Determinants of firm survival: a duration analysis using the generalized gamma distribution

18

ORIGINAL PAPER Determinants of firm survival: a duration analysis using the generalized gamma distribution Serguei Kaniovski Michael Peneder Published online: 26 October 2007 Ó Springer Science+Business Media, LLC 2007 Abstract We use parametric duration analysis to study the survival of Austrian firms. We find that hazard rates in both manufacturing and services initially increase, reach a peak after the first year of operation and then decrease with age. The max- imum hazard rate is higher in services. We also find differences in hazard rates among different types of manufacturing industries distinguished by the nature of their sunk costs, their reliance on human resources and inputs from external services. Finally, we find that larger initial size and higher market growth, and at the same time lower net entry and declining market concentration prolong the life of an entrant. Keywords Firm survival Duration analysis Sectoral taxonomies JEL Classifications L25 L11 C41 1 Introduction The availability of administrative data on the full populations of business units has spurred on a large body of research on the patterns and determinants of their entry and performance. It has also enabled the use of statistical techniques that cannot be applied to aggregate data. A prominent line of research within this literature uses regression analysis to study the determinants of the duration of firms. This research has yielded a number of valuable insights on aspects of competition that shape the process of growth and renewal in industries. Unfortunately, no comparable studies S. Kaniovski (&) M. Peneder Austrian Institute of Economic Research (WIFO), Vienna, P.O. Box 91, Vienna 1103, Austria e-mail: [email protected] M. Peneder e-mail: [email protected] 123 Empirica (2008) 35:41–58 DOI 10.1007/s10663-007-9050-3

Transcript of Determinants of firm survival: a duration analysis using the generalized gamma distribution

ORI GIN AL PA PER

Determinants of firm survival: a duration analysis usingthe generalized gamma distribution

Serguei Kaniovski Æ Michael Peneder

Published online: 26 October 2007

� Springer Science+Business Media, LLC 2007

Abstract We use parametric duration analysis to study the survival of Austrian

firms. We find that hazard rates in both manufacturing and services initially increase,

reach a peak after the first year of operation and then decrease with age. The max-

imum hazard rate is higher in services. We also find differences in hazard rates

among different types of manufacturing industries distinguished by the nature of

their sunk costs, their reliance on human resources and inputs from external services.

Finally, we find that larger initial size and higher market growth, and at the same time

lower net entry and declining market concentration prolong the life of an entrant.

Keywords Firm survival � Duration analysis � Sectoral taxonomies

JEL Classifications L25 � L11 � C41

1 Introduction

The availability of administrative data on the full populations of business units has

spurred on a large body of research on the patterns and determinants of their entry

and performance. It has also enabled the use of statistical techniques that cannot be

applied to aggregate data. A prominent line of research within this literature uses

regression analysis to study the determinants of the duration of firms. This research

has yielded a number of valuable insights on aspects of competition that shape the

process of growth and renewal in industries. Unfortunately, no comparable studies

S. Kaniovski (&) � M. Peneder

Austrian Institute of Economic Research (WIFO), Vienna,

P.O. Box 91, Vienna 1103, Austria

e-mail: [email protected]

M. Peneder

e-mail: [email protected]

123

Empirica (2008) 35:41–58

DOI 10.1007/s10663-007-9050-3

have been carried out for Austria so far. This paper fills this gap by providing an

empirical analysis of the patterns and determinants of firm survival in Austria. In

our analysis we focus on the impact of the market structure and demographic

characteristics of an industry on survival. In terms of statistical technique our focus

lies on modelling the age dependency of survival rates––thus our choice of a

parametric rather than a non-parametric or a semi-parametric approach.

The literature on firm survival has produced several robust empirical regularities,

or ‘stylized facts.’1 Some of these empirical regularities concern the effect of firm-

specific characteristics such as the firm’s age and size on the survival of firms, while

most of them record the effect of market structure. The gist of this literature, as

succinctly put by Geroski (1995, p. 435), is that ‘entry appears to be relatively easy,

but survival is not.’ This conclusion is based on a large number of entrants coupled

with a short average duration typically observed in most industries. Our analysis

shows this to be especially true for the service industry.

Another robust empirical regularity is that most entrants start small and end

small. Nonetheless, an entrant’s initial size seems to have a positive effect on its

duration.2 This has been reported many times, starting from the early studies for US

manufacturing establishments by Evans (1987) and Dunne et al (1988). More

general is the finding that the probability of exit declines with current size and age.

There may be several reasons why young and small firms are exposed to a higher

risk of exit. For one, older and larger firms often harness more resources (capital and

human) and more managerial experience (tacit knowledge). Such firms can better

withstand external shocks, for example those emanating from demand or the stock

market. Second, older and larger firms will typically have more market power and

endurance. In many product markets a larger size confers more influence on the

market price, while endurance often derives from long-established market niches

and brands that insulate the firm’s own market segment by reducing its sensitivity to

the competitive challenge. Older and larger firms are also more likely to be

diversified and therefore less susceptible to fluctuations in demand.

A key parameter in the duration analysis of firms is the firm’s age measured from

its date of entry. It is a well-established fact that the probability of exit falls with

age. In the terminology of organizational ecology, new firms suffer from the liability

of newness (Freeman et al. 1983). Beyond this, the existing empirical evidence is

not entirely conclusive, as both strictly decreasing and non-monotonic hazard rates

are found. Decreasing hazard rates have been reported for US manufacturing

establishments by Evans (1987), Dunne et al. (1988), Audretsch (1991) and

Audretsch and Mahmood (1995); for Canadian manufacturing establishments by

Baldwin and Gorecki (1991); for Portuguese manufacturing firms by Mata and

Portugal (1994) and Mata et al. (1995). In duration regression the effect of age can

1 Surveys of the literature on the mobility of firms, of which the literature on firm survival is a permanent

strand, include Siegfried and Evans (1994), Geroski (1995), Sutton (1997) and Caves (1998). Of related

interest is the sociological literature on organizational ecology exemplified by Hannan and Carroll (1992)

and Carroll and Hannan (2000).2 In the framework of empirical duration analysis, the positive effect of an explanatory variable

on duration derives from its negative effect on the probability of exit. We will return to this point

in Sect. 3.2.

42 Empirica (2008) 35:41–58

123

be tested using a suitably parameterized hazard function. Roughly speaking, the

hazard function gives the probability of exit in the next time period. It is a function

of time elapsed since entry and hence that of age. To test the curvature of a hazard

function, earlier studies often used the Weibull model, which can only describe

monotonic hazard rates (Baldwin and Gorecki 1991, Mata and Portugal 1994).

More recent studies have tested several models, including those allowing for

non-monotonic hazard functions. In a study of small German manufacturing

establishments, Wagner (1994, p. 141) finds ‘hazard rates tend to increase during

the first years and to decrease afterwards.’ Agarwal et al. (2002) find inverted

U-shaped hazard rates using data on US manufacturing firms. In a study of the

impact of innovation activities on firm survival in the Dutch manufacturing

industry, Cefis and Marsili (2005) also report inverted U-shaped hazard functions.

