Confidential BUSINESS PLAN August 2008

81

IWC INTERNATIONAL WOOD CORPORATION FOREST & NATURAL RESOURCES MANAGEMENT Recipient ___________________ Plan Number ___________________ Confidential BUSINESS PLAN August 2008 Roy I. Schwartz, President and Director +1 954 746-8845 www.iwcusa.net

Transcript of Confidential BUSINESS PLAN August 2008

IWC INTERNATIONAL WOOD CORPORATION FOREST & NATURAL RESOURCES MANAGEMENT

Recipient ___________________ Plan Number ___________________

ConfidentialBUSINESS PLANAugust 2008

Roy I. Schwartz, President and Director+1 954 746-8845www.iwcusa.net

© 2008 Growthink, Inc.This confidential document contains proprietary information that constitutes trade secrets. It is not to be

shared, copied, disclosed, or otherwise compromised without the prior written consent of themanagement of Growthink, Inc.

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 2

This Business Plan (and any/all drafts and parts thereof) is/are based uponinformation supplied by International Wood Corporation, its managingexecutives, and its stockholders or membership shareholders (collectively the“Company”, and/or “management”, and is being furnished on a confidentialbasis, solely for use by prospective investors in and/or potential strategicbusiness associates of the Company (collectively “recipient”). The use ordistribution of this Business Plan to any other parties or for any otherpurposes is not authorized.Neither the author (Growthink, Inc., and its employees and contractors) northe Company, nor any of its employees, affiliates or representatives makes anyrepresentation or warranty, express or implied, as to the accuracy orcompleteness of any of the information contained in this Business Plan or inany other written or oral communication transmitted or made available to arecipient. Each of such parties expressly disclaims any and all liabilityrelating to or resulting from the use of this Business Plan or suchcommunications by a recipient or any of its affiliates or representatives.Only those specific, express representations and warranties, if any, which maybe made to a recipient in one or more definitive written agreements when, asand if executed, and subject to all such limitations and restrictions as maybe specified in such definitive written agreements, may be relied on by arecipient or have any legal effect whatsoever.Material portions of the information presented in this Business Planconstitute “forward-looking statements” which can be identified by the use offorward-looking terminology such as “may”, “will”, “expect”, “anticipate”,“estimate”, “plan”, or “continue” or the negative form thereof or othervariations thereon or comparable terminology. Such forward-looking statementsrepresent the subjective views of the management of the company, andmanagement’s current estimates of future performance are based on assumptionswhich management believes are reasonable but which may or may not prove to becorrect. There can be no assurance that management’s views are accurate orthat management’s estimates will be realized, and nothing contained herein isor should be relied on as a representation, warranty or promise as to thefuture performance or condition of the Company. Industry experts may disagreewith these assumptions and with management’s view of the market and theprospects of the Company.The sole purpose of the Business Plan is to assist a recipient in decidingwhether to proceed with further investigation, but this Business Plan does notpurport to contain all material information that an interested party mightconsider in investigating the Company. A recipient should conduct his or herown independent analysis and investigation. This Business Plan shall not beconstrued to indicate that there has not been any change in the financialcondition, business, operations, plans or other affairs of the Company sincethe date of preparation. The Company does not expect to update or otherwiserevise this Plan to reflect any such changes.

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 3

The recipient of this Business Plan acknowledges and agrees that: (a) all ofthe information contained herein or received in written or oral form from theCompany will be kept confidential; (b) the recipient will not reproduce thisPlan, in whole or in part; (c) if the recipient does not wish to pursue thismatter, it will return the Business Plan to the Company as soon aspracticable, together with any other material relating to the Company whichthe recipient may have received from the Company; and (d) proposed actions bythe recipient which are inconsistent in any manner with the foregoingagreement will require the prior written consent of the Company.THIS BUSINESS PLAN IS FOR INFORMATIONAL PURPOSES ONLY AND DOES NOT CONSTITUTEAN OFFER TO SELL OR THE SOLICITATION OF AN OFFER TO BUY ANY SECURITIES.The Company reserves the right, in its sole discretion, to reject any and allproposals made by or on behalf of any recipient, to accept any such proposal,to negotiate with one or more recipients at any time, and to enter into adefinitive agreement without prior notice to other recipients. The Companyalso reserves the right to terminate, at any time, further participation inthe investigation and proposal process by, or discussions or negotiationswith, any recipient without reason.

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 4

Table of Contents

Executive Summary...........................................................5International Wood Corporation.....................................................5Products...........................................................................5Revenue............................................................................5IWC and sustainability.............................................................7Government regulations.............................................................8Management team....................................................................8Financial plan.....................................................................9Summary of financial projections...................................................9Corporate structure and headquarters...............................................9

Carbon Market Overview.....................................................10Greenhouse effect.................................................................10Greenhouse gases..................................................................10Kyoto Protocol....................................................................11Emission trading scheme (ETS).....................................................13Market structure and market players...............................................13Exchange centers..................................................................14Case studies......................................................................16

Carbon Market Analysis.....................................................18The carbon market (volumes and values)............................................18Market growth.....................................................................19Market challenges.................................................................21Key market trends.................................................................22The buyers........................................................................25The sellers.......................................................................25Market outlook....................................................................26

Chicago Climate Exchange (CCX) Overview....................................28CFI contracts (the CCX tradable commodity)........................................28CCX mission.......................................................................28CCX offsets program...............................................................28Forestry Carbon Emission Offsets..................................................29Harvest option and protocol for sustainably managed forests.......................29

Operational Plan...........................................................32Organizational structure..........................................................32Staffing..........................................................................32Implementation plan...............................................................33Management team...................................................................34

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 5

Facilities and insurance..........................................................35Financial Plan.............................................................36

Capitalization....................................................................36Use of private placement proceeds.................................................36Summary of financial projections..................................................37Exit strategy.....................................................................37

Key Investment Considerations..............................................38Proprietary knowledge.............................................................38Unique position in the market.....................................................38Ongoing relationships with key industry players...................................38Time to profitability.............................................................38Exceptional management team.......................................................38Dividends, returns, and exit strategies...........................................39

Risk Factors...............................................................40Nature of the company.............................................................40Performance risk..................................................................40Market risk.......................................................................41Competition.......................................................................41Growth and continuing operations..................................................41

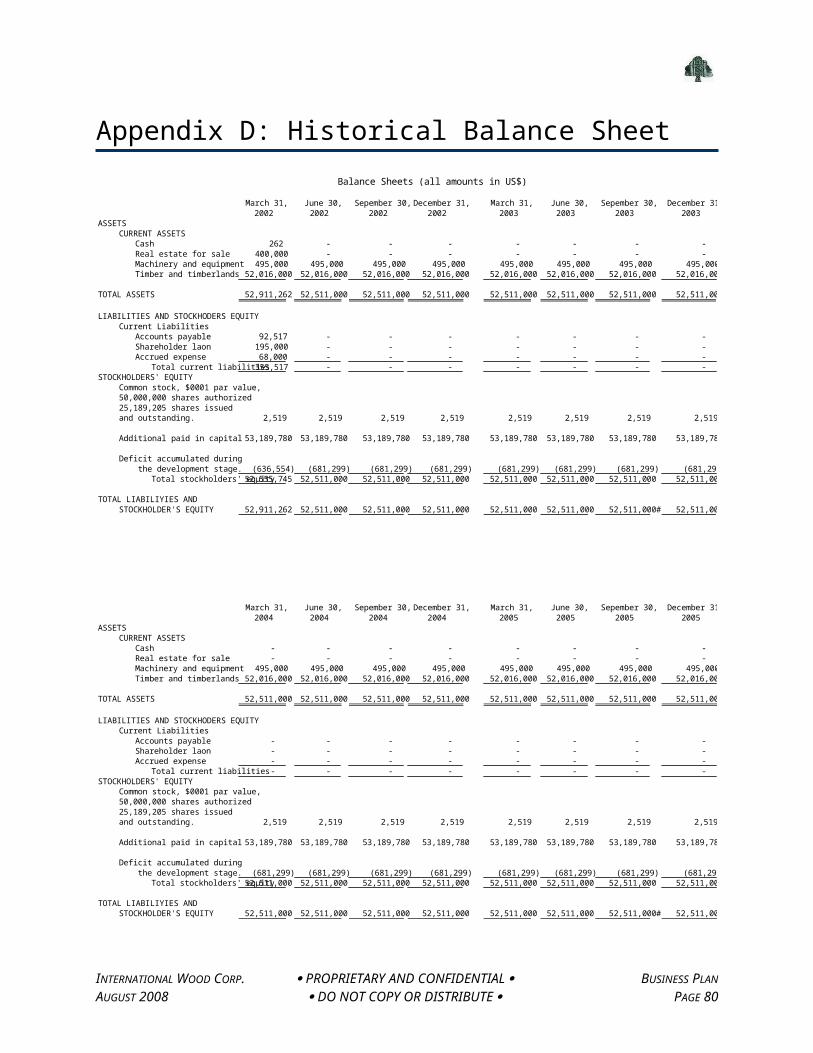

Appendix A: Assumptions And Financial Projections..........................42Appendix B: Kyoto Protocol Glossary........................................47Appendix C: 1998 Appraisal Of IWC-Owned Land...............................51Appendix D: Historical Balance Sheet.......................................59

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 6

Executive SummaryInternational Wood Corporation

International Wood Corporation (“IWC” or the “Company”), along with itspredecessors and subsidiaries, owns approximately forty four thousand acres ofmanaged forest in Brazil. The Company also has options to purchase up to anadditional two million acres (from a predecessor company or directors of IWC).The Company’s forestry holdings, including options, are valued at more than$900 million.A Colorado corporation with its main office in Ft. Lauderdale, Florida, IWC isnow seeking new capital to begin various activities designed to generate salesexceeding $100 million within 5 years. The Company will accomplish this byutilizing production from existing owned forests, acquisition of new land,lumber purchased from existing local growers, the export of commodities, andthe creation certified carbon credits for sale on international markets.

