Chapter: One Introduction

121

Chapter: One Introduction

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of Chapter: One Introduction

Chapter: One

Introduction

1.1 Introduction Modern Banking is a result of evolutions driven by changing

economic activities and lifestyles. Entering a new millennium,

banking needs have become more diverse and exotic than ever

before. After our independence from Pakistan, apart from the

foreign Banks all the commercial Banks were nationalized. In 1983,

the government of Bangladesh gave permission to establish private

Banks in this country. After this regulation most of these

nationalized commercial Banks were shifted into the private

sector. Many private Banks were established in this country.

Shahjalal Islami Bank Limited emerged as Islamic Bank on April 01,

2001. The Bank’s rules and procedures are based on “Islamic

Shariah” of course; the Mymensingh Branch is Islamic Branch from

its opening.

Banks are financial institutions and have to utilize their

generated fund effectively by investing in different sectors. Its

team of dedicated professionals is committed to provide an

unparalleled service by using the latest technology to make

bankable proposals harvest maximum benefits for the customers, the

shareholders and the society at large. In order to ensure a

satisfactory level of recovery rate from its investing activities,

banks should have a sound customer service. Identifying the

reliable and real clients in providing cash, credit and advances

in foreign business is essential for banking business and

application of an appropriate customer services can help this

respect. As foreign business is one of the most important

considerations in the banking sector, they should be given a

chance to exchange their views and ideas about the export, import

and foreign remittance procedures. This study attempted to reveal

the facts about the strengths and weakness, if any, of the foreign

exchange operations of Shahjalal Islami Bank Limited with a view

to have an in-depth idea about the foreign business of the banking

business. As an integral part of the Internship of the BBA

program, this study has been completed and submitted for

evolution. Foreign exchange division is a major part of the bank

and management is sincerely concerned with the credit disbursement

and recovery of loan related with foreign exchange. In order to

strengthen foreign exchange operations of the bank, it has been

decided to follow some techniques for performance appraisal. With

the use of such techniques the management of Shahjalal Islami Bank

Limited has shown their efficiency.

1.2 Background of the studyIn today’s modern and globalization world, business sector is

competitive. Theoretical knowledge is not enough for a business

student because there is a gap between theoretical knowledge and

practical field. The BBA program of Jatiya Kabi Kazi Nazrul Islam

University, Trishal, Mymensingh is designed to focus on

theoretical and professional development of students to take up

business as a profession as well as service as a career. This

internship provides the students to link up their theoretical

knowledge into practical fields.

This report on “Evaluation of Foreign Exchange Operations: A Case

Study on Shahjalal Islami Bank Limited” has been prepared as a

requirement of the three months internship program. As the

practical orientation is an integral part of the BBA degree

requirement, I was sent to Shahjalal Islami Bank Limited

(Mymensingh Branch) to take the real life exposure of the

activities of banking financial institutions from September 16,

2012 to December 15, 2012. Assigned by the Internship Supervisor,

this report is prepared by the author and submitted to the

Accounting and Information Systems Department. This study mainly

covered the areas of performance of Shahjalal Islami Bank and its

services on export, import and foreign remittance operations.

1.3 Objective of the study The Specific objectives of the study are:

To gather knowledge about the Export Operations and evaluate

the performance.

To gather knowledge about the Import Operations and evaluate

the performance

To gather knowledge about the Remittance Operations and

evaluate the performance

To explore the problems of Foreign Exchange operations.

To recommend solutions of the problems faced by SJIBL.

1.4 Scope of the studyShahjalal Islami Bank Limited is one of the leading Banks in

Bangladesh. The scope of the study is

limited to the Mymensingh Branch only. The report covers the

export business, import business and foreign remittance operations

of the bank.

1.5 MethodologyThis report is a descriptive one, which is administered by

collecting primary and secondary data. Descriptive Research has an

important objective: gives description of something marketing

characteristics of function (Malhotra, 2001) and also the

description of phenomenon or characteristic associated with an

object population (who, what, when, where and how of a topic,

Copper, 2001).

1.6 Sources of DataThis study covered two types of data, which are:

Primary Sources 1.Information discussed and

observed

2.

Daily dairy

3.

Practical deskwork.

Secondary sources 1.Various publication of

SJIBL

2. Annual

statements of the bank.

3. SJIBL website.

4. Different books about banking.

All this Primary and Secondary data were collected, organized,

analyzed and interpreted to draw some findings.

1.7 Limitations of the studyLike any other articles and theories, this study is not free from

limitations. It is tried level best to overcome these limitations

through extensive study, hard and sincere devotion to the assigned

duty. The major limitations are:

This paper has focused on the most sensitive part of the

organization i.e., foreign exchange operations. So the bank

authority hesitated to disclose important information to

maintain business secrecy.

Only three months time is not enough to complete such a study

in a lucid manner.

The whole report was prepared on the Mymensingh branch of

SJIBL and so it didn’t not focus on the whole banking sector

of the country.

The bank personnel and officials were very busy with their

occupational activities. Hence it was little bit difficult for

them to help within their high schedule.

Lack of opportunity to work in all departments for a longer

period.

1.8 Time Line of the StudySeptember 16, 2012 - December 15, 2012 (in SJIBL, Mymensingh

Branch)

Chapter: TwoOverview of Shahjalal Islami Bank

Limited

2.1 History and Growth of Islamic BankingThe Islamic Banking movement as we know it today is a recent

phenomenon. The history of modern Islamic Banking dates back to

the 1950s when a small private Islamic Bank appeared in Pakistan

but subsequently wound up. In the decade of 1950s, the concept of

Islamic Banking was a matter of thinking & research and the result

was preserved in the papers of different scholars of the Muslim

World. The 1960s was the decade of practical experiment and 1970s

was the decade for establishment. The decade of 1980s was thedecade of success and expansion at a faster rate.

During 1960s, it was observed that the Muslims of Malaysia used to

save primarily for performing Hajj and such savings were mostly

kept idle in pillows, under mattresses and floors for avoiding

interest, which was unproductive & damaging for the growth &

development of the economy. For utilizing these savings, the

Malaysian Government in 1962 established an interest free

financial institution known as “Pilgrims Savings Corporation”.

Though it was not a full-fledged bank, even then we can say that

it was the beginning of an institution free of interest, which is

unconditionally prohibited in Islam.

‘Mitghamr Bank’ is the pioneer modern Islamic Banking which was

established by Dr. Ahmed-El-Nagger in 1963 by his personal

endeavor at Mitghamr in Egypt with a view to bring some

development in socio-economic field through Islamic banking. The

bank conducted its banking operation successfully in the light of

Islamic Shari’ah for about five years. Now the Islamic Bankers of

the world has treated the short life of Mitghamr Bank as the first

model of Islamic Banking. A survey report by the National

Institute for Management Development, Cairo, Egypt shows that the

Mitghmr Bank was tremendously successful in achieving its

objectives. In addition, the tremendous success of the bank was

the cause of its closure by the vested interest in 1967.

Islamic Development Bank (IDB) was established in 1975 and during

the following three years 7 (seven) Islamic Banks & financial

institutions namely (i) Dubai Islami Bank, (ii) Kuwait Finance

House, (iii) Faisal Islami Bank, Sudan, (iv) Jordan Islami Bank

for Finance and Investment, (v) Islamic Banking System

International Holding S.A., Luxembourg, (vi) Faisal Islami Bank of

Egypt and (vii) Islamic Investment Co. Ltd., Shari’ah, were

established.

In 1978, Islamic Foreign Ministers Conference in Dakar (Senegal)

recommended to the members of OIC to make systematic efforts to

establish Islamic Banks gradually and during the next three years

of their recommendation, 20 Islamic Banks and financial

institutions came into being.

Till now, near about 300 Islamic banks and financial institutions

in about 40 countries of Asia, Africa, Europe, America and

countries like U.K., U.S.A., Germany, Argentina, Denmark,

Luxembourg, Switzerland and India have been established. The

banking system of Iran and Sudan has been totally remodeled on the

basis of islami shari’ah.

2.2 Islamic Banking in BangladeshBangladesh is one of the largest Muslim Countries in the World.

The people of this country are deeply committed to Islamic way of

life as enshrined in the Holy Qur’an and the Sunnah. Naturally, it

remains a keen ordeal desire in their hearts to fashion and design

their economic lives in accordance with the precepts of Islam.

With these end in view, in August 1974, Bangladesh signed the

charter of Islamic Development Bank (IDB) and committed itself to

reorganize its economy and financial system as per Islamic Shari’ah.

In November 1980, Bangladesh Bank, the country’s Central Bank,

sent a representative to study the working system of several

Islamic Banks abroad.

In January 1981, the then President of the Peoples Republic of

Bangladesh while addressing the 3rd Islamic Summit Conference held

at Makkah and Taif suggested, “The Islamic Countries should

develop a separate Banking system of their own in order to

facilitate their trade and commerce”. This statement of the

President reflected the people’s desire, attitude & commitment of

Bangladesh towards establishing Islamic Banks and financial

institutions in the country.

In November 1982, a delegation of Islamic Development Bank (IDB)

visited Bangladesh and showed keen interest to participate in

establishing a joint venture Islamic Bank in the private sector.

They found a lot of works have already been done and Islamic

Banking was in a ready from for immediate introduction. Two

professional bodies namely Islamic Economics Research Bureau

(IERB) and Bangladesh Islamic Bankers Association (BIBA) made

significant contribution towards introduction of Islamic Banking

in Bangladesh. At last, the long drawn struggle to establish an

Islamic Bank in Bangladesh became a reality and Islamic Bank

Bangladesh Limited (IBBL) was incorporated on March 13, 1983 and

commenced banking operations on and form March 30, 1983 as the

first Islamic Bank in the South East Asia. It is the first joint

venture Bank in Bangladesh with the equity participation of

Islamic Development Bank (IDB), Kingdom of Saudi Arabia, Bahrain

and Kuwait.

Thereafter, as of now, nine other Bangladesh Bank and one foreign

Bank have launched banking operations in the private sector based

on Islamic Shari’ah. Shahjalal Islami Bank Limited is one of them.

It was established on April 01, 2001 and commenced its operation

in accordance with Islamic Shahriah on the 10th May 2001.The

Emergence of Islamic Banking system creates a new dimension in the

economic development of Bangladesh. In the financial sector of

Bangladesh, Islamic Bank plays a new horizon in the private

financial sector with a new phenomena of Investment i.e., Shari’ah

Banking system. The Philosophy of these Banking activities is to

maintain the Islamic rules and at the same time the principle of

business followed by the great prophet Mohammed (SM).

2.3 Overview of Shahjalal Islami Bank Limited:Shahjalal Islami Bank Limited (SJIBL) is based on Islamic Shariah.

It is named after the name of a saint Hajrat Shahjalal (R) who

dedicated his life for the cause of peace in this world and

hereafter and served the humanity. It was incorporated as a Public

Limited Company on 1st April 2001 under companies Act 1994.It

commenced its commercial operation in accordance with principle of

Islamic Shariah on the 10th May 2001 under the Bank Companies Act,

1991. During last eleven years SJIBL has diversified its service

coverage by opening new branches at different strategically

important locations across the country offering various service

products both investment & deposit. Islamic Banking, in essence,

is not only INTEREST-FREE banking business, it carries deal wise

business product thereby generating real income and thus boosting

GDP of the economy. Board of Directors enjoys high credential in

the business arena of the country, Management Team is strong and

supportive equipped with excellent professional knowledge under

leadership of a veteran Banker Alhaj Anwer Hossain khan.

At present, SJIBL has been carrying on business through its 73

branches and 6 SME centers spread all over the country. The Bank

has in its use the latest information technology services of

SWIFT. SJIBL is actively involved in Scholarship as well as in

various Socio-Cultural activities.

Banking is not only a profit-oriented commercial institution but

it has a public base and social commitment. Admitting this true

SJIBL is going on with its diversified banking activities.

Inspired by its social obligation and commitment and

responsibility, In CAMEL rating SJIBL’s Position is in “A”

category.

2.4 Location of Mymensingh Branch of ShahjalalIslami Bank Limited Address Noor Fatema Tower (1st Floor), 25 Swadesi Bazar,

Mymensingh-2200.Banking Hours Sunday – Thursday 10 AM. To 4 PM. Telephone No. 091-64397-101Fax 091-62370Email [email protected]

2.5 Vision

To be the unique modern Islami Bank in Bangladesh and to make

significant contribution to the national economy and enhance

customers’ trust & wealth, quality investment, employees’ value

and rapid growth in shareholders’ equity.

2.6 Mission

To provide quality services to customers.

To set high standards of integrity.

To make quality investment.

To ensure sustainable growth in business.

To ensure maximization of Shareholders’ wealth.

To extend our customers’ innovative services acquiring state-of-the-art technology blended with Islamic principles.

To ensure human resource development to meet the challengesof the time.

2.7 Strategies

To strive for customers best satisfaction & earn theirconfidence.

