EACT Regulatory framework, legal and tax constraints for centralized cash management Guides ECHNICAL

336

EACT Regulatory framework, legal and tax constraints for centralized cash management Guides ECHNICAL March 2009 T Austria - Belgium - Brazil China - Czech Republic Denmark - France - Germany India - Ireland - Italy Japan - Luxembourg Mauritius - Mexico The Netherlands - Poland Portugal - South Africa Spain - Switzerland United Kingdom United States of America

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of EACT Regulatory framework, legal and tax constraints for centralized cash management Guides ECHNICAL

December 2008

EACTRegulatory framework,legal and tax constraints for centralized cash management

GuidesECHNICAL

Marc

h 2

009

T

Austria - Belgium - BrazilChina - Czech Republic

Denmark - France - GermanyIndia - Ireland - Italy

Japan - LuxembourgMauritius - Mexico

The Netherlands - PolandPortugal - South Africa

Spain - SwitzerlandUnited Kingdom

United States of America

Price : 100 € (including VAT)

The information presented in this present document may under no circumstances be construed to be advice or legal assistance,as defined by the French Law no 90-1259, dated December, 31st, 1990.

DÉPOT LEGAL n° 13353

EACT – the European Association of Corporate Treasurers – includes 18 associations of corporate treasurers of 17 countries of the EuropeanUnion. It brings together about 8,100 members representing 4,600 groups/companies located in the EU.

HistoryWhen it was formally set-up in May 2002, EACT wasnamed the Euro Associations of Corporate Treasurersand was restricted to associations of corporatetreasurers of the euro area.In October 2004, EACT became the EuropeanAssociations of Corporate Treasurers and is open toany association of corporate treasurers and financeprofessionals of the European Union.

MissionsThe European Association of Corporate Treasurers(EACT) is a grouping of national associationsrepresenting treasury and finance professionals.Speaking with a united voice, the EACT creates agreater impact than the sum of its individualcomponent actions. This gives prominence to theissues faced by treasury and finance professionalsacross Europe with the European authorities,national governments, regulators and standard-setters.Together we promote the value of treasury skillsthrough best practice and education. We ensure thatthe treasury role continues to evolve as an essentialcomponent within a dynamic financial environment.

Technical CommissionsThe Board of Directors selects the topics on whichEACT will work as well as the general objectives. TheEACT Board member in charge will in most casesset-up a Commission headed by a Chairman andwith members in several EACT associations.

They are:- Means of payment and SEPA: Gianfranco Tabasso- Transfer pricing in treasury: Luc Vlaminck and

Bruno Resseguier- International accounting standards:

François Masquelier and Mark Kirkland- Rating agencies: John Grout and Patrice Tourlière- Compliance and codes of conduct:

Charles-Henri Taufflieb- CAST: Gianfranco Tabasso.

Current EACT MembersEACT includes 18 associations of 17 countries of the European Union representing about 4,600 companies/groups and 8,100 corporatetreasurers and finance professionals.

The 18 associations are:- ACT, The Association of Corporate Treasurers (UK)- AFTE, Association Française des Trésoriers

d’Entreprise- AITI, Associazione Italiana Tesorieri d’Impresa- ASSET, Asociacion Espanola de Financieros y

Tesoreros de Empresa- ATEB, Association of Corporate Treasurers in

Belgium- ATEL, Association des Trésoriers d’Entreprise au

Luxembourg- CAT, Czech Association of Treasury- DACT, Dutch Association of Corporate Treasurers- FACT, Finnish Association of Corporate Treasurers- GEFIU, German Financial Executives Institute

(Gesellschaft fûr Finanzwirtschaft in der Unternehmensführung e.V.)

- HTC, Hungarian Treasury Club- IACT, Irish Association of Corporate Treasurers- ÖPWZ, Forum Finanzen (Austria)- PCTA, Polish Corporate Treasurers Association- SACT, Swedish Association of Corporate

Treasurers- SAF, Slovak Association of Finance and Treasury- SCTA, Slovenian Corporate Treasurers Association- VDT, Verband Deutscher Treasurer.

For further information, you may visit EACT websitewww.eact.eu

or send an email [email protected]

Phone: +33 (0)1 42 81 53 98

or write to EACT, 20 rue d’Athènes, F 75 009 Paris

EGULATORY FRAMEWORK, LEGAL AND TAX CONSTRAINTSFOR CENTRALIZED CASH MANAGEMENT

March 2009

RSUMMARY

CONTRIBUTORS 3

INTRODUCTION 5

CASH MANAGEMENT IMPLEMENTATION:

ISSUES TO BE CONSIDERED 7

CASH MANAGEMENT IN: Austria 9Belgium 23Brazil 37China 47Czech Republic 67Denmark 79France 89Germany 111India 125Ireland 137Italy 147Japan 165Luxembourg 177Mauritius 191Mexico 205The Netherlands 217Poland 229Portugal 247South Africa 261Spain 277Switzerland 291United Kingdom 303United States of America 317

REGULATORY FRAMEWORK, LEGAL AND TAX CONSTRAINTSFOR CENTRALIZED CASH MANAGEMENT

2

March 2009

Technical guides EACT

3

CONTRIBUTORSThis publication has been drawn up by:

AUSTRIA * Stefan Tiefenthaler - Klemens Keferböck Binder Grösswang Rechtsanwälte OEG

BELGIUM * Benoit Feron - Frédéric Heremans - Benoit Malvaux NautaDutilh

BRAZIL Robert E Williams - Alexandre Leander Delgado Noronha Advogados

CHINA Charles Qin Llinks Law Offices

CZECH REPUBLIC * Josef Otcenasek Havel & Holasek s.r.o., Advokátní kancelářDita Sulcova - Věra Pastikova Tacoma Tax Consulting s.r.o.

DENMARK Claus Molbech Bendtsen - Ricki Boye Lett

FRANCE * Jean-François Adelle - Joel Lambert Jeantet Associés

GERMANY * Georg Edelmann - Sebastian Bock Nörr Stiefenhofer Lutz

INDIA Shivendra Kundra - Rama Kant Rai Kundra & Bansal

IRELAND * William Johnston - Niamh Caffrey Arthur Cox

ITALY * Goffredo Guerra DLA PiperGilberto Comi Carnelutti Studio Legale Associato

JAPAN Hiromasa Ogawa - Hitomi Sakai Kojima Law Offices

LUXEMBOURG * Jean-Marc Delcour Loyens & loeff

MAURITIUS Iqbal Rajahbalee - Joel Lambert BLC

MEXICO Jorge A. Sánchez Dávila - Rosario Huet Covarrubias Goodrich, Riquelme y Asociados

THE NETHERLANDS * R.L.S. Verjans - S.W.A. Deckers - S. den Boer Simmons & SimmonsC.W.Plugge - C. Scholten Simmons & Simmons

POLAND * Łukasz Szegda - Michał Bernat Wardynski & Partners

PORTUGAL Antonio de Mendonça Raimundo - Rute Martins Santos Albuquerque & Associados

SOUTH AFRICA Clinton van Loggerenberg - Kefiloe Kgomo Deneys Reitz Attorneys

SPAIN * Pere Kirchner Baliu Cuatrecasas

SWITZERLAND Martin Hess - Simone Hofbauer Wengerlaw RechtsanwâlteRegula Grunder - Remy Bärlocher Wengerlaw Rechtsanwâlte

UNITED KINGDOM * Gwendoline Godfrey DMH Stallard LLPGeorge Hardy Ernst & Young

UNITED STATES Elizabeth Leckie Allen & OveryBill Satchell O’Melveny & Myers

EACT thanks all participants and specially Jean-François Adelle, partner Jeantet Associés,for their contribution to this publication.

* EACT member"Any copy or reproduction, in whole or in part, of this document made without the authorisation of the author(s) or the persons possessing the legal right thereto, or their heirs, is forbidden by the Law of March 11th 1997, paragraph 1 of article 40. Any copy or reproduction, by any means whatsoever, would represent a forgery and as such could be sanctioned in accordance with articles 425 and seq of the French Penal Code. The Law of March 11th 1957 only authorises, in accordance with paragraphs 2 and 3 of article 41, copies or reproductions that are strictly reserved for the private usage of the person copying the document and not for general usage, or for short quotations and analyses."

