effects of Debt financing to Microfinance institutions

89

DECLARATION I Nduhukyire Lawrence of registration number 11/U/24301/NTI do declare that the work presented in this research report is my original work and has never been presented to any other University or institution of higher learning for the award of any academic qualification. Signature: ……………………………… Date: ……………………………. Nduhukyire Lawrence (Student) i

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of effects of Debt financing to Microfinance institutions

DECLARATION

I Nduhukyire Lawrence of registration number 11/U/24301/NTI do

declare that the work presented in this research report is my

original work and has never been presented to any other

University or institution of higher learning for the award of any

academic qualification.

Signature: ……………………………… Date: …………………………….

Nduhukyire Lawrence

(Student)

i

APPROVALThis is to certify that this research report has been submitted

in partial fulfillment of the requirement for the award of A

Degree in Social Development of Makerere University under my

supervision.

Signed: ……………………………………….. Date: ……………………………..

Mr. Mugabe Moses

(Supervisor)

ii

DEDICATIONWith great Joy and heartfelt feelings, I dedicate this research

work to my great and beloved parents Mr. Rwamuhanda Levi & Mrs.

Barahuka Edith for their endless financial, spiritual and moral

support towards me and my education;

To my brothers Enold, Humphrey, Aggrey, Edgar, Anthony and my

Sister Claire, beloved friends, Pamela and lastly to my uncles

especially Mr. Tumwebaze Philemon for his support in all ways;

God bless you abundantly.

iii

ACKNOWLEDGEMENT

I acknowledge with deep pressure, the almighty God for enabling

me complete the course and this research work safely and for the

wisdom he has given me.

My gratitude and sincere thanks also goes to my parents; Mr. Levi

and Mrs. Edith and relatives for their great and consistent

efforts, sacrifice and their supportive words of encouragement

towards my success in education.

My thanks also go to the staff and members of Kayonza

Microfinance Sacco for the Advice, guidance, encouragement given

to me during the period of data collection.

I also Love to extent my gratitude appreciation to my university

supervisor Mr. Mugabe Moses for his tremendous efforts in guiding

me during the time I started research work up to the time of

submission, and to all lectures for equipping me with skills

required by a researcher and as a social worker.

Finally, massive appreciation goes Mr. & Mrs. Philemon

Tumwebaze, Mr. Kamutu and to my dear friends especially Kembabazi

Pamela, Hildah, and course mates for their guidance and moral

support rendered to me during the researcher work.

iv

TABLEOFCONTENTSDECLARATION.................................................i

APPROVAL...................................................ii

DEDICATION................................................iii

ACKNOWLEDGEMENT............................................iv

TABLEOFCONTENTS.............................................v

LIST OF TABLES...........................................viii

LIST OF FIGURES............................................ix

CHAPTER ONE: INTRODUCTION TO THE STUDY......................1

I.0 Introduction............................................1

1.1 Background of the Study.................................1

1.2 Statement of the Problem................................3

1.3 Objectives of the Study.................................4

1.3.1 General Objective.....................................4

1.3.2 Specific objectives...................................4

1.4 Research Questions......................................4

v

1.5 Significance of the Study...............................5

1.6 Scope of study;.........................................5

1.7Operational definitions..................................6

CHAPTER TWO: LITERATURE REVIEW..............................7

2.0 Introduction............................................7

2.1 Different Sources of Debt Finances and SACCOs...........7

2.2 Survival Levels of SACCOs...............................9

2.3 Relationship between Debt Financing and Survival of SACCOs.

...........................................................11

CHAPTER THREE: METHODOLOGY.................................13

3.0 Introduction...........................................13

3.1 Research design........................................13

3.2 Study Area.............................................13

3.3 Population of Study....................................14

3.4 Sample Size............................................14

3.5 Sampling procedure.....................................15

3.6 Sources of Data........................................15

3.6.1 Primary Data.........................................15

3.6.2 Secondary Source.....................................15

3.7 Reliability and Validity of research instruments.......16

3.7.1Validity..............................................16

3.7.2 Reliability..........................................16

3.8 Data Collection Methods................................16

3.8.1 Questionnaire method.................................16

3.8.3 Interview method.....................................17

3.8.4 Focus Group interviews...............................17

1.8.5 Documentary review...................................18vi

3.9 Data Processing and Analysis...........................18

3.9.1 Organizing...........................................19

3.9.2 Editing..............................................19

3.9.3 Coding...............................................19

3.9.4 Tabulation...........................................19

3.10 Limitations of the study..............................20

CHAPTER FOUR:..............................................21

DATA PRESENTATION, INTERPRETATION AND ANALYSIS.............21

4.0 Introduction...........................................21

4.1 Background information of the Respondents..............21

4.1.1 Gender distribution of the respondents...............21

4.1.2 Age of the Respondents...............................22

4.1.3 Respondents Marital Status...........................23

4.1.4 Level of education of respondents....................25

4.1.5 Respondents positions held in SACCOs.................26

4.2 Sources of Debt Finances...............................28

4.2.1. Debt finances as a major source of Sacco finances...28

4.3 Effective performance Levels of SACCOs.................32

4.3.1 Period of operation in their enterprises (SACCO).....32

4.4 Relationship between Debt Finances and the effective

performance of SACCOs......................................35

CHAPTER FIVE...............................................37

SUMMARY, CONCLUSIONS AND RECOMMENDATIONS...................37

5.0 Introduction...........................................37

5.1Summary.................................................37

5.2 Conclusions............................................38

5.3 Recommendations........................................39vii

5.3.1 TO THE GOVERNMENT....................................39

5.3.1 TO SACCOs............................................39

REFERENCES.................................................41

APPENDIX A:................................................43

viii

LIST OF TABLESTable 1: Sampling Population.............................14

Table 2: A table showing Gender distribution of the respondents

.........................................................21

Table 3: Showing age intervals of respondents............22

Table 4: Showing marital status of respondents...........23

Table 5: Showing level of education of respondents.......25

Table 6; Showing respondents’ position held in SACCOs. . . .26

Table 7: Showing Respondent’s response on whether debt financing

is a major source of finances for SACCOs.................28

Table 8: Showing Responses on the different sources of debt

financing employed by SACCOs.............................29

Table 9: Showing Managers responses on whether commercial banks

are the major sources of debt financing employed by small scale

enterprises..............................................30

Table 10: Showing Managers and other respondent’s responses on

whether they face difficulty in trying to access debt finances

from different sources available.........................31

Table 11: A table showing the managers and other respondents’

responses on period of operation in their enterprise (SACCO)

.........................................................32

Table 12: Showing Managers and SACCO member’s responses on

whether financial constraints undermine the effective performance

of SACCOs................................................33

Table 13: Managers and other SACCO member’s responses on whether

government policies have supported the effective performance of

ix

SACCOs...................................................34

Table 14: Showing Respondent’s responses on whether debt finances

had been fundamental towards the development of their SACCOs.

.........................................................35

Table 15: Showing the Respondent’s responses on whether they face

difficulty in paying back the interest and the principle. 36

x

LIST OF FIGURES.