To manage & operate the Bank in the most effective manner.

To identify customers’ needs & monitor their perceptiontowards meeting those requirements.

To review & update policies, procedures & practices toenhance the ability to extend better services to thecustomers.

To train & develop all employees & provide them adequateresources so that the customers’ needs are reasonablyaddressed.

To promote organizational efficiency by communicating companyplans, polices & procedures openly to the employees in atimely fashion.

To ensure a congenial working environment.

To diversify portfolio in both the retail & wholesalemarkets.

2.8 Motto

Committed to Cordial Service.

2.9 Corporate Philosophies

At present the bank has as many as 73 branches in different places

of the country. The sponsors of Shahjalal Islami Bank Limited are

leading business personalities and renowned industrialist of the

country. Now this bank has paid up capital 4453 million and No. of

Directors – 23.

2007 2008 2009 2010 20110

10

20

30

40

50

60

70

80

Branches

Branches

Figure: Last five years branches of SJIBL

2.10 Objectives of Shahjalal Islami Bank LimitedThe objective of Shahjalal Islami Bank Limited is not only to earn

profit but also to keep the social commitment and to ensure its

co-operation to the person of all level, to the businessmen,

industrialist specially who are engaged in establishing large

scale industry by consortium and the agro-based export oriented

medium and small scale industries by self inspiration.

2.11 Corporate Information

Name of theCompany Shahjalal Islami Bank Limited

Legal Form

A public limited company incorporated inBangladesh on 1st April 2001 under the companiesAct 1994 and listed in Dhaka Stock ExchangeLimited and Chittagong Stock Exchange Limited.

Commencementof Business 10th May 2001

Head OfficeUday Sanz, Plot No. SE (A)2/B Gulshan South Avenue,Gulshan – 1, Dhaka-1212.

Telephone No. 88-02-8825457,8828142,8824736,8819385,8818737

Fax No. 88-02-8827607Website www.shahjalalbank.com.bdSWIFT SJBL BD DHE-mail [email protected] Alhaj Anwer Hossain KhanManagingDirector Md. Abdur Rahman Sarker

CompanySecretary Emran Hossain

Auditors

M/S. Hoda Vasi Chowdhury & Co. Chartered Accountants Ispahani Bhaban, 14-15 Motijheel C/ADhaka-1000 Phone: 88-02-9555915, 9560332

Tax Advisor

M/S K.M Hasan & Co. Chartered Accountants 87, New Eskaton Road Dhaka. Phone: 88-02-9351457, 9351564

Legal AdvisorHasan & AssociatesChamber of Commerce Building(6th floor), 65-66 Motijheel C/A, Dhaka

No. ofBranches 73

No. of ATMBooth 15

No. of SMECenters 06

Off-Shorebanking Unit 01

No. ofEmployees 1624

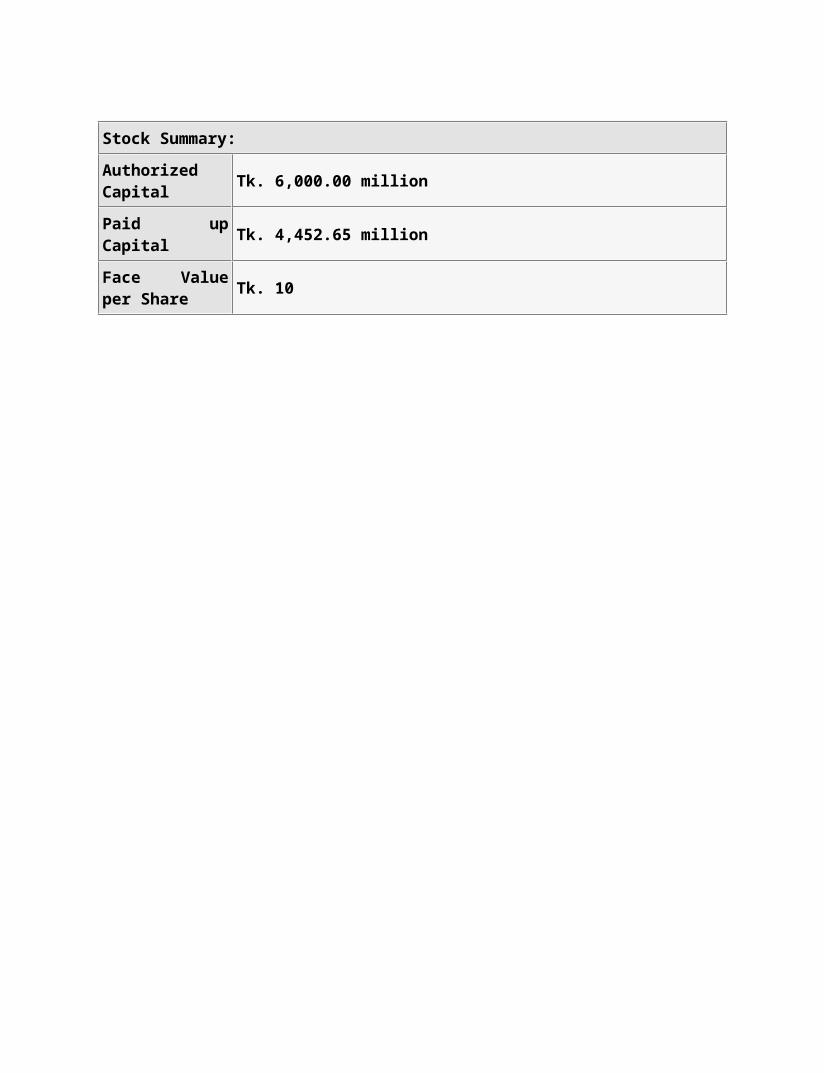

Stock Summary:AuthorizedCapital Tk. 6,000.00 million

Paid upCapital Tk. 4,452.65 million

Face Valueper Share Tk. 10

2.12 Organizational Hierarchy

2.13 Organizational Structure

Chairman Board of Directors

Executive Committee Managing Director

Additional ManagingDirector

Deputy Managing Director Senior Executive Vice

President

Executive Vice President

Senior Vice President Vice President

Senior AssistantVice President

First Assistant VicePresident

Top Management

Executive LevelManagement

Assistant Vice President Senior Principal Officer

Principal Officer

Senior Officer Probationary Officer

Junior Officer Assistant Officer

Fig: Levels of Management

2.14 Departments of Shahjalal Islami Bank Limited

If the Jobs are not organized considering their interrelationship

and are not allocated in a particular department it would be very

difficult to control the system effectively. If the any

departments are not fitted for the particular works there would be

haphazard situation and the performance of a particular department

would not be measured. Shahjalal Islami Bank Limited (SJIBL) has

done this work very well. Different departments of Shahjalal

Islami Bank Limited (SJIBL) are as follows:

Mid Level Management

Junior Level Management

Human Resources Division

Computer and Information Technology Division

Finance & Accounts Division

Financial Institution Division

Audit & Risk Management Division

Board Secretariat & Share Division

General Banking

Accounts opening section

Cash section

Remittance section

Bills and clearing section

Accounts section

Foreign Exchange Division

Import section

Export section

Foreign remittance section

Investment

2.15 Products & service of Shahjalal Islami Bank

Limited

2.15.1 Products of Shahjalal Islami Bank Limited

In shahjalal Islami Bank Limited, product area is broadly

categorized as:

A. Liability Products

B. Asset Products

A. Liability Products:

Demand Deposit

Al-wahida Current Deposit (ACD)

Mudaraba Saving Deposit (MSD)

Mudaraba Short Notice Deposit (MSND)

Time Deposit

Mudaraba Small Business Deposit Scheme

Mudaraba Term Deposit Receipt

MTDR-Special Scheme

Mudaraba Foreign Currency Deposit

Mudaraba Millionaire Scheme

Mudaraba Monthly Income Scheme

Mudaraba Double/Triple Benefit Scheme

Mudaraba Monthly Deposit Scheme

Mudaraba Hajj Scheme

Mudaraba Cash waqf Deposit Scheme

Mudaraba Housing Deposit Scheme

Mudaraba Lakhapoti Deposit Scheme

Mudaraba Mohor Deposit Scheme

Mudaraba Education Deposit Scheme

Mudaraba Marriage Deposit Scheme

B. Asset Products:

SME & Retail:

Prottasha (SME)

Household Durable Scheme

CNG Conversion Investment Scheme

Investment Scheme for Doctors

Investment Scheme for Executives

Investment Scheme for Education

Housing Investment Scheme

Corporate investment:

Trade Investment

WC Investment

Tern Investment

Mode of investment:

HPSM

Bai-Muajjal Commercial TR

Lease/Ijara

Mudaraba LC

MPITR

2.15.2. Services of Shahjalal Islami Bank Limited: Branch Banking

Retail and Institutional Banking

Corporate Banking

Correspond Banking

SJIBL Credit Card

Secured Overdraft

Personal Loan

Car Loan

Private Foreign Currency Accounts

International Trade & Foreign Exchange

Lease Financing

Capital Market Services

SWIFT Service (Society for Worldwide Inter-Bank Financial

Telecommunication)

2.16 Shariah Council

Shariah Council of the Bank is playing a vital role in guiding and

supervising the implementation and compliance of Islamic Shariah

principles in all activities of the Bank since its very inception.

The Council, which enjoys a high status in the structure of the

Bank, consists of prominent ulema, reputed banker, renowned lawyer

and eminent economist.

Members of the Shariah Council meet frequently and deliberate on

different issues confronting the Bank on Shariah matters. They

also conduct Shariah inspection of branches regularly so as to

ensure that the Shariah principles are implemented and complied

with meticulously by the branches of the Bank.

Members of Shariah Council

1. Chairman Moulana Mufti Abdur Rahman

Founder DirectorIslamic Research Centre Bangladesh

2. MemberProf. Dr. Muhammad Mustafizur Rahaman

Former Vice ChancellorIslamic Uiversity, Kustia.

3. Member Prof. Hamidur Rahman

Islamic University of Technology (IIUT)Gazipur

4. MemberShah Abdul HannanFormer Chairman

Islami Bank Bangladesh Ltd.

5. Member Barrister M. Ziaul Hasan

Head of the Chamber Hassan & Associates

6. MemberM. Kamaluddin Chowdhury

CEOShahjalal Islami Bank Securities Ltd.

7. MemberAlhaj Anwer Hossain Khan

Chairman, Board of Directors Shahjalal Islami Bank Ltd.

8. MemberMd. Abdur Rahman Sarker

Managing DirectorShahjalal Islami Bank Limited

2.17 Customer ServiceShahjalal Islami Bank Limited is committed to cordial service to

customers. The continuous improvement in delivery of products and

services, diversification of products, reduction of turnaround

time for investment processing, on line deposits, Debit card, SMS

Push-Pull, Mobile banking and arrangement with Western Union for

early remittance payment have been the key indicators of

customers’ satisfaction. The authority of bank firmly believes

profitability, growth and market share of business depended on

quality of customer service. They provide a full range of

financial services to individuals, small and medium sized

companies, entrepreneurs and corporate bodies.

2.18 Branch NetworkWith the opening of 10 (ten) new branches during the year 2011,

the Bank provided its satisfactory service to its customer with a

network of total 73 (seventy three) branches all over the country.

The bank is working to expand its business by opening more 10

(ten) branches, 5 (five) SME Centers and 5 branches of Brokerage

House in Dhaka and some other important business location of the

country in the year 2012.

2.19 Human Resource DevelopmentPeople working in the Bank are real assets. The bank wants to

attract trained and retain talented people in the service of the

Bank. The dedication, skills and professionalism of the employees

are factors that contributed to success of the Bank. In

recognition to their contribution, the Board has formulated a

number of policies for their welfare. The board has introduced

superannuation fund, gratuity, social security, house building

finance, car investment facility and other benefits for

executives/officers/staff of the bank.

2.20 Corporate Social ResponsibilityAs an Islamic bank, the bank is committed to serve the causes of

humanities. In this course, they expanded their helping hand to

the natural destruction affected people of various regions of the

country. They awarded scholarship to the poor and meritorious

students for their brilliant result in the level of S.S.C & H.S.C

to forward their future education smoothly. There is a plan to

establish a hospital and an educational institution where the

common people as well as the employees of the Bank can avail the

high standard of physical aid and education at a minimal cost.

The social spectrum under which the bank operates desires that

they can carry on their business responsibly and contribute

positively to the society and the environment. They are committed

to responsible business practice and to a policy of continuous

improvement in applying sound environment and social standards in

their dealings with all their stakeholders.