© 2009 European Association of Corporate Treasurers (EACT)

REGULATORY FRAMEWORK, LEGAL AND TAX CONSTRAINTSFOR CENTRALIZED CASH MANAGEMENT

March 2009

Technical guides EACT

5

INTRODUCTION

Cash management includes all forms of management and allocation of financial resources within agroup of companies. It includes intra-group cash pooling, which consists in centralizing cash surplusesand cash needs, and payments and debt collection arrangements.

Centralizing cash management fulfils several objectives. Redistribution of available cash enables abetter use of resources and reduces the need for more costly banking facilities. Centralizedmanagement also allows the group signature on debt instruments markets to be concentrated at oneplace within the group. As a result it allows each member company to obtain better conditions.Centralized cash management also enables a better forecast and management of financial risks.

Surplus cash of member entities is routed through the centralizing company to the other memberentities having cash needs, and any group surplus remaining is invested. The centralizing company andthe centralized participant companies each maintain accounts, respectively the “central account” andthe “secondary accounts”. The centralizing company is, often in practice, the parent company. Cashpooling is usually performed by regular transfers from secondary accounts into the central account(zero balance account). These transfers are executed by the depository with which the accounts wereopened. Centralization of cash management therefore implies effective cash transfers between theaccounts of participating companies.

Cash pooling can sometimes take the form of a simple pooling of interest, without movement offunds, called notional pooling. In such case, each company holds an account with the same depositoryinstitution. This depository agrees either to charge interest, commissions and fees or allocate rebateson a net basis, as if all accounts were merged into one single account, giving rise to “intellectual”netting among the participating companies.

In cash management of payments and debt collection schemes, internal payment transactions aremade by debiting or crediting the relevant company’s clearing accounts, maintained by the centralizingentity. Payments due to external third parties are made by the centralization structure out of thecentralization bank account on behalf of a centralized participant and are settled internally by debitingthe clearing account maintained by the relevant participating companies. Likewise, payments receivedby the centralizing entity on behalf of a participant are credited to the relevant group-internal clearingaccounts.

The development of centralized cash management arrangements, in recent years, has been fuelled bya search for greater profitability. Centralization has often followed restructuring transactions.Centralized cash management has taken a unique role in groups having member companies in multipleEuropean countries, due to the lifting of tax impediments on the flow of interest, to the taxcompetition intended to attract centralizing companies, and to the changeover to the Euro. The singleEuropean currency facilitates centralized management between companies situated in differentcountries of the monetary union, both because the circulating capital is denominated in the samecurrency, and because the banking conditions have been made substantially more comparable. Inaddition, having eliminated the need to change currency, the Euro has greatly simplified thetransactions necessary for centralized cash management. Centralized cash management is alsodeveloping outside of the context of the Euro and the European Union, most notably in the Dollar zoneand emerging countries.

REGULATORY FRAMEWORK, LEGAL AND TAX CONSTRAINTSFOR CENTRALIZED CASH MANAGEMENT

6

Centralized cash management raises tax and legal issues which one needs to identify and understandin order to safely execute and implement agreements. Such issues mostly relate to constraints underbanking regulation, company laws, tax law, mandatory reporting to central banks, and specific aspectslinked to the use of the internet.

The activities of the centralizing company, particularly the reception and the remuneration of deposits,the granting of credit and the management of payments and debt collection, are generally classifiedas banking or investment services operations, and as such may fall under the ambit ofbanking/investment services monopoly. Accordingly, it is necessary to determine whether theseactivities require a banking license (or equivalent), or whether they benefit from an exemption whencarried out exclusively within a group of companies. Other issues include notional pooling, monopolyof investment services and banking secrecy aspects.

Company law aspects primarily relate to whether the cash management agreement conforms to thecorporate benefit of the participating companies, so as to preclude the possibility of invalidly orreassessment of the agreement, protect the directors and/or shareholders against liability and avoidpropagation of insolvency procedures within the centralization perimeter. Prevention of conflict-of-interest procedures also needs to be considered. As regards tax legislations, several questions will haveto be considered: mainly VAT treatment of the financial operations, issues relating to withholdingtax/limitations on the deductions of interest paid and availability of favourable tax regime.

In the context of groups operating in more than one country, familiarity with the relevant domesticlaws of each country is imperative in order to maximize the choice of law, select the most adequateform for the centralizing company and assess the appropriateness of the contemplated remunerationterms. Within the European Union itself, despite principles held in common by the laws of the involvedcountries, there exist important differences.

Prepared under the auspices of the European Associations of Corporate Treasurers (EACT), thisTechnical Guide updates the 2004 edition by expanding it both geographically (new to this edition areBrazil, India, China and several countries from Latin America, Africa, Eastern Europe and South East Asia)and thematically (it newly covers management of payments and debt collections, foreign exchangeand rates).

The aim of this Technical Guide is to furnish an outline of the legal, regulatory and tax constraintsinvolved in the setting up of a cash management program. It is aimed at those who wish to put in placecentralized cash management involving different countries. It is not intended as a substitute forappropriate legal advice, which should take into consideration the specific nature of an actual group,the situation of each participating company, the goals to be met and the allocated resources. All errorsand omissions are exclusively the responsibility of the individual author. Any legal developmentsfollowing 30 June 2008 have not been taken into account.

Richard RAEBURN Olivier BRISSAUD Jean-François ADELLEEACT Chairman EACT Board Member Partner

European Affairs Jeantet Associés

March 2009

Technical guides EACT

7

CASH MANAGEMENT IMPLEMENTATION:ISSUES TO BE CONSIDERED

CASH MANAGEMENT STRUCTURE

IV.CENTRAL BANKING REPORTING

• Balance of payments

III. TAX ISSUES• Operations subject to VAT

• Taxation of interest

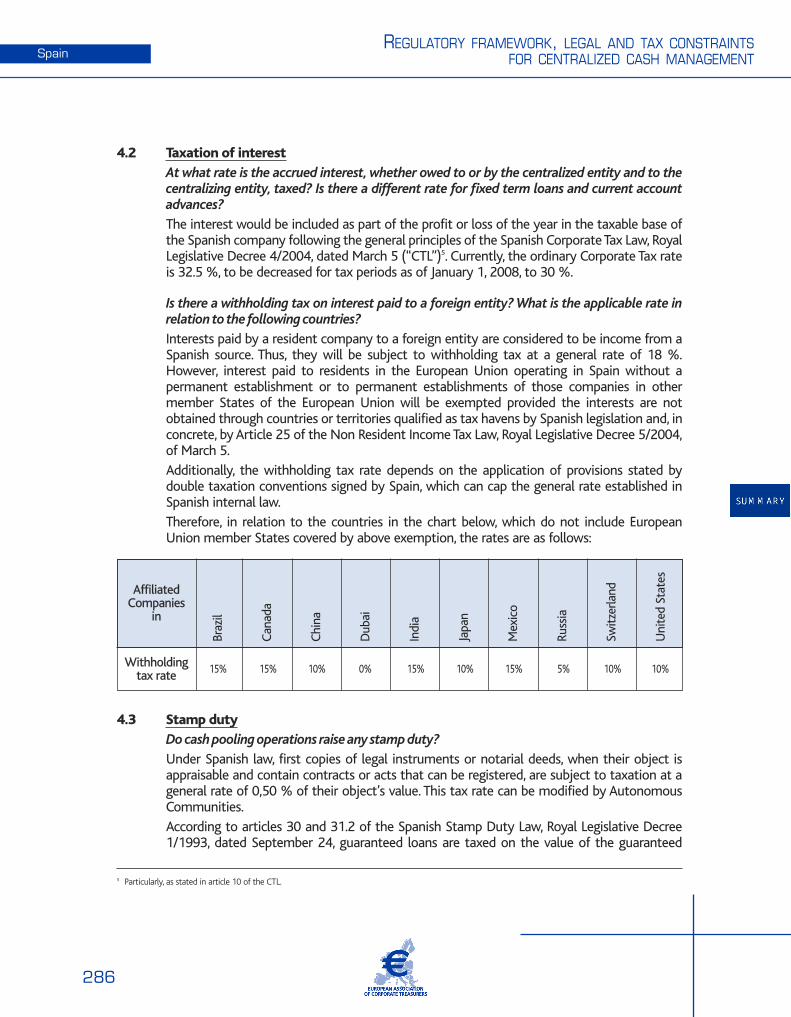

• Withholding tax on interest paid

• Deductibility of interest

• Transfer price issues

II. COMPANY LAW• Regulated agreements

• Corporate benefit of the participatingcompanies

• Liabilities of directors and shareholders

• Bankruptcy

• Centralizing company form

I. BANKING LAW• Banking / investment services monopoly?

• Exemptions for cash management activities within a group:- Concept of effective control- Authorized operations

• Limitations to remuneration of cash deposited and to notional pooling of current accounts?

