Integration of Waqf, Zakat, Sadaqat, in Islamic Microfinance

41

A Review Of Affordability and Integration Of Zakat And Waqf In Islamic Microfinance PRESENTED BY: Assoc .Prof. Dr. Mohammad Tahir Sabit Haji Mohammad 29 JUNE 2013

Transcript of Integration of Waqf, Zakat, Sadaqat, in Islamic Microfinance

A Review Of Affordability and Integration Of Zakat

And Waqf In Islamic Microfinance

PRESENTED BY:Assoc .Prof. Dr. Mohammad Tahir Sabit Haji Mohammad29 JUNE 2013

Contents • Introduction• The problem (questions about the effectiveness

of Microfinance of the poor)• Current scenario

– The cost of microcredit– The effect– Affordability of Loan– Over-indebtedness and debt-trap

– Sustainability of IsMFI• The Proposal for tomorrow

– Ideal Islamic micro finance– A zakat, sadaqat and waqf based microfinance

• Suggestions for strong Islamic micro finance• Conclusion

INTRODUCTION• Normally, if A wishes to start a business

– A (borrower) asks B (lender/ bank) for a loan,

– B demands collateral for security of the loan.

– A provides land, building, or some negotiable instrument as security.

– If satisfied, then, B lends money to A. (A is bankable)

• The big majority of the poor have no property, and hence they are unable to borrow from conventional banks. (they are not bankable)

• Poor therefore is unable to start his business.

• Micro finance fills the above gape: replaces traditional security with individual and group guarantees and strict monitoring.

• Micro Finance is now offered in conventional and Islamic forms.

Micro finance is for the unbankableWho lack collateral and security for loan

• Conventional Microfinance was praised for providing to non-bankable person ‘access to credit to start or run a business, or offering them savings and insurance services that help them maintain and improve their human and social capital throughout their lives’ (See Matin, Hulme, and Rutherford, 1999)

• But conventional micro-financing institutions are not looked favourably today (Morduch and Haley, 2002; Amin et al, 2003; Roodman and Morduch, 2009; Young, 2010).

• They are making high profits at the expense of the poor (Mishra, 2006; Vakulabharanam, 2005; Mitias, 2010).

• Islamic microfinance in the Middle East is viewed even expensive.

MFI was praised because it presumably helped the poor

But now it is criticized for being expensive

IsMFIs are viewed by some to be even more expensive

The problemThe questions to be asked:• Does microfinance help the poor and hence effective, or is it a tool to trap the poor in poverty and make the predators richer.

• Is this true about Islamic Microfinance? • If yes, then why? and • how to improve it?The following discussion answers these questions in terms of cost and affordability of microcredit, the issue of sustainability and efficiency of micro financing institutions, and affirms the suggested solution through waqf and zakat and the need for further refinement of such solution.

Current scenario

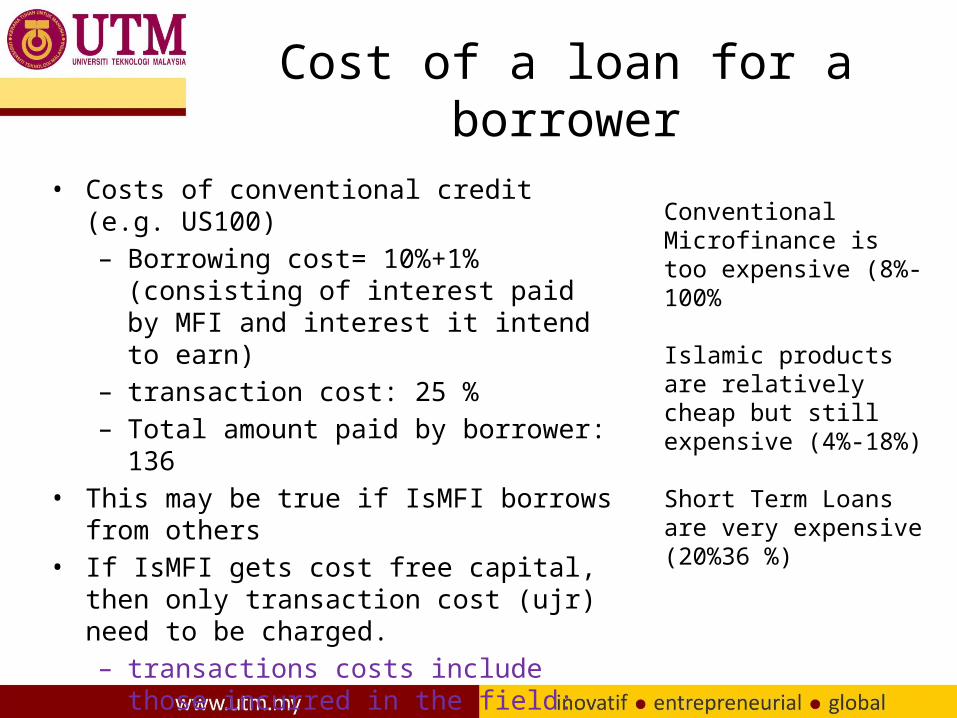

Cost of a loan for a borrower

• Costs of conventional credit (e.g. US100)– Borrowing cost= 10%+1% (consisting of interest paid by MFI and interest it intend to earn)

– transaction cost: 25 %– Total amount paid by borrower: 136

• This may be true if IsMFI borrows from others

• If IsMFI gets cost free capital, then only transaction cost (ujr) need to be charged.– transactions costs include those incurred in the field: supervision and monitoring, and those in the headquarters of the MFI or IsMFI, overhead and fixed costs.

