difficulties that were faced that the principles have been defined as voluntary and non-binding. In effect, the agreement requires banks to consider the impact of their loans not only on their finan-cial portfolio but also on society, and it defines six principles for signatory banks to comply with. These six principles have internal and external objec-tives. Externally, the principles work toward banks enticing their customers to adopt sustainable practices aligned with the 2015 Paris Agreement emis-sions reduction goals. On the internal front, the principles relate to target setting and seek to promote effective corporate governance and a culture of responsible banking (i.e. mindfulness of stakeholders and greater transpar-ency and accountability). Over and above the difficulty of designing the PRB and persuading banks to adhere to them, there is the challenge of enforcing their application by those banks that have accepted the costs, as well as the benefits, of doing so. As we discuss in the later stages of this paper, adhering to the principles will imply significant changes in bank operations, particu-larly in the processes associated with loan origination, the monitoring of the implementation and maintenance of all the greenhouse gas emissions (GHG) prevention and mitigation actions defined by the bank as terms for the loans made to clients, and in producing the reports required by the prin-ciples for the different stakeholder groups to a high standard. Many of these processes will require complex activities, such as the development of envi-ronmental impact studies, beyond traditional bankers’ comfort zones, and be organizationally boundary-spanning and thus hard to control.

There has been a proliferation of applications for trading in the financial markets within the financial services sector. These include applications used in the instant payments markets, to facilitate financial inclusion, to manage high-quality liquid assets and the related topic of collateral mobility, as well as many other initiatives where the efficiency, integrity, security, transpar-ency, traceability, speed, and resilience of processes underlying financial transactions, such as ‘Know Your Customer’ (KYC), are required (Demarco, 2019; Manif, Marsh, 2017; Sostakaite, 2019). Digitalization is critical to main-taining inter-organizational relationships and enhancing innovation (Kin et

1. https:// www .unepfi .org/ banking/ bankingprinciples/

II Journal of Innovation Economics & Management 2022 – pre-published

Paul David Richard Griffiths, Patricia Baudier

© D

e B

oeck

Sup

érie

ur |

Tél

écha

rgé

le 2

5/08

/202

2 su

r w

ww

.cai

rn.in

fo (

IP: 6

5.21

.229

.84)

© D

e Boeck S

upérieur | Téléchargé le 25/08/2022 sur w

ww

.cairn.info (IP: 65.21.229.84)

al., 2021). Through automation, banks can focus on added-value tasks while at the same time reducing costs (Biot-Paquerot et al., 2021). Indeed, disruptive innovations (e.g. Software as a Service) can be viewed as leading to lower costs (Ashta, Patel, 2013). However, the Janus face of finance: one turned toward the past and the other to the future, should be considered when implementing innovations within the finance sector (Laperche, Burger-Hemchen, 2019).

Disruptive technologies such as blockchain can support the banking sector by providing transparency, traceability etc. There are three types of blockchain: (1) the public permissionless blockchain visible to everyone on the Internet that anyone can join, control, or add a block of transactions to an existing blockchain; (2) the public permissioned blockchain that is visible to everyone where all contributors are known but not necessarily trusted; (3) the private permissioned blockchain that does not require public visi-bility/verifiability and all contributors are known but not necessarily trusted (Casino et al., 2019; Wüst, Gervais, 2018).

The transformational impact of blockchain on business models and ecosystems is important (Schneider et al., 2020). Turk and Kline (2017), for example, investigated the potential of blockchain in information manage-ment. This technology can provide an entire data history, including any modifications made. Smart or insurance contracts are just some of the appli-cations of the second generation of blockchain, transforming services and improving processes. Often ignored by firms with a low adoption rate of innovative technologies, blockchain solutions are now used in various indus-trial sectors. A recent study highlights the relationship between the banking sector and blockchain technology (Chang et al., 2020; Cong et al., 2021; Garg et al., 2021) and the impact of this on the banking sector and sustainability (Badunenko et al., 2020; Moufty et al., 2021). However, as far as we know, there has been no study that covers the topic of the PRB and blockchain.

The PRB are in the early stages of being adopted and implemented. Therefore, the aim of this study is to address the following questions: Would the application of blockchain-based solutions facilitate the implementation of the PRB? If so, how could this be achieved?

To address the research questions raised, we interviewed ten experts in blockchain and/or banks.

The article is organized as follow: in the following section, the literature on the PRB and on the potential benefits of blockchain for the banking system in general is reviewed. A Methodology section follows, after which our results are presented and discussed. Finally, we present the theoretical and managerial implications of our study.

pre-published – Journal of Innovation Economics & Management 2022 III

Enabling Responsible Banking through the Application of Blockchain

© D

e B

oeck

Sup

érie

ur |

Tél

écha

rgé

le 2

5/08

/202

2 su

r w

ww

.cai

rn.in

fo (

IP: 6

5.21

.229

.84)

© D

e Boeck S

upérieur | Téléchargé le 25/08/2022 sur w

ww

.cairn.info (IP: 65.21.229.84)

Literature Review

Background to the Principles of Responsible Banking

It is perhaps ironic that a set of principles for banking issued and agreed upon by a significant proportion of society should be called ‘PRB’. Did society tolerate irresponsible banking before that point? The reality is that the role of banks in society has expanded significantly over the years as society has come to expect players in the banking system to take on many of the functions that were originally developed or should have been exercised by the state. This is an indication that banks have, in accordance with the premises of the knowledge economy, become socially and physically integrated into the com-munities they serve to become responsible by adopting an ethical approach to their business and customers (Relano, Paulet, 2016). The public disclosure by banks of their Environmental, Social and Governance (ESG) practices, at both a financial or non-financial level (Jensen, Berg, 2012), can favour-ably impact the performance of European banks in terms of their Return on Assets or on Equity and their market valuation according to Buallay (2018). ESG reports can, by providing greater transparency, enhance companies’ reputation and provide them with a competitive advantage (Simnett et al., 2009; Eccles et al., 2015). But Corporate Social Responsibility (CSR) stan-dards are not static, as expectations evolve over time and as new stakeholders come to the fore. Several studies on the banking sector have analyzed the impact of CSR on the efficiency (Belasri et al., 2020), loans (Francis et al., 2016), reputation (Lorena, 2018) or financial performance (Zhou et al., 2021) of banks.

The changing role of banks in modern times and, in particular, the evolu-tion from an industrial economy to a knowledge economy can be observed through the lens of stakeholder management theory. Stakeholders are defined as ‘any group or individual who can affect or is affected by the achievement of an organizational purpose’ (Freeman, 2010, p. 53) or that contribute, voluntarily or involuntarily, to the value creation process of the company and are either ‘beneficiaries or risk bearers’ of its activities (Post et al., 2002). CSR calls for a stakeholder-centred approach to management, which does not mean that an organization will satisfy all the expectations of every stakeholder group. Quite the contrary, in fact. It means that the organization is sensitive to the impact of its activities on different stakeholder groups and uses that knowl-edge to define its priorities. One of the interesting aspects of CSR is precisely the fact that stakeholder groups have opposing interests (Bhattacharya et al., 2009; Venturelli et al., 2018). During the early industrial economy, the key stakeholders for banking were its shareholders (Kusi et al., 2018) and its clients

IV Journal of Innovation Economics & Management 2022 – pre-published

Paul David Richard Griffiths, Patricia Baudier

© D

e B

oeck

Sup

érie

ur |

Tél

écha

rgé

le 2

5/08

/202

2 su

r w

ww

.cai

rn.in

fo (

IP: 6

5.21

.229

.84)

© D

e Boeck S

upérieur | Téléchargé le 25/08/2022 sur w

ww

.cairn.info (IP: 65.21.229.84)

(Demetriades, 2018; Shaikh et al., 2019). In the later industrial economy, when certain banks became systemically critical and ‘too big to fail’, the taxpayer became a significant stakeholder (Kane, 2018; Massoc, 2020). As Western society transitioned from an industrial to a knowledge economy, banks were given a ‘policing’ role, with responsibility for fraud detection (e.g. AntiMoney Laundering, AML), with security forces and fiscal authorities added as key stakeholders (Hartsink, 2018; Marsh, 2019; Metzger, Paulowitz, 2018). The current era is known as the ‘banker as environmentalist’ era, in which governmental environmental authorities and environmental NGOs have become key stakeholders to whom banks owe environmental protection responsibilities which are delivered through activities such as environmental impact assessments of project loans and the monitoring of the honouring of GHG emissions mitigation commitments throughout the lifecycle of a loan.

