Education for opportunity - World Bank Documents & Reports

10

Accounting and Auditing Education Comm-ý-unity of Practice EduCoP Cuw rru-m fo Uni=r- sitrr, sp4 uc 5-12 eru CFRR, 0: Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

Documents

-

view

3 -

download

0

Transcript of Education for opportunity - World Bank Documents & Reports

Accountingand AuditingEducation

Comm-ý-unityof Practice

EduCoP

Cuw rru-m fo Uni=r- sitrr, sp4uc 5-12 eru

CFRR, 0:

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

ST A R EP Accounting and Auditing Education Community of Practice Workshop

Education for opportunity: Developing the AccountingCurriculum for Universities

25 - 26 Febiuary 2015Kiev, Ukraine

The questionnaire sent to the STAREP EduCoP participants, prior to the workshop held in Tbilisi in

October 2014, asked what learning outcomes should be included in a bachelor's degree under the

following six subject areas:

1. Management and Management Accounting2. Financial Accounting and Reporting3. Audit and Assurance4. Financial Management5. Law6. Tax

Since that time a significant amount of work has been carried out on subject areas 1 to 4 and the

purpose of this workshop is to facilitate the Tax and Law Working Groups developing similar syllabus

structures for the remaining two subject areas.

The main objective of this workshop is to focus on developing syllabi for law and tax that is

appropriate for undergraduate students studying accounting in STAREP countries. It should be noted

that under the ACCA qualification structure, there is only one law paper and the second tax paper

(P6 - Advanced Taxation) is an elective paper. Thus under the ACCA structure it is possible to gain a

professional qualification having studied law and taxation only at undergraduate level. Such a

structure may not be appropriate within the STAREP Region and this is a key issue that should be

addressed over the coming two days.

Specific objectives for the two areas are:

1) Law

Table 1 shows the extent to which there was consensus among the respondents: The learning

outcomes highlighted in light green show those outcomes that all POAs that responded believed

should be part of the undergraduate syllabus.

There is a basic template' for the ACCA F4 Corporate and Business Law Paper which contains some

eight key learning outcomes as illustrated in Diagram 1 below.

' This is based on a comparison the English, Scottish, Irish, Russian and Global variants of Paper F4.

1 Page

-STAREP Accounting and Auditing Education Community of Practice Workshop

Table 1 - Law Learning Outcomes in Initial Questionnaire

5 LawLearning Outcome

N1 Identify the essential elements of different legal systems including the main sources of law,the relationship between the different branches of a state's constitution, and the need forinternational legal regulation, and explain the roles of international organisations in thepromotion and regulation of international trade, and the role of international arbitration asan alternative to court adjudication

N2 Recognise and apply the appropriate legal rules relating to the law of obligationsN3 Explain and apply the law relating to employment relationships02 Recognise and compare types of capital and the financing of companies

Diagram 1 - Relational Diagram of Main Capabilities for Law

AThe Essential Elements of the Legal System

DThe Law of Obligations CFormation and Constitution(Contractual and Non- Employment Law

Cont etul) f Business Organizations- ---Contractual)-0

FE

Company GCapital and Management InsolvencyFinancing of and LawCompanies Administration

HCorporate Fraudulent and Criminal Behaviour

Therefore in addition to the four learning outcomes covered in the initial questionnaire, the Law

Working Group will need to consider whether the following additional learning outcomes should be

included:

* Distinguish between alternative forms and constitutions of business organizations* Describe and explain how companies are managed and administered* Recognize the legal implications relating to insolvency* Demonstrate an understanding of corporate fraudulent and criminal behaviour.

Once the learning outcomes have been agreed, these can be referenced to specific legislation in

each country and the process of developing programs and teaching materials can begin.