To us, the absence of definitive results on the shape of the hazard function appears

to derive, at least in part, from the different parametric survival regression models

used to estimate them. Our findings point toward the varying degree of coverage of

small and large firms as another likely source of differences.

What difference does it make? For one, non-monotonic hazard rates are

consistent with the standard stochastic models of industry dynamics by Jovanovic

(1982) and Ericson and Pakes (1995). In these models entrants only learn their

relative efficiency with passage of time. If industries indeed differ in the time it

takes for an entrant to learn its competitiveness, then such differences should be

reflected in hazard rates. A still simpler explanation for non-monotonic hazard rates

alludes to the fact that an entrant will need some time to burn its initial capital

endowment, which is another reason to control for the effect of entry size when

estimating hazard functions. Beyond theoretical concerns, the knowledge of when

the firms become subject to the maximum risk of exit is useful in framing

consultancy and crediting programs for small and medium enterprises.

We estimate a parametric survival regression with a hazard function derived from

the generalized gamma distribution. This highly flexible functional form allows for

a large number of possible shapes of the hazard function. Special cases of the

generalized gamma distribution include the exponential (constant hazard), Weibull

(monotonically increasing or decreasing hazard) and log-normal (skewed inverted

U-shape, non-monotonic hazard) distributions. Ours is not the only distributional

choice that accommodates non-monotonic hazard functions. Such functions can also

be described using much simpler log-logistic and Gompertz–Makeham distribu-

tions. The main advantage of the family of gamma distributions lies in the variety of

functional forms nested in one general specification. One can thus discriminate

between them using the Likelihood-ratio and Wald tests. The main disadvantage is

the computational intensity of the maximum likelihood estimation.

Following this introduction we describe the dataset obtained using the Austrian

social security files. Section 3 then defines the explanatory variables and

generalized gamma regression. The explanatory variables include three taxonomies

of manufacturing industries designed to capture an industry’s general reliance on

tangible and intangible investment, human resources and inputs from external

services. Section 4 discusses the estimation results. Section 5 summarizes and

concludes.

Empirica (2008) 35:41–58 43

123

Briefly anticipating our results, we find that hazard rates first increase and then

decrease with age. This is true both for manufacturing and services, although firms

in the service sector are subject to a higher maximum hazard rate. We also find

differences in maximum hazard rates among the types of manufacturing industries

described by three sectoral taxonomies. These findings point to the importance of

sunk costs and the human resource dimension on survival rates, and in general to the

intensity of competition. Finally, we find that entry size, market growth, market

concentration, net entry and the vintage index––a rough proxy for the industry life-

cycle––have their predicted effects on the duration of firms.

2 Data

Our analysis is based on data from the Austrian social security files. The parent

administrative dataset covers all employers with one or more employees in all

sectors of the economy between 1975 and 2004, with less than complete coverage in

the years from 1972 to 1975. We use the employers’ records to construct a dataset of

business units. The main advantage of this dataset when compared to others

available for Austria lies in its comprehensiveness. It covers about one million

business units, seventy percent of which are assigned to a 6-digit NACE industry.

Of these, only 10% operate in manufacturing, while 61% operate in market services.

Despite having the largest output and employment share, the service sector is still

underrepresented in most of the datasets studied in the literature. The remaining

29% operate in the primary sector, utilities, or non-market services.3

Our dataset covers 29 years of daily operation, making it especially well-suited

for the study of firm duration. Measuring the duration in days as opposed to years

allows for a precise analysis of the effect of age on duration. The longer the time

period covered, the lower is the share of truncated durations that occur when either

the entry or the exit date is unobserved. It is this comprehensiveness and time

coverage that makes these data so appealing for the duration analysis. However, as

is common for administrative employment data in other countries, the comprehen-

siveness comes at the cost of scarce information on other characteristics of the

business unit such as productivity, financial performance, type of ownership and

relations to other business units.4 With only a few firm-specific variables available,

we focus on the impact of market structure and the demographic characteristics of

the industry on firm survival.

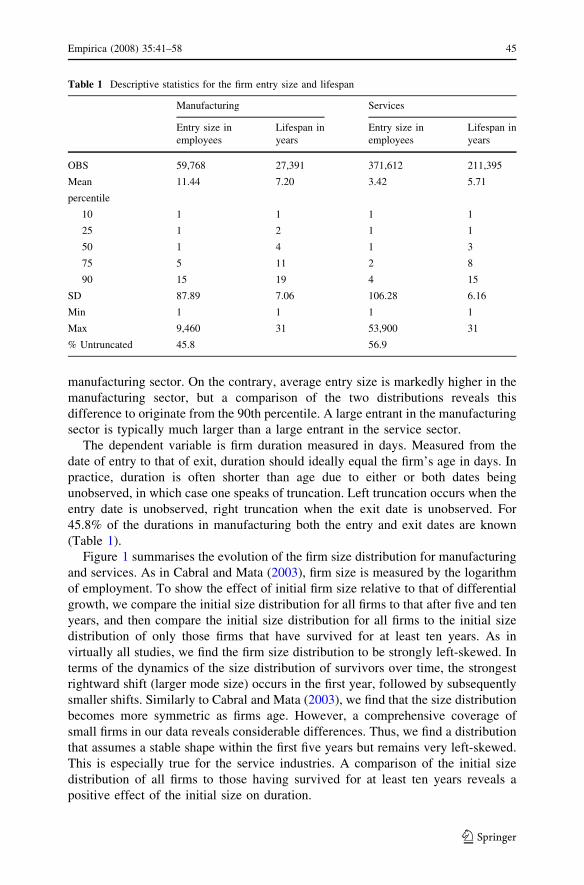

Table 1 shows that more than one half of all entrants in the manufacturing and

service sectors have only one employee. The median entry size and the median

lifespan or duration of manufacturing firms is only slightly higher than that of

service firms, which is surprising given the typically higher start up costs in the

3 We exclude these for various reasons. Competition in the farming industry is largely shaped by its

unique regulatory environment. Data on mining and utilities are sparse, while non-market services mostly

belong to the public sector.4 Stiglbauer (2003) argues that, due to the economies of scale in administrative reporting, the bulk of the

data can be found on the level of enterprises, not establishments. Clearly, this uncertainty is negligible for

small firms.

44 Empirica (2008) 35:41–58

123

manufacturing sector. On the contrary, average entry size is markedly higher in the

manufacturing sector, but a comparison of the two distributions reveals this

difference to originate from the 90th percentile. A large entrant in the manufacturing

sector is typically much larger than a large entrant in the service sector.

The dependent variable is firm duration measured in days. Measured from the

date of entry to that of exit, duration should ideally equal the firm’s age in days. In

practice, duration is often shorter than age due to either or both dates being

unobserved, in which case one speaks of truncation. Left truncation occurs when the

entry date is unobserved, right truncation when the exit date is unobserved. For

45.8% of the durations in manufacturing both the entry and exit dates are known

(Table 1).