Products

IWC will generate revenue from the sale of exportable lumber such as Mahogany,Teak, Cedar, Cherrywood, Jatoba, Iroko, Sucupira, Meyranti, Ipe, and otherexotic woods. The Company also plans to export pepper, cocoa, soybeans,ethanol, various minerals and metals, and other crops. Presently, more than 65percent of arboreal resources owned by the Company are at maturity andharvestable.The Company will also harvest owned and joint venture managed forests andreforestation of these areas with new growth. These managed forests will beused for the creation of carbon credits for trading on international marketsover the growth period (typically with 15- to 30-year contracts). An importantuse of the new capital is to begin the certification process for the creationof carbon credits.Long term, IWC has the potential to certify more than two million accessibleacres of manageable forest area, containing millions of tons of certifiablecarbon credits. In addition, there are coniferous woods in the Companyportfolio that are available for harvest and quick re-growth; these aresuitable for short term carbon credit contracts, as well as for use in themanufacture of plywood, blockwood, and other finished products (i.e., afterexpiration of the carbon credit contract period).

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 7

Revenue

Wood salesIWC presently owns approximately 45,000 acres (18,000 hectares) of tropicaltimberland in the states of Acre and Para in the Amazon Basin, Brazil. Thetimber includes a variety of mature tropical woods including mahogany, cedarand teak. The Company owns two sawmills in the states of Acre that will beutilized in the processing of timber. IWC also owns vehicles and maritimeequipment used to extract and process timber from the forest.The Company has the ability to obtain the required permits and governmentapprovals to harvest and export up to 40,000 cubic meters of wood per year.Elliott Sassoon and I. Motta will lead the Company’s operation in Belem, nearthe property. Mr. Sassoon and Mr. Motta have more than 25 years of experiencewith harvesting timber, and the production of exotic wood for export. TheCompany will contract with a local harvesting and processing company to carryout the Company’s operational plan. These contractors will assist in theextraction, processing, grading, packing, and shipping of goods for export.

The property currently owned by the Company has sufficienttropical hardwoods to last for approximately 40 years, basedon an annual harvest of 400 hectares (approximately 40,000cubic meters of wood products). The current market value ofthe complete inventory of tropical hardwoods is $200 million.

Each year, a 400-hectare plot will be harvested. Only the most mature andcommercially profitable trees will be harvested. At the end of the harvest,ground cover and overhang cover will be thinned and sold, and the plot will bereforested with fast-growing eucalyptus (or equivalent) tree saplings. TheCompany also holds purchase contracts with affiliated or non-affiliatedcompanies on lumber at prices established during the early growth periods ofother forest areas, and will execute these options to increase exports duringthe reforestation periods of company owned areas. The newly planted trees willadd to the carbon credit value of the land within one year of planting. Inaddition, the thinning will also increase the carbon credit value of the landduring the next annual verification cycle.While timber processing and export will take place all year, the actualharvesting of tropical wood will occur during the Brazilian dry seasonbeginning in June and lasting until the end of November.IWC plans to acquire additional land to maintain a ready supply of tropicalhardwoods. As soon as the timber operation is running smoothly, the Companyplans to explore other business opportunities, including the export and saleof medicinal herbs, cosmetic herbs, and culinary spices.There is a large and growing demand for tropical hardwoods throughout theworld. The United States is the leading importer of such woods, followedclosely by the United Kingdom, Europe, Caribbean countries, and Japan. Brazil

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 8

lumber exports are currently less than 5 percent of the world total. Due totight credit availability in Brazil, the Company will have little competitionfrom other local producers.

Carbon creditsWhile there are a growing number of Emission Trading Schemes (ETS) enabled bythe Kyoto Protocol, the Company has selected the Chicago Climate Exchange(CCX) as the most appropriate exchange for its carbon credit program. CCX,launched in 2003, is the world’s first and North America’s only active,voluntary, legally binding integrated trading system to reduce emissions ofall six major greenhouse gases (GHG), with offset projects in North Americaand Brazil.1

CCX issues tradable Carbon Financial Instrument (CFI) contracts to owners oraggregators of eligible projects on the basis of sequestration, destruction orreduction of GHGs. Projects must undergo verification from a third partyinstitution certified by CCX. Only Members, Offset Providers and OffsetAggregators can register offset projects. Providers and Aggregators must nothave significant GHG emissions. CCX has developed standardized rules governingwhat types of projects can receive CFI contracts.IWC, with its significant land holdings in Brazil, will operate as an OffsetProvider. The Company has identified a Managed Forest Project as theappropriate model for its business plan. A Managed Forest Project sustainablymanages forests such that their growth in carbon stocks exceeds their harvest.Eligible projects increase forest carbon stocks by planting after harvest ornatural disturbances. The Company’s model is based on a successful Managed Forest Project in CostaRica that was reforested using 72 percent Teak and 21 percent Pochote andother native species. The average harvest cycle in the project was 18-20 yearsfor the Teak and 24 years for the Pochote. The owner of the land, PreciousWoods, exports the wood from final harvests to India; the company sells thewood from thinnings and minor harvests as raw material. In 2006, PreciousWoods sold 22,000 metric tons of CCX CFI contracts to the World Bank to offsetits operational emissions.In general, CCX requires forest managers to engage in harvest systems thatmaintain partial forest cover, reduce soil erosion, and avoid destructiveharvesting practices. CCX requires that landowners provide evidence thatforest holdings are sustainably managed, through certification from agenciesendorsed by CCX.2

All CCX offset projects go through the same standardized registration,verification and crediting process. Verification and validation are usually

1 http://www.chicagoclimatex.com/content.jsf?id=8212 http://www.chicagoclimatex.com/images/content/File/CCX_Case_Study_Managed_Forest_Offsets.pdf

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 9

done at the same time by the same auditor and are called “project verificationand enrollment.” Credits are calculated (generated) after verification.

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 10

The CCX-mandated verification steps are as follows3:1. IWC submits a project proposal for an eligible project to the CCX,

including proof of ownership of the forestland.2. The proposal is reviewed by the CCX Committee on Offsets; they provide a

preliminary approval if the project is eligible (the project may bereferred to a scientific technical advisory committee).

3. Once approved by the Committee, IWC must obtain independent verificationby a CCX-approved verifier (including site visits) to accurately assessa project’s annual GHG sequestration or destruction potential.

4. The verification reports are reviewed by CCX staff, as well as theirregulatory service provider (FINRA) for completeness and accuracy.

5. IWC can then join the CCX and enroll the project.The baselines and methodologies for calculating emission reductions aredefined for each project type. Some baselines are project-specific (e .g.,large reforestation projects are credited relative to measured site-specificcarbon levels prior to the start of the project). Other baselines are based onperformance standards (e.g., abandoned deforestation projects in Brazil arecredited using predetermined annual deforestation rates for specific stateswithin Brazil).There is no explicit information regarding the exact timeframe forverification and accreditation. However, the Company is expecting the processto take a minimum of 6 months. Before CCX issues the credits, an independentverifier must undertake site visits and record inspections to confirm projecteligibility. The verifier inspects project performance data (e.g., treemeasurements, visual inspections) and calculations to confirm a project’sactual, annual GHG destruction, sequestration or emission avoidance. TheCompany’s offset project is subject to initial verification, as well as annualverification for the duration of its enrollment in CCX.4

A Managed Forest Project is a long-term commitment. IWC is required to sign acontract attesting that the land will be maintained as forest for at least 15years from the date of enrollment in CCX. In addition, all participants arerequired to sign a letter of good faith stating that they will maintainenrolled land in forest beyond the 15-year contract period required by theprogram.

Based on available species inventories, aerial photographs,and the review of similar offest projects, IWC believes thatthe Company’s initial 18,000-hectare Managed Forest Projectwill generate $4-6 million per year in carbon credit revenue,depending primarily on the CCX trading price.

