Minority Rights, Culture, and Ethiopia's "Third Way" to Governance

Upload

addisababaCategory

view

1download

0

CHALLENGES AND PROSPECTS OF ETHIOPIA'S CEMENT INDUSTRY : CHALLENGES AND PROSPECTS OF ETHIOPIA'S CEMENT INDUSTRY :

STRATEGIC PERSPECTIVE (2015STRATEGIC PERSPECTIVE (2015--2025)2025)

By

Gemechu Waktola, Ph.D.

Assistant Professor, Adama Science & Technology University

Team Leader, Ethiopia’s Cement Industry Development Strategy

(2015-2025)

[email protected] or [email protected] +251911629011

In this presentation …In this presentation …

1.1. Brief Background & Current StatusBrief Background & Current Status

2.2. Critical Challenges & LimitationsCritical Challenges & Limitations

3.3. Opportunities & ProspectsOpportunities & Prospects

4.4. Strategic RecommendationsStrategic Recommendations4.4. Strategic RecommendationsStrategic Recommendations

11

Brief Background Brief Background

& Current Status & Current Status & Current Status & Current Status of Ethiopia’s Cement Industry

Development

4/20/2015 3

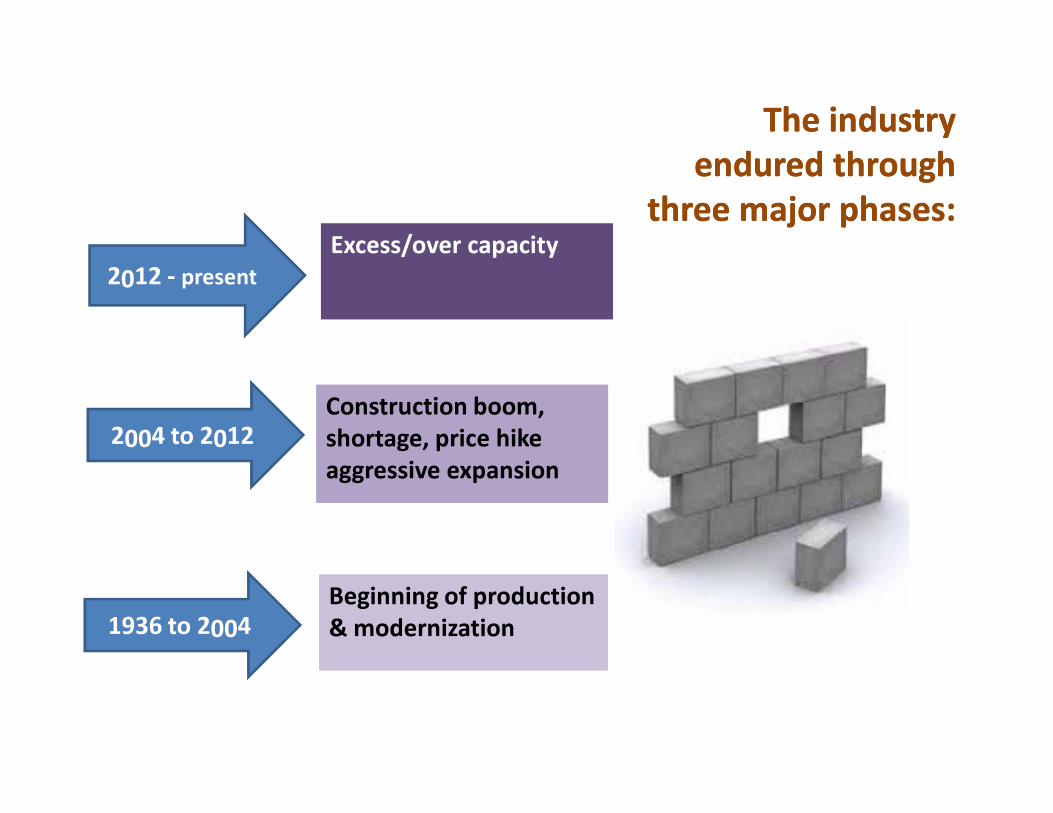

The industry The industry

endured through endured through

three major phases: three major phases:

