Determinants of Bank Profitability (Return of Equity)

52

MASTER THESIS Determinants of Bank Profitability (Return of Equity) Collins Chigozie Nnakuba 10681787 Master International Finance MSc University of Amsterdam August 2016 Supervised by: Dennis Jullens

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Determinants of Bank Profitability (Return of Equity)

MASTER THESIS

Determinants of Bank Profitability

(Return of Equity)

Collins Chigozie Nnakuba

10681787

Master International Finance MSc

University of Amsterdam

August 2016

Supervised by: Dennis Jullens

1

Abstract

This paper is a practical based analysis conducted for ING Bank. The purpose is to analyze

the drivers of profitability particularly return on equity of banks competing with ING. The

competitors are banks that offer similar financial products as ING across the globe. This paper

examines whether internal factors such as management strategy, assets size, operational

efficiency, capitalization, risk management, diversification, business model, ownership and

external factors such as inflation, interest rate, supervisory influence and tax regime have an

impact on the bank profitability. I observed that internal factors such as the management

strategy/decision, bank model, and operational efficiency have an impact on individual bank

profitability while external factors have an impact on the overall industry. This paper also

investigated whether business model has an impact on the profitability. This business model

was derived by clustering the assets composition of the sample (selected banks) into lending,

hybrid and investment bank using the percentage of the net loan. Lending banks have net loan

above 50%, Hybrid banks have net loan between 50% and 37%, while investment banks have

net loan below 37%. The observable outcome is that some lending banks are more profitable

than hybrid and investment. Hybrid banks profit from a more diverse income stream

specifically fee income whilst investment bank sometimes profits during the downturn

economy. Furthermore, I decomposed return on equity into profitability, sanity, risk weight

and leverage factor using DuPont analysis to capture the underlying drivers of RoE. The

observation with DuPont analysis is that banks with sustainable RoE showed high

profitability ratio, good sanity, moderate risk weight and leverage ratio within the regulatory

requirement. Finally, an indicative regression analysis using OLS model was conducted to

capture the variables that correlate with RoE.

2

Table of Contents

1. Introduction ......................................................................................................................... 3

2. Literature Review on bank profitability .............................................................................. 5

3. Bank business Model (Clustering of Bank model) ........................................................... 13

4. Bank Performance (model, income share, and DuPont analysis) ..................................... 26

5. Statistical model and result ............................................................................................... 34

6. Conclusion ........................................................................................................................ 37

7. Appendices ........................................................................................................................ 39

8. References ......................................................................................................................... 50

3

1. Introduction

European Banks profitability is heavily under pressure as a result of ever increasing

regulations, a slowdown in economic growth (volatility in commodities prices, negative

interest rates), new entrants (Fintech) and pressure from shareholders to receive a decent

return on investment. Despite the above-mentioned pressure, some banks still posted an

impressive result with a decent return on equity (RoE) at year-end 2015.

As part of the project during my short term assignment with ING Wholesale Banking Strategy

and Business Management team (WB S&BM), I was given the assignment to analyze ING

competitors financial performance. ING competitors are banks that offer similar financial

products, operate in the same geography and co-exist in some businesses. This triggered my

research as I wanted to understand the core drivers of ING competitors profitability especially

the return on equity. The analysis was conducted from the selection of 21 top European banks

which include some global systemically important financial institutions (G-SIFIs) and other

local banks. The data used for the analysis was last five years result (2011-2015) extracted

from Bankscope.

To narrow my research on the determinants of bank profitability, the samples were analyzed

on the total level and then clustered into three categories: lending, hybrid, and investment

based on the asset composition. By this clustering, I wanted to investigate whether the

categories or individual bank strategy plays a major role in determining the bank’s

profitability. Furthermore, I decomposed the return of equity of each bank using DuPont

analysis; these are Profitability (net income / total income), Sanity (total income / average

risk-weighted assets (RWA)), risk weight (average RWA / total assets) and leverage factor

(total assets / average common equity). This is geared towards understanding the underlying

drivers of RoE of ING competitors.

4

I hope the outcome of the analysis will add to the empirical studies which suggested that the

determinants of bank profitability are banks-specific factors (internal), macroeconomic factors

and structural factors by fully concentrating on individual bank RoE driver. I also hope that

ING WB S&BM team will use the outcome of the analysis in decision making. The rest of

this paper is organized into five sections. The first section analyses the literature review of the

empirical studies on determinants of bank profitability. In the second section, I introduced the

bank business model, the current model, changes in the business model and the highlight of

year-end 2015 performance result of the sample. The third section introduced the mechanism

used in clustering the samples, the analysis of the income composition of the sample, the

impact on RoE and the decomposition of RoE. In the fourth section, I did an indicative

regression analysis using OLS model to capture the variables that significantly

impact/correlate with RoE. The last section summarizes the outcome of the analysis and the

observations on the drivers of bank profitability.

5

2. Literature Review on bank profitability

In the literature, bank profitability is commonly expressed as a function of both internal and

external determinants. The internal determinants might be called bank-specific determinants

of profitability while the external determinants are variables that are not related to bank

management but reflect the economic and legal environment that affects the operation and

performance of the banks. For the purpose of this paper, Bank profitability is simply what the

financial institutions return to the shareholder, which is denoted as Return on Equity (RoE).

To get a proper understanding of the variables that could impact the profitability of the bank, I

visited both the internal and external factors that have an impact on the profitability. A large

body of empirical studies has investigated the role of different factors influencing bank

performance. These factors are shown and broadly discussed below;

Figure 1. Factors influencing Bank Profitability

Internal factors

Banks size/Assets

Efficiency

Capitalization

Risk management

Diversification

Business model

Ownership

External factors

Macroeconomics

Inflation

Interest rate

Industry specifics

Supervisory influence

Tax regime

Profitability (RoE)

6

Bank-specific factors (internal factors)

Bank-specific determinants of profitability include factors that are internally controlled by

bank management decision and strategy, namely bank size with respect to balance sheets

volume, efficiency, Agile way of working and innovation-minded, risk and prudent costs

management, solid capital base and assets diversification.

Bank size

The empirical literature evidence exploring the impact of bank size on profitability is highly

unsettled. According to Shehzad and Scholten (2013), the proponents of size benefits argue

that larger banks are likely to have a higher degree of product and loan diversification than

smaller banks and should benefit from economies of scale and scope, which in turn leads to

higher profits. Goddard et al. (2004) findings suggest that size/profitability relationship may

be either non-linear. They stated that growth regressions reveal little or no evidence of mean-

reversion bank sizes. Banks that maintain a high capital-assets ratio tend to grow slowly, and

growth is linked to macroeconomic conditions. Otherwise, there are few systematic influences

on bank growth. The persistence of profit appears higher for savings and co-operative banks

than for commercial banks. Banks that maintain high capital assets or liquidity ratios tend to

record relatively low profitability. Berger and Humphrey (1997) argues that even if large

banks are more efficient than small ones, profitability benefits derive from emulating industry

best practice in terms of technology, management structure, instead of focusing on increasing

the size of the bank. Tregenna (2009) argued that economies of scale only exist for smaller

banks and that larger banks suffer from diseconomies of scale owing, for example, to agency

costs, overhead costs of bureaucratic processes and other costs related to managing large

banks. My view is that the size of the bank plays some role in determining the profitability of

the bank. However, strategy and decision of the management play more vital role in bank's

7

profitability. Management decides how, when, and where to expand the organization. After

the crisis of 2007-2009, governments bailed some vulnerable banks on the conditions that

they deleverage and become smaller and concentrate on the core banking business. They

argue that banks are more manageable and profitable when they are smaller. Adding to above

literature on the impact of size on bank profitability, large banks might profit from economies

of scale and scope. However, some smaller banks are easily manageable, efficient and

profitable. It really depends on the management style, strategy and business model.

Operational Efficiency

Bank expenses are also a very important determinant of profitability, closely comparable to

the idea of efficient management. Many empirical studies stated that operational efficiency is

an important driver of bank profitability. Most studies find that higher efficiency typically

measured by cost to income ratio or risk adjusted cost to income (including risk cost)

positively affects bank profitability. Bourke (1989) and Molyneux and Thornton (1992) found

a positive relationship between better-quality management and profitability. Lower ratios

related to higher efficiency, other factors such as the business model, bank size, and

management intent play a measured role in determining profitability.

Bank Capitalization

Bank capitalization is another vital factor influencing profitability, based on various research.

This is a number of capital banks are required to hold to withstand shocks/market volatility by

the regulators. Existing literature suggests that the impact of bank capital on profitability is

unclear, despite that the majority of the studies came out with a positive relationship.

Nevertheless, banks with higher capital ratios tend to face lower funding costs owing to lower

probability of default. However, higher capitalization could also mean lower risk taking

which could negatively impact return and profitability.

8

Risk Management

Risk management and the level of risk are among the most important bank-specific factors

determining performance. Risk management in the banking is essential due to the nature of

the business. Poor asset and liquidity management are among the major causes of bank

failures. Banks might choose to diversify their portfolio or raise liquidity in a time of

uncertainty. Molyneux and Thornton (1992), among others, find a negative and significant

relationship between the level of liquidity and profitability. In contrast, Bourke (1989) reports

an opposite result, Miller and Noulas (1997) result on the effect of credit risk on profitability

appears clearly negative. The inclusiveness in the empirical results and differences on how

bank manage risk triggered the implementation of Standard Approach of calculating risk by

the regulators instead of the Advance Internal Rating Based traditionally used by banks. In my

view, banks profitability partly depend on the willingness and risk appetites of the individual

banks. Using the standard approach of calculating the risk-weighted assets will create more

visibility and transparency in the banking industry.