The history of the engagement of banks with the climate crisis and cli-mate risk initiatives is long and incremental as shown in Figure 1, culmi-nating in the recently-issued PRB.

Figure 1 – History of banks’ engagement with climate change initiatives

Principles of Responsible Banking

As shown in Figure 1, it took nearly twenty eight years to arrive at these Principles, which require banks to consider the impact of their loans not only on their financial portfolio but also on society. The six principles are sum-marized as follows:

• PRB1. Align their credit origination criteria with the 2015 Paris Agreement targets to contain and eventually reduce anthropogenic global warming• PRB2. Set targets to increase ‘positive impacts’ and reduce ‘negative impacts’ on people and the environment

pre-published – Journal of Innovation Economics & Management 2022 V

Enabling Responsible Banking through the Application of Blockchain

© D

e B

oeck

Sup

érie

ur |

Tél

écha

rgé

le 2

5/08

/202

2 su

r w

ww

.cai

rn.in

fo (

IP: 6

5.21

.229

.84)

© D

e Boeck S

upérieur | Téléchargé le 25/08/2022 sur w

ww

.cairn.info (IP: 65.21.229.84)

• PRB3. Work with their customers to encourage sustainable practices• PRB4. Consult, engage and partner with relevant stakeholders to achieve society’s goals• PRB5. Implement their commitment to the Principles through devel-oping effective governance and a corporate culture of responsible banking• PRB6. Be transparent on how they report their progress and be accountable for outcomes. According to Reuters (Green, 2019)2, critics of the accord ‘argue that banks

should go much further by explicitly committing to phasing out financing for fossil fuel projects and agribusiness that drive deforestation in the Amazon, Southeast Asia and other regions’. The fact that the agreement is a step in the right direction but modest in its ambition could be another indication of how inadequate the nation-state as a political organization has become for tack-ling global problems. In this case, it is quite evident that the nation-states have delegated responsibility to an international institution (UNEP-FI) and a group of banks that act internationally to define a vital policy, i.e. the con-tainment of the climate crisis. Incidentally, Bloomberg points out that only three of the largest ten banks in the world by assets (i.e. Citigroup, Mitsubishi UFJ Financial Group and Industrial & Commercial Bank of China) have signed up (Kishan, Chasan, 2019)3.

So, is the introduction of the PRB just an exercise to make society feel as if something is being done, but that will have no practical effect? According to Bloomberg, in a discussion forum held on September 19th, 2019, Satya Tripathi, Assistant Secretary General of the UN, stated that the fact that the largest banks had not signed up indicates that the agreement has teeth and the banks do not wish to be held accountable for their lending policies (Kishan, Chasan, 2019)3. That the signatory banks have invested a significant effort in this exercise reflects at least two further factors. First, banks have not yet recovered from the severe loss of trust from the public, from banking regulators and authorities and from governments that resulted from the 2008 financial crisis. The sight of governments using taxpayers’ money to rescue these corporate behemoths whose leaders maintained most of their privi-leges has had a devastating and durable effect on their standing in society (European Central Bank, 2016; European Commission, 2015; Griffiths, 2020; Haddad, Hornuf, 2019). The PRB therefore provide an opportunity for them

2. GREEN, M. (2019), Banks Worth $47 Trillion Adopt New U.N.-backed Climate Principles, Reuters, https:// www .reuters .com/ article/ us -climate -change -un -banks -idUSKBN1W70QO3. KISHAN, S., CHASAN, E. (2019), Biggest Banks Sit Out New Industry Commitment on Climate Goals’, published on Bloomberg.com on September 22, 2019. Retrieved from https:// www .bloombergquint .com/ business/ biggest -banks -sit -out -new -industry -commitment -on -climate -goals

VI Journal of Innovation Economics & Management 2022 – pre-published

Paul David Richard Griffiths, Patricia Baudier

© D

e B

oeck

Sup

érie

ur |

Tél

écha

rgé

le 2

5/08

/202

2 su

r w

ww

.cai

rn.in

fo (

IP: 6

5.21

.229

.84)

© D

e Boeck S

upérieur | Téléchargé le 25/08/2022 sur w

ww

.cairn.info (IP: 65.21.229.84)

to be seen as taking a key role in diverting investments away from green-house gas-emitting sectors towards elements of a green economy. Second, as a result of the 2008 crisis, governments and regulators have passed tough new regulations in terms of capital and liquidity to fend off the excesses of the past. These include the Dodd-Frank Act in the United States and a series of international regulations, BISIII. There is speculation that these regulations will evolve to incorporate climate risk, so banks are keen to demonstrate that they are capable of self-regulation (Zou et al., 2015).

Blockchain in Banking

Fintech, the association of finance with technology, has changed the landscape of the traditional financial industry by providing new and innova-tive technologies such as blockchain-based solutions (Brem et al., 2017) and by accelerating the fourth industrial revolution in the finance field (Su et al., 2020). One of the most well-known applications of blockchain is that of cryptocurrencies (e.g. bitcoin), invented by Satoshi Nakamoto in 2008. Banks play a key role in fintech, especially when it comes to the adoption of new technologies such as blockchain. However, before being adopted by banks, blockchain needs to demonstrate its robustness and reliability. Several banks (e.g. Bank of America) have deposited patents related to blockchain.

Benefits of Blockchain for Banks

Blockchain offers a number of benefits for banks, such as: (1) Security: the blockchain, as a decentralized system, is considered as immutable and unal-terable (Yoo, 2017). Blockchain is based on the encryption of information using a security code. (2) Control: each stakeholder can access their informa-tion and check whether something untoward has happened. (3) Real time recoding and validation: transactions are recorded in real time and all records must be validated by all the actors involved in that blockchain. This pro-cess automatically lowers the risk of fraudulent transactions. (4) Efficiency improvement: Blockchain’s tamper-proof characteristics enable banks to improve their back-office efficiency and infrastructure. (5) Avoidance of anti-money laundering: other research asserts that blockchain could be an anti-money-laundering tool as all transactions are registered and cannot be altered (Lai, 2018). (6) Cost and time reduction: Blockchain solutions allow for the removal of trusted third parties, eliminating the need for intermedi-aries in favour of peer-to-peer based transactions, consequently decreasing both the cost and the time taken (Kim, Laskowski, 2017; Shermin, Kalinov, 2017; Tapscott, Tapscott, 2017). (7) Anonymity: one of the main principles of blockchain is the guarantee of anonymity of users as they can decide to keep

pre-published – Journal of Innovation Economics & Management 2022 VII

Enabling Responsible Banking through the Application of Blockchain

© D

e B

oeck

Sup

érie

ur |

Tél

écha

rgé

le 2

5/08

/202

2 su

r w

ww

.cai

rn.in

fo (

IP: 6

5.21

.229

.84)

© D

e Boeck S

upérieur | Téléchargé le 25/08/2022 sur w

ww

.cairn.info (IP: 65.21.229.84)

their identity secret by using an alphanumeric address, reducing the risk of privacy leakage.

