Changing landscape of enterprise search and ... - Rocket Software

16

Changing landscape of enterprise search and publishing June 2014 A Vanson Bourne survey

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Changing landscape of enterprise search and ... - Rocket Software

Changing landscape of

enterprise search and publishing

June 2014

A Vanson Bourne survey

2 |

Contents

Aims of the research 3

Summary of key findings 4

Solutions and perceptions 6

Solutions being used 6

How are these products perceived? 6

Cost of search 7

Usage and features 8

Factors influencing adoption 8

Specific search and publishing features 9

Challenges and consequences 10

Barriers to realizing objectives 10

Coping with changing demands 10

Consequences of failure 11

Time and effort 12

Offline access to data 12

Increasing efficiency and reducing time losses 12

Conclusion 14

Research methodology 15

3 |

This study explores the solutions that

organizations are using to index and deploy their

content to end-users. It looks at how respondents

perceive their current solution and whether they

feel satisfied about content delivery, affordability,

and how up-to-date it is. There is specific focus on

how the perceptions of Rocket Folio and NXT

compare with those of other software offerings in this category.

Another focus of investigation will be on the

specific features that respondents can access,

which they consider most important, and which

they do not have but would like. Looking at the

wider landscape, the study considers how the

demands on search and publishing have shifted in

recent years and what impact this is having on

the organization. What are the consequences of failure to cope with these changes?

Finally, what impact has offline access to data had

on those who have implemented it? The study will

see whether or not this has addressed the time

and cost challenges associated with enterprise search.

Aims of the research

4 |

Although only a minority

currently use Rocket software

solutions, these users have a better experience

Figure S1: Analysis showing the percentages of respondents a) overall and b) only Rocket software users that rate their software top in each criteria. Asked to all respondents (200)

Technical respondents estimate

greater spend on enterprise search

Figure S2: “In 2013, what do you estimate was the overall financial cost of searching for, and retrieving, specific information?” Asked to all respondents (200), split by technical vs non-technical

Over three quarters gave a

significant amount of

consideration to security and

subscription management

when choosing their search solution

Figure S3: “How much consideration did you give to the following before deciding to purchase your current publishing and enterprise search solution?” Asked of all respondents (200), showing percentages that gave a lot of consideration to each

Only 7% are fully satisfied with

their solution’s existing features

Figure S4: Analysis of “Which features would you like to see in your publishing and enterprise search solutions?” Asked of all respondents (200)

17% 15% 16%

40%37%

50%

Extremely good

ability to deliver

content

Very reasonable

cost

Totally up-to-

date

Overall average Rocket Folio/NXT

$577,785

$375,513

Technical respondents Non-technical respondents

77%

72%

71%

65%

62%

Security and subscriptionmanagement

Cost oflicensing/implementation

Level of maintenance (bothtime and cost)

Ability to edit documentswith unique features

Depth of search features

93%

7%

Percentage of respondents that would like to see newfeatures added to their existing solution