• Banking secrecy

VI. CONTRACTUAL ENVIRONMENT• E-cash management: data security aspects

• Legal qualifications

V. EXCHANGE CONTROL• Exchange control issues

REGULATORY FRAMEWORK, LEGAL AND TAX CONSTRAINTSFOR CENTRALIZED CASH MANAGEMENT

8

March 2009

Technical guides EACT

9

Austria

REGULATORY, LEGAL AND TAX FRAMEWORK FOR INTERNATIONAL CASH MANAGEMENT

UNDER AUSTRIAN LAW

This contribution does not constitute legal advice. Its purpose is to give an overview of the laws andregulations that are applicable to cash management in Austria. The principles set out below should beconsidered in relation to individual circumstances, with legal and tax counsel.

Binder Grösswang Rechtsanwälte OEG

Sterngasse 131010 Vienna, Austria

Dr. Stefan Tiefenthaler LL.M. PartnerBanking & Finance

T +43 1 534 80-310F +43 1 534 [email protected]

Dr. Klemens Keferböck LL.M. Senior AssociateBanking & Finance

T +43 1 534 80-464F +43 1 534 [email protected]

REGULATORY FRAMEWORK, LEGAL AND TAX CONSTRAINTSFOR CENTRALIZED CASH MANAGEMENT

10

Austria

1. BANKING/FINANCIAL REGULATION

1.1 Banking authorities’ approval or exemption

1.1.1 ZBA cash pooling

Do loans/advances to other group entities require banking authorities’ approval for thecentralized entities or the centralizing entity? Is a distinction to be made between short term,mid term and long-term loans/advances?

The granting of loans in Austria may constitute banking business under the Austrian BankingAct (Bankwesengesetz) and consequently requires the centralizing entity to obtain a bankinglicense, if carried out on a commercial basis (gewerblich). According to the leading authority,dealings are carried out on a commercial basis if they occur (i) repeatedly (wiederholt) or withthe intention to be repeated (mit Wiederholungsabsicht) and (ii) are aimed at the realizationof proceeds (Einnahmenerzielungsabsicht). In this respect, the Austrian Banking Act does notdifferentiate between short term, mid term and long term loans.

Generally, a case by case approach is to be adopted when determining if the granting of loansis carried out on a commercial basis in the meaning of the Austrian Banking Act.Unfortunately, no guidelines or decisions of the competent Austrian Financial MarketAuthority exist for such determination in relation to cash pooling arrangements and, thus,uncertainties prevail.

However, it is often argued that in relation to intragroup loans and loans granted inconnection with cash pooling arrangements (assuming that the account management isconducted by a bank) the standard to be applied in relation to such determination is lenientand, thus, such loans regularly do not qualify as banking business requiring a banking license.

In practice, the Austrian Financial Market Authority (FMA) does currently not qualifyintragroup loans and loans granted in connection with cash pooling arrangements (assumingthat the account management is conducted by a bank) as banking business requiring abanking license.

Do investments in financial instruments including derivative products carried out by thecentralizing entity on behalf of the centralized entities require banking authorities’ approval forthe centralized entities or the centralizing entity? Is an exemption available in groupcompanies?

Investing in financial instruments in Austria on behalf of the centralized entities may requirethe centralizing entity to obtain the banking authorities’ approval (i.e. a license), if carried outon a commercial basis (gewerblich; please see above for further details with respect to thisrequirement). In relation to cash pooling schemes, such activity most likely would be carriedout on a commercial basis in the meaning of the applicable laws and, thus, would require alicense.

In this respect, there are no specific exemptions under the Austrian Banking Act relating togroup companies.

March 2009

Technical guides EACT

11

Austria

In both cases, is there an exemption available for operations within groups of companies? Whatare the sanctions, if any, for breaching this requirement? There are no specific exemptions under the Austrian Banking Act with respect to operationswithin groups of companies.Principally, a breach of the requirement to obtain a banking license may result in a fine of upto EUR 50,000. Further, the lender is not entitled to receive any remuneration (e.g. interest)for the loan granted.

1.1.2 Notional pooling Is there any prohibition/restriction on banks/participating entities implementing notionalpooling (i) by way of bank margins reductions, (ii) by way of merging current account balancesof the centralizing and centralized entities in order to create a single balance, or (iii) by way ofcalculating interest payable to each account based on merged scales of interest? Do banksrequire cross guarantees from participating entities? Can such guarantees be capped?In Austria, there are no specific banking regulatory prohibitions/restrictions in respect ofnotional pooling schemes (i.e. pooling arrangements which do not provide for an “actual” butmerely for a “notional” merging of current account balances).There are no specific banking regulatory provisions requiring banks in any case to obtain crossguarantees in relation to notional pooling schemes.

1.1.3 Centralized management of exchange rates and risksDoes the arrangement whereby a centralized entity agrees to buy from and sell to thecentralizing entity all its foreign currencies require banking authorities’ approval or consent?Buying and selling foreign currencies in Austria may constitute banking business under theAustrian Banking Act and consequently requires the centralizing entity to obtain a bankinglicense, if carried out on a commercial basis (gewerblich; please see above for further detailswith respect to this requirement). In relation to cash pooling schemes, such activity mostlikely would be carried out on a commercial basis in the meaning of the applicable laws and,thus, would require a license.

1.1.4 Centralized management of payments and debt collectionsAre the centralizing entity’s activities as the operator of a management of payments/collectiveprogram subject to approval requirements under any applicable banking regulatory laws? The activities usually conducted by the centralizing entity in relation to managing an effectivecash pooling scheme may constitute banking business under the Austrian Banking Act andconsequently requires the centralizing entity to obtain a banking license, if carried out on acommercial basis (gewerblich). We refer to our elaborations above.

1.2 Banks duty of confidentialityCan the centralizing entity obtain from banks holding the accounts of centralized entitiesinformation on such accounts?Austrian law expressly recognises and protects a bank’s duty of confidentiality (sometimesreferred to as “banking secrecy”) with respect to information received by or relating to its

REGULATORY FRAMEWORK, LEGAL AND TAX CONSTRAINTSFOR CENTRALIZED CASH MANAGEMENT

12

Austria

customers. According to these rules of banking secrecy banks may also, generally said, notdisclose information on accounts of centralized entities. However, the banks are not bound tosuch banking secrecy and therefore may transfer information on accounts to centralizingentities to the extent the centralized entities expressly and in writing waived their respectedright and assented to such transfer.

1.3 Other regulatory requirements Are there specific requirements in regulated financial activities (e.g. insurance industry, assetmanagement etc.)?In Austria, there are no specific requirements for financial activities conducted with respect tocash pooling. However, there are numerous general requirements which can be relevant withrespect to financial services as provided by the insurance and asset management industry, such as requirements set forth in the Austrian Banking Act (Bankwesengesetz), in the Austrian Commerce Regulation Act (Gewerbeordnung), the Austrian SecuritiesSupervision Act (Wertpapieraufsichtsgesetz) and the Austrian Insurance Supervision Act(Versicherungsaufsichtsgesetz).

Is there a requirement that the global effective rate be stated in the centralization agreement? There is no specific requirement to state the global effective rate in the centralizationagreement(s) between the centralizing entity and the centralized entities.

Are there specific requirements in connection with the opening of bank accounts (KYC,language…)?In order to fulfill Austria’s obligations under European and international law to fight moneylaundering and terrorism the Banking Act provides for various KYC requirements.In particular, credit and financial institutions shall register the identity of a customer

(i) when entering into a permanent business relationship (this includes the opening of bank accounts for a new customer); and

(ii) in all transactions not falling within the scope of an ongoing business relationship and involving a sum amounting to at least 15,000 Euros or an equivalent value in Euros (irrespective of whether the transaction is carried out in a single operation or in several operations which are obviously closely linked).

The banks have to determine the identity of a corporation’s authorized representatives byphoto identification. Under certain circumstances, the representatives are not obliged toappear in person for the purpose of such identification. Further, the identity of a corporationand the representatives’ authority to act on behalf of it is to be determined by the banks byappropriate documents available in the jurisdiction of the corporation’s incorporation.

1.4 OutsourcingCan the cash pooling function be entrusted in whole or in part to an agent that is not memberof the group? In general, Austrian law does not prevent entities not being member of a group to act as agentin relation to cash pooling schemes. Of course, the conduct of such activities in Austria mostlikely requires a banking license.