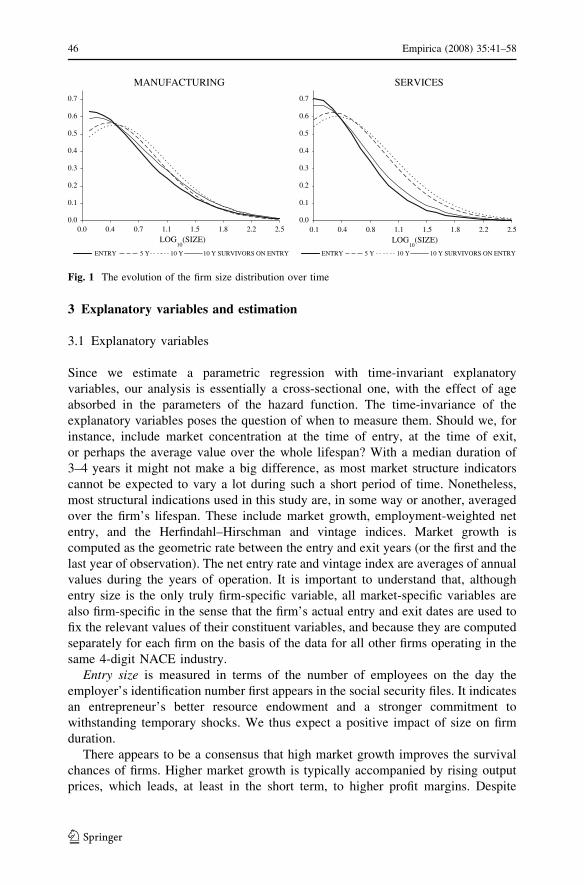

Figure 1 summarises the evolution of the firm size distribution for manufacturing

and services. As in Cabral and Mata (2003), firm size is measured by the logarithm

of employment. To show the effect of initial firm size relative to that of differential

growth, we compare the initial size distribution for all firms to that after five and ten

years, and then compare the initial size distribution for all firms to the initial size

distribution of only those firms that have survived for at least ten years. As in

virtually all studies, we find the firm size distribution to be strongly left-skewed. In

terms of the dynamics of the size distribution of survivors over time, the strongest

rightward shift (larger mode size) occurs in the first year, followed by subsequently

smaller shifts. Similarly to Cabral and Mata (2003), we find that the size distribution

becomes more symmetric as firms age. However, a comprehensive coverage of

small firms in our data reveals considerable differences. Thus, we find a distribution

that assumes a stable shape within the first five years but remains very left-skewed.

This is especially true for the service industries. A comparison of the initial size

distribution of all firms to those having survived for at least ten years reveals a

positive effect of the initial size on duration.

Table 1 Descriptive statistics for the firm entry size and lifespan

Manufacturing Services

Entry size in

employees

Lifespan in

years

Entry size in

employees

Lifespan in

years

OBS 59,768 27,391 371,612 211,395

Mean

percentile

11.44 7.20 3.42 5.71

10 1 1 1 1

25 1 2 1 1

50 1 4 1 3

75 5 11 2 8

90 15 19 4 15

SD 87.89 7.06 106.28 6.16

Min 1 1 1 1

Max 9,460 31 53,900 31

% Untruncated 45.8 56.9

Empirica (2008) 35:41–58 45

123

3 Explanatory variables and estimation

3.1 Explanatory variables

Since we estimate a parametric regression with time-invariant explanatory

variables, our analysis is essentially a cross-sectional one, with the effect of age

absorbed in the parameters of the hazard function. The time-invariance of the

explanatory variables poses the question of when to measure them. Should we, for

instance, include market concentration at the time of entry, at the time of exit,

or perhaps the average value over the whole lifespan? With a median duration of

3–4 years it might not make a big difference, as most market structure indicators

cannot be expected to vary a lot during such a short period of time. Nonetheless,

most structural indications used in this study are, in some way or another, averaged

over the firm’s lifespan. These include market growth, employment-weighted net

entry, and the Herfindahl–Hirschman and vintage indices. Market growth is

computed as the geometric rate between the entry and exit years (or the first and the

last year of observation). The net entry rate and vintage index are averages of annual

values during the years of operation. It is important to understand that, although

entry size is the only truly firm-specific variable, all market-specific variables are

also firm-specific in the sense that the firm’s actual entry and exit dates are used to

fix the relevant values of their constituent variables, and because they are computed

separately for each firm on the basis of the data for all other firms operating in the

same 4-digit NACE industry.

Entry size is measured in terms of the number of employees on the day the

employer’s identification number first appears in the social security files. It indicates

an entrepreneur’s better resource endowment and a stronger commitment to

withstanding temporary shocks. We thus expect a positive impact of size on firm

duration.

There appears to be a consensus that high market growth improves the survival

chances of firms. Higher market growth is typically accompanied by rising output

prices, which leads, at least in the short term, to higher profit margins. Despite

MANUFACTURING SERVICES

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.1 0.4 0.8 1.1 1.5 1.8

LOG10

(SIZE)2.2 2.5

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.0 0.4 0.7 1.1 1.5 1.8

LOG10

(SIZE)2.2 2.5

ENTRY 5 Y 10 Y 10 Y SURVIVORS ON ENTRYENTRY 5 Y 10 Y 10 Y SURVIVORS ON ENTRY

Fig. 1 The evolution of the firm size distribution over time

46 Empirica (2008) 35:41–58

123

market growth signifying an opportunity, the prospects of a single firm depend on

how many competitors it has. For an analysis of firm survival, one should therefore

take into account whether market expansion comes in the form of internal or

external growth. By separating the employment growth of an average firm from the

net entry rate, we identify a market growth component that is independent of

changes in the total number of firms. We thus aim to separate the general growth

prospects of a firm in an industry from the impact of changes in the number of its

potential rivals emanating from the influx of entrants to and the outflow of

incumbents from that same industry.

Our first measure of market growth is a geometrically computed growth rate of

the average number of employees per firm. Denote by E the ratio of total

employment of a NACE 4-digit industry to the total number of firms operating in

that industry. Then,

GROWTH ¼ffiffiffiffiffi

Ex

Ee

l�1

r

� 1: ð1Þ

The subscript x denotes the value in the firm’s year of exit (or the last year of

observation if the exit date is unobserved), and e denotes the value in the firm’s year

of entry (or the first year of observation if the entry date is unobserved). Finally, ldenotes the number of years of operation. It is well-known that small firms

experience higher average growth rates than large firms, thereby violating Gibrat’s

law of proportional effects (Sutton 1997). Beyond that, we expect this variable to

positively correlate with firm duration, reflecting the general opportunities prevalent

in the market.