Conventional Microfinance is too expensive (8%-100%

Islamic products are relatively cheap but still expensive (4%-18%)

Short Term Loans are very expensive (20%36 %)

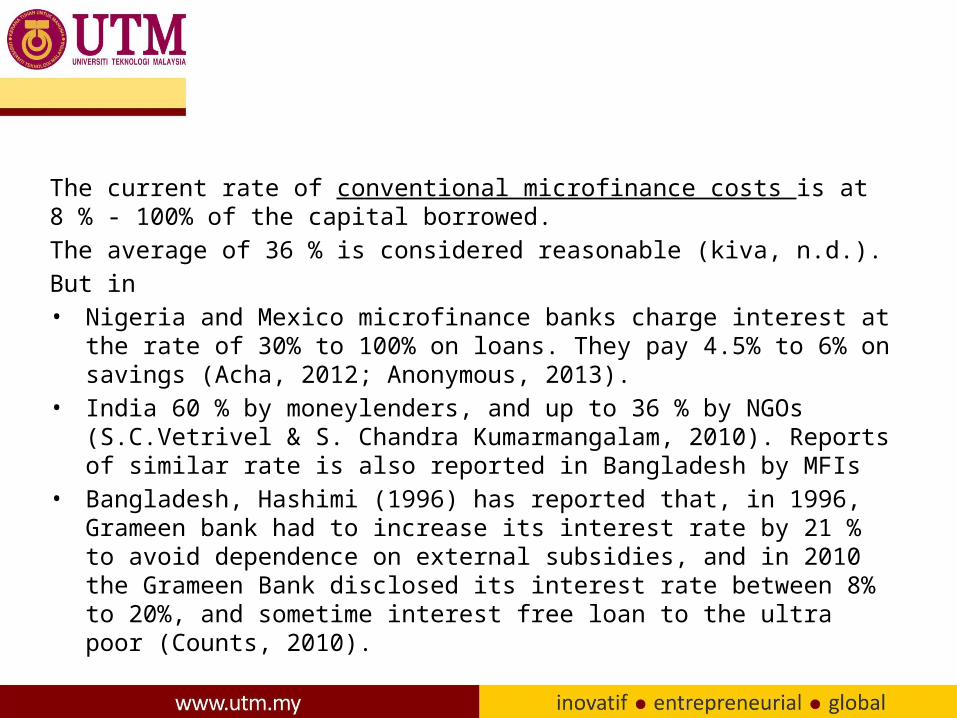

The current rate of conventional microfinance costs is at 8 % - 100% of the capital borrowed.The average of 36 % is considered reasonable (kiva, n.d.).But in • Nigeria and Mexico microfinance banks charge interest at

the rate of 30% to 100% on loans. They pay 4.5% to 6% on savings (Acha, 2012; Anonymous, 2013).

• India 60 % by moneylenders, and up to 36 % by NGOs (S.C.Vetrivel & S. Chandra Kumarmangalam, 2010). Reports of similar rate is also reported in Bangladesh by MFIs

• Bangladesh, Hashimi (1996) has reported that, in 1996, Grameen bank had to increase its interest rate by 21 % to avoid dependence on external subsidies, and in 2010 the Grameen Bank disclosed its interest rate between 8% to 20%, and sometime interest free loan to the ultra poor (Counts, 2010).

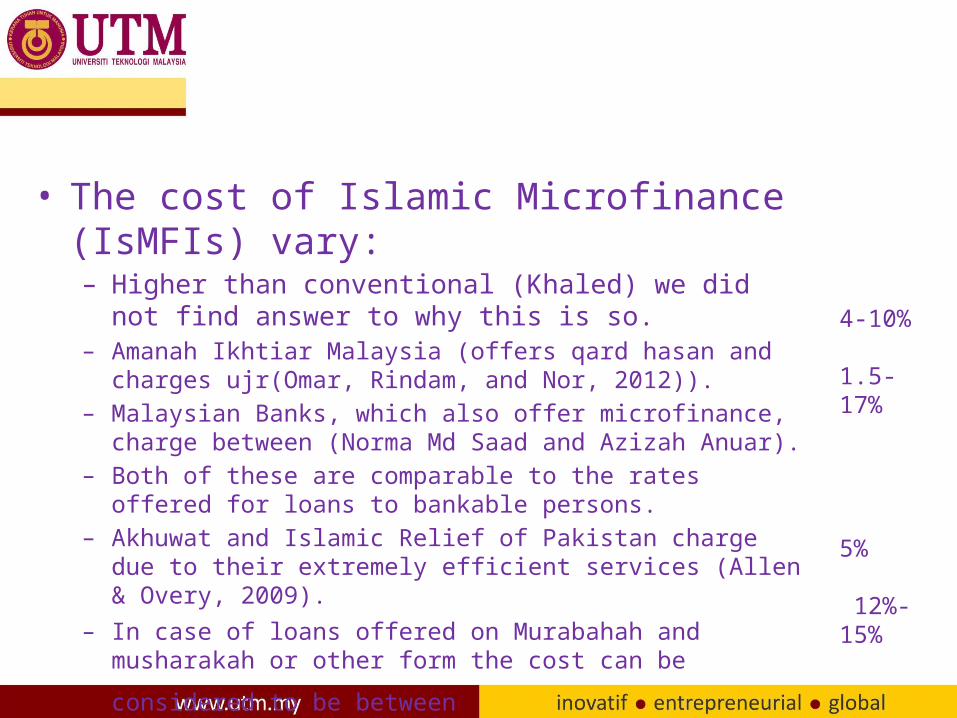

• The cost of Islamic Microfinance (IsMFIs) vary:– Higher than conventional (Khaled) we did not find answer to why this is so.

– Amanah Ikhtiar Malaysia (offers qard hasan and charges ujr(Omar, Rindam, and Nor, 2012)).

– Malaysian Banks, which also offer microfinance, charge between (Norma Md Saad and Azizah Anuar).

– Both of these are comparable to the rates offered for loans to bankable persons.

– Akhuwat and Islamic Relief of Pakistan charge due to their extremely efficient services (Allen & Overy, 2009).