2.21 Future lookThe bank expects higher growth of business in 2012. The growth

will predictably generate from the diversified Corporate Sector,

Retail Banking, Treasury Operations, Syndication and Structured

Financing and Export Oriented initiatives. They have introduced

Mudaraba Principle based Monthly Deposit Scheme (MDS), Double

Benefit Scheme, Triple Benefit Scheme, Monthly Income Scheme,

Millionaire Scheme, Small business Deposit Scheme, Marriage

Deposit Scheme, Mohar Deposit Scheme, Education Deposit Scheme,

Special deposit Scheme, Hajj Deposit Scheme, Housing Deposit

Scheme, Cash Waqf Scheme, SMS/Push Pull Service, Visa Debit Card,

money transfer, capital market services, Off-Shore Banking, to

serve the customers to their highest satisfaction. They hope that

they will be able to upgrade, co-ordinate and integrate the above-

mentioned products and initiatives to register excellent growth of

business in 2012. They will seek additional financial assistance,

human and material resources to manage their institution to add

more value for shareholders, customers, employees and the

community as well.

Chapter: ThreePerformance Analysis

3.1 SJIBL Performances at a Glance:SJIBL was incorporated as a public limited company on the 1st April

2001 under Company Act 1994. The Bank started commercial banking

operations effective from 10th May 2001. During this short span of

time the Bank has been successful to position itself as a

progressive and dynamic financial institution in the country. The

Bank widely acclaimed by the business community,

from small business/entrepreneurs to large traders and

industrial conglomerates, including the top rated corporate

borrowers from forward-looking business outlook and innovative

financing solutions.

SHAHJALAL ISLAMI BANK LIMITEDFinancial Summary of last five years

( TK. In Million)Particulars 2011 2010 2009 2008 2007Total Investment 80,592 61,440 43,958 32,919

20,617(Loans & Advances)Total Deposits 83,350 62,965 47,459 34,28022,618Investment 5,292 2,229 3,483 1,144 859(Share & Securities)

Operating Profit 2,998 3,529 2,041 1,810 1,315Total Expenditure 9,009 5,980 5,076 3,475 2,274Profit after Tax 1,168 2,072 1,071818 647Dividend:

Cash (%) - - - - -Bonus (%) *25 30 25

22 20Total Shareholders’ 7,917 6,748 4,676 3,605 2,788 Equity

Source: Annual report 2011

SHAHJALAL ISLAMI BANK LIMITEDFive years Projected Major Financial Growth

Particulars 2007 (%) 2008 (%) 2009 (%) 2010 (%) 2011 (%)Investment(General)

32.88% 59.67% 33.53% 39.77% 31.17%

Deposits 25.02% 51.56% 38.45% 32.67% 32.38%Investment(Shares& - 33.18% 204.46% (36)% 137.42%

Bond)Operating Profit

55.62% 37.64% 12.76% 72.91%(15.05)%

Expenditure 32.36% 52.81% 46.07% 17.81% 50.65%

Net Profit afterTax

39.74% 26.43% 30.93% 93.46%(43.63)%

Dividend: Cash - - - - - Bonus

- 10% 13.64% 20%(16.67)%

Shareholder’sEquity

131.37% 29.30% 29.71% 44.31% 17.32%

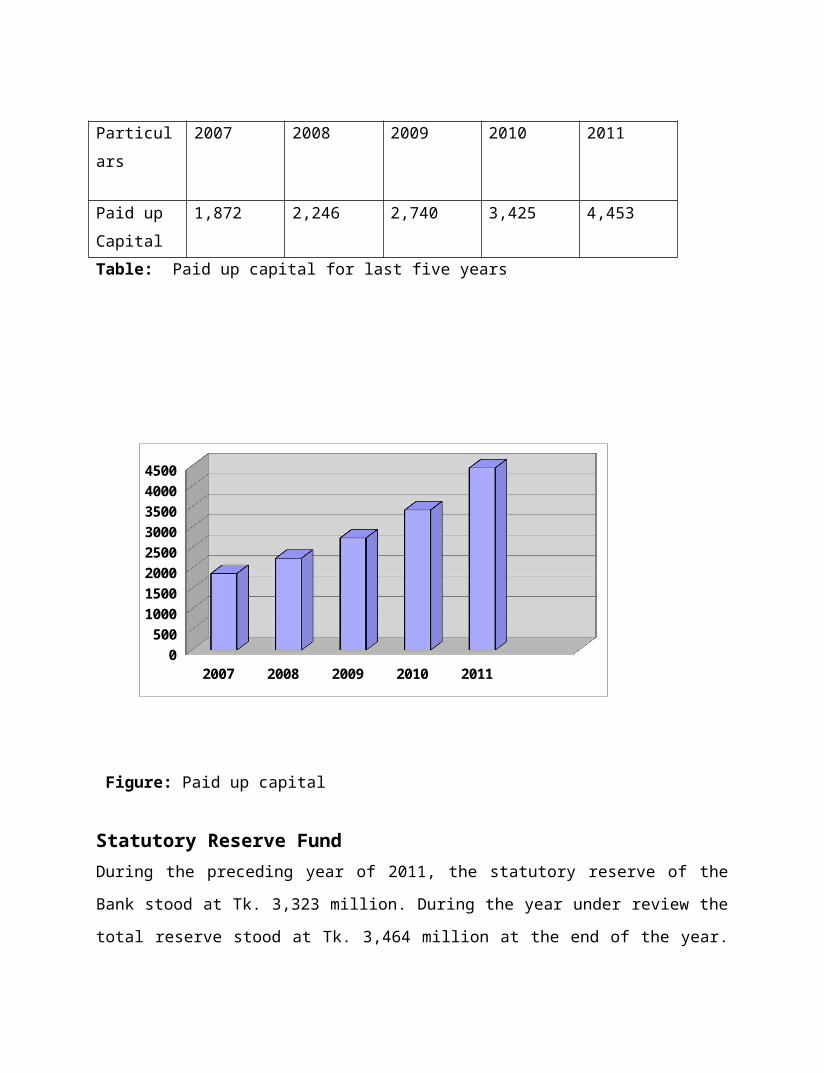

3.2 Share Capital:The authorized capital of the Bank is Tk. 6000 million dividedinto 600 million ordinary shares of Taka 10.00 each. The paid upcapital of the Bank is Tk. 4453 million divided into 445.3 millionordinary shares of Tk. 10.00 each.

The authorized capital of the Bank is Tk.6000 million. The paid up

capital of the Bank is

increased by Tk. 1028 million to Tk.4453 million while the Reserve

Fund increased by Tk. 141 million to Tk. 3464 million during the

year 2011.

(Taka in Millions)

Particulars

2007 2008 2009 2010 2011

Paid up Capital

1,872 2,246 2,740 3,425 4,453

Table: Paid up capital for last five years

Figure: Paid up capital

Statutory Reserve FundDuring the preceding year of 2011, the statutory reserve of the

Bank stood at Tk. 3,323 million. During the year under review the

total reserve stood at Tk. 3,464 million at the end of the year.

2007 2008 2009 2010 20110

50010001500200025003000350040004500

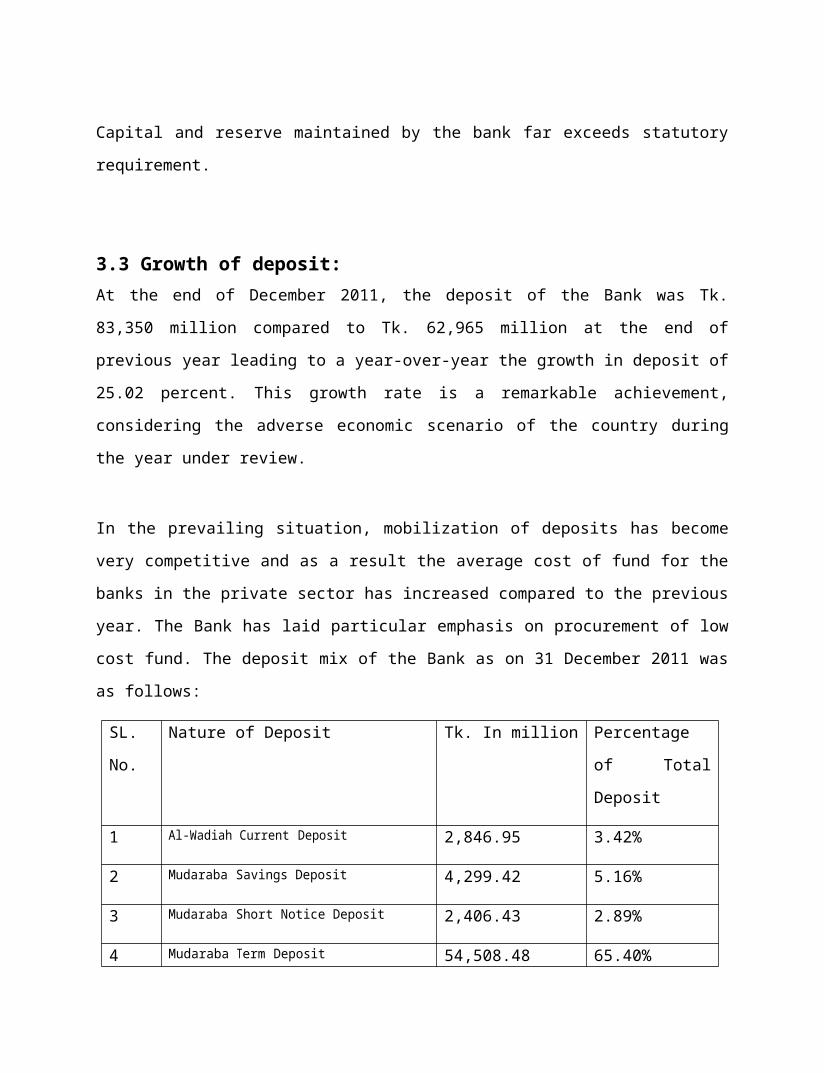

Capital and reserve maintained by the bank far exceeds statutory

requirement.

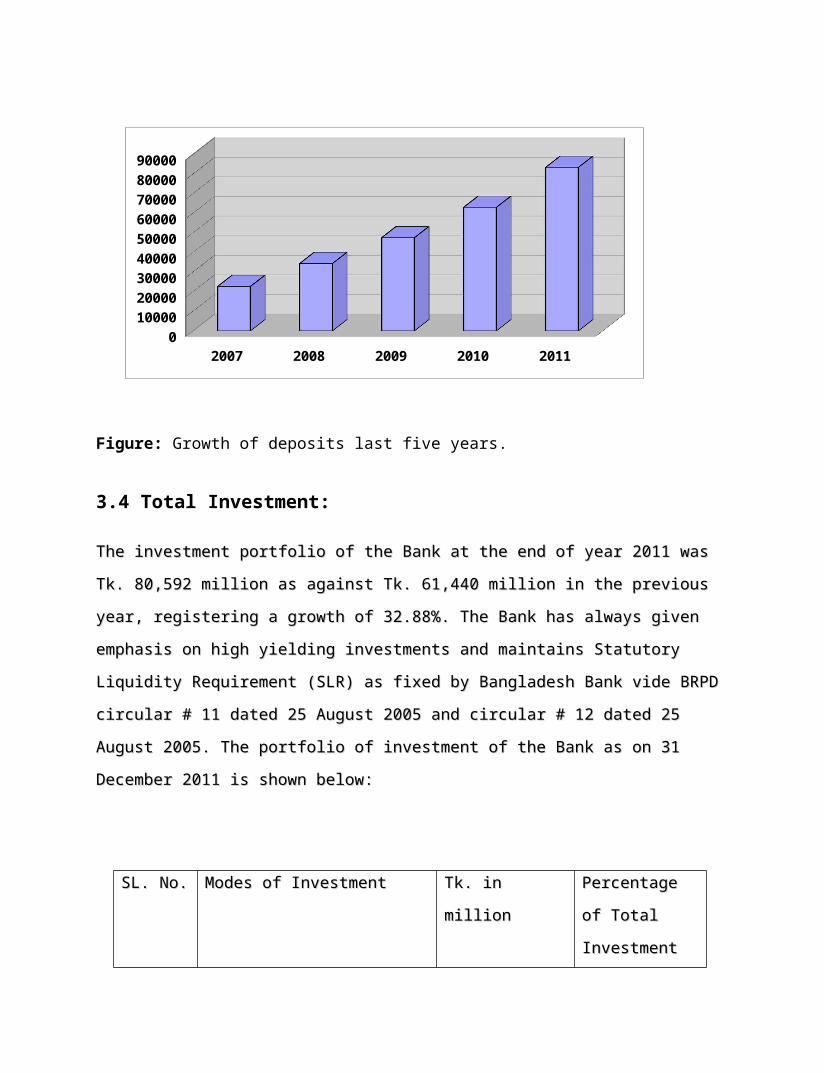

3.3 Growth of deposit:At the end of December 2011, the deposit of the Bank was Tk.

83,350 million compared to Tk. 62,965 million at the end of

previous year leading to a year-over-year the growth in deposit of

25.02 percent. This growth rate is a remarkable achievement,

considering the adverse economic scenario of the country during

the year under review.

In the prevailing situation, mobilization of deposits has become

very competitive and as a result the average cost of fund for the

banks in the private sector has increased compared to the previous

year. The Bank has laid particular emphasis on procurement of low

cost fund. The deposit mix of the Bank as on 31 December 2011 was

as follows:

SL.