Percentage of respondents that would not like to seeany new features added

Summary of key findings

5 |

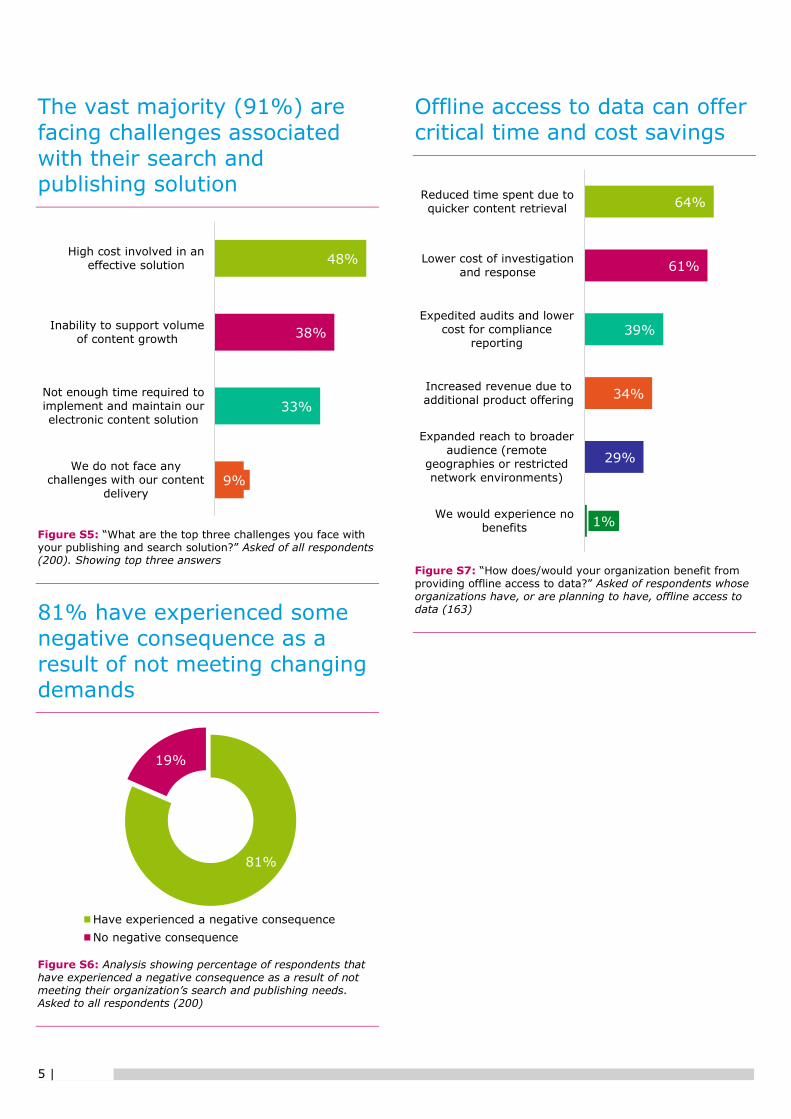

The vast majority (91%) are

facing challenges associated

with their search and publishing solution

Figure S5: “What are the top three challenges you face with your publishing and search solution?” Asked of all respondents (200). Showing top three answers

81% have experienced some

negative consequence as a

result of not meeting changing demands

Figure S6: Analysis showing percentage of respondents that have experienced a negative consequence as a result of not meeting their organization’s search and publishing needs. Asked to all respondents (200)

Offline access to data can offer critical time and cost savings

Figure S7: “How does/would your organization benefit from providing offline access to data?” Asked of respondents whose organizations have, or are planning to have, offline access to data (163)

48%

38%

33%

9%

High cost involved in aneffective solution

Inability to support volumeof content growth

Not enough time required toimplement and maintain ourelectronic content solution

We do not face anychallenges with our content

delivery

81%

19%

Have experienced a negative consequence

No negative consequence

64%

61%

39%

34%

29%

1%

Reduced time spent due toquicker content retrieval

Lower cost of investigationand response

Expedited audits and lowercost for compliance

reporting

Increased revenue due toadditional product offering

Expanded reach to broaderaudience (remote

geographies or restrictednetwork environments)

We would experience nobenefits

6 |

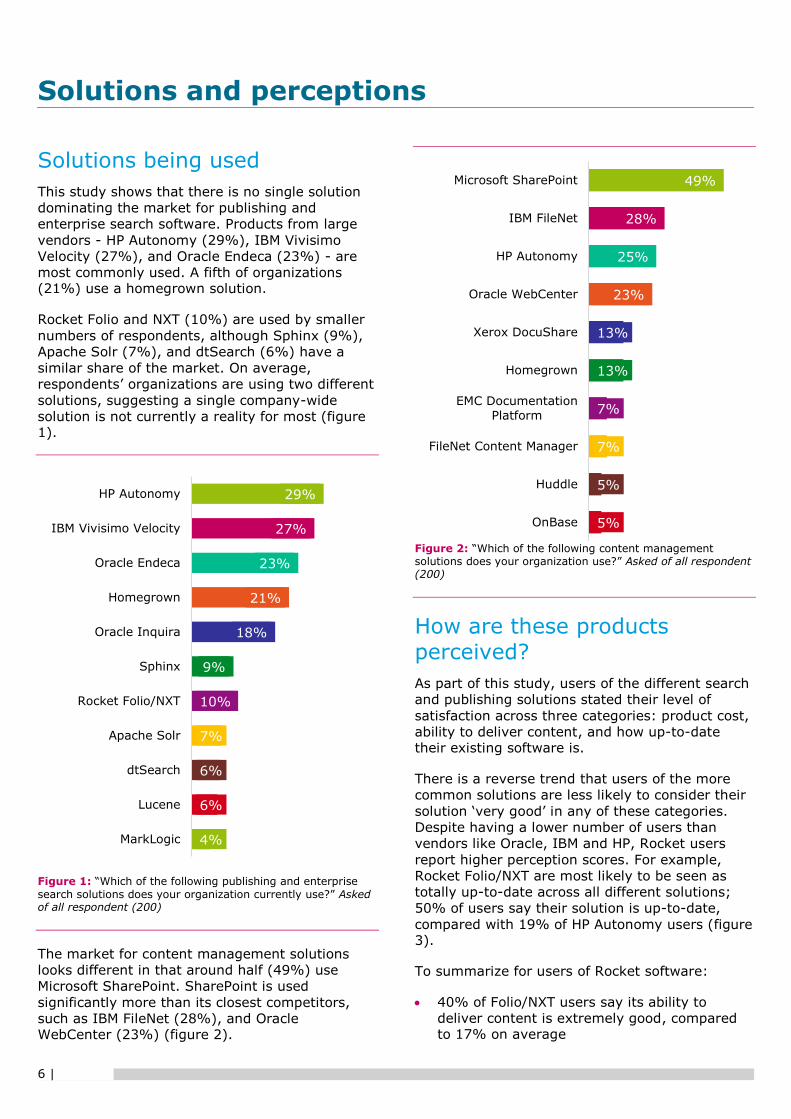

Solutions being used

This study shows that there is no single solution

dominating the market for publishing and

enterprise search software. Products from large

vendors - HP Autonomy (29%), IBM Vivisimo

Velocity (27%), and Oracle Endeca (23%) - are

most commonly used. A fifth of organizations (21%) use a homegrown solution.