The second measure relating to market growth is the employment weighted netentry of firms, defined as

NET ENTRY ¼ Le � Lx

L; ð2Þ

where Le – Lx is the net inflow of employment due to entry and exit in a given sector

and year, and L is the total employment in that sector. In our regression we include

the mean of L over the firm’s lifespan. Since our first measure of average firm

growth already controls for the opportunities an expanding market offers to

individual firms, a higher net entry reflects the increasing competition due to a

growing firm population.5

The Herfindahl–Hirschman index of market concentration, HHI, is computed using

the firm’s share in total employment of a NACE 4-digit industry. The index takes

values between the reciprocal of the number of firms operating in the sector and one,

with the value of one corresponding to the maximum concentration. In the regression

we include the difference between index values recorded over the lifespan

DHHI ¼ HHIx � HHIe ¼X

i

s2ix �

X

i

s2ie: ð3Þ

5 At the same time, net entry can proxy opportunities perceived by entrants (Peneder 2007).

Empirica (2008) 35:41–58 47

123

The sums are over the squares of the market shares of all firms in the 4-digit industry.

The change in market concentration is expected to have a negative effect on duration.

Agarwal and Audretsch (2001) and Agarwal et al. (2002) link the patterns of firm

duration to the industry life cycle hypothesis.6 The latter uncover differences in the

pattern of firm survival between the growth and the maturity phases. The growth

phase is characterized by low but rising mortality rates coupled with a moderate

liability of smallness but no liability of newness. Mature industries are characterized

by high but constant or falling mortality rates, and a stronger liability of newness.

Although quite long, the time-span of our data does not allow us to directly test

the effects of an industry life cycle. Instead we rely on the industrial vintage indexas a proxy (Desai et al. 2003). The index reflects the relative weight of young firms

in the overall population and is defined as the employment weighted average age

distribution of firms in an industry:

VINTAGE ¼X

i

LiAGEi

L: ð4Þ

The index is a weighted sum of the employment shares of all firms in a given

sector and year, with the firm’s age serving as the weights. A high vintage means

that a large portion of the overall productive capacity is employed in older

companies––a sign of a mature industry. Conversely, a low vintage characterises

‘entrepreneurial’ industries, where the predominance of younger firms indicates

either an early stage of a life cycle, or a competitive regime with a sustained

‘rejuvenation’ of the firm population through the displacement of incumbents by

new entrants (‘creative destruction’).

The theoretical literature recognizes the role of sunk costs as a barrier to both

entry and exit (Dixit 1989; Sutton 1991; Sutton 1998; Amir and Lambson 2003).

Sunk costs also consist of fixed investments in tangible and intangible assets, such

as superior technology or high reputation. These investments are sunk because most

if not all of their economic value will be lost on exit. As a barrier to exit, they also

discourage entry by dampening the expected post-entry profits due to aggressive

pricing by incumbents. Typical direct measures of sunk costs include industry’s

capital, R&D and advertising expenditures.

The turnover rate, measured as the sum of entry and exits divided by the total

number of firms, is an alternative indirect proxy that can be directly derived from data

on firm demography. The rationale is that higher sunk costs cause entry and exit rates

to fall, which by definition implies lower rates of firm turnover. In a study of entry and

exit in Austrian industries, Holzl (2005) confirms the negative effect of tangible and

intangible sunk costs on the level and volatility of firm turnover. Peneder (2007) uses

the turnover rate as a proxy for the ‘cost of experimentation’, that is, sunk costs, in a

sectoral study of firm demography in the OECD countries. In this study, we use the

turnover rate as a proxy for sunk costs in our basic specification.

6 This hypothesis takes a bird’s eye view of the evolution of industries by identifying several stages of

development, starting with an embryonic industry environment, to a growing industry followed by

eventual shakeout (a mass exit), maturity and decline (Klepper 1996).

48 Empirica (2008) 35:41–58

123

Sunk costs are notoriously difficult to measure empirically, and firm turnover is a

distant proxy. In an alternative specification we apply three distinct taxonomies ofmanufacturing industries that were explicitly designed to capture an industry’s

general reliance on intangible investments, human resources and inputs from

external services as distinct sources of competitive advantage. In addition to the

discrimination of industries according to the extent and nature of sunk costs, the

three taxonomies also capture broad patterns of competitive strategies typically

pursued in these industries (Kaniovski and Peneder 2002).

Taxonomy I is specifically designed to differentiate industries according to factor

intensities and the distinct nature of various sunk costs stemming from R&D,

advertising or gross fixed capital formation. In addition to this, Taxonomies II and

III are used to distinguish manufacturing industries according to their reliance on

human resources and inputs from external services. All three taxonomies were

developed using statistical cluster analysis––a technique specifically designed for

classifying observations on behalf of their relative similarities with respect to a

multidimensional array of variables. The basic idea is that of dividing a body of data

into subsets having a maximum homogeneity within and a maximum heterogeneity

between them, the result being a complete categorisation of 98 NACE 3-digit

manufacturing industries into mutually exhaustive types for each of the three

taxonomies (Table 2). Detailed information on the taxonomies, data sources and

methodology of industry classification is presented in Peneder (2001 and 2005).

3.2 The generalized gamma regression

In this section we briefly review the parametric duration regression.7 A duration

model seeks to explain the average probability of exit per unit time period, given

Table 2 The WIFO taxonomies of the manufacturing industry

Taxonomy I: Factor input combinations

MM: Mainstream manufacturing MDI: Marketing driven industries

LI: Labour intensive industries TDI: Technology driven industries

CT: Capital intensive industries

Taxonomy II: Skill requirements

LS: Low-skill industries MWC: Medium-skill white-collar industries

MBC: Medium-skill blue-collar industries HS: High-skill industries

Taxonomy III: External service inputs

O: Other industries IR&S: Industries with high inputs from retail

and advertising services

ITRS: Industries with high inputs from

transport services

IKBS: Industries with high inputs from

information- and knowledge-based services

Source: Peneder (2001)

7 Our discussion draws heavily on the exposition by Lancaster (1990). Other references on duration

models include Kalbfleisch and Prentice (1980), Cox and Oakes (1984), Le (1997), and Cleves et al.

(2004).

Empirica (2008) 35:41–58 49

123

that the firm has survived until time T. This probability is formally defined by the

hazard function over a short time interval of length dt after t as

hðtÞ ¼ limdt!0

Pðt� T � t þ dtjT � tÞdt

: ð5Þ

Roughly speaking, the hazard function gives the instantaneous probability of exit

in the next time period, given that the firm has survived until then (i.e., in the event

T ‡ t). The hazard function is usually expressed in terms of the probability

distribution F and the density function f = F0 of the firm’s duration as

hðtÞ ¼ limdt!0

Fðt þ dtÞ � FðtÞdt

� 1

1� FðtÞ ¼f ðtÞ

1� FðtÞ : ð6Þ

Different functional forms of the relationships between the instantaneous

probability of exit and duration can be modelled by choosing a suitable functional

form for F. This is the essence of the parametric approach to the analysis of

durations. The parametric approach has two advantages. First, specifying the

functional form of F helps us to adequately deal with truncated durations and,

second, choosing a suitably flexible functional form of F allows us to test a variety

of shapes of the hazard function, leading to possibly distinct models of the age

dependency.