Hurdles Posed by Blockchain

Nevertheless, blockchain is not yet widely adopted by banks, as some potential disadvantages have been identified: (1) Lack of regulation: due to the popularity of the use of blockchain worldwide many countries have decided to regulate it to reduce potential fraud (Till et al., 2017). Some countries have decided that the use of cryptocurrency within their frontiers should be made illegal (Desmond et al., 2019). What would happen in the event of failure or bankruptcy? Which laws and regulations would apply? The lack of laws and regulations could slow down the implementation of blockchain solu-tions (Andolfatto, 2018). (2) Scalability: Jackson (2018) found that the level of transactions per second for the bitcoin is extremely low compared to other methods of payment (as shown in Table 1). (3) Energy consumption: the other issue raised relates to sustainability. Indeed, executing and storing data in the distributed manner used in a blockchain requires rapidly increasing levels of computing power and thus energy consumption (Chang et al., 2020). A bitcoin transaction requires three times more energy than a Visa one. (4) Hacking issues: Depending on how they have been designed, public block-chain solutions may be more vulnerable to cyberattack depending on the way in which they are designed (Price, 2020). Several thefts of millions of crypto-currencies have occurred (Werbach, 2018). (5) Given that blockchain offers anonymity to its users, it could contribute to illegal activities such as money laundering (Yeoh, 2017). Nguyen (2016) questions the idea that blockchain could be a financial solution for the development of future sustainability proj-ects such as the PRB.

Table 1 – Number of financial transactions per second

Number of transactions per second

Visa 24 000

PayPal 193

Bitcoin 20

Methodology

As both the PRB and the practical applications of blockchain as an inno-vative technology are in their infancy, our research strategy was to apply a qualitative approach to arrive at some theoretical conjectures. Our approach

VIII Journal of Innovation Economics & Management 2022 – pre-published

Paul David Richard Griffiths, Patricia Baudier

© D

e B

oeck

Sup

érie

ur |

Tél

écha

rgé

le 2

5/08

/202

2 su

r w

ww

.cai

rn.in

fo (

IP: 6

5.21

.229

.84)

© D

e Boeck S

upérieur | Téléchargé le 25/08/2022 sur w

ww

.cairn.info (IP: 65.21.229.84)

to evidence collection and analysis is the Knowledge Café (KC), a method that allows us to draw on the experience of a significant number of par-ticipants. The KC is a technique used to bring together a group of knowl-edgeable people to increase their knowledge by talking and listening to each other on a subject of common interest and its context. It can be used as an active learning tool or as a research technique for testing ideas through active conversation. In this case, it is used as the latter, but it is expected that the participants will learn from each other in the process (Remenyi, 2004; Singh, 2017). The theoretical underpinning for the KC is that it seeks to converting tacit into explicit knowledge (Griffiths, Arenas, 2014) that can then be docu-mented. This is done through the confrontation of ideas in the discussions. The KC requires an experienced moderator to guide the proceedings, a role performed by the authors in this case. The KC allows space for interaction between the informants – through moderating and observing these interac-tions researchers are able to obtain deeper insights into the phenomenon under study. The KC took place on June 30th, 2020, and the proceedings were recorded with the agreement of the participants. Usually KCs are run face-to-face, but due to the pandemic lockdown we used a virtual platform (Zoom). This has the advantage of accommodating participants from different geog-raphies. Some participants were members of “la fabrique du future”, a think tank focussing on innovations. Authors also mobilized their personal net-work using the snow ball effect to select respondents. All participants had a strong knowledge in both banks and/or blockchain topics (Table 2).

Table 2 – Profiles of participants in the Knowledge Café

Participants GenderArea of

expertisePosition Location

#1 FemaleBlockchain and Fintech

Senior Project Manager

Vienna

#2 Male Bank

Executive Director, Wealth Management

London

#3 Male BankExecutive Director, Digital Bank

London

#4 Male Bank

Senior Manager, Investment Bank

London

pre-published – Journal of Innovation Economics & Management 2022 IX

Enabling Responsible Banking through the Application of Blockchain

© D

e B

oeck

Sup

érie

ur |

Tél

écha

rgé

le 2

5/08

/202

2 su

r w

ww

.cai

rn.in

fo (

IP: 6

5.21

.229

.84)

© D

e Boeck S

upérieur | Téléchargé le 25/08/2022 sur w

ww

.cairn.info (IP: 65.21.229.84)

Participants GenderArea of

expertisePosition Location

#5 Female Fintech

Member of Founding Team, Blockchain Network

Paris

#6 Male Bank

Ex Managing Director of Banking Association, CEO Fintech

Santiago, CL

#7 MaleBank-consultant

Director Banking Practice, Global Consulting

London

#8 Male Consultant

Senior Manager, Banking sector

Bahamas

#9 FemaleBlockchain and Fintech

Partner, Blockchain Practice Lead

Zurich

#10 Male Blockchain

Senior Lawyer specializing in Smart Contracts

Munich

A group of ten people (bankers and/or blockchain practitioners) was invited to participate and provided with a description of the theme to be discussed.

The total duration of the meeting was ninety minutes. After a short pre-sentation to introduce members and the topics, the group was divided into two breakout groups of five participants each to discuss the following ques-tion: Would the application of blockchain-based solutions facilitate the implemen-tation of the six PRB? If so, how could it be achieved?

To make this question more tangible, the following sub-questions were proposed:

1) We know that there are no current blockchain solutions for the PRB, but can you think of applications of blockchain in other domains from which leading practices can be extracted for the implementation of PRB?2) Based on your experience with smart-contracts and other applica-tions of blockchain, can you think of possible risks or roadblocks that need to be considered for the application of blockchain to the implemen-tation of the PRB?

X Journal of Innovation Economics & Management 2022 – pre-published

Paul David Richard Griffiths, Patricia Baudier

© D

e B

oeck

Sup

érie

ur |

Tél

écha

rgé

le 2

5/08

/202

2 su

r w

ww

.cai

rn.in

fo (

IP: 6

5.21

.229

.84)

© D

e Boeck S

upérieur | Téléchargé le 25/08/2022 sur w

ww

.cairn.info (IP: 65.21.229.84)

A moderator in each breakout group ensured that none of the partici-pants monopolized the conversation and prompted quiet participants to intervene. This breakout session lasted some thirty-five minutes. After that, the group re-convened in a plenary session where the moderators prompted a general discussion on the same question and sub questions. This meeting lasted thirty-five minutes, followed by a wrap-up session of five minutes. The KC was video recorded, transcribed and observed by the researchers as many times as necessary to capture subtle nuances as part of the analysis of evi-dence. The first step in the analysis of the data was to align the transcript of the KC along the six PRBs, with identification of verbal statements, to produce a clear chain of evidence.