March 2009

Technical guides EACT

13

Austria

2. CORPORATE LAW

2.1 Form of participating entities

Are there restrictions as regards the form of entities that can participate in cash poolingarrangements, either as a centralized or centralizing entities (certain forms of entities,groupings, partnerships…) and/or the form or the nationality of shareholders (state ownedentities, foreign shareholders…)?

We do not see any such restrictions as regards the form of entities under Austrian law.

2.2 Corporate purpose

Do the activities carried out in cash pooling arrangement need to be expressly contemplated inthe bylaws?

The activities carried out in a cash pooling arrangement do not need to be expresslycontemplated in the bylaws of an Austrian corporation.

2.3 Corporate benefit

How is defined corporate benefit? Is it different when it relates to entities belonging to a samegroup?

Under Austrian law it is illegal for a corporation to grant a financial assistance (corporatebenefit) to its (direct or indirect) shareholders (or affiliates of such shareholders) other thanin the course of a distribution of dividends or a formal reduction of the share capital.Therefore, the entering into any kind of agreement by a corporation with its parent (or sister)company is, generally, only licit to the extent such corporation receives an adequate economicbenefit and would also enter into such agreement with a third, not affiliated party on thesame terms and conditions (arm’s length principle). In this respect, no distinction is madebetween direct and indirect shareholdings or different group members. Generally, thisprinciple also applies to limited partnerships (Kommanditgesellschaft), where no naturalperson is fully liable for the partnerships’ debts.

Are there restrictions on the participation of certain entities due to their financial structure(ratios, etc.)?

We are not aware of any specific restrictions on the participation of corporations in cashpooling schemes due to the corporations’ corporate or financial structure and the structure ofthe corporate group intending to take part in a cash pooling scheme.

Of course, the entering into a cash pooling arrangement by a company may infringe theAustrian rules of financial assistance if such arrangement entails, for example, financial risksdue to the low credit rating of (up-stream or cross-stream) affiliated companies.

Is there an obligation to offer all participating entities equivalent terms and conditions?

Principally, according to the rules on financial assistance, there (only) is an obligation to enterinto agreements with affiliated companies on arm’s length terms. Therefore, it might be licitto offer different terms and conditions, provided, however, that those different terms areeconomically justified (e.g. different interest rates due to different ratings). Yet, the standards

REGULATORY FRAMEWORK, LEGAL AND TAX CONSTRAINTSFOR CENTRALIZED CASH MANAGEMENT

14

Austria

to be applied in this respect are to be very strict. In many cases, different terms and conditionsmay indicate that an arrangement is not entered into on arm’s length terms.

Are there restrictions on the type of operations that the centralizing entity may undertake withthe cash of the centralized entities?

We are not aware of any specific restrictions in this respect. Certainly, any agreement betweena corporation and an affiliated company on the type of operations to be conducted isprincipally to be made on arm’s length terms.

Is there an obligation to offer the participating entities market financial conditions (i.e. the“arm’s length principle”)?

Principally, there is an obligation for a corporation to enter into agreements with affiliatedcompanies on arm’s length terms.

What are the liabilities and sanctions in case of violation of the corporate benefit of aparticipating entity (cancellation of the agreement, management liability, extension ofbankruptcy proceedings etc.)? Do they apply to directors, officers and shareholders?

Agreements entered into in violation of the Austrian rules on financial assistance are void(potentially triggering a repayment claim) and a company’s management may be heldpersonally liable for concluding such agreements.

2.4 Remuneration of the centralizing entity

Are there any prescriptions as to the remuneration of the centralizing entity difference oflending/borrowing rates, lump sum fee…)?

There are no such specific prescriptions. Of course, any remuneration scheme is to be inaccordance with the rules on financial assistance briefly set out above.

2.5 Investment of excess cash by the centralizing entity

Are there prudential investment rules?

There are no such specific rules for companies. Under general corporate law, however, anymanagement decision is to be taken with reasonable care.

2.6 Approval of cash pooling arrangement

Does the cash pooling arrangement need to be approved by the management board /supervisory board or the shareholders?

Stock corporation: Most likely, the management board of a stock corporation requires prior approval of thesupervisory board prior entering into an effective cash pooling arrangement. The entering intoa notional cash pooling arrangement, however, not necessarily requires the managementboard to obtain prior supervisory board approval. Of course, the stock corporation’s supervisory board itself or the corporation’s bylaws maystipulate a requirement for the management board to seek prior approval from thesupervisory board before entering into any kind of cash pooling scheme.

March 2009

Technical guides EACT

15

Austria

Limited liability company:

In any case, the management board of a limited liability company requires prior approval ofthe company’s shareholders prior entering into an effective cash pooling arrangement. Theentering into a notional cash pooling arrangement, however, might not necessarily require themanagement board to obtain prior approval. Yet, it would be prudent for a management toobtain a shareholder approval also in relation to notional cash pooling schemes.

In case a supervisory board exists, the same rules as described above in relation to stockcorporations apply.

Of course, the limited liability company’s bylaws may stipulate a requirement for themanagement board to seek prior approval (from any corporate body) before entering into anykind of cash pooling scheme.

2.7 Specific aspects relating to acquisition financing exit

Are there restrictions on the use of cash of the target or the target’s subsidiaries to repay theacquisition loan? Does the existence of a cash pooling arrangement modify the rules? Does anycompany law restriction prevent the centralizing entity from exercising its contractual right toterminate the agreement?

In relation to stock corporations, Austrian law explicitly prohibits the use of monies of a targetor the target’s subsidiaries (other than received as dividends or in the course of a formaldecrease of the statutory capital) in order to finance an acquisition. Therefore, the setting upof a cash pooling arrangement with a target (or a target’s subsidiary) aiming to finance itsacquisition is illicit under Austrian law. It is sometimes argued (although also disputed) inliterature that the same applies to other companies, such as limited liability companies. In anycase, any such cash pooling arrangement would most likely also violate Austrian capitalmaintenance (financial assistance) rules (please see above).

3. BANKRUPTCYWhat are the legal consequences of a participating entity being insolvent or nearly insolvent onthe operations involving the entity (ZBA and notional)?

Principally, arrangements enabling the set-off of receivables between participating entitiesmay be invalid in relation to an insolvent participating entity, if by means of such set-off acredit balance attributable to such insolvent entity is set-off against a debit balance ofanother participating entity. Any such prior set-off may also be subject to a right to avoidanceunder the Austrian avoidance for preference rules.

Further, upon the opening of insolvency proceedings with respect to a participating entity anypayments made to or securities granted in favor of a creditor by such entity may be subjectto a right to avoidance if, in particular, (i) within the preceding twelve months, making suchpayments or granting such securities constituted (compared to other creditors) a preferentialtreatment of the respective creditor in the meaning of the applicable law or (ii) within thepreceding six months, the beneficiary of such payments or security was aware of theinsolvency of the entity.

REGULATORY FRAMEWORK, LEGAL AND TAX CONSTRAINTSFOR CENTRALIZED CASH MANAGEMENT

16

Austria

Moreover, in case of an o pening of insolvency proceedings with respect to a participatingentity, any rights to securities or other rights acquired by enforcement proceedings within 60 days prior to such date will immediately cease to exist.Generally said, the above mentioned consequences would be applicable for both ZBA andnotional cash pooling (albeit those in relation to actual payments made should not berelevant with respect to notional cash pooling schemes). Lastly, if loans are granted to a participating entity being insolvent, over-indebted or fulfillingcertain reorganization requirements by a (direct or indirect) shareholder having a controllinginfluence on such entity (or, upon such shareholder's instruction, by an affiliated entity), suchloans may be qualified as substitute for equity. Consequently, receivables arising from suchloans may be subordinated in relation to other creditors' receivables. Further, any securitygranted by such participating entity to secure such loans will cease to exist upon the openingof insolvency proceedings.

Would this limit the centralizing entity’s ability to exercise its contractual right to terminate theAgreement?

Generally, the commencement of insolvency proceedings with respect to a participatingentity will not limit the centralizing entity’s ability to exercise its contractual right toterminate the Agreement. Please note that enforcement action against an insolventparticipating entity may be significantly limited (see previous question). A contractual right to termination based upon the commencement of insolvency proceedingswill – except for applicable exemptions (e.g. with respect to employment contracts) – be validunder Austrian law. Please note, however, that a right to termination merely due to thecommencement of composition or reorganization proceedings may be invalid.