Figure 1: A pie chart showing the marital status of respondents

.........................................................24

Figure 2: A pie chart showing the respondents positions held in

SACCOs...................................................27

Figure 3: A pie chart showing the different sources of debt

financing employed SACCOs................................29

xi

xii

ACRONYMS/ABBREVIATIONS

ILO: International Labor Organization

IMF: International Monetary Fund

KGTF: Kayonza Growers Tea Factory

NCR: National Credit Regulator

RURAL ‘SPEED’: Savings Promotion & Enhancement of Enterprise

Development

SACCO: Savings and Credit Cooperative

SBA: Small Business Administration

SPSS: Special statistical package for social scientists

UIA: Uganda Investment Authority

USAID: United States Agency for International Development

UTDAL: Uganda Tea Development Agency Ltd.

xiii

ABSTRACT

The purpose of the study was carried out to investigate the

effects of debt financing on survival of savings and credit co-

operatives in Kanungu district particularly a case of Kayonza

microfinance SACCO.

The study was guided by specific objectives which were meant to

establish sources of debt finances in Butogota Town council,

Kanungu district, examine the survival levels of savings and

credit cooperatives in Butogota town council and also to find out

the relationship between debt financing and the survival levels

of SACCOs in Butogota Town council.

Regarding the review of literature; in chapter two, variable by

variable was reviewed under themes that constituted sub-headings.

They included sources of debt financing, survival levels of

SACCOs and relationship between debt financing and survival of

SACCOs.

The research study used both explanatory and descriptive designs.

Explanatory design was used to explain the effects of debt

financing and survival of SACCOs, and explain why things happen

the way they do in such SACCOs whereas descriptive design was

xiv

used to explore the magnitude of the problem that was under

study.

The selection of respondents was by simple random and purposive

sampling basing on a sample size of 120 respondents who included

the staff, shareholders, the SACCO members and business people

with in the area.

Self-administered questions were used to collect data,

interview method, focus group discussion and review of documents

like ledgers, draft act all which helped the researcher to access

the data needed for the research.

Data collected was analysed using SPSS to get sample

characteristics, distribution of frequency and to generate the

intended results in form of tables and pie-charts.

In Four, Findings from sources of debt finances showed that most

SACCOs are financed using debt finances in their operation. Other

findings showed that SACCOs use private sources like friends,

relatives, credit unions and government programs like prosperity

for all.

However, findings showed that the majority of the respondents

showed concern that financial constraints undermine the effective

performance of SACCOs especially due to high interests for

borrowed funds. Other factors that hinder performance of SACCOs

pointed out included entrepreneurial skills, unfavourable

government policies like high taxes for commodities, among

others.

xv

Basing on findings, it is therefore recommended that the

government through the central Bank should provide a frame work

that will regulate the interest rate offered by financial and

other lending institutions to the SACCOs and other people.

xvi

CHAPTER ONE: INTRODUCTION TO THE STUDY

I.0 Introduction

This chapter covers the background to the study, statement of the

problem, objectives of the study, research questions, scope of

the study, significance of the study and limitations of the

study.

1.1 Background of the Study

Debt financing is a strategy that involves borrowing money from a

lender or investor with the understanding that the full amount

will be repaid in the future, usually with interest (Beck T et

al, 2005). Beck T et al added that, debt financing does not

include any provision for ownership of the company (although some

types of debt are convertible to stock). Instead, small

businesses that employ debt financing accept a direct obligation

to repay the funds within a certain period of time. Interest rate

charged on the borrowed funds reflects the level of risk that the

lender undertakes by providing the money, for example, a lender

might charge a startup company a higher interest rate than it

would to a company that had shown a profit for several years.

Since lenders are paid off before owners in the event of business

liquidation, debt financing entails less risk and thus usually

commands a lower return.

1

The term ‘debt financing’ is a broad term also referring to

borrowing other people’s money in order to generate profits

(Gitman, 2000). ‘Debt financing’ includes the loans, credit cards

and revolving credit provided by financial institutions such as

banks and micro-lenders operating within the ambit of the

National Credit Regulator (NCR).

According to Beck T et al, 2005, Savings and credit cooperative

schemes (SACCOS) are estimated to contribute 30-35% of the gross

domestic product. The sector consists of more than 1 million

business activities engaging 3-4 million persons, about 20 to 30%

of the labour force. There has been an expansion of SACCOS for

income and employment generation between 2000- 2010 following the

adoption of economic reforms creating some space for the self-

employment and private sector activities.

The recent financial crisis has raised fundamental issues about

the role of bank equity capital. Various proposals have been put

forth which argue that banks (SACCOs) should hold more capital

(e.g., Kashyap, Rajan, and Stein 2009, Hart and Zingales 2009,

Acharya, Mehran, and Thakor 2010, Basel III (2010). An underlying

premise in all of these proposals is that there are externalities

due to the safety net provided to banks and thus social

efficiency can be improved by requiring banks to operate with

more capital, especially during financial crises. Bankers,

however, have typically argued that being forced to hold more

capital would jeopardize their performance, especially

profitability, and the argument that higher capital need not be2

beneficial has found some support in the academic literature as

well (e.g., Calomiris and Kahn 1991).

In the world over, small businesses face more constraints at a

startup developmental phases than when established (Bourne C,

1998). In Africa, for example, the rate of SACCOs to fail is 85%

out of every 100 cooperatives due to lack of skills and access to

capital (Cull R & Davisle, 2004). This according to World Bank

report (2000) has created a "Finance gap" in most markets between

US$50,000 to US$1 25 Million. The small businesses are able to

source and obtain micro finance as a result of debt financing

mostly from the informal sector like friends and relations while

large or medium enterprises, access these funds from Banks. This

unequal access to finance by SACCOs and large enterprises has

undermined the role of small scale business firms in the economic

development of African countries at large and Ugandan economy in

particular (Beck et al, 2005).

According to MFPED (2006) survey, 62% of Uganda‘s population has

no access to financial services. The difference between urban and

rural areas is significant, with 52% of the urban population and

65% of the rural population. The government is implementing a

Rural Financial Services Strategy that involves having a strong

Savings and Credit Cooperative‘s (SACCOs) in every sub county.

However, the formal financial systemhas continued to be extremely

fragile and underwent a serious crisis between 1997 and 1999 and

therefore much remains to be done to have promoted a savings and

3

credit cooperatives through debt financing and to have

sustainable SACCOs and greater financial inclusion.

According to USAID/Rural SPEED (Savings Promotion & Enhancement

of Enterprise Development) (2006) report, Kayonza Microfinance

SACCO is a tea improvement input loan product aimed at providing

Tea Improvement Input Loans and the Tea Improvement Labor Loan

and small business/investors to its members. During the initial

meetings with the SACCO’s and Kayonza Growers Tea Factory’s

managements (KGTF) it became evident that one single input loan

product would not be sufficient to meet the needs of both the

medium and large tea farmers, as well as the smaller growers. The

SACCO converts immediately available savings deposits and tea

input loan product into loans with longer maturities. Individual

savings deposits and tea input loan products are also typically

much smaller than an average loan, requiring multiple deposits to

fund a single loan.

Kayonza Micro finance SACCO also converts savings deposits and

tea input loan products with an absolute expectation of safety

and repayment into credit-risky loans to members (credit risk

transformation). And finally, the loans a SACCO makes, typically

carry a fixed interest rate for their entire term, while the

interest on savings deposits and more importantly on any

additional borrowings from banks or microfinance support programs

is variable and can be adjusted at any time according to changes

in market interest rates (interest rate risk transformation).

