contemporary investment and development of waqf assets in ...

35

CONTEMPORARY INVESTMENT AND DEVELOPMENT OF WAQF ASSETS IN SINGAPORE IN SINGAPORE Presented By: Dr. Shamsiah Abdul Karim At International Islamic Capital Market Forum Sasana Kijang, Kuala Lumpur Malaysia b 20 September 2012 1

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of contemporary investment and development of waqf assets in ...

CONTEMPORARY INVESTMENT AND DEVELOPMENT OF WAQF ASSETS IN SINGAPOREIN SINGAPORE

Presented By:Dr. ShamsiahAbdul KarimAt International Islamic Capital Market ForumSasana Kijang, Kuala LumpurMalaysia

b20 September 2012

1

“Thanks to the prodigious development of the waqf institution, a person could be born in a house belonging to a waqf sleep in a cradle belonging to a waqf, sleep in a cradle of that waqf and fill up on its food, receive instruction through waqf‐receive instruction through waqfowned books , become a teacher in a waqf school, draw a waqf financed salary and at his death, be placed in a waqf provided coffin for burial in a

f t ” ( Y di ildiwaqf cemetery” ( Yediyildiz 1990:5)

2

Presentation FlowPresentation Flow

• Features of Waqf

Sharia’ • Properties that can be sequestered for waqf• Sharia ‘ issues related to waqf

Investments

• Investments of WaqfAssets• Issues on the Investments of WaqfAssets

• Traditional financingFinancing and Development

model

g• Contemporary Financing• Conclusion

3

Features of WaqfFeatures of Waqf

Permanent Charitable, Permanent Dedication pious

Movable or immovable properties

4

ADMINISTRATIONOFMUSLIM LAWACTADMINISTRATION OF MUSLIM LAW ACT

WAKAF WAKAF AM WAKAF KHAS

“Wakaf “ means the

Wakaf khas means a dedication in perpetuity of the

WAKAF

“Wakaf “ means the permanent dedication by a Muslim of any movable or

immovable property for any purpose recognised by Muslim

law as pious religious or

Wakaf am means a dedication in perpetuity of the capital and income of property for pious, religious or charitable purposes recognised by the Muslim law

p p ycapital of property for pious,

religious or charitable purposes recognised by the

Muslim law, the income of the property being paid to law as pious, religious or

charitable.

g yand the property so dedicated;

p p y g ppersons or for purposes

specified in the wakaf, and the property so dedicated.

5

INVESTMENT OF WAQF ASSETSQ

6

Assets Assets

Movable or immovable Wholly own

Free from encumbrances

Shari’ahCompliance

7

Asset AllocationProperty Based Physical assetsProperty Based – Physical assetsEquities / REITsS k kSukukAlternative InvestmentDirect Business/JV______________________________________

MUIS KuwaitHarvard

Real Estate Equities

Sukuk/Fixed Income Alternative Invt

Direct Biz /JV Cash/FD 8

Comparison of Investment Portfolio Portfolio

WaqfAssets Property /Real Equities/ Sukuk Business/ others WaqfAssets Property /Real Estate(%)

Equities/ Sukuk(%)

Business/ others (%)

Singapore 79 5 16 ( cash & cash equivalent)

Kuwait 53 47Kuwait 53 47 ‐

Trust ( Oxford 23 46/13 16Foundation)

9

Investment Challenges for Waqf

Capital Guarantee NonGuaranteedGuaranteed

Income Yearly disbursement

Income ploughback to capitalp

Investment Horizon

Short term Long term

Asset classes High risk Low risk

10

Shari’ah and Decision Issues On Investment of Wakaf Assets

P t tPermanent vs temporaryMovable vs immovableCapital depreciation/appreciationCapital guarantee Risk and return profileIncome accumulation vs capital appreciationIncome accumulation vs capital appreciationNegative income Istibdal and sale of waqf assetsIstibdal and sale of waqf assets