No.

Nature of Deposit Tk. In million Percentage

of Total

Deposit

1 Al-Wadiah Current Deposit 2,846.95 3.42%

2 Mudaraba Savings Deposit 4,299.42 5.16%

3 Mudaraba Short Notice Deposit 2,406.43 2.89%

4 Mudaraba Term Deposit 54,508.48 65.40%

5 Mudaraba Schemes Deposit 14,101.42 16.92%

6 Other Deposits 5,187.35 6.22%

Total 83,350.05 100%

The deposits products have been diversified to suit wide range of customers. The present strategy is to increase deposit base through maintaining competitive interest rates and having low costof funds that would ensure a better spread with the lending rate.

(Taka in Millions)Particulars

2007 2008 2009 2010 2011

Total Deposits

22,618 34,280 47,459 62,965 83,350

Growth 25.02% 51.56% 38.45% 32.67% 32.38%

Table: Growth of deposit in last five years.

Figure: Growth of deposits last five years.

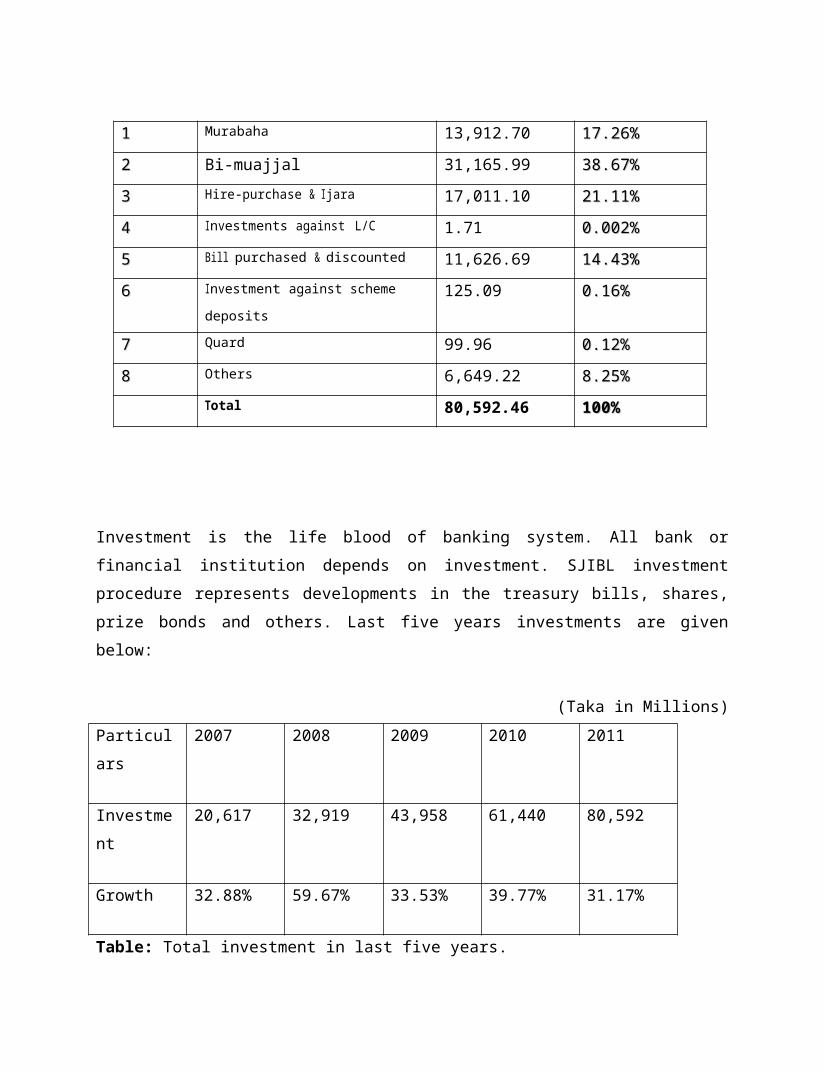

3.4 Total Investment:

The investment portfolio of the Bank at the end of year 2011 was The investment portfolio of the Bank at the end of year 2011 was

Tk. 80,592 million as against Tk. 61,440 million in the previous Tk. 80,592 million as against Tk. 61,440 million in the previous

year, registering a growth of 32.88%. The Bank has always given year, registering a growth of 32.88%. The Bank has always given

emphasis on high yielding investments and maintains Statutory emphasis on high yielding investments and maintains Statutory

Liquidity Requirement (SLR) as fixed by Bangladesh Bank vide BRPD Liquidity Requirement (SLR) as fixed by Bangladesh Bank vide BRPD

circular # 11 dated 25 August 2005 and circular # 12 dated 25 circular # 11 dated 25 August 2005 and circular # 12 dated 25

August 2005. The portfolio of investment of the Bank as on 31 August 2005. The portfolio of investment of the Bank as on 31

December 2011 is shown below:December 2011 is shown below:

SL. No.SL. No. Modes of InvestmentModes of Investment Tk. in Tk. in

millionmillionPercentage Percentage

of Total of Total

InvestmentInvestment

2007 2008 2009 2010 20110

100002000030000400005000060000700008000090000

11 Murabaha 13,912.70 17.26%17.26%

22 Bi-muajjal 31,165.99 38.67%38.67%

33 Hire-purchase & Ijara 17,011.10 21.11%21.11%

44 Investments against L/C 1.71 0.002%0.002%

55 Bill purchased & discounted 11,626.69 14.43%14.43%

66 Investment against scheme

deposits125.09 0.16%0.16%

77 Quard 99.96 0.12%0.12%

88 Others 6,649.22 8.25%8.25%Total 80,592.46 100%100%

Investment is the life blood of banking system. All bank orfinancial institution depends on investment. SJIBL investmentprocedure represents developments in the treasury bills, shares,prize bonds and others. Last five years investments are givenbelow:

(Taka in Millions)Particulars

2007 2008 2009 2010 2011

Investment

20,617 32,919 43,958 61,440 80,592

Growth 32.88% 59.67% 33.53% 39.77% 31.17%

Table: Total investment in last five years.

Figure: Total investment in last five years.

International Trade:The international trade financing constitutes a major business

activity conducted by the Bank. The Bank’s foreign trade related

activities, carried out through 40 AD branches across the country,

have earned confidence of importers, exporters and Bangladeshi

work force working abroad. For smooth conduct of international

trade, The Bank has as many as 383 foreign correspondents

throughout the world. In addition, the Bank is maintaining 39

NOSTRO Accounts with the world’s leading banks.

Import-Export Business

The import business of the Bank during the year 2011 was Tk.

82,341 million. The export business handled by the Bank during the

year 2011 stood at Tk. 79,225 million. The slow growth rate in

2007 2008 2009 2010 20110

20000

40000

60000

80000

100000

export business is attributable to the volatile situation in the

world economy.

Foreign Remittance Business

Since beginning, the bank has been highly active in remittance Since beginning, the bank has been highly active in remittance

operations to facilitate disbursement of remittance received from operations to facilitate disbursement of remittance received from

Bangladeshi wage earners working abroad. Inward Foreign RemittanceBangladeshi wage earners working abroad. Inward Foreign Remittance

also played a significant role in decreasing the bank’s dependencyalso played a significant role in decreasing the bank’s dependency

on inter-bank market for payment of import bills in foreign on inter-bank market for payment of import bills in foreign

currency.currency.

The remittances of the Bank resulted in steady increase of The remittances of the Bank resulted in steady increase of

revenues for the Bank in spite of the downward trend in revenues for the Bank in spite of the downward trend in

international trade. international trade.

In the year 2011 the total remittance stood at Tk.5, 340 million In the year 2011 the total remittance stood at Tk.5, 340 million

as against Tk.6,156 million in the year 2010. The Bank continues as against Tk.6,156 million in the year 2010. The Bank continues

Taka Draft/ Electronics Fund Transfer arrangements with a number Taka Draft/ Electronics Fund Transfer arrangements with a number

of overseas exchange companies/banks. The Bank has strengthened of overseas exchange companies/banks. The Bank has strengthened

its overseas network by operating through a total its overseas network by operating through a total of 35 exchangeof 35 exchange

companies/banks, covering Middle East, the Gulf States, South-Eastcompanies/banks, covering Middle East, the Gulf States, South-East

Asia and Italy.Asia and Italy.

The Bank has started instant payment remittance with the

assistance of Money Gram, Transfast, and Remit One and IME. The

inflow of the remittance through the bank will increase remarkably

in the coming days.

0

5,000

10,000

15,000

20,000

25,000

Tk. in crore

2009

2008

2007

2006

2005

FOREIGN EXCHANGE BUSINESS

i. Imports:

ii. Exports:

iii. Remittances:

3.5 Total growth of Export:The export businesses handle by the SJIBL during 2003. At presentsituation SJIBL maintain different type of export business. Herefive years total growth of export business described.

(Taka in Millions)Particulars

2007 2008 2009 2010 2011

Export Business

15,084 26,347 29,434 48,857 79,225

Table: Total growth of Export business in last five years.

Figure: Total growth of Export business in last five years.

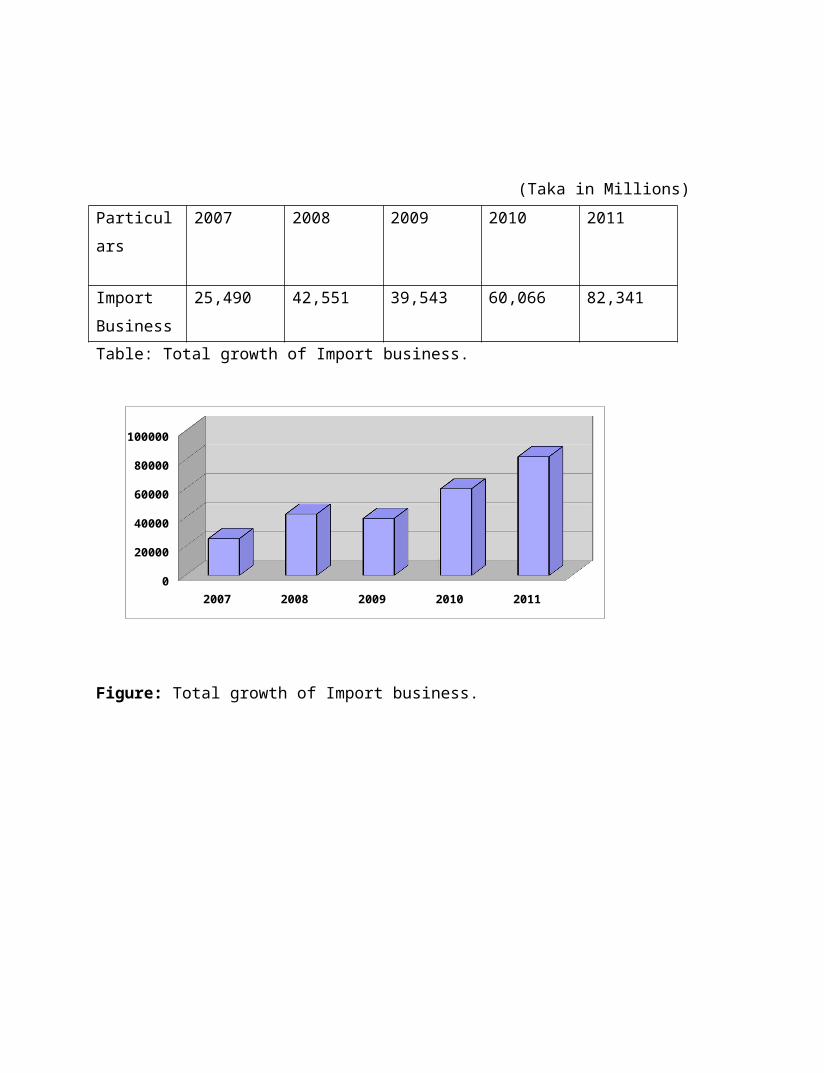

3.6 Total Import Business:Import means lawfully carrying out of anything from one country tocountry for buying. It will be occurred according to theGovernment law. The total import business handled by SJIBL during2011 Tk. 82,341 million.

2007 2008 2009 2010 20110

1000020000300004000050000600007000080000

(Taka in Millions)Particulars

2007 2008 2009 2010 2011

Import Business

25,490 42,551 39,543 60,066 82,341

Table: Total growth of Import business.

Figure: Total growth of Import business.