– In case of loans offered on Murabahah and musharakah or other form the cost can be considered to be between

4-10%

1.5-17%

5%

12%-15%

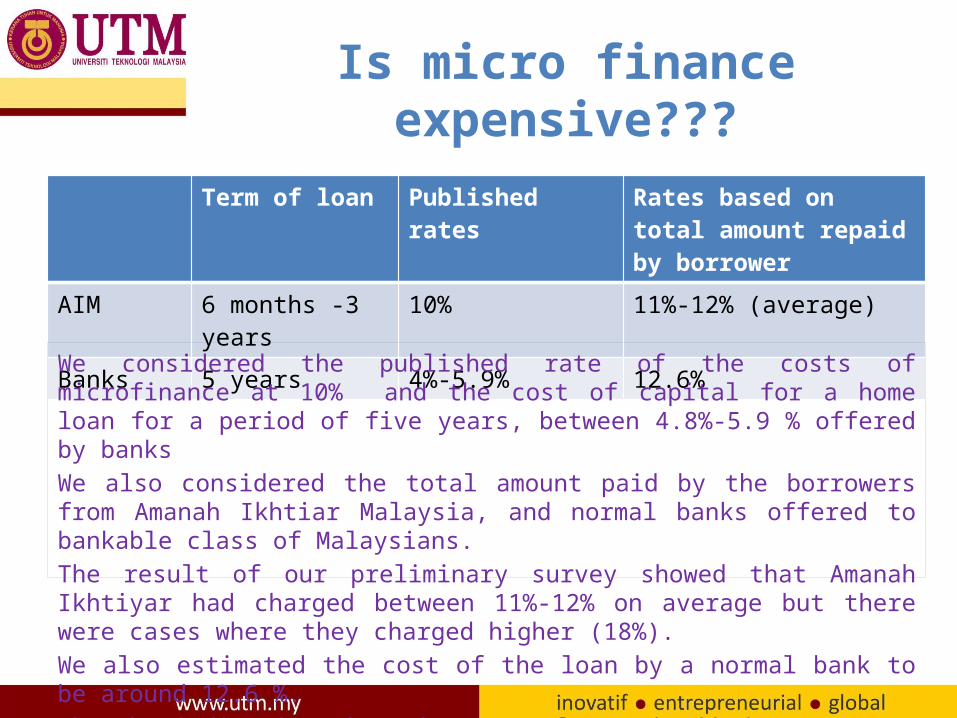

Is micro finance expensive???

Term of loan Published rates

Rates based on total amount repaid by borrower

AIM 6 months -3 years

10% 11%-12% (average)

Banks 5 years 4%-5.9% 12.6%We considered the published rate of the costs of microfinance at 10% and the cost of capital for a home loan for a period of five years, between 4.8%-5.9 % offered by banksWe also considered the total amount paid by the borrowers from Amanah Ikhtiar Malaysia, and normal banks offered to bankable class of Malaysians. The result of our preliminary survey showed that Amanah Ikhtiyar had charged between 11%-12% on average but there were cases where they charged higher (18%). We also estimated the cost of the loan by a normal bank to be around 12.6 %.Thereby indicating that the rate of Amanah Ikhtiar was most of time the same and sometime slightly cheaper, provided the term of loan is not less than one year.

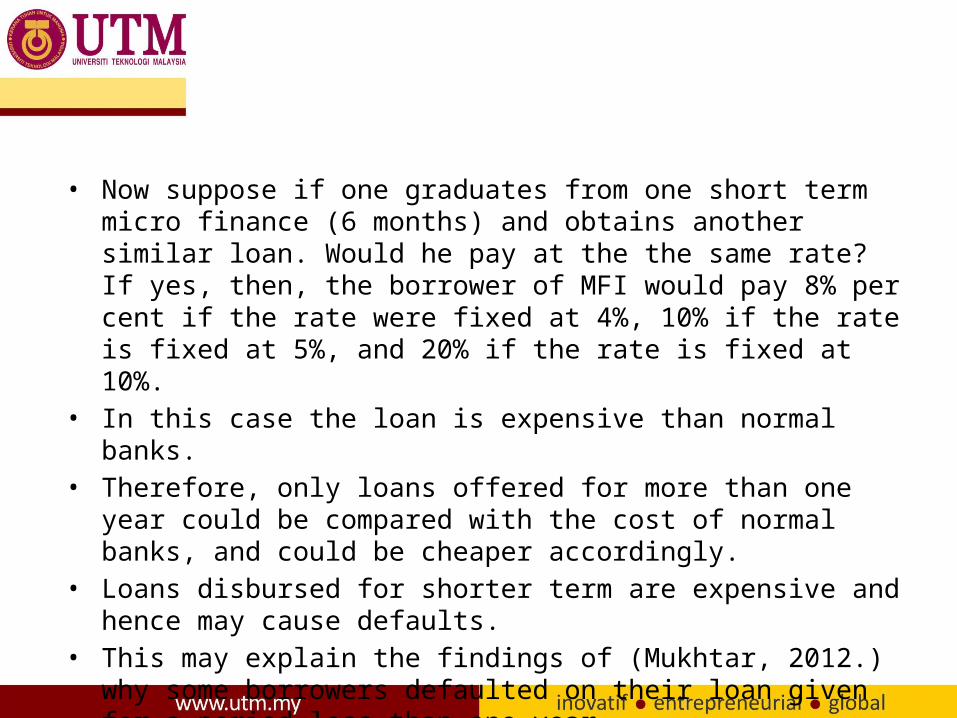

• Now suppose if one graduates from one short term micro finance (6 months) and obtains another similar loan. Would he pay at the the same rate? If yes, then, the borrower of MFI would pay 8% per cent if the rate were fixed at 4%, 10% if the rate is fixed at 5%, and 20% if the rate is fixed at 10%.

• In this case the loan is expensive than normal banks.

• Therefore, only loans offered for more than one year could be compared with the cost of normal banks, and could be cheaper accordingly.

• Loans disbursed for shorter term are expensive and hence may cause defaults.

• This may explain the findings of (Mukhtar, 2012.) why some borrowers defaulted on their loan given for a period less than one year.