4

1.2 Statement of the Problem

Despite considerable progress in the expansion of Uganda‘s

financial services, 62%of Ugandans (about 18.1 Million people)

are unnerved by any kind of financial institution, formal or

informal and the demand for rural debt financing is more a

function of ease of access than of cost, however, low rates of

interest on loans, while possibly inducing a higher level of

desired investment, may reduce actual investment because of the

negative effects on available credit (IMF, 2002). Further, low

loan interest rates have an adverse influence on the allocative

efficiency of the financial system with effects on the

productivity of investment. In particular, low interest rates

encourage the use of capital-intensive technologies thus reducing

the employment generating potential of investment.

Kanungu District Community Department report on financial

institutions (2011) particularly SACCOs demonstrated that,

however, much as most SACCOs have tried to acquire debt finance

from different sources available to fund their operations in the

district, the SACCOs have still not achieved the expected

performance since they have continued experiencing financial

constraints. The report explained that, Kayonza micro finance

SACCO in Kanungu District, Butogota Town Council presents one of

the most appropriate ways and it is the only SACCO that serves

the remote rural areas where the majority of the green tea

producers are located. The SACCO provides mainly savings, loans

and credit cooperative services in the area, However, Kayonza

5

micro finance SACCO in the area is faced with many challenges

particularly those resulting from poor governance system and

structures and hence, to a large extent, failed to meet the

expectations of the members in terms of access to financial

services. The SACCO also suffers from a low savings rate, low

levels of lending, high costs, and high margins among many

others. These problems therefore forced the researcher to carry

out a study focusing on the effects of debt financing on the survival of SACCOs

in Butogota Town Council, Kanungu District specifically taking a

case study of Kayonza micro finance SACCO.

1.3 Objectives of the Study

1.3.1 General Objective

The general objective of the study was to investigate the

effect of debt financing on the survival of savings and credit

cooperatives in Butogota Town Council, Kanungu District.

1.3.2 Specific objectives

To identify different sources of debt finances used by SACCOs in

Butogota Town Council, Kanungu district

To examine the survival levels of savings and credit cooperatives

(SACCOs) in Butogota Town Council, Kanungu district

To find out the relationship between debt financing and the

survival of savings and credit cooperatives (SACCOs) in Butogota

6

Town Council, Kanungu district

1.4 Research Questions

The following research questions guided the researcher during the

research study;

What are different sources of debt finance for savings and credit

cooperatives (SACCOs)?

What could be the survival levels for savings and credit

cooperatives (SACCOs)?

What is the relationship between debt financing and the survival

of savings and credit cooperatives (SACCOs)?

1.5 Significance of the Study

The results of this study benefited in the following ways;

The study acted as an eye opener to future researchers in making

more analysis and criticizes the problems related to the study

phenomenon. The available data will be of great importance to the

academicians interested in the field of the study phenomenon.

Therefore academicians who wish to undertake further research on

debt financing also found the literature arising from this study

to be of great value.

Helped Small business owners by providing them with full

knowledge about the debt financing, and be easy for them to

obtain funds from the most appropriate sources available.

7

The study helped the Government, financial analysts and

administrators like managers to realize and assess the effects of

debt financing on the survival of savings and credit cooperatives

(SACCOs), the problems affecting small SACCOs and perhaps to

identify the possible solutions to such problems that affect

their performance.

Training Institutions such as Universities, colleges and other

microfinance institutions found the study useful as a reference

source. During their training, institutions stressed the emphasis

of imparting more skills on how to handle microfinance and

related issues with the help of the study material used in the

research.

The research findings were also of importance to policy makers at

national and local levels as they design policies aimed at

enhancing economic growth through a better savings and credit

system.

1.6 Scope of study;

The study was carried out in Butogota central, Western ward,

Butogota Town council where the Sacco is located. The study

covered the view of Sacco management, clients who benefit

directly and the community members. The study was limited to only

60 members because the researcher could not cover the entire

population of the area and Sacco at large due to financial

constraints.

8

1.7Operational definitions

Debt is a way to make an investment that could not otherwise be

made, to buy an asset (such as house, car, and corporate stock)

that you couldn’t buy without borrowing.

Debt financing is a strategy that involves borrowing money from a

lender or investor with the understanding that the full amount

will be repaid in the future, usually with interest.

Savings and Credit Cooperative; according to this study, Savings

and Credit Cooperative (SACCO) is a type of cooperative whose

objective is to pool savings for the members and in turn provide

them with credit facilities.

9

CHAPTER TWO: LITERATURE REVIEW

2.0 Introduction

This chapter covers the views of the researcher and those of

other scholars about the topic/problem under study. The

literature therefore focuses on the general and different sources

of debt financing, survival levels of small scale enterprises as

well as the relationship between debt financing and the survival

of small scale enterprise in Uganda and in the whole worldat

large.

2.1 Different Sources of Debt Finances and SACCOs

A Savings and Credit Cooperative (SACCO) is a type of cooperative

whose objective is to pool savings from the members and in turn

provide them with credit facilities. Other objectives of SACCOS

are to encourage thrift amongst the members and also to encourage

them on the proper management of money and proper investments

practices. Whereas in urban areas salary and wage earners have

formed Urban SACCOs, in rural areas, farmers have formed Rural

SACCOS. There are also traders, transport, and community-based

SACCOS.

Kennedy, T. et al. (1995) asserts that, a business can obtain

money from different sources depending on its needs and financial

situations. He added that, Banks and credit unions are

10

traditional sources for borrowing money and offer a variety of

options especially for businesses. If a business does not yet

have established credit, or its credit is poor to be able to get

the money needed through a commercial finance company, which

offers loans with higher interest rates to high risk borrowers.

Commercial financial institutions are available for loaning money

as well as for providing funds for inventory or equipment

purchases (Lee & Jong-Soo, 2000).

Small businesses can obtain debt financing from a number of

different sources (Schlitz P, 2000). These sources can be broken

down into general categories, private and public sources. Private

sources include friends, and relatives, banks, credit unions,

consumer finance companies, commercial finance companies, trade

credit, insurance companies, factor companies, and leasing

companies. Public sources of debt financing include a number of

loan programs provided by the state and federal governments to

support small businesses.

Lee & Jong-Soo (2000) contends that, many entrepreneurs begin

their enterprises by borrowing money from friends and relatives.

They added that, the main advantage of this type of arrangement

is that friends and relatives are likely to provide more flexible

terms of repayment than banks or other lenders. In addition,

these investors may be more willing to invest in an unproven

business idea, based upon their personal knowledge and

relationship with the entrepreneur, than other lenders. A related

disadvantage; however is that friends and relatives who loan11

money to help establish a small business may try to become

involved in its management. Experts recommend that small business

owners create a formal agreement with such investors to help

avoid future misunderstandings (Balunywa, 2006).

MFPED report (2007) assets that Banks are the sources that most

people immediately think of for debt financing. The report added

that, there are many different types of Banks, although in

general they exist to accept deposits and make loans. Most Banks

tend to be fairly risk averse and proceed cautiously when making

loans. As a result, it may be difficult for a young business to

obtain this sort of financing. Commercial banks usually have more

experience in making business loans than do regular savings

Banks. It may be helpful to review the differences among Banks

before choosing one as the target of a loan request. Credit

unions are another common source of business loans. Since these

financial institutions are intended to aid the members of a labor

union, they often provide funds more readily and under more

favorable terms than Banks. However, the amount of money that may

be borrowed through a credit union is usually not as large.