Are there any risks that bankruptcy proceedings issued against the centralizing entity or acentralized entity could be extended to other participating group entities?

If insolvency proceedings have been commenced with respect to the centralizing entity or acentralized entity, the remedies available in such case (as described above) may result incertain monetary claims against other participating entities. This may cause a furtherreduction of liquidity of the participating entities and, consequently, could eventually resultin other participating entities being subject to insolvency proceedings.

4. TAX ISSUESOur answers in relation to the tax issues are based on the following assumptions:

(i) The Austrian entity is not a bank;(ii) The Austrian entity is a corporation (either a limited liability company

(Gesellschaft mit beschränkter Haftung – GmbH) or a joint stock corporation (Aktiengesellschaft – AG);

(iii) The foreign entities resemble a corporation under Austrian law (GmbH/AG);(iv) The foreign companies do not maintain a permanent establishment in Austria;(v) The loans granted according to the cash pooling agreement are not secured by

mortgages on domestic (i.e. Austrian) real property.

March 2009

Technical guides EACT

17

Austria

4.1 Value added tax (VAT)

Are the operations between the centralizing entity and the centralized entities subject to VAT?If so, at what rate?

Austrian VAT legislation is based on the 6. EC-VAT Directive and therefore generally conformswith VAT legislation in other EU member states.In general, according to Austrian VAT law, a 20% VAT is imposed on services rendered inAustria.In general, financial services are performed where the customer has established its businessor has a fixed establishment to which the service is supplied. Financial transactions (e.g. thegranting of loans) in general are exempt from VAT. Consequently, no Austrian VAT falls dueon interest charged with respect to loans granted by or to any foreign entity.If any input VAT incurred is connected to specific services such as finance transactions thatare exempt from VAT, a refund of input VAT will not be possible for the centralizing entity.Hence, if an Austrian entity pays VAT for goods or services, it may not deduct such VAT if thesegoods or services are connected with its interest income deriving from the cash poolingarrangement.

4.2 Taxation of interest

At what rate is the accrued interest, whether owed to or by the centralized entity and to thecentralizing entity, taxed? Is there a different rate for fixed term loans and current accountadvances?

In principle, income from interest on loans (granted in accordance with the cash poolingarrangement) earned by an Austrian entity constitutes taxable income of the Austrian entity.Corporations are taxed on their net profit and are subject to Corporate Income Tax with a flattax rate of 25%.Income of foreign entities resulting from loans granted to an Austrian entity will, in general,not be taxable in Austria. Pursuant to sec 1 (3) Corporate Income Tax Act, corporations whichdo neither have their place of management nor their seat in Austria are subject to limited taxliability only. Sec 21 CITA stipulates that persons subject to limited tax liability are taxable in Austria onlywith income listed in Sec 98 Income Tax Act (“ITA” – "Einkommensteuergesetz"). With regardto loans, sec 98 ITA provides that interest income is taxable only if the loan is secured bymortgages on domestic, i.e. Austrian, real property or ships registered with a domestic shipregister or if the loan is granted by an Austrian permanent establishment of the foreign entity.Therefore, income of a foreign entity from loans granted to an Austrian entity is not taxablein Austria. In this respect, also no withholding tax will fall due.

Is there a withholding tax on interest paid to a foreign entity?

As mentioned above, income of a foreign entity from loans granted to an Austrian entity isnot taxable in Austria and therefore not subject to Austrian withholding tax. In addition, please note that income from interest on loans (granted in accordance with thecash pooling arrangement) earned by the Austrian entity will be taxable income of theAustrian entity, however, not being subject to withholding tax but rather to regular corporateincome tax.

REGULATORY FRAMEWORK, LEGAL AND TAX CONSTRAINTSFOR CENTRALIZED CASH MANAGEMENT

18

Austria

4.3 Stamp duty

Do cash pooling operations raise any stamp duty?

The Austrian Stamp Duty Act provides that certain legal transactions, including loanagreements or credit agreements (which are commonly part of any cash poolingarrangement) are subject to a stamp duty assessed on the value of the transaction. The taxrate is 0.8% of the loan/credit facility granted. However, revolving credit facilities with aduration of more than five years are subject to a stamp duty of 1.5%.

Stamp duties fall due if written agreements are executed in or brought into Austria. However,not only written agreements, but also other documentations trigger stamp duties, e.g. awritten acceptance of an oral offer, a documented oral acceptance of an offer, minutes on anagreement signed by one party to the agreement, certified copies of the agreement etc.

Even if no qualifying documentation has been produced, stamp duty will fall due in case ofshareholder’s loans. In this case, stamp duties fall due at the time when the loan/credit facilityis entered into the books of the Austrian borrower (i.e. the Austrian entity). This provisionwould not be applicable to loans granted by the Austrian entity to a foreign entity.

In order to avoid any stamp duties in connection with cash pooling schemes, it should bearranged that no foreign entity which grants a loan to an Austrian entity does directly hold ashare in the Austrian entity. No qualifying documentation on the cash pooling arrangementshall be executed in or brought into Austria. In addition, no party shall be entitled or obligedto receive performance of/perform an obligation with respect to the cash pooling agreementin Austria. Ultimately, high deliberateness must apply regarding any written correspondencebetween the foreign entities and an Austrian entity with respect to the cash poolingagreement in order to avoid the trigger of Austrian stamp duty.

4.4 Deductibility of interest

Are there limitations to the deductibility of interest paid by the centralized or the centralizingentity (such as a thin capitalization rule - debt / equity capital ratio)?

In general, interest payments made by the Austrian entity are tax deductible businessexpenses.

Austrian tax law does not contain specific thin-capitalization rules. As a rule, according to thepractice of Austrian tax authorities, an equity ratio of 20% should be sufficient. In the practiceof Austrian tax authorities, a shareholder loan constitutes hidden equity if it is granted as asubstitute for the shareholder equity. It is to be shown, however, that a supply of equity wouldclearly have been necessary at the time the loan was granted (to the Austrian entity) and thatthe loan is a substitute for the required entity. Hidden equity is not assumed if the company’sequity ratio is in accordance with general commercial practice.

In general, interest payments by an Austrian entity must comply with the arm’s lengthprinciple. Failure to comply with the arm’s length principle may result that inter-companyinterest rates which have been applied by the parties are adjusted for corporate income taxpurposes (please see 3.6. below). Consequently, inadequate high interest rates to be paid bythe Austrian entity to group companies would constitute a hidden distribution of profits (suchhidden distribution is also illicit financial assistance – please see above).

March 2009

Technical guides EACT

19

Austria

Is it possible to obtain a ruling from the tax authorities as to the deductibility of interest? If so,at what conditions may it be obtained?

In a particular case, it is possible to obtain a ruling from the competent tax office based onspecific facts. In complicated cash pooling or transfer pricing issues, there remains a risk thata tax inspector may in a later tax audit easily come to the conclusion that not all the factshad been properly disclosed. Consequently, the ruling issued previously is not longer bindingin the very case. In our experience, a binding ruling concerning the spread will take a quite long time becausethe competent tax office usually forwards such request to the tax audit department forassistance.

4.5 Tax havens

Are there specific provisions as to the interest accrued in tax havens?

There are no specific Austrian provisions with respect to interest accrued in tax heavens.

4.6 Favorable tax regime

Is there a favorable tax regime for (i) corporate tax of centralizing entities, (ii) taxation of cashpooling operations (VAT, interest)?

With reference to Austrian tax law, there is no favorable tax regime on these matters.

4.7 Transfer price issues

Do cash pooling operations raise transfer-pricing issues?

In general, if loans are granted to affiliated companies, the terms and conditions of the loan,in particular the interest rate, have to comply with the principle of dealing at arm’s length.Interest payments are considered not to comply with this principle if the interest rates agreedbetween related parties deviate from those that would have been agreed upon betweenunrelated parties. Accordingly, from an Austria tax law perspective, inadequate high interestrates to be paid by the Austrian entity to a foreign entity will have the followingconsequences:

(i) the profits/losses of the Austrian entity will be readjusted; and(ii) the interest payments will be deemed a hidden distribution of profits from the

Austrian entity.Inadequate low interest rates to be paid to the Austrian entity by a foreign entity will also bereadjusted (e.g. increasing profits/reducing losses of the Austrian entity).

5. CENTRAL BANK REPORTINGAre there central bank reporting obligations (balance of payments), bearing upon thecentralizing entity / each centralized entity / the banks?