Rocket Folio and NXT (10%) are used by smaller

numbers of respondents, although Sphinx (9%),

Apache Solr (7%), and dtSearch (6%) have a

similar share of the market. On average,

respondents’ organizations are using two different

solutions, suggesting a single company-wide

solution is not currently a reality for most (figure 1).

Figure 1: “Which of the following publishing and enterprise

search solutions does your organization currently use?” Asked of all respondent (200)

The market for content management solutions

looks different in that around half (49%) use

Microsoft SharePoint. SharePoint is used

significantly more than its closest competitors,

such as IBM FileNet (28%), and Oracle WebCenter (23%) (figure 2).

Figure 2: “Which of the following content management solutions does your organization use?” Asked of all respondent (200)

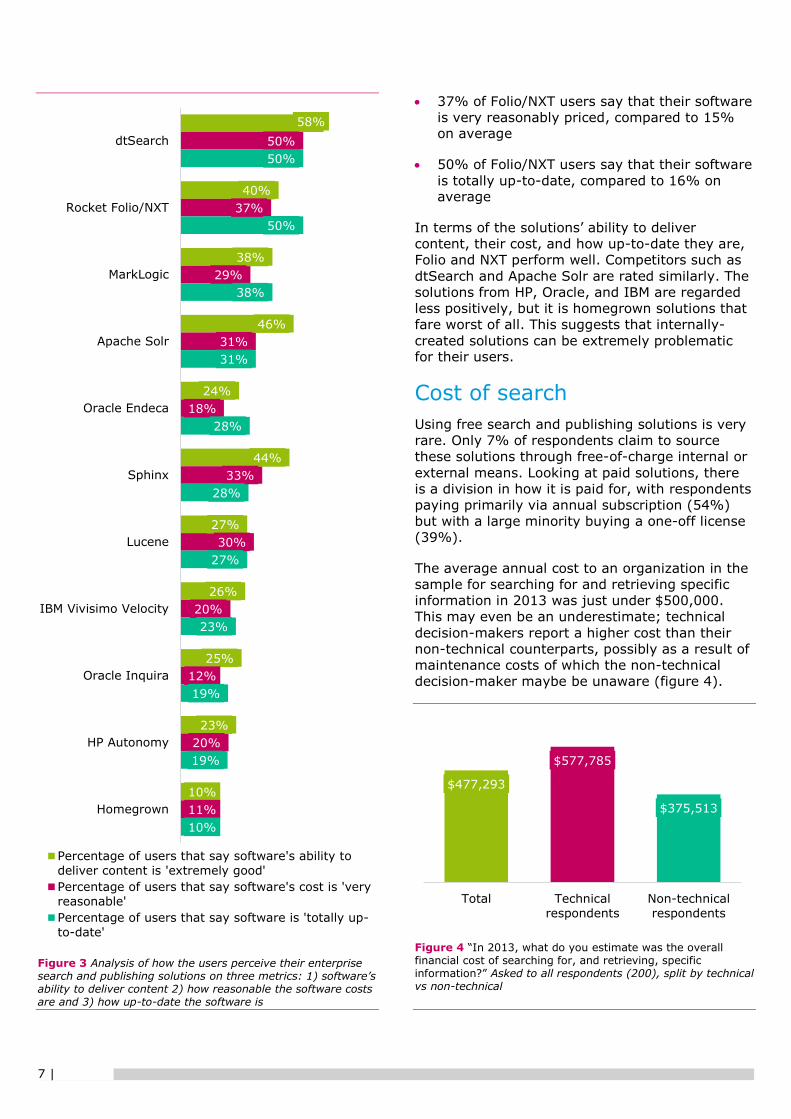

How are these products perceived?

As part of this study, users of the different search

and publishing solutions stated their level of

satisfaction across three categories: product cost,

ability to deliver content, and how up-to-date their existing software is.

There is a reverse trend that users of the more

common solutions are less likely to consider their

solution ‘very good’ in any of these categories.

Despite having a lower number of users than

vendors like Oracle, IBM and HP, Rocket users

report higher perception scores. For example,

Rocket Folio/NXT are most likely to be seen as

totally up-to-date across all different solutions;

50% of users say their solution is up-to-date,

compared with 19% of HP Autonomy users (figure 3).

To summarize for users of Rocket software:

40% of Folio/NXT users say its ability to

deliver content is extremely good, compared to 17% on average

29%

27%

23%

21%

18%

9%

10%

7%

6%

6%

4%

HP Autonomy

IBM Vivisimo Velocity

Oracle Endeca

Homegrown

Oracle Inquira

Sphinx

Rocket Folio/NXT

Apache Solr

dtSearch

Lucene

MarkLogic

49%

28%

25%

23%

13%

13%

7%

7%

5%

5%

Microsoft SharePoint

IBM FileNet

HP Autonomy

Oracle WebCenter

Xerox DocuShare

Homegrown

EMC Documentation

Platform

FileNet Content Manager

Huddle

OnBase

Solutions and perceptions

7 |

Figure 3 Analysis of how the users perceive their enterprise search and publishing solutions on three metrics: 1) software’s ability to deliver content 2) how reasonable the software costs are and 3) how up-to-date the software is

37% of Folio/NXT users say that their software

is very reasonably priced, compared to 15% on average

50% of Folio/NXT users say that their software

is totally up-to-date, compared to 16% on average

In terms of the solutions’ ability to deliver

content, their cost, and how up-to-date they are,

Folio and NXT perform well. Competitors such as

dtSearch and Apache Solr are rated similarly. The

solutions from HP, Oracle, and IBM are regarded

less positively, but it is homegrown solutions that

fare worst of all. This suggests that internally-

created solutions can be extremely problematic for their users.

