Chinese banks - Debt 101

36

Deutsche Bank Markets Research Asia China Banking / Finance Banks Industry Chinese banks - Debt 101 Date 9 January 2017 Industry Update Dealing with debt... pivoting from corporate to government & household What is in this report? ________________________________________________________________________________________________________________ Deutsche Bank AG/Hong Kong Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MCI (P) 057/04/2016. Hans Fan, CFA Research Analyst (+852 ) 2203 6353 [email protected] Jacky Zuo Research Associate (+852 ) 2203 6255 [email protected] Stephen Andrews, CFA Research Analyst (+852 ) - 2203 6191 [email protected] Top picks ICBC (1398.HK),HKD4.73 Buy China Merchants Bank (3968.HK),HKD18.62 Buy Source: Deutsche Bank Companies Featured ICBC (1398.HK),HKD4.73 Buy China Construction Bank (0939.HK),HKD5.83 Buy Agri. Bank of China (1288.HK),HKD3.26 Hold Bank of China (3988.HK),HKD3.52 Buy Bank of Communications (3328.HK),HKD5.74 Hold China Merchants Bank (3968.HK),HKD18.62 Buy China CITIC Bank (0998.HK),HKD5.12 Hold China Minsheng Bank (1988.HK),HKD8.45 Hold CEB (6818.HK),HKD3.62 Hold Chongqing Rural Bank (3618.HK),HKD4.58 Hold Huishang Bank (3698.HK),HKD3.97 Sell Bank of Chongqing (1963.HK),HKD6.69 Sell Shanghai Pudong Bank (600000.SS),CNY16.18 Sell Industrial Bank (601166.SS),CNY16.18 Sell Ping An Bank (000001.SZ),CNY9.13 Hold Bank of Beijing (601169.SS),CNY9.84 Buy Bank of Nanjing (601009.SS),CNY11.22 Sell Bank of Ningbo (002142.SZ),CNY17.25 Sell Source: Deutsche Bank We value Chinese banks using a three- stage Gordon Growth Model (PV= (ROE- g)/(COE-g)), with target prices based on 2016E book values. Upside risk: the removal or softening of the GDP target. Downside risk: a property price correction. China’s rapidly-growing debt has been the market’s focus for years. In this report we summarize our comprehensive proprietary studies into this issue. We mainly aim to answer three simple questions: 1) How big is China’s debt issue? 2) How to deal with it? 3) How does it impact Chinese banks? We use a structured framework to assess China’s debt risks, which breaks down the debt balance by funding source, financing channel and borrower (Fig 4). We expect a structural downtrend in ROE of the China banking sector, as China will leverage up govt while restructuring corporate debt. The only sweet spot is household leveraging-up, which should benefit retail-orientated banks. How big is China’s debt issue? (page 2-7) China boasts a total debt balance of Rmb195tr (or US$28tr) as of Sept 2016, accounting for 275% of GDP, we estimate. The absolute level of debt leverage is not the highest globally, but the pace of increase indeed is. Amid elevated leverage, we estimate around 8-11% of debt has higher risks. Corporate debt is the key (c.60% of total debt), 13-18% of which is “evergreened” in 2018E. From borrowers’ perspective, how to deal with it? (page 8-10) The root cause of China’s debt issue is the GDP targeting. With a 6.5% target in place, there is double-digit credit growth embedded and we model China’s debt-to-GDP ratio to rise above 300% by 2018. In contrast to deleveraging the whole economy, a more likely scenario is to leverage up China’s government and household, while attempting to delever the corporate sector. How does it impact Chinese banks? (page 11-19) The likelihood of a hard landing and systemic banking crisis is very low, as government could leverage up and liquidity risk is limited both externally and internally. However, government leveraging-up and the ongoing restructuring of SOE debts are likely to compress the asset yield of Chinese banks, leading to a structural downtrend in ROE. The only positive is household leveraging-up, which should benefit retail-orientated banks, i.e., CMB and big-four. From the perspective of funding sources, how to deal with it? (Page 20-24) There is an increasingly uneven distribution of risks within China’s banking system. Big banks and CMB have been de-risking, while other banks are growing their asset base aggressively. Policy banks are growing rapidly to support infrastructure build, which is effectively government leveraging itself up. Smaller banks are the weaker link in the banking system, featuring heavy shadow banking exposure and mounting capital risks. We expect more consolidation among smaller banks to happen, which is positive for big banks. From the perspective of financing channels, how to deal with it? (page 25-27) Among the financing channels, shadow banking has experienced remarkable growth, leading to rising capital and liquidity risk for the banking system. However, all financial regulators have been tightening up on shadow banking since May 2016, which may impact the capital and earnings of smaller banks. Prefer retail-orientated banks over the long run; CMB is our top pick While sector ROE may decline structurally, we expect retail banks to record sustained profitability. In the long run, CMB is our top pick, as it is the only bank to achieve ROA recovery and to sustain a mid-teen ROE. Distributed on: 08/01/2017 22:12:27 GMT

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Chinese banks - Debt 101

Deutsche Bank Markets Research

Asia

China

Banking / Finance

Banks

Industry

Chinese banks - Debt 101

Date

9 January 2017

Industry Update

Dealing with debt... pivoting from corporate to government & household

What is in this report?

________________________________________________________________________________________________________________

Deutsche Bank AG/Hong Kong

Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MCI (P) 057/04/2016.

Hans Fan, CFA

Research Analyst

(+852 ) 2203 6353

Jacky Zuo

Research Associate

(+852 ) 2203 6255

Stephen Andrews, CFA

Research Analyst

(+852 ) - 2203 6191

Top picks

ICBC (1398.HK),HKD4.73 Buy

China Merchants Bank (3968.HK),HKD18.62

Buy

Source: Deutsche Bank

Companies Featured

ICBC (1398.HK),HKD4.73 Buy

China Construction Bank (0939.HK),HKD5.83

Buy

Agri. Bank of China (1288.HK),HKD3.26 Hold

Bank of China (3988.HK),HKD3.52 Buy

Bank of Communications (3328.HK),HKD5.74

Hold

China Merchants Bank (3968.HK),HKD18.62

Buy

China CITIC Bank (0998.HK),HKD5.12 Hold

China Minsheng Bank (1988.HK),HKD8.45 Hold

CEB (6818.HK),HKD3.62 Hold

Chongqing Rural Bank (3618.HK),HKD4.58 Hold

Huishang Bank (3698.HK),HKD3.97 Sell

Bank of Chongqing (1963.HK),HKD6.69 Sell

Shanghai Pudong Bank (600000.SS),CNY16.18

Sell

Industrial Bank (601166.SS),CNY16.18 Sell

Ping An Bank (000001.SZ),CNY9.13 Hold

Bank of Beijing (601169.SS),CNY9.84 Buy

Bank of Nanjing (601009.SS),CNY11.22 Sell

Bank of Ningbo (002142.SZ),CNY17.25 Sell

Source: Deutsche Bank

We value Chinese banks using a three-

stage Gordon Growth Model (PV= (ROE-

g)/(COE-g)), with target prices based on

2016E book values.

Upside risk: the removal or softening of

the GDP target. Downside risk: a

property price correction.

China’s rapidly-growing debt has been the market’s focus for years. In this report we summarize our comprehensive proprietary studies into this issue. We mainly aim to answer three simple questions: 1) How big is China’s debt issue? 2) How to deal with it? 3) How does it impact Chinese banks? We use a structured framework to assess China’s debt risks, which breaks down the debt balance by funding source, financing channel and borrower (Fig 4). We expect a structural downtrend in ROE of the China banking sector, as China will leverage up govt while restructuring corporate debt. The only sweet spot is household leveraging-up, which should benefit retail-orientated banks.

How big is China’s debt issue? (page 2-7) China boasts a total debt balance of Rmb195tr (or US$28tr) as of Sept 2016, accounting for 275% of GDP, we estimate. The absolute level of debt leverage is not the highest globally, but the pace of increase indeed is. Amid elevated leverage, we estimate around 8-11% of debt has higher risks. Corporate debt is the key (c.60% of total debt), 13-18% of which is “evergreened” in 2018E.

From borrowers’ perspective, how to deal with it? (page 8-10) The root cause of China’s debt issue is the GDP targeting. With a 6.5% target in place, there is double-digit credit growth embedded and we model China’s debt-to-GDP ratio to rise above 300% by 2018. In contrast to deleveraging the whole economy, a more likely scenario is to leverage up China’s government and household, while attempting to delever the corporate sector.

How does it impact Chinese banks? (page 11-19) The likelihood of a hard landing and systemic banking crisis is very low, as government could leverage up and liquidity risk is limited both externally and internally. However, government leveraging-up and the ongoing restructuring of SOE debts are likely to compress the asset yield of Chinese banks, leading to a structural downtrend in ROE. The only positive is household leveraging-up, which should benefit retail-orientated banks, i.e., CMB and big-four.

From the perspective of funding sources, how to deal with it? (Page 20-24) There is an increasingly uneven distribution of risks within China’s banking system. Big banks and CMB have been de-risking, while other banks are growing their asset base aggressively. Policy banks are growing rapidly to support infrastructure build, which is effectively government leveraging itself up. Smaller banks are the weaker link in the banking system, featuring heavy shadow banking exposure and mounting capital risks. We expect more consolidation among smaller banks to happen, which is positive for big banks.

From the perspective of financing channels, how to deal with it? (page 25-27) Among the financing channels, shadow banking has experienced remarkable growth, leading to rising capital and liquidity risk for the banking system. However, all financial regulators have been tightening up on shadow banking since May 2016, which may impact the capital and earnings of smaller banks.

Prefer retail-orientated banks over the long run; CMB is our top pick While sector ROE may decline structurally, we expect retail banks to record sustained profitability. In the long run, CMB is our top pick, as it is the only bank to achieve ROA recovery and to sustain a mid-teen ROE.

Distributed on: 08/01/2017 22:12:27 GMT

9 January 2017

Banks

Chinese banks - Debt 101

Page 2 Deutsche Bank AG/Hong Kong

How big is China’s debt issue?

China boasts a total debt balance of Rmb195tr (or US$28tr) as of Sept 2016, accounting for 275% of GDP, we estimate.

The absolute level of debt leverage is not the highest globally, but the pace of increase indeed is. This is the reason for market concerns on banks’ asset quality.

Figure 1: China’s debt-to-GDP ratio has spiked since 2008

38 40 40 40 42 48 55 56 53 55 61 61 58 53 48 44 43 56 58 57 53 49 49 49 46 45 44 42 45 50 58 58 63 70 73 83 85 88 91 15 16 17 18 19 22

26 27 26 28 32 33 33 31 29 28 28

40 44 45 41 43 47 52 54 48 46 43 39 50

50 48 53

57 62 67 69 69 66

2 2 3 3 3 4

7 8 9

11 12 14 16 17 17 17 19 18

23 31 32

33 38

39 41 42 44 46

2 2 2 2 2 2 2

2 4 4 5

6 8 9 11 11

15 17 16

16 14 18 16

17 16 15

15 16

17

18 18 18 19

1 2 3 4

5 6 7 8 9

11 13 14 15 16 17 18

26 26 27

30 32

38

44 47 51 53

53 57 58 58 62 71

83 86 81 85 96 99 96 89 85 82 84

114 124 127 124 125

137 147 147 141 139 139 135

166 182 180

195

213 228

253 261

270 275

0

50

100

150

200

250

300% China's debt-to-GDP ratio during 1980-3Q16

Local

governments

Central

government

Households

Private enterprises

SOEs

+140ppt in

7.75 years

Source: Deutsche Bank estimates, PBOC, CBRC, CIRC, SAFE, NBS, MOF, CEIC, WIND, Chinabond.com.cn, Trustee Association of China, SAC, HKMA, media reports Note: 1) We have included loans, bonds, shadow banking and offshore credit; 2) We have eliminated the overlapping between different financing channels; 3) We classify LGFV debt into local government debts.

9 January 2017

Banks

Chinese banks - Debt 101

Deutsche Bank AG/Hong Kong Page 3

Figure 2: China’s credit leverage is not the highest… Figure 3: …but its pace of increase is one the of fastest

23

26

54

50

45

51

66

106

83

72

168

89

156

105

75

115

99

17

16

16

10

25

71

71

90

123

79

42

61

44

59

88

100

66

28

36

16

69

75

32

55

43

35

97

46

110

69

91

89

72

213

6 8

7 8

8 6

1 2 9

1 4 5

1 5 3

1 9 2

2 3 9

2 4 5

2 5 5

2 5 5

2 6 0

2 7 1

2 7 8

0 100 200 300 400

Indonesia

Mexico

Russia

India

Brazil

Thailand

Malaysia

Korea

Australia

US

China - BIS

Singapore

China - DBe

Euro area

UK

Canada

Japan

Global comparison - Credit-to-GDP ratio (1H16)

Non-financial corporation

Household

Government

(%)

3 9 7

2 9 5

2 7 0

129.7

106.6

70.0

62.0

55.3

46.0

45.3

39.0

38.0

37.8

33.2

27.8

23.4

19.5

16.1

9.6

0.5

0 10 20 30 40 50 60 70 80 90 100 110 120 130 140

China - DBe

China - BIS

Japan

Canada

Singapore

Australia

Malaysia

Thailand

Korea

Euro area

Brazil

UK

Mexico

Russia

US

Indonesia

India

Global comparison - Credit-to-GDP ratio change during 2008-1H16

(%) Source: Deutsche Bank estimates, BIS Source: Deutsche Bank estimates, BIS

How high is the risk and where are the weaker links?

