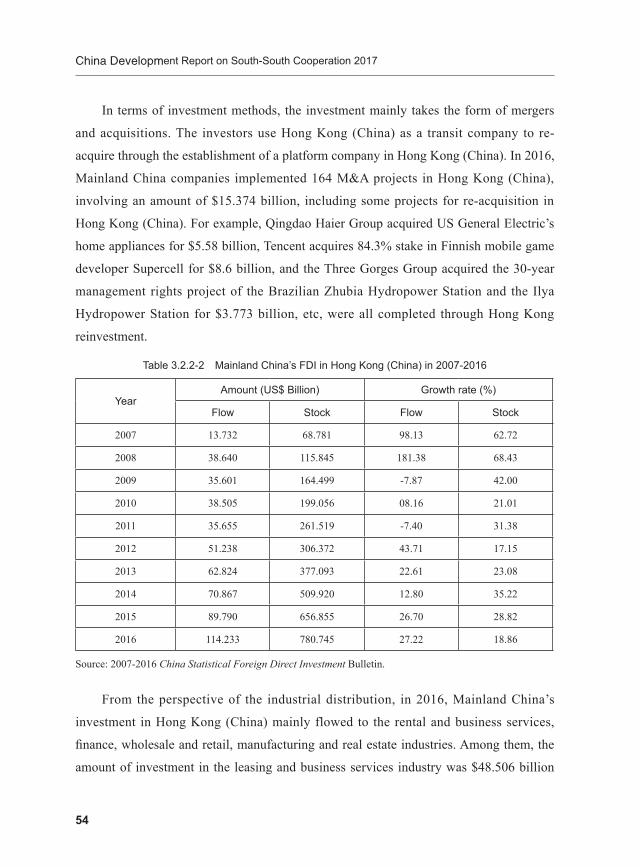

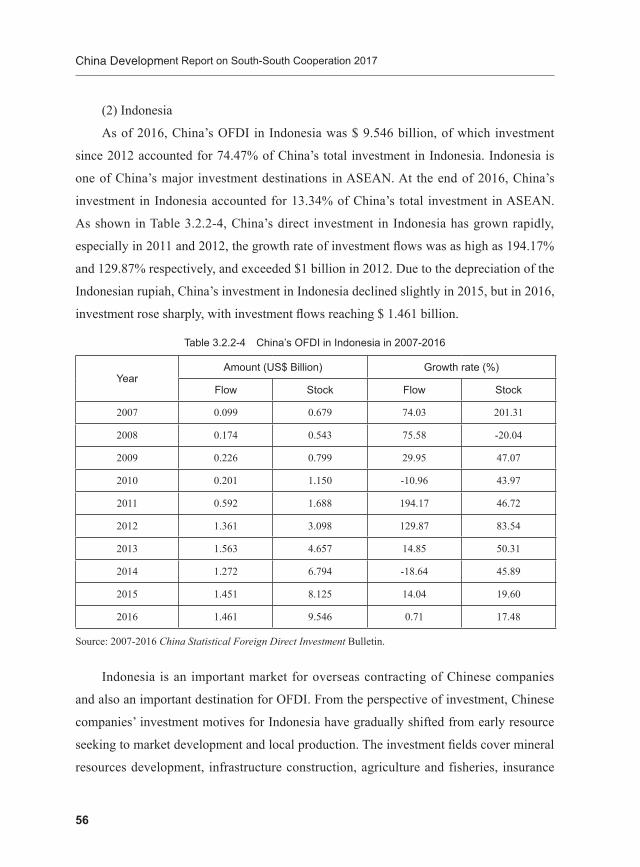

South-South cooperation – policy and practice by the Export Import Bank of China

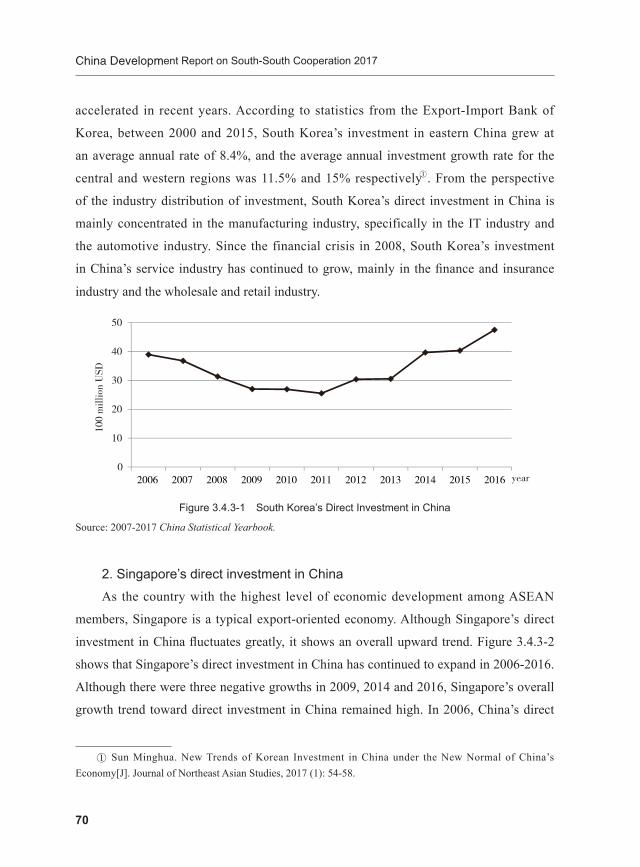

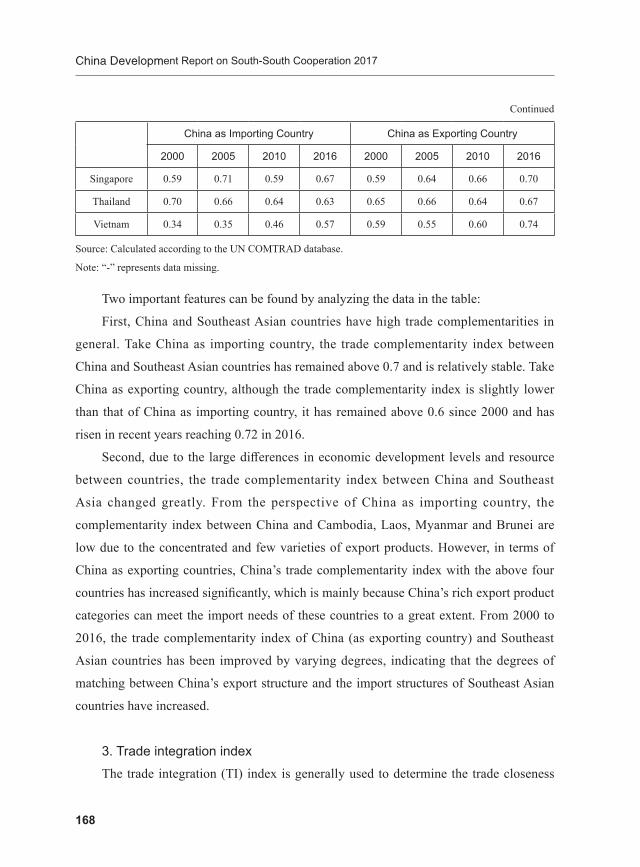

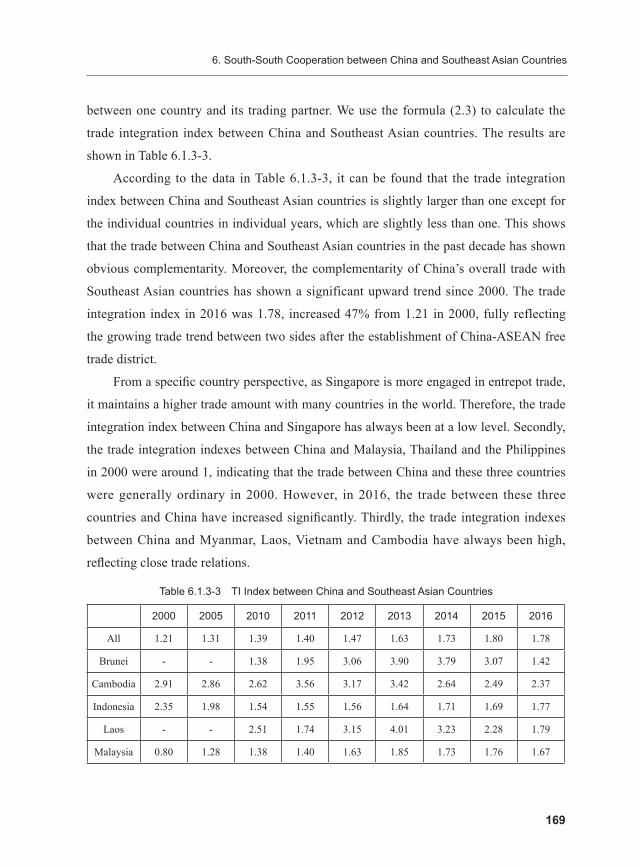

Upload

khangminh22Category

view

1download

0

China Development Report on South-South Cooperation

2017

—Trade and Investment Relations between China and Asian Developing Countries

Edited by Li, Ronglin and Zheng, Zhaoyang

China Commerce and Trade Press

China Development Report on South-South Cooperation 2017中国南南合作发展报告 2017—中国与亚洲发展中国家之间的贸易投资合作

ZHONGGUO NANNANHEZUO FAZHAN BAOGAO 2017

主编 李荣林 郑昭阳 Edited by Li, Ronglin and Zheng, Zhaoyang

出 版:中国商务出版社

地 址:北京市东城区安定门外大街东后巷 28 号 邮编: 100710

责任部门:教育培训事业部(010-64243016 [email protected] )

责任编辑:刘姝辰

总 发 行:中国商务出版社发行部 (010-64208388 64515150 )

网购零售:中国商务出版社考培部 (010-64286917)

网 址:http://www.cctpress.com

网 店:https://shop162373850.taobao.com/

开 本:787 毫米 ×980 毫米 1/16

印 张:23.50 字 数:440 千字

版 次:2018 年 12 月第 1 版 2018 年 12 月第 1 次印刷

书 号:ISBN 978-7-5103-2677-6

定 价:69.00 元

凡所购本版图书有印装质量问题,请与本社总编室联系(电话:010-64212247)

版权所有 盗版必究 (盗版侵权举报可发邮件到此邮箱:[email protected] 或致电:010-64286917)

图书在版编目(CIP)数据

中国南南合作发展报告 . 2017 : 英文 / 李荣林 , 郑

昭阳主编 . -- 北京 : 中国商务出版社 , 2018.12

ISBN 978-7-5103-2677-6

Ⅰ. ①中… Ⅱ . ①李… ②郑… Ⅲ . ①南南合作-研

究报告-中国- 2017 -英文②对外贸易关系-研究报告-

中国- 2017 -英文 Ⅳ . ① F114.43 ② F752.7

中国版本图书馆 CIP 数据核字 (2018) 第 258839 号

Acknowledgement

China Development Report on South-South Cooperation 2017: Trade and

Investment Relations between China and Asian Developing Countries is the fifth annual

development report delivered by Study Center for South-South Cooperation of Nankai

University (SCSSC-NKU). It reports the economic relations between China and all Asian

developing countries and transitional economies in Asia from the perspective of trade,

investment, foreign aid, and regional economic cooperation. It also reports the relations in

different regions of South, Southeast, West, and Central Asia respectively. By providing

empirical evidences with possible detailed statistics and specific cases, the report is to

reveal the overall situation, achievements, challenges and encountered problems of south-

south cooperation between China and Asian countries.

The report is written by professors and experts at Nankai University and from other

institutes. Some PhD students and graduates in the Institute of International Economics

(IIE), Nankai University and SCSSC-NKU also involve in the task. I would like to

acknowledge their chapter contribution as the following:

Chapter one: Introduction is written by Mr. Ronglin Li, Professor at SCSSC of

NanKai University, and Mr. Zhaoyang Zheng, Associate Professor at IIE, Nankai

University; Chapter Two: Trade Relations between China and Asian Developing

Countries, written by Mr. Ronglin Li and Ms. Huiling Zhang, PhD at IIE, Nankai

University; Chapter Three: Investment Relations between China and Asian Developing

Countries, by Mr. Tong Zhu, Professor at IIE, and Ms. Nana Fan, PhD at SCSSC of

NanKai University; Chapter Four: China’s Foreign Assistance to Asian Developing

Countries, by Mr. Zhaoyang Zheng, Associate professor at IIE, Nankai University;

Chapter Five: Regional Economic Cooperation between China and Developing Countries

in Asia, by Mrs. Wei Geng, Professor at Tianjin Finance and Economic University, and

Mr. Bangdong Xu, PhD at IIE and SCSSC of NanKai University; Chapter Six: South-

South Cooperation between China and Southeast Asian Countries, by Dr. Jianzhong Li

China Development Report on South-South Cooperation 2017

2

and Mr. Kai Feng and Ms. Yuxin Zhan, PhD and graduate at IIE and SCSSC, NanKai

University; Chapter Seven: South-South Cooperation between China and South Asian

Countries, by Mr. Xin Gu, Associate Professor at Zhejiang Industry and Commerce

University and Mr. Zeyu Zhang, graduate at IIE, NanKai University; Chapter Eight:

South-South Cooperation between China and West Asian Developing Countries, by Mrs.