The generalized gamma distribution is a highly flexible functional form that

allows for a large number of possible shapes of the hazard function. The exponential

(constant hazard), Weibull (monotonically increasing or decreasing hazard) and log-

normal (skewed inverted U-shape, non-monotonic hazard) distributions are all

special cases of the generalized gamma distribution. It is a three-parameter

distribution with a probability density function

f ðtÞ ¼akamtam�1e�kata

CðmÞ t [ 0

0 t� 0

�

a [ 0; m [ 0; k [ 0: ð7aÞ

The corresponding hazard function cannot be written in closed form, as Finvolves an incomplete gamma integral

CðmÞ ¼Z

1

0

xm�1e�xdx; m [ 0: ð7bÞ

Parameters a and m define the shape of the function, while k is a scale parameter.

Depending on the values of a and m, the hazard function can assume linear,

monotonically increasing or decreasing, or, in the case am [ 1 and a \ 1, non-

monotonic inverted U-shaped forms. For m = 1 it reduces to the probability density

function of the Weibull distribution; for m = a = 1 to the exponential density. Using

a parameterization, it can be shown to yield the log-normal distribution as m ? ?.

In this parameterization, the tested parameter assumes the value of zero under the

null-hypothesis leading to the log-normal model. The log-normal model implies an

inverted U-shaped hazard function.

50 Empirica (2008) 35:41–58

123

We have estimated an accelerated life regression. Without censoring or

truncation, the regression model can be written as8

log T ¼ X0bþ e: ð8Þ

Here X is the matrix of explanatory variables, b the vector of coefficients to be

estimated and e a random variable with a distribution independent of X or b. Vector

b contains the effect of changes in the explanatory variables on the expected

logarithmic duration. If exp(–xibx) [ 1, then an increase in the ith variable

shortens the expected logarithmic duration, whereas it has the opposite effect if

exp(–xibx) \ 1. The distribution of e is defined by the choice of the parametric

model. For example, in the generalized gamma model e is distributed as a positive

power of a standard gamma variate, whose density function is given by (7a), while

choosing the log-normal distribution for e would lead to a normally distributed error

term. In any case, ei’s are i.i.d. with unknown variance and known distributional

form. The expected lifetime given by e’s distribution is accelerated in the former

case and decelerated in the latter, hence the name of the regression model.

Several remarks are in order before we proceed with the estimation of the above

specification. First, the above regression model is essentially a cross-sectional

model. The explanatory variables are time-invariant. This raises the question of the

time period at which to measure them. How we deal with this issue is discussed in

Sect. 3.1. Second, the model is homoscedastic. In particular, the hazard function

obtained by estimation implies that in 1975 a five-year-old firm was subject to the

same probability of exit as was a five-year-old firm in 1995, or in any other year.

Hazard rates depend on duration, not entry date. Third, we would like to use the

dummy variables indicating membership in the types of industries distinguished by

the taxonomies. The inclusion of a dummy variable changes the estimates for the

coefficients and the parameters of the hazard function, but is unlikely to change the

functional form of the hazard function. A complete test would involve attaching

indicator variables to every parameter of the hazard function. Such a test would be

extremely computationally intensive given the size of the dataset and the number of

estimated parameters. Despite its flexibility, the generalized gamma model cannot

produce bimodal hazard functions, such as the ‘bathtub’ that describes the lifespan

of a human (higher mortality in infancy and near certain death upon reaching high

age). Thus, the model can be used to test either the liability of newness or the

liability of the age hypothesis, but not both. While we find strong support for the

first hypothesis, we surmise that data of even longer duration is required to

adequately test the second hypothesis.

4 Results

Our basic specification includes the five variables defined in Sect. 3.1, without the

dummy variables indicating different types of industries as discriminated by the

8 For a discussion of censoring and truncation in parametric models see, for example, chapter 4 in Cleves

et al. (2004).

Empirica (2008) 35:41–58 51

123

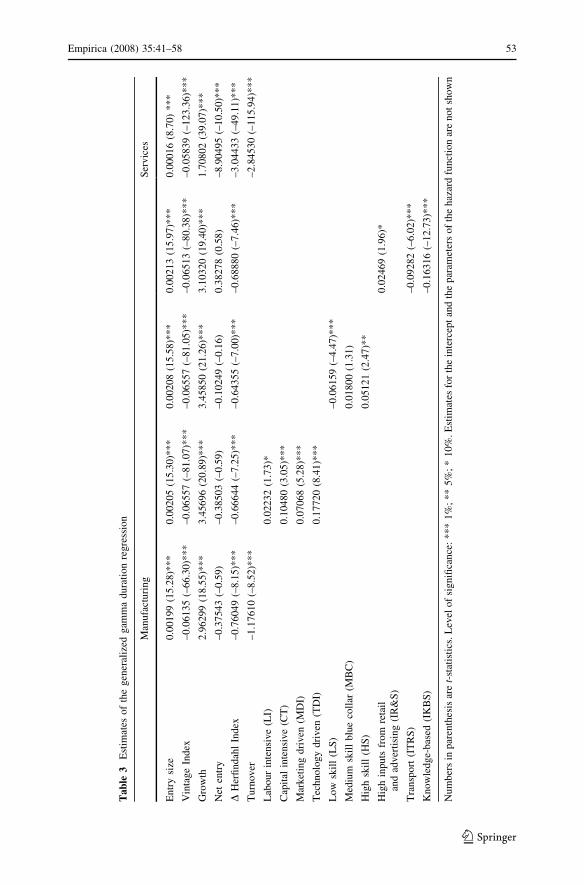

taxonomies. To reduce the computational burden and to highlight the differences

between manufacturing and market services, we have estimated this specification

separately for NACE industries 15 to 37 and NACE industries 50–74. The estimates

for the basic specification are shown in the second and sixth columns of Table 3,

which reports the non-exponentiated coefficient vector b. The positive sign on a

coefficient signifies a duration-prolonging effect of the respective variable.

Large initial size, measured in terms of the total number of employees, prolongs

the entrant’s life in both manufacturing and market services. Its influence is

somewhat higher in manufacturing, arguably because of the higher initial labour and

capital endowments required to start a manufacturing business. On average, firms

that start with more employees also have higher initial capital endowments, which

may serve as an indicator of their ability to withstand external shocks. However, in

our case this finding must be interpreted with caution, as large entry size could be

related to the establishment of a subsidiary of an already existing large enterprise––

a possibility we cannot exclude in our data.

We use industrial vintage as a crude control for the phase of the industry life-

cycle. The higher the share of old and large firms in the sector’s total

employment, the higher is the vintage index. High values of the index signify

mature industries and have a significant negative impact on firm duration. To

compete with older (presumably more experienced) firms in the same industry

appears to reduce one’s own prospect of survival. Increasing market concentration

as measured by the Herfindahl–Hirschman index has a negative effect on firm

duration. The coefficient on the vintage index is higher in manufacturing.

However, we are surprised to find that the negative effect of the change in the

Herfindahl-index is more than three times higher in services than in manufac-

turing, despite manufacturing industries being more concentrated. The data

suggest that, for services, the Herfindahl-index indeed indicates market concen-

tration, because firms tend to compete for the same local market. In contrast, the

same index for more export-oriented manufacturing sectors may conflate the effect

of increasing market concentration with that of growing industrial specialisation

due to comparative advantages.