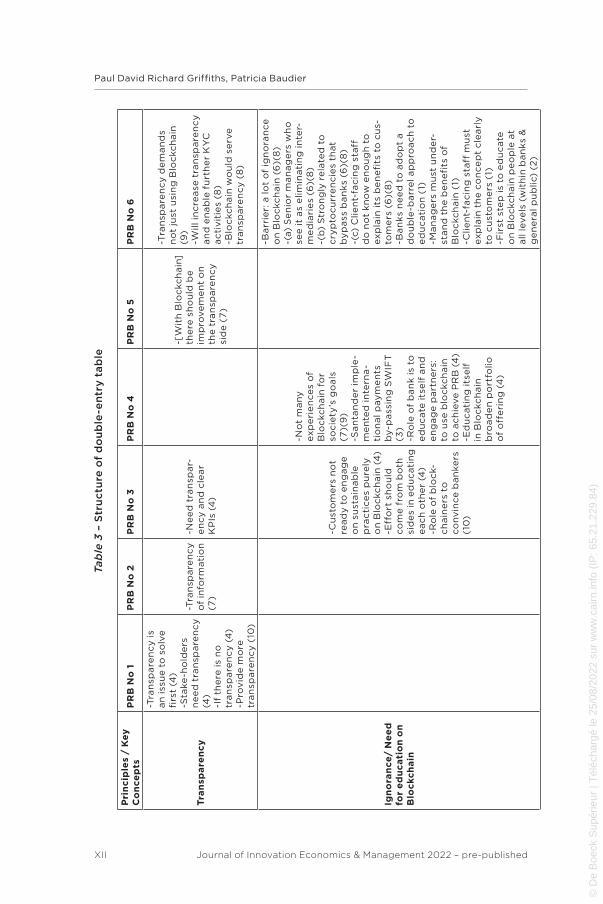

The second step was to code the text manually at a phrase-by-phrase level. Open coding was followed by axial coding along the six PRB using Post-its to build a tree. We then trawled through the data presented in this way to identify a series of nine key concepts (using a different colour for each concept) that cut across the six PRB. A double-entry table with the PRB on one axis and the nine key concepts on the other, linked to verbal statements, was constructed (Table 3).

Finally, we developed a concept-driven narrative on the phenomenon of applying blockchain to enable the implementation of the PRB, which is shown in our Results section below.

After the findings were written up, a meeting was held with the Wholesale Banking Director and the Sustainability Manager at one of the signatory banks to present our conclusions and to receive feedback as a form of practi-tioner validation.

Results and Discussion

The nine concepts and their connections are represented in Figure 2. We develop explanations for these in the remainder of this section where we present our results and a discussion of each of the nine concepts. The names of constructs (2) and (7) have been changed slightly for clarity.

pre-published – Journal of Innovation Economics & Management 2022 XI

Enabling Responsible Banking through the Application of Blockchain

© D

e B

oeck

Sup

érie

ur |

Tél

écha

rgé

le 2

5/08

/202

2 su

r w

ww

.cai

rn.in

fo (

IP: 6

5.21

.229

.84)

© D

e Boeck S

upérieur | Téléchargé le 25/08/2022 sur w

ww

.cairn.info (IP: 65.21.229.84)

XII Journal of Innovation Economics & Management 2022 – pre-published

Paul David Richard Griffiths, Patricia Baudier

Ta

ble

3 –

Str

uctu

re o

f d

ou

ble

-en

try t

ab

le

Pri

ncip

les

/ K

ey

C

on

ce

pts

PR

B N

o 1

PR

B N

o 2

PR

B N

o 3

PR

B N

o 4

PR

B N

o 5

PR

B N

o 6

Tra

nsp

are

ncy

-Tra

nsp

are

ncy is

an

iss

ue t

o s

olv

e

firs

t (4

)-S

take

-ho

lde

rs

ne

ed

tra

nsp

are

ncy

(4)

-If

the

re is

no

tr

an

spa

ren

cy (

4)

-Pro

vid

e m

ore

tr

an

spa

ren

cy (

10)

-Tra

nsp

are

ncy

of

info

rmati

on

(7

)

-Ne

ed

tra

nsp

ar-

en

cy a

nd

cle

ar

KP

Is (

4)

-[W

ith

Blo

ckch

ain

] th

ere

sh

ou

ld b

e

imp

rove

me

nt

on

th

e t

ran

spa

ren

cy

sid

e (

7)

-Tra

nsp

are

ncy d

em

an

ds

no

t ju

st u

sin

g B

lockch

ain

(9

) -W

ill in

cre

ase

tra

nsp

are

ncy

an

d e

na

ble

fu

rth

er

KY

C

ac

tiv

itie

s (8

)-B

lockch

ain

wo

uld

se

rve

tra

nsp

are

ncy (

8)

Ign

ora

nce

/ N

ee

d

for

ed

uca

tio

n o

n

Blo

ckch

ain

-Cu

sto

me

rs n

ot

rea

dy t

o e

ng

ag

e

on

su

sta

ina

ble

p

rac

tice

s p

ure

ly

on

Blo

ckch

ain

(4

) -E

ffo

rt s

ho

uld

co

me f

rom

bo

th

sid

es

in e

du

cati

ng

e

ach

oth

er

(4)

-Ro

le o

f b

lock-

ch

ain

ers

to

co

nv

ince b

an

ke

rs

(10

)

-No

t m

an

y

exp

eri

en

ce

s o

f B

lockch

ain

fo

r so

cie

ty’s

go

als

(7

)(9

)-S

an

tan

de

r im

ple

-m

en

ted

in

tern

a-

tio

na

l p

ay

me

nts

b

y-p

ass

ing

SW

IFT

(3

)-R

ole

of

ba

nk is

to

ed

uc

ate

its

elf

an

d

en

ga

ge p

art

ne

rs:

to u

se b

lockch

ain

to

ach

ieve P

RB

(4

)-E

du

cati

ng

its

elf

in

Blo

ckch

ain

b

roa

de

n p

ort

folio

o

f o

ffe

rin

g (

4)

-Ba

rrie

r: a

lo

t o

f ig

no

ran

ce

on

Blo

ckch

ain

(6

)(8

)-(

a)

Se

nio

r m

an

ag

ers

wh

o

see it

as

elim

inati

ng

in

ter-

me

dia

rie

s (6

)(8

)-(

b)

Str

on

gly

re

late

d t

o

cry

pto

cu

rre

ncie

s th

at

by

pa

ss b

an

ks

(6)(

8)

-(c)

Clie

nt-

facin

g s

taff

d

o n

ot

kn

ow

en

ou

gh

to

exp

lain

its

be

ne

fits

to

cu

s-to

me

rs (

6)(

8)

-Ba

nks

ne

ed

to

ad

op

t a

do

ub

le-b

arr

el a

pp

roa

ch

to

e

du

cati

on

(1)

-Ma

na

ge

rs m

ust

un

de

r-st

an

d t

he b

en

efi

ts o

f B

lockch

ain

(1)

-Clie

nt-

facin

g s

taff

mu

st

exp

lain

th

e c

on

ce

pt

cle

arl

y

to c

ust

om

ers

(1)

-Fir

st s

tep

is

to e

du

cate

o

n B

lockch

ain

pe

op

le a

t a

ll leve

ls (

wit

hin

ba

nks

&

ge

ne

ral p

ub

lic)

(2

)

© D

e B

oeck

Sup

érie

ur |

Tél

écha

rgé

le 2

5/08

/202

2 su

r w

ww

.cai

rn.in

fo (

IP: 6

5.21

.229

.84)