Cost of search

Using free search and publishing solutions is very

rare. Only 7% of respondents claim to source

these solutions through free-of-charge internal or

external means. Looking at paid solutions, there

is a division in how it is paid for, with respondents

paying primarily via annual subscription (54%)

but with a large minority buying a one-off license

(39%).

The average annual cost to an organization in the

sample for searching for and retrieving specific

information in 2013 was just under $500,000.

This may even be an underestimate; technical

decision-makers report a higher cost than their

non-technical counterparts, possibly as a result of

maintenance costs of which the non-technical

decision-maker maybe be unaware (figure 4).

Figure 4 “In 2013, what do you estimate was the overall financial cost of searching for, and retrieving, specific information?” Asked to all respondents (200), split by technical vs non-technical

58%

40%

38%

46%

24%

44%

27%

26%

25%

23%

10%

50%

37%

29%

31%

18%

33%

30%

20%

12%

20%

11%

50%

50%

38%

31%

28%

28%

27%

23%

19%

19%

10%

dtSearch

Rocket Folio/NXT

MarkLogic

Apache Solr

Oracle Endeca

Sphinx

Lucene

IBM Vivisimo Velocity

Oracle Inquira

HP Autonomy

Homegrown

Percentage of users that say software's ability to

deliver content is 'extremely good'

Percentage of users that say software's cost is 'very

reasonable'

Percentage of users that say software is 'totally up-

to-date'

$477,293

$577,785

$375,513

Total Technical

respondents

Non-technical

respondents

8 |

Internal

audiences

External

audiences

Factors influencing adoption

Selecting the most appropriate solution can be

challenging as there are numerous factors to consider prior to the decision.

Security and subscription management is the top

consideration (77% of respondents afford it

significant consideration). Other key factors which

respondents’ organizations were most likely to

have considered are cost of licensing/

implementation (72%), level of maintenance

(71%), and the ability to edit documents with unique features (65%) (figure 5).

Figure 5: “How much consideration did you give to the following before deciding to purchase your current publishing and enterprise search solution?” Asked of all respondents (200), showing percentages that gave a lot of consideration to each

One possible explanation for security and

subscription management being the top factor is

the large number of audiences that require access to content.

Almost four fifths (79%) of IT departments within

the organizations surveyed need to access the

publishing and enterprise search solution,

followed by 65% of organizations’ finance

departments. There are six departments named

by more than half of respondents as needing

access to the publishing and enterprise search solution.

In terms of external audiences, around half of

respondents (48%) need their customers to have

access, and two fifths (41%) need to provide it to

partners (figure 6). Overall, three quarters (76%)

need to provide access to at least one external party.

On average, each respondent says four different

internal departments and two different external

groups use their organization’s search and publishing solution.

Figure 6: “Which of the following audiences require access to your publishing and enterprise search solution?” Asked to all respondents (200)

77%

72%

71%

65%

62%

54%

49%

49%

Security and subscriptionmanagement

Cost oflicensing/implementation

Level of maintenance (bothtime and cost)

Ability to edit documentswith unique features i.e.

hyperlinks, doc annotationsetc.

Depth of search features

Time required to implementsoftware

Automatic formatting acrossdevices for greater user

experience

Available content connectors

79%

65%

56%

55%

55%

53%

46%

27%

48%

41%

35%

27%

IT

Finance

Human resources

Support

Professional services

Legal

Marketing

R&D

Customers

Partners

Suppliers

Regulatory/governance

bodies

Usage and features

9 |

Specific search and publishing features

Affordability is another major consideration, as

evidenced by the fact that most respondents say

that the cost of licensing/implementation and

maintenance were considerations when making

their decision.

However the functionality of the product itself is

also at the forefront of respondents’ minds;

significant consideration is given to the ability to

edit in-document (65%) and the depth of search

features (62%).

Delving deeper into search functionality, this

study investigates some of the specific features

that users value and those they want if currently

absent.

Figure 7: “Which of these features do you believe are the most important?” Asked of all respondents (200), respondents only see features that their solution already has

Each respondent identified which of the existing

features they consider most important. Access

control (65%), in-document editing and cross-

referencing (62%), and scalability (61%) feature

strongly in the list of most important available

features (figure 7). This again reflects concern as

to the most appropriate way content can be

delivered to search and publishing users.

Despite the large number of features that

respondents’ solutions have, 93% would

nonetheless welcome certain additional features,

suggesting that they are not entirely satisfied with

the existing range of features that their solution offers (figure 8).

Full query search and text retrieval (52%) is the

feature desired by most if they do not have it

already.