Diversification

Recent studies on the impact of diversification on bank performance argue that more

diversified banks are more profitable. Other studies identified a “diversification quality”,

inferring that banks with more diversified revenue streams are more profitable. According to

the study of Stiroh, potential diversification benefits in the U.S. banking industry from the

steady shift toward activities that generate fee income, trading revenue, and other types of

non-interest income. In the aggregate, declining volatility of net operating revenue reflects

reduced volatility of net interest income, not diversification benefits from noninterest income,

which is quite volatile and increasingly correlated with net interest income. At the bank level,

greater reliance on noninterest income, particularly trading revenue, is associated with lower

9

risk-adjusted profits and higher risk. I partly support that diversification especially in the

income stream contribute to bank profitability but to a certain degree.

Business model

A recent research on the identification of banks business models and the evaluation of banks

performance and risk across these business models. According to the result from the study of

Gambacorta and van Rixtel (2013), retail (or diversified retail) banks tend to outperform

banks with other business models, such as wholesale and investment banks. My view is that

banks engage deliberately in different intermediation activities and select the balance sheet

structure (model) to fit their business objectives. In a pursuit of growth opportunities in a

competitive environment, banks choose a business model that suits the strategy of the

organization to leverage their strengths.

Ownership

Some studies explore the relationship between ownership type and bank performance, the

results varies according to the geographical region and/or time period of the investigation.

Recent evidence for European banks by Iannotta et al (2007) on the performance of the bank

and the evaluation of the impact of alternative ownership models, together with the degree of

ownership concentration, on their profitability, cost efficiency and risk. Three main results

emerge. Firstly, mutual banks and government-owned banks exhibit a lower profitability than

privately owned banks, in spite of their lower costs. Secondly, public sector banks have

poorer loan quality and higher insolvency risk than other types of banks while mutual banks

have better loan quality and lower asset risk than both private and public sector banks. Lastly,

while ownership concentration does not significantly affect a bank’s profitability, a higher

ownership concentration is associated with better loan quality, lower asset risk, and lower

insolvency risk.

10

Macroeconomic factors (external factors)

A Large number of studies combine the macroeconomic variables into the analysis in order to

examine cyclical impact in bank performance and behavior. Albertazzi and Gambacorta

(2009) study find that bank profits pro-cyclicality derive from the effect that the economic

cycle uses on net interest income (via lending activity) and loan loss provisions (via credit

portfolio quality). An increase in economic activity through higher demand for bank

intermediation services which includes lending, securities underwriting, advisory services and

trading activities will tend to increase banks' net interest income and income generated from

fees and commissions. In contrary, downturn economic activity contributes to a worsening of

banks asset quality and higher loan loss provisioning, thus demonstrating a negative influence

on bank profits. Current negative interest environment is a case whereby most of the

traditional lending banks are under margin pressure.

Inflation and Interest rate

Other macroeconomic factors such as inflation and the term structure of interest rates

supposed to have an impact on bank profitability. The inflation rate, the long-term interest

rate and/or the growth rate of money supply. Revell (1979) introduces the issue of the

relationship between bank profitability and inflation. He noted that the effect of inflation on

bank profitability depends on whether banks’ wages and other operating expenses increase at

a faster rate than inflation. The question is how mature an economy is so that future inflation

can be accurately forecasted and thus banks can accordingly manage their operating costs.

Perry (1992) indicated that the extent to which inflation affects bank profitability depends on

whether inflation expectations are fully anticipated. An inflation rate fully anticipated by the

bank’s management implies that banks can appropriately adjust interest rates in order to

increase their revenues faster than their costs and thus acquire higher economic profits. Other

11

studies from Bourke (1989), Molyneux and Thornton (1992) have shown a positive

relationship between either inflation or long-term interest rate and profitability.

Structural factors (external factors)

Turning to structural factors affecting bank profitability, Mirzaei et al ( 2013) investigated the

effects of market structure on profitability and stability for 1929 banks in 40 emerging and

advanced economies over 1999–2008 by incorporating the traditional structure-conduct-

performance (SCP) and relative-market-power (RMP) hypotheses. They observed that a

greater market share leads to higher bank profitability being biased toward the RMP

hypothesis in advanced economies, yet neither of the hypotheses is supported for profitability

in emerging economies. The SCP appears to exert a destabilizing effect on advanced banks,

suggesting that a more concentrated banking system may be vulnerable to financial instability,

however, the RMP seems to perform a stabilizing effect in both economies. Their evidence

also highlights that profitability and stability increase with an increased interest-margin

revenues in a less competitive environment for emerging markets. By contrast, the “efficient

structure” hypothesis states that the positive relationship between profitability and

concentration can be driven by efficiency, in that more efficient banks gain market share and

improve profitability. Another structural factor that could impact the profitability of the bank

is the capital market orientation, the evidence of the impact on bank profitability is

inconclusive. Supervisory power is expected to have some impact on bank profitability.

However, the empirical evidence is again inconclusive despite the extensive amount of on-

going work at the Basel Committee on Banking Supervision (BCSB) and European Banking

Authority (EBA) to evaluate the possible impact of regulatory measures to bank business

model. A global overview of the potential implications for business models resulting from the

collective implementation of the regulatory measures developed since the financial crisis (see

appendix VI) for the recent regulatory measures to bank business model.

12

In summary, bank profitability is commonly expressed as a function of both internal and

external determinants. The internal determinants are known as bank-specific determinants of

profitability while the external determinants are variables that are not related to bank

management but reflect the economic and legal environment that affects the operation and

performance of the banks. The empirical studies and literature review on the determinants of

profitability are in some case inconclusive. Just like the study of Shehzad and Scholten (2013)

which argue that larger banks are likely to have a high degree of product and loan

diversification than the smaller bank. Larger banks might profit from diversification but this is

not a guarantee for higher profitability. Operational efficiency plays a vital role in the profit

maximization just like Bourke (1989) and Molyneux and Thornton (1992) find a positive

correlation between quality management and profitability. Empirical research on the impact

of risk management, diversification capitalization, and ownership structure is inconclusive.

However, risk management is crucial for effective portfolio management. Diversification help

in tapping into other source of revenue generation and capitalization could demonstrate that

bank will withstand shocks and market volatility. Macroeconomic factors such as inflation

and interest rate have shown a positive relationship with profitability based on the studies of

Bourke (1989), Molyneux and Thornton (1992).The impact of supervisory power is rather

inconclusive. Based on the summary of the literature review some internal and external

factors have an either positive or negative relationship with bank profitability. Despite my

support for the studies, I am of the opinion that banks profitability should be analyzed on the

individual basis and return on equity fully decompose using DuPont analysis, to capture the

real determinant of the profitability. This will be the value added of this paper to the study of

the bank profitability.

13

3. Bank business Model (Clustering of Bank model)

According to Porter (1979), The concept of business models originates from the literature

concerning strategic groups that basically mean sets of firms that are active in a single sector

and use similar strategies. The notion of business strategies in banking, and also the business

models originate from a number of strategic variables that reflect the long-term choices of

bank management with respect to assets, funding, capitalization, and diversification. Seeing

that a strategy is essentially a long-term concept, my conclusion is that individual banks

business models will be stable over the years. This means that the differences between banks

are more important than changes over time within banks to identify the performance impact of

business model choices.

There are many types of banks model namely; private banking & asset management, retail

banking/commercial bank and Investment bank. Most of the banks with the exception of

American bank operate as universal bank meaning that they offer all products ranging from

private banking to investment banking. Seeing that this paper is built around ING competitors,

I will focus on the retail/commercial banking model. The identification of retail/commercial

bank business models requires a set of variables that determine the possible strategies. With

this in mind, the use of balance sheet data seems logical for the composition of bank business

model. From the assets composition of the samples, three categories of bank model were

derived.

Firstly, the lending banks which are traditional lenders that provide loans to individuals,

organizations and other institutions. Banks in this category mostly dependent on interest

income and to lesser extend non-interest income as a source of income. Secondly, the hybrid

banks which have more diversified asset composition than lending banks. Income source is

also well-diversified between interest and non-interest income (notable fee). Lastly, the

14

investment banks are mostly trading in derivatives and securities. Main income stream

revenue are other income, fee income and also interest income.

Giving the introduction of bank business model, the rest of this section will concentrate on the

current model, the change in business model and FY 2015 financial performance of the

sample (ING competitors analysis).

3.1 Current model

Bank has simply two functions: deposit and lender. This means that bank has two clients

namely one that deposits money and one that borrows. The bank intermediates between the

borrower and depositor. This means that bank offers lower interest to depositors and lend to

borrowers at a higher rate. The spread is the profit margin. This is the basic business model of

the bank.

Individuals, businesses, and institutions will have the preference of keeping money in the

bank rather than in a safe, cellar or other places. They prefer to deposit the money in the bank

and sometimes receive an interest payment. They trust that the bank will safeguard their

money and make it available when needed. For the borrowers perspective, they prefer to go

the bank to lend money at a slightly higher interest rate.