Mingyan Yu, Associate Professor at Tianjin Municipal Party School, and Ms. Mingwang

Yang, graduate at IIE, NanKai University; Chapter Nine: South-South Cooperation

between China and Central Asian Countries, by Mrs. Weiwei Wang, Associate Professor

at Tianjin Finance and Economic University, and Ms. Xiaohui Dai, graduate at IIE,

NanKai University; and Chapter Ten: Belt and Road Initiative and Asian Economic

Development is written by Mr. Tong Zhu, Professor at NanKai University, and Ms. Lilin

Yuan, PhD at SCSSC of NanKai University. The report is generally co-edited by Mr.

Ronglin Li and Zhangyao Zheng, and the English version of the report is translated and

edited by Mr. Xin Gu. I would like to sincerely thank all of them for their contribution

and excellent work.

The report has as always supported by the United Nation Office of South-South

Cooperation and China International Center for Economic and Technology Exchange,

Ministry of Commerce, as well as China Commerce and Trade Press. Let me thank in

particular Mr. Yongli Zhao, Mrs. Wei Zhang, Mr. Xuexin Li, and Mrs. Xingguang Xie for

their strong backing to the study and publication of the report.

The Study Center for South-South Cooperation, Nankai University conducts the

report and all the possible mistakes are attributed to the center, however, the points of

view in the Chapters are belong to author themselves. We sincerely welcome critiques

and comments.

Ronglin Li

Professor and Director

The Study Center for South-South Cooperation

Nankai University

November 4, 2018

1

CONTENTS

1. Introduction .............................................................................................................1

1.1 Basic Situations of Asian Countries .......................................................................1

1.2 A History of China- Asia Cooperation ...............................................................4

1.3 Structure of This Report ........................................................................................10

2. Trade Relations between China and Asian Developing Countries ...................................................................................................................................12

2.1 The Scale and Growth ..........................................................................................12

2.2 The Structure or Pattern of Trade .........................................................................16

2.3 The Structure of Trade in Different Regional in Asia ...........................................23

2.4 Trade Competitiveness and Complementarity .....................................................27

2.5 Summary ...............................................................................................................38

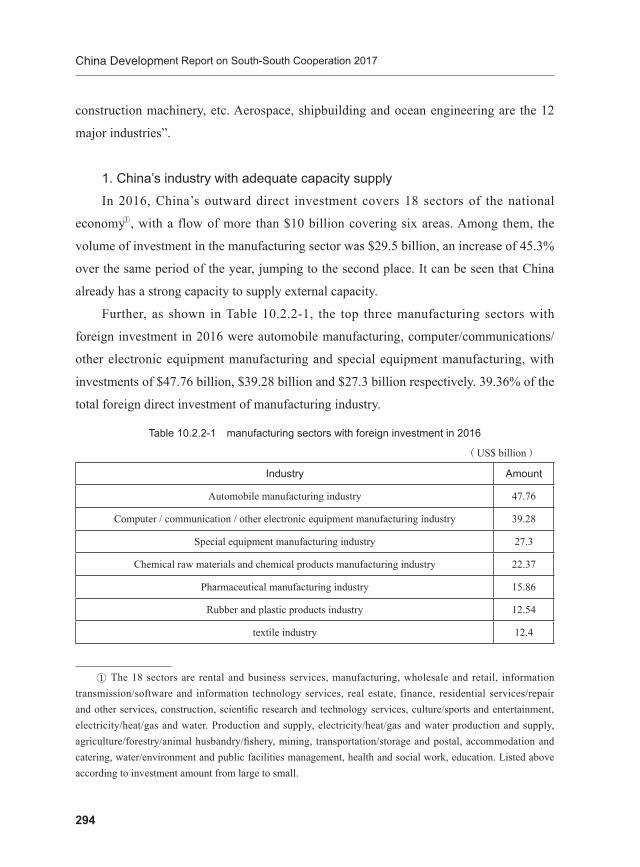

3. Investment Relations Between China and Asian Developing Countries ................................................................................................................40

3.1 General Features of China’s OFDI in Asian Countries .........................................40

3.2 China’s OFDI in Asia by Region and Country ......................................................45

3.3 Industrial Characteristics of China’s OFDI in Asia ..............................................58

3.4 Asian Countries’ Direct Investment in China ........................................................65

3.5 Two-Way Investment between China and Asian Countries ..................................71

3.6 Summary ...............................................................................................................73

4. China’s Foreign Assistance to Asian Countries ...............................75

4.1 Concepts and Ways of the Assistance ...................................................................75

4.2 History of China’s Assistance to Asian Countries .................................................78

4.3 Characteristics of China’s Assistance to Asian Countries .....................................87

2

China Development Report on South-South Cooperation 2017

4.4 Economic and Social Effects of the Assistance ..................................................102

4.5 Problems and Challenges ...................................................................................107

4.6 Summary .............................................................................................................112

5. Regional Economic Cooperation between China and Developing Countries in Asia ....................................................................115

5.1 China’s Regional Trade Agreements in Asia .......................................................115

5.2 Sub-Regional Cooperation between China and Asian Developing Countries ....126

6. South-South Cooperation between China and Southeast Asian Countries ...............................................................................................................148

6.1 The Trade Relations between China and Southeast Asian Countries ..................148

6.2 Investment Relationship between China and Southeast Asian Countries ...........170

6.3 China’s Foreign Assistance to Southeast Asian Countries ..................................177

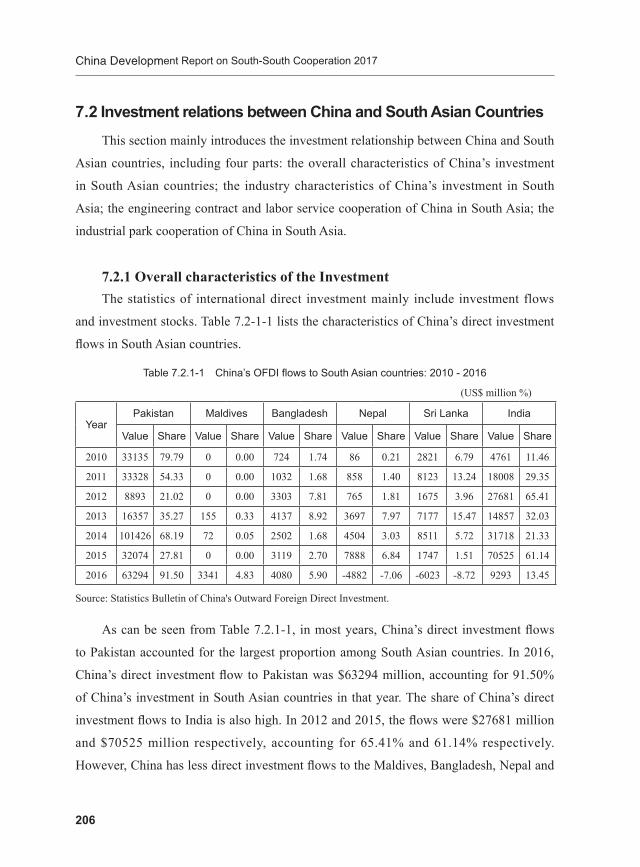

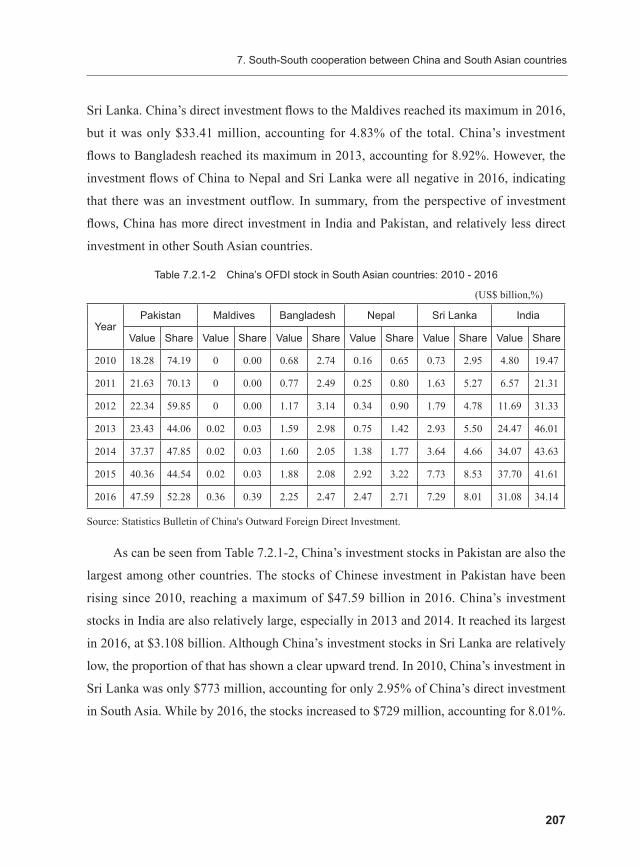

7. South-South cooperation between China and South Asian countries ...............................................................................................................182

7.1 Trade relations between China and South Asian countries .................................182

7.2 Investment relations between China and South Asian Countries ........................205

7.3 China’s Assistance to South Asian Countries ......................................................214

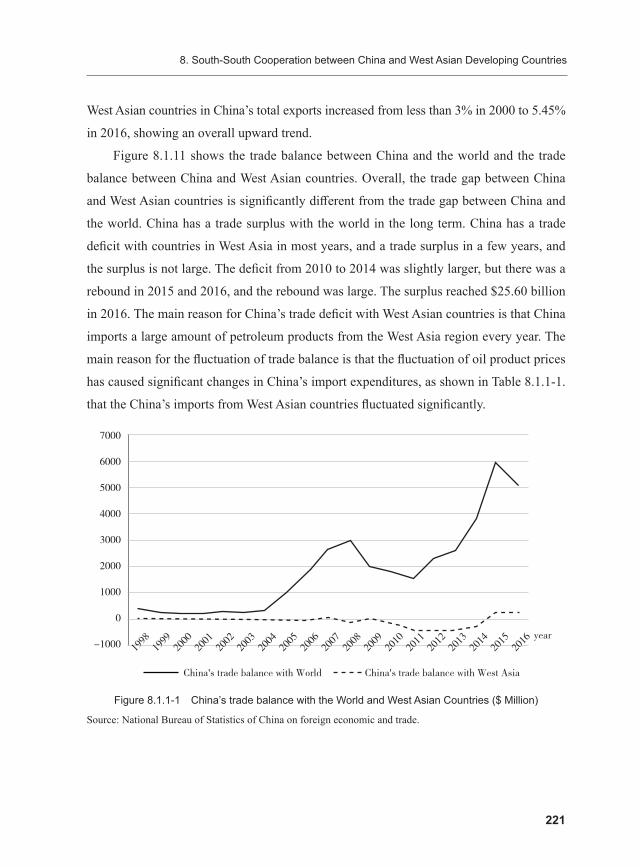

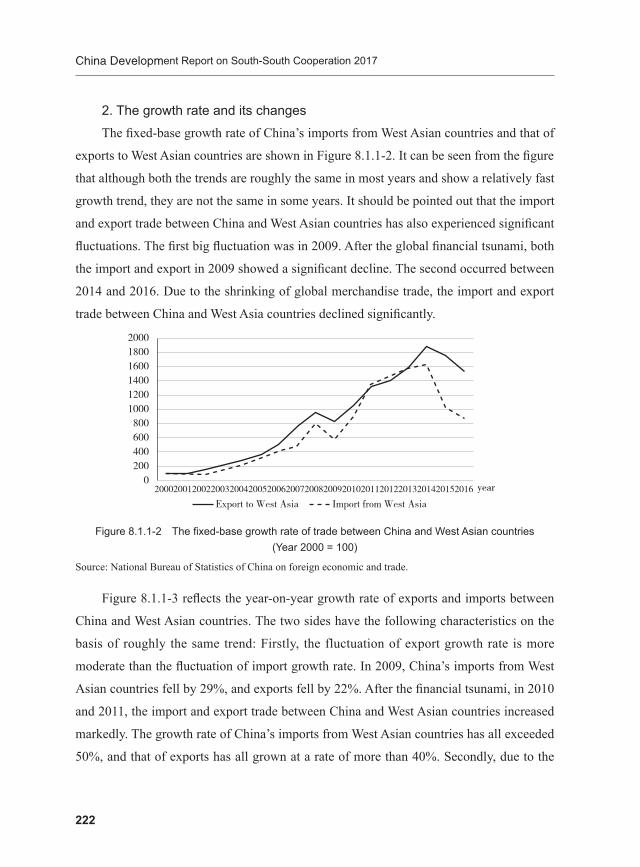

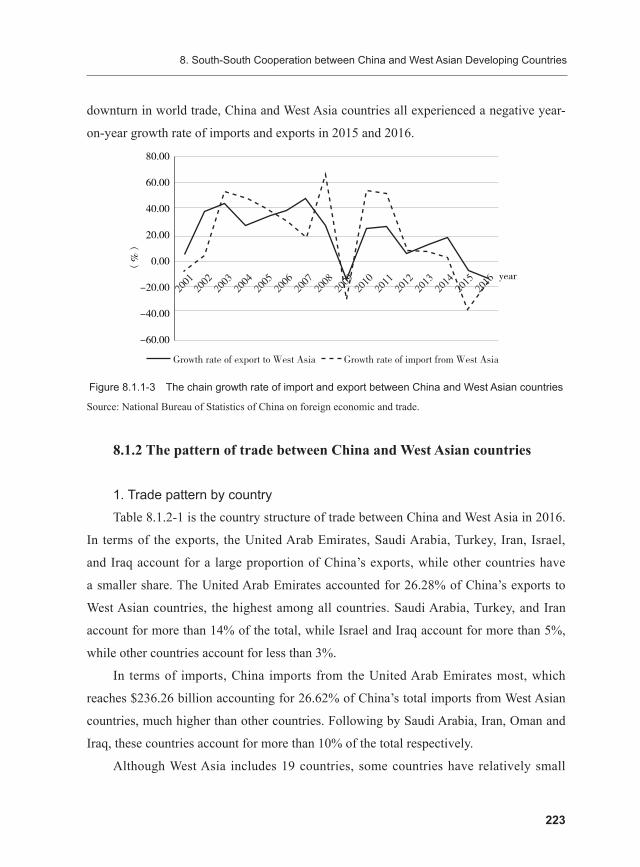

8. South-South Cooperation between China and West Asian Developing Countries ....................................................................................219