Oriaro, M. & Kerre, M. (2001) postulates that Trade credit is

another form of debt financing; They added that, whenever a

supplier allows a small business to delay payment on the products

or services it purchases, the small business obtain trade credit

from that supplier. Trade credit is readily available to most

small businesses, if not immediately then certainly after a few

orders. But the payment terms may differ between suppliers, so it12

may be helpful to compare or negotiate for the best terms. A

small business’s customer may also be interested in offering a

form of trade credit for example, by paying in advance for

delivery of products they will need on a future date in order to

establish a good relationship with a new supplier (Jamuar, R.S.,

et al, 1992).

The state and federal governments sponsor a wide variety of

programs that provide funding to promote the formation and growth

of small businesses (Donald P Stegall 2000). He added that, many

of these programs are handled by the U.S. Small Business

Administration (SBA) and involve debt financing. The SBA helps

small businesses obtain funds from Banks and other lenders by

guaranteeing loans up to $500,000 to a maximum of 70-90 percent

of the loan value, for only 2.75 percentage points above the

prime lending rate. In order to qualify for SBA guaranteed loan,

an entrepreneur must first be turned down for a loan through

regular channels. He or she must also demonstrate good character

and a reasonable ability to run a successful business and repay a

loan. SBA guaranteed loan funds can be used for business

expansion or for purchasing inventory, equipment, and real

estate. In addition to guaranteeing loans provided by other

lenders, the SBA also offers direct loans of up to $150000 as

well as seasonal loans, handicapped assistance loans, and

pollution control financing.

13

Finance companies are another option for small business loans

(Wendy & Mayer, 1998). Although they generally charge higher

interest rates than banks and credit unions, they also are able

to approve more requests for loans. Most loans obtained through

finance companies are secured by a specific asset as collateral

and that asset can be seized if the entrepreneur defaults on the

loan. Consumer finance companies provide small businesses with

loans for inventory and equipment purchases and are a good

resource for manufacturing enterprises. Insurance companies often

make commercial loans as a way of reinvesting their income (Wendy

& Mayer, 1998). They usually provide payment terms and interest

rates comparable to a commercial bank, but require a business to

have more assets available as collateral.

2.2 Survival Levels of SACCOs

Wendy & Mayer, (1998) postulates that, small business may be

thought of as having a financial growth cycle in which financial

needs and options change as the business grows, gains further

experience, and become less informational opaque. He further

explained that, if the firms remain in existence and continue to

grow, they may gain access to public equity and debt markets.

They emphasized that, the growth cycle paradigm is not intended

to fit all small businesses, and that firm size, age, and

information availability are far from perfectly correlated.

Bank failures can impose a long-run cost because of the loss of

bank-borrower relationships and the information built up through

14

contact over time, making it difficult for some borrowers to

continue finding investments that have positive net present

values (Slovin and Polonochek 1993). This would most likely

affect informally opaque small businesses that depend on their

Banks and would have difficulty finding external finance

elsewhere. In turn, this reduction in investment may exacerbate

regional or macroeconomic difficulties (Bemanke 1983). The

regulation and supervision of Banks to keep them safe and sound

is often justified at least in part on the basis of avoiding

systemic crises that might substantially reduce the supply of

credit to Bank-dependent small businesses.

The process of small scale enterprises in Uganda has especially

since the 1950s been in existence. Uganda inherited an

educational system which is by and large patterned after the

British educational system and the emphasis is on academic

education that prepares its products for lettered or white color

jobs (Ruth M, 1992). It is a common spectacle in all major cities

of developing countries to find the local citizens busily engaged

in a variety of formal sector activities. These enterprises are

important and they provide services and consumer goods to the

poor and low income groups (David B.Ekpenyong 1992).

Beck, T et al (2000) asserts that, of 5.2 million households in

the USA countries, only 0.6 percent can access mortgage loans

through commercial banks, 19.9 percent can access housing

microfinance loans through microfinance deposit taking

institutions, 7.2 percent can access loans from microfinance15

institutions and savings and credit cooperatives, 10.3 percent

can access loans through savings and credit cooperatives only,

and 62.3 percent have no access to financial services.

Early research treated small enterprises as peripheral survival

mechanisms whose Developmental impact was marginal (Ongile and

McCormick, 1996). This view was irrevocably changed by the 1972

International Labor Organization report that demonstrated the

significant employment and wealth creation potential of the

burgeoning, and often informal, small enterprise sector (ILO,

1972). Since the ILO report, the general outlook towards MSEs has

shifted dramatically. Benign neglect has been replaced by

recognition that the sector could be the lynchpin for improving

economic prospects in the developing world (King, 1996). But the

shift after the 1970s also benefited from a heightened

realization that a high and rising share of industrial employment

was still in the small enterprise sector.

The capacity for SACCOs to fulfill their potential in an economy

depends on the availability of finance (Cook, 2001; Whincop,

2001). Finance in general and credit in particular is especially

important for SACCOs since they are unable to finance themselves

through retained earnings or equity financing. According to the

researcher’s understanding, small scale enterprises need debt

finances from different sources in order to be sustainable since

they normally have inadequate equity to fund their activities.

Owners of SACCOs are still ignorant about the different sources

available to them as well as the survival levels of such SACCOs.16

2.3 Relationship between Debt Financing and Survival of SACCOs.

According to Robert D Hisrich (2007) explains that, debt

financing (also called asset based financing) requires that some

asset such as a car, house, plant, machine or land be used as

collateral. Debt financing requires the business owner to payback

the amount of funds borrowed as well as a fee expressed in terms

of the interest rate. There can also be an additional fee

sometimes referred to as points for using or being able to borrow

the money.

According to Christianet, (2008), debt financing can be a useful

tool for a business in need of additional cash flow. However, it

is meant to be a means to an end, namely of generating more money

for a business in order to grow it. He concluded that, business

owners should try to avoid falling into the revolving trap of

getting their business into an unmanageable state of debt.

The introduction of debt financing in the financing of the firm

introduces the element of leverage and hence the financing risk.

Leverage refers to a situation where the firm uses fixed

financing costs in its operations. Fixed cost such as agency

costs, bankruptcy costs and interest costs and interest costs on

debt give rise to financial leverage because these costs are

fixed and have to be met thus there is a high risk factor

attached to employment of debt. Financing risk is the probability

that the earnings of the firm will not be as projected just

because of the methods of financing used. Financing risk arises

17

debt has fixed financing obligations usually in the form of

interest which must be met before the shareholders can share in

the available (Kakuru, 2007).

Whincop, (2001) asserts that, very young enterprises often

experience shortages in cash flow that may make regular payments

difficult. He added that, most lenders provide severe penalties

for late or missed payments which may include charging late fees,

taking possession of collateral, or calling the loan due early.

Failure to make payments on a loan, even temporarily can

adversely affect a small businesses since lenders obtain loans.

Finally, the amount of money small businesses may be able to

obtain via debt financing is likely to be limited, so they need

to use other sources of financing as well.

According to Brian & Hamilton, (2002), like other types of

financing available to small businesses, debt financing has both

advantage and disadvantages. The primary advantage of debt

financing is that it allows the founders to retain ownership and

control of the company. In contrast equity financing, the

entrepreneurs are able to make key strategic decisions and also

to keep and reinvest more company profits (Oriaro, M. & Kerre, M.

2001).Furthermore, a debt that is paid on time can enhance a

small business’s credit rating and make it easier to obtain

various types of financing in the future. Debt financing is also

easy to administer as it generally lacks the complex reporting

requirements that accompany some forms of equity financing.

Finally, debt financing tends to be less expensive for small18

businesses over the long term though more expensive over the

short term than equity financing.

Financial leverage is commonly defined as the effect of using

debt financing on the owners’ return on equity (Reynolds, A.