We use a structured framework to assess the risks of China’s debt, splitting Rmb195tr debt by: 1) funding source; 2) financing channel; 3) borrower. In this report, we firstly focus on the risk profile of different borrowers, and then we also provide detailed analysis on key risks in funding sources and channels.

From borrowers’ perspective, we assign a debt-at-risk ratio to each type of borrower and we estimate the system debt-at-risk ratio to be around 8-11%

under a hard-landing scenario. Corporate debt (57% of total debt) is the key, for which we assign a notably higher debt-at-risk ratio of 13-18%.

9 January 2017

Banks

Chinese banks - Debt 101

Page 4 Deutsche Bank AG/Hong Kong

Figure 4: Overview of total system credit by funding source, financing channel, borrower and risk profile

On-

B/S

Non-bank financial

institutions (9%)

Corporates (7%)

Individuals (6%)

SOEs (Rmb64tr, 33% of total)

Bank loans(Rmb106tr, 55% of total)

FUNDING SOURCES FINANCING CHANNELS BORROWERS

Private enterprises (Rmb47tr, 24% of total)

Households(Rmb32tr, 17% of total)

Local governments(Rmb37tr, 19% of total)

Central governments(Rmb13tr, 7% of total)

Bonds(Rmb41tr, 21% of total)

Shadow banking(Rmb42tr, 22% of total)

Offshore credit (2% of

total)

Banks (78%)

13-18%

5%

0%

DEBT AT RISK

RATIO

8-11%

SYSTEM

DEBT AT RISK

RATIO

$ $

Source: Deutsche Bank estimates, PBOC, CBRC, CIRC, SAFE, NBS, MOF, CEIC, WIND, Chinabond.com.cn, Trustee Association of China, SAC, HKMA, media reports Note: 1) We have eliminated the overlapping between different financing channels; 2) We classify LGFV debt into local government debts.

How to assess corporate debt risks? It is about the degree of evergreening

We define “evergreening debt” as when underlying corporate borrowers are unable to generate sufficient cash flows and/or do not have sufficient excess cash to meet their debt obligations, so that they have to borrow new credit to repay their debt. This represents a stress test on corporate debt servicing capacity.

9 January 2017

Banks

Chinese banks - Debt 101

Deutsche Bank AG/Hong Kong Page 5

Our proprietary studies suggest that approximately 12-15% of corporate credit, or Rmb13-17tr, was evergreening in 2016, and the proportion might

increase to 13-18% by 2018. We did two studies, i.e. top-down and bottom-up.

Top-down study: One can quantify the evergreening credit for all corporates in China by sizing the gap between 1) debt services, item (1) in the below table, which measures the principal due and interest repayment for all corporates for one year; and 2) corporate debt serving capacity, item (2) in the below table, which include operating cash flows, excess cash and equity raising.

For more details, please see our report The degree of evergreening, dated 23 February 2016.

Figure 5: Our proprietary top-down analysis of China’s evergreening credit

Rmb trn Item 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017E 2018E

Corporate debt services (1) 7.7 8.8 10.5 12.1 12.9 14.5 16.1 18.3 23.4 29.5 35.9 44.8 53.5 60.9 68.9 75.8 83.4

- Principal repayment 7.1 8.1 9.7 11.1 11.7 12.9 14.7 16.6 20.7 25.7 31.5 39.5 47.1 54.7 62.4 68.6 75.5

- Interest repayment 0.6 0.7 0.9 1.0 1.2 1.6 1.3 1.7 2.8 3.8 4.4 5.3 6.3 6.2 6.5 7.2 7.9

Corporate debt serving capacity (2) 7.2 7.5 8.7 11.7 14.6 16.6 18.8 23.3 28.4 31.5 35.7 42.3 47.5 50.5 55.5 60.1 64.9

- Operating cash flows 3.6 3.3 3.7 5.8 7.5 8.2 8.9 12.0 12.8 14.1 18.5 22.3 24.0 23.6 25.0 26.6 28.3

- Excess cash 3.5 4.2 4.9 5.8 6.7 7.8 9.4 10.8 14.8 16.8 16.8 19.7 22.8 25.0 27.2 29.1 31.0

- Equity raising 0.0 0.1 0.1 0.1 0.3 0.6 0.5 0.5 0.8 0.6 0.4 0.3 0.7 1.9 3.3 4.4 5.6

Evergreening debt (3) = (1) - (2) 0.5 1.3 1.8 0.3 (1.7) (2.1) (2.7) (5.1) (4.9) (2.0) 0.2 2.5 6.0 10.4 13.4 15.8 18.5

- As a % of corporate credit (4) = (3) / (6) 5% 9% 12% 2% -9% -9% -10% -15% -11% -4% 0% 3% 7% 10% 12% 13% 13%

- As a % of system credit (5) = (3) / (7) 3% 6% 8% 1% -6% -6% -6% -9% -7% -2% 0% 2% 4% 6% 7% 7% 8%

Total corporate credit balance (6) 11.7 13.9 16.0 17.3 19.7 22.8 26.6 34.6 44.2 51.3 62.4 74.8 85.9 101.1 114.0 125.4 138.0

Total system credit balance (7) 16.5 20.1 23.6 26.2 30.2 37.3 42.9 57.5 74.3 87.1 104.1 125.3 145.2 171.2 200.9 221.0 243.1 Source: Deutsche Bank estimates, PBOC, CBRC, CIRC, SAFE, NBS, MOF, CEIC, WIND, Chinabond.com.cn, Trustee Association of China, SAC, HKMA, media reports

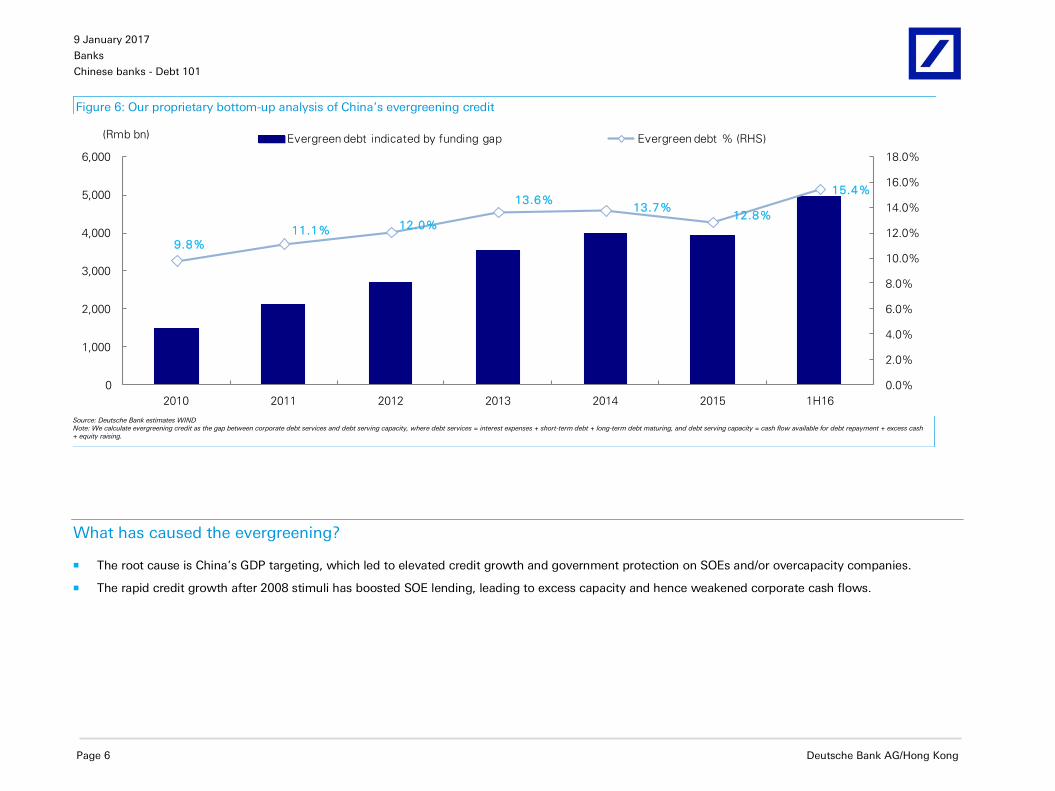

How to assess corporate debt issue? The bottom-up study on the degree of evergreening

The top-down study on evergreening debt may underestimate the problem, as it nets out the weaker part of corporates due to the aggregate data. So we did another bottom-up study, which checked the debt service on 1,500 corporate bond issuers.

Using the same methodology as the top-down analysis, we calculate the debt service amount and debt serving capacity per annum for every single sampled company. We add all the debt balance of corporates that could not generate sufficient debt serving capacity to cover their debt services, and divided by total debt of the entire sample.

Our bottom-up study concludes that the evergreening debt amounted to 15.4% of the total debt of these companies as of 1H16.

9 January 2017

Banks

Chinese banks - Debt 101

Page 6 Deutsche Bank AG/Hong Kong

Figure 6: Our proprietary bottom-up analysis of China’s evergreening credit

9.8%

11.1% 12.0%

13.6%13.7%

12.8%

15.4%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

0

1,000

2,000

3,000

4,000

5,000

6,000

2010 2011 2012 2013 2014 2015 1H16

Evergreen debt indicated by funding gap Evergreen debt % (RHS)(Rmb bn)

Source: Deutsche Bank estimates WIND Note: We calculate evergreening credit as the gap between corporate debt services and debt serving capacity, where debt services = interest expenses + short-term debt + long-term debt maturing, and debt serving capacity = cash flow available for debt repayment + excess cash + equity raising.

What has caused the evergreening?

The root cause is China’s GDP targeting, which led to elevated credit growth and government protection on SOEs and/or overcapacity companies.

The rapid credit growth after 2008 stimuli has boosted SOE lending, leading to excess capacity and hence weakened corporate cash flows.

9 January 2017

Banks

Chinese banks - Debt 101

Deutsche Bank AG/Hong Kong Page 7

Figure 7: China’s SOE debt has grown faster than private sector debt since 2008

52

24

0

10

20

30

40

50

60

70

80

% Corporate credit breakdown 1980-3Q16 - SOEs vs. private enterprises

SOE debt

(SOE+LGFV)

% total credit

Private debt

% total credit

2008-now -

"Guo Jin Min Tui"

Faster growth in SOE

credit

1998-2008 -

"Guo Tui Min Jin"

Faster growth in

private sector credit

after SOE reform

1980-1998 - SOE-dominated economy

Before SOE reform in 1998

144

66

0

20

40

60

80

100

120

140

160

% Credit-to-GDP during 1980-3Q16 - SOEs vs. private enterprises

SOE debt

(SOE+LGFV)

% GDP

Private debt

% GDP

2008-now -

"Guo Jin Min Tui"

Faster growth in SOE

credit

1998-2008 -

"Guo Tui Min Jin"

Faster growth in

private sector credit

after SOE reform

1980-1998 - SOE-dominated economy

Before SOE reform in 1998

Source: Deutsche Bank estimates, PBOC, CBRC, CIRC, SAFE, NBS, MOF, CEIC, WIND, Chinabond.com.cn, Trustee Association of China, SAC, HKMA, media reports Note: 1) We have eliminated the overlapping between different financing channels; 2) We classify LGFV debt into local government debts.