Figure 8: Analysis of “Which features would you like to see in your publishing and enterprise search solutions?” Asked of all respondents (200)

65%

62%

61%

61%

60%

59%

57%

54%

54%

50%

Access control of documents(governing who sees what

documents)

In document editing and cross-referencing including

hyperlinks, annotations

Scalability to support increasein content volume

Full query search and textretrieval

In depth search filters

Analytics and visualization forinsight into content

Ability to gather and indexstructured, semi-structuredand unstructured content

Faceted search (enablesbrowsing information by

application of filters)

Language support/languagespecific search

Federated search (allowssimultaneous search of

multiple search resources)

93%

7%

Percentage of respondents that would like to see new

features added to their existing solution

Percentage of respondents that would not like to see

any new features added

10 |

Barriers to realizing objectives

The vast majority (91%) report some challenge

associated with their current content solution.

Inability to support a growing volume of content

(38%) and difficulty in connecting and integrating

various content types (32%) are among the most

commonly encountered, but high cost is the top

challenge and experienced by around half (48%)

(figure 9).

Notably, only 25% of Rocket users see high cost as one of their primary challenges.

Figure 9: “What are the top three challenges you face with your publishing and search solution?” Asked of all respondents (200)

The fact that no single answer dominates here

shows that each organization is experiencing its

own individual problems, making a one-size-fits-all solution inappropriate.

Coping with changing demands

One of the top challenges associated with search

and publishing solutions is the ability to scale

solutions to cope with increasing volumes of data.

On average, data scalability is predicted to

increase from 168TB to 223TB by 2017, an increase of 33% (figure 10).

An increase is predicted in every country and in every sector. The largest increase is in the US.

Figure 10: Analysis of “What is your current scalability requirements for your publishing and search solution?” Asked to all respondents (200) Split by country. Showing average number of TB of scalability requirement for now and three years’ time

Just 4% of all respondents have not experienced

any changing search and publishing needs in the

last five years. The most pressing demands from

the last five years are exponentially growing

volume (58%), and expanding to more devices

(55%) and platforms (55%) (figure 11).

Have these changing demands been met? While

there has been some limited success, over half

(56%) report some degree of failure to meet the demands (figure 12).

48%

38%

33%

32%

32%

29%

26%

19%

18%

9%

High cost involved in aneffective solution

Inability to support volume ofcontent growth

Not enough time required toimplement and maintain ourelectronic content solution

Difficulty in connecting andintegrating various content

types

Insufficient content securityand subscription

management

Lack of resources required toimplement and maintain ourelectronic content solution

Inadequate navigation andsearch experience for our

end-users

Inability to ingest content inan reasonable timeframe

Inability to provide uniquecontent through document

annotations, hyperlinks, side-bar comments, notes etc.

We do not face anychallenges with our content

delivery

168 174 166149

223247

202188

Total USA UK Brazil

Current scalability requirement

Predicted scalability requirement in three years

Challenges and consequences

11 |

Figure 11: “In what ways have your publishing and enterprise search needs as an organization changed over the last 5 years?” Asked of all respondents (200)

Rocket users have been able to meet these

challenges with greater success; 100% of

Folio/NXT users say they been able to provide

access to more specialist content, compared with

68% on average. Folio/NXT users (83%) are also

more likely to say that they have met the

challenge of contending with a wider number of

unstructured formats well, compared to 58%

overall.

Figure 12: Analysis of “To what extent has your organization's publishing and enterprise search solution been able to meet these changing demands?” Asked of all respondents (200)