2007 2008 2009 2010 20110

20000

40000

60000

80000

100000

3.7 Financial Statements:Shahjalal Islami Bank

LimitedBalance Sheet

As at 31st December, 2011

2011 2010No t e Ta k a Ta k a

PROPERTY AND ASSETS cash in hand (including Foreign currencies) 3 828,581,466

757,585,771Balance with Bangladesh Bank & Sonali Bank ltd(Including Foreign currencies) 4 8,670,266,207 6,442,098,480

9,498,847,673 7,199,684,251 Balance with other Banks and Financial Institutions

Inside Bangladesh 771,921,272684,337,121

Outside Bangladesh 667,820,627473,022,125

5 1,439,741,8991,157,359,246

Placement with other Banks & Financial Institutions 6 6,835,381,6354,336,581,235

Investments in Shares & SecuritiesGovernment 2,000,000, 1,400,000,Others 3,291,918,

927828,851,5997 5,291,918,

9272,228,851,599Investments

General investment etc. 68,795,477,946

54,295,073,642Bills Purchased and Discounted 11,796,983,

7377,145,002,2638 80,592,461,

68361,440,075,905

Fixed Assets Including Premises 9 1,525,267, 1,472,502,Other AssetsNon Banking Assets

Total AssetsLIABILITIES AND

CAPITAL Liabilities

10

11

2,045,242,088

- 107,228,861

,656

965,347,663

- 78,800,401,

984Deposits and Other Accounts

mudaraba Savings Deposits 4,299,417,084

3,861,423,717mudaraba term Deposits 54,508,485,

45638,104,072,325Other mudaraba Deposits 16,507,850,

21814,806,640,228al-Wadeeah current & Other Deposit

accounts7,464,055,139

5,665,293,559

Bills Payable 570,242,984

527,518,23612 83,350,050,

88162,964,948,065

Other Liabilities 13 5,084,677, 3,278,501,Deferred Tax Liabilities 14 107,340,6

6676,413,085Total Liabilities

Capital/Shareholders’ EquityPaid-up capital 15

99,312,068,926

4,452,655,

72,052,052,654

3,425,119,Statutory Reserve 16 2,252,105,068

1,774,626,888Retained earnings 17 1,212,032,

3121,548,602,942Total Shareholders’ Equity

7,916,792,73 Total Liabilities & Shareholders’ Equity 107,228,861

,65678,800,401,984

S h a h j a l a l I s l a m i B a n kL i m i t e d

P r o f i t a n d L o s s A c c o u n tF o r t h e y e a r e n d e d , 2 0 1 1

No t e

2011Ta k a

2010Ta k a

investment income 21 10,107,768, 6,416,784,less: Profit paid on Deposits 22 7,376,422, 4,657,924,Net Investment Income 2,731,346,

0141,758,860,227income from investment in Shares/securities 23 112,733,5

461,104,473,288commission, exchange and Brokerage 24 1,473,366, 1,721,532,

Other Operating income 25 312,948,7 266,097,1,899,049, 3,092,103,

Total Operating Income 4,630,395, 4,850,963,Salaries and allowances 26 943,767,8 701,531,Rent, taxes, insurances, electricity etc. 27 212,171,1 174,301,legal expenses 28 882,0 1,071,7Postage, Stamps, telecommunication etc. 29 27,567,1 16,487,Stationery, Printings, advertisements etc. 30 40,291,6 53,811,chief executive’s Salary & Fees 31 12,600,0 6,428,3Directors’ Fees & expenses 32 4,096,1 6,468,9Shariah Supervisory committee’s Fees & 33 196,3 134,6auditors’ Fees 300,0 250,0Depreciation & Repairs of Bank’s assets 35 114,033,3 76,787,Zakat expenses 36 59,228,9 32,277,Other expenses 37 217,369,7 252,702,Total Operating Expenses 1,632,504,

3381,322,254,120Profit before Provision 20 2,997,890,

8993,528,709,244Specific provision for classified investment (130,000,0

00)(150,000,000)General Provision for Unclassified investment (180,000,0 (240,000,0

General Provision for Off-Balance Sheet items (63,000,0 (130,000,0Provision for deminution in value of (237,500,0 (47,500,0Provision for Other assets - (1,000,Total Provision 38 (610,500, (568,500,0Profit before Provisions for Taxation 2,387,390,

8992,960,209,244Deferred tax expenses 39 30,927,5

8136,978,993current tax expenses 13.

21,188,019,918

850,889,8881,218,947,

499887,868,881Net Profit after Taxation 1,168,443,

4002,072,340,363

Shahjalal Islami Bank Limited

Cash Flow StatementFor the year ended 31 December, 2011

No t e 2011Ta k a

2010Ta k a

Cash Flow from Operating ActivitiesInvestent income receipt in cash 41 10,011,527,

6907,539,360,233Profit Paid on Deposits 42 (6,615,795,

601)(4,249,153,395)Dividend Receipts 63,168,

86010,345,139Fees & commission receipt in cash 1,473,366,

9561,721,532,422cash Payments to employees (956,367,8

23)(707,960,285)cash Payments to Suppliers (40,291,6

88)(53,811,688)income tax Paid (735,394,1

37)(664,659,041)Receipts from other Operating activities 43 312,948,

721266,097,427Payments for other Operating activities 44 (535,335,3

98)(493,678,098)Operating Profit before changes in Operating

Assets2,977,827,580

3,368,072,714Changes in Operating Assets and Liabilities

investment to customers (19,152,385,778)

(17,481,815,194)Other assets 45 (934,088,8

41)(635,051,433)Deposits from other Banks 236,741,

927(174,115,363)Deposits received from customers 20,148,360,

88915,679,831,935Other liabilities on account of customers 19,969,

41528,546,959Other liabilities 46 (37,546,2

94)90,855,887Sub Total 281,051,3

18(2,491,747,209)ANet Cash from Operating Activities 3,258,878,

898876,325,505Cash flows from Investing Activities

Proceeds from sale of Securities 100,676, 1,987,184Payment for purchases of securities (3,163,744,

115)(983,513,581)Proceeds from Sale of fixed assets 32,044,

730-

Purchases of Property, Plant & equipments (185,319,825)

(918,839,673)Purchase/Sale of subsidiaries - -

B)Net Cash from Investing Activities (3,216,342,

423)84,831,109Cash flows from Financing Activities

Receipts from issue of Debt instruments 2,539,009,600

1,183,389,806Payments for redemption of Debt

instruments- -

Receipts from issue of ordinary shares - -Dividend Paid in cash - -

C)Net Cash from Financing Activities 2,539,009,

6001,183,389,806D

)Net Increase/(Decrease) in Cash & Cash Equivalents (A+B+C)

2,581,546,075

2,144,546,420e

)cash and cash equivalents at the beginning of the year

F

)Cash and cash equivalents at the end of theyear (D+E)

47 10,938,589,572

8,357,043,497

Shahjalal Islami Bank LimitedStatement of Changes in EquityFor the year ended 31 December, 2011

Particulars Paid-up Statutory retained TotalCapital reserve Earnings

Taka Taka Taka Taka

Balance as at 01 January 2011 3,425,119,5001,774,626,888 1,548,602,942

6,748,349,330 Changes in accounting policy - - -- Restated Balance 3,425,119,500 1,774,626,8881,548,602,942 6,748,349,330Bonus shares issued for the year 2010 1,027,535,850 -(1,027,535,850) - Net profit for the year 2011 - 477,478,180

690,965,220 1,168,443,400Total Shareholders’ Equity as at 31 December 2011 4,452,655,350

2,252,105,0681,212,032,3127,916,792,730

Total Equity for thepurpose of CapitalAdequacy

Equity as per above 7,916,792,730add: General Provision for Unclassified investment 925,479,

add: General Provision for Off-Balance Sheet items 341,000,000Total Equity as at 31 December 2011 9,183,271,

730

3.8 Evaluation of Bank’s performance Despite changing macro-economic condition and volatile money

market & foreign exchange market, Shahjalal Islami Bank Limited

Limited was successful in achieving much higher than national

growth in deposit, Investment (loans), export, import &

remittance business. As on 31st December 2011 total deposit of

the Bank stood at Tk. 83,350 million showing a growth rate of

32.38%, total amount of Investment of the Bank stood at Tk.

80,592 million with a growth rate of 31.17%. During the year

import volume stood at Tk. 82,341 million with a growth of 37.08%

compared to that of the previous year. The growth of the export

business has been increased by 30,368 million and it stood at Tk.

79,225 million as of December 31, 2011 against 48,857 million of

the previous year which indicate 62.16% growth over previous

year. Foreign Remittance of the Bank stood at Tk. 5,340 million

as of December 31, 2011 as against Tk. 6,156 million of 2010 with

a negative growth of 13.26% over previous year. The ratio of

classified investment is within the acceptable range of 1.89%.

The fact that non-performing investment ratio remained below 2%

indicated that the strategy of quality growth by adhering to

compliance in all spheres of operations is working well.

Management of the bank is frequently reviewed by the Board and

also appropriate decisions are being adopted time to time to

strengthen the banking performance.

3.9 Comments on Financial Statements:Investments:Investments occupy major portion of the Bank’s assets. The Bankgives emphasis to acquire quality assets and does appropriateinvestment risk analysis while approving investment facilities tothe clients. Investment has been considered on the basis ofpreceding year’s growth and to achieve targeted profit.

Deposits:Deposit growth is expected to be at the higher rate of targetedgrowth of investment to have more investment facilities.

Profit:Over all business of the bank has increased significantly sincethe last five years. As such it is assumed that in the next fiveyears, business will increase accordingly and profit willincrease in the same line.

Operating Income:Operating income has been calculated on the basis of fund basedincome and expenses. Other income of non funded businessincluding exchange gain has also been considered.

Operating expenses:We have considered expenses at a rate based on the growth ofoperational activities of the bank for the next five years underconsideration.

Net profit After Tax:Net profit after tax is a calculated position after making allprovisions required by different regulatory authorities as perour assumed investment size, number of employees and theirprobable consequences.

Chapter: FourForeign exchange

4.1 Definition of Foreign Exchange

Foreign Exchange means exchange of foreign currency between two

countries. If we consider ‘Foreign Exchange’ as a subject, then

it means all kinds of transaction related to foreign currency. In

other words, foreign exchange deals with foreign financial

transactions.

4.2 Necessity of foreign exchange

No country is self-sufficient in this world. Everyone is, more or

less, dependent on another, for goods or services. Say,

Bangladesh has cheap manpower whereas Saudi Arabia has cheap

petroleum. So Bangladesh is dependent on Saudi Arabia for

petroleum and Saudi Arabia is dependent on Bangladesh for cheap

manpower. People of one country are going to abroad for

Education, Medical service etc. Thus there is exchange of foreign

currency.

4.3 Regulations for foreign exchange

4.3.1 Local Regulations:

Our foreign exchange transactions are being controlled by the

following rules & regulation.

Foreign Exchange Regulation Act 1947.

Bangladesh Bank issues foreign exchange circular from time

to time to control the export, import & remittance business.

Ministries of commerce issues export & import policy giving

basic formalities for import & export business.

Sometime CCI&E issues public notice for any kind of change

in foreign exchange transaction.

Bangladesh bank published two volumes in 1996. This is

compilation of the instructions to be followed by the

authorized dealers in transitions relation to foreign

exchange.

4.3.2 International regulations of foreign exchange:

There are also some international organizations, influencing our

foreign exchange transactions. Few of them are discussed bellow:

International Chamber of Commerce (ICC) is a world wide

non-governmental organization of thousands of companies. It

was founded in 1919. ICC has issued some publications like

UCPDC, URC, & URR etc, which are being followed by all the

member countries. There is also an international court of

arbitration to solve the international business disputes.

World Trade Organization (W.T.O) is another international

trade organization established in 1995. General Agreement

on Tariff & Trade (GATT) was established in 1948, after

completion of it’s 8th round; the organization has been

abolished & replaced by W.T.O. This organization has vital

role in international trade, through its 124 member

countries.

4.4 Foreign Exchange MechanismForeign exchange department plays significant roles through

providing different services for the customer. Facilitating the

trade with foreign country is the most important among those

services the key instrument which facilitates this trade is L/C

(Letter of Credit).