11

Matching Investment Horizon With Investment Strategies*

Time Horizon What Matters

d k lImmediate Market Values

Immediate Market Val es and Immediate Market Values and Income

Perpetual Income

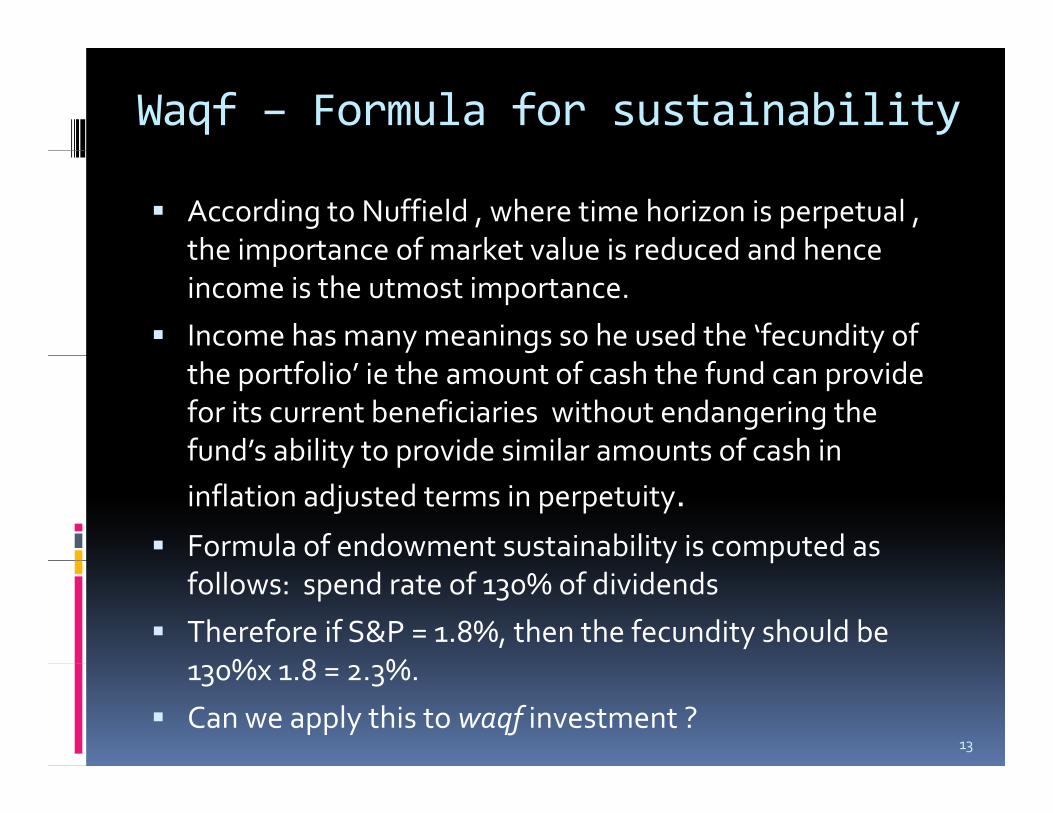

* (Nuffield , 5 Mar 2007)12

Waqf – Formula for sustainability

According to Nuffield , where time horizon is perpetual , the importance of market value is reduced and hence the importance of market value is reduced and hence income is the utmost importance.

Income has many meanings so he used the ‘fecundity of the portfolio’ ie the amount of cash the fund can provide for its current beneficiaries without endangering the fund’s ability to provide similar amounts of cash in fund s ability to provide similar amounts of cash in inflation adjusted terms in perpetuity.Formula of endowment sustainability is computed as y pfollows: spend rate of 130% of dividends

Therefore if S&P = 1.8%, then the fecundity should be % 8 % 130%x 1.8 = 2.3%.