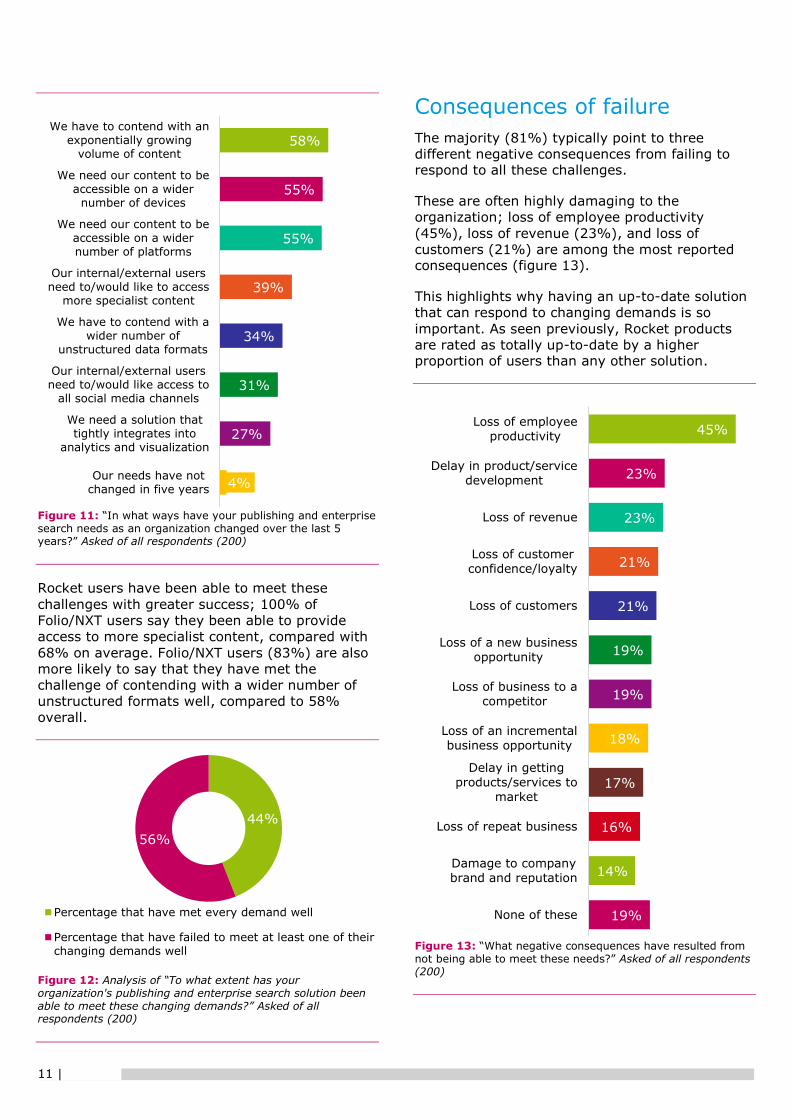

Consequences of failure

The majority (81%) typically point to three

different negative consequences from failing to respond to all these challenges.

These are often highly damaging to the

organization; loss of employee productivity

(45%), loss of revenue (23%), and loss of

customers (21%) are among the most reported consequences (figure 13).

This highlights why having an up-to-date solution

that can respond to changing demands is so

important. As seen previously, Rocket products

are rated as totally up-to-date by a higher proportion of users than any other solution.

Figure 13: “What negative consequences have resulted from not being able to meet these needs?” Asked of all respondents (200)

58%

55%

55%

39%

34%

31%

27%

4%

We have to contend with anexponentially growing

volume of content

We need our content to beaccessible on a wider

number of devices

We need our content to beaccessible on a widernumber of platforms

Our internal/external usersneed to/would like to access

more specialist content

We have to contend with awider number of

unstructured data formats

Our internal/external usersneed to/would like access to

all social media channels

We need a solution thattightly integrates into

analytics and visualization

Our needs have notchanged in five years

44%

56%

Percentage that have met every demand well

Percentage that have failed to meet at least one of theirchanging demands well

45%

23%

23%

21%

21%

19%

19%

18%

17%

16%

14%

19%

Loss of employee

productivity

Delay in product/service

development

Loss of revenue

Loss of customer

confidence/loyalty

Loss of customers

Loss of a new business

opportunity

Loss of business to a

competitor

Loss of an incremental

business opportunity

Delay in getting

products/services to

market

Loss of repeat business

Damage to company

brand and reputation

None of these

12 |

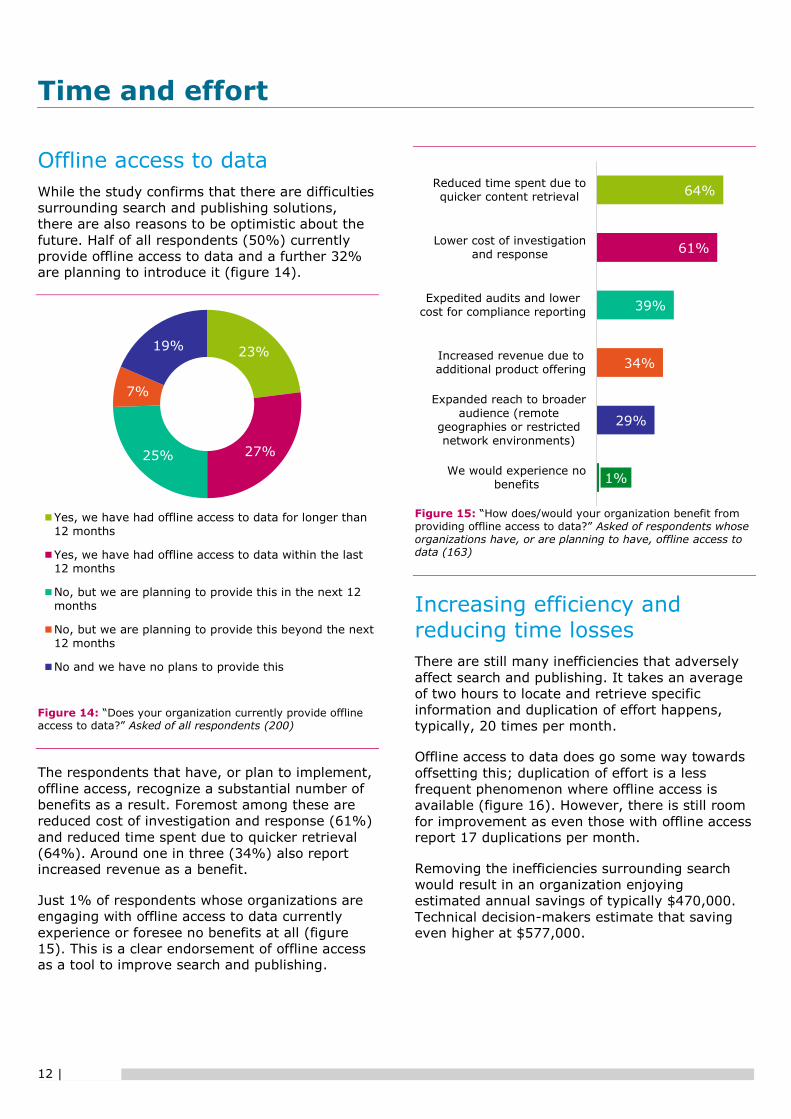

Offline access to data

While the study confirms that there are difficulties

surrounding search and publishing solutions,

there are also reasons to be optimistic about the

future. Half of all respondents (50%) currently

provide offline access to data and a further 32% are planning to introduce it (figure 14).