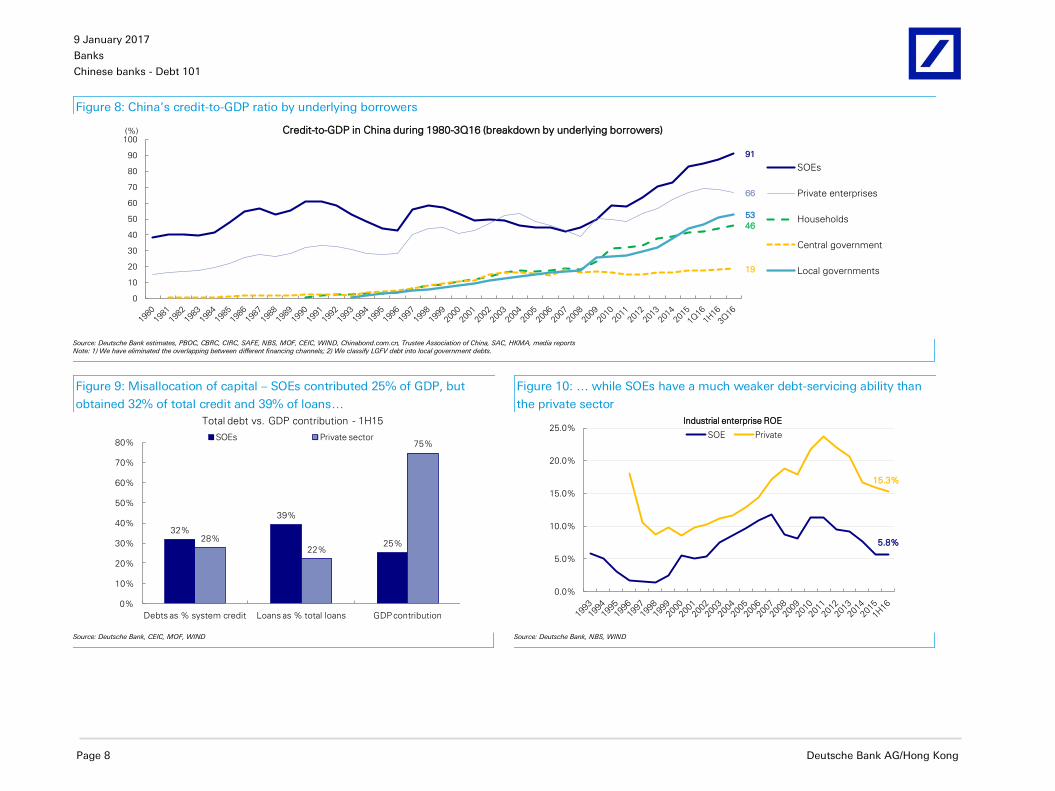

What has caused the evergreening?

The protection on SOEs has led to misallocation of capital in the system and hence lower productivity and mounting risks. The SOE sector has gained stronger credit support from financial institutions, which are disproportionate to their GDP contribution and despite their weaker profitability.

9 January 2017

Banks

Chinese banks - Debt 101

Page 8 Deutsche Bank AG/Hong Kong

Figure 8: China’s credit-to-GDP ratio by underlying borrowers

91

66

46

19

53

0

10

20

30

40

50

60

70

80

90

100Credit-to-GDP in China during 1980-3Q16 (breakdown by underlying borrowers)

SOEs

Private enterprises

Households

Central government

Local governments

(%)

Source: Deutsche Bank estimates, PBOC, CBRC, CIRC, SAFE, NBS, MOF, CEIC, WIND, Chinabond.com.cn, Trustee Association of China, SAC, HKMA, media reports Note: 1) We have eliminated the overlapping between different financing channels; 2) We classify LGFV debt into local government debts.

Figure 9: Misallocation of capital – SOEs contributed 25% of GDP, but

obtained 32% of total credit and 39% of loans…

Figure 10: … while SOEs have a much weaker debt-servicing ability than

the private sector

32%

39%

25%28%

22%

75%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Debts as % system credit Loans as % total loans GDP contribution

Total debt vs. GDP contribution - 1H15

SOEs Private sector

5.8%

15.3%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%SOE Private

Industrial enterprise ROE

Source: Deutsche Bank, CEIC, MOF, WIND Source: Deutsche Bank, NBS, WIND

9 January 2017

Banks

Chinese banks - Debt 101

Deutsche Bank AG/Hong Kong Page 9

How to deal with it? Why can’t China banks recognize evergreening debt as NPLs and write them off in one go?

The root cause of China’s debt issue, in our view, is the GDP target. As China has targeted to grow GDP by 6.5% annually by 2020, there is a double-digit credit growth rate embedded in order to support this target. If China banks recognize all evergreening debt as NPLs, credit growth is likely to fall sharply and GDP growth to drop, which is against China’s GDP target.

Thus we expect China’s debt-to-GDP to rise to over 300% by 2018E, if China sticks to its 6.5% GDP target. In absolute terms, we model that China needs

to generate US$12-13tr of new credit during 2016-18. For details please refer to our report FITT – Waking the consumer banking giants, dated 6 April 2016.

Figure 11: Modeling China’s credit growth: Debt to GDP could rise above 300% by YE18

(RMB bn) 2010 2011 2012 2013 2014 2015 2016E 2017E 2018E

Nominal GDP 40,890 48,412 53,412 58,802 63,591 67,671 73,115 79,247 84,485

Nominal growth rate 18.3% 18.4% 10.3% 10.1% 8.1% 6.4% 8.0% 8.4% 6.6%

US$ bn 6,041 7,490 8,466 9,564 10,320 10,767 10,891 11,321 11,721

Avg FX rate 6.77 6.46 6.31 6.15 6.16 6.28 6.71 7.00 7.21

M2 72,585 85,159 97,415 110,652 122,837 139,228 158,720 179,988 201,587

Growth rate 18.9% 17.3% 14.4% 13.6% 11.0% 13.3% 14.0% 13.4% 12.0%

Total Credit Assets (BIS

data)76,650 90,645 108,195 129,088 148,721 171,308 197,713 225,373 254,483

YoY 21.5% 18.3% 19.4% 19.3% 15.2% 15.2% 15.4% 14.0% 12.9%

Credit/GDP 187% 187% 203% 220% 234% 253% 270% 284% 301%

Credit multiplier 1.18x 0.99x 1.87x 1.91x 1.87x 2.37x 1.92x 1.67x 1.95x

Total Bank assets 96,161 113,787 133,686 152,475 172,203 199,156 226,739 257,743 289,277

YoY growth 18.8% 18.3% 17.5% 14.1% 12.9% 15.7% 13.9% 13.7% 12.2%

US$ bn 14,593 18,079 21,457 24,835 27,757 30,670 32,391 36,820 39,091

Source: Deutsche Bank, CEIC, Bank of International Settlements

9 January 2017

Banks

Chinese banks - Debt 101

Page 10 Deutsche Bank AG/Hong Kong

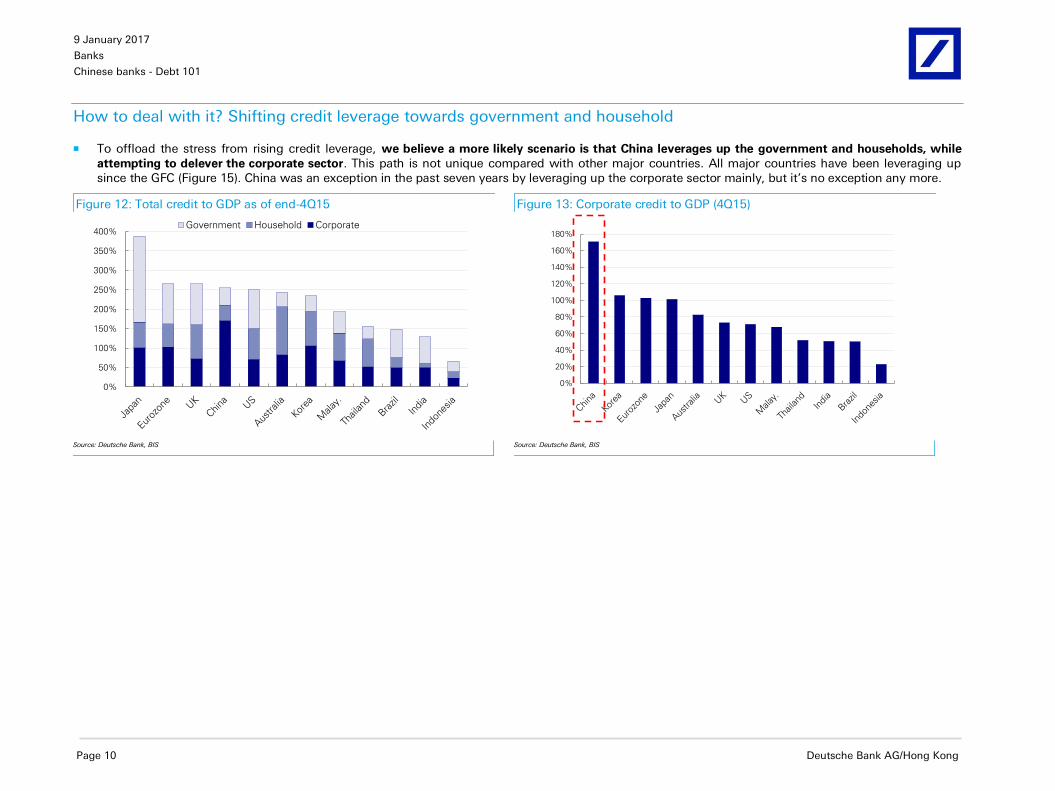

How to deal with it? Shifting credit leverage towards government and household

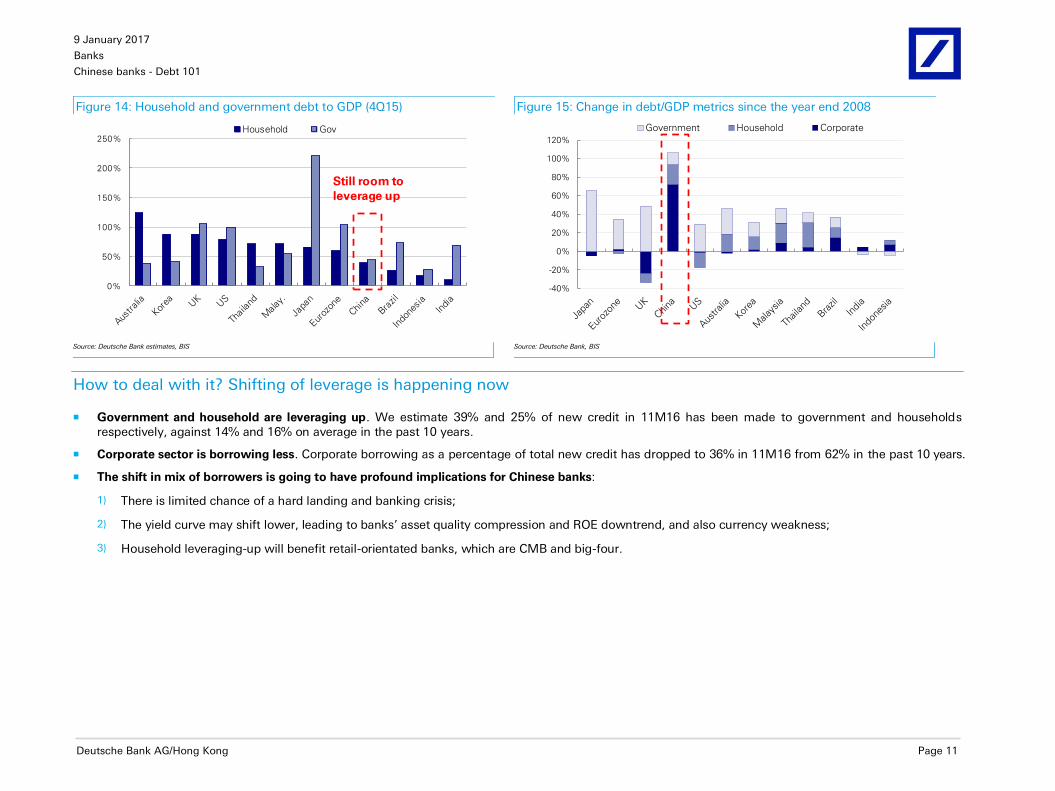

To offload the stress from rising credit leverage, we believe a more likely scenario is that China leverages up the government and households, while

attempting to delever the corporate sector. This path is not unique compared with other major countries. All major countries have been leveraging up since the GFC (Figure 15). China was an exception in the past seven years by leveraging up the corporate sector mainly, but it’s no exception any more.

