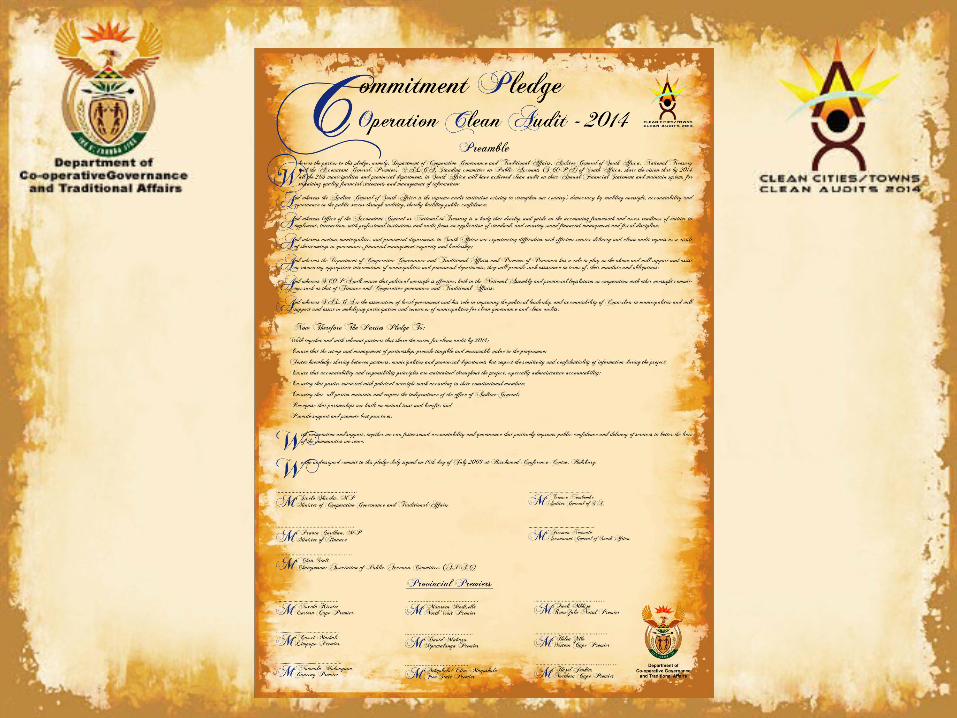

Clean Audit

34

Clean Audit Presentation DATE: 14/07/2009 TIME: 10: 00 -12HOO Venue: S-37

-

Upload

johannesburg -

Category

Documents

-

view

4 -

download

0

Transcript of Clean Audit

Clean Audit Presentation

DATE: 14/07/2009 TIME: 10: 00 -12HOO

Venue: S-37

Purpose & objectives of the meeting

• Sharing of information and approach with regard

to ‘Operation Clean Audit 2014 programme’

• To gain support with regard to the

implementation of the project

• Build and strengthen interdepartmental

relations and public-private partnerships beyond 2014

•

• Learn from each other and make sure our efforts are coordinated within the

public sector

• To gain and share experiences on governance in general,

• corporate governance in particular

Guiding Vision

• By 2014, all the 283 municipalities and 9 provinces departments in South Africa will have achieved clean audits on their Annual Financial Statements and maintaining systems for sustaining quality financial statements and management information.

Programme Goal

• Assist all the municipalities and provincial departments to achieve clean audit opinions by 2014, improve and sustain the quality of financial statements.

Programme Purpose

• To address all issues raised by Auditor General and reduce vulnerability of risks in the provincial departments and municipal audit reports through targeted projects central to the sustainability of sound financial management accountability and best practices.

2. Background

• Post 1994, the government has and still puts service delivery improvement on the agenda. However, Auditor-General’s reports continue to spell-out queries relating to ineffective institutions, ineffective structures (internal audit units and audit committees), poor performance or absence of systems, especially financial management and systems. This negative picture seriously affects government service delivery plans in general and corporate governance in particular.