© D

e Boeck S

upérieur | Téléchargé le 25/08/2022 sur w

ww

.cairn.info (IP: 65.21.229.84)

pre-published – Journal of Innovation Economics & Management 2022 XIII

Enabling Responsible Banking through the Application of BlockchainP

rin

cip

les

/ K

ey

C

on

ce

pts

PR

B N

o 1

PR

B N

o 2

PR

B N

o 3

PR

B N

o 4

PR

B N

o 5

PR

B N

o 6

En

erg

y c

on

-su

mp

tio

n (

by

Blo

ckch

ain

)

-Ho

weve

r,

Blo

ckch

ain

co

nsu

me

s ve

ry

larg

e a

mo

un

ts o

f e

ne

rgy (

9)

-Blo

ckch

ain

co

n-

sum

es

ve

ry la

rge

am

ou

nt

of

en

erg

y

(9)

-Re

pu

tati

on

of

be

ing

hig

h c

on

-su

me

r o

f e

ne

rgy

(8)

-En

erg

y c

on

sum

p-

tio

n is

da

rk s

ide o

f B

lockch

ain

(8

)-E

ne

rgy c

on

sum

p-

tio

n is

no

t so

lve

d

ye

t (6

)-M

ore

po

siti

ve

wh

ere

Blo

ckch

ain

is

po

we

red

by n

on

-fo

ssil o

r n

ucle

ar

sou

rce

s o

f e

ne

rgy

(6)

© D

e B

oeck

Sup

érie

ur |

Tél

écha

rgé

le 2

5/08

/202

2 su

r w

ww

.cai

rn.in

fo (

IP: 6

5.21

.229

.84)

© D

e Boeck S

upérieur | Téléchargé le 25/08/2022 sur w

ww

.cairn.info (IP: 65.21.229.84)

XIV Journal of Innovation Economics & Management 2022 – pre-published

Paul David Richard Griffiths, Patricia Baudier

Pri

ncip

les

/ K

ey

C

on

ce

pts

PR

B N

o 1

PR

B N

o 2

PR

B N

o 3

PR

B N

o 4

PR

B N

o 5

PR

B N

o 6

Re

jec

tio

n/

Ba

rrie

rs t

o a

do

p-

tio

n o

f B

lockch

ain

-Ove

rco

me b

ar-

rie

rs:

-Ba

nks

will a

do

pt

Blo

ckch

ain

fo

r o

the

r co

mm

erc

ial

are

as

(10

)-A

lre

ad

y u

sin

g

gre

en

fo

r in

ve

st-

me

nt

po

rtfo

lio

: N

o r

ea

son

wh

y it

sho

uld

no

t w

ork

fo

r lo

an

po

rtfo

lio

(1

0)

-Leve

rag

e

Blo

ckch

ain

to

m

ee

t su

sta

in-

ab

ilit

y t

arg

ets

(1

0)

-Ho

weve

r,

do

ub

ts w

he

the

r B

lockch

ain

is

alig

ne

d w

ith

PR

B

(9)

-Old

ge

ne

rati

on

of

ba

nk le

ad

ers

sti

ll

he

av

ily p

ap

er-

ba

sed

(5

)-B

lockch

ain

co

n-

sum

es

ve

ry la

rge

am

ou

nt

of

en

erg

y

(9)

-Pa

rtic

ula

rly in

co

un

trie

s w

he

re

en

erg

y m

atr

ix

relia

nt

on

fo

ssil

fue

ls (

6)

-Ba

rrie

r: a

lo

t o

f ig

no

ran

ce

on

Blo

ckch

ain

(6

)(8

)-R

eje

cti

on

of

ba

nks

ste

ms

als

o o

n: (1

0)

-(a)

Ori

gin

al d

eve

lop

ers

o

f B

lockch

ain

we

re a

nti

-sy

ste

m a

nd

an

ti-b

an

ks

(10

)-(

b)

Str

uc

tura

l id

ea if

dis

-tr

ibu

ted

re

lati

ng

to

alt

ern

a-

tive f

ina

nce (

10)

-© A

re

al w

orl

d p

oliti

ca

l p

ers

pe

cti

ve

: (1

0)

-Sh

ifti

ng

th

e E

uro

pe

an

fi

na

ncia

l sy

ste

m f

rom

b

an

k-b

ase

d t

o f

ina

ncia

l m

ark

ets

ba

sed

(10

)-(

d)

Ma

ny p

ress

he

ad

lin

es

lin

kin

g c

ryp

tocu

rre

ncie

s to

mo

ney la

un

de

rin

g a

nd

o

the

r d

ub

iou

s a

cti

vit

y (

10)

© D

e B

oeck

Sup

érie

ur |

Tél

écha

rgé

le 2

5/08

/202

2 su

r w

ww

.cai

rn.in

fo (

IP: 6

5.21

.229

.84)

© D

e Boeck S

upérieur | Téléchargé le 25/08/2022 sur w

ww

.cairn.info (IP: 65.21.229.84)

pre-published – Journal of Innovation Economics & Management 2022 XV

Enabling Responsible Banking through the Application of BlockchainP

rin

cip

les

/ K

ey

C

on

ce

pts

PR

B N

o 1

PR

B N

o 2

PR

B N

o 3

PR

B N

o 4

PR

B N

o 5

PR

B N

o 6

Da

ta i

n

Blo

ckch

ain

-Qu

ality

of

data

in

to B

lockch

ain

is

ess

en

tia

l (1

0)

-Co

mfo

rta

ble

w

ith

clie

nt

data

& K

YC

is

sue

s (8

)

-To

sto

re a

nd

sh

are

d

ata

(9

)-E

ach

tra

nsa

c-

tio

n n

ee

ds

to b

e

rep

lic

ate

d in

va

st

nu

mb

er

of

no

de

s (8

)

-Blo

ckch

ain

co

uld

elim

i-n

ate

or

dim

inis

h h

um

an

e

rro

rs (

8)

-…b

ut

als

o r

oo

tin

g o

ut

pro

ble

m d

ata

(9

)-I

t is

no

t e

no

ug

h t

o p

ut

yo

ur

rep

ort

ing

data

on

B

lockch

ain

(9

)-T

wo

big

ch

alle

ng

es

for

imp

lem

en

tin

g P

RB

: (9

)-(

a)

Va

lid

ate

th

e d

ata

e

nte

red

(w

hat

is o

n

Blo

ckch

ain

is

tru

e (

9)

-Wit

h B

ig D

ata

an

d I

oT

yo

u

have m

ass

ive a

mo

un

ts o

f d

ata

(9

)-(

b)

Clo

sin

g t

he g

ap

b

etw

ee

n t

he r

ea

l w

orl

d a

nd

v

irtu

al o

ne r

ep

rese

nte

d b

y

Blo

ckch

ain

(e

.g.,

ca

rbo

n

cre

dit

s) (

9)

-Bu

t th

e in

ters

ec

tio

n

be

twe

en

Blo

ckch

ain

an

d

the r

ea

l w

orl

d is

the d

if-

ficu

lt p

oin

t (9

)-N

ee

d t

rust

in

pe

rso

n t

hat

ce

rtif

ies

data

in

Blo

ckch

ain

(8

)-T

he

re a

re s

en

siti

ve iss

ue

s su

ch

as

to s

tore

an

d s

ha

re

cu

sto

me

r-re

late

d d

ata

(8

)-T

rackin

g d

ata

of

cu

sto

me

r (8

)-T

rackin

g d

ata

if

sup

plie

r o

f fu

nd

s (8

)