8.1 Trade relations between China and West Asian countries ...................................219

8.2 Investment relationship between China and West Asian countries .....................240

8.3 China’s assistance to West Asian countries .........................................................248

9. South-South Cooperation between China and Central Asian Countries ..............................................................................................................252

9.1 Trade relations between China and Central Asian countries ...............................252

3

CONTENTS

9.2 Investment Relationship between China and Central Asian Countries ...............266

9.3 China’s Assistance to Central Asian Countries ...................................................274

10. Belt and Road Initiative and Asian Economic Development .282

10.1 Main contents of China’s “Belt and Road Initiative” ........................................282

10.2 “Belt and Road” and productivity cooperation .................................................291

10.3 “Belt and Road” and Infrastructure Cooperation ..............................................302

10.4 The Opportunities and challenges .....................................................................316

Annex ..........................................................................................................................319

Annex 1: Basic situation of Asian Countries ............................................................319

Annex 2: Classification of Asian Countries by income .............................................321

Annex 3: Global Competitiveness of Asian Countries .............................................322

Annex 4: Import and export of Asian countries with G7 and China .........................324

1

1. Introduction

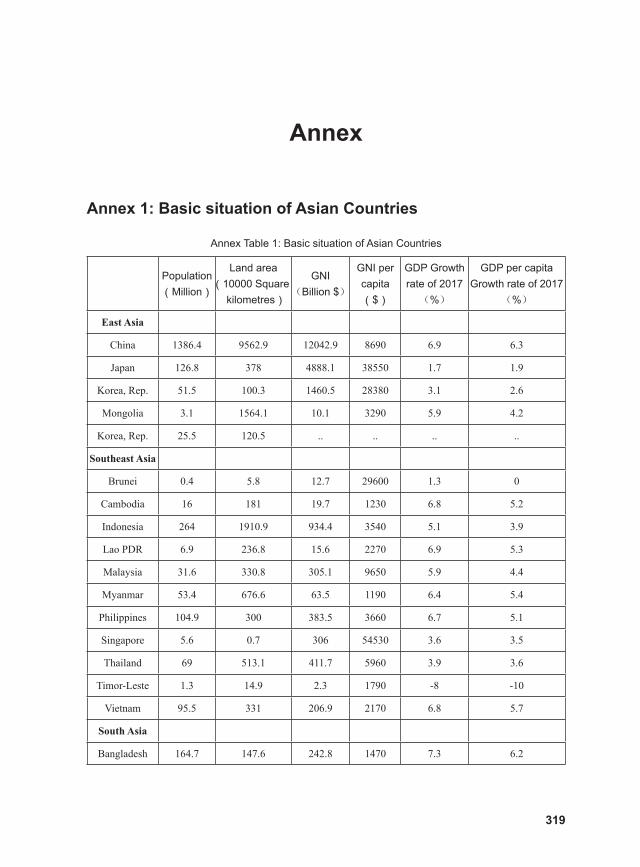

1.1 Basic Situations of Asian Countries Asia is the largest continent, with 44.570 million square meters in land, accounting

for 29.4% of the land around the world. Asia is also the most populous continent in the

world. Based on statistics of United Nations Economic and Social Council (ECOSOC),

in 2016 the overall population in Asia is around 4.462 billion, accounting for 59.8%

of global population. There are 48 sovereign countries. Only Japan is the developed

countries, while the rest are developing countries.

Geographical Location of Asian CountriesGeographically, we can divide Asia into East Asia, Southeast Asia, South Asia,

Middle Asia and West Asia, those five regions. East Asia contains China, Japan, South

Korea, Mongolia and North Korea five countries. East Asia covers 11.7 million square

meters, amounting to 26.24% of Asia. The topography of East Asia is complicated. It

has the “roof of the world” locating at Qinghai-Tibet Plateau in southwest of East Asia,

temperate grass land in its northwest, temperate regions and subtropical monsoon regions

in its east. East Asia has 1.642 billion people, accounting for 36.8% of total population.

Southeast Asia contains Vietnam, Laos, Cambodia, Myanmar, Thailand, Malaysia,

Singapore, Indonesia, Philippines, Brunei, Timor-Leste those 11 countries. Southeast

Asia covers 4.48 million square meters of land, amounting to 10.05% of total land. The

topography of Southeast Asia includes Indo-China Peninsula and Malay Archipelago two

parts, which has the world’s largest number of volcanos. It has tropical rainforest climate,

and the north part of Indo-China Peninsula has subtropical forest climate. The population

is 642 million, accounting for 14.4% in Asia.

South Asia includes Sri Lanka, Maldives, Pakistan, India, Bangladesh, Nepal and

Bhutan those seven countries. It covers 4.37 million square meters of land in Asia,

China Development Report on South-South Cooperation 2017

2

accounting for 9.8%. In its north, it is mountainous area south to Himalaya. It is Deccan

Highland in the southern part of India Peninsula. In its middle, it has Indus-Ganges River

Plateau. The topography of South Asia contains subtropical and tropical areas. It includes

subtropical forest climate, subtropical grassland climate, tropical grassland climate,

and tropical rain forest climate. It is the most populous region in Asia, has 1.732 billion

people, accounting to 38.8% of all Asian population.

West Asia includes Iran, Turkey, Cyprus, Syria, Lebanon, Palestine, Israel, Jordan,

Iraq, Kuwait, Saudi Arabia, Yemen, Omen, United Arab Emirates (UAE), Qatar, Bahrain,

Georgia, Armenia and Azerbaijan those 19 countries. It covers 7.23 million square meters,

amounting to 16.22% of Asia. The main topography in this region is highlands. In its

middle, it lies Mesopotamian Plateau, the origin of ancient civilization. The majority of

this region has few rainfalls. The total population of it is 343 million, accounting for 7.7%

of Asian population. The residents are Arabians, Persians, Turkish and Jews.

Middle Asia includes Turkmenistan, Uzbekistan, Kyrgyzstan, Kazakhstan and

Afghanistan those 5 countries. It covers 4.65 million square meters, amounting to

10.43%. In southeast, it has mountainous areas with high likelihood of earthquakes, and is

mountain climate. The rest of it are plateaus and hills with desert coverage in most of the

area. It includes temperate desert and subtropical desert and grassland climates. The total

population of this region is 104 million, only accounting for 2.3% of Asian population.

The residents are mainly Kazak, Turks, Uzbeks, Kyrgyz, Puthtu, and Russian and Slavic

immigrants during the Soviet Union era.

Natural Resources in Asia Asia has huge amount of natural resources; however, the stock of different natural

resources varies greatly. Of those resources, the stock of oil, natural gas, and coal stand

out and ranks top among seven continents. In 2016, the oil stock in West Asia accounts

for 47.7% around the globe. Adding that in East Asia and Southeast Asia, the weight of

oil stock is over 50%. Of those countries, Saudi Arabia, Iran, Iraq, Kuwait and UAE’s

oil stocks are all above 10 billion tons. In 2016, exploited natural gas stock in Asian

countries amounts to 60.4% in the world. That in West Asia is 42.5%, Middle Asia is

1. Introduction

3

10.5%, and 7.4% in East Asia, South Asia and Southeast Asia, respectively. China and

India have the largest amount of coal stock in Asia. In 2016, the exploited tin ores amount

to 49% around the world, and they are mainly in China, Indonesia, Malaysia, Thailand

and Vietnam. Tungsten ores amount to 64% in the world, and mainly locates at China and

Vietnam. Yet, the stocks of mental resources, e.g. coper, iron, aluminum and manganese,

are less than 20% compared to other regions.

Economic Development in Asian CountriesThe economic development level varies among Asian countries significantly.

According to categorization from UN Industrial Development OrganizationA, Asia still

has the eight least developed countries, which are Afghanistan, Bangladesh, Bhutan,

Cambodia, Laos, Myanmar, Nepal and Yemen. In 2016, GDP per capita in Afghanistan

is only US$565 and economic growth turned to -8.1%. In addition, there are middle low-

income countries in Asia, which are Vietnam, Philippines, Indonesia, Mongolia, India,

Pakistan, Sri Lanka, Kyrgyzstan, Uzbekistan, Syria, Armenia, and Yemen. There are 12

middle high-income countries in Asia, which are Azerbaijan, Iran, Iraq, Jordan, Lebanon,

Turkey, China, Malaysia, Thailand, Maldives, Kazakhstan and Turkmenistan. There are

10 high-income countries in Asia, which are Japan, South Korea, Brunei, Israel, Bahrain,

Kuwait, Omen, Qatar, Saudi Arabia, and UAE. In 2016, oil production country Qatar’s

GDP per capita is as high as $60,786, which is over 100 times as in Afghanistan.

In 2016, top 10 countries in terms of GDP in Asia are China, Japan, India, South

Korea, Indonesia, Turkey, Saudi Arabia, Thailand, Iran and UAE. China’s GDP is $11.2

trillion, and GDP of UAE, the last country in the top 10, is $37.1 billion. The top 10

countries in terms of GDP per capita are Qatar, Singapore, Japan, UAE, Israel, Brunei,

Kuwait, Bahrain and Saudi Arabia. The top one, Qatar’s GDP per capita is $60,786, while

that of Saudi Arabia, ranked the tenth position, is $20,150 (details in Appendix 1) B.

AUN Industrial Development Organization reports do not list Palestine, Timor-Leste and North Korea. Based on GDP per capita, North Korea is a low-income country, Palestine and Timor-Leste are middle low-income countries.

B Source: IMF, World Economic Outlook, April, 2017.

China Development Report on South-South Cooperation 2017

4

The economic development in Asia is highly unbalanced. Asia has a developed

country, high-income countries with oil exports, and also least developed countries. In

particular, the least developed countries and middle low-income countries are desperate

for an effective way to stimulate economic development, and to alleviate poverty. In

terms of economic growth rate, the difference between the least developed countries and

middle low-income countries are substantial. In 2016, the economic growth rate in Iraq

reached 10.1%. Ten countries’ economic growth is above 6% and they include China,

India, Bangladesh, Bhutan, Cambodia, Laos, Myanmar, Philippines, Vietnam, Iran,

Kyrgyzstan and Turkmenistan. However, the economic growth rate of Yemen, Azerbaijan

and Brunei was negative. Yemen was disrupted by interwar and its economic growth rates

were -28.1% and -9.8% in 2015 and 2016, respectively. Therefore, Asian countries should

confront with economic development from various perspectives. In addition to take full

utilization of external aids, they need to improve internal environment, optimize industrial

structure, take advantage of resources, and focus on backbone industries, to promote fast

and stable economic growth.

1.2 A History of China- Asia Cooperation

1.2.1 Development Stages of the Cooperation International economic cooperation between China and other Asian developing

countries can be traced back for quite a long history. It can be divided into ancient,

modern and contemporary stage.

1. Trade of Goods in Ancient TimeThe trade between China and other Asian countries, in ancient time, was mainly

conducted through two ways: Silk Road and Maritime Silk Road. Since 139 BC when

Zhang, Qian took an adventure to exploit western area of China as the envoy, China had

established trade relationship with many Asian countries. The Conventional Silk Road

has three routines: the first is “Northwest Silk Road” exploited by Zhang, Qian in Western

Han Dynasty. It connected countries like Afghanistan, Iran, Iraq and Syria, and reached

1. Introduction

5

Mediterranean area; the second is “Grassland Silk Road” that passed from Mongolian

highland in the north, and through Mountain Tianshan in its west; and the third started

from Chang’an to Chengdu and to India, named “Southwest Silk Road”. The Silk Road

is considered as the cross road that bridges Western and Oriental cultures. Businessmen

traveled along this road tirelessly, largely increasing trade volume between China and

other Asian countries at that time.

Maritime Silk Road was formed up from Han Wu Emperor, almost 2,000 years

ago. Based on Geography Record of “Han History”, Chinese businessmen then traveled

overseas, and visited countries with modern names as Vietnam, Thailand, Myanmar, India

and Sri Lanka. During Wei Dynasty and Jin Dynasty, China did not only connect its close

trade relationship with Southeast Asian countries, but also expanded its trade to region in

Indian Ocean, the Red Sea and Persian Bay. In Sui Dynasty and Tang Dynasty (from 6

AD to 7 AD), Maritime Silk Road was more than Silk Road, due to endless wars in areas

covering Silk Road. This trend continued till the era when Zheng, He traveled southeast.

Maritime Silk Road also covers the routine that reached Korea Peninsula and Japanese

islands, and this routine played a secondary role in trade development.

2. International Trade in Modern TimeAfter 15 century, maritime trade dominated the international trade in modern time.

At this stage, Zheng, He had started trade relationship with countries in Southeast Asia,

South Asia and Arab Peninsula within 28 years (from 1405 to 1433). As the increasingly

number of countries became trade partners with China, China had become the great

power in trade during that time. However, after Zheng’s adventure, administrations from

Ming Dynasty to Qing Dynasty preferred the “close-door” policy, gradually weakening

the influence of China’s maritime trade. From the first Opium War to the foundation of

People’s Repu, China had lost her independence in international trade, and was forced to

trade with only a few western countries. At this stage, the economic and trade cooperation

between China and other Asian countries was limited.