3 http://assets.panda.org/downloads/vcm_report_final.pdf4 http://www.theccx.com/docs/offsets/General_Offsets_faq.pdf

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 11

IWC and sustainability

Amazonia contains more than 5 million square kilometers of trees andvegetation, making it the largest continuous expanse of tropical rain forestin the world. Although such forests cover only 7 percent of the land surfaceof the planet, they contain 50 percent of the plants and animals found in theworld.Due to the unique heritage of the rainforest, IWC intends to operate in themost sensitive ecological manner and will dedicate a portion of its netprofits to research that will identify new products of Amazonia. The Companywill not engage in “strip cutting” of the any Amazon lands. Instead, IWC willemploy a “select cut” technique, harvesting only mature trees with anidentifiable commercial market. After harvest, the Company will reforest withnew trees. Through the Company’s sustainability program, timber resources willbe renewed and increased.Local waterways and existing roads will be used for transporting logs tosawmills. Use of the rivers and existing road structure will be economical andconvenient, with little environmental impact.

Government regulations

IWC has secured or is in the process of securing the governmental permits,licenses and approvals necessary to harvest, process and export tropicalhardwoods at a rate of up to 80,000 cubic meters per year. The Company plansto export approximately 40,000 cubic meters from IWC lands in its firstcomplete year of operation.A long-standing Brazilian ban on the export of tropical wood logs will notaffect the Company's operations – IWC will only export processed lumber.The Company is unaware of any pending legislation in Brazil or the UnitedStates that would have an adverse impact on the proposed operations.As the Company is resident and organized under the laws of the United Statesthere is no restriction of profits or capital with respect to any aspect ofthe Company's business in Brazil.

Management team

IWC has an outstanding management team with forest management experience and asuccessful entrepreneurial track record. An important use of investmentproceeds will be the attraction of certain new key employees, includingadditional management executives. In anticipation of funding, the Company hasinitiated discussion with a few outstanding candidates for these positions.The Company’s CEO and director, David Lilly, was one of the founders of andlegal counsel to the predecessor to IWC. Roy Schwartz, the Company’s

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 12

president, is a retired Certified Public Accountant, an investor in multiplereal estate ventures, and a venture capitalist.Zafquir Latkha is an international finance expert who has been involved inmore than $500 million in development in Dubai and other Middle Easternnations, and holds an MBA from University of Miami. Harvey Scholl, Esq., theCompany’s chief legal counsel is a practicing attorney specializing ininternational investments, currently representing clients with more than onebillion dollars in international investments worldwide.Esther Bittelman, the Company’s Secretary, is director of Gorski Sober LivingCenters, and affiliated company. Dennis Thomas is president of GeothermalPower of America, Inc., and has been named businessman of the year by Inc.Magazine and Entrepreneur of the Year by Business Week. J. Bittelman is anexperienced operations manager and US Agent for the Company, specializing inpublic relations.The Company’s director of Brazilian operations, Elliott Sassoon, has more than25 years of experience in the Brazilian lumber industry. Mr. Sassoon isrecognized for implementing large forestry, pulp and paper operations inBrazil. He is well connected to Brazilian forest, lumber and environmentalentities, as well as political and governmental agencies. In the early 1980s,Mr. Sassoon served as vice president of the West Amazon Lumber ExportersAssociation.The Company’s VP of Brazilian Operations, I. Motta, has been involved in thelumber and fine wood export field for over 25 years. He is presently presidentof the Pyramid Group of Companies, with control over 720,000 hectares ofmanaged forest in Brazil. He is a recognized expert in both forestry andcarbon credit producing managed forest development.

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 13

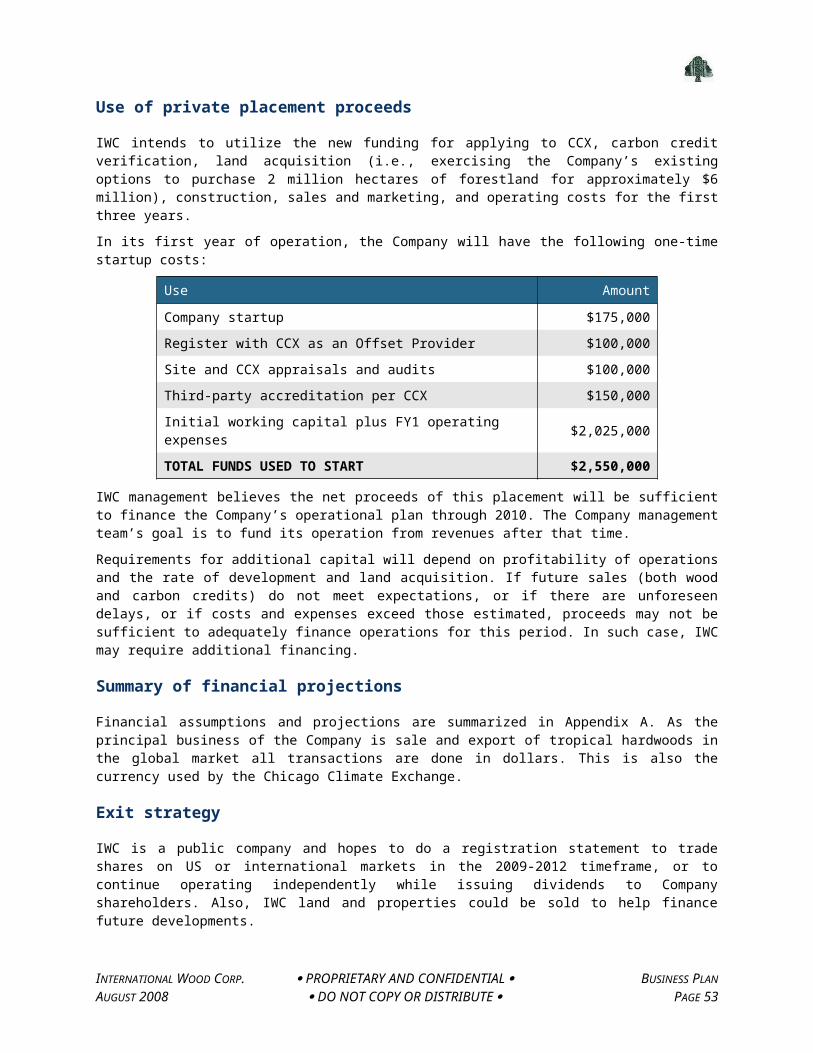

Financial plan

IWC is seeking combined equity participation and/or credit line of $12 millionfor applying to CCX, carbon credit verification, land acquisition,construction, sales and marketing, and operating costs for the first threeyears. Interest only payments will be made on any line of credit through thefirst three years, after which any initial debt will be repaid throughpermanent financing or through a convertible debt structure. The projectedmarket value of the project after three years is $36 million.The Company has all the equipment, personnel, timber and customers to operateits business. This working capital will allow the export of approximately40,000 cubic meters per year, with a market value of approximately $5 millionannually. The present holdings of the Company will allow harvesting at thislevel for a period of 40 years.The Company plans to retain a portion of its earnings, so that IWC will beself-financed after a period of five years.

Investor opportunity. For an initial investment of $12million, the project will generate an estimated $30,000,000 inrevenue (see Appendix A) during the first three years ofoperation.

Summary of financial projections

As the principal business of the Company is sale and export of tropicalhardwoods in the global market all transactions are done in dollars. This isalso the currency used by the Chicago Climate Exchange.

2008 2009 2010 2011 2012 Carbon credits -$ 122,400,000$ 122,400,000$ 122,400,000$ 122,400,000$ Lumber sales -$ 44,000,000$ 44,000,000$ 44,000,000$ 44,000,000$ Total Revenue -$ 166,400,000$ 166,400,000$ 166,400,000$ 166,400,000$ Direct Expenses -$ 25,800,000$ 25,800,000$ 25,800,000$ 25,800,000$ Gross Profit -$ 140,600,000$ 140,600,000$ 140,600,000$ 140,600,000$ Gross Profit (%) - 84% 84% 84% 84% Other Expenses 733,750$ 4,042,200$ 4,060,920$ 4,081,248$ 4,103,854$ EBITDA (733,750)$ 136,557,800$ 136,539,080$ 136,518,752$ 136,496,146$ Depreciation $0 $0 $0 $0 $0 Income Tax Expense -$ 40,747,230$ 40,961,720$ 40,955,640$ 40,948,840$ Net Income (733,750)$ 95,810,570$ 95,577,360$ 95,563,112$ 95,547,306$ Net profit (%) - 58% 57% 57% 57%

Corporate structure and headquarters

IWC is a C corporation registered in the state of Colorado. All inquiriesshould be directed to:

Roy I. Schwartz, President and DirectorInternational Wood Corporation

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 14

8358 W. Oakland Park Blvd, Suite 100Sunrise, FL 33351+1 954 224 7475http://www.iwcusa.net

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 15

Carbon Market OverviewGreenhouse effect

If the Earth had no atmosphere, its average surface temperature would be verylow—approximately -18 deg C, rather than the comfortable 15 deg C found today.The difference in temperature is due to a family of gases called greenhousegases that affect the overall energy balance of the Earth by absorbinginfrared radiation. In its existing state, the Earth’s atmospheric systembalances absorption of solar radiation by emission of infrared radiation tospace. Due to greenhouse gases, the atmosphere absorbs more infrared energythan it re-radiates to space, resulting in a net warming of the Earth’ssurface temperature. This is the Natural Greenhouse Effect. With more greenhousegases released to the atmosphere due to human activity, more infraredradiation is trapped in the Earth's surface, contributing to the EnhancedGreenhouse Effect.Individual greenhouse gases affect the energy balance differently. In order toassist policymakers in measuring the impact of various greenhouse gases onglobal warming, the Intergovernmental Panel on Climate Change (IPCC)introduced the concept of Global Warming Potential (GWP) in its 1990 report.5 GWPreflects the relative strength of individual greenhouse gases with respect toits impact on global warming. It is defined as the cumulative radiative forceover time caused by a unit mass of greenhouse gas emitted now, expressedrelative to CO2.