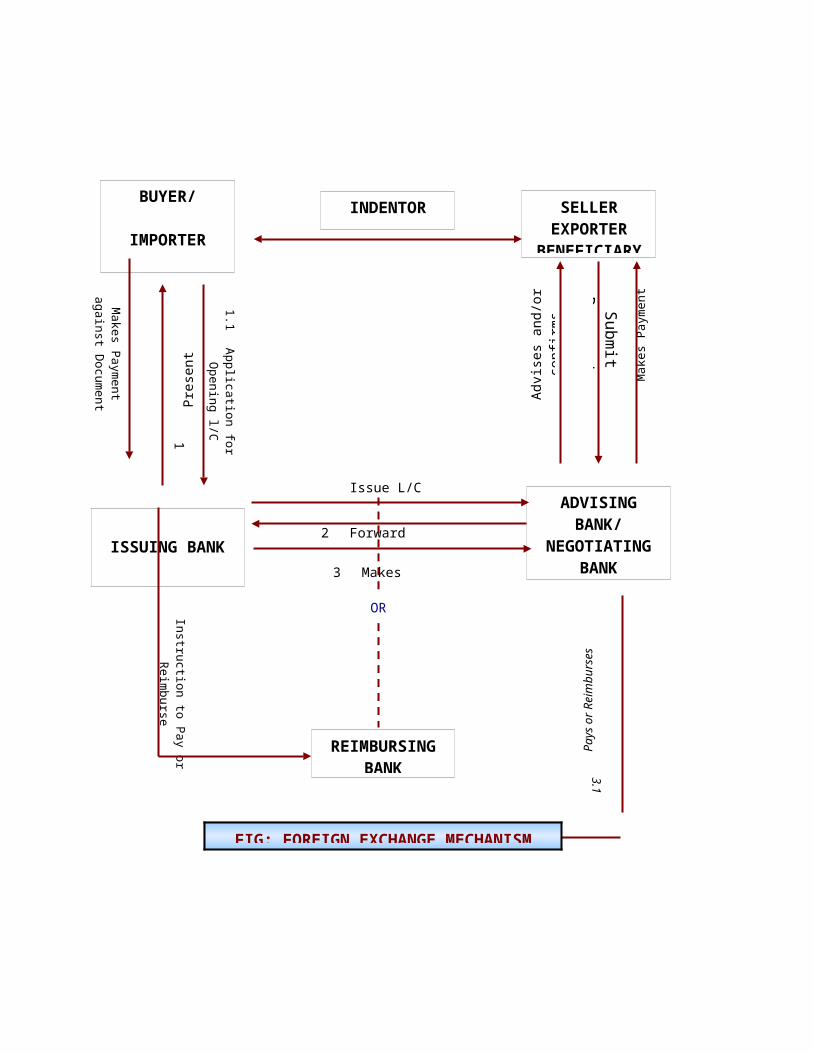

Letter of Credit: Letter of Credit may be defined as an arrangement or guarantee

issued by a bank at the request of the customer to make payment

to or order of the beneficiary or authorized another bank to

effect such payment or to pay, accept or negotiate such bill of

exchange against stipulated documents, provided that the terms

and conditions of the L/C are complied with. (UCPDC-500, 1993)

The Advising Bank:It is the bank in the Exporter’s (Normally the exporter’s bank),

which is usually the foreign correspondent of Importer’s bank

through which the L/C is advised to the supplier. If the

intermediary bank simply advises/notifies the L/C to the exporter

without any obligation on its part, it is called “Advising Bank”.

The Confirming Bank:If the Advising Bank also adds its own undertaking to honor the

credit while advising the same to the beneficiary, he becomes the

Confirming Bank, in addition, becomes liable to pay for documents

in conformity with the L/C’s terms and conditions.

The Negotiating Bank:

The Bank that negotiates the bill of exporter drawn under the

credit is known as Negotiating Bank. If the advising bank is also

authorized to negotiate the bill drawn by the exporter, he

becomes the Negotiating Bank.

The Accepting Bank:A Bank that accepts time or unasked drafts on behalf of the

importer is called an Accepting Bank. The Issuing Bank can also

be the Accepting Bank.

The Paying Bank and the Reimbursing Bank:If the Issuing Bank does not maintain any account with a bank

that will be negotiating the documents under a L/C, then

arrangement is made to reimburse the negotiating bank for the

amount to be paid under from some other bank with which the

Issuing Bank maintains his account.

4.4 Graphical Representation of Foreign ExchangeMechanism:

SubmitDocuments Ma

kes

Payment

1.1Application for

Opening l/C1.1.1.1.1.1.1.1.1

Present

Do

Makes Paymentagainst Document

Issue L/C

2 Forward Document

3 Makes Payment

Instruction to Pay orReimburse

3.1

Pa

ys o

r Rei

mbu

rses

BUYER/

IMPORTER

INDENTOR SELLEREXPORTER

BENEFICIARY

ISSUING BANK

ADVISINGBANK/

NEGOTIATINGBANK

Advi

ses and/or

confirms

OR

REIMBURSINGBANK

FIG: FOREIGN EXCHANGE MECHANISM

4.5 Activities of foreign exchange

There are three kinds of foreign exchange transaction:

1. Import.

2. Export.

3. Foreign Remittance.

Chapter five:Overview of Import

5.1 Understanding: Imports are foreign goods and services purchased by consumers,

firms, & Governments in Bangladesh. The importers are asked by

their exporters to open letter of credits so that their payment

against goods is ensured.

5.2 Classification of importersGoods are being imported for personal use, commercial purpose or

industrial use. So, there are three kinds of importers such as:

1. Personal importer: if the importer is insisting to import

goods from the abroad for his need this importer called

personal importer.

2. Commercial importer: if the importer is insisting to import

goods for commercial purpose then it is called commercial

importer.

3. Industrial importer: if the importer is insisting to import

goods for industrial purpose then it is called Industrial

importer.

5.3 Import Policy:Under the import and export control Act, 1950 the Government of

Bangladesh formulates the Import policy through Ministry of

Commerce.

The existing Import policy (1997-02) has come into effect from

June 14, 1998 to June 30, 2002. (It can be reviewed every year if

needed)

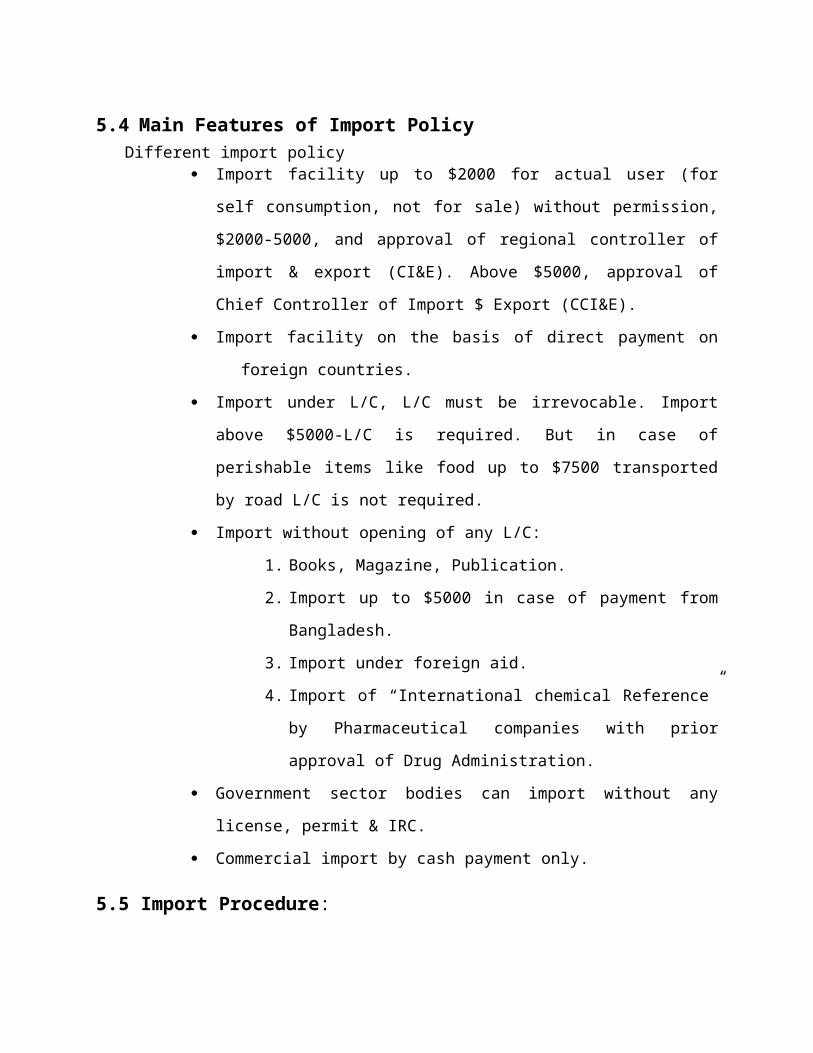

5.4 Main Features of Import PolicyDifferent import policy

Import facility up to $2000 for actual user (for

self consumption, not for sale) without permission,

$2000-5000, and approval of regional controller of

import & export (CI&E). Above $5000, approval of

Chief Controller of Import $ Export (CCI&E).

Import facility on the basis of direct payment on

foreign countries.

Import under L/C, L/C must be irrevocable. Import

above $5000-L/C is required. But in case of

perishable items like food up to $7500 transported

by road L/C is not required.

Import without opening of any L/C:

1. Books, Magazine, Publication.

2. Import up to $5000 in case of payment from

Bangladesh.

3. Import under foreign aid.

4. Import of “International chemical Reference”

by Pharmaceutical companies with prior

approval of Drug Administration.

Government sector bodies can import without any

license, permit & IRC.

Commercial import by cash payment only.

5.5 Import Procedure:

To import through SJIBL, a customer requires-

(i) Bank account(ii) Import Registration Certificate (IRC)(iii) Tax Paying Identification Number(iv) Proforma-Invoice Indent(v) Membership Certificate(vi) LCA (Letter of Credit Authorization) form duly attested(vii) One set of IMP Form(viii) Insurance Cover note with money receipt

5.6 Import Mechanism:To import, a person should be competent to be ‘Importer’.

According to Import and Export Control Act, 1950, the Office Of

Chief Controller Of Import and Export provides the registration

(IRC) to the importer. After obtaining this person's has to

secure a letter of credit authorization (LCA) from Bangladesh

Bank. And then a person becomes a qualified importer. He is the

person who requests or instructs the opening bank to open an L/C.

He is also called opener or applicant of the credit.

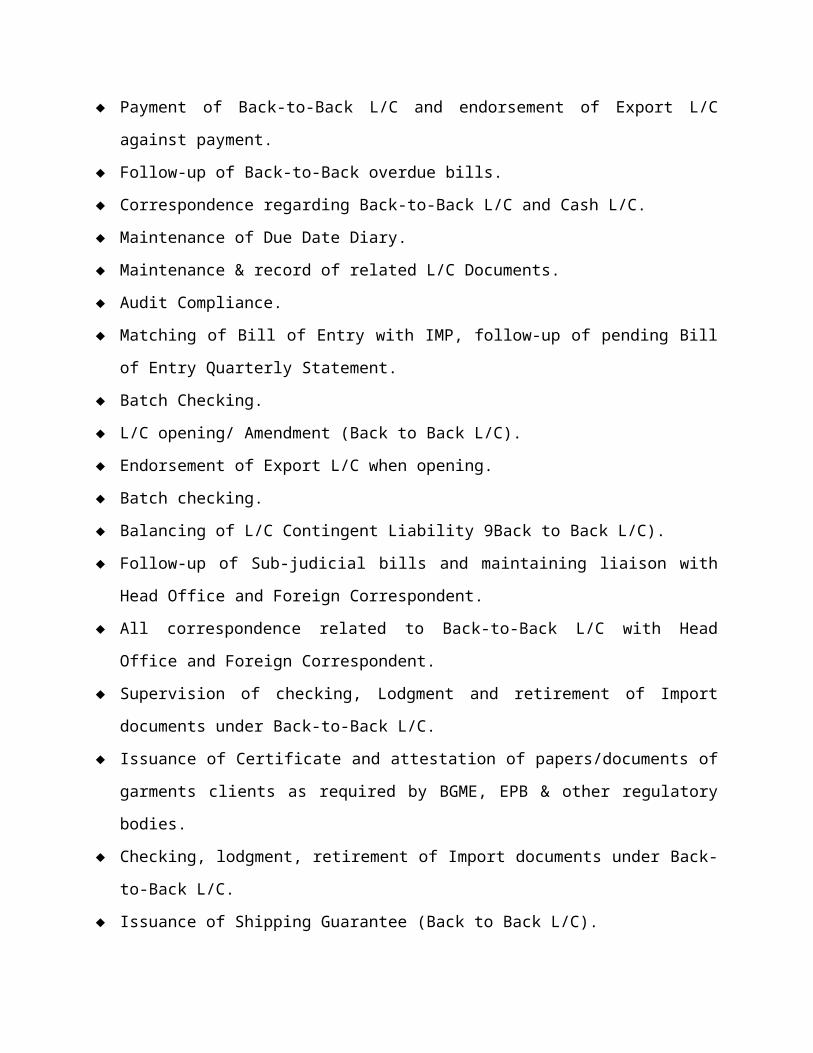

Things, which are done here:

The following things are done in this department:

Total supervision of Import Department (Cash/Back to Back

L/C).

Foreign Correspondence related to above.

Payment of Back-to-Back L/C and endorsement of Export L/C

against payment.

Follow-up of Back-to-Back overdue bills.

Correspondence regarding Back-to-Back L/C and Cash L/C.

Maintenance of Due Date Diary.

Maintenance & record of related L/C Documents.

Audit Compliance.

Matching of Bill of Entry with IMP, follow-up of pending Bill

of Entry Quarterly Statement.

Batch Checking.

L/C opening/ Amendment (Back to Back L/C).

Endorsement of Export L/C when opening.

Batch checking.

Balancing of L/C Contingent Liability 9Back to Back L/C).

Follow-up of Sub-judicial bills and maintaining liaison with

Head Office and Foreign Correspondent.