China Development Report on South-South Cooperation 2017

6

3. Economic Cooperation in Contemporary EraSince the foundation of People’s Republic of China, the friendship has been

strengthened between Chinese and people from Asia, Africa and Latin America, in the

process of fighting against colonialism and invasion. The trade cooperation between

China and other Asian countries can be divided into three periods.

The first period: from the foundation of People’s Republic of China to the economic

reform in 1978. People’s Republic of China administration actively engaged in

international trade with many countries with the principles of equality and mutual benefit.

Till 1956, due to the blockade by western countries, the main trade partners of China

then were Soviet Union, countries in East Europe and some Asian countries. China’s

imports from developing countries and regions in AsiaA increased from $301 million in

1950 to $614 million in 1956B. In April 1955, Premier Zhou, Enlai led Chinese delegation

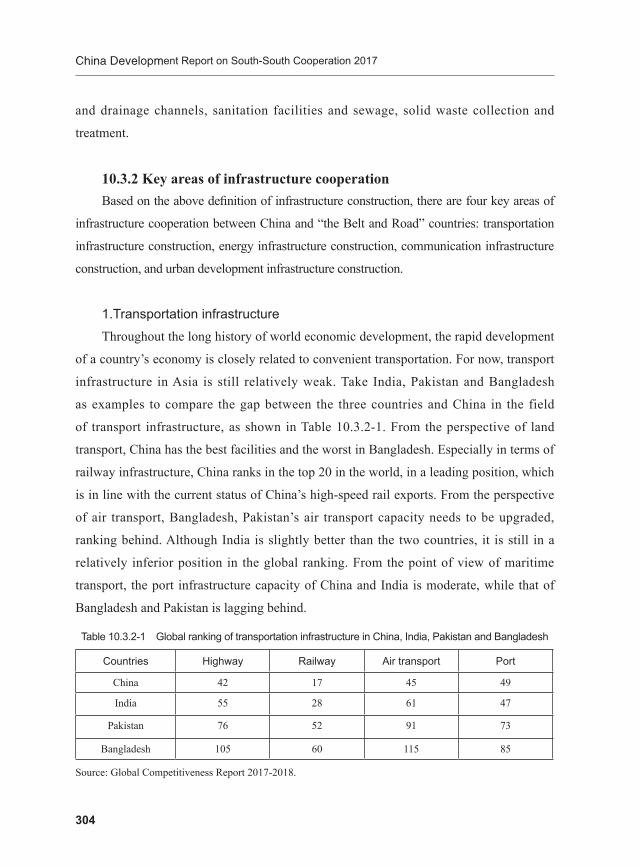

to attend Asia-Africa Conference in Indonesia, expanding China’s influence on Asian

and African countries, and strengthening trade cooperation between China and those

Asian countries. By the end of 1950s and in the early of 1960s, the China-Soviet Union

relationship worsened. China expanded its trade with Asian developing countries. The

trade volume between China and other Asian countries had increased from $591 million

in 1957 to $1.306 billion in 1966C. In “Culture Revolution” between 1966 and 1976,

China’s international trade slowed down. The imports and exports in 1966 ranked 16 and

20, respectively, in the world. Those dropped to 35 and 33, respectively, in 1976D. After

that, China was breeding the force of economic reforms, and international trade took off.

The commodity trade volume between China and other Asian countries in this time had

increased from $3.9 billion in 1976 to $5.32 billion in 1978E.

The second period: from 1978 economic reforms to 2001 before China’s entry to

A Based on statistics by UN, Hong Kong (China), Macau (China) and Taiwan (China) are independent tax identity, considered as developing economies. Without further specification, developing countries and regions in this chapter include those independent tax identities.

B Source: China Foreign Trade Yearbook (1984).

C Ibid.

D Source: History of China’s Foreign Trade, China Commerce and Trade Press, 2015.

E Source: China Foreign Trade Yearbook (1984).

1. Introduction

7

World Trade Organization (WTO). In this period, China’s economy transmitted from

planned economy to “planned economy dominated and market economy supported”,

and quickly to market economy. In international trade, China involved in globalization

effectively, and extended economic and trade cooperation with developing countries

in Asia. The commodity trade volume between China and other Asian countries had

increased from $7.054 billion in 1979 to $154.609 billion in 2000, with average annual

growth rate of 15.84%. It was above the world average growth rate. In addition, China

and other Asian countries and regions experienced Southeast Asian financial crisis that

took place in 1997-1998. China stood up as a responsible country to support its currency

value stable so that the regional economic stability was ensured. To that end, however,

China suffered a great pressure and substantial cost. China’s action was pivotal for

economic and financial stability globally and regionally.

The third period: entry to WTO till now. On December 11, 2001, China became

the member of WTO finally, which was marked as international consensus of China’s

economic development and reforms. It also promotes the trade and economic

development within the region. In this period, China has obtained mountainous progresses

in trade development with developing countries in Asia. In commodity trade, the imports

and exports increased from $160.751 billion in 2001 to $1.35 trillion in 2016. Affected

by Subprime Crisis in USA, the trade volume in 2008 between China and other Asian

countries slide significantly. In 2015 and 2016, trade volume between China and other

Asian countries picked up in the context of global recession. In this period, China does

not only utilize the foreign direct investment from Asian countries and regions to develop

domestic economy, but also start overseas investment in this area. In 2016, investment

flows from China to other Asian countries and regions worth $130.252 billion, accounting

for 66.4% of total foreign direct investment of China in that year. By the end of 2016, the

investment stock from China to Asia was $909.45 billion, amounting to 67% of China’s

foreign investment stock.

1.2.2 Opportunities and Challenges With decade’s effort, China has made a great leap in economic cooperation with

China Development Report on South-South Cooperation 2017

8

Asian developing countries and regions, and also confront with great opportunities. China

proposed “One Belt One Road Initiative” to concentrate on the following five areas:

policy communication, infrastructure connection, trade facilitation, funding support, and

people binding. It lies the solid foundation for further South-South cooperation between

China and other Asian developing countries. In policy communication, China tirelessly

pursues to get different policies of countries and regions compatible. Various countries’

development plans, for example, Kazakhstan’s “Bright Avenue”, Mongolia’s “Grassland

Road”, Russia’s “Cross Asia-Europe Passthrough Construction”, and Indonesia’s “Global

Maritime Support” are compatible with China’s “One Belt One Road Initiative”. In

infrastructure connection, infrastructure like transportation, energy, telecommunication

and electricity are the key sectors. In trade facilitation, China is actively promoting Free

Trade Agreements among Asian countries, to enhance trade and investment facilitation. In

funding support, China has established Asia Infrastructure Investment Bank (AIIB) and

provided $40 billion as Silk Road Fund in 2014, to address the problem of insufficient

funds among Asian developing countries, and provided financial support for Asia’s

economic development. In people biding, China continues to improve people-to-people

exchange mechanism, high-level visits, student exchange, visa facilitation, and offers

good opportunities for cultural exchanges between China and other Asian countries.

No doubt that there are still many challenges ahead. First, there is a huge imbalance

in trade between China and other Asian countries. China runs substantial trade deficits

with some countries in East Asia, while China runs significant trade surplus with

countries in South Asia, for example, with India. Trade imbalance builds up barriers in

further economic cooperation with China. Second, the imbalanced trade structure between

China and other Asian developing countries is obvious. Exports from China mainly are

from labor-intensive and capital-intensive production sectors, imports for China is mainly

in resource-intensive sector. Third, investment from China to other Asian countries varies.

Volatility of investment stock is not negligible in some countries and regions.

1. Introduction

9

1.2.3 Benefits for Economic and Trade Cooperation

1. Benefits for ChinaFirstly, it is good for China to improve its industrial structure in economic trade

cooperation with other Asian developing countries. China has experienced 30-year

fast economic growth, and had a complete set of manufacturing system. So far, China

is in the key period of economic transition. On the one hand, China needs to import

more advanced technology to increase its industrialization level. On the other hanl, the

great number of abundant productive capacity, advanced equipment and technologies

accumulate from those years have become the main source of international capacity

export. Among those developing countries in Asia, some countries and regions have more

advanced industrialization than China, and some desperately demand for more capacity

for they are in the course of industrialization. China and other Asian countries cooperation

in economic development is mutual benefit.

Secondly, China could increase its independence as cooperating with other Asian

countries. China is highly relied on imports such as oil, and the economy is vulnerable

for shocks of such imports. Many Asian countries possess comparative advantages in

energy field over China, and are close to China in geography. They could become reliable

sources for China’s demand, weakening the volatility of international shocks to economic

development.

Thirdly, Asian countries are the indispensable part of China’s “One Belt One Road

Initiative”. This Initiative provides China with many new opportunities in foreign trade.

Asian countries take a pivotal position in this Initiative, and many countries locate at

significant pots in Silk Road and Maritime Silk Road. South-South cooperation between

China and other Asian countries is possible for China to succeed in “One Belt One Road”

building.

2. Benefits for Other Asian Developing CountriesFirstly, less developed countries could take a faster stride in industrialization and

economic development. China’s industrialization has been undertaken by 60 years, has

China Development Report on South-South Cooperation 2017

10

many experiences and solid economic foundation. Thus, China is able to provide support

for those countries in industrialization either financially, technologically or human

resource side. Policy suggestions are also available. In particular, cooperation in areas of

infrastructure and capacity cooperation, China’s advanced technology and management

experience could increase those developing countries’ independence and promote

industrialization.

Secondly, South-South cooperation between China and other Asian countries

is good for optimization of Asian developing countries industrial structure. Some

developing countries in Asia are low-income countries, with simple industrial structure

and low-quality products. China, with years development, has many technologies that

are compatible with its development, which is valuable for those Asian developing

countries. The positive spillovers of knowledge and technology transfer are beneficial for

developing countries in Asia to breed capacity and upgrade industrial structure.

Thirdly, it provides the chance for Asian developing countries to take full advantage

of resources in “One Belt One Road”. South-South cooperation between China and other

Asian countries and “One Belt One Road” are compatible, and generate a good “feedback

loop”. Asian countries could use Silk Road Fund and AIIB when participating in “One

Belt One Road” construction, to promote local economic development.

1.3 Structure of This ReportThis report is No. 5 China South-South Cooperation Report, focusing on cooperation

in Asia, between China and other Asian countries. The rest of the report can be broken

down into three parts.

The first part (including Chapter 2 to Chapter 5) gives a bird view of South-South

cooperation between China and Asian developing countries and regions, including trade

cooperation, investment cooperation, foreign aid and regional economic cooperation.

Chapter 2, from the trade scale, commodity structure in trade, geographical distribution

in trade and trade compatibility and competitiveness, analyzes China’s trade promotion

and deepening in Asia. Chapter 3, based on the analysis of China’s investment to other

1. Introduction

11

Asian countries, further discusses the national characteristics, regional characteristics,

investment modules. It shows the upward trend of China’s investment in Asia and also

indicates that China is the key area for Asian countries’ investment. However, investments

are highly concentrated and have large volatilities. In the future, China should be more

aware of the structural adjustment in investment, to realize balanced investment with

other Asian countries. Chapter 4 takes an overview of China’s foreign aids first, and

focuses on China’s foreign aid since the 21st century in Asian countries. It analyzes the

effectiveness of China’s foreign aids in terms of economic growth, social development,

income increase, poverty alleviation, and environmental protection. Chapter 5, from the

perspective of regional economic cooperation, analyzes South-South cooperation between

China and other Asian countries. It mainly contains the signed and on-negotiating free

trade agreements, border economic cooperation zones, cross-border economic cooperation

areas with other Asian countries. These regional and sub-regional economic cooperation

is vital for South-South cooperation in this area.

The second part (including Chapter 6 to Chapter 9) introduces the features of

cooperation from the geographical perspective, i.e., China’s cooperation with countries in

Southeast Asia, South Asia, West Asia and Middle Asia. This part does not only introduce

the general characteristics of China’s South-South cooperation with countries in those

regions, but also analyzes the specific features in cooperation.

Chapter 10 is taken as the third part of this report. It looks forward to future

development in South-South cooperation given China’s “One Belt One Road Initiative”.

The purpose of this Initiative is to promote economic cooperation between China and

countries related. It is in an attempt to build policy communication, infrastructure

connection, trade facilitation, funding support, and people binding. In detail, productive

capacity and infrastructure are the two important areas in cooperation, and AIIB and Silk

Road Fund offer necessary financial support for this Initiative.

12

2. Trade Relations between China and Asian Developing Countries

Since the reform and opening up, with the rapid growth of China’s economic

strength, the economic relations between China and developing countries and regions in

Asia have been strengthened, and trade relations have been comprehensively enhanced

and deepened.

2.1 The Scale and Growth Developing countries in Asia are important trading partners of China and have

always been an important source of import and export destinations for China. This section

will analyze the trade relations between China and Asian developing countries and

regions in terms of trade scale and growth rate.

2.1.1 The Scale of TradeRegarding the scale of trade between China and Asian developing countries and

regions, this report reveals the import volume and its proportion of China’s total imports,

the amount of exports and its share in China’s total exports, and the total trade. From

these aspects, the report demonstrates a general overview of trade between China and

Asian developing countries and regions from 1998 to 2016.