Greenhouse gases

Greenhouse gases are essential to maintaining the temperature of the Earth.However, an excess of greenhouse gases can raise the temperature of a planetto lethal levels.6 Greenhouse gases are produced by many natural andindustrial processes, which today result in CO2 levels of 380 ppmv7 in theatmosphere. Based on ice-core samples and records, current levels of CO2 areapproximately 100 ppmv higher than during immediately pre-industrial times,when direct human influence was negligible.On Earth, the most abundant greenhouse gases are (in order of relativeabundance):

6. Water vapor 7. Carbon dioxide

5 http://www.hko.gov.hk/wxinfo/climat/greenhs/e_grnhse.htm6 On Venus, for example, the 90 bar partial pressure of carbon dioxide (CO2) contributes to a surface temperature of about 467 deg C (872 deg F).7 Parts per million, by volume.

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 16

8. Methane 9. Nitrous oxide 10. Ozone 11. CFCs

The most important greenhouse gases are:1. Water vapor—causes between 36 percent and 70 percent of the greenhouse

effect 2. Carbon dioxide—causes between 9 percent and 26 percent 3. Methane—causes between 4 percent and 9 percent4. Ozone—causes between 3 percent and 7 percent

Note that this is a combination of the strength of the greenhouse effect ofthe gas and its abundance. For example, methane is a much stronger greenhousegas than CO2, but present in much smaller concentrations. It is not possible to state that a certain gas causes a certain percentage ofthe greenhouse effect, because the influences of the various gases are notadditive. (The higher ends of the ranges quoted are for the gas alone; thelower ends, for the gas counting overlaps.)

Kyoto Protocol

The Kyoto Protocol is an international agreement linked to the United NationsFramework Convention on Climate Change8. The major feature of the KyotoProtocol is that it sets binding targets for 37 industrialized countries andthe European community for reducing greenhouse gas (GHG) emissions. Theseamount to an average of 5.2 percent against 1990 levels over the five-yearperiod between 2008 and 2012. Recognizing that developed countries are principally responsible for thecurrent high levels of GHG emissions in the atmosphere as a result of morethan 150 years of industrial activity, the Protocol places a heavier burden ondeveloped nations under the principle of common but differentiated responsibilities. The Kyoto Protocol was adopted in Kyoto, Japan, on December 11, 1997, andentered into force on February 16, 2005. More than 180 nations have ratifiedthe treaty to date, with the United States as the most notable exception. Thedetailed rules for the implementation of the Protocol were adopted at inMarrakech in 2001, and are called the Marrakech Accords.According to the Kyoto Protocol, GHG emissions can be reduced by:

Reducing domestic emissions, drawing on a wide range of policies andmeasures (e.g., carbon tax, carbon trading, standards, subsidies, etc.)

Trading (Article 17) emission permits Assigned Amount Units (AAUs) amonggovernments (Article 3)

8 http://unfccc.int/kyoto_protocol/items/2830.php

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 17

Purchasing emission reductions credits from Clean Development Mechanism(CDM) and Joint Implementation (JI) projects.

Emissions trading (ET)Parties with commitments under the Kyoto Protocol (Annex B Parties) haveaccepted targets for limiting or reducing emissions. These targets areexpressed as levels of allowed emissions, or assigned amounts, over the 2008-2012commitment period. The allowed emissions are divided into Assigned Amount Units(AAUs).Emissions trading, as set out in Article 17 of the Kyoto Protocol, allowscountries that have emission units to spare—i.e., emissions permitted but notused—to sell this excess capacity to countries that exceed their targets.9

Thus, a new commodity was created in the form of emission reductions orremovals. Since carbon dioxide is the principal greenhouse gas, people speaksimply of trading in carbon. Carbon is now tracked and traded like any othercommodity. This is known as the Carbon Market.

Joint Implementation (JI)The mechanism known as Joint Implementation (JI), defined in Article 6 of theKyoto Protocol, allows a country with an emission reduction or limitationcommitment under the Kyoto Protocol to earn emission reduction units (ERUs) from anemission-reduction or emission removal project in another Annex B Partycountry, each equivalent to one ton of CO2, which can be counted towardsmeeting its Kyoto target.10

Joint implementation offers Parties a flexible and cost-efficient means offulfilling a part of their Kyoto commitment, while the host Party benefitsfrom foreign investment and technology transfer.

The Clean Development Mechanism (CDM)11

The Clean Development Mechanism (CDM), defined in Article 12 of the Protocol,allows a country with an emission-reduction or emission-limitation commitmentunder the Kyoto Protocol to implement an emission-reduction project indeveloping countries. Such projects can earn saleable certified emission reduction(CER) credits, each equivalent to one ton of CO2 (tCO2), which can be countedtowards meeting Kyoto targets.The mechanism is seen by many as a trailblazer. It is the first global,environmental investment and credit scheme of its kind, providing astandardized emissions offset instrument, the CER.

9 http://unfccc.int/kyoto_protocol/mechanisms/emissions_trading/items/2731.php10 http://unfccc.int/kyoto_protocol/mechanisms/joint_implementation/items/1674.php11 http://en.wikipedia.org/wiki/Clean_Development_Mechanism

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 18

A CDM project might involve, for example, a rural electrification projectusing solar panels or the installation of more energy-efficient boilers. Themechanism stimulates sustainable development and emission reductions, whilegiving industrialized countries some flexibility in how they meet theiremission reduction or limitation targets.A CDM project must provide emission reductions that are additional to whatwould otherwise have occurred. The projects must qualify through a rigorousand public registration and issuance process. The designated nationalauthorities give approval. Operational since the beginning of 2006, the mechanism has already registeredmore than 1,000 projects and is anticipated to produce CERs amounting to morethan 2.7 billion ton of CO2 equivalent in the first commitment period of theKyoto Protocol (2008–2012).12

The CDM is supervised by the CDM Executive Board (CDM EB) and is under theguidance of the Conference of the Parties (COP/MOP) of the United NationsFramework Convention on Climate Change (UNFCCC).The CDM gained momentum in 2005 after the entry into force of the KyotoProtocol. Before the Protocol entered into force, investors considered this akey risk factor. The initial years of operation yielded fewer CDM credits thansupporters had hoped for, as Parties did not provide sufficient funding to theEB. This left it understaffed.The Adaptation Fund was established to finance concrete adaptation projects andprograms in developing countries that are Parties to the Kyoto Protocol. TheFund is financed with a share of proceeds from clean development mechanism(CDM) project activities and receives funds from other sources. In the CDM system, a Certified Emission Reduction (CER) accounts for thetrading amount (1 ton CO2 = 1 CER). Offset providers and carbon credit buyerscalculate the amount of trade by CERs. An offset providing candidate has to gothrough the 8 steps in the validation process13:

1. Project Formulation—the project is described in the project design document(PDD)

2. National approval by Designated National Authority (DNA)3. Validation by Designed Operational Entity (DOE)4. Registration5. Monitoring—systematic surveillance of project performance by project

participants6. Verification by DOE—periodic independent review of emission reductions7. Certification by DOE

12 http://unfccc.int/kyoto_protocol/mechanisms/clean_development_mechanism/items/2718.php13 http://www.wbcsd.org/DocRoot/ZKZmI5uWD1gwkb3QVPV5/CDM_TERI.pdf

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 19

8. Issuance of CERs—the offset provider is required to submit a 2 percentshare of proceeds for Adaptation Fund.

Emission trading scheme (ETS)14

The World Bank, one of the main players in carbon financing, estimates thevalue of carbon traded in 2005 to be about $10 billion. The Bank believes thecarbon market has the potential to bring more than $25 billion in newfinancing for sustainable development to the poorest countries and thedeveloping world.Trading firms, brokers and banks are among those expected to make moneythrough commissions for organizing carbon deals. The Bank's own carbon financefund has more than doubled from $415 million in 2004 to $915 million lastyear.There are two main ways to exchange carbon. The first is what is called a cap-and-trade scheme whereby emissions are limited and can then be traded. UnderKyoto developed countries can trade between each other. The European Trading Scheme (ETS) is a cap-and-trade scheme and the largestcompanies-based scheme around. It is mandatory and includes 12,000 sitesacross the 25 European Union member states. It came into force in 2005 andcovers heavy industry and power generation, including non-European companies. Beside cap-and-trade, there are also voluntary cap-and-trade schemes—the ChicagoClimate Exchange (CCX) is such a scheme. (Interest in carbon trading atregional level is increasing in America, even though the U.S. governmentdecided not to ratify Kyoto.) The UK also has its own voluntary scheme, forwhich companies cut their emissions in return for incentive payments. The second main way of trading carbon is through credits from projects thatcompensate for or offset emissions. The Kyoto protocol's Clean DevelopmentMechanism (CDM), for example, allows developed countries to gain emissionscredits for financing projects based in developing countries. The JointImplementation (JI) mechanism also involves project-based schemes whereby onecountry can receive emissions credits for financing projects that reduceemissions in another developed country.