We are not aware of any particular reporting obligations with regard to cash pooling schemesunder Austrian law. However, any entity (bank, financial institution) within the scope of theAustrian Banking Act has numerous reporting requirements. Further, other laws such as the

REGULATORY FRAMEWORK, LEGAL AND TAX CONSTRAINTSFOR CENTRALIZED CASH MANAGEMENT

20

Austria

Austrian Foreign Exchange Act (Devisengesetz) and the relating Reporting Regulation(Meldeverordnung) provide for certain obligations of banks, financial institutions and otherpersons to report to the Austrian Central Bank (Österreichischen Nationalbank) with regardsto matters involving foreign accounts and foreign exchange. Banks and financial institutionsare subject to comprehensive reporting requirements, such as reports on movements on theirforeign accounts and accounts of foreigners in Austria or the sale and purchase of any foreignexchange. Some reporting requirements concern persons which are neither banks nor financialinstitutions and might therefore also involve the centralizing entity or each centralized entityin the course of participation in a cash pooling system (such as specific reportingrequirements on foreign accounts, account balances, set-off of receivables and financialobligations, and collective money transfers to or via a paying agent).

6. EXCHANGE CONTROL REGULATIONSAre there any restrictions to the transfer of cash to foreign entities of the same group or theconversion of the local currency in other currencies?

The Austrian National Bank (Österreichische Nationalbank) is authorised to regulate, interalia, legal transactions concerning or acts disposing of foreign currency or (in case of non-Austrian entities) domestic currency in order to meet obligations arising from the Treaty onthe European Community or certain international obligations or in order to protect nationalor foreign interests. Current restrictions on money and capital flows concern measures againstterrorist organisations and groups and certain members thereof.Apart from these restrictions, we are not aware of any other restrictions to the transfer of cashto foreign entities or the conversion of local currency into other currencies.

7. ACCOUNTANCY OBLIGATIONS AND STANDARDSWhat if any are the specific accountancy obligations and standards for entities participating ina cash pooling arrangement?

We are not aware of any specific accountancy obligations and standards under Austrian lawfor entities participating in cash pooling arrangements. However, irrespective of any cashpooling arrangements entered into, the applicable general accountancy obligations andstandards will have to be met by each of the participating entities.

8. E-CASH POOLINGAre there data securitization aspects to be addressed regarding the relations between thecentralizing entity, the centralized entities and the banks?

Ideally, the extent of processing and transferring personal data in respect of the centralizingentity, the centralized entities and the banks should be agreed upon in the respective cashpooling agreement (i.e. each entity giving its consent to the processing of specified data fieldsand their transfer to specified entities). However, any processing and transferring of data

March 2009

Technical guides EACT

21

Austria

(other than specific sensitive data) required to fulfil the respective cash pooling arrangementwhich has been entered into by the cash pooling entity on the one side and the dataprocessing entity (i.e. the centralizing entity or bank as “data controller”) on the other sideshould generally qualify as permitted data processing under the applicable Austrian DataProtection Act 2000.Please note that the data security measures set forth under the Austrian Data Protection Act2000 (or the respective applicable laws of another EU-member state) have to be met not onlyby “data controllers” but also by any “data processors” (such as IT service providers) which actfor or on behalf of “data controllers”. Lastly, notification and/or permission requirements maybe applicable in respect of the processing and/or transfer of personal data.

9. FINANCIAL REPORTING, EVALUATION AND CONTROLAre there financial reporting, evaluation and control obligations associated with cash poolingarrangements?We are not aware of any specific financial reporting, evaluation or control obligations requiredunder Austrian law in relation to cash pooling arrangements. However, also in the light of therules on financial assistance described above, cash pooling arrangements should include a setof reporting obligations in order to enable effective monitoring of the financial situation ofeach of the participating entities.

REGULATORY FRAMEWORK, LEGAL AND TAX CONSTRAINTSFOR CENTRALIZED CASH MANAGEMENT

22

March 2009

Technical guides EACT

23

Belgium

REGULATORY, LEGAL AND TAX FRAMEWORK FOR INTERNATIONAL CASH MANAGEMENT

UNDER BELGIAN LAW

This contribution does not constitute legal advice. Its purpose is to give an overview of the laws andregulations that are applicable to cash management in Belgium. The principles set out below should beconsidered in relation to individual circumstances, with legal and tax counsel.

NautaDutilh

Terhulpsesteenweg 177/6 Chaussée de la Hulpe1170 Brussels - Belgium

[email protected] - T +32 2 566 80 00 - F +32 2 566 80 01

Benoit FeronRegulatory & Legal

Frédéric HeremansRegulatory & Legal

Benoit MalvauxTax

REGULATORY FRAMEWORK, LEGAL AND TAX CONSTRAINTSFOR CENTRALIZED CASH MANAGEMENT

24

Belgium

1. BANKING/FINANCIAL REGULATION

1.1 Banking authorities’ approval or exemption

1.1.1 ZBA cash pooling

Do loans/advances to other group entities require banking authorities’ approval for thecentralized entities or the centralizing entity? Is a distinction to be made between short-term,mid-term and long-term loans/advances?

The Act of 22 March 1993 on the legal status and supervision of credit institutions (the"Banking Act") sets forth (among other rules) the conditions governing the provision ofbanking services in Belgium by credit institutions governed by the laws of another EU MemberState (“EU credit institutions”). A credit institution is defined by Article 1 of the Banking Actas "any Belgian or foreign undertaking whose business is to receive deposits or otherrepayable funds from the public and to grant credit for its own account". Activities which onlyconsist in lending or cash management, but do not include the receipt of deposits or fundsfrom the public, are not as such subject to the approval to the Banking, Finance and InsuranceCommission (the "CBFA") or any prior notification in Belgium. In addition, Article 9 of the Royal Decree of 7 July 1999 on the public status of financialtransaction provides that a company which receives deposits and funds of affiliatedcompanies for its own purpose or for the purpose of these affiliated companies, is not deemedto receive deposits or other repayable funds from the public.Finally, cash management is defined as an accessory financial service by Article 46.2° of theAct of 6 April 1995 on secondary markets, on the legal status and supervision of investmentfirms (the “Investment Firm Act”). Article 45.3° of the Investment Firm Act, however, providesthat the Act is not applicable to companies which provide financial services exclusively to theirparent company, their subsidiaries or to subsidiaries of their parent company.

Do investments in financial instruments including derivative products carried out by thecentralizing entity on behalf of the centralized entities require banking authorities’ approval forthe centralized entities or the centralizing entity? Is an exemption available in groupcompanies?Pursuant to Article 45.3° of the Investment Firm Act, investments in financial instrumentscarried out by a centralizing entity on behalf of other group companies does not require anyprior approval.

In both cases, is there an exemption available for operations within groups of companies? Whatare the sanctions, if any, for breaching this requirement?

Exemption is indeed available (see above).

1.1.2 Notional pooling

Is there any prohibition/restriction on banks/participating entities implementing notionalpooling (i) by way of bank margins reductions, (ii) by way of merging current account balancesof the centralizing and centralized entities in order to create a single balance, or (iii) by way ofcalculating interest payable to each account based on merged scales of interest? Do banks

March 2009

Technical guides EACT

25

Belgium

require cross guarantees from participating entities? Can such guarantees be capped?

1. Restrictions on notional pooling:Belgian law does not impose any specific restrictions on the banks regarding the possiblemerger of current accounts or calculation of interest. Parties are free to determine the termsand conditions of the cash pooling (in accordance with Article 1134 of the Civil Code andsubject to the provisions generally applicable to all kind of credits). The CBFA however issued a Circular 97/9 dated 18 December 1997 regarding practices andmechanisms that may encourage tax fraud by third parties. This Circular identifies thepractice where members of a same group open several accounts with the same creditinstitution which function as one sole account for the purpose of calculating the interest ofthe accounts as a mechanism which may encourage tax fraud. The Circular provides that:

- the statement giving the breakdown of interest of these accounts must make a reference to the agreement existing at the group level;

- any statement regarding any sub-account must make a reference to the account to which it is linked; in addition, the annual account statement calculating the interest applicable on the account must contain the balance of all related accounts,

failing which the practice may be considered as contrary to the Banking Act.

2. Cross guarantees from participating entities:The banks usually require a cross guarantee from all participating entities to the cash pooling.As far as guarantees are granted by Belgian entities, these guarantees are usually capped inorder to comply with their corporate interest (see 2.3. below).