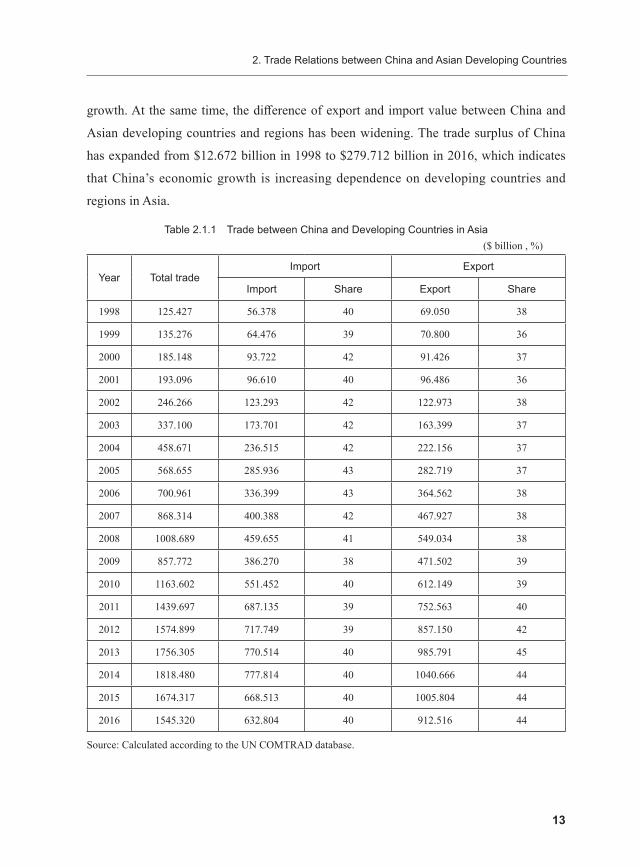

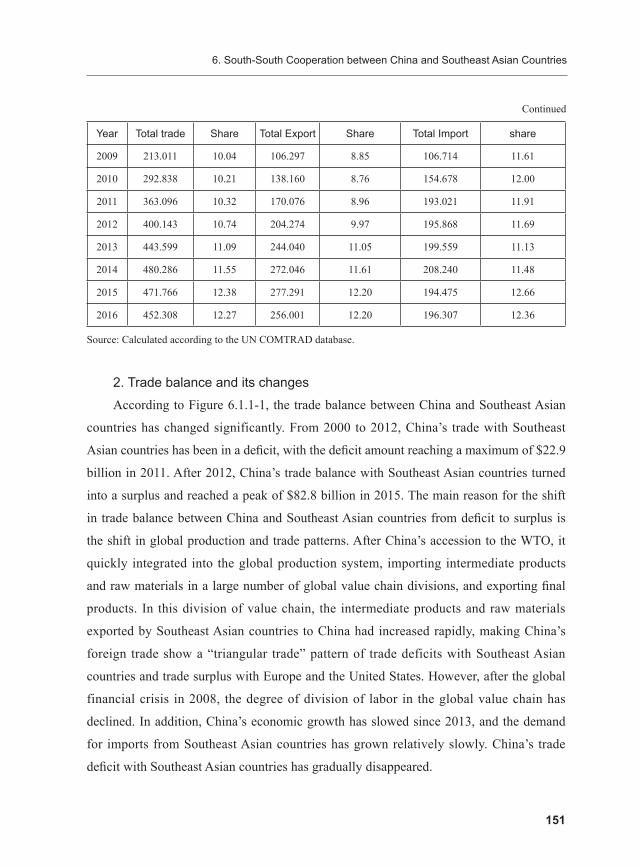

As can be seen from Table 2.1.1, the total trade volume between China and Asian

developing countries and regions has surged from $125.427 billion in 1998 to $1545.320

billion in 2016, an increase of about 12 times. In terms of imports, the import value

was $56.378 billion in 1998, which reached $632.804 billion in 2016. And for exports,

the export value was $69.050 billion in 1998 and reached $912.516 billion in 2016. It

indicates that with the expansion of trade between China and Asian developing countries

and regions, the volume of exports and imports also showed a trend of simultaneous

2. Trade Relations between China and Asian Developing Countries

13

growth. At the same time, the difference of export and import value between China and

Asian developing countries and regions has been widening. The trade surplus of China

has expanded from $12.672 billion in 1998 to $279.712 billion in 2016, which indicates

that China’s economic growth is increasing dependence on developing countries and

regions in Asia.

Table 2.1.1 Trade between China and Developing Countries in Asia ($ billion , %)

Year Total tradeImport Export

Import Share Export Share

1998 125.427 56.378 40 69.050 38

1999 135.276 64.476 39 70.800 36

2000 185.148 93.722 42 91.426 37

2001 193.096 96.610 40 96.486 36

2002 246.266 123.293 42 122.973 38

2003 337.100 173.701 42 163.399 37

2004 458.671 236.515 42 222.156 37

2005 568.655 285.936 43 282.719 37

2006 700.961 336.399 43 364.562 38

2007 868.314 400.388 42 467.927 38

2008 1008.689 459.655 41 549.034 38

2009 857.772 386.270 38 471.502 39

2010 1163.602 551.452 40 612.149 39

2011 1439.697 687.135 39 752.563 40

2012 1574.899 717.749 39 857.150 42

2013 1756.305 770.514 40 985.791 45

2014 1818.480 777.814 40 1040.666 44

2015 1674.317 668.513 40 1005.804 44

2016 1545.320 632.804 40 912.516 44

Source: Calculated according to the UN COMTRAD database.

China Development Report on South-South Cooperation 2017

14

In terms of the proportion of imports and exports, China’s imports from developing

countries and regions in Asia accounted for about 40% of China’s total imports. China’s

exports to developing countries and regions in Asia accounted for a significant change

in China’s total exports around 2010. From 1998 to 2000, China’s exports to Asian

developing countries accounted for less than 40% of China’s total exports, and after 2011

they were all above 40%. It is worth noting that the scale of trade between China and

Asian developing countries and regions is expanding, which accounts for more than 40%

of China’s import and export volume. However, from a trend perspective, from 1998

to 2016, China’s share of imports and exports to developing countries and regions in

Asia did not fluctuate significantly and continued to fluctuate around 40%. It shows that

due to geographical and cultural factors, China has maintained a high trade dependence

on developing countries and regions in Asia for a long time. South-South cooperation

between China and Asian developing countries and regions has a solid trade base.

2.1.2 The Growth RateFurther, from the perspective of trade growth rate, we intend to reveal the

development trend in trade between China and Asian developing countries and regions in

order to fully reflect its overall situation. We are going to make the analysis based on two

kinds of growth, e.g. fixed-base growth and chain growth (or year-on-year growth).

In terms of the chain growth, China’s trade with developing countries and regions

in Asia has experienced three stages of rapid development. The first stage is from 1999

to 2000. Imports increased by 45.36% in 2000, and exports grew by as much as 29.13%.

This is mainly because China had not yet joined the WTO at this stage, and the degree

of international openness is still not high, and the impact of the Asian financial crisis that

began in 1997 was small, also at the same time China began to revitalize the country’s

economy. The second stage is from 2000 to 2010. In this stage, China entered into the

WTO, both import and export grew very fast with reaching 41% and 33% respectively

in 2003. The third stage is from 2010 to 2011, when import and export trade between

China and Asian developing countries and regions continually grew at smaller rate even

though the subprime mortgage crisis broke out in 2007 and continued until 2009 when

2. Trade Relations between China and Asian Developing Countries

15

trade growth was suppressed. After the rapid growth in 2011, the growth rate of trade was

further reduced by the emergence of the European sovereign debt crisis in 2012, which

slowed the growth of trade in the context of slowing global trade growth. It is worth

noting that in 2015 and 2016, both China and Asian developing countries and regions

experienced negative growth in both imports and exports. This was mainly due to the

weak global economic recovery and the deepening of international trade which inhibited

import and export trade.Table 2.1.2 Trade between China and Developing Countries in Asia

(%)

YearImport Export

Chain growth Fixed-Base Growth Chain growth Fixed-Base Growth

1999 14.36 14.36 2.54 2.54

2000 45.36 66.24 29.13 32.41

2001 3.08 71.36 5.53 39.73

2002 27.62 118.69 27.45 78.09

2003 40.88 208.10 32.87 136.64

2004 36.16 319.52 35.96 221.73

2005 20.90 407.18 27.26 309.44

2006 17.65 496.69 28.95 427.97

2007 19.02 610.19 28.35 577.67

2008 14.80 715.31 17.33 695.13

2009 -15.97 585.15 -14.12 582.85

2010 42.76 878.14 29.83 786.53

2011 24.60 1118.81 22.94 989.89

2012 4.46 1173.11 13.90 1141.35

2013 7.35 1266.70 15.01 1327.65

2014 0.95 1279.65 5.57 1407.13

2015 -14.05 1085.78 -3.35 1356.64

2016 -5.34 1022.44 -9.27 1221.54

Source: Calculated according to the UN COMTRAD database.

China Development Report on South-South Cooperation 2017

16

In terms of the fixed-base growth, China’s imports from developing countries in Asia

generally show a rapid growth trend. Based on 1998, the fixed base growth was 14.36%

in 1999 and 1022.44% in 2016, an increase of about 10 times. In view of China’s exports

to developing countries and regions in Asia, based on 1998, the fixed base growth in 1999

was 2.54% and reaching 1221.54% in 2016, an increase of about 12 times. Trade between

China and Asian developing countries and regions showed a strong growth trend.

2.2 The Structure or Pattern of Trade This section examines the structural characteristics of commodity trade between

China and Asian developing countries from a variety of perspectives, classifying

commodity trade structure according to Standard International Trade Classification (SITC),

Economic Big Classification (BEC) and Factor Intensity.

2.2.1 The Structure of Trade by SITCAccording to the first digit of SITC, traded products can be divided into 10

categories, including food and live animals (SITC-0), beverages and tobacco (SITC-

1), non-edible raw materials (SITC-2), fossil fuels (SITC-3), animal and vegetable

oils (SITC-4), chemicals (SITC-5), manufactured goods (SITC-6), machinery and

transportation vehicles (SITC-7), miscellaneous products (SITC-8) and other unclassified

products (SITC-9).

Table 2.2.1-1 shows the product trade structure classified by SITC first digit, which

reflects the export value, import value and their proportion in total trade between China

and developing countries in Asia. As can be seen from the Table, the export between

China and Asian developing countries is mainly concentrated on finished products of raw

materials (SITC-6), machinery and transportation equipment (SITC-7) and miscellaneous

products (SITC-8). For these three categories of products, total exports value in 2000,

2005, 2010 and 2015 were $74.914 billion, $244.25 billion, $530.06 billion and $883.418

billion, respectively. However, in 2016, exports of these three major categories declined

to $791.552 billion. In terms of proportion or share, SITC-6, SITC-7 and SITC-8 as

2. Trade Relations between China and Asian Developing Countries

17

a total account for more than 80% of total exports, specifically, the proportions in

2000, 2005, 2010, 2015 and 2016 were 81.93%, 86.49%, 86.68%, 87.83% and 86.75%

respectively, further illustrating that China’s exports to developing countries in Asia are

highly concentrated in these three categories of products.

Table 2.2.1-1 The Export Structure by SITC (US$ billion, %)

Year 0 1 2 3 4 5 6 7 8 9

2000$ 4.455 0.578 1.584 4.293 0.082 5.094 20.033 32.642 22.239 0.426

% 4.87 0.63 1.73 4.70 0.09 5.57 21.91 35.70 24.32 0.47

2005$ 7.946 0.871 2.382 10.579 0.153 15.555 57.637 136.046 50.842 0.708

% 2.81 0.31 0.84 3.74 0.05 5.50 20.39 48.12 17.98 0.25

2010$ 16.263 1.381 4.757 18.444 0.217 40.129 108.416 319.235 102.955 0.351

% 2.66 0.23 0.78 3.01 0.04 6.56 17.71 52.15 16.82 0.06

2015$ 28.556 2.622 6.435 19.851 0.271 62.371 188.400 504.197 190.821 2.279

% 2.84 0.26 0.64 1.97 0.03 6.20 18.73 50.13 18.97 0.23

2016$ 30.892 2.837 6.056 19.328 0.270 58.190 172.712 453.439 165.401 3.391

% 3.39 0.31 0.66 2.12 0.03 6.38 18.93 49.69 18.13 0.37

Source: Calculated according to the UN COMTRAD database.

Note: 0 to 9 in the first row refers to SITC-0 to SITC-9 respectively. $ and % in second column refers to the

value of trade and its share in the total.

Table 2.2.1-2 The Import Structure by SITC ($ billion, %)

Year 0 1 2 3 4 5 6 7 8 9

2000$ 1.015 0.018 5.320 14.616 0.628 14.930 21.322 31.441 4.288 0.144

% 1.08 0.02 5.68 15.60 0.67 15.93 22.75 33.55 4.58 0.15

2005$ 2.023 0.026 16.556 37.951 2.167 39.676 34.223 122.037 30.841 0.437

% 0.71 0.01 5.79 13.27 0.76 13.88 11.97 42.68 10.79 0.15

2010$ 5.671 0.168 44.225 106.588 6.267 75.528 43.359 210.843 55.410 3.394

% 1.03 0.03 8.02 19.33 1.14 13.70 7.86 38.23 10.05 0.62

China Development Report on South-South Cooperation 2017

18

Year 0 1 2 3 4 5 6 7 8 9

2015$ 12.303 0.560 31.869 118.361 5.535 83.960 49.201 295.865 56.725 14.134

% 1.84 0.08 4.77 17.71 0.83 12.56 7.36 44.26 8.49 2.11

2016$ 11.924 0.572 30.732 99.784 4.846 77.384 43.869 286.611 52.340 24.742

% 1.88 0.09 4.86 15.77 0.77 12.23 6.93 45.29 8.27 3.91

Source: Calculated according to the UN COMTRAD database.