The customers of the bank (borrowers and depositors) are from Retail and Corporate. Retail

clients are individuals, household or private persons whilst Corporates are commercial

institutions, businesses, and governments. Banks offer many services to the clients; for retails

clients bank offer mortgages, car loans, personal loan and wealth management. To corporate

clients, the bank offers different services and intermediation from loans for project, hedging,

advisory, structured finance. The key element in lending is the ability to manage client risk

15

profile. This is to ensure that customer will be able to pay the principal and also the interest.

Banks will usually do a risk assessment of customers before lending.

Banks use multiple channels to reach out to their customers. This ranging from operating from

branches to physically meet clients to installing ATM in some convenient locations to

encourage self-services. Some banks are using direct banking using internet and mobile apps

to offer a basic product to customers.

Due to complexities in product offering, packaging, risk management, regulatory requirement,

competition and operational excellence, Banks are partnering with technology (FinTech) to

create innovative and simplify banking models such as dis-intermediation, multi-channel

integration, business intelligence and predictive analysis.

The banking industry is well regulated by many institutions and governmental organizations

ranging from local bank authority, European Banking Authority, Basel Committee on

Banking Supervision. It is essential that banks are constantly supervised due to the importance

of banks to the economy. The supervision is also to protect the taxpayers and depositors. This

is the reason why the regulators set the minimum reserves that each bank must hold.

Some basic income streams of the banks are interest income from the lenders, fee income for

operations such as trading portfolios, advisory, and other income. Costs line are the channel

costs, interest paid to depositors, risk cost from loan loss and other operational costs.

Despite that, most of the banks in the European union/community are labeled universal bank

which may offer credit, loans, deposits, asset management, investment advisory, payment

processing, securities transactions, underwriting and financial analysis. While a universal

banking system allows banks to offer a multitude of services, it does not require them to do

so. Banks in a universal system may still choose to specialize in a subset of banking services.

16

Universal banking combines the services of a commercial bank and an investment bank,

providing all services from within one entity. The services can include deposit accounts, a

variety of investment services and may even provide insurance services. Deposit accounts

within a universal bank may include savings and checking. Under this system, a bank can

choose to participate in any or all of the permitted activities. They are expected to comply

with all guidelines that govern or direct proper management of assets and transactions. Since

not all institutions participate in the same activities, the regulations in play may vary from one

institution to another.

3.2 Change in business model

After the financial crisis of 2007-09 as banks were bailed with tax payers money,

policymakers, regulators, and supervisors have worked toward improving the safety and

soundness of the global financial system through a range of regulatory changes towards

banks. Banks are being forced to consider radical changes to the business models that support

some of their core banking services. Changes are in various stages of progress, with some

already taken place, some just starting, and others still to be determined. Few changes to the

banking model after the crisis are discussed below;

Originate to distribute: Traditionally, banks used deposits to fund loans and book it on their

balance sheets awaiting maturity. Recently, banking model started to change. Banks started

to increase the funding source with alternative products such as bond financing, commercial

paper financing, and repurchase agreement (repo) funding. Some Bank even started to replace

the traditional originate-to-hold model of lending with another strategic securitization

mechanism named originate-to-distribute model. At the earlier stage, banks limited the

distribution model to mortgages, credit card credits, and car and student loans, but over time

they started to apply it to even corporate loans. Few plausible reason for so called originate to

17

distribute is that banks will share the risk with other banks, shrink the balance sheet, gain

from lower risk-weighted assets, gain from higher fee income via income diversification and

possibly increase profitability (RoE).

Regulators influence: The highlight of the regulatory debate has been concentrated on the

"too-big-to-fail". International and domestic regulators are identifying SIFIs, the largest and

most interconnected firms, for greater scrutiny and additional regulation. The regulators are

being given new tools to manage the buildup of credit in the system, including countercyclical

capital buffers. The name too big to fail is not well appreciated by the regulator and they

simply want to shrink banks either directly through regulation or indirectly through rules that

make some businesses less appealing or limit the benefits of scale. Some regulators want

SIFIs banks to pay an insurance premium for the risks they represent to society or to limit the

potential capital advantage SIFIs may have over smaller banks.

Customer Centric and Clients profitably: Banks are making major changes to the business

models of their core services, and the growing cost of delivery requires major investments in

information technology. This is to improving customer service as a means to improve the

industry’s reputation and create pathways to more loyal, profitable customer and client

relationships. Few banks are moving from product driven organization to a more client focus.

Activities like know your client (KYC), Net promoter score, new innovations to empower

clients and digitalization are a key focus of bank to promote customer services and

profitability.

Risk governance: Banks are focusing on their ability to react quickly to stress scenarios so

they can be agile as the crises and uncertainties continuously exist within the industry. Banks

are constantly working with the regulator to improve regulatory reporting. Even the regulators

suggested a shift from Advance Internal Reporting method of calculating risk-weighted asset

18

to more standardize method. Banks are not in favor of this due to the anticipated increase in

risk-weighted assets. This is still to be decided by the regulators in the course of 2016.

Focus on growth and profitability levels: Banks will have to reduce costs radically, deploy

capital more dynamically and efficiently, capture growth opportunities in emerging markets,

and consider material changes to compensation levels. They must also redesign service

delivery and business models while rethinking the fundamental rationale for some existing

businesses. Banks are streamlining and moving some activities to a low-cost environment.

On the revenue generation, well-diversified income source such as an increase in non-interest

income will ultimately contribute to higher profitability/return on equity of the banks.

3.3 Analysis of the bank full year 2015 figures (at a glance)

Looking back, 2015 will be remembered as a year in which the global and domestic economic

landscape remained difficult to navigate. Factors like a higher regulatory requirement,

volatility in oil and commodity prices, negative in interest rate and economic sentiments

weighted heavily on the profitability of banks in 2015. Despite the pressure, few EU bank

posted a good result in 2015. As curiosity emerges on the drivers of financial performance

and profitability, Table 1. shows the performance of ING competitors financials of FY 2015

and the last reported full years. Key results as income lines (net interest and non-interest

income), costs, risk costs, efficiency (cost/income ratio), Net interest margin, Return on

equity, total assets, common equity, average risk-weighted assets, loan to asset and loan to

customer deposit were analyzed.

19

Table 1 Full Year 2015 banks key results and performance indicators

Net interest income (NII) is the different between interest earned from loan and interest paid

on deposit

Net Interest Income = Interest paid on earning assets - Interest paid on deposits

The net-interest income generated by the selected in FY 2015 is € 291bln compared to FY

2014 € 277bln showing a growth of 5% (see appendix I). One observation is that banks with

higher NII growth do not necessary have higher total assets with the exception of BBVA and

Santander (appendix I). This could be an evidence that higher interest income growth does not

fully correlate with assets growth. Another observation is that traditional lending banks such

as ING, Santander, ABN, and Rabo have high NII dependency (see graph A).

FY 2015 key result

in EUR bln & %

Net

interest

income

Fees &

other

income

Total

incomeCosts

Risk

costsPBT PAT

C/I

ratioNIM RoE

Total

assets

common

equity

Average

RWALTA LTD

ABN 6.1 2.4 8.5 5.2 0.5 2.7 1.9 61.8% 1.6% 11.9% 390.3 16.2 108.8 66.4% 114.5%

Barclays 17.1 17.0 34.1 22.5 2.9 2.8 0.8 66.0% 1.1% 1.0% 1524.5 85.9 502.2 35.6% 96.6%

BBVA 16.4 6.8 23.2 12.1 4.2 4.6 3.3 52.2% 2.7% 6.3% 750.1 52.8 376.1 54.3% 112.1%

BNPP 23.1 19.8 42.9 29.3 3.6 10.4 7.0 68.2% 1.2% 7.6% 1994.2 93.2 622.0 34.1% 101.7%

BPCE 11.3 12.5 23.7 16.2 1.6 6.1 3.8 68.4% 1.1% 6.1% 1166.5 62.1 392.1 50.6% 128.2%

Commerz 5.8 3.9 9.7 7.2 0.7 1.8 1.2 74.0% 1.1% 4.1% 532.6 29.1 206.7 38.3% 83.4%

Credit Agricole 21.3 10.6 31.8 19.8 2.3 9.4 6.4 62.3% 1.3% 6.9% 1698.9 93.4 247.5 43.3% 114.9%

Credit Suisse 8.6 11.7 20.3 18.6 0.3 -2.2 -2.7 91.7% 1.3% -6.6% 759.9 41.3 257.9 33.3% 80.0%

Deutsche 15.9 17.2 33.1 31.9 0.9 -6.1 -6.8 96.4% 1.1% -10.0% 1629.1 68.0 397.0 26.3% 76.5%

HSBC 30.0 24.0 54.0 36.5 3.3 17.3 13.9 67.7% 1.4% 7.7% 2213.3 180.1 1008.9 38.4% 72.4%

ING 12.8 3.7 16.5 9.3 1.3 6.4 4.7 56.3% 1.6% 11.9% 838.5 39.9 307.3 63.9% 106.5%

Intesa Sanpaolo 10.3 7.2 17.4 11.0 3.4 4.2 2.8 62.8% 1.7% 6.0% 676.5 47.0 277.1 51.7% 162.7%

Lloyds 14.6 8.3 22.9 14.1 0.6 1.9 1.0 61.3% 1.5% 1.6% 1113.3 66.4 307.4 55.7% 109.5%