1999). He added that, as a low margin business, Banks rely

heavily on debt (deposits, long-term borrowings, interbank

purchased funds etc.) to improve the ultimate return on equity.

Using high degrees of financial leverage is risky, because it

increases the volatility of the residual net income and it

increases the risk that an adverse business event consumes the

equity and brings about bankruptcy. Exploiting financial leverage

and providing generous equity coverage for adverse business

eventualities are inherently conflicting goals.(Anderson D.

1982). Hence, the eternal debate between shareholders/owners and

regulators and creditors of financial institutions about the

amount of equity to hold: owners would prefer to use as little

equity as possible and work mostly with “other peoples’ money” as

a way to improve returns, while creditors and depositors feel

safer, if owners invest more of their own money as an equity risk

buffer into the institution.

19

CHAPTER THREE: METHODOLOGY

3.0 Introduction

This chapter presents the methodology that was used during the

study; it gives a description of the research design and the

methods that was used to collect data from the field by the

researcher. It also gives a summary of the study area, population

of the study, sample size, sampling procedure, data collection

instruments, source of data, Data analysis, and the problems

encountered during data collection for the purpose of getting the

description of the effects of debt financing on the survival of

SACCOs in Kanungu, using a case study of Kayonza micro finance

SACCO.

3.1 Research design

The study used both explanatory and descriptive research designs.

Explanatory research design was used to explain the effects of

debt financing on the survival of SACCOs in Kayonza SACCO,

Butogota Town council, Kanungu District. It was used to explain

why things happen the way they do.

Descriptive research design was also used to explore the

magnitude and generate a clear insight with the aim of

discovering the content of the problem that was under study. The

selected designs were preferred due to economic status of the

researcher, coupled with limited time under which the study was

carried out. They were used to help the researcher to get

20

explanations and descriptions of the phenomenon under the study.

This helped the researcher to understand the variables in a bid

to bring new knowledge to the field of research.

3.2 Study Area

The study area was Butogota central, Butogota Town council around

22Km from Kanungu district Head Quarters along Buhoma-Bwindi

Impenetrable National park Road where Kayonza Micro finance SACCO

is located. The study covered the views of Kayonza Micro finance

SACCO Management and staff, clients who benefit directly

especially tea growers and the community members within the Town

Council.

3.3 Population of Study

The study population included the staff of Kayonza Micro finance

SACCO especially those who work in the savings department and the

members of the SACCO. A list of members from which the

respondents was chosen was obtained from the SACCO offices thus

acting as a sampling frame for the study. This study was limited

to only 60 members because the researcher could not cover the

entire population of Kayonza Micro finance SACCO members due to

financial constraints.

3.4 Sample Size

According to Emiru (2000), a sample is a representation of the

entire whole. The researcher selected 120 respondents to

21

represent the whole population of 760 people in the Town council

where 10 were from the management staff, 35 shareholders, 60

Kayonza microfinance SACCO members, and 15 business people, all

just within Butogota Town council.

Table 1: Sampling Population

Category of

Respondents

Target number of

people

Sample

size

Sample Technique

used

Management staff 25 10 Purposive

sampling

Shareholders 630 35 Purposive

sampling

Kayonza Sacco

Members

600 60 Simple random

sampling

Business people 220 17 Simple random

sampling

TOTAL 1475 120 Simple random

sampling

Source: field findings

22

3.5 Sampling procedure

The study the sampling procedures of both probability and non-

probability and consisted of random and purposive sampling

techniques.

Random sampling method involved selecting respondents from the

study population. Here, every respondent had an equal chance of

being chosen in the sample population. This method was used

especially to select non-members of Kayonza Micro-Finance Sacco

including business owners in Butogota Town Council.

Purposive sampling involved selecting a certain number of

respondents based on the nature of work. This method was

appropriate because it enables selection of informed persons who

knew important comprehensive information that enabled the

researcher gain a better insight into a problem. In the study,

respondents were contacted in person as the researcher wanted

fast hand information from them and the study keenly inquired

respondents’ views on the subject/problem under study.

3.6 Sources of Data

3.6.1 Primary Data

Primary data was gathered from respondents fromButogota Town

council, Kanungu District who were assumed to give firsthand

information on the researcher topic under study.

23

3.6.2 Secondary Source

Secondary data was obtained from sources like; Annual reports of

Kayonza Micro-Finance SACCO and Town council records, Journal

articles, internet, magazines, and text books related to the

subject under study and these were consulted at length to extract

the information required to support the findings from the study

respondents.

3.7 Reliability and Validity of research instruments

3.7.1 Validity

Law and kelton 1991 suggests that if a questionnaire model is

valid, then the decisions made with the questionnaire model

should be similar to those that would be made by physically

experimenting with the system. A questionnaire model is said to

be credible when its results are acceptable by respondents as

being valid, and being valid and used as an aid tool in

collecting data.

The validity of questionnaires was obtained by presenting it to

at least 5 professionals, including my research supervisor

because according to Amin (2005), content and construct validity

is determined by expert judgment.

24

3.7.2 Reliability

Reliability, according to Miles & Huber man (1994), has to do

with the extent to which the instruments generate consistent

responses over several trials with different audiences in the

same circumstances. The reliability of research instruments and

data was established following a pre-tested procedure of

instruments before their use with actual research respondents.

3.8 Data Collection Methods

The study was incorporated with the use of various methods in the

process of data collection in a bid to come up with better,

concrete and credible research findings. The researcher therefore

used a number of methods that included questionnaires, interviews

and documentary analysis in the process of collecting primary

data.

3.8.1 Questionnaire method

According to Robson (1993), a questionnaire is commonly applied

to research, designed to collect data from a specific population

or a sample from that population. Questionnaires are commonly

used as research instruments because of the distinct advantages

they yield (Leary, 1995). This method was used to collect data

because it is time saving and some respondents are literate

therefore there was no need of interviewing some of these

respondents. The Questionnaires were applied to the management

staff of Kayonza Micro-Finance Sacco, and some literate

25

shareholders. Therefore it made the work easy and enabled the

researcher to obtain accurate data.

Questionnaires consisted of open and closed ended questions

rather than forcing respondents to choose between limited

responses. This open form of Questionnaire also permitted the

respondents to answer freely and fully in their own words and

frame of reference. This method of collecting data gave the

responds an opportunity to reveal their motives or attitudes and

to specify the back ground of provisional conditions upon their

answers. Questionnaires are stable, consistent and provide

uniform measure without variations (Salantokos, 1997).

3.8.3 Interview method

This method was used in such a way that an interview schedule was

designed where research questions were used. These were posed to

different people especially the SACCO members, Business people

(Males and Women) and shareholders. The method was used in order

to help the researcher to get clear information and it also

helped the researcher to compare different views of the

respondents where the researcher used each respondent

individually. The researcher also asked questions to the

respondents as data was recorded down. This made the work easy

and enabled the researcher to repeat questions to the respondents

who were unable to understand some of the questions.

26

3.8.4 Focus Group interviews

This method was selected and applied to Kayonza Micro finance

members, this was used because all the selected members belonged

to the SACCO and benefit from programs acquire loans and they

come from the same area. Questions surrounding perceptions of

SACCO members on SACCO formation, SACCO selection, requirement

for accessing credit and the general implementation and the

effects of debt financing on the survival of SACCOs were asked.