Note: 0 to 9 in the first row refers to SITC-0 to SITC-9 respectively. $ and % in second column refers to the

value of trade and its share in the total.

As far as the imported structure is concerned, China’s imports from developing

countries in Asia account for the largest proportion of machinery and transportation

equipment (SITC-7), and its share has increased from 31.42% in 2000 to 45.6% in 2016.

In view of China’s exports to developing countries in Asia, the proportion of exports

of machinery and transportation equipment also reached 52.15%. This means that the

international vertical specialization of machinery and transportation equipment is clear.

China’s trade characteristics on such products are mainly importing spare parts and export

the finished goods.

From 2000 to 2016, the proportion of fossil fuels, lubricants and related raw

materials (SITC-3) and unspecified chemicals and related products (SITC-5) staid

generally stable, of which the proportion of fossil fuels, lubricants and related raw

materials reached a maximum of 19.33% in 2010. Moreover, the proportion of their

imports far exceeds the proportion of their exports. This means that China is highly

dependent on the energy supply of developing countries and regions in Asia. The most

fluctuated proportion of imported products, which are mainly classified by raw materials

(SITC-6), fell from 22.75% in 2000 to 6.93% in 2016, reflecting the decline in demand

for such products in China.

2.2.2 The Structure of Trade by BECNow we look at the structure of trade between China and Asian developing countries

according to the Economic Broad Classification (BEC). In the first digit of the BEC, the

Continued

2. Trade Relations between China and Asian Developing Countries

19

trade products can be divided into 7 categories, e.g. food and beverage, uncategorized

industrial supplies, fuels and lubricants, capital goods (excluding transportation

equipment) and their spare parts, transportation equipment and its spare parts and

uncategorized consumer products.

Overall, the largest trade between China and Asian developing countries and

regions is the uncategorized industrial supplies (BEC-2) and capital goods (excluding

transportation equipment) and their spare parts (BEC-4). The import and export trade

volume of uncategorical industrial supplies increased from $71.704 billion in 2000 to

$426.641 billion in 2016, an increase of about 6 times. The import and export trade

volume of capital goods (excluding transportation equipment) and its spare parts

increased from $57.503 billion in 2000 to $715.86 billion in 2016, an increase of

approximately 12.4 times. In terms of exported products, the proportion of these two

products in the total product was 59.7% in 2000 and reached 72.1% in 2016. Similarly,

in terms of imported products, the proportion of these two products in total products was

79.6% in 2000 and fell to 76.4% in 2016. This shows that in the trade with developing

countries and regions in Asia, although the import and export of industrial supplies and

capital goods account for a large proportion, however, with the development of China’s

economy, China’s imports of industrial supplies and capital goods are decreasing while

exports are increasing.

Table 2.2.2-1 The Export Structure by BEC

(US$ billion, %)

Year BEC-1 BEC-2 BEC-3 BEC-4 BEC-5 BEC-6 BEC-7

2000Export 3.848 27.833 4.175 26.771 4.7 23.64 0.458

% 4.21 30.44 4.57 29.28 5.14 25.86 0.5

2005Export 7.648 77.209 10.249 124.511 12.674 49.614 0.814

% 2.71 27.31 3.63 44.04 4.48 17.55 0.29

2010Export 16.889 156.782 17.778 284.642 40.739 94.234 1.086

% 2.76 25.61 2.9 46.5 6.66 15.39 0.18

2015Export 30.262 270.604 19.099 459.507 53.945 171.452 0.933

% 3.01 26.9 1.9 45.69 5.36 17.05 0.09

China Development Report on South-South Cooperation 2017

20

Year BEC-1 BEC-2 BEC-3 BEC-4 BEC-5 BEC-6 BEC-7

2016Export 32.654 247.822 18.767 410.341 46.522 153.705 2.706

% 3.58 27.16 2.06 44.97 5.1 16.84 0.3

Source: Calculated according to the UN COMTRAD database.

Table 2.2.2 The Import Structure by BEC

(US$ billion, %)

Year BEC-1 BEC-2 BEC-3 BEC-4 BEC-5 BEC-6 BEC-7

2000Import 1.492 43.871 14.354 30.732 0.732 2.396 0.146

% 1.59 46.81 15.32 32.79 0.78 2.56 0.16

2005Import 3.955 94.678 37.078 140.22 4.129 5.438 0.438

% 1.38 33.11 12.97 49.04 1.44 1.9 0.15

2010Import 11.108 175.386 102.304 240.396 9.408 9.453 3.397

% 2.01 31.8 18.55 43.59 1.71 1.71 0.62

2015Import 17.08 189.13 108.292 314.93 10.85 21.157 7.074

% 2.55 28.29 16.2 47.11 1.62 3.16 1.06

2016Import 15.905 178.819 92.33 304.745 10.394 18.935 11.675

% 2.51 28.26 14.59 48.16 1.64 2.99 1.84

Source: Calculated according to the UN COMTRAD database.

Regarding to the balance of trade, China suffer a trade deficit in fuel and lubricants

(BEC-3) and uncategorical consumer products (BEC-6). Among them, the export trade

of fuels and lubricants is much smaller than the import, and the difference is constantly

expanding. China has large trade deficits in energy products with Asian developing

countries and relies on their energy supply. For uncategorical consumer goods, the

export volume is much larger than the import volume, and the trade surplus is gradually

increasing, which compensates for the trade deficit of energy products to some extent.

These explain that, except for the trade of uncategorized industrial supplies and capital

goods (excluding transportation equipment) and their spare parts, China mainly imports

energy while Asian developing countries mainly import Chinese consumer goods.

Continued

2. Trade Relations between China and Asian Developing Countries

21

2.2.3 The Trade Structure by Factor IntensityAccording to the theory of comparative advantage, the basis of international trade

is the relative difference in factor endowments owned by countries. Trade products can

be divided into resource-intensive, labor-intensive, and capital-and-technology-intensive

products according to Factor Intensity.A The structure of import and export are analyzed

in this section based upon factor intensity.

In general, labor-intensive products account for more than 50% of the import

and export between China and Asian developing countries, and resource-intensive

products account for the smallest proportion. In terms of labor-intensive products, it

takes a proportion of 56.95% in 2000 and reached 61.9% in 2016. The share of capital

and technology-intensive products fell from 25.45% in 2000 to 24.684% in 2016. The

proportion of resource-intensive products also showed a tendency of decline, from 17.6%

in 2000 to 13.41% in 2016. It shows that China’s trade with developing countries in Asia

is mainly concentrated in labor-intensive products.

Table 2.2.3 Trade Structure Classified by Factor Intensity

(US$ billion)

YearResource-intensive Products Labor-Intensive Products

Capital- and Technology-Intensive Products

Export Import Export Import Export Import

2000 10.993 21.596 52.675 52.763 27.759 19.363

2001 11.283 19.791 57.896 55.332 27.307 21.487

2002 12.876 20.778 76.445 74.667 33.651 27.848

2003 15.714 31.068 103.294 102.988 44.391 39.645

2004 16.824 47.167 147.921 130.863 57.412 58.485

2005 21.931 58.723 193.682 156.26 67.106 70.954

2006 22.724 75.461 257.614 179.567 84.225 81.371

2007 28.214 96.471 327.307 205.805 112.406 98.112

A This report defines resource-intensive products as SITC-0 to SITC-4 products based on SITC first digit. Labor-intensive products are defined as SITC-6 and SITC-7 products, capital and technology-intensive product are defined as SITC-5, SITC-8 and SITC-9 products.

China Development Report on South-South Cooperation 2017

22

YearResource-intensive Products Labor-Intensive Products

Capital- and Technology-Intensive Products

Export Import Export Import Export Import

2008 33.793 148.675 386.346 205.73 128.896 105.25

2009 31.684 104.334 329.761 187.23 110.057 94.706

2010 41.063 162.919 427.651 254.201 143.435 134.332

2011 49.131 240.264 516.262 287.603 187.17 159.268

2012 49.308 250.317 573.158 305.158 234.683 162.273

2013 57.283 255.98 660.062 345.509 268.446 169.025

2014 62.663 248.596 680.412 365.765 297.591 163.452

2015 57.734 168.627 692.597 345.067 255.472 154.819

2016 59.383 147.858 626.151 330.479 226.982 154.466

Source: Calculated according to the UN COMTRAD database.

From the perspective of both import and export, before 2005, China’s imports of

labor-intensive products from developing countries in Asia were slightly higher than

exports, showing a small trade deficit. However, since 2005, China’s exports of labor-

intensive products have significantly exceeded imports, and the trade balance has

gradually expanded, showing a trade surplus. For capital and technology intensive

products, China’s exports to developing countries in Asia have been greater than their

imports since 2006, showing a trade surplus. In terms of resource-intensive products,

China’s imports were greater than exports from 2000 to 2016, during which the value

of exports increased only from $10.993 billion to $59.383 billion, while imports were

$21.596 billion in 2000 and rose to $147.858 billion in 2016. It shows that with the

development of China’s economy, China’s dependence on resource-intensive exports has

gradually decreased, but import demand has increased. Such a trade structure has also

enabled other developing countries and regions in Asia, especially those with relatively

backward industries, to take advantage of the increase in import demand brought about by

China’s economic growth to expand exports and achieve economic growth.

Continued

2. Trade Relations between China and Asian Developing Countries

23

2.3 The Structure of Trade in Different Regional in AsiaDue to the different geographical location, income level and stage of economic

development of Asian countries, the trade structure between China and other Asian

regions will also have different characteristics. In view of this, this section mainly

examines the trade structure characteristics between China and different regions of Asia,

countries with different levels of development and major trading partners in order to

further reveal the trade characteristics between China and different types of developing

countries and regions in Asia.

2.3.1 Trade Structure by RegionAsia can be divided into East Asia, South Asia, Southeast Asia, West Asia and

Central Asia by region.A Based on the geographical division, we will examine China’s

import and export trade scale and the growth rate of trade in various regions of Asia and

explore the trade structure between China and other parts of Asia. Table 2.3.1 shows the

trade profiles of China and Asian developing countries and regions from 1998 to 2016.

In terms of trade scale, China’s trade with developing countries and regions in Asia

is mainly concentrated in East Asia and Southeast Asia. This on the one hand is due to

the similar geographical proximity, cultural homology and similar level of economic

development in East Asia, Southeast Asia and China. On the other hand, there is a lot

of entrepot trade with Hong Kong (China), Macao (China) and Taiwan (China). As far

as Hong Kong (China), Macao (China) and Taiwan (China) regions are concerned, the

average annual export volume of China mainland to Hong Kong (China), Macao (China)

and Taiwan (China) was $203.44 billion from 1998 to 2016, while the average annual

import volume was $93.346 billion. Due to the existence of entrepot trade, the export

volume of China mainland with Hong Kong (China), Macao (China) and Taiwan (China)

is far greater than the import value.

From the perspective of trade growth, although the export volume of China and

A East Asia here includes Taiwan (China), Hong Kong (China), Macau (China), South Korea, Mongolia and North Korea.

China Development Report on South-South Cooperation 2017

24

Central Asia, South Asia and West Asia is limited, the average ring growth rate of export

volume is very impressive, showing great trade potential. In terms of imports, import

volume growth of China with West Asia and Central Asia is the fastest, with an average

annual growth rate of 27.44% and 23.79%, respectively. This is mainly because China

imports a large amount of energy, mineral and other resource products from West Asia

and Central Asia. Although the average annual growth rate of trade between China and

East Asia and Southeast Asia is not high, it is still an important source of imports and an

export market country due to its large base.

Table 2.3.1 China’s Trade with Different Regions in Asia: 1999-2016

(US$ billion, %)

Southeast Asia East Asia South Asia West Asia Central Asia

Average Export 113.74 258.3 39.236 58.349 11.358

Average growth rate of exports 19.9 13.76 23.56 20.8 29.18

Proportion in the total exports 23.65 53.7 8.16 12.13 2.36

Average import 108.071 200.917 12.75 64.864 9.152

Average growth rate of imports 17.84 13.44 18.02 27.44 23.79

Proportion in the total import 27.31 50.77 3.22 16.39 2.31

Source: Calculated according to UN COMTRAD database.

We can see that mainly trade with East Asia and Southeast Asia. In terms of China’s

export, East Asia and Southeast Asia accounted for 53.7% and 23.65% respectively, and

the two regions accounted for 77.35% of China’s total exports to Asia. In terms of China’s

import, East Asia and Southeast Asia accounted for 50.77% and 27.31% respectively, and

the two regions accounted for 78.08% of China’s total import in Asia. This means that

East Asia and Southeast Asia are important trading partners of China in Asia, and China’s

trade with Central Asia, South Asia and West Asia shows great potential.