Nordea 5.1 4.9 10.0 4.9 0.5 4.7 3.7 49.4% 0.8% 12.3% 646.9 29.8 144.4 46.6% 165.3%

Rabo 9.1 3.5 12.6 8.5 1.1 2.9 2.2 67.1% 1.5% 6.9% 670.4 31.9 212.5 65.4% 132.6%

RBS 11.9 5.4 17.3 20.4 -1.2 -3.7 -1.6 117.9% 1.1% -2.2% 1109.9 72.5 393.9 37.5% 91.2%

Santander 33.3 12.3 45.5 25.2 10.2 9.5 7.3 55.4% 2.9% 7.5% 1340.3 98.1 585.4 56.6% 128.7%

SocGen 10.0 15.3 25.3 17.5 2.4 6.1 4.4 69.2% 0.9% 7.9% 1334.4 55.6 355.0 28.9% 111.5%

Standard Chartered 8.7 4.6 13.3 10.3 4.4 -1.4 -2.0 77.0% 1.7% -4.7% 588.3 43.1 279.8 40.2% 73.5%

UBS 6.2 21.3 27.5 22.2 0.1 5.0 5.8 80.6% 1.0% 11.5% 873.3 51.1 190.5 33.2% 77.9%

Unicredit 12.8 9.3 22.0 15.9 4.8 2.4 2.0 72.1% 1.6% 3.8% 860.4 53.7 399.9 51.8% 123.1%

Total 290.5 221.4 511.9 358.6 48.0 84.9 59.4 70.1% 22,712 1,311 7,572

Average 24.4 10.5 24.4 17.1 2.3 4.0 2.8 70.4% 1.4% 4.6% 1,082 62 361 45.3% 107.8%

Data compiled March 31, 2016

List containing FY 2015 key results for 21 top EU Banks (Source Bankscope BvD)

20

Graph A: net interest share of the sample

Non-interest income of the bank income derived primarily from fees including deposit, and

transaction fees, fees from financial market trading portfolios, advisory fees annual fees, and

other alternative income not related to Interest income. From the sample, Investment banks

such as UBS, SocGen, Credit Suisse Deutsche generate more non-interest income than

lending banks (see graph B).

Graph B: non-interest share of the sample

77%73% 72% 72% 71% 69% 67% 66% 64%

60% 59% 58%56% 54%

51% 50% 48% 48%42%

40%

23%

Net interest income dependency

23%27% 28% 28% 29% 31% 33% 34% 36%

40% 41% 42%44% 46%

49% 50%52% 52%

58%60%

77%

Non-interest income share

21

Costs are total expenses the business spend during the normal business operations. Costs

include rent, payroll, professional services, regulatory costs and other expenditures. One of

the key responsibility of the management is to effectively reduce costs without massively

affecting the company ability to compete with the peers. From our sample, FY 2015 costs

were € 359bln this an increase of 7% compared to FY 2014. Drivers to costs increases were

regulatory costs (all banks), impairments of goodwill & intangibles and litigation costs

(Deutsche).

Risk cost includes the net impairment charge in relation to the bank's loans and advances as

well as off-balance sheet. Risk cost is mostly higher in lending banks an even higher amongst

bank that operate in some geography. Santander, Unicredit, Standard Chartered and BBVA

reported risk cost of € 10bln, € 5bln, € 4bln and € 4bln respectively. However, overall risk

costs from our sample declined by -5% compared to FY 2014.

Efficiency ratio is commonly regarded as the cost to income ratio which the is a measure of

total expenses as the percentage of total income.

Cost income ratio = total expenses / total income

Efficiency ratio measures operating expense as a percentage of operating income, it is

basically used to evaluate the efficiency and productivity of a corporation. Lower ratios

basically show higher efficiency, however, few factors can impact the ratio such as bank

business model (asset class), the size of the organization and other unforeseen costs. From our

sample, average C/I slightly increased in 2015 mainly observed within the investment banks

such as RBS, Deutsche, Credit Suisse, and UBS.

22

Net interest margin (NIM) is a measure of the difference between the interest income

generated by banks (interest received) and interest paid (customer deposit) over total earning

assets.

NIM = (interest received-interest paid) / total earning assets

The sample average NIM at 1.4% was at the same level as FY 2014 despite pressure on the

interest rate (negative interest rate environment). With the exception of Santander and BBVA

which profit with higher interest margin due to high yield bonds in South Americas but also a

very risky business, all other banks NIM are under pressure due to ultra-interest rate

environment.

Return on Equity (RoE) is a profitability ratio that measures the ability of a firm to generate

profits from the shareholder's investments in the organization. It basically shows how much

profit each amount invested in the by the shareholder returns. It calculated as:

RoE = Net income / Equity

In this paper, RoE was decomposed using DuPont analysis. This is to properly analyze the

underlying drivers of RoE (this will be discussed in the next chapter). From the sample,

Nordea, ING, ABN and UBS reported RoE of 12% in 2015 whilst Deutsche, Credit Suisse,

Standard Chartered and RBS reported -10%,-7%,-5% and -2% respectively. Deutsche bank

lower RoE was mainly due to higher litigation costs, Credit Suisse due to higher costs,

Standard Chartered was primarily driven by higher risk costs while RBS was attributable to

higher costs base.

Total assets are the total amount of assets owned by an entity. It is basically referred to items

of economic value which are used over a period of time to generated profit for the owners.

Viewing from the sample, total asset of the banks decreased by -2.2% vs 2014 (€ 22.7tln vs

23

€-23.3tln). One reason for assets decline might be the balance sheet optimization and

deleveraging exercise going on in some banks.

Common equity refers to the amount that all common shareholders have invested in a

company. This includes the value of the common shares, retained earnings, and additional

paid-in capital. From the sample, common equity increased by 10% compared to 2014. One

possible reason for higher common equity is the ability to reinvest the income instead of

distribution to shareholders (plow-back).

Risk-weighted asset (RWA) is a bank's assets or off-balance-sheet exposures, weighted

according to risk. It is used for the calculation of asset and computing the capital requirement

or Capital Adequacy Ratio (CAR) for the banks. Viewing from the sample, average RWA

slightly decreased compared to 2014 (0.5%). Few observations are; lending banks such as

BBVA and Santander reported higher RWA. Again, lending banks have higher risk weight

(average RWA / total assets) compared to investment banks. This means that investment used

originate to distribute mechanism to reduce RWA on the book, unlike the originate and hold

strategy mostly seen with lending banks.

Loan to assets ratio measures the total net loans as a percentage of total assets. The higher

this ratio indicates a bank is loaned up and its liquidity is low. However, there is a strong

correlation between higher loan to asset and Net interest margin. Banks with higher LTA tend

to show higher NIM.

Loan to asset = Net loan / total assets

24

Graph C: loan to asset of the sample

Loan to customer deposit is a measure loan to deposit ratio is used to calculate a lending

institution's ability to cover withdrawals made by its customers.

Loan to deposit = Net loan / deposit

It is also a measure of stable funding. A lending bank that received a deposit and gives loans

to the customer must have must have a certain amount of reserve (liquidity) to maintain it

normal operation. However, a bank with LTD in the in the range of 100% has stable funding

base. If the LTD of a bank is higher than 100% that means that the bank might not have

enough liquidity for fund requirement. On the other hand, if LTD is too low, the bank may not

be earning enough as expected. From the sample RBS, Barclays, ING, and Lloyds have LTD

in the range of 100%, Nordea, Intesa Sanpaolo and Rabo have higher LTD whilst HSBC,

Standard Chartered, Deutsche, and UBS reported lower LTD (see graph D).

66% 65% 64%

57% 56% 54%52% 52% 51%

47%43%

40%38% 38% 38%

36% 34% 33% 33%29%

26%

Loan to asset

25

Graph D: loan to deposit of the sample

In conclusion, Bank chooses a business model that suits the strategy of the organization

despite flexibility in the universal banking model. Some bank is more into private banking,

some are in retail/commercial banking and some are leverage more in investment banking.

Bank business experience slight changes after the financial crises of 2007-2009 ranging from

Originate-to-hold model, to originate to distribute model, a more regulatory power to hold

more capital, plan to introduce standard approach methodology in calculating risk-weighted

asset, customer centric, increase profitability and investment in innovation. These are the

strategies implemented by banks to maximizes profitability and regulators to ensure the

sustainability of the industry. Comparing the overall financial performance of the ING

competitors (sample) in FY 2015 vs. FY 2014, total income increased by 5.2%, total costs

increased by 6.6 % mostly due to higher regulatory costs, risk costs decreased by -5.5%, total

assets decreased by -2.2% mainly due to deleveraging and balance sheet optimization,

shareholders common equity increased by 10.1% and risk-weighted asset decreased by 0.5%.

All in all, FY 2015 financial demonstrate that banks are much better shape despite the all the

headwinds (see appendix I for delta FY 2015 and FY 2014).