Figure 14: “Does your organization currently provide offline access to data?” Asked of all respondents (200)

The respondents that have, or plan to implement,

offline access, recognize a substantial number of

benefits as a result. Foremost among these are

reduced cost of investigation and response (61%)

and reduced time spent due to quicker retrieval

(64%). Around one in three (34%) also report increased revenue as a benefit.

Just 1% of respondents whose organizations are

engaging with offline access to data currently

experience or foresee no benefits at all (figure

15). This is a clear endorsement of offline access as a tool to improve search and publishing.

Figure 15: “How does/would your organization benefit from providing offline access to data?” Asked of respondents whose organizations have, or are planning to have, offline access to data (163)

Increasing efficiency and reducing time losses

There are still many inefficiencies that adversely

affect search and publishing. It takes an average

of two hours to locate and retrieve specific

information and duplication of effort happens,

typically, 20 times per month.

Offline access to data does go some way towards

offsetting this; duplication of effort is a less

frequent phenomenon where offline access is

available (figure 16). However, there is still room

for improvement as even those with offline access report 17 duplications per month.

Removing the inefficiencies surrounding search

would result in an organization enjoying

estimated annual savings of typically $470,000.

Technical decision-makers estimate that saving even higher at $577,000.

23%

27%25%

7%

19%

Yes, we have had offline access to data for longer than12 months

Yes, we have had offline access to data within the last12 months

No, but we are planning to provide this in the next 12months

No, but we are planning to provide this beyond the next12 months

No and we have no plans to provide this

64%

61%

39%

34%

29%

1%

Reduced time spent due toquicker content retrieval

Lower cost of investigationand response

Expedited audits and lowercost for compliance reporting

Increased revenue due toadditional product offering

Expanded reach to broaderaudience (remote

geographies or restrictednetwork environments)

We would experience nobenefits

Time and effort

13 |

Figure 16: “In your organization, how frequently do you believe efforts are duplicated in the cases where information is already available?” Asked of all respondents (200), split by offline access vs no offline access. Showing average number of duplications per month

However, spending a large amount on search and

publishing does not necessarily increase

efficiency. The data shows that the opposite is

true. A respondent who says that their

organization pays more is actually more likely to

see higher search times - those spending over $1

million in total see an average search time of

three hours compared with under two hours for

those spending less than $50,000. This suggests

that those spending on multiple solutions are

failing to integrate, whereas those with a single,

intelligent, more cost-effective solution perform

better (figure 17).

Figure 17: “Using your current technology and processes, how long would it take – in man-hours – for you to determine if specific information existed within your enterprise and then actually retrieve it?” Asked of all respondents (200), split by overall cost of search in 2013. Showing average number of man-hours spent to search for and retrieve a specific piece of information

2017

22

Total Yes, offline access

to data

No offline access

to data

1.742.05

2.81 2.70

3.10

Less than$50,000

$50,000 -$100,000

$100,000 -$500,000

$500,000 -$1 million

More than$1 million

14 |

There is no single search and publishing solution

that dominates the marketplace, although HP

Autonomy, IBM Vivisimo Velocity, and Oracle Endeca are the most commonly used.

Solutions created by Rocket Software are less in

evidence; 10% of respondents either use Rocket

Folio, Rocket NXT, or both of them. Despite

smaller numbers of users, these tools elicit a

more positive impression than those from the

leading vendors and homegrown solutions. Rocket

outperforms competitors across a number of

criteria: content delivery, affordability, and being

up-to-date. For example, users of Folio and NXT

are over twice as likely to consider their solution

very reasonably priced when compared with the

average respondent (37% compared with 15% overall).

Pricing is one of the major battlegrounds for

providers of search and publishing software. Most

respondents have given significant consideration

to cost of licensing/implementation (72%) and

level of maintenance (in time and cost) (71%)

when selecting their solutions. The average sum

spent on search in 2013 was $477,000, rising to

$578,000 when an IT decision-maker is asked the question.

Aside from cost, the only factor given significant

consideration by a higher number of respondents

is security. Over three quarters (77%) considered

security and subscription management when

sourcing their solution. This is further evidenced

by the top features: access control of documents

is identified as important by the highest number

of users (65%). On average, respondents report

that four different internal departments and two

different external groups (customers, partners etc.) require access to their solution.

Managing search and publishing across an

enterprise is not an easy task. Over the last five

years, nearly all respondents (96%) have had to

cope with their organization’s changing

requirements, and the large majority (91%) are

still experiencing those challenges. The challenge

being faced by the highest number of respondents is cost (48%).

Demands change and the majority (56%) have

not been able to meet these demands ‘well’. If

respondents do not feel that their current

solutions are meeting their organizations’ needs

adequately, how well positioned are they to face inevitable future changes in demand profile?