Can we apply this to waqf investment ?13

Examining some Investment decisions (Kuwait Awqaf)

Mi i i i k d i l iMinimise risk and capital protectionDiversification of Investment instruments‐d ff f ldifferent portfoliosDiversification in sectors eg. Financial real estate and servicesDiversification based on geographical locationsSome investment ceilings for each sector.

14

FINANCING OF WAKAF PROPERTIES

15

Traditional Method of WaqfTraditional Method of WaqfFinancing

H k /Hik L l l l Hukr/Hikr ‐ Long lease or perpetual lease use for renting or leasing.

lIjaratyn – two leases.Khulluw – loan contract made to waqf . Contract commonly used in Egypt for rental of waqf properties.

16

Contemporary Sharia’MethodContemporary Sharia Method

S k kSukukMusharakahIj hIjarahIntifa’a

REITREITsIstisna

17

MusharakahMusharakah Bond (Bond (SukukSukuk))MusharakahMusharakah Bond (Bond (SukukSukuk) )

• Development of Waqf S Omar AljuniedMixed Development at Bencoolen StrMixed Development at Bencoolen Str – 2001

18

Before Refurbishment After Refurbishment

Case Study Case Study 1: 1: BencoolenBencoolen

Proceeds

InvestorsIssues S$35m Musharaka Bonds

MUIS (waqf)MUIS (Baitumal) Warees

Financial resources of S$35m

Land & financial resources Managerial and financial resources

Musharaka Arrangement

19

Bencoolen StDevelopment

Case Study Case Study 1: 1: BencoolenBencoolen

Investors

Coupon Payment on Musharaka Bonds

MUIS (Baitumal) Warees

P fit h i

~3.5%

Profit sharing

Ser iced Ascott InternationalIjarah Contract

20

Serviced Apartments

Ascott International

Guaranteed Income

For 10 years

Sukuk Issues for Development pof Waqf Assets

M / ll l B i l lMortgage /collaterals ‐ BaitulmalGuarantee income ‐( need to sign the lease

f )agreement upfront )Period of work in progress –Baitulmal and contractual agreementLag time from selling the property to the time of investment ‐ ( a bridging finance)

21

Case Study 2: Sukuk Intifa’aCase Study 2: Sukuk Intifa aZam Zam Towers

Th W f f Ki Abd l A i i MThe Waqf of King Abdul Aziz in MeccaMunshaat‐ a Kuwait based International

CLease Investment Co.24 year reversionary ground lease with the waqfConcept of time –share vacation facilities and fractional ownership

22

Fractional OwnershipFractional Ownership

Land belong to waqfLand belong to waqfBuilding belongs to Munshaat ( IDB)The munfa’a or benefit of space sold for 24 yearsThe munfa a or benefit of space sold for 24 yearsMunshaat entered BOT contract with a builder‐US$390 million contractC f d d b I l i i iContract funded by Islamic securities.Shares were price according to season, unit location and view. location and view. Shares made fully exchangeable and rep. 24‐year guaranteed right for a specific time and specific spacespecific space.

23

Zam –Zam towersZam Zam towers

S i i ld i iSecurities sold prior to constructionSukuk represents a forward lease of the property

24

REITsREITs

REIT d i 6REITs started in 1960sIslamic REITS – I‐ REITs started in 2006 Islamic Property Funds‐US$9 billion*

real estate ‐ 30% Private equities – 70%

First I‐ REITs issued on 1st Feb 2007‐ HadharahBoustead REITs ; plantation based.

25

Successful structuring of REITsSuccessful structuring of REITs

Underlying assets

Capital Structure

Ownershipp

Tax and DividendTax and Dividend26

Consideration for Structuring Consideration for Structuring of REITs

• Commercial value

d l• Commercial value• Quality assets with high potential• Halal /Perm• issible activities• Perpetuity?