Market structure and market players

Emissions trading is poised to become one of the key tools to support thetransition to a low- carbon economy. As countries take steps toward meetingtheir commitments under the Kyoto Protocol, the global carbon market hasexperienced extremely rapid growth over the past few years. Strong market growth continued in 2007 as the market more than doubled invalue at $64 billion, compared to $31 billion in 2006 and almost $11 billionin 2005.

14 http://news.bbc.co.uk/2/hi/business/4919848.stm

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 20

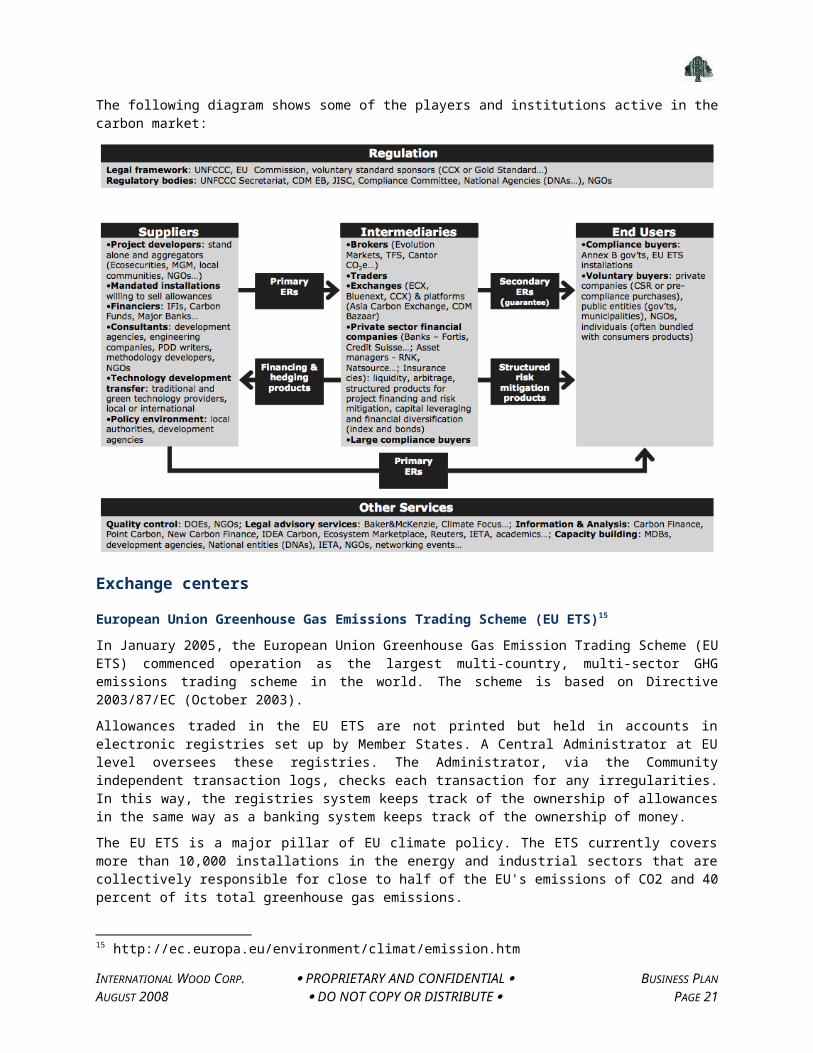

The following diagram shows some of the players and institutions active in thecarbon market:

Exchange centers

European Union Greenhouse Gas Emissions Trading Scheme (EU ETS)15

In January 2005, the European Union Greenhouse Gas Emission Trading Scheme (EUETS) commenced operation as the largest multi-country, multi-sector GHGemissions trading scheme in the world. The scheme is based on Directive2003/87/EC (October 2003).Allowances traded in the EU ETS are not printed but held in accounts inelectronic registries set up by Member States. A Central Administrator at EUlevel oversees these registries. The Administrator, via the Communityindependent transaction logs, checks each transaction for any irregularities.In this way, the registries system keeps track of the ownership of allowancesin the same way as a banking system keeps track of the ownership of money.The EU ETS is a major pillar of EU climate policy. The ETS currently coversmore than 10,000 installations in the energy and industrial sectors that arecollectively responsible for close to half of the EU's emissions of CO2 and 40percent of its total greenhouse gas emissions.

15 http://ec.europa.eu/environment/climat/emission.htm

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 21

European Climate Exchange (ECX)16

The European Climate Exchange (ECX) manages marketing and product developmentfor ECX Carbon Financial Instruments (ECX CFIs), listed and admitted totrading on the ICE Futures Europe's electronic platform. ECX/ICE FuturesEurope is the most liquid platform for carbon emissions trading, attractingover 85 percent of the exchange-traded volume in the European carbon market.ECX CFI Contracts include standardized futures and options based on EUAllowances (EUAs) and Certified Emission Reductions (CERs). More than 90leading businesses have signed up for membership to trade ECX products. Inaddition, several thousand ICE clients can access the emissions market dailyvia banks and brokers.ECX volumes for EUA and CER Contracts are experiencing increasing growth.Since its launch in April 2005, the ECX EUA Futures Contract alone has seenover 2 billion tCO2 traded on the platform with an underlying market value of€24 billion. The cash value of carbon traded worldwide grew from US$33 billionin 2006 to US$60 billion in 2007.17

ECX is a member of the Climate Exchange Plc group of companies. Other membercompanies include the Chicago Climate Exchange (CCX) and the Chicago ClimateFutures Exchange (CCFE). Climate Exchange Plc (CLE) is listed on the AIMmarket of the London Stock Exchange.

Nord Pool18

The business of the Nordic power exchange is to provide a marketplace fortrading in physical and financial contracts in the Nordic countries (Finland,Sweden, Denmark and Norway). Its physical market accounts for over 60 percentof the total value of the Nordic region’s power consumption. Price formationin the physical market provides players in the financial market with acredible and secure reference price for financially settled contracts. Thismakes Nord Pool’s physical and financial markets far more liquid than anyother European power exchange. Exchange services are offered through the NordPool group, which comprises Nord Pool ASA and Nord Pool Spot AS. Nord Poolalso provides a carbon market, being the first exchange in Europe to offerstandardized contracts for emission allowances (EUA) and carbon credits (CER).Nord Pool Spot AS and its subsidiaries Nord Pool Finland Oy and Nord Pool SpotAB are owned by the national grid companies Fingrid, Energinet.dk, Statnett,Svenska Kraftnät and Nord Pool ASA (twenty percent ownership for each). TheNord Pool group has offices in Lysaker (Oslo), Fredericia, Stockholm,Helsinki, Berlin and Amsterdam.The Nord Pool group has more than 420 members in total, including exchangemembers, clearing clients, members and representatives in 20 countries.

16 http://www.europeanclimateexchange.com/default_flash.asp17 Point Carbon.18 http://www.nordpool.com/en/asa/General-information/

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 22

Chicago Climate Exchange (CCX)19

Chicago Climate Exchange (CCX), launched in 2003, is the world’s first andNorth America’s only active voluntary, legally binding integrated tradingsystem to reduce emissions of all six major greenhouse gases (GHGs), withoffset projects worldwide. CCX Members are leaders in greenhouse gas (GHG) management and represent allsectors of the global economy, as well as public sector innovators. Reductionsachieved through CCX are the only reductions made in North America through alegally binding compliance regime, providing independent, third partyverification by the Financial Industry Regulatory Authority (FINRA, formerlyNASD). The founder, Chairman and CEO of CCX is economist and financialinnovator Dr. Richard L. Sandor, who was named a Hero of the Planet by TimeMagazine in 2002 for founding CCX, and in 2007 as the "father of carbontrading."CCX emitting Members make a voluntary but legally binding commitment to meetannual GHG emission reduction targets. Those who reduce below the targets havesurplus allowances to sell or bank; those who emit above the targets comply bypurchasing CCX Carbon Financial Instrument (CFI) contracts. The commodity traded at CCX is the CFI contract, each of which represents 100metric tons of CO2 equivalent. CFI contracts are comprised of ExchangeAllowances and Exchange Offsets. Exchange Allowances are issued to emittingMembers in accordance with their emission baseline and the CCX EmissionReduction Schedule. Exchange Offsets are generated by qualifying offsetprojects.