2.3.2 Trade Structure by Level of DevelopmentAccording to the income level, developing countries in Asia are divided into high-

income, middle-income and low-income countries respectively. With which, we can

2. Trade Relations between China and Asian Developing Countries

25

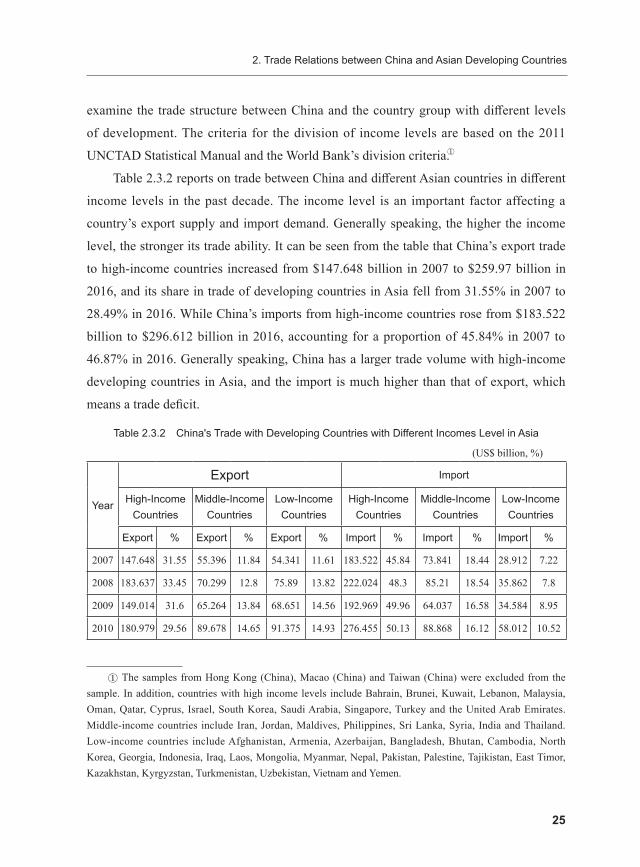

examine the trade structure between China and the country group with different levels

of development. The criteria for the division of income levels are based on the 2011

UNCTAD Statistical Manual and the World Bank’s division criteria.A

Table 2.3.2 reports on trade between China and different Asian countries in different

income levels in the past decade. The income level is an important factor affecting a

country’s export supply and import demand. Generally speaking, the higher the income

level, the stronger its trade ability. It can be seen from the table that China’s export trade

to high-income countries increased from $147.648 billion in 2007 to $259.97 billion in

2016, and its share in trade of developing countries in Asia fell from 31.55% in 2007 to

28.49% in 2016. While China’s imports from high-income countries rose from $183.522

billion to $296.612 billion in 2016, accounting for a proportion of 45.84% in 2007 to

46.87% in 2016. Generally speaking, China has a larger trade volume with high-income

developing countries in Asia, and the import is much higher than that of export, which

means a trade deficit.

Table 2.3.2 China's Trade with Developing Countries with Different Incomes Level in Asia

(US$ billion, %)

Year

Export Import

High-Income Countries

Middle-Income Countries

Low-Income Countries

High-Income Countries

Middle-Income Countries

Low-Income Countries

Export % Export % Export % Import % Import % Import %

2007 147.648 31.55 55.396 11.84 54.341 11.61 183.522 45.84 73.841 18.44 28.912 7.22

2008 183.637 33.45 70.299 12.8 75.89 13.82 222.024 48.3 85.21 18.54 35.862 7.8

2009 149.014 31.6 65.264 13.84 68.651 14.56 192.969 49.96 64.037 16.58 34.584 8.95

2010 180.979 29.56 89.678 14.65 91.375 14.93 276.455 50.13 88.868 16.12 58.012 10.52

A The samples from Hong Kong (China), Macao (China) and Taiwan (China) were excluded from the sample. In addition, countries with high income levels include Bahrain, Brunei, Kuwait, Lebanon, Malaysia, Oman, Qatar, Cyprus, Israel, South Korea, Saudi Arabia, Singapore, Turkey and the United Arab Emirates. Middle-income countries include Iran, Jordan, Maldives, Philippines, Sri Lanka, Syria, India and Thailand. Low-income countries include Afghanistan, Armenia, Azerbaijan, Bangladesh, Bhutan, Cambodia, North Korea, Georgia, Indonesia, Iraq, Laos, Mongolia, Myanmar, Nepal, Pakistan, Palestine, Tajikistan, East Timor, Kazakhstan, Kyrgyzstan, Turkmenistan, Uzbekistan, Vietnam and Yemen.

China Development Report on South-South Cooperation 2017

26

Year

Export Import

High-Income Countries

Middle-Income Countries

Low-Income Countries

High-Income Countries

Middle-Income Countries

Low-Income Countries

Export % Export % Export % Import % Import % Import %

2011 218.925 29.09 113.267 15.05 114.922 15.27 346.619 50.44 111.173 16.18 88.777 12.92

2012 245.891 28.69 114.432 13.35 133.896 15.62 363.293 50.62 102.331 14.26 101.75 14.18

2013 273.163 27.71 122.714 12.45 161.611 16.39 386.816 50.2 99.422 12.9 111.277 14.44

2014 296.621 28.5 144.564 13.89 186.533 17.92 390.306 50.18 103.693 13.33 118.974 15.3

2015 296.525 29.48 149.883 14.9 179.448 17.84 330.084 49.38 86.11 12.88 96.184 14.39

2016 259.97 28.49 150.312 16.47 171.614 18.81 296.612 46.87 83.008 13.12 97.497 15.41

Source: Calculated according to the UN COMTRAD database.

While China’s export trade to middle-income and low-income countries is generally

growing with a slight upward trend of the proportion in the total. In terms of import

and export, China’s trade with middle-income and low-income countries showed an

increasing trend in general, trade volume reaching the maximum in 2014, followed a

downward trend from 2015 to 2016 due to the global trade decline.

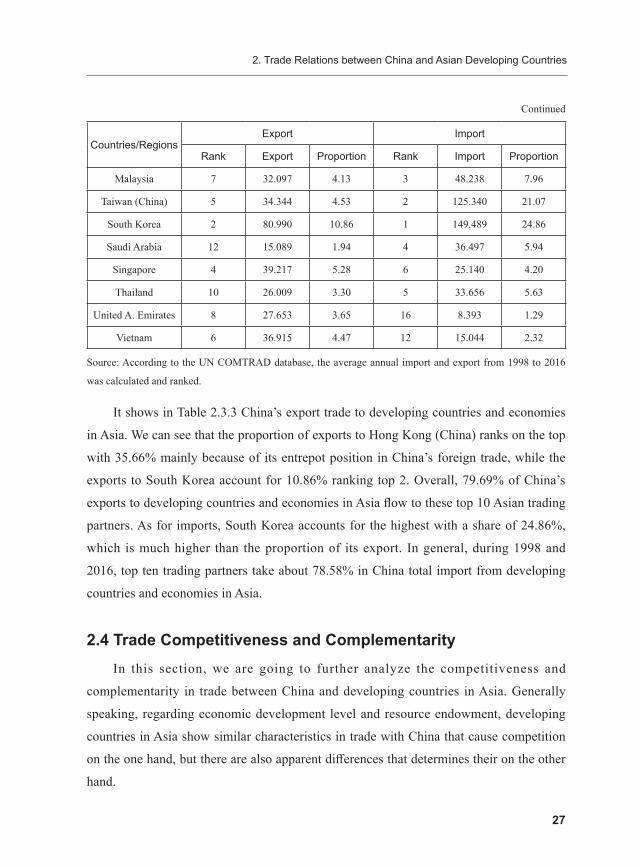

2.3.3 China’s Major Trading Partners in AsiaWe are going to use the average annual import and export data from 1998 to 2016

to analyze the trade structure of China with its major trading partners in Asia by both

country and region. China’s top ten trading partners in Asia are Hong Kong (China),

South Korea, Taiwan (China), Malaysia, Singapore, Thailand, India, Saudi Arabia,

Vietnam and the United Arab Emirates.

Table 2.3.3 Top Ten Trading Partners of China in in Asia: 1998-2016

(US$ billion, %)

Countries/RegionsExport Import

Rank Export Proportion Rank Import Proportion

Hong Kong (China) 1 271.640 35.66 10 13.835 2.35

India 3 44.371 5.85 11 17.007 2.96

Continued

2. Trade Relations between China and Asian Developing Countries

27

Countries/RegionsExport Import

Rank Export Proportion Rank Import Proportion

Malaysia 7 32.097 4.13 3 48.238 7.96

Taiwan (China) 5 34.344 4.53 2 125.340 21.07

South Korea 2 80.990 10.86 1 149.489 24.86

Saudi Arabia 12 15.089 1.94 4 36.497 5.94

Singapore 4 39.217 5.28 6 25.140 4.20

Thailand 10 26.009 3.30 5 33.656 5.63

United A. Emirates 8 27.653 3.65 16 8.393 1.29

Vietnam 6 36.915 4.47 12 15.044 2.32

Source: According to the UN COMTRAD database, the average annual import and export from 1998 to 2016

was calculated and ranked.

It shows in Table 2.3.3 China’s export trade to developing countries and economies

in Asia. We can see that the proportion of exports to Hong Kong (China) ranks on the top

with 35.66% mainly because of its entrepot position in China’s foreign trade, while the

exports to South Korea account for 10.86% ranking top 2. Overall, 79.69% of China’s

exports to developing countries and economies in Asia flow to these top 10 Asian trading

partners. As for imports, South Korea accounts for the highest with a share of 24.86%,

which is much higher than the proportion of its export. In general, during 1998 and

2016, top ten trading partners take about 78.58% in China total import from developing

countries and economies in Asia.

2.4 Trade Competitiveness and Complementarity In this section, we are going to further analyze the competitiveness and

complementarity in trade between China and developing countries in Asia. Generally

speaking, regarding economic development level and resource endowment, developing

countries in Asia show similar characteristics in trade with China that cause competition

on the one hand, but there are also apparent differences that determines their on the other

hand.

Continued

China Development Report on South-South Cooperation 2017

28

Complementarity refers to the trade structure compatibility between two countries. If

a country’s imports happen to be exports from another country, the two countries are said

to be fully complementary in trade. Obviously, the degree of complementarity depends

on the resource endowment and technical differences between the two countries, that is,

the comparative advantage of the two. In general, the greater the resource endowment

and technological differences between countries, the stronger the complementarity

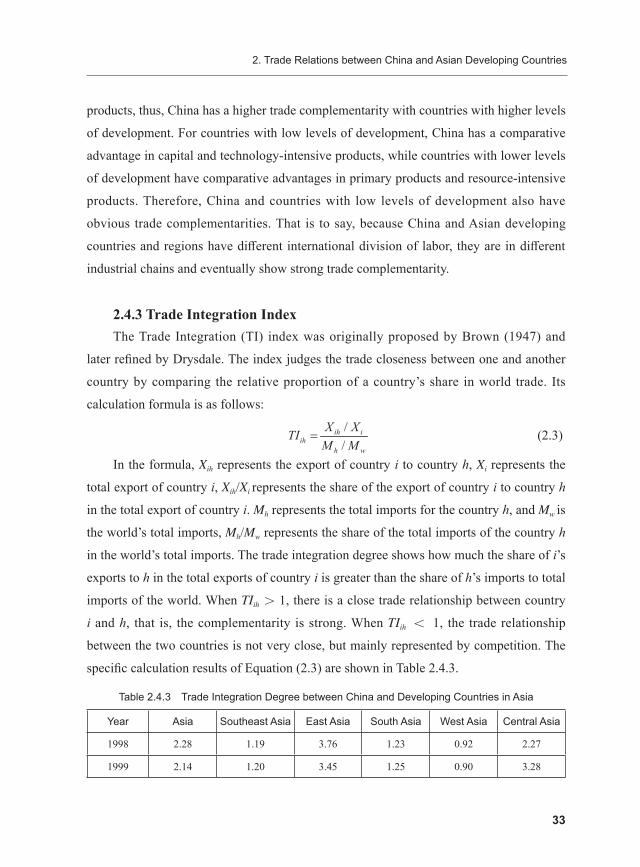

of trade, and vice versa. The Trade Complementarity Index is the most used index to

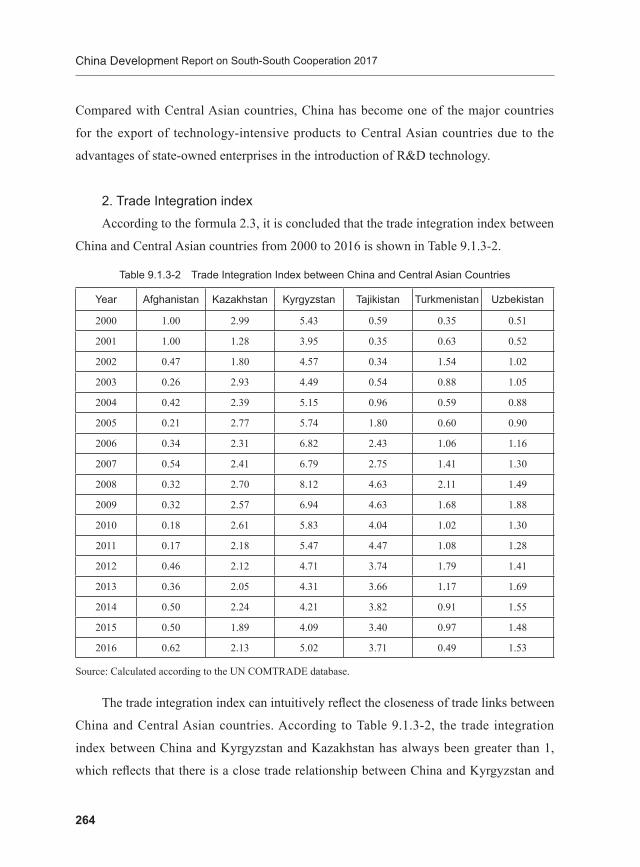

measure complementarity, and the Trade Integration index can also intuitively reflect

the closeness of trade links between the two countries and economies. Revealed

Comparative Advantage and the Intra-industry Trade Index can also clearly reflect the

degree and source of complementarity. Therefore, we use these four indices to analyze

the complementarity and source of trade between China and Asian developing countries

and regions. Regarding to the fact that the trade between China and Asian developing

countries is not only complementary but also competitive, we are going to use the

Trade Competitiveness Index to measure the level of competition between China and

developing countries and regions in Asia.