1.1.3 Centralized management of exchange rates and risks

Does the arrangement whereby a centralized entity agrees to buy from and sell to thecentralizing entity all its foreign currencies, require banking authorities’ approval or consent?

No, as long as the centralizing entity does not receive deposits or other repayable funds fromthe public and that the cash management arrangements are entered into between affiliatedcompanies (see 1.1.1. above).

1.1.4 Centralized management of payments and debt collections

Are the centralizing entity’s activities as the operator of a management of payments/collectiveprogram subject to approval requirements under any applicable banking regulatory laws?

No, as long as the centralizing entity does not receive deposits or other repayable funds fromthe public and that the cash management arrangements are entered into between affiliatedcompanies (see 1.1.1. above).

1.2 Banks duty of confidentiality

Can the centralizing entity obtain from banks holding the accounts of centralized entitiesinformation on such accounts?

The centralizing entity may be contractually authorized to obtain information about theaccounts of the centralized entities.

REGULATORY FRAMEWORK, LEGAL AND TAX CONSTRAINTSFOR CENTRALIZED CASH MANAGEMENT

26

Belgium

Can/must the banks disclose the account statements of centralized entities to the anti-moneylaundering agency?The Act of 11 January 1993 on the prevention of the use of the financial system for purposesof money laundering (the "Money laundering Act") provides for (i) identification obligationsfor various professionals of the financial sector, such as - among others - credit institutions,EU credit institutions operating in Belgium through a branch, investment companies orentities issuing or managing credit cards; (ii) disclosure obligations to the Financial IntelligenceProcessing Unit. In particular, the persons above must verify the identity of their clients by means of asupporting document at the time that they establish business relationship that will makethem regular clients. This same identification procedure is required when a client wishes toconduct a transaction involving EUR 10,000 or more, regardless of whether performed in asingle transaction or several seemingly related transactions. Identification is also requiredeven if the transaction involves less than EUR 10,000 whenever suspicion arises regarding thelaundering of money or the financing of terrorism.

Can/must a bank disclose account statements to the tax authorities? In general, any third party is obliged to provide the tax authorities, upon request, withinformation it avails about a taxpayer. However, tax authorities must respect the bank secrecyand may not request to disclose any account statements in view of taxing any of the banks'clients. Following a recent judgement of the Court of Cassation, the same applies to leasingcompanies.

1.3 Other regulatory requirements Are there specific requirements in regulated financial activities (e.g. insurance industry, assetmanagement etc.)? Is there a requirement that the global effective rate be stated in thecentralization agreement? Are there specific requirements in connection with the opening ofbank accounts (KYC, language…)?Cash management is defined as an accessory financial service by Article 46.2° of theInvestment Firm Act. However, Article 45.3° provides that the Act is not applicable tocompanies which provide financial services exclusively to their parent company, theirsubsidiaries or to subsidiaries of their parent company (see 1.1.1 above).In addition, the opening of a bank account is subject to the Money Laundering Act (see 1.2.above) which contains KYC requirements.

1.4 OutsourcingCan the cash pooling function be entrusted in whole or in part to an agent that is not a memberof the group? Belgian law does not prevent an entity which is not a member of the group from beingentrusted with the cash management of such group.However the outsourcing of the cash management to a person or an entity outside the groupmay lead to the application of the Banking Act and/or the Investment Firm Act (see 1.1.1.above), in which case such activity would have to be approved by the CBFA or require a priornotification in Belgium.

March 2009

Technical guides EACT

27

Belgium

2. CORPORATE LAW

2.1 Form of participating entities

Are there restrictions as regards the form of entities that can participate in cash poolingarrangements, either as a centralized or centralizing entities (certain forms of entities,groupings, partnerships…) and/or the form or the nationality of shareholders (state ownedentities, foreign shareholders…)?

Belgian law does not contain restrictions as regards the form or the nationality of the entities(or their shareholders) which participate in cash pooling arrangements.

2.2 Corporate purpose

Do the activities carried out in cash pooling arrangement need to be expressly contemplated inthe bylaws?

The articles of association of the centralizing company must provide that the company isentitled to carry out lending and cash management activities for affiliated companies.

Violation of the corporate purpose has different effects, depending on the form of the companyinvolved:

- For legal entities incorporated under the form of a SPRL//BVBA, SA/NV, SCA/CVA and SCRL/CVBA: Any transaction entered into by the competent organ of a company will bind the company even though such transaction exceeds the company's corporate purpose, unless the company proves that the third party was aware or could under the circumstancesnot have been unaware that the transaction exceeded the company's corporate purpose.Moreover, any transaction entered into in excess of the company’s corporate purpose couldengage the liability of the directors towards the company as well as towards third parties.

- For the other forms of legal entities: the company is not bound by the transaction entered into by its competent organ which exceeds its corporate purpose. In addition, the violation of the corporate purpose can be invoked by the third parties to refuse to perform the obligations under a transaction which violates the corporate purpose.

2.3 Corporate benefit

How is corporate benefit defined? Is it different when it relates to entities belonging to a samegroup? Are there restrictions on the participation of certain entities due to their financialstructure (ratios, etc.)? Is there an obligation to offer all participating entities equivalent termsand conditions?

Any transaction entered into by a Belgian company must be in the company’s corporateinterest. It is generally considered that the corporate interest prevails over the interest of thegroup to which the company belongs. However, respected legal authors also consider that theinterest of the group may justify sacrifices for the benefit of all the companies of the group.

Accordingly, a subsidiary can take part to an inter-company transaction provided that:

- this decision is not clearly detrimental to the corporate interest of the company; and

- the decision has some beneficial effects for the company, either directly or indirectly.

REGULATORY FRAMEWORK, LEGAL AND TAX CONSTRAINTSFOR CENTRALIZED CASH MANAGEMENT

28

Belgium

In assessing this rule and identifying the corporate benefit to the company, the board ofdirectors must take care that the agreements to which it is a party:- are dictated by a common economical, social or financial interest assessed on the basis of a

strategy elaborated for the benefit of the group;- are not entered into without any consideration and do not disrupt the balance between the

different undertakings of the group companies; and- do not exceed the financial means of the Belgian company (so that the existence of the

company would be jeopardised).

When considering the obligations of a subsidiary within a group, the Belgian Courts usuallyapply a reasonable proportionality test between the net assets of the subsidiary and theliabilities that the subsidiary assumes in favour of the third party. That assessment is to bemade reasonably at the time of execution of the agreements involved. It is therefore prudentto insure that the obligations that a Belgian company assumes in favour of other companies ofthe group are not manifestly contrary to their own interests and do not exceed their financialmeans. This may require that (i) the obligations of the Belgian company be capped (e.g. by wayof a target-balancing which limits the participation of an entity so as to allow it to keep somefunds available and to ensure its own development) and/or (ii) the cash pooling agreementdetermines the conditions under which each entity of the group may use the proceedsresulting from cash management.

Are there restrictions on the type of operations that the centralizing entity may undertake withthe cash of the centralized entities? Is there an obligation to offer the participating entitiesmarket financial conditions (i.e. the “arm’s length principle")?

Article 629 of the Company Code prevents any illegal financial assistance (loan, advance orsecurity interest) by a Belgian company for the acquisition of its shares by a third party. Anybreach of the financial assistance provision may induce the annulment of the relatedtransaction. In addition, a breach of that provision constitutes a criminal offence. The cash ofthe Belgian companies centralised by the centralizing entity should therefore not be used tosecure the acquisition of the shares of these entities. In addition, the transaction between the parties should be made at arm’s length.

What are the liabilities and sanctions in case of violation of the corporate benefit of aparticipating entity (cancellation of the agreement, management liability, extension ofbankruptcy proceedings etc.)? Do they apply to directors, officers and shareholders?

If a transaction entered into by a company is not in the company’s corporate interest, thecompany will nevertheless be bound by this transaction, unless it can be demonstrated thatthe third party was aware of that excess. In the latter case, the commitment of the companycould be declared void.Violation of the corporate interest may result in the liability of the directors and possibly, in thenullity of the transaction. However, by its very nature, the concept of corporate interest offersa broad discretion to the management of the Belgian company and does not permit to applymathematical measures insuring the validity of the obligations of that company. As aconsequence, the control of the corporate interest by the Court is only marginal and theviolation of the corporate interest should only be retained by the Court if the transaction ismanifestly contrary to the corporate interest of the company involved.

March 2009

Technical guides EACT

29

Belgium

2.4 Remuneration of the centralizing entityAre there any prescriptions as to the remuneration of the centralizing entity difference oflending/borrowing rates, lump sum fee…)?Belgian law does not contain any specific provisions. The centralizing entity should beremunerated for its services at arm’s length.