Figure 12: Total credit to GDP as of end-4Q15 Figure 13: Corporate credit to GDP (4Q15)

0%

50%

100%

150%

200%

250%

300%

350%

400%Government Household Corporate

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

Source: Deutsche Bank, BIS Source: Deutsche Bank, BIS

9 January 2017

Banks

Chinese banks - Debt 101

Deutsche Bank AG/Hong Kong Page 11

Figure 14: Household and government debt to GDP (4Q15) Figure 15: Change in debt/GDP metrics since the year end 2008

0%

50%

100%

150%

200%

250%Household Gov

Still room to

leverage up

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

Government Household Corporate

Source: Deutsche Bank estimates, BIS Source: Deutsche Bank, BIS

How to deal with it? Shifting of leverage is happening now

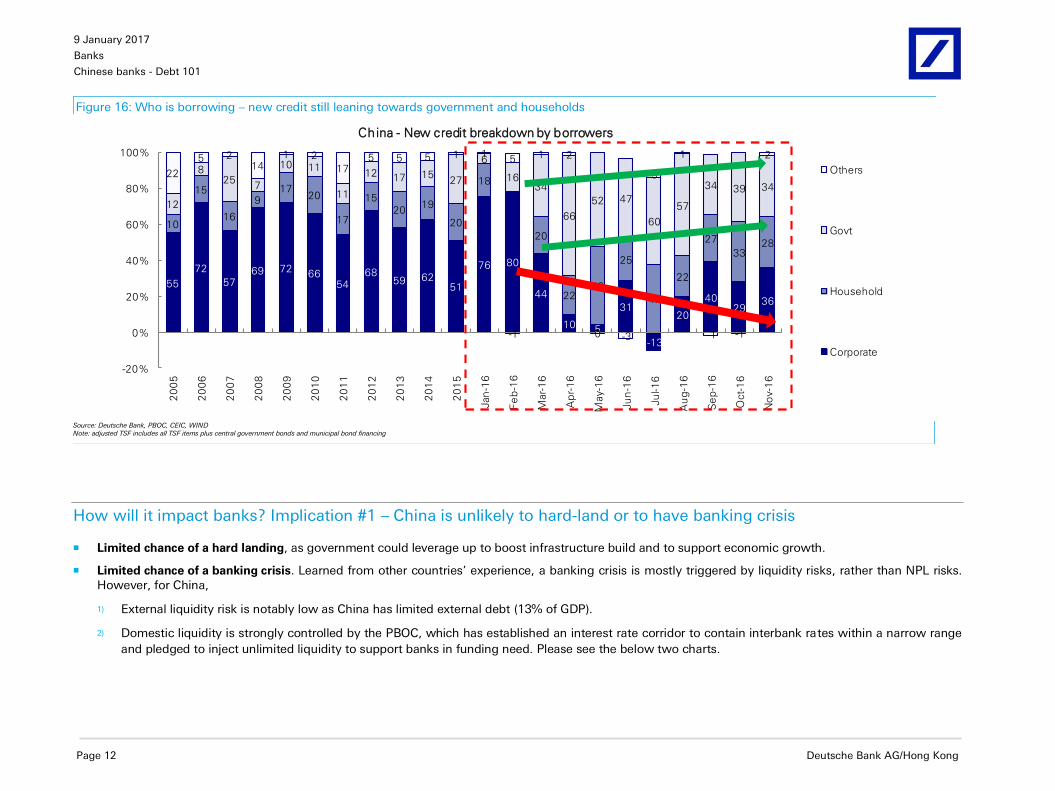

Government and household are leveraging up. We estimate 39% and 25% of new credit in 11M16 has been made to government and households respectively, against 14% and 16% on average in the past 10 years.

Corporate sector is borrowing less. Corporate borrowing as a percentage of total new credit has dropped to 36% in 11M16 from 62% in the past 10 years.

The shift in mix of borrowers is going to have profound implications for Chinese banks:

1) There is limited chance of a hard landing and banking crisis;

2) The yield curve may shift lower, leading to banks’ asset quality compression and ROE downtrend, and also currency weakness;

3) Household leveraging-up will benefit retail-orientated banks, which are CMB and big-four.

9 January 2017

Banks

Chinese banks - Debt 101

Page 12 Deutsche Bank AG/Hong Kong

Figure 16: Who is borrowing – new credit still leaning towards government and households

55

72

5769 72

6654

6859 62

51

76 80

44

10 5

31

-13

20

4029

36

10

15

16

917

20

17

15

2019

20

18

-1

20

2243

25

47

22

27

3328

12

825

7

10 11

11

12 17 1527

6

1634

66

52 47

60

57

34 39 34

22

5 214

1 2

175 5 5 1 1

5 1 2

0 -3

5

1

-1 -1

2

-20%

0%

20%

40%

60%

80%

100%

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

Jan

-16

Fe

b-1

6

Mar-

16

Ap

r-1

6

May-1

6

Ju

n-1

6

Ju

l-1

6

Au

g-1

6

Se

p-1

6

Oct-

16

No

v-1

6

China - New credit breakdown by borrowers

Others

Govt

Household

Corporate

Source: Deutsche Bank, PBOC, CEIC, WIND Note: adjusted TSF includes all TSF items plus central government bonds and municipal bond financing

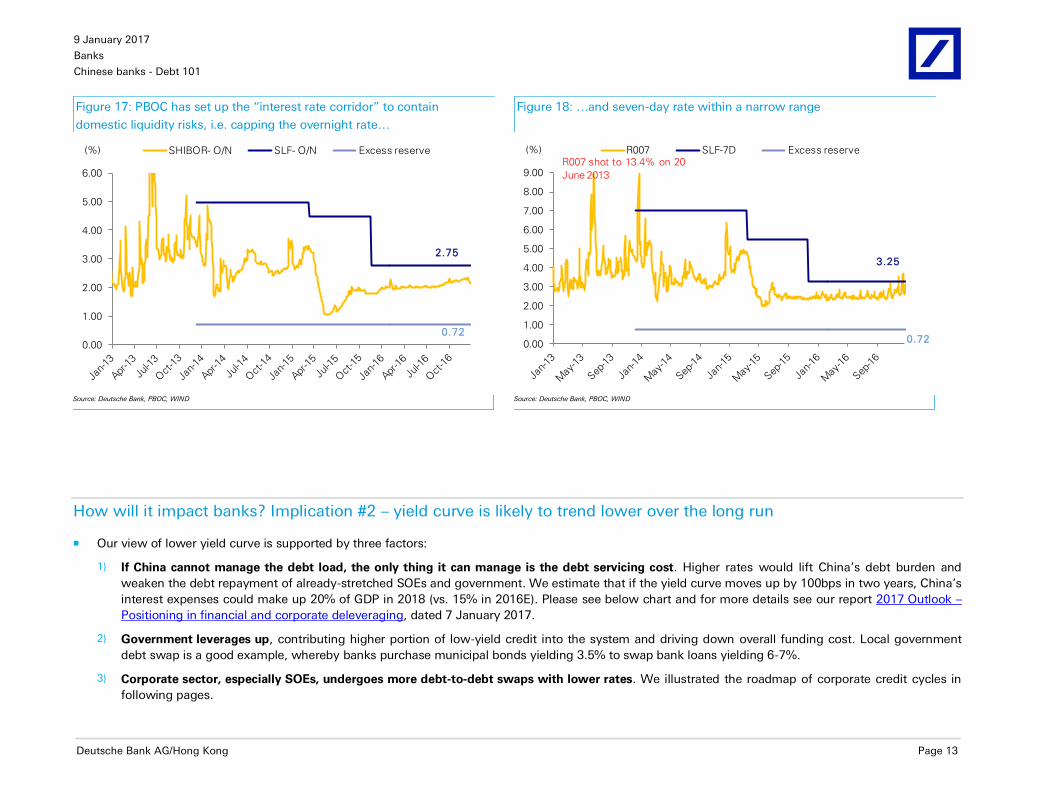

How will it impact banks? Implication #1 – China is unlikely to hard-land or to have banking crisis

Limited chance of a hard landing, as government could leverage up to boost infrastructure build and to support economic growth.

Limited chance of a banking crisis. Learned from other countries’ experience, a banking crisis is mostly triggered by liquidity risks, rather than NPL risks. However, for China,

1) External liquidity risk is notably low as China has limited external debt (13% of GDP).

2) Domestic liquidity is strongly controlled by the PBOC, which has established an interest rate corridor to contain interbank rates within a narrow range

and pledged to inject unlimited liquidity to support banks in funding need. Please see the below two charts.

9 January 2017

Banks

Chinese banks - Debt 101

Deutsche Bank AG/Hong Kong Page 13

Figure 17: PBOC has set up the “interest rate corridor” to contain

domestic liquidity risks, i.e. capping the overnight rate…

Figure 18: …and seven-day rate within a narrow range

2.75

0.72

0.00

1.00

2.00

3.00

4.00

5.00

6.00

SHIBOR- O/N SLF- O/N Excess reserve(%)

3.25

0.720.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

R007 SLF-7D Excess reserve(%)

R007 shot to 13.4% on 20

June 2013

Source: Deutsche Bank, PBOC, WIND Source: Deutsche Bank, PBOC, WIND

How will it impact banks? Implication #2 – yield curve is likely to trend lower over the long run

Our view of lower yield curve is supported by three factors:

1) If China cannot manage the debt load, the only thing it can manage is the debt servicing cost. Higher rates would lift China’s debt burden and

weaken the debt repayment of already-stretched SOEs and government. We estimate that if the yield curve moves up by 100bps in two years, China’s

interest expenses could make up 20% of GDP in 2018 (vs. 15% in 2016E). Please see below chart and for more details see our report 2017 Outlook –

Positioning in financial and corporate deleveraging, dated 7 January 2017.

2) Government leverages up, contributing higher portion of low-yield credit into the system and driving down overall funding cost. Local government

debt swap is a good example, whereby banks purchase municipal bonds yielding 3.5% to swap bank loans yielding 6-7%.

3) Corporate sector, especially SOEs, undergoes more debt-to-debt swaps with lower rates. We illustrated the roadmap of corporate credit cycles in

following pages.

9 January 2017

Banks

Chinese banks - Debt 101

Page 14 Deutsche Bank AG/Hong Kong

Figure 19: If yield curve moves up by 100bps in two years, China’s interest expenses may make up 20% of GDP in 2018E (vs. 15% in 2016E)

2.2%

10.0%

7.9%

9.5%

6.8%

15.7%

13.6%

16.5%

19.5%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

China's interest burdens (total interest expenses as a % of GDP)DB

estimates

+100bps

flat yield

- 100bps

Source: Deutsche Bank estimates, PBOC, CBRC, CIRC, SAFE, NBS, MOF, CEIC, WIND, Chinabond.com.cn, Trustee Association of China, SAC, HKMA, media reports

How will it impact banks? Implication #2 – yield curve is likely to trend lower over the long run (Continued)

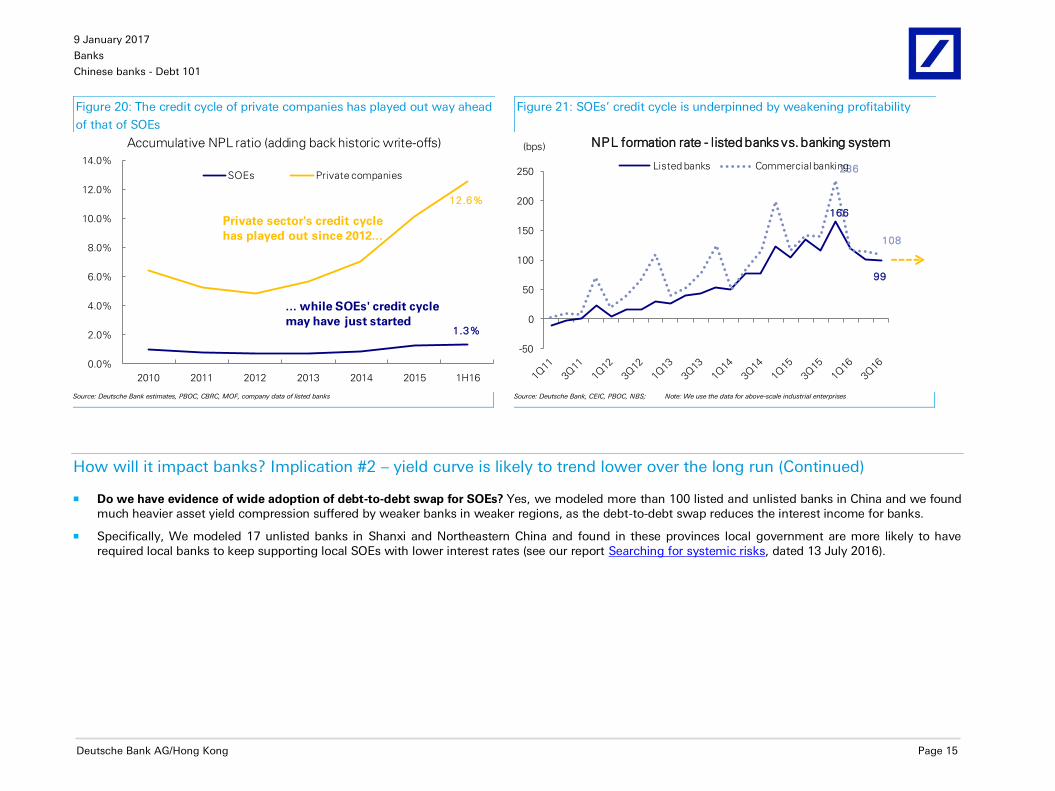

China’s corporate sector is running two credit cycles in parallel but at different stages. While the credit cycle for private companies has likely peaked out with an NPL ratio of 13%, the SOE credit cycle has probably just started, with NPL ratio of only 1.3% (Figure 20). Please see our report Transition between two credit cycles, dated 19 September 2016, for more details.