Higher market growth unambiguously improves chances of survival. However,

our analysis shows that there is an important demographic dimension to this effect.

Separating market growth into the effects of net entry––that is, an increase in the

total population of firms, and the average employment growth per firm, we find

higher growth rates of an average firm to increase the lifespan of an entrant, whereas

a growing firm population, measured as the employment weighted net entry rate, has

the opposite effect. The negative effect of net entry is especially high and

statistically significant in the service industries. This finding strongly points to

displacement effects being the norm rather than the exception in services, which is

consistent with our previous argument about the more local nature of competition in

services when compared to manufacturing.

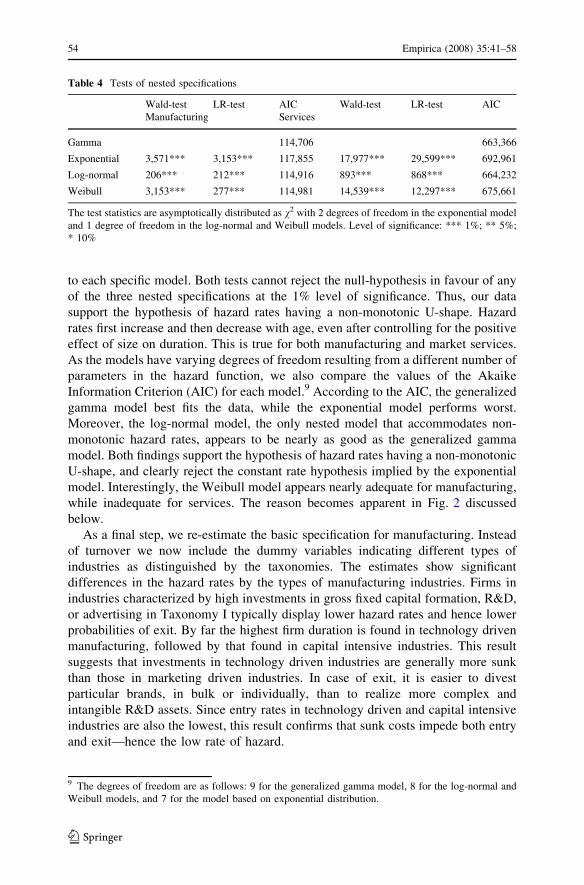

Next, we test the shape of the hazard function using the Likelihood-ratio-test

based on the numerical maximum of the log likelihood function, and the Wald test

on the relevant shape parameters of the generalized gamma distribution described in

Sect. 2.3 (Table 4). The null-hypothesis provides the parameter restrictions leading

52 Empirica (2008) 35:41–58

123

Tab

le3

Est

imat

esof

the

gen

eral

ized

gam

ma

dura

tion

regre

ssio

n

Man

ufa

ctu

rin

gS

erv

ices

En

try

size

0.0

01

99

(15

.28)*

**

0.0

02

05

(15

.30

)**

*0

.002

08

(15

.58)*

**

0.0

02

13

(15

.97)*

**

0.0

00

16

(8.7

0)

**

*

Vin

tag

eIn

dex

–0

.06

13

5(–

66

.30

)**

*–

0.0

65

57

(–8

1.0

7)*

**

–0

.06

55

7(–

81

.05

)**

*–

0.0

65

13

(–8

0.3

8)*

**

–0

.05

83

9(–

12

3.3

6)*

**

Gro

wth

2.9

62

99

(18

.55)*

**

3.4

56

96

(20

.89

)**

*3

.458

50

(21

.26)*

**

3.1

03

20

(19

.40)*

**

1.7

08

02

(39

.07

)**

*

Net

entr

y–

0.3

75

43

(–0

.59)

–0

.38

50

3(–

0.5

9)

–0

.10

24

9(–

0.1

6)

0.3

82

78

(0.5

8)

–8

.90

49

5(–

10

.50

)**

*

DH

erfi

nd

ahl

Ind

ex–

0.7

60

49

(–8

.15)*

**

–0

.66

64

4(–

7.2

5)*

**

–0

.64

35

5(–

7.0

0)*

**

–0

.68

88

0(–

7.4

6)*

**

–3

.04

43

3(–

49

.11

)**

*

Tu

rnov

er–

1.1

76

10

(–8

.52)*

**

–2

.84

53

0(–

11

5.9

4)*

**

Lab

our

inte

nsi

ve

(LI)

0.0

22

32

(1.7

3)*

Cap

ital

inte

nsi

ve

(CT

)0

.104

80

(3.0

5)*

**

Mar

ket

ing

dri

ven

(MD

I)0

.070

68

(5.2

8)*

**

Tec

hn

olo

gy

dri

ven

(TD

I)0

.177

20

(8.4

1)*

**

Lo

wsk

ill

(LS

)–

0.0

61

59

(–4

.47)*

**

Med

ium

skil

lb

lue

coll

ar(M

BC

)0

.018

00

(1.3

1)

Hig

hsk

ill

(HS

)0

.051

21

(2.4

7)*

*

Hig

hin

pu

tsfr

om

reta

il

and

adv

erti

sin

g(I

R&

S)

0.0

24

69

(1.9

6)*

Tra

nsp

ort

(IT

RS

)–

0.0

92

82

(–6

.02)*

**

Kn

ow

led

ge-

bas

ed(I

KB

S)

–0

.16

31

6(–

12

.73

)**

*

Nu

mb

ers

inp

aren

thes

isar

et-

stat

isti

cs.

Lev

elof

signifi

cance

:***

1%

;**

5%

;*

10%

.E

stim

ates

for

the

inte

rcep

tan

dth

epar

amet

ers

of

the

haz

ard

funct

ion

are

not

show

n

Empirica (2008) 35:41–58 53

123

to each specific model. Both tests cannot reject the null-hypothesis in favour of any

of the three nested specifications at the 1% level of significance. Thus, our data

support the hypothesis of hazard rates having a non-monotonic U-shape. Hazard

rates first increase and then decrease with age, even after controlling for the positive

effect of size on duration. This is true for both manufacturing and market services.

As the models have varying degrees of freedom resulting from a different number of

parameters in the hazard function, we also compare the values of the Akaike

Information Criterion (AIC) for each model.9 According to the AIC, the generalized

gamma model best fits the data, while the exponential model performs worst.