• A corelationship however is not established yet

The effect• Norma and Azizah (2009) surveyed 1803 program participants in Malaysia. She found that – 42.7 % felt they were either indifferent or worse.

• Her study does not shed light on the ability of the participants to pay their loans, or on the reasons why the 42 per cent of the population was unable to escape from poverty.

• This therefore makes one asking: – is Islamic finance affordable?

The Poor is indifferent or worse off

Why???

Are such loans affordable?

AFFORDABILITY OF LOAN

• The capacity of the borrower to repay the loan with ease, its positive effect on the borrowers (Lashley, 2004) is significant as well as the sustainability of the Islamic MFI itself.

• An Islamic micro finance should be judged based on the capacity of the borrower first.

Consider

affordability and

sustainability of IsMFI

• We consider the aggregate periodical income of the borrower before and after the loan.

• The income after the deduction for the amount of the loan

• The sum for gross periodical repayment (loan repayment, savings, and others)

• If the deductions exceeds the limit where provisions from the borrowed sum makes the borrower unable to pay for the costs of necessaries, then it would be unaffordable and expensive,

• We followed the normal criteria for the affordability of house loans. This may seem too high but micro borrowers subjected to even higher.

Consider the income of borrower• before the

loan• After the

loan• And after

the deduction

Can the borrower pay for his necessaries?

Housing loans affordability criteria was followed (33%38%)

• We did not find clear answer from previous studies in regard to the affordability of the loans offered by Islamic Micro financing Institutions. Mere increase of income (50%-215%) was reported. – Microfinance indicate the increase of income at

rang of 50%-215% after the loans were given (AIM 1988, 1990, 2008; Kasim, 2000, and 2005, Salma 2006; and Omar, Rindam, and Nor, 2012; Mokhtar, 2012), Bangladesh (Khandker, Samad and Khan, 1998; Hossain, 1988), Ghana and South Africa (Afrane, 2002). Ahmad (2002) reported increase in volume of goods/services, diversification into new goods/services, increase in assets, improved premises.

– However they do not prove whether such increase was after the deduction of loan payment or otherwise

Both Increase of income and change of lifestyles are reported.

This may indicate in some cases affordability of the loan

• Since the amount of loans and repayment is fixed, we assume affordability of the loan may depend on the amount borrowed and income earned.

• Supposing the income of the borrower is 1000 before the credit, and was increased 100% to 2000, but had to repay 900 per month, there would be an increase of 100 per month after repayment. Here the cost of loan could be acceptable.

• But if we suppose the income of the borrower has increased from one 1000 to 1800 or less, and the monthly instalment is 900, in such a case, if 50 per cent of the gross income were spent on repayment of the loan the borrower would be worse off than he was before.

• The loan therefore may benefit the MFI rather the borrower. Where income decreases further, to that extent the borrower may sink in poverty.

• As loan can be granted for a week (Davis, n.d), for a year (Mokhtar, 2012), 3 years (Omar, 2012) small loans given on a very short-term basis would be less affordable. One would doubt the claim of 50%-215 of increase in income could solve the question of unaffordability.

But it is assumed all borrowers may not be lucky

Default of loans or over-indebtedness may occur

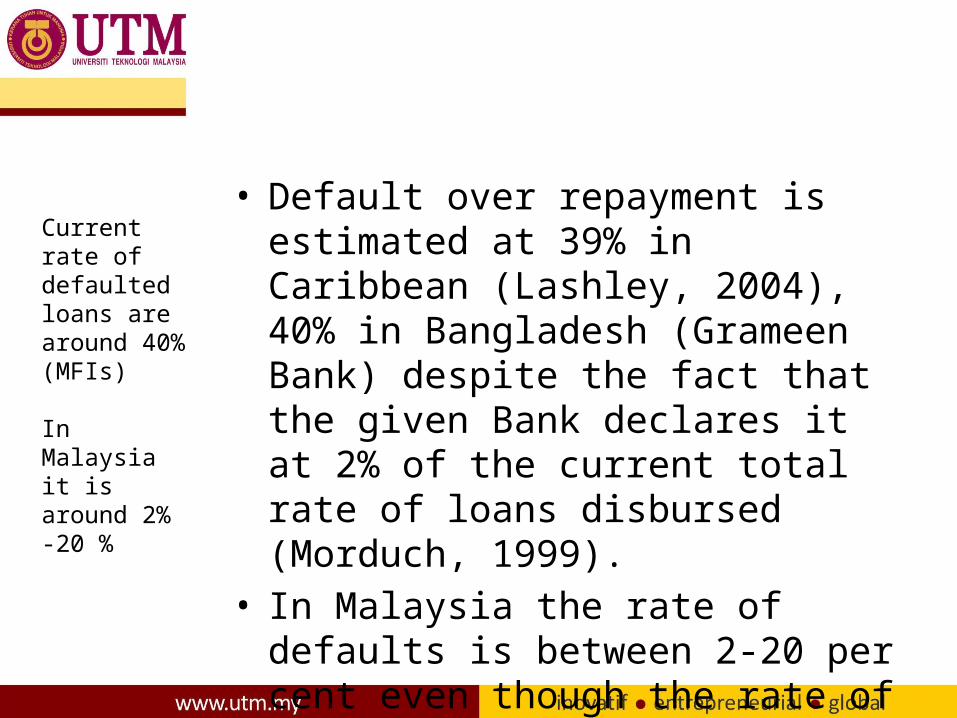

• Default over repayment is estimated at 39% in Caribbean (Lashley, 2004), 40% in Bangladesh (Grameen Bank) despite the fact that the given Bank declares it at 2% of the current total rate of loans disbursed (Morduch, 1999).

• In Malaysia the rate of defaults is between 2-20 per cent even though the rate of periodical instalments is not as high as in other countries.