81% of respondents say they have experienced

negative consequences from failing in this area.

Respondents report having already experienced

loss of employee productivity (44%), loss of

revenue (23%) and loss of customers (21%)

because they have not been able to keep pace with the changes.

Despite these repercussions, some respondents

are embracing new innovations to improve their

position and increase search efficiency. 50%

currently provide offline access to data and a

further 32% plan to start in the future. The most

frequent benefits of doing this include reducing

content retrieval time (64%) and lowering

investigatory costs (61%).

Spending large sums on search and publishing

does not necessarily increase search efficiency,

and the data shows that the opposite is true.

Intelligent purchasing and features such as offline

access to data yield significant results. Duplication

of search effort is frequent, occurring twenty

times per month on average. Reduction of this

duplication can lead to a potential estimated

saving of $470,000 over the course of a year on average.

Conclusion

15 |

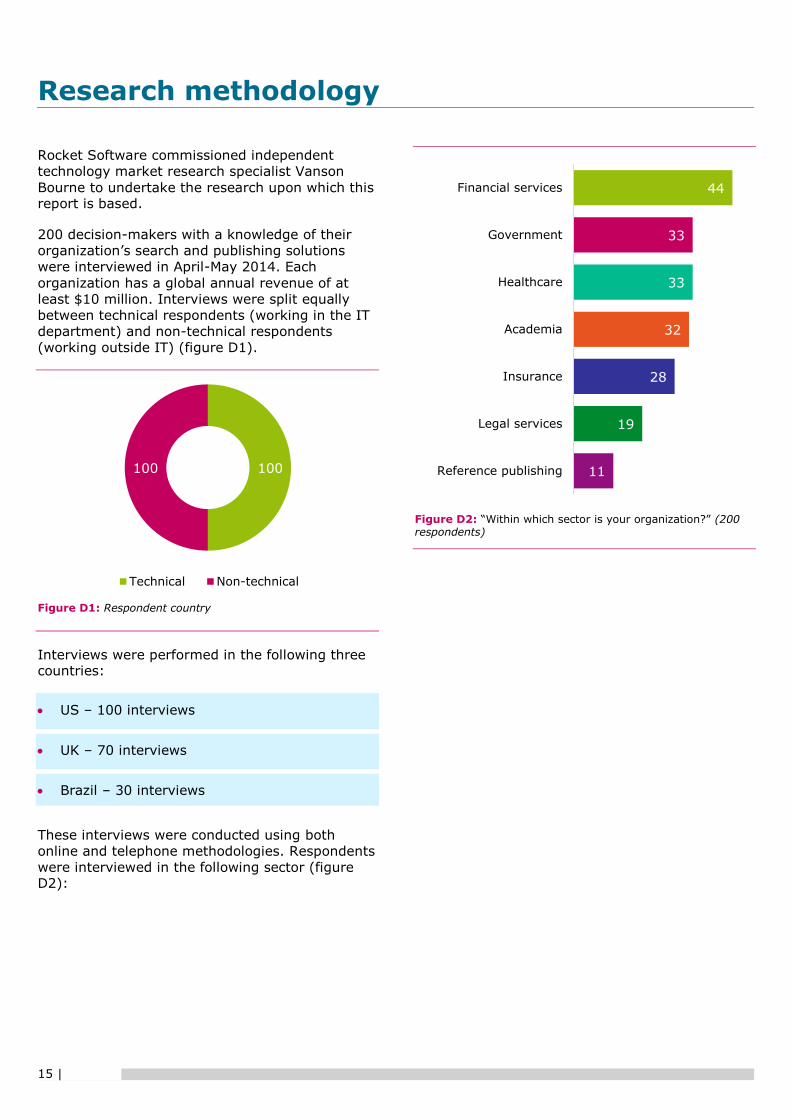

Rocket Software commissioned independent

technology market research specialist Vanson

Bourne to undertake the research upon which this report is based.

200 decision-makers with a knowledge of their

organization’s search and publishing solutions

were interviewed in April-May 2014. Each

organization has a global annual revenue of at

least $10 million. Interviews were split equally

between technical respondents (working in the IT

department) and non-technical respondents

(working outside IT) (figure D1).

Figure D1: Respondent country

Interviews were performed in the following three countries:

US – 100 interviews

UK – 70 interviews

Brazil – 30 interviews

These interviews were conducted using both

online and telephone methodologies. Respondents

were interviewed in the following sector (figure D2):

Figure D2: “Within which sector is your organization?” (200 respondents)

100100

Technical Non-technical

44

33

33

32

28

19

11

Financial services

Government

Healthcare

Academia

Insurance

Legal services

Reference publishing

Research methodology

About Rocket Software:

Rocket Software is a leading global developer of software products that help corporations, government

agencies and other organizations reach their technology and business goals. For more information, visit

www.rocketsoftware.com

About Vanson Bourne:

Vanson Bourne is an independent specialist in market research for the technology sector. Our reputation

for robust and credible research-based analysis, is founded upon rigorous research principles and our

ability to seek the opinions of senior decision makers across technical and business functions, in all

business sectors and all major markets. For more information, visit www.vansonbourne.com