165% 163%

133% 129% 128%123%

115% 114% 112% 112% 110% 107%102%

97%91%

83% 80% 78% 76% 74% 72%

Loan to deposit

26

4. Bank Performance (model, income share, and DuPont analysis)

Bank business model is structured based on the vision and strategy of the management of an

organization. Bank’s strategy defines the asset class and the business model. To understand

the business model of the sample, I constructed an asset composition of the banks using five

years (2011-2015) average asset split into loans, derivatives & securities, other earning assets,

and non-earning assets. Based on the outcome of asset class, the banks were clustered in

lending, hybrid and investment banks (graph E). the reason is to actually see the average

assets composition of ING competitors in the 5-years period.

lending banks (LB) with loan asset above 50%

Hybrid banks (HB) with loan asset in the range of 49% - 37%

Investment banks (IB) with loan portfolio below 37%

Graph E: 5-years average asset composition of the sample (ING competitors)

67%65% 63%

57% 56% 55% 55%53%

49%46%

42% 41%39%

37%34%

31%33%

29%27% 26%

22%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Loans Der & Ser others EA Non-NEA

Lending banks

Hybrid banks Investment banks

27

4.1 Income composition and RoE of the sample

The supporters of diversification often claim that well-diversified income stream improves the

overall income and profitability of the bank. However looking at the income diversification of

the sample (graph F), there is no much deviation in the income composition of the sample in

the last five years. Interest income was in the range 56%-58%, fee income 27%-29% and

other income 13%-16%. The conclusion is that banks do not often deviate from chosen

strategy. Looking at the RoE trend of the sample in the last five years, the average RoE was

highest in 2015 (5.7%) and lowest in 2013 (3.6%). The is an indication that banks are in a

better financial shape in 2015.

Graph F: income share and RoE of the sample

Analyzing the income composition of the three categories lending, hybrid, and

investment banks:

Lending banks income share was consistency in the last five years. Interest income share was

in the range of 65% to 69%, fee income was in the range of 21% to 23% and other income

was in the range of 8% to 13%. From the average income composition of the last five years, it

is obvious that lending banks do not have a well-diversified income source. Banks operating

58% 56% 56% 58% 58%

28% 27% 28% 29% 29%

13%16% 16%

13% 13%

2011 2012 2013 2014 2015

Income split sample

Interest Fee Other

4.9

3.5 3.0

5.0 4.6

2011 2012 2013 2014 2015

RoE Sample (in %)

28

with this model might experience interest margin pressure in a low/negative interest

environment due to high-interest income dependency. Looking at the RoE trend, 2015 was the

best year for lending banks with average RoE around 7%. RoE was under pressure in 2011

and 2013 driving by higher risk cost (write-offs) from Intesa Sanpaolo and Unicredit.

Graph G: income share and RoE lending banks

Hybrid banks are BCPE, Nordea, Standard Chartered, Credit Agricole, HSBC, Commerz,

and Nordea. These banks have on average lower interest income compared to lending banks

but higher fee income. Hybrid banks have better income stream diversification than lending

banks but that does not result in higher profitability. Looking at the RoE, there is a declining

trend for banks in this cluster. However, looking on the individual bank, Nordea reported RoE

above 12% in 2015 due to prudent cost management while Standard chartered reported low

RoE due higher costs base and risk cost.

Graph H: income share and RoE hybrid banks

69%65% 65%

69% 68%

23% 21% 23% 22% 22%

8%13% 13%

8% 9%

2011 2012 2013 2014 2015

Income split Lending Banks

Interest Fee Other

1.5

4.5

0.6

6.0

7.0

2011 2012 2013 2014 2015

RoE Lending Banks (in %)

60% 60% 61% 59% 58%

28% 27% 29% 30% 30%

12% 13% 11% 12% 12%

2011 2012 2013 2014 2015

Income split Hybrid Banks

Interest Fee Other

7.8

5.5

7.3

6.4

5.4

2011 2012 2013 2014 2015

RoE Hybrid Banks (in %)

29

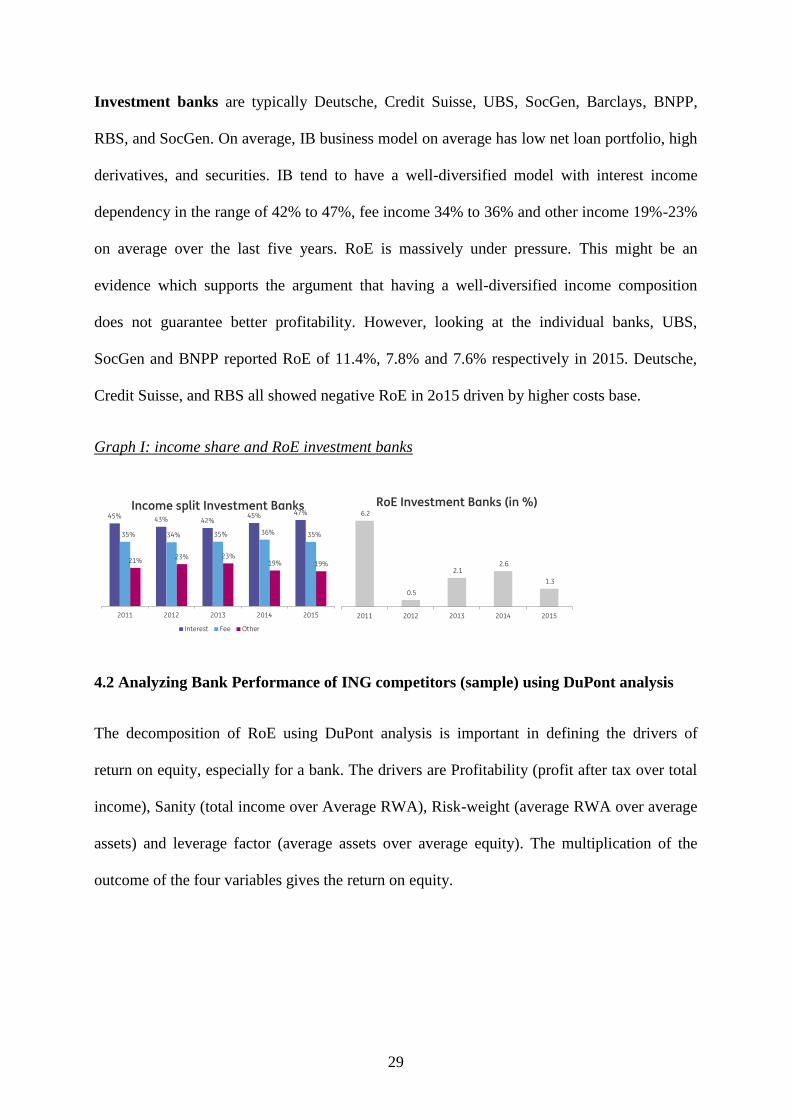

Investment banks are typically Deutsche, Credit Suisse, UBS, SocGen, Barclays, BNPP,

RBS, and SocGen. On average, IB business model on average has low net loan portfolio, high

derivatives, and securities. IB tend to have a well-diversified model with interest income

dependency in the range of 42% to 47%, fee income 34% to 36% and other income 19%-23%

on average over the last five years. RoE is massively under pressure. This might be an

evidence which supports the argument that having a well-diversified income composition

does not guarantee better profitability. However, looking at the individual banks, UBS,

SocGen and BNPP reported RoE of 11.4%, 7.8% and 7.6% respectively in 2015. Deutsche,

Credit Suisse, and RBS all showed negative RoE in 2o15 driven by higher costs base.

Graph I: income share and RoE investment banks

4.2 Analyzing Bank Performance of ING competitors (sample) using DuPont analysis

The decomposition of RoE using DuPont analysis is important in defining the drivers of

return on equity, especially for a bank. The drivers are Profitability (profit after tax over total

income), Sanity (total income over Average RWA), Risk-weight (average RWA over average

assets) and leverage factor (average assets over average equity). The multiplication of the

outcome of the four variables gives the return on equity.

45% 43% 42%45% 47%

35% 34% 35% 36% 35%

21%23% 23%

19% 19%

2011 2012 2013 2014 2015

Income split Investment Banks

Interest Fee Other

6.2

0.5

2.1 2.6

1.3

2011 2012 2013 2014 2015

RoE Investment Banks (in %)

30

RoE = Profit after / Average equity

Profitability (P)= Profit after tax / Total revenue

Sanity (efficiency) (S)= Total revenue / Average risk-weighted assets

Risk weight (RW) = Average risk-weighted assets / Average assets

Leverage factor (LR)= Average assets / average equity

RoE for total sample: looking at the average five-year trend of the sample, RoE was in the

range of 3%-5%. 2014 and 2011were on the high side with average RoE of 5.0% and 4.9%

respectively. Analyzing the average RoE drivers of 4.9% in 2011, profitability ratio was 9%,

Sanity was 7%, risk weight was 34% and leverage ratio 4.2% (100/24). The observation is

that on average, bank leverage ratio was very low resulting from high debt in 2011. In 2014,

the outcome shows that profitability was at 12% and leverage ratio improved to 5.0%

(100/20). Examining 2015 average RoE of the sample which ended at 4.6%. I observed that

profitability ratio is moderate at 11%, sanity ratio was at the same level as other years, risk

weight was stable whilst leverage ratio improved to 5.6% (100/18). This proofs that on

average banks are more capitalized than preceding years.