Current rate of defaulted loans are around 40% (MFIs)

In Malaysia it is around 2% -20 %

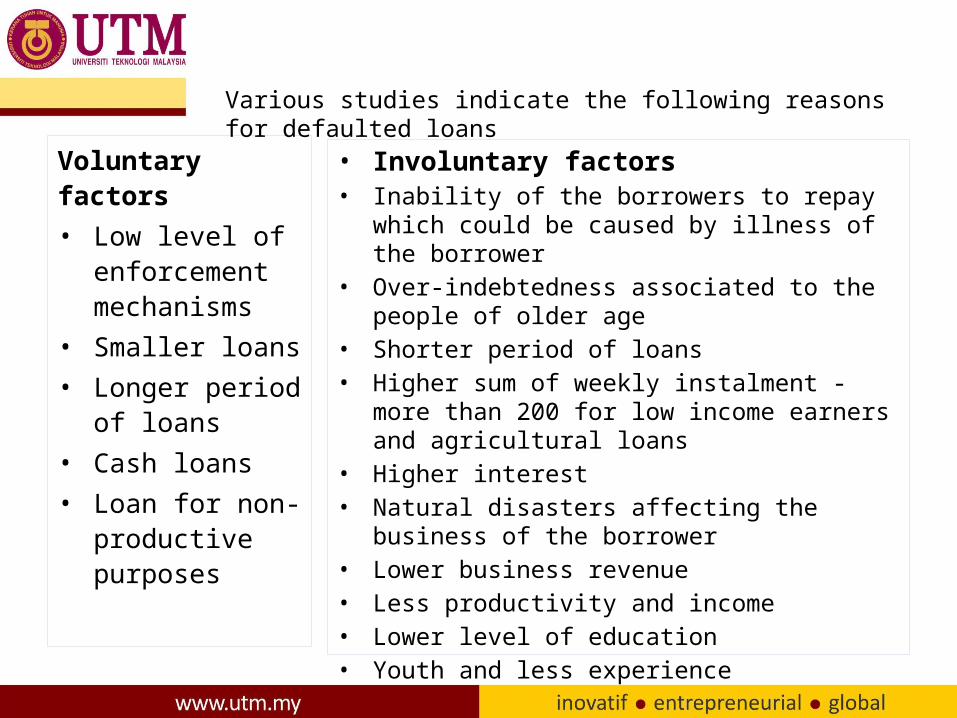

Voluntary factors• Low level of

enforcement mechanisms

• Smaller loans • Longer period

of loans • Cash loans • Loan for non-

productive purposes

• Involuntary factors• Inability of the borrowers to repay

which could be caused by illness of the borrower

• Over-indebtedness associated to the people of older age

• Shorter period of loans• Higher sum of weekly instalment -

more than 200 for low income earners and agricultural loans

• Higher interest • Natural disasters affecting the

business of the borrower • Lower business revenue• Less productivity and income • Lower level of education • Youth and less experience

Various studies indicate the following reasons for defaulted loans

OVER-INDEBTEDNESS AND DEBT-TRAP

• Expensive loans • Higher weekly payments, may cause loan defaults as a result of lower income.

• Consequent penalty and higher interest may be charged.

• For these more money may be borrowed and

• eventually this could results in over-indebtedness.

• Over-Debtedness is the worst of all results.

• This ties the borrower to the lender, which is a trap that cripples borrowers.

• It will not only be considered the contemporary form of slavery but it may also bring down the given MFI, as it would not be able to lend funds and hence become unsustainable.

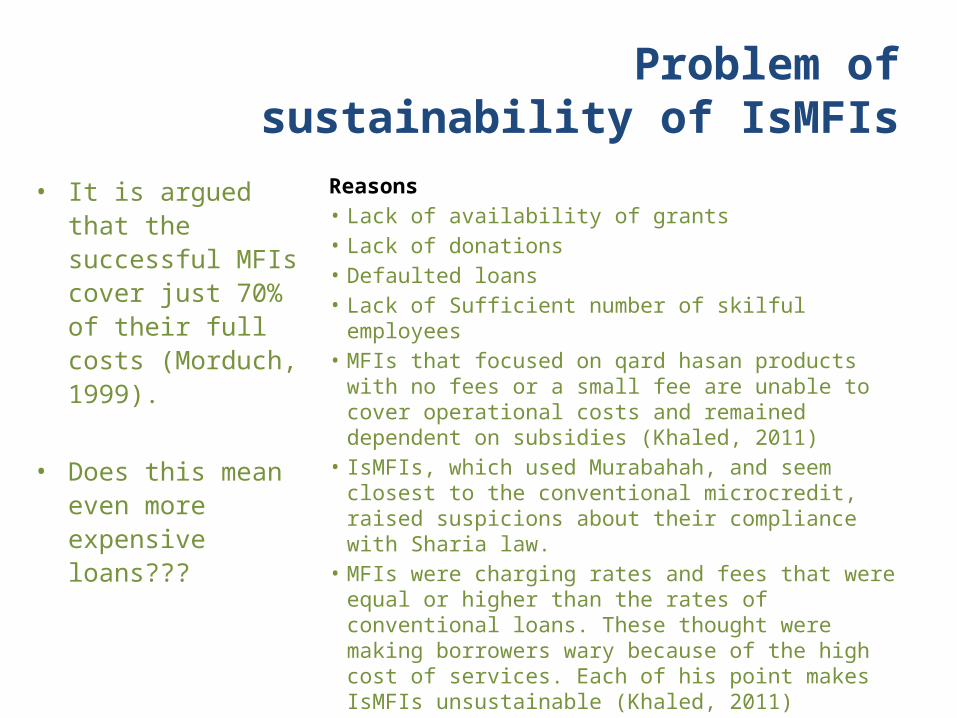

Problem of sustainability of IsMFIs

• It is argued that the successful MFIs cover just 70% of their full costs (Morduch, 1999).

• Does this mean even more expensive loans???

Reasons• Lack of availability of grants• Lack of donations• Defaulted loans• Lack of Sufficient number of skilful employees

• MFIs that focused on qard hasan products with no fees or a small fee are unable to cover operational costs and remained dependent on subsidies (Khaled, 2011)

• IsMFIs, which used Murabahah, and seem closest to the conventional microcredit, raised suspicions about their compliance with Sharia law.