All correspondence related to Back-to-Back L/C with Head

Office and Foreign Correspondent.

Supervision of checking, Lodgment and retirement of Import

documents under Back-to-Back L/C.

Issuance of Certificate and attestation of papers/documents of

garments clients as required by BGME, EPB & other regulatory

bodies.

Checking, lodgment, retirement of Import documents under Back-

to-Back L/C.

Issuance of Shipping Guarantee (Back to Back L/C).

IMP Form Fill-up (Cash L/C).

Inform negotiating Bank about maturity date of Back-to-Back

L/C.

Quarterly statements for Bonded ware House.

Balancing of Accepted Liability.

Statement of outstanding accepted import bills under Back-to-

Back L/C.

L/C opening and Amendment of Cash L/C (and Inland L/C).

Maintenance and record of Passbook and IRC.

Maintenance & Record of related L/C (s) & Documents.

Credit Report.

Statement of IRC Renewal fees to CCI&E.

Preparation of monthly foreign exchange business position.

L/C Lodgment (Cash).

Checking of Cash L/C documents.

L/C Retirement.

LCA Issue.

BLC Statement.

Differed Payment (Cash).

Follow-up of outstanding BLC.

Correspondent (Cash L/C).

Proof Sheet of LC Margin and Contingent Liability (Cash L/C).

Issuance of shipping guarantees (cash) IMP forms fill-up

(cash).

5.7 L/C Opening:If an importer wants to import some goods from outside the

country, at first he has to apply to a bank for opening a L/C.

Letter of Credit (L/C) is a written undertaking of a bank written

to the seller and issued at the request of the buyer to pay at

site or a determinable future date. According to Import Policy,

unless or otherwise specified, all import is to be made by

opening irrevocable letter of credit (amendment or cancellation

with the agreement of the opening bank, advising bank,

beneficiary, and importer). L/C can be opened against Performa

invoice if the exporter has no agent and L/C can be opened

against Indent if the foreign supplier has indenting agent.

Documents Require for Opening a L/C:

For opening letter of credit an importer is required to have some

documents, which are to be submitted to the L/C issuing or

popularly known as opening bank.

A valid Import Register Certificate (IRC)

Membership Certificate from the registered local Chamber of

Commerce and Industry or valid trade license

TIN

Letter of Credit Authorization form (LCA)

Insurance cover note for L/C amount

Indents for goods issued by indenter or Performa Invoice

issued by foreign supplier

Charge Documents duly signed

IMP form duly signed

The opener has to have a current account with the bank

5.8 Procedure involved in L/C opening:There are few steps involved in L/C opening process. These are: -

At first the L/C opener is required to fill up the

prescribed application form for requesting to open a L/C

for him.

After receiving the application form with other required

documents submitted by the opener they are to be thoroughly

scrutinized. The points, which shall be scrutinized, are

describing bellow-

a. The amount and description of goods in the application

should be relevant with the indent or Performa invoice or

import contract.

b. The amount is covered by the insurance amount.

c. The item is not a banned one.

d. The indent produced has the Import Registration

Certificate number and the indenter’s registration

number. The indent has indenting agent’s signature and

importer’s signature.

e. Whether transshipment and partial shipment is allowed.

If all the documents along with the application are in

order, the financial position and credit worthiness of the

importer, market demand of the good is assessed. Margin for

letter of credit will also be determined. The rate of

margin depends on the financial condition of the banker,

Importers previous performance, status of relationship with

the importer, nature of goods etc. This margin is to be

retained from the importer either in cash or debiting the

importer’s current account with the bank. The importer is

also required to pay the other concerning charges like

foreign corresponding charge, telex charge (if any),

handling charges, and commission etc.

After all these steps of letter of credit is opened and forwarded

to the advising bank.

Accounting Procedure Involved in L/C opening:

There are two types of accounting procedure involved in L/C. One

is L/C opening, and another is Liability Register, which includes

Liability amount, Margin, Foreign correspondent etc. While

opening L/C there are few accounting entries.

► For Margin importer account with bank is debited and Margin A/C

is credited.

► For contingent liability (L/C amount) Customer’s liability on

L/C cash is debited and Banker’s liability on cash is credited.

►For other charges customer’s current account is debited and

commission A/C, income A/C, Foreign correspondent charge A/C and

other related A/C is credited.

Advising a Letter of Credit:

The advising or notifying bank is the bank through which the L/C

is advised to the exporter. It is a bank situated in the

exporting country and it may be a branch of the opening bank. It

becomes customary to advise a credit to the beneficiary through

an advising bank.

Adding Confirmation:

The confirming bank does adding confirmation. Confirming bank is

a bank, which adds its confirmation to the credit, and it is done

at the request of the issuing bank. The confirming bank may or

may not be the advising bank.

L/C Transmitting:Letter of credit can be transmitted to the advising bank through

three methods. They are in Telex, Courier, or SWIFT (Society for

Worldwide Inter-bank Financial Telecommunication). L/C is send to

advising bank in three copies. The advising bank authenticates

the original copy of L/C and delivers it to the exporter. The

duplicate copy is kept with the advising bank.

Negotiating:The beneficiary (exporter) receives the letter of credit from

advising bank. After proper shipment of goods as per terms and

conditions of the L/C, required documents like Commercial

Invoice, Bill of Lading, and bill of exchange are presented to

the negotiating bank by the beneficiary for negotiation. If the

documents are in order as per L/C then the negotiating bank

negotiates the drafts making payment to the beneficiary. Then the

negotiating bank forwards the drafts along with the shipping

documents to the L/C opening bank. The negotiating bank

reimburses the amount paid against the draft from reimbursement

bank.

Amendment:

Parties involved in a L/C, particularly the seller and the buyer

cannot always satisfy the terms and conditions in full as

expected due to some obvious and genuine reasons. In such a

situation, the credit should be amended National Bank transmits

the amendment by tested telex to the advising bank .In case of

revocable credit it can be amended or cancelled by the issuing

bank at any moment and without prior notice to the beneficiary.

But in case of irrevocable letter of credit, it can neither be

amended nor cancelled without the consent of the issuing bank,

the confirming bank (if any) and the beneficiary. If the L/C is

amended, service charge and telex charge is debited from the

party account accordingly.

Examination of Documents:National Bank officials check whether these documents have any

discrepancy or not. Here, Discrepancy means the dissimilarity of

any of the documents with the terms and conditions of L/C.

Adding Confirmation:Add the confirming Bank gives confirmation. An Add confirmation

letter contains the followings,

1) L/C No.

2) L/C amount

3) Items to be imported, etc.

Lodgment:

The opening bank receives import bills, which have been

negotiated. After receiving the documents, they are to be

thoroughly scrutinized before lodgment.

Scrutiny of the Documents:

First of all it must be ensured that full set of documents as

mentioned in the L/C has been received.

Documents have been negotiated within the negotiation period.

The Bill of Lading/Air-Way Bill/ Railway receipt is not dated

later than the last date of shipment mentioned in the L/C.

The L/C has not been amended or subjected to any special

instructions, which might alter the value of L/C

Import bills include following documents, which are to be

scrutinized.

Bill of Exchange

Commercial Invoice

Bill of Lading

Certificate of Origin

Others

Bill of Exchange:

It has to be verified that the bill of exchange has been

properly drawn and signed by the beneficiary according to the

terms and conditions of L/C.

The amount in the Bill is identical with that mentioned in the

invoice.

The amount drawn does not exceed the amount mentioned in the

L/C.

The amount in words and figures should be same.

The bill of exchange should be properly endorsed.

Commercial Invoice:

It has to be verified that the commercial invoice has been

properly drawn and signed by the beneficiary according to the

terms and conditions of L/C.

The beneficiary should properly invoice the merchandise.

The merchandise is invoiced to the importer on whose account

the L/C is opened.

The description of merchandise and the unit price correspond

with that given in the L/C.

The import license or IRC number of the importer, indenter’s

registration number and number of Letter of Credit

Authorization number are incorporated in the Invoice.

Bill of Lading:

First of all it has to be cleared that the Bill of Lading is

showing “Shipped on Board” and it has to be properly endorsed to

the bank.

The B/L should include the description of the merchandise

according to invoice.

The port of shipment and destination, date of shipment and the

name of the consignee are in agreement with those mentioned in

the L/C.

The shipping company or their authorized agents properly sign

the B/L.

The date on the B/L is not ‘stale’ which means it is not dated

in unreasonably long time prior to negotiation.

Certificate of Origin:

The Merchandise described in the Certificate is in accordance

with the L/C.

Others:

There are some other documents, which are also attached, with the

shipping documents like packing list, pre-shipment inspection

certificate etc. These documents are also verified carefully

before lodgment.

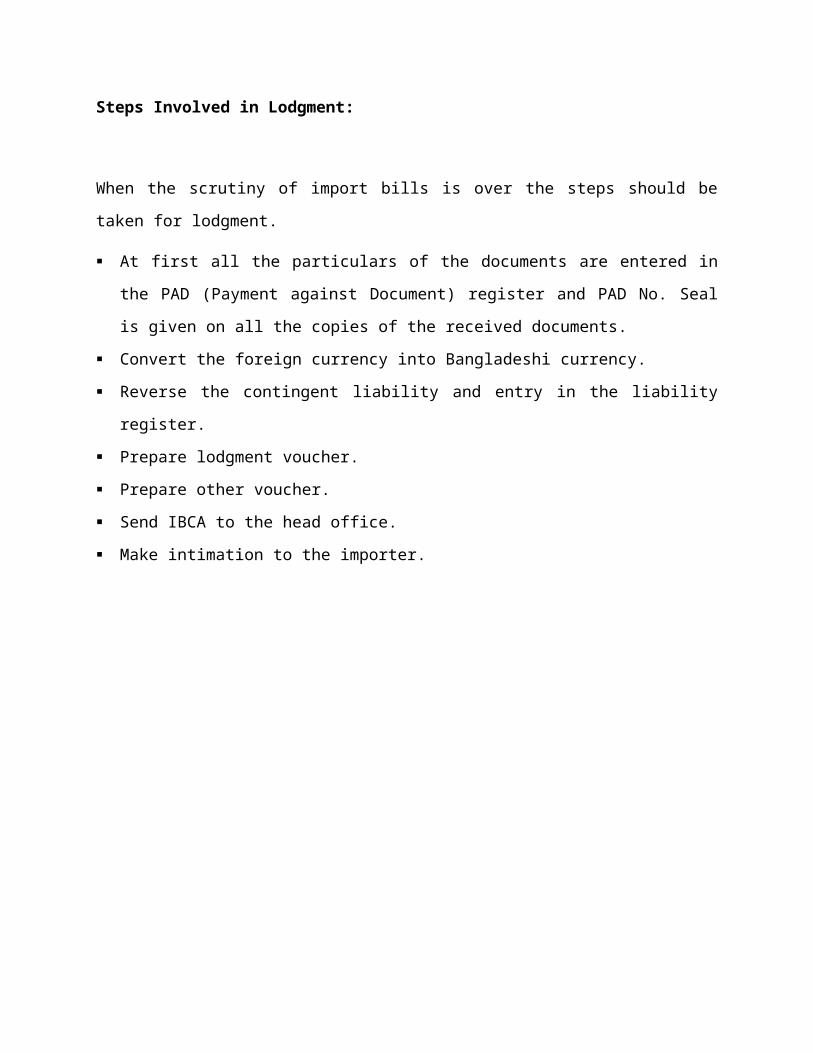

Steps Involved in Lodgment:

When the scrutiny of import bills is over the steps should be

taken for lodgment.

At first all the particulars of the documents are entered in

the PAD (Payment against Document) register and PAD No. Seal

is given on all the copies of the received documents.

Convert the foreign currency into Bangladeshi currency.

Reverse the contingent liability and entry in the liability

register.

Prepare lodgment voucher.

Prepare other voucher.

Send IBCA to the head office.

Make intimation to the importer.