2i Page

ST A R FP Accounting and Auditing Education Community of Practice Workshop

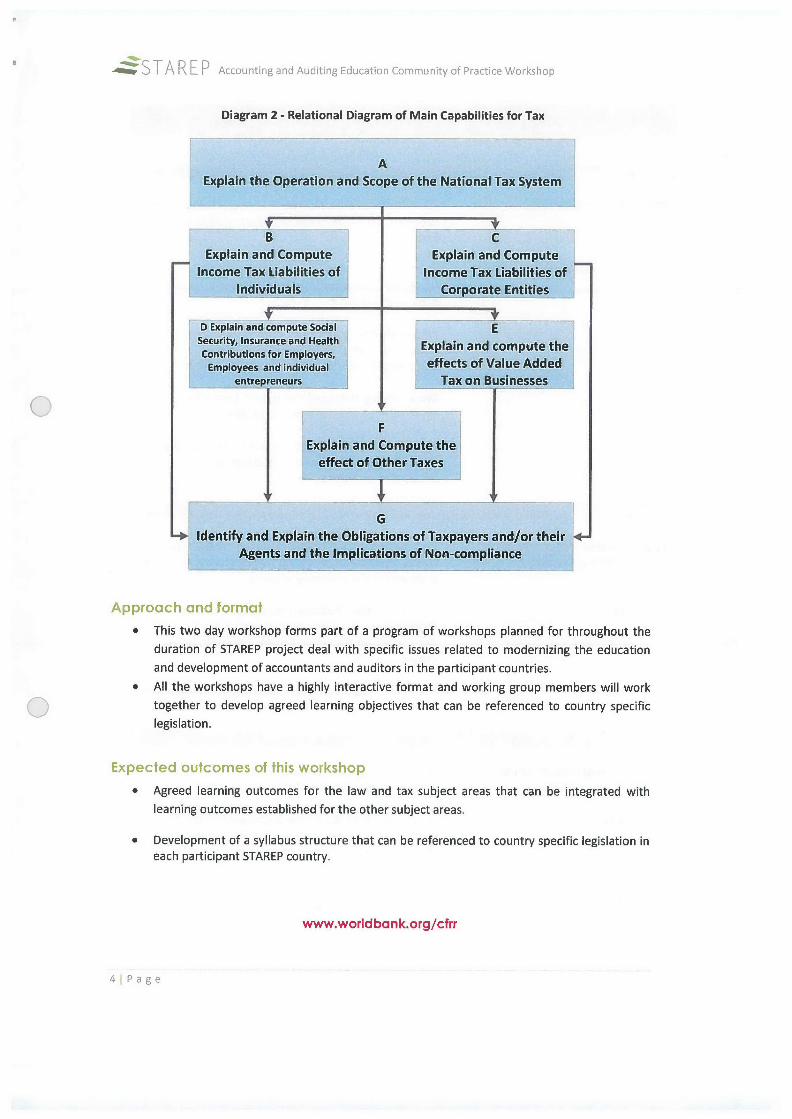

2) Tax

The eight learning outcomes identified for the tax subject area are set out in Table 2 below. Tax was

the only area where no single learning objective received 100% support for inclusion in the

undergraduate syllabus.

Table 2 shows the extent to which there was consensus among the respondents: The learning

outcomes highlighted in light green show those outcomes that all POAs that responded believed

should be part of the undergraduate syllabus whereas those which are not highlighted shows there

was no consensus. There was no consensus among the universities.

Table 2 - Proposed Learning Outcomes for Tax

6 TaxLearning Outcome

P1 Explain the operation and scope of the tax systemP2 Explain and compute the income tax liabilities of individuals

Explain and compute the corporation tax liabilities of individual companies and groups ofP3 companiesP4 Explain and compute the chargeable gains arising on companies and individualsP5 Explain and compute the inheritance tax liabilities of individuals

P6 Explain and compute the effect of national insurance contributions on employees,employers and the self employed

Explain and compute the effects of value added tax on incorporated and unincorporatedbusinesses

P8 Identify and explain the obligations of tax payers and/or their agents and the implicationsof non-compliance

There is a basic template2 for the ACCA F6 Taxation Paper which contains some seven key learning

outcomes as illustrated in diagram 2 below.

The comparison of the variants shows that they are very country specific. For example, the UK

variant includes chargeable gains and inheritance tax but feedback from the Tbilisi workshop

indicated that these issues were not relevant within the STAREP countries.

On the other hand there are various real estate and land taxes together with excises and

environmental taxes that are important within the region. This would suggest that the "other taxes"

element of the module will have to be designed on a country by country basis rather than a regional

basis.

Once the learning outcomes have been agreed, these can be referenced to specific legislation in

each country.

2This is based on a comparison the variants of Paper F6 for the UK, Poland, Czech Republic English, Romaniaand Russia..

3 Page

S TA REP Accounting and Auditing Education Community of Practice Workshop

Diagram 2 - Relational Diagram of Main Capabilities for Tax

AExplain the Operation and Scope of the National Tax System

B CExplain and Compute Explain and Compute

Income Tax Liabilities of Income Tax Liabilities ofIndividuals Corporate Entities

D Explain and compute Social ESecurity, Insurance and Health Explain and compute theContributions for Employers,

Employees and individual effects of Value Addedentrepreneurs Tax on Businesses

FExplain and Compute the

effect of Other Taxes

GIdentify and Explain the Obligations of Taxpayers and/or their +

Agents and the Implications of Non-compliance

* This two day workshop forms part of a program of workshops planned for throughout theduration of STAREP project deal with specific issues related to modernizing the education

and development of accountants and auditors in the participant countries.* All the workshops have a highly interactive format and working group members will work

together to develop agreed learning objectives that can be referenced to country specificlegislation.