This method allowed SACCO members to remind themselves on issues

that were affecting them and built confidence while putting

forward their mind. 3 FGD was held to interview 60 original SACCO

members who started the SACCO. Each group was composed of 20

SACCO members and this was intended to get information from at

least every member.

Focus group discussions helped the researcher to gather data

relating to feelings and opinions of a group of the respondents

sampled from the SACCO. Listening to other group members’ views

encouraged respondents to voice their own opinions readily and

this helped the researcher acquire information on the study the

more. This methodology provided rich data and insights that were

less accessible without the interaction within groups.

1.8.5 Documentary review

Review of documents for Kayonza SACCO was made on how the Sacco

assesses the debt financing and its survival, background

information among others. This was because for a SACCO to be27

effective in reaching the people, it should have a databank

showing the baseline, client characteristics and criteria for

defining the rich and poor.

Documents were accessed regarding the operation of Kayonza Micro-

Finance SACCO which was important in the implementation process

analysis of SACCO draft Act, internal SACCO rules and

regulations. The researcher also reviewed Kayonza Micro-Finance

SACCO operational manuals, supervision manuals, lending policy

manuals, monthly reports, ledger cards, account controls, general

ledgers and other related literature to obtain secondary data

which helped the researcher to effectively interpret the primary

data that was collected and analyzed. This information was got

from the SACCO, and other stakeholders in addition to interviews.

3.9 Data Processing and Analysis

During the process of data processing and analysis, the data

collected was designed and put it in order to obtain meaningful

form and make it look simpler and easier for interpreting and

reading by other readers.

Qualitative and quantitative methods of data analysis were used.

Quantitative analysis methods included personal communication.

Quantitative data collected was organized and presented according

to the objectives and research questions. Using the qualitative

methods, responses obtained were organized, coded and tabulated

28

for easy analysis. The coded data was analyzed to generate the

intended results in form of pie-charts, tables and graphs.

3.9.1 Organizing

This method was used in data processing and was organized through

labeling on data according to the targeted category of

respondents so as to get easy differentiation of data in

accordance to editing, coding and tabulation. All these were used

in order to promote accuracy of data that was collected during

the research process.

It also helped the researcher to identify the gaps in the data

collection methods and easily classify responses according to the

questions set into a meaningful information. Tables were used in

the presentation of the data and percentages used in the data

analysis.

3.9.2 Editing

This was done in order to check and reduce on mistakes and errors

of responses obtained from questionnaires and other unnecessary

information. This assisted the researcher to ensure that there is

accuracy and conformity of data collected. Follow-up of interview

schedules was done by the interviewer/Researcher to ensure that

data collected had no errors and omissions so that mistakes were

corrected before coding took place.

29

3.9.3 Coding

The information needed by the researcher was obtained by making

coding frames to tabulate the collected data into simple tables,

percentages according to the respondent regarding particular

questions. Coding was used to identify and put similar

responses/information together in order for the researcher to

come up with quality data and with a clear meaning for easy

understanding.

3.9.4 Tabulation

The researchers after organizing, editing, coding, tabulated the

coded information and presented it into a table form and

expressed the data into percentages from the tools used during

data collection. This helped the researcher to come up with

quality information on the study problem.

3.10 Limitations of the studyThe study was faced with the following constraints;

Time; the time allowed to do this research may not be enough to

allow exhaustive study and obtain all the essential information

for much more suitable conclusions. The problem will be minimized

by putting much effort on this research so as to meet the

deadline.

Financial Constraints; the Researches faced financial resources

problems such as the transport costs and stationery to carry out

the research effectively.

30

In an effort to mitigate this shortcoming, the researcher tried

to source for funds from a few sponsors and were possible would

ignore undesirable necessities.

Slow and Non- response; since the researcher did not know the

kind of respondents that were being dealt with, some of them

would failed to respond to questionnaires, delayed to fill them

and others were rear.

Therefore this required the researcher to set an appropriate

appointment with the respondents in order to ensure that data is

availed in time.

Information hiding; Due to the sensitivity of the study, some

respondents refused to give some data to the researcher citing

the reason behind the study.

The researcher however tried to overcome this by showing an

introductory letter acquired from the university fully explaining

the purpose of the research. The researcher also assured

respondents that their ideas would be treated with the

necessarily confidentiality.

31

CHAPTER FOUR:

DATA PRESENTATION, INTERPRETATION AND ANALYSIS

4.0 Introduction

This chapter attempts to analyze the data collected and its

interpretation in relation to the studied themes. The empirical

findings of the study are presented, analyzed and interpreted in

this chapter. The collected data was organized from the responses

on the questionnaires and the interview guide administered to the

Management staff and other share-holders in the Sacco.

The chapter also highlights the demographic characteristics of

the respondents in terms of gender, age of respondents, marital

status, level of education and the positions they held in SACCO

in relation to their views and perceptions towards the effect of

debt financing on the effective performance of SACCOs. The reason

for including the biographic data was such that variables would

assist in generating varied information in all aspects hence

helping the researcher to understand the relationship between the

study variables.

4.1 Background information of the Respondents

4.1.1 Gender distribution of the respondentsTable 2: A table showing Gender distribution of the respondents

32

Sex Frequency

(No_)

Percent (%)

Valid

Male 52 43

Female 68 57

Total

120

100

Source: Primary data, 2014

Table II above shows that the numbers of respondents in terms of

sex that was 52(43%) male and 68(57) female. This enabled the

researcher to acquire data from all sexes as his respondents

during the study.

4.1.2 Age of the Respondents

Further analysis was made on the age of respondents to determine

whether decisions made when running the individual’s businesses

are dependent on age. The respondents were therefore asked to

identify their age and responses were tabulated as below;

Table 3: Showing age intervals of respondents

Age

Bracket

Frequency

(No_)

Percent (%) Valid Percent

(%)

15-30 21 17.5 18

33

Vali

d

31-40 39 32.4 32

41+ 60 50.0 50

Total 120 100.0 100

Source: primary data, 2014

Majority of the respondents were in the age brackets of 41 and

above representing 60(50%) while the age bracket of 31-40 were

rated at 39(32%), 15-30 who were 21(18%) respectively. This

implies that small scale enterprises members/managers in the area

of study are between the ages of 41 and above. Therefore basing

on the age groups interviewed it can be interpreted that data was

obtained from mature respondents who were believed to reliable.

4.1.3 Respondents Marital Status

The researcher also considered the marital status background of

respondents to establish how it relates to the effects of debt

financing on the effective performance of SACCOsin Butogota Town

council, Kanungu District. The findings are presented in table

III below

Table 4: Showing marital status of respondents

34

Marital

Status

Frequency

(No_)

Percent

(%)

Valid Percent

(%)

Valid

Single 30 25.0 25

Married 66 55.0

55

Widow 8 6.6

7

Separated 16 13.3 13

Total 120 99.9 100

Source: Primary data, 2014

The majority of the respondents that is 66 (55%) were the

married, separated respondents were 16(13%), while the single

ones were 30(25%) and the widows were represented by the

percentage of 7 and a frequency of 8 people, who participated in

the study. This implied that majority of the respondents were

married. The study therefore dealt with the right respondents who

determined the relationship between debt financing and the

effective performance of SACCOs inButogota Town council, Kanungu

Districtand these respondents deemed fit for the study.

35

36

Figure 1: A pie chart showing the marital status of respondents

single25%

married55%

widow7%

separated13%

Marital status of respondents

Figure1 revealed that 55% of the respondents that participated in

the study were married, 25% were single, 13% separated and 7%

widowed. This means that both respondents are much aware of the

effects of the effects of debt financing on the effective

performance of SACCOs.