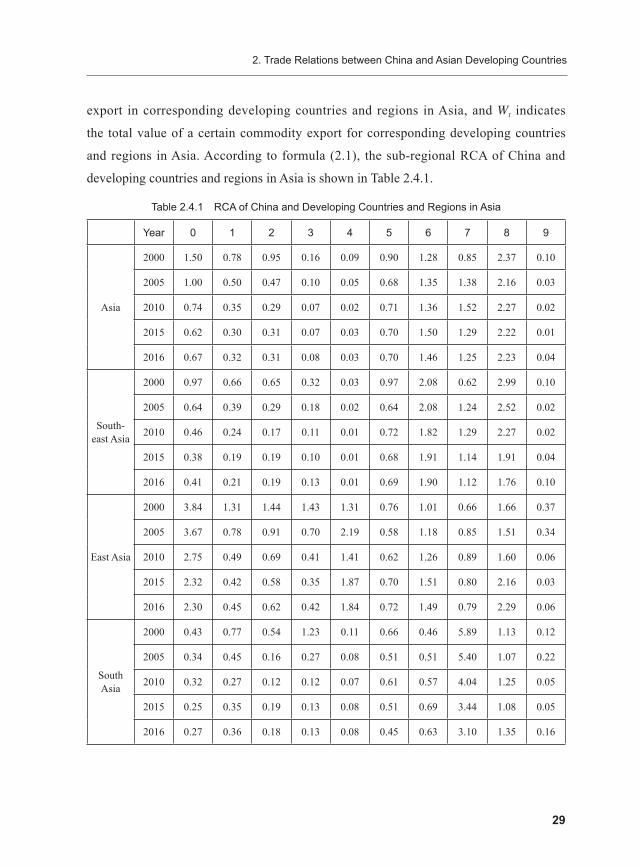

2.4.1 Revealed Comparative AdvantageRevealed Comparative Advantage (RCA), also known as the Export Performance

Index, is a measure of whether a product in a country or region has a comparative

advantage. The indicator can be calculated as the ratio of the proportion of a country’s

exports to its total exports and the proportion of such goods in the world to the world’s

total exports. If a country’s RCA on a product is greater than 1, it indicates that the

country has a revealed comparative advantage on such goods; if the RCA is less than

1, it indicates that the country does not have a revealed comparative advantage on the

commodity. The formula for calculating the RCA is as follows:

(2.1)

In the formula, Xi indicates the export value of a commodity in China, Xt indicates

the China’s total export value of the commodity, Wi indicates the value of a commodity

2. Trade Relations between China and Asian Developing Countries

29

export in corresponding developing countries and regions in Asia, and Wt indicates

the total value of a certain commodity export for corresponding developing countries

and regions in Asia. According to formula (2.1), the sub-regional RCA of China and

developing countries and regions in Asia is shown in Table 2.4.1.

Table 2.4.1 RCA of China and Developing Countries and Regions in Asia

Year 0 1 2 3 4 5 6 7 8 9

Asia

2000 1.50 0.78 0.95 0.16 0.09 0.90 1.28 0.85 2.37 0.10

2005 1.00 0.50 0.47 0.10 0.05 0.68 1.35 1.38 2.16 0.03

2010 0.74 0.35 0.29 0.07 0.02 0.71 1.36 1.52 2.27 0.02

2015 0.62 0.30 0.31 0.07 0.03 0.70 1.50 1.29 2.22 0.01

2016 0.67 0.32 0.31 0.08 0.03 0.70 1.46 1.25 2.23 0.04

South-east Asia

2000 0.97 0.66 0.65 0.32 0.03 0.97 2.08 0.62 2.99 0.10

2005 0.64 0.39 0.29 0.18 0.02 0.64 2.08 1.24 2.52 0.02

2010 0.46 0.24 0.17 0.11 0.01 0.72 1.82 1.29 2.27 0.02

2015 0.38 0.19 0.19 0.10 0.01 0.68 1.91 1.14 1.91 0.04

2016 0.41 0.21 0.19 0.13 0.01 0.69 1.90 1.12 1.76 0.10

East Asia

2000 3.84 1.31 1.44 1.43 1.31 0.76 1.01 0.66 1.66 0.37

2005 3.67 0.78 0.91 0.70 2.19 0.58 1.18 0.85 1.51 0.34

2010 2.75 0.49 0.69 0.41 1.41 0.62 1.26 0.89 1.60 0.06

2015 2.32 0.42 0.58 0.35 1.87 0.70 1.51 0.80 2.16 0.03

2016 2.30 0.45 0.62 0.42 1.84 0.72 1.49 0.79 2.29 0.06

South Asia

2000 0.43 0.77 0.54 1.23 0.11 0.66 0.46 5.89 1.13 0.12

2005 0.34 0.45 0.16 0.27 0.08 0.51 0.51 5.40 1.07 0.22

2010 0.32 0.27 0.12 0.12 0.07 0.61 0.57 4.04 1.25 0.05

2015 0.25 0.35 0.19 0.13 0.08 0.51 0.69 3.44 1.08 0.05

2016 0.27 0.36 0.18 0.13 0.08 0.45 0.63 3.10 1.35 0.16

China Development Report on South-South Cooperation 2017

30

Year 0 1 2 3 4 5 6 7 8 9

West Asia

2000 1.85 0.53 1.40 0.05 0.37 1.20 1.80 5.20 7.09 0.06

2005 1.14 0.43 1.11 0.04 0.20 1.00 1.70 5.73 5.54 0.02

2010 0.88 0.45 0.63 0.03 0.20 0.86 1.72 6.40 6.28 0.01

2015 0.85 0.38 0.53 0.03 0.17 0.82 1.76 4.66 4.65 0.00

2016 0.94 0.38 0.52 0.03 0.15 0.84 1.67 4.57 4.12 0.01

Central Asia

2000 4.68 0.92 0.32 0.06 2.00 15.01 4.03 34.74 65.50 0.01

2005 1.26 0.70 0.14 0.03 1.18 2.49 1.02 34.09 67.37 0.13

2010 0.74 0.76 0.14 0.02 0.36 1.30 1.24 67.68 71.49 0.03

2015 0.60 0.38 0.12 0.02 0.31 0.91 1.24 28.10 37.10 0.05

2016 0.53 0.38 0.09 0.02 0.22 0.97 0.96 21.87 16.29 0.12

Source: Calculated according to the UN COMTRAD database.

Note: 0 to 9 in the first row refers to SITC-0 to SITC-9 respectively.

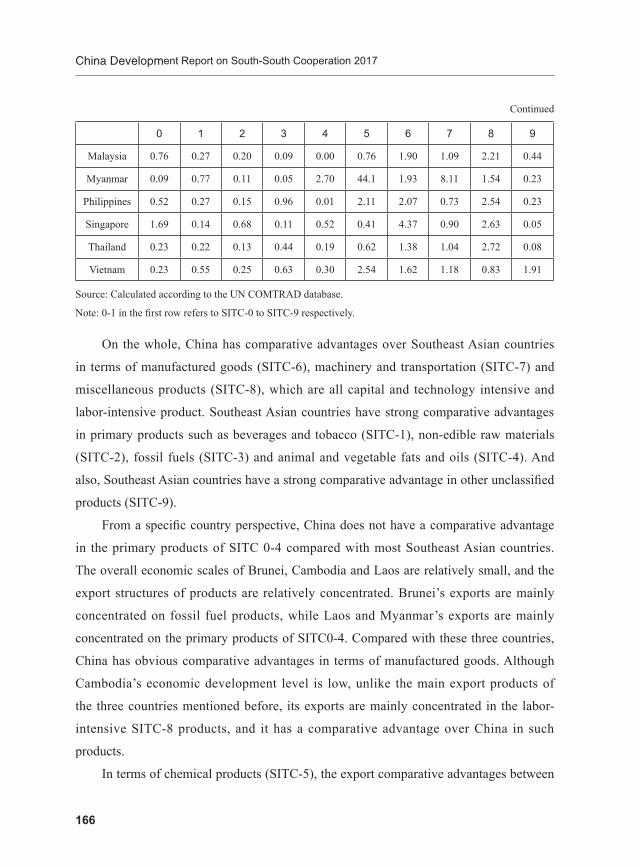

According to the calculation results of the reveled comparative advantage, we can

find the following characteristics:

Firstly, China’s comparative advantage is mainly reflected in SITC-6, -7 and -8. The

comparative advantages of SITC-6 and SITC-8 products illustrate China’s advantages in

labor-intensive products. The RCA of SITC-7 products increased from 0.85 in 2000 to 1.25

in 2016, which shows that China has gradually demonstrated comparative advantages

in capital and technology-intensive products, which is consistent with China’s industrial

transformation and development.

Secondly, in terms of regions, China’s labor-intensive products, capital and

technology-intensive products have shown comparative advantages in trade with South

Asia, Southeast Asia, West Asia and Central Asia. Southeast Asia, West Asia and Central

Asia are mainly represented by comparative advantages in primary products and resource

products showing a relatively high complementarity.

Thirdly, in the trade with East Asia, China’s comparative advantages are mainly on

the products of food and live animals, animal and vegetable oils, manufactured goods

and miscellaneous products. However, there is no comparative advantage in the capital

Continued

2. Trade Relations between China and Asian Developing Countries

31

and technology-intensive products. This shows that the trade complementarity between

China and East Asia mainly comes from the mutual trade of labor-intensive products and

technology-intensive products.

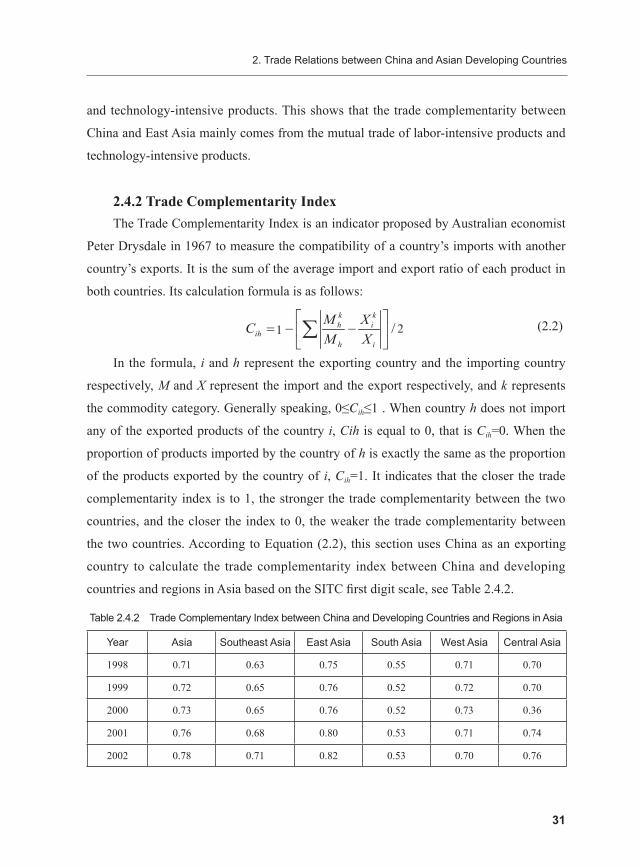

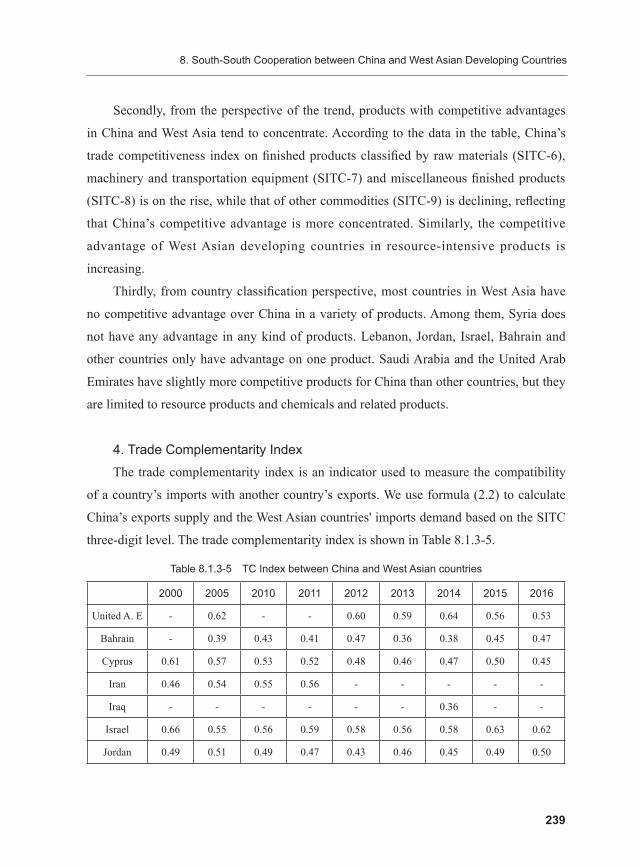

2.4.2 Trade Complementarity IndexThe Trade Complementarity Index is an indicator proposed by Australian economist

Peter Drysdale in 1967 to measure the compatibility of a country’s imports with another