Construction boom, Construction boom,

Excess/over capacityExcess/over capacity

2012 - present

Beginning of production

& modernization

Beginning of production

& modernization1936 to 2004

Construction boom,

shortage, price hike

aggressive expansion

Construction boom,

shortage, price hike

aggressive expansion

2004 to 2012

GT

P I

, P

roje

cte

d c

ap

aci

ty 2

7M

T, P

er

cap

ita

, 3

00

kg

GT

P I

, P

roje

cte

d c

ap

aci

ty 2

7M

T, P

er

cap

ita

, 3

00

kg

March 2012

Import ban

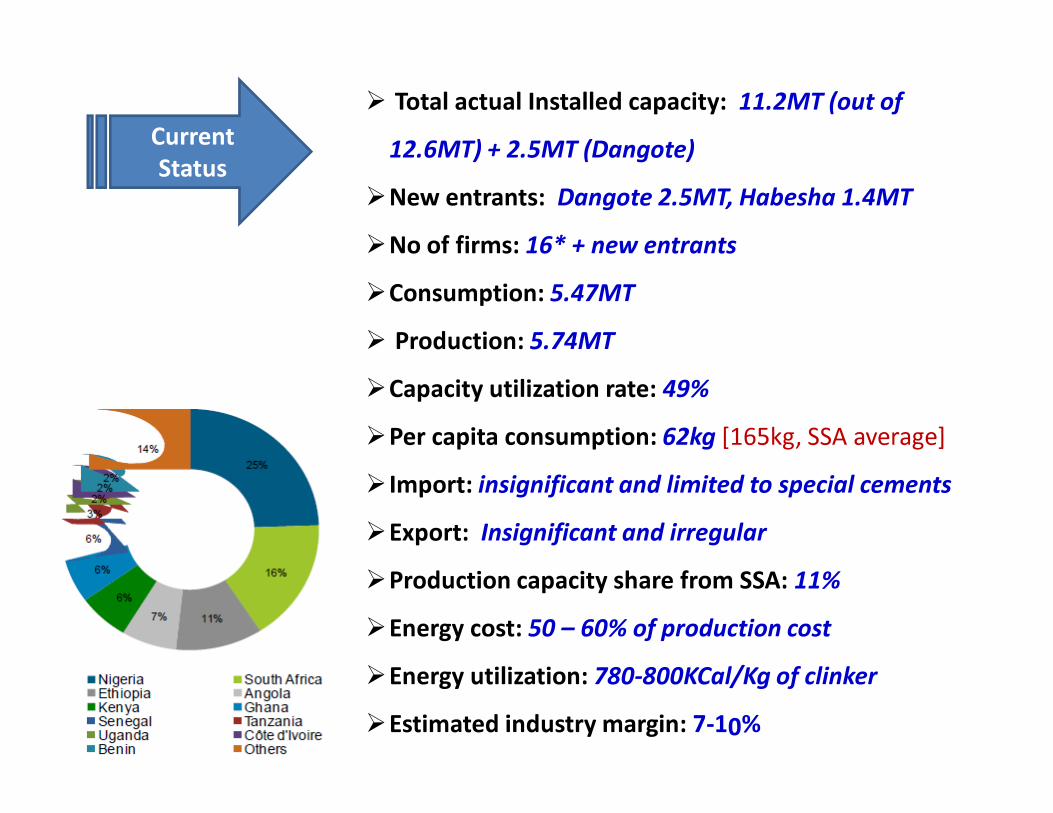

Current

Status

� Total actual Installed capacity: 11.2MT (out of

12.6MT) + 2.5MT (Dangote)

�New entrants: Dangote 2.5MT, Habesha 1.4MT

�No of firms: 16* + new entrants

�Consumption: 5.47MT

� Production: 5.74MT

�Capacity utilization rate: 49%

�Per capita consumption: 62kg [165kg, SSA average]

� Import: insignificant and limited to special cements

�Export: Insignificant and irregular

�Production capacity share from SSA: 11%

�Energy cost: 50 – 60% of production cost

�Energy utilization: 780-800KCal/Kg of clinker

�Estimated industry margin: 7-10%

22

Critical Challenges & Critical Challenges &

LimitationsLimitationsof Ethiopia’s Cement Industry of Ethiopia’s Cement Industry

Critical Challenges & Limitations of the Industry’s Value ChainCritical Challenges & Limitations of the Industry’s Value Chain

Su

pp

ort

Act

ivit

ies

Industry Infrastructure Limited access to finance;

Inadequate product, environment and energy standards and regulatory enforcement capacity;

Insufficient support institutions; existing ones are weak having limited capacity;

Industry Infrastructure Limited access to finance;