• MFIs were charging rates and fees that were equal or higher than the rates of conventional loans. These thought were making borrowers wary because of the high cost of services. Each of his point makes IsMFIs unsustainable (Khaled, 2011)

• In all fairness, IsMFIs may have benefited many poor Muslims, nevertheless, lessons need to be learned from the failures of conventional MFIs.

• There is no harm in rebranding old concepts but, as Muslims, we have to uphold our own divine concepts of zakat and waqf which were and would be truly effective in eradication of poverty in Muslim societies

The Proposal for tomorrow

• What can distinguish an Islamic institution from a conventional is the the essence and spirit of Islamic financial products it offers to the market.

• This is achievable through utilisation of zakat, sadaqat and awqaf funds and properties.

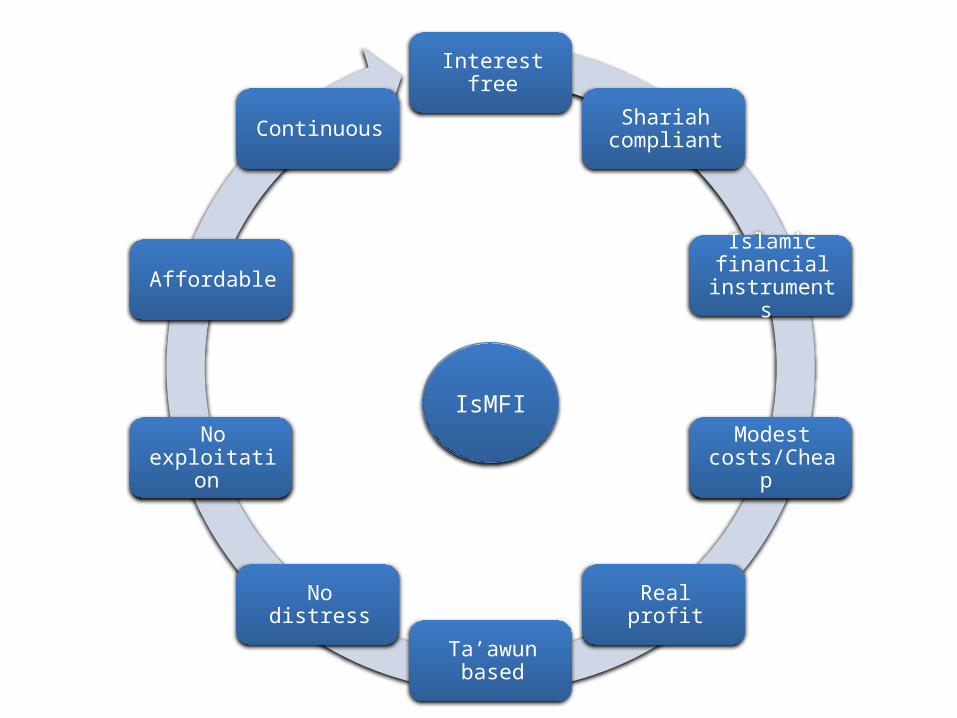

IDEAL ISLAMIC MICRO FINANCE

IsMFI

Interest free

Shariah compliant

Islamic financial instrument

s

Modest costs/Chea

p

Real profit

Ta’awun based

No distress

No exploitati

on

Affordable

Continuous

A ZAKAT, SADAQAT AND WAQF BASED MICROFINANCE

• Ahmad (2004), Obaidullah and Khan (2008), Obaidullah, 2008a) revived this idea. And why not?

• Poverty eradication is one of objective of charitable funds in Islam, as clearly mentioned in al-Quran, 9:60.

• Since the objective of an IsMFI would be the alleviation of poverty, zakat and sadaqat are ideal for its eradication.

• The mission of an IsMFI would be the attraction of charitable funds, their investment and income generation, in case of waqf, and the mobilisation of disposable funds to the asnaf and the beneficiaries of awqaf.

• Some (IMF, 2002; Nimrah Karim, Michael Tarazi, and Xavier Reille, 2008) may tell us not to rely on such funds, but to us charitable funds should form the essence of Islamic microfinance.

• The use of zakat for qard hasan fund, for the benefit of the extremely poor when they are unable to make their timely payments or for the development project of community has been reported by UNDP (2012).

• In the context of microfinance the first point would be to allow some loans to be written off and the subsidy should come from the zakat and other disposable charitable funds.

• The use of zakat funds should be in line with Asnaf mentioned in al Quran, which should at least be for their benefit, in the sense of possession of the ruqbah, manf’ah, or intifa’.

• Investment and loans should come from awqaf properties and funds (cash and real estates).

• A basic illustration based on opinions of Ubaidullah and other scholars with some modification is offered below.