Moreover, the log-normal model, the only nested model that accommodates non-

monotonic hazard rates, appears to be nearly as good as the generalized gamma

model. Both findings support the hypothesis of hazard rates having a non-monotonic

U-shape, and clearly reject the constant rate hypothesis implied by the exponential

model. Interestingly, the Weibull model appears nearly adequate for manufacturing,

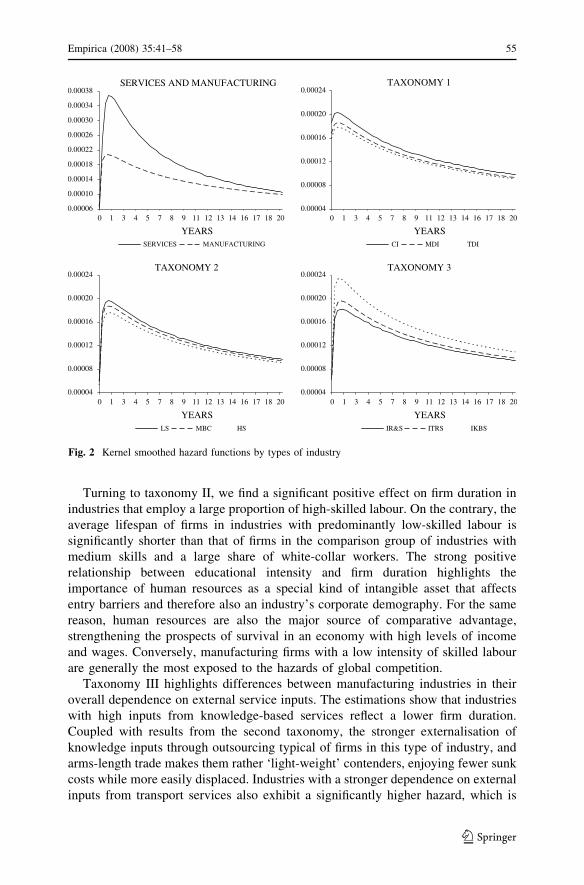

while inadequate for services. The reason becomes apparent in Fig. 2 discussed

below.

As a final step, we re-estimate the basic specification for manufacturing. Instead

of turnover we now include the dummy variables indicating different types of

industries as distinguished by the taxonomies. The estimates show significant

differences in the hazard rates by the types of manufacturing industries. Firms in

industries characterized by high investments in gross fixed capital formation, R&D,

or advertising in Taxonomy I typically display lower hazard rates and hence lower

probabilities of exit. By far the highest firm duration is found in technology driven

manufacturing, followed by that found in capital intensive industries. This result

suggests that investments in technology driven industries are generally more sunk

than those in marketing driven industries. In case of exit, it is easier to divest

particular brands, in bulk or individually, than to realize more complex and

intangible R&D assets. Since entry rates in technology driven and capital intensive

industries are also the lowest, this result confirms that sunk costs impede both entry

and exit––hence the low rate of hazard.

Table 4 Tests of nested specifications

Wald-test LR-test AIC Wald-test LR-test AIC

Manufacturing Services

Gamma 114,706 663,366

Exponential 3,571*** 3,153*** 117,855 17,977*** 29,599*** 692,961

Log-normal 206*** 212*** 114,916 893*** 868*** 664,232

Weibull 3,153*** 277*** 114,981 14,539*** 12,297*** 675,661

The test statistics are asymptotically distributed as v2 with 2 degrees of freedom in the exponential model

and 1 degree of freedom in the log-normal and Weibull models. Level of significance: *** 1%; ** 5%;

* 10%

9 The degrees of freedom are as follows: 9 for the generalized gamma model, 8 for the log-normal and

Weibull models, and 7 for the model based on exponential distribution.

54 Empirica (2008) 35:41–58

123

Turning to taxonomy II, we find a significant positive effect on firm duration in

industries that employ a large proportion of high-skilled labour. On the contrary, the

average lifespan of firms in industries with predominantly low-skilled labour is

significantly shorter than that of firms in the comparison group of industries with

medium skills and a large share of white-collar workers. The strong positive

relationship between educational intensity and firm duration highlights the

importance of human resources as a special kind of intangible asset that affects

entry barriers and therefore also an industry’s corporate demography. For the same

reason, human resources are also the major source of comparative advantage,

strengthening the prospects of survival in an economy with high levels of income

and wages. Conversely, manufacturing firms with a low intensity of skilled labour

are generally the most exposed to the hazards of global competition.

Taxonomy III highlights differences between manufacturing industries in their

overall dependence on external service inputs. The estimations show that industries

with high inputs from knowledge-based services reflect a lower firm duration.

Coupled with results from the second taxonomy, the stronger externalisation of

knowledge inputs through outsourcing typical of firms in this type of industry, and

arms-length trade makes them rather ‘light-weight’ contenders, enjoying fewer sunk

costs while more easily displaced. Industries with a stronger dependence on external

inputs from transport services also exhibit a significantly higher hazard, which is

SERVICES AND MANUFACTURING

1 3 4 5 7 8 9 11 12 13 14 16 17 18 20

YEARS

0.00006

0.00010

0.00014

0.00018

0.00022

0.00026

0.00030

0.00034

0.00038

0

1 3 4 5 7 8 9 11 12 13 14 16 17 18 200

SERVICES MANUFACTURING

TAXONOMY 2 TAXONOMY 3

0.00004

0.00008

0.00012

0.00016

0.00020

0.00024

TAXONOMY 1

0.00004

0.00008

0.00012

0.00016

0.00020

0.00024

0 1 3 4 5 7 8 9 11 12 13 14 16 17 18 20

0 1 3 4 5 7 8 9 11 12 13 14 16 17 18 20

YEARSCI MDI TDI

0.00004

0.00008

0.00012

0.00016

0.00020

0.00024

YEARSLS MBC HS

YEARSIR&S ITRS IKBS

Fig. 2 Kernel smoothed hazard functions by types of industry

Empirica (2008) 35:41–58 55

123

consistent with the expectation of rising intensity of competition the more tradable

the goods, and hence the more distant their shipments are.

Note that introducing dummy variables only slightly changes the estimates of the

variables that have been kept from the basic specification, preserving their statistical

significance. This fact underscores the robustness of our basic specification.

Figure 2 shows the smoothed estimated hazard functions for the manufacturing

industries by type of industry. To generate them, we have used a very simple

specification with entry size as the only explanatory variable. Our results strongly

confirm the liability of the newness hypothesis. Younger firms are subject to higher

probabilities of exit than older firms, even after controlling for the positive effect of

initial size on survival. Both for manufacturing and services, hazard rates first

increase and then decrease with age, although firms in service industries experience

markedly higher maximum hazard rates. Hazard rates peak at the beginning of the

second year of operation. One year seems to be the average experimentation time

required for an entrant to learn its competitiveness.

5 Summary

This paper presents an empirical analysis of the patterns and determinants of firm

survival and the evolution of firm size distribution in Austria. Our analysis is based

on micro-level data from the Austrian social security files that covers all employers

with one or more employees in all sectors of the economy between 1975 and 2004.

We estimate parametric regressions with a flexible hazard function based on the

generalized gamma distribution, and use it to test the shape of the hazard function.

Our dependent variable is firm duration measured in days. Our explanatory

variables focus on the impact of market structure and demographic characteristics of

the industry. We use (i) the initial number of employees as a measure of entry size;

(ii) an index of industrial vintage to proxy the maturity of an industry in terms of

life cycle hypotheses; (iii) the difference between the Herfindahl-index of marketconcentration at the time of entry and the time of exit of the firm to capture the

impact of changes in the intensity of competition. Further, we separate the impact of

market growth into (iv) the average employment growth of firms in the industry and

(v) the employment weighted net entry rate, which controls for the impact from the

overall growth or decline in the number of firms. Finally, we use (vi) the turnover

rate, and alternatively, a series of dummy variables from (vii) three distinct sectoral

taxonomies to test for the influence of sunk costs on the survival of firms.