Chapter Six:Overview of Export

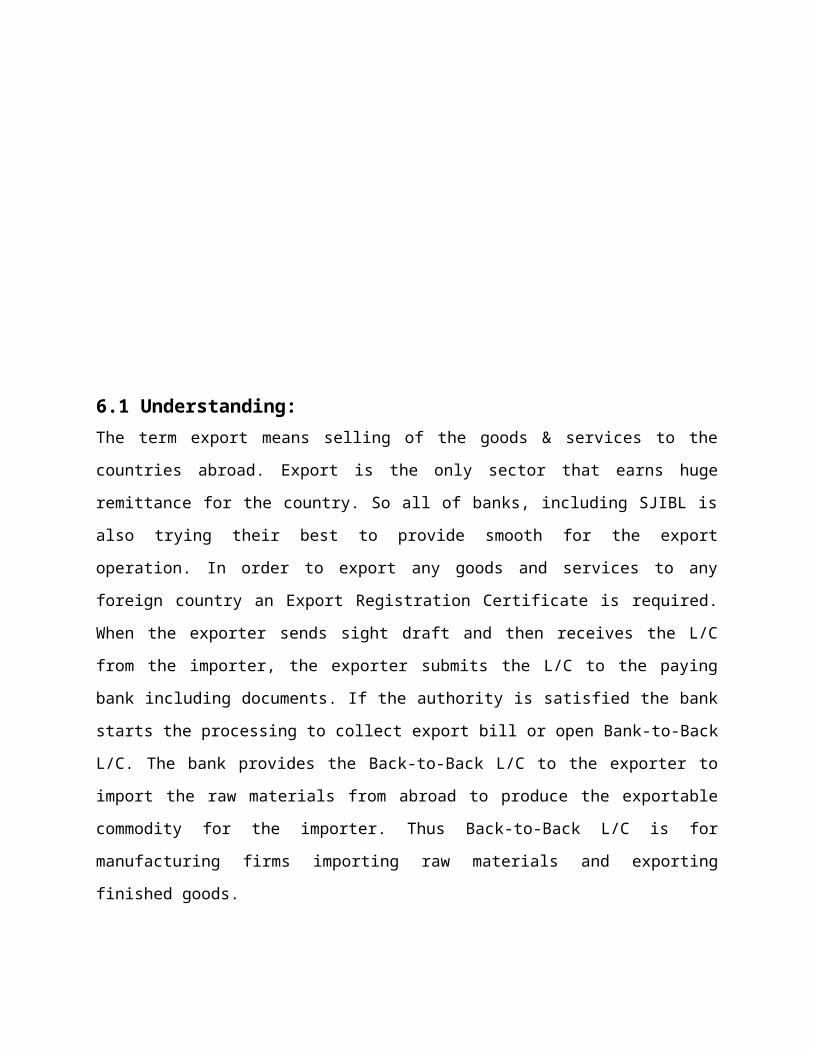

6.1 Understanding:The term export means selling of the goods & services to the

countries abroad. Export is the only sector that earns huge

remittance for the country. So all of banks, including SJIBL is

also trying their best to provide smooth for the export

operation. In order to export any goods and services to any

foreign country an Export Registration Certificate is required.

When the exporter sends sight draft and then receives the L/C

from the importer, the exporter submits the L/C to the paying

bank including documents. If the authority is satisfied the bank

starts the processing to collect export bill or open Bank-to-Back

L/C. The bank provides the Back-to-Back L/C to the exporter to

import the raw materials from abroad to produce the exportable

commodity for the importer. Thus Back-to-Back L/C is for

manufacturing firms importing raw materials and exporting

finished goods.

In the Export section, two types of L/C s are opened-

Back to Back L/C

Export L/C

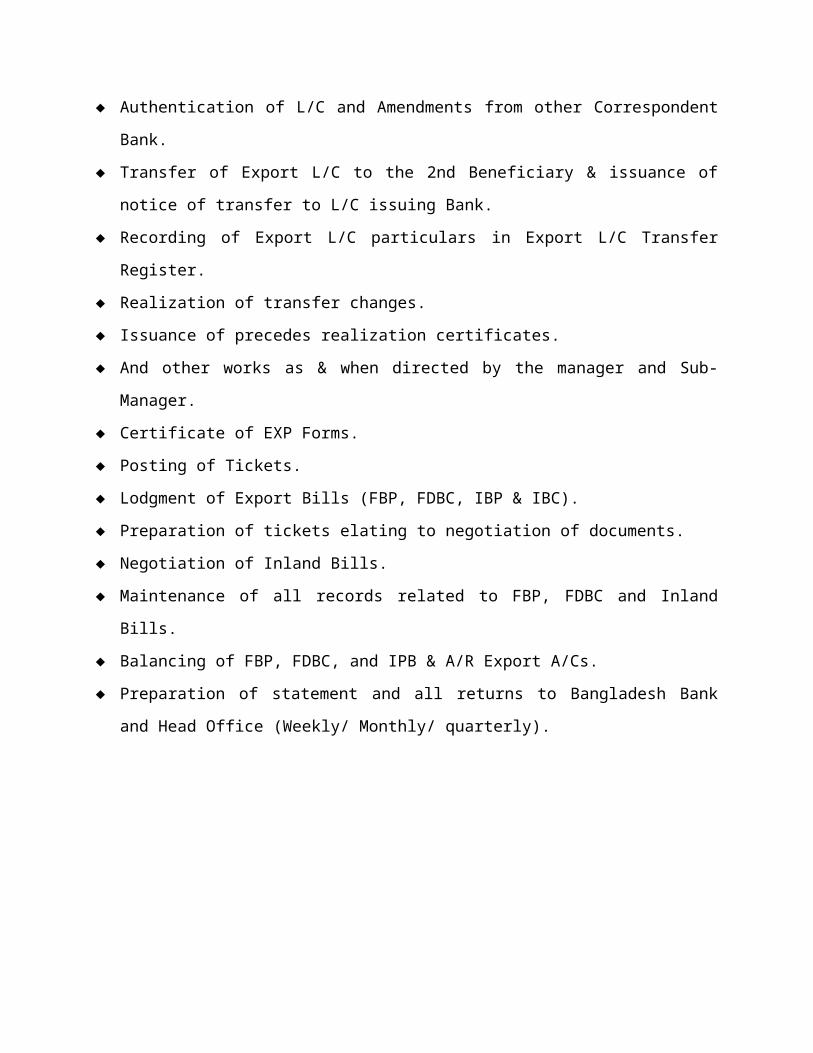

6.2 Things done here:

The following things are done in this department:

Scrutiny of Export Shipping Documents.

Follow-up for realization of Export Proceeds.

All Correspondence relating to Export Department.

Compliance of Audit & Inspection.

Advising of Export L/Cs to the beneficiary.

Authentication of L/C and Amendments from other Correspondent

Bank.

Transfer of Export L/C to the 2nd Beneficiary & issuance of

notice of transfer to L/C issuing Bank.

Recording of Export L/C particulars in Export L/C Transfer

Register.

Realization of transfer changes.

Issuance of precedes realization certificates.

And other works as & when directed by the manager and Sub-

Manager.

Certificate of EXP Forms.

Posting of Tickets.

Lodgment of Export Bills (FBP, FDBC, IBP & IBC).

Preparation of tickets elating to negotiation of documents.

Negotiation of Inland Bills.

Maintenance of all records related to FBP, FDBC and Inland

Bills.

Balancing of FBP, FDBC, and IPB & A/R Export A/Cs.

Preparation of statement and all returns to Bangladesh Bank

and Head Office (Weekly/ Monthly/ quarterly).

6.3 Export Bill Scrutiny

Scrutinizes the export bill on the following points,

A. General:

Late shipment.

Late presentation.

L/C expired.

L/C overdrawn.

Partial shipment or transshipment beyond L/C

terms.

B. Bill Of Exchange:

Amount of bill differs with Invoice.

Not drawn on L/C issuing bank not signed.

Tenor of B/E not identical with L/C

Full set not submitted Invoice:

Not issued by the beneficiary

Not signed by the beneficiary

Not made out in the name of the Applicant

Description, Price, quantity, sales terms of the

goods not corresponds to the credit.

Not marked one fold as original Shipping marks

differs with B/L & packing list.

C. Packing List:

Gross weight, net weight, & measurement, number of

cartoons/ packages differs with B/L.

Not marked one fold as original.

Not signed by the beneficiary.

Shipping marks differs with B/L.

D. Bill of Lading/Air Way Bill:

Full set of bill not submitted.

B/L is not drawn or endorsed to the Order Of

National Bank.

“Shipping On Board”, “Freight Prepaid” or “Freight

Collect” etc. notations are not marked on the B/L.

B/L not indicate the name and capacity of the party

i.e. carrier or master, on whose behalf the agent is

signing the B/L.

Shipped on Board Notation not showing name of pre-

carriage vessel/ intended vessel.

Shipped on Board Notation not showing port of

loading and vessel name (In case B/L indicates a

place of receipt or taking in charge different from

the port of lading).

Short Form B/L.

Charter party B/L.

Description of goods in B/L not agrees with that of

Invoice, B/E & P/L.

Alterations in B/L not authenticated.

Loaded on deck.

B/L bearing clauses or notations expressly declaring

defective condition of the goods and / or the

packages.

E. Others:

Non-Negotiable documents not forwarded to buyers or

forwarded beyond L/C terms.

Inadequate number of Invoice, Packing List, & others

submitted.

Short shipment certificate not submitted.

6.4 Export Finance

Pre-shipment credit:

Pre-shipment credit usually takes the following forms:

Overdraft against hypothecation of exportable commodities.

Overdraft against Trust Receipt (T.R.)

Packing Credit (P.C.)

Post shipment Credit:

Post shipment credit refers to credit facilities extended to

export after actual shipment of goods against shipping documents.

It is usually provided in the following ways.

Bill negotiation / purchase.

Bill for collection.

Bill Negotiation / Purchase:

The most usual method of financing exporters at the post-shipment

stage is negotiation of documents under L/C. Here the bank acts

as negotiating bank. After the shipment of the goods, the

exporter submits the relative documents to the branch for

negotiation. The documents generally include a) Bill of Exchange

b) Bill of Lading, c) Insurance policy d) Invoice e) Certificate

of origin etc. The documents are to submit within the period

mentioned in the L/C. The documents are sent to the L/C opening

branch with a forwarding letter. Then the branch claim

reimbursement from the issuing bank or from the reimbursing bank.

On negotiation/ Purchase of the export bills, the exporter is

paid the value of the bill (converted into Bangladeshi Tk at the

ruling bill buying rates).

Documents on Collection Basis:

The documents, which are not negotiable by the branch due to some

discrepancies, are sent to L/C opening bank on collection basis.

The bank mentions the discrepancies on their forwarding schedule.

On receiving the documents, the L/C opening bank will further

scrutinize the document with the L/C and inform the importer

regarding discrepancies found in the documents. If these are

acceptable to the importer and or permissible with the exiting

Exchange control regulation, the documents will be lodged and L/C

opening bank will send the payment instruction to the collection

bank.

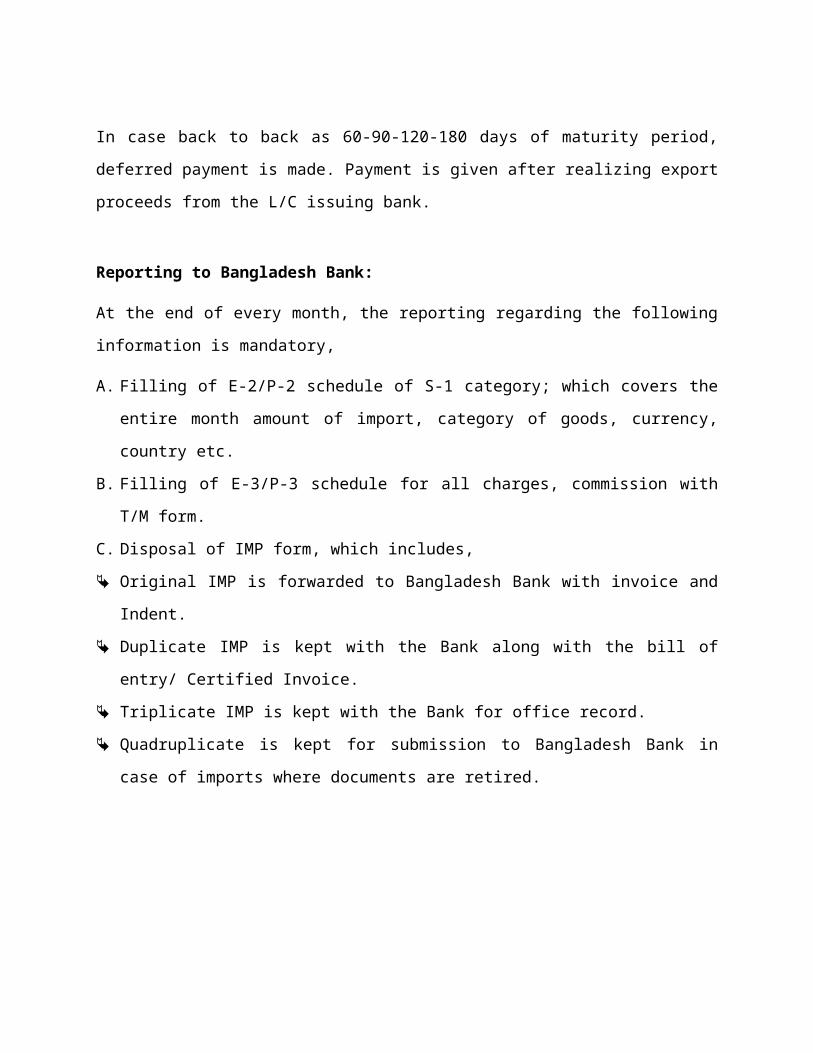

Back-To-Back L/C:

In case of a Back to back letter of credit, a new L/C (an Import

L/C) is opened on the basis of an original L/C (an Export L/C).