31

Graph J: RoE drivers and RoE Sample (Profitability, sanity, risk weight in %)

RoE Lending banks: I observed that on average, lending banks RoE was under pressure in

2011 and 2013 (graph K). This was due to higher pressure on profitability driven by high-risk

costs and write-off of some bank in this cluster .Some bank operates in risk region like Latin

Americas where the interest rate is very high but also risk costs. FY 2015 was a good year for

lending banks as profitability ratio surged to 16%, sanity ratio 7%, risk-weight was on the

better side at 38% and leverage ratio at 5.5% (100/18). All these drivers pushed RoE of the

lending banks to 7% in 2015. Analyzing the drivers of RoE of individual banks within this

cluster (see alsoAppendix IILending Banks income split, asset composition, and drivers RoE),

I observed the result varies per bank for example, ING and ABN posted the same RoE of 12%

in 2015 but the drivers are different (ING 29%, S 5%, RW 37% and LR 4.8% (100/21) whilst

ABN P 23%, S 8%, RW 28% and LR 4.2%). This is an evidence that banks use different

strategies and mechanism in achieving the return on equity. Another observation was that

some bank in this category didn’t perform well due to the nature of the business and

geographical presence such as the aforementioned Latin Americas.

9 75

12 11

7 7 7 7 7

34 3436

34 34

2422

20 2018

2011 2012 2013 2014 2015

Drivers of RoE sample

Profitability Sanity Risk weight Leverage factor

4.9

3.5 3.0

5.0 4.6

2011 2012 2013 2014 2015

RoE Sample (in %)

32

Graph K: RoE drivers and RoE lending banks (Profitability, sanity, risk weight in %)

RoE Hybrid banks: the observation from this cluster is that the bank in this segment profit

from a well-diversified income. However, the diversified income stream does not guarantee

higher returns. Looking at the RoE drivers, Profitability ratio is in the range of 14%-19% this

is best in class compared to lending and investment banks, Sanity is also on a moderate level,

risk weight is on moderate side and lower than lending banks. Leverage ratio increased

toward 2015 meaning that the best are well capitalized. However one can argue that on

average banks in this cluster are a bit conservative and not aggressive in taking a risk. RoE

drivers for the bank in this cluster also varies, some banks are very profitable while some are

still navigating a stormy water. For the dynamics of RoE driver for the banks in this cluster

(see Appendix III – Hybrid Banks income split, asset composition, and drivers RoE)

Graph L: RoE drivers and RoE hybrid banks (Profitability, sanity, risk weight in %)

0

10

-1

1416

6 6 6 6 7

42 40 4239 38

20 19 18 19 18

2011 2012 2013 2014 2015

Drivers of RoE Lending Banks

Profitability Sanity Risk weight Leverage factor

1.5

4.5

0.6

6.0

7.0

2011 2012 2013 2014 2015

RoE Lending Banks (in %)

17

14

19 1816

6 6 6 6 7

37 37 3734 34

2421

20 1917

2011 2012 2013 2014 2015

Drivers of RoE Hybrid Banks

Profitability Sanity Risk weight Leverage factor

7.8

5.5

7.3

6.4

5.4

2011 2012 2013 2014 2015

RoE Hybrid Banks (in %)

33

RoE Investment banks: Bank in this cluster on average are deemed a very risky bank with

an exception of BNPP, SocGen, and UBS (see Appendix IV – Investment Banks income split,

asset composition, and drivers RoE). Looking at the RoE trend, 2011 was the best year for the

banks in this cluster. They performance better than lending banks. This might be an evidence

that IB profits in an adverse market scenario.

Graph M: RoE drivers and RoE investment banks (Profitability, sanity, risk weight in %)

In conclusion, using the assets composition of the ING competitors (sample) in clustering the

banks into lending, hybrid, and investment banking help in understanding the dynamics,

business model and return on equity drivers. Banks profitability highly depend on the

decision of the management, the strategy of the organization and the business model. From

the decomposition of the RoE, I observed that lending banking which is retail/commercial

bank like are on average much profitable than hybrid bank and investment bank. Hybrid

banks on average profit from a well-diversified revenue stream such as fee and other income

but some of them are well capitalized and practically risk averse. The investment bank is the

best in class when it comes to income diversification but higher costs in running IB business

have massive pressure on the returns of some bank in this cluster. To maximize profitability

and have a decent RoE on equity, a bank should make the right decision, choose a sustainable

business model and effectively manage costs and risk.

11

-1

14

2

8 8 8 8 8

2426

2927

2928

2622 23

20

2011 2012 2013 2014 2015

Drivers of RoE Investment Banks

Profitability Sanity Risk weight Leverage factor

6.2

0.5

2.1 2.6

1.3

2011 2012 2013 2014 2015

RoE Investment Banks (in %)

34

5. Statistical model and result

This section shows an indicative statistical analysis. Explaining and summarizing the data of

the sample selection. Seeing that the number of observations is limited, the outcome of

analysis will be deemed indicative and might not robust enough.

Firstly, I constructed the correlation table to capture the variables that correlate with RoE.

Few observations were;

Table 2: Correlation matrix for several variables

Cost income ratio (CIR) negatively correlates with the RoE, the higher the CIR, the lower the

RoE. this is in-line with the empirical studies.

Loan loss provision over total loan (LLPOTL) as well negatively correlates with RoE, an

increase in write-off and risk costs lead to a decrease in RoE. This is in-line with empirical

studies.

Total loan growth (TLGr) positively correlates with RoE, an increase in loan might result in

an increase in revenue.

Total assets growth (TAGr) positively correlates with RoE, this is similar to loan growth.

RoE RoA NIM CIR EOTA ETR FC GDP IIS LLPOTL LTD LTIR TLGr TAGr TLS NIOTI TIORWA RWA0TL LF

RoE 1.00

RoA 0.96 1.00

NIM 0.12 0.21 1.00

CIR -0.49 -0.47 -0.06 1.00

EOTA -0.05 0.09 0.71 0.05 1.00

ETR -0.05 -0.12 -0.02 0.12 -0.19 1.00

FC 0.21 0.20 0.54 -0.09 0.06 0.26 1.00

GDP 0.11 0.09 0.07 -0.16 0.06 -0.17 -0.12 1.00

IIS 0.08 0.07 0.63 -0.06 0.28 -0.02 0.39 0.07 1.00

LLPOTL -0.36 -0.30 0.59 0.47 0.48 0.19 0.41 -0.19 0.30 1.00

LTD -0.07 -0.16 0.26 -0.02 0.11 0.13 0.35 -0.01 0.42 0.32 1.00

LTIR -0.03 -0.09 -0.01 0.14 -0.28 0.76 0.35 -0.34 -0.02 0.20 0.18 1.00

TLGr 0.33 0.34 0.20 -0.27 0.06 -0.15 0.08 0.20 -0.16 -0.17 -0.08 -0.12 1.00

TAGr 0.37 0.37 0.33 -0.29 0.07 -0.15 0.34 0.34 0.18 0.03 0.19 0.13 0.48 1.00

TLS 0.12 0.08 0.56 -0.05 0.30 0.01 0.41 0.01 0.72 0.26 0.60 -0.03 -0.05 0.11 1.00

NIOTI 0.98 0.96 0.09 -0.55 -0.03 -0.11 0.16 0.10 0.07 -0.39 -0.05 -0.09 0.31 0.37 0.11 1.00

TIORWA 0.15 0.14 -0.19 -0.07 -0.18 -0.02 -0.12 0.05 -0.61 -0.25 -0.39 -0.06 0.37 -0.06 -0.41 0.12 1.00

RWA0TL -0.14 -0.04 0.76 0.15 0.79 0.06 0.24 -0.04 0.51 0.64 0.28 0.03 -0.09 0.09 0.48 -0.15 -0.58 1.00

LR -0.23 -0.09 0.66 0.13 0.97 -0.13 0.04 0.04 0.26 0.53 0.14 -0.26 -0.02 -0.03 0.29 -0.21 -0.20 0.79 1.00

35

Net income over total income (NIOTI) is profitability ratio. An increase in profitability ratio

will ultimately result in an increase in RoE keeping all the other variable of DuPont analysis

stable.

The rest of the variables are less than 0.25 and -0.25 which I consider not significant.

Secondly, I conducted an empirical study using OLS estimation using the following linear

regression equation;

RoEit = c + β1CIRit + β2EOTA it + β3ETR it + β4FCit + β5GDPit + β6IISit + β7LLPOTLit +

β8LTD it + β9TAGR it + β10TLGR it + β11TLS it + ε it

Where profitability = RoE, c is a constant term; i = 1,…,N and t =1,…N is the dependent

variable, the rest on the right part of equation are the independent of bank internal specific

factor, macro-economic factors.

The R-square of the regression showed that 44% of the model was explained. The results

showed that funding costs, loan loss provisions, and total asset growth are significant

determinants of bank profitability. Despite the limited number of the observations, the

outcome in-line with the empirical studies.