37

4.1.4 Level of education of respondents

The researcher also had an interest in the academic

qualifications of the respondents as part of their bio data and

the responses acquired were given as in the table below;

Table 5: Showing level of education of respondents

Level of

education

Frequency

(No_)

Percentage

(%)

Valid

Percentage (%)

Vali

d

No formal

education

10 8.3 8

Primary Level 12 10.0 10

Secondary

Level

30 25.0 25

Tertiary 68 56.6 57

Total 120 99.9 100

Source: Primary data, 2014

Table V shows that most of respondents represented by 68 (57%)

had attained tertiary level education, 30 (25%) had attained38

secondary level education (10%) of the respondents had attained

primary level while 10 of the respondents representing (8%) had

no formal education. This meant that most of the SACCOs in

Butogota Town Council are managed by people who have attained

education.

4.1.5 Respondents positions held in SACCOsTable 6; Showing respondents’ position held in SACCOs

39

Occupation of

Respondents

Frequency

(No_)

Percent

(%)

Valid Percent

(%)

Vali

d

Management staff

10

8.3

8

Shareholders

35

29.1

29

SACCO Members

60

50.0

50

Business people

15

12.513

Total

120

99.9

100

Source: Primary data 2014

From table VI above, findings revealed that 50% were SACCO

members, 29% were shareholders, 13% were business people, and

management staff constituted of 8%. This implies that the

researcher was not biased with the type of respondents he used in

the study. Therefore this was why the researcher considered and

used their responses to draw conclusions. This therefore shows

that SACCO members were much aware of the effects of debt

40

financing on the effective performance of SACCOs since it was the

group that was affected and because of their economic status.

41

Figure 2: A pie chart showing the respondents positions held in SACCOs

mgt staff8%

Shareholders29%

Sacco members50%

Bussiness people13%

A pie chart showing percetange of the respondents positions held in SACCOs

Source: field findings 2014

Figure 2 revealed that 50% of the respondents that participated

in the study were SACCO members, 29% were shareholders, 13%

business people and management staff constituted 8% respondents.

This means that both SACCO members and business people were much

aware of the effects of debt financing on the effective

performance of SACCOs.

42

4.2 Sources of Debt Finances

4.2.1. Debt finances as a major source of Sacco finances

Most SACCOs are financed usually using debt finances in their

operations. This is because owners of these SACCOs are always

having insufficient equity funds basing on their entrepreneurial

background hence a need for debt finances to finance the

effective performance of their SACCOs.

Table 7: Showing Respondent’s response on whether debt financing is a major source of finances for SACCOs

Category of

responses

Frequency

(No_)

Percent

(%)

Valid Percent

(%)

Vali

d

Strongly agree 66 55.0 55

Agree 50 41.3 41

Not sure - - -

Strongly

disagree

2 1.6 2

Disagree 2 1.6 2

43

Total 120 99.8 100

Source: Primary data, 2014

It was observed from the study that majority of SACCOs that use

debt financing as a major source of finances for their effective

operations. This was revealed by the response of 66(55%) of the

respondents who strongly agreed that debt financing is a major

source of finances for SACCOs, 41(41%) of the respondents also

agreed with the variable though 2(2%) of the respondents

disagreed. This therefore means that most of members of Kayonza

Micro Finance Sacco finance their businesses through use of loans

borrowed from lending institutions.

Table 8: Showing Responses on the different sources of debt financing employed by SACCOs

Sources of Debt

Financing

Frequency

(No_)

Percent

(%)

Valid Percent

(%)

Val

id

Private sources 92 76.6 77

Public sources 28 23.3 23

Total 120 99.9 100

Source: Primary data, 2014

From the table VIII above it was revealed that most SACCOs use

private sources of debt finances. Private sources pointed out by44

respondents included friends, relatives, commercial banks and

credit unions. This was supported by almost all respondents that

added up to 92 of number sampled (77%). However only 28 (23%)

respondents revealed that they obtained their debt finances from

the government especially from the “Prosperity for All”

arrangements as brought about by the current government in Uganda

which some respondents lamented that it no longer works these

days.

Figure 3: A pie chart showing the different sources of debt financing employed SACCOs

private sources77%

public sources23%

Different sources of debt financing employed by SACCOs

Source: field findings 2014

Figure 4.3 revealed that 77% of the respondents that participated

in the study agreed that, most SACCOs use private sources of debt

finances while, 23% of the respondents revealed that they have

always obtained their debt finances from the government

especially from the program “Prosperity for All” arrangements as

brought about by the current government in Uganda.

45

Table 9: Showing Managers responses on whether commercial banks are the major sources of debt financing employed by small scale enterprises

Responses Frequency

(No_)

Percent

(%)

Valid Percent

(%)

Valid

Strongly

agree

85 70.8 71

Agree 25 20.4 20

Not sure - - -

Strongly

disagreed

3 2.5 3

Disagree 7 5.8 6

Total 120 99.5 100

Source: Primary data, 2014

From the table IX above 85 respondents representing 71% strongly

agreed that small scale enterprises obtain their debt finances

from commercial banks since these commercial banks charge

relatively lower interest compared to individual lenders and

credit societies commonly known as SACCOs. However 7 respondents

representing 6% disagreed with a view that commercial banks are

not the major sources of debt finances since they do not cover

all the localities thus they do not operate in some rural areas

46

of Uganda compared to local lenders like friends, relatives and

credit unions like the SACCOs. Only 3 respondents representing 3%

strongly disagreed.

It was therefore concluded that most small scale enterprises in

rural areas of Uganda obtain their debt finances from other

private sources like friends, relatives and savings and credit

societies other than commercial banks. This was because most

commercial banks do not operate from rural areas of Uganda

compared to saving and credit societies which are commonly

situated in rural set up areas.

Table 10: Showing Managers and other respondent’s responses on whether they face difficulty in trying to access debt finances from different sources available

Responses Frequency Percent Valid Percent

Vali

d

Strongly

agree

21 17.5 18

Agree 82 68.3 68

Not sure 2 1.6 2

Strongly

disagree

4 3.3 3

Disagree 11 9.1 9

Total 120 99.8 100

47

Source: Primary data, 2014

From table X above 45 respondents representing 68% of managers

and other members of Kayonza Micro Finance SACCO agreed that they

face more difficulties when trying to access debt finances from

different sources open for them. Respondents argued that such

difficulties are unfavorable interest charges and unfavorable

credit terms. Only 11 respondents representing 9% of managers

disagreed and other members of the same SACCO while 2 respondents

were not sure about the difficulty in trying to access debt

finances from different sources available.

Respondents further explained that, they are given too short

repayment period and with high interest fees, no enough grace

period among others. They said this could be because too big

loans with wrong repayment frequencies further encourage creation

of delinquent loans as clients fail to pay their loan

obligations.

This therefore means that the Managers of other lending

institutions do not provide appropriate and convenient repayment

periods to other cooperatives especially SACCOs. This information

mainly was got from monitoring reports using document review

method provided by credit officers from the loan register and

summary of the loans outstanding for the members. This was

explained as in form of some lending institutions asking for

daily, weekly or monthly repayment when some businesses have not

made profits.