New South Wales (NSW)20

The NSW Greenhouse Gas Abatement Scheme (GGAS) commenced in January 2003. Itis one of the first mandatory greenhouse gas emissions trading schemes in theworld. GGAS aims to reduce greenhouse gas emissions associated with theproduction and use of electricity. It achieves this by using project-basedactivities to offset the production of greenhouse gas emissions.In November 2005, the Premier confirmed the Government’s commitment to extendthe NSW Greenhouse Gas Abatement Scheme to 2020 and beyond. The decision toextend the scheme recognizes the need to provide certainty to investors ingreenhouse gas abatement activities.GGAS establishes annual statewide greenhouse gas reduction targets, and thenrequires individual electricity retailers and certain other parties who buy orsell electricity in NSW to meet mandatory benchmarks based on the size oftheir share of the electricity market. If these parties, known as benchmark19 http://www.chicagoclimatex.com/content.jsf?id=82120 http://www.greenhouse.nsw.gov.au/actions/agencies/pricing_and_regulatory_tribunal/greenhouse_gas_abatement_scheme

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 23

participants, fail to meet their benchmarks, then a penalty is assigned. TheIndependent Pricing and Regulatory Tribunal of NSW (IPART) monitors theperformance of benchmark participants in its role as Compliance Regulator.

Case studies

The Pacific Forest Trust’s Forests Forever Fund21

The Pacific Forest Trust, founded in 1993 and now celebrating 15 years ofconservation and climate solutions, is the only organization solely dedicatedto conserving America’s working forests for all their public benefits—wood,water, wildlife, and a well-balanced climate. They strive to keep forestsworking by pursuing a comprehensive strategy to “retain, sustain and gain”.They help retain our forest infrastructure by raising awareness of the threatsto America’s private working forests and by directly conserving criticalforestlands in partnership with landowners and communities in California,Oregon and Washington. They lead the country in the use of working forestconservation easements that ensure productive forests stay working. They alsohelp protect the integrity of important public forests by conservingneighboring private lands threatened by development. To date, they haveconserved more than 50,000 acres of forestlands.They help both landowners and the public gain from working forests bydeveloping and promoting new forest eco-services. These forest eco-servicesserve as the basis for a sustainable business model that yields financialreturns from management practices that reduce forest-based carbon dioxide(CO2) emissions, watershed quality, and fish and wildlife habitat. In this category, the Pacific Forest Trust is especially focused on advancingthe climate benefits of forests. By leading regional and national efforts toenact climate change policies that unite conservation and management withmarket-based incentives to reduce greenhouse gas emissions, they are promotingthe positive role forests can play to help mitigate global warming. Thisleadership has led to the creation of a first-in-the-nation, California-basedprogram that allows forest landowners to register and sell CO2 emissionsreductions generated by conservation and sustainable management.

Western Oregon Carbon Sequestration Project22

Oregon was the first state to establish a regulation of GHG emissions frompower production. In 1997, Oregon passed House Bill 3283, creating the OregonClimate Trust, requiring new power plants to offset their CO2 emissions byapproximately 17 percent. Emitters may finance the Oregon Climate Trust to undertake mitigation projectsto offset emissions. Many of these offset projects include fuel efficiencyimprovements, as well as forestry sequestration projects.

21 http://www.pacificforest.org/about/index.html22 http://204.154.137.14/energy-analyses/pubs/slfinal_1.pdf

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 24

In April 2004, Washington passed House Bill 3141, which requires new powerplants rated 25 MW or greater to offset 20 percent of their CO2 emissions over30 years of plant operations. Similar to Oregon law, Washington power plantoperators may opt to pay a state-approved third party at the rate of $1.60 pertCO2 for offset projects. The Oregon offset rate was $0.57 per tCO2 at the inception of House Bill 3283,subject to a 50 percent increase or decrease by the Oregon Energy FacilitySiting Council in any two-year period after 2000. Although Massachusetts andNew Hampshire also have CO2 emissions restrictions for power plants in theirmulti-pollutant emissions legislation, they do not explicitly definemechanisms for power plant operators to reduce emissions. Massachusetts 310CM4 7.29, passed in April 2001, restricts CO2 emissions to 1,800 pounds perMWh by 2008 with an overall goal of reducing total plant emissions by 10percent. New Hampshire HB 284, passed in January 2002, requires a return to1990 emissions levels by the end of 2008.

Peugeot in Brazil23

Peugeot has teamed up with two service providers to implement this majorenvironmental project. The first, I'Office National des Forets (ONF), isrecognized internationally for its technical expertise and is one of theleading managers of public forests in the world. The second, Pro-NaturaInternational, is a Franco-Brazilian non-governmental organization (NGO) basedin Paris, with experience in protecting tropical forests and promoting forestmanagement systems in more than 25 countries.The program puts into action the carbon sink concept discussed at the KyotoConference on climate change and represents a tangible contribution byindustry to controlling global warming. The carbon sink concept entailsrecreating ecosystems that can absorb large amounts of the excess carbondioxide (CO2) from the atmosphere. This concept complements measures tomitigate the greenhouse effect by reducing emissions at the source.The carbon sink will be created in Juniena, Mato Grosso state. It will cover12,000 hectares (nearly twice the area of Paris) and have a carbon storagecapacity of 50,000 metric tons per year, which corresponds to 183,000 metrictons CO2 per year equivalent. ONF has provided a 40-year guarantee to Peugeot.A system of internal and external assessment through independent audits isplanned to ensure that the agreed targets are met.Special care will be taken to integrate the project into the region's socio-economic environment, as this is a key success factor. The carbon sink willnot be created from scratch but will include three components: 5,000 hectaresof deforested farm land that will be fully replanted, 7,000 hectares of oldand second-growth forest, and managed forest lands.

23 Peugeot will invest FF65 million in the project, which is the first of its kind worldwide by its size and organization. http://www.cwn.org.uk/motoring/peugeot/1998/10/981012-carbon-sink.htm

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 25

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 26

Carbon Market AnalysisClimate change captured the public’s imagination in 2007, as a major reportprepared by the Intergovernmental Panel on Climate Change (IPCC), a NobelPeace Prize and the launch in Bali of the negotiation process for a post-2012climate change regime, contributed to making climate change a key part of theglobal economic and environmental debate. January 1, 2008 also marked theformal start of the compliance period of the Kyoto Protocol and of Phase II ofthe European Union Emission Trading Scheme (EU ETS).

The carbon market (volumes and values)

The carbon market is the most visible result of early regulatory efforts to mitigate climate change. Regulation constraining carbon emissions has spawned an emerging carbon market that was valued at $64 billion in 2007.24

24 State and Trends of the Carbon Market 2008, supported by resources from the CF-Assistprogram managed by the World Bank Institute.

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 27

Market growth

The carbon market’s biggest success thus far has been to send market signalsfor the price of mitigating carbon emissions. This in turn has stimulatedinnovation and carbon abatement worldwide, as motivated individuals,communities, companies and governments have cooperated to reduce emissions.

Allowance marketsThe EU ETS market has been successful in its mission of reducing emissionsthrough internal abatement at home25, and of stimulating emission reductionsabroad. The European Commission, learning from the experience of Phase I, hasstrengthened several important design elements for EU ETS Phase II. Along withrecent EU proposals for Phase III26, these improvements include tighteremission targets, stronger flexibility provisions for compliance (at least forEU Allowances, or EUA, although not for project-based credits), more attentionto internal EU harmonization and, most importantly, longer-term visibility foraction to reduce emissions until 2020. These proposed reforms have helpedcreate confidence in emissions trading as a credible and cost-effective toolof carbon mitigation.27 In 2007, $50 billion in Phase II allowances and derivative contracts weretraded over-the counter, bilaterally, and, increasingly on exchange platformsthat publish transparent data about price formation in the markets.28 Energyutilities and industrial companies hedged their carbon exposure by buying theEUA and financial companies bought and sold the EUA for their clients (“flowtrading”) and for their own account (“proprietary trading”).

Project-based markets In 2007, buyers also continued to show a strong appetite for primary project-based emission reductions, reflected by continued growth in the projectpipeline showing that 68 countries had identified and offered to reduce 2,500million ton of carbon dioxide equivalent (MtCO2e) through more than 3,000projects. This potential supply received strong interest, mainly from privatesector buyers and investors, who in 2007 transacted 634 MtCO2e from primary

25 D. Ellerman and B. Buchner (2008). Over-Allocation or abatement? A Preliminary Analysis of the EU ETS Based on the 2005-06 Emissions Data, Environmental and Resource Economics, forthcoming.26 On January 23, 2008 the European Commission proposed the "Climate action and renewable energy package", a pillar of its climate change strategy with a vision to 2020 and beyond.27 Australia, Japan and others announced that they too would develop their ownemissions trading schemes (ETS).28 The major European carbon marketplaces are the European Climate Exchange (ECX) and the London Energy Brokers Association (LEBA). Markets and exchanges also emerged around the world, including New York, New Delhi & Mumbai, India and elsewhere.

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 28

project-based transactions (up 8 percent from 2006) for a corresponding valueof $8.2 billion, up 34 percent from 2006.