36

Abbreviations

CIR Cost-to-income ratio

EOTA Equity-over-total loan

ETR Effective tax rate

FC Funding cost

GDP Global domestic product

IIS Interest income share

LLPOTL Loan loss provision-over-total loan

LTD Loan to deposit

LTIR Long term interest rate

RoE Return on equity

TAGr Total asset growth

TLGr Total loan growth

TLS Total loan share

Summary RoE banks

Regression Statistics Regression Statistics

Multiple R 0.664

R Square 0.440

Adjusted R Square 0.367

Standard Error 5.064

Observations 105

ANOVA

df SS MS F Significance F

Regression 12 1855.368 154.614 6.030 0.000

Residual 92 2358.838 25.640

Total 104 4214.207

Coefficients Standard Error t Stat P-value Lower 95% Upper 95%

Intercept -49.520 46.451 -1.066 0.289 -141.776 42.735

CIR -0.073 0.045 -1.620 0.109 -0.163 0.017

EOTA 0.415 0.523 0.793 0.430 -0.624 1.454

ETR 3.089 2.361 1.308 0.194 -1.600 7.778

FC 2.242 1.062 2.112 0.037 0.134 4.351

GDP -0.793 0.653 -1.213 0.228 -2.090 0.505

IIS -0.011 0.056 -0.190 0.849 -0.122 0.100

LLPOTL -4.923 1.577 -3.122 0.002 -8.055 -1.791

LTD -0.038 0.022 -1.696 0.093 -0.082 0.006

LTIR -0.960 0.930 -1.033 0.304 -2.806 0.886

TLGr 0.053 0.102 0.515 0.608 -0.150 0.256

TAGr 0.248 0.097 2.564 0.012 0.056 0.440

TLS 0.087 0.065 1.344 0.182 -0.042 0.216

37

6. Conclusion

Banking Industry, especially in the Eurozone, is experiencing some headwinds rising from the

ultra-low interest rate, increases in regulatory requirement, increases in bank tax, competition

from non-licensed financial services institutions and disruptors commercial known as

financial technology (Fin-tech). Profitability in the industry is massively under pressure,

simplification, automation, costs reduction, jobs cut, branch closure and consultation with the

regulatory are the hype and headline of almost all the bank's annual report. Amongst all the

headwinds, some banks still make a reasonable profit and report a higher return on equity.

The key question is what drive the profitability of the bank? Considering that RoE is one of

the key measure of bank profitability and without disputing the results of the empirical

studies. It is of great important to decompose the Return on equity into profitability, sanity

(efficiency), risk weight and leverage factor to capture the drivers of return on equity. From

the sample, I observed that in general, higher income does not correlate with higher

profitability. The chosen business model and management strategy might impact the

profitability of the bank. On average, Lending banks are more profitable than Hybrid and

Investments Banks due to stable interest income but are also more vulnerable in a low-interest

rate environment. Hybrid banks do not necessarily deliver higher returns but benefit from

more diversified sources of income (interest, fee and other income). Most of the investment

banks are not delivering up to expectation despite the well-diversified source of income

mainly due to a high-cost base.

In conclusion, it is very difficult and unrealistic to quantify the determinants of bank

profitability notable return on equity without decomposing and analyzing the core drivers

from individual bank perspectives. By using DuPont analysis in decomposing RoE, It is

obvious and transparent to see the sustainable banks from risky ones. A sustainable and

38

profitable bank return on equity should show high profitability ratio, good sanity, moderate

risk weight and leverage ratio within the regulatory requirement. This paper might have some

limitation, further investigation is necessary on this topic.

39

7. Appendices

Appendix I – List of banks in the data sample FY 2015 key figures

FY 2015 key result

in EUR bln & %

Net

interest

income

Fees &

other

income

Total

incomeCosts

Risk

costsPBT PAT

C/I

ratioNIM RoE

Total

assets

common

equity

Average

RWALTA LTD

ABN 6.1 2.4 8.5 5.2 0.5 2.7 1.9 61.8% 1.6% 11.9% 390.3 16.2 108.8 66.4% 114.5%

Barclays 17.1 17.0 34.1 22.5 2.9 2.8 0.8 66.0% 1.1% 1.0% 1524.5 85.9 502.2 35.6% 96.6%

BBVA 16.4 6.8 23.2 12.1 4.2 4.6 3.3 52.2% 2.7% 6.3% 750.1 52.8 376.1 54.3% 112.1%

BNPP 23.1 19.8 42.9 29.3 3.6 10.4 7.0 68.2% 1.2% 7.6% 1994.2 93.2 622.0 34.1% 101.7%

BPCE 11.3 12.5 23.7 16.2 1.6 6.1 3.8 68.4% 1.1% 6.1% 1166.5 62.1 392.1 50.6% 128.2%

Commerz 5.8 3.9 9.7 7.2 0.7 1.8 1.2 74.0% 1.1% 4.1% 532.6 29.1 206.7 38.3% 83.4%

Credit Agricole 21.3 10.6 31.8 19.8 2.3 9.4 6.4 62.3% 1.3% 6.9% 1698.9 93.4 247.5 43.3% 114.9%

Credit Suisse 8.6 11.7 20.3 18.6 0.3 -2.2 -2.7 91.7% 1.3% -6.6% 759.9 41.3 257.9 33.3% 80.0%

Deutsche 15.9 17.2 33.1 31.9 0.9 -6.1 -6.8 96.4% 1.1% -10.0% 1629.1 68.0 397.0 26.3% 76.5%

HSBC 30.0 24.0 54.0 36.5 3.3 17.3 13.9 67.7% 1.4% 7.7% 2213.3 180.1 1008.9 38.4% 72.4%

ING 12.8 3.7 16.5 9.3 1.3 6.4 4.7 56.3% 1.6% 11.9% 838.5 39.9 307.3 63.9% 106.5%

Intesa Sanpaolo 10.3 7.2 17.4 11.0 3.4 4.2 2.8 62.8% 1.7% 6.0% 676.5 47.0 277.1 51.7% 162.7%

Lloyds 14.6 8.3 22.9 14.1 0.6 1.9 1.0 61.3% 1.5% 1.6% 1113.3 66.4 307.4 55.7% 109.5%

Nordea 5.1 4.9 10.0 4.9 0.5 4.7 3.7 49.4% 0.8% 12.3% 646.9 29.8 144.4 46.6% 165.3%

Rabo 9.1 3.5 12.6 8.5 1.1 2.9 2.2 67.1% 1.5% 6.9% 670.4 31.9 212.5 65.4% 132.6%

RBS 11.9 5.4 17.3 20.4 -1.2 -3.7 -1.6 117.9% 1.1% -2.2% 1109.9 72.5 393.9 37.5% 91.2%

Santander 33.3 12.3 45.5 25.2 10.2 9.5 7.3 55.4% 2.9% 7.5% 1340.3 98.1 585.4 56.6% 128.7%

SocGen 10.0 15.3 25.3 17.5 2.4 6.1 4.4 69.2% 0.9% 7.9% 1334.4 55.6 355.0 28.9% 111.5%

Standard Chartered 8.7 4.6 13.3 10.3 4.4 -1.4 -2.0 77.0% 1.7% -4.7% 588.3 43.1 279.8 40.2% 73.5%

UBS 6.2 21.3 27.5 22.2 0.1 5.0 5.8 80.6% 1.0% 11.5% 873.3 51.1 190.5 33.2% 77.9%

Unicredit 12.8 9.3 22.0 15.9 4.8 2.4 2.0 72.1% 1.6% 3.8% 860.4 53.7 399.9 51.8% 123.1%

Total 290.5 221.4 511.9 358.6 48.0 84.9 59.4 70.1% 22,712 1,311 7,572

Average 24.4 10.5 24.4 17.1 2.3 4.0 2.8 70.4% 1.4% 4.6% 1,082 62 361 45.3% 107.8%

Data compiled March 31, 2016

List containing FY 2015 key results for 21 top EU Banks (Source Bankscope BvD)

FY 2014 key result

in EUR bln & %

Net

interest

income

Fees &

other

income

Total

incomeCosts

Risk

costsPBT PAT

C/I

ratioNIM RoE

Total

assets

common

equity

Average

RWALTA LTD

ABN 6.0 2.0 8.0 5.3 1.2 1.5 1.1 66.2% 1.6% 8.0% 386.9 14.2 109.3 67.7% 123.5%

Barclays 15.5 16.9 32.5 23.0 2.8 2.9 1.1 70.9% 1.0% 1.5% 1745.8 75.1 522.5 31.5% 101.3%

BBVA 14.9 5.5 20.4 10.6 4.3 4.0 3.1 51.8% 2.8% 6.5% 631.9 47.1 337.2 52.2% 116.8%

BNPP 20.9 18.3 39.2 26.5 3.7 3.2 0.5 67.7% 1.2% 0.6% 2077.8 87.6 618.2 31.7% 107.7%

BPCE 11.8 11.7 23.5 16.3 1.7 5.3 3.4 69.4% 1.1% 5.6% 1223.3 59.6 380.9 47.4% 132.9%

Commerz 5.4 3.4 8.7 6.9 1.1 0.6 0.4 79.5% 1.0% 1.4% 558.3 27.2 202.9 37.7% 94.3%

Credit Agricole 21.0 9.5 30.5 19.2 2.7 7.8 5.3 62.8% 1.4% 6.3% 1762.8 83.9 485.9 40.1% 119.0%

Credit Suisse 7.5 12.8 20.3 17.4 0.2 3.0 1.9 85.4% 1.2% 5.2% 767.4 36.9 232.7 29.6% 74.1%

Deutsche 14.3 16.8 31.0 27.2 1.1 3.1 1.7 87.6% 1.0% 2.7% 1708.7 63.6 348.5 23.7% 77.1%

HSBC 28.8 21.3 50.1 34.0 3.3 15.4 12.1 67.8% 1.4% 7.8% 2169.7 154.6 898.5 37.0% 73.1%

ING 12.6 2.9 15.5 10.2 1.6 3.9 2.8 65.9% 1.6% 8.1% 828.6 35.0 298.6 62.3% 106.8%

Intesa Sanpaolo 10.6 6.4 17.0 10.4 4.6 3.0 1.3 61.1% 1.8% 2.9% 646.4 45.1 273.0 49.8% 168.5%