Underlying Assets

• Private REITs• Public REITs

Capital Structure

• Fragmenting the tenure• Cross border REITs with other waqf authorities• shareholders

Ownershipshareholders

• REITs have tax advantage‐ no tax on the capital growth• Waqf tax exemption status in S’pore

Tax and Di id d

q p p• Cross border REITs in turkey where waqf is taxableDividend

27

Issues in Waqf REITsIssues in Waqf REITs

• Perpetuity

Assets

• Perpetuity• Halal activities• Enough quality assets

Ownership

• Muslims and non‐muslims

• Selling of waqfassets

Managment

Control

• Trustees and mutawallis

• Board of DirectorsControl

• Pte vs Public REITs

Cost and Competit

• Transaction cost‐ 7‐8%

• Return vs assets Competitiveness

Return vs assets classes

• Investors concerned

28

Overcoming issuesOvercoming issues

IssuesIssues

Assets‐ perpetuity Sell the waqf assets to the REITs mgtco. on a leasehold property

‐ quality assets Consider cross border Reits

Ownership No problem as it is sold on a leaseholdOwnership No problem as it is sold on a leaseholdbasis

Mgt Control ‐ Pte vs Public To go private first solely based on cost and the sensitivity dealing with waqfand the sensitivity dealing with waqfproperties

Investors concerned A lot of public education needed

29

Using Using IstibdalIstibdal, , SukukSukukMusharakahMusharakah

• Acquistion/Refurbishment New waqf6-storey office building at Beach Rd y g– 2002

30

Before Refurbishment After Refurbishment

Case Study Case Study 3 3 (Asset Migration):(Asset Migration):11 Beach Rd11 Beach Rd-- SukukSukuk11 Beach Rd11 Beach Rd SukukSukuk

Many Low Quality AssetsSingle High Quality Asset

Asset MigrationParticipation from 45 awqaf Asset Migration

(5 years programme)

Shophouses Office Bldg20 units – 34,000 sf 1 building - 34,000 sf

Income: Increase 5 fold

Office Bldg

31

Yield 1% Yield 3.9%

WaqfWaqf DevelopmentDevelopmentWaqfWaqf Development Development –– Case Study : 11 Beach RdCase Study : 11 Beach Rd

Musharaka Partnership

MUIS as Bond Issuer

$ $Investors MUIS waqf Fund

$0.875 mil $0.315 mil

$25 mil $9 mil73.5% Share

SPV1

Advance $34 milReturn $1.19 mil

EBITDA $1.19 mil

SPV2

Ijara AgreementBuilding Expenses

Rental $1.19 mil

EBITDA $1.5 mil

32

SPV2$0.31 mil (Aft Rental $0.31 mil)

Gross Revenue $1.8 mil

Akin to REITs structureAkin to REITs structureParticipation from 45 awqafE h f d th b ildi th h h Each waqf owned the building through share ownership in the company holding the propertypropertyIncome distributed to the waqf shareholders based on the amount contributedbased on the amount contributedValuation based on market valuation of share

ti i tiupon participationAdvantages‐ owning property through share

hiownership.

33

SNAPSHOT OF WAKAF IN SINGAPORE

Assets worth abt half a billion.Assets worth abt half a billion.101 awqafAnnual income of about $12 millionAnnual income of about $12 million.Annual disbursement exercise done for beneficiariesbeneficiariesAudited accounts h ll d b d k fWholly owned subsidiary to manage wakaf

development. ISO 9001 on wakaf administration and processes. 34

ConclusionConclusionThere are wide ranges of opportunities and availability of investment products for waqfavailability of investment products for waqfto invest in to suit waqf nature of investmentFinancing and development is possible for Financing and development is possible for waqf assets and should not be a deterrent for the further development of waqfthe further development of waqfWhere trusts have thrived , waqf could also mirror the manner trusts have evolved in its mirror the manner trusts have evolved in its investment and its legal advancement.More creativity should be exercise as waqf is More creativity should be exercise as waqf is based on ijtihadi laws

35