Compliance-driven market CDM accounted for the vast majority of project-based transactions (at 87percent of volumes and 91 percent of values) and JI saw transacted volumesdoubling and values tripling in 2007 over the previous year. The CDM alone sawprimary transactions worth $7.4 billion, with demand coming mainly fromprivate sector entities in the EU, but also from EU governments and Japan. Thevoluntary markets, supporting activities to reduce emissions not mandated bypolicymakers, also saw transacted volumes doubling to 42 MtCO2e and valuetripling to $265 million in 2007. There were reports of growing demand forvoluntary “pre-compliance” credits for U.S.-based forestry projects under theCalifornia Climate Action Registry (CCAR).

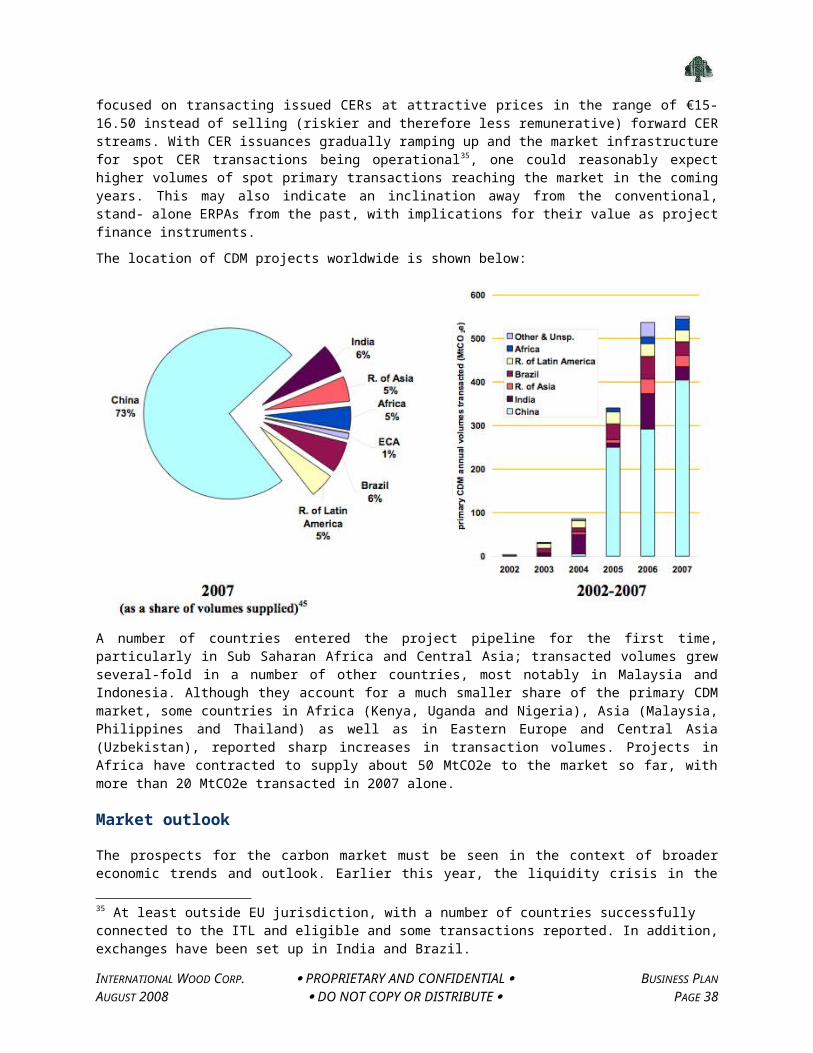

China dominates, Africa emerges China was again the biggest seller, and expanded its market share of CDMtransactions to 73 percent. Countries in Africa (5 percent) and Eastern Europeand Central Asia (1 percent) emerged in the carbon market and offered buyersan opportunity to diversify their China-overweight portfolios. The share ofIndia and Brazil (6 percent) reflected a preference from some sellers favoringthe sale of already issued Certified Emission Reductions (CER), of which thereare a total of only 130 MtCO2e in the market so far.

CDM delivers on clean energyCarbon contracts from clean energy projects (energy efficiency and renewableenergy) accounted for nearly two-thirds of the transacted volume in theproject-based market, appropriately reflecting the CDM’s mission of supportingemission reductions and sustainable development. These project types typicallyuse sound, road-tested technology, are operated by utilities or experiencedoperators, and have predictable performance, resulting in CER issuances thatare expected to yield between 70-90 percent of expected Project DesignDocument (PDD) volumes, based on current expectations. This explains why theyare being targeted by buyers, now that the known industrial gas project typeshave been more or less contracted.

Prices and price differentiation The growth in transacted values reflected higher prices for primary forwardcontracts, which had an average price of €10 in 2007. Prices for primarymarket forward transactions were in the range of €8-13 in 2007 and early 2008.The generally higher prices reflected the intense competition and activity inthe global market to encourage projects that reduce global emissions. Pricesin the higher end of that range typically rewarded projects that were furtheralong in the CDM process (such as registered projects), projects that werebeing developed by experienced and established sponsors (low credit risk andperformance risk), and/or for projects with high expected issuance yields.

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 29

Spot contracts of issued Certified Emission Reductions were transacted at €16-17, a nice premium to the primary CER, but still at a discount to the EUA,reflecting a combination of the impact of the European Commission’s 2020proposal the time value of money, and some remaining procedures related to thedelay in connectivity of the International Transaction Log (ITL) to the EU.

Climate-friendly investment Analysts estimated that $9.5 billion were invested in 2007 in 58 public andprivate funds that either purchase carbon directly or invest in projects andcompanies that can generate carbon assets. The total capitalization of carbonvehicles could reach $13.8 billion in 2008, with 67 such carbon funds andfacilities. This capital inflow was characterized by a substantial increase inthe number of funds seeking to provide cash returns to investors and by morefunds getting involved earlier in the project development process, takinglarger risks through equity investment in expectation of larger returns.29 In2007 alone, CDM leveraged $33 billion in additional investment for cleanenergy, which exceeded what had been leveraged cumulatively for the previousfive years since 2002.

Secondary marketsThe biggest overall market development in 2007 and early 2008 was theemergence of the secondary markets. In 2007, as a wide range of proceduraldelays and risks of CER registration and issuances grew, the carbon marketinnovated by providing portfolio-based guarantees. In these transactions, asecondary seller, typically a market aggregator, sold guaranteed CER (gCER)contracts that were secured through a slice of its carbon portfolios. Theseguarantees were also usually credit-enhanced through the balance sheet of ahighly-rated bank engaged by the secondary seller for this purpose.30

Some banks originated CER through spot contracts and sold gCER contractsforward, making small margins on a large number of transactions. This segmenthad greater price transparency and gCER contracts were listed on majorexchanges.

Market challenges

At the end of March 2008, there were 3,188 projects in the CDM pipeline, ofwhich roughly one-third are registered (978), or in the process ofregistration (188) while roughly two-thirds are at validation stage (2,022).The project-based market became, in some ways, a victim of its own success and

29 T I. Cochran and B. Leguet (2007). Carbon Investment Funds: The Influx of Private Capital, Mission Climat Caisse des Dépôts (Paris:France).30 Some aggregators and banks also provided services warehousing, selling or swapping other tranches of the risk with partial guarantees. Some banks also structured equity- or debt-like notes to institutional investors looking for some exposure and diversification to carbon.

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 30

obtaining timely CER issuance proved to be quite challenging in 2007. Marketinfrastructure and institutions as well as regulators are struggling to keeppace with the huge momentum of CDM supply. Increased scrutiny by the CDMExecutive Board contributed to further delays.

Procedural delays in the CDM In spite of its success, or perhaps because of it, the carbon market cameunder close public scrutiny in 2007. The success of the CDM was weighed downby a creaking infrastructure that, despite efforts to streamline it, is stillstruggling to process the overwhelming response from project developersworldwide in a timely manner.Procedural inefficiencies and regulatory bottlenecks have strained thecapacity of the CDM infrastructure to deliver sufficient CER volumes onschedule, as too many projects await registration and issuance:

Out of 3,188 projects in the currently pipeline, 2,022 are at validationstage.

Market participants report that it is currently taking them up to sixmonths to engage a Designated Operational Entity (DOE), causing largebacklogs of projects even before they reach the CDM pipeline.31

Projects face an average wait of 80 days to go from registration requestto actual registration. The Executive Board has requested a review ofseveral projects received for registration, has rejected some of them,and has asked project developers to re-submit their projects using newlyrevised methodologies. There is a very short grace period allowed tograndfather the older methodology, and the additional work adds todelays and backlogs.

Projects are currently taking an average of one to two years to reachissuance from the time they enter the pipeline. Over 70 percent ofissued CER volumes come from industrial gas projects, with the vastmajority of energy efficiency and renewable energy projects remainingstuck somewhere in the pipeline.

Complex rules and the capacity constraint DOEs, who are accredited to validate and verify CDM projects, are unable tokeep up with a large backlog of projects awaiting registration, and arefinding it difficult to recruit, train and retain qualified, technical staffto apply the complex rules consistently. As a result, some projects have been31 DOEs report staffing shortages, especially for hiring and retaining trainedtechnical staff with appropriate language skills (for example, in Chinese). The process for accreditation of a new DOE, for example, a national accreditor, requires an application fee of €150,000. Since the accreditation process takes eighteen months or more, it would only make sense for a company to apply to become a DOE if it had confidence in market continuity since that would impact their long-term business viability beyond 2012.