2.5 Investment of excess cash by the centralizing entityAre there prudential investment rules? Belgian law does not contain any specific provisions.

2.6 Approval of cash pooling arrangementDoes the cash pooling arrangement need to be approved by the management board /supervisory board or the shareholders? Under Belgian law, the cash pooling arrangement should be approved by the managementboard (unless otherwise stated in the articles of association of the company).As regards the representation of the company vis-à-vis third parties, most of the articles ofassociation of the Belgian company limited by shares (SA/NV) provide that the company isvalidly represented by two directors acting jointly. Such a provision is valid and anytransaction executed by two directors will bind the company.

2.7 Specific aspects relating to acquisition financing exitAre there restrictions on the use of cash of the target or the target’s subsidiaries to repay theacquisition loan? Does the existence of a cash pooling arrangement involving the target,modify the rules? The use of cash of the target to repay an acquisition loan is prohibited by Article 629 of theCompany Code (see 2.3. above). It is however generally considered that the financialassistance prohibition must be interpreted restrictively and therefore only prohibits: (i) anyfinancial assistance (loan or security interest); (ii) provided by the company involved; (iii) forthe acquisition of its own shares; (iv) by a third party. On the contrary, that provision shouldnot prevent the financial assistance by other companies of the same group (includingsubsidiaries).

2.8 TerminationDoes any company law restriction prevent the centralizing entity from exercising itscontractual right to terminate the agreement?Termination clauses are usually determined freely by the parties.

REGULATORY FRAMEWORK, LEGAL AND TAX CONSTRAINTSFOR CENTRALIZED CASH MANAGEMENT

30

Belgium

3. BANKRUPTCYWhat are the legal consequences of a participating entity being insolvent or nearly insolvent onthe operations involving the entity (ZBA and notional)? Would this limit the centralizingentity’s ability to exercise its contractual right to terminate the Agreement? A distinction must be made between the opening of (i) judicial composition betweencreditors and (ii) any other insolvency proceedings (including bankruptcy).Any termination claim in respect of the relevant agreement based solely on the opening of ajudicial composition between creditors will be held invalid. This will be the casenotwithstanding any provisions to the contrary in the relevant agreement. However, atermination claim brought by a party based on any other contractual ground (which arosebefore or after the opening of judicial composition proceedings) should be held valid. Conversely, a contractual term providing that the agreement will terminate upon the openingof a bankruptcy (or any insolvency proceedings other than the judicial composition betweencreditors) is valid.

Are there any risks that bankruptcy proceedings issued against the centralizing entity or acentralized entity could be extended to other participating group entities?Bankruptcy proceedings issued against the centralizing entity or a centralized entity will onlybe extended to another participating group entity if the conditions related to the bankruptcyproceedings are met.

4. TAX ISSUES

4.1 Value added tax (VAT)Are the operations between the centralizing entity and the centralized entities subject to VAT?If so, at what rate?Generally, cash management is a service for VAT purposes and thus subject to VAT.However, certain exemptions may apply, such as:- allocation and negotiation of credits, and the management of credits by the person

allocating the credits;- negotiation of guaranties, and management of guaranties on credits, accomplished by the

person allocating the credits;- certain activities, such as the negotiation concerning the deposits of cash, financial claims,

checks, with the exception of recovery of financial claims;- operations of payment, including the negotiation, with the exception of recovery of claims.These exemptions are in line with the European VAT Directive.To the extent that no exemption would be available, services are generally subject to the 21%rate.

March 2009

Technical guides EACT

31

Belgium

4.2 Taxation of interestAt what rate is the accrued interest, whether owed to or by the centralized entity, taxed? Isthere a different rate for fixed term loans and current account advances?Belgian source interest or interest received through a Belgian intermediary is generally subjectto a 15% interest withholding tax. There is no different rate for fixed term loans and currentaccount advances.However, several domestic exemptions may apply. Exemptions will mainly depend on thetype of beneficiary (non-resident, Belgian company, bank, etc.). The most relevant exemptionsin the context of cash management, and with respect to interest owed by the centralizingentity, are the following:

1. The X/N clearing exemption: this exemption applies only to fixed-income securities(bonds, commercial paper) that are held through the X/N clearing system operated by theNational Bank of Belgium and provided that the lender is eligible for an X (exempt) accountin that system. Generally speaking, only Belgian individuals or legal entities (other thancompanies) are not eligible for an X account. (They must hold a non-exempt or N account.)Certain formalities apply.

2. The foreign bank exemption: this exemption applies only to straight-forward loans, andprovided the lender is a foreign credit institution resident in the EU or in a country withwhich Belgium has concluded a bilateral tax treaty.

3. The "alternative" coordination centre exemption: this exemption applies to (inter alia)Belgian companies (i) that belong to a group of affiliated companies (within the meaningof the Code of Companies), (ii) that exercise their activities exclusively for the benefit ofthe companies of the group, (iii) that exclusively or predominantly render financial services,(iv) that seek financing exclusively with Belgian or foreign companies or legal entities withthe sole purpose of financing their own or the affiliated companies' transactions, and (v)which do not own stock the acquisition value of which exceeds 10% of their fiscal netvalue. The exemption applies to both straight-forward loans as bonds or CP, and providedthe lender is a non-resident. Certain formalities apply.

4. The registered bond exemption: this exemption applies only to registered bonds andprovided the lender is a non-resident. Specific conditions apply, such as the non-transferability between interest payment dates. Certain formalities apply.

5. The intra-group exemption: this exemption applies to both straight-forward loans as bondsand provided the lender is an EU-resident affiliated company. Certain formalities apply.

To the extent that interest is due by a Belgian resident company or intermediary, interestowed to the centralizing entity is generally exempt.Aside from the domestic exemptions (inclusive of the implementations of EU Directives),treaty exemptions may apply.

REGULATORY FRAMEWORK, LEGAL AND TAX CONSTRAINTSFOR CENTRALIZED CASH MANAGEMENT

32

Belgium

Is there a withholding tax on interest paid to a foreign entity? What is the applicable rate inrelation to the following countries?The below chart does not take into account the exemptions that may apply pursuant todomestic law (see above), but is limited to the treaty rates.

4.3 Stamp duty

Do cash pooling operations raise any stamp duty?

No stamp taxes should be due pursuant to cash pooling operations. Nominal stamp taxesmay be due pursuant to credit agreements concluded with credit institutions.

4.4 Deductibility of interest

Are there limitations to the deductibility of interest paid by the centralized or the centralizingentity (such as a thin capitalization rule - debt / equity capital ratio)?

There are various limitations to the deductibility of interest.

1. Non-arm's length interestInterest paid at non-arm's length terms is not deductible. Such interest may even berecharacterized into dividends, if payment is made to an individual shareholder or a corporate

Aus

tria

Belg

ium

Braz

il

Can

ada

Chi

na

Cze

ch R

epub

lic

Dub

ai

Engl

and

Ger

man

y

Hon

g Ko

ng

Hun

gary

Indi

a

Irela

nd

Ital

y

Japa

n

AffiliatedCompanies

in

Withholdingtax rate 15% N/A 10

1

/15% 10% 10% 02

/10% No treaty 15% 04

/15% 03

/10% 03

/15% 101

/15% 15% 15% 10%

Luxe

mbu

rg

Mex

ico

Net

herla

nds

Pola

nd

Port

ugal

Russ

ia

Sing

apor

e

Slov

akia

Sout

h Af

rica

Spai

n

Switz

erla

nd

Taiw

an

Turk

ey

USA

AffiliatedCompanies

in

Withholdingtax rate 0

5

/15% 101

/15% 05

/10% 01

/5% 15% 01

/10% 10% 03

/10% 02

/10% 03

/10% 01

/10% 10% 15% 0%

Notes: 1. banks, etc2. banks, bank deposits, etc.3. current accounts, interbank payments4. unaffiliated enterprises, etc.5. company, bank, etc.

March 2009

Technical guides EACT

33

Belgium

shareholder holding a director or liquidator mandate in the paying entity. The measure doesnot apply with respect to interest on publicly issued bonds or loans from Belgian companies.

Non-arm's length interest may further be added to the taxable basis of the company (i.e., inaddition to the non-deductibility), if such interest is paid to a foreign affiliated or lowly taxedindividual / company (or establishment), or to a foreign individual / company sharing acommon interest with an aforementioned individual or company.