How will the SOE credit cycle play out? We believe debt-to-debt swaps, i.e. lengthening loan tenors and lowering interest rates, are likely to be much

more widely adopted than other measures (which may include debt-to-equity swap, bankruptcy and M&As). The debt restructuring plan for Shanxi’s seven major coal companies is a good example, whereby banks are lengthening short-term loans into long-term ones and also lowering the interest rates. Before and after the restructure, the troubled SOEs are all classified as performing loans.

As such, the impact on banks from the SOE credit cycle would be asset yield compression, not a bad debt charge. This partly explains why NPL formation of China banking system has moderated recently (Figure 21).

For more details, please see our report The roadmap of SOE credit cycle dated 19 October 2016.

9 January 2017

Banks

Chinese banks - Debt 101

Deutsche Bank AG/Hong Kong Page 15

Figure 20: The credit cycle of private companies has played out way ahead

of that of SOEs

Figure 21: SOEs’ credit cycle is underpinned by weakening profitability

1.3%

12.6%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

2010 2011 2012 2013 2014 2015 1H16

Accumulative NPL ratio (adding back historic write-offs)

SOEs Private companies

Private sector's credit cycle

has played out since 2012...

... while SOEs' credit cycle

may have just started

166

99

236

108

-50

0

50

100

150

200

250

NPL formation rate - listed banks vs. banking system

Listed banks Commercial banking

(bps)

Source: Deutsche Bank estimates, PBOC, CBRC, MOF, company data of listed banks Source: Deutsche Bank, CEIC, PBOC, NBS; Note: We use the data for above-scale industrial enterprises

How will it impact banks? Implication #2 – yield curve is likely to trend lower over the long run (Continued)

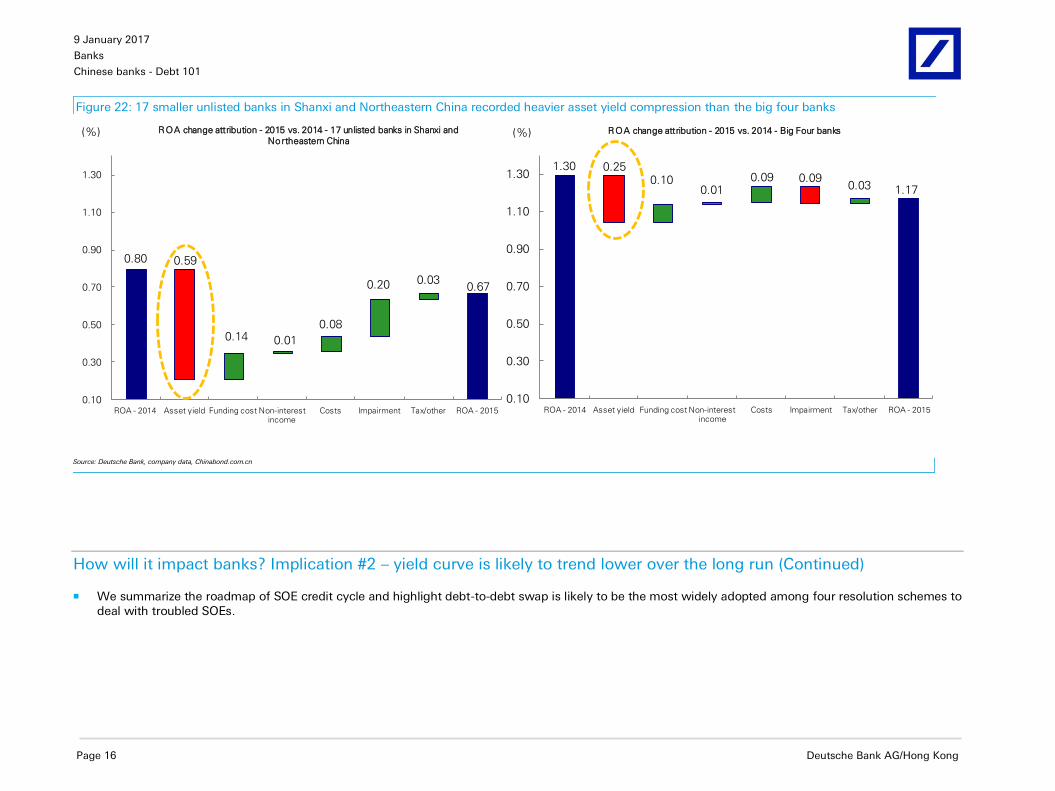

Do we have evidence of wide adoption of debt-to-debt swap for SOEs? Yes, we modeled more than 100 listed and unlisted banks in China and we found much heavier asset yield compression suffered by weaker banks in weaker regions, as the debt-to-debt swap reduces the interest income for banks.

Specifically, We modeled 17 unlisted banks in Shanxi and Northeastern China and found in these provinces local government are more likely to have required local banks to keep supporting local SOEs with lower interest rates (see our report Searching for systemic risks, dated 13 July 2016).

9 January 2017

Banks

Chinese banks - Debt 101

Page 16 Deutsche Bank AG/Hong Kong

Figure 22: 17 smaller unlisted banks in Shanxi and Northeastern China recorded heavier asset yield compression than the big four banks

0.80 0.59

0.14 0.01

0.08

0.20 0.030.67

0.10

0.30

0.50

0.70

0.90

1.10

1.30

ROA - 2014 Asset yield Funding cost Non-interest income

Costs Impairment Tax/other ROA - 2015

(%) ROA change attribution - 2015 vs. 2014 - 17 unlisted banks in Shanxi and

Northeastern China

1.30 0.250.10

0.010.09 0.09

0.03 1.17

0.10

0.30

0.50

0.70

0.90

1.10

1.30

ROA - 2014 Asset yield Funding cost Non-interest income

Costs Impairment Tax/other ROA - 2015

(%) ROA change attribution - 2015 vs. 2014 - Big Four banks

Source: Deutsche Bank, company data, Chinabond.com.cn

How will it impact banks? Implication #2 – yield curve is likely to trend lower over the long run (Continued)

We summarize the roadmap of SOE credit cycle and highlight debt-to-debt swap is likely to be the most widely adopted among four resolution schemes to deal with troubled SOEs.

9 January 2017

Banks

Chinese banks - Debt 101

Deutsche Bank AG/Hong Kong Page 17

Figure 23: The roadmap to deal with distressed SOEs and the impacts on banks would mostly be asset yield compression, rather than bad debt charges

Bankruptcy

M&A or asset disposal

Debt-to-equity swap

Debt-to-debt swap

(i.e. lowering lending

rates & lengthening

durations)

Resolution schemes

Banks

Social capital

(e.g. WMPs, social

security funds,

insurers)

Governments and

SOEs

Funding sources

3rd party entities for DES

Impacts on banks

Banks’ own subsidiaries

State-owned capital mgmt cos.

AMCs

Insurers’ asset mgmt arms

Hybrid schemes

NPL

Asset quality pressure

Int. income Risks Fees

Int. income Asset quality pressure

P&L impact from haircut

Int. income Asset quality pressure

Int. income Asset yield compression

Asset quality pressure

LT benefit

Source: Deutsche Bank, CBRC, State Council, Caixin report Note: 1) The size of the colored boxes largely represents the size of the resolution schemes; 2) regarding the impacts on banks, the color of arrows refers to positive or negative – if green, positive; if red, negative – the direction of arrows refers to the trends.

How will it impact banks? Implication #2 – yield curve is likely to trend lower over the long run (Continued)

Looking ahead, we expect a lower yield curve to lead to a structural downtrend in the asset yield and ROE of Chinese banks. As shown in the below chart, asset yield compression is likely to become the single largest contributing factor to ROA decline, rather than bad debt charge.

9 January 2017

Banks

Chinese banks - Debt 101

Page 18 Deutsche Bank AG/Hong Kong

Figure 24: The roadmap to deal with distressed SOEs and the impacts on banks would mostly asset yield compression, rather than bad debt charge

1.13 1.16

0.590.03

0.35 0.010.05 0.92

-0.20

0.00

0.20

0.40

0.60

0.80

1.00

1.20

(%) Listed banks' ROA change attribution - 2015 vs 2018E

Source: Deutsche Bank estimate, company data

How will it impact banks? Implication #3 – Household leverage-up to benefit retail-orientated banks

Can Chinese households leverage up further? This is probably the first question investors think of when referring to household leverage.

We believe so, as China’s household leverage looks low:

1) From the perspective of household balance sheet (Figure 25), household debt is modest when compared with household financial assets. We estimate the total household debt balance accounted for only 29% of household financial assets in China as of 1H16.

9 January 2017

Banks

Chinese banks - Debt 101

Deutsche Bank AG/Hong Kong Page 19

2) From the perspective of household income statement (Figure 26), the average household in China needs to manage annual retail loan repayments (interest + principal) equivalent to 16% of their disposal income in 1H16, lower than 45% for Korea and 27% for the US.

For more details, please see our report Analyzing the property exposure, dated 10 November 2016.

Figure 25: Household leverage (debt % financial assets) is low in China

even for less wealthy families

Figure 26: Household debt services as a % of disposal income in China is

lower than other countries

22%

33%

29%

10%

15%

20%

25%

30%

35%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 1H16

Household debts as % of household financial assets - CNHigh net worth family Common family CN household

16%

27%

45%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

1H

16

Household debt services as % disposal income

( i nterest rates adjusted)China US Korea

Source: Deutsche Bank Estimate, BCG China Private Banking Report 2015, PBOC Note: High net worth family is defined as household financial assets above Rmb6mn

Source: Deutsche Bank, PBOC, US Federal Reserve, Statistics Korea Note: we assume on average 15-year payment time for mortgage loans in each country and adjust interest rate level using the average interest rate in history

How will it impact banks? Implication #3 – Households’ leverage-up to benefit retail-orientated banks (continued)

Households leveraging-up is a long-term positive for retail-orientated banks (i.e. CMB and big-four), as it is likely to create notable revenue opportunities for the retail banking business. Please refer to our report FITT – Waking the consumer banking giants, dated 6 April 2016. We have already witnessed rising retail profit contributions for retail-oriented banks (Figure 27). Looking ahead, the improving return profile of retail banking (Figure 29 & 30) should help offset the asset yield compression for the big-four and CMB.

9 January 2017

Banks

Chinese banks - Debt 101

Page 20 Deutsche Bank AG/Hong Kong

Figure 27: Rising retail banking profit contribution Figure 28: Estimated capital allocation of big-four vs. joint-stock banks

60%

34%

17%

0%

10%

20%

30%

40%

50%

60%

70%

2010 2011 2012 2013 2014 2015 1H16

Retail banking PBT contribution - 1H16

CMB

Big 4

banks

Other

banks

63% 68%

30% 16%

8%17%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Big 4 JSB

Treasury/other Retail Corporate

Source: Deutsche Bank, company data Source: Deutsche Bank, company data

Figure 29: China big 4 banks division ROA for corporate vs. retail banking Figure 30: China big 4 banks division ROE for corporate vs. retail banking

0.96%

1.04%

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

1.60%

1.80%

Retail banking - big-four Corporate banking - big-four

19.3%

10.8%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%Retail banking - big-four Corporate banking - big-four

Source: Deutsche Bank estimate, company data Source: Deutsche Bank estimate, company data

How will it impact banks? Implication #3 – Households’ leverage-up to benefit retail-orientated banks (continued)

We estimate retail banks are likely to generate higher, more sustained profitability than corporate banks. Hence our top picks are CMB and ICBC.

9 January 2017

Banks

Chinese banks - Debt 101

Deutsche Bank AG/Hong Kong Page 21

Figure 31: Retail banks (big-four + CMB) should have higher ROA… Figure 32: … and higher ROE than corporate banks

0.60%

0.70%

0.80%

0.90%

1.00%

1.10%

1.20%

1.30%

1.40%

1.50%

1.60%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E 2017E 2018E

ROA

CMB Big-four Other listed banks

DB estimates

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

22.0%

24.0%

26.0%

28.0%

30.0%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E 2017E 2018E

ROE

CMB Big-four Other listed banks

DB estimates

Source: Deutsche Bank estimate, company data Source: Deutsche Bank estimate, company data

Figure 33: Chinese banks’ exposure to SOEs Figure 34: Chinese banks’ retail banking PBT contribution

31%

27%

25% 25%24% 24%

22% 22% 21% 21% 21% 21% 21% 20% 20% 19%18% 18%

22%

0%

5%

10%

15%

20%

25%

30%

35%

IND

B

SP

DB

CN

CB

BO

NJ

CE

B

BO

CQ

BO

NB

ICB

C

Huis

hang

PA

B

CR

CB

CC

B

BO

C

BoC

om

AB

C

MS

B

BO

BJ

CM

B

Avg

SOE exposure % total assets (on- & off-BS)

Retail banks

60%

38%35% 35% 34%

30%28% 26%

24%

16%14%

10% 10% 9%

-5%

32%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

CM

B

ICB

C

CC

B

AB

C

CR

CB

BO

NB

BO

C

BoC

om

CE

B

CN

CB

BO

BJ

MS

B

BO

CQ

Huis

hang

PA

B

Avg

Retail PBT contribution % (1H16)

Retail banks Source: Deutsche Bank estimate, company data Source: Deutsche Bank estimate, company data

9 January 2017

Banks

Chinese banks - Debt 101

Page 22 Deutsche Bank AG/Hong Kong

How to deal with it? From the perspective of funding sources, we see changing dynamics

In the above analysis we discuss how to deal with China’s debt from the perspective of borrowers. In the following pages we discuss the debt issue from the perspective of funding providers. Banks are obviously the key funding providers in China, financing nearly 80% of credit.