Inadequate product, environment and energy standards and regulatory enforcement capacity;

Insufficient support institutions; existing ones are weak having limited capacity;

Limited flexibility to respond to global and regional product, energy, and environmental trends;

Development of Industry Human Resource Shortage of trained HR in cement technology and management

Development of Industry Human Resource Shortage of trained HR in cement technology and management

Lack of strategic HRD

Limited knowledge and technology transfer capacity and system;

Cement Technology Development Limited knowledge and technology transfer capacity and system;

Weak strategic R&D plans; lim

ite

d g

row

th,

sust

ain

ab

ilit

y, a

nd

co

mp

eti

tive

ne

ss o

f

ce

me

nt

Ind

ust

ry

Weak strategic R&D plans;

Supply of Cement Inputs HFO and coal;

Absence or limited use of alternative energy;

Supply of Cement Inputs Heavy dependence on expensive imported energy – HFO and coal;

Absence or limited use of alternative energy;

Frequent electricity interruption;

Inbound

Logistics

• Inefficient,

insufficient and

expensive logistics

and customs

procedures

Cement

Production

• Inefficient

production and

energy

utilization,

mainly by mini-

plants

Outbound Logistics

• Inefficient, insufficient

and expensive logistics

• Lack of strategic focus

on core business

Demand & Marketing

• Inadequate current demand; higher

cement price

• High market concentration at center

• Inadequate product diversification and

value addition; weak Remicon, Remitar,

& other support industries

Sm

all

pro

fit

ma

rgin

s;li

mit

ed

gro

wth

,

sust

ain

ab

ilit

y, a

nd

co

mp

eti

tive

ne

ss o

f

the

ce

me

nt

Ind

ust

ry

Primary Activities

33

Opportunities Opportunities Opportunities Opportunities

& Prospects& Prospects

of Ethiopia’s Cement Industry

Strong Strong

demand demand

drivers drivers

Middle Income Vision

(2025)

Lower Cement Per Capita

(62kg)