© D

e B

oeck

Sup

érie

ur |

Tél

écha

rgé

le 2

5/08

/202

2 su

r w

ww

.cai

rn.in

fo (

IP: 6

5.21

.229

.84)

© D

e Boeck S

upérieur | Téléchargé le 25/08/2022 sur w

ww

.cairn.info (IP: 65.21.229.84)

XVI Journal of Innovation Economics & Management 2022 – pre-published

Paul David Richard Griffiths, Patricia Baudier

Pri

ncip

les

/ K

ey

C

on

ce

pts

PR

B N

o 1

PR

B N

o 2

PR

B N

o 3

PR

B N

o 4

PR

B N

o 5

PR

B N

o 6

Tru

st

-Clie

nt

is t

ruth

ful

an

d h

on

ou

rs m

iti-

gati

on

ag

ree

me

nt

(4)

-Blo

ckch

ain

d

efi

nit

ely

use

ful to

ke

ep

tra

ck (

4)

-He

lps

deve

lop

tru

st

be

twe

en

in

ve

sto

r a

nd

b

an

k (

9)

-Tru

st is

at

the

co

re o

f b

an

kin

g

ind

ust

ry (

4)

-Ba

nks

have n

ot

do

ne g

oo

d jo

b in

th

e p

ast

(10

)-D

isin

ter-

me

dia

tio

n m

ay

sou

nd

att

rac

tive

, b

ut

socie

ty n

ee

ds

the

ir e

xp

ert

ise o

n

cre

dit

ris

k (

10)

-Blo

ckch

ain

co

uld

be

me

an

s to

re

sto

re t

rust

in

b

an

ks

(1)

-Id

ea

l m

ed

ium

to

bu

ild

tr

ust

in

ba

nk

’s in

form

a-

tio

n (

8)

-Ro

le o

f b

an

ks

is t

o a

ct

as

tru

ste

d p

art

ies

(2)

-Ba

nks

ne

ed

to

re

-bu

ild

tr

ust

to

ea

rn ‘lice

nse

to

o

pe

rate

’ (2

)-C

oro

lla

ry: B

lockch

ain

c

an

’t c

om

ple

tely

su

bst

itu

te

tru

st (

8)

-Ne

ed

tru

st in

pe

rso

n t

hat

ce

rtif

ies

data

in

Blo

ckch

ain

(8

)-[

Blo

ckch

ain

] e

na

ble

s co

nse

nt/

Ag

ree

me

nt

in a

tru

stfu

l e

nv

iro

nm

en

t (1

)

Te

ch

no

log

y a

lon

e

is n

ot

the

an

swe

r

-No

t ju

st t

hru

stin

g

Blo

ckch

ain

on

b

an

ke

rs (

4)

-Te

ch

no

t th

e

solu

tio

n t

o e

ve

ry-

thin

g (

4)

-Ba

nks

to k

ee

p

hu

ma

n c

on

tac

t ra

the

r th

an

d

ele

gate

all t

o

tech

(4

)-D

o n

ot

see s

us-

tain

ab

ilit

y d

eci-

sio

ns

de

leg

ate

d

to t

ech

(4

)-B

eyo

nd

te

ch

to

h

um

an

in

tera

c-

tio

n (

4)

-Acq

uir

e

Blo

ckch

ain

sta

rt-

up

s to

leve

rag

e

exis

tin

g t

ech

(4

)-A

cq

uir

e n

ew

te

ch

(B

lockch

ain

) to

in

cre

ase

ca

pa

cit

y

(4)

-Pri

vate

Blo

ckch

ain

w

ou

ld a

vo

id h

ug

e

co

nsu

mp

tio

n o

f p

ap

er

(5)

© D

e B

oeck

Sup

érie

ur |

Tél

écha

rgé

le 2

5/08

/202

2 su

r w

ww

.cai

rn.in

fo (

IP: 6

5.21

.229

.84)

© D

e Boeck S

upérieur | Téléchargé le 25/08/2022 sur w

ww

.cairn.info (IP: 65.21.229.84)

pre-published – Journal of Innovation Economics & Management 2022 XVII

Enabling Responsible Banking through the Application of BlockchainP

rin

cip

les

/ K

ey

C

on

ce

pts

PR

B N

o 1

PR

B N

o 2

PR

B N

o 3

PR

B N

o 4

PR

B N

o 5

PR

B N

o 6

Fin

an

cin

g S

ME

s

-Blo

ck-c

hain

to

ea

se f

ina

n-

cia

l in

clu

sio

n

of

SM

Es

(6)

(9)

-Off

er

ser-

vic

es

in lo

w

co

st r

eg

ion

s (8

)

-Ba

nks

no

t p

lay

ing

we

ll in

p

rov

idin

g f

ina

nce

to S

ME

s (1

0)

-Pro

vid

e S

ME

s w

ith

fu

nd

ing

th

rou

gh

fin

an

cia

l m

ark

ets

(10

)

Sta

ke

ho

lde

rs

-De

ma

nd

s lo

ts o

f e

ffo

rt f

rom

sta

ke

-h

old

ers

(4

)-S

take

-ho

lde

rs

ne

ed

tra

nsp

are

ncy

(4)

-Wo

rk h

an

d-

in-h

an

d w

ith

cu

sto

me

rs &

st

ake

ho

lde

rs (

4)

-Ac

tive

ly s

ee

k

pa

rtn

ers

an

d k

ey

sta

ke

ho

lde

rs (

4)

-En

ga

ge w

ith

st

ake

ho

lde

rs t

hat

wo

rk b

eyo

nd

tr

ad

itio

na

l fi

na

nce

(en

vir

on

me

nt

Imp

ac

t) (

10)

-Tra

nsf

orm

th

eir

st

ake

ho

lde

rs (

4)

-Blo

ck-c

hain

co

uld

e

na

ble

all p

ar-

ticip

an

ts t

o a

cce

ss

info

rmati

on

th

ey

ne

ed

(5

)-E

na

ble

s p

ap

erl

ess

b

an

kin

g p

roce

ss

an

d r

ela

tio

nsh

ip t

o

clie

nts

(8

)

© D

e B

oeck

Sup

érie

ur |

Tél

écha

rgé

le 2

5/08

/202

2 su

r w

ww

.cai

rn.in

fo (

IP: 6

5.21

.229

.84)

© D

e Boeck S

upérieur | Téléchargé le 25/08/2022 sur w

ww

.cairn.info (IP: 65.21.229.84)

Figure 2 – Model for enabling the PRB through blockchain.

Transparency

The first key concept that emerged from our analysis of the data was Transparency. It is not possible to align credit origination with the Paris Agreement criteria or to ensure that the necessary mitigation actions are carried out (PRB1) throughout the lifecycle of the project if there is no trans-parency towards the multiple stakeholders involved.