Within the banking system, we have long argued that there exists an uneven distribution of risks, with big banks having been de-risking while other

banks are taking more risks. While unlisted banks account for 40% of total banking assets, they are growing their asset base much faster than listed big-four banks and joint-stock banks.

There are two types of banks that have been expanding assets aggressively, i.e. policy banks and smaller city/rural commercial banks. The asset expansion of each type is going to have profound implications for listed banks.

Figure 35: China banking system structure – by total assets of 2015

Figure 36: Big-five banks grew their assets much more slowly than city-

commercial banks and JSBs

39%

19%

10%

4%

11%

12%

3%

1%

Big-four banks

- ICBC

- CCB

- ABC

- BOC

Policy banks

- China Development Bank

- China Agricultural Development Bank

- Export and Import Bank of China

Joint-stock banks

Postal Bank of China

City commercial banks

Rural FIs

- Rural commercial banks

- Rural credit cooperatives

Non-Bank FIs

Foreign banks

Listed banks

accounted for

~60% of total

Relatively riskier

part of the system

1 0 .3%

1 5 .7%

2 3 .8%

1 6 .1%

2 6 .1%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

Banking assets yoy growth by type

Large commercial bank Joint-stock commercial bank

City commercial bank Rural financial institutions

Policy banks & other FIs

Source: Deutsche Bank, CBRC Source: Deutsche Bank, CBRC

9 January 2017

Banks

Chinese banks - Debt 101

Deutsche Bank AG/Hong Kong Page 23

How to deal with it? From the perspective of funding sources, we see rise of policy banks as government leverages up

China’s big three policy banks now in aggregate have over US$3trn of assets (c.10% of banking system). Their growth rate has been impressive at a 20% CAGR for the past five years. They have been major funding providers for China’s booming infrastructure build.

Funding side, policy banks rely on bond issuance and PBOC funding. Bond issuance still makes up 60% of policy banks’ funding in China. Elsewhere, the PBOC has been supporting policy banks’ asset expansion by injecting capital (US$100bn in 2015) and direct lending via the PSL scheme (US$290bn).

The implications of a rise in policy banks include:

1) It takes some of the strain of supporting China’s economic growth off the shoulders of listed banks;

2) It is also a way that government leverages itself up, which may lead to fewer credit risks but lower bank returns.

3) This can help lower financial risk in the short term, but comes at the expense of rising national debt in the medium to long term and can prolong misallocation of capital.

For details please refer to our report Policy banks: Driving growth and restructuring, dated 12 October 2016.

Figure 37: Asset growth of China’s three policy

banks has been rapid

Figure 38: Funding mix of policy banks vs. Big-4

and JSBs

Figure 39: Aggregate Equity Capital raisings of

China commercial banks vs. policy banks

(US$bn)

1,176

1,494

1,825

2,069

2,551

3,024

0

500

1,000

1,500

2,000

2,500

3,000

3,500

US$ bnTotal assets of policy banks in China

EXIM ADBC CDB

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Policy Banks Big 4 JSBs

Equity Other Debt securities Deposits Due to Banks/ Financials

0

20

40

60

80

100

120

Big A & H-share listed commercial banks Policy Banks

Source: Deutsche Bank, company data Source: Deutsche Bank, company data Source: Deutsche Bank, PBOC, company data

9 January 2017

Banks

Chinese banks - Debt 101

Page 24 Deutsche Bank AG/Hong Kong

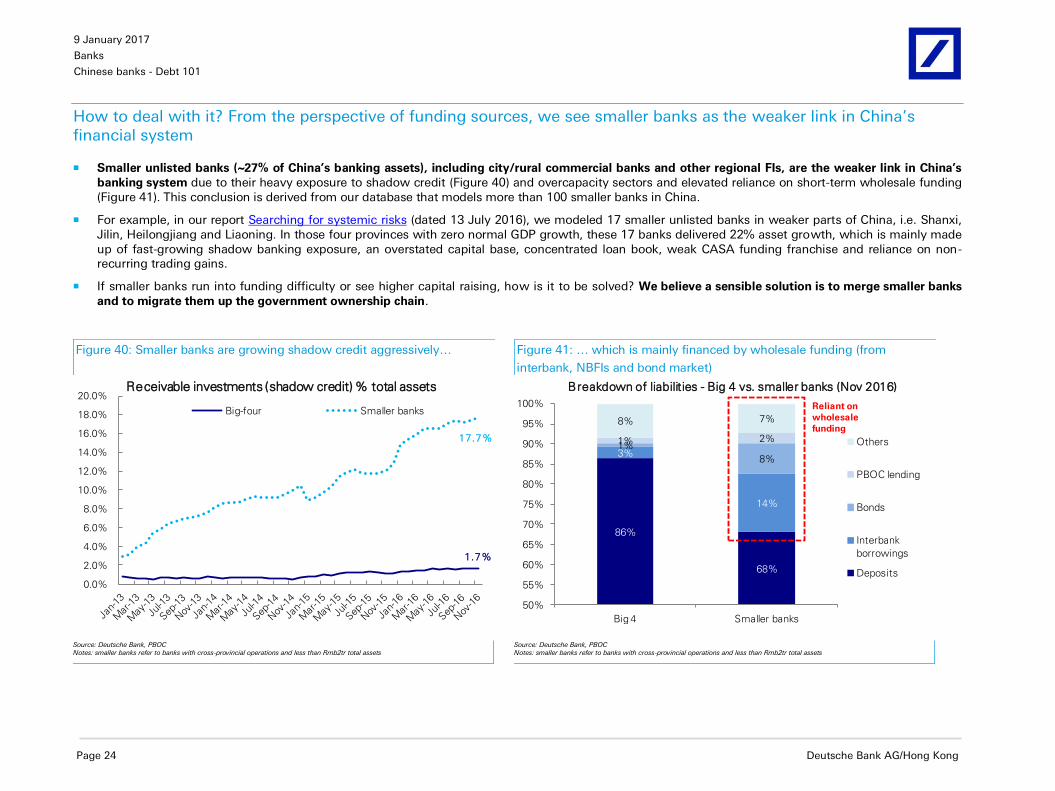

How to deal with it? From the perspective of funding sources, we see smaller banks as the weaker link in China’s financial system

Smaller unlisted banks (~27% of China’s banking assets), including city/rural commercial banks and other regional FIs, are the weaker link in China’s

banking system due to their heavy exposure to shadow credit (Figure 40) and overcapacity sectors and elevated reliance on short-term wholesale funding (Figure 41). This conclusion is derived from our database that models more than 100 smaller banks in China.

For example, in our report Searching for systemic risks (dated 13 July 2016), we modeled 17 smaller unlisted banks in weaker parts of China, i.e. Shanxi, Jilin, Heilongjiang and Liaoning. In those four provinces with zero normal GDP growth, these 17 banks delivered 22% asset growth, which is mainly made up of fast-growing shadow banking exposure, an overstated capital base, concentrated loan book, weak CASA funding franchise and reliance on non-recurring trading gains.

If smaller banks run into funding difficulty or see higher capital raising, how is it to be solved? We believe a sensible solution is to merge smaller banks

and to migrate them up the government ownership chain.

Figure 40: Smaller banks are growing shadow credit aggressively…

Figure 41: … which is mainly financed by wholesale funding (from

interbank, NBFIs and bond market)

1.7%

17.7%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%Receivable investments (shadow credit) % total assets

Big-four Smaller banks

86%

68%

3%

14%

1%

8%

1% 2%

8% 7%

50%

55%

60%

65%

70%

75%

80%

85%

90%

95%

100%

Big 4 Smaller banks

Breakdown of liabilities - Big 4 vs. smaller banks (Nov 2016)

Others

PBOC lending

Bonds

Interbank

borrowings

Deposits

Reliant on

wholesale

funding

Source: Deutsche Bank, PBOC Notes: smaller banks refer to banks with cross-provincial operations and less than Rmb2tr total assets Source: Deutsche Bank, PBOC

Notes: smaller banks refer to banks with cross-provincial operations and less than Rmb2tr total assets

9 January 2017

Banks

Chinese banks - Debt 101

Deutsche Bank AG/Hong Kong Page 25

How to deal with it? Migrating up the government ownership chain to cope with troubled smaller banks

The sensible solution to cope with troubled smaller banks is consolidation and migration up the government ownership chain. This has been the typical solution for troubled smaller banks in the past 20 years, i.e. merge them together, with a higher level of government injecting capital and carving out NPLs.

The implication on big banks would be positive, as it would rebut the market perception that big banks may be required to acquire the smaller ones. However, over the past 20 years, we see no case for big banks buying smaller ones. We expect government to keep the core assets clean in the system.

Figure 42: Ownership structure of China banking sector – we may see more consolidation in small banks and risk migration up to higher level government

Ownership Bank category

Policy banks (CDB, ADBC, EXIMB) and

Postal Bank

Big 4: ICBC, CCB, ABC, BOC

JSBs (BoCom, CEB, CMB, CNCB)

Central Huijin MOF

Central SOEs AMCs

Huarong Xiangjiang Bank etc.

JSBs (SPDB, INDB, Zheshang Bank,

Bohai Bank, etc.)

City Commercial banks: BOBJ, BOSH,

Huishang Bank, Jiangxi Bank,

Zhongyuan Bank, etc.

Provincial

Finance Bureau

Provincial

SOEs

Large POEsForeign strategic

investors

Rural commercial banks: CRCB, Tianjin

Rural Commercial Bank, etc.

~16

banks

20-25

banks

Municipal

Finance Bureau

Municipal

SOEs

POEs and

individuals

Foreign strategic

investors

City Commercial banks: BONJ, BONB,

Shengjing Bank etc.

Rural commercial banks

POEs and

individuals

Foreign strategic

investors

Private-owned banks: MSB, PAB,

WeBank, etc.

Rural commercial banks and credit

unions

>110

banks

>2,200

banks

5 private

banks

approved

in 2014

Migrating

risks up to

higher level

govt

Central

Provincial

Municipal

Private

~62% of

banking

assets

~11% of

banking

assets

~27% of

banking

assets

Source: Deutsche Bank, CBRC, PBOC

9 January 2017

Banks

Chinese banks - Debt 101

Page 26 Deutsche Bank AG/Hong Kong

How to deal with it? Migrating up the government ownership chain to cope with troubled smaller banks (continued)

In fact, a new round of consolidation may have already begun. We identified a list of seven provincial-level banks set up since 2010 by merging municipal-level banks, or simply upgrading the ownership from municipal to provincial governments (Hebei Bank).

Figure 43: Summary of set up of provincial-level commercial banks during 2010-2015

Bank Merge date Type Merger targetsOwnership nature

before merger

Ownership nature

after mergerMajor shareholders after merger

Jiangxi Bank 15/12/2015City Commercial

Bank

Nanchang Bank absorbs Jingdezhen Commercial

Bank and renamed as Jiangxi Bank.Municipal Provincial

Jiangxi Provincial Expressway Investment

Group (20.04%, SOE);

Jiangxi Financial Holding Group (5.98%,

SOE);

Nanchang MOF (5.42%, Gov);

Zhongyuan Bank 26/12/2014City Commercial

Bank

13 city commercial banks based in Henan

Province: Kaifeng Bank, Anyang Bank, Hebi Bank,

Xinxiang Bank, Puyang Bank, Xuchang Bank,

Luohe Bank, Sanmenxia Bank, Nanyang Bank,

Shangqiu Bank, Xinyang Bank, Zhoukou Bank and

Zhumadian Bank - merged into a new entity -

Zhongyuan Bank.

Municipal Provincial

Henan Investment Group (9.02%, SOE);

Yongcheng Median Holding Group (7.4%,

SOE);

Henan Shengrui Holding Group (4.5%,

POE);

Guizhou Bank 11/10/2012City Commercial

Bank

Merged and restructured from Zunyi Commercial

Bank, Liupanshui Commercial Bank, and Anshun

Commercial Bank, backed by Guizhou provincial

government.

Municipal Provincial

Guizhou MOF (9.6%, Gov);

63.95% of bank's shares are held by the

Gov&SOEs.

Hebei Bank 25/07/2012City Commercial

Bank

Hebei Bank was upgraded to a provincial

governed bank from a municipal governed bank

in 2012.