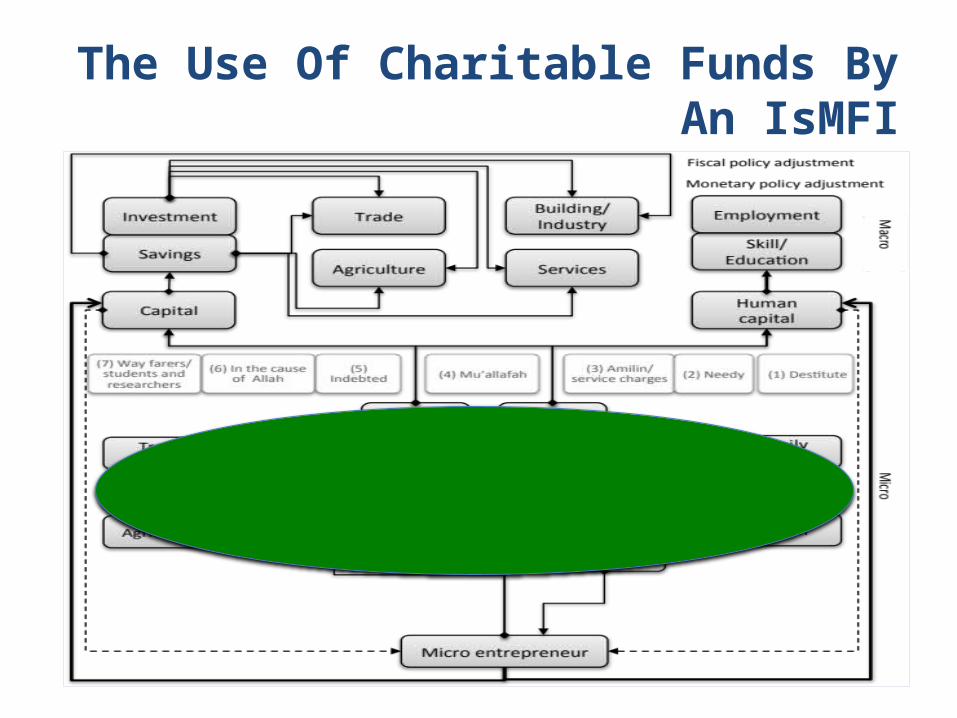

The Use Of Charitable Funds By An IsMFI

• Suggestions for a strong Islamic Micro Finance

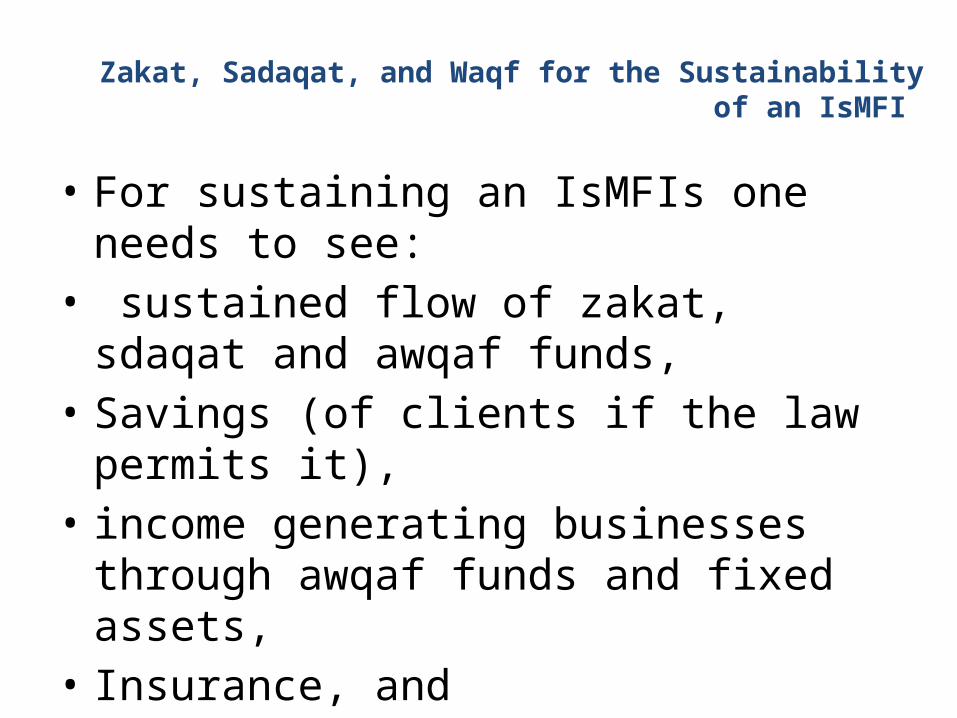

Zakat, Sadaqat, and Waqf for the Sustainability of an IsMFI

• For sustaining an IsMFIs one needs to see:

• sustained flow of zakat, sdaqat and awqaf funds,

• Savings (of clients if the law permits it),

• income generating businesses through awqaf funds and fixed assets,

• Insurance, and • Professional and systematic management.

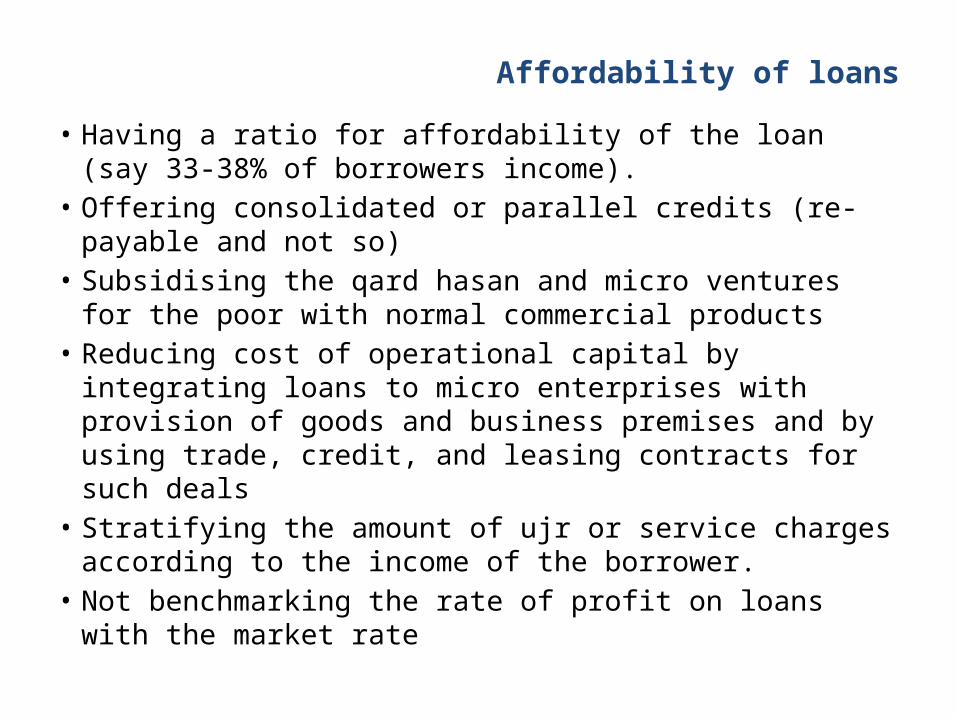

Affordability of loans• Having a ratio for affordability of the loan (say 33-38% of borrowers income).