* Agreed learning outcomes for the law and tax subject areas that can be integrated with

learning outcomes established for the other subject areas.

* Development of a syllabus structure that can be referenced to country specific legislation ineach participant STAREP country.

www.worldbank.org/cfrr

4 Page

ST A R EP Accounting and Auditing Education Community of Practice Workshop

Wednesday, 25 February 2015 - Day 1

.: ......

09:00 Welcome Remarks Presenter: Alex Fawcett, Senior Financial ManagementSpecialist, Centre for Financial Reporting Reform, WorldBank

09:15 Overview of the Workshop Presenters:Ian Ritchie, Consultant, Centre for Financial ReportingReform, World Bank

Prof. Radoslaw Ignatowski, Head of InternationalAccounting Unit, Department of Accounting.Management Faculty, University of Lodz, Poland

Mark Fielding-Pritchard, Consultant, Centre forFinancial Reporting Reform, World Bank

This session introduces participants to the key issues tobe addressed in the workshop and highlights theanticipated outcomes.

11:15 Parallel sessions of the In these first sessions participants will consider theWorking Groups overall structure of the syllabi for law and tax and set a

program for the remaining sessions.

Law Moderator: Prof. Radoslaw Ignatowski, Head ofInternational Accounting Unit, Department ofAccounting. Management Faculty, University of Lodz,Poland

Tax Moderator: Mark Fielding-Pritchard, Consultant, Centrefor Financial Reporting Reform, World Bank

14:00 Parallel sessions of the In these sessions participants will start to consider theWorking Groups detailed content of the syllabi for law and tax.

Law Moderator: Prof. Radostaw Ignatowski, Head ofInternational Accounting Unit, Department ofAccounting. Management Faculty, University of Lodz,Poland

Tax Moderator: Mark Fielding-Pritchard, Consultant, Centrefor Financial Reporting Reform, World Bank

5 Page

'STARFP Accounting and Auditing Education Community of Practice Workshop

16:00 Parallel sessions of the In these sessions participants will continue consideringWorking Groups the detailed content of the syllabi for law and tax.

Law Moderator: Prof. Radoslaw Ignatowski, Head ofInternational Accounting Unit, Department ofAccounting. Management Faculty, University of Lodz,Poland

Tax Moderator: Mark Fielding-Pritchard, Consultant, Centrefor Financial Reporting Reform, World Bank

1D 7 0_- En0o&Dy0

Thursday, 26 February 2015 - Day 2

09:00 Parallel sessions of the In these sessions participants will continue consideringWorking Groups the detailed content of the of the syllabi for law and tax

Law Moderator: Prof. Radoslaw Ignatowski, Head ofInternational Accounting Unit, Department ofAccounting. Management Faculty, University of Lodz,Poland

Tax Moderator: Mark Fielding-Pritchard, Consultant, Centrefor Financial Reporting Reform, World Bank

104 C e a

11:15 Parallel sessions of the In these sessions participants will continue consideringWorking Groups the detailed content of the of the syllabi for law and tax

Law Moderator: Prof. Radoslaw Ignatowski, Head ofInternational Accounting Unit, Department ofAccounting. Management Faculty, University of Lodz,Poland

Tax Moderator: Mark Fielding-Pritchard, Consultant, Centrefor Financial Reporting Reform, World Bank

6 Page

ST A R EP Accounting and Auditing Education Community of Practice Workshop

14:00 Parallel sessions of the In these sessions participants will finalize work andWorking Groups prepare a presentation of the key points to share with

all participants.

Law Moderator: Prof. Radoslaw Ignatowski, Head ofInternational Accounting Unit, Department ofAccounting. Management Faculty, University of Lodz,Poland

Tax Moderator: Mark Fielding-Pritchard, Consultant, Centrefor Financial Reporting Reform, World Bank

16:00 Wrap-up Session Presenters:Prof. Radoslaw Ignatowski, Head of InternationalAccounting Unit, Department of Accounting.Management Faculty, University of Lodz, Poland

Mark Fielding-Pritchard, Consultant, Centre forFinancial Reporting Reform, World Bank

Ian Ritchie, Consultant, Centre for Financial ReportingReform, World Bank

Alex Fawcett, Senior Financial Management Specialist,Centre for Financial Reporting Reform, World Bank

This session brings together the results of work ofundertaken over the duration of the workshop andoutlines how it is anticipated that the syllabusdevelopment will move forward.

7 Page

Schweizerische EidgenossenschaftAustrian Confédération suisse

Development Cooperation Confederazione SvizzeraConfederaziun svizra

41 LF GOUVERNFMENTDU GRAND DUCHÉ DF LUX1MBOURG

PEOHRAL MINISTRY MnisteiedesFinancesGP PINANCE

ぐう

・ )