It would be naïve to think that the PRB merely involves the inclusion of measurements of some ESG indicators in traditional reporting practices. Two of our contributors considered that blockchain would be extremely useful for giving transparency to stakeholders (contributors #4, #10). It also emerged that developing more stable cryptocurrencies with more transparency of informa-tion would have a highly positive impact (PRB2, #7). Similarly, one participant noted that to successfully reduce environmental impact, banks and customers should mutually encourage sustainable practices (PRB3) and particular care should be made to avoid greenwashing, for which transparency and clear KPIs are needed (#4). Being transparent is seen an essential attribute of corporate governance (PRB5, #7); hence, it is not surprising that the application of blockchain emerged as a powerful tool for rooting out dubious transactions (e.g. Panama Papers). In relation to this, it was noted that banks are facing

XVIII Journal of Innovation Economics & Management 2022 – pre-published

Paul David Richard Griffiths, Patricia Baudier

© D

e B

oeck

Sup

érie

ur |

Tél

écha

rgé

le 2

5/08

/202

2 su

r w

ww

.cai

rn.in

fo (

IP: 6

5.21

.229

.84)

© D

e Boeck S

upérieur | Téléchargé le 25/08/2022 sur w

ww

.cairn.info (IP: 65.21.229.84)

a crisis of confidence which they need to overcome to re-build trust, hence improving the transparency of their reporting (PRB6) through the implemen-tation of blockchain would be highly positive (#9). Banks handle many privacy issues, such as the storing and sharing of customer data, and work on sensi-tive issues such as Know Your Customer (KYC) and Anti-Money Laundering (AML); Blockchain could serve as a platform to help them be more account-able for outcomes: Blockchain will increase transparency and enable further KYC activities (#8).

These findings reinforce theoretical findings on the role that blockchain can play in reducing money laundering and other fraudulent activities, as highlighted by Lai (2018); they also confirm blockchain’s potential for trans-parency in the narrow sense that ‘transactions are recorded in real time and all records must be validated by all actors in the blockchain concerned’ (Yoo, 2017). Moreover, they reinforce the beneficial role of cryptocurrencies to indi-viduals through reduced transaction times and costs. However, the results of our empirical study go further in emphasizing blockchain’s potential for transparency in a broader informational sense, in that it enables banks and customers to work together towards a world of lower anthropogenic GHG emissions through the application of the PRB.

Ignorance about Blockchain

It emerged from conversations in the KC that bankers know little about innovations such as blockchain, and have many pre-conceptions about its meaning and potential uses. This concept is synthesized as Ignorance/Need for education on blockchain. Blockchain technology alone will not encourage banks’ customers to engage in sustainable practices (PRB3) because, amongst other reasons, customers are also quite ignorant about the technology: Customers are not ready to engage in sustainable practices purely on block-chain… Effort should come from both sides (banks and customers) in educating each other (#4). So, customers need to have the advantages of this innova-tive technology and its applications explained to them, and this must be complemented by human interaction. It was also apparent that blockchain experts (‘block-chainers’) need to be pro-active in convincing bankers of the benefits of their technology to encourage green practices: The role of block-chainers is to convince bankers (#10). There are a few, but not many, instances of banks partnering with stakeholders to achieve society’s goals (PRB4) through the application of blockchain, as stated by participants #7 and #9. Santander Bank provides a successful example, having developed an international multi-currency payment solution on blockchain that by-passes SWIFT and significantly reduces the cost to all parties, as confirmed

pre-published – Journal of Innovation Economics & Management 2022 XIX

Enabling Responsible Banking through the Application of Blockchain

© D

e B

oeck

Sup

érie

ur |

Tél

écha

rgé

le 2

5/08

/202

2 su

r w

ww

.cai

rn.in

fo (

IP: 6

5.21

.229

.84)

© D

e Boeck S

upérieur | Téléchargé le 25/08/2022 sur w

ww

.cairn.info (IP: 65.21.229.84)

by participant #3: Santander implemented international payments by-passing SWIFT. Here, it would appear that banks have a role to play in educating their staff and customers about blockchain and in engaging with partners to develop and implement solutions that will broaden the bank’s offering for the benefit of society. More generally, blockchain could help banks to be more transparent about how they report their progress in driving their customers towards a green economy (PRB6). For this to materialize, banks must over-come ignorance-based pre-conceptions of blockchain at all levels: One of the barriers is a lot of ignorance about blockchain (#8). It is possible that, from their limited knowledge of cryptocurrencies, senior managers panic at the notion that blockchain disintermediates banks. As participant #8 notes, blockchain is strongly related to cryptocurrencies that bypass banks. Also, client-facing staff is ignorant about the functioning of blockchain and are thus incapable of explaining its benefits to customers: Client-facing staff do not know enough to explain its benefits to customers (#6). So, banks need to engage in block-chain education both top-down, from the board to the rank-and-file, and horizontally, from its staff to its customers: Banks need to adopt a double-barrel approach to education…Managers must understand the benefits of blockchain (#1); First step is to educate people at all levels (within banks & general public) about blockchain (#2).

As noted by participants, the implementation of blockchain in the banking sector involves all stakeholders, including competitors. Blockchain can increase the operating and management efficiency of all stakeholders (Wu, Duan, 2019) by reducing operating times of transactions and simpli-fying data management (Haiss, Moser, 2017). As an example, in Asia, the Korea Federation of Banks launched a consortium of 16 banks to conduct research on processes such as customer authentication and the control of e-documents (Oh, Shong, 2017).

Our findings regarding the problem of ignorance and the need to educate bankers and their customers about blockchain applications make a positive contribution to the existing literature. Our findings also highlight the need to supplement the blockchain with human interaction to allow it to perform a broad-based societal service, such as reducing GHG emissions.

Energy Consumption

The next key concept relates to Energy consumption (by blockchain), which is extremely high. We have ranked it so highly because, first, there was a great deal of fervent discussion about it at the KC, and, second, it seems contentious for banks to ask their customers to use tools that are clearly not

XX Journal of Innovation Economics & Management 2022 – pre-published

Paul David Richard Griffiths, Patricia Baudier

© D

e B

oeck

Sup

érie

ur |

Tél

écha

rgé

le 2

5/08

/202

2 su

r w

ww

.cai

rn.in

fo (

IP: 6

5.21

.229

.84)

© D

e Boeck S

upérieur | Téléchargé le 25/08/2022 sur w

ww

.cairn.info (IP: 65.21.229.84)

environmentally sustainable when encouraging sustainable practices (PRB3): Blockchain consumes very large amounts of energy (#9). As well as developing effective governance and a culture of responsible banking (PRB5), block-chain can contribute significantly to achieving a paperless bank thereby reducing emissions, but it has not been demonstrated that this offsets the unresolved problem of high energy consumption: Energy consumption is the dark side of blockchain (#8) and Energy consumption is not solved yet (#6). Of course, this issue becomes irrelevant in those cases where blockchain can be powered by non-fossil fuels as perceptions will be more positive if blockchain is powered by non-fossil or nuclear sources of energy (#6).

Hence, this research supports the finding that storing and sharing data on blockchain requires substantial computing power and an ever-increasing consumption of energy (Chang et al., 2020) leading to GHG emissions. As an example, a substantial amount of electricity is required in the mining process of cryptocurrencies such as Bitcoin and this has tarnished the reputation of blockchain (Li et al., 2018). Nevertheless, Sedlmeir et al. (2020) consider that, while the energy consumed is huge, it will not represent a threat to the climate in the future. However, they suggest part of those emissions would be offset if banks adopted paperless processes and, of course, energy consump-tion would be lower if the servers were fuelled by non-fossil fuel sources.