• Both provincial and local governments are faced with challenges which among others include:

• Inadequate skills on planning, budgeting; public financial management, including expenditure management

• Poor interface between financial and non-financial information (in-year-monitoring and quality annual reporting)

• Inability to manage cash-flow significantly

• Inadequate skills on credit control and debt management, including basic financial accounting and filling or record keeping in most instances

• Duplication of payments in some instances and amounts not accounted for (lack of financial accountability)

• Lack of systems to manage audit queries and recommendations, both internal and external auditing

• Inadequate systems with regard to corporate governance (especially, conflict of interest and accountability frameworks, and effective Integrated risk management system) within provincial departments and municipalities

• Leadership and management issues, especially decision making with regard to audit queries, both from internal auditors and external auditors (leadership)

• Non-existence or dysfunctional of audit committees and internal audit committees (governance)

• Inadequate administrative and political oversight to strengthen accountability and responsibility (oversight)

3. Purpose, goal and measurable objective: Operation clean audit

• The project has the following purpose, goal and measurable objective:

• Purpose: The main purpose of the project is to address challenges faced by both municipalities and provinces with regard to audit management, especially audit findings and queries from the Auditor-General.

Strategic Goal:

• Clean audits both in municipalities and provincial departments by 2014.

• Measurable objective: Provision of technical assistance to both provinces and municipalities on management of audit queries in order to improve financial management, corporate governance, including systems, more importantly to improve the lives of ordinary people.

4. Operation clean audit: Scope and standards

• Operation clean audit will focus on both provinces and municipalities so that the relationship between spheres of government is strengthened. This could assist the project itself, to be coherent, coordinated and sustainable.

4.1 Project focuses on:

• Improvement of Annual Financial Statements and their rate of timeous submission to the Auditor General

• Strengthening accountability and governance mechanisms, systems and procedures

• Mechanisms to implement remedial plans to audit findings and queries raised in the audit reports

• Strengthening the capacity of provinces to support and oversee municipalities, in relation to financial management

• Development of a corporate governance manual and corporate governance pledge for municipalities, especially on conflict of interest

• Mechanisms to improve revenue and expenditure management

• Developing an accountability framework to strengthen oversight and support: Provincial and local government strategic relationship

5. Consultative Process: Stakeholders

• For this project to succeed and have an impact, both within government and our communities, a robust inclusive consultative process has to be done and implemented.

This consultative process is designed to achieve the following:

• Effective political management of the project

• Improved departmental coordination and support

• Enhanced intra-departmental coordination • Improved and strengthened public-private partnership on matters of corporate governance and service delivery

• Improve transversal relations between government departments to support good governance

• Enhanced intergovernmental relations between spheres of government within the constitutional spirit of co-operative governance

• Commitment and buy-in to the goals and outcomes of the project

5.1 Internal: Department of

Co-operative Governance and Traditional Affairs

• Municipal Performance Monitoring and support (MPMS) unit

• Performance management/ monitoring system

• Intergovernmental fiscal relations• Anti-corruption / Ethics• Local government leadership academy

5.2 External stakeholders: Interdepartmental

• MINMEC, especially MEC’s on local government Presidential Co-ordinating Council (PCC)

• National Treasury• Department of Public Service and Administration (DPSA)

• Heads of provincial Treasuries through National Treasury

• National Department of Water Affairs and Environmental

• National Department of health (DoH)• Provincial Departments of local government• South African local government association (SALGA)

• All provincial Directors-General (Premiers offices)

• Some Heads of all provincial departments• Office of the Auditor-General

• National Treasury/ Office of the Accountant-General

• Provincial offices of Auditor-General through their National office (Pretoria)

• Public Service Commission (PSC) • Provincial offices (PSC) through their National office, Pretoria.

• National Assembly and Provincial legislatures

Table 5.1.1 External stakeholders

5.3 External stakeholders: private-public partnership

• Institute of Directors (IoD), adivise on corporate governance

• Business South Africa (BUSA), supportive venture on corporate governance

• Development Bank of Southern Africa (DBSA), for funding

• Commercial Banks, funding the project and partners in corporate governance

• Key reputable individual consultants and companies on financial management auditing, financial systems and corporate governance, to advise and develop frameworks on the above.

• Institute of Municipal Finance Officers (IMFO)

• South African Institute of Chartered Accountants (SAICA), providing technical advise on accounting and auditing.

5.4 Other projects

• Ayihlome Campaign • Road shows on waste management (Clean cities/towns)

• Corporate governance conferences/Seminars

Conclusion

• Leadership

• Technical skills

• Effective political oversight

• Support from the private sector

• Support from other departments (horizontal and vertical) and other Chapter nine institutions, eg AG and PSC

• Effective Communication • Attitude towards public finances and systems