Lloyds 13.1 8.4 21.5 14.4 0.9 2.9 2.4 66.8% 1.4% 4.0% 1113.9 60.1 312.5 55.1% 108.3%

Nordea 5.5 4.7 10.2 5.1 0.5 4.3 3.3 49.5% 0.9% 11.4% 669.3 29.2 177.4 44.6% 174.2%

Rabo 9.1 3.6 12.7 8.5 2.8 1.7 1.8 67.0% 1.5% 6.0% 681.1 30.9 211.3 65.1% 139.7%

RBS 11.9 7.1 19.0 17.1 -1.7 3.4 -3.5 90.1% 1.0% -4.9% 1351.2 71.6 459.0 31.8% 99.2%

Santander 30.0 12.4 42.4 23.4 10.5 10.7 6.9 55.3% 2.9% 8.2% 1266.3 85.0 537.5 56.8% 131.5%

SocGen 10.4 13.4 23.8 16.4 2.6 4.4 3.0 68.9% 0.9% 5.9% 1308.1 51.1 347.9 27.2% 113.5%

Standard Chartered 9.1 5.8 15.0 9.1 1.8 3.5 2.2 60.8% 1.9% 5.8% 597.9 38.5 257.5 39.2% 69.7%

UBS 5.5 17.6 23.0 20.7 0.1 2.1 3.0 90.0% 1.0% 7.0% 884.7 43.4 185.0 29.7% 77.1%

Unicredit 13.1 8.9 21.9 14.6 4.8 3.7 2.4 66.4% 1.7% 4.6% 844.2 51.6 416.5 52.5% 135.8%

Total 277.1 209.2 486.4 336.3 50.6 90.2 56.4 69.1% 23,224 1,191 7,613

Average 24.4 10.0 23.2 16.0 2.4 4.3 2.7 69.1% 1.4% 5.0% 1,106 57 363 43.5% 111.6%

Delta 2015 vs 2014

figures

Net

interest

income

Fees &

other

income

Total

incomeCosts

Risk

costsPBT PAT

Total

assets

common

equity

Average

RWA

ABN 0.9% 20.0% 5.6% -1.5% -56.9% 76.1% 69.7% 0.9% 14.4% -0.5%

Barclays 10.1% 0.2% 4.9% -2.3% 1.5% -2.7% -21.9% -12.7% 14.4% -3.9%

BBVA 10.2% 23.4% 13.8% 14.7% -1.3% 15.6% 8.0% 18.7% 12.1% 11.5%

BNPP 10.9% 8.1% 9.6% 10.3% -1.0% 229.5% 1289.3% -4.0% 6.3% 0.6%

BPCE -4.6% 6.5% 0.9% -0.5% -4.6% 16.0% 12.9% -4.6% 4.2% 2.9%

Commerz 7.9% 15.9% 11.0% 3.3% -39.2% 185.8% 216.4% -4.6% 7.0% 1.9%

Credit Agricole 1.5% 10.5% 4.3% 3.4% -15.9% 21.6% 21.8% -3.6% 11.3% -49.1%

Credit Suisse 14.4% -8.8% -0.2% 7.2% 93.7% -174.2% -240.9% -1.0% 11.9% 10.8%

Deutsche 11.3% 3.0% 6.8% 17.5% -21.9% -295.7% -500.5% -4.7% 6.9% 13.9%

HSBC 4.0% 12.7% 7.7% 7.5% -1.2% 12.6% 14.5% 2.0% 16.5% 12.3%

ING 1.3% 30.2% 6.7% -9.0% -15.5% 66.4% 67.6% 1.2% 13.9% 2.9%

Intesa Sanpaolo -3.4% 12.7% 2.6% 5.4% -26.4% 40.7% 114.2% 4.7% 4.0% 1.5%

Lloyds 11.4% -0.7% 6.7% -2.1% -36.2% -36.5% -57.0% -0.1% 10.4% -1.6%

Nordea -6.8% 3.3% -2.1% -2.2% -12.5% 9.2% 9.9% -3.4% 2.2% -18.6%

Rabo 0.2% -3.2% -0.8% -0.6% -58.9% 70.7% 20.2% -1.6% 3.2% 0.5%

RBS 0.3% -24.1% -8.9% 19.3% -33.6% -208.3% -53.7% -17.9% 1.2% -14.2%

Santander 11.0% -1.1% 7.4% 7.6% -3.1% -10.6% 5.8% 5.8% 15.4% 8.9%

SocGen -3.9% 14.1% 6.2% 6.6% -9.0% 39.6% 46.9% 2.0% 8.9% 2.0%

Standard Chartered -4.4% -21.4% -11.0% 12.8% 151.7% -140.1% -190.5% -1.6% 11.7% 8.7%

UBS 14.1% 21.1% 19.5% 7.0% 66.8% 143.4% 92.4% -1.3% 17.8% 3.0%

Unicredit -2.3% 4.6% 0.5% 9.0% 0.0% -34.9% -14.3% 1.9% 4.0% -4.0%

Total 4.8% 5.8% 5.2% 6.6% -5.1% -5.9% 5.3% -2.2% 10.1% -0.5%

40

Appendix II – Lending Banks income split, asset composition, and drivers RoE

(Profitability, sanity, risk-weight, RoE in %)

66%69%

74% 75%72%

24% 21% 23% 21% 22%

10% 9%4% 4% 6%

2011 2012 2013 2014 2015

Income split ABN

Interest Fee Other

9

16 1614

23

7 6 6 7 8

2930 31

28 28

3331

28 27

24

2011 2012 2013 2014 2015

Drivers of RoE ABN

Profitability Sanity Risk weight Leverage factor

67% 67% 69% 67% 66%

20% 20% 20%24%

21%

8% 8% 6% 4% 4%5% 5% 5% 5%9%

2011 2012 2013 2014 2015

Asset composition ABN

Loans Der & Ser others EA Non-NEA

5.6

9.0 8.6 8.0

11.9

2011 2012 2013 2014 2015

RoE ABN

82% 80% 78% 81%77%

15% 14% 15% 15% 14%

3% 6% 7%4%

9%

2011 2012 2013 2014 2015

Income split ING

Interest Fee Other

2522

2018

29

5 5 5 5 5

37 36 37 36 37

28

23 2224

21

2011 2012 2013 2014 2015

Drivers of RoE ING

Profitability Sanity Risk weight Leverage factor

60%65% 64% 62% 64%

23% 25% 26%30% 28%

5% 5% 5% 4% 3%

12%

5% 4% 4% 5%

2011 2012 2013 2014 2015

Asset composition ING

Loans Der & Ser Non-NEA Non-NEA

11.9

9.2 8.8 8.1

11.9

2011 2012 2013 2014 2015

RoE ING

76%69% 70% 72% 72%

19% 17% 15% 15% 15%

5%

15% 14% 14% 13%

2011 2012 2013 2014 2015

Income split Rabo

Interest Fee Other

22

15 15 1418

5 6 6 6 6

30 3032

31 32

21 21 21 22 21

2011 2012 2013 2014 2015

Drivers of RoE Rabo

Profitability Sanity Risk weight Leverage factor

62% 63%66% 65% 65%

19% 21% 20%23%

20%

3% 3% 3% 3% 2%

15% 13% 11% 9%13%

2011 2012 2013 2014 2015

Asset composition Rabo

Loans Der & Ser others EA Non-NEA

7.5

5.9 6.3

6.0

6.9

2011 2012 2013 2014 2015

RoE Rabo

69% 68% 67%71% 73%

23% 23% 25% 23% 22%

8% 9% 8% 6% 5%

2011 2012 2013 2014 2015

Income split Santander

Interest Fee Other

14

7

1416 16

8 8 7 8 8

4744

4742 44

17 1614 15 14

2011 2012 2013 2014 2015

Drivers of RoE Santander

Profitability Sanity Risk weight Leverage factor

58%55% 57% 57% 57%

24% 25% 27%29% 29%

4% 4% 3% 1% 1%

14% 16% 14% 12% 13%

2011 2012 2013 2014 2015

Asset composition Santander

Loans Der & Ser others EA Non-NEA

8.6

3.8

6.5

8.2 7.5

2011 2012 2013 2014 2015

RoE Santander

57%

36% 37%

61%64%

16% 16% 15% 14%11%

27%

48% 48%

25% 25%

2011 2012 2013 2014 2015

Income split Lloyds

Interest Fee Other

-4-6

-2

11

56 6 7 7 7

3835 34

28 28

20 19 18 19 17

2011 2012 2013 2014 2015

Drivers of RoE Lloyds

Profitability Sanity Risk weight Leverage factor

59%54%

57% 55% 56%

27% 27% 25%29% 28%

5% 5% 4% 4% 4%10%

14% 13% 12% 13%

2011 2012 2013 2014 2015

Asset composition Lloyds

Loans Der & Ser others EA Non-NEA

-1.6

-2.5

-0.8

4.0

1.6

2011 2012 2013 2014 2015

RoE Lloyds

69% 71% 70% 73% 71%

23% 20% 21% 20% 20%

8% 9% 8% 6% 9%

2011 2012 2013 2014 2015

Income split BBVA

Interest Fee Other

17

1114 15 14

6 7 6 6 6

54 5256