Other Objections/Barriers to Adoption

Given the deeply engrained resistance to implementing blockchain in banks, we introduced a concept articulated as Objections/barriers to adop-tion of blockchain. This resistance goes deeper than ignorance about block-chain within banks or doubts about blockchain’s alignment with the PRB due to its high energy consumption. It stems from several factors. First, the old generation of bank leaders is still strongly attached to paper (#5) and they do not provide opportunities for the development of a corporate culture of responsible banking (PRB5) through the use of innovative technologies such as blockchain. Second, the fact that the original blockchain developers were anti-system and anti-banks creates anti-bodies in the banking establishment (#10). There is a third structural reason for resistance based on the fact that block-chain is used by entrepreneurs as a platform for alternative finance (e.g. payments and crowdfunding) (#4) and for creating payments services and solutions that erode the banks’ revenue streams. There is a fourth real-world political factor to resist in the EU (#10), where there is an initiative to unite financial markets with the aim of displacing the EU financial system from one heavily depen-dent on banks, to one far more dependent on financial markets (#10). Finally, the negativity generated by many press headlines that link cryptocurrencies

pre-published – Journal of Innovation Economics & Management 2022 XXI

Enabling Responsible Banking through the Application of Blockchain

© D

e B

oeck

Sup

érie

ur |

Tél

écha

rgé

le 2

5/08

/202

2 su

r w

ww

.cai

rn.in

fo (

IP: 6

5.21

.229

.84)

© D

e Boeck S

upérieur | Téléchargé le 25/08/2022 sur w

ww

.cairn.info (IP: 65.21.229.84)

to money laundering and other dubious activities (#10) produces further resis-tance to blockchain. All these reasons for resistance to blockchain impede its adoption by banks and the associated benefits of transparency in reporting and accountability, hampering any progress in persuading their customers to become green (PRB6). Notwithstanding, there are some positive signs that these barriers can be overcome, for example, in the adoption of blockchain in other commercial areas of banks. As blockchain is seen to generate revenue or increase profitability in commercial activities (#9), there will be more enthu-siasm for applying it to encourage customers to adopt sustainable practices (PRB3). The fact that the concept of a green portfolio is strengthening its hold in the investments space makes it easier to think about applying the concept to loan portfolios (#10) as well.

In summary, as seen in our literature review, there is extant theory on why banks have not adopted blockchain more enthusiastically (Till et al., 2017), and some of the causes, such as high energy consumption and the applica-tion of blockchain to disintermediate banking altogether (Lai, 2018), are sup-ported by our findings. However, our findings do not confirm other causes cited in the literature, such as lack of scalability. Moreover, our research reveals previously unexplored barriers to adoption by banks, such as political factors within the EU and, more globally, the negativity deriving from bad press about cryptocurrencies.

Data Quality

The crucial concept of quality of data in blockchain (#10), departs from the premise that once data is on the blockchain it is secure and transparent. The question remains of how blockchain users can be sure that what is uploaded is totally accurate. For example, are the emissions data that emerge from environmental impact analyses rigorous and are they uploaded accurately (PRB1)? Or, as mentioned by contributor #8, can users be assured that KYC procedures are well implemented and thus client and other stakeholder data is valid and ready to facilitate low-cost transactions in low-income communities (PRB2)? This is say, blockchain technology is a great facilitator, but it needs to be embedded in well thought-through data governance processes and in an ethical corporate culture (PRB5): If these conditions are not met the data stored and shared through blockchain will be unreliable no matter on how many servers, it is replicated (#9). However, these individual challenges should not distract bankers from the multitude of benefits that come with it: Blockchain would eliminate human error (#8) and help root out problem data (#9) and thus effortlessly close the gap between the real world and the virtual blockchain world: The maturity of the Internet of Things (IoT) and the proliferation of Big

XXII Journal of Innovation Economics & Management 2022 – pre-published

Paul David Richard Griffiths, Patricia Baudier

© D

e B

oeck

Sup

érie

ur |

Tél

écha

rgé

le 2

5/08

/202

2 su

r w

ww

.cai

rn.in

fo (

IP: 6

5.21

.229

.84)

© D

e Boeck S

upérieur | Téléchargé le 25/08/2022 sur w

ww

.cairn.info (IP: 65.21.229.84)

Data make the validation and certification of data on entry even more critical (#9). Only by doing this will the PRB signatory banks be able to be more transparent about how they report their progress and be accountable for their progress (PRB6).

The extant theory is clear on the security virtues that arise from block-chain as a decentralized system (Yoo, 2017), which is considered immutable, unalterable and resistant to tampering (Lai, 2018). Our findings support that theory but reveal an additional aspect, which is that the vulnerability of blockchain lies in the risk that the original data uploaded is not a reflection of reality. It is vitally important for the credibility of the system, therefore, that data input is audited and certified by a trustworthy person or entity.

Trust

Trust, one of the key concepts, is at the core of the banking industry (#4) and needs to be mutual if banks are going to work with their customers to encourage sustainable practices (PRB3). The customer needs to trust that their bank has implemented its own sustainable practices. Blockchain applications already exist in the smart contract form for ‘green investments’, allowing an investor to keep track of where their funds are being invested to ensure that they have a positive impact on people and the environment (PRB2). This is very similar to banks using smart contracts based on blockchain to monitor that borrowers are honouring the GHG emissions mitigation activities speci-fied under the terms of their loan. Thus, blockchain, as stated by participant #4, is useful for banks to monitor that their loan portfolio is working towards containing and eventually reducing anthropogenic global warming (PRB1). Since the 2007/8 financial crisis, banks have lost public trust, which makes it more difficult for them to engage and partner with relevant stakeholders to achieve society’s goals (PRB4). Not only that, but the idea that banks can be disinter-mediated using an alternative source of trust such as blockchain sounds attrac-tive (#10). However, society relies on the banks’ distinctive competences to manage credit risk and monitor the performance of loans. In fact, blockchain could be a means of restoring trust in banks, as it is the ideal medium for building trust through information used to report on progress and account-ability of outcomes (PRB6): One key role of banks in society is to act as trusted parties (#2) and this cannot be fully substituted by smart contracts, so banks need to re-build trust to earn their license to operate (#1). Moreover, blockchain could be an enabler of consent/agreement in a trusting environment if there is trust in the person or entity that certifies that the data in blockchain reflects reality (#8). As seen in our literature review, as a result of the reckless behaviour that led to the 2007-8 financial crisis, banks’ standing in society was dealt a

pre-published – Journal of Innovation Economics & Management 2022 XXIII

Enabling Responsible Banking through the Application of Blockchain

© D

e B

oeck

Sup

érie

ur |

Tél

écha

rgé

le 2

5/08

/202

2 su

r w

ww

.cai

rn.in

fo (

IP: 6

5.21

.229

.84)

© D

e Boeck S

upérieur | Téléchargé le 25/08/2022 sur w

ww

.cairn.info (IP: 65.21.229.84)

devastating and lasting blow (European Central Bank, 2016; Griffiths, 2020; Haddad, Hornuf, 2019). Banks need opportunities to recover from this. Our study finds that the combination of a transparent platform such as block-chain together with the banks’ expertise in managing credit risk and moni-toring loan performance offers a powerful means for restoring trust. However, incorporating environmental impact criteria into credit origination is an extraordinarily complex endeavour, and this is made even more challenging by the fact that banks need to monitor their clients’ compliance with GHG emissions mitigations actions committed to in their loan contract throughout the whole lifecycle of each project. Blockchain has a role to play as a great enabler for banks by becoming the custodians of GHG emissions control on behalf of society by enabling the PRB. This would be an extension of already complex applications of blockchain in other areas of financial services, such as trading, payments, financial inclusion and the management of liquid assets (Demarco, 2019; Manif, Marsh, 2017; Marsh, 2019; Sostakaite, 2019).

Blockchain and Human Interactions