Municipal Provincial

GD Power Development Co (19.02%,

SOE);

Hebei Port Group (9.55%, SOE);

China City Construction Holding Group

(9.29%, SOE)

Gansu Bank 11/11/2011City Commercial

Bank

Merged and restructured from Pingliang

Commercial Bank and Baiyin Commercial Bank,

with newly introduced shareholders including

provisional SOEs, strategic investors and POEs.

Municipal Provincial

Gansu Provincial Highway Aviation Tourism

Investment Group (15.78%, SOE);

Baoshang Bank (11.48%, POE);

Gansu Electricity Power Investment (8.6%,

SOE);

Hubei Bank 27/02/2011City Commercial

Bank

Merged and restructured from Huangshi Bank,

Yichang Commercial Bank, Fanxiang Commercial

Bank, Jinzhou Commercial Bank, and Xiaogan

Commercial Bank.

Municipal Provincial

Hubei Energy (9.28%, SOE);

China Three Gorges Corp (9.28%, SOE);

Wuhan Iron&Steel Group (9.28%, SOE);

Yichang MOF (6.23%, Gov)

Huarong Xiangjiang Bank 12/10/2010City Commercial

Bank

Merged from Hunan Xiangtan, Zhuzhou,

Yueyang, Hengyang Commercial Bank and

Shaoyang City Credit Union. Besides, Huarong

Asset Management injected capital into and take

full control of the newly established entity.

Municipal Central govtChina Huarong Asset Management

(50.98%, SOE)

Source: Deutsche Bank, company data, media news

9 January 2017

Banks

Chinese banks - Debt 101

Deutsche Bank AG/Hong Kong Page 27

How to deal with it? From the perspective of financing channels, there is no more hiding from shadow

Among the financing channels, shadow banking in China has experienced remarkable growth in recent years. We estimate total shadow banking credit recorded a 27% CAGR during 2011-3Q16 to Rmb42tr, or 22% of the system credit balance.

Since May 2016, we note all financial regulators, including PBOC, CBRC, CSRC and CIRC, have intensified the tightening of shadow banking. The directions are to deleverage shadow credit by requiring banks to set aside sufficient capital and provisions and lowering SPVs’ leverage at NBFIs.

For details, please refer to three of our reports: 1) No more hiding from shadow, dated 19 May 2016; 2) Tightening regulatory noose on shadow credit, dated 6 June 2016; and 3) New WMP draft rules: continued tightening on shadow credit, dated 28 July 2016.

Figure 44: Intensified, more coordinated regulatory actions on shadow credit since May 2016

Receivable

investments

Corporate lending

• LGFVs (the majority)

• PPP projects

• Property developers

• Overcapacity sectors

• NPLs (relatively rare)

Discounted bills

Interbank deposits

$$

Funding sourcesSPVs packaged by

NBFIsUnderlying assets

Trust plans

Brokers’ asset mgmt

schemes

Mutual funds’ asset

mgmt schemes

Private funds

Insurance debt

schemes

Corporate bonds

A-share market

Banks’ shadow credit

Other assets

$

Reverse repos

Wealth

management products

On-B/S of

banks

Off-B/S of

banks

MOF/AMC bonds

$

$

Treasury bonds

PBOC and CBRC

[5/May]

CBRC

[18/Mar]

CBRC

Circular 82

[28/Apr]

CBRC

Window

guidance

[1/Jun]

CSRC &

AMAC

[18/May]

CIRC

[end-May]

CSRC

[16/Jul]

New draft rules on

WM businesses

[27/Jul]

Further regulation

on entrusted

management

[25/Jul]

Risk inspection

in 2H16

[26/Jul]

PBOC to include

WMP into MPA

[26/Nov]

Source: Deutsche Bank, PBOC, CBRC, CSRC, CIRC, media reports. Note: the underlying structure is how China’s shadow banking works. The red circles represent the recent new regulation or window guidance.

9 January 2017

Banks

Chinese banks - Debt 101

Page 28 Deutsche Bank AG/Hong Kong

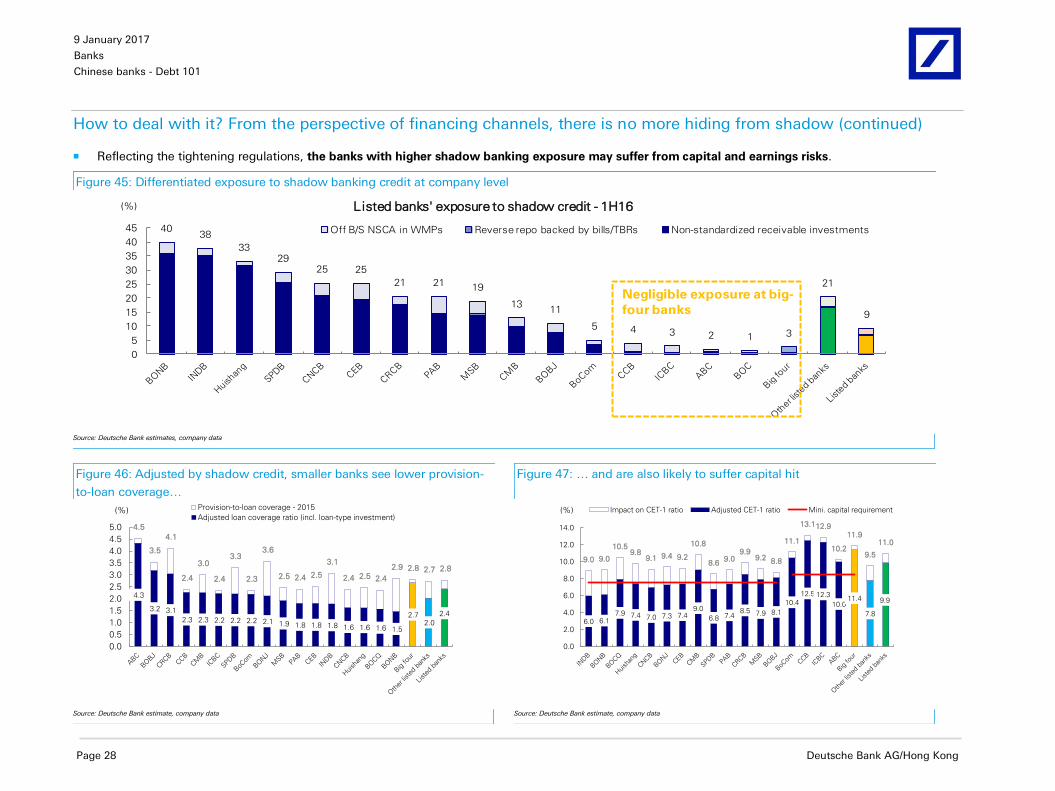

How to deal with it? From the perspective of financing channels, there is no more hiding from shadow (continued)

Reflecting the tightening regulations, the banks with higher shadow banking exposure may suffer from capital and earnings risks.

Figure 45: Differentiated exposure to shadow banking credit at company level

4038

3329

25 25

21 2119

1311

5 4 3 2 1 3

21

9

0

5

10

15

20

25

30

35

40

45

(%) Listed banks' exposure to shadow credit - 1H16

Off B/S NSCA in WMPs Reverse repo backed by bills/TBRs Non-standardized receivable investments

Negligible exposure at big-

four banks

Source: Deutsche Bank estimates, company data

Figure 46: Adjusted by shadow credit, smaller banks see lower provision-

to-loan coverage…

Figure 47: … and are also likely to suffer capital hit

4.3

3.2 3.1

2.3 2.3 2.2 2.2 2.2 2.1 1.9 1.8 1.8 1.8 1.6 1.6 1.6 1.5

2.7 2.0

2.4

4.5

3.5

4.1

2.4

3.0

2.4

3.3

2.3

3.6

2.5 2.4 2.5

3.1

2.4 2.5 2.4

2.9 2.8 2.7 2.8

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

(%) Provision-to-loan coverage - 2015

Adjusted loan coverage ratio (incl. loan-type investment)

6.0 6.17.9 7.4 7.0 7.3 7.4

9.0

6.8 7.48.5 7.9 8.1

10.4

12.5 12.3

10.011.4

7.8

9.9

9.0 9.0

10.59.8

9.1 9.4 9.2

10.8

8.69.0

9.99.2 8.8

11.1

13.112.9

10.2

11.9

9.5

11.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

(%) Impact on CET-1 ratio Adjusted CET-1 ratio Mini. capital requirement

Source: Deutsche Bank estimate, company data Source: Deutsche Bank estimate, company data

9 January 2017

Banks

Chinese banks - Debt 101

Deutsche Bank AG/Hong Kong Page 29

Appendix – Total credit breakdown by financing channels and total social funding cost

Figure 48: Total social funding cost has been declining since implementation of monetary easing in 4Q14, with further room to decline

Total system credit (Rmb bn) and funding cost (%) 2011 2012 2013 2014 2015 1H16 3Q16 2011 2012 2013 2014 2015 1H16

Outstanding balance Funding cost (%)

Large + medium corporate (excl. LGFVs) 21,990 25,813 28,530 32,918 39,266 42,322 43,118 6.76 6.70 6.44 6.50 5.60 5.10

MSEs + personal business loan 14,661 17,262 20,088 23,075 25,743 27,577 28,028 9.39 9.30 8.94 9.03 7.78 7.09

Personal consumption loan 1,742 2,344 3,181 3,856 4,489 5,160 5,604 10.15 10.05 9.66 9.75 8.40 7.65

Mortgage 7,137 8,100 9,800 11,520 14,180 16,550 17,806 7.00 6.63 6.37 6.71 5.32 4.63

LGFVs 9,118 9,300 10,119 10,119 9,107 8,652 8,219 7.52 7.44 7.16 7.22 6.22 5.67

Others (incl. FCY loans, overseas loans, etc.) 3,117 3,860 3,013 2,972 2,822 3,376 3,618 7.52 7.44 7.16 7.22 6.22 5.67

Total bank loans (RMB&FCY) 57,763 66,679 74,731 84,460 95,607 103,636 106,392 7.72 7.63 7.37 7.48 6.35 5.75

Bonds Outstanding balance Funding cost (%)

Treasury bonds 6,993 7,783 9,296 10,248 11,382 11,878 12,447 3.02 2.89 3.91 4.00 2.96 2.66

Local govt bonds 600 650 862 1,162 4,826 8,289 9,717 3.75 3.19 3.80 3.73 3.39 2.99

Corporate bonds 5,226 7,481 9,293 11,690 14,630 16,470 17,310 5.78 5.51 5.63 5.86 4.48 3.98

ABS 19 39 48 298 706 746 837 4.92 4.92 5.62 5.94 5.06 4.58

Private placement bonds 9 39 109 623 900 990 8.92 9.14 8.88 7.14 5.35

Non-bank fins bonds 54 37 36 45 123 153 176 5.60 4.65 5.42 5.90 4.29 3.58

Foreign bonds 4 4 3 3 1 1 4 5.73 5.49 5.57 6.43 4.74 4.19

Total bonds 12,897 16,004 19,577 23,555 32,292 38,438 41,481 4.19 4.14 4.74 4.96 3.85 3.40

Shadow banking Outstanding balance Funding cost (%)

Entrusted Loans 3,391 4,675 7,221 9,330 10,930 12,060 12,520 13.53 13.40 14.31 14.44 11.20 10.21

Trust Loans 1,708 2,993 4,833 5,350 5,390 5,730 5,930 12.03 12.22 11.80 12.13 11.84 10.31

Undiscounted bank acceptance 5,059 6,108 6,884 6,760 5,850 4,580 3,800 7.96 5.83 4.30 5.67 4.26 3.62

Banks' wealth mangement products 4,590 7,100 10,240 15,000 23,000 27,000 28,000 7.83 7.84 7.64 7.97 7.63 6.71

Brokers' asset management schemes 282 1,890 5,200 7,946 11,890 15,003 15,753 12.53 12.72 12.30 12.63 12.34 10.81

Fund subsidiaries' asset management schemes 971 3,739 8,571 11,060 11,613 12.53 12.72 12.30 12.63 12.34 10.81

Insurers' debt schemes 294 582 1,100 1,161 1,439 1,550 9.36 9.59 9.42 8.40 7.65

Financial leasing 930 1,550 2,100 3,200 4,440 4,746 4,888 10.15 10.05 9.66 9.75 8.40 7.65

Group finance companies 1,112 1,300 1,570 1,698 1,715 6.50 5.60 5.10

Small loan company 392 592 819 942 941 936 920 19.99 19.99 19.30 17.88 17.25 16.76

Pawn loans 55 71 87 86 103 115 115 21.59 21.59 20.30 19.99 19.22 18.35

Private lending 3,380 3,380 4,090 3,681 2,660 2,400 2,400 21.59 21.59 20.30 19.99 19.22 18.35

P2P loan 1 6 27 104 439 621 713 18.90 19.13 21.25 16.26 13.81 11.38

Total shadow banking 13,644 18,424 27,869 34,145 38,333 41,511 42,328 13.11 11.92 10.87 11.31 10.00 9.07

Offshore credit Outstanding balance Funding cost (%)

External government debt 313 341 355 342 723 750 750 4.00 4.00 4.00 4.00 4.00 4.00

Corporate foreign debt 2,477 2,697 2,811 2,712 4,217 4,093 4,093 5.00 5.00 5.00 5.00 5.00 5.00

Foreign debt 2,790 3,038 3,166 3,055 4,940 4,843 4,843 4.89 4.89 4.89 4.89 4.85 4.85

Total system credit 87,094 104,144 125,344 145,215 171,171 188,428 195,044 Total system funding cost (%)

% of GDP 184% 200% 213% 228% 253% 270% 275% 7.95 7.77 7.67 7.91 6.65 5.98 Source: Deutsche Bank estimates, PBOC, CBRC, CSRC, WIND, CEIC, Chinabond.com.cn, Trustee Association of China, HKMA, NBS Note: We have adjusted for overlapping among shadow banking components

9 January 2017

Banks

Chinese banks - Debt 101

Page 30 Deutsche Bank AG/Hong Kong

Valuation and risks

We value Chinese banks using a three-stage Gordon Growth Model (PV= (ROE-g)/(COE-g)), with target prices based on 2017E book values. Our valuations of

the Chinese banks under our coverage assume a near-term (2016-18E) ROE of 11.0-16.0%, a medium-term (2019-21E) ROE of 10.0-13.0% and a terminal ROE

of 7.5-11.5%, with a COE of 11-13.5%. In the below chart, we highlight our valuation comparison of the listed banks. On our estimates, H-share/A-share listed

Chinese banks are trading at 2017E P/Bs of 0.70x/0.78x and 2017E P/Es of 5.45x/6.06x.