48

4.3 Effective performance Levels of SACCOs

The study also aimed at establishing the effective performance

levels of debt finances in the area of study that is and findings

are there presented below;

4.3.1 Period of operation in their enterprises (SACCO)Table 11: A table showing the managers and other respondents’ responses on period of operation in their enterprise (SACCO)

Period of

operation

Frequency Percent (%) Valid Percent

(%)

Vali

d

Less than a

year

2 1.6 2

Less than two

years

15 12.3 12

More than two

years

98 81.6 82

Not sure 5 4.1 4

Total 120 99.8 100

Source: Primary data, 2014

From the table, XI above it was revealed that most SACCOs in

Butogota Town Council have effectively worked with SACCOs for

more than two years as confirmed by 98 respondents representing

49

81% of respondents. This means that effective performance levels

of SACCOs are high. However 11 respondents representing 12% said

that they had worked with SACCOs for less than two years, 2

respondents representing 2% had operated in SACCOs for less than

year which showed that some new members were coming up to join

the SACCO because of its effective performance in the area of

study while only 5 respondents representing 4% were not sure of

the period they had spent in the SACCO.

Table 12: Showing Managers and SACCO member’s responses on whether financial constraints undermine the effective performanceof SACCOs

Responses Frequency(NO

_)

Percent

(%)

Valid Percent

(%)

Vali

d

Strongly agree 30 25.0 25

Agree 86 71.3 71

Not sure

2

1.6 2

Disagree 2 1.6 2

Strongly

disagree

00 0.0 0

Total 120 98.2 100

Source: Primary data, 2014

50

From table XII above, respondents were probed to find responses

on whether financial constraints undermine the effective

performance of SACCOs. It was therefore found out that the

effective performance of SACCOs was majorly influenced by

financial factors such as high interest rates for the borrowed

funds and insufficient equity funds. This was confirmed by 86

respondents representing 71% of the total respondents who agreed

with the variable.

However 2 respondents representing 2% of the total respondents

disagreed. They revealed that there are other factors like stiff

competition, economic factors like inflation, unfavorable

government policies and natural calamities depending on the type

of the SACCO. Only 2 respondent representing 2% of managers and

other members of Kayonza Micro Finance SACCO under the study were

not sure.

Table 13: Managers and other SACCO member’s responses on whether government policies have supported the effective performance of SACCOs

Responses Frequency(NO_

)

Percent (%) Valid Percent

(%)

Vali

d

Strongly

agree

43 35.8 36

Agree 64 53.3 53

Not sure 3 2.5 3

51

Strongly

disagree

4 3.3 3

Disagree 6 5.0 5

Total 120 99.9 100

Source: Primary data, 2014

From table XIII above the researcher found out that effective

performance of most SACCOs was as a result of favorable

government policies such as peace and stability among others in

the area of study, prosperity for all schemes and this was

confirmed by 64 respondent representing 53% of the total

respondents who agreed.

However, 6 (5%) respondents disagreed by revealing that some

government policies were not favorable towards their operation

and that their performance had been as a result of other factors

other than favorable policies.

Respondents pointed out factors as entrepreneurial skills and

persistence as their major factors for their effective

performance. They also pointed out unfavorable government

policies like high taxes for some commodities which increase the

prices for such commodities hence reducing the overall demand of

such commodities. This hinders the performance of SACCOs in the

long run due to reduced revenues.

52

Only 3 respondents representing 3% of total respondents were not

sure on whether government policies have supported the effective

performance of SACCOs.

4.4 Relationship between Debt Finances and the effective performance of SACCOs.

Table 14: Showing Respondent’s responses on whether debt financeshad been fundamental towards the development of their SACCOs.

Responses Frequenc

y

Percent Valid

Percent

Vali

d

Strongly agree 47 39.1 39

Agree 73 60.8 61

Not sure - - -

Strongly

disagree

- - -

Disagree - - -

Total 120 99.9 100

Source: Primary data, 2014

From the table XIV above, 47 of the respondents representing 39%

strongly agreed that the long time performance of their SACCO

depended on the use of debt finances and 73 respondents

53

representing 61% agreed on the view that debt finances were

fundamental towards the development of their effective

performance.

This was because debt finances was associated with fixed

financing obligations in form of regular interest payments that

increase the outflows of the business hence reducing the revenues

of the enterprise in the long run.

54

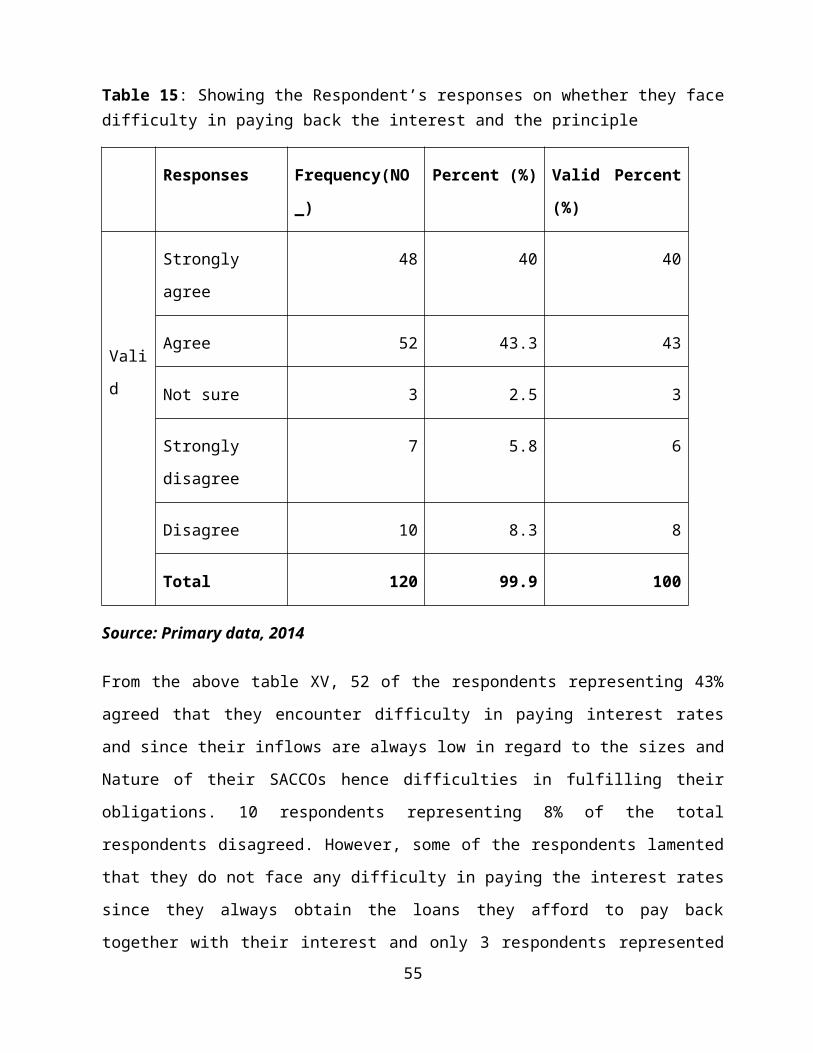

Table 15: Showing the Respondent’s responses on whether they facedifficulty in paying back the interest and the principle

Responses Frequency(NO

_)

Percent (%) Valid Percent

(%)

Vali

d

Strongly

agree

48 40 40

Agree 52 43.3 43

Not sure 3 2.5 3

Strongly

disagree

7 5.8 6

Disagree 10 8.3 8

Total 120 99.9 100

Source: Primary data, 2014

From the above table XV, 52 of the respondents representing 43%

agreed that they encounter difficulty in paying interest rates

and since their inflows are always low in regard to the sizes and