Mega projects

Infrastructure

etc

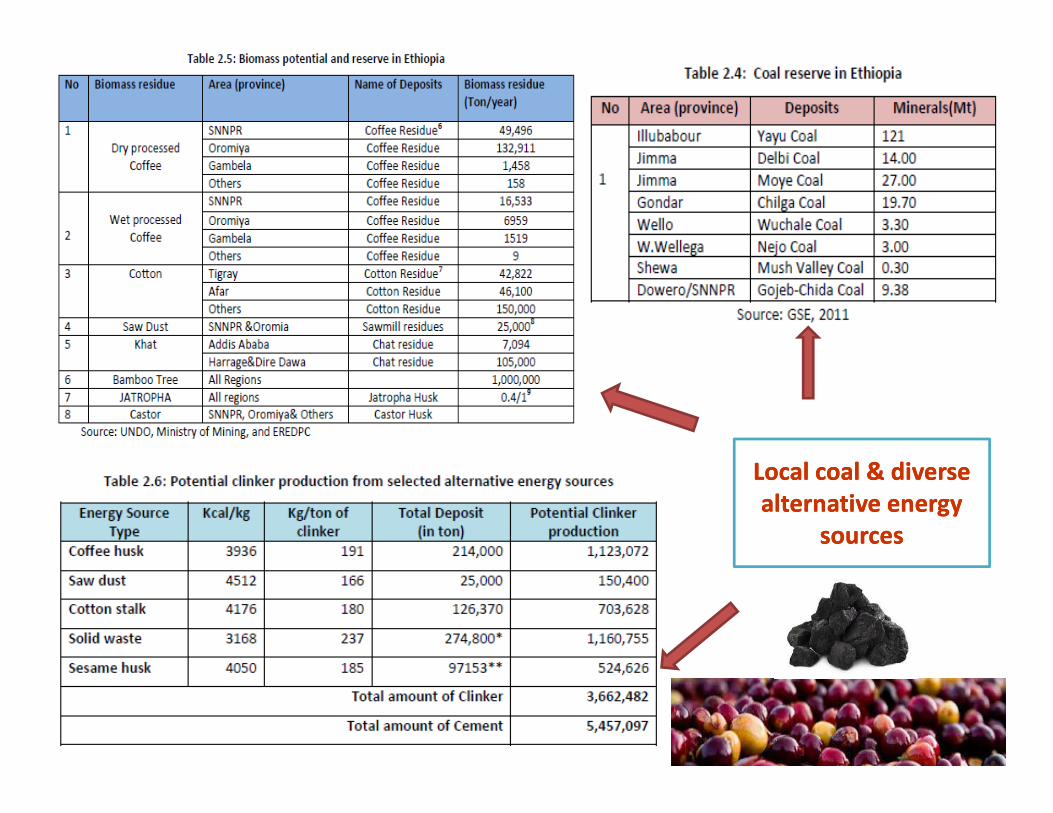

Local coal & diverse Local coal & diverse

alternative energy alternative energy

sources sources

… other critical opportunities… other critical opportunities

• Upcoming railway network

• Potential to diversify cement uses

• Young and trainable labor

• Widespread, accessible raw materials reserve

• Potential for localizing• Potential for localizingsignificant parts of selected cement technologies

• emerging professional associations and universities

• Strategic industry with government will to support

• Availability of environmentally friendly technologies `and carbon trading schemes

44

Strategic Strategic

RecommendationsRecommendationsRecommendationsRecommendations

for development of Ethiopia’s

Cement Industry (2015-2025)

1. Short1. Short--term term

demand demand

stimulation stimulation

measures measures

• Induce demand for additional consumption of 12.22 MT until

2020 mainly from replacing asphalt roads with cement concrete

• Increase capacity utilization rate to 75% during the first three

years of the strategy period [2015-17] and sustainably maintain

the rate at 80% for the rest of the strategy period.

Ke

y T

arg

ets

• By end of 2015 with fully defined structure, roles,

responsibilities, and accountabilities to members

and the government

• At least ten joint projects annually on HRD, R&D

and K&T transfer, energy improvement, and

environmental protection.

2. Strong cement 2. Strong cement

associationassociation

Ke

y T

arg

ets

• Meet over all energy [local coal, biomass,

33. Replacement of . Replacement of

Imported Energy Imported Energy

• Meet over all energy [local coal, biomass,

municipal waste] replacement of at least 60% for

the industry by 2025.

• Fulfill 10% thermal energy requirement from

locally developed coal supply by 2020 and reach

30% by 2025.

• Reach share of energy substituted to at least 20%

of thermal energy requirement with alternative

energy by 2020 and at least 30% at the end of

2025.