Figure 49: Chinese banks’ valuation summary

Ticker Rating TP Price Upside Mkt. Cap

LC LC (%) (US$mn) 15A 16E 17E 15A 16E 17E 15A 16E 17E 15A 16E 17E 15A 16E 17E 15A 16E 17E

ICBC-H 1398.HK Buy 5.73 4.71 21.6% 226,565 5.12 5.43 5.32 0.82 0.78 0.71 3.1 3.3 3.1 17.1% 15.2% 14.0% 1.30% 1.22% 1.16% 5.9% 5.6% 5.7%

CCB-H 0939.HK Buy 6.67 5.85 14.1% 189,027 5.37 5.68 5.59 0.87 0.82 0.75 3.1 3.2 3.0 17.2% 15.3% 14.0% 1.30% 1.20% 1.15% 5.6% 5.3% 5.4%

ABC-H 1288.HK Hold 3.56 3.26 9.3% 146,587 4.98 5.26 5.18 0.78 0.75 0.68 2.8 3.1 2.9 16.8% 15.0% 13.8% 1.07% 0.99% 0.93% 6.1% 5.8% 5.9%

BOC-H 3988.HK Buy 4.20 3.50 19.9% 143,649 5.20 5.53 5.53 0.72 0.69 0.64 3.0 2.9 3.1 14.6% 13.1% 12.0% 1.07% 0.97% 0.89% 6.0% 5.6% 5.6%

BCOM-H 3328.HK Hold 6.13 5.73 7.0% 58,933 5.36 5.68 5.60 0.69 0.67 0.62 3.2 3.3 3.2 13.4% 12.2% 11.4% 1.00% 0.90% 0.84% 5.6% 5.3% 5.4%

CMB-H 3968.HK Buy 23.37 18.74 24.7% 65,319 6.82 6.72 6.02 1.10 1.03 0.92 2.9 2.8 2.6 17.1% 16.3% 16.2% 1.06% 1.05% 1.10% 4.4% 4.5% 5.0%

CITIC Bank-H 0998.HK Hold 4.26 5.12 -16.8% 43,405 5.10 5.31 5.28 0.66 0.64 0.58 2.2 2.1 1.9 14.3% 12.6% 11.5% 0.89% 0.76% 0.68% 4.9% 4.7% 4.7%

Minsheng-H 1988.HK Hold 7.91 8.51 -7.0% 46,577 5.64 5.94 5.77 0.86 0.81 0.73 2.7 2.7 2.5 17.0% 14.5% 13.3% 1.10% 0.99% 0.93% 3.3% 3.1% 3.2%

CEB-H 6818.HK Hold 3.10 3.62 -14.4% 25,985 4.79 5.04 5.00 0.70 0.67 0.61 2.3 2.4 2.3 15.4% 13.9% 12.8% 1.00% 0.91% 0.82% 6.3% 6.3% 6.4%

CRCB 3618.HK Hold 5.26 4.62 13.8% 5,541 4.98 5.00 4.64 0.77 0.73 0.65 2.8 2.7 2.4 16.4% 15.4% 14.8% 1.08% 1.00% 0.98% 5.2% 5.2% 5.6%

Huishang 3698.HK Sell 2.89 3.97 -27.1% 5,657 5.96 5.94 5.29 0.89 0.85 0.76 3.2 2.7 2.4 15.9% 15.1% 15.1% 1.10% 0.94% 0.92% 4.8% 4.8% 5.4%

BOCQ 1963.HK Sell 5.28 6.75 -21.8% 2,722 5.58 5.33 4.59 0.83 0.78 0.69 3.3 2.7 2.3 17.0% 15.5% 16.0% 1.07% 1.00% 1.01% 4.7% 4.9% 5.7%

H-share sector mean 5.31 5.58 5.45 0.81 0.77 0.70 3.0 3.0 2.9 16.3% 14.6% 13.5% 1.16% 1.07% 1.01% 5.6% 5.3% 5.4%

ICBC-A 601398.SS Buy 5.47 4.44 23.1% 226,565 5.76 5.76 5.65 0.93 0.83 0.75 3.5 3.5 3.3 17.1% 15.2% 14.0% 1.30% 1.22% 1.16% 5.3% 5.3% 5.4%

CCB-A 601939.SS Buy 6.37 5.49 16.1% 189,027 6.02 6.01 5.91 0.97 0.87 0.79 3.5 3.4 3.2 17.2% 15.3% 14.0% 1.30% 1.20% 1.15% 5.0% 5.0% 5.1%

ABC-A 601288.SS Hold 3.40 3.13 8.7% 146,587 5.71 5.68 5.61 0.90 0.81 0.74 3.2 3.3 3.2 16.8% 15.0% 13.8% 1.07% 0.99% 0.93% 5.3% 5.3% 5.4%

BOC-A 601988.SS Hold 4.01 3.46 15.8% 143,649 6.14 6.16 6.15 0.85 0.77 0.71 3.5 3.2 3.5 14.6% 13.1% 12.0% 1.07% 0.97% 0.89% 5.1% 5.0% 5.0%

BCOM-A 601328.SS Hold 5.85 5.80 0.9% 58,933 6.47 6.48 6.38 0.83 0.76 0.70 3.8 3.8 3.6 13.4% 12.2% 11.4% 1.00% 0.90% 0.84% 4.7% 4.6% 4.7%

CMB-A 600036.SS Buy 22.32 18.10 23.3% 65,319 7.87 7.31 6.55 1.27 1.12 1.00 3.4 3.0 2.8 17.1% 16.3% 16.2% 1.06% 1.05% 1.10% 3.8% 4.1% 4.6%

CITIC Bank-A 601998.SS Sell 4.07 6.79 -40.1% 43,405 8.07 7.93 7.88 1.05 0.95 0.87 3.5 3.1 2.9 14.3% 12.6% 11.5% 0.89% 0.76% 0.68% 3.1% 3.2% 3.2%

Minsheng-A 600016.SS Sell 7.56 9.08 -16.8% 46,577 7.18 7.13 6.93 1.10 0.98 0.88 3.5 3.2 3.0 17.0% 14.5% 13.3% 1.10% 0.99% 0.93% 2.6% 2.6% 2.7%

SPDB 600000.SS Sell 12.26 16.30 -24.8% 51,174 6.73 6.83 6.68 1.17 1.02 0.91 3.2 3.1 2.9 18.7% 16.4% 14.4% 1.08% 0.96% 0.88% 3.2% 2.8% 2.9%

Industrial Bank 601166.SS Sell 13.78 16.33 -15.6% 45,183 6.20 6.00 5.98 1.08 0.96 0.85 2.9 2.7 2.6 18.8% 16.9% 15.1% 0.96% 0.91% 0.83% 3.7% 3.9% 3.9%

CEB - A 601818.SS Sell 2.96 3.94 -24.9% 22,779 6.23 6.18 6.13 0.90 0.82 0.75 3.0 2.9 2.8 15.4% 13.9% 12.8% 1.00% 0.91% 0.82% 4.8% 4.9% 4.9%

Ping An Bank 000001.SZ Hold 9.44 9.17 2.9% 22,866 7.20 6.74 6.22 0.97 0.86 0.77 2.7 2.2 2.0 15.0% 13.6% 13.0% 0.93% 0.86% 0.87% 1.7% 1.5% 1.6%

Bank of Beijing 601169.SS Buy 12.80 9.88 29.6% 21,819 7.44 7.20 6.64 1.12 0.99 0.88 4.1 3.8 3.5 16.2% 14.6% 14.1% 1.00% 0.90% 0.89% 2.3% 2.3% 2.5%

Bank of Nanjing 601009.SS Sell 7.02 11.40 -38.4% 10,031 9.87 9.54 9.11 1.46 1.30 1.17 4.4 3.6 3.1 17.6% 14.5% 13.5% 1.02% 0.78% 0.64% 3.5% 2.0% 2.1%

Bank of Ningbo 002142.SZ Sell 10.95 17.32 -36.8% 9,809 10.32 9.40 8.95 1.68 1.48 1.32 5.7 4.5 4.1 17.6% 16.8% 15.6% 1.03% 0.92% 0.80% 2.6% 2.9% 3.0%

A-share sector mean 6.28 6.20 6.06 0.97 0.87 0.78 3.4 3.3 3.1 16.2% 14.5% 13.4% 1.12% 1.03% 0.98% 4.5% 4.5% 4.6%

P/E (x) P/B (x) P/PPOP ROAE ROAA Div. Yield (%)

Source: Deutsche Bank estimates, Bloomberg Finance LP; Note: market cap is sum of A and H shares; data as of January 5 2017

Downside risks: property price correction, as 25% of banking assets are closely tied to the property market; failure of PBOC to contain interbank rates amid

tight liquidity; and maintaining of 150% provision coverage ratio by the CBRC.

Upside risks: removal or softening of GDP targeting, signaling reform may start; real progress of supply-side reform to cut excess capacity; softer-than-

expected regulation on shadow credit; and better-than-expected improvement in corporate financial health.

9 January 2017

Banks

Chinese banks - Debt 101

Deutsche Bank AG/Hong Kong Page 31

Appendix 1

Important Disclosures

*Other information available upon request

Prices are current as of the end of the previous trading session unless otherwise indicated and are sourced from local exchanges via Reuters, Bloomberg and other vendors . Other information is sourced from Deutsche Bank, subject companies, and other sources. For disclosures pertaining to recommendations or estimates made on securities other than the primary subject of this research, please see the most recently published company report or visit our global disclosure look-up page on our website at http://gm.db.com/ger/disclosure/DisclosureDirectory.eqsr. Aside from within this report, important conflict disclosures can also be found at https://gm.db.com/equities under the "Disclosures Lookup" and "Legal" tabs. Investors are strongly encouraged to review this information before investing.

Analyst Certification

The views expressed in this report accurately reflect the personal views of the undersigned lead analyst about the subject issuers and the securities of those issuers. In addition, the undersigned lead analyst has not and will not receive any compensation for providing a specific recommendation or view in this report. Hans Fan

Equity rating key Equity rating dispersion and banking relationships

Buy: Based on a current 12- month view of total share-holder return (TSR = percentage change in share price from current price to projected target price plus pro-jected dividend yield ) , we recommend that investors buy the stock.

Sell: Based on a current 12-month view of total share-holder return, we recommend that investors sell the stock

Hold: We take a neutral view on the stock 12-months out and, based on this time horizon, do not recommend either a Buy or Sell.

Newly issued research recommendations and target prices supersede previously published research.

53 %

37 %

10 %17 % 19 % 20 %

050

100150200250300350400450500

Buy Hold Sell

Asia-Pacific Universe

Companies Covered Cos. w/ Banking Relationship

9 January 2017

Banks

Chinese banks - Debt 101

Page 32 Deutsche Bank AG/Hong Kong

Additional Information

The information and opinions in this report were prepared by Deutsche Bank AG or one of its affiliates (collectively

"Deutsche Bank"). Though the information herein is believed to be reliable and has been obtained from public sources

believed to be reliable, Deutsche Bank makes no representation as to its accuracy or completeness.

If you use the services of Deutsche Bank in connection with a purchase or sale of a security that is discussed in this

report, or is included or discussed in another communication (oral or written) from a Deutsche Bank analyst, Deutsche