Our analysis reveals the following:

1. The firm size distribution is extremely left-skewed but becomes more

symmetric as firms age, albeit at a diminishing rate. In the service industries

the firm size distribution assumes a relatively stable shape within the first five

years;

2. Initial size has a significant positive effect on firm survival, indicating an

entrepreneur’s better resource endowment and a stronger commitment to

withstanding temporary shocks;

56 Empirica (2008) 35:41–58

123

3. High values of industrial vintage, indicative of mature industries, have a

significant negative impact on firm duration. Having to compete with older and

more experienced firms in the same industry appears to have an adverse effect

on a firm’s prospect of survival;

4. Although market growth signifies an opportunity, the prospects of a single firm

depend on how many competitors are after it. When growth is internal,

measured by rising average employment per firm, the effects are significant and

positive. When market growth is largely absorbed by a growing firm population

via positive net entry rates, competition rises while the average duration

declines;

5. We generally expect sunk costs to lower entry and exit rates and therefore

improve the prospects of survival for firms already in the market. This

hypothesis is confirmed by our estimations using the turnover rate as an indirect

proxy of their overall extent, as well as by the use of sectoral taxonomies that

additionally distinguish between different kinds of tangible and intangible

sources of competitive advantage. Overall, membership in an industry that can

be characterised as technology driven, capital intensive, and human resource

intensive showed the highest positive impact on firm duration;

6. We find an inverted U-shape hazard function in both manufacturing and market

services, reaching a peak twelve months after entry. Firms in services

experience markedly higher maximum hazard rates. The latter finding supports

the liability of the newness hypothesis drawn in the literature on organizational

ecology, but only partially, as the relationship between the probability of exit

and age is not monotonic. This finding is consistent with the recent literature on

firm survival, while earlier studies often find monotonously decreasing hazard

rates.

Acknowledgments This paper benefited from comments and suggestions by Werner Holzl, PeterHuber, Michael Pfaffermayr and Egon Smeral, and the editorial assistance of Christine Kaufmann andAstrid Nolte. We are particularly indebted to Marianne Schoberl and Peter Huber, who invested muchtime, effort and ingenuity in compiling the micro-data from the Austrian social security files and sharedthem with us. All remaining errors are the sole responsibility of the authors. Both authors gratefullyacknowledge financial support from the Jubilaumsfond of the Austrian National Bank (Grant No. 11092).

References

Agarwal R, Audretsch DB (2001) Does start-up size matter? The impact of technology and product life

cycle on firm survival. J Ind Econ 49:21–44

Agarwal R, Sarkar MB, Echambadi R (2002) The conditioning effect of time on firm survival: a life cycle

approach. Acad Manage J 45:971–994

Amir R, Lambson V (2003) Entry, exit, and imperfect competition in the long run. J Econ Theory

110:191–203

Audretsch DB (1991) New firm survival and the technological regime. Rev Econ Stat 68:441–450

Audretsch DB, Mahmood T (1995) New firm survival: new results using a hazard function. Rev Econ Stat

77:97–103

Baldwin JR, Gorecki PK (1991) Firm entry and exit in Canadian manufacturing sector, 1970–1982. Can

J Econ 24:300–323

Cabral LMB, Mata J (2003) On the evolution of the firm size distribution: facts and theory. Am Econ Rev

93:1075–1090

Empirica (2008) 35:41–58 57

123

Carroll GR, Hannan MT (2000) The demography of corporations and industries. Princeton University

Press

Caves RE (1998) Industrial organization and new findings on the turnover and mobility of firms. J Econ

Lit 36:1947–1982

Cefis E, Marsili O (2005) A matter of life and death: innovation and firm survival. Ind Corpor Change

14:1–26

Cleves MA, Gould WW, Gutierrez RG (2004) An introduction to survival analysis using STATA1, Stata

Press

Cox DR, Oakes D (1984) Analysis of survival data, Chapman & Hall

Desai M, Gompers P, Lerner J (2003) Institutions, capital constraints and entrepreneurial firm dynamics:

evidence from Europe. NBER Working Papers 10165, National Bureau of Economic Research

Dixit A (1989) Entry and exit decisions under uncertainty. J Polit Econ 97:620–638

Dunne T, Roberts MJ, Samuelson L (1988) Patterns of firm entry and exit in US manufacturing industries.

RAND J Econ 19:495–515

Ericson R, Pakes A (1995) Markov-perfect industry dynamics: a framework for empirical work. Rev

Econ Stud 62:53–82

Evans D (1987) Tests of alternative theories of firm growth. J Polit Econ 95:657–674

Freeman J, Carroll GR, Hannan MT (1983) The liability of newness. age dependence and organizational

death rates. Am Sociol Rev 48:692–710

Hannan MT, Carroll GR (1992) Dynamics of organizational populations: density, legitimation, and

competition. Oxford University Press

Geroski PA (1995) What do we know about entry? Int J Indust Organ 13:421–440

Holzl W (2005) Tangible and intangible sunk costs and the entry of firms in a small open economy: the

case of Austria. Appl Econ 37:2429–2443

Jovanovic B (1982) Selection and the evolution of industry. Econometrica 50:649–670

Kalbfleisch JD, Prentice RL (1980) The statistical analysis of failure time data. John Wiley & Sons

Kaniovski S, Peneder M (2002) On the structural dimension of competitive strategy. Ind Corpor Change

113:557–579

Klepper S (1996) Entry, exit, growth, and innovation over the product life cycle. Am Econ Rev 86:562–583

Lancaster T, The econometric analysis of transition data, 1990, Econometric Society Monographs No. 17

Le CT (1997) Applied survival analysis. John Wiley & Sons

Mata J, Portugal P (1994) Life duration of new firms. J Indust Econ 42:227–245

Mata J, Portugal P, Guimaraes P (1995) The survival of new plants: start-up conditions and post-entry

evolution. Int J Indust Organ 13:459–481

Peneder M (2001) Entrepreneurial competition and industrial location. Edward Elgar, Cheltenham, UK

Peneder M (2005) Creating industry classifications by statistical cluster analysis. Estudios de Economica

Aplicada 23:451–463

Peneder M (2007) Firm entry and turnover: the nexus with profitability and growth. Small Bus Econ

(forthcoming)

Siegfried JJ, Evans LB (1994) Empirical studies of entry and exit: a survey of the evidence. Rev Indust

Organ 9:121–155

Stieglbauer A, Job and worker flows in Austria 1978–1998, Ph.D. thesis, University of Linz

Sutton J (1991) Sunk costs and market structure. MIT Press, Cambridge, MA

Sutton J (1997) Gibrat’s legacy. J Econ Lit 35:40–59

Sutton J (1998) Technology and market structure. MIT Press, Cambridge, MA

Wagner J (1994) The post-entry performance of new small firms in German manufacturing industries.

J Indust Econ 42:141–154

58 Empirica (2008) 35:41–58

123