Ke

y T

arg

ets

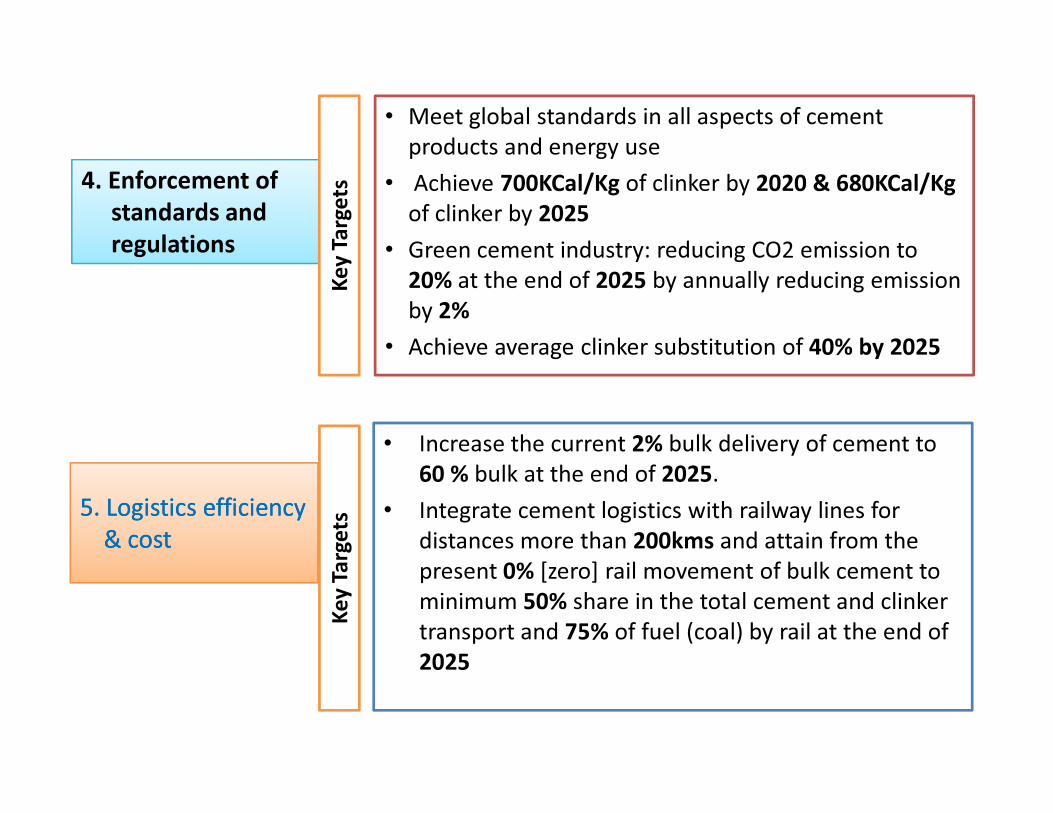

• Meet global standards in all aspects of cement

products and energy use

• Achieve 700KCal/Kg of clinker by 2020 & 680KCal/Kg

of clinker by 2025

• Green cement industry: reducing CO2 emission to

20% at the end of 2025 by annually reducing emission

by 2%

• Achieve average clinker substitution of 40% by 2025

4. Enforcement of

standards and

regulations

Ke

y T

arg

ets

55. Logistics efficiency . Logistics efficiency

& cost& cost

• Increase the current 2% bulk delivery of cement to

60 % bulk at the end of 2025.

• Integrate cement logistics with railway lines for

distances more than 200kms and attain from the

present 0% [zero] rail movement of bulk cement to

minimum 50% share in the total cement and clinker

transport and 75% of fuel (coal) by rail at the end of

2025

Ke

y T

arg

ets

77. . R&D, knowledge and technology transfer• 100 R&D and 50 K&T projects

• Localize 60% of cement technologies by 2025

Other

Strategic

Issues

66. . HRD system and programs• Produce operators; cement engineers &

technology managers

• 95% of OJT using S-OJT

• Operate and manage the cement industry with

98% local experts at the end of the strategy period.

• Localize 60% of cement technologies by 2025

8. Product diversification and value addition• Promote industries such as Remicon and prefabs as

major consumers for at least 50% of cement supply

by 2020

99. . Access to finance for cement and support

industries • financial access and loan guarantees for investments on

strategic priority areas

Issues

Projections

Projection

Components

In million tons/%/Kg

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

A Baseline Installed

Capacity11.2 15.6 17.15 17.15 17.15 17.15 17.15 17.15 17.15 17.15 17.15 17.15

BProjected Consumption 5.47 6.34 7.25 8.30 9.47 10.82 12.02 13.35 14.80 16.40 18.11 19.97

C Stimulation Adjusted

Consumption

Projection*

5.47 8.11 10.29 11.15 11.83 12.18 12.86 13.72 14.80 16.40 18.11 19.97

D Production Projection 5.74 8.52 10.80 11.70 12.43 12.79 13.51 14.41 15.54 17.22 19.01 20.97

D Production Projection

[=C*1.05]5.74 8.52 10.80 11.70 12.43 12.79 13.51 14.41 15.54 17.22 19.01 20.97

E Required Installed

Capacity [=D*1.20]6.89 10.22 12.97 14.05 14.91 15.35 16.21 17.29 18.65 20.66 22.82 25.16

F Required Additional

Capacity [=E-A]0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.14 1.50 3.51 5.67 8.01

G Forecasted Capacity

Utilization (%)[=D/A]49 55 63 68 72 75 79 84 91 100 111 122

H Required Stimulation

[=C-B]1.77 3.04 2.85 2.36 1.36 0.84 0.37 0.00 0.00 0.00 0.00

I Projected Population

(Mil.)87.90 90.10 92.20 94.30 96.50 98.70 100.80 102.90 105.20 107.30 109.50 111.6

J Per capita consumption

(in kg) [=C/I]62 90 112 118 123 123 128 133 141 153 165 179

� Policies, Regulations and Directives

� Strategic Projects

� Organizational Setups

Recommendations Recommendations

For For

Implementation Implementation

4/20/2015 20

� Organizational Setups

� Support Institutions

� Support Industries

� Key partners

Credits: Credits:

Strategy Team membersStrategy Team members

MoIMoI, ASTU, , ASTU,

Steering committee Steering committee

EKI, Korea EKI, Korea

Thank you for your attention! Thank you for your attention!

4/20/2015 21

Copyright © 2022 FDOKUMEN