• Offering consolidated or parallel credits (re-payable and not so)

• Subsidising the qard hasan and micro ventures for the poor with normal commercial products

• Reducing cost of operational capital by integrating loans to micro enterprises with provision of goods and business premises and by using trade, credit, and leasing contracts for such deals

• Stratifying the amount of ujr or service charges according to the income of the borrower.

• Not benchmarking the rate of profit on loans with the market rate

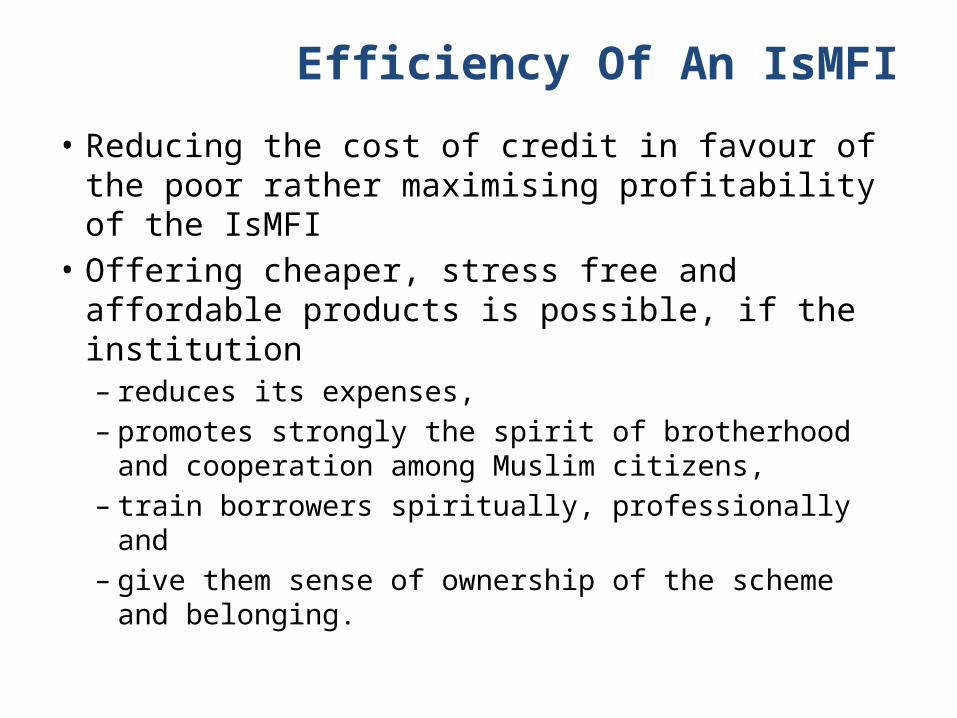

Efficiency Of An IsMFI• Reducing the cost of credit in favour of the poor rather maximising profitability of the IsMFI

• Offering cheaper, stress free and affordable products is possible, if the institution – reduces its expenses, – promotes strongly the spirit of brotherhood and cooperation among Muslim citizens,

– train borrowers spiritually, professionally and

– give them sense of ownership of the scheme and belonging.

Alternative Way For Effective IsMFI

• Offering credit for a term not less than one year and demand monthly instalments, except when weekly instalments are needed. These may reduce the cost

• Employing few capable but religiously motivated individuals who possess the spirit of volunteerism (tatawu’)

• Exploiting the current Internet-based technology for monitoring and enforcement purposes from headquarters and regional offices

Continue…• Utilising the existing online banking system, if any, for loan application, monitoring, and collection of loan instalments

• Reducing training sessions by employees

• Providing training to the trainers in few selected geographically strategic centres without adducing additional cost or with relatively less costs.

Continue…• Appointing mosques and community leaders to monitor and collect loans, to be trained and train new clients as well as to conduct workshops regularly in their mosques and community halls.

• Elevating IsMFIs to Waqf (and zakat) banks and thus reduce cost of capital, transactions, and operation

Continue…• Venturing in wholesale businesses or • investing in companies that provide goods needed by the majority of clients of the institution, or

• appointing panels that agree to sell, and deliver goods to the customers at no costs attributed to the latter

• Using zakat, and sadaqat funds for operational expenses, for instance, training, workshops, occasional monitoring and enforcement, purchase of equipment and technology.

• collaboration with a network of donors of charitable funds, distributors of donated funds, governmental agencies, and other organisations who target poverty eradication as part of their corporate social responsibility.

Continue…• Collaboration should not be restricted to the attraction and distribution of funds or identifying the right beneficiaries, but also working on a comprehensive strategic plan for the overall development of the poor on individual, village and regional levels.

CONTINUE..• Supposing there is a waqf bank it can collaborate with other Islamic MFIs

• Its funds can be used for – income generating enterprises, – Trust IsMFI to screen the eligible poor and needy entrepreneurs and

– give grants for microbusiness on Murabahah, and mudarabah basis.

CONTINUE…– Collected loans and profits can be recycled once again.– Loan to poor can be given on qard hasan basis with some service charges (2-3%) for basic needs.

– Awqaf properties can be leased to the poor. • These will need additional planning for development and construction of waqf lands and buildings to cater for microbusinesses, training and educational centres

–Can establish a not-for-profit goods and products businesses of its own and then –Use their income for the benefit of poor in terms of their income and supply to the poor micro entrepreneurs.

CONCLUSION…• To fill the gap, a waqf, and zakat based microfinance is needed,

• It could be effective in eradication of poverty if charitable funds are effectively utilised.

• A good business plan and legal framework is in place, and

• A wider and comprehensive planning in terms of collaboration with governmental agencies and other NGOs is made.

Wa Billah al Tawfiq wa alhidayahand

Thank You