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 31

registered incorrectly, resulting in a call for more reviews being requestedby the CDM Executive Board, which, in turn, causes even more delays.Important concerns have been voiced about CDM on issues of its additionality,its procedural efficiency and ultimately, its sustainability. Some critics ofthe CDM maintain that its rules are too complex, that they change too oftenand that the process results in excessively high transaction cost; they askfor relief from the rules. Other critics question whether certain projectactivities are truly additional, or whether CDM can create perverseincentives; they ask for even more rules.

Delays can and do impact carbon payments CDM project registration and CER issuances are generally lower and slower thanexpected and regulatory efforts to reform and streamline the process areurgently needed.9It can take between one and two years for a project to go from validation toregistration and technical delays. This does not even include the six monthsor so that it is taking to book the services of a DOE. Project delays costproject developers valuable financial resources, cost buyers valuable emissionreductions and can delay desired environmental outcomes. Delays for any reason—since payment for carbon is often linked to delivery—can put elements of thefinancing package of projects in jeopardy. This, in turn, may further impacton the expected delivery schedule, not to mention dampening the enthusiasm forfurther innovation, which is urgently needed to mitigate climate change.Clearing bottlenecks and accelerating the application of necessary procedureshas become a priority challenge.

Private companies and commercial risks There is a troubling tendency of some companies in the market to point afinger at the CDM and to hold its procedural delays to be solely responsiblefor the poor performance of their companies. In a market where the“production” of the asset or commodity is not in the control of marketplayers, but rather in the hand of a regulator, the risk of regulatory delaymust be treated as a core element of commercial risk. Some companies clearlymade incorrect and imprudent commercial decisions, for example, by taking onexcessive risk or burning too much cash, or guaranteeing too many CERs fordelivery by a certain date against penalties without adequate risk management.Their commercial contracts should balance the risks and rewards of variousparties. While the carbon regulatory infrastructure clearly needs reform, itis simply wrong to blame the regulator for all problems. Companies also haveto examine at the appropriateness of their commercial and business decisions.

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 32

Key market trends

Carbon market momentum is strong for now After some growing pains in its first phase, the EU ETS has created a robuststructure to cost- effectively reduce greenhouse gas emissions. Created byregulation, the carbon market’s biggest risk is caused, perversely, by theabsence of market continuity beyond 2012 and this can only be provided bypolicymakers and regulators. This will require increased efforts well beyondwhat is envisaged by the current policies of major world emitters.

The CDM is at a crossroads The European Commission’s post-2012 proposal, which strengthened severaldesign elements of the EU ETS, however, did not provide much comfort for theproject-based market, which, after its strongest year yet, finds itself at asignificant crossroad. By linking additional EU ETS demand for CDM and JIcredits to the success of post-2012 global climate change negotiations, theEuropean Commission proposal has the risk, surely unintended, of slowing themomentum for the project-based mechanisms. Under the proposal, the resultingissued CERs and the Emission Reductions Units (ERUs) would be less flexibleand less fungible, limiting their risk management and compliance utility vis-à-vis the EUA. The EUA spread over the secondary CER widened to nearly €10 atthe time of this writing, and even higher for most primary CER contracts. Thekey challenge is not how to reduce the success of the CDM, but rather how toraise the ambition of the world, including the EU, to set science-basedemission reduction targets and meet them cost-effectively.

Time to re-think the CDM The CDM’s biggest strength has been its ability to bring developing anddeveloped countries and the public and private sectors together to reduceemissions cost-effectively. In the years ahead, all countries will want toscale up their efforts to reduce emissions while growing their economies in asustainable manner. As the world considers scaling up serious action to combatclimate change, it would be desirable to re-think the CDM as a helpful toolfor the challenges ahead.

The forest for the trees In its next phase, the CDM needs to move up the learning curve and evolvetoward approaches and methodologies that conservatively estimate emissionreduction trends on the aggregate level, and away from the current focus ontrying to account for every last ton reduced or removed from the atmosphere.The next generation CDM should focus on catalyzing step changes in emissiontrends, and on creating incentives for large-scale, transformative investmentprograms.

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 33

Built to last Several jurisdictions, including various states, regions, and countries areconsidering whether and how to link up with international opportunities forreducing emissions. It would be helpful to find ways for them to learntogether from and build on the CDM experience so far, with the goal ofencouraging efficiency, reducing transaction costs, avoiding unnecessaryduplication and creating, from the start, compatible infrastructure withstrong linkages and inter-operability.

Global cooperation on climate change Given enough incentive and a long lead-time, developing countries can deliverlarge volumes of cost- effective emission reductions that can help meetscience-based emission reduction targets. This puts a special responsibilityon countries to cooperate under the Bali Action Plan to reach an ambitiousinternational agreement to reduce emissions. It also makes it important forthe EU, the U.S. and other major emitters to find ways to encourage thecontinued engagement of developing countries in mitigation activities.International negotiators (and regulators of domestic programs) shouldconsider providing incentives for early action with sufficient lead-time todevelop emission reduction programs and projects. The experience of the carbon market so far shows that the private sector iscapable and willing to cooperate in solving the problem, provided thatpolicies are predictable, consistent and transparent and regulations areefficient.

The EU is still far and away the major carbon marketThe EU ETS is the major market for greenhouse gas (GHG) emission allowances,and is the engine, perhaps even the laboratory, of the global carbon market.Its most notable achievement is that it helps discover the price to emit GHGin Europe. Several exchanges now transparently disclose prices at whichallowances change hands: for example, the EUA for December 2008 delivery (EUA-Dec-08) has durably traded in the €20-25 price band since May 2007. This pricesignal also encourages project developers to reduce emissions globally throughclimate-friendly CDM projects in developing countries and JI projects in AnnexB countries that generate carbon credits for sale into the EU ETS. The EU Emission Trading Scheme (EU ETS) continued to dominate the globalcarbon market in 2007, both in transaction volume and monetary value. Morethan two billion EUAs changed hands for a market value of $50 billion in 2007.This corresponds to nearly a doubling in both volume and value transacted in2005.Smaller, but also important, is the continued growth in the voluntary ChicagoClimate Exchange (CCX) which benefited from increased interest and activity asmarket players responded to state-level, regional and federal developments inclimate policy in the U.S. The pioneering New South Wales (NSW) market saw asharp increase in volumes traded, but prices slumped because of a temporary

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 34

over-supply of credits and from clarity about transition arrangements toAustralia’s proposed national emissions trading market, which is to beoperational by 2010. New Zealand launched its own ETS, covering all GHG andprogressively including all sectors, starting with forestry in 2008. Japan isreportedly still finalizing the contours of its own emissions trading scheme.

Volumes transacted in the primary market levels off In 2007, buyers continued to show strong interest in the CDM and JI, and thiswas supported by higher flows of capital into the carbon arena. Whiletransacted volumes grew slightly to 634 MtCO2e for finalized primary project-based transactions (up 8 percent from 2006), the value of all primary carbonpurchase transactions was much higher, at $8.2 billion, up 34 percent from2006, a sign of the intense competition and activity in the market.

CDM accounts for most of the project-based market activity (at 87 percent ofvolumes and 91 percent of value transacted). JI and the voluntary market as awhole each experienced a doubling of transacted volumes and a tripling oftransacted values. The dynamic of the project-based market changed in early2008, as buyers became more cautious in response to a combination of mountingdelivery and issuance challenges, higher perceived credit risks amid thegenerally bearish sentiment in the financial markets32, as well as continuinguncertainty about the role of and demand for CDM and JI in the post-2012climate regime(s).These market trends, as well as the limits to demand from the EU ETS have thepotential to leave behind, in particular, projects in poorer countries whichhave only just begun to take advantage of the carbon compliance market. Manyof these sellers have begun to look increasingly toward voluntary and pre-compliance markets for buyers. 32 Through 2006 and H1’07, the number of new projects entering the pipeline (public comment period of the validation stage in the CDM project cycle) grew extremely rapidly, from 35 to a record-breaking 176 by July 2007. Since then, this number decreased sharply and is currently around 100-120 or so.

INTERNATIONAL WOOD CORP. PROPRIETARY AND CONFIDENTIAL BUSINESS PLANAUGUST 2008 DO NOT COPY OR DISTRIBUTE PAGE 35

Annual volumes (MtCO2e) of project-based emission reductions transactions(vintages up to 2012) are shown below:

The buyers

Europe dominatesFor the second consecutive year, European buyers dominated the CDM and JImarket for compliance and at the close of 2007, their market share reachedalmost 90 percent (up from 2006). Private companies have been the most activebuyers, with 79 percent of volume transacted in 2007, up slightly from 77percent in 2006. The most active buyers (large European compliance buyers withinstallations in several countries, project developers and aggregators, aswell as financial institutions with an eye to the booming secondary markets)largely operate or are administered out of London, which, at 59 percent, isstill considered the carbon finance hub of the world (up from 54 percent in2006).